Trade and the Greenhouse Gas Emissions from International Freight ...

57

NBER WORKING PAPER SERIES TRADE AND THE GREENHOUSE GAS EMISSIONS FROM INTERNATIONAL FREIGHT TRANSPORT Anca D. Cristea David Hummels Laura Puzzello Misak G. Avetisyan Working Paper 17117 http://www.nber.org/papers/w17117 NATIONAL BUREAU OF ECONOMIC RESEARCH 1050 Massachusetts Avenue Cambridge, MA 02138 June 2011 We thank the OECD for funding, Ron Steenblik for suggesting and encouraging the work. We also thank Bruce Blonigen, Tim Cason, Lata Gangadharan, Tom Hertel, Pete Minor, Paul Raschky, Christis Tombazos, Terrie Walmsley, and seminar participants at the ASSA meetings 2011, and the International Workshop on Current Issues in CGE Analysis for suggestions and help. The views expressed herein are those of the authors and do not necessarily reflect the views of the National Bureau of Economic Research. NBER working papers are circulated for discussion and comment purposes. They have not been peer- reviewed or been subject to the review by the NBER Board of Directors that accompanies official NBER publications. © 2011 by Anca D. Cristea, David Hummels, Laura Puzzello, and Misak G. Avetisyan. All rights reserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permission provided that full credit, including © notice, is given to the source.

Transcript of Trade and the Greenhouse Gas Emissions from International Freight ...

NBER WORKING PAPER SERIES

TRADE AND THE GREENHOUSE GAS EMISSIONS FROM INTERNATIONALFREIGHT TRANSPORT

Anca D. CristeaDavid HummelsLaura Puzzello

Misak G. Avetisyan

Working Paper 17117http://www.nber.org/papers/w17117

NATIONAL BUREAU OF ECONOMIC RESEARCH1050 Massachusetts Avenue

Cambridge, MA 02138June 2011

We thank the OECD for funding, Ron Steenblik for suggesting and encouraging the work. We alsothank Bruce Blonigen, Tim Cason, Lata Gangadharan, Tom Hertel, Pete Minor, Paul Raschky, ChristisTombazos, Terrie Walmsley, and seminar participants at the ASSA meetings 2011, and the InternationalWorkshop on Current Issues in CGE Analysis for suggestions and help. The views expressed hereinare those of the authors and do not necessarily reflect the views of the National Bureau of EconomicResearch.

NBER working papers are circulated for discussion and comment purposes. They have not been peer-reviewed or been subject to the review by the NBER Board of Directors that accompanies officialNBER publications.

© 2011 by Anca D. Cristea, David Hummels, Laura Puzzello, and Misak G. Avetisyan. All rightsreserved. Short sections of text, not to exceed two paragraphs, may be quoted without explicit permissionprovided that full credit, including © notice, is given to the source.

Trade and the Greenhouse Gas Emissions from International Freight TransportAnca D. Cristea, David Hummels, Laura Puzzello, and Misak G. AvetisyanNBER Working Paper No. 17117June 2011JEL No. F17,F18,Q56

ABSTRACT

We collect extensive data on worldwide trade by transportation mode and use this to provide detailedcomparisons of the greenhouse gas emissions associated with output versus international transportationof traded goods. International transport is responsible for 33 percent of world-wide trade-related emissions,and over 75 percent of emissions for major manufacturing categories like machinery, electronics andtransport equipment. US exports intensively make use of air cargo; as a result two-thirds of its export-relatedemissions are due to international transport, and US exports by themselves generate a third of transportemissions worldwide. Inclusion of transport dramatically changes the ranking of countries by emissionintensity. US production emissions per dollar of exports are 16 percent below the world average, butonce we include transport US emissions per dollar exported are 59 percent above the world average.We use our data to systematically investigate whether trade inclusive of transport can lower emissions.In one-quarter of cases, the difference in output emissions is more than enough to compensate forthe emissions cost of transport. Finally, we examine how likely patterns of trade growth will affectmodal use and emissions. Full liberalization of tariffs and GDP growth concentrated in China andIndia lead to transport emissions growing much faster than the value of trade, due to trade shiftingtoward distant trading partners. Emissions growth from growing GDP dwarfs any growth from tariffliberalization.

Anca D. CristeaUniversity of [email protected]

David HummelsKrannert School of Management403 West State StreetPurdue UniversityWest Lafayette, IN 47907-1310and [email protected]

Laura PuzzelloMonash [email protected]

Misak G. AvetisyanPurdue University425 W State Str, KCTR 237West Lafayette, IN [email protected]

1

TradeandtheGreenhouseGasEmissionsfrom

InternationalFreightTransport

AncaCristea,UniversityofOregonDavidHummels,PurdueUniversityandNBER

LauraPuzzello,MonashUniversityMisakAvetisyan,UniversityofSouthernCalifornia

May2011

Abstract:Wecollectextensivedataonworldwidetradebytransportationmodeandusethistoprovidedetailedcomparisonsofthegreenhousegasemissionsassociatedwithoutputversusinternationaltransportationoftradedgoods.Internationaltransportisresponsiblefor33percentofworld‐widetrade‐relatedemissions,andover75percentofemissionsformajormanufacturingcategorieslikemachinery,electronicsandtransportequipment.USexportsintensivelymakeuseofaircargo;asaresulttwo‐thirdsofitsexport‐relatedemissionsareduetointernationaltransport,andUSexportsbythemselvesgenerateathirdoftransportemissionsworldwide.Inclusionoftransportdramaticallychangestherankingofcountriesbyemissionintensity.USproductionemissionsperdollarofexportsare16percentbelowtheworldaverage,butonceweincludetransportUSemissionsperdollarexportedare59percentabovetheworldaverage.Weuseourdatatosystematicallyinvestigatewhethertradeinclusiveoftransportcanloweremissions.Inone‐quarterofcases,thedifferenceinoutputemissionsismorethanenoughtocompensatefortheemissionscostoftransport.Finally,weexaminehowlikelypatternsoftradegrowthwillaffectmodaluseandemissions.FullliberalizationoftariffsandGDPgrowthconcentratedinChinaandIndialeadtotransportemissionsgrowingmuchfasterthanthevalueoftrade,duetotradeshiftingtowarddistanttradingpartners.EmissionsgrowthfromgrowingGDPdwarfsanygrowthfromtariffliberalization.

JELclassification:Q56;F18.Keywords:Greenhousegasemissions;internationaltransportemissions;worldtradegrowth;internationaltradebytransportmodeAcknowledgements:WethanktheOECDforfunding,RonSteenblikforsuggestingandencouragingthework.WealsothankBruceBlonigen,TimCason,LataGangadharan,TomHertel,PeteMinor,PaulRaschky,ChristisTombazos,TerrieWalmsley,andseminarparticipantsattheASSAmeetings2011,andtheInternationalWorkshoponCurrentIssuesinCGEAnalysisforsuggestionsandhelp.

E‐mailaddresses:[email protected](A.Cristea);[email protected](D.Hummels);[email protected](L.Puzzello);[email protected](M.Avetisyan).

I. Introduction

Internationaltradegeneratesgreenhousegas(GHG)emissionsfromtwosources:theproductionof

tradedgoods,andtheirtransportationbetweentradingpartners.Alargeliteraturehasfocusedon

2

theemissionsassociatedwithproduction,examiningquestionsrelatedtohowtrademayreallocate

productionbetweencountrieswithdifferingemissionintensities,orundermineeffortstocontrol

emissionsvia“carbonleakage”.1However,theemissionsassociatedwithinternational

transportationarelargelyoverlooked,bothinthetextofexistingagreementssuchastheKyoto

Protocolregulations,andindatacollectionefforts.2

EffortstomeasurethecontributionofinternationalfreighttransporttoGHGemissionshave

beenlimitedinscope.Thecasestudybasedlifecycleanalyses(LCA)literaturetypicallyfocuseson

aparticularproductandgeographicmarket,andassessestheenvironmentalimpactofeveryinput

intheproductionanddeliveryofthatproduct.Forexample,Simetal.(2007)estimatethatthe

globalwarmingimpactofKenyanandGuatemalanbeansshippedtotheUKare20‐26timeslarger

thanUKproduction.Incontrast,Williams(2007)findsthatcutrosesairdeliveredfromKenyato

theUKgenerateemissionsthataresignificantlylowerthanrosessourcedfromtheneighboring

Netherlands(Williams,2007).WhileLCAstudiesprovidedetailedcalculationsoftransport

emissionsforaparticularproductandtradeflow,theyarenotinformativefortheworldtrading

systemasawhole.3Moregenerally,welackdatasourcesthatattributeinternationaltransport

emissionstooriginanddestinationcountries.Asaconsequence,thereislittlesystematic

informationregardingthemagnitudeoftransportationemissionsrelativetoproduction,andhow

theyaredistributedacrosstradeflows.

1ExamplesincludeEderingtonandMinier(2003),Babiker(2005),Levinson(2009),LevinsonandTaylor(2008)amongothers.SeealsoCopelandandTaylor(2004)foracomprehensiveliteraturesurvey. 2vanVeen‐GrootandNijkamp(1999)arguethatthekeyresearchfocusinadvancingtheinvestigationontheenvironmentaleffectsofinternationaltradeshouldbeon“buildingupamonitoringsystemanddatabase”tofacilitate“measuringtheenvironmentaleffectsofinternationaltransport”.ForadiscussionofthechallengesinmeasurementandtheomissionofinternationaltransportfrompolicyprotocolsseeOlivierandPeters(1999),MiljøstyrelsenMiljøministeriet(2003)–theDanishEnvironmentalProtectionAgency,DanishMinistryfortheEnvironment,aswellastheTransportationResearchBoard,2009. 3 Afewrecentpapersemployinput‐outputtablestomeasureinternationaltradeemissions,andattempttoincorporateinternationaltransportemissionsintothecalculation(Gretheretal.,2010;PetersandHertwich,2008;Cadarsoetal.,2010).However,dataonthemodesoftransportbywhichgoodstravelisnotreadilyavailableataglobalscale,sothesepaperseitherrestricttheirattentiontoasingleimportingcountryortheybasetheircalculationsonentirelyimputeddata.

3

Howimportantareinternationaltransportemissionsrelativetoemissionsfromtheoutput

oftradedgoods?TheInternationalTransportForum(ITF2010)providesaggregatetransport

emissionsdataforinternationalaviationandmaritimetransportbycombiningdataonfuel

consumptionfromtheInternationalEnergyAgency(IEA2010),alongwithinformationonGHG

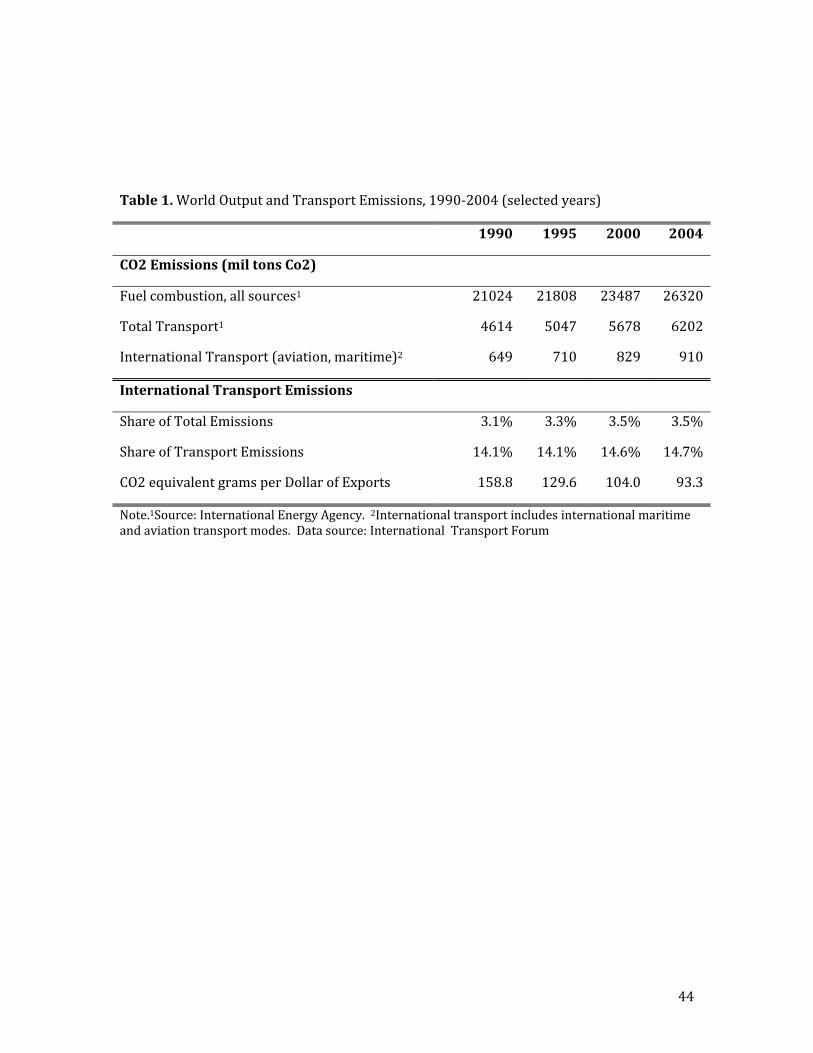

emissionsbyfueltype.Table1providestheITFestimatesalongwithadditionalcalculationsbythe

authors.From1990‐2004,internationaltransportemissionsroseslightlyfasterthantotal

emissionsoremissionsfromalltransport.Focusingon2004,internationalmaritimeplus

internationalaviationtransportationwasresponsibleforjust3.5percentoftotalemissions.This

seemssmall,buttotalemissionsincludemanyactivities(e.g.,residentialenergyusage,domestic

transportation),whicharenotdirectlyrelatedtotradeortheoutputoftradablegoods.TheIEA

estimatesthatindustrialproductionrepresentsonlyafifthofworldwideemissions,andmost

industrialoutputemissionsareunrelatedtotrade–e.g.,ifaquarterofsteeloutputistradedthen

threequartersoftheoutputemissionsfromsteelcorrespondtodomesticconsumption.This

suggeststhatinternationaltransportmeasuredasashareoftrade‐relatedemissions(whichwe

defineasemissionsgeneratedbytheproductionandtransportofexportedgoods)couldbe

substantial,butcarefulmeasurementisneeded.

