Tourism in Egypt

51

Q2 2013 www.businessmonitor.com EGYPT TOURISM REPORT INCLUDES 5-YEAR FORECASTS TO 2017 ISSN 1747-888X Published by:Business Monitor International

description

Business Monitor report in 2013

Transcript of Tourism in Egypt

Q2 2013www.businessmonitor.com

EGYPTTOURISM REPORTINCLUDES 5-YEAR FORECASTS TO 2017

ISSN 1747-888XPublished by:Business Monitor International

Egypt Tourism Report Q2 2013INCLUDES 5-YEAR FORECASTS TO 2017

Part of BMI’s Industry Report & Forecasts Series

Published by: Business Monitor International

Copy deadline: March 2013

Business Monitor InternationalSenator House85 Queen Victoria StreetLondonEC4V 4ABUnited KingdomTel: +44 (0) 20 7248 0468Fax: +44 (0) 20 7248 0467Email: [email protected]: http://www.businessmonitor.com

© 2013 Business Monitor InternationalAll rights reserved.

All information contained in this publication iscopyrighted in the name of Business MonitorInternational, and as such no part of thispublication may be reproduced, repackaged,redistributed, resold in whole or in any part, or usedin any form or by any means graphic, electronic ormechanical, including photocopying, recording,taping, or by information storage or retrieval, or byany other means, without the express written consentof the publisher.

DISCLAIMERAll information contained in this publication has been researched and compiled from sources believed to be accurate and reliable at the time ofpublishing. However, in view of the natural scope for human and/or mechanical error, either at source or during production, Business MonitorInternational accepts no liability whatsoever for any loss or damage resulting from errors, inaccuracies or omissions affecting any part of thepublication. All information is provided without warranty, and Business Monitor International makes no representation of warranty of any kind asto the accuracy or completeness of any information hereto contained.

CONTENTS

BMI Industry View ............................................................................................................... 7

SWOT .................................................................................................................................... 9

Political ................................................................................................................................................. 10

Economic ............................................................................................................................................... 11

Business Environment .............................................................................................................................. 13

Industry Forecast .............................................................................................................. 14Inbound Tourism .................................................................................................................................... 15

Table: Egypt Inbound Tourism, 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Table: Egypt Inbound Tourism, Top 10 Markets By Arrivals, 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

Outbound Tourism ................................................................................................................................. 17Table: Egypt Outbound Tourism, 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Table: Egypt Outbound Tourism, Top 10 Destinations By Departures, 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

Travel .................................................................................................................................................. 19Table: Egypt International Tourism Receipts for Transport and Travel, 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 19

Table: Egypt Breakdown of Methods of Tourist Travel . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Hotels .................................................................................................................................................. 21Table: Egypt Hotel Accommodation, 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Table: Egypt Hotels and Restaurants Industry Value, 2010-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Industry Risk Reward Ratings .......................................................................................... 24Tourism Risk Rewards Ratings ................................................................................................................. 24

Table: Middle East and Africa Risk Rewards Ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

Security Risk Reward Ratings ................................................................................................................... 25Table: Middle East And Africa Defence & Security Ratings . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 26

Market Overview ............................................................................................................... 27Table: Top 10 Global Hotel Group Presence . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

Table: Egypt Transport Infrastructure Projects - Airports . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 30

Company Profile ................................................................................................................ 31Egyptian General Company for Tourism & Hotels ......................................................................................... 31

Travco ................................................................................................................................................... 32

Global Industry Overview .................................................................................................. 34Table: Global Tourism Indicators, International Tourist Arrivals, 2009-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

Table: global tourism indicators, hotel and establishment units, 2009-2017 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Table: Global Sporting Calendar, 2013-2022 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Global Assumptions .......................................................................................................... 40Table: Global Assumptions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Table: Global & Regional Real GDP Growth, % chg y-o-y . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Table: Developed States - Real GDP Growth Forecasts, % . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Egypt Tourism Report Q2 2013

© Business Monitor International Page 4

Table: Emerging Markets - Real GDP Growth Forecasts, % . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 44

Table: BMI VERSUS BLOOMBERG CONSENSUS REAL GDP GROWTH FORECASTS (%) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Demographic Forecast ..................................................................................................... 47Table: Egypt's Population By Age Group, 1990-2020 ('000) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 48

Table: Egypt's Population By Age Group, 1990-2020 (% of total) . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Table: Egypt's Key Population Ratios, 1990-2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Table: Egypt's Rural And Urban Population, 1990-2020 . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Methodology ...................................................................................................................... 51How We Generate Our Industry Forecasts ................................................................................................... 51

Tourism Industry .................................................................................................................................... 51

Tourism Ratings - Methodology ................................................................................................................ 52

Egypt Tourism Report Q2 2013

© Business Monitor International Page 5

BMI Industry View

This quarter BMI has revised and restructured its tourism reports, incorporating a greater range of data and

focusing on the hotel industry, the value of the tourism industry itself, and the impact of macroeconomic

factors.

The report also analyses the investment potential which Egypt offers to large tourist industries - particularly

global hotel groups - as they seek to maximise the growth opportunities being offered by the local market at

the present time.

BMI is relatively upbeat on the outlook for Egyptian tourism in 2013, predicting a 9% increase in tourist

arrivals, to reach 13.2mn. However, we do not envisage a return to 2010's level of tourist arrivals until at

least 2014.

Political uncertainty remains a major impediment to Egypt's tourism industry recovering over the short

term, with the late February 2013 air balloon crash in Luxor - which reportedly killed at least 19 tourists -

also reviving fears as to the safety record of some local tour operators.

Before the balloon accident, there had been some signs that tourism demand was recovering. However, this

crash, coupled with ongoing political uprisings and other demonstrations across the country, continues to

remind tourists of the dangers associated with travel to the country.

An overview of Egypt's top ten inbound tourism markets highlights the fact that its tourism source markets

are fairly well diversified around the globe. Although the top 6 markets all lie in Europe, and are inevitably

showing some signs of slowing down, given the ongoing economic uncertainty the number one market,

Russia, should continue to show strong growth in outbound tourism demand. This is due to its own rising

prosperity, despite the economic difficulties elsewhere in the European continent.

Below the Top 6, there is then good diversification in the Top 10 markets, with Saudi Arabia (Middle East),

Libya (Africa) and the USA (North America) taking seventh to ninth positions, before the Netherlands

(Europe) rounds out the Top 10. BMI believes that the strong diversification presented by these various

source markets could bode well for future tourism development over the forecast period.

Overall, BMI remains optimistic about the outlook for the Egyptian tourism industry, provided tourist areas

remain free of the demonstrations and other political risk factors that have plagued other cities across the

Egypt Tourism Report Q2 2013

© Business Monitor International Page 7

country. A weak outlook for the Egyptian pound could also see it favoured by tourists from the US and

Europe.

■ Among new hotel openings scheduled for 2013 and 2014 are several properties reportedly beingdeveloped by InterContinental Hotels Group (ICHG), such as the 300-room Holiday Inn AlexandriaWest, the 418-room Crowne Plaza Sharm El Sheikh Citystars and the 256-room InterContinental Sharmel Sheikh.

■ Marriott Hotels' independently-operated Ritz-Carlton division is also undertaking extensive renovationworks ahead of its assumption of management for the former Nile Hilton, owned by local partner MisrHotels. The new 331-room Nile Ritz-Carlton, Cairo is scheduled to open in 2014 and will mark Ritz -Carlton's debut in the Egyptian capital.

■ Carlson Rezidor is also reportedly due to open the 991-room Radisson Blu Sharm El Sheikh Lagoonlater in 2013, according to media reports.

■ Outbound air traffic looks set for good growth over our forecast period to 2017, rising from 5.89mn in2013, to 6.38mn in 2017.

■ This quarter, BMI has given Egypt an overall Industry Risk Rewards Rating of 49.64, putting it inseventh position for the MEA region, behind Jordan and ahead of South Africa.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 8

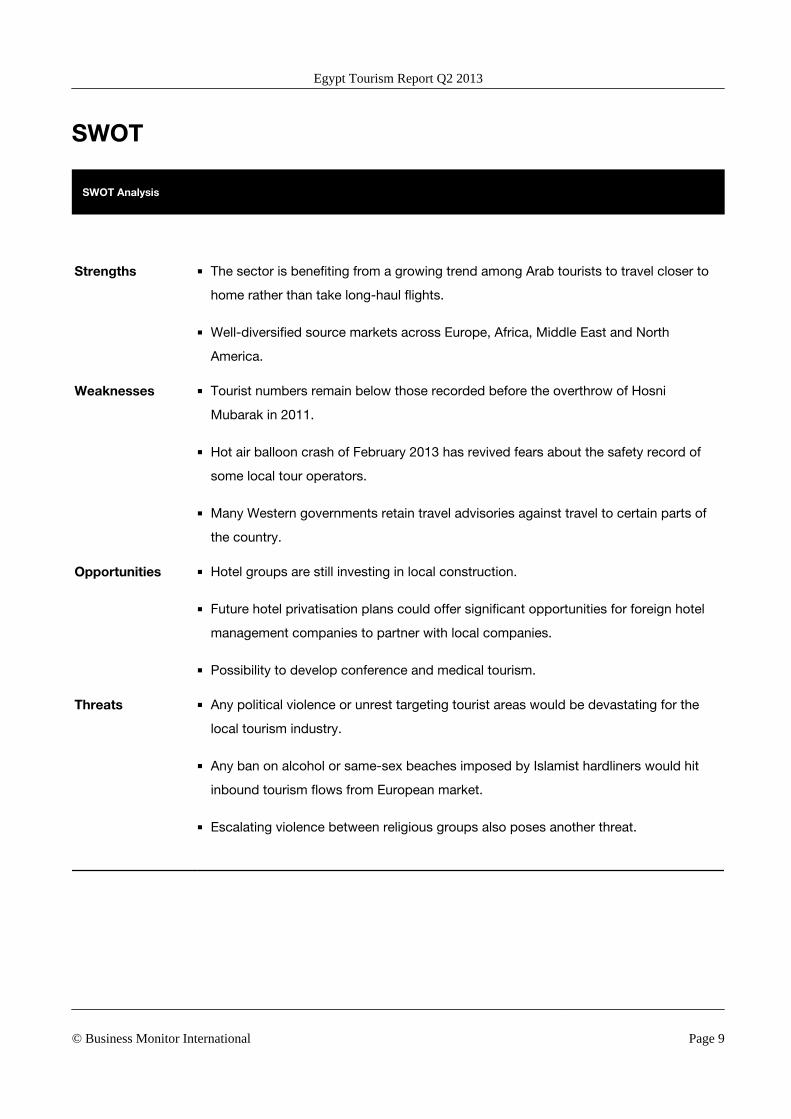

SWOT

SWOT Analysis

Strengths ■ The sector is benefiting from a growing trend among Arab tourists to travel closer to

home rather than take long-haul flights.

