Trading-off Volatility and Distortions?

49

Trading-off Volatility and Distortions? Economics and Politics of Food Policy During Price Spikes Hannah Pieters and Jo Swinnen LICOS – KU Leuven 2015 – FERDI Workshop 1 100 120 140 160 180 200 220 240 janv.-06 juil.-06 janv.-07 juil.-07 janv.-08 juil.-08 janv.-09 juil.-09 janv.-10 juil.-10 janv.-11 juil.-11 janv.-12 juil.-12 janv.-13 juil.-13 Food Price Index (2002-2004 =100)

Transcript of Trading-off Volatility and Distortions?

Trading-off Volatility and Distortions?

Economics and Politics of Food Policy During Price Spikes

Hannah Pieters and Jo Swinnen

LICOS – KU Leuven

2015 – FERDI Workshop 1

100

120

140

160

180

200

220

240

janv

.-06

juil.

-06

janv

.-07

juil.

-07

janv

.-08

juil.

-08

janv

.-09

juil.

-09

janv

.-10

juil.

-10

janv

.-11

juil.

-11

janv

.-12

juil.

-12

janv

.-13

juil.

-13

Food Price Index (2002-2004 =100)

Related literature includes e.g. …• Price Volatility and Stabilization

• Newberry and Stiglitz (1981)• Turnovsky et al (1980)• Gouel et al (2014, 2015)• Anderson, Ivanic and Martin (2013)• Barrett, Bellamare and Just (2013)• Minot (2014)

• Political Economy of Food Policy • Anderson (2009)• Anderson, Rausser and Swinnen (2013)• Rausser, Swinnen and Zusman (2011)

• Reactions to Price Spikes• Ivanic and Martin (2014)• Guariso, Squicciarini and Swinnen (2014)• Swinnen (1996, 2011)

• Politics and Economics of Instrument Choice• OECD (2011)• Swinnen (2009)• Swinnen, Olper and Vandemoortele (2011)

Everybody is Everybody is Everybody is Everybody is concerned about concerned about concerned about concerned about pricepricepriceprice volatilityvolatilityvolatilityvolatility (we thought …)

“The crux of the food price challenge is about price volatility, ratherthan high prices per se” (Kharas 2011)

“Food price levels are important, but so too is food price volatility. … it makes planning very difficult and … can lead to hunger and

malnutrition.”

Senior IFPRI researcher, Nov 2014 (Wall Street

“The EU’s Common Agricultural Policy [400 billion euro !] is a crucial instrument to provide a safety net for farmers in times of high price

volatility”

EU Commissioner for Agriculture, 2013

4

Rice markets and prices in China2006-2013

0

0,1

0,2

0,3

0,4

0,5

0,6ja

n/06

mar

/06

may

/06

jul/0

6se

p/06

nov/

06ja

n/07

mar

/07

may

/07

jul/0

7se

p/07

nov/

07ja

n/08

mar

/08

may

/08

jul/0

8se

p/08

nov/

08ja

n/09

mar

/09

may

/09

jul/0

9se

p/09

nov/

09ja

n/10

mar

/10

may

/10

jul/1

0se

p/10

nov/

10ja

n/11

mar

/11

may

/11

jul/1

1se

p/11

nov/

11ja

n/12

mar

/12

may

/12

jul/1

2se

p/12

nov/

12ja

n/13

mar

/13

may

/13

jul/1

3se

p/13

nov/

13

USD

/kg

INTERNATIONAL PRICES, USA: Gulf, Wheat (No. 2 Hard Red Winter), Export, (USD/Kg) Pakistan, Karachi, Wheat, Retail, (USD/Kg)5

