TRANSITIONING TO THE FUTURE - Sasol portfolio profitable through the cycle Developing future...

24

TRANSITIONING TO THE FUTURE SASOL LIMITED FINANCIAL RESULTS for the six months ended 31 December 2016 JSE: SOL NYSE: SSL

Transcript of TRANSITIONING TO THE FUTURE - Sasol portfolio profitable through the cycle Developing future...

TRANSITIONING TO THE FUTURE

SASOL LIMITED FINANCIAL RESULTS for the six months ended 31 December 2016

JSE: SOL NYSE: SSL

2

Forward-looking statements

Sasol may, in this document, make certain statements that are not historical facts and relate to analyses and other

information which are based on forecasts of future results and estimates of amounts not yet determinable. These

statements may also relate to our future prospects, developments and business strategies. Examples of such

forward-looking statements include, but are not limited to, statements regarding exchange rate fluctuations, volume

growth, increases in market share, total shareholder return, executing our growth projects and cost reductions, including

in connection with our Business Performance Enhancement Programme and Response Plan. Words such as "believe",

"anticipate", "expect", "intend", "seek", "will", "plan", "could", "may", "endeavour", "target", "forecast" and "project" and

similar expressions are intended to identify such forward-looking statements, but are not the exclusive means of identifying

such statements. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general

and specific, and there are risks that the predictions, forecasts, projections and other forward-looking statements will not

be achieved. If one or more of these risks materialise, or should underlying assumptions prove incorrect, our actual results

may differ materially from those anticipated. You should understand that a number of important factors could cause

actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such

forward-looking statements. These factors are discussed more fully in our most recent annual report on Form 20-F filed

on 27 September 2016 and in other filings with the United States Securities and Exchange Commission. The list of factors

discussed therein is not exhaustive; when relying on forward-looking statements to make investment decisions, you should

carefully consider both these factors and other uncertainties and events. Forward-looking statements apply only as of the

date on which they are made, and we do not undertake any obligation to update or revise any of them, whether as a result

of new information, future events or otherwise.

Please note: A billion is defined as one thousand million. All references to years refer to the financial year ended 30 June.

Any reference to a calendar year is prefaced by the word "calendar".

Comprehensive additional information is available on our website: www.sasol.com

INTRODUCTION

Bongani Nqwababa and Stephen Cornell

Joint Presidents and Chief Executive Officers

JSE: SOL NYSE: SSL

4

Key messages

● Strong results delivery and capital excellence focus despite continued market volatility

● Resilient operational and financial performance across our global business

● Improving focus on capital allocation to drive total shareholder return

● Lake Charles Chemicals Project (US) – on track and delivering on key project milestones

● Mozambique Production Sharing Agreement (PSA) – steady progress with drilling activities

yielding positive results

Secunda Chemicals Operations, South Africa Lake Charles Chemicals Project, Lake Charles, US

What you will hear today

5

● Operating model continues to deliver further efficiencies and effectiveness

● Foundation businesses safe, highly efficient and driving continuous improvement

● Proactive financial risk mitigation measures to protect and grow balance sheet

● Current portfolio profitable through the cycle

● Developing future investment opportunities

Lake Charles Chemicals Project, Lake Charles, US

Wax Expansion Project, Sasolburg, South Africa

Strong results delivery and capital excellence focus

despite continued market volatility

6

● Group safety performance, excluding illnesses, remained solid with an RCR of 0,27

● Regrettably three tragic fatalities in HY17

● Strong business performance across most of the value chain

● Secunda Synfuels Operations production volumes ▲1%, Eurasian operations ▲5%

● Normalised sales volumes ▲11% for Base Chemicals, ▲2% for Performance Chemicals

and liquid fuels ▼2%

● Cash fixed costs ▼1% in real terms, despite impact of mining strike

● Cost and cash savings initiatives exceeding targets, developing further opportunities

● Headline EPS ▼38% to R15,12 per share, EPS ▲19% to R14,21

● Interim dividend of R4,80 per share – based on annual 2,8x cover/36% payout

Sasol Mining, Secunda, South Africa Satellite Operations, Durban, South Africa

Resilient operational and financial performance

across our global business

7

● Long-term strategy being further refined

● Ensure robust capital allocation approach aimed at maximum sustainable returns to shareholders

