TOPIC: WEIGHTED AVERAGE COST OF CAPITAL (WACC) Firm Value should be Maximized when WACC is Minimized...

16

TOPIC: WEIGHTED AVERAGE COST OF CAPITAL (WACC) • Firm Value should be Maximized when WACC is Minimized • Factors that impact on WACC include operating profitability, business risk, interest rates at specified debt levels, and the tax rate 1 RW Melicher

-

Upload

priscilla-carter -

Category

Documents

-

view

230 -

download

0

Transcript of TOPIC: WEIGHTED AVERAGE COST OF CAPITAL (WACC) Firm Value should be Maximized when WACC is Minimized...

TOPIC: WEIGHTED AVERAGE COST OF CAPITAL (WACC)• Firm Value should be Maximized

when WACC is Minimized

• Factors that impact on WACC include operating profitability, business risk, interest rates at specified debt levels, and the tax rate

1RW Melicher

ADJUSTED PRESENT VALUE (APV)

• APV is often used to estimate the impact of using financial leverage

• APV = present value (PV) of an all equity firm + PV of tax benefits from debt – financial distress or bankruptcy-related costs

2

APV EXAMPLE

• PV of All Equity Firm: future free cash flows to equity discounted by the cost of equity capital (e.g., $7 million)• PV of Tax Benefits: perpetual debt amount x

tax rate (e.g., $2 million x .40 = $.8 million)• PV financial distress costs (e.g., est. $.1

million)• APV = $7 mill. + $.8 mill. - $.1 mill. = $7.7

mill. 3

4

5

A. DETERMINE PERCENTAGE WEIGHTS FOR DEBT & EQUITY IN THE CAPITAL STRUCTURE

1. Capital Structure Value (V)

V = Long-Term Debt (D) + Equity (S)

2. Current Versus Target Capital Structures

3. Market Value-Based Weights Versus Book

Value-Based Weights

6

B. DETERMINE AFTER-TAX COSTOF EACH CAPITAL STRUCTURE COMPONENT (kd and ks)

C. ESTIMATE THE WACC FOR

SPECIFIED CAPITAL STRUCTURE

WACC = D/V(kd)(1 - tax rate) + S/V(ks) Where “V” is “D” + “S”

7

D. COST OF DEBT CAPITAL: USE OF BOND RATINGS

1. Investment Grade Debt (Aaa, Aa, A, & Baa)

[Estimate the bond rating and determine the

market interest rate for that bond rating.]

2. High-Yield (“Junk”) Bonds (Ba or lower

bond ratings)8

E. COST OF COMMON EQUITY CAPITAL

1. The CAPITAL ASSET PRICING MODEL (CAPM) APPROACH

[CAPM describes the relationship between required rates of return and risk on assets held in well-diversified portfolios]

9

10

11

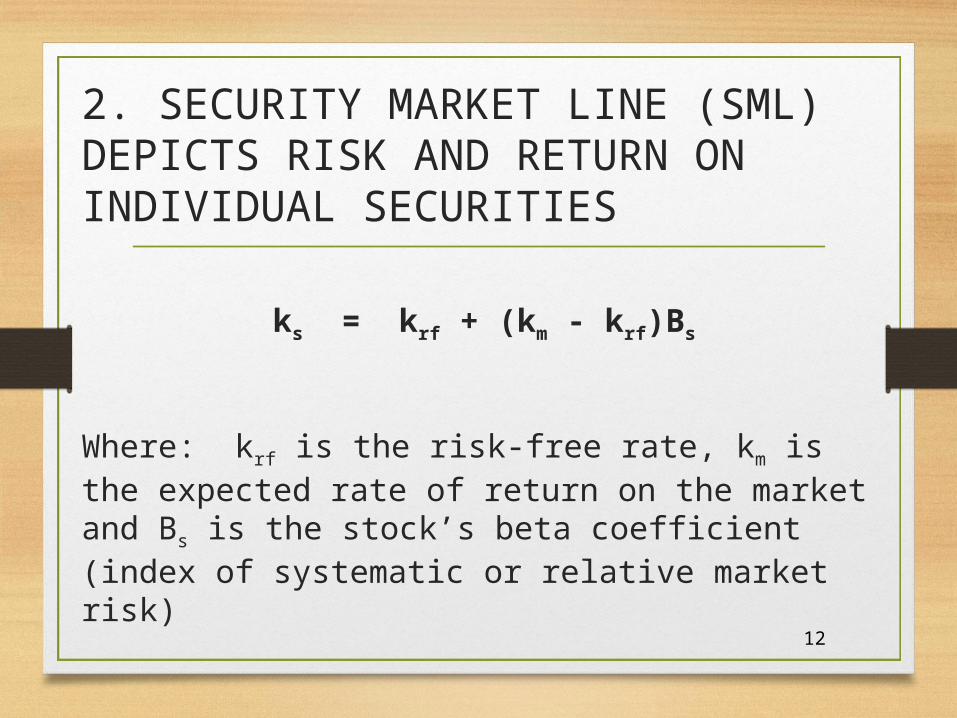

2. SECURITY MARKET LINE (SML) DEPICTS RISK AND RETURN ON INDIVIDUAL SECURITIES

ks = krf + (km - krf)Bs

Where: krf is the risk-free rate, km is the expected rate of return on the market and Bs is the stock’s beta coefficient (index of systematic or relative market risk)

12

a. Estimating the Average Annual Market Risk Premium (MRP)

Market Risk Premium = [km - krf]

[Estimate the future MRP by first determining an average historical MRP. Then, adjust the historical MRP if the future returns are expected to differ from historical average expectations.] 13

b. Business Risk

[Unlever Equity Beta (the observed Beta, BL) to get to the Asset Beta (BU) which reflects business risk]

BU = BL/[1 + D/S(1 - tax rate)]

Where “D” is debt and “S” is equity

14

c. Financial Risk

[Relever the Asset Beta (BU) to reflect the new capital structure and the new Equity Beta (BL)]

BL = BU[1 + D/S(1 - tax rate)]

15

d. New Cost of Common Stock

[Use new Beta estimate to re-estimate the ks using the SML]

ks = krf + (km - krf)Bs

16