Wheat markets and prices in Pakistan2006-2013

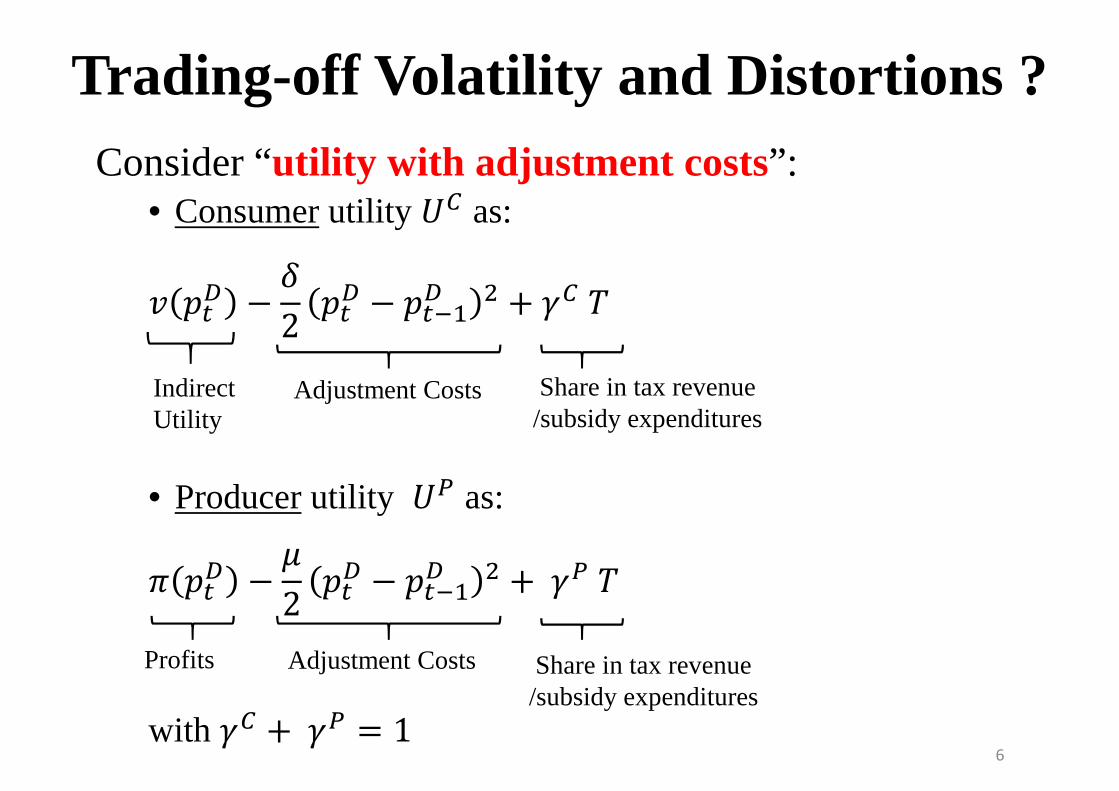

Trading-off Volatility and Distortions ? Consider “utility with adjustment costs”:

• Consumer utility �� as:

� ��� − �2 ��� − ���� � + �� �

• Producer utility �� as:

� ��� − �2 ��� − ���� � +���

with �� +�� = 1

Indirect Utility

Adjustment Costs Share in tax revenue /subsidy expenditures

Profits Adjustment Costs Share in tax revenue /subsidy expenditures

6

Socially optimal combination of volatility and distortions for a given price shock

7

But …. 1: Reviewer of the paper

•“ a long literature, notably Newbery and Stiglitz's 1981 book etc show that consumers may benefit from increased food price uncertainty ”

But … But … But … But … 2: Not everybody 2: Not everybody 2: Not everybody 2: Not everybody is is is is equally concerned equally concerned equally concerned equally concerned

about about about about pricepricepriceprice volatilityvolatilityvolatilityvolatility

• “Why food price volatility doesn’t matter”

(Barrett & Bellemare 2011)

• “Standard assessment of the welfare cost of food price volatility… suggest that … the cost to consumers is small if not negative. The only people who can expect significant gains from pricestabilization are the producers – and especially affluentproducers” (Christophe Goeul, 2013)

=> “Price stabilization is regressive” (i.e. benefits the rich)

Waugh (QJE 1944)

Waugh (QJE 1944)

Impact of price instability on consumer surplus

= G – L > 0

Oi (1961, Econometrica)

Samuelson (QJE 1972)

Samuelson (QJE 1972)

So: back to the drawing board …

• A new model based on Waugh, Oi, Newbery andStiglitz, Turnovsky et al, Barrett, Bellemare et al,Gouel et al, ….