● Focused interventions to close the current value gap

● Policy and structures in place to protect and strengthen the balance sheet

● Approach to be shared with investors in future engagements

Lake Charles Chemicals Project, Lake Charles, US

Sasol Synfuels, Secunda, South Africa

Improving focus on capital allocation

to drive total shareholder return

8

● Overall project almost two thirds complete with engineering at 94%

● Procurement activities nearly completed

● Capital expenditure to date of US$6,0 billion – tracking revised estimate

● Modularisation approach benefitting overall construction progress

● Above ground construction productivity tracking plan

● Good progress on operation and business readiness

● LCCP remains a sound investment that will return value to shareholders

● Confident that risks can be managed within current cost and schedule targets

Lake Charles Chemicals Project, Lake Charles, US

Lake Charles Chemicals Project, Lake Charles, US

LCCP on track and delivering

on key project milestones

9

● Mozambique facing major fiscal challenges

● Working very closely with all our partners to support them

● Confident that the challenges will be overcome

● Mitigating actions in place to minimise impact on Sasol

● Investments secure and will deliver future value to shareholders and other stakeholders

● Positive results from four wells drilled

● Nine additional wells to be drilled by end of 2018

● Loop Line 2 completed within schedule and significantly below budget

● Focus on securing gas feedstock to further enable our 2050 strategy

Central Processing Facility, Temane, Mozambique Drilling rig, Temane, Mozambique

Mozambique PSA – steady progress

with drilling activities yielding positive results

FINANCIAL AND OPERATIONAL

PERFORMANCE

Paul Victor

Chief Financial Officer

JSE: SOL NYSE: SSL

11

● Volatile macro environment continues, current rand strength will negatively impact earnings

● Continued focus on factors within our control

● Operational stability and production volumes remain a key deliverable

● Cost and cash savings initiatives providing headroom

● Protection and strengthening of balance sheet continues, liquidity remains strong

● Driving value-based growth strategy through sound and transparent capital allocation principles

● Outlook for FY17

Sasolburg Operations, Sasolburg, South Africa ORYX GTL, Ras Laffan, Qatar

Key messages

12

Chemical product prices trending up but exchange rate remains volatile

% c

han

ge

y-o

-y

Solvents basket Polymers basket Brent

$/m

mb

tu (

ga

s p

rice)

US

$/b

bl

Brent Product price Henry Hub

Product price differentials under pressure

US

$1 =

ZA

R

Volatile currency

Base chemical prices vs Brent

1H16 1H17

$2,44 $2,95

$47

$60

$48

1H16

Macro environment remains challenging

Prices reflect international commodities or baskets of commodities and are not necessarily Sasol specific

Sources: RSA Department of Energy, ICIS-LOR, Reuters, Platts, International Energy Agency

2% (7%)

4%

1H16 1H17

R13,62 R13,99

1H17

Product prices

R12,17

R15,48 R14,71

R13,74

US$/unit

Average

HY17

% ∆ vs

HY16

Brent/bbl 47,68 2▲

Fuel products/bbl 60,36 8▼

Base Chemicals/ton 764 6▼

Performance Chemicals/ton 1 255 6▼

Export coal/ton 71 35▲

Opening/closing rate Average rate during period

$65

13

11

2

34

13

40

Mining EPI PC BC Energy Group

Strong business performance across most of the value chain despite macro challenges

Group profitability

Solid operational performance supported by continued effective cost management

HY17 HY16 % ∆

Mining 1 534 2 359 35▼

Exploration and Production

International (EPI) 204 (8 289) >100▲

Performance Chemicals (PC) 4 647 5 161 10▼

Base Chemicals (BC) 1 733 3 178 45▼

Energy 5 529 10 261 46▼

Group Functions 25 2 246 99▼

Operating profit (Rm) 13 672 14 916 8▼

Earnings per share (R) 14,21 11,97 19▲

Headline earnings per share (R) 15,12 24,28 38▼

Dividend per share (R) 4,80 5,70 16▼

Capital expenditure (Rbn) 30,2 33,6 10▼

Operating profit %

14

Operating profit impacted by volatile macro environment

Headwinds

● Impact of stronger closing

exchange rate

● Steep decline in product

differentials and refining

margins, trending upwards

since November

● Lower average Base

Chemicals margins,

trending upwards since

November

Tailwinds

● Resilient Performance

Chemicals margins

● Cost and cash initiatives

delivering

● Higher sales volumes

● Higher average oil prices

since November

13 672

14 916

1%

1%

21%

(16%)

