TRADE AUDIT REPORT OF THE KYRGYZ REPUBLICsiteresources.worldbank.org/.../4_Trade_Audit_eng.pdf ·...

42

TRADE AUDIT REPORT OF THE KYRGYZ REPUBLIC Second draft Souleymane Coulibaly June 2007

Transcript of TRADE AUDIT REPORT OF THE KYRGYZ REPUBLICsiteresources.worldbank.org/.../4_Trade_Audit_eng.pdf ·...

TRADE AUDIT REPORT OF THE

KYRGYZ REPUBLIC

Second draft

Souleymane Coulibaly

June 2007

wb275803

Text Box

Background paper prepared for the Kyrgyz Republic under Country Economic Memorandum TA

wb275803

Text Box

World Bank

ABBREVIATIONS

ADB: Asian Development Bank

BEEPS: Business Environment and Enterprise Performance Survey

CCT: Common Customs Tariff

CDS: Country Development Strategy

CEM: Country Economic Memorandum

EU-TACIS: European Union Technical Assistance to Commonwealth Independent States

EURASEC: Eurasian Economic Community (EAEC)

IECC: International Express Carriers’ Conference

FTA: Free Trade Agreement

GATS: General Agreement on Trade in Services

GCR: Global Competitiveness Report

GTZ: German Technical Cooperation Agency

HS: Harmonized System

ILAC: International Laboratory Accreditation Cooperation

ISO: International Organization for Standardization

ITC: International Trade Center

MEDIT: Ministry of Economic Development, Industry and Trade

NISM: National Institute for Standards and Metrology

OIE: International Office of Epizooties

PSA: Private Sector Assessment

RCA: Revealed Comparative Advantage

SECO: Swiss State Secretariat for Economic Affairs

SME: Small and Medium Enterprise

SPS: Sanitary and Phytosanitary

TBT: Technical Barriers to Trade

UNDP: United Nations Development Program

VAT: Value-Added Tax

WEF: World Economic Forum

WTO: World Trade Organization

2

Table of Content Page 1) Introduction .................................................................................................................. 4

a) Context........................................................................................................................ 4 b) Methodology............................................................................................................... 4

2) Trade performance and overall business environment............................................. 5 a) The 2006 WTO Trade Policy Review ........................................................................ 5 b) Kyrgyzstan trade performance.................................................................................... 7

Overall performance ................................................................................................... 7 Trade complementarity with neighboring countries................................................... 9 Revealed Comparative Advantage ............................................................................ 11

c) Kyrgyzstan business environment ............................................................................ 12 The 2006 Global competitiveness report on Kyrgyzstan .......................................... 12 The 2006 Doing Business report on Kyrgyzstan....................................................... 13 The 2005 BEEPS results for Kyrgyzstan .................................................................. 14

3) Key Impediments to export expansion in Kyrgyzstan ............................................ 16 a) Infrastructure quality and Transport flows ............................................................... 16

Transport flows and modal split ............................................................................... 16 Roads......................................................................................................................... 17 Railways .................................................................................................................... 18 Airports ..................................................................................................................... 18

b) Technical and administrative barriers to trade ......................................................... 19 Technical procedures................................................................................................ 19 Customs procedures.................................................................................................. 20 Administrative barriers ............................................................................................. 21

c) Other impediments to trade expansion ..................................................................... 22 Tax issues .................................................................................................................. 22 Finance issues ........................................................................................................... 23 Diagnosis of the textile sector................................................................................... 23 Diagnosis of the dairy sector .................................................................................... 27

4) Ongoing governmental initiatives and policy recommendations ........................... 30 a) Ongoing initiatives of the government to reduce barriers to trade ........................... 30

Technical regulation initiatives ................................................................................ 30 Administrative regulation initiatives......................................................................... 31

b) Policy recommendations........................................................................................... 32 Appendices....................................................................................................................... 34

Appendix 1: Documents required for Customs clearance ...................................... 34 Appendix 2: List of documents needed in the export process................................. 37 Appendix 3: List of documents needed in the import process ................................ 38 Appendix 4: Formal and informal costs born by freight forwarding companies . 41 Appendix 5: Formal and informal costs born by the dairy firm MIS ................... 42

3

1) Introduction

a) Context

1. The 2005 CEM of the Kyrgyz Republic aimed at understanding the divergence between the sound liberal policy of the Government and the somewhat disappointing export performance of the country failing to tap in the potential demand from its fast-growing neighbors (China, Kazakhstan and Russia). The report identified on the one hand the strong reliance on agriculture, mining and hydropower, and on the other hand some structural, policy and institutional deficiencies (e.g. high formal and informal transit and transport costs, poor infrastructures, limited competitive pressures, corruption, regulatory and standards regimes, customs and tax regimes…) as the main causes of this divergence. To address these shortcomings, a three-pronged strategy were proposed: leverage the WTO rules obligation to accelerate reforms in domestic trade related institutions (standards regimes, customs administration, and telecommunication services); focus on EURASEC membership to rationalize border, customs and transit procedures as well as technical standards; and design a new organizational arrangements allowing for capacity building and coordination on national, regional and international policy issues.

2. In its recent report to the WTO Trade Policy Review Body, the Kyrgyz Government has identified as future trade policy direction the active diversification of on-gold industrial sectors with a clear focus on value added sectors and export of finished goods such textile and clothing, agro-industry, energy, mining and construction. It is particularly seeking the technical assistance of the World Bank through the CEM follow-up to identify the set of interventions that could lower the costs of getting Kyrgyz goods to export markets. This Trade Audit report is a contribution to the CEM follow-up report.

b) Methodology

3. The World Bank Trade Audit methodology1 has been designed to examine and evaluate difficulties and obstacles presented to cross-frontier movement of a routine consignment and its associated payment. It proposes a series of questionnaires to be used to conduct structured interviews with some key actors involved in international trade such as importers, exporters, freight forwarders, customs brokers, customs, border crossing points, port, airport, financial institutions, chamber of commerce, department of trade…

4. However, since the launching of this methodology in 2000, many studies have been initiated by the World Bank and other donors dealing with some of the issues covered by the Trade Audit methodology. To avoid duplicating these works, the proposed methodology combines a comprehensive desk study aiming at collecting any relevant information from existing or ongoing trade and transport facilitation studies on Kyrgyzstan, with a series of interviews with some selected stakeholders based on the

1 The World Bank – IECC, Trade and Transport Facilitation: an Audit Methodology, February 2000.

4

Trade Audit methodology. The study is then completed with two case studies evaluating the different costs borne by two Kyrgyz SMEs operating in dairy and textile sectors. These costs can be categorized in four groups:

i) Costs borne within the plant (production and packaging costs, loading costs in the container…)

ii) Costs borne within the exporting country (transport costs, administrative costs, informal payments made from the gate of the plant to the border crossing point…)

iii) Costs borne in international transit (transit cost, transport costs, other informal and formal payments from the border crossing point of the first transit country to the border crossing point of the destination country…)

iv) Costs borne within the destination country (custom duties, transport costs, other formal and informal costs from the border crossing point to the distribution center…)

5. The report is organized as follows. Section 2 describes the current trade performance and overall business environment, Section 3 presents the key impediments to export expansion based on existing studies and findings from the Trade Audit mission, and Section 4 addresses the policy issues by reviewing the ongoing activities of the government on these issues and proposing some policy recommendations.

