Townsend Mutual Insurance Company

31

Townsend Mutual Insurance Company Financial Statements December 31, 2015

Transcript of Townsend Mutual Insurance Company

Townsend Mutual Insurance Company

Financial Statements

December 31, 2015

Townsend Mutual Insurance CompanyIndex to Financial Statements

December 31, 2015

Page

MANAGEMENT'S RESPONSIBILITY FOR FINANCIAL REPORTING 2

INDEPENDENT AUDITORS' REPORT 3

FINANCIAL STATEMENTS

Statement of Financial Position 4

Statement of Surplus 5

Statement of Income 6

Schedule of General Expenses 7

Statement of Cash Flow 8

Notes to Financial Statements 9 - 30

1

INDEPENDENT AUDITORS' REPORT

To the Members of Townsend Mutual Insurance Company

We have audited the accompanying financial statements of Townsend Mutual Insurance Company, whichcomprise the statement of financial position as at December 31, 2015 and the statements of income,surplus and cash flow for the year then ended, and a summary of significant accounting policies andother explanatory information.

Management's Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these financial statements inaccordance with International Financial Reporting Standards, and for such internal control asmanagement determines is necessary to enable the preparation of financial statements that are free frommaterial misstatement, whether due to fraud or error.

Auditors' Responsibility

Our responsibility is to express an opinion on these financial statements based on our audit. Weconducted our audit in accordance with Canadian generally accepted auditing standards. Thosestandards require that we comply with ethical requirements and plan and perform the audit to obtainreasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures inthe financial statements. The procedures selected depend on the auditors' judgment, including theassessment of the risks of material misstatement of the financial statements, whether due to fraud orerror. In making those risk assessments, the auditor considers internal control relevant to the entity'spreparation and fair presentation of the financial statements in order to design audit procedures that areappropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness ofthe entity's internal control. An audit also includes evaluating the appropriateness of accounting policiesused and the reasonableness of accounting estimates made by management, as well as evaluating theoverall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour audit opinion.

Opinion

In our opinion, the financial statements present fairly, in all material respects, the financial position ofTownsend Mutual Insurance Company as at December 31, 2015 and its financial performance and itscash flow for the year then ended in accordance with International Financial Reporting Standards.

February 24, 2016 Chartered Professional AccountantsSimcoe, Ontario Licensed Public Accountants

3

Townsend Mutual Insurance CompanyStatement of Surplus

Year ended December 31, 2015

2015 2014

Balance - beginning of year $ 9,979,067 $ 9,668,517

Net income (loss) for the year (179,668) 310,550

BALANCE - END OF YEAR $ 9,799,399 $ 9,979,067

See accompanying notes

5

Townsend Mutual Insurance CompanyStatement of Income

Year ended December 31, 2015

2015 2014

UNDERWRITING OPERATIONSGross premiums written $ 9,033,776 $ 7,776,771Deduct: Reinsurance ceded (1,741,526) (1,513,936)

Net premiums written 7,292,250 6,262,835

Deduct: Increase in unearned premiums (689,597) (195,779)

Net premium earned 6,602,653 6,067,056

Service charges Service charges 161,921 111,168Other 9,274 13,626

171,195 124,794

Total underwriting revenue 6,773,848 6,191,850

Direct losses incurredGross claims and adjustment expenses 7,257,157 5,058,967Reinsurer's share of claims and adjustment expenses (2,565,372) (794,968)

4,691,785 4,263,999

Expenses Fees, commissions and other acquisition expenses (Note 15) 1,136,216 1,039,224General expenses (see schedule on page 7) 1,779,387 1,523,169Premium deficiency adjustments (8,040) (2,059)

2,907,563 2,560,334

Underwriting income (loss) (825,500) (632,483)

Investment income (Note 16) 560,832 985,686

Income (loss) before income taxes (264,668) 353,203

Income taxes (Note 17)Current - 56,156Deferred (85,000) (13,503)

(85,000) 42,653

NET INCOME (LOSS) FOR THE YEAR $ (179,668) $ 310,550

See accompanying notes

6

Townsend Mutual Insurance CompanySchedule of General Expenses

Year Ended December 31, 2015

2015 2014

Advertising $ 40,112 $ 41,406Association fees 45,395 43,023Bad debts 8,265 6,400Bank charges and interest 26,835 25,718Computer 179,912 191,129Contracted services - 2,985Directors fees 53,304 53,142Donations 30,428 21,307Inspections and investigations 52,385 46,510Insurance 43,291 47,304Loss prevention rebates and supplies 1,884 1,072Occupancy cost 238,350 159,102Other 13,250 18,679Postage 27,705 29,567Premium tax 18,441 15,710Printing and stationery 35,630 30,892Professional fees 129,075 104,268Recruiting 28,433 -Salaries and benefits 660,833 531,031Scholarships 10,000 10,400Seminars, conventions and meetings 50,251 55,164Statistics and reports 34,197 23,097Telephone 15,290 13,832Vehicle and travel 36,121 51,431

$ 1,779,387 $ 1,523,169

See accompanying notes

7

Townsend Mutual Insurance CompanyStatement of Cash Flow

Year ended December 31, 2015

2015 2014

OPERATING ACTIVITIESNet income (loss) for the year $ (179,668) $ 310,550Items not affecting cash:

Amortization of property and equipment 102,341 51,059Deferred income taxes (85,000) (13,503)Realized gain on sale of investments (158,561) (103,851)Unrealized loss (gain) on investments 23,773 (438,364)

(297,115) (194,109)

Changes in non-cash working capital: Due from policyholders (556,906) (211,041)Due from reinsurer (70,480) (21,220)Reinsurers' share of unearned premiums (38,448) 1,634Prepaid expenses 7,489 25Deferred policy acquisition costs (98,993) (42,739)Reinsurers' share of provision for unpaid claims 352,936 (323,807)Accounts payable 93,196 27,765Due to other insurance companies 61,120 35,393Income taxes payable 16,357 (81,216)Amounts due to Facility Association (32,870) (896)Unearned premiums 735,906 194,145Unearned commission revenue (1,465) (108)Provision for unpaid claims and adjustment expenses 354,660 1,209,367

