Transfer of Income Without Transfer of Assets (

28

-

Upload

yash-taneja -

Category

Documents

-

view

215 -

download

0

Transcript of Transfer of Income Without Transfer of Assets (

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 1/28

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 2/28

` Sec 60-Transfer of income without transfer of assets

` Sec 61- Revocable Transfer of Assets` Sec 62-Exceptions under revocable transfer of Assets` Sec 64- Remuneration Of Spouse

Income from Assets transferred tospouseIncome from Assets transferred toson¶s wifeIncome from assets transferred to a person for benefitof son¶s wife

(2) - Conversion of Self-acquired Property into Joint-family Property and Subsequent Partition

- Transfer by a member to HUF without adequateconsideration- Income from the accretion to assets

Sec 64 - Clubbing of Negative Income

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 3/28

If any person transfers income without transferring

the ownership of the asset, such income is taxable

in the hands of the transferor. It will not make any

difference whether the transfer is revocable or irrevocable or it was effected before or after the

commencement of the Act.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 4/28

(a) A transfer shall be deemed to be revocable if-(i) It contains any provision for the re-transfer directly or indirectly of the whole or any part of theincome or assets to the transferor, or

(ii) It, in any way, gives the transferor a right to re-assume power directly or indirectly over the wholeor any part of the income or assets;

³Transfer" includes any settlement, trust,covenant, agreement or arrangement

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 5/28

Illustration:

A owns Debentures worth Rs 10,00,000 of X

Ltd., (annual) interest being Rs. 100,000. On April 1, 2009, he transfers interest income to P,

his friend without transferring the ownership of

these debentures.

Although during 2009-10, interest of Rs.

1,00,000 is received by P, it is taxable in the

hands of A as per Section 60.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 6/28

Any income arising to any person by virtue of a

revocable transfer of assets is chargeable to tax

as the income of the transferor . This is subject tothe following two exceptions laid down by section

62

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 7/28

` Exceptions under Sec. 62:

Where the income arises to any person by virtue of a

transfer by way of trust which is not revocable during the

lifetime of the beneficiary and, in case of any other

transfer, which is not revocable during the lifetime of the

transferee.

Where the income arises to any person by virtue of atransfer made before Apr il 1, 1961, which is not

revocable for a period of 6 years of more.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 8/28

An individual is chargeable to tax in respect of anyremuneration received by the spouse from aconcern in which the individual has substantialinterest.

1. When clubbing is not attr acted- Remunerationsolely attributable to the application of technical or

professional knowledge and experience of thespouse is not clubbed, irrespective of the fact

whether such remuneration is received form a firmor any other person

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 9/28

Substantial Inter est ± An individual is deemed to

have substantial interest, if he (individually or

along with his relatives) beneficially holds equityshares carrying not less than 20% voting power in

the case of a company or is entitled to not less

than 20% of the profits in the case of a concern

other than a company at any time during theprevious year.

Remuneration of Spouse

(Sec. 64(1)(ii))

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 10/28

³Relative´ in relation to an individual, means the

husband, wife, brother or sister or any lineal

ascendant or descendant of that individual.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 11/28

2.When both husband and wife have a substantial

inter est in a concer n ±

Where both husband and wife have a substantial

interest in the concern and both are in receipt of remuneration from such concern, remuneration will

be included in the total income of husband or wife

whose total income excluding such remuneration is

greater.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 12/28

` Income eligible for clubbing ± Income to be

clubbed in the hands of individual is limited to

salary, commission, fees, or any other

remuneration received by the spouse, directly or indirectly, whether in cash or in kind. Any other

income, not covered by the aforesaid categories

is, however, outside the scope of this section even

if it accrues to the spouse from a concern in whichthe individual has a substantial interest

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 13/28

Illustration:

X has a substantial interest in A Ltd. and Mrs.X is employed by A Ltd. without any technical or

professional qualification to justify the

remuneration.

