Transforming the business of retail banking · PDF fileTransforming the business of retail...

20

Transforming the business of retail banking How retail banks could use innovation to reduce their costs while regaining customers

Transcript of Transforming the business of retail banking · PDF fileTransforming the business of retail...

Transforming the business of retail bankingHow retail banks could use innovation to reduce their costs while regaining customers

“The railroads did not stop growing because the need for passenger and freight transportation declined. That grew. The railroads are in trouble today not because that need was filled by others (cars, trucks, airplanes, and even telephones) but because it was filled by the railroads themselves. They let others take customers away from them because they assumed themselves to be in the railroad business rather than in the transportation business. The reason they defined their industry incorrectly was that they were railroad oriented instead of transportation oriented; they were product oriented instead of customer oriented.”

Theodore Levitt, Marketing Myopia, Harvard Business Review, 1960

2

What business are banks in, if they’re not in the banking business?In a famous essay, Theodore Levitt coined the phrase ‘marketing myopia’ to describe companies who lost sight of their business aims. As well as railways, Levitt talked about Hollywood’s early relationship with TV, explaining that, because Hollywood defined its business as ‘movies’ rather than ‘entertainment’ the industry saw TV as a threat rather than an opportunity.

Sound familiar?

It’s obvious that, whatever economic conditions consumers are in and wherever they live, people will continue borrowing money, trying to save money and moving money from one place to another. If they trusted their banks more – a confidence lost over the last 30 years – they would even seek advice from them.

So in light of Levitt’s comments, what business are banks in if they are not in the banking business? Put simply, retail banks are in the business of helping people, communities and enterprises achieve their financial goals.

In that sense, we could consider PayPal as a form of retail bank; its famous digital wallet now counts 110 million active users among which 2.6 million make an average of 98 online purchases per year, spending an average of $4,214 annually.*

And this company did not exist at all 10 years ago…

(*Source: www.paypal.com)

3

4

Helping people, communities and enterprises achieve their financial goalsAs a definition of retail banking, this is hardly a groundbreaking idea, but not one that bankers spend a lot of their time and energy addressing. Let’s be realistic: while shareholders and regulators can’t be ignored, customers really don’t care about the bank’s net interest margin or the duration of its loan book.

Helping customers achieve financial goals means being there when they need you and being able to answer their questions without delay; making it simpler and easier for everyone to move money, borrow money or save money. That doesn’t necessarily mean having a branch in each village; besides the high costs associated with this, there’s little to differentiate from other banks or in comparison with pure online players.

Banks that thrive in this new era will find new ways to be relevant and provide value to their customers, and some of those ways may not involve traditional banking products. Bankers need to really listen to their customers, discover their financial pain points and embrace creative ways to address them.

If they don’t, someone else will.

Bankers sometimes take too much comfort in the perceived protection of operating in a highly regulated sector. But relying on regulations to protect the industry will only hasten its reduction to utility status.

The healthcare industry is one of the most heavily controlled and regulated. And yet, out of the top 20 companies by research and development spending, eight are in healthcare.

Despite a highly regulated environment, the healthcare industry invests 11% to 19.6% of its revenues back into R&D. According to a Booz & Co. Global Innovation 1000 study, healthcare accounted for 20.9% of the $603 billion spent globally on R&D in 2011.

Among all sectors, financial institutions don’t even make the list, lumped in instead with the 2% of “other” industries, collectively in last place.

Regulation: a poor excuse for not innovating

5

Why banks, and especially the retail branches, need to changeThere are three sides to this: the bank, the customer and the market.

1. Banks

Over the past fifteen years, many banks have developed online services, using various forms of telecommunications technologies (PSTN kiosk services such as Minitel, internet, WAP or even 3G) to provide most of their traditional services without customers having to visit a branch.

The power of the web, combined with the spread of consumer technologies has changed the dynamic in the branch, as customers can feel that they know more about the market or the products than many of the agents.

