Transform research: The age of omnichannel banking 2015

53

The age of omnichannel banking Why omnichannel is the next wave of retail banking innovation

-

Upload

transformuk -

Category

Business

-

view

779 -

download

5

Transcript of Transform research: The age of omnichannel banking 2015

The age of omnichannel banking

Why omnichannel is the next wave of retail banking innovation

2

Introduction: The Omnichannel age of retail banking

The death and destruction of traditional bank branches caused by digital and changing customer dynamics is widely foretold.

But even digital natives are dual citizens of the physical world. Branch location is still customers’ strongest reason for switching current account and retail customers still want branches for important elements of sales and service.

Retail is increasingly moving towards Omnichannel; enabling customers to do business on whatever mix of channels they choose. How channels are integrated is becoming as important as what channels are available.

This has big implications for banks. Too often today, it is almost as if the digital and bank branch experience is designed and built by different companies. In the future, digital will underpin how banks deliver great customer experiences across channels.

In this report we explore what drives the shift towards Omnichannel, how banks are performing today and a vision for Omnichannel banking in the future.

Simon is a Transform Associate and a former Head of Product at Barclays Bank

James is Financial Services practice lead for Transform

3

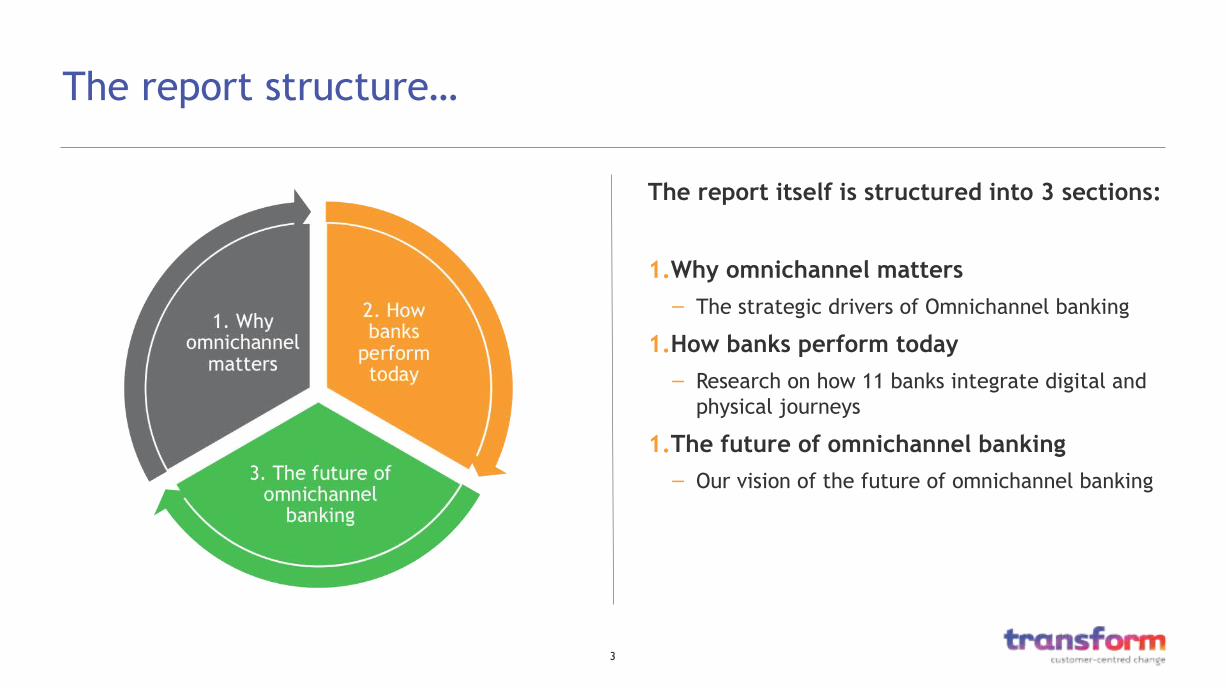

The report structure…

The report itself is structured into 3 sections:

1.Why omnichannel matters

– The strategic drivers of Omnichannel banking

1.How banks perform today

– Research on how 11 banks integrate digital and physical journeys

1.The future of omnichannel banking

– Our vision of the future of omnichannel banking

4

The banks we surveyed..

• Transform’s primary research was concluded in March 2015 across 11 high street retail banks. The research focussed on the experience delivered to new customers and comprised:– a mystery shopping exercise testing

aspects of branch customer experience

– a feature benchmark of digital capabilities

Executive Summary

6

Executive Summary

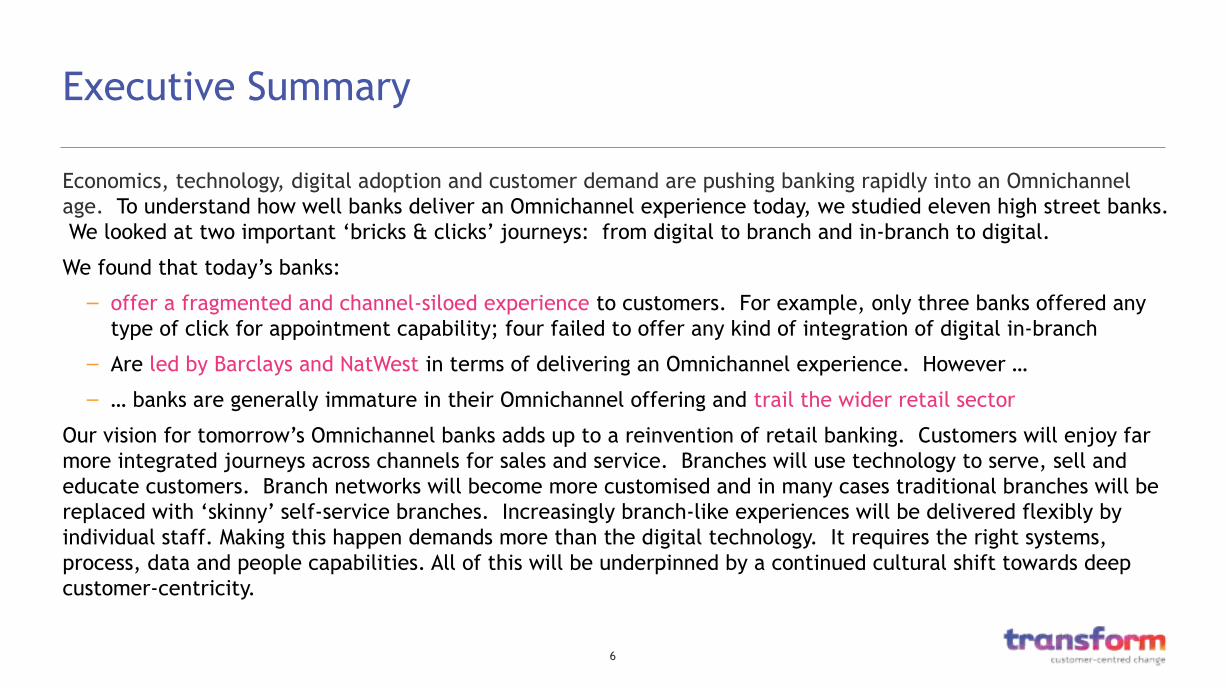

Economics, technology, digital adoption and customer demand are pushing banking rapidly into an Omnichannel age. To understand how well banks deliver an Omnichannel experience today, we studied eleven high street banks. We looked at two important ‘bricks & clicks’ journeys: from digital to branch and in-branch to digital.

We found that today’s banks:

– offer a fragmented and channel-siloed experience to customers. For example, only three banks offered any type of click for appointment capability; four failed to offer any kind of integration of digital in-branch

– Are led by Barclays and NatWest in terms of delivering an Omnichannel experience. However …

– … banks are generally immature in their Omnichannel offering and trail the wider retail sector

Our vision for tomorrow’s Omnichannel banks adds up to a reinvention of retail banking. Customers will enjoy far more integrated journeys across channels for sales and service. Branches will use technology to serve, sell and educate customers. Branch networks will become more customised and in many cases traditional branches will be replaced with ‘skinny’ self-service branches. Increasingly branch-like experiences will be delivered flexibly by individual staff. Making this happen demands more than the digital technology. It requires the right systems, process, data and people capabilities. All of this will be underpinned by a continued cultural shift towards deep customer-centricity.

Why omnichannel matters

The strategic drivers of omnichannel banking

8

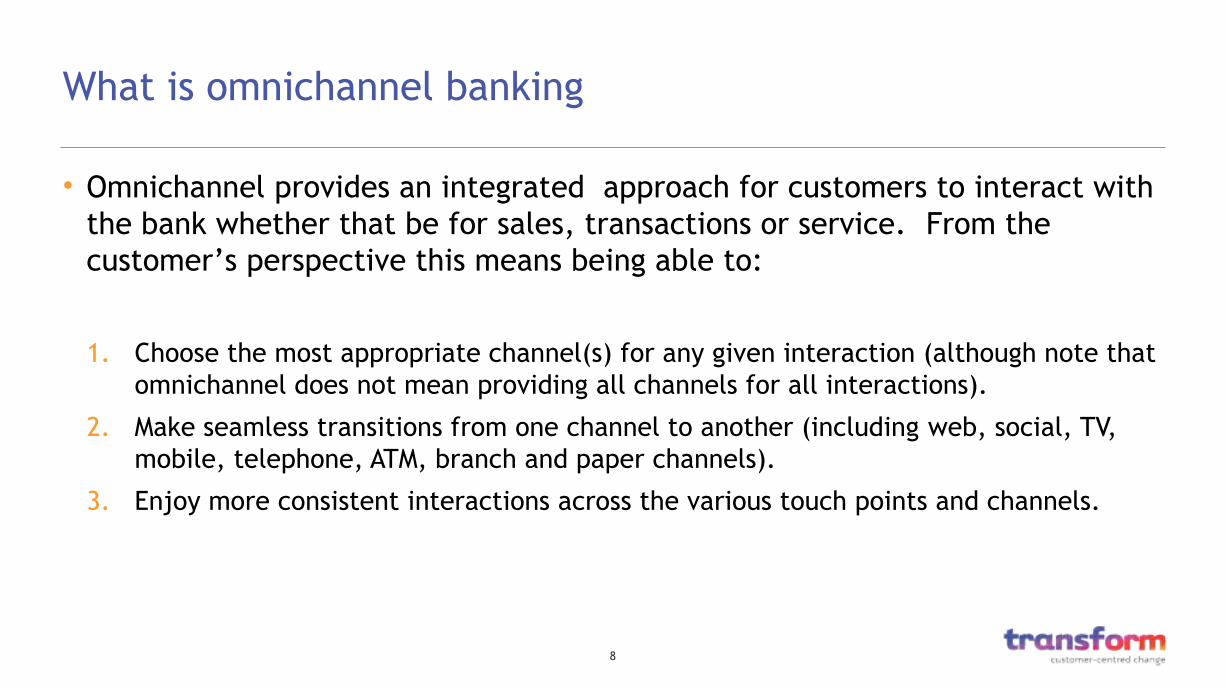

What is omnichannel banking

• Omnichannel provides an integrated approach for customers to interact with the bank whether that be for sales, transactions or service. From the customer’s perspective this means being able to:

1. Choose the most appropriate channel(s) for any given interaction (although note that omnichannel does not mean providing all channels for all interactions).

2. Make seamless transitions from one channel to another (including web, social, TV, mobile, telephone, ATM, branch and paper channels).