822,502 787,302

Cash flow from operating activities 525,387 593,193

INVESTING ACTIVITIESPurchase of property and equipment (939,126) (35,738)Purchase of investments (5,639,618) (3,597,153)Proceeds on disposition of investments 5,353,697 3,336,322

Cash flow used by investing activities (1,225,047) (296,569)

INCREASE (DECREASE) IN CASH (699,660) 296,624

Cash - beginning of year 933,489 636,865

CASH - END OF YEAR $ 233,829 $ 933,489

See accompanying notes

8

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

1. NATURE OF BUSINESS

Townsend Mutual Insurance Company is a mutual insurance company and is owned by the memberpolicyholders. The Company was incorporated in 1879 under the laws of Ontario and is subject tothe Insurance Act of Ontario. It is licensed to write property, liability, automobile, hail, boiler andmachinery and certain types of fidelity and accident and sickness insurance in Ontario. TheCompany is located in Waterford, Ontario.

The Company is subject to rate regulation in the automobile business it writes. Before automobileinsurance rates can be changed, a rate filing is prepared as a combined filing for most Ontario FarmMutuals by the Ontario Mutuals Auto Rate Filing Committee. The rate filing must include actuarialjustification for rate increases or decreases. All rate filings are approved or denied by the FinancialServices Commission of Ontario. Rate regulation may affect the automobile revenues that areearned by the Company. The actual impact of rate regulation would depend on the competitiveenvironment at that time.

These financial statements have been authorized for issue by the Board of Directors on February 24,2016.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of presentation

These financial statements have been prepared in accordance with International Financial ReportingStandards (IFRS).

These financial statements were prepared on a historical cost basis except for those financial assetsthat have been measured at fair value. The Company's functional and presentation currency is theCanadian dollar. The financial statements are presented in Canadian dollars.

Insurance contracts

In accordance with IFRS 4, Insurance Contracts, the Company has continued to apply theaccounting policies it applied in accordance with pre-changeover Canadian GAAP. Balances arisingfrom insurance contracts primarily include unearned premiums, provisions for unpaid claims andadjustment expenses, the reinsurers' share of unpaid claims and adjustment expenses, deferredpolicy acquisition expenses, and salvage and subrogation recoverable.

Premiums and unearned premiums

The Company earns premium income over the term of the insurance policy on a pro rata basis. Theportion of the premium related to the unexpired portion of the policy at the end of the fiscal year isreflected in unearned premiums. Premiums receivable are recorded at amounts due less anyrequired provision of doubtful amounts.

Reinsurers' share of unearned premiums

The reinsurers' share of unearned premiums are recognized as an asset using principles consistentwith the Company's method for determining the unearned premium liability.

(continues)

9

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Deferred policy acquisition costs

Acquisition costs are comprised of agents' commissions, premium taxes, and other expenses whichrelate directly to the acquisition of premiums, including salaries for underwriting personnel andinspection fees. These costs are deferred and amortized over the terms of the related policies to theextent that they are considered to be recoverable from unearned premiums, after considering therelated anticipated claims and expenses and investment income.

Provision for unpaid claims and adjustment expenses

Individual loss estimates are provided on each claim reported. In addition, provisions are made foradjustment expenses, changes in reported claims and for claims incurred but not reported, based onpast experience and business in force. The estimates are regularly reviewed and updated, and anyresulting adjustments are included in current income. Claim liabilities are carried on anundiscounted basis.

Liability adequacy test

At each reporting date the Company performs a liability adequacy test on its insurance liabilities lessdeferred policy acquisition expenses to ensure the carrying value is adequate, using currentestimates of future cash flows, taking into account the relevant investment return. If that assessmentshows that the carrying amount of the liabilities is inadequate, any deficiency is recognized as anexpense to the statement of comprehensive income initially by writing off the deferred policyacquisition expense and subsequently by recognizing an additional claims liability for claimsprovisions.

Reinsurers' share of provision for unpaid claims for adjustment expenses

Incurred reinsurance recoveries are recorded as reductions of the claims incurred accounts.Expected reinsurance recoveries on unpaid claims and adjustment expenses are recognized asassets at the same time and using principles consistent with the Company's method for establishingthe related liability. A contingent liability exists with respect to reinsurance ceded which couldbecome a liability of the Company in the event that the reinsurer might be unable to meet itsobligations under the reinsurance agreements.

Fire Mutuals Guarantee Fund

The Company is a member of the Fire Mutuals Guarantee Fund ("the Fund"). The Fund wasestablished to provide payment of outstanding policyholders' claims if a member company becamebankrupt. As a result, the Company may be required to contribute assets to their proportionate sharein meeting this objective.

(continues)

10

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Property and equipment

Property and equipment is initially recorded at cost and subsequently measured at cost lessaccumulated amortization and accumulated impairment losses, with the exception of land which isnot amortized. Amortization is recognized in net income and is provided on a straight-line basis overthe estimated useful life of the assets as follows:

Buildings 35 yearsLeasehold improvements 10 yearsOffice equipment 10 yearsComputer equipment 5 yearsSigns 5 yearsPaving & Sidewalks 10 yearsMotor vehicles 5 years

Amortization methods, useful lives and residual values are reviewed annually and adjusted ifnecessary. Property and equipment acquired during the year are amortized at one-half of the normalrate.

Income taxes

Income tax expense comprises of current and deferred tax. Current and deferred tax are recognizedin net income except to the extent that it relates to a business combination, or items recognizeddirectly in equity or in other comprehensive income.

Current income taxes are recognized for the estimated income taxes payable or receivable ontaxable income or loss for the current year and any adjustment to income taxes payable in respect ofprevious years. Current income taxes are determined using tax rates and tax laws that have beenenacted or substantively enacted by the year-end date.

