TOTAL TRAINING SOLUTIONS [email protected]/ALLLPJ051915.pdf ·...

33

1 TOTAL TRAINING SOLUTIONS Bankers Insight Group Jeffery W. Johnson [email protected] The ALLL represents one of the most significant estimates in an institution’s financial statements and regulatory reports Each institution as of the end of each quarter, or more frequently if warranted, must analyze the collectability of its loans and leases appropriate and determined in accordance with GAAP. 5/18/2015 Bankers Insight Group 2

Transcript of TOTAL TRAINING SOLUTIONS [email protected]/ALLLPJ051915.pdf ·...

1

TOTAL TRAINING SOLUTIONSBankers Insight Group

Jeffery W. [email protected]

The ALLL represents one of the most significant estimates in an institution’s financial statements and regulatory reports

Each institution as of the end of each quarter, or more frequently if warranted, must analyze the collectability of its loans and leases appropriate and determined in accordance with GAAP.

5/18/2015Bankers Insight Group 2

2

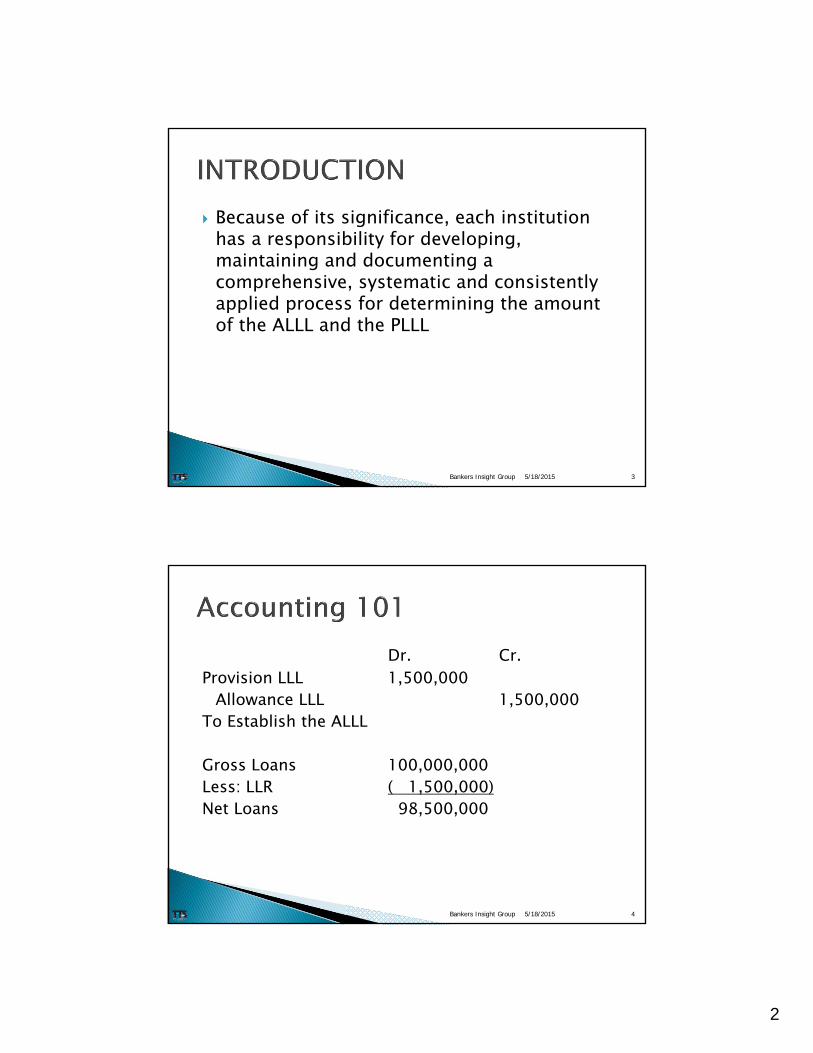

Because of its significance, each institution has a responsibility for developing, maintaining and documenting a comprehensive, systematic and consistently applied process for determining the amount of the ALLL and the PLLL