■ Well-diversified source markets across Europe, Africa, Middle East and North

America.

Weaknesses ■ Tourist numbers remain below those recorded before the overthrow of Hosni

Mubarak in 2011.

■ Hot air balloon crash of February 2013 has revived fears about the safety record of

some local tour operators.

■ Many Western governments retain travel advisories against travel to certain parts of

the country.

Opportunities ■ Hotel groups are still investing in local construction.

■ Future hotel privatisation plans could offer significant opportunities for foreign hotel

management companies to partner with local companies.

■ Possibility to develop conference and medical tourism.

Threats ■ Any political violence or unrest targeting tourist areas would be devastating for the

local tourism industry.

■ Any ban on alcohol or same-sex beaches imposed by Islamist hardliners would hit

inbound tourism flows from European market.

■ Escalating violence between religious groups also poses another threat.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 9

Political

SWOT Analysis

Strengths ■ Egypt has no serious disputes with neighbouring states, although its relations with

Syria and Iran are relatively tense.

Weaknesses ■ There is considerable domestic opposition to the government's relations with the US

and Israel, and, increasingly, to recent economic reforms.

■ Tension exists between the military and Islamist groups, including the popular Muslim

Brotherhood.

■ The transition away from authoritarian rule and the creation of necessary democratic

institutions will be a protracted process, and there is no certainty that the end result

will be a fully consolidated representative regime going forward.

Opportunities ■ The country is a major player in the Arab-Israeli peace process.

■ Any success for Barack Obama's plans to re-engage with Syria and Iran would

benefit Egypt.

Threats ■ Although the level of militant attacks, particularly on tourists and Western targets,

appears to have fallen in recent years, sporadic incidents should not be ruled out.

■ Demands for the military to quicken the transition process away from authoritarian

rule may not be met, which could increase the risk of large-scale unrest.

■ The reported presence of Hizbullah operatives in Sinai, apparently planning to attack

tourist sites in Egypt, has highlighted the lack of effective policing in the region and

added to security risks in the area.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 10

Economic

SWOT Analysis

Strengths ■ Exposure to the liquidity story in the Gulf should insulate Egypt against external

shocks to some degree and keep growth positive, assuming a relatively quick

recovery for the region from the current turmoil.

■ Low wages in global terms are advantages for foreign investors, particularly for those

wishing to use Egypt as a base for export-oriented manufacturing.

■ With a population of 84 million, Egypt is the largest market in the Arab world.

Weaknesses ■ Unemployment is high, which subdues demand.

■ Egypt has a widening fiscal deficit owing to a surging subsidies bill and rising public

wage costs.

■ There are relatively high levels of corruption and bureaucracy.

Opportunities ■ The formation of a more representative government that is democratically elected

could help reduce graft.

■ Future tenders will most likely be more transparent, helping those firms not politically

connected with the government secure lucrative contracts.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 11

SWOT Analysis - Continued

Threats ■ The widening fiscal deficit is adding to the costs of servicing debt, most of which is

held domestically.

■ High unemployment may lead to political resistance to privatisation plans.

■ Militant attacks on tourist sites pose a downside risk to revenues from the key tourist

sector, although increased security spending appears to have been successful in this

regard.

■ Piracy in the Gulf of Aden has resulted in large numbers of shipping companies opting

for alternative routes that do not use the Suez canal. If the situation is not resolved,

this key geo-strategic advantage will be lost.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 12

Business Environment

SWOT Analysis

Strengths ■ The country's geographical location is good for trade as Egypt has access to both the

Mediterranean and the Red Sea, not to mention the key Suez canal route, which

connects Europe and Asia.

■ The legal system has issued adjudications in favour of foreign firms, although there

are frequent procedural delays.

Weaknesses ■ Egypt ranks 112th out of 180 states surveyed in Transparency International's

Corruption Perceptions Index 2011, comparing unfavourably with regional peers.

■ The labour market is relatively inflexible, with Egypt performing markedly worse than

the Organisation for Economic Co-operation and Development average, and also

inferior to the regional average on the World Bank's Hiring and Firing Workers index.

Opportunities ■ Efforts towards banking-sector consolidation should bring down the cost of private-

sector credit and fuel small business growth over the long term.

Threats ■ Patronage networks impede attempts at fighting corruption and cutting bureaucracy.

■ Although levels of education are relatively high, there is a considerable mismatch

between the skills taught in schools and those required by most employers.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 13

Industry Forecast

Egypt's tourism industry has been badly affected by

the recent years of political turmoil and instability

following the overthrow of President Hosni Mubarak

in February 2011. According to official figures,

tourist arrivals fell dramatically over 2011, with a

return to 2010's level of tourist arrivals not expected

by BMI until 2014 or 2015.

Political uncertainty remains a major impediment to

Egypt's tourism industry recovering over the short

term, with the late February 2013 air balloon crash

in Luxor - which reportedly killed at least 19 tourists

- also reviving fears concerning the safety of some

local tour operators.

Before this balloon crash, there had been signs that

tourism demand was recovering. However, this latest

crash, coupled with continued political and other

demonstrations across the country, continues to

remind tourists of the dangers associated with travel to the country.

The UK Foreign and Commonwealth Office currently advises against all travel to the Governatorate of

North Sinai and advises against all but essential travel to the Governorate of South Sinai, with the exception

of: the Red Sea Resorts including those in the entire region of Sharm el Sheikh, Taba, Nuweiba and Dahab;

road travel between these resorts; and transfers between the resorts and the airports of Taba and Sharm el

Sheikh.According to the FCO, 'the security situation outside the resort areas in the Governorate of South

Sinai has deteriorated since early 2012 and there have been a number of hijacks, robberies and kidnaps in

the interior of the Governorate'. However, its advice adds that 'major tourist resorts remain stable and calm'.

Either way, it is clear that Egypt's tourist industry will continue to face significant challenges over 2013.

More Tourists, More Money

Total Arrivals ('000), Tourism ReceiptsBreakdown (US$bn), 2000-2017f

International tourism, receipts~ US$bn (LHS)International tourism, receipts for transport services~ US$bn (LHS)International tourism, receipts for travel items~ US$bn (LHS)Total arrivals, '000 (RHS)

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

e20

13f

2014

f20

15f

2016

f20

17f

0

10

20

30

5,000

10,000

15,000

20,000

0

Source: World Bank/Ministry of Tourism, Egypt/CAPMAS/

BMI

Egypt Tourism Report Q2 2013

© Business Monitor International Page 14

On a longer-term basis, it remains to be seen if the increasing presence of Islamist hardliners in local

politics will lead to a ban on alcohol and same-sex beaches, both of which would be devastating to inbound

tourism flows.

The chart shows the strong correlation between arrivals and overall tourism receipts. It also reveals that

travel items tourism receipts form by far the largest share of the overall receipt value, only a fraction of

which is derived from transport receipts.

Inbound Tourism

Looking at inbound tourism flows by region, Europe is the largest source market for Egypt, accounting for

69% of the total forecast for 2013, a figure we see remaining largely constant for the overall forecast for

2017.

Egypt is also reportedly taking steps to boost the number of tourists from the Middle East and other Arab

nations. According to a February 2013 report in the UK's Daily Telegraph newspaper, the Egyptian tourism

minister recently visited Tehran to encourage greater flows of medical tourists between the two nations.

Moreover, if a crackdown on alcohol and different-sex beaches was to be enacted in future, then BMI

would expect a sharp drop in European inbound tourism, which could partially be offset by higher numbers

of Middle Eastern arrivals.

As a result of initiatives such as medical tourism, BMI forecasts arrivals from the Middle East to increase

by 31.2% between 2013 and 2017, to reach over 3mn tourists.

Table: Egypt Inbound Tourism, 2010-2017

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Total Arrivals, '000 14,731.00 9,845.07 12,109.43 13,219.63 14,261.35 15,254.17 16,364.36 17,567.14

Total Arrivals, '000, %change y-o-y

17.51 -33.17 23.00 9.17 7.88 6.96 7.28 7.35

In-bound, arrivals byregion, Africa, '000

411.27 379.61 519.74 579.49 623.04 651.08 688.72 739.14

In-bound, arrivals byregion, Africa, % chg y-o-y

1.71 -7.70 36.92 11.50 7.51 4.50 5.78 7.32

In-bound, arrivals byregion, North America,'000

388.39 365.89 401.33 538.13 561.39 594.81 641.41 676.97

In-bound, arrivals byregion, North America,% chg y-o-y

-5.24 -5.79 9.69 34.09 4.32 5.95 7.83 5.54

Egypt Tourism Report Q2 2013

© Business Monitor International Page 15

Egypt Inbound Tourism, 2010-2017 - Continued

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

In-bound, arrivals byregion, Asia Pacific,'000

441.99 399.93 513.70 523.61 557.00 602.90 665.62 727.07

In-bound, arrivals byregion, Asia Pacific, %chg y-o-y

17.77 -9.51 28.45 1.93 6.38 8.24 10.40 9.23

In-bound, arrivals byregion, Europe, '000

7,904.08 6,938.00 8,372.63 9,142.17 9,854.86 10,617.31 11,403.85 12,235.24

In-bound, arrivals byregion, Europe, % chgy-o-y

-8.74 -12.22 20.68 9.19 7.80 7.74 7.41 7.29

In-bound, arrivals byregion, Middle East,'000

1,855.85 1,613.34 2,216.79 2,343.89 2,573.15 2,693.47 2,863.18 3,076.05

In-bound, arrivals byregion, Middle East, %chg y-o-y

8.37 -13.07 37.40 5.73 9.78 4.68 6.30 7.44

f = BMI forecast. Source: Ministry of Tourism Egypt, CAPMAS, BMI Calculation

In terms of the Top 10 most important source markets for Egypt, Russia is the largest provider of tourist

arrivals. Indeed, our forecasts call for Russian arrivals to increase by some 57.8% over the coming five

years, as greater disposable incomes and desire for outbound tourism fuel demand. In second place, behind

Russia, is Germany, followed by the UK, Italy, France and Poland; all of which lie in Europe.