3. Enjoy more consistent interactions across the various touch points and channels.

9

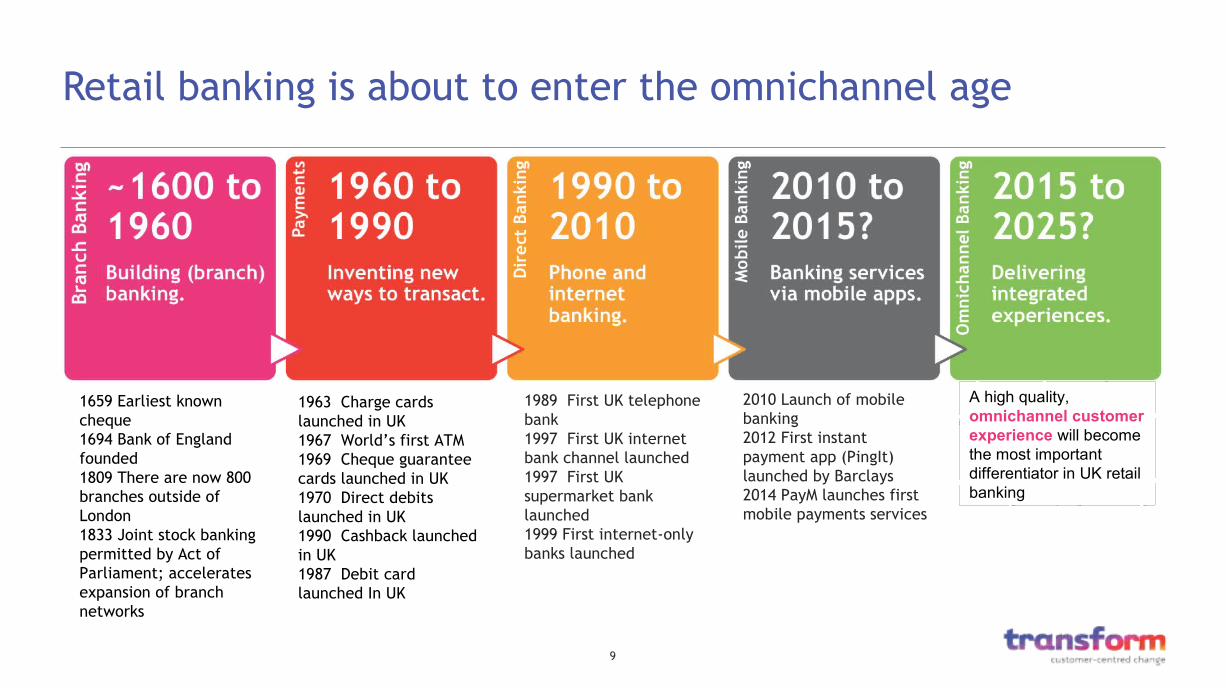

Retail banking is about to enter the omnichannel age

1963 Charge cards launched in UK1967 World’s first ATM1969 Cheque guarantee cards launched in UK1970 Direct debits launched in UK1990 Cashback launched in UK1987 Debit card launched In UK

1989 First UK telephone bank1997 First UK internet bank channel launched1997 First UK supermarket bank launched1999 First internet-only banks launched

2010 Launch of mobile banking2012 First instant payment app (PingIt) launched by Barclays2014 PayM launches first mobile payments services

A high quality, omnichannel customer experience will become the most important differentiator in UK retail banking

1659 Earliest known cheque1694 Bank of England founded1809 There are now 800 branches outside of London1833 Joint stock banking permitted by Act of Parliament; accelerates expansion of branch networks

10

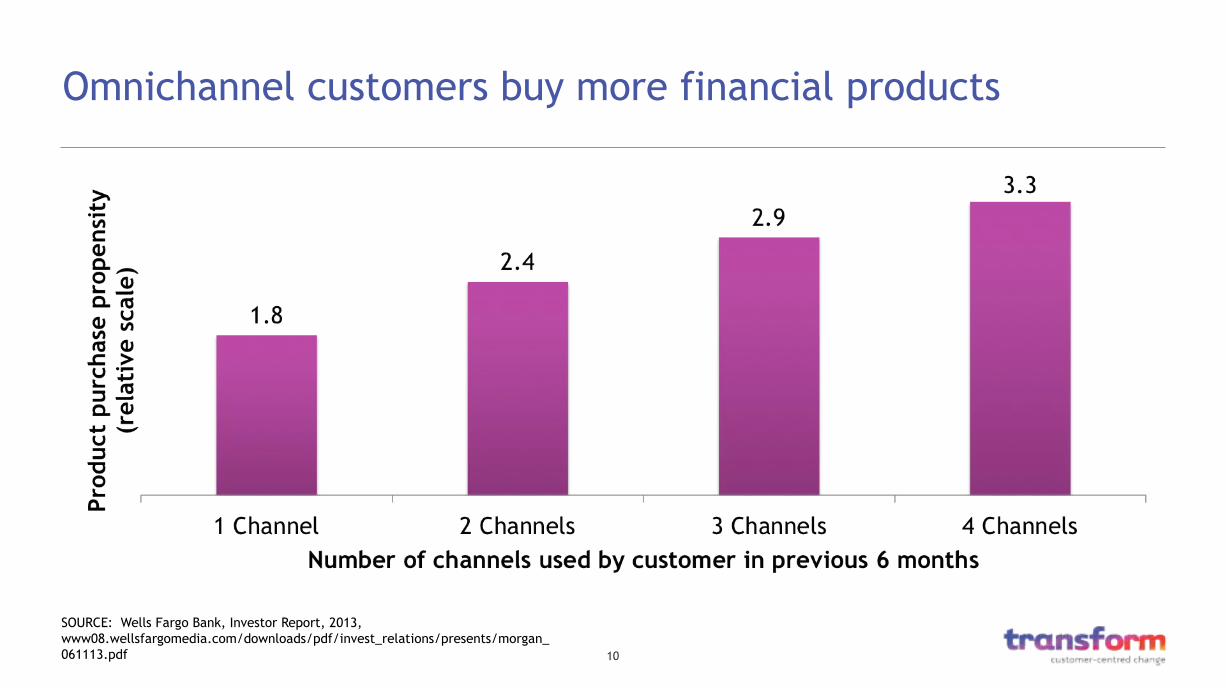

Omnichannel customers buy more financial products

SOURCE: Wells Fargo Bank, Investor Report, 2013, www08.wellsfargomedia.com/downloads/pdf/invest_relations/presents/morgan_061113.pdf

11

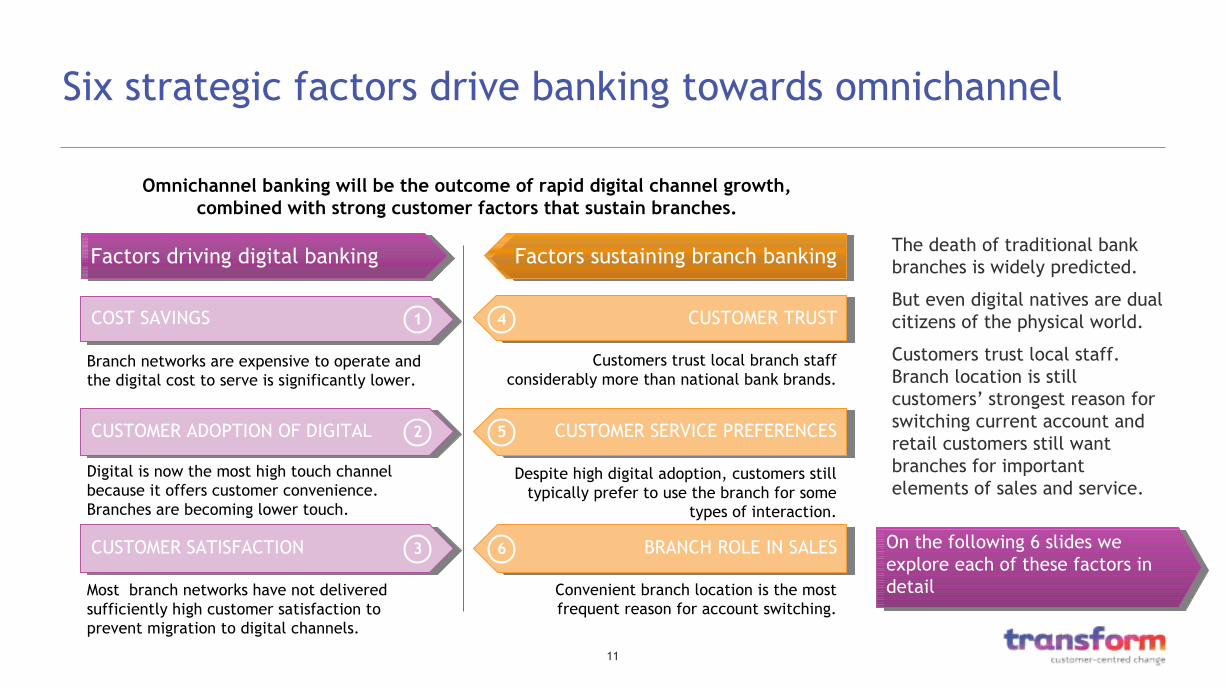

Six strategic factors drive banking towards omnichannel

The death of traditional bank branches is widely predicted.

But even digital natives are dual citizens of the physical world.

Customers trust local staff. Branch location is still customers’ strongest reason for switching current account and retail customers still want branches for important elements of sales and service.

Factors driving digital banking Factors sustaining branch banking

CUSTOMER TRUST

CUSTOMER SERVICE PREFERENCES

BRANCH ROLE IN SALES

1

2

3

4

5

6

COST SAVINGS

CUSTOMER ADOPTION OF DIGITAL

CUSTOMER SATISFACTION

Branch networks are expensive to operate and the digital cost to serve is significantly lower.

Digital is now the most high touch channel because it offers customer convenience. Branches are becoming lower touch.

Customers trust local branch staff considerably more than national bank brands.

Despite high digital adoption, customers still typically prefer to use the branch for some

types of interaction.

Most branch networks have not delivered sufficiently high customer satisfaction to prevent migration to digital channels.

Convenient branch location is the most frequent reason for account switching.

Omnichannel banking will be the outcome of rapid digital channel growth, combined with strong customer factors that sustain branches.

On the following 6 slides we explore each of these factors in detail

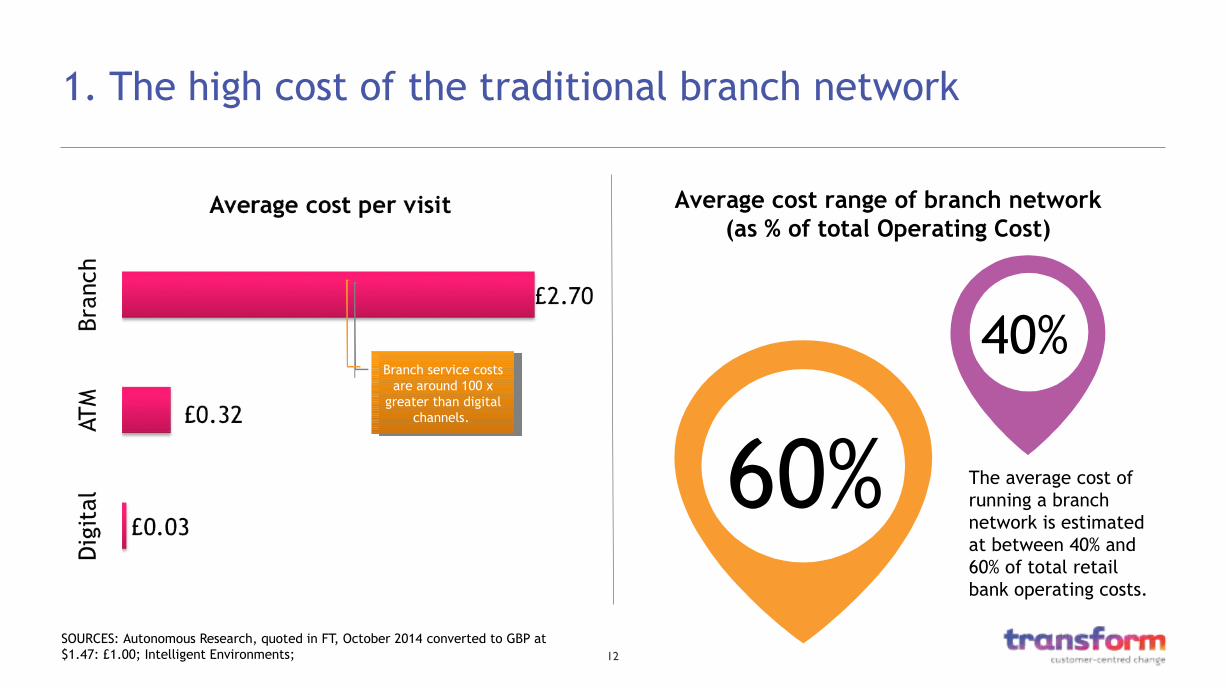

12SOURCES: Autonomous Research, quoted in FT, October 2014 converted to GBP at $1.47: £1.00; Intelligent Environments;

1. The high cost of the traditional branch network

Average cost range of branch network (as % of total Operating Cost)

Branch service costs are around 100 x

greater than digital channels.

Branch service costs are around 100 x

greater than digital channels.

60% The average cost of running a branch network is estimated at between 40% and 60% of total retail bank operating costs.

