Short-Term Prediction of Demand for Ride-Hailing Services ...

Decarbonization, Transportation and the Changing Oil Market: The Role of Politics and Policies in the Peak Demand Debate

Robert Johnston

CEO, Director, Global Energy & Natural Resources

IEEJ:July 2018 © IEEJ2018

2

Table of contents

Exploring key drivers of changes in the oil/transportation system: are these structural changes to global oil demand?

• Role of public policy

• Headwinds for policymakers

• What other factors should be explored?

IEEJ:July 2018 © IEEJ2018

Role of public policy: ambitious or unrealistic?

IEEJ:July 2018 © IEEJ2018

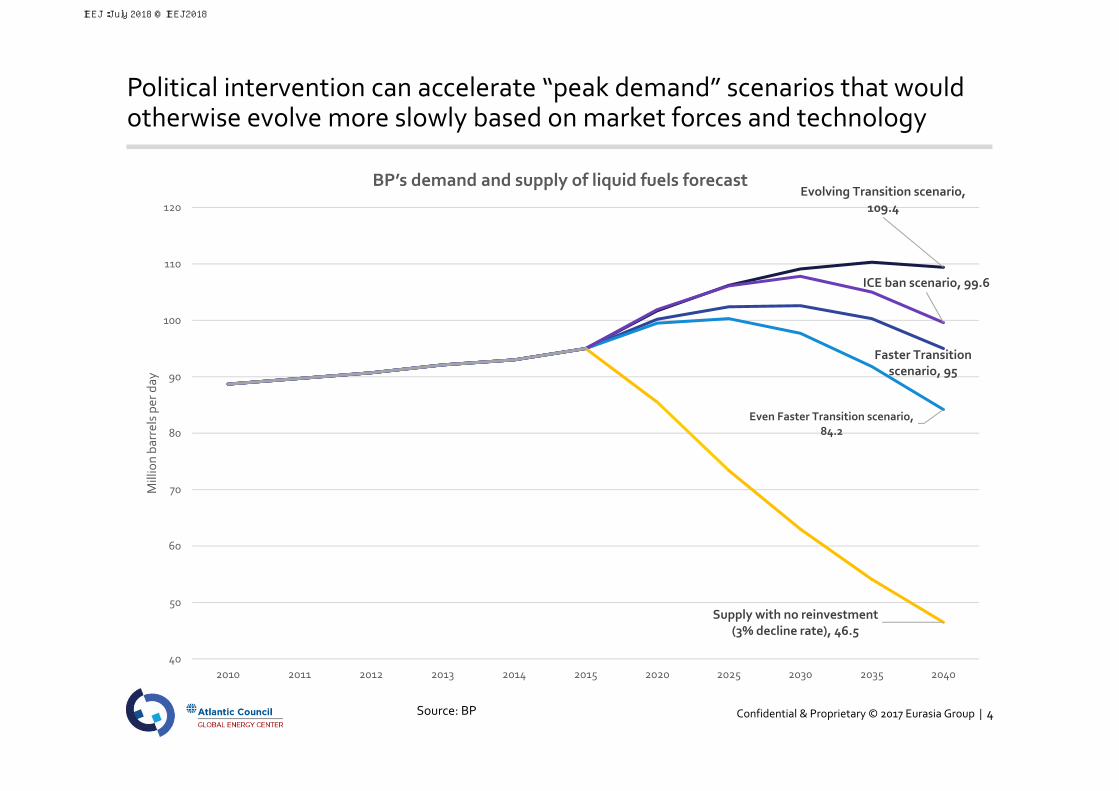

Confidential & Proprietary © 2017 Eurasia Group | 4

Political intervention can accelerate “peak demand” scenarios that would otherwise evolve more slowly based on market forces and technology

Source: BP

Evolving Transition scenario, 109.4

Faster Transition scenario, 95

Even Faster Transition scenario, 84.2

ICE ban scenario, 99.6

Supply with no reinvestment (3% decline rate), 46.5

40

50

60

70

80

90

100

110

120

2010 2011 2012 2013 2014 2015 2020 2025 2030 2035 2040

Million ba

rrels pe

r day

BP’s demand and supply of liquid fuels forecast

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 5

Ambitious transportation sector polices could have important consequences for oil demand destruction