BymeasuringactualfuelusetheITF“top‐down”approachisanaccuratewaytoassess

worldwideaviationandmaritimeemissionsinaparticularyear.However,theITFapproachhas

twokeydrawbacks.First,roadandrailtransportrepresentasignificantfractionofinternational

tradeforland‐adjacentpartnersbuttheiremissionsareomittedfromtheITFnumbersbecause

internationalanddomesticfuelusageisindistinguishable.Thisisespeciallyproblematicbecause

roadandrailtransportisarisingshareofworldtradeasregionaltradeliberalization,especiallyin

NorthAmericaandEurope,concentratedtradegrowthbetweenpartnercountriessharingland

borders.RoadandrailgrowthisomittedfromITFemissionnumbers,whichraisesthequestionof

whetherthesharpdeclineinemissionsperdollaroftradeshowninTable1isrealorspurious.

4

TheseconddrawbackisthatonecannotusetheaggregateITFnumberstoassesswhereorhow

maritimeoraviationfuelwasused.Evenifoneweretotrackfuelloadedtoindividualportsthis

wouldbeoflimiteduseasshipsandplanesrefuelinginaparticularportcouldbecarryingcargoof

anytypebetweenanycountrypairintheworld.Withoutknowingwherefuelisusedwecannot

evaluatethetotalemissionsassociatedwithaparticulartradeflow(i.e.,aspecificproducttraded

betweenacountrypair).Norcanweestimatewhetheremissionswillrisefasterorslowerthan

overalltradegrowth,orunderstandwhichtradeflowswouldbemostaffectedbyeffortstomitigate

emissions.

Complicatingmattersfurther,thecontributionoftransporttotrade‐relatedemissionscan

differdramaticallyacrosstradeflows.Standardanalysesinthetradeliteraturefocusontrade

value,whileignoringtheweightoftradeandhowgoodsmove.Butemissionsdependonthemode

employedandweight,notvalue,transported.Onemilliondollarsofcoalisvastlyheavierthana

milliondollarsofmicrochips,withcorrespondinglylargertransportemissions.Trucks,rail,

airplanesandshipshavesignificantlydifferentGHGemissionsandmodalusevarieswidelyacross

tradeflows.Onekilogramofcargoflownonekilometeronaplanegeneratesbetween50and200

timestheemissionsofthatsamekg‐kmonabulkcargocarrier.Theproductandpartner

compositionoftradehasafirst‐orderimpactonthetypesoftransportationemployed,andonthe

associatedGHGemissions.Asaconsequence,welearnlittlefromtheaggregateincidenceof

transportemissionsthatcanbedirectlyappliedtoparticulartradeflows.

Thepurposeofthispaperistoprovidetwoexercises,bothofwhicharenovelinthe

literature.Inthefirstwebuildanextensivedatabaseonoutputandtransportemissionsassociated

witheveryorigin‐destination‐producttradeflowworldwideinabaseyear2004.Weemploythis

databasetoquantifythecontributionofinternationaltransporttototalemissions,andtohighlight

systematicpatternsoftransportemissionintensitiesacrossproductsandtradepairs.Inthesecond

exercise,wecalculatetheemissionsgrowthduetoasimulatedchangeinglobaltradearisingfrom

5

tariffliberalizationandunevenlydistributedGDPgrowth.Inanalyzingthesimulatedchangesin

overallGHGemissions,wedistinguishbetweenscale(i.e.,changesinthederiveddemandfor

internationaltransportservices)andcompositioneffects(i.e.,changesintherelativeuseof

transportmodesofvaryingemissionintensities).4

Webeginbycombiningtradeandemissionsdatabymodeinordertoprovideafull

accountingoftheemissionsassociatedwithinternationaltransportationforeachindividualtrade

flow.This“bottom‐up”accountingofemissionsyieldsaggregateworldwideemissionsthatare

remarkablyclosetomatchingthe“top‐down”accountingprovidedbytheITF2010.UnliketheITF

aggregatedata,theseemissionsnumbersarespecifictoeachorigin‐product‐industrialsector.This

allowsustocalculatetheemissionsassociatedwithadollaroftradeanddecomposeitintoa

productionandatransportcomponent.

Wenextdescribetheimportanceoftransportrelativetoproductionemissionsforspecific

tradeflows,andshowwhichtradeflowsareespeciallyemissionsintensiveoncebothcomponents

aretakenintoaccount.World‐wide,33percentoftrade‐relatedemissionscomefrominternational

transport,thoughthisnumberisconsiderablyhigherinthemanufacturingsectors:80percentof

trade‐relatedemissionsinmachineryexportscomefrominternationaltransportation.Thereis

alsowidevariationacrosscountriesinthecontributionoftransporttotrade‐relatedemissions.At

thelowend,only14percentofIndianandChineseexportemissionscomefromtransport,while

transportisresponsiblefor66percentofUSexportemissionsduetosubstantialuseofaircargo.

Themagnitudeoftransport’scontributiontototalemissionssuggeststhatpoliciesdesignedto

mitigatecarbonoutputmusttakeinternationaltransportintoaccountandfurther,thatthedesign

ofsuchpoliciescouldhavepronounceddistributionaleffects.Forexample,theUSisresponsible

foronethirdoftransportemissionsbutonly12percentofoutputemissions.AndwhileUSimports

4Inoursimulationexercises,thetechniqueeffect(i.e.,changesintheemissionintensityoftransportservices)isheldconstantatthebaseyearlevel.Noticethatwhileseveralstudieshavedecomposedtheoverallchangeinproductionemissionsintoscale,compositionandtechniqueeffects(seeforexampleLevinson,2009;Gretheretal.,2010),ourfocusinthispaperisontrade‐relatedemissions.

6

andexportsareverysimilarintermsoftheemissionintensitiesofproduction,onceweinclude

transport,itsexportshavedoubletheemissionintensity.Whethertransportemissionsare

allocatedtotheexporterortheimporterthusbecomesasignificantissueforwelfareanalysis.

Risingtradeinducesemissionchangesbyboostingtransportemissions,andbyreallocating

productiontowardcountrieswithdifferentproductionemissionintensities.Bycharacterizingboth

productionandtransportemissionsfromtradeflowswecanaddresssystematicallythequestions

answeredpreviouslyusingcasestudies,namely,doesconsumingforeigngoodsraiseorlowerGHG

emissionsonceinternationaltransportisaccountedfor?Weexamineasetof“partialequilibrium”

reallocationsinwhichacountrylowersitsownproductionandinsteadbuysthegoodfromabroad.

Justoveraquarterofchangesinspecializationwouldleadtoareductioninemissions,withmuch

highernumbersinresource‐basedindustriesandinthedevelopingworld.5

Thesepartialequilibriumreallocationsaremeanttobeillustrative.Theydonot

contemplatewhetherthereallocationisfeasible,whatkindsofshockswouldinduceit,orwhat

possiblegeneralequilibriumeffectsmightexacerbateorattenuatethechange.Toconsiderthese

issueswenextsimulatethelevelandcompositionoftradegrowthinfourscenariosrelatedtotrade

liberalizationandafifthscenarioexaminingdifferentialchangesincountryGDPgrowthrates

throughtheyear2020.Tradeliberalizationandoutputgrowtharelikelytoleadnotonlytogrowth

inthequantityoftradebutalsotochangesinitsproductandcountry‐paircomposition.The

questionisthenwhethergrowthwilloccurinhighorlowemissionscategories,andwhether

transportemissionsarelikelytogrowmorerapidlythanoutputemissions.Combiningsimulated

outputandtradechangeswithouremissionsdatawecanthencalculatethepredictedgrowthin

emissionsfromtrade.

Ourfindingsareasfollows.TradeliberalizationscenarioscurrentlycontemplatedundertheDoha

WTOroundgenerateverysmallchangesinoutput,exports,andGHGemissions.Fullliberalization

5Theseemission‐reducingtradepairsarenon‐trivial,correspondingto31percentofglobaltradebyvalue.

7

resultsina6percentincreaseintrade,concentratedinthoseproductsthataresubjecttothe

highestratesofprotection.Moreimportantly,liberalizationeliminatestariffpreferencesenjoyed

primarilybynearbytradingpartners(e.g.,NAFTAandtheEU).Tradeshiftsawayfromproximate

partnersandtowarddistantpartnerswhocannotbereachedbylandtransport.Useofaircargo

rises,andwithit,GHGemissionrise23‐42percentfasterthantrade.

Incontrasttothemodesteffectsfromtariffliberalization,projectedoutputgrowth(a75percent

increaseingrossworldproductby2020)leadstoprofoundchangesintradeandemissions.

Exportsriseat3.8percentperyear,80percentcumulatively,whiletransportservices(kg‐km)rise

173percentcumulativelyastradeshiftstodistantbutrapidlygrowingChinaandIndia.Transport

emissionsgrowfasterthantradebyvalueandfasterthanoutputemissions,withespeciallyrapid

growthinmaritimeemissions.

Thepaperproceedsasfollows.SectionTwodescribesthemethodologyandSectionThree

describestheconstructionofthemaindatacomponentsforourexercises.SectionFourprovides

evidenceoncurrentcontributionofinternationaltransportationtoGHGemissionsfrom

internationaltrade.SectionFiveprovidessimulationsoftradegrowth,andcalculateshowthis

growthwouldaffectmodaluseandemissions.SectionSixconcludes.

II. Methodology:BaseYearEmissions

TheInternationalTransportForum(ITF2010)usesdataonfuelconsumptiontocalculate

emissionsassociatedwithinternationaltransport.Asdiscussedintheintroduction,this“top‐

down”approachprovidesaccuratemeasuresofworldwideemissions,buthasanumberof

significantdrawbacksbecauseitcannotassignemissionstoparticulartradeflows.Weusea

“bottom‐up”approachinwhichweconstructtheemissionsassociatedwithatradeflowby

calculatingthequantityoftransportationservicesforthatflowprovidedbyeachtransportation

mode,andmultiplyingbyemissionsperunitoftransportationservices.

8

Denote astheGHGemissions6associatedwithtransportinggoodgfromoriginoto

destinationd.VAListhevalueofthatflow,andWVistheweighttovalueratiosothat

isthequantityoftheflowinkilograms.Acountrypairmayshipproductgusingmultiple

transportationmodes.Thequantityshareofmodeminthatflowis ,so

givesthequantityoftheflowforeachmode,inkg.Multiplyingby thedistancetraveled

fromotodformodemgivesusameasureoftransportationservices,foreachmode,measuredina

commonunit(onekgofcargomovedonekilometer).Finally,multiplyingby ,theGHG

emissionsproducedbymodemwhenprovidingonekg‐kmoftransportationservices,and

summingoverallmodesyieldsthetotalemissionsassociatedwiththattradeflow.

(1)

Thisbottomupapproachhasafewlimitationsowingtodataavailability.Thisformulationimposes

aconstraintthatemissionsforagivenmodearecommontoallproductsandcountrypairsandare

linearinweightanddistance.Assuchitmaskstwopotentiallyimportantsourcesofheterogeneity.

One,sometradeflowsmayemployolder,smallershipsandplaneswithhigheremissionsperkg‐km

oftransportationservices.Wepartiallyadjustforthisprobleminthedatabyallowingformultiple

typesofoceanvesselsthatarespecifictocertaincargos,andbyexperimentingwithaviation

emissionsdatathatreflectthemostefficientplanesversusthoseinuseinexistingfleets.Two,

thereareemissionsassociatedwith“fixedcosts”oftransport,incurredindependentofdistance

traveled,includingporttimeforshipsandhigherlanding/takeoffemissionsforplanes.We

providecalculationstosuggestthattheseproblems,whilesignificantatveryshortdistances,

becomeinsignificantattheinternationaldistancesseeninthedata.

Anadditionallimitationrelatestoemissionsfromdomestictransportlinkedtotrade.All

productionrequiresdomestictransport,andwecapturethisinputanditsassociatedemissionsas

6“GHGemissions”refertobothCO2andnon‐CO2emissions,representedasCO2equivalents.

TodgE

*odg ogVAL WV

modgQS * * m

odg og odgVAL WV QS

modDIST

me

* * * *T m m modg odg og odg odm

E VAL WV QS DIST e

9

partofoutputemissions.Ifproductionforexternaltradeusesdomestictransporttothesame

extentasproductionfordomesticuse,thenwecapturedomestictransportemissionsaccurately.