In this case, salary income of Mrs. X shall be

taxable in the hands of X as per section 64 (1)

(ii)

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 14/28

Where an asset (other than house property) is

transferred by an individual to his spouse directly

or indirectly, otherwise than for adequate

consideration or in connection with an agreement to live apart , any income from such asset is

deemed to be the income of the transferor.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 15/28

Illustration:X transfers 500 debentures of IFCI to his wife

without adequate consideration.

Interest income on these debentures will be

included in the income of X as per section 64(1)(IV)

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 16/28

If an individual, directly or indirectly, transfers

assets after May 31, 1973, without adequate

consideration to son¶s wife, income arising from

such assets is included in the total income of thetransferor.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 17/28

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 18/28

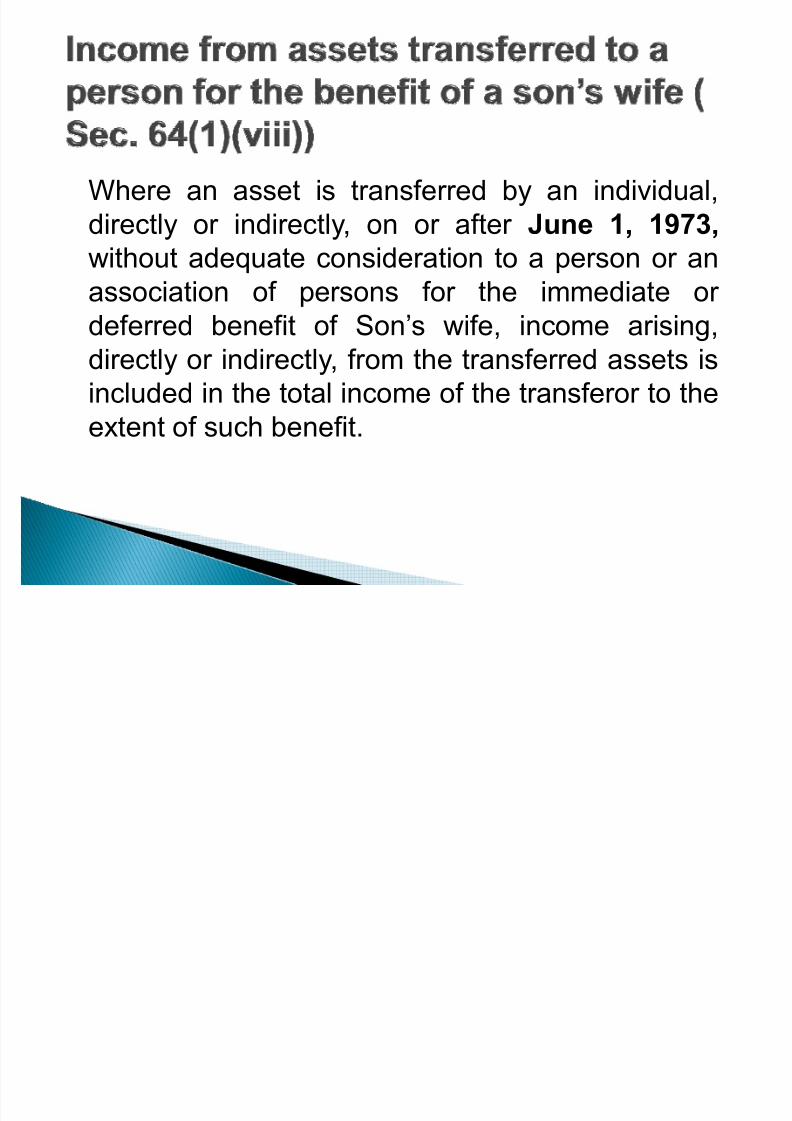

Where an asset is transferred by an individual,

directly or indirectly, on or after June 1, 1973,

without adequate consideration to a person or an

association of persons for the immediate or

deferred benefit of Son¶s wife, income arising,

directly or indirectly, from the transferred assets is

included in the total income of the transferor to the

extent of such benefit.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 19/28

Illustration:

Mr. Raman is a C.A. in practice. He engages hiswife Sita as an employee for audit work andpays a sum of Rs20,000 p.m. towards salary.Sita before marriage has completed her C.A.

article ship training and is presently awaitingresult of the final examination.