Source: BPNote: Non‐transportation includes industry, non‐combusted, buildings, and power. Transportation includes non‐road (aviation, marine, rail), trucks (most SUVs in North America), cars (includes 2‐and‐3‐wheelers)

2018 Eurasia Group

0

20

40

60

80

100

120

2000 2005 2010 2015 2020 2025 2030 2035 2040

Million ba

rrels pe

r day

Liquids demand forecast

Non‐transportation Transportation

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 6

Clean transportation policies likely to be more effective when accounting for and influenced by a “national interest approach”

Stronger political imperative on climate change

Rising air‐quality problems from diesel

Industrial policy to motivate advanced domestic manufacturing of

Energy security

2018 Eurasia Group

Major drivers of decarbonization in the transportation sector include:

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 7

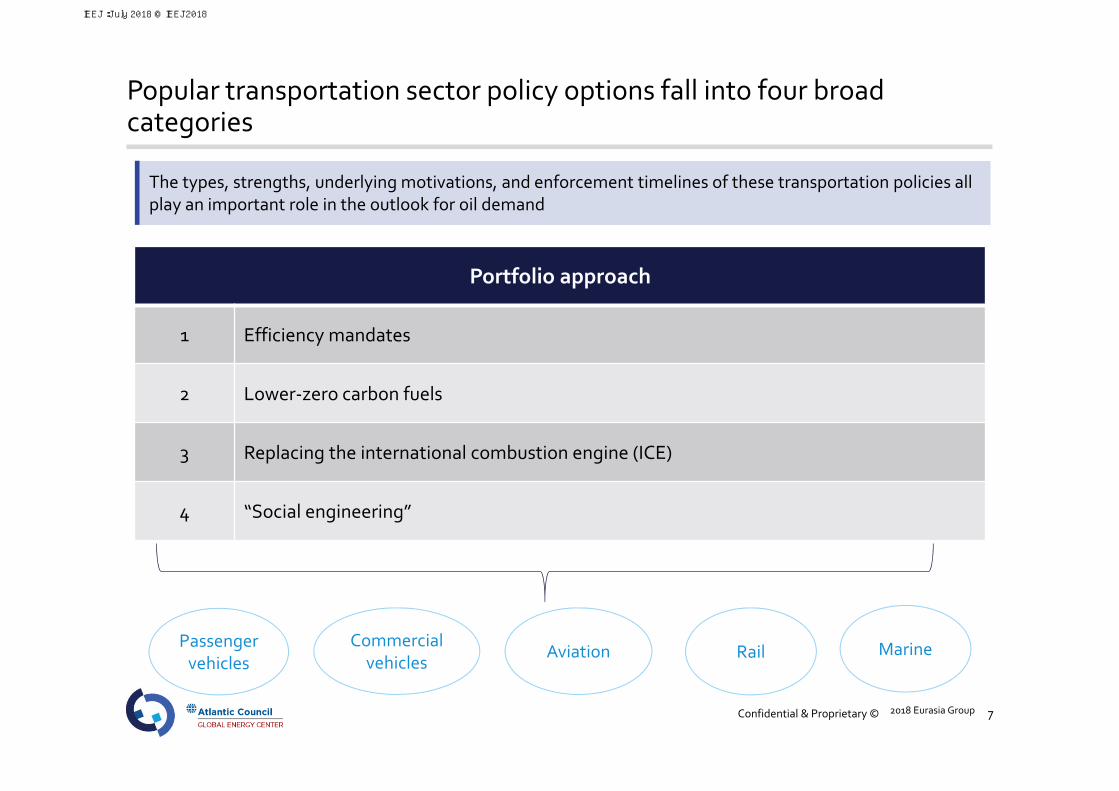

Popular transportation sector policy options fall into four broad categories

2018 Eurasia Group

Portfolio approach

1 Efficiency mandates

2 Lower‐zero carbon fuels

3 Replacing the international combustion engine (ICE)

4 “Social engineering”

The types, strengths, underlying motivations, and enforcement timelines of these transportation policies all play an important role in the outlook for oil demand