2) Trade performance and overall business environment

6. Kyrgyzstan is a fascinating mountainous country landlocked by China on the West side, Kazakhstan on the North side, Uzbekistan on the East side, and Tajikistan on the South side. In 2005, its population represented 0.4% of that of these neighbors, its exports to these countries represented 27% of its total export, and its imports from them represented 31% of its total imports. The average GDP per capita growth rate of these neighbors was 7.5% and their average import growth rate was 25%, while Kyrgyzstan GDP per capita was declining at a -1.2% rate. These simple physical and economic facts clearly set export-led growth strategy as the only sustainable growth policy of Kyrgyzstan. This policy option is clearly reflected in the recent and first WTO Trade Policy review of Kyrgyzstan.

a) The 2006 WTO Trade Policy Review

7. The Trade Policy Review is a tool used by the WTO to oversee the national trade policies of its members. To give a comprehensive picture of the situation, the member is requested to provide its own evaluation of the trade environment. Kyrgyzstan’s trade policy was reviewed for the first time in 2006, since its accession to the WTO. According to the review committee, many revised legislation covering key trade-related areas such as customs, enterprise activity, intellectual property, investment, and specific sectors,

5

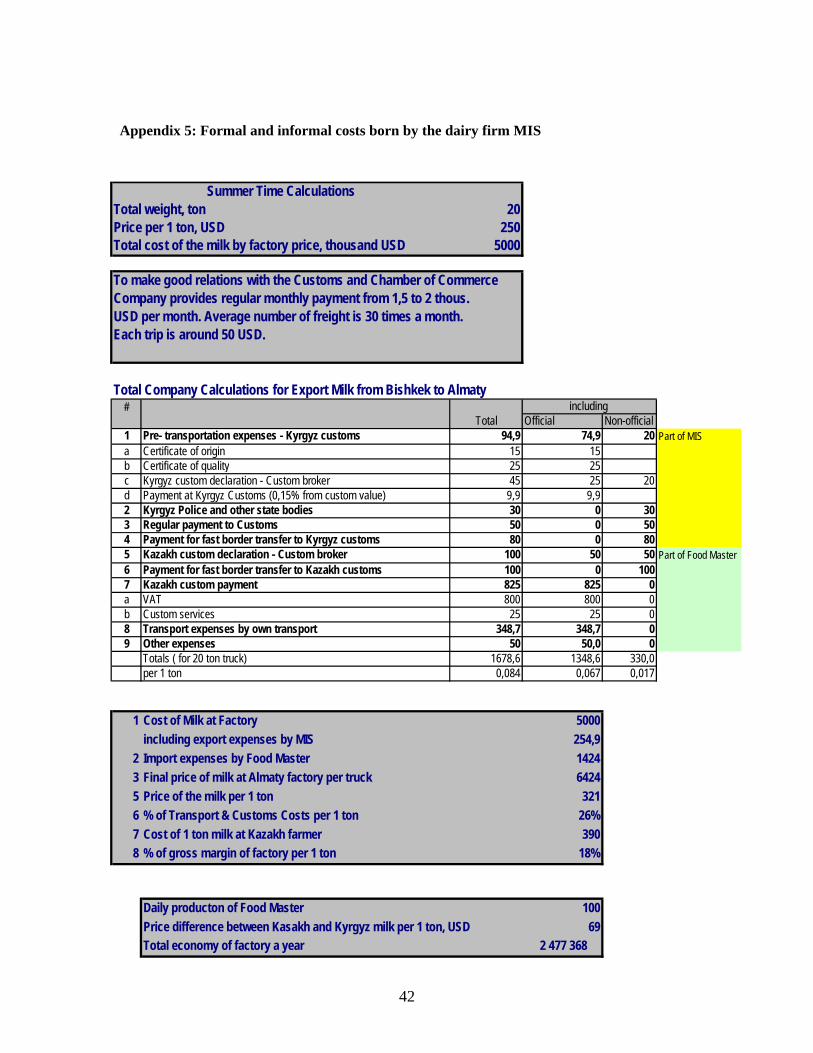

such as banking, insurance, and telecommunications are now taking into account the WTO agreements. Equal and non-discriminatory national treatments have been extended to foreign investors and domestic commodity taxes such as VAT no longer discriminate against imports (except for cigarettes). The government is also currently negotiating the signature of the Agreement on Government Procurement (GPA).

8. Since the WTO accession, the tariff (which is the country’s main trade policy instrument) has been considerably reduced: the simple average applied MFN (Most Favored Nation) rate is 4.9%, down from 5.2% in 2005 and 8.7% in 1999. Tariffs are higher on agricultural (8.1%) than industrial goods (4.1%). The modal rate of 10% is covering 34% of tariff lines, 13% of the line are 5% or less and 46% are duty free. Except for a few sugar items with rates of 20% and 30%, the highest rate is 15%. Almost all the rates are ad-valorem (98.7%), which improves transparency. A non-cost-based customs fee of 0.15% of c.i.f. value is payable on all imports to cover costs of providing customs services. On the transport side, foreign haulers who do not have special permits or TIR carnets are charged a US$250 fee to enter the Kyrgyz Republic. Transit restrictions by neighboring countries, especially Uzbekistan and until recently Kazakhstan, impede Kyrgyz exports.

9. No anti-dumping, countervailing or safeguard measures have been applied by the country. Customs valuation is made by using transaction values and no pre-shipment inspection is required. Nevertheless, customs formalities and procedures, both formal and informal, as well as corruption, restrict imports through duplicative and excessive physical inspections. Improved customs cooperation with neighboring countries to facilitate trade is a government priority. Smuggling is substantial. Kyrgyz exports to industrial markets are eligible for non-reciprocal preferential treatment under the Generalized System of Preferences (GSP), but except for the EU’s granted preferences, the other schemes such as those of Japan and the United States are of limited value to Kyrgyz exporters due to complexity and restrictive rules of origin.

10. Exports are unregulated, except for non-ferrous metal fragments and waste, and there are no export taxes. No direct export subsidies apply, including on agricultural products. A few export licenses are administered to a range of products for reasons of human safety and public health, environmental protection, national security, and preservation of art, historical and archaeological treasures, and exhaustible natural resources.

11. However, despite all these improvements the review committee considers the overall business and regulatory environment unfriendly. In addition, the participation in multiple preferential trading agreements adds uncertainty to the country’s trade regime. Indeed, the country is currently negotiating three potential customs union (CIS excluding Ukraine, EAEC2, and CACO3). Only EAEC is operating and making any real progress, and there are recent initiatives to integrate CACO into EAEC. The Kyrgyz trade regime is further complicated by the array of regional and bilateral FTAs covering nine CIS 2 EuroAsian Economic Community, initiated in 1995 by Russia and Belarus and including today Kazakhstan, Kyrgyzstan, Tajikistan, and Uzbekistan. 3 Central Asian Cooperation Organization, initiated in 1991 by Kazakhstan, Kyrgyzstan, Turkmenistan as the Central Asian Commonwealth, including today Tajikistan and Russia in addition and without Turkmenistan.

6

states (six at the time of accession). This “spaghetti bowl” of agreements combined with scarce human resources and capacity bottlenecks weaken the transparency of the country’s trade regime. In addition to this, the poor capacity of ministries and agencies to fulfill WTO obligations hinders trade policy development. Technical assistance is needed to implement commitments, including new arrangements resulting from the Doha negotiations. Areas requiring particular attention are: implementation of SPS rules by the Ministry of Agriculture, Water Resources and Processing Industry, and the Ministry of Health; GATS services obligations; and negotiations to join the Government Procurement Agreement.

b) Kyrgyzstan trade performance

Overall performance

12. Since the collapse of the FSU, Kyrgyzstan’s fate has been tied to the desire of its leaders to fully take part in the world economy. As an illustration, three months after its independence in October 1991, the newly elected President signed the new Commonwealth of Independent States, and the country joined the UN 1992. The application to WTO membership followed on early 1996. Since then, the successive Kyrgyz governments have clearly opted for an export-led growth strategy, which is the only sustainable growth strategy given the country’s geographical and economic constraints. As a result, the country has been more and more involved in the world economy as depicted by the trend of its trade openness.

Figure 1: Kyrgyzstan’s trade openness indicators

0%

20%

40%

60%

80%

100%

120%

2000 2001 2002 2003 2004 2005

X/GDP (X+M)/GDP

Source: WDI 2006 and author’s calculations.

13. However, this openness has been led by imports: Kyrgyzstan’s export to GDP ratio remained stable at 40% over the period 2000-2005. In 2006, 80% of the imports were made of mineral fuels, nuclear and electrical machinery, transportation and

7

professional equipments, chemical and plastic products, wood products, and vegetables products and foodstuffs, while 80% of the exports were precious stones and metals, mineral fuels, nuclear and electrical machinery, nuclear and electrical machinery, transportation equipment, plastic products, textile products, and animal and vegetable products.