• Following Barrett (1996):• a two-period model• product prices unknown when production decisions are

made• post-harvest prices announced before the consumer

makes its decision.

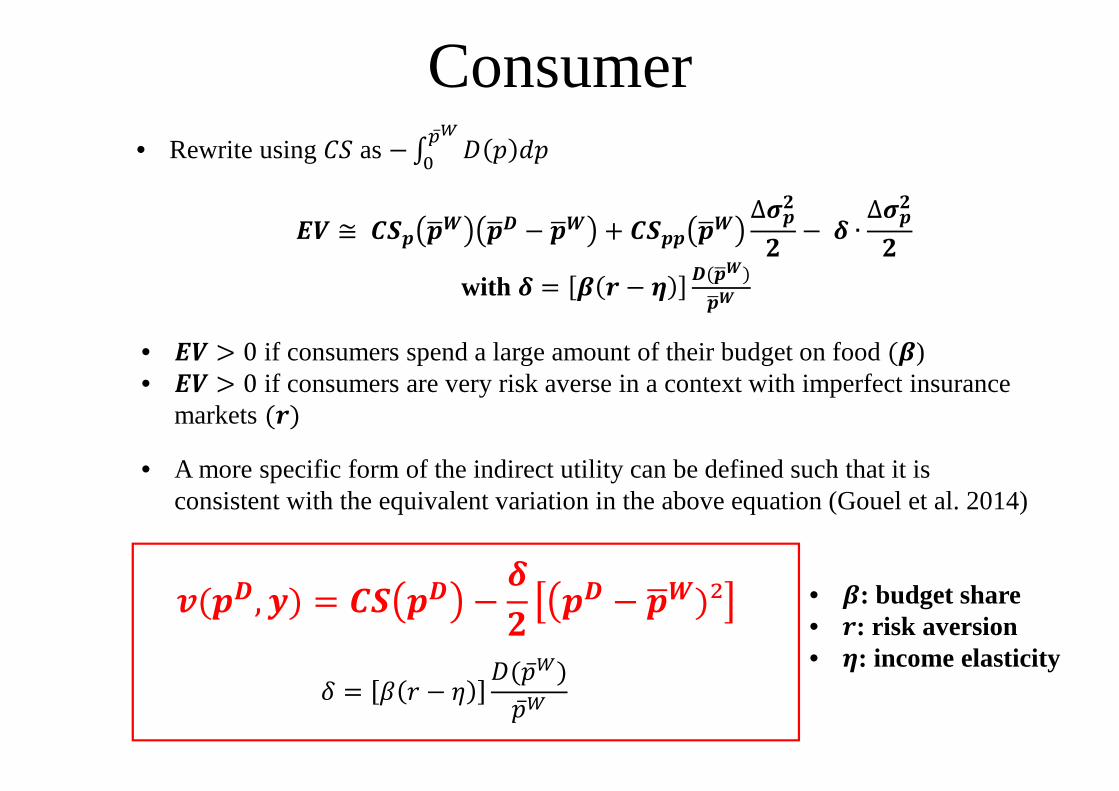

Consumer

����� � �(��, � • Maximization problem

• Benefit of price stabilization policy is analysed by looking at the Equivalent Variation

� �(�!, � + �") = � �(��, �)(Equivalent Variation measures consumer benefits of stabilization policy)

• Using Turnovsky et al. (1980) :

�" ≅ −� �%! ∙ �%� − �%! + ' ( − ) − * � �%! ∆,�-

-�%!

• ': budget share spend on food (. ≤ ' ≤ 0)• ): relative risk aversion of the consumer () ≥ .)• (: income elasticity of consumption (( ≥ .)

• * : price elasticity of consumption (* ≤ .)

Consumer

�" ≅ 23� �%! �%� − �%! + 23�� �%! ∆,�-

- − 4 ∙ ∆,�-

-with 4 = ' ) − ( �(�%!)

�%!

