TOPIC 2.ASSET RELATIONSHIPS. -...

41

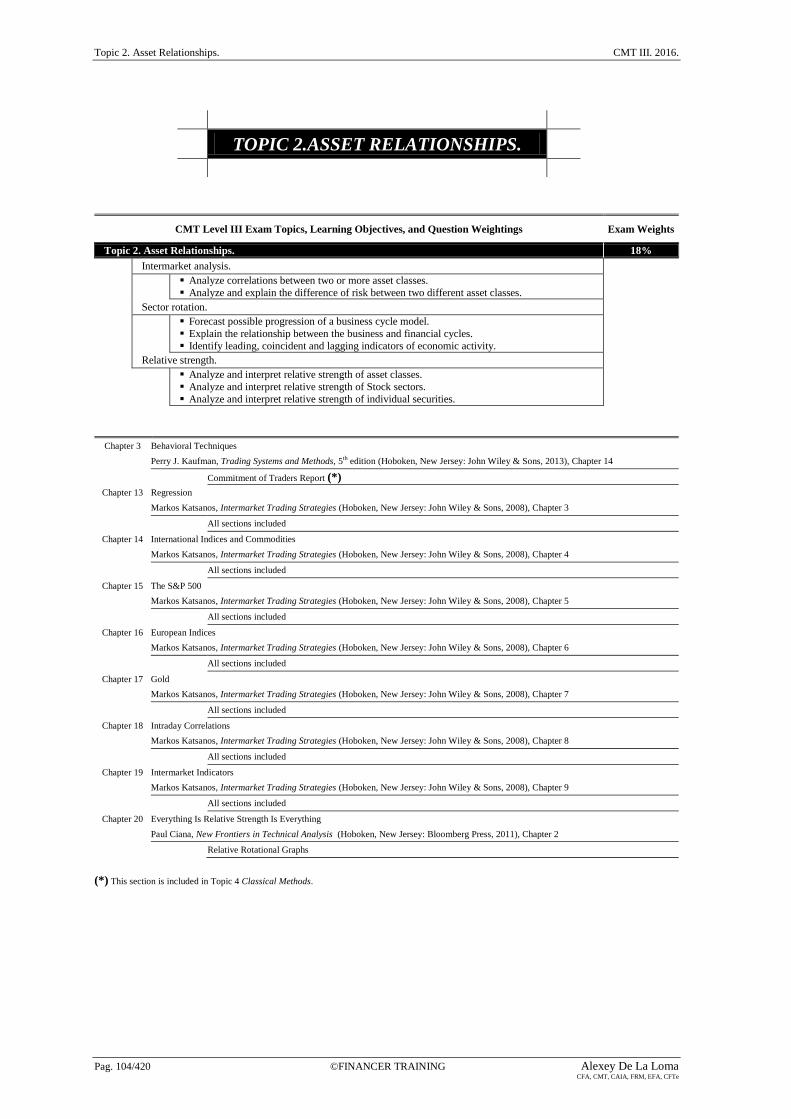

Topic 2. Asset Relationships. CMT III. 2016. Pag. 104/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe TOPIC 2.ASSET RELATIONSHIPS. CMT Level III Exam Topics, Learning Objectives, and Question Weightings Exam Weights Topic 2. Asset Relationships. 18% Intermarket analysis. Analyze correlations between two or more asset classes. Analyze and explain the difference of risk between two different asset classes. Sector rotation. Forecast possible progression of a business cycle model. Explain the relationship between the business and financial cycles. Identify leading, coincident and lagging indicators of economic activity. Relative strength. Analyze and interpret relative strength of asset classes. Analyze and interpret relative strength of Stock sectors. Analyze and interpret relative strength of individual securities. Chapter 3 Behavioral Techniques Perry J. Kaufman, Trading Systems and Methods, 5 th edition (Hoboken, New Jersey: John Wiley & Sons, 2013), Chapter 14 Commitment of Traders Report (*) Chapter 13 Regression Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 3 All sections included Chapter 14 International Indices and Commodities Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 4 All sections included Chapter 15 The S&P 500 Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 5 All sections included Chapter 16 European Indices Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 6 All sections included Chapter 17 Gold Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 7 All sections included Chapter 18 Intraday Correlations Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 8 All sections included Chapter 19 Intermarket Indicators Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 9 All sections included Chapter 20 Everything Is Relative Strength Is Everything Paul Ciana, New Frontiers in Technical Analysis (Hoboken, New Jersey: Bloomberg Press, 2011), Chapter 2 Relative Rotational Graphs (*) This section is included in Topic 4 Classical Methods.