(15%)

0 4 000 8 000 12 000 16 000

HY17

Sales volumes

Cost and other

Once-off items andyear-end adjustments

Crude oil andproduct prices

Exchange rate

HY16

Rm

Operating profit

Macro

environ-

ment

Costs

and

volumes

15

22 628

21 307

21 429

0 5 000 10 000 15 000 20 000 25 000

HY17

Exchange rate

Inflation

Cash cost

Normalised cost

Mining strike

Cost increasebelow inflation

Sustainablebusiness savings

HY16

Rm

Cash fixed costs down 1% in real terms

Tailwinds

● Cost and value mindset

culturally entrenched

● Increased BPEP and

Response Plan savings

delivering in excess of

internal targets

● Maintaining focus and

priority, developing further

savings opportunities

Headwinds

● Strike action at Secunda

mines

Cash fixed costs

Costs and

volumes

Restructuring,

study and

growth cost

Macro

environment

1,6%

1,1%

(2,1%)

0,9%

(7,0%)

(0,1%)

16

FY14 FY15 FY16 FY17 FY18

Ra

nd

bill

ion

Project implementation cost Actual savings

Annualised expected savings

Targeting to deliver upper end of Response Plan range

● Savings of R54,9 billion achieved

since January 2015

● FY17 target increased to R26,0 billion

● Additional opportunities continuously

identified and implemented

● Sustainable savings target remains

R2,5 billion by FY19

● Delivered R4,9 billion in sustainable

savings to date

● On track to deliver FY17 target

of R5,0 billion

● Sustainable savings of R5,4 billion

by end FY18

0 5 10 15 20 25 30 35

Capital portfolio reductions and phasing

Cash cost savings

Capital structuring

Margin and working capital

Rbn

Actual savings to date Minimum target Upper target

Response Plan cost savings to end FY18 (42 months)

Business Performance Enhancement Programme

1,3 0,5

1,9 2,5

0,3

4,5

5,0 5,4

17

Mining and EPI Operating Business Units

Mining

● Operating profit decreased by 35%

● Export coal market prices higher

● Strike significantly impacted

profitability

● Business ramp-up from January 2017

on target

● Impact of strike

EPI ● Operating profit of R204 million

delivered through focused management interventions

● Strong Mozambique operations, volumes up 3%

● Canadian asset de-risking yielding benefits

● Gabon loss lower due to lower depreciation and increased prices

HY16 HY17

mm

to

ns

Production

HY16 HY17

mm

to

ns

External purchases

256

359

HY16 HY17

R/to

n

Unit cost/sales ton

HY16 HY17

Rm

Mozambique*

437

HY16 HY17

Op

era

tin

g p

rofit/(lo

ss)

Rm

Canada*

HY16 HY17

Rm

Gabon*

(7 769)

(312)

(512)

(41)

988

2,4

4,4

19,8

16,6

* Producing assets

18

Chemicals Strategic Business Units

Base Chemicals

● Sales volumes increased by 11%

● Operating profit down 45% to

R1 733m

● Strong closing R/US$ exchange rate

results in ~R900 million loss

● US$ prices anticipated to recover

during second half of FY17

Performance Chemicals

● Normalised sales volumes up 2%

● Operating profit down 10% to

R4 647m

● R527m impairment in US Phenolics

● Significant decline in ammonia pricing

● Phase 2 of FTWEP expected to reach

beneficial operation in March 2017

HY16 HY17

kt

Sales volumes

19

10

HY16 HY17

%

Operating profit margin

HY16 HY17

Rm

Operating profit

HY16 HY17

kt

Sales volumes

HY16 HY17

%

15 14

Operating profit margin

HY16 HY17

Rm

Operating profit

1 727 1 702 5 161 4 647

1 469 1 624

3 178

1 733

19

Energy Strategic Business Unit

Energy

● Liquid fuels sales volumes 2% lower

● Cash fixed costs down 2%

● Operating profit down 46% to

R5 529 million

● Petrol differential 38% lower, diesel

differential 12% lower

● Margins starting to recover

● ORYX GTL achieves 95% utilisation

● Normalised profit from joint ventures

10% higher

● EGTL scheduled to ramp-up during

first quarter of CY2017

Synfuels refined product Retail centres Liquid fuels sales

HY16 HY17

mm

bb

l

378 392

HY16 HY17

nu

mb

er

HY16 HY17

bscf

90 95

HY16 HY17

% 31

18

HY16 HY17

%

HY16 HY17

mm

bb

l

Operating profit margin Gas sales ORYX utilisation

30,2 29,6

17,1 15,8

29,4 29,6

20

Focused value-based capital allocation Maintain strong balance sheet and liquidity