40%

13

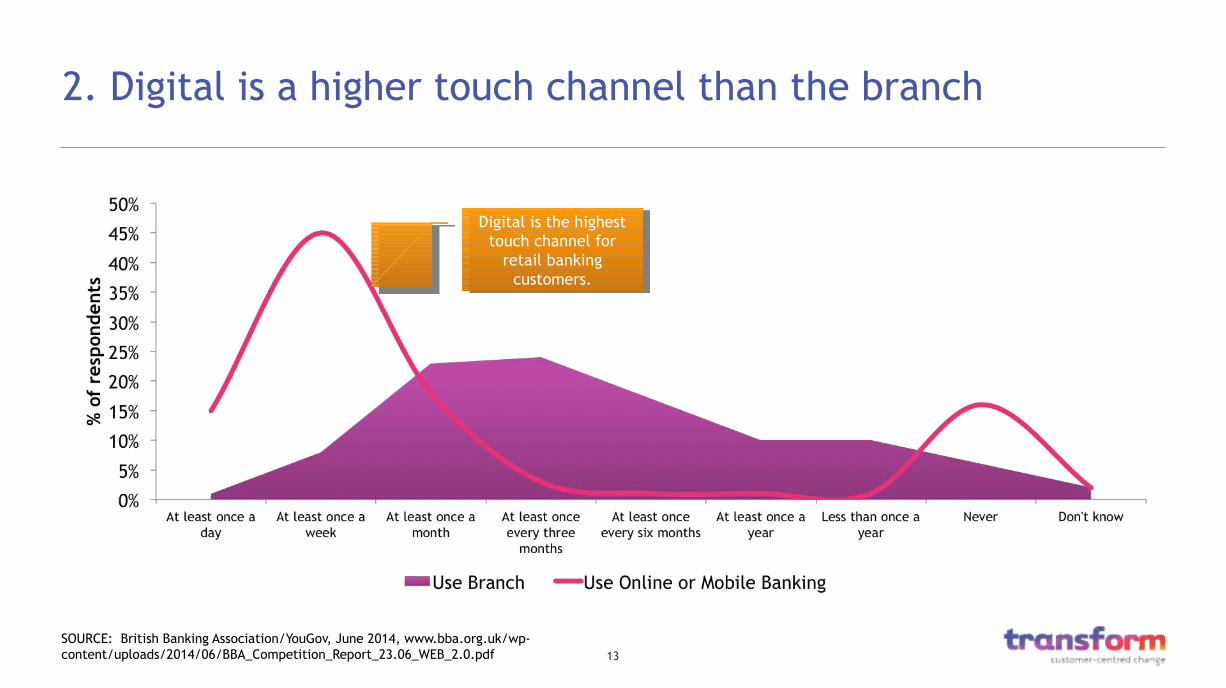

2. Digital is a higher touch channel than the branch

SOURCE: British Banking Association/YouGov, June 2014, www.bba.org.uk/wp-content/uploads/2014/06/BBA_Competition_Report_23.06_WEB_2.0.pdf

Digital is the highest touch channel for

retail banking customers.

Digital is the highest touch channel for

retail banking customers.

14

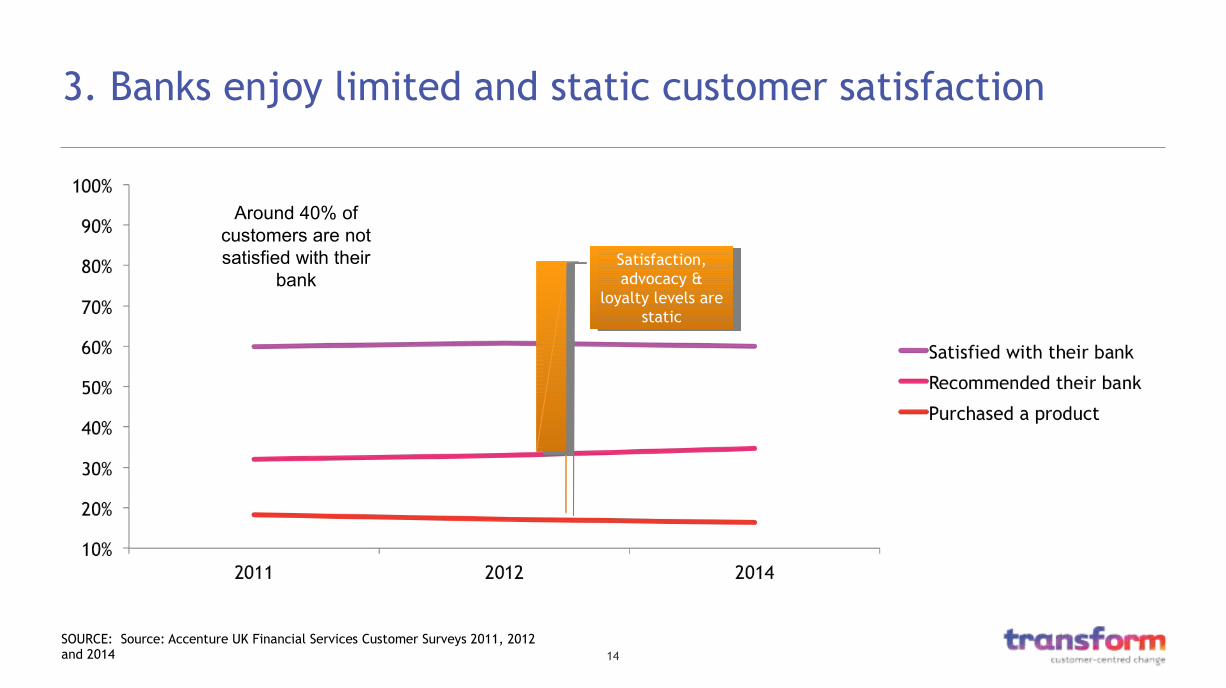

3. Banks enjoy limited and static customer satisfaction

SOURCE: Source: Accenture UK Financial Services Customer Surveys 2011, 2012 and 2014

Satisfaction, advocacy and

loyalty levels have not changed in 3

years

Satisfaction, advocacy and

loyalty levels have not changed in 3

years

Satisfaction, advocacy and

loyalty levels have not changed in 3

years

Satisfaction, advocacy and

loyalty levels have not changed in 3

years

Satisfaction, advocacy &

loyalty levels are static

Satisfaction, advocacy &

loyalty levels are static

Around 40% of customers are not satisfied with their

bank

15

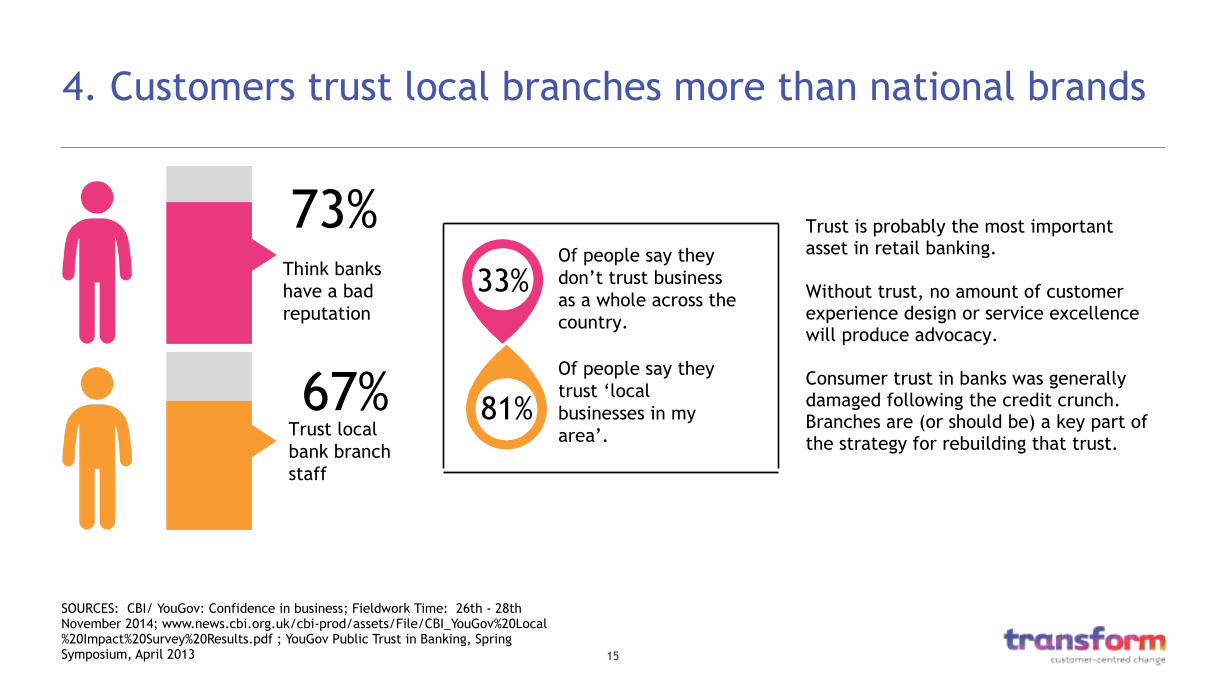

4. Customers trust local branches more than national brands

Trust is probably the most important asset in retail banking.

Without trust, no amount of customer experience design or service excellence will produce advocacy.

Consumer trust in banks was generally damaged following the credit crunch. Branches are (or should be) a key part of the strategy for rebuilding that trust.

SOURCES: CBI/ YouGov: Confidence in business; Fieldwork Time: 26th - 28th November 2014; www.news.cbi.org.uk/cbi-prod/assets/File/CBI_YouGov%20Local%20Impact%20Survey%20Results.pdf ; YouGov Public Trust in Banking, Spring Symposium, April 2013

73%Think banks have a bad reputation

67%Trust local bank branch staff

33%Of people say they don’t trust business as a whole across the country.

81%Of people say they trust ‘local businesses in my area’.

16

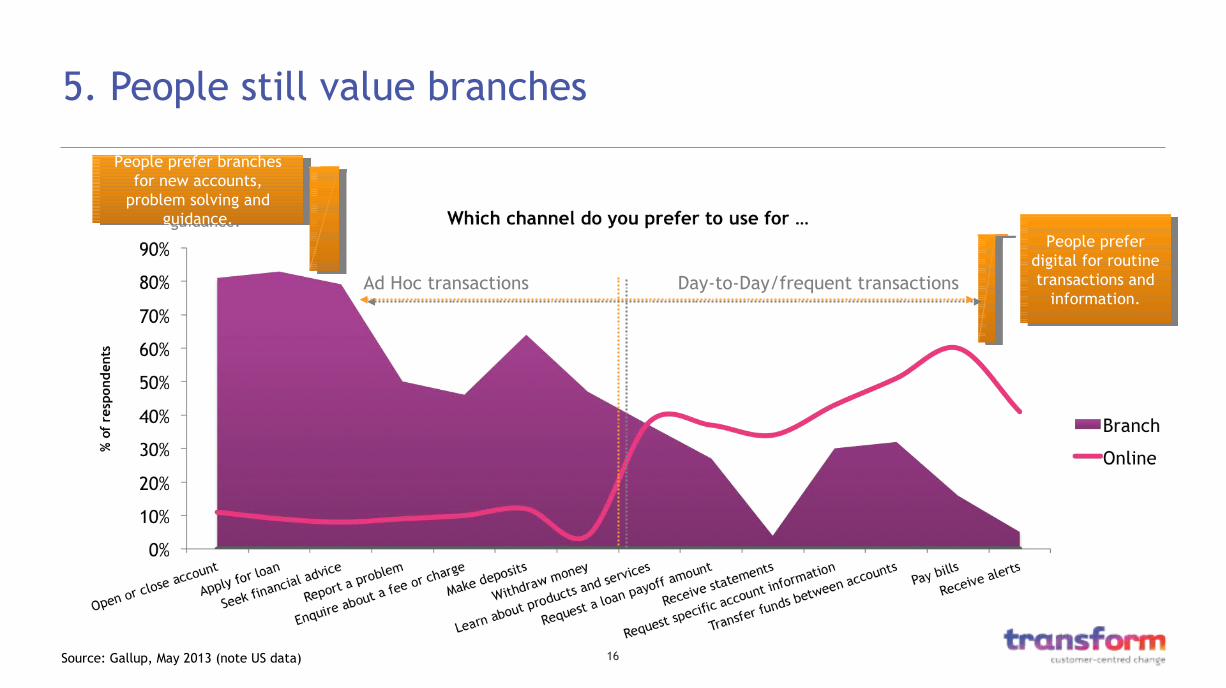

5. People still value branches

Source: Gallup, May 2013 (note US data)

People prefer branches for new accounts,

problem solving and guidance.

People prefer branches for new accounts,

problem solving and guidance.

People prefer digital for routine transactions and

information.