Transcript of TOPIC 2.ASSET RELATIONSHIPS. -...

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 104/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

TOPIC 2.ASSET RELATIONSHIPS.

CMT Level III Exam Topics, Learning Objectives, and Question Weightings Exam Weights

Topic 2. Asset Relationships. 18%

Intermarket analysis.

Analyze correlations between two or more asset classes.

Analyze and explain the difference of risk between two different asset classes.

Sector rotation.

Forecast possible progression of a business cycle model.

Explain the relationship between the business and financial cycles.

Identify leading, coincident and lagging indicators of economic activity.

Relative strength.

Analyze and interpret relative strength of asset classes.

Analyze and interpret relative strength of Stock sectors.

Analyze and interpret relative strength of individual securities.

Chapter 3 Behavioral Techniques

Perry J. Kaufman, Trading Systems and Methods, 5th edition (Hoboken, New Jersey: John Wiley & Sons, 2013), Chapter 14

Commitment of Traders Report (*)

Chapter 13 Regression

Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 3

All sections included

Chapter 14 International Indices and Commodities

Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 4

All sections included

Chapter 15 The S&P 500

Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 5

All sections included

Chapter 16 European Indices

Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 6

All sections included

Chapter 17 Gold

Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 7

All sections included

Chapter 18 Intraday Correlations

Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 8

All sections included

Chapter 19 Intermarket Indicators

Markos Katsanos, Intermarket Trading Strategies (Hoboken, New Jersey: John Wiley & Sons, 2008), Chapter 9

All sections included

Chapter 20 Everything Is Relative Strength Is Everything

Paul Ciana, New Frontiers in Technical Analysis (Hoboken, New Jersey: Bloomberg Press, 2011), Chapter 2

Relative Rotational Graphs

(*) This section is included in Topic 4 Classical Methods.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 105/420 CFA, CMT, CAIA, FRM, EFA, CFTe

1-year trendline shows inflation

Seasonal lows

Seasonal highs

6-month moving average

2.1. Regression Analysis.

Regression analysis is a way of measuring the relationship between two or more sets of data. A stock analyst

might want to know the relationship between the price of gold per ounce and the share price of Barrick Gold

Corporation. Regression analysis involves statistical measurements to determine the type of relationship that

exists between the data studied. Many of the concepts are important in technical analysis and should be

understood by all technicians.

2.1.1. Components of a time series.

Regression analysis is often applied separately to the basic components of a time series. These basic

components are the trend, seasonal, and cyclic elements. These three factors are present in all price data. The

part of the data that cannot be explained by these three elements is considered random, or unaccountable

price movement.

Trends are the basis of many trading systems. Long-term trends can be related to economic factors, such as

changing interest rates, inflation, and even consumer confidence.

Major fluctuations above and below the long-term trend are attributed to cycles. Both business and industrial

cycles respond to changes in supply and demand.

Seasonality, the third component of price movement, is a form of cycle that depends on the calendar year.

The travel industry is much more active in the summer than winter, and there is a much higher demand for

electricity in the summer. This chapter concentrates on trend identification, using the methods of regression

analysis.

2.1.2. Characteristics of Price Data.

A time series is not just a series of numbers, but ordered pairs of price and time. Most trading strategies use

one price per day, usually the closing price, although some methods average the high, low, and closing

prices. The use of less frequent data causes a smoothing effect. The highest and lowest prices will usually not

appear, and the data will seem less volatile. Even when using daily closing price data, the intraday highs and

lows have been eliminated, and the closing prices show less erratic movement.