Passenger vehicles

Commercial vehicles

Aviation Rail Marine

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 8

Policies that promote electric vehicles (EVs) are getting the most attention

Source: IEA, Clean Technica, FleetCarma, Quartz 2018 Eurasia Group

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

2010 2011 2012 2013 2014 2015 2016

Number of new EV registrations

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 9

Europe is pushing the envelope on electric and hybrid vehicles

0

10

20

30

40

50

60

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

%

Share of diesel in new passenger cars in Western Europe

Source: European Automobile Manufacturers Association (ACEA)2018 Eurasia Group

IEEJ:July 2018 © IEEJ2018

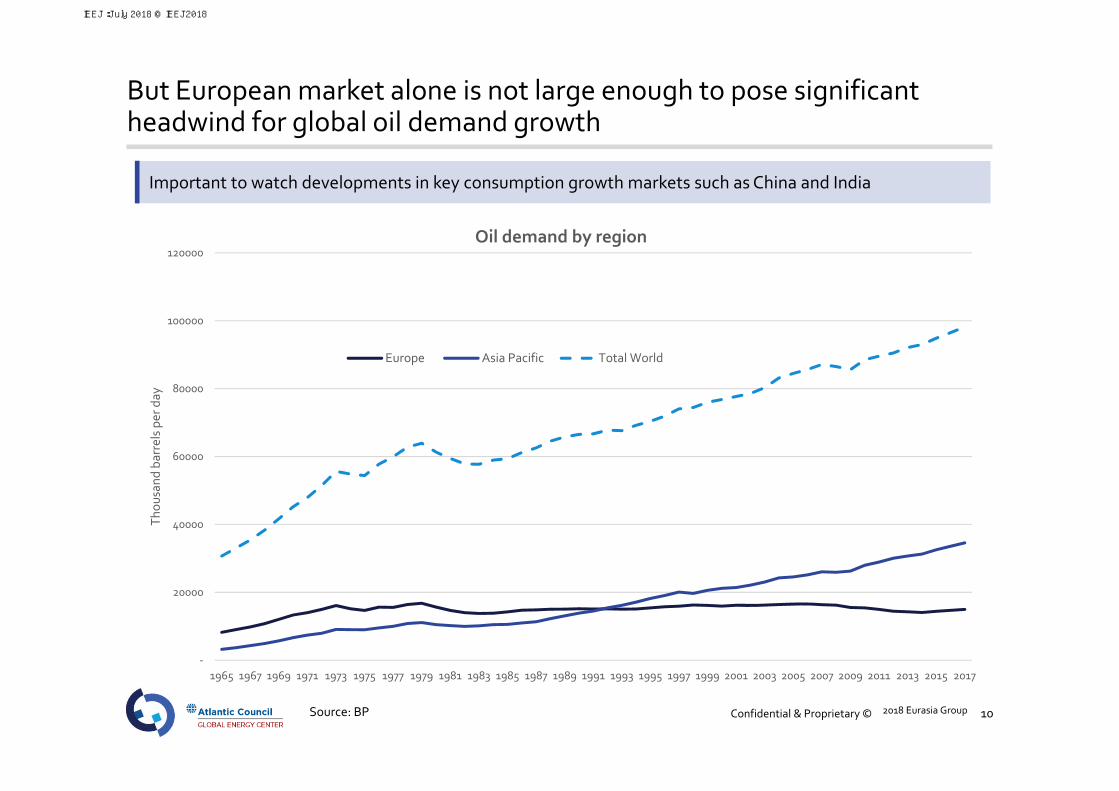

Confidential & Proprietary © 2017 Eurasia Group | 10

But European market alone is not large enough to pose significant headwind for global oil demand growth

Important to watch developments in key consumption growth markets such as China and India

2018 Eurasia Group

‐

20000

40000

60000

80000

100000

120000

1965 1967 1969 1971 1973 1975 1977 1979 1981 1983 1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017

Thou

sand barrels per day

Oil demand by region

Europe Asia Pacific Total World

Source: BP

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 11

The Chinese government’s generous EV incentives have proven effective in driving sales—how much more upside is there?