However,insomeinstancesexternaltrademayrequiremovementofgoodsovergreatinternal

distances,whileinothers(productionnearborders,ornearairorseaports)externaltrademay

employverylittledomestictransport.Thismayresultinunder‐orover‐countingtrade‐related

emissions,butwehavenoclearindicationifthereisabiasorwhichwayitruns.Notethatthisis

fundamentallysimilartoanycaseinwhichaheterogeneousproductiontechnologyischaracterized

byanaggregatetechnology.

Startingfromequation(1),wecanprovideanumberofcomparisonsandcalculations.

Tradeflowsaremostcommonlyreportedinvalueterms.Pullingthevalueofthetradeflowoutof

thissummationwecandecomposethequantityoftransportationemissionsfromtheflowintoa

scalemeasureandanintensitymeasure

(2)

Usingthisbasicdecompositionwecancomparethetransportemissionsfromexportsacross

countries.Summingoverimportersandproducts,anexportero’semissionsare

(3)

where istheshareofdestinationd,goodgintotaltradefororigino.Transportemissions

dependonthescaleoftradeandthetransportemissionintensityofadollaroftrade.Thelatterisa

trade‐weightedaverageofemissionsfromindividualflows.Ifanexporterengagesintradewith

moredistantpartners,tradesheaviergoods,orusesaviationmorethanmaritimetransportitwill

haveahigheraggregatetransportemissionintensity.Wecanprovidesimilaraggregationsby

importers(aggregatingoverexportersandproducts)orbyproducts(aggregatingovercountry

pairs).

* * * *T T T m m modg odg odg odg og odg odm

E VAL e where e WV QS DIST e

* * *T T To o o o odg odgdg

E VAL e VAL s e

odgs

10

Wecanalsousethisdecompositiontocomparetheemissionintensityoftradearisingfrom

twodistinctsources:productionoftradedgoodsandtransportoftradedgoods.Beginbywriting

theemissionsfromoutputofgood(orservice)gincountryoastheproductofoutput(indollars)

andemissionsperdollarofoutput,

(4)

sothataggregateemissionsinacountryareanoutputweightedaverageofemissionsforeach

activity.

EoY Yo * sgg

*eogY

Aggregatingagainoverallcountriesyieldsworldwideemissions,similartothatfoundinTable1.

Ifweinsteadmeasurebothoutputandtransportemissionsasanintensity(i.e.,CO2equivalentsper

dollar),wecancalculatethecontributionofeachemissioncomponenttothetotalemission

associatedwithaparticulartradeflow.Foranyparticularo‐d‐gflowwehave:

(5)

Thisrepresentationisalsoconvenientasitallowsforanimmediatecalculationofthetariff

equivalentofpoliciesdesignedtoreducetotaltrade‐relatedemissions.Supposeatradeflow

produces200gramsofCO2equivalentemissionsperdollaroftrade,andfacesacarbontaxof$50

perton.Thecarbontaxraisesthecostofthattradeflowbyonepercent,andsoisequivalenttoa

1%tariff.

Muchofouranalysiswillconsistofafewbasicbutinformativecalculations.Wewill

comparethemagnitudesof forparticulartradeflows,andintheaggregatefordifferent

regions.Wewillalsoanalyzewhethermovingoutputfromahighemissiontoalowemission

producerinducesemissionchangesthatarelargeorsmallrelativetoreallocatingtradeacross

partnersfromhightransportemissiontradeflowtoalowtransportemissiontradeflow.

*Y Yog og ogE Y e

*T Yodg odg og odgE e e VAL

,T Yodg oge e

11

III. Data

InthissectionwedescribethemaindatacomponentsnecessarytodescribeGHGemissionsfrom

outputandinternationaltransportationinthebaseyear.Thesedatacomponentsare:theweight,

value,andmodalsharesoftradeforeachbilateralpairandproduct;theGHGemissionintensityfor

eachtransportationmode;andGHGemissionsassociatedwithoutputforeachproducerxsector.

Giventheimprovementinqualityandcoveragethatthesenewsourcesofdataprovide,andtheir

likelyuseinfutureresearchontransportandtrade‐relatedemissions,wedevotemuchattentionto

documenttheconstructionofthedataset.

A. Aggregation

Thesedisparatedatacomponentsmustfittogetherprecisely,usingthesamelevelofregionaland

productaggregation.Inthiswearemostconstrainedbythedataavailableforoutputemissions,

whichwetakefromthedatabaseunderlyingversion7oftheGlobalTradeAnalysisProject(GTAP)

model.TheGTAPdatabaseisidealforourpurposesbecauseitcontainsdetailedinformationon

energyusageandGHGemissionsbyorigincountryandsector,andbecausewecanusetheGTAP

computablegeneralequilibriummodelinthefinalsectionofthepaperforperformingtrade

liberalizationandoutputgrowthsimulations.

Atitsmaximumdisaggregation,GTAP7allowsonetomodelproductionandtradefor57

tradedandnon‐tradedsectorsbetween113countries.Whileitisnotcomputationallyfeasibleto

runtradeexperimentswiththefull113countryx57sectorversionofthemodel,GTAPallowsfor

flexibleaggregationacrossregionsandsectorsinordertoexaminecertainespeciallyinteresting

subsetsofthewholedataset.Forcurrentpurposes,weemployanaggregationofthemodelwith40

regions(i.e.,1600bilateralpairs),and23tradedgoodsand6non‐tradedgoodssectors,thedetailed

listingofwhichisreportedinAppendix1.

Thisparticularaggregationschemewaschosentoservetwopurposes.One,countriesand

sectorswith“similar”transportationcharacteristicsareaggregatedtogether.Forexample,allsub‐

12

categoriesofbulkagriculture,whichprimarilyusesmaritimetransport,areaggregatedintoone

categorywhilesub‐categoriesofprocessedagriculture,whichismorelikelytoemployair

transport,areaggregatedintoasecondcategory.Two,weemploycountrylevelaggregationin

caseswherewehavedetailedweight/valueandtransportationmodedata,andbroadergeographic

aggregationforregionswherethesedataarelacking.Forexample,werepresenttheMiddleEast

andAfricainonly3aggregatedregions,whileEuropeisrepresentedwith15individualcountries

and3aggregatedregions.Thisallowsustominimizetheamountofimputationthatmustbe

employedtocompletethedatabase.

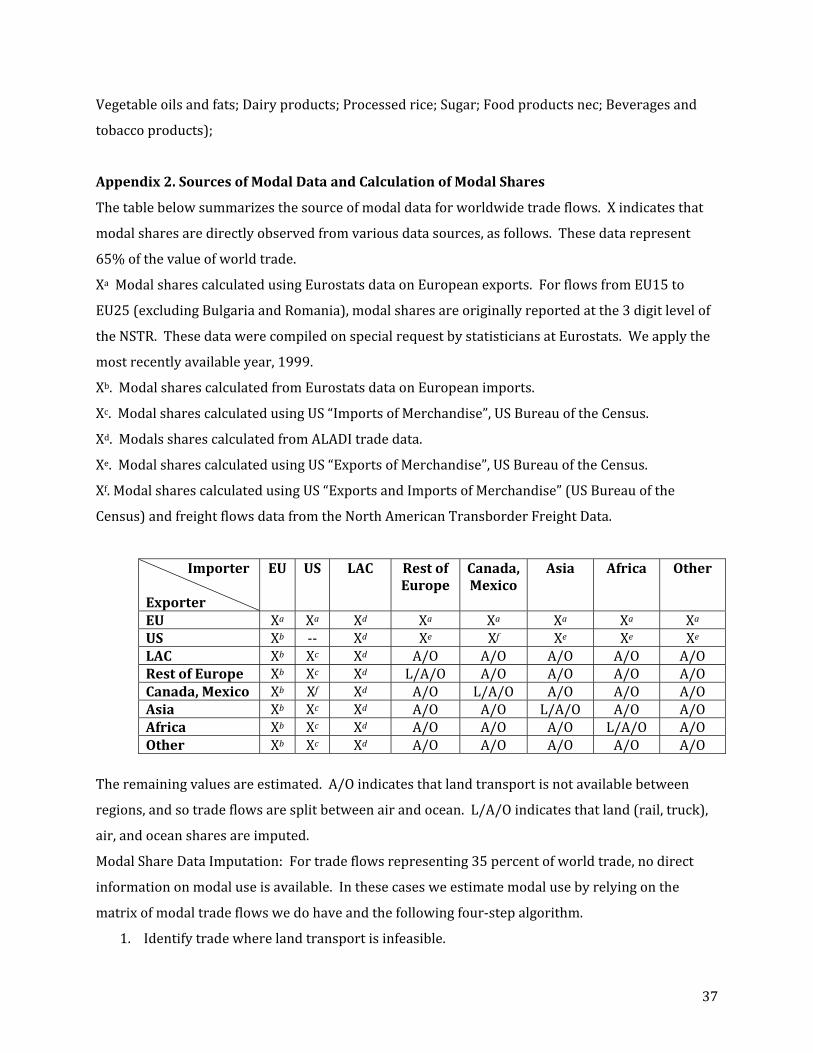

B. TradeandOutputintheBaseYear:Weight/Value,andModalShares

Recallingequation(1),weneeddataonthevalueoftrade,theweight/valueratio,andthequantity

sharesofeachmode.

OurbasedatasetforthevalueofoutputandtradecomesfromtheGTAP7database,

aggregatedto40regionsand29sectors(23traded)in2004.Bymultiplyingvaluesindollarsbya

weight/valueratio(kg/dollar)thatisspecifictoeachoriginxsector,weconvertthesevalueof

tradenumbersintokilograms.Thisphysicalunitofmeasurementisconsistentacrosscountries

andproducts,ismeaningfulfromatransportationperspective,andcanbeuseddirectlytocalculate

GHGemissionsfromtransport.

Toconstruct wedrawonthreeprimarydatasourcesthatreporttradebyvalueand

weightatthe6digitleveloftheHarmonizedsystem(roughly5000products).Theseare:US

ImportsandExportsofMerchandise;EurostatsTrade(coveringtheimportsandexportsof27EU

countries)7,andtheALADItradedatabase,coveringtheimportsof11LatinAmericancountries

(Argentina,Bolivia,Brazil,Chile,Colombia,Ecuador,Mexico,Paraguay,Peru,Uruguayand

7DataontradeoutsidetheEUbytransportmodeareavailableattheHS6level.DataonexportsfromEU15toEU25countries(excludingBulgariaandRomania)bytransportmodearereportedatthe3digitleveloftheNSTRandwerecompiledonspecialrequestbystatisticiansatEurostats.

ogWV

13

Venezuela)fromallexportersworldwide.Thebilateralpaircoveragerepresentedbythesethree

datasetsisdisplayedinAppendix2.

ItisnecessarytoconcordtheHS6datatothe23merchandisetradesectorsusedinour

aggregationoftheGTAPmodel.Thismeansthatforeachimporterandexportertheremaybe

severalhundredHScodescorrespondingtoasingleGTAPsectorsuchas"electronicequipment".

Toarriveataweight/valueratioforeachexporterandproduct,weseparatelysumtheweightof

tradeandthevalueoftradeandexpressthemasaratio.Thisisequivalenttoashare‐weighted

averageoftheweight/valueratioforeachHS6producttradedbythatexporter.8

ForreferencewereportdatabycommodityinAppendixTableA1.Thisincludesinitialtariffrates

andweight/valueratios(eachexpressedasatrade‐weightedaverageoverallcountrypairs),along

withtheshareofeachcommodityinworldoutput,worldtradebyvalue,andworldtradeby

transportationservicesunits(kg‐km).Ofinterest,someofthegoodsthatrepresentalargervalue

shareintrade(electronicequipmentandmachinery)representasignificantlysmallersharein

transportationservices.Thisreflectslargedifferencesinweight/valuebetweenthese

manufacturedgoodsandheavyproductssuchasbulkagriculture,minerals,andoil.

Thedataformodalshares, ,comefromthesamethreesourcesastheweight/value

datadescribedabove.Eachofthosedatasetscontainsinformationontheweightandvalueoftrade

byorigin‐destination‐productandtransportmode.TheUSdatasplittradeintoairandocean

modes,buthasnomodalinformationonoverlandtransportfromMexicoandCanada.To

disaggregatetheseflowsintotruckandrailweusesupplementarydatafromtheTransborder

8Wedonotemployweight/valueratiosthatvaryacrossimportersbecausewedonothaveweightdataforeveryo‐d‐gtripletinthedata.Apartfromtheo‐dpairswithnodata,theweightfieldismissingfromroughly20percentofEUobservations,thoughthesetendstoberelativelysmallvalueflowsandunrelatedtomodaluse.Ingeneral,becauseaggregatingoverimportersforagivenexporterandproductreducesmeasurementerrorinthemorenoisyweightdata.

modgQS

14

SurfaceFreightData.9TheEUandALADIdatasetsreporttradebyair,ocean,rail,andtruckmodes.

ModalusefortheUS,ALADI,andEUtradewithnon‐EUpartnersaremeasuredattheHS6level.

Intra‐EUtradeismeasuredattheNSTR3digitlevel.Toconstructmodalquantityshares,wefirst

concordtheHS6(orNSTR3)productcodestoGTAPsectorgroupings,andaggregatesothatwe

havetheweightoftradeforeachmodewithineacho‐d‐gtriplet.