14. At the product level, the total number of exported products has been decreasing over the period 2000-2006, while the number of products exported at more than 50,000 US$ were increasing (Figure 2). This suggests an increase in the market share of more products over time, hence a rationalization of the export process. Indeed, to fully tap in scale economies, exporting firms need to increase their production; in other word, size matters for export efficiency.

Figure 2: Number of 6-digit HS products and trading partners over 2000-2006

0200400600800

10001200140016001800

2000 2001 2002 2003 2004 2005 2006

All

prod

ucts

0

50

100

150

200

250

300

350

400

Prod

uct w

ith v

alue

>50,

000$

All products Value>50,000$

0102030405060708090

2000 2001 2002 2003 2004 2005 2006

Num

ber o

f tra

de p

artn

ers

All partners Partners w ith export>50,000$

Source: COMTRADE and author’s calculation.

8

15. Figure 2 also presents the evolution of the number of Kyrgyzstan’s trading partners. Over the period 2000-2006, the total number of export partners has been increasing from about 60 to 80, while the number of export partners buying more than 50,000 US$ of Kyrgyz products per year has been stable around 50. This suggests a diversification of export markets which is a positive trade performance for Kyrgyzstan in line with the government strategy of more involvement in the world economy. In 2006, the top 10 export partners of Kyrgyzstan were Switzerland, Kazakhstan, Russia, Afghanistan, China, Uzbekistan, Turkey, Tajikistan, United Emirate Arab and Iran. Given the considerable trade barriers faced by Kyrgyzstan because of its landlockedness, a realistic growth policy targeting the short to medium term should first try to tap in the increasing demand in its fast-growing: China, Kazakhstan and Russia. For an illustration purpose, some trade performance indicators emphasizing the interaction with these neighboring countries are analyzed.

Trade complementarity with neighboring countries

16. The trade complementarity index shows how well the export profile of a country matches the import profile of a potential trading partner. The index of trade complementarity between countries k and j is defined as:

∑ −×−=i

ijikkj xmC 5.0100

where xij is the share of good i in global exports of country j and mik is the share of good i in all imports of country k. The index is zero when no goods are exported by country i or imported by country k, and 100 when the export and import shares of countries i and k exactly match. Figure 3 shows the evolution of the complementarity index between Kyrgyzstan and China, Kazakhstan and Russia over the period 2000-20054.

17. Starting from a relatively low level in 2000, the complementarity between Kyrgyzstan and China and Kazakhstan has been increasing over time, indicating an increasing export potentiality of Kyrgyz products to these markets. On the other hand, the relatively high complementarity between Kyrgyzstan and Russia in 2000 shrank over time, although depicting a reversed trend since 2004. A close look at the trade statistics indicate that the Kyrgyz products exported to these markets over this period were quite diversified (Figure 4).

4 The index has been computed using the 6-digit HS products from the COMTRADE database.

9

Figure 3: Kyrgyzstan trade complementarity with its neighbors

0

2

4

6

8

10

12

14

16

18

2000 2001 2002 2003 2004 2005

Com

plem

enta

rity

inde

x

Complementarity w ith China

Complementarity w ith Kazakhstan

Complementarity w ith Russia Source: COMTRADE and author’s calculation

Figure 4: Average number of products exported over 2000-2006

0 10 20 30 40 50

Animals

Chemicals

Foodstuffs

Footw ear

Hides

Machinery

Metals

Minerals

Miscellaneous

Plastics

Stone

Textiles

Transportation

Vegetables

Wood

Export to CHN>50,000$ Export to KAZ>50,000$ Export to RUS>50,000$

Source: COMTRADE and author’s calculations.

10

18. On average, more than 20 specific products of textile, machinery, metal, hide, chemicals and vegetables were exported to China, Kazakhstan and Russia during the period 2000-2006. Figure 4 also reveals a geographical concentration of some exports: textile and vegetable products are mainly exported to Russia; machinery products are mainly exported to Kazakhstan and Russia; hides, metals and chemicals are mainly exported to China. However, the traded volumes of these products are still quite small (Table 1).

Table 1: Kyrgyzstan exports (in ‘000 US$)

HS code Partner 2000 2001 2002 2003 2004 2005 2006

Textiles 50-63 China 990 939 2591 2161 1743 2679 2028

Metals 71-83 China 35233 7389 11482 10789 20687 12636 9217

Machinery 84-85 China 667 29 30 6 1 289 2730

Textiles 50-63 Kazakhstan 1053 1154 1572 3125 5087 3427 2205

Metals 71-83 Kazakhstan 243 2294 4187 1101 1654 2384 2423

Machinery 84-85 Kazakhstan 2183 3170 4236 5343 7024 9613 10761

Textiles 50-63 Russia 16660 14982 32762 38341 49086 56507 77379

Metals 71-83 Russia 1643 2007 1820 1582 2751 1973 4962

Machinery 84-85 Russia 10094 8848 8334 12541 13133 7059 11111

Source: COMTRADE.

Revealed Comparative Advantage

19. The Revealed Comparative advantage (RCA) is generally used to assess a country’s export potential. In order to focus attention on other non-traditional products that might be successfully exported, the lowest disaggregated (6-digit) product classification is used to estimate the Kyrgyz RCAs. The RCA index of country i for product j is calculated as:

wt

wj

it

ij

ij

XX

XX

RCA =

where Xij and Xwj are respectively the values of country i’s and World exports of product j, and Xit and Xwt are respectively country i and World total exports. An RCA index higher than one indicates that a country has a strong revealed comparative advantage in the export of the product, an RCA index lower than one indicates a comparative disadvantage in that product, and an RCA index equal to one indicates that the country has neither advantage nor disadvantage in this product.

20. Table 2 presents the ten products with the highest RCA. It also presents the Kyrgyz share of the trading partners’ imports in these products, and the Kyrgyz export share of these products in the country’s total export. The low import share of Kyrgyzstan

11

in these trading partners’ imports and the low export share of these products in Kyrgyzstan total export indicate a strong export potential of these products in these markets.

Table 2: Kyrgyzstan top ten products with a strong RCA in 2005

HS code Products description Partners Import

share

Export

share RCA

071130 Capers (edible vegetables) Turkey 14% 0.10% 428

252921 Calcium product Russia 5% 0.09% 73

510129 Wool product India 1% 0.13% 145

510220 Coarse animal hair China 1% 0.01% 80

510330 Waste of coarse animal hair China 3% 0.00% 163

China 1%

Russia 15% 520100 Cotton product

Turkey 4%

6.60% 82

620413 Women's garments of synthetic fibers Germany 11% 0.79% 184

620690 Women's garments of other textile materials Germany 6% 0.66% 74

700529 Glass product China 14% 3.14% 119

853922 Electric filament USA 4% 2.09% 164

Source: Author’s calculation based on COMTRADE data

21. To tap in these export potentials, Kyrgyz firms need to have an efficient production technology, some high-productivity factors, efficient costs, good information on the targeted export markets, and a simplified access to credit. In other word, the economic environment needs to be business friendly.

c) Kyrgyzstan business environment

22. In 2006, the Kyrgyz government has revised tax rates and coverage to make the tax system more investor and business friendly, while increasing the efficiency of tax collection. Both income and profit tax rates fell from 20% to 10%. Farmers are no longer obliged to pay VAT, and the revenue threshold for business being subject to VAT increased from 500,000 soms (US$ 12,500) to 2,500,000 soms (US$ 62,500). However, despite these positive changes the business environment is still perceived to be unfavorable by the business community. The new tax code draft is still under discussion.

The 2006 Global competitiveness report on Kyrgyzstan

12

23. The Global Competitiveness Report (GCR) published annually by the World Economic Forum (WEF) since 1996 aims to evaluate the economic competitiveness of a large sample of countries including Kyrgyzstan. The main indicator (the Global Competitiveness Indicator) is calculated by collecting national business executives’ opinion and official statistics on 9 factors: institutions, infrastructure, macro-economy, health and primary education, higher education and training, market efficiency, technological readiness, business sophistication and innovation. In 2006, Kyrgyzstan ranked 107 out of 125.

