TOTVS S.A. - DFP 2016_ENG_final.pdf · TOTVS Digital is a completely new digital environment,...

77

(A free translation of the original in Portuguese) TOTVS S.A. Financial Statements December 31, 2016 and 2015

Transcript of TOTVS S.A. - DFP 2016_ENG_final.pdf · TOTVS Digital is a completely new digital environment,...

(A free translation of the original in Portuguese)

TOTVS S.A. Financial Statements

December 31, 2016 and 2015

2

Contents

Management report and comments on company’s performance ........................................ 3

Independent auditor’s report on the financial statements ..................................................13

Report of the audit committee ...........................................................................................19

Financial statements ........................................................................................................22

Balance sheets .............................................................................................................................. 22

Statement of income ...................................................................................................................... 23

Statement of comprehensive income ............................................................................................ 24

Statements of changes in shareholders’ equity ............................................................................ 25

Statements of cash flow ................................................................................................................ 26

Statements os value added ........................................................................................................... 27

Notes to the financial statements .................................................................................................. 28 1. Operations ............................................................................................................................................ 28

2. Basis of Preparation and Summary of the Main Accounting Practices ................................................. 28

3. Business combination ........................................................................................................................... 35

4. Financial instruments and sensitivity analysis of financial assets and liabilities .................................... 38

5. Cash and cash equivalents ................................................................................................................... 44

6. Trade accounts receivable .................................................................................................................... 45

7. Stocks ................................................................................................................................................... 46

8. Taxes recoverable ................................................................................................................................. 46

9. Income and social contribution taxes .................................................................................................... 46

10. Related-party balances and transactions ............................................................................................ 48

11.Investments .......................................................................................................................................... 51

12 .Property, plant and equipment ............................................................................................................ 53

13. Intangible assets ................................................................................................................................. 55

14. Payroll and labor obligations ............................................................................................................... 59

15. Loans and financing ............................................................................................................................ 59

16. Debentures ......................................................................................................................................... 61

17. Liabilities due to investment acquisition .............................................................................................. 62

18. Provision for contingencies related to legal proceedings .................................................................... 63

19. Equity .................................................................................................................................................. 68

20. Dividends and Interest on Equity......................................................................................................... 69

21. Stock option plan................................................................................................................................. 70

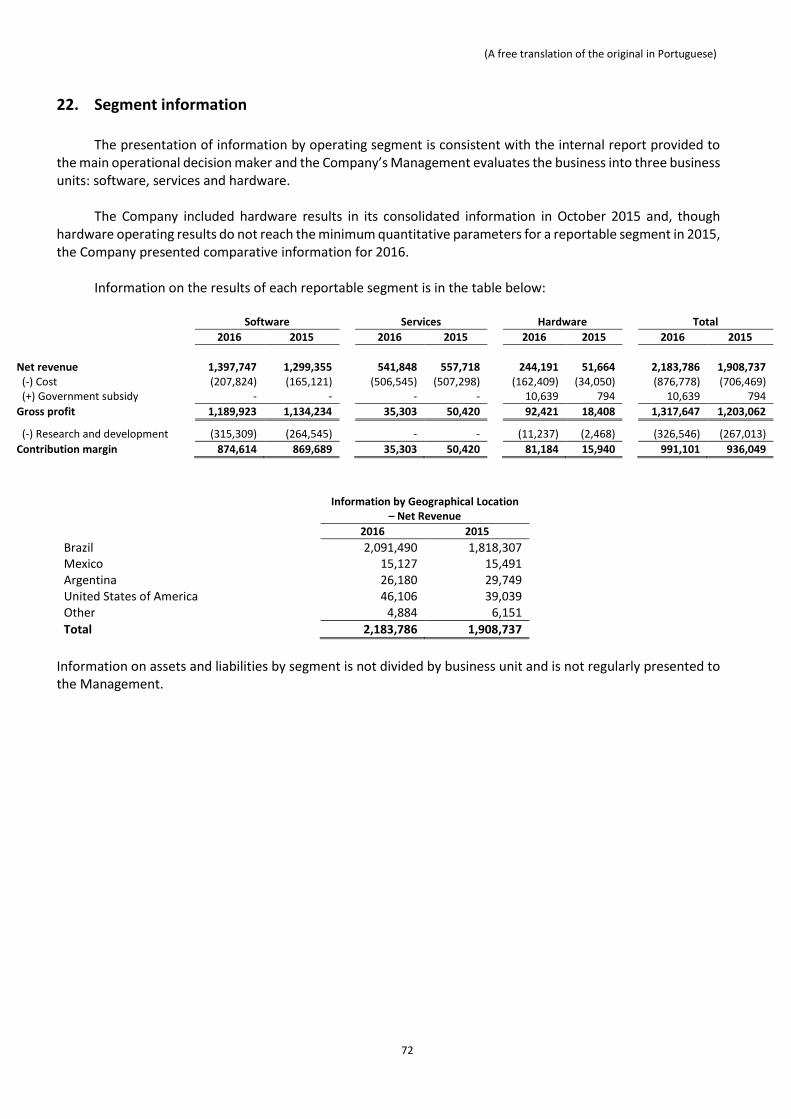

22. Segment information ........................................................................................................................... 72

23. Earnings per share ............................................................................................................................. 73

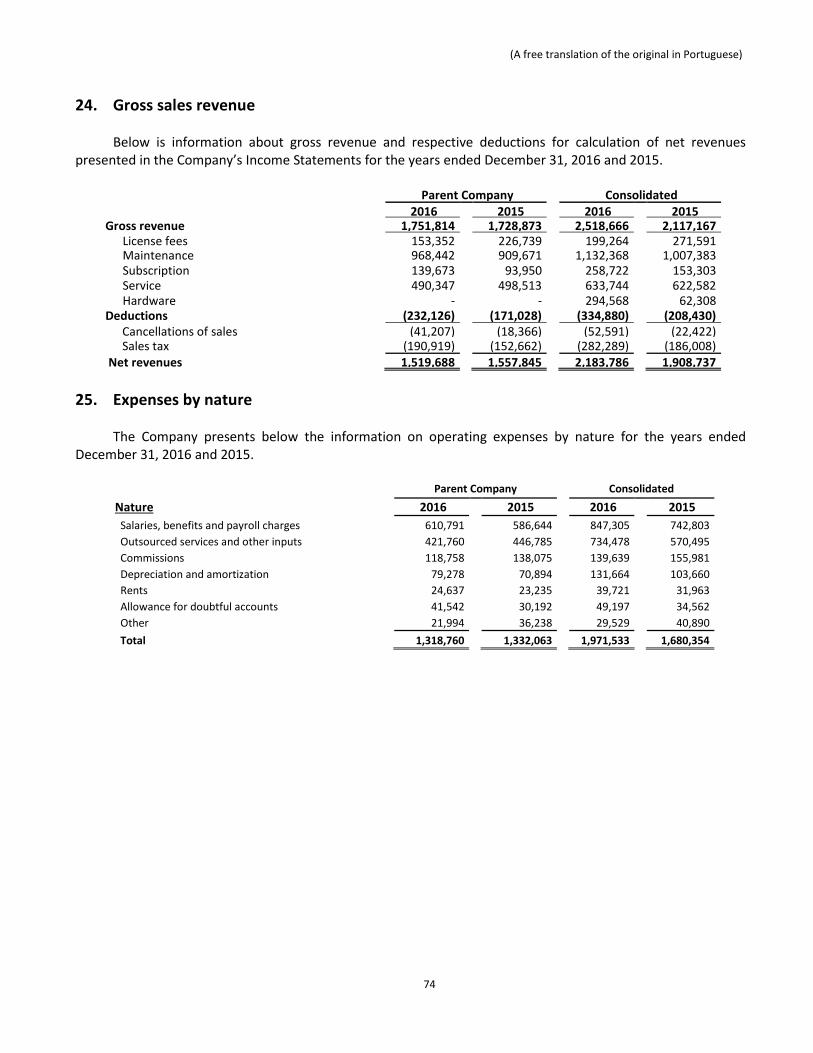

24. Gross sales revenue .......................................................................................................................... 74

25. Expenses by nature ............................................................................................................................ 74

26. Financial income and expenses .......................................................................................................... 75

27. Private pension plan – defined contribution ........................................................................................ 75

28. Commitments assumed ...................................................................................................................... 76

29. Non-cash items ................................................................................................................................... 76

30. Insurance coverage ............................................................................................................................. 77

3

MANAGEMENT REPORT AND COMMENTS ON COMPANY’S PERFORMANCE

Dear Shareholders,

Pursuant to legal provisions, TOTVS S.A., the largest developer of application software,

collaboration and productivity platforms, hardware and consulting services in Brazil and Latin

America, submits for the appreciation of its shareholders the Management Report and the

corresponding Financial Statements, accompanied by the independent auditor's opinion for the

fiscal years ended December 31, 2016 and 2015, prepared in accordance with the accounting

practices adopted in Brazil.