5/18/2015Bankers Insight Group 3

Dr. Cr.Provision LLL 1,500,000

Allowance LLL 1,500,000To Establish the ALLL

Gross Loans 100,000,000Less: LLR ( 1,500,000)Net Loans 98,500,000

5/18/2015Bankers Insight Group 4

3

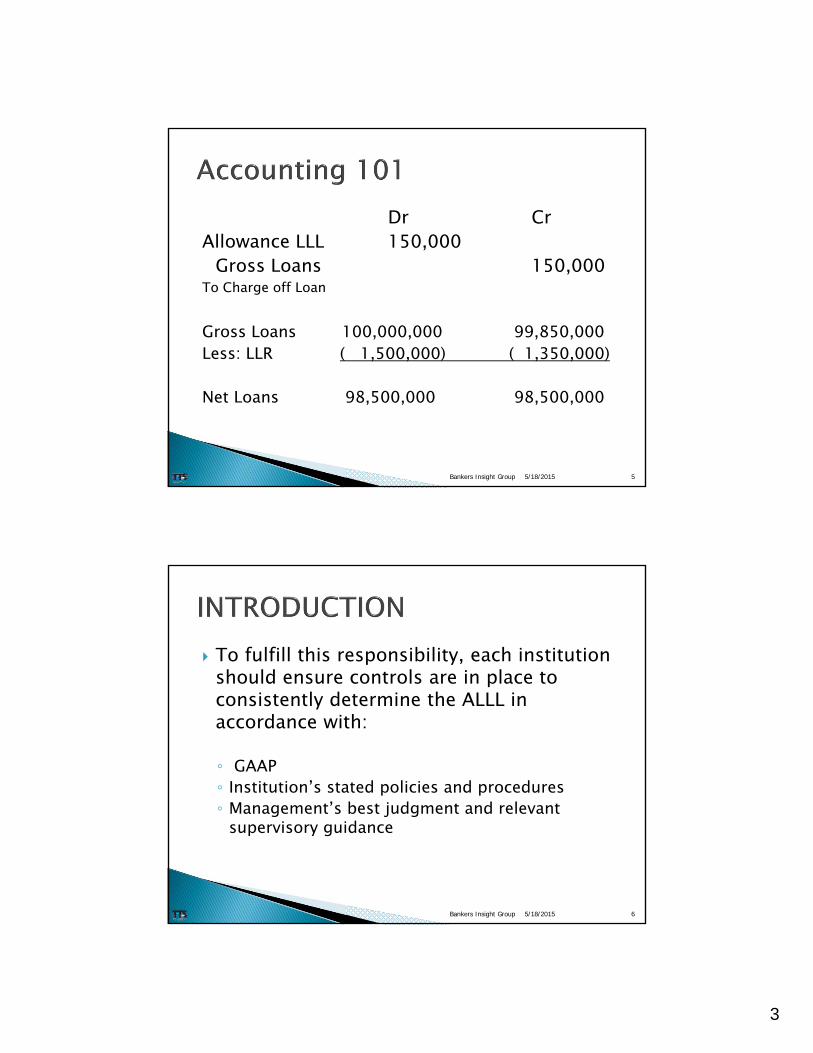

Dr CrAllowance LLL 150,000

Gross Loans 150,000To Charge off Loan

Gross Loans 100,000,000 99,850,000Less: LLR ( 1,500,000) ( 1,350,000)

Net Loans 98,500,000 98,500,000

5/18/2015Bankers Insight Group 5

To fulfill this responsibility, each institution should ensure controls are in place to consistently determine the ALLL in accordance with:

◦ GAAP◦ Institution’s stated policies and procedures ◦ Management’s best judgment and relevant

supervisory guidance

5/18/2015Bankers Insight Group 6

4

Loan Loss Provisioning Methodology has become afocus for regulators of community banks.

Having an adequate Allowance for Loan and LeaseLosses (“ALLL”) is required for community banksalso

The methodology for arriving at a proper ALLL is afunction of the institution’s characteristic

5/18/2015Bankers Insight Group 7

Regulators look for 3 things in ALLL Methodology:

1. Policies and procedures that described how banks segment portfolios

2. Policies and procedures for determining how to measure the impairment of individually evaluated loans per ASC 310

3. Methodology on how to determine and measure impairment in homogenous loans per ACS 450

5/18/2015Bankers Insight Group 8

5

Former Reference New Accounting Standards Codification

FASB 5: Accounting for Contingencies

FASB 114: Accounting for Creditors for Impairment of a Loan

ASC 450-20: Contingencies Loss Contingencies

ACS 450-10-35-2 through 30: Receivables–Overall –Subsequent-Measurement -Impairment

5/18/2015Bankers Insight Group 9

Former Reference New Accounting Standards Codification

FASB 15: Accounting by Debtors & Creditors for Troubled Debt Restructuring

ASC 310-40: Receivables-Trouble Debt Restructuring by Creditors

5/18/2015Bankers Insight Group 10

6

Interagency Policy Statement on the ALLL, 12/2006

Interagency Policy Guidance, July 2001

Questions & Answers on Accounting for Loans and Lease Losses

OCC Bulletin 2001 - 37

ASC 450-20 & ASC 310-10-35-2 through 30

5/18/2015Bankers Insight Group 11

In addition to the Regulatory Guidance Documents on the ALLL, the Regulatory Community states there must be two systems in banks to properly calculate the ALLL:

1. Adequate Loan Review System2. Adequate Risk Rating System

5/18/2015Bankers Insight Group 12

7

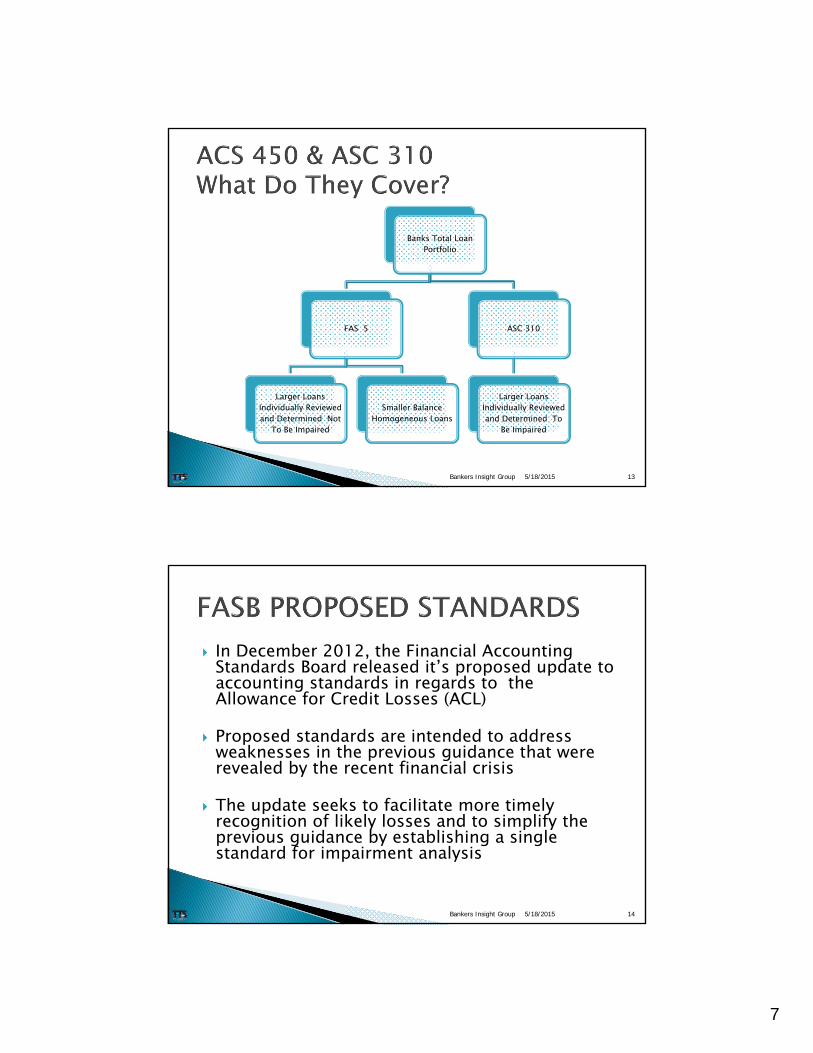

Banks Total Loan Portfolio

FAS 5

Larger Loans Individually Reviewed and Determined Not

To Be Impaired

Smaller Balance Homogeneous Loans

ASC 310

Larger Loans Individually Reviewed and Determined To

Be Impaired

5/18/2015Bankers Insight Group 13

In December 2012, the Financial Accounting Standards Board released it’s proposed update to accounting standards in regards to the Allowance for Credit Losses (ACL)

Proposed standards are intended to address weaknesses in the previous guidance that were revealed by the recent financial crisis

The update seeks to facilitate more timely recognition of likely losses and to simplify the previous guidance by establishing a single standard for impairment analysis

5/18/2015Bankers Insight Group 14

8

An estimated loss contingency shall be accrued by a charge to income if BOTH of the following conditions are met:

◦ Information available prior to issuance of the financial statements indicates that is probable that an asset had been impaired or a liability had been incurred at the date of the financial statement. It is implicit in this condition that it must be probable that one or more future events will occur confirming the fact of the loss

◦ “The amount of loss can be reasonably estimated”

5/18/2015Bankers Insight Group 15

These conditions may be considered in relation to individual loans or in relation to groups of similar types of loans. If the conditions are met, an accrual should be made even though the particular loans that are uncollectible may not be identifiable.

This is the entire premise of ASC 450-20

5/18/2015Bankers Insight Group 16

9

An individual loan is impaired when, based oncurrent information and events, it is probablethat a creditor will be unable to collect allamounts due (P&I) according to the contractualterms of the loan agreement. It is implicit inthese conditions that it must be probable thatone or more future events will occur confirmingthe fact of the loss.

This means loans fitting the description of aloan classified “doubtful”

5/18/2015Bankers Insight Group 17

ASC 310-10 does not specify how aninstitution should identify loans that are tobe evaluated for collectability nor does itspecify how to determine if a loan isimpaired. An institution should apply itsnormal loan review procedures in makingthose judgments.