Deferred tax assets and liabilities are recognized where the carrying amount of an asset or liabilitydiffers from its tax base, except for taxable temporary differences arising on the initial recognition ofgoodwill and temporary differences arising on the initial recognition of an asset or liability in atransaction which is not a business combination and at the time of the transaction affects neitheraccounting or taxable profit or loss.

Recognition of deferred tax assets for unused tax losses, tax credits and deductible temporarydifferences is restricted to those instances where it is probable that future taxable profit will beavailable against which the deferred tax asset can be utilized. Deferred tax assets are reviewed ateach reporting date and are reduced to the extent that it is no longer probable that the related taxbenefit will be realized.

The amount of the deferred tax asset or liability is measured at the amount expected to be recoveredfrom or paid to the taxation authorities. This amount is determined using tax rates and tax laws thathave been enacted or substantively enacted by the year-end date and are expected to apply whenliabilities/(assets) are settled/(recovered).

(continues)

11

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Financial instruments

The Company classifies its financial instruments into one of the following categories based on thecharacteristics of the financial instruments and management's choices and intentions. Alltransactions related to financial instruments are recorded on a trade date basis. The Company'saccounting policy for each category is as follows:

Financial assets at fair value through profit or loss

A financial asset is classified at fair value through profit or loss if it is classified as held-for-trading oris designated as such upon initial recognition. Financial assets are designated as fair value throughprofit or loss of the Company manages such investments and makes purchases and sale decisionsbased on their fair value in accordance with the Company's documented risk management orinvestment strategy. Upon initial recognition, attributable transaction costs are recognized in profit orloss as incurred. Financial assets at fair value through profit or loss are measured at fair value, andchanges therein are recognized in profit or loss.

Loans and receivables

These comprise of amounts due from policyholders, reinsurers', Facility Association andmiscellaneous receivables. These assets are non-derivative financial assets resulting from thedelivery of cash or other assets by a lender to a borrower in return for a promise to repay on aspecified date or dates, or on demand. They are initially recognized at fair value plus transactioncosts that are directly attributable to their acquisition or issue and subsequently carried at amortizedcost, less any impairment losses. Impairments are recognized when there is objective evidence thatthe Company will be unable to collect all of the amounts due under the terms receivable. Onconfirmation that the amounts receivable will not be collectable, the gross carrying value of the assetis written off and the loss is recognized in net income.

Other financial liabilities

Other financial liabilities include all financial liabilities and comprise of accounts payable andamounts due to other insurance companies. These liabilities are initially recognized at fair value netof any transaction costs directly attributable to the issuance of the instrument and subsequentlycarried at amortized cost.

(continues)

12

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (continued)

Standards, amendments and interpretations not yet effective

There are no new standards, interpretations and amendments, effective for the first time fromJanuary 1, 2015 that have had a material effect on the financial statements.

Certain new standards, amendments and interpretations have been published that are mandatory forthe Company's accounting periods beginning on or after January 1, 2016 or later periods that theCompany has decided not to early adopt. The standards, amendments and interpretations that maybe relevant to the Company are:

IFRS 9 Financial Instruments is part of the IASB's wider project to replace IAS 39 'FinancialInstruments: Recognition and Measurement'. IFRS 9 retains but simplifies the mixedmeasurement model and establishes two primary measurement categories for financial assets,amortized cost and fair value. The basis of classification depends on the entity's business modeland the contractual cash flow characteristics of the financial asset. The standard is effective forannual periods beginning on or after January 1, 2018. The Company is in the process ofevaluating the impact of the new standard.

IAS 1 Presentation of Financial Statements is part of a major initiative to improve disclosurerequirements in IFRS financial statements. The amendments clarify the application of materialityto note disclosure and the presentation of line items in the primary statements provide options onthe ordering of financial statements and guidance on the presentation of other comprehensiveincome related to equity accounted investments. The effective date for these amendments isJanuary 1, 2016. The Company is in the process of evaluating the impact of these amendments.

IFRS 15 Revenue from Contracts with Customers is based on the core principles to recognizerevenue to depict the transfer of goods or services to customers in an amount that reflects theconsideration to which the entity expects to be entitled in exchange for those goods or services.IFRS 15 focuses on the transfer of control. IFRS 15 replaces all of the revenue guidance thatpreviously existed in IFRSs. The effective date for IFRS 15 is January 1, 2018. The Company isin the process of evaluating the impact of the new standard.

None of the new standards, interpretations and amendments, which are effective for the Company'saccounting periods beginning after January 1, 2016 and which have not been adopted early, areexpected to have a material effect on the Company's future financial statements.

13

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

3. ACCOUNTING ESTIMATES AND JUDGMENTS

The Company makes estimates and assumptions about the future that affect the reported amountsof assets and other liabilities. Estimates and judgments are continually evaluated and based onhistorical experience and other factors, including expectations of future events that are believed tobe reasonable under the circumstances. In the future, actual experience may differ from theseestimates and assumptions.

The effect of a change in an accounting estimated is recognized prospectively by including it inincome in the period of the change, if the change affects that period only; or in the period of thechange and future periods, if the change affects both.

See notes 13 and 14 Provision for Unpaid Claims and Adjustment Expenses and InsuranceContracts for estimates and assumptions that have a significant risk of causing material adjustmentto the carrying amounts of assets and liabilities within the next financial year.

4. INVESTMENTS

The book and fair values of investments at December 31 are shown as follows:

Book Value Fair Value Book Value Fair Value

Held-for-Trading Bonds issued by:Federal 631,089 631,089 231,206 231,206 Provincial 1,704,763 1,704,763 4,020,314 4,020,314 Corporate 6,923,013 6,923,013 4,878,206 4,878,206

9,258,865 9,258,865 9,129,726 9,129,726

Equity InvestmentsCommon shares 4,009,715 4,009,715 3,769,830 3,769,830 Preferred shares 14,430 14,430 10,221 10,221 Equity pooled funds 596,419 596,419 555,920 555,920

4,620,564 4,620,564 4,335,971 4,335,971

Total investments 13,879,429 13,879,429 13,465,697 13,465,697

The maximum exposure to credit risk would be the fair value as shown above.