MESSAGE FROM THE CHAIRMAN OF THE BOARD OF DIRECTORS

In 2016, we reinforced the Company's corporate governance structure with the publication of our first Integrated Reporting and the creation of the Governance and Designation Committee. The main objectives of this committee are to evaluate the adoption of good corporate governance practices and evaluate the appointment of new members to the Board of Directors and to the Senior Executive Team of TOTVS.

We renewed a part of the vice-presidents and officers in 2016, with the hiring of new executives aligned to the culture of a subscription-based company, as part of the Company's succession plan. Today, we have a collaborative, digital and results-driven team that uses technology and business knowledge to promote innovation and understands that the client success is also our success.

We will continue our journey to turn TOTVS into a Single Subscription Company, developing solutions for clients of our clients and increasingly connecting people, things and businesses. As Brazil's leading technology provider, we aim to help companies to rethink the way they do business and how they can become more agile and competitive.

MESSAGE FROM THE CEO

TOTVS registered significant progress in its transition from the licensing model to the software

subscription model in 2016. This progress is evidenced by the 21.4% growth in subscription revenue,

which contributed to the stability of the software revenue in the year, despite the worsening

economic scenario observed throughout the period.

We made progress in integrating Bematech operations and expanded our market share in the

micro segment with the launch of Bemacash, a solution that combines the management software

Fly01 of TOTVS with Bematech’s hardware solutions, and Fly01 Start, an agnostic application that

functions as a point-of-sale integrated with the new generation of payment terminals. We also

4

intensified our investments in the specialization of our solutions, in mobile and cloud, developing

specialized solutions for clients of our clients, thus making the management of their businesses even

more efficient.

We evolved in the alignment of commercial incentives related to the subscription model, as

well as in the elaboration of a new marketing plan, increasingly digital, aiming to increase sales leads,

especially in the subscription model. We also made progress in the development of TOTVS Digital,

to be launched in the first quarter of 2017. TOTVS Digital is a completely new digital environment,

focused on the interaction between TOTVS, channels, salespeople, clients, prospects and partners.

The combination of these investments with the migration to subscription model and the

deterioration of the Brazilian economic scenario resulted in a decrease in the Company's

profitability, especially in the software and services businesses, leading to a reduction in the

contribution margins and, consequently, in the Company's EBITDA in 2016.

We will continue our journey to make TOTVS a “Single Subscription Company”, promoting the

digital transformation in our clients through specialized business solutions, digital platforms, cloud

infrastructure, mobility and the Internet of things. The progress made in the transition to

subscription over the last 18 months, combined with the Company’s investments and the

opportunities in Brazil, give us the confidence that TOTVS is on the right path to resume growth and

profitability in 2017.

ECONOMIC SCENARIO

The estimated global economic growth for 2016 indicated a deceleration compared to 2015,

especially due to the slowdown of the US economy and the growth deceleration in China, which

presented the lowest growth in the last 26 years.

In a context of growing uncertainties about the Brexit's success in June and the elections in

Germany and France in 2017, the growth in the Eurozone also slowed down in 2016, despite the

good performance of the economies of Germany and Spain. Latin America was negatively impacted

by the Mexican growth slowdown and the deterioration of the Brazilian economic scenario.

Brazilian GDP contracted again in 2016, contributing to the closure of 1.3 million formal jobs,

according to the General Register of Employed and Unemployed (Caged). Inflation measured by the

IPC-A closed the year at 6.29%, the lowest rate in the last three years and below the inflation target

set by the Central Bank. The Selic interest rate, which closed 2015 at 14.25%, reached 13.75% in

December 2016, while the US dollar depreciated 17.7% in the year against the Real, the first annual

decline since 2010.

5

The year was also marked by changes in the country's political landscape. In August, after a

nine-month process, President Dilma Rousseff was permanently removed from the Presidency and

replaced by the Vice-President Michel Temer. The appointment of Temer and the Lava-Jato

investigation triggered many changes in the Brazilian political-economic team. Henrique Meirelles

took over the Finance Ministry, replacing Nelson Barbosa, and Eduardo Cunha, then president of

the Chamber of Deputies, was removed from office and replaced by Rodrigo Maia.

Despite the negative effects of the economic crisis, Brazil continues to be a country with many

business opportunities, with a relevant consumer market and strong and independent institutions.

The reduction of internal political tensions, combined with the reduction of interest rates and

inflation, sustain the expectation of recovering from the recession and resume the Brazilian

economic growth for the next two years.

CONSOLIDATED OPERATING AND FINANCIAL PERFORMANCE

The comparability of the consolidated results for the years 2015 and 2016 is impacted by the

following events: (i) the corporate reorganization with Bematech, whose results were consolidated

by TOTVS in November 2015; and (ii) the sale of the wholly-owned subsidiary TOTVS Resultados em

Outsourcing Ltda. ("TOTVS RO"), which had its results consolidated by TOTVS until July 2016.

In 2016, net revenue totaled R$2,183,786 thousand, an increase of 14.4% over the previous

year. This growth was mainly due to the consolidation of Bematech's results in 2015. When

considering the 12-month Bematech result in 2015 (pro-forma), net revenue decreased by 3.5% in

2016, as shown in table below: Consolidated

2016

2015

(Pro-forma)

Variation

Licensing fees 167,759 245,937 -31.8%

Maintenance 1,000,753 965,949 3.6%

Subscription 229,235 188,790 21.4%

Services 541,848 593,571 -8.7%

Hardware 244,191 268,001 -8.9%

Net Revenues from services and sales 2,183,786 2,262,248 -3.5%

The reduction in revenues from licensing fees reflects the 25.8% decrease in the number of

sales. This reduction was mainly due to the following: (i) the downturn in economic activity in Brazil

in 2016, which lengthened the conversion period of the sales cycle, especially among large clients;

and (ii) the migration of a part of the sales pipeline of new clients to the subscription model,

especially smaller clients. In the other hand, the reduction in the average ticket is mainly associated

to sales to existing clients, because of the economic scenario.

6

The growth in maintenance revenue below the average IGP-M of 2016 was mainly due to the

following factors: (i) reduction of license sales in previous periods; (ii) contract cancellations due to

clients’ defaults; and (iii) partial contracts cancellations due to reductions in clients’ staff, especially

large clients.

The growth in subscription revenue was due to the higher share of sales to new small and

medium clients, especially under the TOTVS Intera model (subscription model launched in June

2015). In addition to TOTVS Intera subscription, Bemacash sales also contributed to the growth in

subscription revenue in 2016. Bemacash is a solution that combines TOTVS’ management software

for microenterprises (Fly01 line), contracted under the subscription model, and the automation and

tax hardware solutions from Bematech.

Services revenue in 2016 was negatively affected by: (i) the reduction in software

implementation services, due to the lower sales pace observed during the year; (ii) to the lower

level of sales of consulting services; and (iii) the sale of TOTVS RO in August 2016.

The reduction in hardware revenue in 2016 was mainly due to the downturn in the economic

activity in Brazil and the changes in tax legislation, especially in the state of São Paulo where fiscal

printer were replaced by S@T fiscal equipment, which has a lower unit value.

One of the key elements of the Company's strategy is to offer specialized business solutions by segment

and integrated with back office solutions and the management and business platform. Please find below

the revenue breakdown by industry sector.

The Manufacturing segment accounted for

24.4% of TOTVS’ total net revenue in 2016. This

segment contributes significantly to the

integration of value chains (Ex: Distribution &

Logistics, Retail and Credit). In addition, this

segment has significant opportunities for adoption

of digital technologies related to the era of

advanced manufacturing - the so-called Industry

4.0 - whose purpose is to encourage the digital

integration of different stages of the value chain of

industrial products, from the development to the

use of these products.