5/18/2015Bankers Insight Group 18

10

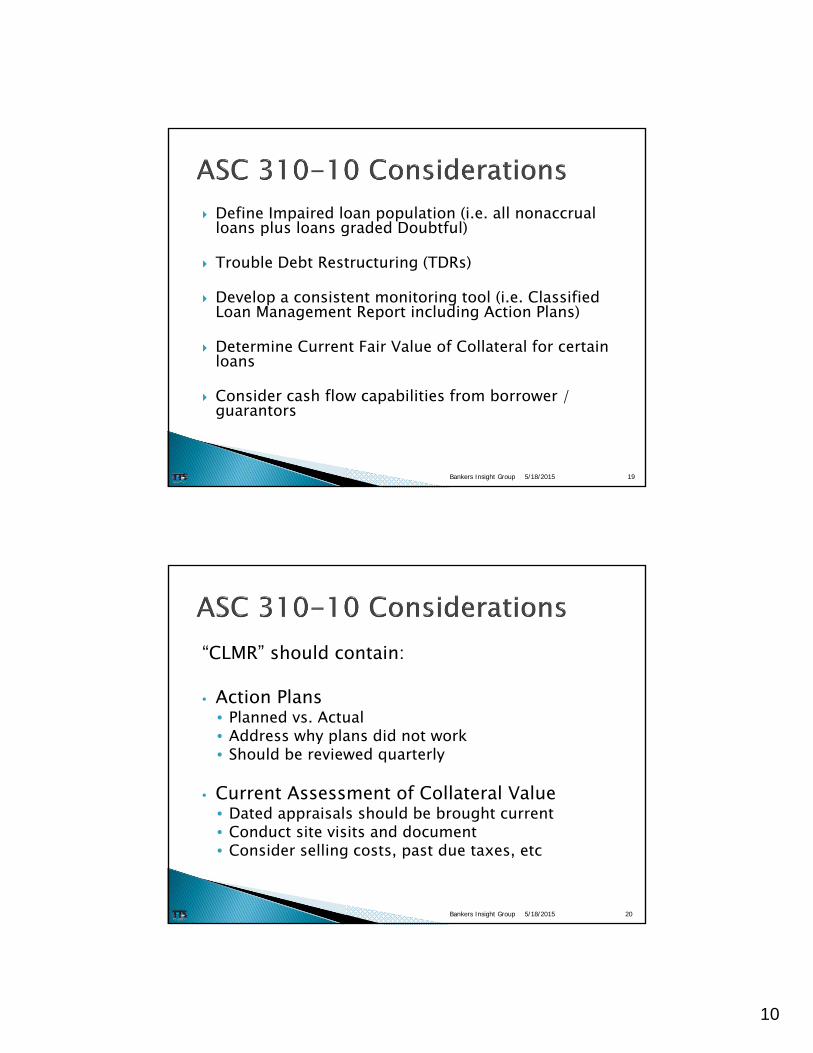

Define Impaired loan population (i.e. all nonaccrual loans plus loans graded Doubtful)

Trouble Debt Restructuring (TDRs)

Develop a consistent monitoring tool (i.e. Classified Loan Management Report including Action Plans)

Determine Current Fair Value of Collateral for certain loans

Consider cash flow capabilities from borrower / guarantors

5/18/2015Bankers Insight Group 19

“CLMR” should contain:

• Action Plans• Planned vs. Actual• Address why plans did not work• Should be reviewed quarterly

• Current Assessment of Collateral Value• Dated appraisals should be brought current• Conduct site visits and document• Consider selling costs, past due taxes, etc

5/18/2015Bankers Insight Group 20

11

5/18/2015Bankers Insight Group 21

1. Segment loan portfolio into pools of loans with similar characteristics

2. Develop the loss rate for each of those portfolio segments over a three-year history (or other supportable time period) net of charge-offs. For De Novo institutions, use of peer banks’ historical losses is permissable

3. Analyze the qualitative factors impacting the loan portfolio by considering environmental factors that impacts the ability to repay