People prefer digital for routine transactions and

information.Day-to-Day/frequent transactionsAd Hoc transactions

17

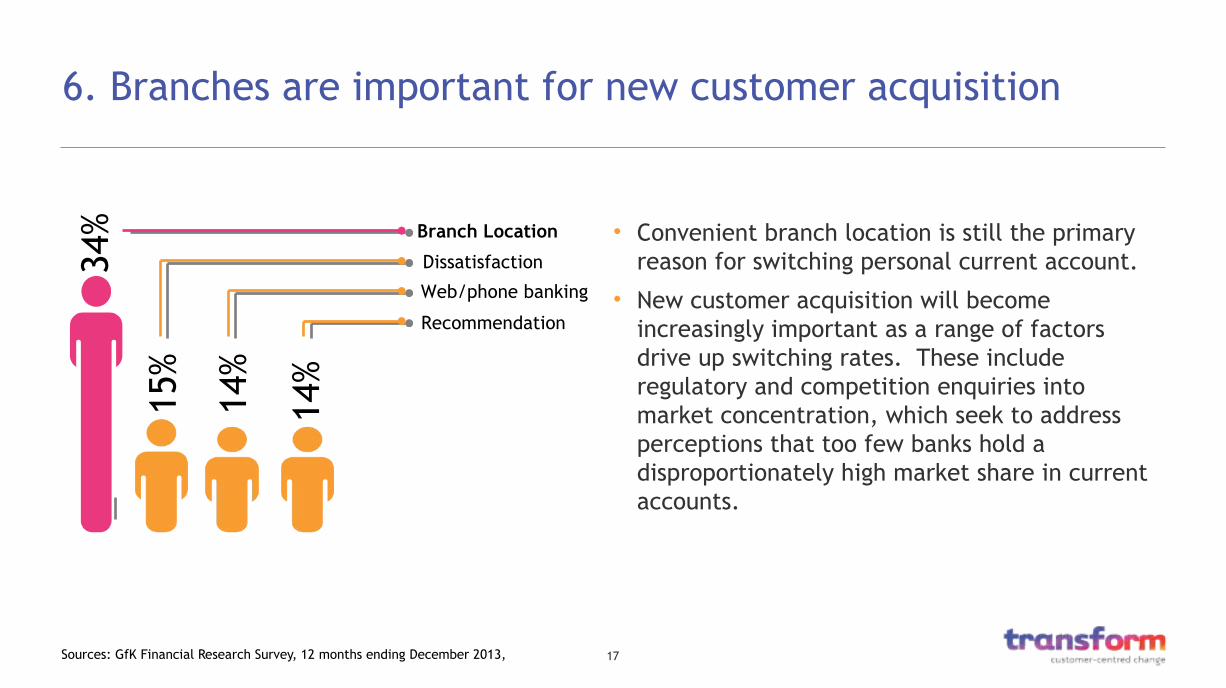

6. Branches are important for new customer acquisition

• Convenient branch location is still the primary reason for switching personal current account.

• New customer acquisition will become increasingly important as a range of factors drive up switching rates. These include regulatory and competition enquiries into market concentration, which seek to address perceptions that too few banks hold a disproportionately high market share in current accounts.

Sources: GfK Financial Research Survey, 12 months ending December 2013,

Branch Location

Dissatisfaction

Web/phone banking

Recommendation

34%

15%

14%

14%

How well do banks deliver omnichannel today?

19

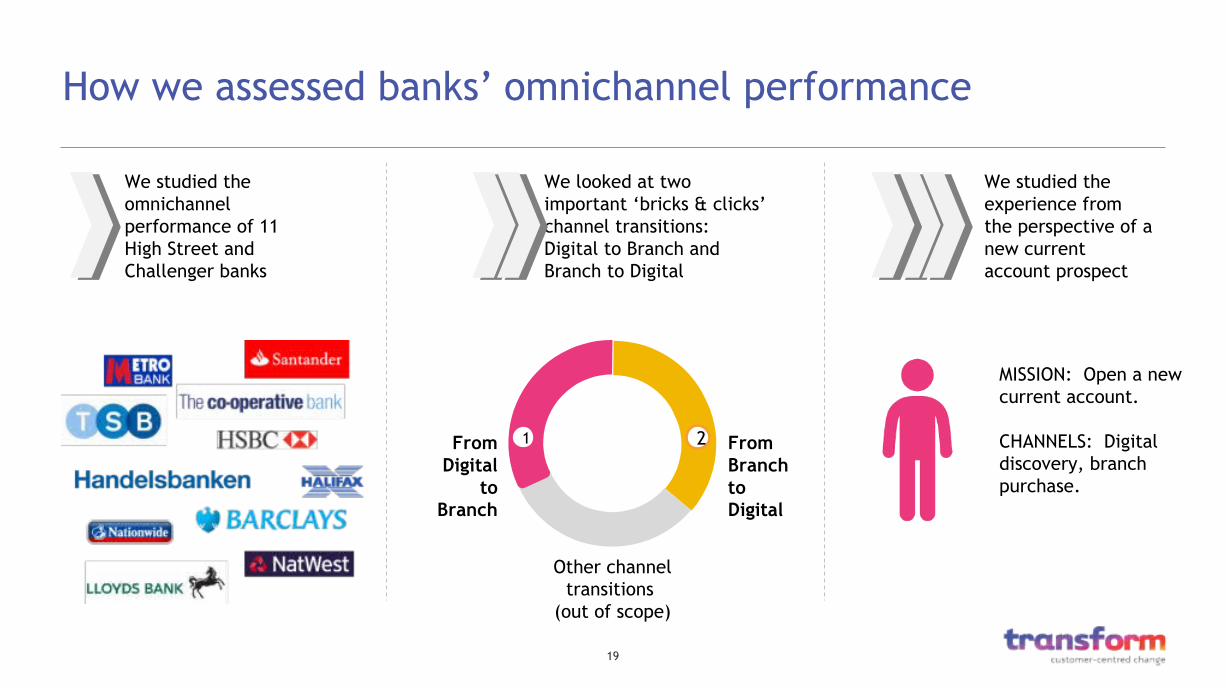

How we assessed banks’ omnichannel performance

From Branch to Digital

From Digital

to Branch

Other channel transitions

(out of scope)

1 2

We studied the omnichannel performance of 11 High Street and Challenger banks

We looked at two important ‘bricks & clicks’ channel transitions: Digital to Branch and Branch to Digital

We studied the experience from the perspective of a new current account prospect

MISSION: Open a new current account.

CHANNELS: Digital discovery, branch purchase.

20

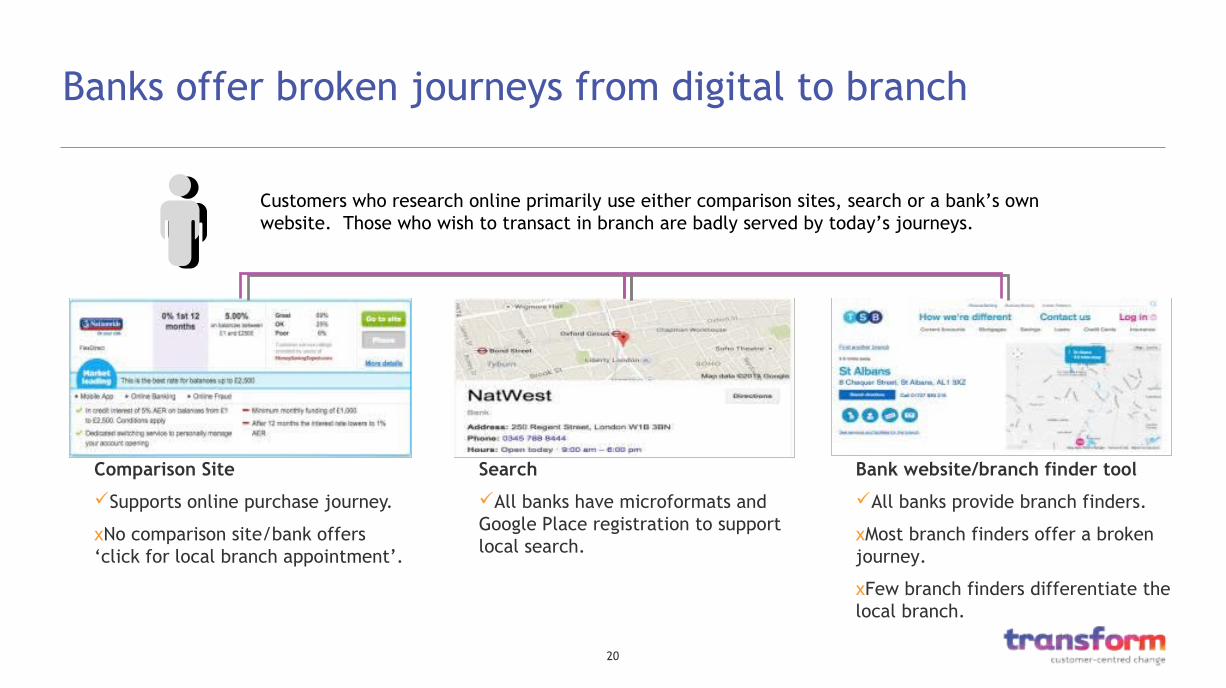

Banks offer broken journeys from digital to branch

Comparison Site

Supports online purchase journey.

xNo comparison site/bank offers ‘click for local branch appointment’.

Customers who research online primarily use either comparison sites, search or a bank’s own website. Those who wish to transact in branch are badly served by today’s journeys.

Search

All banks have microformats and Google Place registration to support local search.

Bank website/branch finder tool

All banks provide branch finders.

xMost branch finders offer a broken journey.

xFew branch finders differentiate the local branch.

21

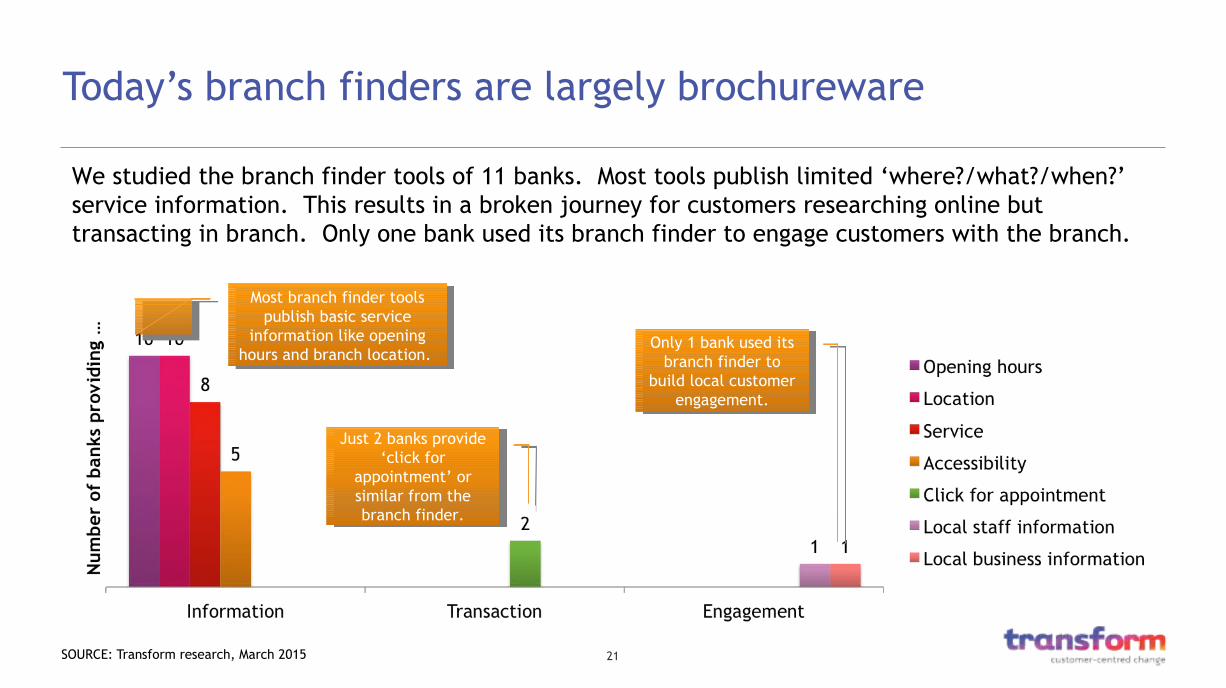

Today’s branch finders are largely brochureware

SOURCE: Transform research, March 2015

Most branch finder tools publish basic service

information like opening hours and branch location.

Most branch finder tools publish basic service

information like opening hours and branch location.

Just 2 banks provide ‘click for

appointment’ or similar from the branch finder.

Just 2 banks provide ‘click for

appointment’ or similar from the branch finder.

Only 1 bank used its branch finder to

build local customer engagement.

Only 1 bank used its branch finder to

build local customer engagement.

We studied the branch finder tools of 11 banks. Most tools publish limited ‘where?/what?/when?’ service information. This results in a broken journey for customers researching online but transacting in branch. Only one bank used its branch finder to engage customers with the branch.