Source: CEIA, hybrid cars.com, EAFO, Macquarie Research, Business Insider

2018 Eurasia Group

72%

33%

33%

108%

75%

0%

20%

40%

60%

80%

100%

120%

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

China Europe US Japan Canada

Share of nationa

l marke

t (% cha

nge ye

ar‐on‐ye

ar)

EV and PHEV sales in select markets in 2017

EV PHEV Total sales YoY

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 12

More attention needs to be paid to the broader transportation sector (trucks, marine, aviation, alternative fuels and smart cities), especially in Asia

China, Japan, and Korea are the world’s 1st, 4th, and 5th largest crude oil importers

“Made in China 2025” program

China‐ Bicycles, rail electrification

China Belt and Road Initiative‐ Super‐grid

Japanese zero‐emissions and hydrogen fuel cellprogram

Korean National Green Growth Strategy

Smart Cities for emerging Asia‐ India, ASEAN

Ride‐sharing and fleet utilization

Industrial policy and government coordination

Energy insecurity and import dependence

Air quality concerns and climate policy

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 13

The role of transportation is shifting owing to developments in “micro‐mobility”

Autonomous vehicles, ride‐sharing, and “micro‐mobility” developments continue to demonstrate technological progress and declining costs in addition to being the subject of rising government interest

The future of fleet ownership and the influence of market design on how consumers own, rent, or lease vehicles is also an important dynamic

0 0.2 0.4 0.6 0.8 1 1.2 1.4

ICE

EV

Ride‐hailing EV

Ride‐hailing autonomous vehicle

Light‐duty vehicle cost per mile (USD per mile)

2030 2017

Total miles (p.a.)

70,000

70,000

13,500

13,500

Source: Bain, World Economic ForumNote: Cost per mile based on compact ICE and compact EV in the US, the figures exclude upfront cost

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 14

All of these factors pose a threat to oil’s supreme role in transportation—key question is by how much and when?

Within the clean transportation and peak oil demand debate there is little consensus about the exact recipe of policy measures and implementation timeframes

There remains a significant level of uncertainty in the analysis and forecasting on this issue particularly outside of the electric passenger vehicle domain.

Decarbonization scenarios and transportation sector policies

Scenario Peak demand forecast

IEA’s Sustainable Development Scenario Around 2020

IEA’s Faster Transition ScenarioAround 2020 (and falls thereafter at a faster rate

than SDS)

IEEJ Peak Oil Demand Case Around 2030

Rocky Mountain Institute’s Reinventing Fire Scenario

China’s oil demand peaks by 2030

Exxon Mobil’s 2D Scenarios Doesn’t forecast exact peak date

Shell’s New Lens Scenarios Varies by scenario

BP’s Evolving Transition scenarioDemand for oil does not plateau and peak until the

end of the 2040‐outlook

IEEJ:July 2018 © IEEJ2018

Challenges for policy makers: are they a deal breaker?

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 16

Lawmakers face key risks and challenges that undermine the transportation decarbonization effort

Will governments be willing to put more political capital behind expensive initiatives that encourage EV sales or implement politically tricky ICE bans/limit sales of fossil‐fueled power vehicles? What about broader carbon policies like economy‐wide carbon taxes?

2018 Eurasia Group

Infrastructure constraints

Higher costs (esp. for EVs compared to ICEs or retrofitting to cleaner fuels for marine shipping)

Political constraints including elections and legal challenges

Questions about the regulation of emerging technologies

Resource availability and environmental concerns for critical minerals

Resistance from politically important groups such as domestic auto industry in India or agriculture/farm lobby in the United States

Overly ambitious EV targets

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 17

Do governments instead prefer a more cautious approach that would signal a less disruptive outlook for global oil demand?

In US, EVs remain very small share of total auto sales: At the federal level, Trump administration’s attempt to weaken fuel efficiency standards will deal a setback to EV uptake

In India, officials have walked back on ambitious EV target

2018 Eurasia Group

There is a risk that overly ambitious or unrealistic policies could have a “snap‐back” effect and unintentionally harm the development of a clean transportation sector

Passenger vehicles, 13%

Commercial vehicles, 3%

Three wheelers, 3%

Two wheelers, 81%

India’s domestic automobile market share (2017‐2018)

Source: US Energy Information Administration, Society of Indian Automobile Manufacturers