Driving disciplined and transparent capital allocation

* Up to 2,2x cover / 45% payout

License to operate

and sustenance capex Minimum

shareholder return

(2,8x cover/

36% payout)

Special dividends

and share buy backs

Balance sheet protection will take precedence

if investment grade credit rating at risk

Deliver maximum sustainable shareholder return

Sources

of capital Allocation of capital

Capital allocation guided by key financial metrics – Gearing, Net debt:EBITDA and ROIC

All three elements

compete equally

for capital

Equity raise

Debt

drawdown

Cash flow

from

operations

Cash

on hand Strengthen

balance sheet

Value-based

growth capex

Premium

shareholder

return*

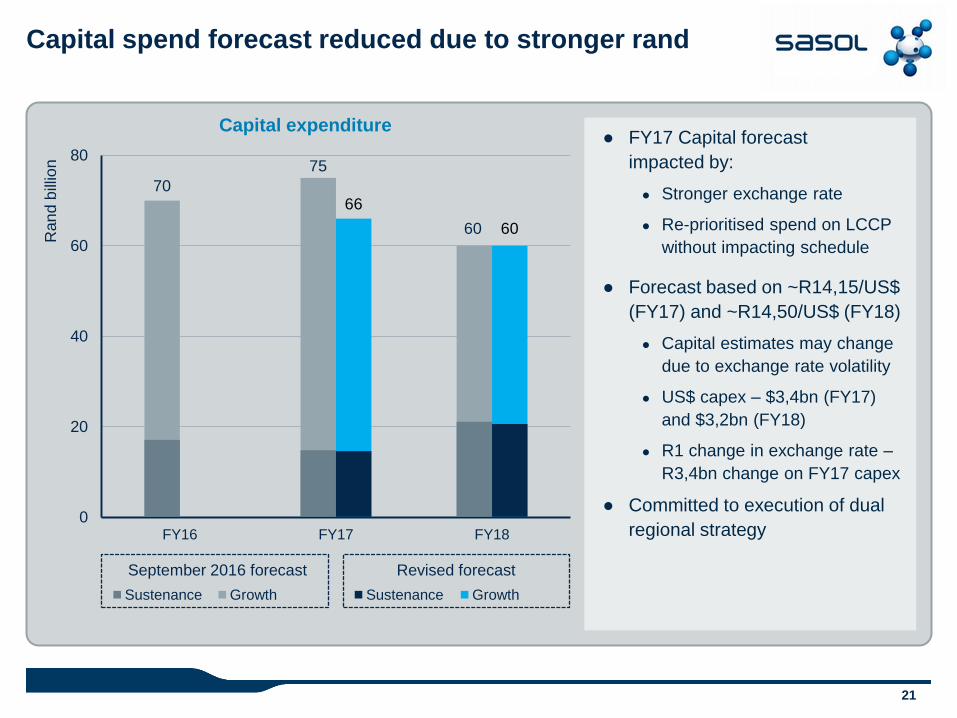

21

70

75

60

66

60

0

20

40

60

80

FY16 FY17 FY18

Ran

d b

illio

n

Capital spend forecast reduced due to stronger rand

● FY17 Capital forecast

impacted by:

● Stronger exchange rate

● Re-prioritised spend on LCCP

without impacting schedule

● Forecast based on ~R14,15/US$

(FY17) and ~R14,50/US$ (FY18)

● Capital estimates may change

due to exchange rate volatility

● US$ capex – $3,4bn (FY17)

and $3,2bn (FY18)