• �" > 0 if consumers spend a large amount of their budget on food (')• �" > 0 if consumers are very risk averse in a context with imperfect insurance

markets ())• A more specific form of the indirect utility can be defined such that it is

consistent with the equivalent variation in the above equation (Gouel et al. 2014)

�(��, �) = 23 �� − 4- 7�� − �%!)²

� = 9 : − ; <(�̅>)�̅>

• Rewrite using ?@ as −A < � B�C̅DE

• ': budget share • ): risk aversion • (: income elasticity

Producer

�" ≅ 3(�%) �%� − �%! − F G − ) + H ∙ ∆,�-

-�%!

• Equivalent Variation is approximated by:

�" ≅ �%� − �%! ����

− ���-��

∙ ∆,�-

• Using Barrett (1996); Bellemare et al (2013) :

• F: dominance of the food crop in the total production (. ≤ F ≤ 0)• ): relative risk aversion of the producer () ≥ .)• G: income elasticity of the marketable surplus (G ≤ .)

• H : price elasticity of the marketable surplus (H ≥ .)

• Rewrite:

�" ≅ I� �%! �%� − �%! + I�� �%! ∆,�-- − J ∙ ∆,�-

-

with K = F() − G) 3(�%!)�%!

Producer�" ≅ I� �%! �%� − �%! + I�� �%! ∆,�-

- − J ∙ ∆,�--

with J = F() − G) 3(�%!)�%!

• A more specific form of the indirect utility can be defined such that it is consistent with the equivalent variation in the above equation (Gouel et al. 2014):

�(��, �) = I �� − J- �� − �%! -

• �" > 0 when producers are highly dependent on the production of food for their incomeL

with μ = L(: − N) O(C̅D)C̅D

• F: dominance of the crop • ): relative risk aversion• G: income elasticity of the

marketable surplus (G ≤ .)

The government

• Policy intervention to stabilize prices (with budgetary implications T):

� = �� − �> (< �� − @ �� )

• Government maximizes social welfare

PQRCS?@ �� − �

2 �� − �̅> � + � �� − T2 �� − �̅> �

+ �� − �> (< �� − @ �� )

Social Optimum with Volatility and Adjustment Costs

• The social welfare maximizing domestic price ��∗ is determined by First order condition :