Industry Trends Economic Trends Geographic Issues Political Issues

4. Develop a range of loss and best estimate within that range

5/18/2015Bankers Insight Group 22

12

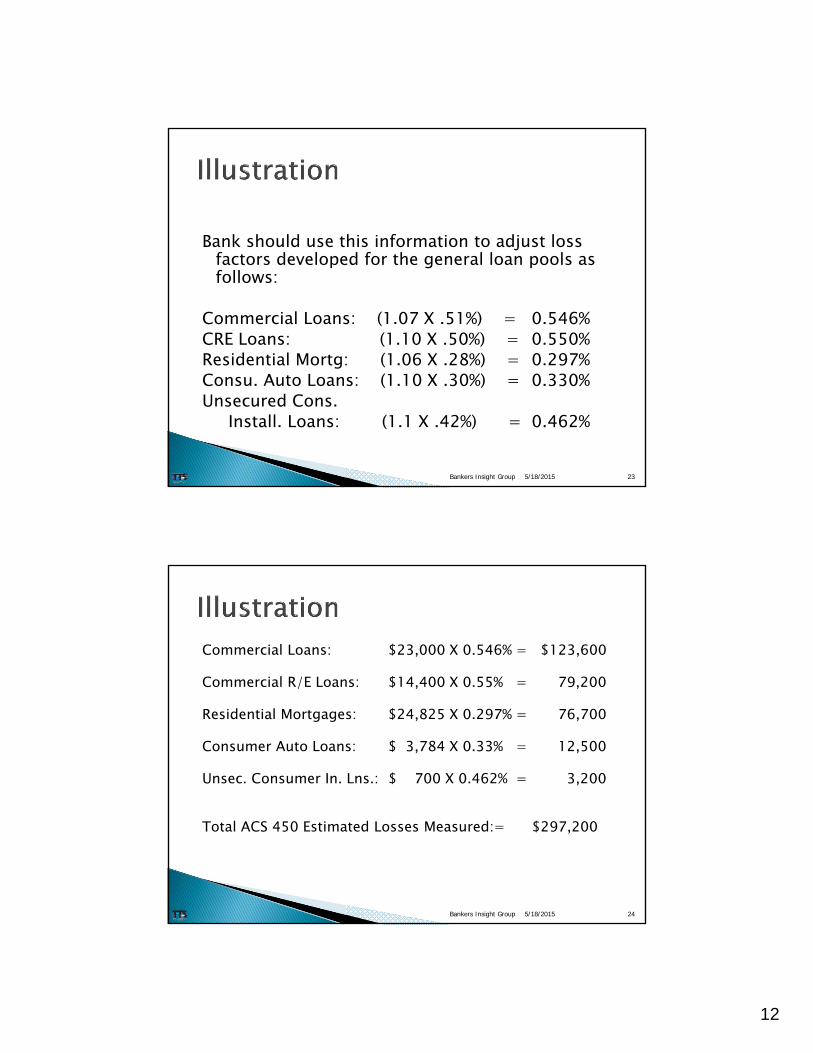

Bank should use this information to adjust loss factors developed for the general loan pools as follows:

Commercial Loans: (1.07 X .51%) = 0.546%CRE Loans: (1.10 X .50%) = 0.550%Residential Mortg: (1.06 X .28%) = 0.297%Consu. Auto Loans: (1.10 X .30%) = 0.330%Unsecured Cons.

Install. Loans: (1.1 X .42%) = 0.462%

5/18/2015Bankers Insight Group 23

Commercial Loans: $23,000 X 0.546% = $123,600

Commercial R/E Loans: $14,400 X 0.55% = 79,200

Residential Mortgages: $24,825 X 0.297% = 76,700

Consumer Auto Loans: $ 3,784 X 0.33% = 12,500

Unsec. Consumer In. Lns.: $ 700 X 0.462% = 3,200

Total ACS 450 Estimated Losses Measured:= $297,200

5/18/2015Bankers Insight Group 24

13

Trend in Internal Loan Grades

5/18/2015 Bankers Insight Group 25

Trends in Concentrations

5/18/2015 Bankers Insight Group 26

14

Tracking of Technical Exceptions

5/18/2015 Bankers Insight Group 27

Are the loan categories the Bank uses too broad on which to estimate loss?

Reserve Percentages as computed by loan type could be the historical average industry information, or the high or low of net charge-offs to loan type

Are they based on historical experience? Has something changed at the bank or its environment that makes historical experience irrelevant?

It is important to not only consider concentrations by loan type but also concentrations by borrowers or related borrowers

Does it make sense to you from your own knowledge and experience and the quantitative and qualitative analysis completed in the previous steps?

5/18/2015Bankers Insight Group 28

15

Qualitative adjustments are a challenge because they are inherently subjective in nature.

The 2006 Interagency Policy Statement on the ALLL provides little direction on how these determinations should be made.

It advises that “management should consider those current qualitative or environmental factors that are likely to cause estimated credit losses as of the evaluation date to differ from the group’s historical loss experience.”

5/18/2015Bankers Insight Group 29

The 2006 Interagency Policy Statement explained that nine qualitative factors should be considered when an institution estimates credit losses.

Certainly other factors can be added to this list according to the Interagency statement

For example, many bankers add a Qualitative Factor between 1999 and 2000 to cover any possible increase in historical losses as a result of Y2K

The nine factors that regulations recommend are:

5/18/2015Bankers Insight Group 30

16

Changes In:

Lending policies and procedures

International, national, regional and local conditions

Experience, depth, and ability of lending management

Volume and severity of past due loans and other similar conditions

Quality of the organization’s loan review system

Value of underlying collateral for collateral dependent loans

Concentrations of credit and changes in the levels of such concentrations

Competition, legal and regulatory requirements)

5/18/2015Bankers Insight Group 31

Since little guidance is provided by regulators, banks must devise their own systems to reduce the subjectivity in applying Qualitative Factors to historical losses

Regulators vaguely explains that these determinations are to be “based on a comprehensive, well-documented and consistently applied analysis of its loan portfolio”

But, what does that mean?

In order to justify why historical losses are adjusted due to some risk factor a bank may face in the immediate future, a system to make the application of Qualitative factors more objective is a requirement.

