Towards a SAARC Investment Area - ris.org.in Kelegama.pdf · • GEP Report Recommended to have a...

24

Towards a SAARC Investment Area Policy Options & Challenges 11/26/2014 Institute of Policy Studies of Sri Lanka 7 th South Asia Economic Summit, Delhi, India 5-7 November 2014

Transcript of Towards a SAARC Investment Area - ris.org.in Kelegama.pdf · • GEP Report Recommended to have a...

Towards a SAARC Investment Area Policy Options & Challenges

11/26/2014

Institute of Policy Studies of Sri Lanka 7th South Asia Economic Summit, Delhi, India

5-7 November 2014

Structure of Presentation

• Introduction

• Analytical Framework

• Trends and Patterns of FDI in SAARC

• FDI Policy Context in South Asia

• Comparative Assessment of Investment Climates

• ASEAN Comprehensive Investment Agreement as a

regional benchmark: Salient Features

• Conclusion & Way Forward

11/26/2014 2

Introduction

• In moving towards deeper economic integration, the SAARC GEP Report

(1999), stressed on the concurrent need for deeper finance and investment

policy integration to complement trade expansion

• GEP Report Recommended to have a investment agreement in place before

the implementation of the FTA

• SAFTA has come into effect, whilst almost a decade on, despite SATIS, a

comprehensive agreement covering investment still remains largely in a

dormant state

• Given the current state of affair - it is timely that a regional investment

framework be instituted to complement the regions trade liberalization

programme

• Need for broad based investment climate reforms at the country level to

complement regional efforts

11/26/2014 3

What are International Investment Agreements (IIAs) ?

• With the surge in global FDI flows, the international investment landscape has

been increasingly dotted with IIAs

• Amongst the many provisions, IIAs seek to attract FDI by addressing issues such

as expropriation, fair and equal treatment and liberalization foreign investors

entry and ownership requirements

• They obligate a host country to abide by international rules on investment and

dispute settlement mechanisms are backed by third-party arbitration

• Countries can undertake unilateral liberalization, however the ‘lock-in effect’

of making investment and services liberalization commitments a part of an IIAs

adds credibility to these commitments

• Whilst Bilateral Investment Agreements (BITs) are by far the most popular,

recent decades have witnessed an uptick in regional and inter-regional IIAs

(EIIAs) established under the broader framework of Economic Integration

Agreements (e.g. NAFTA, EU, ASEAN, etc.)

11/26/2014 4

• The market enlargement effect of EIAs (Economic Integration Agreements) ‘allows for gains from specialization (division of labour), differences in resource endowments, and from economies of scale in manufacturing and technology’

• Removal of trade barriers is a major step in this direction; however the removal of barriers to other types of international transactions such as investment expands the extent and range of such benefits.

• EIAs dealing with trade would also see an increase in investment flows into and within the EIA area, driven by two factors

• First, the enlargement effect resultant from the removal of trade barriers allows firms to benefit from greater scale, which in consequence helps attract market-seeking production activities, from both within and outside the EIA area

• Second, to facilitate change in the location of production within EIA member countries

11/26/2014 5

Rationale for a Regional Investment Agreement

• Trade liberalization reduces the need for maintaining horizontal operations for MNEs and allows them to focus on assigning MNE affiliates to specialize in specific product lines to the region market

• Relocation of production is essentially driven by comparative advantage, however it is closely linked to adoption of investment rules that relax market entry restrictions and provide for legal protection.

• After the implementation of the EU single Market Plan, EU shares of global FDI rose from 30% to 50%. Similarly the creation of NAFTA saw Mexico’s FDI increase from US$12 bn to US$54 bn per year (Kumar 2008)

• To ensure the combined efficiency effects of scale and comparative advantage, lowering tariffs alone is not sufficient. Very little could be gained if countries within an EIA area maintain substantial investment barriers between themselves

11/26/2014 6

Rationale for a Regional Investment Agreement (contd.)