−< ��∗ − � ��∗ − �̅> + �� < ��∗ − @ ��∗

+�� ��∗ − �> <V ��∗ − @V ��∗ +

@ ��∗ − � ��∗ − �̅> +�� < ��∗ − @ ��∗

+�� ��∗ − �> (<V ��∗ − @V ��∗ )= 0

21

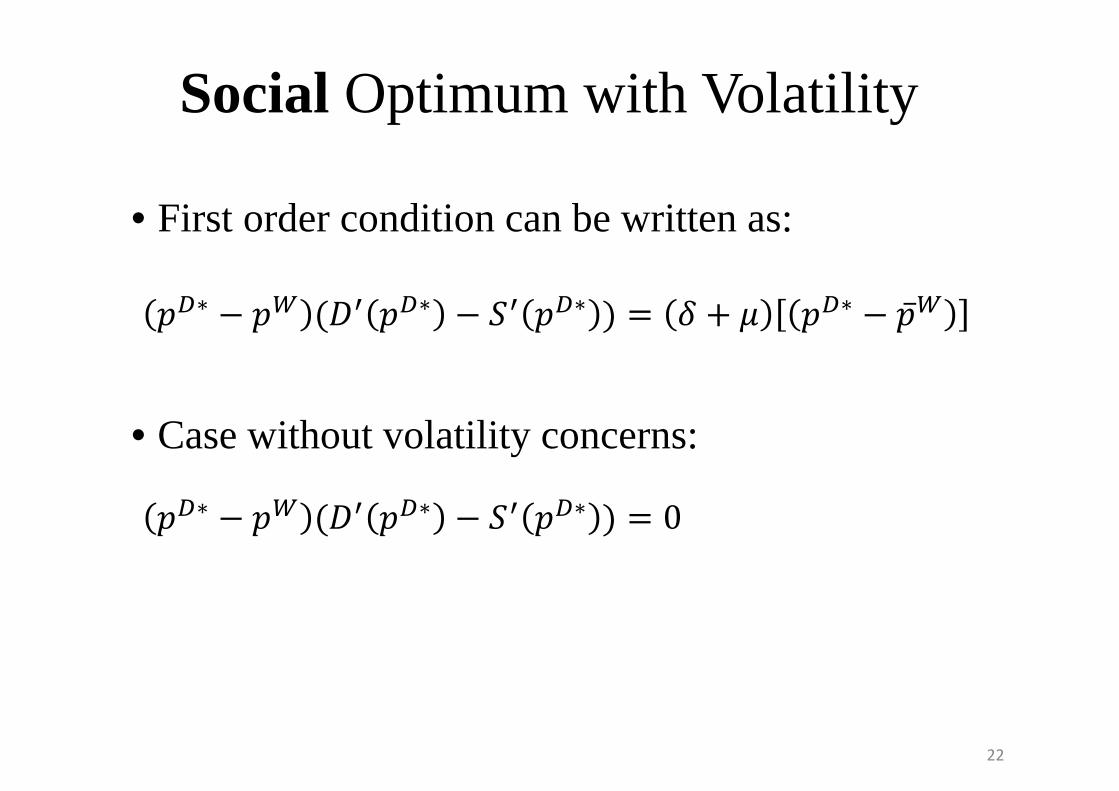

Social Optimum with Volatility

• First order condition can be written as:

• Case without volatility concerns:

��∗ − �> (<V ��∗ − @V ��∗ ) = � + � ��∗ − �̅>

��∗ − �> (<V ��∗ − @V ��∗ ) = 0

22

• First order condition can be written as:

or

Social Optimum with Volatility

��∗ = W�%! + 0 − W �!

withW = 4XJ4XJX3V�V ≥ . and . ≤ W ≤ 0

��∗ − �> = Y ��∗ − �̅>

with Y = ZX[�\OV = ]

]� ≤ 023

Social Optimum for different

24

• First order condition can be written as:

or

Social Optimum with Volatility

��∗ = ^�̅> + 1 − ^ �>

with^ = ZX[ZX[XOV�V ≥ 0 and 0 ≤ ^ ≤ 1

��∗ − �! = H ��∗ − �%!

with H = 4XJ�\3V = W

W0 ≤ .25

International price shocks and trade-off between distortions and volatility

26

Optimal combinations of observedvolatility and distortions for a givenprice shock

27

Empirical Evidence From developing countries

• Volatility (the coefficient of variation)

� = _�

• Distortions:

B = `1�

a

�bE��� − ��c

28

Distortions and volatility (2007-2013)

D (V=0): Minimum distortions at zero volatility V (D=0): Volatility at zero distortions (= world market price volatility)