$ $2015 2014

14

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

5. DUE FROM REINSURER

The continuity of amounts due from reinsurer are as follows:

2015 2014$ $

Balance, beginning of year 78,828 57,608 Submitted to reinsurer 2,918,309 494,503 Received from reinsurer (2,847,829) (473,283)

Balance, end of year 149,308 78,828

At year-end, the Company reviewed the amounts owing from its reinsurer and determined that noallowance is necessary. All amounts are expected to be received within one year.

6. REINSURERS' SHARE OF UNEARNED PREMIUMS

The continuity of reinsurers' share of unearned premiums are as follows:

2015 2014$ $

Balance, beginning of year 31,932 33,566 Submitted to reinsurer 1,779,974 1,512,302 Premiums earned during the year (1,741,526) (1,513,936)

Balance, end of year 70,380 31,932

7. DEFERRED POLICY ACQUISITION COSTS

The continuity of deferred policy acquisition costs are as follows:

2015 2014$ $

Balance, beginning of year 600,394 557,655 Acquisition costs incurred 1,371,381 1,142,502 Expensed during the year (1,272,388) (1,099,763)

Balance, end of year 699,387 600,394

Deferred policy acquisition costs will be recognized as an expense within one year.

15

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

8. DEFERRED INCOME TAXES

The movement in 2015 deferred tax assets are:

Opening Closing balance at Recognized in balance atJan 1, 2015 net income Dec 31, 2015

$ $ $

Deferred tax assetsProperty and equipment 12,000 4,000 16,000 Losses carried forward - 73,000 73,000 Claims liabilities 53,000 8,000 61,000

65,000 85,000 150,000

The movement in 2014 deferred tax assets are:

Opening Closing balance at Recognized in balance atJan 1, 2014 net income Dec 31, 2014

$ $ $

Deferred tax assetsProperty and equipment 9,504 2,496 12,000 Claims liabilities 41,993 11,007 53,000

51,497 13,503 65,000

The Company has income tax losses of approximately $271,000 which may be carried forward toreduce future year's taxable income. These losses have been recognized in the deferred income taxbenefit on the financial statements. These losses expire in 2035.

16

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

9. PROPERTY AND EQUIPMENT

Leasehold Office Computer Paving & Motor Land Building Improvements Equipment Equipment Signs Sidewalks Vehicles Total

Cost $ $ $ $ $ $ $ $ $Balance on December 31, 2014 180,000 593,086 239,948 104,054 126,742 - - 54,921 1,298,751

Additions - 730,115 - 97,378 3,142 33,082 75,410 - 939,127 Disposals - - - - - - - - -

Balance on December 31, 2015 180,000 1,323,201 239,948 201,432 129,884 33,082 75,410 54,921 2,237,878

Accumulated amortizationBalance on December 31, 2014 - - 194,229 83,606 107,153 - - 27,357 412,345

Amortization expense - 27,376 22,210 25,317 9,376 3,308 3,770 10,985 102,342 Disposals - - - - - - - - -

Balance on December 31, 2015 - 27,376 216,439 108,923 116,529 3,308 3,770 38,342 514,687

Net book value

December 31, 2014 180,000 593,086 45,719 20,448 19,589 - - 27,564 886,406

December 31, 2015 180,000 1,295,825 23,509 92,509 13,355 29,774 71,640 16,579 1,723,191

17

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

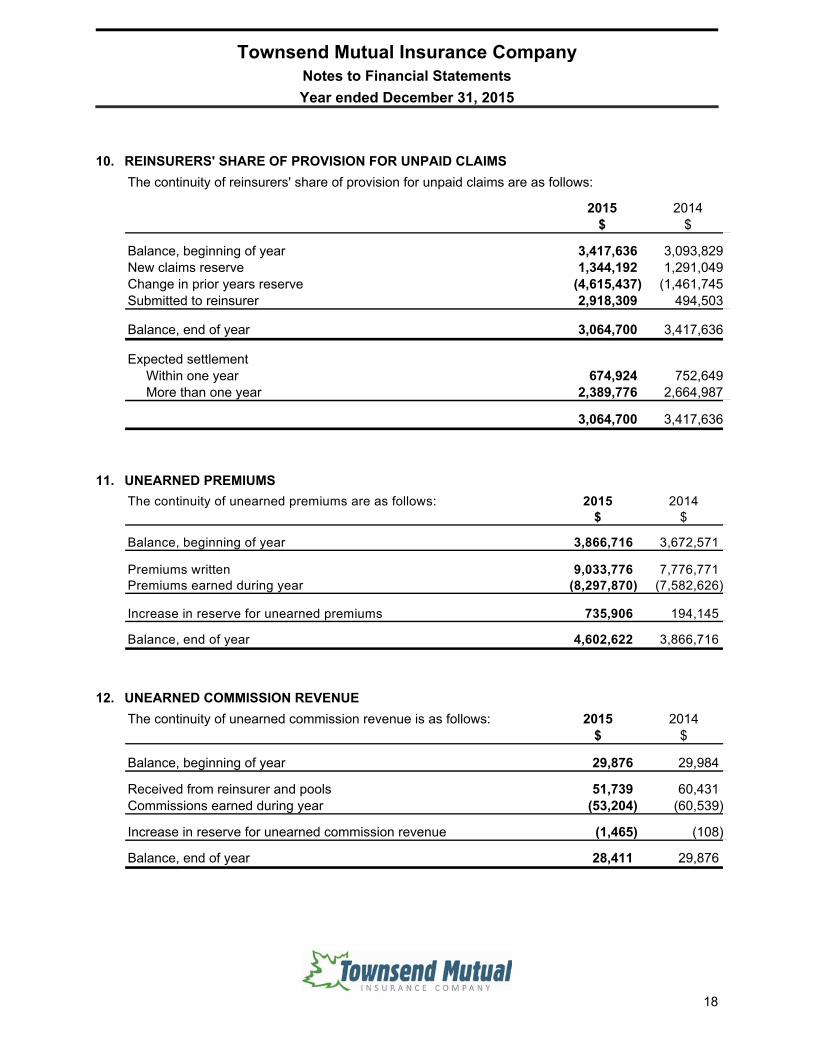

10. REINSURERS' SHARE OF PROVISION FOR UNPAID CLAIMS

The continuity of reinsurers' share of provision for unpaid claims are as follows:

2015 2014$ $

Balance, beginning of year 3,417,636 3,093,829 New claims reserve 1,344,192 1,291,049 Change in prior years reserve (4,615,437) (1,461,745) Submitted to reinsurer 2,918,309 494,503

Balance, end of year 3,064,700 3,417,636

Expected settlement Within one year 674,924 752,649 More than one year 2,389,776 2,664,987

3,064,700 3,417,636

11. UNEARNED PREMIUMS

The continuity of unearned premiums are as follows: 2015 2014$ $

Balance, beginning of year 3,866,716 3,672,571

Premiums written 9,033,776 7,776,771 Premiums earned during year (8,297,870) (7,582,626)

Increase in reserve for unearned premiums 735,906 194,145

Balance, end of year 4,602,622 3,866,716

12. UNEARNED COMMISSION REVENUE

The continuity of unearned commission revenue is as follows: 2015 2014$ $

Balance, beginning of year 29,876 29,984

Received from reinsurer and pools 51,739 60,431 Commissions earned during year (53,204) (60,539)

Increase in reserve for unearned commission revenue (1,465) (108)

Balance, end of year 28,411 29,876

18

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

13. PROVISION FOR UNPAID CLAIMS AND ADJUSTMENT EXPENSES

Changes in claim liabilities recorded in the statement of financial position for the years ended December 31, 2015 and 2014 and their impact on claims and adjustment expenses are as follows:

2015 2014$ $

Balance, beginning of year 7,530,133 6,320,766 New claims reserve 8,348,823 5,779,425 Change in prior years' reserve (1,093,540) (720,585) Paid claims Current year (4,664,940) (2,350,632) Prior year (2,235,683) (1,498,841)

Balance, end of year, gross 7,884,793 7,530,133

Reinsurers' share of provision for unpaid claims (3,064,700) (3,417,636)

Balance, end of year 4,820,093 4,112,497

Expected settlement Within one year 2,437,335 2,327,150 More than one year 5,447,458 5,202,983

7,884,793 7,530,133

The determination of the provision for unpaid claims and adjustment expenses and the relatedreinsurers' share requires the estimation of reinsurance recoveries and future development ofclaims. The provision for unpaid claims and adjustment expenses and related reinsurers' share areestimates subject to variability, and the variability could be material in the near term. The variabilityarises because all events affecting the ultimate settlement of claims have not taken place and maynot take place for some time. Variability can be caused by receipt of additional claim information,changes in judicial interpretation of contracts, or significant changes in severity or frequency ofclaims from historical trends. The estimates are principally based on the Company's historicalexperience. Methods of estimation have been used which the Company believes producereasonable results given current information. The Company must participate in industry automobileresidual pools of business, and recognizes a share of this business based on its automobile marketshare. The Company records its shares of the liabilities provided by the actuaries of the pools.

An actuary is retained by the Company's Board of Directors to review the policy liabilities of theCompany. The actuary's responsibility is to carry out a valuation of the Company's policy liabilities inaccordance with accepted actuarial practices and report thereon to the Company. In performing thevaluation, the actuary makes assumptions as to the future loss ratios, trends, future rates of claimsfrequency and severity, inflation and both internal and external adjustment expenses, taking intoconsideration the circumstances of the Company. The actuary also makes use of the work of theexternal auditor in verifying the underlying data used in the valuation. The actuary's report outlinesthe scope of work performed and recommendation.

(continues)

19

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

13. PROVISION FOR UNPAID CLAIMS AND ADJUSTMENT EXPENSES (continued)

The following is a summary of the insurance contract provisions and related reinsurance assets

Gross Re-Insurance NetDecember 31, 2015 $ $ $

Outstanding claims provision Property 1,841,791 1,185,662 656,129 Automobile 3,764,313 1,098,038 2,666,275 Liability 507,983 - 507,983 Facility Association and other residual pools 643,706 - 643,706 Provisions for claims incurred but not reported 1,127,000 781,000 346,000

Balance, end of year 7,884,793 3,064,700 4,820,093

Gross Re-Insurance NetDecember 31, 2014 $ $ $

Outstanding claims provision Property 2,145,470 1,088,101 1,057,369 Automobile 2,678,485 1,223,484 1,455,001 Liability 838,180 319,051 519,129 Facility Association and other residual pools 761,998 - 761,998 Provisions for claims incurred but not reported 1,106,000 787,000 319,000

Balance, end of year 7,530,133 3,417,636 4,112,497

14. INSURANCE CONTRACTS

Claim Development

The estimation of claim development involves assessing the future behaviour of claims, taking intoconsideration the consistency of the Company's claim handling procedures, the amount ofinformation available, the characteristics of the line of business from which the claim arises andhistorical delays in reporting claims. In general, the longer the term required for the settlement of agroup of claims the more variable the estimates. Short settlement term claims are those which areexpected to be substantially paid within a year of being reported.

The tables that follow present the development of claims payments and the estimated ultimate costof claims for the claim years 2007 to 2015. The upper half of the tables shows the cumulativeamounts paid or estimated to be paid during successive years related to each claim year. Theoriginal estimates will be increased or decreased, as more information becomes known about theoriginal claims and overall claim frequency and severity.

In 2011, the year of adoption of IFRS, only information from periods beginning on or after January 1,2007 is required to be disclosed. This is being increased in each succeeding additional year, untilten years of information is included.