For35percentofworldtradebyvaluewehavenodirectdataonmodaluse.Inthesecases

weestimatemodalsharesasafunctionofgeography,country,andproductcharacteristicsbasing

ourestimationsampleonthosecountrypairsthatdoreportmodaldata.Theseregressionshave

goodexplanatorypower,especiallyinthevastmajority(allbut2percent)oftheremainingcases

wherelandtransportisnotanoption.DetailsareprovidedinAppendix2.

Theresultsofourdatacollectiongenerateafullmatrixofmodalsharesforeachorigin‐destination‐

GTAPsectorbyvalue,weight,andtransportationserviceunits(kg‐km).Table2providesmodal

sharesfortheimportsandexportsofeachcontinent,bytradevalueandKG‐KM.AppendixTable

A2reportsthenumbersbytradedsectors.

Afewthingsarenotable.Therearelargedifferencesacrossregionsinthevaluesharesof

thetransportationmodesthatlargelyreflectgeography.Forexample,NorthAmericaandEurope,

withimportantland‐adjacenttradepartners,relymuchmoreheavilyonroadtransport.10

Substitutionbetweenairandoceancargoisespeciallyimportantasitreflectsthelargestgapin

emissionintensities.Worldwide18percentoftradebyvalueisair‐borne,withmuchhigherratios

inNorthAmericanandEastAsianexports.Excludingland‐basedmodes,airtransportrepresents

9TheTBSFdatahaverailv.roadsplitsattheHS2level.Wetakeeachland‐basedtradeflowfromthemoredisaggregatedHS6dataanddivideitusingthesplitsfoundinthecorrespondingHS2data.Wethenaggregatetothebroader23sectorsfoundintheGTAPdata. 10MostofAsiahasverysmallsharesoflandtransportbecausethelargesttradingpartnersareseparatedby(short)stretchesofocean.SouthAmerica,forwhichlandtransportisactuallyanoptionhasratherlowlandtransportshares,probablybecauseeconomicactivityisconcentratedoncoastsratherthanintheinteriorsclosetolandborders.Whenwedisaggregatetothecountryleveltherearemoredramaticdifferences.Europeasawholehasveryhighsharesofrailandroadtransport,exceptforcountriesliketheUK,Ireland,andFinland.

15

48percentofinternational(air+ocean)cargoforNorthAmericanexportsand27percentfor

EuropeanandAsianexports.

Itisalsoinstructivetocontrastthevalueoftradewiththetransportationservices(KG‐KM)

employedbytrade.Here,seatransportdominateswith95percentoftransportationservices

provided.Productsthatareheavy,andthataretransportedlongdistances,aremuchmorelikelyto

besea‐borne.Thelargestdifferencerelativetovaluesharescomesintheuseofroad‐based

transport:whileitrepresentsnearlyhalfofEuropeanimportsbyvalueitisonly5percentof

EuropeanimportsbyKG‐KM.Roadtransportconstitutesalargeshareofvalueandweightmoved

inEuropeantrade;howeveritisconcentratedinthetradeofproximatepartners.Asaresult,road

transportrepresentsaverysmallshareofkilogram‐kilometersshipped.

C.GreenhouseGasEmissionsbyTransportMode

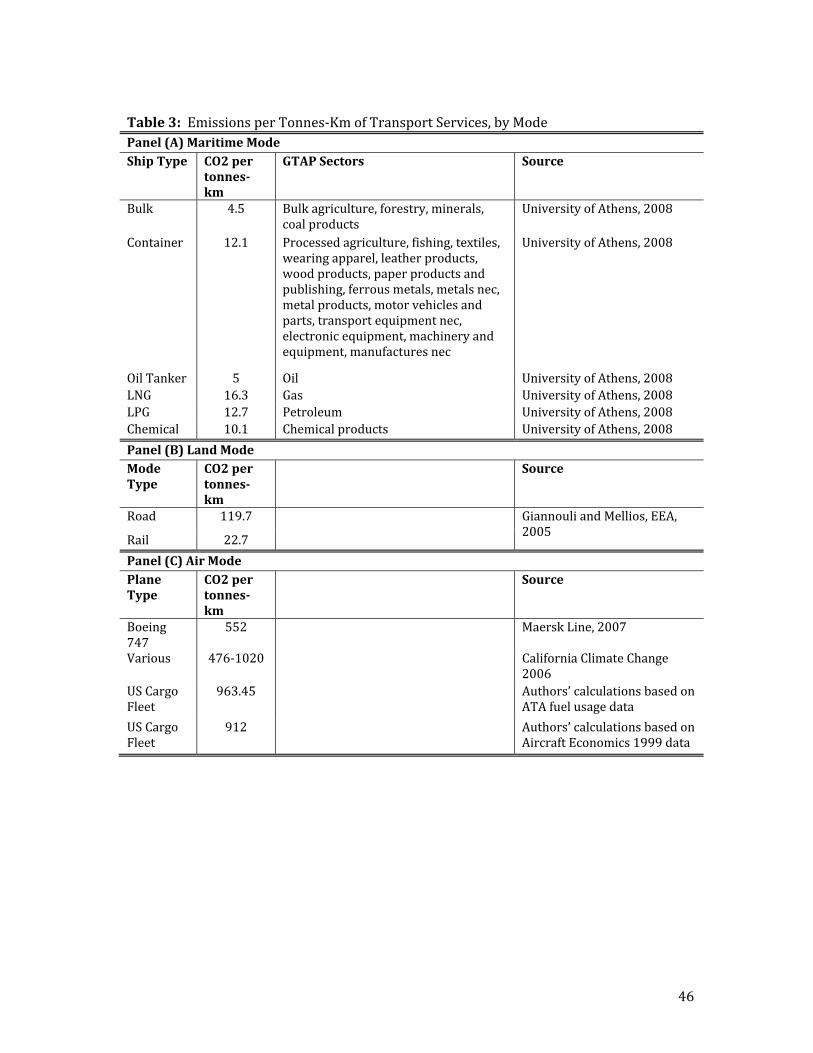

Wedrawondatafromseveralstudiestocalculateemissionsperkg‐kmofcargomovedbyeachof

thefourtransportmodes:ocean,air,rail,androad.Thesesources,anddataonemissions,are

reportedinTable3.Webrieflyremarkonthedataformaritimeandaviationemissionshere.

Themostrecentandcomprehensivestudyformaritimetransportcomesfrom"ShipEmissions

Study",NationalTechnicalUniversityofAthensLaboratoryforMaritimeTransport(2008).It

reportsemissionsingramsofCO2pertonne‐kmshippedformanydistinctshiptypes,aswellas

variabilityacrossvesselsofdifferentsizeswithineachtype.11InTable3,wereproducethefleet

averagesforsixshiptypes,andnotetheshiptypesemployedforeachtradedgoodssectorinour

model.Whileotherstudieslackthedetaileddatabyshiptypereportedinthatstudy,thosestudies

(Kristensen2006,GiannouliandMellios,2005)thatprovidedataforcontainerizedcargoarriveat

similaremissionnumbers.

11Ingeneral,CO2emissionspertonne‐kmshippedaremuchlowerforlargervesselswithineachtype.Forexample,post‐Panamax(>4400TEU)containershipsproduce1/3theemissionsofalessthan500TEUfeedership.Becausewehavenodataontheshipsizecompositionofflows,weemployfleetaveragesforeachfleettype.ThestudyalsoprovidesdataforhighlyspecializedshiptypessuchasReefersandRo‐Ros.Wedonotemploythisdataasourbroadertradeaggregatescontainamixofgoodsthatwouldemploythesespecializedtypesasasmallsubsetofgoodsthatgenerallyemploycontainervessels.

16

Insearchingtheliteraturewefoundfewestimatesofemissionsassociatedwithaircargo.These

arriveatwidelyvaryingestimatesofemissionspertonne‐km,andprovidelittledetailon

methodology.Forexample,aMaersk2007pamphletcitedintheUniversityofAthens(2008)study

reportsthataBoeing747‐400emits552gramsofCO2pertonne‐kmshipped.ACaliforniaClimate

Changepamphletfor2006reportsemissionspertonne‐kmshippedrangingfrom476‐1020grams

ofCO2.

Giventhiswiderange,weattemptedourowncalculationsbasedonfuelusageandfleet

characteristics.TheAirTransportAssociationofAmericareportsfleetwidefuelusageandton‐

milesofcargoshippedforUScargoairlines.UsingthesetotalswecalculatethatUScargoairlines

used163.6gallonsofjetfuelperthousandton‐milesshipped.Convertinggallonsofjetfuelinto

gramsofCO2andcargosintotonne‐km,wecalculateCO2emissionsof963.5gramsofCO2per

tonne‐km.

WealsoattemptedtoconstructanindependentestimateofCO2emissionsassociatedwith

aircargousingdatatakenfromAircraftEconomics,1999,“FreighterCostComparisons”.This

sourceprovidesdatafor14majorcargoplanetypesincludingtotalfueluse,revenueton‐miles

flown,andshareinthefleet.Combiningfueluse,emissionspergallonofjetfuel,andton‐kmflown

itispossibletoconstructameasureofaverageCO2emissionspertonne‐kmflown.Thenumbers

rangefrom493to1834,dependingontheplanetypeandhowitwasused(i.e.forshortv.longhaul

cargocarriage).Forcomparison,applyingthismethodtotheBoeing747yieldsemissionsof700

gramsofCO2pertonne‐km,whichisclosetotheMaerskstudy.Takingaweightedaverageof

theseemissionnumbersoverthefleetsharesreported,wearriveataverageemissionrateof972

grams.Finally,ifweupdatethefleetcompositionusing2008shares(fromATA)wearriveat

averageemissionsof912.1grams.

Inthecalculationsthatfollowweemploy552g/t‐kmasa“LOW”emissionsvaluefor

aviation.Thiscorrespondstouseofthemostefficientaircraftonthelongestflights.Weuse950

17

g/t‐kmasa“HIGH”emissionsscenario,anditcorrespondstoauseofamixedfleetofsmaller

planesonshorterflights.

Toamplifythislastpoint,landing/takeoff(LTO)requireshighfueluserelativetocruising,but

thiseffectismostpronouncedatshortdistances.WecollecteddetaileddatafromEEAEmission

InventoryGuidebook2007onfuelusageonLTOandcruiseforavarietyofplanesandcalculated

emissionsperton‐kmforvarioustriplengthstoseehowthiswouldaffectourcalculations.For

example,a747‐400witha60%loadfactorona1852kmflightemits556g/t‐km(closetoourLOW

scenario),whilethatsameplaneandloadfactoremits912g/t‐kmona463kmflight.This

representsanimportantdiseconomyofscaleformuchshorterflightsofthekindonewouldsee

withdomesticUScargousage.However,onceonegetstoflightsofinternationaldistances,the

effectsbecomemuted.At463km,LTOfuelrepresentsnearly55%oftotalfueluse,droppingbelow

5%fordistancesabove6000km.Themediantraveldistanceinourdatais8000km.

Thefinalcomponentweneedtocalculatetransportemissionsisdistancetraveled.Forrail,

road,andairtransportwerelyonthesimpledistancesreportedbytheCEPII.12Bilateraldistances

betweencountrypairsarecalculatedfollowingthegreatcircleformula,whichuseslatitudesand

longitudesofthemostimportantcityineachcountry.13Foroceantransportdirectlinedistances

significantlyunderstateactualdistancestraveled.Containershipsrarelytravelpointtopoint

betweenimporterandexporterandfrequentlystopatmultipleportsofcallenroute.Wedrawona

datasetofactualshipitinerariesfromHummelsandSchaur(2011)thatallowustocalculateactual

distancestraveledduetotheseindirectroutings.

D.GreenhouseGasEmissionsfromOutput

TheGTAP7databaseprovidesdataonGHGemissionsproducedbyeachsectorgineachcountryo,

inequation(4).Webrieflysummarizehowthesedatawereconstructed,anddirectreadersto

12TheCEPIIdatasetisavailablefordownloadathttp://www.cepii.fr/anglaisgraph/bdd/distances.htm. 13Foraggregationattheregionallevelweweightedeachconstituentcountry’sdistancebyitsGDPshareintheregion’sGDP.

YogE

18

moredetaileddiscussionsavailablefromLee(2008)andRoseetal(2010).Foreacho‐gpair,the

databasecontainsinformationonuseofsixenergyinputs(coal,oil,gas,petroleumproducts,

electricity,andgasdistribution).Energyusediffersacrosscountriesandsectorsasafunctionof

theenergyintensityofproduction,theefficiencywithwhichenergyisused,andtheavailabilityof

energyinputsintherespectivecountry.UsingastandardformulationprovidedbyIPCC(1997)

guidelines,thequantityofenergyinputsisthenconvertedintoCO2emissions.Finally,thesedata

aresupplementedbycalculatingnon‐CO2greenhousegasesemittedasaby‐productofproduction

(primarilyinagriculture).TheseareconvertedintoCO2equivalentsbasedontheirglobalwarming

potentials,followingthemethodologyinUSEPA(2006).

CombiningthesedatawehavetotalGHGemissionsforeachcountryoandsectorg.To

providecomparisonstoourtransportationemissions,wedescribetheseasemissionintensitiesper

dollarofoutput bydividingtotalemissionsforo‐gbythemarketvalueofoutput.