29

Rice Wheat

Maize

Empirical Evidence Measuring the inefficiency of the actual

policy

Dis

tort

ion

Volatility

Vertical Distance

Horizontal Distance

Overall Distance

Country A

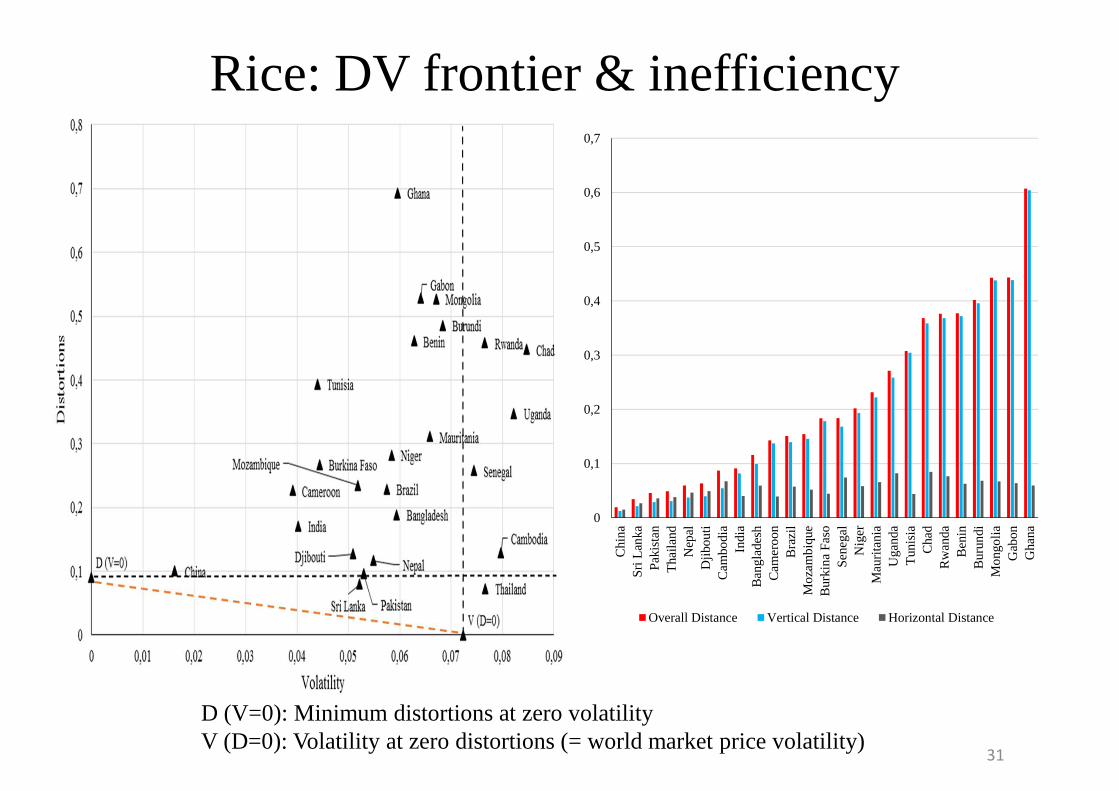

Rice: DV frontier & inefficiency

D (V=0): Minimum distortions at zero volatility V (D=0): Volatility at zero distortions (= world market price volatility)

31

0

0,1

0,2

0,3

0,4

0,5

0,6

0,7

Chi

na

Sri

Lan

kaP

akis

tan

Tha

iland

Nep

alD

jibou

tiC

ambo

dia

Indi

aB

angl

ades

hC

amer

oon

Bra

zil

Mo

zam

biq

ueB

urki

na

Fas

oS

eneg

alN

iger

Mau

rita

nia

Uga

nda

Tun

isia

Cha

dR

wan

daB

enin

Bur

undi

Mo

ngo

liaG

abon

Gha

na

Overall Distance Vertical Distance Horizontal Distance

WhyWhyWhyWhy sosososo muchmuchmuchmuch “policy “policy “policy “policy inefficiencyinefficiencyinefficiencyinefficiency” ? ” ? ” ? ” ? (even allowing for stability objectives)

Possible explanations:

1. Political determinants

2. Measurement problems

32

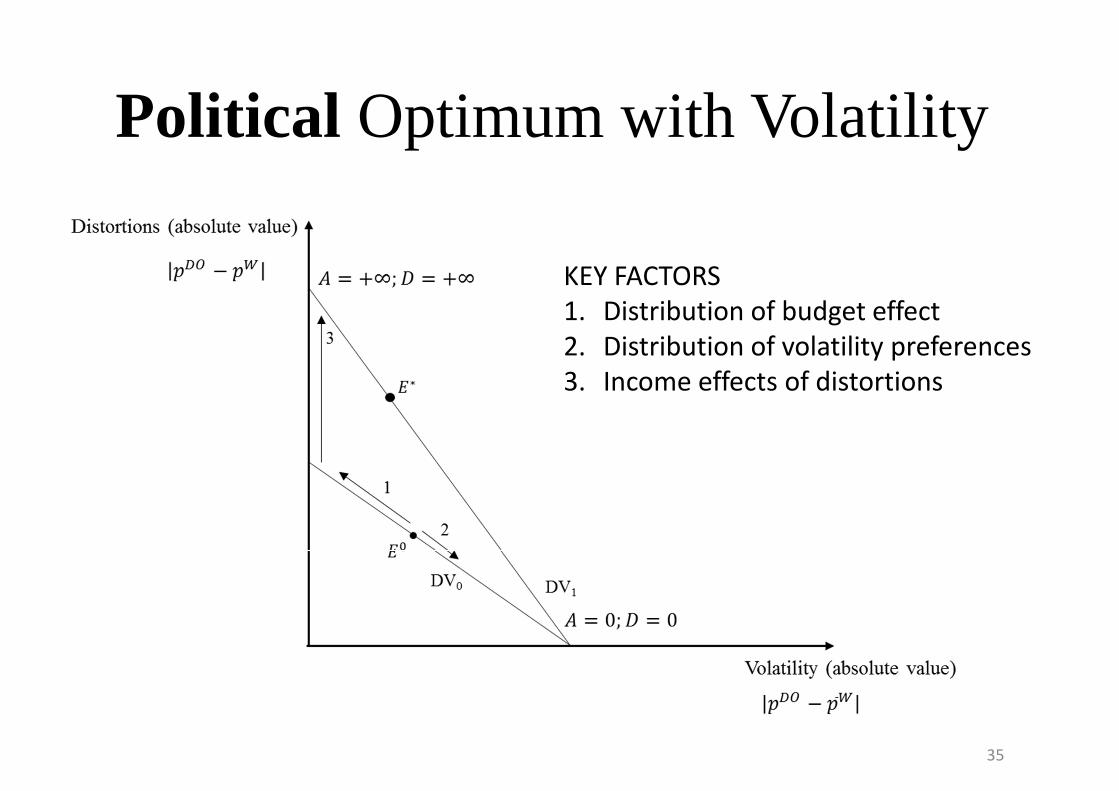

Political Optimum with Volatility and Adjustment costs

• Adjusted Grossman and Helpman (1994) model: the government maximizes:

PQRCS de?e(��) + dC?C(��) +f(��)

• de and dCare relative strength of the consumer and producer lobby

• ?e is the truthful contribution schedule of consumers• ?� is the truthful contribution schedule of producers• f(��) is social welfare

33

Political Optimum with Volatility

• First order condition :

34

��g − �! =hi ��g − �%!

− h ∙ 2i ∙ i + 2 ��g − �%!

+ �iX2 ��g − �%!

+� − 2 ∙ ji + 2

k = (� + �)

l = <V ��m − @V ��m

? = de�e + dC�C

< = d�� + d��

n = d�< ��m − d�@ ��m

o = < ��m − @ ��m

Political Optimum with Volatility

35

KEY FACTORS

1. Distribution of budget effect

2. Distribution of volatility preferences

3. Income effects of distortions

Let’s look at the correlation withsome empirical factors

Note:

• Almost all empirical indicators have a “politicaleconomy” aspect and a “measurement problem” aspect

• Observed distortions will reflect interaction of political influence and price moment

36

37

40.8

11.08

99.2

134.88

19.31

24.60

Distortions (2000-2005) Distortions (2007-2013)

MeasuredMeasuredMeasuredMeasured distortiondistortiondistortiondistortion, , , , politicalpoliticalpoliticalpolitical power, power, power, power, andandandand pricepricepriceprice movementmovementmovementmovement

DV Inefficiency & Absolute ea-NRA

38

Rice

Wheat

Maize

DV Inefficiency & Tax Revenues

39

Import/Export Subsidies

Import/ExportTariffs

Mean Overall Inefficiency 0.106 0.274Variance 0.014 0.024Observations 8 13Hypothesized Mean Difference 0df 18t Stat -2.795P(T<=t) one-tail 0.006t Critical one-tail 1.734P(T<=t) two-tail 0.012t Critical two-tail 2.101

Rice

Import/Export Subsidies

Import/ExportTariffs

Mean Overall Inefficiency 0.031 0.067Variance 0.000 0.003Observations 3 3Hypothesized Mean Difference 0df 2t Stat -1.161P(T<=t) one-tail 0.183t Critical one-tail 2.920P(T<=t) two-tail 0.365t Critical two-tail 4.303

Import/Export Subsidies

Import/ExportTariffs

Mean Overall Inefficiency 0.129 0.128Variance 0.008 0.004Observations 11 7Hypothesized Mean Difference 0df 16t Stat 0.030P(T<=t) one-tail 0.488t Critical one-tail 1.746P(T<=t) two-tail 0.976t Critical two-tail 2.120