IEEJ:July 2018 © IEEJ2018

Conclusions and Discussion

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 19

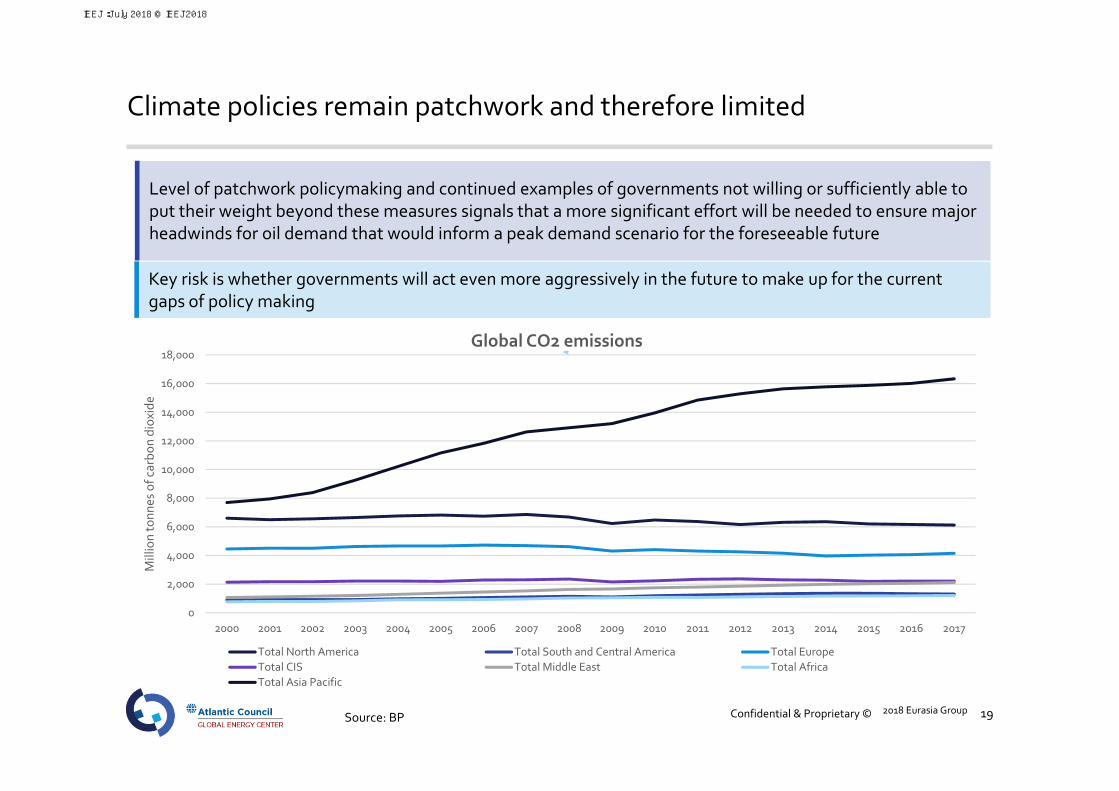

Climate policies remain patchwork and therefore limited

Level of patchwork policymaking and continued examples of governments not willing or sufficiently able to put their weight beyond these measures signals that a more significant effort will be needed to ensure major headwinds for oil demand that would inform a peak demand scenario for the foreseeable future

2018 Eurasia Group

Key risk is whether governments will act even more aggressively in the future to make up for the current gaps of policy making

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Million tonn

es of c

arbo

n diox

ide

Global CO2 emissions

Total North America Total South and Central America Total EuropeTotal CIS Total Middle East Total AfricaTotal Asia Pacific

Source: BP

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 20

However, the peak demand debate is already complicating investment outlook for long‐cycle upstream projects

2018 Eurasia Group

IEA New Policies Scenario

IEA Sustainable Development Scenario

IEA Current Policies Scenario

OPEC Reference Case

IEEJ Reference Scenario

IEEJ Peak Oil Demand Scenario

0

20

40

60

80

100

120

140

Varying long‐term oil demand forecasts

Source: International Energy Agency, the Institute for Energy Economics, OPEC

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 21

In the short‐term, a shift to short‐cycle plays such as US shale is underway

Companies and investors are looking to minimize risk in this environment (US shale is the big initial winner)

Source: International Energy Agency

‐20%

‐10%

0%

10%

20%

30%

40%

50%

60%

Africa Latin America Middle East Russia US Shale

Upstream oil and gas investment (2017 vs. 2016)

2018 Eurasia Group

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 22

What do governments do with stranded assets?