IV. TransportandOutputEmissionsintheBaseYear

Inthissectionweprovidethreemainexercises.First,wecompareour“bottom‐up”approachto

calculatinginternationaltransportemissionstotheITF“top‐down”approachasamethodological

check.Second,wecomparetransporttooutputemissionsforagiventradeflowtogaugethe

importanceoftransportemissionsintrade.Third,weusethetransportandoutputdatain

combinationtoconsiderwhethersomepartialequilibriumchangesinthepatternofspecialization

andtradewillyieldrisingorfallingGHGemissions.

A. AggregateEmissionsfromInternationalTransport:ComparingMethodologies

Our“bottom‐up”approachtoemissionscalculatesthequantityoftransportationservices(KG‐KM)

performedbyeachmodeineachorigin‐destination‐producttradeflow,andthenmultipliesby

emissionsperKG‐KMforeachmode.Thisyieldstransportationemissionsthatarespecificto

nearly36,000individualtradeflows.Summingoveralltradeflowswehaveanalternativeestimate

Yoge

19

oftotalCO2emissionsfrominternationaltransport.Howdoesthisbottomupapproachcompareto

thetopdownITF(2010)approachbasedonworldwidefuelusage?Theansweris:surprisingly

well.In2004,theITFcalculatesthatinternationalaviationandmaritimetransportwasresponsible

for910milliontonsofCO2production,520frommaritimeand390fromaviation.Wecalculate

522milliontonsofmaritimeemissions.WhenweemploytheLOWemissionsintensitywe

calculateaviationemissionsof419(andatotalof941milliontons)in2004.14Accordingly,wewill

focusmostofoursubsequentcalculationsontheLOWaviationemissionsscenario.Whilethereare

largemethodologicaldifferencesbetweenourapproachandtheITF,wematchemissionaggregates

quiteclosely.Thisgivesusconfidencethatourestimatesfordisaggregatedflowswillalsobe

informative.

Usingourmorecomprehensiveemissionsdatawecalculatethattotalinternational

transportemissionsare1205milliontonsin2004.Measuredrelativetothevalueofworldtrade,

internationaltransportemits146gramsperdollaroftrade,whileoutputoftradedgoodsgenerates

300gramsperdollaroftrade.Thatis,totaltrade‐relatedemissionsare446gramsperdollar,of

which33percentcomefrominternationaltransport.Forperspective,a$50pertoncarbontax

appliedtotheaverageinternationaltransportemissionswouldbeequivalenttoa0.73percent

tariff.

Ourcalculationof1200milliontonsofCO2equivalentcontrastswiththe910milliontons

calculatedbytheITF.Byomittingroadandrail,theITFcalculationmisses28percentof

internationaltransportemissions.ThismayhelptoexplainacuriouspatterninTable1.Usingthe

ITFemissionnumbersweseethatinternational(maritimeplusaviation)transportemissionsper

dollarofworldtradedroppedsharplyfrom159g/$in1990to93g/$in2004.Whydidtrade

14NotethattheHIGHaviationintensity,basedonthecurrentcompositionoftheUSaircargofleet,yieldsaviationemissionsof721milliontons,muchhigherthantheITFvalues.Therearetwopossibleexplanationshere.One,theITFseparatesfueluseintodomesticandinternationalusage.Ifsomeinternationalfuelusewereinaccuratelyrecordedasdomesticusage,theywouldunder‐estimateemissions.Two,itmaybethatthecompositionoftheUSaircargofleet,includingsmallerplanesandshorterroutesthanaretypicallyfoundininternationalaviation,mayoverstateemissions.

20

appeartobecomelessemissionintensivefrom1990‐2004?Thekeyisthatland‐basedtrade,

omittedfromtheITFemissionvalues,interactsinaninterestingwaywiththestructureof

protection.Inthisperiodtradegrewespeciallyfastwithland‐adjacentpartners,15promotedby

policymeasuresthatofferpreferentialtariffrates,investmentrules,regulatoryharmonizationand

currencyunionwiththoseclosepartners.Table2showsthatinternationalroadandrailare

responsiblefornearlyathirdofworld‐tradebyvalue–halfofintra‐Europeantradebyvalueisland

based.

Note,however,thatthispatternneednotpersist.Weretradeliberalizationatthe

multilateralleveltoerodepreferentialtariffrates,orwereoutputtogrowmorerapidlyoutsideof

NorthAmericaandEurope,tradewouldlikelyshifttowardsdistantpartners.Werevisitthispoint

inSectionFive.

B. EmissionsfromTrade:ComparingOutputandInternationalTransportation

Webeginbycomparingtrade‐relatedemissionsfromoutputoftradedgoodsandinternational

transportatthelevelof35,880individualtradeflows(thatis,40exportersx39importersx23

tradedgoodssectors).WeplotthedistributionofemissionintensitiesasCO2gramsperdollarof

tradeinFigure1.Outputandtransportemissionsaresimilarlydistributedbecausetheyhave

similarmedians(transport‐120g/$,output‐137g/$)andarehighlycorrelatedatthelevelof

individualtradeflows.16

Thereisawidevarianceinbothtransportandoutputemissions,rangingfromclosetozero

gramsofcarbonperdollartowellover2kgofCO2.Thisvarianceisnotablebecausetheaverage

15Thispattern,insharpcontrasttotheconventionalwisdompointingtothe“deathofdistance”hasbeenpointedoutbyseveralauthorslookingattheeffectofdistancevariablesingravityregressions(DisidierandHead,2008;BerthelonandFreund2008),andotherswhohavenotedtheremarkablylargeeffectofNAFTAandEUliberalizationpoliciesontradewithinthoseregions. 16Tradeflowswithhighoutputemissionsalsohavehightransportemissions,andthisistruewhetherwelookattotalemissionsoremissionsintensities.Aregressionoftransportemissionintensitiesonoutputemissionintensitiesfortheexporteryieldsanelasticityof0.26andanR2=0.10.Aregressionoftotalemissionsfromtransportontotaloutputemissionsyieldsanelasticityof0.76andanR2=0.73.

21

valueof145grams/$fortransportasawholeisdrivenbyaconcentrationoftradeino‐d‐gflows

withverylowemissionintensities.Therearemanyflowswithmuchhigheremissions,andcarbon

taxationwouldhaveapronouncedeffectonthesegoods.Forcomparison,theworld‐wideaverage

tariffrateinourdatais3.2percent,whichisequivalenttoacarbontaxof$50appliedtoatrade

flowwithtransportemissionsof650grams/$.

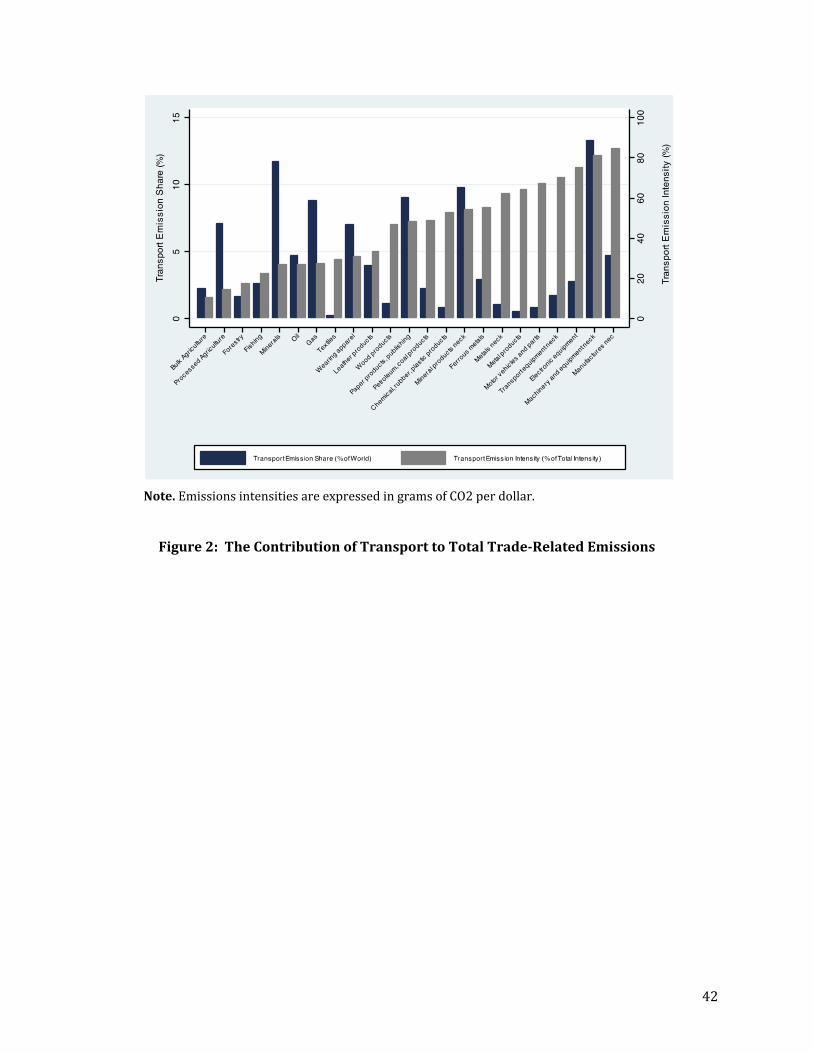

Nextweexaminethecontributionoftransportemissionstotrade‐relatedemissionswhen

calculatedonacommonperdollarbasis.Weaggregatetransportemissionsforeachindustryby

summingoverallcountrypairs.Takingthetransportemissionsforeachindustryanddividingby

thevalueoftradeyieldsa(weightedaverage)transportemissionintensityforthatindustry.A

similarprocedureyieldstheaverageoutputemissionsintensity.Addingthesetogetherasin

equation(5)enablesustocalculatetheshareoftransportemissionsintotaltrade‐related

emissionsforeachindustry.Figure2providesthiscomparisonwithindustriessortedfrom

smallesttolargesttransportemissionsshare(dataingrey,scaledisplayedontherightvertical

axis).Forperspectivewealsodisplaytransportemissionsforthatindustryasashareoftotal

transportemissions(datainblue,scaledisplayedontheleftverticalaxis).

Recallthatworldwidetransportisresponsiblefor33percentoftraderelatedemissions.Atthe

industrylevelweseewidedispersioninthesenumbers.Atthelowendarebulkproducts

(agriculture,mining)withsignificantoutputemissions,andwhichtendtobeshippedusingthe

mostefficientmaritimebulkcarriers.Atthehighendaremanufacturedgoods.Over75percentof

thetrade‐relatedemissionsoftransportequipment,electronicequipment,machinery,and

manufacturesnotelsewhereclassifiedcomefromtransportation.

InTable4weprovidesimilarcalculationsforinternationaltransportandoutputemissions

byregionalgroupingsandforselectedcountries(forthefullsampleofcountriesseeAppendix

TableA3).Thefirstthreecolumnsshowthecontributionofeachregiontotrade‐relatedemissions

worldwide,includingemissionsfromindustrialoutputandfrominternationaltransport.Thereare

22

severalnotablepatternshere.First,thereisasignificantdifferencebetweentheoutputshareof

emissionsandthetradeshareofemissions.NorthAmericaandEuropearetogetherresponsible

forjustoverathirdofoutputemissionsbutover60percentoftransportemissions.TheUSaloneis

responsibleforalmostathirdofworldemissionsfromtransportationofexports.Theopposite

patternholdsforChina,whichisresponsiblefor20.8percentofoutputemissions,andonly3.5

percentoftransportemissionsfromexports.Second,formanyregionsthereisalargeimbalance

betweeninternationaltransportemissionsinimportsandexports.TheUSexportemissionsshare

ismuchlargerthanitsimportemissionssharewhilethisimbalanceisreversedfromtheEuropean

andEastAsianperspective.

Tosomeextentthesesharesaredrivenbythesizeofeachregion,relianceontrade,and

tradeimbalances.Toeliminatetheseeffects,intheremainingcolumnswecalculateemission

intensitiesforexportsandimports,measuredingramsofCO2equivalentperdollaroftrade.To

makethenumberscomparable,bothoutputandtransportemissionsarereportedasweighted

averagesofcountryxsectoremissions,wheretheweightsineachcasereflecttradeshares.17

Hereweseelargedifferencesbetweenregionsintheemissionintensitiesofoutputandtransport.

Thereissignificantvariationinoutputintensities,drivenlargelybythecommoditycompositionof

trade.SouthAmerica,OceaniaandtheMiddleEast/Africahaveveryhighoutputemissionsper

dollaroftrade,drivenbytheirrelianceonemissionintensivecommodityproduction.

Manufacturingorientedexportersseemuchsmalleroutputintensities.Perhapsmoresurprising

therearealsoverylargedifferencesinthetransportintensities.ThetransportationofUSexportsis

nearlyeighttimesmoreemissionintensivethanthetransportationofChineseexports,andsix

timesmoreemissionintensivethanEurope.Thisisaconsequenceofanunusuallylargerelianceon

aircargoinUSexports.

17Byusingtradeshares,theimportanceofaparticularsectoristhesameforbothoutputandtransportemissions.Werewetouseoutputsharesforoutput,goodswithalargeshareofoutputbutasmallshareoftradewouldskewtheaverages.

23

Thesenumbersmakeclearthatincludingtransportsignificantlychangesourperspectiveon

whichregionshaveemissionintensivetrade.India’sproductionoftradedgoodshas143percent

moreemissionsthantheUSperdollaroftrade,butafterincorporatingtransportation,itsexports

arelessemissionintensiveintotal.Wealsoseeastrongimbalanceinemissionintensities.East

Asianimportsaremuchmoreemissionintensivethantheexports,whilethereverseistrueforthe

US.