20

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

14. Insurance Contracts (continued)

Gross claims

2007 2008 2009 2010 2011 2012 2013 2014 2015 Total

$ $ $ $ $ $ $ $ $ $

Gross estimate of cumulative

claims cost

End of year claim 3,620,324 6,011,118 7,770,472 5,015,330 5,082,931 4,779,163 4,133,796 5,810,242 8,348,823

One year later 3,908,785 4,243,667 7,029,913 3,616,237 4,824,576 3,922,888 3,729,340 5,199,094

Two years later 3,526,318 3,976,544 5,554,017 3,042,102 4,440,105 4,143,224 3,988,292

Three years later 3,739,734 3,495,198 4,989,480 2,728,624 4,225,891 3,696,198

Four years later 3,287,850 3,221,627 4,265,903 2,680,956 3,983,562

Five years later 3,012,328 3,252,446 4,299,168 2,778,330

Six years later 2,921,153 3,146,536 4,176,899

Seven years later 2,894,941 3,129,606

Eight years later 2,889,941

Current estimate of cumulative

claims cost 2,889,941 3,129,606 4,176,899 2,778,330 3,983,562 3,696,198 3,988,292 5,199,094 8,348,822 38,190,744

Cumulative payments 2,886,941 3,111,336 4,124,703 2,575,321 3,600,350 3,269,820 2,858,314 3,969,487 4,664,940 31,061,212

Outstanding claims 3,000 18,270 52,196 203,009 383,212 426,378 1,129,978 1,229,607 3,683,882 7,129,532

Outstanding claims 2006 and prior 755,261

Total gross outstanding claims 7,884,793

21

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

14. Insurance Contracts (continued )

Net claims after reinsurance

2007 2008 2009 2010 2011 2012 2013 2014 2015 Total

$ $ $ $ $ $ $ $ $ $

Net estimate of cumulative

claims cost

End of year claim 2,696,242 3,322,023 3,045,066 1,746,713 2,687,310 2,152,088 3,616,021 4,519,192 4,948,979

One year later 2,842,880 2,817,912 2,729,811 1,522,745 2,908,070 2,169,393 3,342,042 4,258,289

Two years later 2,458,951 2,719,360 2,510,890 1,390,625 2,603,233 2,376,384 3,516,979

Three years later 2,504,680 2,583,338 2,390,404 1,377,582 2,525,511 2,189,572

Four years later 2,288,294 2,458,915 2,320,389 1,338,466 2,477,493

Five years later 2,262,010 2,492,700 2,369,654 1,415,501

Six years later 2,209,835 2,449,052 2,306,385

Seven years later 2,192,725 2,440,122

Eight years later 2,192,725

Current estimate of cumulative

claims cost 2,192,725 2,440,122 2,306,385 1,415,501 2,477,493 2,189,572 3,516,979 4,258,289 4,948,979 25,746,045

Cumulative payments 2,192,725 2,430,852 2,291,189 1,292,118 2,258,004 1,929,139 2,693,255 3,336,211 2,609,288 21,032,781

Outstanding claims - 9,270 15,196 123,383 219,489 260,433 823,724 922,078 2,339,691 4,713,264

Outstanding claims 2006 and prior 106,829

Total net outstanding claims 4,820,093

22

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

15. FEES, COMMISSIONS AND OTHER ACQUISITION EXPENSES

2015 2014

Agent commissions and benefits $ 657,424 $ 721,390Brokers commissions 327,927 215,772Commission paid to pools 35,443 49,698Sales salaries 169,933 111,668Commission revenue (54,511) (59,304)

$ 1,136,216 $ 1,039,224

16. INVESTMENT INCOME

Investment income was derived from the following:

2015 2014

Interest income $ 423,789 $ 454,363Dividend income 63,430 49,400Gain on sale of investments 158,561 103,851Market value adjustments (23,773) 438,364Investment fees (61,175) (60,292)

$ 560,832 $ 985,686

23

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

17. INCOME TAXES

Reasons for the difference between tax expense for the year and the expected income taxes basedon the statutory tax rate of 26.5% are as follows:

2015 2014$ $

Income (loss) before income taxes (264,668) 353,203

Expected taxes based on the statutory rate of 26.5% - 93,599 Small business deduction of 11% - (39,852) Other - 2,409

Current income tax expense - 56,156

Deferred tax expense (recovery)

Origination and reversal of temporary differences (85,000) (13,503)

18. RELATED PARTY TRANSACTIONS

The Company entered into the following transactions with key management personnel, which aredefined by IAS 24, Related Party Disclosures, as those persons having authority and responsibilityfor planning, directing and controlling the activities of the Company, including directors andmanagement:

CompensationSalaries, benefits and directors fees $ 529,884 $ 486,243Pension and other post-employment benefits 54,830 53,363

$ 584,714 $ 539,606

Premiums for key management personnel during 2015 amounted to approximately $196,616 (2014 -$84,580). There were claims paid to key management personnel during 2015 $11,111 (2014 -none).

24

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

19. PENSION PLAN

The Company makes contributions on behalf of its employees to “The Retirement Annuity Plan forEmployees of the Ontario Mutual Insurance Association and Member Companies”, which is a multi-employer plan. Each member company has signed an Ontario Mutual Insurance AssociationPension Plan Agreement. Eligible employees participate in the defined benefit plan and salesagents participate in the defined contribution plan. The defined benefit plan specifies the amount ofthe retirement benefit to be received by the employee based on the number of years the employeehas contributed and his/her final average earnings.

The Company funds the excess defined benefit plan based on the Company’s percentage ofpensionable earnings as calculated by the Pension Plan actuaries. The Pension Plan agreementstates that the Company is responsible for its share of any deficit as a result of any actuarialvaluation or cost certificate. The minimum funding requirement is the solvency valuation amountdetermined by the Pension Plan actuary on the valuation dates prescribed by the Pensions BenefitAct. In the event of a wind-up, voluntary withdrawal or bankruptcy, either by the Company or thegroup as a whole, the Company is responsible for its portion of all expenses and deficit related tosuch.