Stranded assets could add financial strain to government and company budgets, as well as logistical challenges from issues such as restructuring

2018 Eurasia GroupPhoto credit: Carbon Tracker report

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 23

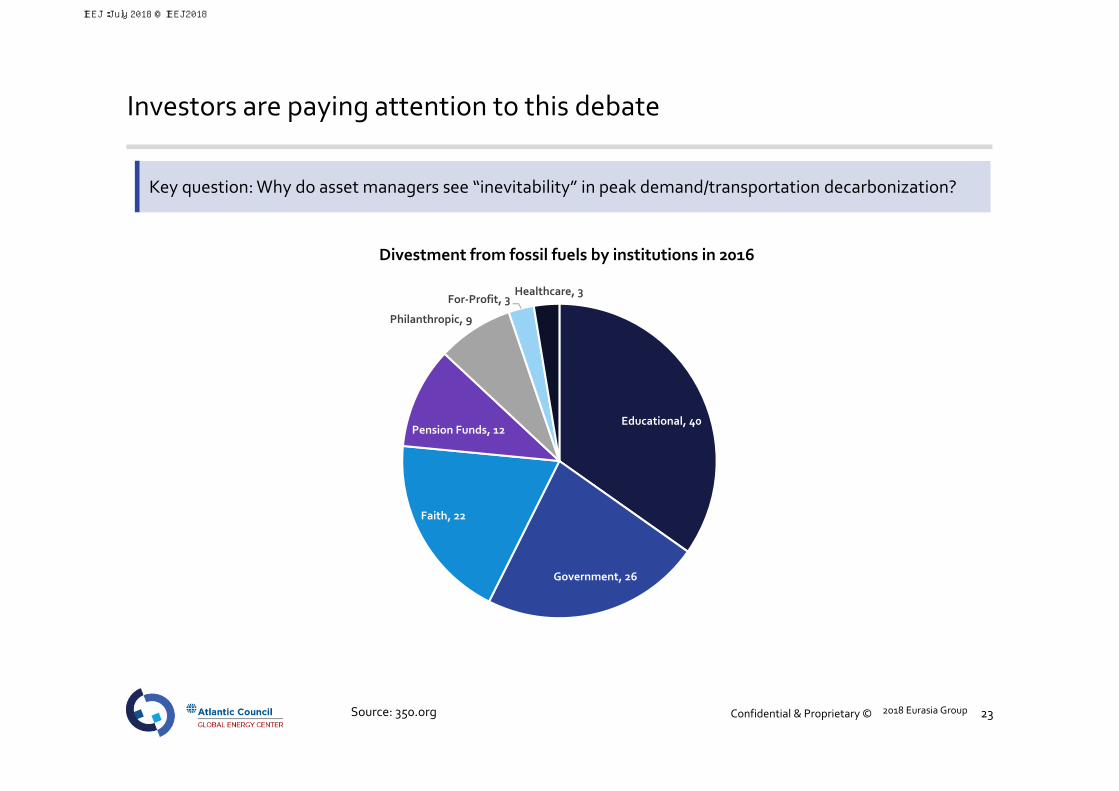

Investors are paying attention to this debate

Key question: Why do asset managers see “inevitability” in peak demand/transportation decarbonization?