5/18/2015Bankers Insight Group 32

17

1. Create a Standard Process of Review

2. Utilize Current Market Information

3. Provide Directional Consistency

4. Conduct Correlation Analysis

5. Use Back-Testing as a Method of Validation

5/18/2015Bankers Insight Group 33

For example, Default Rate Adjustments should be developed and implemented to prevent subjective rate changes from prior periods as shown below:

5/18/2015Bankers Insight Group 34

18

Measurable Point Factor

Robust Improvement From Prior Period -10 BPModerate Improvement From Prior Period -08 BPSoft Improvement From Prior Period 04 BPNo Change from Prior Period 00 BPSoft Decline From Prior Period +04 BPModerate Decline From Prior Period +08 BPSignificant Decline From Prior Period +10 BPHard Recession +20 BPDepression +40 BP

*basis point ranges may be adjusted depending upon the loan category,risk rating, or other factors.

5/18/2015Bankers Insight Group 35

Attach comments to each adjustment which will document the reasoning for the rate change from the prior period and decrease the likelihood of examiners finding the rate adjustments to be without soundreason or too subjective.

Comments added will satisfy the “Standards of Care” principle which poses the questions what would a reasonable and prudent banker have done under the same circumstances.

5/18/2015Bankers Insight Group 36

19

Lending Policies and Procedures Changes in lending policies and procedures Changes in underwriting standards and collection Charge-off and recovery practices Increased speculative lending Increased lending in high-risk products or markets Origination of loans with marginal debt coverage ratios (DCRs) High loan-to-value (LTV) ratios Increased granting of unsecured lending Subprime lending Preponderance of loans approved with exceptions Loans to high-risk industries not normally permitted by policy High degree of loan documentation waivers, deficiencies, or an

abundance of matured loans (refinance risk) Financial statement exceptions or originations without them

5/18/2015Bankers Insight Group 37

Business Conditions

Economic factors (national, local behavior, or both, if applicable)

Should consider a variety of drivers, such as inflation, consumer price index (CPI), interest rate environment, housing starts, bankruptcy rates, producer price index (PPI), etc.

Should reflect distinctions among geographies (material)

Industry/Sector trends (manufacturing, investment real estate, hospitality, etc.)

Regional business closings

5/18/2015Bankers Insight Group 38

20

Lending Staff

Economics on turnover rates and loss of expertise

Absence of qualified staff for workout activities

Training issues

General lending experience and experience in assigned lending sector

Length of employment with the organization

5/18/2015Bankers Insight Group 39

Considering current market information, economic trends, and events within institutions’ lending footprints can help add objectivity and structure.

External environmental factors include:◦ changes in unemployment rates, ◦ bankruptcy rates, or ◦ foreclosure numbers.

Internal factors include changes in:◦ portfolio concentrations, ◦ bank policies/procedures, or ◦ management experience.

All these internal and external environmental factors should be identified, analyzed and potentially reflected in the quantitative adjustments.

Examiners expect adjustments to mirror the improvement and decline of both internal and external economic factors.

5/18/2015Bankers Insight Group 40

21

It is critical that determinations are always directionally consistent with credit quality trends. According to the 2006 Guidance:

Changes in the level of the ALLL should be directionally consistent with changes in the factors, taken as a whole, that evidence credit losses, keeping in mind the characteristics of an institution’s loan portfolio.

For example, if declining credit quality trends relevant to the types of loans in an institution’s portfolio are evident, the ALLL level as a percentage of the portfolio should generally increase, barring unusual charge-off activity. Similarly, if improving credit quality trends are evident, the ALLL level as a percentage of the portfolio should generally decrease.

5/18/2015Bankers Insight Group 41

Directional consistency validates that as drivers and factors change directions, an institution’s qualitative factors change directions as well and in accordance with the proper correlation to the driver and factor.

Documentation of sequential changes to factor rates, supported with driver graphs and/or measurements, ensures directional consistency has been maintained.

Internal management reports can be developed to track and support loan payment delinquencies, collateral values, and loan concentrations which would be very useful in supporting changes in any of the nine factors.

5/18/2015Bankers Insight Group 42

22

Correlation analysis measures the strength of the relationship between two variables: how well changes in one variable can be predicted by changes in another.

Let’s suppose management perceives a correlation between changes in commercial vacancy rates and the commercial real estate (“CRE”) losses they recognize.

By calculating the correlation coefficient (measured on a scale from -1.00 to +1.00, where +/-1.00 equals a perfect correlation between variables), management can determine the degree to which the change in vacancy rates affects CRE losses.

With the coefficient calculated, an institution can multiply the coefficient by the actual published vacancy rates to forecast probable changes in future CRE losses.

This can aid management in any necessary adjustments to the historic loss rates.

5/18/2015Bankers Insight Group 43

The use of back-testing allows management to test current assumptions or adjustments against actual historical data, in an effort to use the results to add credibility when making those same assumptions or adjustments today.

5/18/2015Bankers Insight Group 44

23

The bank should maintain supporting documentation for historical loss rates developed for each group of loans

The bank should support qualitative adjustments to historical loss rates with reasonable documentation

5/18/2015Bankers Insight Group 45

Changes in the level of the ALLL should be directionally consistent

◦ If declining credit quality trends are evident, the ALLL as a % of loans should generally increase

◦ If improving credit quality trends are evident, the ALLL as a % of loans should generally decrease

5/18/2015Bankers Insight Group 46

24

Does the Bank expect to collect all P & I_ A Yes answer indicate the loan is not impaired and will,

therefore, be pooled with similar loans in the ACS 450 section

_ A No answer would lead you to the next question below

Would the shortfall of the loan be insignificant?_ A Yes answer would put the loan into a pool of classified

loans.