Asignificantadvantageofourapproachtoassessingtransportemissionsisthatitgivesus

theabilitytosortoutwhichregionsareengagedinespeciallyemissionintensivetrade.Aclear

implicationofthesenumbersisthatbothproductionandtransportationemissionsshouldbe

consideredwhenevaluatingpolicychangesdesignedtocurtailemissions.Insomecountriesthe

impactwillbefeltmostacutelyontheproductionside,whereasincountriesliketheUS,themain

effectwillprimarilybeontransport.Similarly,insomeclimatechangemitigationproposals,

internationaltransportemissionsaretobeincludedaspartofacountry’scarbonallocation.The

largedifferencesbetweenimportandexportemissionsshowninTable4suggesttheprecise

mannerinwhichthisisdonecouldbeveryimportant.Thatis,NorthAmericawouldmuchprefer

animportbasedallocationratherthananexportbasedallocation,whileEastAsiancountrieswould

prefertheopposite.

C. ReallocatingProduction:DoesMoreTradeMeanMoreEmissions?

Acentralquestionofthepreviousliteratureontradeandcarbonemissionsisthis:willrisingtrade

leadtohigherorloweremissions?Iftwocountriesengagedintradehavesimilaroutputemission

intensities,thenmoretrademeansmoreinternationaltransportandhigheremissions.However,if

thedifferenceinoutputemissionsislargeenoughtooffsetthetransportemissions,tradecould

loweremissions.

Thisquestionhasbeenpreviouslyaddressedwithcasestudies(Jones,2006;Simsetal.,

2007;Williams,2007)orwithlargelyimputeddata(PetersandHertwich,2008).Wecanuseour

24

datatoaddressitcomprehensively.Tobeginweprovideastraightforwardpartialequilibrium

calculation.Welookatallpossiblereallocationsofproductioninwhichacountryreducesdomestic

productionofasectorandimportsthesamevalueofthegoodfromabroad.Denotingtheexporter

ororiginas“o”,thedestinationcountryas“d”,andthegood“g”,wecancalculatethechangein

emissionsassociatedwithconsumingthegoodas

(6) eodgc (edg

Y eogY ) eodg

T

Wewillconsiderallpossiblereallocationsoverallcountrypairs,whichmeansthatthefirsttermin

bracketswillbesymmetricallydistributedaroundzero.(Forexample,therearetwoobservations

fortheUSandChinatradingelectronics,oneinwhichtheUSistheorigin,andanotherinwhich

Chinaistheorigin.)Thequestioncanthenbeframedas:isthevariationinoutputemissionslarge

orsmallrelativetotransportemissions,andwhatfractionofreallocationscouldreduceemissions

despiteincorporatingtransport?

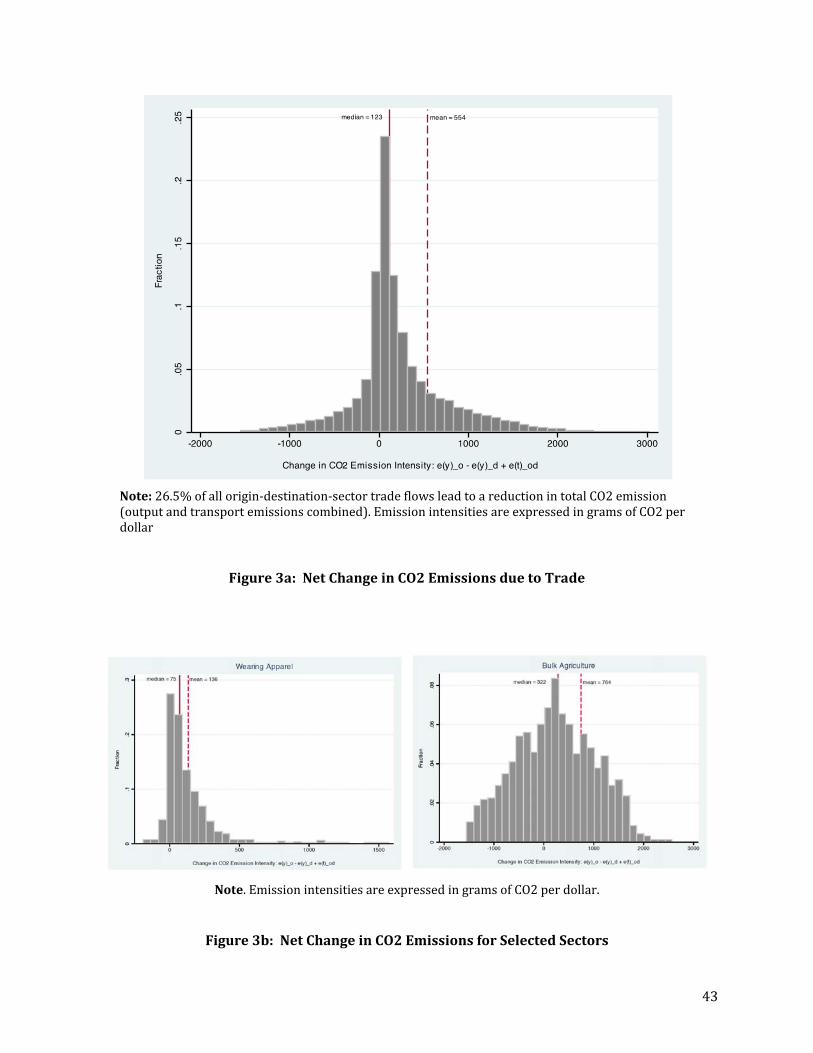

InFigure3aweprovideahistogramof29,300productionreallocations,withunitsingrams

ofCO2perdollartraded.18Themedianreallocationfromtradeincreasesemissionsby123grams

perdollartraded,whilethemeanreallocationincreasesemissionsby554grams.Negative

observationsrepresentareductioninemissionsfromtrade;26.5%ofallpossiblereallocations

reduceemissions,andthesetradepairsaccountforabout31percentofworldtradebyvaluein

2004.

Tounderstandthemechanicsofthisreallocationbetter,weprovideasimilardistribution

fortwoillustrativesectors:wearingapparelandbulkagriculture.Forwearingapparel,thereare

quitesmalldifferencesacrosscountriesinoutputemissions.Thismeansthatrisingtradeacts

primarilytoincreaseemissionsfromtransport.Only15.8%ofproductionreallocationsreduce

emissions,andtheaggregatechangesinemissionsfromtradearequitesmall(mean136).In

contrast,therearelargedifferencesacrosscountriesinoutputemissionsfrombulkagriculture,and

18Wedropthetopandbottom5%ofvaluestoeliminateoutliersthatdistortthehistogram.

25

aswenotedinFigure2,transportisasmallshareoftrade‐relatedemissions.Inthiscase,41.6

percentofproductionreallocationsreduceemissions,andtheaggregatechangeinemissionsfrom

tradeisverylarge(mean764grams).

Table5providesdataforeachcountryandproducingsectorincludingthefractionoftrade

reallocationsthatareGHGemissionreducing,andtheaveragechangeinemissionsfromtrade.

Highincomecountriestendtohavelowoutputemissionsandintensivelyuseairplanesintrade,

andhere,fewtradeexchangesareCO2reducing.Lowincomecountrieshavehighoutputemissions

andintensivelyusemaritimetransport.Here,morethanhalfoftradereallocationsareemission

reducing.

ThesecalculationsaremechanicallyfocusedonlyonGHGemissions,anddonotaddress

whetheranyparticulartradeflowislikelytotakeplace.Assuchtheyaremeanttobeillustrativeof

thecapacityofthetradingsystemtoincreaseordecreaseemissions,butnotthefeasibilityofthe

change.Inthenextsectionweconsidergeneralequilibriumshockstothetradingsysteminorder

toanalyzehowlikelyfuturepatternsoftradegrowthwillaffectemissions.

V. TradeGrowthandChangesinInternationalTransportEmissions

Theemissionintensityofindividualtradeflowsvariesdramaticallydependingonwhatproductis

beingtraded,whichcountriesaretrading,andhowtheyaretransportingit.Asaconsequence,

tradegrowththatalsochangesthecompositionoftradecanresultinpronounceddifferencesin

trade‐relatedemissions.

InthissectionwewilluseaCGEsimulationtogeneratechangesinthevalueand

compositionoftraderesultingfromtariffliberalizationandGDPgrowth.Combiningthiswithour

scalevs.intensitydecompositionwecancalculatetheeffectofgrowingtradeonemissionsgrowth.

Fixingtheemissionintensityofaparticularoutputsectoro‐g,thegrowthinoutputrelated

emissionsis:

26

(7)

Fixingtheemissionintensityofaparticularo‐d‐gtradeflow,thegrowthoftrade‐relatedemissions

isthen

(8)

Thisexerciseholdsfixedthemodalsharesforeacho‐d‐gflow,andtheemissionintensityofeach

mode.Putanotherway,thisexercisetakesthetransportationsystemasgivenandexamineshow

changesintradeaffectthegreenhousegasemissionsfrominternationaloutputandtransport.We

donotmodelhowchangesinfuelprices,spurredeitherbyrisingdemandforfuelorchangesin

carbon/fueltaxes,affectmode‐specificprices.Nordoweexplicitlyexamineendogenous

technologicalchangeintransportation,althoughwedoexploresensitivityofourresultsto

assumptionsonthefuelandemissionintensityofairtransport.Onecanimagineanadditional

exercise,motivatedbyandmadepossiblebythedataconstructedinthispaper,focusedonthe

effectofcarbontaxationonfuelpricesandthereforemodalchoice,andhowthatwouldfeedback

intochangesintradepatterns.Weleavethisconsiderablymoreinvolvedexerciseforfuturework.

Ourapproachoffixingmodalsharesforeacho‐d‐gflowyieldsareasonableapproximationof

aggregatechangesinmodaluseandemissionsintwocases.One,iftariffliberalizationorGDP

growthdoesnotgeneratelargechangesinrelativetransportationprices(e.g.thepriceofair

relativetooceanshipping),thenwewouldnotexpectmodalshareswithinano‐d‐gflowtochange

much.Thiswouldbethecaseiftherearefewaggregatechangesinmodaluse,oriftradegrowth

doesnotaffectinputcostsdifferentiallyacrossmodes.Two,supposethatmodalusevaries

primarilyacross(ratherthanwithin)o‐d‐gflowsduetoimmutablegeography,infrastructure,and

productcharacteristics.Forexample,land‐adjacentcountrieswillcontinuetomovegoodsviaroad

andrailindependentofoceanshippingpriceswhilecountriesseparatedbyanoceanwillbeunable

touseroadandrail.Similarly,productweightwillforcegrainontobulkcargocarriersregardless

*Y Yog og ogE Y e

*T Todg odg odgE VAL e

27

ofthepriceofaircargo.Inthesecases,smallchangesovertimeinmodalusewithineacho‐d‐gflow

willbeswampedbychangesinthetradesharesofflowsthatuseonemodemorethananother.19

A. SimulatedTradeGrowth

Wewishtosimulatethechangesinworldwideoutputandtrade( and inequations(7)

and(8)respectively)associatedwithvarioustariffliberalizationandoutputgrowthscenarios,

whichrequirestheuseofacomputablegeneralequilibrium(CGE)modeloftrade.Weemploy

version7oftheGTAPmodel,aggregatingthemodelto40regionsand23tradedand6non‐traded

goods.AhighlydetaileddescriptionofthiswidelyusedmodelcanbefoundinHertelandTsigas

(1997).Webrieflysummarizekeycharacteristicshere.

Withineachsectorfirmsareconstantreturnstoscalewithaproductionstructurethatis

Leontiefinfactorinputs(labor,capital,andland)andintermediateinputsincludingenergy

commodities.SubstitutionbetweenfactorinputsisgovernedbyaCESstructure,asissubstitution

betweenintermediateinputsthatareArmingtondifferentiatedbyorigin.Ontheconsumptionside,

householdshaveCobb‐Douglaspreferencesoverconsumption,governmentspendingandsaving.

DemandsoverconsumptiongoodsemployaCDE(constantdifferenceofelasticities)form,and

householdsregardtheoutputofeachsourcecountryasArmingtondifferentiated.