So traditional banks have succeeded in their online strategy, but unfortunately this strategy was standalone and not thought of in correlation with a transformation programme for branch services. The result is that fewer customers come into the branch and find no real value in doing so.

In the meantime, new players have come onto the scene and thrived with a pure online model which avoids the fixed costs attributable to the thousands of high street retail branches. While many of these new pure players struggled in the early 2000s, new distribution channels have risen, contributing to a steady 5%-7% p.a. erosion of branch activity.

Traditional retail banks now face the challenge of changing their retail model and demonstrating the value of a physical branch where customers can meet informed advisors. In Europe, branches account for 60% of the total costs of retail banking activity, with an average of 450 branches per million inhabitants (or 600 in France).*

(*Source: Score Advisor)

2. Customers

There are new consumers around on both sides of the spectrum: older babyboomers and Gen-Y customers. The former are not fully up to speed when it comes to new technologies but they manage a sizeable amount of consumer wealth (as an example, the annual income of the over 50s in the UK represents > 80 % of the UK private wealth, tied up in houses, shares etc). They’ll live much longer than their parents but will most likely develop more illnesses, such as Parkinson’s or Alzheimer’s (a recent study in the USA showed that in 2050, there will be 32 million people over 80, with half of them having Alzheimer’s and 3 million having Parkinson’s).

Gen-Y consumers are born into the technology and don’t fully understand the concept of loyalty to a bank. They use many channels simultaneously to engage with friends or shop and will probably face massive financial issues. As a more general trend across all generations, the consumer’s approach to the high street has changed, with a massive move to shopping malls.

6

3. Market

The financial sector at large now faces ever-increasing regulatory pressure. This drives banks to reduce CAPEX, which increases the costs for addressing regulatory and compliance constraints. Added to this are the tougher economic conditions we’ve seen in the West, where many are in an almost recessionary status.

We’ll examine the benefits innovation has already brought, or could bring, to retail banking whether in Western countries, other fast growing regions such as Asia and the Middle East, or even in ‘underbanked’ areas like Africa.

How can retail branches become:

• customer-focusedfit for all purposes, capable of actually answering a customer’s question while the customer is still in the branch

• socially responsiblenot only green and sustainable, but also with a particular attention to the wellbeing and expectations of their personnel as well as their customers

• thinwith low operational costs

• agilescalable (to accommodate seasonal or demographic effects), but nevertheless still physically present where their customers want them be

…while balancing the three sides (banks, customers, market) described above?

Competitive challenges traditional retail banks are facing

7

Customer focused: meeting the challenge of changing expectationsBT undertakes a lot of research in the financial services sector, focusing in particular on what banking customers are most unhappy about and what they expect from their bank.

A joint study by BT and the Henley Centre for Customer Management shows that reducing “customer effort” when it comes to banking activities is a key measure for customer loyalty. While 94% of the customers who reported low effort said they’d buy again, 81% of customers who had a hard time solving their problems said they’d spread negative word of mouth.

BT’s regular Youbiquity Finance research with Avaya focuses on the branch and face-to-face communication, to highlight the changes in consumer behaviour. These studies have found:

• 62% of retail banking customers go to their branch to solve a complicated issue

• 50% say they wait too long in the branch to see an advisor

• 33% say the staff either do not have the power or knowledge to resolve problems immediately

• 43% say negative feedback on social media would make them move bank or avoid a bank

• 69% agree that a good experience with branch or contact centre staff improves loyalty

• 34% want more knowledgeable staff and 36% want a friendly welcome when they walk into a branch (when comparing banks to retailers).

So what can you do to address these concerns?