MaizeWheat

Regression

40

Coefficients Standard Error P-valueAbsolute Ex-ante NRA 0.212 0.118 0.085Taxation indicator -0.062 0.051 0.234Intercept 0.113 0.033 0.002R-Square 0.120Observations 28

pqrsstutrqu�t = '0(r�_wxh)t+'-y���zt{qt +Ht

Taxation = 1 if the country has import or export tariffsAbsolute Ex-ante NRA is a measure for the power of lobby groups

DV Inefficiency & Import Share

41

Rice

Maize

Wheat

DV Inefficiency & Landlocked

42

Rice

Wheat Maize

Regression

43

Coefficients Standard Error P-valueAbsolute Ex-ante NRA 0.145 0.114 0.218Taxation indicator 0.001 0.056 0.989Net-Import share 0.032 0.031 0.310Landlocked 0.119 0.056 0.046Maize dummy -0.060 0.050 0.245Wheat dummy -0.095 0.061 0.132Intercept 0.101 0.044 0.033R-square 0.377Observations 28

|}~�����~}��� =9�(~Q_��k)�+9��QRQ���}� +9� |P��:��+ 9� �Q}B����~B�+9� f�~Q��+9��Q��~� + Y�

Taxation = 1 if the country has import or export tariffsAbsolute Ex-ante NRA is a measure for the power of lobby groupsLandlocked = 1 if country is landlockedNet-Import share = share of net imports in total trade

D (V=0): Minimum distortions at zero volatility V (D=0): Volatility at zero distortions (= world market price volatility)

44

0

0,1

0,2

0,3

0,4

0,5

0,6

Overall Distance Vertical Distance Horizontal Distance

Trading off distortions and

volatility in Chinese rice markets

Major inefficiencies in some countries

Concludingcomments

• Issues :

• How much “distortions” in the “distortion measures” ?

• Interaction of politics and price direction

• Policy instrument choice• Short run : “Fire Brigade Policy-Making” (Swinnen, 1996)

• Medium run : political economy / social optimum

• Long run: use different instruments (development-related)

• Overall implications ? • Ignoring externalities (Anderson et al argument) : how important ?

45

Concludingcomments

46

Derivation of utility function

47

����� � �(��, � • Maximization problem

• Benefit of price stabilization policy is analysed by looking at the equivalent variation

� �(�!, � + �") = � �(��, �)• Equivalent Variation is approximated by:

�" ≅ �%� − �%! ����

− ���-��

∙ ∆,�-

• Using Turnovsky et al. (1980) and Roy’s identity:

�" ≅ −� �%! ∙ �%� − �%! + ' ( − ) − * � �%! ∆,�-

-�%!

• Rewrite using ?@ as −A < � B�C̅DE with ?@C =�?@ ��⁄ = −<(�) and ?@CC =

−<C(�): �" ≅ 23� �%! �%� − �%! + 23�� �%! ∆,�-

- − 4 ∙ ∆,�-

-with 4 = ' ) − ( �(�%!)

�%!

Derivation of utility function

48

�" ≅ 23� �%! �%� − �%! + 23�� �%! ∆,�-

- − 4 ∙ ∆,�-

-with 4 = ' ) − ( �(�%!)

�%!

• �" > 0 if consumers spend a large amount of their budget on food• �" > 0 if consumers are very risk averse in a context with imperfect insurance

markets

• A more specific form of the indirect utility can be defined such that it is consistent with the equivalent variation in the above equation

�(��, �) = ?@ �� − �2 (�� − �̅>)²

� = 9 : − ; <(�̅>)�̅>

Political Optimum with Volatility

• First order condition can be written as:

49

��g − �! = hi + 2 ��g − �%! + �

i+ 2 ��g − �%! + � − 2 ∙ ji + 2

k = (� + �)

l = <V ��m − @V ��m

? = de�e + dC�C

< = d�� + d��

n = d�< ��m − d�@ ��m

o = < ��m − @ ��m