2018 Eurasia Group

Educational, 40

Government, 26

Faith, 22

Pension Funds, 12

Philanthropic, 9

For‐Profit, 3Healthcare, 3

Divestment from fossil fuels by institutions in 2016

Source: 350.org

IEEJ:July 2018 © IEEJ2018

Confidential & Proprietary © 2017 Eurasia Group | 24

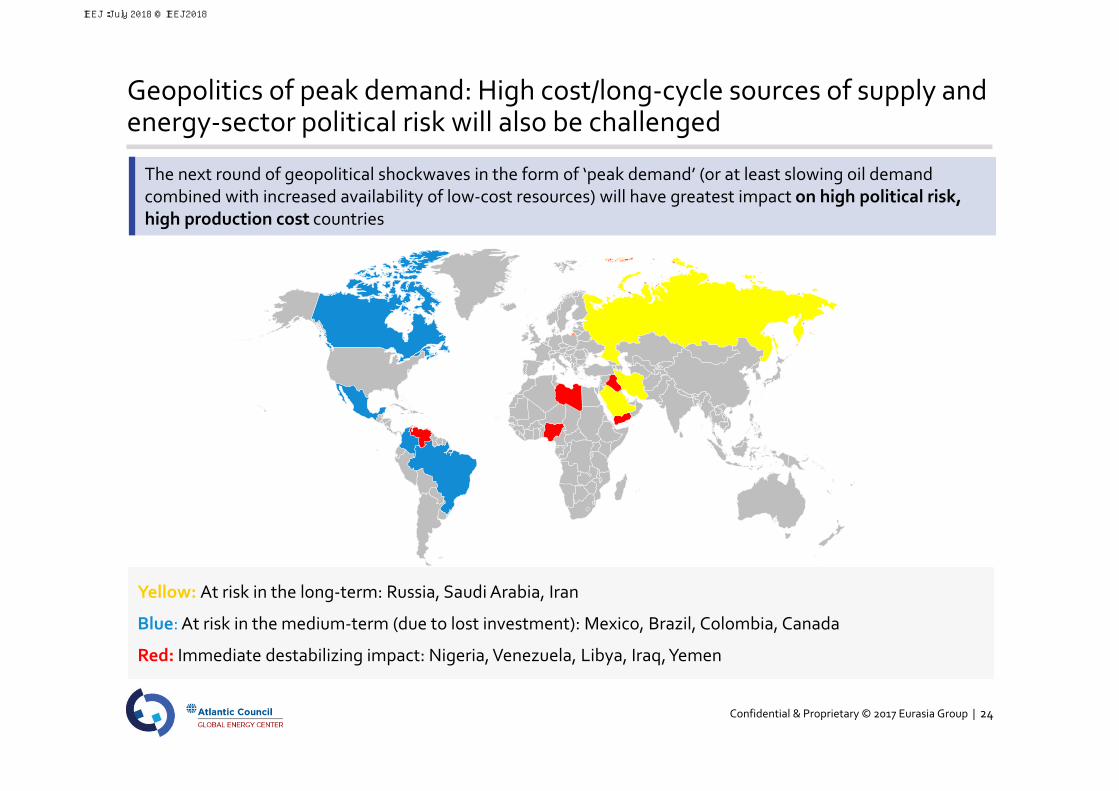

Geopolitics of peak demand: High cost/long‐cycle sources of supply and energy‐sector political risk will also be challenged

Yellow: At risk in the long‐term: Russia, Saudi Arabia, Iran

Blue: At risk in the medium‐term (due to lost investment): Mexico, Brazil, Colombia, Canada

Red: Immediate destabilizing impact: Nigeria, Venezuela, Libya, Iraq, Yemen

The next round of geopolitical shockwaves in the form of ‘peak demand’ (or at least slowing oil demand combined with increased availability of low‐cost resources) will have greatest impact on high political risk, high production cost countries

IEEJ:July 2018 © IEEJ2018

Eurasia Group is the world’s leading global political risk research and consulting firm. This presentation is intended solely for internal use by the recipient and is based on the opinions of Eurasia Group analysts and various in‐country

specialists. This presentation is not intended to serve as investment advice, and it makes no representations concerning the credit worthiness of any company. This presentation does not constitute an offer, or an invitation to offer, or a recommendation to enter into any transaction. Eurasia Group maintains no affiliations with government

or political parties.

© 2017 Eurasia Group | www.eurasiagroup.net

London New York San Francisco São Paulo Singapore Tokyo Washington DC

Eurasia Group is the world’s leading global political risk research and consulting firm. This presentation is intended solely for internal use by the recipient and is based on the opinions of Eurasia Group analysts and various in‐country

specialists. This presentation is not intended to serve as investment advice, and it makes no representations concerning the credit worthiness of any company. This presentation does not constitute an offer, or an invitation to offer, or a recommendation to enter into any transaction. Eurasia Group maintains no affiliations with government

or political parties.

© 2017 Eurasia Group | www.eurasiagroup.net

IEEJ:July 2018 © IEEJ2018

Contact :[email protected]