The Retail segment accounted for 23.5% of total revenue in 2016. After the corporate

reorganization with Bematech, TOTVS became the largest provider of business solutions to this

segment in Brazil, besides expanding its share of the microenterprises market with the Bemacash,

Fly01 and Fly01 Start solutions.

7

When considering Bematech's 12-month results in 2015 (pro-forma), operating costs and

expenses presented behavior as shown in the following table: Consolidated

2016

2015

(pro-forma)

Variation

Cost of Software (77,284) (83,472) -7.4%

Cost of Support (130,540) (112,248) 16.3%

Cost of Services (506,545) (545,771) -7.2%

Cost of Hardware (162,409) (170,151) -4.6%

Research and Development (326,546) (292,656) 11.6%

Advertising and Marketing Expenses (47,029) (57,261) -17.9%

Commercial Expenses (203,818) (188,386) 8.2%

Commissions Expenses (139,639) (160,111) -12.8%

General and Administrative Expenses (204,532) (228,453) -10.5%

Management Fees (19,176) (29,146) -34.2%

Depreciation and Amortization Expenses (128,350) (114,970) 11.6%

Allowance for Doubtful Accounts (49,197) (38,791) 26.8%

Government Subsidy 10,639 15,991 -33.5%

Other revenues (expenses) 12,893 (4,209) -406.3%

Custos e despesas operacionais (1,971,533) (2,009,634) -1.9%

The cost of software reduction in 2016 reflects the drop in licensing fees sales and the

transition to the subscription model, as partners for complementary solutions are remunerated

according to the business model that TOTVS practices to its clients.

The growth in support costs in the year is mainly due to the investments made in improving

the customer service and support processes, involving adjustments to routines, teams and the

Company's service tools.

The reduction in the cost of services in 2016 is mainly a result of the lower personnel

expenditure, including layoffs for the cost structure adjustments, net of the collective wage

increases that occurred during the year.

The decrease in hardware costs in 2016 is mainly due to the reduction in hardware sales in

the year and to the appreciation of the Brazilian Real against the US dollar, which is an important

variable in the cost formation of components used in the hardware production. It is worth

mentioning that the cost of hardware in 2016 also includes depreciation expenses, in the amount

of R$3,314 thousand (R$3,891 thousand pro-forma in 2015).

The growth in research and development expenses in the year mainly reflects the wage

adjustments resulting from collective bargaining agreements occurred during the year, the

investments in the integration of the solutions portfolio of Bematech to TOTVS.

8

The year-on-year reduction in advertising expenses mainly reflects the revision of the general

marketing plan of the Company and the synergies from integration of marketing activities of TOTVS

and Bematech.

Selling expenses and commissions jointly increased from 15.4% (pro-forma) to 15.7% of net

revenue. These expenses are directly related to the change in sales mix between franchises and own

branches, as well as related to the net revenue mix, due to the different levels of variable

remuneration and commissioning applied to the revenue lines.

The reduction in general and administrative expenses in 2016 is mainly due to the net effect

of wage increases for the period and the lower amount of supplementary provision for

contingencies made during the year, as a consequence of the review of the past outcomes of

lawsuits and the circumstances surrounding the new proceedings in which TOTVS is the defendant.

The decrease in management fees for the year resulted primarily from the optimization of

the Company's administrative structure, the integration of Bematech operations, as well as the

provisioning of bonuses associated to the achievement of the financial and individual goals for the

executives in the period.

The increase in depreciation and amortization expenses in 2016 resulted mainly from the

amortization of intangible assets from the corporate reorganization with Bematech and the

depreciation of investments made in infrastructure such as equipment and installations.

Allowance for doubtful accounts corresponded to 2.3% of net revenue in 2016, compared to

1.7% in 2015 (pro-forma). The increase in this provision is mainly due to the additional provision of

R$17,221 thousand related to the higher credit risk of a large client from the services segment.

Below is a reconciliation of the profit before financial effects and consolidated equity pick and

consolidated pro-forma for the year 2015:

CONCILIATION OF CONSOLIDATED PRO-FORMA PROFIT 2015

(A)

Consolidated

(B)

Bematech

(Nov-Dec)

(C)

Bematech

(Jan-Dec)

(A – B + C)

Consolidated

(pro-forma)

Net revenue from services and sales 1,908,737 80,483 433,994 2,262,248

Operational costs and expenses (1,680,354) (76,374) (405,654) (2,009,634)

Income before financial effects and

equity pick up 228,383 4,109 28,340 252,614

The variation of the financial result from positive R$26,526 thousand in 2015 to negative of

R$36,732 thousand in 2016 is mainly due to: (i) the change in the Company’s capital structure, from

a net cash position in 3Q15 to net debt in 4Q15, due to the payment of R$473,585 thousand in the

corporate reorganization with Bematech in the 4Q15; (ii) the gain from the sale of the minority

9

interest in ZeroPaper in 1Q15; and (iii) the higher Long-term Interest Rate (TJLP) in 2016, which is

used as the inflation adjustment index for the main financial costs of most financing lines and

debentures.

Income Tax and Social Contribution expenses decreased by 61.2% in 2016, totaling R$23,252

thousand. This reduction is mainly due to the decrease in the income before income tax and social

contribution and to the greater representativeness of interest on equity when compared to income

before tax and social contribution in the period.

Net Income decreased by 21.9% in 2016, mainly due to: (i) the 7.1% reduction in profit before

financial effects and equity pick up; (ii) the negative financial result for the year; and (iii) the

reduction of expenses with Income Tax and Social Contribution.

EBITDA(*) for 2016 totaled R$343,917 thousand, 7.4% lower than the Pro-forma EBITDA for

2015. Adjusted EBITDA for 2016 totaled R$358,728 thousand, 21.5% lower than the Pro-forma

Adjusted EBITDA for 2015. The Adjusted EBITDA margin ended 2016 at 16.4%, compared to 20.2%

in 2015. The evolvement of the subscription model, combined with labor inflation and investments

in portfolio integration and customer service, essentially explain this reduction in margin.

(*) EBITDA is a non-accounting measure prepared by the Company and consists of net income for the year, plus

income taxes, financial expenses net of financial revenues, and depreciation and amortization. Adjusted EBITDA represents

EBITDA, net of extraordinary effects related to layoffs from the organizational restructuring, additional provisions for

contingencies and doubtful accounts, reversal of provision for acquisitions, gain on the sale of equity interests, provision

for impairment and expenses related to the corporate reorganization with Bematech.

CAPITAL MARKETS

TOTVS ended the year with capital of R$541,374 thousand, same amount of 2015. At the end

of 2016, the capital stock of the Company was composed of 165,637,727 common shares, with

66.9% of free float, of which 97.4% was held by institutional investors and 92.9% by foreign

investors.

Free float is calculated as the total number of Company shares, excluding shares owned by

Management and related persons, Fundação Petrobras de Seguridade Social (PETROS) and BNDES

Participações (BNDESPar), and those held in treasury.

In 2016, TOTVS shares (BM&FBovespa:TOTS3) depreciated 22.5%, while the Bovespa Index

(IBovespa) increased 38.9%. Average financial volume in 2016 stood at R$18.6 million/day, versus

R$21.0 million registered in the last two years.

10

Dividends for 2015: proposed by the Board of Directors on March 15, 2016, and approved at

the Ordinary General Meeting on April 26, 2016, dividends for the year totaled R$66,579 thousand,

to shareholders of TOTVS as of April 26, 2016. The dividends were paid on May 11, 2016.

Interest on equity for 2016: On August 1, 2016, the board of directors approved the payment

of interest on equity of R$43,605 thousand to its shareholders related to the first semester of 2016,

having made entitled do the benefit the shareholders of TOTVS as such on August 4, 2016. The

interest on equity were paid on August 24, 2016.

On December 16, 2016, the board of directors approved the payment of interest on equity of

of R$40,615 thousand to its shareholders related to the second semester of 2016, having made

entitled do the benefit the shareholders of TOTVS as such on December 21, 2016. The interest on

equity were paid on May 10, 2017.

The payment regarding the fiscal year of 2016 and were imputed to the minimum mandatory

dividend in accordance with Article 34 of TOTVS’ Bylaws.

Interest on equity for 2015: On December 18, 2015, the board of directors approved the

payment of interest on equity of R$31,319 thousand for the second semester of 2015, having made

entitled do the benefit the shareholders of TOTVS as such on December 21, 2015. This interest on

equity was paid on January 13, 2016.