_ A No answer would make the loan subject to ASC 310 impaired loans calculation.

5/18/2015Bankers Insight Group 47

Under ASC 310, a loan is impaired when itis probable that the bank will be unable tocollect all amounts due (P&I) according tothe contractual terms of the loanagreement.

This means loans fitting the description of aloan classified “doubtful”

5/18/2015Bankers Insight Group 48

25

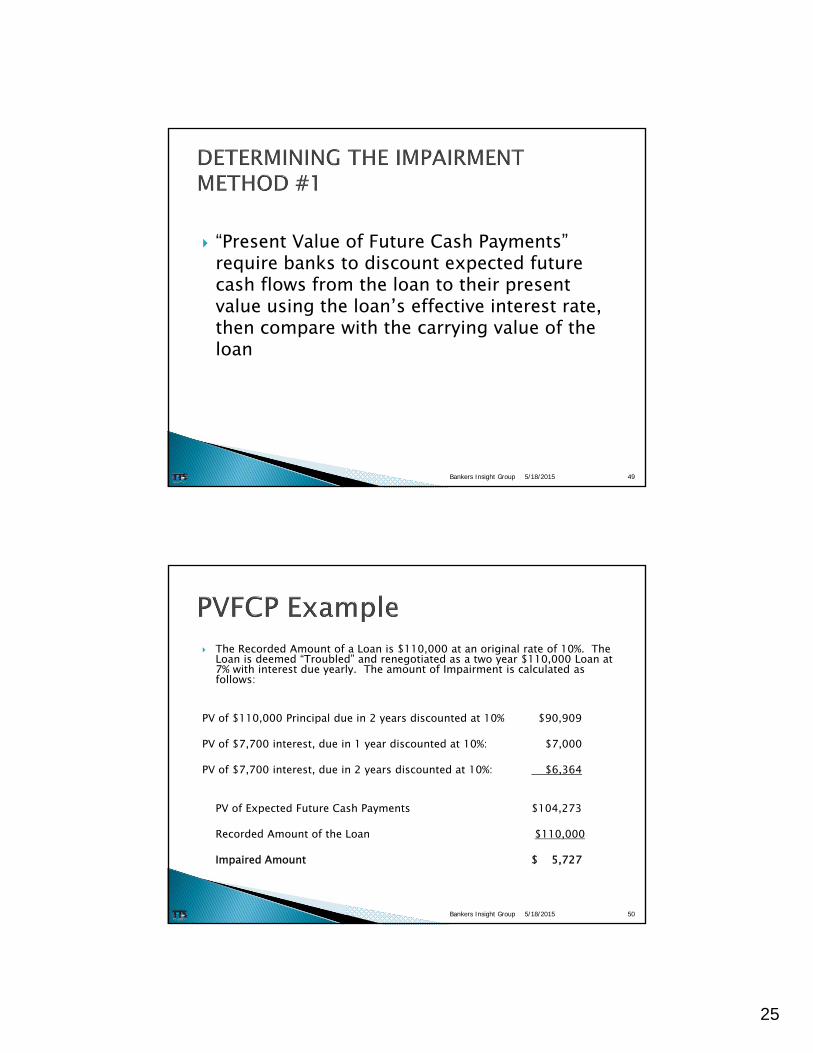

“Present Value of Future Cash Payments” require banks to discount expected future cash flows from the loan to their present value using the loan’s effective interest rate, then compare with the carrying value of the loan

5/18/2015Bankers Insight Group 49

The Recorded Amount of a Loan is $110,000 at an original rate of 10%. The Loan is deemed “Troubled” and renegotiated as a two year $110,000 Loan at 7% with interest due yearly. The amount of Impairment is calculated as follows:

PV of $110,000 Principal due in 2 years discounted at 10% $90,909

PV of $7,700 interest, due in 1 year discounted at 10%: $7,000

PV of $7,700 interest, due in 2 years discounted at 10%: $6,364

PV of Expected Future Cash Payments $104,273

Recorded Amount of the Loan $110,000

Impaired Amount $ 5,727

5/18/2015Bankers Insight Group 50

26

Impairment may be measured based on the loan’s observable market price

If loan is collateral dependent, impairment may be measured based upon the fair value of the collateral

5/18/2015Bankers Insight Group 51

When foreclosure is probable, ASC 310 requires that the measure of impairment be based on the fair value of the collateral.

Regardless of probability of foreclosure, Regulators expect reserves for all impaired collateral dependent loans be based on the fair value of the collateral for regulatory reports.