Selection of calculation period.

A regression analysis, which can identify price direction over a specific time period, will not be

influenced by cyclical patterns or short-term trends that are the same length as the time interval used in

the analysis. For example, if wide seasonal swings occurred during the year but prices ended at about the

same level each year (rising slightly due to inflation), a two-year regression line would be a straight line

that split the fluctuations in half. This is illustrated in Figure 2-1.

The time interval used in regression analysis is selected to be long if the impact of short-term patterns is

to be reduced. If you do not want to remove the effects of seasonality or longer cycles, the time interval of

the regression analysis should be less than one-half of that period (e.g. a 3- or 6-month trend will show

the seasonal price changes).

Source: Perry Kaufman Figure 2-1

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 106/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

2.1.3. Linear Regression

When most people talk about regression, they think about drawing a straight line through the center of some

period of price movement. But regression is a simple and powerful tool for explaining the relationship

between two time series. Those series may be two related stocks or futures or, in the case of a single time

series, the relationship between price and time series. At the end of this chapter, we will use the slope of a

linear regression applied to a single price series to create a trend trading method.

In this chapter we focus on explaining the price movement of one market by using another. Both are time

series, that is, they post a new price each day. We start with the linear relationship between two price series,

X and Y. A linear relationship will try to find the value of Y for each value of X using the formula for a

straight line, Y=aX+b, where a is the slope of the line, and b is the Y-intercept, the point where the line

crosses the Y axis when the value of X is zero. The linear regression is also called a straight-line fit or simply

a best fit.

Explaining, not predicting.

You may have noticed that we refer to explaining instead of predicting when talking about the regression

implications. We are finding the past relationship between two price series. The regression analysis may

establish what you see as a fair value for one market based on the price of the other. In order to forecast a

price, you will need to establish that conditions at the date of your forecast are likely to be the same as the

period over which the regression was calculated.

Calculating the best straight-line fit.

The simplest example of linear regression is the one used most often by traders, calculating the best

straight-line fit through a selected period of price movement. This is done in the same way as finding the

relationship between two price series, except that we will substitute the simple sequence 1, 2, 3, 4, …. for

the second series. The technique used is called the method of least squares. We choose ten days of price

movement in Wall-Mart during 2001 (Table 2-1). In order to find the best straight-line fit, we begin with

the equation for a straight line:

( 2.1)

In this equation, Y is the dependent variable because it is created from the value of X, the independent

variable. The slope, b, is the relative change in Y for every unit change in X. Therefore, if b=2 then Y

moves twice as fast as X. The Y-intercept, a, is an adjustment in the price level to bring X and Y into

alignment. It is also the point at which the straight line crosses the Y-axis when X=0.

Method of Least Squares.

The method of least squares finds the straight line which comes closest to all prices. To do this, calculate

the sum of the squares of all the differences between the price and the corresponding value of the straight

line and choose the line that has the smallest total deviation. The mathematical expression for this is:

( 2.2)

where,

S = the sum of the squares of the error at each of the ten points on the straight line (one

point for each price, designated by i = 1, 2, 3,…)

n = number of data points (10 in our example)

yi = one of the actual prices of Wal-Mart

ŷi= the estimated value of this price on the straight line (it is usually written with a hat)

yi – ŷ = the difference between the actual value of y at i and the predicted line value at ŷi

Graphically, the individual deviations, or errors, for the first four points may look like those in Figure 2-2.

Each actual data point is (1, y1), (2, y2), (3, y3),….., and the corresponding position on the straight line is

(1, ŷ1), (2, ŷ2), (3, ŷ3),….. The square of all (yi – ŷi) is always positive, thereby magnifying the importance

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 107/420 CFA, CMT, CAIA, FRM, EFA, CFTe

Approximation line

Approximated point Price

Actual point (observed)

Time

y1

y2

y3

y4 ŷ1

ŷ2 ŷ3

ŷ4

x1 x2 x3 x4

of those data points that are farther from the approximated line on either side and reducing the

significance of those points for which the approximation is good.