The payment is for the second half of 2015 and the amount was calculated towards the

minimum mandatory dividend in accordance with Article 34 of the Bylaws of TOTVS.

CORPORATE GOVERNANCE

Novo Mercado: TOTVS was the first Brazilian software company to join the segment that

meets the highest corporate governance standards of the São Paulo Stock Exchange

(BM&FBovespa).

Board of Directors: TOTVS’ Board of Directors is composed of 9 members, of which 8 of them

are external and independent members, in accordance with Novo Mercado regulations. 11 officers

compose the Executive Board. The list containing the names, position and a brief resume of the

Board members and Executive Officers is available on the Company´s Reference Form, in

http://ir.totvs.com.

Audit Committee: It is an advisory body to support the Board of Directors, and its mission is to monitor, evaluate and ensure the best operation of processes, management of internal and external audit mechanisms and controls related to risk management and consistency of financial policies with the strategic guidelines and business risk profile. Currently, the Audit Committee is composed

11

of 4 independent external members elected by the Board of Directors, chaired by an independent member of the Board of Directors.

Remuneration Committee: assists the Board in setting compensation policies and benefits

for directors, officers and participants. The company currently has 4 members elected by the Board

of Directors, of which 1 is external, and is chaired by an independent member of the Board of

Directors.

Governance and Designation Committee: Composed of 3 members of the Board of Directors,

its main duties are to promote changes in the Company's corporate governance, to evaluate the

adoption of good practices and to select and appoint members to the Board of Directors and the

Board of Executive Officers.

Arbitration: according to Novo Mercado Regulations and the Company’s Bylaws, the

controlling shareholder, administrators, the Company itself and the Fiscal Council members should

undertake to settle all and any dispute or controversy arising from or relating to Novo Mercado

Regulations, the Novo Mercado Adhesion Agreement, Arbitration Clauses, especially, regarding its

application, validity, effectiveness, interpretation, breach and their effects through arbitration.

Disputes regarding the sale of the Company’s control shall also be solved through arbitration.

Management Statement: in accordance with subparagraphs V and VI, Article 25 - CVM

Instruction 480/09, the officers of TOTVS declare that they discussed, reviewed and agreed with the

views expressed in the independent auditors' report and financial statements for the fiscal year

ended on December 31, 2016.

RELATIONSHIP WITH INDEPENDENT AUDITORS

The Company’s policy on engaging services not related to external audit by independent

auditors is grounded on the principles that preserve their autonomy. These principles consist of

internationally accepted standards, namely: (a) auditors must not audit their own work; (b) auditors

must not exercise management functions at their clients; and (c) auditors must not create conflicts

of interest with their clients.

Procedures adopted by the Company pursuant to item III, article 2 of CVM Instruction 381/03:

The Company and its subsidiaries adopt as a formal procedure, before hiring independent auditors

for professionals services not related to external audit, ensuring that the execution of these other

services does not affect their autonomy and objectivity necessary for the performance of

independent audit services, and obtaining the approval of their Audit Committee. In addition, formal

statements are requested from the auditors regarding their autonomy in the execution of services

not related to audit.

12

Other services were provided in addition to those related to the audit of financial statements

in 2016. The fees for these services totaled R$202,614 thousand and corresponded to 15.65% of

total fees related to external audit.

ACKNOWLEDGEMENTS

We thank all those who contributed to the success of TOTVS in 2016, especially our clients,

employees, partners and shareholders.

13

INDEPENDENT AUDITOR’S REPORT ON THE FINANCIAL STATEMENTS

To the Board of Directors and Stockholders TOTVS S.A. Opinion

We have audited the accompanying parent company financial statements of TOTVS S.A. ("Company"), which comprise the balance sheet as at December 31, 2016 and the statements of income, comprehensive income, changes in equity and cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies. We have also audited the accompanying consolidated financial statements of TOTVS S.A. and its subsidiaries ("Consolidated"), which comprise the consolidated balance sheet as at December 31, 2016 and the consolidated statements of income, comprehensive income, changes in equity and cash flows for the year then ended, and notes to the financial statements, including a summary of significant accounting policies. Opinion on the parent company financial statements In our opinion, the parent company financial statements referred to above present fairly, in all material respects, the financial position of TOTVS S.A. as at December 31, 2016, and its financial performance and cash flows for the year then ended, in accordance with accounting practices adopted in Brazil. Opinion on the consolidated financial statements In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of TOTVS S.A. and its subsidiaries as at December 31, 2016, and their financial performance and cash flows for the year then ended, in accordance with accounting practices adopted in Brazil and with the International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). Basis for opinion

We conducted our audit in accordance with Brazilian and International Standards on Auditing. Our responsibilities under those standards are further described in the Auditor's Responsibilities for the Audit of the Parent Company and Consolidated Financial Statements section of our report. We are independent of the Company and its subsidiaries in accordance with the ethical requirements established in the Code of Professional Ethics and Professional Standards issued by the Brazilian Federal Accounting Council, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

14

Key audit matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the parent company and consolidated financial statements of the current period. These matters were addressed in the context of our audit of the parent company and consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

Why it is a key audit matter How the matter was addressed in the audit

Measurement of revenue from consulting services or implementation software services rendered (Notes 2.8 and 24)

We decided to focus on this area in our audit because the measurement of revenue from consulting or software implementation services, which represents 3% of the total revenues for 2016, requires management to use estimates and critical judgment that are mainly related to the identification of the hours to be incurred up to the conclusion of the contracted services. This matter affects the measurement of unrecognized revenue in the year, yet to be billed.

Regarding the recognition of unbilled revenue, we performed the following procedures during our audit:

• We obtained an understanding of the main controls related to the revenue recognition and tested their effectiveness;

• We analyzed related documents, such as contracts and bills, and the subsequent financial settlement, which are evidence that can support the effective performance of the service, the proper accrual basis, and the correct amount of the related revenue;

• For the tested controls, we confirmed that the management's calculations of recognized revenue included the relevant aspects of the contracts' terms; and

• We inquired the Company's management and the commercial team in order to assess (i) the reasonableness of the data and criteria adopted to estimate revenue, and (ii) the uniformity of the criteria in comparison with those adopted in the previous year. In addition, we tested the comparison of this estimate with the revenue billed in the following month.

We consider that the measurement of the unbilled revenue and the estimates involved in the recording in the proper period are supported by data and corresponding documents.

15

Why it is a key audit matter How the matter was addressed in the audit

Provision for contingencies (Note 18)

As disclosed in the parent company and consolidated financial statements, the Company and its subsidiaries are party to legal and administrative civil, labor, and tax proceedings filed mainly by former employees, service providers, tax and labor authorities, and customers. The total accounted for, related to proceedings whose likelihood of loss is probable, amounts to R$ 102,225 thousand. We decided to focus on this matter in our audit because of the critical judgment necessary to determine the likelihood of loss attributed to each proceeding and the estimated amount of loss for them. This judgment as well as the criteria used to establish these amounts involve consideration about the complexity of the Brazilian legislation, of the applicable case law, and of the legal system itself. Any change in projections, judgment, or criteria used to attribute the amount may significantly affect the financial statements.

Regarding the provision for contingencies, we performed the following procedures during our audit, among others:

• We obtained an understanding of the main related internal controls and tested their effectiveness;

• We reviewed documents, on a sample basis, containing information related to contingent matters and with the respective proceedings involved;

• We obtained a confirmation from external legal advisors in order to validate the amounts as well as the likelihood of positive and/or negative outcome for each proceeding; and

• When necessary, we obtained a second opinion from legal advisors other than those who are working on the matters in order to compare them as well as to analyze the defense's arguments and/or thesis.

Because of these procedures, we consider that the criteria used by management to measure the provision for contingencies are adequate, and that the opinions and judgment used are consistent with the assessment of legal advisors.

Intangible assets, including goodwill - Impairment (Note 13.2)

Management assess the impairment of intangible assets, including goodwill. This assessment requires critical judgment regarding the determination of the future cash flows, which is projected as from the business plan approved by the Board of Directors. We decided to focus on this area in our audit because this assessment involves judgment regarding the financial and economic assumptions.