22

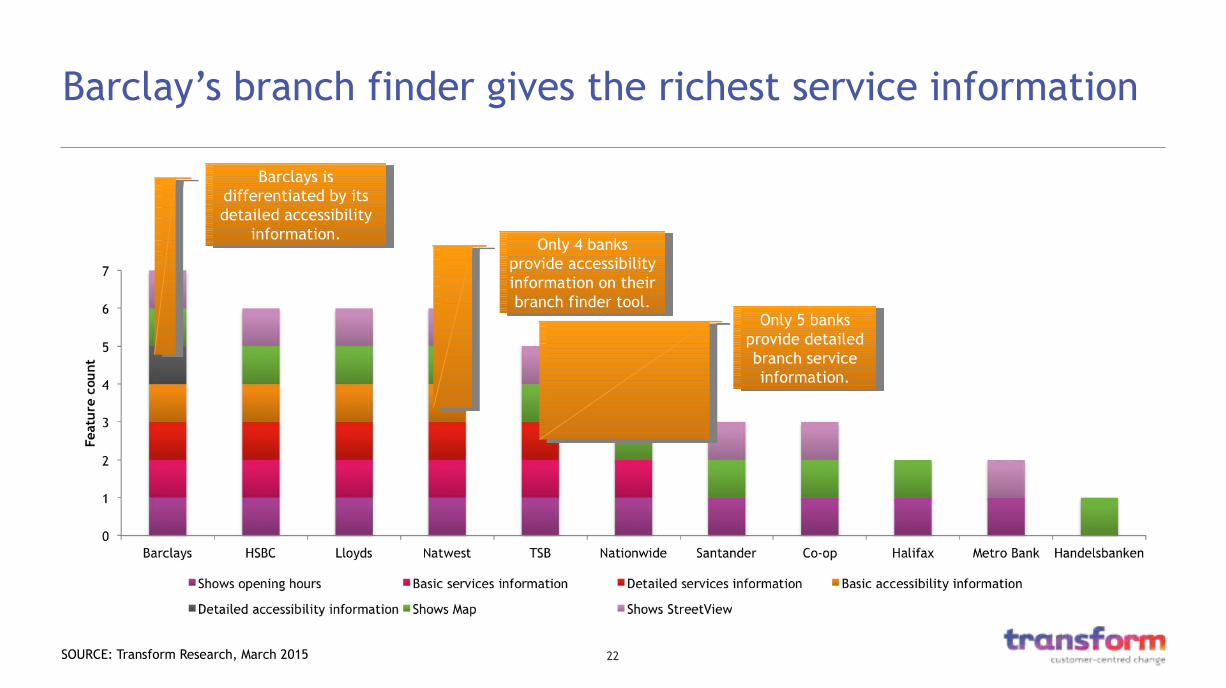

Barclay’s branch finder gives the richest service information

SOURCE: Transform Research, March 2015

Barclays is differentiated by its detailed accessibility

information.

Barclays is differentiated by its detailed accessibility

information.Only 4 banks

provide accessibility information on their branch finder tool.

Only 4 banks provide accessibility information on their branch finder tool.

Only 5 banks provide detailed branch service information.

Only 5 banks provide detailed branch service information.

23

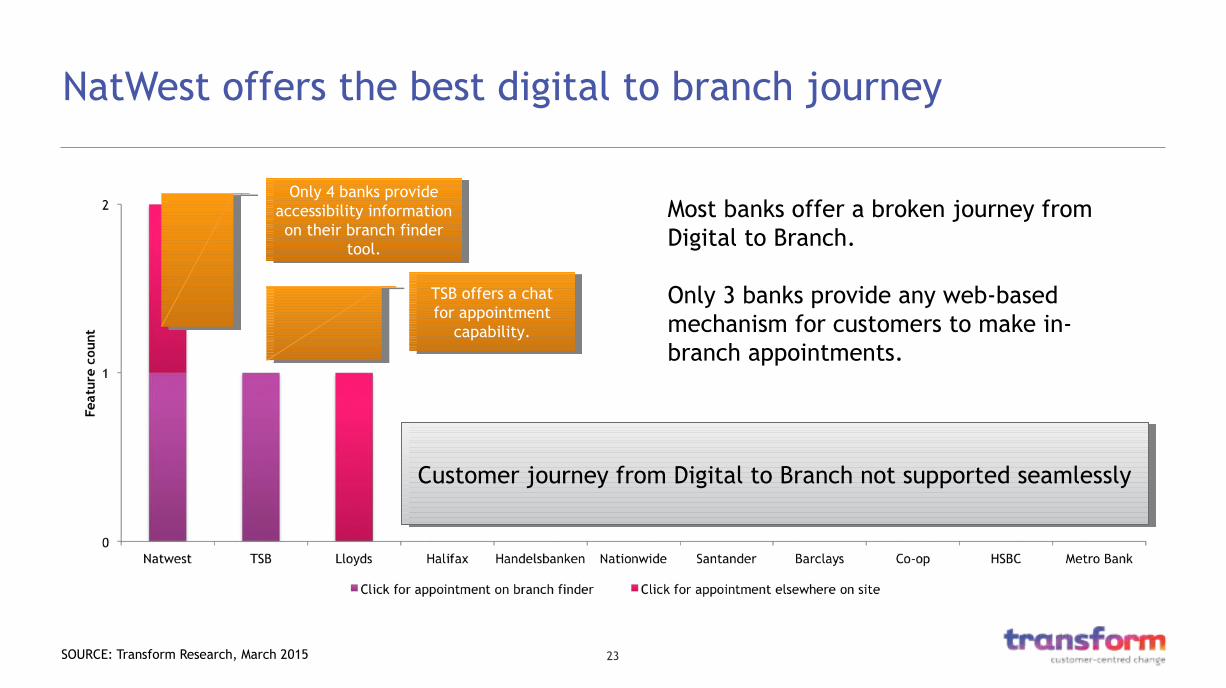

NatWest offers the best digital to branch journey

SOURCE: Transform Research, March 2015

Only 4 banks provide accessibility information on their branch finder

tool.

Only 4 banks provide accessibility information on their branch finder

tool.

TSB offers a chat for appointment

capability.

TSB offers a chat for appointment

capability.

Most banks offer a broken journey from Digital to Branch.

Only 3 banks provide any web-based mechanism for customers to make in-branch appointments.

Customer journey from Digital to Branch not supported seamlesslyCustomer journey from Digital to Branch not supported seamlessly

24

How we assessed banks’ in-branch omnichannel offering

• To assess how well banks deliver omnichannel experiences in branches, we benchmarked digital transaction, service and decision support functionality in branch.

• We benchmarked two branches per bank and as far as possible benchmarked like-for-like full-service branches.

• Please note that a number of services (e.g. beacons, video conferencing) are at a pilot stage by several banks.

SOURCE: www.virgin.com/news/virgin-moneys-new-lounge-reaches-manchester

25

In-branch digitally integrated omnichannel services are immature

SOURCE: Transform Research, March 2015

NatWest and Barclays provided the most digitally integrated

branches.

NatWest and Barclays provided the most digitally integrated

branches.Metro offered unique instant digital printing of account collateral.

Metro offered unique instant digital printing of account collateral.

Other banks did not deliver any digitally integrated omnichannel service.

Other banks did not deliver any digitally integrated omnichannel service.

26

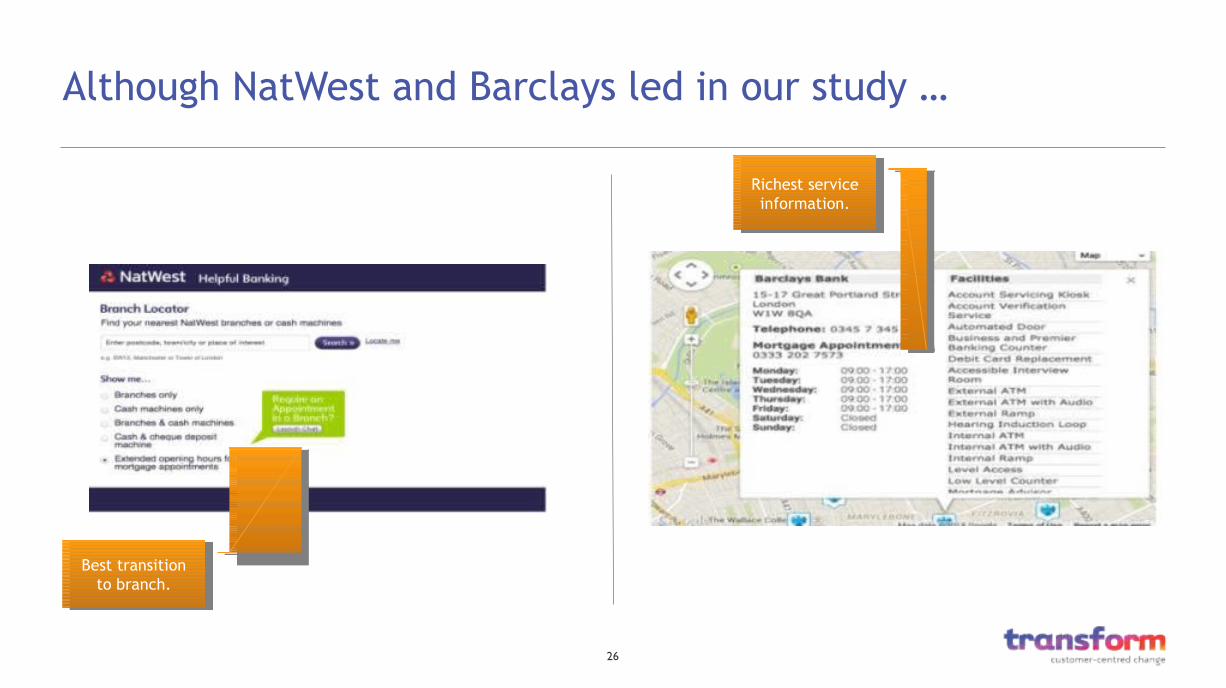

Although NatWest and Barclays led in our study …

Richest service information.

Richest service information.

Best transition to branch.

Best transition to branch.

27

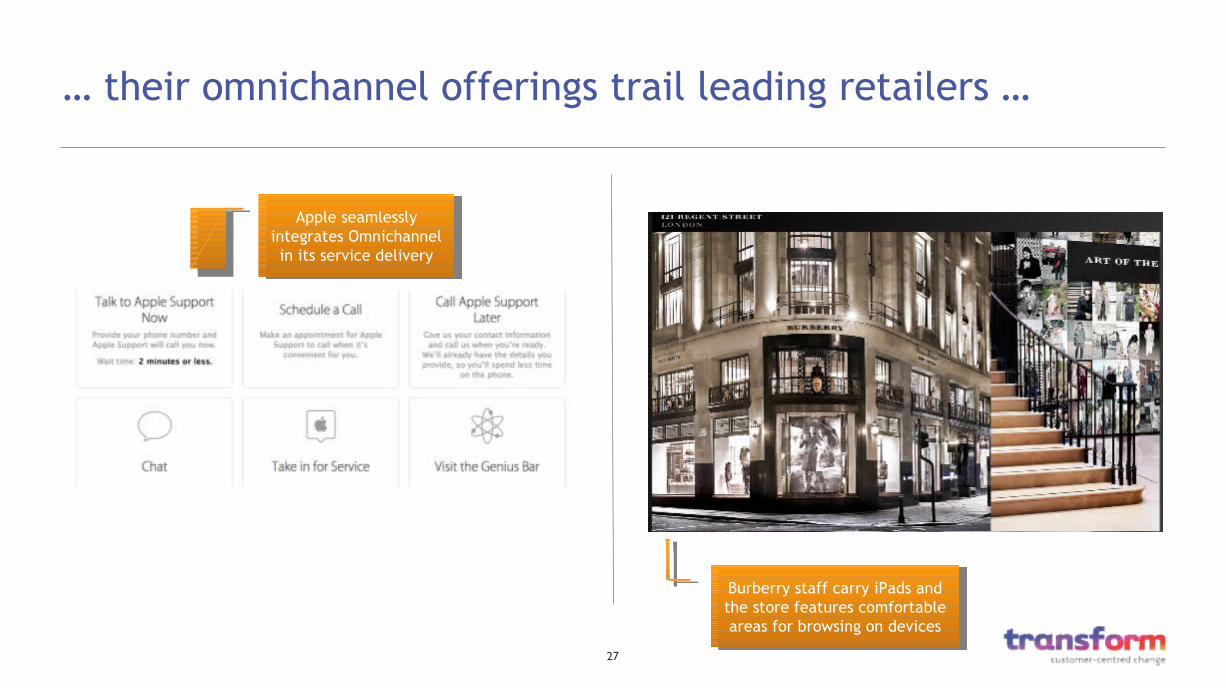

… their omnichannel offerings trail leading retailers …

Apple seamlessly integrates Omnichannel in its service delivery

Apple seamlessly integrates Omnichannel in its service delivery

Burberry staff carry iPads and the store features comfortable areas for browsing on devices

Burberry staff carry iPads and the store features comfortable areas for browsing on devices