However, encouragingly for the longer-term development of the local tourism industry, there is then some

diversification in the Top 10 markets, with Saudi Arabia (Middle East), Libya (Africa) and the US (North

America) taking seventh to ninth position, before the Netherlands (Europe) rounds out the Top 10. BMI

believes that the strong diversification presented by these various source markets could bode well for future

tourism development over the forecast period.

Table: Egypt Inbound Tourism, Top 10 Markets By Arrivals, 2010-2017

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Russia 1,976.17 1,907.79 2,589.95 2,986.38 3,343.16 3,740.66 4,215.65 4,714.04

Germany 1,139.82 1,037.03 1,222.88 1,218.92 1,190.73 1,192.98 1,216.45 1,263.96

UK 845.34 737.21 780.98 871.67 959.46 1,059.98 1,151.90 1,190.91

Italy 979.96 549.56 636.68 742.72 868.96 922.59 992.21 1,012.56

Egypt Tourism Report Q2 2013

© Business Monitor International Page 16

Egypt Inbound Tourism, Top 10 Markets By Arrivals, 2010-2017 - Continued

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

France 519.83 457.56 499.21 563.27 623.34 622.53 632.40 654.07

Poland 474.05 456.85 568.15 652.73 775.39 932.24 1,009.07 1,102.50

Saudi Arabia 434.36 338.80 426.20 391.88 429.68 435.62 452.54 477.17

Libya 366.80 285.02 485.15 596.66 690.34 732.52 786.87 855.27

USA 293.07 277.96 291.48 427.93 460.20 496.67 540.84 571.81

Netherlands 244.56 220.11 254.79 263.32 257.27 262.96 274.90 293.54

f = BMI forecast. Source: Ministry of Tourism Egypt, CAPMAS, BMI Calculation

Outbound Tourism

Despite its many domestic political and economic challenges, outbound tourism from Egypt is growing

strongly and should continue to do so over BMI's forecast period to 2017. Indeed, we forecast a 34%

expansion in outbound travel on the part of Egyptian citizens over the coming five years.

The majority of outbound travel is to other Middle Eastern destinations, with Europe coming in second

place. This reflects longstanding cultural and business ties that Oman has around the Mediterranean and

beyond. Very few Egyptians travel to Africa or Latin America at the present time. Looking forward,

although BMI is forecasting a doubling in the number of Egyptians travelling to other African destinations

over the forecast period to 2017, this will still only amount to 15,380 departures.

Table: Egypt Outbound Tourism, 2010-2017

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Total Out-bound, touristdepartures, '000

1,298.23 1,749.09 1,679.93 1,814.64 1,988.16 2,121.37 2,255.16 2,431.22

Out-bound, tourist departures, %chg y-o-y

22.51 34.73 -3.95 8.02 9.56 6.70 6.31 7.81

Average Tourist Departure per1000 of the population

0.02 0.02 0.02 0.02 0.02 0.02 0.03 0.03

Out-bound, resident departuresby destination, Africa, '000

5.97 6.25 6.41 7.70 9.49 11.15 13.00 15.38

Out-bound, resident departuresby destination, Africa, % changey-o-y

19.36 4.76 2.54 20.08 23.28 17.53 16.60 18.31

Out-bound, resident departuresby destination, North America,'000

57.44 61.72 59.46 65.98 74.61 81.53 88.55 97.47

Egypt Tourism Report Q2 2013

© Business Monitor International Page 17

Egypt Outbound Tourism, 2010-2017 - Continued

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Out-bound, resident departuresby destination, North America, %chg y-o-y

15.26 7.44 -3.66 10.96 13.08 9.28 8.61 10.07

Out-bound, resident departuresby destination, Latin America,'000

1.24 1.56 1.35 1.62 1.96 2.21 2.47 2.80

Out-bound, resident departuresby destination, Latin America, %chg y-o-y

54.79 25.26 -13.10 19.36 21.61 12.68 11.66 13.35

Out-bound, resident departuresby destination, Asia Pacific, '000

41.65 39.14 42.80 50.68 60.27 67.27 73.90 82.49

Out-bound, resident departuresby destination, Asia Pacific, %chg y-o-y

17.95 -6.03 9.36 18.42 18.91 11.62 9.86 11.61

Out-bound, resident departuresby destination, Europe, '000

213.54 235.64 237.56 266.85 301.80 325.55 349.48 386.17

Out-bound, resident departuresby destination, Europe, % chg y-o-y

-2.74 10.35 0.82 12.33 13.09 7.87 7.35 10.50

Out-bound, resident departuresby destination, Middle East, '000

978.39 1,404.79 1,332.34 1,421.81 1,540.04 1,633.66 1,727.75 1,846.91

Out-bound, resident departuresby destination, Middle East, %chg y-o-y

30.60 43.58 -5.16 6.72 8.31 6.08 5.76 6.90

f = BMI forecast. Source: National Sources, BMI Calculation

The most visited destination by Egyptian tourists is Saudi Arabia. Many of these travellers are visiting holy

cities or participating in Muslim pilgrimages such as Hajj. The second-most visited destination is the UK,

which has a relatively large ex-pat population.

In third place is the UAE. A portion of these departures could well include not only holidaymakers, but also

numbers of Egyptian workers heading to jobs in the UAE. That said, there is clearly growing demand for

outbound travel on the part of Egyptian citizens to all parts of the globe.

Table: Egypt Outbound Tourism, Top 10 Destinations By Departures, 2010-2017

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Saudi Arabia 763.90 1,157.81 1,089.48 1,146.12 1,221.11 1,281.25 1,342.25 1,419.75

UK 42.31 40.70 44.14 46.32 49.00 51.06 52.46 56.83

UAE 150.56 164.04 161.51 181.81 208.70 230.25 252.12 279.90

Egypt Tourism Report Q2 2013

© Business Monitor International Page 18

Egypt Outbound Tourism, Top 10 Destinations By Departures, 2010-2017 - Continued

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Turkey 61.56 79.67 78.35 92.09 108.59 118.57 129.31 147.35

USA 57.44 61.72 59.46 65.98 74.61 81.53 88.55 97.47

Italy 56.00 71.00 70.17 78.00 87.43 94.25 100.70 108.40

Oman 28.27 29.27 28.31 34.00 41.52 47.56 53.68 61.46

Jordan 35.66 53.67 53.03 59.89 68.71 74.59 79.70 85.80

Hong Kong 11.78 10.76 12.22 13.80 15.93 17.66 19.43 21.88

f = BMI forecast. Source: National Sources, BMI Calculation

Travel

BMI estimates that receipts for transport services during 2013 will increase by some 16% in US dollar

terms, to US$1.4bn, in line with higher visitor numbers entering the country. Transport items cover costs by

tourists on all tourist transportation within Egypt, fares on buses, railways, airplanes and boat trips where

the company operating is domestic, carrier charges and fees, excess baggage fees, car transportation costs,

package holiday trips within that country excluding cruises, possibly car hire within that country, food and

drink costs the transport in question.

Table: Egypt International Tourism Receipts for Transport and Travel, 2010-2017

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

International tourism, receipts fortransport services, US$bn

1.26 0.91 1.20 1.40 1.63 1.88 2.19 2.53

International tourism, receipts fortransport services, US$bn, % changey-o-y

25.53 -27.90 32.88 15.79 16.66 15.62 16.10 15.73

International tourism, receipts fortransport services, EGPbn

7.09 5.39 7.32 9.21 9.77 11.10 12.67 14.62

International tourism, receipts fortransport services, EGPbn, % changey-o-y

27.45 -23.94 35.72 25.88 6.06 13.69 14.14 15.33

International tourism, receipts fortransport services, EURbn

0.95 0.65 0.95 1.12 1.36 1.57 1.82 2.11

International tourism, receipts fortransport services, EURbn, % changey-o-y

32.48 -31.20 45.44 17.65 21.53 15.62 16.10 15.73

International tourism, receipts for travelitems, US$bn

13.78 10.06 12.40 13.89 15.72 17.71 20.09 22.79

International tourism, receipts for travelitems, US$bn, % change y-o-y

28.14 -27.00 23.25 12.04 13.13 12.69 13.42 13.43

Egypt Tourism Report Q2 2013

© Business Monitor International Page 19

Egypt International Tourism Receipts for Transport and Travel, 2010-2017 - Continued

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

International tourism, receipts for travelitems, EGPbn

77.65 59.80 75.28 91.69 94.30 104.49 116.51 131.70

International tourism, receipts for travelitems, EGPbn, growth y-o-y

30.10 -22.99 25.89 21.80 2.85 10.81 11.50 13.03

International tourism, receipts for travelitems, EURbn

10.39 7.24 9.76 11.11 13.10 14.76 16.74 18.99

International tourism, receipts for travelitems, EURbn, % change y-o-y

35.24 -30.33 34.90 13.83 17.84 12.69 13.42 13.43

f = BMI forecast. Source: World Bank, UN, BMI Calculation

However, it is the receipts for travel items which are account for the largest share of the money pie, forecast

by BMI to reach US$13.89bn in 2013 (up 12% y-o-y in US dollar terms) and then to rise to US$22.79bn by

2017. International tourism receipts for travel items are expenditures by international inbound visitors in the

reporting economy. These receipts include any prepayment made for goods or services received in the

destination country. They also may include receipts from same-day visitors, except in cases where these are

so important as to justify a separate classification. Travel items can include such things as sun cream and

other common travel accessories, travel luggage bought in Egypt, tickets to get into national parks, cruise

excursions and so on.

The breakdown of tourist travel into specific sectors shows that Egypt is massively weighted towards air

travel in the tourist sector, both in domestic tourism and outbound tourism. Outbound air traffic looks set for

good growth over our forecast period to 2017, rising from 5.89mn in 2013, to 6.38mn in 2017.