8

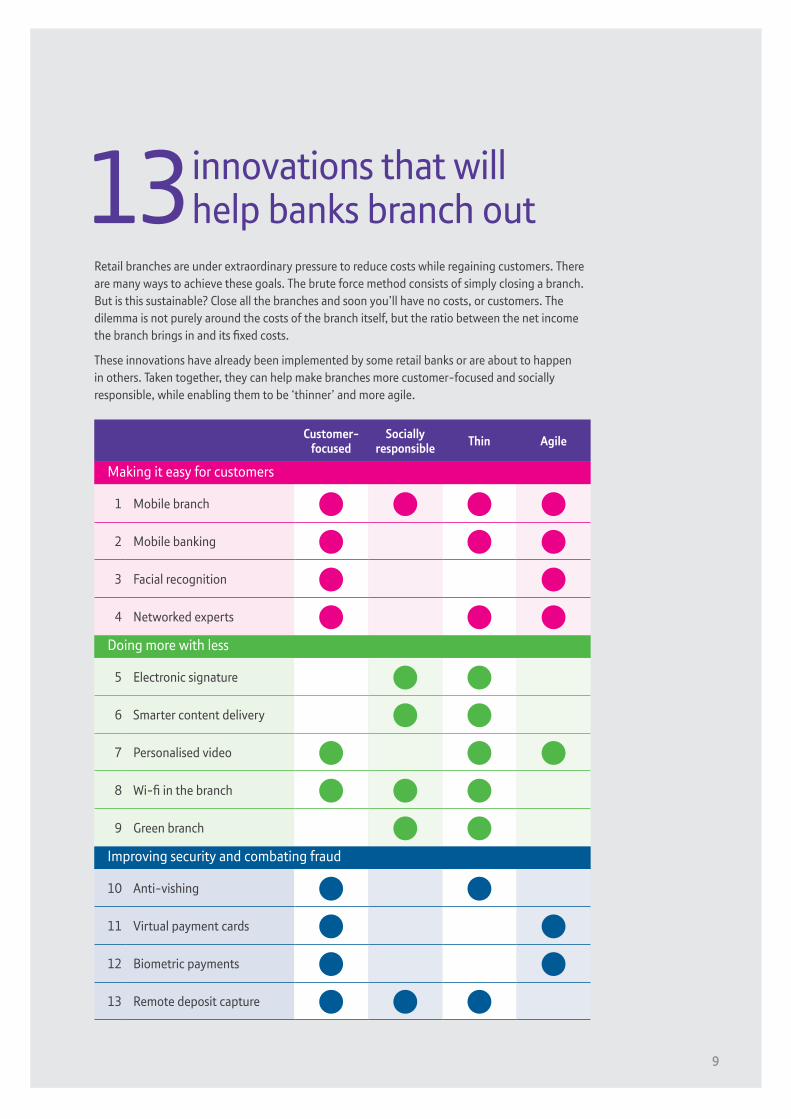

13 innovations that will help banks branch out

Retail branches are under extraordinary pressure to reduce costs while regaining customers. There are many ways to achieve these goals. The brute force method consists of simply closing a branch. But is this sustainable? Close all the branches and soon you’ll have no costs, or customers. The dilemma is not purely around the costs of the branch itself, but the ratio between the net income the branch brings in and its fixed costs.

These innovations have already been implemented by some retail banks or are about to happen in others. Taken together, they can help make branches more customer-focused and socially responsible, while enabling them to be ‘thinner’ and more agile.

Customer-focused

Socially responsible Thin Agile

Making it easy for customers

1 Mobile branch

2 Mobile banking

3 Facial recognition

4 Networked experts

Doing more with less

5 Electronic signature

6 Smarter content delivery

7 Personalised video

8 Wi-fi in the branch

9 Green branch

Improving security and combating fraud

10 Anti-vishing

11 Virtual payment cards

12 Biometric payments

13 Remote deposit capture

9

10

Making it easy for customers

1. Mobile branch

For most customers, mobile banking is an app on a smartphone that allows them to check their account and make payments. But in some remote parts, mobile banking is a customised vehicle that visits isolated communities at regular intervals.

These branches have all the facilities of a brick and mortar branch, and reach more customers at a much reduced operating cost. Other low-cost options, including off-site ATMs and unstaffed kiosks, offer a more restricted range and are not suitable for really remote locations because they need a power supply and security for restocking them with cash.