28

… who are investing in digital to improve the customer experience

Thomson embracing technology to improve the booking experience and

inspire customers

Thomson embracing technology to improve the booking experience and

inspire customers

Disney using digital technology to provide a frictionless

experience

Disney using digital technology to provide a frictionless

experience

The future of omnichannel banking

A vision

30

If Apple were a bank …

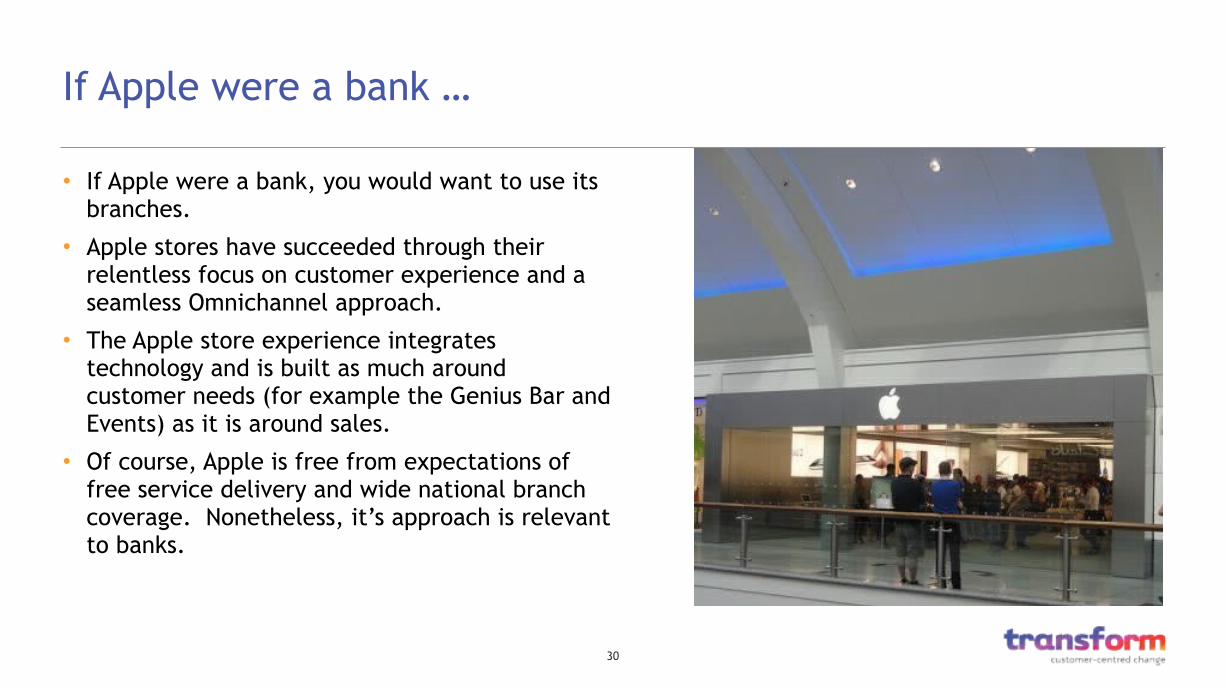

• If Apple were a bank, you would want to use its branches.

• Apple stores have succeeded through their relentless focus on customer experience and a seamless Omnichannel approach.

• The Apple store experience integrates technology and is built as much around customer needs (for example the Genius Bar and Events) as it is around sales.

• Of course, Apple is free from expectations of free service delivery and wide national branch coverage. Nonetheless, it’s approach is relevant to banks.

31

Customers’ omnichannel expectation driven by retail

Argos enables customers to shop online and collect in-store with its ‘Click & Collect’ functionality.

Hammerson is equipping its shopping centres with beacon technology to give customers helpful directions and relevant promotions.

Sainsbury’s Scan & Go gets customers through checkout more quickly. Customers scan their own items via mobile app.

C&A (Brazil) displays real-time Facebook likes for fashion items displayed on hangers.

Customers are having more and better omnichannel experiences from a retail sector that is continuously innovating with digital integration in store.

32

A few banks are also omnichannel, digital innovators

Digital EaglesBarclays has 6,500 ‘Digital Eagles’ across its branch network to help customers use Barclay’s digital services and related technologies.

Code PlaygroundBarclays teaches coding for children at bookable sessions at its local branches.

In-branch BeaconsBarclays is trialing in-branch beacon technology that alerts staff when a customer with an accessibility need enters the branch.

Mobile AppointmentsING Belgium’s mobile app allows customers to click for an appointment with a named staff member in-branch.

SOURCE: www.newsroom.barclays.com/releases/ReleaseDetailPage.aspx?releaseId=3099; www.newsroom.barclays.com/releases/ReleaseDetailPage.aspx?releaseId=3068; www.ing.be/en/retail/day-to-day-banking/self-banking/Pages/mobile_smartphone.aspx

33

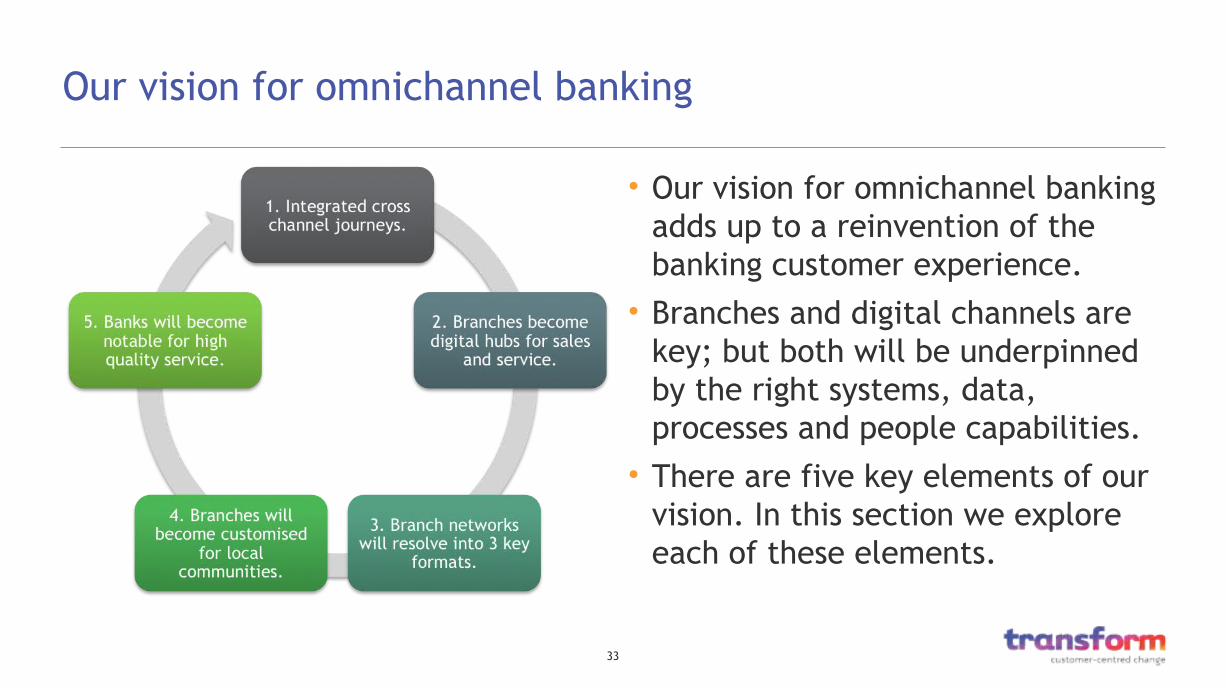

Our vision for omnichannel banking

• Our vision for omnichannel banking adds up to a reinvention of the banking customer experience.

• Branches and digital channels are key; but both will be underpinned by the right systems, data, processes and people capabilities.

• There are five key elements of our vision. In this section we explore each of these elements.

34

1. Customer journeys will become integrated across channels

Digital branch experience

Web

Branch: Person

Branch: co-browse

Branch display

Mobile

Phone

Paper

John SmithMission: open a new current account.

Key motivations•Values personal relationships.•Trusts local businesses.•Values both digital and branch/face-to-face channels.•Feels that banks are all the same, but hopes to be surprised.

start

Online journey offers click, call and

visit to open account options.

Online journey offers click, call and

visit to open account options.

Text/email reminder

Search

Demonstrators and tools support sale

and build personalised illustration

Demonstrators and tools support sale

and build personalised illustration

Selects Product

Click for Appointment

Arrives at branch

Meets branch staff

Uses tools and product

demonstratorsDigital signage

Comparison

Click for Appointment offers

rich information about local branch.

Click for Appointment offers

rich information about local branch.

Option to enrol mobile device as ID

key for branch visits.

Option to enrol mobile device as ID

key for branch visits.

Messaging includes contribution of local

branch to local community.

Messaging includes contribution of local

branch to local community.

Personalised experience if

customer’s mobile device identified.

Personalised experience if

customer’s mobile device identified.

Instant fulfillment through digital

printing in-branch.

Instant fulfillment through digital

printing in-branch.

35

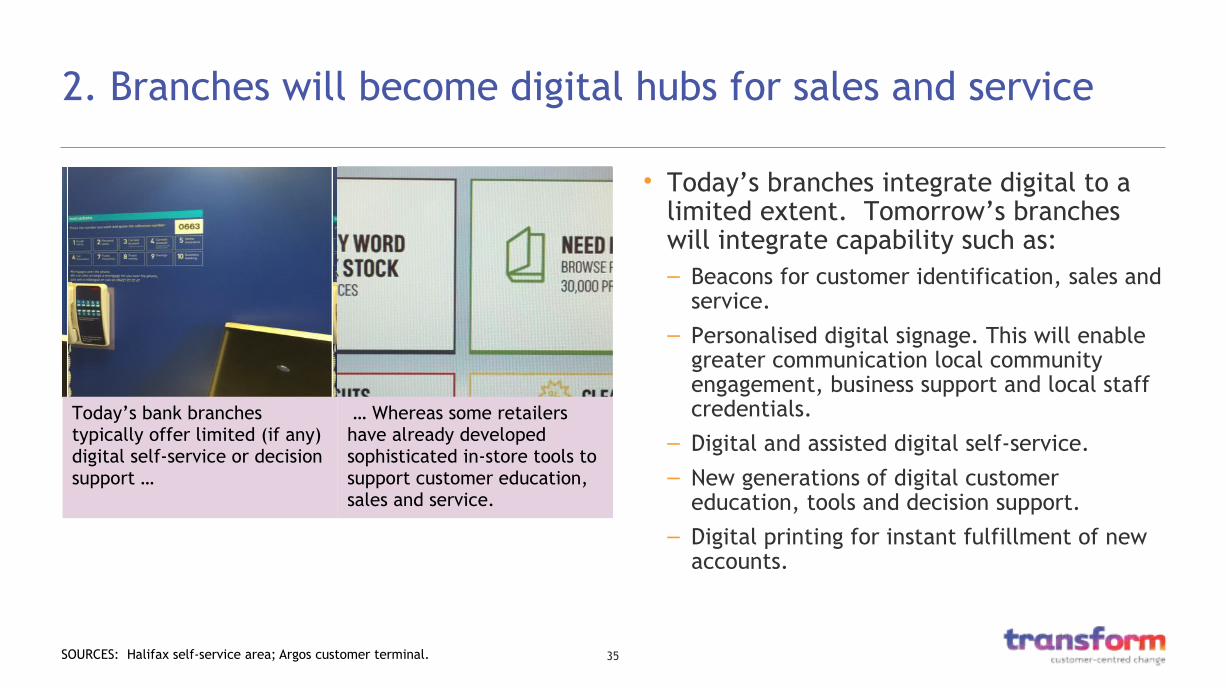

2. Branches will become digital hubs for sales and service

SOURCES: Halifax self-service area; Argos customer terminal.

Today’s bank branches typically offer limited (if any) digital self-service or decision support …

… Whereas some retailers have already developed sophisticated in-store tools to support customer education, sales and service.

• Today’s branches integrate digital to a limited extent. Tomorrow’s branches will integrate capability such as:– Beacons for customer identification, sales and

service.

– Personalised digital signage. This will enable greater communication local community engagement, business support and local staff credentials.

– Digital and assisted digital self-service.

– New generations of digital customer education, tools and decision support.

– Digital printing for instant fulfillment of new accounts.