Moving forward, however, BMI believes that cruise ship tourism will also play an ever-increasing role in

Egypt's overall tourism industry over our forecast period to 2017, especially if there is a return of political

stability.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 20

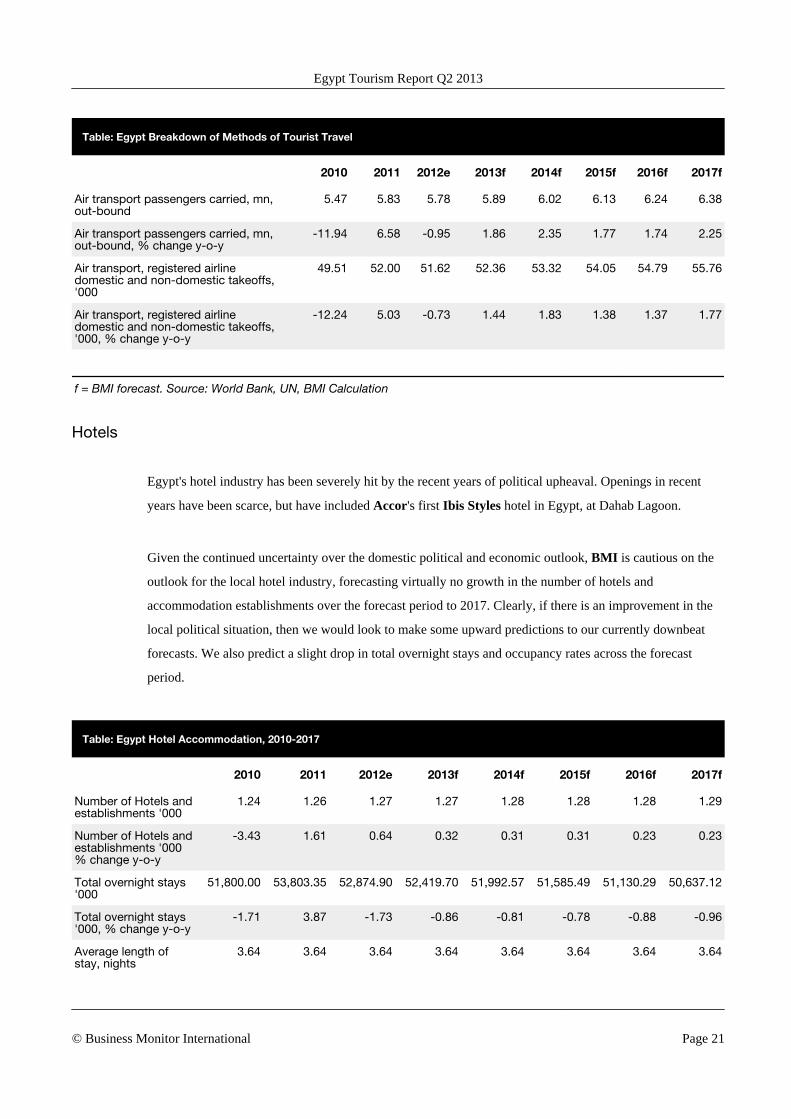

Table: Egypt Breakdown of Methods of Tourist Travel

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Air transport passengers carried, mn,out-bound

5.47 5.83 5.78 5.89 6.02 6.13 6.24 6.38

Air transport passengers carried, mn,out-bound, % change y-o-y

-11.94 6.58 -0.95 1.86 2.35 1.77 1.74 2.25

Air transport, registered airlinedomestic and non-domestic takeoffs,'000

49.51 52.00 51.62 52.36 53.32 54.05 54.79 55.76

Air transport, registered airlinedomestic and non-domestic takeoffs,'000, % change y-o-y

-12.24 5.03 -0.73 1.44 1.83 1.38 1.37 1.77

f = BMI forecast. Source: World Bank, UN, BMI Calculation

Hotels

Egypt's hotel industry has been severely hit by the recent years of political upheaval. Openings in recent

years have been scarce, but have included Accor's first Ibis Styles hotel in Egypt, at Dahab Lagoon.

Given the continued uncertainty over the domestic political and economic outlook, BMI is cautious on the

outlook for the local hotel industry, forecasting virtually no growth in the number of hotels and

accommodation establishments over the forecast period to 2017. Clearly, if there is an improvement in the

local political situation, then we would look to make some upward predictions to our currently downbeat

forecasts. We also predict a slight drop in total overnight stays and occupancy rates across the forecast

period.

Table: Egypt Hotel Accommodation, 2010-2017

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Number of Hotels andestablishments '000

1.24 1.26 1.27 1.27 1.28 1.28 1.28 1.29

Number of Hotels andestablishments '000% change y-o-y

-3.43 1.61 0.64 0.32 0.31 0.31 0.23 0.23

Total overnight stays'000

51,800.00 53,803.35 52,874.90 52,419.70 51,992.57 51,585.49 51,130.29 50,637.12

Total overnight stays'000, % change y-o-y

-1.71 3.87 -1.73 -0.86 -0.81 -0.78 -0.88 -0.96

Average length ofstay, nights

3.64 3.64 3.64 3.64 3.64 3.64 3.64 3.64

Egypt Tourism Report Q2 2013

© Business Monitor International Page 21

Egypt Hotel Accommodation, 2010-2017 - Continued

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Average length ofstay, nights, %change y-o-y

0.74 - - - - - - -

Hotel rooms '000 141.19 139.78 138.38 138.65 138.93 139.28 139.56 139.84

Hotel rooms '000, %change y-o-y

-4.90 -1.00 -1.00 0.20 0.20 0.25 0.20 0.20

Occupancy rate % 55.00 55.10 55.49 55.41 55.33 55.24 55.16 55.08

f = BMI forecast. Source: N/A. Occupancy Rate = Room occupancy rate

Lastly, BMI believes that the overall value of Egypt's hotel and restaurant industry will climb from US

$4.29bn in 2013, to US$5.03bn by end-2017, representing growth of 17.2%.In GDP terms, the contribution

of the hotels and restaurants industry to overall GDP will fall slightly from 1.59%, to 0.95%.

Table: Egypt Hotels and Restaurants Industry Value, 2010-2017

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Domestic Hotels andRestaurants Industry ValueEGPbn

33.76 28.30 28.06 28.30 28.50 28.74 28.88 29.07

Domestic Hotels andRestaurants Industry ValueEGPbn, % change y-o-y

9.49 -16.15 -0.88 0.88 0.71 0.83 0.51 0.63

Domestic Hotels andRestaurants Industry Value, US$bn

5.99 4.76 4.62 4.29 4.75 4.87 4.98 5.03

Domestic Hotels andRestaurants Industry Value, US$bn, % change y-o-y

7.84 -20.52 -2.95 -7.21 10.78 2.54 2.24 0.98

Domestic Hotels andRestaurants Industry Value,EURbn

4.52 3.43 3.64 3.43 3.96 4.06 4.15 4.19

Domestic Hotels andRestaurants Industry Value,EURbn, % change y-o-y

13.82 -24.15 6.21 -5.72 15.39 2.54 2.24 0.98

Domestic Hotels andRestaurants Industry Value, %of GDP

2.65 1.99 1.78 1.59 1.38 1.21 1.06 0.95

Domestic Hotels andRestaurants Industry Value, US$per capita

73.85 57.69 55.04 50.23 54.73 55.24 55.61 55.32

Egypt Tourism Report Q2 2013

© Business Monitor International Page 22

Egypt Hotels and Restaurants Industry Value, 2010-2017 - Continued

2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

Domestic Hotels andRestaurants Industry Value, US$per capita, % change y-o-y

5.98 -21.88 -4.60 -8.75 8.98 0.92 0.68 -0.52

Domestic Hotels andRestaurants Industry Value peremployee, US$

12,876.07 9,834.96 9,185.92 8,215.44 8,782.94 8,701.70 8,606.28 8,690.32

Domestic Hotels andRestaurants Industry Value peremployee, US$, % change y-o-y

3.46 -23.62 -6.60 -10.56 6.91 -0.92 -1.10 0.98

f = BMI forecast. Source: UN, ILO

Egypt Tourism Report Q2 2013

© Business Monitor International Page 23

Industry Risk Reward Ratings

Tourism Risk Rewards Ratings

Table: Middle East and Africa Risk Rewards Ratings

Rewards Risks

Limits ofpotentialreturns

TourismMarket

CountryStructure

Risks to realisationof potential returns

Marketrisks

CountryRisk

TourismRating

Rank

UAE 65.31 66.67 63.28 62.42 77.53 50.06 64.44 1

Qatar 61.15 63.33 57.88 64.65 75.08 56.11 62.20 2

Israel 62.00 53.33 75.00 61.61 62.69 60.74 61.88 3

Bahrain 59.55 66.67 48.86 66.86 68.00 65.93 61.74 4

Kuwait 58.13 66.67 45.33 61.55 65.19 58.58 59.16 5

Jordan 53.22 61.67 40.54 61.06 62.37 59.99 55.57 6

Egypt 48.69 52.50 42.96 51.87 60.84 44.52 49.64 7

SouthAfrica

42.66 41.67 44.15 61.94 60.51 63.10 48.44 8

Oman 43.37 50.00 33.43 56.36 75.53 40.67 47.27 8

SaudiArabia

38.12 38.33 37.79 60.95 74.70 49.70 44.97 8

Kenya 39.21 35.00 45.51 40.09 48.85 32.93 39.47 8

Morocco 32.07 36.67 25.16 53.82 57.95 50.44 38.59 9

Source: BMI

Limits Of Potential Returns

This is an evaluation of the sector's size and growth potential in each state, along with broader industry and

state characteristics that may inhibit its development. The reward ratings for tourism take into account the

numbers and percentage growth of tourist arrivals over the past year and our forecasts for future growth

over 2013.

BMI expects tourist arrivals figures to see a steady rise in Egypt over the coming years, despite domestic

political uncertainty. As such, we believe Egypt will continue to see good growth in annual tourism arrivals

and tourism revenues. This gives Egypt a Tourism Market figure of 52.50 this quarter.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 24

Indeed, the major Red Sea tourist resorts have been largely unaffected by demonstrations against the

government. However, we would have to revise Egypt's score significantly were tourists to become

involved in any violent political unrest.

The Country Structure score takes into account labour costs and infrastructure. Egypt is fortunate in that it

already has quite well developed tourism infrastructure and fairly low labour costs. Egypt's Country

Structure score is consequently 42.96 this quarter.

Risks To Realisation Of Returns

This offers an evaluation of industry-specific dangers and those emanating from the state's political and

economic profile that call into question the likelihood of anticipated returns being realised over the assessed

time period. The market risks score takes into account short term political stability and regional stability and

also takes into account vulnerability to external factors. Egypt has an overall market risks score of just 60.84

this quarter, the fourth-lowest in the region, reflecting continued uncertainty as to its future political

direction.