24. Figure 5 reports the factors hindering business in Kyrgyzstan according to the business executives interviewed. The five most problematic factors appear to be, in order of severance: corruption, policy instability, tax regulation, tax rates, and government instability. In other word, the business community is pointing to corruption, tax system and political instability as the three main factors hindering business expansion in the country. The limited access to financing comes just after.

Figure 5: Most problematic factors for doing business in Kyrgyzstan

% of responses

0 5 10 15 20

Restrictive labor regulations

Foreign currency regulations

Poor work ethic in national labor force

Inflation

Inadequate supply o f infrastructure

Inadequately educated workforce

Inefficient government bureaucracy

Crime and theft

Access to financing

Government instability/coups

Tax rates

Tax regulations

Policy instability

Corruption

Source: GCR 2006-2007

The 2006 Doing Business report on Kyrgyzstan

25. The IFC/World Bank Doing Business database provides measures of business regulations and their enforcement in 175 countries. The information collected cover the

13

ease of starting a business, dealing with licenses, employing workers, registering property, getting credit, prospecting investors, paying taxes, trading across borders, enforcing contracts and closing a business. In 2006, Kyrgyzstan was among the bad performers in trade across borders (ranked 173 out of 175), tax issues (150 out of 175), licensing issues (143 out of 175) and business closure issues (127 out of 175).

26. Concerning the ease of trading across border, the 2006 report identifies 18 documents required for import (against 10 in the region and 6 in the OECD on average), 127 days to get the import (against 37 in the region and 12 in the OECD on average), and 3,000 US$ paid per container (against 1,600 in the region and 880 in the OECD on average). Concerning the ease of paying taxes, the report identified 89 different tax payments (against 50 in the region and 15 in the OECD on average), and a total tax rate amounting to 67% of profit (against 56 in the region and 47 in the OECD on average). Concerning the ease of dealing with licenses, the report identified 20 procedures required (against 21 in the region and 14 in the OECD on average), 218 days to complete all these procedures (against 243 in the region and 150 in the OECD on average), and costing 510% of the country’s income per capita (against 565 in the region and 72 in the OECD on average). Despite its overall bad ranking on this factor, Kyrgyzstan is performing better than the other Central Asian countries. Finally concerning the ease of closing a business, the report estimated at 4 years the time necessary to deal with a bankruptcy (against 3.5 in the region and 1.5 in the OECD on average), and costing 14.5% of the company’s estate (14.3 in the region and 7 in the OECD on average).

The 2005 BEEPS results for Kyrgyzstan

27. The 2005 BEEPS survey provides information on 202 Kyrgyz firms selected through a random process and surveyed anonymously. The survey addresses the following issues: bureaucracy, corruption, courts, crime, finance, informality, infrastructure, innovation, jobs, tax and trade. Table 3 presents a set of variables characterizing the most the Kyrgyz business environment. For the sake of comparison, two comparators (Georgia and Tajikistan) and the 2002 results for Kyrgyzstan are also included.

28. Echoing the Global Competitiveness Report result that identified corruption as the most problematic factor for doing business, 66% of the firms interviewed in the BEEPS survey report to be obliged to pay bribes to get things done, a level that is worse than in 2002 (59%). A larger percent of firms are paying bribes when dealing with tax inspectors (85%). The situation in Tajikistan, although to a lesser extent, is also worse compared to Georgia. This corruption context is associated with a quite significant informality: in 2005, 13% of sales amount were not reported to the tax administration compared to 7% in Tajikistan and 10% in Georgia. The situation was worse in 2002 (26% of sales amount not reported). The causality between illegal payment to tax inspectors and firms’ under-declaration of their sales can go in both directions, the overall impact being a less attractive and less transparent business environment.

14

29. Also echoing the Global Competitiveness Report result identifying limited access to financing as a major obstacle to business, 83% of the investments of the firms interviewed were financed by their own resources in 2005, while this figure was 72% in 2002. This low financing from banks is probably due to the high collateral needed to obtain a loan (almost twice the loan amount). The situation is the same in Georgia and Tajikistan.

30. With regard to infrastructure, the performance of Kyrgyzstan on electricity, water and telephone services has improved with a more than half reduction in the number of days of supply failures over the period 2002-2005. In addition, the number of firms using Web interaction with their clients/suppliers increased from 29% to 43%. On the other hand, the delay in obtaining a mainline telephone connection increased from 11 to 13 days.

Table 3: Summary of the 2005 enterprises survey results

Georgia Tajikistan Kyrgyz

Republic

2005 2005 2002 2005

Pays Bribes to get things done (% firms) 11.11 45.73 58.78 66.33

Firms expected to give gifts in meetings with tax inspectors (%) 35.71 67.51 75.76 84.97

Sales amount reported by a typical firm for tax purposes (%) 89.94 92.45 73.85 86.7

Internal finance for investment (%) 63.36 88.87 72.08 82.73

Bank finance for investment (%) 24.59 0.78 5.34 8.81

Informal finance for investment (%) 2.4 5.83 8.6 4.06

Value of collateral needed for a loan (% of the loan amount) 188.51 180.91 106 180.55

Loans requiring collateral (%) 93.59 76.74 75.56 89.89

Number of electrical outages (days) 39.01 32.06 21.34 9.6

Number of water supply failures (days) 3.26 5.71 4.44 2.41

Delay in obtaining a mainline telephone connection (days) 16 8.96 10.9 12.92

Unavailable telephone service (days) 1.9 2.35 4.8 1.23

Firms using the Web in interaction with clients/suppliers (%) 44 24 28.9 43.07

Average time to clear direct exports through customs (days) 3.43 4.75 2.36 4.13

Longest time to clear direct exports through customs (days) 4.97 10.08 4.87 7.92

Average time to claim imports from customs (days) 2.77 4.62 2.63 4.35

Longest time to claim imports from customs (days) 3.78 8.18 81.96 10.15

Domestic sales (% sales) 92.23 92.05 93.38 90.57

Sales exported directly (% sales) 7.68 7.7 5.83 8.63

Sales exported indirectly (% sales) 0.1 0.25 0.78 0.8

Domestic inputs (% inputs) 68.67 80.4 68.29 58.64

Inputs imported directly (% inputs) 22.35 14.1 16.78 25.31

Inputs imported indirectly (% inputs) 8.97 5.5 14.93 16.05

Source: EBRD-World Bank 2005 BEEPS.

15

31. Concerning trade issues, the average time to clear direct exports and imports through customs increased by 75% and 65% respectively, a result that is in line with the Doing Business bad ranking (173 out of 175) of the country’s ease of trading across borders. This result should be put in perspective with the large share of firms’ domestic sales (90%) compared to 9% of direct exports and 1% of indirect exports on the one hand, and the more than 40% of imported inputs (directly and indirectly).

3) Key Impediments to export expansion in Kyrgyzstan

32. In 1993, the World Bank country study on Kyrgyzstan was mentioning that “Kyrgyzstan transport sector is relatively developed and potentially able to serve the needs of the economy adequately. The infrastructure appears to be of sound quality and equipment is available in sufficient quality. A major challenge of the coming years will be to ensure that these assets are properly maintained and efficiently operated” 5. Unfortunately, the country failed to deal with this challenge, and the quality of the inherited infrastructure from the Soviet Union deteriorated over time (World Bank 2006)6. In addition to the poor quality of transport infrastructure, many technical, administrative and operational procedures are impeding Kyrgyz firms to expand and be able to conquer foreign markets.

a) Infrastructure quality and Transport flows

33. Given the landlocked and mountainous landscape of the country, the quality of the transportation infrastructure is a key success factor for increasing the accessibility of the country to world markets. However, given the government’s budget constraints, the maintenance and reconstruction of the stock of infrastructure need to be prioritized in accordance with actual transport flows and modal split.

Transport flows and modal split

34. The 2003 Trade Audit of Kyrgyzstan reported a modal split of export cargos of about 87% for road and 13% for railways, while about 78% of the imports were shipped by rail and the rest by road. An estimated 650 trucks transited Kyrgyzstan in 2001. Transport by road was much faster than by rail, with 10 to 15 days by road to Germany, where the train trip may have taken 3 weeks for instance. For specific commodities, air transport was preferred, at a transport cost of about $2,5 per kilo.