Regarding the measurement and presentation of intangible assets, including goodwill, in the context of an audit, we performed the following procedures, with the support of our internal experts on assessment: • Understanding of the main related controls and

testing of their effectiveness;

• Obtaining of management's business plan, as approved by the Board of Directors, regarding the acquired entity, which is the object of the generation of intangible assets and goodwill, and comparison with the assumptions used in the assessment;

• Comparison of the base year's balances used in the projection with the historical accounting information;

• Inquiring about the reasonableness of the methodology and of the main financial and

16

Why it is a key audit matter How the matter was addressed in the audit

economic assumptions used, such as discount rates, inflation, growth of income and expenses, investment, among others;

• Recalculation tests involving the projections prepared by management.

Our audit procedures evidenced that the assumptions used by management are reasonable and consistent with observable data and information.

Other matters

Statements of Value Added

The parent company and consolidated Statements of Value Added for the year ended December 31, 2016, prepared under the responsibility of the Company's management and presented as supplementary information for IFRS purposes, were submitted to audit procedures performed in conjunction with the audit of the Company's financial statements. The presentation of these Statements of Value Added is required by the Brazilian corporate legislation for listed companies. For the purposes of forming our opinion, we evaluated whether these statements are reconciled with the financial statements and accounting records, as applicable, and if their form and content are in accordance with the criteria defined in Technical Pronouncement CPC 09 - "Statement of Value Added". In our opinion, these Statements of Value Added have been properly prepared in all material respects, in accordance with the criteria established in the Technical Pronouncement, and are consistent with the parent company and consolidated financial statements taken as a whole.

Other information accompanying the parent company and consolidated financial statements and the auditor's report

The Company's management is responsible for the other information that comprises the Management Report. Our opinion on the parent company and consolidated financial statements does not cover the Management Report, and we do not express any form of audit conclusion thereon. In connection with the audit of the parent company and consolidated financial statements, our responsibility is to read the Management Report and, in doing so, consider whether this report is materially inconsistent with the financial statements or our knowledge obtained in the audit or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement in the Management Report, we are required to report that fact. We have nothing to report in this regard.

17

Responsibilities of management and those charged with governance for the parent company and consolidated financial statements

Management is responsible for the preparation and fair presentation of the parent company financial statements in accordance with accounting practices adopted in Brazil and of the consolidated financial statements in accordance with accounting practices adopted in Brazil and with the IFRS as issued by the IASB, and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error. In preparing the parent company and consolidated financial statements, management is responsible for assessing the ability of the Company and its subsidiaries to continue as going concerns, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company and its subsidiaries or to cease operations, or has no realistic alternative but to do so. Those charged with governance are responsible for overseeing the financial reporting process of the Company and its subsidiaries. Auditor's responsibilities for the audit of the parent company and consolidated financial statements

Our objectives are to obtain reasonable assurance about whether the parent company and consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditor's report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Brazilian and International Standards on Auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these parent company and consolidated financial statements. As part of an audit in accordance with Brazilian and International Standards on Auditing, we exercise professional judgment and maintain professional skepticism throughout the audit. We also: • Identify and assess the risks of material misstatement of the parent company and consolidated financial

statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

• Obtain an understanding of internal control relevant to the audit in order to design audit procedures that

are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the internal control of the Company and its subsidiaries.

• Evaluate the appropriateness of accounting policies used and the reasonableness of accounting

estimates and related disclosures made by management.

18

• Conclude on the appropriateness of management's use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the ability of the Company and its subsidiaries to continue as going concerns. If we conclude that a material uncertainty exists, we are required to draw attention in our auditor's report to the related disclosures in the parent company and consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditor's report. However, future events or conditions may cause the Company and its subsidiaries to cease to continue as going concerns.

• Evaluate the overall presentation, structure and content of the parent company and consolidated

financial statements, including the disclosures, and whether the parent company and consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

• Obtain sufficient appropriate audit evidence regarding the financial information of the entities or

business activities within the Group to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit. We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards. From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the parent company and consolidated financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditor's report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication. São Paulo, February 20, 2017 PricewaterhouseCoopers Ricardo Novaes de Queiroz Auditores Independentes Contador CRC 1DF012332/O-2 "S" SP CRC 2SP000160/O-5

(A free translation of the original in Portuguese)

19

REPORT OF THE AUDIT COMMITTEE

Introduction

In accordance with its charter, approved by the Board of Directors on February 27, 2015, the Audit Committee

is charged with ensuring that the internal and external audit processes and management, as well as the risk

management mechanisms and controls are functioning, ensuring the alignment of financial policies with the

strategic guidelines and risk profile of the business, and ensuring the quality and integrity of the Company's

financial statements, making recommendations to the Management regarding the approval of financial

reports and actions to improve internal controls and reduce risks.

The Audit Committee is formed by four members (three independent members and one external

independent member), who are currently in full exercise of their terms of office.

Activities of the Audit Committee

The Committee held nine (9) ordinary meetings and three (3) extraordinary meetings in 2016 and one (1)

ordinary meeting in 2017 to approve the financial statements. In this period, the Audit Committee also

periodically conducted private meetings with the chief legal officer, the risk, internal controls and compliance

officer and internal audit, as well as meetings with the human resources officer, the independent audit firm

and meetings among its members, totaling ten (10) meetings. At each ordinary meeting of the Board of

Directors, a report on the Committee’s activities in the previous period was presented by the Committee

Chairman and discussed with the directors.

Topics discussed by the Audit Committee

The Audit Committee held meetings with vice presidents and executive officers of the Company, internal

auditors, independent auditors and external advisors to understand the processes, internal controls, risks,

possible weaknesses and plans for improvement, and submitted its recommendations to the Board of

Directors and Management of the Company. A total of eighty-three (83) meetings were conducted to discuss

forty-two (42) topics. The main aspects discussed were:

Independent Audit - Discussing the plan, scope and main conclusions from the quarterly reviews (ITR) and issuing a report

on the financial statements for fiscal year 2016 (DFP 2016);

- Weaknesses and recommendations for improvements mentioned in the internal controls report and

the respective action plans of internal areas to correct or improve the aspects;

- Monitoring the preliminary and final results for issuing the ISAE 3402/2016 report;

- Learning about new audit procedures, especially the new audit report format;

- Annual cycle of appraisal of the performance of independent auditor;

- Selecting and discussing proposals and making recommendations regarding the hiring of

independent auditors for next year.

(A free translation of the original in Portuguese)

20

Internal Audit - Discussing the risk matrix and approval of internal audit schedule for the 2016 cycle; - Monitoring the reports on the work of internal audit issued for own units and franchises, including

weaknesses, justifications and correction plans;

- Monitoring compliance with timetable, scope of hours and result of investigations carried out in

special tasks;

- Monitoring the assessment made by independent advisory on the quality of processes and sufficiency

of resources available to internal audit and subsequent monitoring of the implementation of

improvement actions recommended;

- Annual cycle of appraisal of the performance of the head of the internal audit department.

Internal controls, corporate risk management, compliance and ombudsman - Monitoring the internal controls plan to map processes, key controls and indicators; - Discussing and evaluating the new map of strategic risks of the company, monitoring the mitigation

plans together with those responsible for their execution, and the respective description of the risk

factors in the Reference Form;

- Monitoring action plans to improve the information technology general controls (ITGC), access

profiles and the segregation of functions;

- Discussing and monitoring the pilot project to reformulate the company’s management system by

processes and indicators;

- Monitoring the implementation of action plans to comply with the integrity program established by

the company’s management;

- Monitoring the adoption of compliance policies and practices by managers and employees to ensure

compliance with the anticorruption law;

- Monitoring the results of the assessment made by independent advisory to review the integrity

program in the companies acquired and the respective action plan for correcting the processes;

- Monitoring the results of the Net Promoter Score (NPS) survey and management’s initiatives to

improve client satisfaction with the services provided by the company.

Financial management, provisions and indicators - Discussing the model and standardization of the company’s budget management; - Discussing, streamlining and monitoring the application of the credit analysis policy, collections

procedures and estimates of losses on doubtful accounts;

- Monitoring the financial management model of the software and hardware businesses;

- Evaluating compliance with CVM Resolution 594 regarding provisions and contingent liabilities and

assets;

- Discussing and monitoring the main lawsuits and the management’s judgment on possible outcomes.