Source: Perry Kaufman Figure 2-2

To use the least-square method for solving the Wal-Mart time/price relationship, look for the solution to

the straight line Y=a+bX, expressed as:

( 2.3)

In order to solve these equations, construct a table where all of the individual expressions in the two

formulas can be calculated (Table 2-1). We can now substitute the values on the Sums line into the two

equations:

The equation for the least-squares approximation is

Selecting values for X and Y and solving for Y gives the results shown in the right column of Table 2-1

and drawn along with the original prices for Wal-Mart in Figure 2-3. The straight line approximation

increased by $0.707 per day and the approximation starts at $45.54, where X=0.

Dates

Wal-Mart

Price

Y

Sequence

Number

X X2 XY Y2

Straight

Line

Value

9/21/2001 44,66 1 1 44,66 1994,52 46,25

9/24/2001 47,28 2 4 94,56 2235,40 46,96 9/25/2001 48,40 3 9 145,20 2342,56 47,66

9/26/2001 49,48 4 16 197,92 2448,27 48,37

9/27/2001 49,39 5 25 246,95 2439,37 49,08 9/28/2001 49,50 6 36 297,00 2450,25 49,78

10/01/2001 49,76 7 49 348,32 2476,06 50,49

10/02/2001 51,60 8 64 412,80 2662,56 51,20 10/03/2001 52,73 9 81 474,57 2780,45 51,90

10/04/2001 51,50 10 100 515,00 2652,25 52,61

Sums 494,30 55,00 385,00 2776,98 24481,69

Source: Perry Kaufman Table 2-1

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 108/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