Mobile branches are not a new concept, but they can mitigate the seasonal effects seen in some touristic areas and can help solve the dilemma of continuing to serve remote locations. Being able to deploy mobile branches instead of investing in a new brick and mortar building also opens new marketing possibilities to the retail bank, such as covering exhibitions and special events for a short period of time.

As it’s capable of testing new geo-marketing outputs at minimal cost, the bank will be in a position to fully exploit all the data that it has stored for years about its customers. Most banks currently lack the power to crunch this huge amount of data, whether structured in its own databases, or unstructured (internet and social media), and are also short of analysts to interpret the outputs. This is where a powerful big data-crunching engine and a user friendly interface, capable of helping a non-expert visually analyse and interpret the output, is needed.

“Not so very long ago banks would expect to incur half a million pounds or dollars in fixed costs and the same in variable costs to establish a presence and would calculate they needed 10,000 people to justify a physical presence. But that was probably not the brightest way to think about it; so they look at the customer footprint to find out what sort of an outlet they wanted where. This could involve providing a service from the back of a van or light planes landing on a beach. It could involve agency banking from a solicitor’s office or sharing the counter of the general store with fishing nets, newspapers and packs of cigarettes.”

Andy Maguire, global head of the retail banking practice, Boston Consulting Group

(Source: www.ft.com)

11

2. Mobile banking

Mobile payments have been growing rapidly in recent years and continue to do so, with Gartner forecasting a 44% jump in the value of mobile payment transactions from 2012. However, as Don Callahan, head of operations & technology at Citigroup, points out: “The shocking part is how little change is actually taking place. Of the world’s seven billion people, more than five billion have mobile phones, but there are just 1.8 billion bank accounts.”

Real opportunities for banks to reach remote customers have emerged with the growth of the internet and the mobile phone. In Africa and other parts of the developing world that lack a traditional banking and fixed line telephone infrastructure, mobile networks have filled the gap, providing mobile-to-mobile payment services.

The use of smartphones to make cash transfers is now spreading to the developed world. We’ve seen new non-bank players like M-PESA and PayPal coming in and thriving, and banks need to be aware of the challenge these competitors pose.

In South Africa, which straddles the developed and developing worlds, FirstRand Bank claims to have turned itself into the country’s largest vendor of iPhones and other smart devices in an attempt to attract customers and increase the range of services used by existing customers.

This year, Barclays launched Pingit for its 12m current account customers, allowing them to transfer money to anyone via a mobile phone. Contactless payments, made by holding a phone against a reader, are also forecast to grow (not without some security concerns as we will see below) and some famous high street names in the US and UK have already trialed these new payment methods.

“It is not a question of competition between the phone companies and the banks, it is more about what are the right terms of co-operation. The phone companies can provide the channels but you will need a bank or a banking structure to facilitate transactions.”

Ranu Dayal, senior partner, BCG’s financial institutions practice

12

3. Facial recognition

Personal video tools like Facetime and Skype are changing our expectations of the way we want to interact with remote colleagues and key suppliers – such as our bank advisor. As customers we don’t want to have to go into a branch (either because it’s not close by, or not open at suitable times). A video call can be a more convenient and richer experience for both the customer and the advisor.

With connected information about their accounts, products or other financial services, customers could either get the answer directly from the advisor in the branch, or take part in a three-way video conference, where an expert could be called in. The video could be recorded and sent to the customer by email at the end of the call, along with some additional information.

Taking video a stage further, a customer could then walk into any branch of his bank and be recognised as a valued customer. Facial recognition features are available on standard CCTV cameras now and (provided the customer has opted-in) could be used to display customised messages on digital screens.

4. Networked experts

With customers increasingly feeling more knowledgeable than advisors, and retail banks unable to afford more specialised personnel due to the enormous pressure to reduce the fixed costs of their branches, how can we make sure customers get the right answers, whichever branch they visit?

The simple way would be to network the appropriate expert with the customer, whether at home, at work or physically in a branch via an advisor.