Monitoring the evolution of the environment of controls in the legal department, mainly related to

the management of lawsuits;

- Discussing and monitoring the procedures adopted to review annual impairment tests;

- Financial impacts caused by changes in law (Lei do Bem);

- Monitoring the methodology and controls for managing service projects.

Corporate Governance - Giving opinion for the Board of Directors approval of quarterly and annual financial statements;

- Evaluating and recommending approval of proposals for dividends and interest on equity;

(A free translation of the original in Portuguese)

21

- Discussing about improvements to the long-term incentive model for company executives from the

perspective of the risks of retention, motivation and alignment with the company’s vision and

strategy;

- Discussing the terms used in notices, material fact notices and earnings release to the market;

- Monitoring and making recommendations to the Board of Directors and the Management on

initiatives and operations involving mergers and acquisitions, as well as assessment of operating risks;

- Discussing and monitoring the process for updating the Reference Form;

- Discussing the content and making recommendations on the proposed Integrated Report of the

company;

- Monitoring the queries and management’s responses to letters from regulatory agencies;

- Reviewing and making improvements to rules for rolling out the crisis management plan;

- Reviewing and discussing about a new hierarchy for policies, standards, procedures, governance and

powers for approval of rules, as well as reviewing existing policies;

- Discussing the terms and scope of the policy on transactions with related parties;

- Monitoring the activities of the Conduct and Ethics Committee, evaluating the complaints received

by the channel and the measures adopted by Management.

- Taking stock of the activities and evaluating the topics discussed in the tax committee.

- Management and governance aspects of TOTVS franchise network;

- Annual self-assessment cycle of the audit committee.

Audit Committee Report

2016 Annual Financial Statements:

The members of the Audit Committee of TOTVS S.A., in the exercise of their legal duties and

responsibilities, pursuant to the Charter of the Audit Committee, examined and analyzed the financial

statements, accompanied by the independent auditors report and the annual management report for the

fiscal year ended December 31, 2016 (“2016 Annual Financial Statements”) and, considering the information

provided by the Company management and by PwC Auditores Independentes, as well as the proposed

allocation of the earnings from fiscal year 2016, unanimously concluded that these adequately reflect, in all

material aspects, the equity and financial position of the Company and its subsidiaries, and recommend the

Board of Directors of the Company to approve said documents and submit them to the Annual Shareholders

Meeting, in accordance with Brazilian Corporation Law.

São Paulo, February 20, 2017

Maria Helena Santana

Chair of the Audit Committee and member of the Board of Directors

Danilo Silva Member of the Audit Committee and the Board of Directors Gilberto Mifano

Member of the Audit Committee

Mauro Rodrigues da Cunha Member of the Audit Committee and the Board of Directors

(A free translation of the original in Portuguese)

22

(A free translation of the original in Portuguese)

TOTVS S.A.

Balance sheets as at December 31, 2016 and 2015 (In thousands of reais)

The accompanying notes are an integral part of these financial statements.

Parent Company Consolidated Parent Company Consolidated

Assets 2016 2015 2016 2015 Liabilities and equity 2016 2015 2016 2015

Current assets 565,602 731,220 951,736 1,157,673 Current liabilities 465,130 475,288 624,197 658,683

Cash and cash equivalents (Note 5) 112,504 314,405 214,772 426,415 Payroll and labor obligations (Note 14) 105,243 99,190 140,539 133,152 Marketable securities (Note 17) 32,165 17,488 74,027 75,213 Trade accounts payable 41,844 37,311 73,553 86,932 Trade accounts receivable (Note 6) 394,382 401,750 569,370 565,002 Loans and financing (Note 15) 180,294 168,643 196,012 177,514 Allowance for doubtful accounts (Note 6) (84,293) (56,551) (105,183) (75,860) Taxes payable 17,293 11,293 28,141 18,923 Stocks (Nota 7) - - 28,219 44,407 Commissions payable 38,343 52,172 43,198 56,579 Taxes recoverable (Note 8) 72,993 27,673 122,521 81,284 Dividends payable (Note 20) 41,097 32,428 41,561 32,885 Other assets 37,851 26,455 48,010 41,212 Liabilities from acquisition of investments (Note 17) 38,960 24,492 80,822 82,220 Debentures (Note 16) - 49,473 12,111 61,915 Other liabilities 2,056 286 8,260 8,563 Non-current assets 1,642,705 1,630,795 1,492,176 1,504,402

Marketable securities (Note 17) 4,676 28,780 11,137 39,534 Non-current liabilities 521,989 649,041 598,799 765,660

Trade accounts receivable (Note 6) 35,842 38,676 36,913 40,953 Loans and financing (Note 15) 339,207 466,532 365,729 500,795

Receivables from related parties (Note 10) 1,644 3,622 - - Debentures (Note 16) 58,784 49,429 78,550 82,371

Taxes recoverable (Note 8) - - 21,572 17,881 Provision for losses on investments (Note 11) 1,208 584 - - Deferred income and social contribution taxes

(Note 9) 30,449 16,954 88,658 63,507 Payables to related parties (Note 10) 13,247 15,023 - -

Financial assets at fair value (Note 4) - - 56,800 68,044 Provision for contingencies related to legal proceedings (Note 18) 85,323 70,392 102,225 90,507

Judicial deposits (Note 18) 29,846 31,688 40,903 43,407 Liabilities from acquisition of investments (Note 17) 17,828 47,065 45,886 88,272 Other assets 23,420 10,405 30,437 18,466 Other liabilities 6,392 16 6,409 3,715

Equity (Note 19) 1,221,188

1,237,686 1,220,916 1,237,732

Investments (Note 11) 976,201 1,001,473 1,350 - Capital 541,374 541,374 541,374 541,374 Property, plant and equipment (Note 12) 154,126 86,235 176,270 113,598 Treasury shares (73,443) (71,012) (73,443) (71,012) Intangible assets (Note 13) 386,501 412,962 1,028,136 1,099,012 Capital reserves 162,024 159,213 162,024 159,213 Other comprehensive income results 1,785 21,329 1,785 21,329 Retained profit reserve 582,073 520,203 582,073 520,203 Proposed additional dividend 7,375 66,579 7,375 66,579 Non-controlling interests - - (272) 46

Total assets 2,208,307 2,362,015 2,443,912 2,662,075 Total liabilities and equity 2,208,307 2,362,015 2,443,912 2,662,075

(A free translation of the original in Portuguese)

23

(A free translation of the original in Portuguese)

TOTVS S.A.

Statement of income Years ended December 31, 2016 and 2015 (In thousands of reais, except by the earnings per share)

Parent Company Consolidated

2016 2015 2016 2015

Licensing fees 125,873 198,511 167,759 239,979

Maintenance 853,505 828,741 1,000,753 918,556

Subscriptions 124,166 86,113 229,235 140,820

Services 416,144 444,480 541,848 557,718

Hardware - - 244,191 51,664

Net revenue from services and sales (Note 24) 1,519,688 1,557,845 2,183,786 1,908,737

Cost of software (66,772) (69,527) (77,284) (75,399)

Cost of support (75,448) (83,974) (130,540) (89,722)

Cost of services (401,760) (388,881) (506,545) (507,298)

Cost of hardware - - (162,409) (34,050)

Gross profit 975,708 1,015,463 1,307,008 1,202,268

Operating income (expenses)

Research and development (231,638) (224,041) (326,546) (267,013)

Advertising expenses (35,391) (38,243) (47,029) (49,281)

Selling expenses (121,547) (106,515) (203,818) (152,230)

Commissions (Note 25) (118,758) (138,075) (139,639) (155,981)

General and administrative expenses (140,729) (156,588) (204,532) (187,277)

Management fees (Note 10) (15,673) (19,280) (19,176) (23,476)

Depreciation and amortization (Notes 12 and 13) (79,278) (70,894) (128,350) (103,077)

Allowances for doubtful accounts (Note 6) (41,542) (30,192) (49,197) (34,562)

Government subsidy - - 10,639 794

Other net operating income (expenses) 9,776 (5,853) 12,893 (1,782)

Income before financial effects and equity pickup 200,928 225,782 212,253 228,383

Financial income (Note 26) 48,400 97,627 74,251 121,165

Financial expenses (Note 26) (80,029) (82,107) (110,983) (94,639)

Equity pick-up (Note 11) (4,737) (4,628) - (75)

Income before income tax and social contribution 164,562 236,674 175,521 254,834

Income tax and social contribution current (15,329) (47,025) (38,260) (69,250)

Income tax and social contribution deferred 3,425 5,880 15,008 9,362

Total of Income tax and social contribution (11,904) (41,145) (23,252) (59,888)

Net income for the year 152,658 195,529 152,269 194,946

Net income attributable to the owners of company 152,658 195,529 152,658 195,529

Net income attributable to non-controlling interest - - (389) (583)

Basic earnings per thousand shares (in Reais) 0.93 1.20 0.93 1.20

Diluted earnings per thousand shares (in Reais) 0.93 1.19 0.93 1.19

The accompanying notes are an integral part of these financial statements.