Lastly, BMI's proprietary country risk scores cover aspects such as legal framework, bureaucracy, market

openness and security risks. Egypt scores fairly poorly for all of these and has achieved a score of 44.52 this

quarter, again placing it towards the bottom of this metric on a regional basis.

Taking all of the risks and rewards together, Egypt obtains an overall Rating of 49.64 this quarter, putting it

in seventh position for the MEA region, behind Jordan and ahead of South Africa.

Security Risk Reward Ratings

BMI sees the growing possibility of a military coup in Egypt, if violence continues unabated. The defence

minister, General Abdel Fattah El-Sissi, warned on January 29 that the country faced the risk of 'collapse'

that could 'threaten future generations'. His comments followed days of violence across Egypt, in which

dozens of people were killed. On January 28, President Mohamed Morsi declared emergency rule in the

cities of Port Said, Suez, and Ismaila, all of which are along the vital Suez Canal. In addition, Egypt has

seen clashes between pro-Morsi Islamists and secularists opposed to the president coinciding with the

second anniversary of the overthrow of former president Hosni Mubarak.

Morsi's assumption of ever greater powers following his election as the country's first democratic and

Islamist president in June 2012 have fuelled fears of creeping Islamist authoritarianism, as opposed to the

liberal democracy that many demanded when Mubarak was deposed. There is also widespread

Egypt Tourism Report Q2 2013

© Business Monitor International Page 25

disappointment that the post-Mubarak era has been so unstable and that the economy has deteriorated over

the past two years, as evidenced by the Egyptian pound falling to record lows in January 2013.

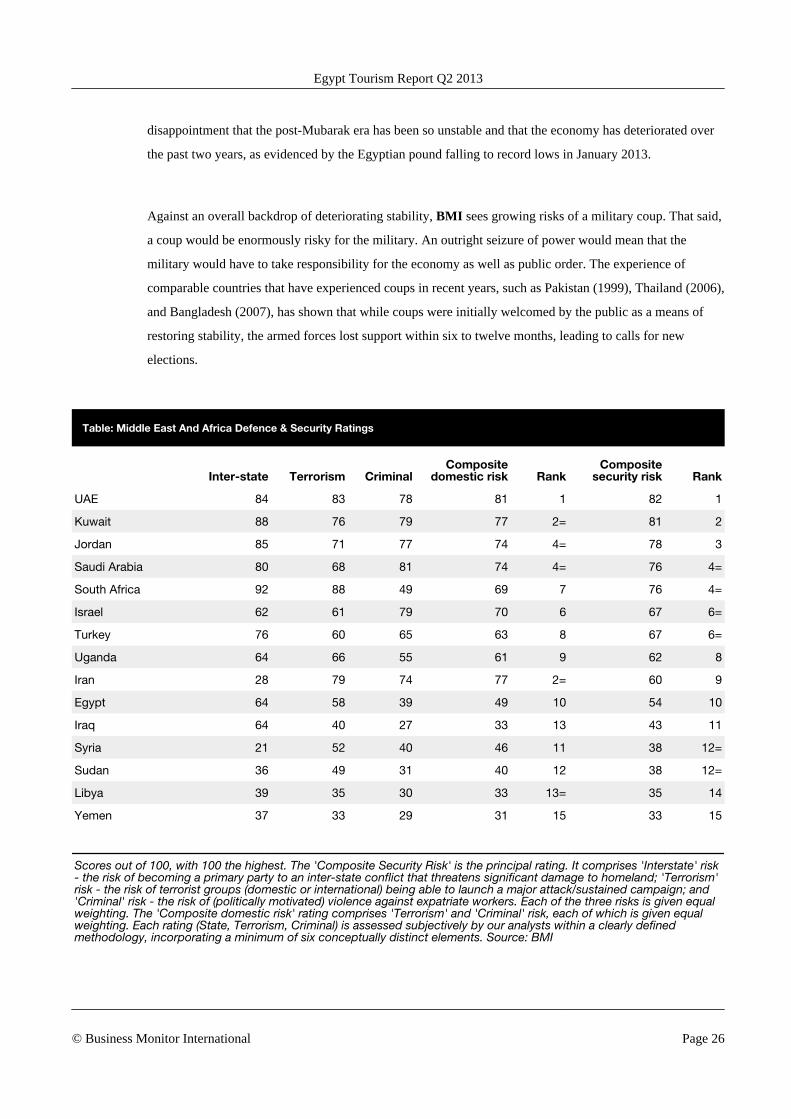

Against an overall backdrop of deteriorating stability, BMI sees growing risks of a military coup. That said,

a coup would be enormously risky for the military. An outright seizure of power would mean that the

military would have to take responsibility for the economy as well as public order. The experience of

comparable countries that have experienced coups in recent years, such as Pakistan (1999), Thailand (2006),

and Bangladesh (2007), has shown that while coups were initially welcomed by the public as a means of

restoring stability, the armed forces lost support within six to twelve months, leading to calls for new

elections.

Table: Middle East And Africa Defence & Security Ratings

Inter-state Terrorism CriminalComposite

domestic risk RankComposite

security risk Rank

UAE 84 83 78 81 1 82 1

Kuwait 88 76 79 77 2= 81 2

Jordan 85 71 77 74 4= 78 3

Saudi Arabia 80 68 81 74 4= 76 4=

South Africa 92 88 49 69 7 76 4=

Israel 62 61 79 70 6 67 6=

Turkey 76 60 65 63 8 67 6=

Uganda 64 66 55 61 9 62 8

Iran 28 79 74 77 2= 60 9

Egypt 64 58 39 49 10 54 10

Iraq 64 40 27 33 13 43 11

Syria 21 52 40 46 11 38 12=

Sudan 36 49 31 40 12 38 12=

Libya 39 35 30 33 13= 35 14

Yemen 37 33 29 31 15 33 15

Scores out of 100, with 100 the highest. The 'Composite Security Risk' is the principal rating. It comprises 'Interstate' risk- the risk of becoming a primary party to an inter-state conflict that threatens significant damage to homeland; 'Terrorism'risk - the risk of terrorist groups (domestic or international) being able to launch a major attack/sustained campaign; and'Criminal' risk - the risk of (politically motivated) violence against expatriate workers. Each of the three risks is given equalweighting. The 'Composite domestic risk' rating comprises 'Terrorism' and 'Criminal' risk, each of which is given equalweighting. Each rating (State, Terrorism, Criminal) is assessed subjectively by our analysts within a clearly definedmethodology, incorporating a minimum of six conceptually distinct elements. Source: BMI

Egypt Tourism Report Q2 2013

© Business Monitor International Page 26

Market Overview

Egypt's hotel industry is slowly recovering from the

impact of the Arab Spring in 2011 and a concomitant

drop in inbound tourism demand. Recent research

from hotel consultancy firm HVS Global would

indicate that 2012 saw a strong rebound in national

occupancy rates; however this was at the expense of

average room rates, which reportedly dropped by

just over 10%.

According to recent information from the Hotelier

Middle East website, there are some 16 major new

hotel projects under construction within Egypt at the

present time, which could add over 4,500 rooms to

the national supply when completed.

These include several properties being developed by

InterContinental Hotels Group (ICHG), such as

the 300-room Holiday Inn Alexandria West, the

418-room Crown Plaza Sharm El Sheikh Citystars and the 256-room InterContinental Sharm el Sheikh.

Marriott Hotels is also undertaking extensive renovation of the former Cairo Hilton, which is scheduled to

open in 2014 as the 331room Nile Ritz-Carlton Cairo, marking its debut in the Egyptian capital. Carlson

Rezidor is also reportedly due to open the 991-room Radisson Blu Sharm El Sheikh Lagoon later in 2013.

All of which indicates that sentiment towards the Egyptian hotel industry from the world's major hotel

chains remains positive, despite the risk of continued short-term political uncertainty. Many of the foreign

hotel chains are looking to partner with smaller, domestic firms for the development of their hospitality

operations in Egypt.

Visible Decline Due to PoliticalUpheaval

Number of Hotels ('000) and Hotel IndustryValue (US$bn), 2000-2017

Number of hotels and establishments, '000 (LHS)Hotels and restaurants industry value, US$bn (RHS)

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

e20

12e

2013

f20

14f

2015

f20

16f

2017

f

0

0.5

1

1.5

0

2.5

5

7.5

Source: CAPMAS/BMI/UN

Egypt Tourism Report Q2 2013

© Business Monitor International Page 27

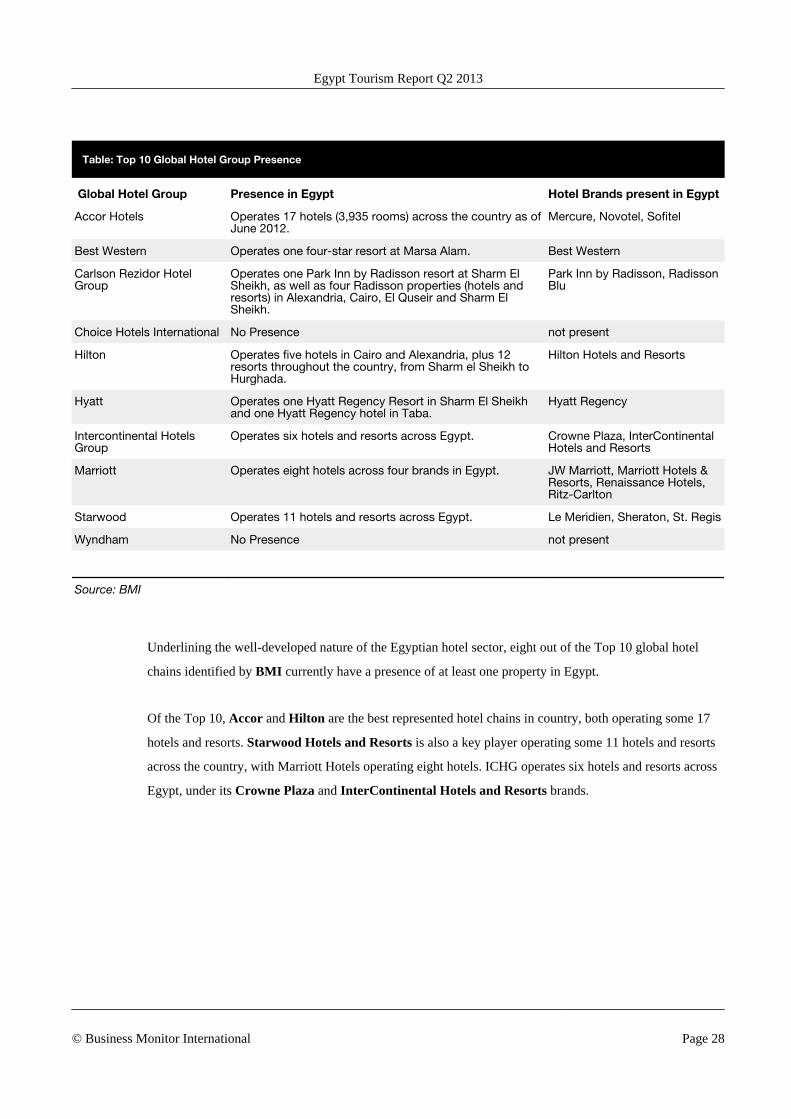

Table: Top 10 Global Hotel Group Presence

Global Hotel Group Presence in Egypt Hotel Brands present in Egypt

Accor Hotels Operates 17 hotels (3,935 rooms) across the country as ofJune 2012.