Therefore, the remuneration paid will not be

subject to clubbing as per Sec 64(1) since Sitahas not yet acquired the qualification andexperience.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 20/28

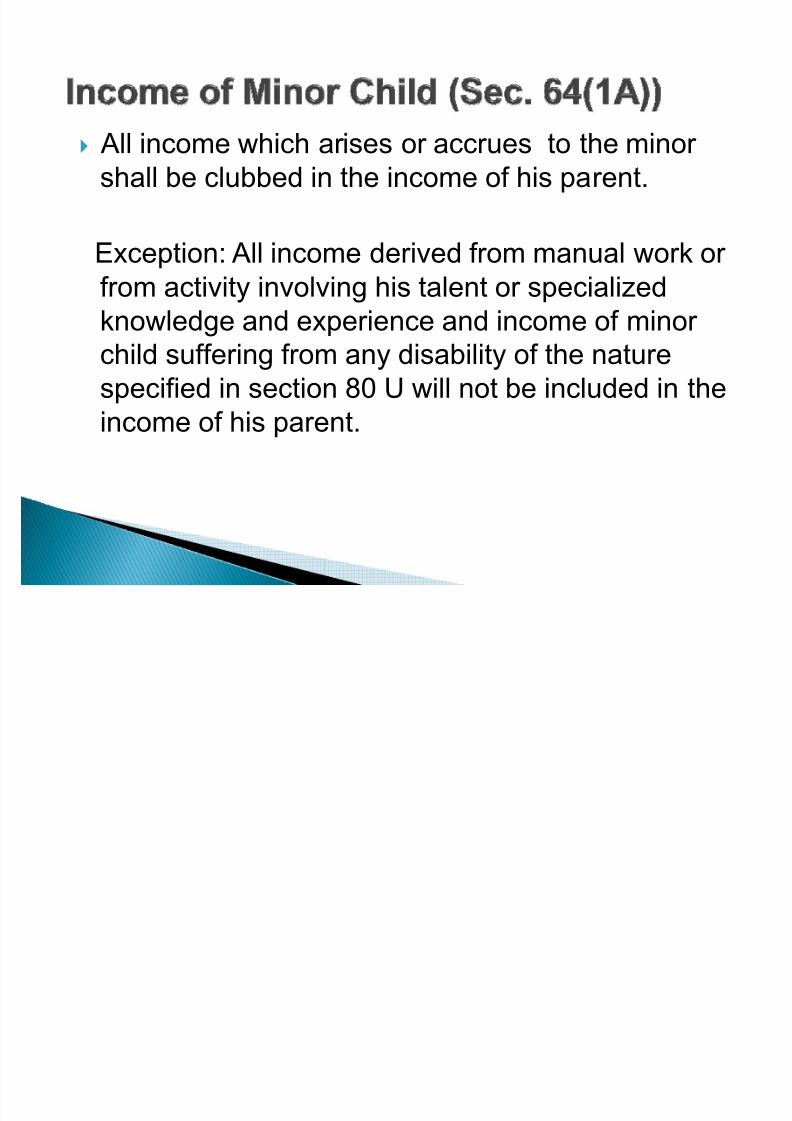

` All income which arises or accrues to the minor shall be clubbed in the income of his parent.

Exception: All income derived from manual work or

from activity involving his talent or specializedknowledge and experience and income of minor