5 World Bank (1993), “Kyrgyzstan - The transition to a market economy”. 6 World Bank (2006), “Infrastructure in Europe and Central Asia Region: Approaches to Sustainable Services”.

16

35. The current picture is further in favor of road transport. In 2005, the share of road transport in freight traffic was about 93%, while the share of rail transport was only 6%, and the share of air transport in freight traffic was less than 1%. Railway mostly transports low-cost bulk cargoes (cement, coal, construction materials, etc.). In most of the cases, the road transport is the only transport means ensuring communication between different regions, since the railway network consists of two parallel branches crossing the southern and the northern part of the country to connect with the trans-Asia rail network in Uzbekistan (Dzhikak) and Kazakhstan (Dzambyl).

36. Transport services other than road are heavily regulated by the state: the inter-city road transport services are largely privatized, while the national air carrier and railways are state-owned and only limited restructuring has taken place. According to ministry of transport technical services, almost all the trucks are now private, the government task being to regulate the transport process through three services: (1) the international freight forwarding department, (2) the transport inspection, and (3) the inspection on load pressure. This latter service was implemented six months ago to collect earmarked fund for road maintenance and rehabilitation through an overload tax. Currently, more than two thousands trucks are involved in international freight forwarding towards Kazakhstan, China, Russia and the EU.

Roads

37. According to the WTO recent Trade Policy Review on Kyrgyzstan, the total road network is 34,000 kilometers, and consists of an inter-city network of about 10,000 kilometers (4,000 kilometers of national roads, the rest being regional roads).7 About 40% of the total network is paved, and 60% requires urgent repair; while only 20% of roads are in good condition. Not all of these roads are suitable for heavy trucks, and the poor condition of major roads adds substantially to road transportation costs. A Road Fund was formed in 1998, but it has had a limited impact since only 200 to 250 million Soms are collected per year (WTO 2006). This amount is reported to be about 15 to 20 percent of the amount necessary to maintain roads in good condition. About 200 kilometers of hard surface roads are lost each year (or 1,000 kilometers over the past five years) due to inadequate funding for maintenance.

38. According to the ADB Private Sector Assessment (PSA), the country’s main transport corridors comprise 2,231 kilometers and 6 routes, of which the main arteries include routes from Bishkek to Osh, to Georgievka, to Chaldovar and to Naryn and onwards to Torugat.8 The condition of these corridors is generally poor and results in high freight transport costs that constitute a high percentage of production and marketing costs which undermine the competitiveness of Kyrgyz enterprises (ADB 2007).

7 World Trade Organization (2006). Trade Policy Review, report prepared by the WTO Trade Policy Review Body. 8 Cyril Lin (2007), “Private Sector Development in the Kyrgyz Republic: Issues and Options”. Report prepared for the ADB.

17

39. Road construction activities are mostly supported by foreign investments. The majority of investments into road development were focused on the reconstruction of the Bishkek-Osh road. Total amount of credits provided by the ADB and the Government of Japan for reconstruction of this road is USD 220.8 million. This is a strategic road, as it links the northern and the southern parts of the country. In addition to the Bishkek-Osh road, there have also been smaller road rehabilitation projects. For instance, the World Bank provided nearly USD 20 million for rehabilitation and maintenance of urban roads.

Railways

40. The Kyrgyz railway network is relatively small, totaling 428 kilometers, of which 320 are of single track. There is no railway communication between the Northern and the Southern regions of the country. Condition of railroads is satisfactory because of small load, yet crossties at some section of the railroad are in poor condition.

41. The Kyrgyz Temir Jolu Company remains the state monopoly and provides the whole scope of railway services. The State Department for Mainline Railway Design and Construction is another monopolist in the railway sector, which is exclusively in charge of the design and construction of mainline railways, as well as establishment, maintenance, development and operation of social infrastructure in construction areas.

42. A recent freight forwarders survey conducted on the behalf of the World Bank to assess the performance of the rail sector in Kyrgyzstan reveals that this monopolistic structure is increasing the time necessary to ship cargos. Indeed, most of the delays in the shipping process are due to the time it takes to be allocated a railcar (60% of the interviewees reported more than one day) and to get it to the trunk-railway (60% of the interviewees reported more than five hours). In addition to this reliability issue, the survey points to the following rail-traffic related problems: corruption and complex customs procedures, high tariff for poor services, obsolete and insufficient rolling stock, lack of logistics centers, and lack of competition.

Airports

43. The Manas International Airport Company (owned at 87.5% by the State) operates the country's three international airports at Bishkek (Manas), Osh, and Issyk-kul. There are in total 24 airports all over the country, including at Karakol, Naryn, Karavan, Jalalabad, and Batken (owned by Batken State Administration).

44. The country initiated reforms in commercial aviation in 1994, when a 20-year program of gradual reconstruction of Manas airport was prepared. Total cost of the project was USD 150 million, of which USD 60 million had to be reinvested during the first phase by focusing on urgent engineering, construction, design and architectural works and modernization of obsolete equipment. According to a recent study of the Center for Social and Economic Research (CASE), the implementation of the first phase

18

started in 1996, upon receipt of a loan in amount of YEN 5.454 million from the Japanese Fund for International Economic Cooperation9. The project was completed in 2000.

45. According to the concept of commercial aviation development approved in 2002, the government intends to proceed with privatization of the sector and promote establishment of sources of finance for airlines through sale of its shares on a competitive investment basis. The state also intends to elaborate and implement concession arrangements for construction and reconstruction of capital-intensive infrastructure of commercial aviation. Special emphasis is expected to be placed on airports, some of which must be closed, while the rest must be privatized (CASE 2007).

b) Technical and administrative barriers to trade

46. According to the WTO, there has been substantial liberalization of the Kyrgyz Republic's trade regime during its economic transition. Tariffs have been reduced and many formal non-tariff barriers eliminated. Import bans and licensing are mainly to protect human health and safety, national security, and the environment, under international conventions. Licensing has been reduced substantially, and is generally automatic when imposed for other reasons, such as on imports of precious metals and stones, and alcoholic beverages. Import quotas, applied only to alcoholic drinks, appear largely non-restrictive. However, because of the pervasive corruption practices in the country, any legal, technical or administrative procedure initially established for the sake of public safety or minimal regulation turns out be an informal source of revenue for many civil servants. A recent GTZ survey estimate at 80% the share of civil servants involved in corruption practices.

Technical procedures

47. The Trade Audit mission interacted with the National Institute for Standards and Metrology (NISM) to better understand its mandate in the trade process and check its efficiency. The institute, also named “Kyrgyzstandard”, is an official body assigned to the State inspectorate for standardization and metrology, and has the following goals:

• Create and develop national standardization system in compliance with the international rules and recommendations;

• Carry-out works in the field of metrology for measurement assurance;

• Develop and maintain national measurement standards base;

• Maintain national information fund (Corpus) of technical regulations and standards.

9 Center for Social and Economic Research (CASE) (2007), “WTO Accession and Services Trade Reforms: the Case of Kyrgyzstan”, Report prepared on the behalf of the World Bank Institute.

19

It hosts a website presenting all the standards available and accessible to entrepreneurs10. 80% of the standards are developed locally, 60% of the new ones being harmonized with international standards. They currently have 20,000 German standards. The official cost of compliance or certification process is not expensive, but many private operators interviewed experienced or are experiencing harassment for informal payments in their interaction with some Kyrgystandard staff.

48. The main obstacle reported by Kyrgystandard is the translation of foreign standards. For instance, the translation of a standard through the Russia ISO bureau costs 200$, and the budget necessary for this translation is not provided by the State budget. These financial constraints impede them to be proactive with the private sector to identify their needs and look for or design competitive standards. Their experience is that the business community seems not interested in contributing financially to the development of new standards. However, they have had a successful experience with some local soft drink producers who are now exporting their standardized products to China.

49. The Trade Audit mission also interacted with the Department of Plant Protection and Quarantine and the Department of State Veterinary to better understand their mandate in the trade process and check for their efficiency. They are involved in the deliverance of SPS certificates for exports and quarantine permission for imports. The legal cost of the operation is not a burden, but private operators complain about informal payments.