Mercure, Novotel, Sofitel

Best Western Operates one four-star resort at Marsa Alam. Best Western

Carlson Rezidor HotelGroup

Operates one Park Inn by Radisson resort at Sharm ElSheikh, as well as four Radisson properties (hotels andresorts) in Alexandria, Cairo, El Quseir and Sharm ElSheikh.

Park Inn by Radisson, RadissonBlu

Choice Hotels International No Presence not present

Hilton Operates five hotels in Cairo and Alexandria, plus 12resorts throughout the country, from Sharm el Sheikh toHurghada.

Hilton Hotels and Resorts

Hyatt Operates one Hyatt Regency Resort in Sharm El Sheikhand one Hyatt Regency hotel in Taba.

Hyatt Regency

Intercontinental HotelsGroup

Operates six hotels and resorts across Egypt. Crowne Plaza, InterContinentalHotels and Resorts

Marriott Operates eight hotels across four brands in Egypt. JW Marriott, Marriott Hotels &Resorts, Renaissance Hotels,Ritz-Carlton

Starwood Operates 11 hotels and resorts across Egypt. Le Meridien, Sheraton, St. Regis

Wyndham No Presence not present

Source: BMI

Underlining the well-developed nature of the Egyptian hotel sector, eight out of the Top 10 global hotel

chains identified by BMI currently have a presence of at least one property in Egypt.

Of the Top 10, Accor and Hilton are the best represented hotel chains in country, both operating some 17

hotels and resorts. Starwood Hotels and Resorts is also a key player operating some 11 hotels and resorts

across the country, with Marriott Hotels operating eight hotels. ICHG operates six hotels and resorts across

Egypt, under its Crowne Plaza and InterContinental Hotels and Resorts brands.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 28

Carlson Rezidor operates five properties across its

Park Inn by Radisson and Radisson Blu brands,

with Hyatt operating two Hyatt Regency properties

and Best Western just one resort at Marsa Alam.

Travco is Egypt's largest leisure group and is

engaged in a number of activities across the tourism

sector, including the operation of hotels, cruise liners

and travel agencies. Travco's hospitality

management company, Jaz Hotels, Resorts &

Cruises, owns and manages more than 73 hotels and

resorts across Egypt and the Middle East. The

company's brands include Jaz, Iberotel, Sol Y Mar

Hotels & Resorts, and Travcotels.

The state-owned Egyptian General Company for

Tourism and Hotels (EGOTH) oversees 14 hotels,

including the Cairo Marriott, the Palestine Hotel

(Alexandria) and the Mena House Oberoi, and one

Nile cruiser, as of August 2012. The company is

owned by HOTAC.

Given ongoing political uncertainty, it is little surprise that the authorities are not prioritising extensive

amounts of expenditure on Egyptian aviation infrastructure at the present time. The below table shows that

current and proposed airport infrastructure projects currently total just over US$1bn in Egypt, a smaller total

than in many of its regional peers.

Increasing Arrivals EncourageIncrease in InfrastructureConstruction Investment

Total Arrivals ('000) and Total Investment (US$bn), 2000-2017

TOTAL ARRIVALS: Total arrivals, '000 (LHS)INVESTMENT: Total capital investment, US$bn (RHS)

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

f20

14f

2015

f20

16f

2017

f

5,000

10,000

15,000

20,000

0 0

25

50

75

100

Source: Ministry of Tourism, Egypt/CAPMAS/BMI/Central

Bank of Egypt

Egypt Tourism Report Q2 2013

© Business Monitor International Page 29

Table: Egypt Transport Infrastructure Projects - Airports

ProjectName

Sector Value (US$mn)

Capacity/ Length Companies Timeframe Status

HurghadaInternationalAirport -constructionof newpassengerterminal

Airports 295 7.5 mn passengers Saudi Bin LadinGroup

na Contractawarded (Jan2010)

Cairo AirportT3 upgrade

Airports 387 7.5 mn passengers Limak 2011- Contractawarded(March 2011)

CairoInternationalAirport T2upgrade

Airports 400 8.5 mn passengers na Constructionscheduled forcompletion in2013

Bidding phase

Source: BMI Key Projects Database

Egypt is, however, making more of an effort to develop its domestic rail infrastructure. Although the

primary purpose of this is to improve the carriage of local residents and cargo across the country, improved

rail infrastructure could also have the side-effect of boosting tourism flows around the country. Certainly,

the proposed Cairo-Alexandria high speed railway could potentially see an increase in two-centre holidays

embracing both cities.

There are rail infrastructure projects presently totalling some US$7.7bn across Oman at the present time,

according to BMI's Key Projects Database.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 30

Company ProfileEgyptian General Company for Tourism & Hotels

Company Overview EGOTH belongs to the Egyptian government through 100% ownership by the Holding

Company for Tourism, Hotels & Cinema (HOTAC). Among the company's hotel

business are branded international establishments such as Marriott, Oberoi Hotels,

Sofitel and Mercure. In Q312, EGOTH property included 14 hotels throughout the

country (Luxor, Cairo, Giza, Alexandria and the Red Sea) and one Nile cruiser. The

group's hotel capacity amounts to approximately 3,750 rooms. The company shares in

18 joint ventures operating in the fields of tourism, hotels and tourist development.

EGOTH also owns plots of land at prime locations in Cairo, Luxor and Hurghada,

allocated for hotel and tourism development projects.

In November 2005, the former government announced plans to partially privatise five

hotels owned by EGOTH, following EGP407mn worth of upgrade and renovation work

to make them more attractive to potential investors. The sale of stakes in the Marriott

Cairo, Mena House Oberoi, Sofitel Cataract Aswan, Winter Palace Luxor and Helnan

Palestine Alexandria will not affect management contracts for the hotels.

Operational Data Key Statistics

■ No. of employees: 2,164 (FY2009/10)■ No. of rooms: approximately 3,750 (August 2012)■ Established: 1976

Company Details ■ EGOTH

■ 4 Latin America StreetGarden City

Cairo

Egypt

Egypt Tourism Report Q2 2013

© Business Monitor International Page 31

Travco

Company Overview Travco is Egypt's largest leisure group and is engaged in a number of activities across

the tourism sector, including the operation of hotels and travel agencies. Since 1995,

Travco has been 50% owned by German leisure conglomerate TUI. Travco's hospitality

management company, Jaz Hotels, Resorts & Cruises, owns and manages more than

73 hotels and resorts across Egypt and the Middle East under the following brands:

Jaz, Iberotel, Sol Y Mar Hotels & Resorts, and Travcotels. By mid-2012, Jaz Hotels,

Resorts & Cruises managed Egypt's largest chain of hotels (52) and a fleet of 20 cruise

liners, which provide regular services along the Nile.

In conjunction with the operators Alpitour Group Egypt and Touring International,

which are both Travco subsidiaries, Travco Travel also organises travel packages to

Egypt.

The Iberotel Hotels and Resorts subsidiary operated a chain of 20 hotels and resorts in

Egypt in mid-2012, and one hotel in Fujairah in the UAE.

In September 2009, Travco Group and UAE-based Air Arabia signed a joint venture

agreement to launch a new low-cost carrier based in Egypt. Air Arabic Egypt will serve

Europe, Africa and the Middle East markets and will represent Air Arabia's third hub

after UAE and Morocco.

In October 2009, as part of a plan to expand its international operations, Travco Group

acquired Frankfurt-based Steigenberger Hotels after three months of negotiation.

Steigenberger Hotels has over 6,500 employees and operates 79 hotels in Germany,

Austria, Switzerland, Italy, the Netherlands and Egypt. It operates two brands:

Steigenberger Hotels and Resorts, with four and five-star hotels; and InterCityHotel,

which has hotels in the upper mid-range. In 2008, Steigenberger generated revenues of

EUR494.9mn. The acquisition makes Travco Group one of the largest operators of

hotels in Europe and the Middle East with about 150 hotels and resorts.

From Q412, Steigenberger will start operating three luxury cruise ships on the Nile and

Lake Nasser in Egypt that were previously managed by Jaz Hotels, Resorts & Cruises.

Operational Data Key Statistics

■ No. of hotels (Egypt): 52 (mid-2012)■ No. of cruise ships: 20 (mid-2012)■ No. of employees: 11,000 (2007)■ Established: 1979

Company Details ■ Travco

■ 26th July CorridorSheikh Zayed

Egypt Tourism Report Q2 2013

© Business Monitor International Page 32

6th of October City

12588

Egypt

Egypt Tourism Report Q2 2013

© Business Monitor International Page 33

Global Industry Overview

BMI View: The global tourist accommodation sector will greatly benefit from the rise in international

tourist arrivals forecasted from 2013-2017. The growing number of outbound and domestic-based tourists

from Asia and Latin America has provided great incentives for the tourist accommodation sector to increase

the number of hotels and rooms on offer across these regions. Even though underlying economic risk

remains, over the next five years we estimate annual growth in total hotel units to be within 3-5% from

2013 to 2017.

Despite the difficult global economic picture, international tourist arrivals are expected to grow across 2013.

Historically the number of tourists has been rising year on year in eight out of the ten years from

2002-2012, the only fall being in 2009 due to the global economic crisis. In 2012, International tourist

arrivals grew by 4.3% in 2012, we saw positive growth stemming from a number of factors including

tourists taking advantage of a weaker euro to travel to eurozone states, as well as a growing middle class in

Asia who have an increasing inclination to travel abroad. We expect this trend to continue. BMI estimates

that international tourist arrivals will report growth of 4.1% at the end of 2013, an increase of 38.6 million

tourists to 971.1 million from 2012 across BMI's tourism universe. We forecast that annual growth in

international tourists arrivals will remain between 4-5% for the next five years from 2013 to 2017.