The amount contributed to the defined benefit plan for 2015 was $ 77,584 (2014 - $ 77,943). Thecontributions were made for current service and these have been recognized in income. TheCompany had a 1.42% share of the total contributions to the Plan in 2015.

An actuarial valuation of the Pension Plan as of December 31, 2010 indicated that the Company wasin a deficit position, resulting in a lump sum additional contribution to the defined benefit plan of$49,263 in 2011. In 2013 there was a contractual requirement to provide additional funding to thedefined benefit plan which resulted in a lump sum payment of $107,860. These contributions havebeen recognized in income. The next actuarial valuation to be filed under the Pension Benefit Act isas of December 31, 2016.

The expected contributions to the defined benefit plan and defined contribution plan for 2016 are$99,040 combined.

The defined benefit plan has been closed to future eligible employees effective December 31, 2012.The Company and all current employees who are accruing benefits under the defined benefit plancontinue to contribute to the defined benefit plan according to the existing terms of the agreement.

The amount contributed to the defined contribution plan for 2015 was $19,035 (2014 - $17,087). Thecontributions were made for current service and these have been recognized in income.

Future eligible employees are enrolled in a new defined contribution plan. The Company’s obligationwith respect to this plan is to make specified monthly contributions based on a percentage ofemployee’s eligible earnings. The amount contributed to the plan for 2015 was $4,486 (2014 -$2,798).

25

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

20. FINANCIAL INSTRUMENTS AND INSURANCE RISK MANAGEMENT

Insurance risk management

The principal risk the Company faces under insurance contracts is that the actual claims and benefitpayments or the timing thereof, differ from expectations. This is influenced by the frequency ofclaims, severity of claims, actual benefits paid and subsequent development of long-term claims.Therefore, the objective of the Company is to ensure that sufficient reserves are available to coverthese liabilities.

The above risk exposure is mitigated by diversification across a large portfolio of insurance. Thevariability of risk is also improved by careful selection and implementation of underwriting strategyguidelines, as well as the use of reinsurance arrangements.

The Company purchases reinsurance as part of its risk mitigation program. Retention limits for theexcess-of-loss reinsurance vary by product line.

Amounts recoverable from reinsurers are estimated in a manner consistent with the outstandingclaims provision and are in accordance with the reinsurance contracts. Although the Company hasreinsurance arrangements, it is not relieved of its direct obligations to its policyholders and thus acredit exposure exists with respect to ceded insurance, to the extent that any reinsurer is unable tomeet its obligations assumed under such reinsurance agreements.

The Company writes insurance primarily over a twelve month duration. The most significant risksarise through high severity, low frequency events such as natural disasters or catastrophes. Aconcentration of risk may arise from insurance contracts issued in a specific geographic locationsince all insurance contracts are written in Ontario.

The Company manages this risk via its underwriting and reinsurance strategy within an overall riskmanagement framework. Exposures are limited by having documented underwriting limits andcriteria. Pricing of property and liability policies are based on assumptions in regard to trends andpast experience, in an attempt to correctly match policy revenue with exposed risk. Automobilepremiums are subject to approval by the Financial Services Commission of Ontario and thereforemay result in a delay in adjusting the pricing to exposed risk. Reinsurance is purchased to mitigatethe effect of the potential loss to the Company. Reinsurance is placed with Farm MutualReinsurance Plan Inc. (FMRP), a Canadian registered reinsurer.

The Company followed a policy of underwriting and reinsuring contracts of insurance which, in themain, limit the liability of the Company to an amount on any one claim of $230,000 in the event of aproperty claim, an amount of $360,000 in the event of an automobile claims, an amount of $350,000in the event of a liability claim, an amount of $20,000 in the event of a farmers' accident claim.

The Company is exposed to a pricing risk to the extent that unearned premiums are insufficient tomeet the related future policy costs. Evaluation is performed regularly to estimate future claimscosts, related expenses and expected profit in relation to unearned premiums.

The risks associated with insurance contracts are complex and subject to a number of variableswhich complicate quantitative sensitivity analysis. The Company uses various techniques based onpast claims development experience to quantify these sensitivities. This included indicators such asaverage claim cost, amount of claims occurrence, expected loss ratios and claims development asdescribed in note 14.

(continues)

26

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

20. FINANCIAL INSTRUMENTS AND INSURANCE RISK MANAGEMENT (continued)

The table found at the end of Note 13, Provision for Unpaid Claims and Adjustment Expenses, setsout the concentration of unpaid claims and adjustment expenses by class of insurance.

A sensitivity analysis is based on the claims loss ratio which is calculated by taking net claimsincurred including adjustment expenses over net premiums earned. A 5% movement in the currentyear claims loss ratio would impact the statement of comprehensive income by approximately$328,000 (2014 - $301,000) before tax.

Fair Value

The Company has categorized its assets that are carried at fair value on a recurring basis, based onpriority of the inputs to valuation techniques used to measure fair value, into a three level fair valuehierarchy. Financial assets measured at fair value are categorized as follows:

Level 1: Fair value is based on unadjusted quoted prices for identical assets or liabilities in an activemarket.

Level 2: Fair value is based on quoted prices for similar assets or liabilities in active markets,valuation that is based on significant observable inputs or inputs that are derived principally for orcorroborated with observable market data through correlation or other means.

Level 3: Fair value is based on valuation techniques that require one or more significantunobservable inputs or the use of broker quotes. These unobservable inputs reflect the Company'sassumptions about the assumptions market participants would use in pricing the assets or liabilities.The Company does not have any amounts classified as Level 3.

Level 1 Level 2 TotalDecember 31, 2015 $ $ $

Cash 233,829 - 233,829 Bonds - 9,258,865 9,258,865 Equities - 4,620,564 4,620,564

Total assets measured at fair value 233,829 13,879,429 14,113,258

There were no transfers between Level 1 and Level 2 for the years ended December 31, 2015and 2014.