36

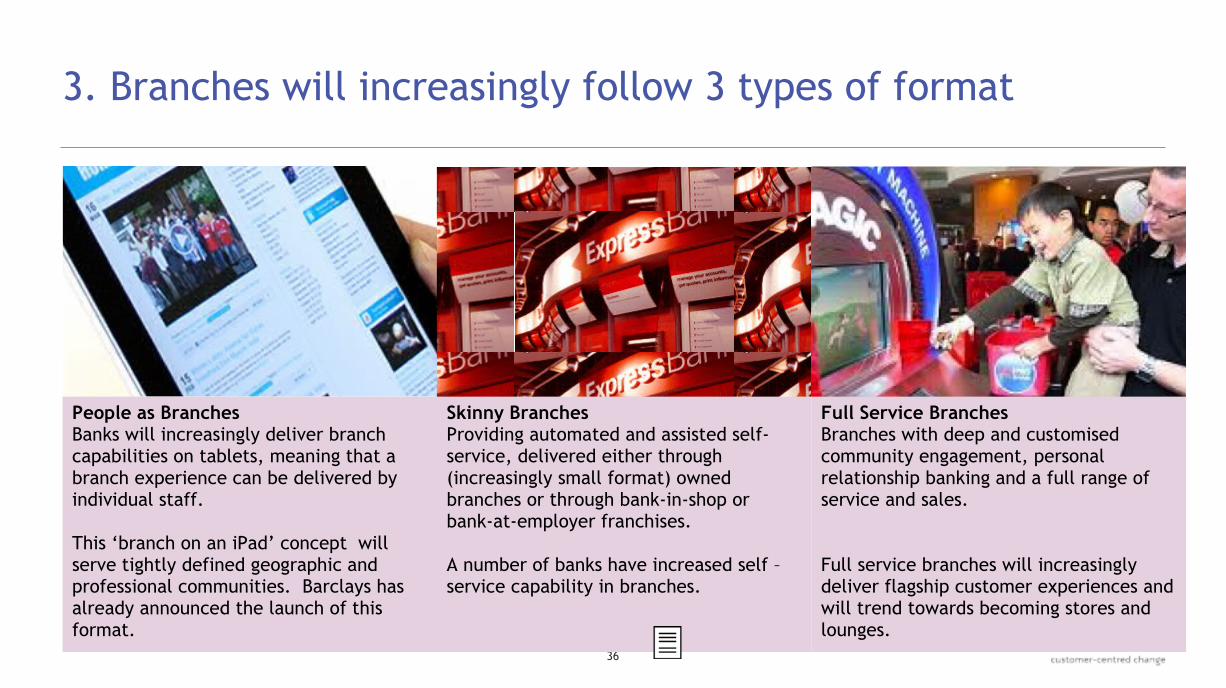

3. Branches will increasingly follow 3 types of format

People as BranchesBanks will increasingly deliver branch capabilities on tablets, meaning that a branch experience can be delivered by individual staff.

This ‘branch on an iPad’ concept will serve tightly defined geographic and professional communities. Barclays has already announced the launch of this format.

Skinny BranchesProviding automated and assisted self-service, delivered either through (increasingly small format) owned branches or through bank-in-shop or bank-at-employer franchises.

A number of banks have increased self –service capability in branches.

Full Service BranchesBranches with deep and customised community engagement, personal relationship banking and a full range of service and sales.

Full service branches will increasingly deliver flagship customer experiences and will trend towards becoming stores and lounges.

James Goldhill, 03/16/2015

is it worth using example of M&S bank as well as HSBC in Post office?

37

4. Banks will increasingly customise branches

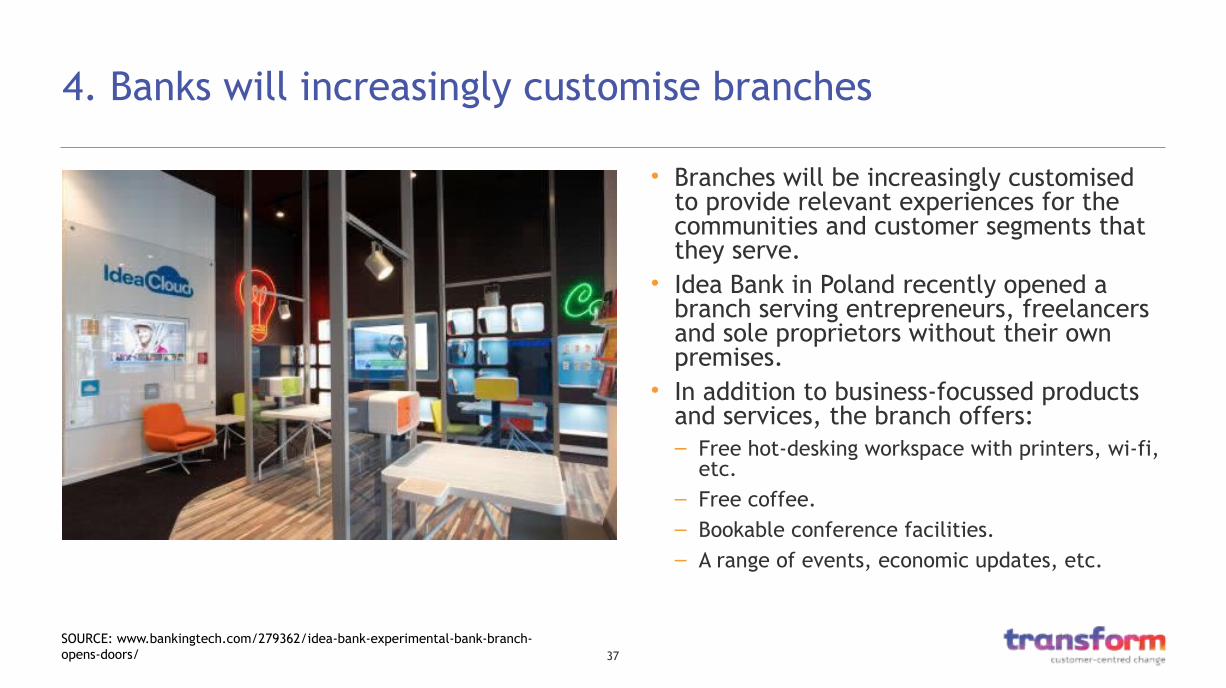

• Branches will be increasingly customised to provide relevant experiences for the communities and customer segments that they serve.

• Idea Bank in Poland recently opened a branch serving entrepreneurs, freelancers and sole proprietors without their own premises.

• In addition to business-focussed products and services, the branch offers:– Free hot-desking workspace with printers, wi-fi,

etc.– Free coffee.– Bookable conference facilities.– A range of events, economic updates, etc.

SOURCE: www.bankingtech.com/279362/idea-bank-experimental-bank-branch-opens-doors/

38

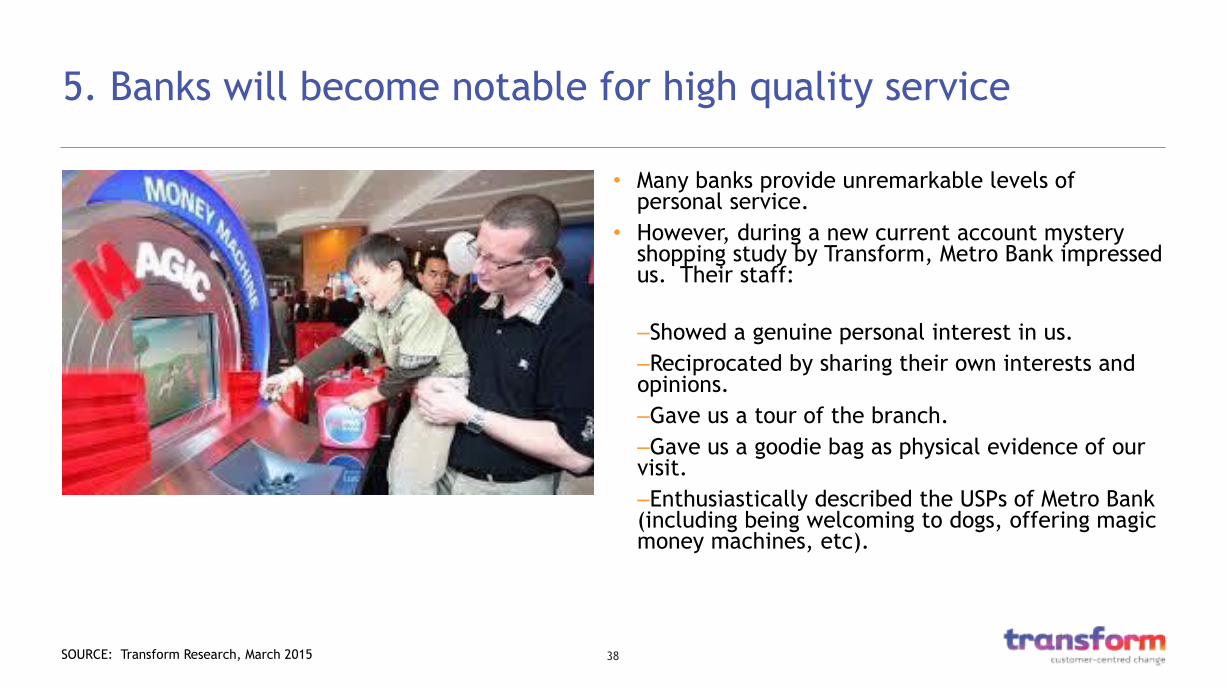

5. Banks will become notable for high quality service

SOURCE: Transform Research, March 2015

• Many banks provide unremarkable levels of personal service.

• However, during a new current account mystery shopping study by Transform, Metro Bank impressed us. Their staff:

–Showed a genuine personal interest in us. –Reciprocated by sharing their own interests and opinions.–Gave us a tour of the branch.–Gave us a goodie bag as physical evidence of our visit.–Enthusiastically described the USPs of Metro Bank (including being welcoming to dogs, offering magic money machines, etc).

39

Making the vision happen

• Omnichannel is not about which channels are offered, it’s about the way that customers navigate across & within the channel mix.

• So it’s about how integrated physical and digital channels are.

• It’s about developing channels in a fit for purpose mix.

• And whilst customer experience is key, digital maturity is an important enabler:

– Channels: Banks have an opportunity to define the omnichannel customer experience (i.e. what is the role of the website v branch etc) e.g when I complete a mortgage application form online, I am able to see this when I walk into the branch

– Culture: it’s important to educate branch staff around digital tools so that they are as proficient as their customers; and use branch staff as advocates and help educate the digital teams & customers

– Technology: well architected and relevant use of technology e.g. don’t use beacons for the sake of it, only use it if you want to offer an experience pertinent to the individual customer

– Customers: central to the design; what are their needs/wants/drivers…ASK them

– Strategy (and organisation): break down the silos between digital and branch. This is about offering a customer service not about the channel; make sure the organisation is structured to support this objective.

Conclusions

41

Conclusions

• Economics, technology and customer demand are pushing banking rapidly into an omnichannel age.

• Customers will judge the quality of their bank against the context of their wider retail experiences.

• Customers will increasingly want omnichannel service for a range of sales and service interactions.

• Banks will use digital capability to deliver omnichannel services that feel more personal, more relevant and, in some cases more local.

• Traditional branch networks will reduce, but branch banking will continue, delivering more value to customers, more efficiently.

• Barclays and NatWest lead the UK banking sector in omnichannel delivery today. But even their offerings lag the best omnichannel experiences from across retail.

• To develop and deliver great, relevant omnichannel services, banks will need to increase their digital maturity.

42

Creating an omnichannel experience

Omnichannel experience ecosystem Based on Transform’s Digital Maturity Index (DMI)

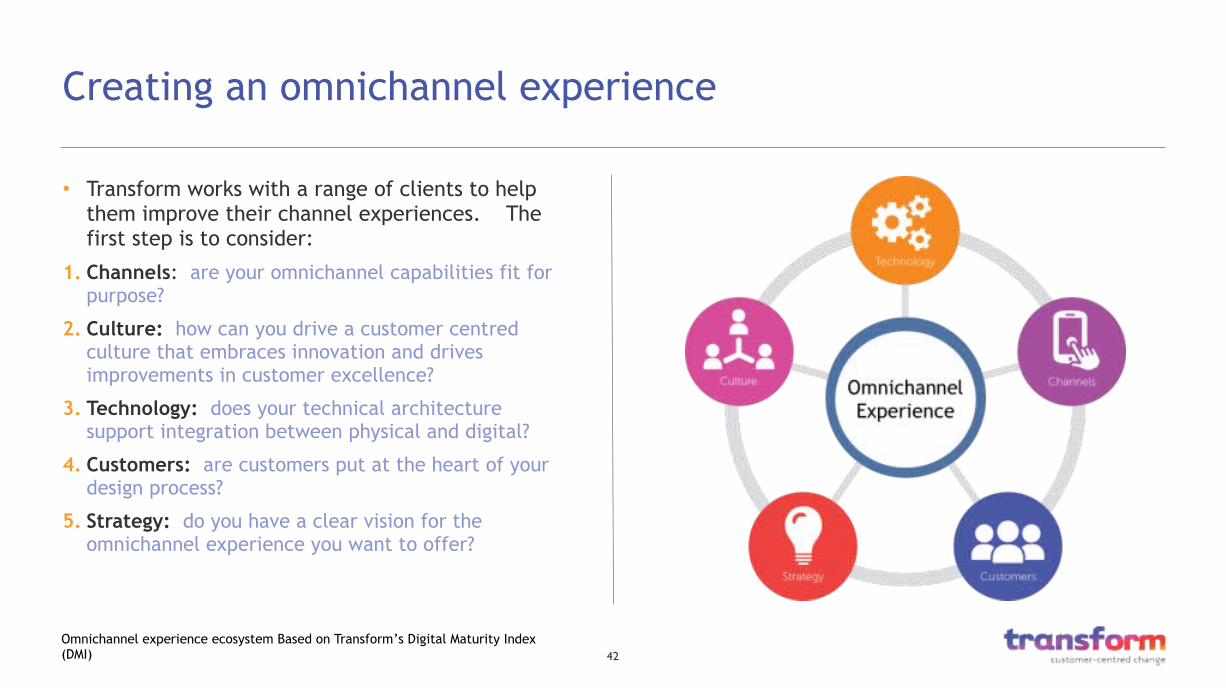

• Transform works with a range of clients to help them improve their channel experiences. The first step is to consider:

1. Channels: are your omnichannel capabilities fit for purpose?

2. Culture: how can you drive a customer centred culture that embraces innovation and drives improvements in customer excellence?