50. The main problem reported by these Departments is the tensions with customs services impeding the SPS, veterinary and epidemiology services at Border crossing points. When the mission met with the Customs services to double check the issue of their collaboration with these control services at border crossing point, they justify their refusal for a combined control service at the border by the inadequacy of the infrastructures at these border crossing points. This seems to be a significant problem and the government needs to properly address it in collaboration with all the donors involved in the country.

Customs procedures

51. Since January 1, 2005, the new Customs Code was enacted in the Kyrgyz Republic. The new provisions on application of modern customs procedures, such as independent assessment, selection, post-entry control (inspection after release of goods), and provisions streamlining the customs formalities and control of goods and vehicles movement through the customs border of the Kyrgyz Republic were laid down. It also introduced important changes to clarify operations of customs brokers and other intermediaries. According to the WTO Trade Policy Review, since the introduction of the new Customs code, the Government has made significant progress in reducing deficiencies in customs administration and customs revenue grew from 0.5% of GDP in 2004 to 1.7% of GDP in 2005.

10 www.nism.gov.kg

20

52 The new customs Code of the Kyrgyz Republic was drafted in compliance with the International Convention on the Simplification and Harmonization of Customs Procedures (revised Kyoto convention). It provides for introduction of information systems and information technologies. The work to introduce the automated system on collection of statistical data on cargo customs declaration, customs receipts, check up and registration of documents for issuance of license for the customs bodies is in progress.

53. However, a typical custom clearance operation requires in addition to the Customs declaration form a series of documents authorizing the good to cross the border, confirming the Customs value of good, describing the type of shipment of the good, confirming the origin of the good, verifying payments between the participants of the transaction, verifying the payment of Customs duties, and a document accompanying goods subject to non-tariff regulation. The Customs body requires this information through one of the documents described in Appendix 1. Collecting all these documents is an additional administrative burden for entrepreneurs, particularly given the pervasive practice of corruption in the country.

Administrative barriers

54. In their day-to-day operation, firms are required to comply with a set of inspection, licensing and certification operations. Some of these operations are technical procedures as described above, some are linked to Customs procedure, and some are purely administrative. A study conducted on the behalf of the World Bank in 2002 highlighted the fact that several decrees, laws and regulations and codes form the principal source of administrative barriers11. The main inspection bodies are the Sanitary-Epidemiological Service, the Veterinary Inspectorate, the Tax Inspectorate, Kyrgyzstandard, and Traffic Police. We can add to these services the Chamber of Commerce and Industry in charge of delivering the Certificates of Origin. In most instances, laws and regulations governing these agencies are broadly written or allow for liberal interpretation by the implementing agencies, hence increasing the sources of bribes extortion.

55. A recent report on import and export procedures prepared on the behalf of the GTZ highlighted the necessity of reducing administrative procedures to improve Kyrgyz firms’ competitiveness12. Indeed, a thorough discussion with Kyrgyz traders help to identify the whole set of administrative documents required for importing or exporting a good. Appendices 2 and 3 report them: 18 documents are needed to export a good, 17 to import a good, all of them involving a large set of public or assimilated agencies.

56. Some international organizations concerned about trade facilitation have initiated the concept of Single Windows, which is defined as “a system allowing traders to lodge information with a single body to fulfill all import or export-related regulatory

11 Global Development Solutions LLC (2002), “Barriers to Competitiveness: An Analysis of Principal Factors Inhibiting the Competitiveness of Kyrgyz Industry”, report prepared for the World Bank. 12 Tapio Naula (2007), “Study on Simplification of Export and Import Procedures in the Republic of Kyrgyzstan”, report prepared on the behalf of the GTZ.

21

requirements”13. This Single Window is managed by only one agency, which informs the appropriate agencies, and/or directs combined controls. Actually, a working group comprising senior representatives from Kyrgyz customs services, relevant ministries representatives, shippers, customs brokers, producers and a GTZ representative has been initiated to discuss all the administrative barriers faced by Kyrgyz firms involved in international trade and propose a reduced set of documents collecting all the relevant information in accordance with the Single Window concept.

c) Other impediments to trade expansion

57. The Trade Audit mission met with some private sector operators to have their viewpoint on the main impediments to business expansion in the country. They mentioned the huge and costly administrative burden to be dealt with by formal enterprises, the difficulty to access finance, and the new tax code considered to be too complex and favoring informal payment extortions by civil servants. This is in line with the diagnosis of the Kyrgyz business environment mentioning the tax system and the access to finance as two key impediments to business expansion. A value chain analysis on some firms operating in specific sectors can also highlight other limiting factors pertaining to internal constraints faced by exporting firms such as the cost of getting relevant information on the targeted foreign market demand trends and quality requirements.

Tax issues

58. According to the latest ADB PSA, the current Kyrgyz tax code imposes a high burden on the business community. Because of the low collection rate of other type of tax, VAT is the most important source to extort bribes. In addition, the level of social fund contribution is perceived by the business community as punitive, leading many enterprises to pay 30 to 90% of their employees’ earnings outside the reported payroll to avoid paying a too large amount of social contribution.

59. The new Tax Code has been challenged by some key business associations who proposed to the Government and the Parliament an alternative Tax Code. This alternative Tax Code contains five concepts on tax administration that are: the maximum inclusion of anti-corruption safeguards; the balance of interests, rights and obligations between taxpayers and the state; the presumption of honesty as the legal basis for formation of all norms in tax legislation; the simplicity and transparency in tax enforcement and administration; and the liberalisation of tax enforcement with regards to honest tax payers and ensuring punishments for tax violations and crime. Four other concepts were proposed for the tax system itself: competitiveness of the tax system and a decrease in the

13 Among these are the United Nations Economic Commission for Europe (UNECE) and its Centre for Trade Facilitation and Electronic Business (UN/CEFACT), World Customs Organization (WCO), SITPRO Limited of the United Kingdom and the Association of Southeast Asian Nations (ASEAN).

22

tax burden that could be underwritten by an increase in the tax collection rate and the legalisation of shadow economic activities; equitable tax burden across sectors and categories of taxpayers; stimulation of priority sectors; and tax legislation oriented towards social development. Until now, only few of these propositions had been agreed with the government (6 out of 50 detailed “conceptual points” by late August 2006), but the discussions are ongoing.

Finance issues

60. Another constraint faced by Kyrgyz firms is the accessibility to financing. According to the ADB PSA, Kyrgyz banks are both reluctant and unable to extend credits for two main reasons. Firstly, their intermediation capability is limited by a low level of deposits due to the lack of confidence of the population in the banking system. Second, the large share of the business community operating in the shadow economy (estimated at 53% by a recent UNDP study) is reluctant to operate in the formal sector which would make them liable to a high tax burden and an excessive regulatory regime.

61. The entry of foreign banks in the Kyrgyz market has widened slightly banks’ product base, but the range of products is still very narrowly limited to short-term working capital and trade financing loans and investment financing. Banks have made progress in diversifying away from collateral-based loans to those geared to the borrower’s capacity to generate cash flow, but the majority of loans are still collateral-based with a flawed, bureaucratic and costly pledge system undermining the lending process.

Diagnosis of the textile sector

62. According to the 2005 CEM, the Kyrgyz market produces about 100,000 ton of cotton through a range of private and state owned cotton farms that average in size from as little as 0.5 hectare family farms to 20 hectare farms. It is estimated that there are 14 cotton private processing facilities in the country with an installed capacity of over 337,000 tons, but this does not account for the growing number of small/micro processing units that have emerged in the past several years.14 The market is segmented into 4 areas, including cotton farming; ginning; yarn/fabric manufacturing; and finished goods manufacturing. This value chain analysis focuses on the finished good segment. It is estimated that approximately 70 enterprises of varying size and capacity are operating in the Kyrgyz textile market. Of this total, 6 enterprises are involved in ready-made garments. These 6 enterprises produce 10 percent of total industry output, with the remaining 90 percent produced by small-scale enterprises. This picture suggests a highly disaggregated textile industry.

14 Some estimates suggest that accounting for small and medium (but not micro ginneries) there are at least 30 ginneries in operation today.