● R1 change in exchange rate –

R3,4bn change on FY17 capex

● Committed to execution of dual

regional strategy

September 2016 forecast

Growth Sustenance

Revised forecast

Sustenance Growth

Capital expenditure

22

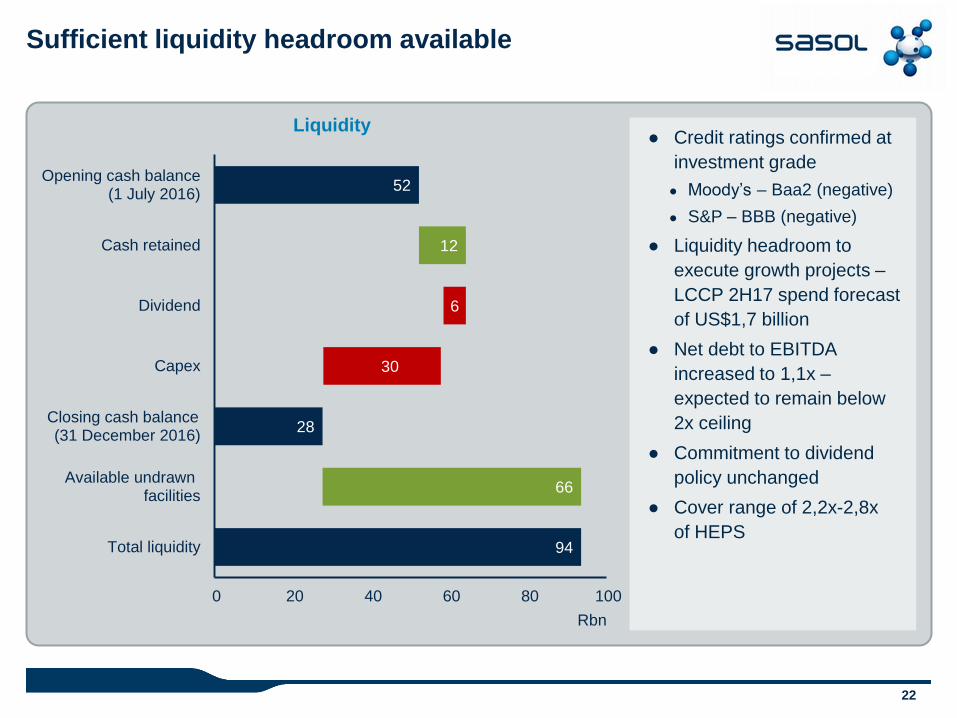

94

28

52

66

12

30

6

0 20 40 60 80 100

Total liquidity

Available undrawn facilities

Closing cash balance (31 December 2016)

Capex

Dividend

Cash retained

Opening cash balance (1 July 2016)

Rbn

Sufficient liquidity headroom available

● Credit ratings confirmed at

investment grade

● Moody’s – Baa2 (negative)

● S&P – BBB (negative)

● Liquidity headroom to

execute growth projects –

LCCP 2H17 spend forecast

of US$1,7 billion

● Net debt to EBITDA

increased to 1,1x –

expected to remain below

2x ceiling

● Commitment to dividend

policy unchanged

● Cover range of 2,2x-2,8x

of HEPS

Liquidity

23

FY17 Outlook

Outlook

Mining Return to full production with corresponding cost performance

to follow inflation

EPI Increased gas production from PPA ● PSA drilling activities to continue

● No drilling activity in Canada

Energy Liquid fuels sales approximately 61 million barrels

● ORYX GTL average utilisation >90%

Base Chemicals Sales volumes 4-6% higher than prior year ● US$ selling prices recovering

● Gemini HDPE to reach mechanical completion by middle CY17

Performance Chemicals Sales volumes 1-2% higher than prior year ● Margins to remain resilient

● FTWEP phase 2 BO imminent, full benefit by FY19

Group

Normalised cash fixed costs to track SA PPI ● RP cash flow contribution

of R22-R26bn ● BPEP cost savings to achieve run-rate of R5,4bn by 2018

● Balance sheet gearing between 30-35%

QUESTIONS AND ANSWERS

Bongani Nqwababa and Stephen Cornell

Joint Presidents and Chief Executive Officers

JSE: SOL NYSE: SSL

![SPENCER LAKE CAMPS CHARLES T. BRATTEN, … LAKE CAMPS CHARLES T. BRATTEN, Proprietor [picture] Gerard Somerset County Maine. Spencer Lake Camps In the Heart of the Great Maine Woods](https://static.fdocuments.net/doc/165x107/5ac422a47f8b9a2b5c8cc974/spencer-lake-camps-charles-t-bratten-lake-camps-charles-t-bratten-proprietor.jpg)