3. Technology: does your technical architecture support integration between physical and digital?

4. Customers: are customers put at the heart of your design process?

5. Strategy: do you have a clear vision for the omnichannel experience you want to offer?

43

Sources

• Transform primary research completed in March 2015

• Deutsche Bank, Retail Bank Strategy Market Research, http://www.tophold.com/uploads/document/pdf/20130918/5238f756f12379adec000062/3ee9255224dfde1524a2e44e3193b115.pdf

• Moray McDonald quoted in FT, http://www.ft.com/cms/s/0/6fc0c5a4-ac96-11e4-beeb-00144feab7de.html

• Autonomous Research, quoted in FT, http://www.ft.com/cms/s/0/a3fbfd2e-5873-11e4-942f-00144feab7de.html

• Gallup research on customer channel preferences http://www.gallup.com/businessjournal/162107/customers-interact-banks.aspx

• Accenture customer survey http://www.accenture.com/SiteCollectionDocuments/PDF/Accenture-UK-Financial-Services-Customer-Survey.pdf

• Intelligent Environments, http://www.intelligentenvironments.com/media/206059/dec-4-2014-what-the-branch-can-learn-from-digital-banking.pdf

About Transform

45

About Transform

15 year old digital & multi-channel consultancy, working with clients to deliver customer-centred change for commercial benefit

Bringing together 100 experts with cross-sector expertise

Innovation, creativity and rigour, to define, design and deliver services relevant to a rapidly changing world

46

Part of the Engine Group, the UK’s #1 independent marketing agency

Creative Agency

Business & Brand Reputation

Digital Creative

Customer Engagement

Consumer

Sponsorship Consultancy

Brand Consultancy

Strategic & Digital

Data Strategies

Experiential & Events

Interactive Marketing

Entertainment & Content Marketing

Research & Insights

…best in class with more than 2500 professionals globally

47

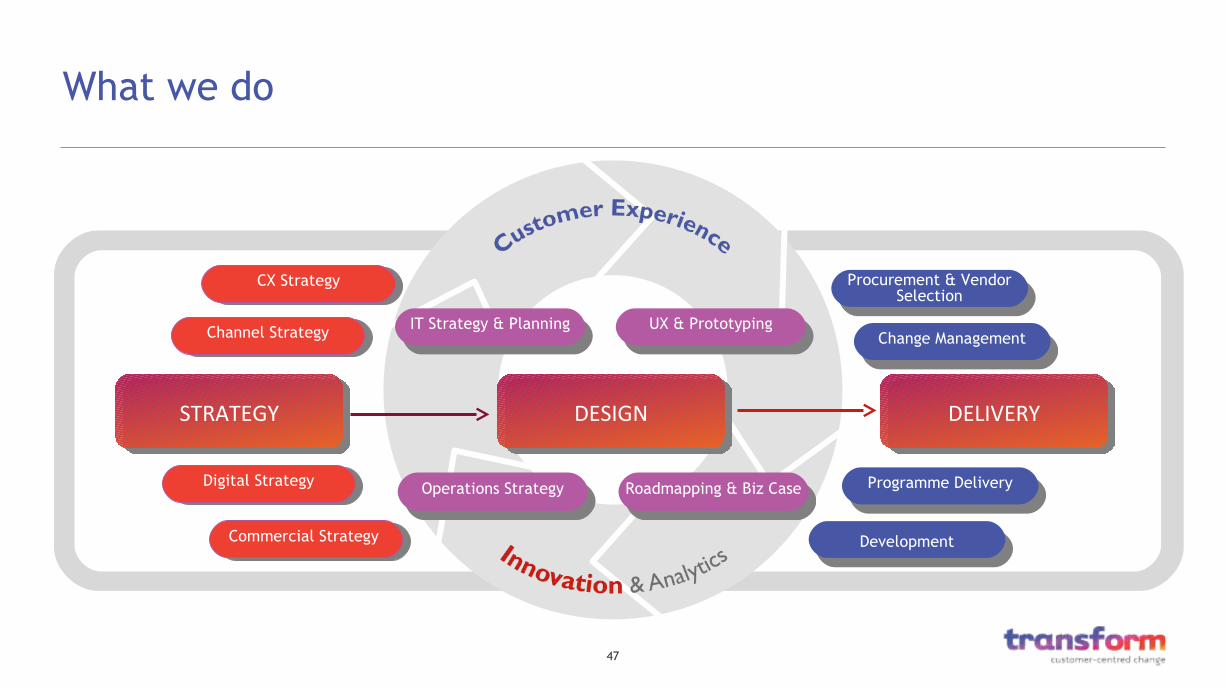

What we do

STRATEGYSTRATEGY DESIGNDESIGN DELIVERYDELIVERY

Digital StrategyDigital Strategy

Channel StrategyChannel Strategy

Operations StrategyOperations Strategy

IT Strategy & PlanningIT Strategy & Planning

Procurement & Vendor Selection

Procurement & Vendor Selection

Programme DeliveryProgramme Delivery

DevelopmentDevelopmentCommercial Strategy Commercial Strategy

CX StrategyCX Strategy

Change ManagementChange Management

Roadmapping & Biz CaseRoadmapping & Biz Case

UX & PrototypingUX & Prototyping

48

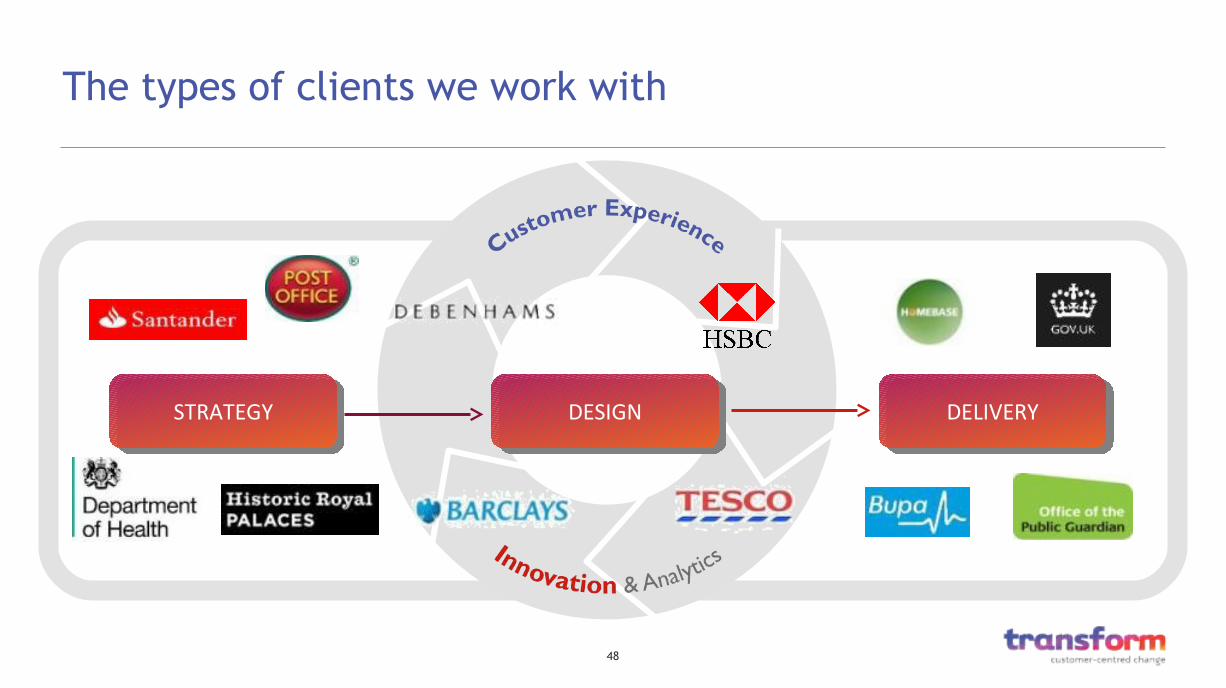

The types of clients we work with

STRATEGYSTRATEGY DESIGNDESIGN DELIVERYDELIVERY

49

What makes us different

• Customer-centred – innovation and creativity, working with clients to deliver customer- centred change

• Expert led – breadth of experience, depth of knowledge, exploit best practice across sectors by focusing on customer not product

• Delivery focused – we believe in delivering outcomes - not presentations

• With you not to you – working collaboratively, recognising where expertise is needed and how to get results

50

Awards for innovation and customer centricity

Most innovative consultancy

Best Customer Engagement Consultancy

Best Healthcare App

Best use of ICT in patient and citizen involvement

in healthcare

PayPal e-Tail awards

51

Experience and expertise

52

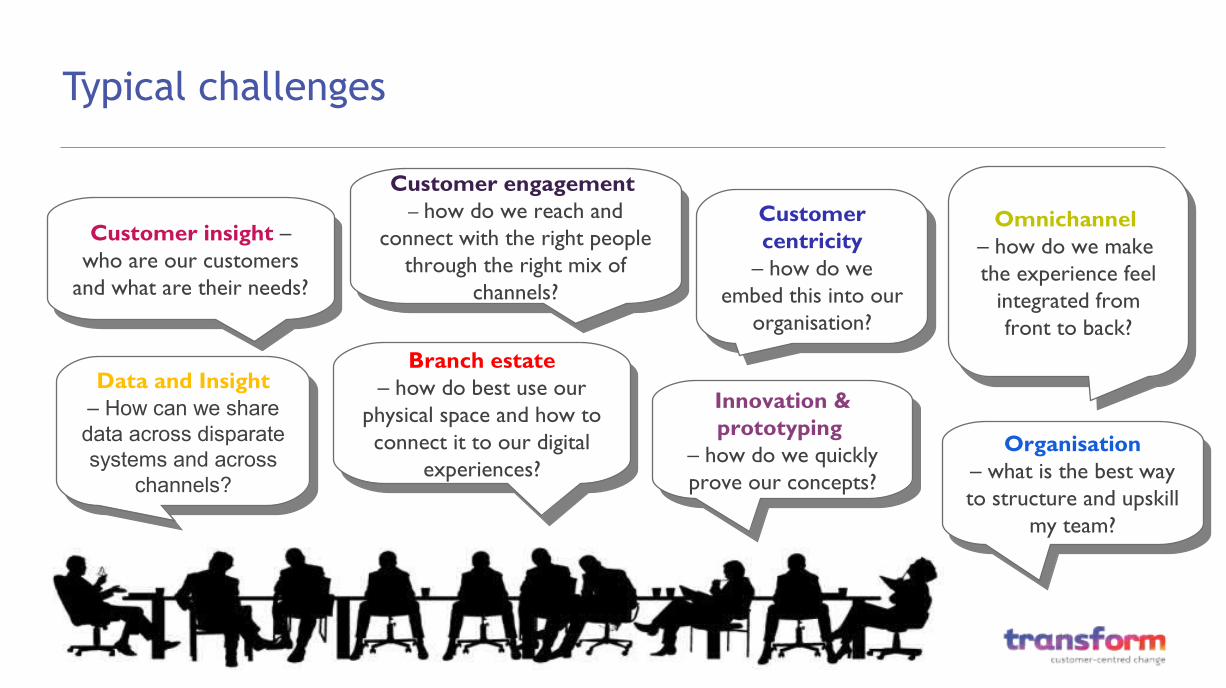

Typical challenges

Customer insight – who are our customers

and what are their needs?

Customer insight – who are our customers

and what are their needs?

Omnichannel – how do we make the experience feel

integrated from front to back?

Omnichannel – how do we make the experience feel

integrated from front to back?

Customer engagement – how do we reach and

connect with the right people through the right mix of

channels?

Customer engagement – how do we reach and

connect with the right people through the right mix of

channels?

Innovation & prototyping

– how do we quickly prove our concepts?

Innovation & prototyping

– how do we quickly prove our concepts?

Data and Insight– How can we share data across disparate systems and across

channels?

Data and Insight– How can we share data across disparate systems and across

channels?

Branch estate– how do best use our

physical space and how to connect it to our digital

experiences?

Branch estate– how do best use our

physical space and how to connect it to our digital

experiences?

Customer centricity

– how do we embed this into our

organisation?

Customer centricity

– how do we embed this into our

organisation?

Organisation– what is the best way to structure and upskill

my team?

Organisation– what is the best way to structure and upskill

my team?

53

For further information, please contact:

James GoldhillTransform60 Great Portland Street, London, W1W 7RT T: +44 20 3128 8018M: +44 7939 540 330E: [email protected] W: www.transformuk.com