Source: Own Elaboration Figure 2-3

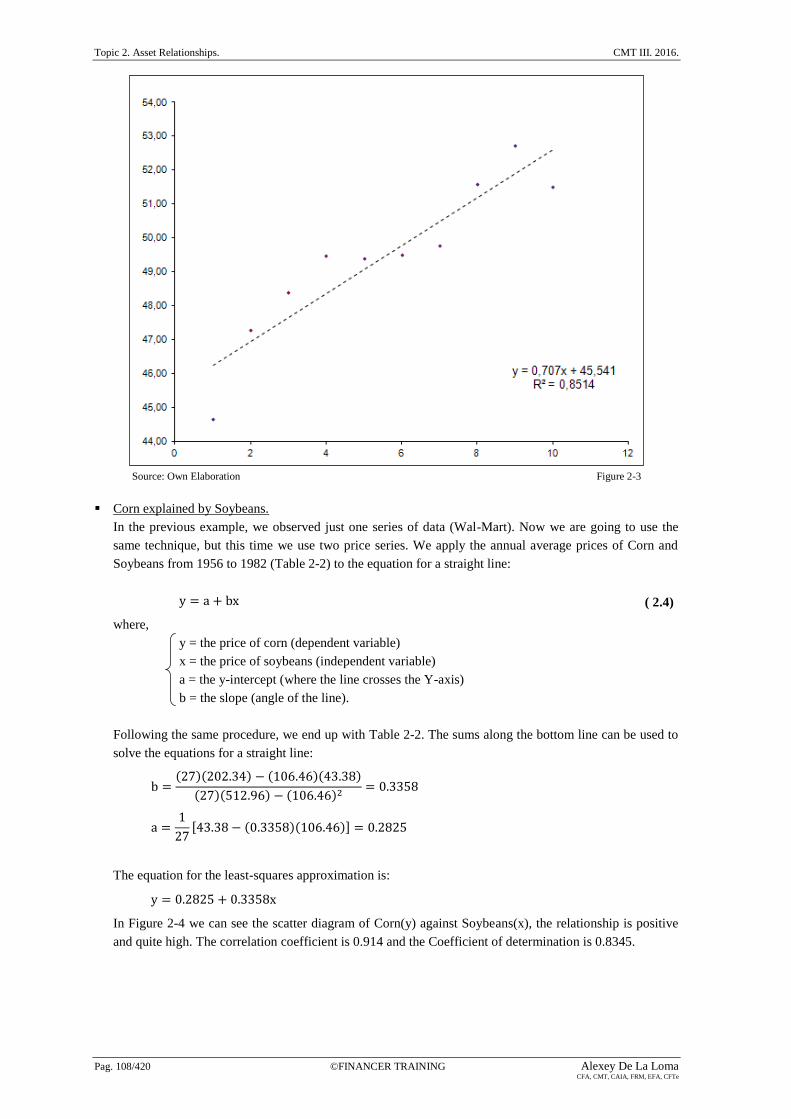

Corn explained by Soybeans.

In the previous example, we observed just one series of data (Wal-Mart). Now we are going to use the

same technique, but this time we use two price series. We apply the annual average prices of Corn and

Soybeans from 1956 to 1982 (Table 2-2) to the equation for a straight line:

( 2.4)

where,

y = the price of corn (dependent variable)

x = the price of soybeans (independent variable)

a = the y-intercept (where the line crosses the Y-axis)

b = the slope (angle of the line).

Following the same procedure, we end up with Table 2-2. The sums along the bottom line can be used to

solve the equations for a straight line:

The equation for the least-squares approximation is:

In Figure 2-4 we can see the scatter diagram of Corn(y) against Soybeans(x), the relationship is positive

and quite high. The correlation coefficient is 0.914 and the Coefficient of determination is 0.8345.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 109/420 CFA, CMT, CAIA, FRM, EFA, CFTe

Source: Own Elaboration Figure 2-4

i

Corn

Yi

Soybeans

Xi Xi

2 XiYi Yi2

1956 1 1,27 2,43 5,90 3,09 1,61

1957 2 1,19 2,26 5,11 2,69 1,42

1958 3 1,10 2,15 4,62 2,37 1,21 1959 4 1,10 2,07 4,28 2,28 1,21

1960 5 1,05 2,03 4,12 2,13 1,10

1961 6 1,00 2,45 6,00 2,45 1,00 1962 7 0,98 2,36 5,57 2,31 0,96

1963 8 1,09 2,44 5,95 2,66 1,19

1964 9 1,12 2,52 6,35 2,82 1,25 1965 10 1,18 2,74 7,51 3,23 1,39

1966 11 1,16 2,98 8,88 3,46 1,35

1967 12 1,24 2,93 8,58 3,63 1,54 1968 13 1,03 2,69 7,24 2,77 1,06

1969 14 1,08 2,63 6,92 2,84 1,17

1970 15 1,15 2,63 6,92 3,02 1,32 1971 16 1,33 3,08 9,49 4,10 1,77

1972 17 1,08 3,24 10,50 3,50 1,17

1973 18 1,57 6,22 38,69 9,77 2,46 1974 19 2,55 6,12 37,45 15,61 6,50

1975 20 3,02 6,33 40,07 19,12 9,12

1976 21 2,54 4,92 24,21 12,50 6,45 1977 22 2,15 6,81 46,38 14,64 4,62

1978 23 2,02 5,88 34,57 11,88 4,08

1979 24 2,25 6,61 43,69 14,87 5,06 1980 25 2,52 6,28 39,44 15,83 6,35

1981 26 3,11 7,61 57,91 23,67 9,67

1982 27 2,50 6,05 36,60 15,13 6,25

Sums Σy

43,38

Σx

106,46

Σx2

512,96

ΣxΣy

202,34

Σy2

82,29

Source: Perry Kaufman Table 2-2

2.1.4. Linear Correlation.

In the previous sections we used price series that had a clear relationship; therefore, the results appeared

valid. The linear correlation, which produces a value called the coefficient of determination (R2), or the

correlation coefficient (r), expresses the strength of the relationship between the data and it can vary from -1

to +1. If R2 is less than about 0.20, then the linear regression has no practical value. To calculate the Pearson

Correlation Coefficient we use the following formula:

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 110/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

( 2.5)

where,

n = number of data points (10 in our example)

cov(x,y) = Covariance between variables X and Y

σx = Standard deviation of variable X

σy = Standard deviation of variable Y

μx = Average of variable X

μy = Average of variable Y.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 111/420 CFA, CMT, CAIA, FRM, EFA, CFTe

In the following examples we can see the different values of r and their significance in a regression analysis

of two price series:

r > 0.