Networking the advisors and experts can even open the door to other possibilities. Retail banks could deploy self-service kiosked ATMs in some remote areas where a physical branch would be too expensive. These full featured ATMs would allow a customer to have a video chat with an advisor or an expert while enjoying the privacy of a closed environment, despite being in a public space.

But there are a number of things to consider before doing this: In order to know which advisor to contact, we would need to know which topics advisors are experts on, which means keeping a central database up to date. How would you control the accuracy of this database, who should have access to it and how could this influence the career of an advisor? All these questions need to be addressed by the bank’s HR department before it can implement a networked expert service.

Also, most branches (if not 100%) are assigned a portfolio of customers which correspond more or less to their geographical footprint. If you had an advisor answering a video call for the benefit of another branch, how should this be rewarded?

So a simple technological solution generates a much more fundamental question about the retail organisation.

13

Doing more with less

5. Electronic signature

We’ve all experienced the process of opening a new bank account or agreeing a new loan – and the paperwork this generates. Once you’ve signed those forms, the bank will have to store them for the duration of the contract and beyond. The cost for this activity is massive.

We now see more and more retail banks adopting electronic documents and signatures. This technology not only saves paper and storage costs, it also increases the bank’s CSR (Corporate Social Responsibility) index and greatly improves the customer experience.

6. Smarter content delivery

How can you deliver high quality video to branches without increasing the bandwidth or congesting the Wide Area Network? There are solutions today that do not require any CAPEX and will dynamically adapt to your existing network, preserving the bandwidth for critical applications. Implementing these solutions can help you make the most of your infrastructure and open the door to new applications.

With smarter content delivery solutions, you’ll be able to play high quality videos in branches to train advisors and tellers in new regulatory and compliance rules, and check that they’ve actually followed the training until the end. You’ll also be able to broadcast content, such as new product brochures, across your network.

Smarter content delivery solutions mean that, without spending more on your network, you’ll be capable of doing much more with it, both for your employees and for your customers.

7. Personalised video

New computing technologies enable banks to send personalised videos to their customers, providing clearer and simpler communications, reducing customer service calls and improving customer experience, loyalty and retention.

Not only is it cheaper for the bank to produce (compared to sending regular paper adverts to customers) but click-through rates are about 20% higher than generic communications.

14

8. Green branch

How do you control the environmental impact of your retail branches? In recent years, many banks have re-negotiated their telco contracts and, without knowing it, have probably opted for cheaper routers or switches which are actually more power-hungry and raise the heat in their comms rooms, increasing the need for more cooling.

There are power management solutions available now that enable you to centrally monitor and manage all the energy consuming equipment in your remote branches and head offices, whether IT equipment or non IT (such as lighting, heating and air conditioning). Not only is this a massive opportunity to save costs, it also increases your CSR index, which improves the perception of your brand as customers are more aware of the impact of CSR.

9. Wi-fi branch

More than 60% of the costs of a bank’s retail organisation come from maintaining branches. Within this, the network infrastructure is a significant aspect. The branch environment is very much constrained in terms of furniture, cabling, offices and customer setup, and any proposed addition to the branch network infrastructure to address new requirements becomes a very touchy subject.

With the rise of 4th generation mobile communications and the evolution of wi-fi technology, both from a bandwidth and security point of view, some banks are now seriously thinking about setting up new branches with a very thin network infrastructure covering all its needs, i.e. through a ‘Branch in a box’ infrastructure including in-branch wi-fi, and secure xDSL access backed up by 3G/4G.

15

Improving security and combating fraud

10. Anti-vishing

Security is in a bank’s DNA. All banks have systems to monitor security events, prevent intrusion or detect attacks – or most likely a combination of all of these. But they’ve usually concentrated their effort on the data network.

When it comes to voice telephony in the branches and head offices, or when talking about contact centres, banks have traditionally taken a more DIY approach, though this may not be the most efficient and reliable way of doing things.

We’ve seen some devastating Telephony Denial of Service (TDoS) attacks over the first quarter of 2013, in both the US and Europe, with massive financial consequences to the banks. TDoS attacks on businesses are profitable for criminals and are difficult for the enterprise to detect.