Table: Global Tourism Indicators, International Tourist Arrivals, 2009-2017

2009 2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

WORLD: Total Arrivals mn* 783.1 840.9 894.3 932.5 971.1 1019.1 1068.7 1121.1 1170.5

WOLRD: Total Arrivals mn,% change y-o-y -4.9 7.4 6.3 4.3 4.1 4.9 4.9 4.9 4.4

BMI

Growing tourist arrivals driving tourist accommodation

With international tourist arrivals set to grow from 2013-2017, the global tourist accommodation sector will

look to support the increase in number of tourists through the construction of new hotel units. Across the

world the tourist accommodation sector is likely to face stiff competition, and competitors look set to

enhance market share through pricing, aesthetics by introducing wide scale renovations and, mass branding

and marketing initiatives in the emerging markets. Over the last few years financial markets have seen an

inflow of capital and the tourist accommodation sector has taken advantage of this by taking the opportunity

Egypt Tourism Report Q2 2013

© Business Monitor International Page 34

to use leverage to initiate wide-ranging hotel renovations and construct new accommodation. Historically

the level of total hotel units globally has been volatile, 2010 posted an increase of 3.7%, in 2011 total units

slowed down to 0.9% and in 2012 total units increased again by 1.7%. Internationally we see the tourist

accommodation sector increasing the number of hotel units across 2013 by 2.2% to 1.099 million units in

total by the end of the year. From 2014-2017, BMI forecasts that annual growth in total hotel units to be

between 2-2.5%.

Table: global tourism indicators, hotel and establishment units, 2009-2017

2009 2010 2011 2012e 2013f 2014f 2015f 2016f 2017f

WORLD: Number of hotels

and establishments, '000* 1011.1 1048.8 1058.6 1076.5 1099.8 1124.0 1149.2 1176.6 1205.9

WORLD: Number of hotels

and establishments, '000,% change y-o-y 4.9 3.7 0.9 1.7 2.2 2.2 2.2 2.4 2.5

BMI

Regionally, Latin America is set to perform the best, with forecasted growth in total hotel units to be 4.32%

in 2013 and 4.35% in 2014. High numbers of growth are dominated by the growing trend in inbound

arrivals within the region, and the rise of domestic tourism in countries such as Brazil. Over the same

forecast period Brazil will see a surge in new hotel developments in preparation for the 2014 FIFA World

Cup to be staged in twelve cities across the country and 2016 Olympics to take place in Rio de Janeiro.

Over the last few years in the Asia-Pacific region there have been many large scale hotel development

projects. With rising middle classes in parts of Asia such as China and India, people are more likely than

ever to travel for leisure. The tourist accommodation sector in the region is likely to capitalize on the greater

number of outbound travellers from these countries and provide a greater number of hotels and facilities to

offer guests. In 2012, total hotel units increased by 153,358 or 3.8% from 2011. Over the next five years

from 2013 to 2017, BMI forecasts the region to grow over 4% annually. In isolation, total hotel units in

China and India have grown by an annual average of 12.87% and 18.36% respectively over the last five

years from 2012. This is on the back of strong rising levels of domestic tourists and international arrivals

that are now attracted by the better infrastructure and facilities on offer at hotels. For 2013 we forecast

annual growth of 9% for China and 13% for India. International hotel chains Marriot International,

Starwood Hotels & Resorts and Hilton Worldwide have outlined expansion plans in China. Starwood Hotels

& Resorts Worldwide, now have 100 hotels in the country and are another 100 have been outlined. Marriot

is looking to double its share of hotels within the country by 2014.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 35

Elsewhere, BMI estimates that total European hotel units will show annual growth of 0.5% for 2012. This

lower pace of growth is largely generated by a 0.1% fall in total hotel units across Western Europe for the

same period. Falls in domestic income have led to a decrease in domestic hotel demand and a shorter length

of stay by international guests have fallen under 4 nights in 2012 for the first time in ten years. Across the

region, many unprofitable hotel units have been closed and others have been relocated. Over the next five

years from 2013, we expect this trend to continue, and estimate total hotel units will grow in the range of

0.5-1% annually. In the Middle East, BMI estimates a bounce back in hotel construction in 2013 buoyed by

a general lift in construction activity within the region, total hotel units will increase by 2.1%.

Hotel rooms also set to increase

For 2013, BMI forecasts that the total number of hotels rooms internationally will grow by 3.3%. The

growth in the total number of rooms will be boosted twofold, firstly by new hotel construction which will

increase the global stock levels of rooms and secondly by the restructuring and renovation of existing hotel

units that will provide greater rooms. BMI forecasts strong growth in the total number of hotel rooms in

Latin-America to be 5-8% annually over the next five years from 2013 to 2017. In other regions Europe will

grow by 1.5-2%, North America by 1.5-1.6%, Asia by 2-5% and the Middle East by 2-5% over the same

forecast horizon.

Room occupancy rates to remain steady

Hotel room occupancy rates remain traditionally high in city based states and locations due to the lack of

availability of new land for new hotel construction. Singapore and Hong Kong remain the best with rates of

86.5% and 82.37% recorded in 2011 and BMI estimates this to be around this level at the end of 2012 and

going forward into 2013. Regionally higher occupancy rates are seen in Asia, Europe and North America.

Globally occupancy rates are estimated to remain between 50-60% over the next five years from 2013 to

2017, where growing room occupation will be counteracted by growth in hotel rooms.

Overnights stays rising in Asia and Middle East

At the end of 2011 total overnight stays internationally saw contractions of 1.6% in North America and

1.9% in Europe from 2010. Africa also noted a contraction of over 6% during the same period with only

Asia, Middle East and Latin America showing growth. Trends in Europe and North America remain

subdued with hotels in major western cities a lot pricier than emerging market equivalents. In 2012, average

length of stay in Western Europe decreased to under 4 nights, the lowest it has been in a decade. We expect

this trend to continue and forecast average length of stay to remain under 4 nights from 2013 to 2017.

Egypt Tourism Report Q2 2013

© Business Monitor International Page 36

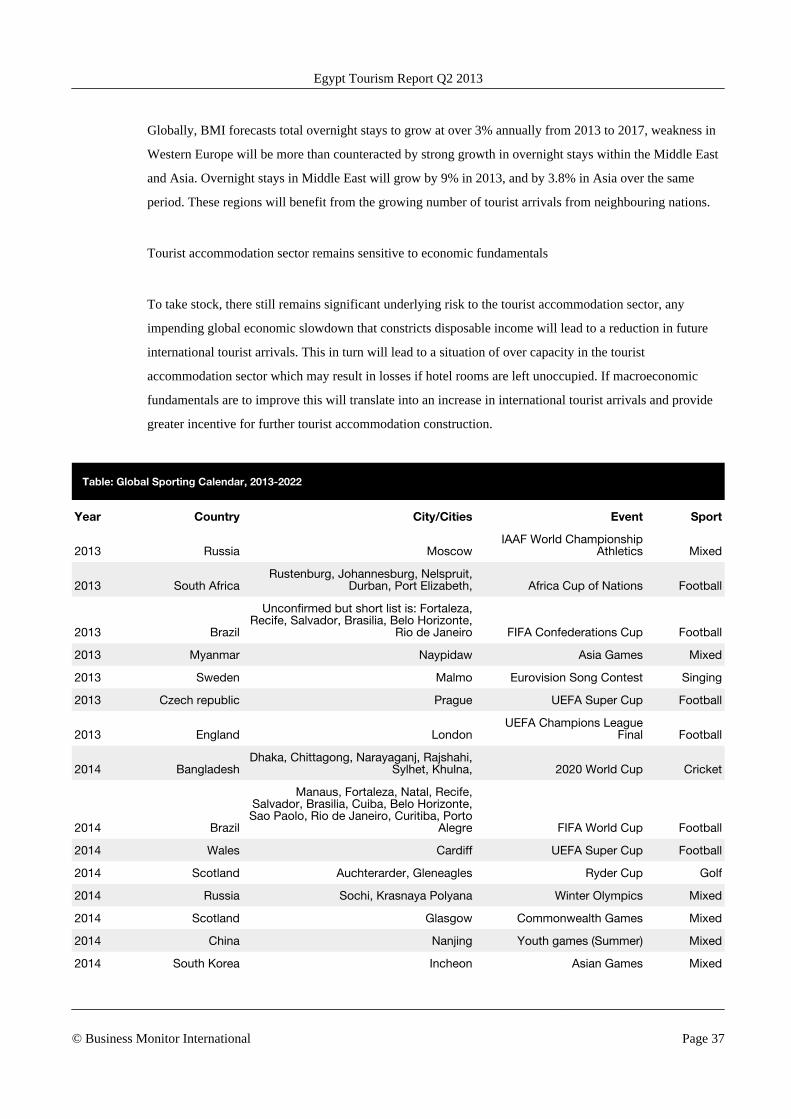

Globally, BMI forecasts total overnight stays to grow at over 3% annually from 2013 to 2017, weakness in

Western Europe will be more than counteracted by strong growth in overnight stays within the Middle East

and Asia. Overnight stays in Middle East will grow by 9% in 2013, and by 3.8% in Asia over the same

period. These regions will benefit from the growing number of tourist arrivals from neighbouring nations.

Tourist accommodation sector remains sensitive to economic fundamentals

To take stock, there still remains significant underlying risk to the tourist accommodation sector, any

impending global economic slowdown that constricts disposable income will lead to a reduction in future

international tourist arrivals. This in turn will lead to a situation of over capacity in the tourist

accommodation sector which may result in losses if hotel rooms are left unoccupied. If macroeconomic

fundamentals are to improve this will translate into an increase in international tourist arrivals and provide

greater incentive for further tourist accommodation construction.