IIAs and their place in the context of FDI location Determinants

• Existence of IIAs is by far, not the only determinant

of FDI

• Other factors, such as the economic attractiveness

of a host country, its market size, its labour force or

its endowment with natural resources are much

more important

• To make key economic determinants more

attractive a number of additional conditions are

needed

11/26/2014 7

Trends and Patterns of Inward FDI

11/26/2014 8

• Despite the recent performance, FDI inflows to SAARC vis-à-vis other regional

groupings is rather limited

-10

0

10

20

30

40

50

60

70

Inward FDI flows, Percentage of World Total, 1970-2013

ASEAN

CARICOM

Euro area

FTAA

MERCOSUR

NAFTA

SAARC

UNCTAD (2014) Statistics Database

11/26/2014 9

Year 1990-2000 2000-2010 2010-2013

ASEAN 2.03 2.28 3.76

CARICOM 0.02 0.04 0.10

Euro area 35.4 40.7 16.4

FTAA 25.4 26.0 30.7

SAARC 0.019 0.67 0.50

Share of Global Outward FDI, SAARC and Selected Regional Groupings

Trends and Patterns of Outward FDI

UNCTAD (2014) Statistics Database

11/26/2014 10

87%

5% 4% 3% 1%

Composition of Inward FDI in SAARC, 2013

India Bangladesh Pakistan Sri Lanka Other

Trends and Patterns of FDI

83%

2% 12%

3%

Composition of Outward FDI, 2013

India

Bangladesh

Pakistan

Sri Lanka

UNCTAD (2014) Statistics Database

Characteristics of Intra-regional FDI Flows (examples from the India-

Sri Lanka FTA)

Largely

Market-seeking

•Sri Lankan MNEs - Ceylon Biscuits, Lion Brewery, John Keels, Hayleys and

Aitken Spence (Hotels)

•Indian MNEs - Indian Oil Corporation (IOC), Tatas (Taj Hotel, VSNL, Tata

Tea, Tata Communication), Bharat Airtel, Apollo Hospital, Aditya Birla

Group (L&T), Ambujas, Rediffusion, Nicholan Piramal, Jet Airways, Ashok

Leyland, and Hero Motors

.

Handful of efficiency-seeking

investment projects

• The MAS fabric park - Chintavaram

• Brandix India Apparel City (BIAC) – Vishakapathnam

• CEAT India - CEAT & Associated Motorways Pvt Ltd (AMW); second

joint venture partnership with Kelani Tyres Pvt Ltd

11/26/2014 11

Is Indian Investment Shifting away from South Asia?

• Majority of Indian outward FDI is destined to developed and

transitional economies

• Investment characteristics of Indian firms (especially in the IT/BPO

Sectors) suggest they want to develop a portfolio of locational assets

as a source of international competitiveness and visibility.

• Hence possibility of Indian FDI shifting away from South Asia

• Growing resistance to Indian Investment in some neighbouring

countries:

• TATA (Urea Fertilizer) and Mittal Group (Steel Mill) –

Bangladesh

• Indian Amul Company (Milk Production) – Sri Lanka

• GMR Group of India (Airport Modernization) - Maldives

11/26/2014 12

FDI Policy Context in South Asia

Ag

ric

ultu

re a

nd

Fo

rest

ry

Min

ing

an

d O

il &

Ga

s

Ma

nu

fac

turin

g

Ele

ctr

icity

Wa

ste

ma

na

ge

me

nt a

nd

wa

ter

sup

ply

Tra

nsp

ort

atio

n

Tou

rism

Me

dia

Tele

co

m

Fin

an

cia

l Se

rvic

es

Ac

co

un

tin

g

Ed

uc

atio

n

South Asia

Afghanistan 100% 100% 100% 80% 100% 92% 100% 0% 87% 100% 100% 100%

Bangladesh 50% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100% 100%

India 50% 100% 100% 100% 100% 75% 100% 63% 74% 42% 100% 100%

Nepal 100% 100% 67% 60% 50% 67% 100% 100% 100% 100% 51% 100%

Pakistan 100% 100% 100% 100% 100% 92% 100% 37% 100% 83% 100% 100%

Sri Lanka 70% 70% 100% 39% 100% 52% 100% 40% 100% 100% 100% 100%

11/26/2014 13

Sector Openness: Foreign Equity Ownership Limits (%), 2012

World Bank (2014) Investing Across Borders Database -2012

Regional Investment Cooperation in SAARC

• Attempts to foster Regional Investment Cooperation in SAARC could be traced back to the Thirteenth SAARC Summit in Dhaka (2005)

• SAARC Limited Multilateral Agreement on Avoidance of Double Taxation and Mutual Administrative Assistance in Tax Matters