If r is positive, we have a positive linear correlation. The data points are

above and below a straight line going upward to the right. In Figure

2-5, r = 0.514.

Figure 2-5

r < 0.

If r is negative, we have a negative linear correlation. The data points

are above and below a straight line going downward to the right. In

Figure 2-6, r = - 0.634. This means that when one variable goes up, the

other goes down.

Figure 2-6

r = 0.

If the correlation coefficient is zero or near zero, we have no linear

correlation at all. In Figure 2-7, r = 0.03.

Figure 2-7

r = +1.

If r is equal to +1, a perfect positive correlation exists. The data points

are along a straight line going upward to the right. In Figure 2-8,

r = 0.98.

Figure 2-8

r = –1.

If r is equal to –1, a perfect negative correlation exists. The data points

are along a straight line going downward to the right. In Figure 2-9, r = –

0.98.

Figure 2-9

Forecasting using Regression.

A distinct advantage of regression analysis is that it allows the analyst to forecast price movement. In the

case of the linear regression, the forecast is simply an extension of the line. For example in the corn (y)

and soybeans (x) model, where the equation for the least-squares approximation is:

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 112/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

95% confidence interval

“Outliers” Price

Regression line

Time

If we have an estimation of soybeans with a value of 30, the forecast value of corn comes from:

Confidence Bands.

Regression analysis includes its own measure of accuracy called confidence bands. It is based on a

probability distribution of the errors in the fitted equation and the size of the data sample. Looking at

Figure 2-9, the straight line cannot touch all the points, but its “goodness of fit” may be measured by

using the standard deviation of the errors to determine the variance over the total number of data points

(n). If the actual data points are yi, their corresponding value on the fitted line ŷi and ei = yi– ŷi , then, the

standard deviation of errors is:

( 2.6)

Referring to the table of normal distribution, the 95% level is equivalent to 1.96 standard deviations.

Then, a confidence band of 95% placed around the forecast line, is written:

( 2.7)

( 2.8)

The points that are outside the band (Figure 2-10) are of particular interest and can be interpreted in two

ways:

They are not representative of normal price behavior and are expected to correct the levels within the

bands.

The model was not performed on representative or adequate data and should be reestimated.

Source: Perry Kaufman Figure 2-10

2.1.5. Nonlinear approximations of two variables.

The linear regression, also called a first-order equation, is the simplest way of finding the relationship

between two price series. It uses only one multiplier (the slope). By adding a third term, cx2, the

approximation can be made much more accurate. The third term, x2, allows the approximation to use a

parabolic curve. The fourth term, dx3, adds inflection. The general polynomial form that approximates any

curve is:

( 2.9)

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 113/420 CFA, CMT, CAIA, FRM, EFA, CFTe

Log

Price

Linear

Time

Exponential

Curvilinear

Price

The first two terms on the right side of the equal sign form the equation for a straight line (where a0 was

called a and a1 was called b). For most price forecasting, the second-order equation, also called curvilinear,

which uses three terms, is sufficient:

( 2.10)

2.1.6.Transforming nonlinear to linear.

Two curves that are often used to forecast prices are logarithmic and exponential. The exponential, curving

up, is used to scale price data that become more volatile at higher levels. Each of these forms can be easily

transformed into linear relationships and solved using the method of least squares. This will allow you to fool

the computer into solving a nonlinear problem using a linear regression tool. To solve the logarithmic

relationship, substitute ln x for x, ln a for a, and ln y for y.