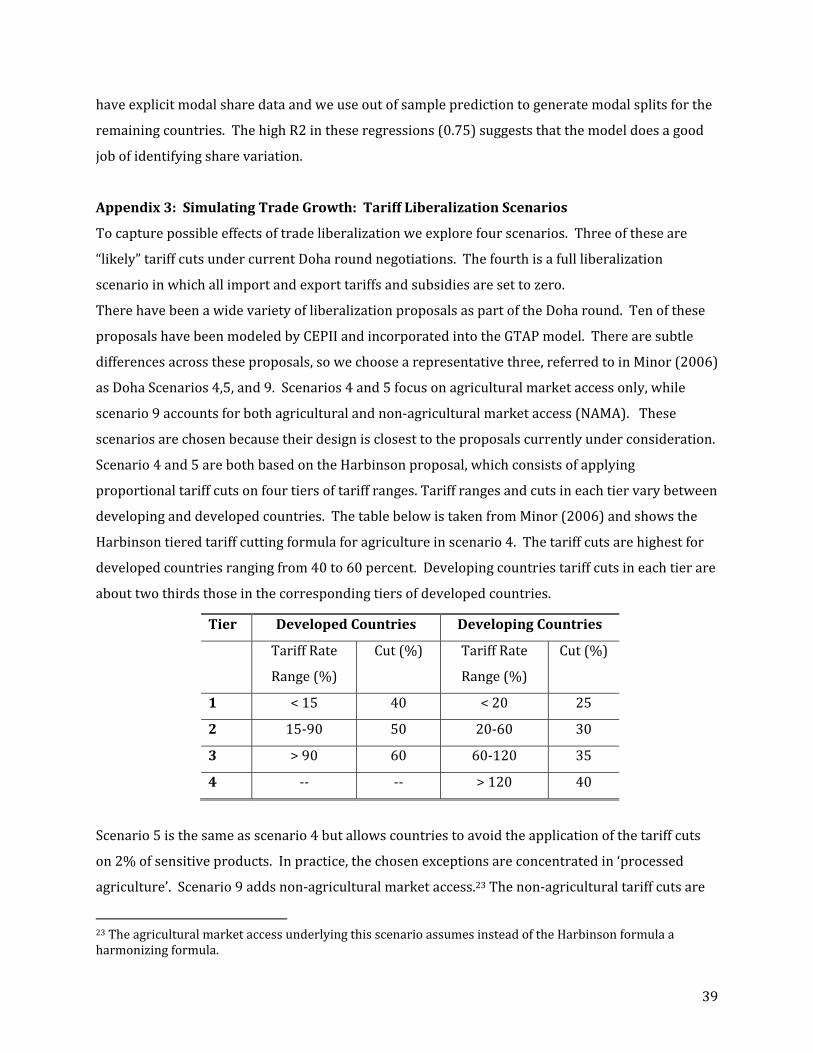

Tocapturepossibleeffectsoftradeliberalizationweexplorefourscenarios.Therehave

beenawidevarietyofliberalizationproposalsaspartoftheDoharoundoftheWTOtalks.We

choosearepresentativethree,referredtoinMinor(2006)asDohaScenarios4,5,and9,because

theirdesignisclosesttotheproposalscurrentlyunderconsideration.Appendix3containsdetailed

notesonthesescenarios.Insummary,scenarios4and5focusonagriculturalmarketaccessonly

withtariffcutsfordevelopedcountriesrangingfrom40to60percent,andthosefordeveloping

countriesbeingonethirdsmaller.Scenario9accountsforbothagriculturalandnon‐agricultural

marketaccess(NAMA),andherenon‐agriculturaltariffsarecutprogressively,i.e.peaktariffsare 19Wealsoholdfixedthewvratiooftradeforagivenflow,assumingthatsmallchangesovertimeinwvwithinano‐d‐gflowwillbeswampedbychangesinthetradesharesoflightversusheavyflows.

ogY odgVAL

28

cutmorethanlowertariffs.Inafinal“fullliberalization”scenario,allimportandexporttariffsand

subsidiesaresettozero.

Tariffliberalizationmayleadtomodestincreasesintrade,butrisingoutputislikelytolead

tomuchmorerapidtradegrowth.Moreover,outputgrowthislikelytobeasymmetricwithsome

developingcountriessuchasChinaandIndiagrowingmuchfasterthandevelopedcountries.To

experimentwithoutputgrowthweuseaspecializedversionoftheGTAPmodelcalledGDyn(or

DynamicGTAP).ThisversionofthemodelcontainsdetailedprojectionsofGDPandfactor

endowmentgrowthratesfrom2004‐2020foreachcountryinthedatabase(Walmsley2006).20

ThismodeltakesbothrealGDPgrowthandfactorinputgrowthasexogenous(valuesshownin

AppendixTableA4),andallowsaHicksneutraltechnologicalchangevariabletoreconcilethese

changeswithothermodelvalues.

Thissimulationallowsustoexaminetwokeypoints.First,predictedGDPgrowthrates

varywidelyacrosscountries,withespeciallyrapidgrowthinChinaandIndia,andslowergrowthin

developedEuropeaneconomies.Second,thisgrowthoccursthroughunevenratesoffactor

accumulation,withsomecountriesrapidlyaccumulatingcapitalandskilledlaborwhileotherssee

relativelyrapidgrowthinunskilledlabor.Thisallowsustomodelchangesinboththescaleofeach

economyandincomparativeadvantagearisingfromchangingfactorsupplies.

B. Results

Table6summarizesthechangesinoutput,exports,modaluse(byvalueandbyKG‐KM),andCO2

emissionsundereachofthefivescenarios.Changesinoutputvalue,outputemissions,andexport

valuescomedirectlyfromtheGTAPmodel.Combiningthesewithourdataontradeweight/value

20Walmsley2006inturnbuildsGDPandinputgrowthestimatesbasedonGlobalEconomicProspects2005,AhujaandFilmer1995,andCPB1999.GDynexplicitlymodelsthedynamicsofcapitalaccumulation,whichmakesiteasierforthemodelertohitagivenGDPgrowthtarget.Itallowsforinternationalcapitalmobilitysothatclosingthemodelrequiresustoallowinvestmenttovaryendogenouslyinonecountry(wechoseSouthAfrica,givenitsrelativeunimportanceforthemajorissuesathand).TheresultwasanunrealisticallyhighrateofcapitalaccumulationinSouthAfrica.Howeverallresultsarerobusttoincluding/excludingSouthAfrica,exceptforthoseinTable7.

29

anddistancewecalculatechangesinexportsbyweightandbytransportationservices.Combining

changesintransportationserviceswithdataonmodaluseandemissionswecalculatechangesin

modaluseandemissions.Forrobustnesswecalculatechangesintransportintensityassuming

bothaHIGHemissionsscenario(aviationemissionsmatchingtheUScargofleet),andaLOW

emissionsscenario(aviationemissionscorrespondingtothemostefficientlongrangeplanes,and

matching2004totalemissionvaluesfromtheITF).

ThethreeDohascenariosarelargelyuninterestingfromatransportandemissions

perspective.Simply,theseliberalizationeffortsaresomodestthattheyyieldlittlegrowthintrade,

intransport,orinemissions.Themostfar‐reachingscenarioyieldsa1.1percentincreaseintrade

(byvalueorKG‐KM),andaslightlyhigher(1.7‐2.1percent)riseintransportemissions.

Thefullliberalizationscenarioeliminatesallimportandexporttariffs.Whilethisisnotcurrently

onthenegotiatingagenda,itisaninterestingexercisebecauseitrevealsanimportantintersection

betweenthestructureofprotectionandemissions.Tariffratesarenotsetuniformlyacrosstrading

partnersandsignificantpreferencesaregiventopartnerswithintradingblocssuchastheEUand

NAFTA.Becausetradingblocstendtobegeographicallyconcentrated,tariffsarelowerformore

proximatepartnersandespeciallyforland‐adjacentpartners.Inourbaseyear,thetrade‐weighted

averagetariffrateforland‐adjacentpartnersis1percent,whiletheaveragetarifffornon‐adjacent

partnersis5.5percent.Thisisanimportantphenomenonfromatransportationperspective

becauserailandroadtransportdominateinternationaltradebetweenland‐adjacentcountries.

Tariffliberalizationthatremovestariffpreferencesforland‐adjacentcountrieswillthenshifttrade

towarddistantpartnersandawayfromroadandrailtransport.

Theseeffectsshowupclearlyinourresults.InTable6weseethatfullliberalization

increasestradeby6percent,concentratedinthoseproducts(agriculture,textilesandwearing

apparel)thataresubjecttothehighestratesofprotection.21Internationaltransportemissionsrise

21Thesmallnegativeeffectonoutputvalueisduetotermsoftradeeffects.Realquantitiesoftraderise.

30

fasterthantrade,dueinparttoariseintradeatadistanceandinparttoanexpansionofemission

intensiveaircargo.AsweseeinTable6,railandroadusageshrinkssubstantiallywhile

internationalaviationandmaritimetransportgrowquickly.

Incontrasttothetariffliberalizationsimulations,theGDPgrowthscenarioyieldsprofoundchanges

inoutput,trade,andgreenhouse‐gasemissions.Outputandtradevaluerisesatsimilarrates,

accumulatingto75‐80percentgrowthoverthisperiod.Trademeasuredbytransportservices(KG‐

KM)risesmuchfaster,6.5percentperannum,accumulatingto173percentgrowth.Not

surprisinglythen,transportemissionsrisefasterthanoutputandtradebyvalue,andfasterthan

outputemissions.

Tounderstandthis,notethattariffliberalizationcreatedtradegrowthbiasedtowardlong

distancetradebecauseoftheerosionofproximity‐basedtariffpreferences.TheGDPgrowth

experimentcreatestradegrowthbiasedtowardlongdistancetradebecausethefastestgrowing

countries(China,India)arefarawayfromotherlargemarkets.Aswithtariffliberalizationthereis

fastergrowthinairandseatransportrelativetorailandroadtransport.

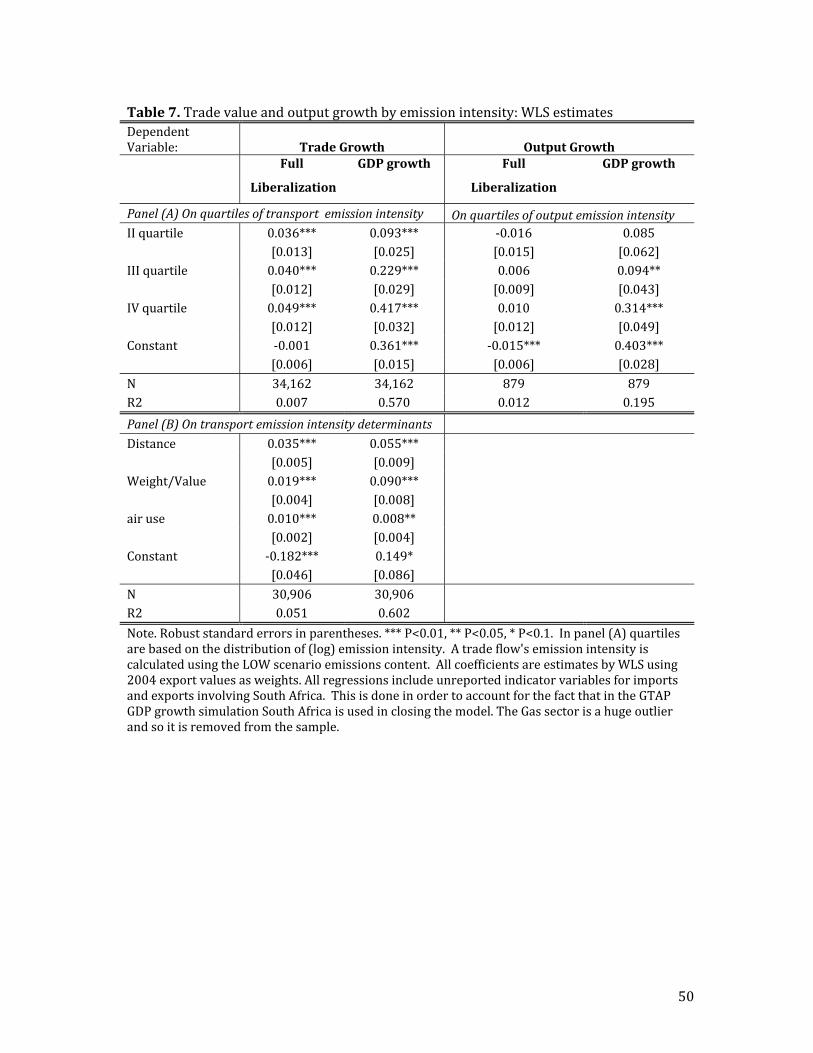

Theseaggregatednumbershideawealthofinterestingvariationwewishtoexplore.Recalling

equation(8),weask:whatistherelationshipbetweentransportemissionintensityinthebase

year,andthesubsequentgrowthintrade?InthetopleftpanelofTable7wegroup30,906o‐d‐g

tradeflowsintoquartilesusingtransportemissionintensity,andassigneacho‐d‐gobservationa

quartiledummyvariable.22Wethenregresstradegrowth(byo‐d‐g)onemissionsquartileswith

theconstantrepresentinggrowthinthelowestemissionquartile.Inboththefullliberalizationand

GDPgrowthscenarios,thehigherthetransportemissionintensityofthetradeflowthefastertrade

grew.ThiseffectwasconsiderablystrongerintheGDPgrowthscenario,bothinthesizeofthe

coefficientsandintheregressionR‐squared.Inthebottomleftpanelweexaminecorrelatesof

22WealsoomittheGASsectorandincorporatefixedeffectsforSouthAfrica.GASisanoutlierthatskewsresultsbadlybecauseitsweight/valueratioandtransportmodalusearepoorlymeasured.FortechnicalreasonsnotedaboveSouthAfricaistreateddifferentlyinthemodelclosure,whichresultsinunrealisticmeasuresofcapitalgrowth.

31

transportemissionintensities.Tradegrowthinbothscenariosisfastestfortradeflowsthatoccur

overlongerdistances,anduseahighershareofaircargo,andinproductswithhigherweight/value

ratios.