• The SAARC agreement for the establishment of SAARC Arbitration Council

• Draft SAARC Agreement on Promotion and Protection of Investments

• SAARC Agreement on Trade in Services (SATIS)

11/26/2014 14

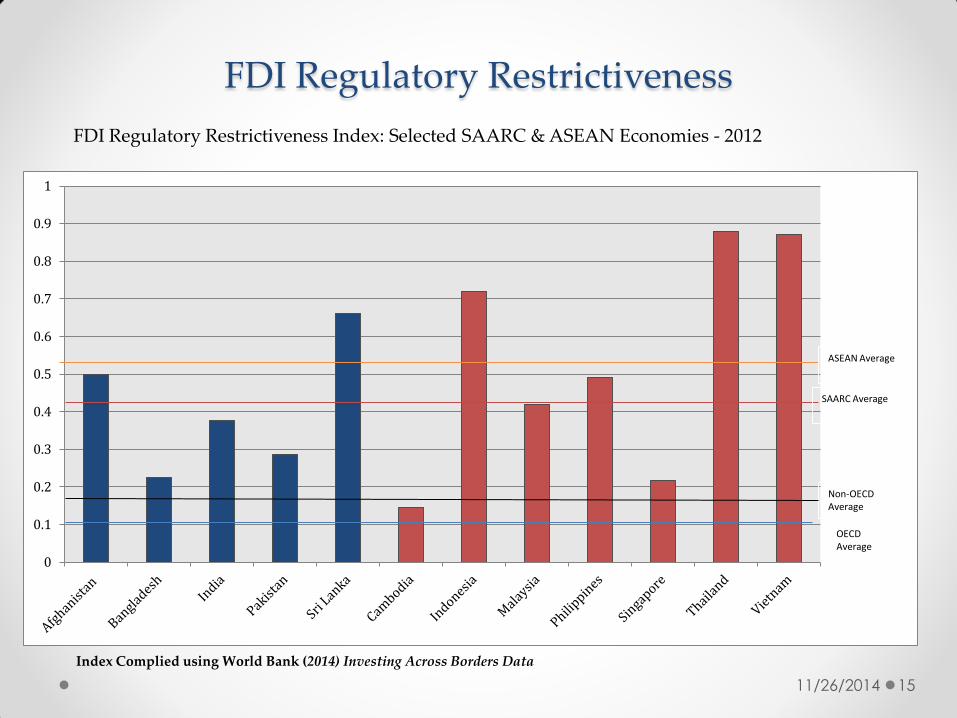

FDI Regulatory Restrictiveness

11/26/2014 15

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

OECD Average

Non-OECD Average

ASEAN Average

SAARC Average

FDI Regulatory Restrictiveness Index: Selected SAARC & ASEAN Economies - 2012

Index Complied using World Bank (2014) Investing Across Borders Data

Investments Freedoms Index

11/26/2014 16

0 10 20 30 40 50 60 70 80 90

Bangladesh

Bhutan

India

Maldives

Nepal

Pakistan

Sri Lanka

Indonesia

Malaysia

Philippines

Singapore

Thailand

Cambodia

Laos

Vietnam

Investment Freedom Score -2014

Heritage Foundation & Wall Street Journal (2014) Economic Freedoms Index Database

Economic Attractiveness of South Asia

Economy Market

attractiveness

Availability of

low-cost labour

and skills

Enabling

infrastructure

Presence of

natural

resources

Overall rank

Afghanistan 124 93 170 118 159

Bangladesh 66 .. 125 86 89

Bhutan 108 .. 116 144 134

India 24 1 79 5 3

Maldives 89 .. 72 173 126

Nepal 142 65 146 145 150

Pakistan 94 6 101 55 50

Sri Lanka 42 23 80 137 68

11/26/2014 17

FDI Potential Index (Ranking) , 2012

UNCTAD (2012) World Investment Report Database

Investment Climates across South Asia:

A Comparative Assessment (Contd.)