Vishing, or voice phishing, is the criminal practice of using features facilitated by Voice over IP (VoIP), to gain access to private personal and financial information.

Implementing anti-vishing solutions in retail banking, such as those BT has deployed for its customers, can preventively save considerable amounts of money.

11. Virtual payment cards

Despite the fact that credit card fraud exists on the internet, the use of virtual payment cards (VPC) is not widespread because the fraud ratio is currently considered “acceptable”.

VPC is, however, a very safe way of preventing credit card fraud and can save the costs of sending fraud alerts to customers and re-issuing credit cards to those customers that have been affected, not counting the detrimental effect on the bank’s image.

12. Biometrics payments

Another way to prevent fraud while improving the customer experience is to use biometric data to authenticate a customer before authorising a payment. There are various ways of using biometrics, the most visible being implemented in new generation ATMs like those you may see in the UAE (using palm vein authentication) or in Japan (finger vein).

BT has successfully used finger vein authentication as a temporary replacement for credit cards during closed events (e.g. festivals). Finger vein technology can also be used to reinforce security before actually validating a transaction (whether mobile or physical) such as a large withdrawal or money transfer.

16

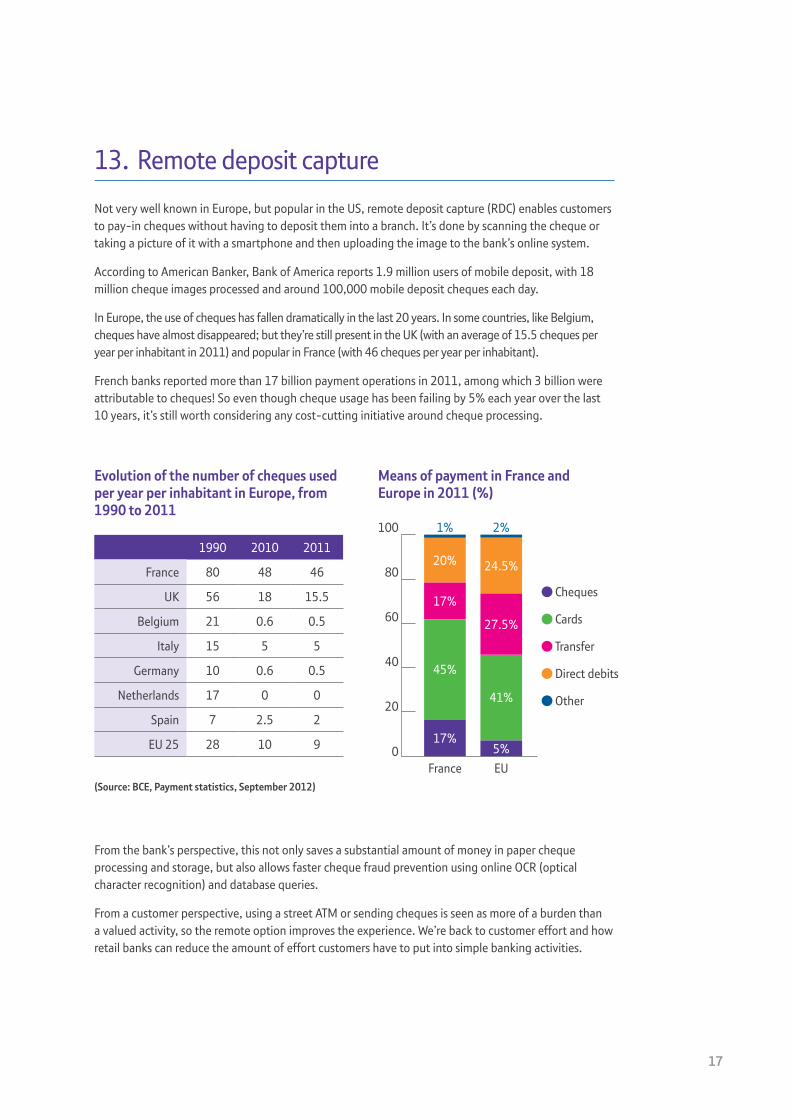

Evolution of the number of cheques used per year per inhabitant in Europe, from 1990 to 2011

From the bank’s perspective, this not only saves a substantial amount of money in paper cheque processing and storage, but also allows faster cheque fraud prevention using online OCR (optical character recognition) and database queries.