23

63. Indeed, the Kyrgyz textile sector comprises some few big textile business groups, some medium producers generally formed by 3 to 5 partners, and a large number of small producers. The big textile groups are generally involved in import/re-export activities, finance, distribution networks, and fashion, and are not facing significant problems in their daily operations. It is estimated that about 200-300 medium size groups are currently operating in the textile sector, compared to 1200-1500 small producers. Medium groups not based on relatives’ connections generally face internal problems related to profit sharing, which threatens their sustainability. Small producers are generally household enterprises, with the production site located in the family’s house.

Box 1: Characteristics of the medium and small textile groups

Medium textile group characteristics: Number of production workers: 50 -80 persons Average turnover: 100-120 thousand USD/month Production site: 350-500 m2

Warehouse: 120-150 m2

Equipment: 60-80 thousand USD Sales agents: 10-15 branches Transport: 2-3 medium size vehicles for supply materials and move ready goods. Usually has own designer, and sales representative in Russia. Small textile group characteristics: Number of production workers: 5 -15 persons Average turnover: 5-10 thousand USD/month Production site: 30-100 m2

Warehouse: no Equipment: 4-10 thousand USD Sales agents: 10-15 branches Transport: 1 vehicle or rent transport services. Usually has 1-2 specialists for design (usually owner), with no sales representatives.

64. Small firms base their strategy on cutting costs and copying fashion products. The small production scale operated in a household enterprise requires very little initial capital to start and make easier to cut costs. Such market structure favors flexibility to adapt to business fluctuations, but it does not generate any scales economies. In addition to the fierce competition among small and medium producers, they have to rely on powerful freight forwarding companies, well-aware of the formal and informal Customs and Transit systems, to transport their products in the targeted markets, which further erodes their profitability. Interviews with some private sector operators revealed that many small textile producers sell their production to some freight forwarders companies via a company officially registered as operating in the light industry sector. The products are then re-labeled by this “intermediary” firm so as to reduce their official value (and

24

thus their Customs values) and transported to Russian and Kazakh markets and sold at very profitable rates.

Figure 6: Strategy of small producers

MAIN FACTORS

MAIN FACTORS

Russian consumers

Cost Cutting StrategyCost Cutting Strategy

Copy design and simple models

Copy design and simple models

Supply by local marketSupply by local market

S m a l l

p ro d u c e rs

S m a l l

p ro d u c e rs

Sales by own network at

local markets

Sales by own network at

local markets

Sales to Trader, or orders from Bigger producers

Sales to Trader, or orders from Bigger producers

Small traders from Kazakhstan

Small traders from Kazakhstan

High CompetitionHigh Competition

Russian wholesale marketRussian wholesale market

Kazakh consumers

Local consumers

Simple technology Simple technology

65. The sector is currently taking advantage of a tax incentive provided by the Kyrgyz Government at the end of 2005 according to which textile production sites could pay tax based on the patent system, which is a small fixed monthly based payment per worker (about 10 $). That Decision entered into force in spring 2006 and led to an impressive activation of the sector. Most of the textile producers started legalizing their hidden production sites, but not their warehouses and logistics infrastructures since this would bring them under the normal Tax Code. In fact, only 20 to 30 Kyrgyz enterprises operate fully officially, most of them originating from old factories from the FSU, the other producers preferring operating in the shadow economy. 66. To better understand the constraints faced by these firms operating in the shadow economy, we conducted a value chain analysis of a typical product of an SME located in Bishkek and operating in the textile sector. It started trade activities in the mid-nineties, and after accumulating enough capital, it started a production site at the end of the nineties. During 1999-2003, the group slowly grows and changed location two times to bigger production sites. The group’s production was stable over these last two years. Its production site is rented monthly at about 2,500 USD. Its capital is estimated at 350-400

25

thousands USD. The machinery investment at the beginning was estimated at 20 thousand USD, with a 25% annual depreciation rate. The current existing equipment complex is estimated at 100 thousand USD. The group fulfills its finance need by soliciting some of its Russian clients, or some of its local suppliers in fabrics (delayed payment of inputs).

67. The production of a women suit (typical production) incurs the following costs:

Table 4: Unit production cost

Cost distribution per 1 female suit USD Fabric 5.5 Additional raw materials 0.4 Labor 1 Energy 0.1 Other production cost 0.5 Administrative and other cost, incl. tax 0.5 Total production cost 8 Factory price 12 Gross Profit 4

Source: Interview with the firm’s manager

This cost structure indicates that raw materials account for the lion’s hare of production costs, followed by labor costs and then administrative and other production costs.

68. The cost of getting relevant information for the export process is included in the administrative costs, but it is estimated to 5 to 6 thousands USD a year, including business trips and workshops for designers. The Group doesn’t use a Bank credits, but uses two types of co-financing due to seasonal shortage of capital: suppliers of fabric (delay payment up to 2 months) and investment from regular Russian buyers. The first case does not induce additional costs, while the second case incurs an interest rate of 8-9 % per annum. These co-financing schemes are used 2 to 3 times a year, and up to 100-150 thousand USD, and most often are not registered officially.

69. The production is then transported to Novosibirk in Russia, using the services of freight forwarding company. Only two freight forwarding companies are serving the Siberian part of Russia, with a price of 1.5 USD per kg. Since the average rate of a suit is 0.4kg, this represents 7.5% of the total production cost of the suit, which is quite high (third highest cost component after raw materials and labor).

70. Freight forwarding companies collect the production of 3 to 4 small producers (about 20 thousands suits) and packed them in a standard 20-feet container, and transport them to the targeted market. Usually, a container is transported every 3-4 days, and the travel from Bishkek to Novosibirk takes about seven days. The textile company provides all the necessary documents for transit and export to the freight forwarding company who bears the legal responsibility of transporting the good. The freight forwarders use the TIR system and some informal payments to easily pass through borders and deliver the good in Russia. In Novosibirsk the goods are passed to the textile company’s Representative

26

Agent who reloads them in its own warehouse and distribute them in the city and send some to other representatives in two other Russian cities. Appendix 4 describes the various costs borne by freight forwarding companies.

Figure 7: Export of a textile product to Russia

71. Total expenses on transportation are estimated to add to factory price an additional 11% of the costs. There are also a number of infrastructural investment and marketing expenses, support of representative offices, logistics costs and losses which altogether bring the profit rate to 20%, presumably divided between the Kyrgyz firm and its Russian representatives.

Diagnosis of the dairy sector

72. After the agricultural reform in 1993-94, almost all the cattle were distributed to rural population, leading to a disaggregated dairy sector. Currently 98% of milk production is made by farmers and rural population, with 58% by rural households. Annually Kyrgyz milk sector produces about 1-1,2 million tons of raw milk. Approximately 50-60% is consumed by the population, including 10% to feed the calf. The remaining part is directly sold to markets (internal and external) or to processing units, or self-processed before being sold.

27

73. Geographically Kyrgyz milk production can be divided into three zones: the North including Naryn, Issyk-Kul and Chu Valleys (49% of milk production and 43% of cows); the South including all Fergana Valley Oblasts, that is, Osh, Jalal-Abat and Batken Oblasts (45% of milk production and 51% of cows); and the Talas Oblast (6% of milk production and cows). The North zone is most developed (both in terms of milk production and processing), with an important export of milk and milk products to Kazakh markets. The South zone mainly produces milk for self-consumption and self-processing, but some of the processed dairy products are shipped to Bishkek. There is also a hidden export activity by private border traders to Uzbek and Tajik markets. The Talas zone is isolated because of the lack of a good road infrastructure linking it to the rest of the country. However, there is an active milk trade with the South-Kazakh sub-market, including Taraz and Shimkent cities.

74. In terms of productivity, the northern zone is ranked top with 2,4 tons per cow a year, followed by the Talas zone (2,2 tons per cow a year), the southern zone lagging behind (1,8 tons per cow a year). However, because of the reproduction cycle of the cows, there is a seasonal fluctuation in the milk production, the summer’s production being higher than the winter’s one. This fluctuation induces a price fluctuation as well: for instance, this winter, the purchasing price was 290 USD per 1 ton of milk, while at the end of May it was down to 197 USD per 1 ton of milk. Furthermore, the current Kazakh agricultural policy of boosting local production through easy access to finance is harming the Kyrgyz agro-business, but this negative impact is counterbalanced by the increased purchasing power both in Kazakhstan (oil boom) and Kyrgyzstan (remittance boom).