11/26/2014 Footer Text 18

World Bank, World Governance Indicators (2013) & AON Risk Map (2014)

0 20 40 60 80 100 120

Afghanistan

Bangladesh

Bhutan

India

Maldives

Nepal

Pakistan

Sri Lanka

Brunei

Indonesia

Malaysia

Philippines

Singapore

Thailand

Cambodia

Myanmar

Laos

Vietnam

Political Stability and Absence of Violence

11/26/2014 19

Comparative Assessment of Investment Climates Across South Asia : Governance

Country Voice and

Accountability

Government

Effectiveness

Regulatory

Quality

Rule of

Law

Control of

Corruption

SAARC

Afghanistan 13.27 7.18 11.00 1.42 1.91

Bangladesh 35.07 22.49 20.57 22.75 20.57

Bhutan 42.65 64.59 13.88 59.24 77.99

India 61.14 47.37 33.97 52.61 35.89

Maldives 34.60 44.98 36.36 28.91 37.80

Nepal 29.86 18.18 22.01 26.07 29.19

Pakistan 24.64 23.44 24.88 20.85 17.70

Sri Lanka 28.91 45.93 47.85 46.45 51.67

ASEAN-6

Brunei 32.23 74.16 82.78 69.19 74.16

Indonesia 48.82 45.45 46.41 36.49 31.58

Malaysia 37.44 81.82 72.25 64.45 68.42

Philippines 47.87 56.94 51.67 41.71 43.54

Singapore 52.13 99.52 100.00 95.26 96.65

Thailand 34.12 61.24 57.89 51.66 49.28

World Bank (2014)World Governance Indicators Database

Quality of

Infrastructure

(Score 0-7)

Inflation,

(annual %

change)

Country credit

rating

(Score 0-100)

Hiring and

firing

practices

(Score 0-7))

Redundancy

costs (in weeks

of salary)

SAARC

Bangladesh 2.8 8.7 29.2 4.5 31

Bhutan 4.9 9.7 28.2 3.9 8.3

India 3.9 9.3 60 4.1 15.8

Nepal 2.9 8.3 20.7 3.2 27.2

Pakistan 3.3 11 23.6 4.3 27.2

Sri Lanka 4.8 7.5 32.6 2.9 58.5

ASEAN-6

Brunei 5.1 0.5 n/a 4.1 3

Indonesia 4 4.3 55.9 4.3 57.8

Malaysia 5.5 1.7 71.7 4.5 23.9

Philippines 3.7 3.1 54.2 3.3 27.4

Singapore 6.4 4.6 92.7 5.6 3

Thailand 4.5 3 61.2 4.4 36

11/26/2014 20

Comparative Assessment of Investment Climates Across South Asia : Other Determinants

World Economic Forum (2014) Global Competiveness Report

ASEAN Comprehensive Investment Agreement (ACIA) as

a regional benchmark: Salient Features of

• Broad definition of investment

• Unique definition of ‘investor’

• Compensation in the event of strife

• Freedom of transferring funds

• Entry, temporary stay and work authorization for investors,

executives, managers and members of the board of directors

of an ASEAN member

11/26/2014 21

Other Features of ACIA • Built on four main pillars: Liberalization, Protection, Promotion and

Facilitation

11/26/2014 22

Liberalization

• Liberalization of Five Sectors

• Reduces or removes restrictions to entry

• Reduce &/or remove restrictive investment measures & other impediments

Protection

• Investor–state

dispute settlement • Full protection and

security, and treatment of compensation for losses resulting from strife

Facilitation

• Streamline and simplify procedures

• Promote the dissemination of investment information, rules, regulations, policies and procedures

Promotion • Promote intra-

ASEAN trade

• Promote industrial complementation and production networks among MNCs in ASEAN

• Undertake Joint investment missions

Conclusion & Way Forward

• Contrary to what the topology of economic integration suggests. Incorporating , FDI at the very early stages of integration process plays a crucial complementary role in spurring the intra-regional expansion of trade

• South Asian countries, have instituted fairly liberal regulatory regimes. However, when it comes to the actual implementation of these policies, regulatory regimes seem to be highly restrictive

• Regional initiatives like SAFTA and SATIS are too shallow to act as incentives to attract investments and regional investment initiatives are in early stages to make any significant impact on regional investment flows

• A regional investment framework would be beneficial, by locking in policy commitments already made

• IIAs only form a sub-component of the overall host country investment environment. Getting the investment climate right, is far more important

• Individual SAARC countries need to unilaterally undertake broad-based investment

climate reforms to take full advantage of a SAARC investment Area. Achieving political stability must be a top most priority

• In designing an effective investment framework for SAARC, the region should draw lessons from other more successful regional groupings such as the ASEAN

11/26/2014 23

Thank you

11/26/2014 Footer Text 24