Credit Risk

Credit risk is the risk of financial loss to the Company if a debtor fails to make payments of interestand principal when due. The Company is exposed to this risk relating to its debt holdings in itsinvestment portfolio and the reliance on reinsurers to make payment when certain loss conditionsare met.

(continues)

27

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

20. FINANCIAL INSTRUMENTS AND INSURANCE RISK MANAGEMENT (continued)

The Company’s investment policy puts limits on the bond portfolio including portfolio compositionlimits, issuer type limits, bond quality limits, aggregate issuer limits, corporate sector limits andgeneral guidelines for geographic exposure. All fixed income portfolios are measured forperformance on a quarterly basis and monitored by management on a monthly basis.

The maximum exposure to credit risk and concentration of this risk is outlined in note 4.

Reinsurance is placed with FMRP, a Canadian registered reinsurer. Management monitors thecreditworthiness of FMRP by reviewing their annual financial statements and through ongoingcommunications. Reinsurance treaties are reviewed annually by management prior to renewal ofthe reinsurance contract.

Amounts receivable are short-term in nature and are not subject to material credit risk.

There have been no significant changes from the previous period in the exposure to risk or policiesprocedures and methods used to measure the risk.

Market Risk

Market risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate asa result of market factors. Market factors include three types of risk: currency risk, interest rate risk,and equity risk.

The Company’s investment policy operates within the guidelines of the Insurance Act. Aninvestment policy is in place and its application is monitored by the Investment Committee and theBoard of Directors. Diversification techniques are utilized to minimize risk.

Currency risk

Currency risk is the risk that fair value or future cash flows of a financial instrument will fluctuatebecause of changes in foreign exchange values. The Company is not significantly exposed toforeign exchange rate risk.

The Company is exposed to currency risk through its holdings in global equity and fixed incomeinvestments. Management monitors its foreign currency exposure regularly and adjusts holdingswhen deemed necessary.

As at December 31, 2015, a 1% change in value of foreign currency would impact the value of theglobal equity and fixed income investments of approximately $22,000.

(continues)

28

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

20. FINANCIAL INSTRUMENTS AND INSURANCE RISK MANAGEMENT (continued)

Interest rate risk

Interest rate risk is the potential for financial loss caused by fluctuations in fair value or future cashflows of financial instruments because of changes in market interest rates.

The Company is exposed to this risk through its interest bearing investments that include termdeposits and bonds.

Historical data and current information is used to profile the ultimate claims settlement pattern byclass of insurance, which is then used in a broad sense to develop an investment policy andstrategy. However, because a significant portion of the Company’s assets relate to its capital ratherthan liabilities, the value of its interest rate based assets exceeds its interest rate based liabilities.As a result, generally, the Company’s investment income will move with interest rates over themedium to long-term with short term interest rate fluctuations creating unrealized gains or losses inother comprehensive income. There are no occurrences where interest would be charged onliabilities, therefore, little protection is needed to ensure the fair market value of assets will be offsetby a similar change in liabilities due to an interest rate change.

The objective and policies and procedures for managing interest rate risk is to diversify the bondportfolio in such a way that the bond portfolio is laddered over a number of years. A portion of thebond portfolio would come due each year and be reinvested. This protects the Company fromfluctuations in the interest rates.

At December 31, 2015 a 1% move in interest rates, with all other variables held constant, couldimpact the market value of interest bearing investments by approximately $501,000.

Equity risk

Equity risk is the uncertainty associated with the valuation of assets arising from changes in equitymarkets. The Company is exposed to this risk through its equity holdings within its investmentportfolio.

The Company’s portfolio includes equity and fixed investment with fair values that fluctuate with thestock markets. A 10% movement in the stock markets would have an estimated affect on the fairvalues of approximately $404,000. For stocks that the Company did not sell during the period, thechange would be recognized in the asset value and in net income. For stocks that the Company didsell during the period, the change during the period and changes prior to the period would berecognized as net realized gains in income during the period.

The Company limits its equity holdings to less than 25% of the total portfolio value.

(continues)

29

Townsend Mutual Insurance CompanyNotes to Financial Statements

Year ended December 31, 2015

20. FINANCIAL INSTRUMENTS AND INSURANCE RISK MANAGEMENT (continued)

Liquidity risk

Liquidity risk is the risk that the Company will not be able to meet all cash outflow obligations as theycome due. The Company mitigates this risk by monitoring cash activities and expected outflows.The current liabilities arise as claims are made. There are no material liabilities that can be calledunexpectedly at the demand of a lender or client. There are no material commitments for capitalexpenditures and there is no need for such expenditures in the normal course of business. Claimpayments are funded by current operating cash flow including investment income. There have beenno significant changes from the previous period in the exposure to risk or policies.

21. CAPITAL MANAGEMENT

The Company's objectives with respect to capital management are to maintain a capital base that isstructured to exceed regulatory requirements and to best utilize capital allocations.

The regulators measure the financial strength of property and casually insurers using a minimumcapital test (MCT). The regulators generally expect property and casualty companies to comply withcapital adequacy requirements. This test compares a Company's capital against the risk profile ofthe organization. The risk-based capital adequacy framework assesses the risk of assets, policyliabilities and other exposures by applying various factors. The regulator indicates that the Companyshould produce a minimum MCT of 150%. During the year, the Company has consistentlyexceeded this minimum. The regulator has the authority to request more extensive reporting andcan place restrictions on the Company's operations if the Company falls below this requirement anddeemed necessary.

The MCT for the Company at December 31, 2015 was 386% (2014 - 413%). On January 1, 2015the calculation for the MCT was amended by the regulators. For comparative purposes, the 2014previously calculated MCT figure of 463% using the 2014 calculation has been replaced with therevised MCT figure of 413% using the amended 2015 calculation.

For the purpose of capital management, the Company has defined capital as surplus.

30