child suffering from any disability of the nature

specified in section 80 U will not be included in the

income of his parent.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 21/28

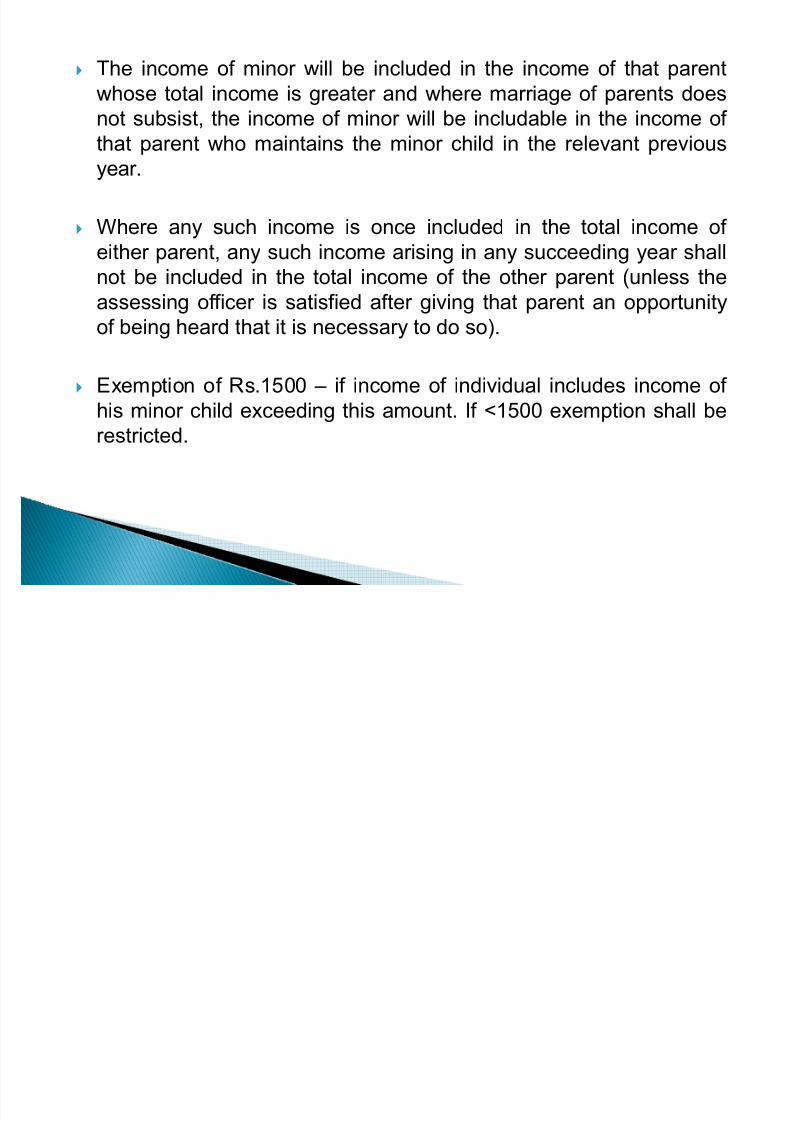

` The income of minor will be included in the income of that parent

whose total income is greater and where marriage of parents does

not subsist, the income of minor will be includable in the income of

that parent who maintains the minor child in the relevant previousyear.

` Where any such income is once included in the total income of

either parent, any such income arising in any succeeding year shall

not be included in the total income of the other parent (unless theassessing officer is satisfied after giving that parent an opportunity

of being heard that it is necessary to do so).

` Exemption of Rs.1500 ± if income of individual includes income of

his minor child exceeding this amount. If <1500 exemption shall berestricted.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 22/28

` Where a member of a Hindu undivided family hasconverted his self-acquired property into jointfamily property after December 31, 1969, income

arising from the converted property will be dealtwith as follows: The entire income from the converted property is taxable

as the income of the transferor

If the converted property is subsequently partitioned

amongst the members of the family, the income derivedfrom such converted property, as is received by thespouse of the transferor will be taxable in his hands.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 23/28