(A free translation of the original in Portuguese)

24

TOTVS S.A.

Statements of comprehensive income Years ended December 31, 2016 and 2015 (In thousands of Reais )

Parent Company

2016 2015

Net income for the year 152,658 195,529

Cumulative adjustment for currency exchange (29,610) 32,272

Deferred income tax 10,066 (10,972)

Cumulative adjustment for currency exchange, net of tax effects (19,544) 21,300

Comprehensive income for the year 133,114 216,829

Consolidated

2016 2015

Net income for the year 152,269 194,946

Cumulative adjustment for currency exchange (29,610) 32,272

Deferred income tax 10,066 (10,972)

Cumulative adjustment for currency exchange, net of taxes

effects (19,544) 21,300

Comprehensive income for the year 132,725 216,246

Net income for the year attributable to controlling shareholders 133,114 216,829

Attributable to non-controlling interest (389) (583)

The accompanying notes are an integral part of these financial statements.

(A free translation of the original in Portuguese)

25

TOTVS S.A. (A free translation of the original in Portuguese) Statements of changes in shareholders´ equity Years ended December 31, 2016 and 2015 (In thousands of reais)

Capital

Premium on

purchase

from non-

controlling

Capital Reserves

Other

Comprehensive

Income

Retained

earnings

Proposed

additional

dividend Equity

Non-

Controlling

Consolidated

Equity

Of

Capital Legal

Profit

retention

Treasury

Share

Balance at December 31, 2014 526,592 (25,518) 118,011 61,961 389,807 (52,212) 29 - 97,704 1,116,374 1,688 1,118,062

Capital transactions with partners -

14,782 - 67,703 - - - - - - 82,485 - 82,485

Stock option plan - - 3,992 - - - - - - 3,992 - 3,992

Dividends - - - - - - - - (97,704) (97,704) (339) (98,043)

Proposed Additional Dividend - - - - - - - (66,579) 66,579 - - -

Interest on capital – distributed - - - - - - - (60,515) - (60,515) - (60,515)

Treasury shares - - (4,975) - - (18,800) - - - (23,775) - (23,775)

Acquisitions of subsidiaries - - - - - - - - - - (1,021) (1,021)

Total comprehensive income - - - - - - - - - - 301 301

Net income for the year - - - - - - 21,300 195,529 - 216,829 (583) 216,246

Other comprehensive income - - - - - - - 195,529 - 195,529 (583) 194,946

Cumulative adjustment for currency

exchange - - - - - - 21,300 - - 21,300 - 21,300

Reserves set up - - - 9,776 58,659 - - (68,435) - - - -

Balance at December 31, 2015 541,374 (25,518) 184,731 71,737 448,466 (71,012) 21,329 - 66,579 1,237,686 46 1,237,732

Capital transactions with partners

Stock option plan - - 2,811 - - - - - - 2,811 - 2,811

Dividends from the previous year - - - - - - - - (66,579) (66,579) - (66,579)

Dividens and interest on capital

Prescribed - - - - - - - 807 - 807 - 807

Dividends - - - - - - - (7,375) 7,375 - - -

Interest on capital – distributed - - - - - - - (84,220) - (84,220) - (84,220)

Treasury shares - - - - - (2,431) - - - (2,431) - (2,431)

Acquisitions of non-controlling interests - - - - - - - - - - - -

Acquisitions of subsidiaries - - - - - - - - - - 71 71

Total comprehensive income - - - - - - (19,544) 152,658 - 133,114 (389) 132,725

Net income for the year - - - - - - - 152,658 - 152,658 (389) 152,269

Cumulative adjustment for currency

exchange - - - - - - (19,544) - - (19,544) - (19,544)

Reserves set up - - - 7,633 54,237 - - (61,870) - - -

Balance at December 31, 2016 541,374 (25,518) 187,542 79,370 502,703 (73,443) 1,785 - 7,375 1,221,188 (272) 1,220,916

The accompanying notes are an integral part of these financial statements.

(A free translation of the original in Portuguese)

26

TOTVS S.A. Statement of cash flow Years ended December 31, 2016 and 2015

(In thousands of Reais)

Parent Company Consolidated

2016 2015 2016 2015

Cash flow from operating activities

Profit before taxation income and social contribution 164,562 236,674 175,521 254,834

Adjustments for:

Depreciation and amortization ( Notes 12 and 13) 79,278 70,894 131,664 103,660

Stock option plan (Note 21) 2,811 3,992 2,811 3,992

Losses (gains) on disposal of fixed assets (7,169) 2,474 (8,005) (1,980)

Allowance for doubtful accounts ( Note 6) 41,542 30,192 49,197 34,562

Equity pick up (Note 11) 4,737 4,628 - 75

Provision for contingencies and legal obligations 32,635 59,538 32,616 56,833

Provision (reversal) for other obligations - (1,388) 2,376 (6,388)

Interest and monetary and exchange variations, net 65,080 63,868 68,400 57,015

Changes in operating assets and liabilities:

Trade accounts receivable (3,598) (24,261) (20,202) (42,110)

Stock - - 12,234 (2,018)

Other assets (20,013) (2,891) (14,447) 5,875

Judicial deposits 1,842 (9,877) 2,504 (9,046)

Labor and social security liabilities 6,053 1,965 7,387 (2,837)

Taxes recoverable (45,320) (26,258) (44,928) (37,886)

Suppliers 3,833 8,662 (14,079) 10,377

Commission payable (13,829) (3,959) (13,381) (2,816)

Taxes payable (2,810) (27,648) (11,946) (40,327)

Other accounts payable (16,325) (944) (27,020) 10,829

Cash flow provided by operations 293,309 385,661 330,702 392,644

Interest paid (43,725) (46,163) (53,098) (46,828)

Income tax and social contributions paid (6,519) (20,237) (17,096) (32,649)

Net cash provided by operating activities 243,065 319,261 260,508 313,167

Cash flow provided by investment activities

Capital increase in subsidiaries (Note 11) (34,211) (67,726) (1,439) -

Dividends received 24,438 15,027 - -

Purchases of intangible assets (Note 13) (34,061) (41,039) (49,938) (43,199)

Acquisitions of subsidiaries, net of cash obtained in the

acquisitions - (502,755) - (423,329)

Cash and cash equivalents of merged subsidiaries - 48,562 - -

Value of sales of fixed assets 1,127 1,448 1,560 845

Purchases of property, plant and equipment (Note 12) (49,725) (42,042) (55,209) (47,524)

Purchases of investments measured at fair value 6,277 - 6,277 6,088

Net cash used in investment activities (86,155) (588,525) (98,749) (507,119)

Cash flow from financing activities Payment of principal on loans and financing (166,262) (27,512) (175,013) (27,452)

Payment of principal on debentures (48,002) (32,002) (58,566) (33,908)

Payment of financial leasing (944) - (994) -

New loans and financing - 181,055 7,368 181,858

Repurchase of debentures - - (2,416) -

Receivables from related companies 202 (470) - -

Dividends and interest on capital paid (141,324) (172,863) (141,350) (174,257)

Treasury shares, net (2,431) (23,775) (2,431) (23,775)

Net cash used in financing activities (358,811) (75,567) (373,402) (77,534)

Increase (decrease) in cash and cash equivalents (201,901) (344,831) (211,643) (271,486)

Cash and cash equivalents at the beginning of the year 314,405 659,236 426,415 697,901

Cash and cash equivalents at the end of the year 112,504 314,405 214,772 426,415

The accompanying notes are an integral part of these financial statements.