2.1.7. Evaluation of two-variable techniques.

Of the three curve-fitting techniques, the curvilinear and exponential results are very similar, both curving

upward and passing through the main cluster of data points at about the same incline. The log approximation

curves downward after passing through the main group of data points at about the same place as the other

approximations. To evaluate objectively whether any of the nonlinear methods are a better fit than the linear

approximation, find the standard deviation of the errors, which gives a statistical measurement of how close

the fitted line comes to the original data points. In the example of Figure 2-11, the curvilinear approximation

is the best, and the logarithmic, which curves downward, is noticeably the worst.

Source: Perry Kaufman Figure 2-11

2.1.8. Multivariate approximations.

Regression analysis is most often used in complex economic models to find the combination of two or more

independent variables that best explain or forecast prices. A simple application of annual production and

distribution of soybeans will determine whether these factors are significant in determining the price of

soybeans. Applying the method of least squares which was used for a simple linear regression, the equation

for two independent variables is:

( 2.11)

where,

y = the resulting price, in this case soybeans

x1 = the total production (supply)

x2 = the total distribution (demand)

a, b, c = constants, or weighting factors, to be calculated

As in the linear approximation, the solution to this problem will be found by minimizing the sum of the

squares of the errors at each point:

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 114/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

( 2.12)

The solution to the multivariate problem of two independent variables x1 and x2 requires the following three

least-squares equations:

( 2.13)

( 2.14)

( 2.15)

If after calculating the sums, we obtain the following equations:

We just solve this three-variable system of three equations and the resulting multiple regression is:

( 2.16)

where,

x1 = the production of soybeans in billions of bushels.

x2 = demand in billions of bushels.

The coefficient of supply is much larger than the coefficient of demand, therefore it is the principal factor in

the determination of price.

2.1.9. Assumptions and nonparametric regression.

Correlation and regression analysis share some characteristics, such as the model assumptions, being linearity

the most relevant assumption in both cases. Although regression analysis can also be calculated as a

non-linear model, the most frequent models are the SLR (simple linear regression) and the MLR (multiple

linear regression). Linearity can be visually assessed by a simple inspection of the scatterplots.

Normality (Gaussian distribution) is another assumption that represents a problem especially when raw stock

or index prices are used, because if we apply log differences or percentage yields, normality is not a big

concern. Normality can be visually assessed by looking at frequency histograms, or it can be assessed

through statistical tests (normality tests), such as the Shapiro-Wilks W test or the Kolmogorov-Smirnov D

test. Finally, long-term tails problem can be partially solved by removing some of the most extreme outliers.

If we are interested in making no assumptions about the population distribution (normality), and relaxing the

assumption about linearity, we should use a nonparametric regression. Markos Katsanos recommends the

following two methods to perform a nonparametric regression:

Smoothing Splines.

This methodology minimizes the sum of squared residuals, adding a term in order to penalize the

roughness of the fit.

Kernel Regression.

This methodology is based on a class of algorithms called SVMs or Support Vector Machines, which are

closely related to neural networks. This method applies a Kernel function to find an optimal separating

hyperplane in order to separate two classes of patterns with maximal margin. This method is usually

preferred because it achieves a good performance in forecasting high noise and non-stationary financial

time series, even when dealing with a large number of inputs.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 115/420 CFA, CMT, CAIA, FRM, EFA, CFTe

2.2. International Indices and Commodities.

When you study this chapter, do not forget that all statistics and characteristics of these indices are based on a

reading assignment published by Markos Katsanos in 2008, so some data could be outdated. Let us stats with

some definitions:

Performance Index.

All income from dividends and bonus distributions are reinvested into the index.

Capitalization-Weighted or market-value weighted Index.

It is a type of market index whose individual components are weighted according to their market

capitalization, so that larger components carry a larger percentage weighting.

Market Capitalization.

It is the total market value (in dollars, euros, etc) of all of a company's outstanding shares. Market

capitalization is calculated by multiplying a company's shares outstanding by the current market price of

each share.

2.2.1. The DAX Index (symbol: GDAXI).

This is the leading index of the Deutsche Börse, and it is composed by the 30 largest and most actively traded

German equities (blue chips). It is highly cyclical and the inclusions and exclusions are performed each

September by the Deutsche Börse. It is a performance and capitalization-weighted index. This index is used

as the underlying for futures (symbol: FDAX) and options in the Eurex Exchange from 8:00 to 22:00 CET.