Figure 8: Structure of the Kyrgyz dairy sector

28

75. The Kyrgyz dairy sector involves a number of intermediate agents from farmers

oduction, and 20% is used for

sis of the milk produced by a dairy company

res land from the local population. Currently

the big milk factory JSC “Bishkeksut”, but

and households to milk processing factories, as depicted in Figure 8. An important role is also played by milk collection and transportation agents. There are two types of milk agents: factory agents (hired by a factory and provided with milk truck), and individual agents. They are trained to check the quality of the milk.

76. Feeding cows requires about 10-15% of milk prauto-consumption. The share of self-processed milk is region-specific. In the South and remote mountain areas (like Naryn oblast) up to 60% of milk is processed by families and sold locally due to the small regional market and absence of the processing capacities, while the self-processed milk doesn’t exceed 10% in the North. Milk processing is dominated by several medium and large enterprises, principally, JSC Bishkek Sut, an affiliate of Wimm Bill Dan which is the biggest milk and juice products Company in CIS countries. In the Chu Valley also operates such producers as Shin Line (milk, condensed milk, and ice creams), El West (milk, butter, cheese, and yoghurts), Ak-Sut (dry milk, butter, and cheese), Dairy Springs (cheese), Elimai (milk, butter, dry milk). There is also a Kazakh company Food Master, the main competitor of JSC “Bishkek Sut” in the Kazakh market, which opened many milk collecting points in the Chu Valley, and also collaborate with some Kyrgyz firms such as Gradient since 2004. These companies process 85-88 percent of milk, which comes onto the market and the remaining share is processed through small local companies.

77. We conducted a value chain analylocated in the Chu valley, the JSC “Mashinoispytatelnaya Stantsia (MIS in short) which is the biggest milk production site in Kyrgyzstan. It is a collective farm of the Soviet type that was created in 1961 for milk production, breeding of the cows and also agro-processing. In 1998 it was privatized and became a cooperative, and then it was restructured again in 2006 as a Joint Stock Company. Currently it has 870 staff, 200 working with cattle and about 600 working in plant production, the remaining being administrative and service department staff.

78. The Company is renting a 4500 hectait has 2500 heads of cattle, including 1100 milking cows. The average milk production per cow is 5,5 tons a year, and the annual production of milk is about 6 thousands tons of milk, while the annual turnover of the milk production is around 50 million soms (approximately 1,3 million USD). The daily production varies from 10 tons a day (winter time) to up to 20 tons a day (summer time).

79. The company’s main trade partner isthis collaboration was interrupted in 2005-2006 when MIS decided to directly sell its milk production to the Kazakh Company Food Master which was proposing higher prices. The collaboration with Food Master was organized as follows: MIS collected milk and provided temperature control, transported the milk to border (about 10 km), provided Customs clearance at the Kyrgyz Customs service; and then the custody of the milk was transferred to Food Master to provide Customs clearance at the Kazakh Customs service, and transported to a factory near Almaty for processing. The purchasing price was 15% higher than local price. However, because of the lack of MIS to properly handle Customs procedures and the harassment for informal payments, the collaboration stopped.

29

80. A previous value chain analysis (CEM 2005) of small Kyrgyz farmers indicated that well over half (59 percent) of the cost of producing a liter of milk was associated

since Soviet time was

ms to improve the acroeconomic and business environments of the country. A new Customs Code and a

rnment to reduce barriers to trade

O, Kyrgyzstan became a party to the WTO Technical arriers to Trade (TBT) and Sanitary and Phytosanitary (SPS) Agreements, thus,

i

with collection and delivery of milk to a processor. A further breakdown of the value chain for collection and delivery indicates that fuel (52.1 percent) and administrative costs (41.1 percent) constitute a dominating factor in the value chain. Appendix 5 describes the formal and informal payments involved in the export process of the MIS Company. The key barriers faced by MIS seem to be the informal payment to the Customs and Chamber of Commerce, as well as the traffic police.

81. The fat content of milk is another source of conflict between producers of milk and milk processing factories. The standard fat content of milk 3,6%, but the disruption of the FSU altered the feeding base and the average fat content of the milk dropped to 3.2% at summer time and 2.9% at winter time. In 2003-2004, milk producers through the Ministry of Agriculture tried to lobby down the standard fat content but they faced a strong opposition from milk processing factories.

4) Ongoing governmental initiatives and policy recommendations

82. The Kyrgyz Government is currently undertaking many reformLaw on Investments in accordance with the WTO agreements has been adopted. The Law on Technical Regulation has been adopted, and the drafting of a new Tax Code and a Law on Licensing are also underway. In addition to these legislative reforms, two ongoing initiatives directly related to trade barriers issues are dealing with technical and administrative regulation issues.

a) Ongoing initiatives of the gove

Technical regulation initiatives

83. By acceding to the WTBcomm tting to create a technical regulation system in full compliance with international rules, norms and standards. To successfully reform the technical regulation system, the Government bodies in collaboration with international organizations worked on the creation of a legislative framework. Since December 2004, the Law on the Fundamentals of Technical Regulation in the Kyrgyz Republic is in force. The Law provides for standardization principles under the WTO Technical Barriers to Trade Agreement. The new Law on Veterinary was also developed and adopted in April 2005. The Law was approved by the OIE. The State Veterinary Department under the Ministry of Agriculture, Water Economy and Processing Industry of the Kyrgyz Republic is a contact point for OIE.

30

84. With the support of multilateral and bilateral donors such as the World Bank, the EU, the Swiss Government and USAID, a series of initiatives have been undertaken to

ission to support the Kyrgyz rk plan to

• ection regime which will need

•

market surveillance training.

Admini

improvement of governance, particularly the fight nd reduction of corruption, high on the agenda. It recognizes that the principal constraint

provide assistance in these areas. The Kyrgyz Government has recently signed a technical assistant loan with the World Bank, named Reducing Technical Barriers for Entrepreneurship and Trade (RTBET), which aims at streamlining the national technical regulation and standards framework for business, developing systems to enhance quality and safety of products and increasing enterprise competitiveness in pilot sectors. A project Steering Committee chaired by the first vice Prime Minister has been established, and a protocol of cooperation between the Ministry of Economic Development, Industry and Trade (MEDIT) and the National Institute for Standards and Metrology (NISM) was signed and approved by the Steering Committee. A PIU has been established to pilot the project, and a Project Operational Manual satisfactory to IDA has been developed by the Recipient. An international advisor has been recruited and is currently providing guidance and methodological support in the development of sector-specific Technical Regulations (food safety and transportation), conformity assessment mechanisms, and market surveillance. A local consultant has also been recruited to provide operational and coordination support throughout project implementation.

85. Other donors are also involved in a series of complementary activities:

• SECO/ITC is planning a technical assistance mAccreditation Center, conduct a needs assessment and help design a wofacilitate its eventual International Laboratory Accreditation Cooperation (ILAC) recognition. In addition, ITC is providing customized marketing and export support to selected agro-processing companies which may also be eligible under the RTBET matching grant facility once effective.

USAID/Pragma under its Business Environment Facility will provide technical assistance to improve the business, notably the inspto be adjusted following the adoption of the first sectoral Technical Regulations.

GTZ is planning to provide technical assistance to NISM in the area of metrology and standardization.

• EU-TACIS will provide complementary assistance in Technical Regulation notably in the area of

strative regulation initiatives

86. The Kyrgyz CDS places the aon economic development is corruption. Government ineffectiveness and poor performance in delivering basic social services can only be tackled by undertaking political reform, deregulating the economy, effective public administration, and legal reform. Corruption will be drastically reduced by reducing rent-seeking opportunities and cumbersome regulation, limiting state intervention in market mechanisms, and increasing

31

the accountability and transparency of state agencies through tougher reporting requirements.

87. Given this backdrop, a working group on Administrative Barriers to Trade ri

dertaken to facilitate trade with

) Policy recommendations

9. All these governmental actions are rightly taken to reinforce the institutional ew

tor, which is characterized by a large e