5/18/2015Bankers Insight Group 52

27

ASC 310 Reserve -Impaired Loans $418,000ACS 450 Reserve-Classified Loans $375,000ACS 450 Reserve-UnclassifiedLoans

$185,000

Calculated Reserve $978,000

Acceptable ALLL Range - per Policy

High 10% $1,100,000Low 10% $850,000

Current ALLL Balance 1,200,000ALLL to Outstanding Loans 1.31%Peer Group ALLL to OutstandingLoans - Current

1.25%5/18/2015Bankers Insight Group 53

There is no magic number for the range. It’s what supportable by the bank’s analysis

If you stray over, say 20%, you need to have good documentation to support why there’s such a large unallocated portion

5/18/2015Bankers Insight Group 54

28

The various considerations and calculations performed by management in the preceding steps should be revised by the Loan Committee on at least a quarterly basis and by the board at least annually

Any changes to the methodology or its application should be approved by both the Loan Committee and/or the Board.

The Interagency Statement requires a periodic validation of the ALLL methodology and application by someone independent of the credit approval and ALLL estimation process

5/18/2015Bankers Insight Group 55

1. Impaired loans identified for evaluation under ASC 310 have not been segregated from the rest of the portfolio in the ALLL methodology.

2. Certain impaired loans are “double counted” in the ALLL calculations (i.e. using both SASC 310 and SACS 450 measurements for the same loan)

3. Unfunded commitments are included in the calculation

4. The recorded ALLL is materially less or materially exceeds the amount supported by the ALLL methodology and related documentation by significant amounts

5/18/2015Bankers Insight Group 56

29

5. Monthly increases are provided to the ALLL based on budgeted amounts as opposed to analyzing the loan portfolio

6. Traditional percentages for loans characterized as special mention, substandard and doubtful are being used without substantiation

7. The Alll is determined based on target and/or peer statistics (e.g., ALLL-to-total loans) without adequate justification or evaluation of the institutions own experience.

*Obtained from the article, ALLL Together Now, by John Koegel (Community Banker, July 2007 Vol. 16 Iss. 7) in Sidebar, ALLL Seven Deadly Sins by Robert J. De Tullio of the Office of Thrift Supervision

5/18/2015Bankers Insight Group 57

Use fields available in your loan system to establish concentration pools other than Call or Collateral Codes

Track migration of loans from within pools for special mention to loss

Utilize date extraction software and other products to establish pivot tables for analysis of original balance to current balance, accrued interest receivable, payment histories, etc.

Utilize Excel in Methodology

Utilize latest FDIC or SEC filings for Banks to determine what other banks are experiencing.

Utilize national, regional, state and local economic data available to support the qualitative factors effecting your portfolio

5/18/2015Bankers Insight Group 58

30

Document, Document, Document

Compliance with all Regulatory Guidances

Compliance with GAAP

Consistency

Proactive and timely identification of problems by management

5/18/2015Bankers Insight Group 59

Impacts CAMELS Ratings◦ Asset Quality Downgrades

◦ Management Downgrades

Retroactive allowance adjustments

Issuance of written agreement

Management & Board embarrassment

External auditor concerns

5/18/2015Bankers Insight Group 60

31

Document, Document, Document

Compliance with all Regulatory Guidances

Compliance with GAAP

Consistency

Proactive and timely identification of problems by management

5/18/2015Bankers Insight Group 61

Impacts CAMELS Ratings◦ Asset Quality Downgrades

◦ Management Downgrades

Retroactive allowance adjustments

Issuance of written agreement

Management & Board embarrassment

External auditor concerns

5/18/2015Bankers Insight Group 62

32

Document, Document, Document

Compliance with all Regulatory Guidances

Compliance with GAAP

Consistency

Proactive and timely identification of problems by management

5/18/2015Bankers Insight Group 63

Impacts CAMELS Ratings◦ Asset Quality Downgrades

◦ Management Downgrades

Retroactive allowance adjustments

Issuance of written agreement

Management & Board embarrassment

External auditor concerns

5/18/2015Bankers Insight Group 64

33

Documentation is a key element to measuring how well a bank is arriving at its allowance

Smaller, less complex community banks can take advantage of portfolio segmentation, however, they do not need to have as fine a segmentation as larger, more complex banks

Establish a written ALLL policy and methodology that is approved by the Board at least annually

Maintain a consistent system of controls

5/18/2015Bankers Insight Group 65

TTSMark [email protected]

5/18/2015Bankers Insight Group 66

Upcoming WebinarsMay 20th - Mortgage Loan Originator Required Training Series Part 1

May 21st - Compliance Perspectives: A Monthly Update

June 2nd - Seven Habits of Effective Credit Administration in Commercial Banks

June 2nd - CRA Nuts & Bolts - Five Steps to Pass the Exam

June 3rd - Advanced Business Account Issues: Multi-tiered Businesses, Agents, Escrows and More

June 9th - Excel Explained: Minimize Spreadsheet Errors

June 9th - Basic Underwriting

June 10th - Employment Records and How to Keep Them

June 10th - Vital Check and Deposit Issues

June 11th - Ten Things to Look For When Analyzing Balance Sheets