ThetoprightpanelofTable7performsasimilarexerciseonoutputemissions.Foreachof

879origin‐productswegroupproductionintoquartilesbasedonoutputemissionintensities,and

regressoutputgrowthonthesequartiles.Fullliberalizationhasverylittleeffectinreorienting

outputgrowthtowardmoreorlessemissionintensiveproduction.However,GDPgrowthorients

outputgrowthtowardthosecountriesandproductswithhighoutputemissions.Thisisprimarily

theeffectofrapidGDPgrowthinChinaandIndia.Becausetheiroutputismoreemissionintensive

(inthefourthquartileofintensities),morerapidGDPgrowthinthosecountrieswillpushoverall

emissionshigher.

VI. ConclusionsandImplications

Mostoftheworkontradeandclimatechangehasignoredinternationaltransportation,or

considereditinthecontextofcasestudies.Thisneglectisdueinparttoalackofdata,andinpart

tothebeliefthatinternationaltransportationrepresentsasmallportionofoverallemissions.

Inthispaperwecombineddataontrade,transportationmodes,transportemissions,andoutput

emissionstocalculatethecontributionoftransportationtotrade‐relatedgreenhousegasemissions

intheaggregateandforalltradeflowsworld‐wide.Whileinternationaltransportationisasmall

fractionofoverallemissionsitisasurprisinglylargefractionoftrade‐relatedemissions.Two‐

thirdsoftrade‐relatedemissionsinUSexportsareduetointernationaltransportation,andworld‐

wideover75percentofthetrade‐relatedemissionsoftransportequipment,electronicequipment,

machinery,andmanufacturesneccomefromtransportation.

Weusedourdatatosystematicallyevaluatewhetherincreasingtradecouldbeemission

reducing.Ifacountryhasveryhighoutputemissions,andtransportsgoodsefficiently,importing

32

thegoodfromalowemissionproducercanreduceemissions.Wefindthatinonequarterof

possibleproductionreallocations,tradecanreduceemissions.Emissionreducingtradesaremore

likelytooccurinagricultureandminingsectorswhilereducingemissionsthroughtrading

manufacturesisrelativelydifficult.

Thesereallocationsaresimplepartialequilibriumchangesanddonotaddresswhether

suchareallocationwouldbefeasibleorlikely.Toexaminelikelychangeswecombinedourdata

withaseriesoftradegrowthsimulationsdesignedtoilluminatetheroleoftariffliberalizationand

GDPgrowth.Tariffliberalizationundoestariffpreferencesthatfavorproximateandland‐adjacent

partnerswhouserailandroadtransportandmovegoodsshortdistances.Thisresultsinashiftin

tradetowarddistantpartners,amoreintensiveuseofaircargo,andtransportemissionsgrowth

thatismorerapidthantradegrowth.Theshareoftransportintrade‐relatedemissionsrises,

reversingadownwardtrendcreatedbypreferentialtradeagreements.However,thesechangesare

smallrelativetothosecausedbyGDPgrowthinChinaandIndia.Weprojecttransportemissions

risingat5percentayearaseconomicgrowthinthesecountriessignificantlyincreasesthedistance

oftrade.

Aclearimplicationofourcalculationsisthatproductionandtransportationemissions

shouldbeconsideredwhenevaluatingpolicychangesdesignedtocurtailemissions.Many

exportersandproductsthatlookrelatively“clean”whenwefocusonlyonoutputemissionsarein

factheavyemittersonceincorporatingtransportation.Insomecountriestheimpactofmitigation

willbefeltmostacutelyontheproductionside,whereasincountriesliketheUS,themaineffect

willprimarilybeontransport.

Therearealsosignificantimplicationsformechanismdesign,specifically,howtotreatthe

internationaltransportsectorwithintheglobalframeworkforemissions.Doesinternational

transport“belong”totheexporter,totheimporter,orshoulditbetreatedasaseparatelycapped

sector,inessenceacountryuntoitself?GiventheimbalanceintransportemissionstheUSwould

33

muchpreferanimportbasedallocationratherthananexportbasedallocation,whileEastAsian

countrieswouldprefertheopposite.Weretransporttreatedasaseparatelycapped“country”the

higherrateoftransportservicesgrowth(andthedifferencesingrowthratesacrossmodes)would

yieldpotentiallylargedistortionaryeffectsontradeascapsbindfasterontransportthanonoutput.

Finally,ourtradeandemissionsgrowthcalculationstakethetransportsectorasgivenandassuch

abstractfromimportantsubstitutionmargins.Weassumeawaychangesinmodalusagewithina

particulartradeflowovertime,anddonotallowfortechnologicalchangeinemissionintensities

dueeithertoinnovationortoupdatingthevintageofthetransportationfleetcapitalstock.

Includingtheseadditionalmarginsofresponseisbeyondthescopeofthecurrentstudy,butin

futureworkthiscouldbeusefulforunderstandinginteractionsbetweentrade,transportationand

emissions.Inparticular,themuchhigherfuelintensityofaircargo,anditsassociatedCO2

emissions,suggeststhatclimatemitigationpoliciescouldhavepronouncedeffectsonhowgoods

moveandthekindsofgoodsthatnationstrade.Thisisespeciallyimportantforcountrieslikethe

US,whoserelianceonaircargoresultsinunusuallyhightransportationemissions.

References

AircraftEconomics,1999.FreighterCostComparisons.AircraftEconomics,45,50‐56.

Ahuja,V.andFilmer,D.,1995.“EducationalAttainmentinDevelopingCountries;NewEstimatesandprojectionsDisaggregatedbyGender,”WorldBankPolicyResearchWorkingPaper1489.

Babiker,M.,2005.ClimateChangePolicy,MarketStructureandCarbonLeakage.JournalofInternationalEconomics,65(2),421‐445.

Berthelon,M.,andFreund,C.,2008.“OntheConservationofDistanceinInternationalTrade”.

JournalofInternationalEconomics,75,310‐20.

Cadarso,M.‐A.,Lopez,L.‐A.,Gomez,N.,Tobarra,M.‐A.,2010.CO2EmissionsofInternationalFreightTransportandOffshoring:MeasurementandAllocation.EcologicalEconomics69,1682‐1694.

CaliforniaClimateChange2006.ComparingEnergyOptions.

Canals,L.M.,Cowell,S.J.,Sims,S.andBesson,L.,2007.ComparingDomesticversusImported

34

Apples:AfocusonEnergyUse.EnvironmentalScienceandPollutionResearch,14(5),

338‐344.

Carlsson‐Kanyama,A.,PippingEkstrom,M.andShanahan,H.,2003.Foodandlifecycleenergy

inputs:consequencesofdietandwaystoincreaseefficiency.EcologicalEconomics,44,

293‐307.

Copeland,B.R.andTaylor,M.S.,2004.Trade,Growth,andtheEnvironment.JournalofEconomicLiterature42(1),7‐71.

CPB,1999.“WorldScan:theCoreVersion,”CPBNetherlandsBureauforEconomicPolicyAnalysis.

De,Prabir,2007.FacilitatingOverlandTradeinSouthAsia.mimeo.

Disdier,A.C.andHead,K.,2008.“ThePuzzlingPersistenceoftheDistanceEffectonBilateral

Trade”.TheReviewofEconomicsandStatistics,90(1),37‐41.

Ederington,J.andMinier,J.,2003.Isenvironmentalpolicyasecondarytradebarrier?Anempiricalanalysis.CanadianJournalofEconomics,36(1),137‐155.

EEA.2007.“EMEP/CORINAIREmissionInventoryGuidebook”,Group8.

Giannouli,M.,andMellios,G.,2005.OverallEnergyEfficiencyandspecificCO2emissionsforpassengerandfreighttransport.EuropeanEnvironmentalAgency,TERM200527EEA32.

Grether,J.‐M.,Mathys,N.A.,deMelo,J.,2010.GlobalManufacturingSO2Emissions:DoesTradeMatter?.ReviewofWorldEconomics145(4),713‐729.

Hertel,T.andTsigas,M.,1997.TheStructureofGTAP.GTAPWorkingPaper413.

Hummels,D.L.,2009.“GlobalizationandTransportCosts”.StudyPreparedforOECDInternationalTransportationForumMeetings.

Hummels,D.L.andSchaurG.,2011.“TimeasaTradeBarrier”.Mimeo.

InternationalTransportForum,2010.TransportGreenhouseGasEmissions2010.ITF/OECD.

InternationalEnergyAgency,2010.Co2EmissionsfromFuelCombustion2010.IEA/OECD.

IPCC/OECD/IEA.1997.Revised1996IPCCGuidelinesforNationalGreenhouseGasInventories.Paris:IntergovernmentalPanelonClimateChange(IPCC),OrganizationforEconomicCo‐operationandDevelopment(OECD),InternationalEnergyAgency(IEA).

Jones,A.,2006.AlifecycleanalysisofUKsupermarketimportedgreenbeansfromKenya.FreshInsightsNo.4.InternationalInstituteforEnvironmentandDevelopment,London,UnitedKingdom.

Kristensen,H.O.,2006.CargoTransportbySeaandRoad–TechnicalandEnvironmentalFactors.NavalEngineersJournal,118,115‐129.

35

Lee,H.‐L.,2008.TheCombustion‐basedCO2EmissionsDataforGTAPversion7DataBase.GTAPWorkingPaper4470.

Levinson,A.,2009.Technology,InternationalTradeandPollutionfromUSManufacturing.AmericanEconomicReview,99(5),2177‐2192.

Levinson,A.andTaylor,M.,2008.UnmaskingthePollutionHavenEffect.InternationalEconomicReview,49(1),223‐253.

MaerskLine,2007.ConstantCarefortheEnvironment.

MiljøstyrelsenMiljøministeriet(DanishEnvironmentalProtectionAgency,DanishMinistryfortheEnvironment),2003.“GreenhouseGasEmissionsfromInternationalAviationandAllocationOptions”.URL:http://www2.mst.dk/common/Udgivramme/Frame.asp?http://www2.mst.dk/udgiv/publications/2003/87‐7972‐489‐2/html/helepubl_eng.htm.

Minor,P.,2006.ProjectedImpactsoftheDohaDevelopmentRoundonEgypt’sTradeandProduction.GTAPWorkingPaper3363.

NationalTechnicalUniversityofAthensLaboratoryforMaritimeTransport,2008.ShipEmissionsStudy.

Olivier,J.,Peters,J.,1999.Internationalmarineandaviationbunkerfuel:trends,rankingofcountriesandcomparisonwithnationalCO2emissions.RIVMreport773301002.NationalInstituteofPublicHealthandtheEnvironment(RIVM),TheNetherlands.

URL:http://www.rivm.nl/bibliotheek/rapporten/773301002.pdf

Peters,G.P.,Hertwich,E.G.,2008.CO2EmbodiedinInternationalTradewithImplicationsforGlobalClimatePolicy.EnvironmentalScienceandTechnology42(5),1401‐1407.

Rose,S.,Avetisyan,M.andHertel,T.,2010.DevelopmentofthePreliminaryVersion7Non‐CO2GHGEmissionsDataset.GTAPWorkingPaper4618.

Sim,S.,Barry,M.,Clift,R.andCowell,S.,2007.Therelativeimportanceoftransportindetermininganappropriatesustainabilitystrategyforfoodsourcing.Acasestudyoffreshproducesupplychains.InternationalJournalofLifeCycleAssessment,12,422‐431.

TransportationResearchBoard,2009.“GuidebookonPreparingAirportGreenhouseGasEmissionsInventories”.ResearchsponsoredbytheFederalAviationAdministration.

USEPA,2006.GlobalEmissionsofNon‐CO2GreenhouseGases:1990‐2020.UnitedStatesEnvironmentalProtectionAgency(US‐EPA),Washington,D.C.,EPAReport430‐R‐06‐003.

VanVeen‐Groot,D.,Nijkamp,P.,1999.Globalization,transportandtheenvironment:newperspectivesforecologicaleconomics.EcologicalEconomics31,331–346.

Walmsley,T.,2006.ABaselineScenariofortheDynamicGTAPModel.GTAPWorkingPaper2854.

Williams,A.,2007.ComparativestudyofcutrosesfortheBritishmarketproducedinKenyaandtheNetherlands.PrécisReportforWorldFlowers,February.

WorldBank,2005.GlobalEconomicProspects2005.

36

Appendix1:ModelAggregation

RegionAggregation:Webeginwith113constituentcountries/regionsavailableintheGTAP

database,thenaggregateintothe40“regions”listedinbold.Someregionsaresinglecountriesand

othersareaggregationsofthe87constituentcountriesavailableintheGTAPdatabase.

NorthAmerica:(2regions)Canada,UnitedStates

CentralAmerica:(2regions)Mexico,OtherCentralAmericaandCaribbean(CentralAmerica,

RestofFTAA,RestofCaribbean)

SouthAmerica:(4regions)Argentina,Brazil,Chile,RestofSouthAmerica(Colombia,Peru,

Uruguay,Venezuela,RestofAndeanPact,RestofSouthAmerica)

Europe:(18regions)Austria,Belgium‐Luxemburg,Denmark,Finland,France,Germany,

Greece,Ireland,Italy,Netherlands,Portugal,Spain,Sweden,UnitedKingdom,Russia,Restof

EuropeanUnion(Cyprus,CzechRepublic,Estonia,Hungary,Latvia,Lithuania,Malta,Poland,

Slovakia,Slovenia,Bulgaria,Romania),OtherEurope–EFTA(Switzerland,Iceland,Liechtenstein,

Norway),OtherCEEandOtherCIS(Albania,Croatia,Turkey,RestofFormerSovietUnion)