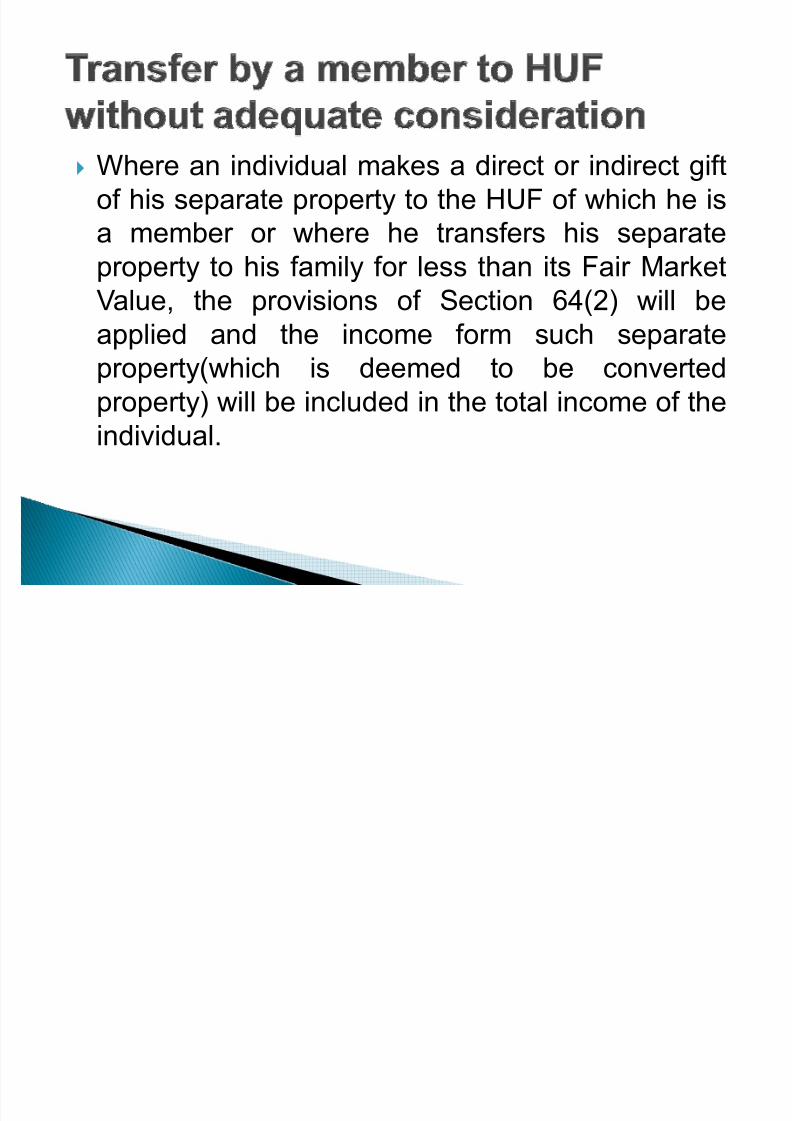

` Where an individual makes a direct or indirect gift

of his separate property to the HUF of which he is

a member or where he transfers his separate

property to his family for less than its Fair MarketValue, the provisions of Section 64(2) will be

applied and the income form such separate

property(which is deemed to be converted

property) will be included in the total income of the

individual.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 24/28

` Income arising to the transferee from the property

transferred is taxable in the hands of the

transferor. However, income arising to the

transferee from the accretion of such property or from accumulated income of such property is not

includible in the total income of the transferor.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 25/28

Illustration:

Mr. A gifts a sum of Rs50 lakhs on the occasion of

wedding anniversary. Mrs A invests this sum in a fixed

deposit, which derives interest income of Rs25,000 p.m.

The interest so derived shall be clubbed in the hands of

Mr. A, despite the fact that it is the income from

converted asset.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 26/28

` The Finance Act 1979, has inserted an

explanation to Sec. 64 to the effect that, for the

purposes of including the income of specified

persons in the income of the individual, the word³income´ will include a loss.

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 27/28

` Taxmann¶s Direct Taxes Ready Reckoner

` Caclubofindia.com

` Investopedia.com

8/8/2019 Transfer of Income Without Transfer of Assets (

http://slidepdf.com/reader/full/transfer-of-income-without-transfer-of-assets- 28/28

` Rashi Agar wal (01)

` Rajvee Chauhan (08)

` Shr uti Gembali (13)

` Medha Mukher jee (32)` Ami Patel (37)

` Kar an Popli (61)