Table: Global Sporting Calendar, 2013-2022

Year Country City/Cities Event Sport

2013 Russia MoscowIAAF World Championship

Athletics Mixed

2013 South AfricaRustenburg, Johannesburg, Nelspruit,

Durban, Port Elizabeth, Africa Cup of Nations Football

2013 Brazil

Unconfirmed but short list is: Fortaleza,Recife, Salvador, Brasilia, Belo Horizonte,

Rio de Janeiro FIFA Confederations Cup Football

2013 Myanmar Naypidaw Asia Games Mixed

2013 Sweden Malmo Eurovision Song Contest Singing

2013 Czech republic Prague UEFA Super Cup Football

2013 England LondonUEFA Champions League

Final Football

2014 BangladeshDhaka, Chittagong, Narayaganj, Rajshahi,

Sylhet, Khulna, 2020 World Cup Cricket

2014 Brazil

Manaus, Fortaleza, Natal, Recife,Salvador, Brasilia, Cuiba, Belo Horizonte,Sao Paolo, Rio de Janeiro, Curitiba, Porto

Alegre FIFA World Cup Football

2014 Wales Cardiff UEFA Super Cup Football

2014 Scotland Auchterarder, Gleneagles Ryder Cup Golf

2014 Russia Sochi, Krasnaya Polyana Winter Olympics Mixed

2014 Scotland Glasgow Commonwealth Games Mixed

2014 China Nanjing Youth games (Summer) Mixed

2014 South Korea Incheon Asian Games Mixed

Egypt Tourism Report Q2 2013

© Business Monitor International Page 37

Global Sporting Calendar, 2013-2022 - Continued

Year Country City/Cities Event Sport

2014 Portugal LisbonUEFA Champions League

Final

2015Australia andNew Zealand Not Decided Cricket World Cup Cricket

2015 England

Cardiff, London, Birmingham, Brighton,Bristol, Coventry, Derbyy, Gloucester,Leeds, Leicester, Manchester, Milton

Keynes, New Castle, Southampton,Sunderland Rugby World Cup Rugby

2015 CanadaVancouver, Edmonton, Winnipeg, Ottawa,

Montreal, and Moncton FIFA Women's World Cup Football

2015 Canada Toronto Pan American Games Mixed

2015 MoroccoCasablanca, Rabat, Fes, Marrakesh,

Tangier, Agadir Africa Cup of Nations Football

2015 Georgia Tibilisi UEFA Super Cup Football

2015 Singapore Not Decided Asian Games Mixed

2015 Australia Melbourne, Sydney Brisbane Canberra Asia Cup Football

2016 FranceLens, Lille, Paris, Bourdeaux, Lyon,

Marseille, Nice, Toulouse, St-Etienne UEFA Euro Football

2016 Brazil Rio de Janeiro Olympics Mixed

2016 India Not Decided 2020 World Cup Cricket

2016 USA Chaska Ryder Cup Golf

2016 Norway Lillehammer Youth Games (Winter) Mixed

2017 Libya Not Decided Africa Cup of Nations Football

2017 England LondonIAAF World Championship

Athletics Mixed

2017 Russia Moscow, Kazhan, Sochi, St Petersburg FIFA Confederations Cup Football

2018 Russia

Kaliningrad, Kazan, Krasnodar, Moscow,Nizhny Novgorod, Rostov-on-Don, Saint

Petersburg, Samara, Saransk, Sochi,Volgograd, Yaroslavl, Yekaterinburg FIFA World Cup Football

2018 South Korea Pyeongchang Winter Olympics Mixed

2018 Australia Gold Coast City Commonwealth Games Mixed

2018 France Paris Ryder Cup Golf

2019England &

Wales Not Decided Cricket World Cup Cricket

2019 JapanTokyo, Sapporo, Yokohama, Osaka,

Toyota, Kobe, Fukuoka, Sendai Rugby World Cup Rugby

2020 USA Sheboygan Ryder Cup Golf

2021 Qatar Not Decided FIFA Confederations Cup Football

Egypt Tourism Report Q2 2013

© Business Monitor International Page 38

Global Sporting Calendar, 2013-2022 - Continued

Year Country City/Cities Event Sport

2022 QatarAl-Khor, Doha, Ash-Shamal, Al Wakrah,

Umm Salar, Al Rayyan FIFA World Cup Football

Source: BMI Key Projects Database

Egypt Tourism Report Q2 2013

© Business Monitor International Page 39

Global Assumptions

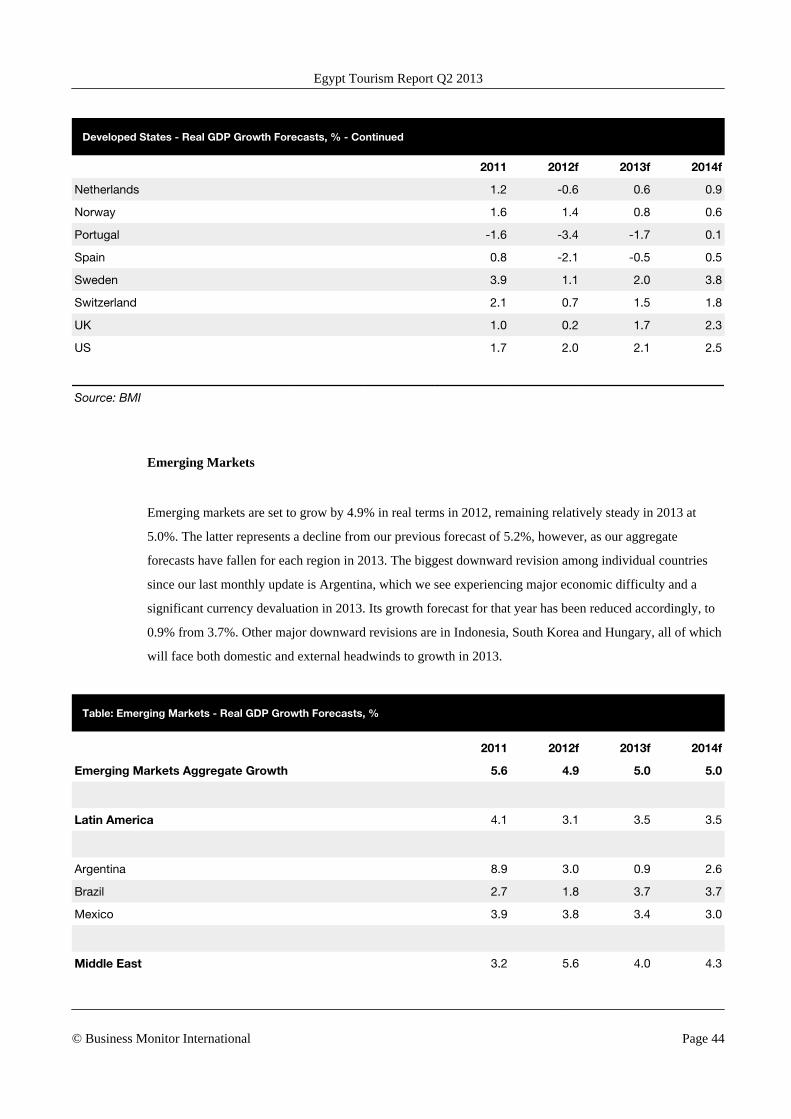

Our global aggregate real GDP growth forecast for 2012 remains 2.6%, though it has dipped slightly for

2013 to 3.0% from 3.1% previously. Our overall outlook on the global economy remains unchanged. Most

of our high-frequency global indicators suggest that output growth is slowing and global trade is stagnant at

best, while demand and confidence are at cyclically low levels. Inflation continues to trend down as well.

Since mid-2010, we have argued that the global economy is on the cusp of recession but that it would

probably take a major policy error to tip it over the edge. The potential for recession still looms large, with

China facing a hard landing amid a major economic transition, the eurozone contracting and the US facing a

fiscal emergency in the new year.

Table: Global Assumptions

2011 2012f 2013f 2014f 2015f 2016f 2017f

Real GDP Growth (%)

US 1.7 2.0 2.1 2.5 2.5 2.3 2.4

Eurozone 1.6 -0.6 0.6 1.4 1.7 1.9 1.9

Japan -0.7 1.5 1.2 1.2 1.2 1.2 1.3

China 9.1 7.5 7.1 6.0 6.0 6.1 6.0

World 3.1 2.6 3.0 3.3 3.5 3.5 3.5

Consumer Inflation (ave)

US 3.0 2.1 2.0 2.0 2.2 2.2 2.3

Eurozone 2.6 2.0 1.7 1.8 1.9 2.1 2.2

Japan -0.2 0.1 0.4 0.8 1.3 1.8 2.3

China 5.6 3.0 3.0 2.9 2.8 2.7 2.7

World 4.1 3.4 3.3 3.2 3.2 3.2 3.3

Interest Rates (eop)

Fed Funds Rate 0.00 0.00 0.00 0.00 0.00 1.00 2.25

ECB Refinancing Rate 1.00 0.50 0.50 0.50 0.50 1.00 1.50

Japan Overnight Call Rate 0.10 0.10 0.10 0.10 0.10 0.25 0.50

Egypt Tourism Report Q2 2013

© Business Monitor International Page 40

Global Assumptions - Continued

2011 2012f 2013f 2014f 2015f 2016f 2017f

Exchange Rates (ave)

US$/EUR 1.39 1.27 1.22 1.20 1.20 1.20 1.20

JPY/US$ 79.74 78.00 75.00 78.00 82.25 84.75 85.25

CNY/US$ 6.46 6.35 6.45 6.55 6.60 6.60 6.60

Oil Prices (ave)

OPEC Basket (US$/bbl) 107.52 107.05 99.10 96.15 95.20 93.25 93.30

Brent Crude (US$/bbl) 111.05 110.00 102.00 99.00 98.00 96.00 96.00

Source: BMI

Stimulatory policy looks to be confined to the monetary rather than fiscal side for the foreseeable future. In

line with our long-standing view, the latter part of 2012 has seen an impressive degree of monetary

stimulus, with the European Central Bank (ECB), the US Federal Reserve (Fed) and the Bank of Japan

(BoJ) all announcing newly accommodative policies in September. The Fed took the biggest step with

'QE3': it will commence open-ended purchases of mortgage-backed securities of US$40bn a month until

'after' the economy improves, and indicated that the Fed funds rate would be anchored at 0-0.25% until at

least mid-2015. The BoJ also decided to expand its government bond buying programme. The ECB,

meanwhile, has revealed a framework allowing unlimited sterilised government bond purchases focused at

the short end of the yield curve, dependent on a sovereign issuer committing to a formal macroeconomic

adjustment programme. In addition, there will be no explicit cap on bond yields, the central bank will

surrender its preferred creditor status and the Securities Market Program will expire. We have pushed back

our expectations for central bank tightening accordingly, with the first Fed funds and ECB refi rate hikes

only in 2016, as opposed to 2014 in our previous set of forecasts. While these measures will not solve the