(A free translation of the original in Portuguese)

27

TOTVS S.A. Statement of Value Added Years ended December 31, 2016 and 2015

(In thousands of Reais) Parent Company Consolidated

2016 2015 2016 2015

1 – REVENUES

1,678,839 1,674,463

2,437,985

2,062,599

1.1 Sales of goods, products and services

1,710,606 1,710,507

2,466,074

2,094,744

1.2 Other revenue 9,775 (5,852) 21,108 2,417

1.3 Allowance for doubtful accounts – recording (41,542) (30,192) (49,197) (34,562)

2 - RAW MATERIALS ACQUIRED FROM THIRD-PARTIES

(includes ICMS and IPI taxes) (540,518) (584,860) (874,117) (726,476)

2.1 Cost of goods and services sold (66,772) (69,527) (258,903) (113,220)

2.2 Materials, energy, outsourced services and other (473,746) (515,333)

(615,214) (613,256)

3 - GROSS VALUE ADDED ( 1-2 ) 1,138,321 1,089,603 1,563,868 1,336,123

4 - DEPRECIATION AND AMORTIZATION (79,278) (70,894) (131,664) (103,660)

5 - NET VALUE ADDED PRODUCED BY THE ENTITY (3-4) 1,059,043 1,018,709 1,432,204 1,232,463

6 - VALUE ADDED RECEIVED THROUGH TRANSFERS 43,663 92,999 74,251 121,090

6.1 Equity pick-up (4,737) (4,628) - (75)

6.2 Financial income 48,400 97,627 74,251 121,165

7 - TOTAL VALUE ADDED TO DISTRIBUTE (5+6) 1,102,706 1,111,708 1,506,455 1,353,553

8 - VALUE ADDED DISTRIBUTION 1,102,706 1,111,708 1,506,455 1,353,553

8.1 Personnel 610,791 586,644 847,305 742,803

8.1.1 Direct Compensation 495,244 472,671 689,552 602,430

8.1.2 Benefits 70,315 68,195 98,653 84,904

8.1.3 FGTS (worker’s severance fund) 45,232 45,778 59,100 55,469

8.2 Taxes and contributions 234,589 224,193 356,809 289,384

8.2.1 Federal 192,879 182,790 279,370 209,980

8.2.2 State 1 5 23,874 25,661

8.2.3 Municipals 41,709 41,398 53,565 53,743

8.3 Interest and rent 104,668 105,342 150,072 126,420

8.3.1 Interest 80,029 82,107 110,984 94,586

8.3.2 Rents 24,639 23,235 39,722 31,963

8.3.3 Others - - (634) (129) 8.4 Remuneration of equity capital 152,658 195,529 152,269 194,946

8.4.1 Interest on capital 84,220 60,515 84,220 60,515

8.4.2 Dividends paid or credited to shareholders 7,375 66,579 7,375 66,579

8.4.3 Retained profit / loss for the year 61,063 68,435 61,063 68,435

8.4.4 Minority interest in retained earnings - - (389) (583)

The accompanying notes are an integral part of these financial statements.

(A free translation of the original in Portuguese)

28

TOTVS S.A. Notes to the financial statements Years ended December 31, 2016 and 2015 (In thousands of Reais)

1. Operations

TOTVS S.A. (“TOTVS”, or “Company”) is a publicly held corporation, headquartered at Av. Braz Leme, 1631 – 2nd floor, in the city and state of São Paulo, whose shares are traded on the Novo Mercado of BM&FBOVESPA - the Securities, Commodities and Futures Exchange.

The Company’s business purpose is to provide business solutions for companies of all sizes,

through the development and sale of management software, productivity and collaboration platform, as well as the provision of implementation, consulting, assistance and maintenance services. With the corporate restructuring of Bematech in 2015, the Company included hardware manufacturing and sale activities, combining specialized solutions for system management, point of sale (POS), commercial automation, tax solutions, e-commerce, mobility and payment methods. The solutions developed by the Company and its subsidiaries are segmented according to the diverse sectors of the economy, resulting in greater importance of the solutions in our clients’ business.

The Financial Statements presented in this document were approved after recommendation

of the Audit Committee at the meeting held on February 15, 2017 and at the Board of Directors’ Meeting held on February 20, 2017.

Non-financial data included in this report, such as the number of clients, average ticket,

market share, and other, were not audited by our independent auditors.

2. Basis of Preparation and Summary of the Main Accounting Practices

The individual and consolidated financial statements were prepared and presented in accordance with the accounting practices adopted in Brazil, including the pronouncements issued by the Accounting Pronouncements Committee (“CPC”) and the rules issued by the Brazilian Securities Commission (“CVM”), as well as the International Financial Reporting Standards (“IFRS”) issued by the International Accounting Standards Board (“IASB”) and show all material information strictly relating to the financial statements, which are consistent with that used by the management.

The financial statements were prepared on the historical cost basis, except for the valuation

of certain assets and liabilities, such as financial instruments from business combinations, which are measured at their fair value.

The preparation of financial statements requires the use of certain critical accounting

estimates and the exercise of judgment by Company management in applying the accounting policies of TOTVS S.A.

Estimates and assumptions that show significant risk and that need a higher level of

judgment and have a great degree of complexity for the Company’s financial statements are:

(A free translation of the original in Portuguese)

29

(i) Allowance for doubtful accounts – Note 6;

(ii) Impairment of tangible and intangible assets, including goodwill – Note 13.2;

(iii) Deferred taxes – Note 9.3;

(iv) Provision for contingencies related to legal proceedings – Note 18.

More information on the estimates and assumptions used in the items mentioned above is provided in the respective notes.

The pronouncements, interpretations and reviews of CPCs / IFRS that came into effect from

2016 did not have any significant impact on the Company's financial statements. Below is a summary of key accounting practices adopted by the Company, highlighting only

information considered relevant by Management.

2.1. Consolidation

The consolidated financial statements include the operations of the Company and the

following subsidiaries. The percentages of the interests held by the Company on the balance sheet

date are summarized below:

Direct interest: % Interest

Corporate Name Head

office Name used 2016 2015

TOTVS Serviços Ltda. BRA TOTVS Serviços 100.00 100.00

TOTVS Nordeste Software Ltda. BRA TOTVS Nordeste 100.00 100.00

TOTVS Brasília Software Ltda. BRA TOTVS Brasília 100.00 100.00

TQTVD Software Ltda. BRA TQTVD 100.00 100.00

TOTVS Ventures Participações Ltda. BRA TOTVS Ventures 100.00 100.00

TOTVS Argentina S.A. ARG TOTVS Argentina 100.00 100.00

Datasul Argentina S.A. ARG Datasul Argentina 100.00 100.00

TOTVS México S.A. MEX TOTVS México 100.00 100.00

Datasul S.A. de CV. MEX Datasul México 100.00 100.00

TOTVS Corporation BVI TOTVS Corporation 100.00 100.00

TOTVS Incorporation USA TOTVS Inc. 100.00 100.00

Virtual Age Soluções em Tecnologia Ltda. BRA Virtual Age 100.00 100.00

Neolog Consultoria e Sistemas S.A. BRA Neolog 60.00 60.00

Ciashop - Soluções para Comércio Eletrônico S.A. BRA Ciashop 70.00 70.00

TOTVS Resultados em Outsourcing Ltda. (a) BRA RO - 100.00

Bematech S.A. BRA Bematech 100.00 100.00

Indirect Interest: % Interest

Corporate Name Head

office Name used Investor 2016 2015

DTS Consulting Partner, SA de CV MEX Partner TOTVS México 100.00 100.00

W&D Participações S.A. BRA W&D TOTVS Brasília - 100.00

PC Informática S.A. BRA PC Informática W&D 100.00 100.00

(A free translation of the original in Portuguese)

30

RMS Software S.A. BRA RMS TOTVS Nordeste 100.00 100.00

Webstrategie Software Ltda. BRA Webstrategie RMS 100.00 100.00

Kerina Software Ltda. BRA Kerina TQTVD 100.00 100.00

Bematech Ásia Co.Ltd. TWN Bematech Ásia Bematech S.A. 100.00 100.00

Bematech Argentina S.A. ARG Bematech Argentina Bematech S.A. e Bematech

Inter. Corp. 100.00 100.00

CMNet Soluções em Informática e Agência de

Viagens e Turismo S.A. BRA CMNet Soluções Bematech S.A. 100.00 100.00

Misterchef Sistemas de Automação Ltda. (b) BRA Misterchef Bematech S.A. - 100.00

Bematech Internacional Corp. EUA BIC Bematech S.A. 100.00 100.00