From a customer perspective, using a street ATM or sending cheques is seen as more of a burden than a valued activity, so the remote option improves the experience. We’re back to customer effort and how retail banks can reduce the amount of effort customers have to put into simple banking activities.

(Source: BCE, Payment statistics, September 2012)

13. Remote deposit capture

Not very well known in Europe, but popular in the US, remote deposit capture (RDC) enables customers to pay-in cheques without having to deposit them into a branch. It’s done by scanning the cheque or taking a picture of it with a smartphone and then uploading the image to the bank’s online system.

According to American Banker, Bank of America reports 1.9 million users of mobile deposit, with 18 million cheque images processed and around 100,000 mobile deposit cheques each day.

In Europe, the use of cheques has fallen dramatically in the last 20 years. In some countries, like Belgium, cheques have almost disappeared; but they’re still present in the UK (with an average of 15.5 cheques per year per inhabitant in 2011) and popular in France (with 46 cheques per year per inhabitant).

French banks reported more than 17 billion payment operations in 2011, among which 3 billion were attributable to cheques! So even though cheque usage has been failing by 5% each year over the last 10 years, it’s still worth considering any cost-cutting initiative around cheque processing.

1990 2010 2011

France 80 48 46

UK 56 18 15.5

Belgium 21 0.6 0.5

Italy 15 5 5

Germany 10 0.6 0.5

Netherlands 17 0 0

Spain 7 2.5 2

EU 25 28 10 9

Means of payment in France and Europe in 2011 (%)

France

100

80

60

40

20

0EU

Cheques

Cards

Transfer

Direct debits

Other

2%1%

20%

17%

45%

17%

24.5%

27.5%

41%

5%

17

18

ConclusionAnalysts agree that retail banking will change dramatically over the next five to ten years. Many predict the closure of branches and loss of jobs, but very few talk about how the business of banking is evolving and what banks have to do to reinforce the relationship between them and their customers.

Not only will customer profiles change for demographic reasons, technology will enable customers to adapt their approach to banking. Driven by the pressure of increasing regulation and the growth of emerging markets, banks will also have to change the way they understand their retail business.

We’ve seen several examples where innovation can help banks get closer to their customers and make it easier for them to efficiently interact with advisors. We’ve also seen how some simple innovations can make the retail bank more customer-focused, more agile and more socially responsible, while decreasing its costs base.

Many of these innovations are fairly simple to implement, but the transformation of retail banking will not be successful if it’s driven from above: it has to be a co-operative transformation.

Retail bank managers will have to accept that the rules of the game have changed, as telecommunications technologies break down geographical barriers. And there will be a strong need for training and motivating tellers and advisors, making them understand how new technologies and innovations can help them get closer to customers, regain their trust, and be perceived as truly bringing value.

In order to be a real success, banks will have to get all retail banking employees, in particular the tellers and financial advisors, on board. These are probably the ones most fearing the future, as they work with the ever-present threat of branch closures, making change a difficult thing to embrace without proper coaching and reassurance.

The transformation in retail banking might not be just a technology transformation, but a business and a human one as well.

19

Offices worldwide

The telecommunications services described in this publication are subject to availability and may be modified from time to time. Services and equipment are provided subject to British Telecommunications plc’s respective standard conditions of contract. Nothing in this publication forms any part of any contract.

© British Telecommunications plc 2013 Registered office: 81 Newgate Street, London EC1A 7AJ Registered in England No: 1800000

Designed by Westhill.co.uk

Printed in England

PHME 68584

Visit www.bt.com/gbfm for more information on BT for Financial Services