The multiplier of the future contract is 25€ per index point, and futures are highly liquid with an average

volume of more than 200,000 contracts per day, according to Markos Katsanos. Although the DAX index is

the leading index of the Deutsche Börse, this market also calculates other indices:

MDAX.

It is based on the 50 largest companies from the classic sector of the Frankfurt Stock Exchange, that rank

below the DAX components in terms of market capitalization and trading volume.

TecDAX.

It is based on the 30 largest companies from the technology sector of the Frankfurt Stock Exchange, that

rank below the DAX components in terms of market capitalization and trading volume. It is equivalent to

the U.S. Nasdaq 100 index.

SDAX.

It is based on 50 shares (small caps) from the classic sector that rank directly below the MDAX in terms

of market capitalization and trading volume. It is equivalent to the U.S. Russell 2000 index.

HDAX.

It is based on the largest (large cap index) 110 German equities from all sectors of the economy. It is

equivalent to the U.S. Russell 1000 index.

LDAX.

It is a late index based on the price development of DAX index after the Xetra electronic-trading system

closes and it is based on the floor trading at the Frankfurt Stock Exchange. It is computed daily between

17:30 and 20:00 CET.

VDAX and VDAX-NEW.

These are DAX Volatility indices that track the implied volatility of the DAX index. The equivalent to the

CBOE volatility index (VIX). Volatility indices measure in percentage terms whether the DAX options

are selling above or below their fair values. The new volatility DAX index is based on options that are

both ATM (at the money) and OTM (out of the money), while the VDAX takes into account only ATM

options.

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 116/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

2.2.2. The CAC 40 Index (symbol: FCHI).

This is the leading index of the French market (Euronext Paris), and it is composed by the 40 largest and

most actively traded French equities (blue chips). The base value of this index was 1000 when it was born on

the 31st of December, 1987. The acronym CAC stands for Cotation Assitée en Continu (Continuous Assisted

Quotation).

It is a performance and capitalization-weighted index. However, since the 1st of December, 2003, CAC-40

index is no longer weighted by the total market capitalization of their component stocks but by their free float

adjusted market capitalization. This methodology is now applied to other major indices and it ensures greater

coherence with the real allocation of companies. It also limits the volatility caused by the difference between

the weight of a stock in the index, and the corresponding free float or available shares in the market. The

index composition (inclusions and exclusions) is reviewed quarterly and the maximum weight allowed for an

individual component is 15%.

This index is used as the underlying for futures and options in the MONEP Exchange (Euronext). The

multiplier of the CAC-40 future contract is 10€ per index point, and futures are highly liquid with an average

volume of more than 120,000 contracts per day, according to Markos Katsanos. MONEP also trades equity

options, and long- and short-term options.

2.2.3. The FTSE 100 Index.

This is the leading index of the British market, and it is composed by the 100 largest and most actively traded

equities on the LSE (London Stock Exchange). The FTSE, pronounced “footsie”, was born on the 3rd

of

January, 1984. It is a performance and capitalization-weighted index, and it is very sensitive to oil prices. The

index composition is reviewed quarterly and it is maintained by the FTSE Group, a now independent

company which originated as a joint venture between the Financial Times and the LSE. Remember that the

acronym FTSE stands for Financial Times Stock Exchange. This index is used as the underlying for futures

and options in LIFFE (London International Futures & Options Exchange).

2.2.4. The Dow Jones Stoxx 50 (STXX50) and the Euro Stoxx 50 (STOXX50E or ESTX50).

The Dow Jones Stoxx 50 is composed by the 50 most actively traded stocks in the pan-European area, while

the Dow Jones Euro Stoxx 50 tracks the 50 most actively traded stocks in the Euro Zone (Austria, Belgium,

Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal and Spain). Both

are market-value weighted indices and both have actively traded futures that trade at the Eurex (DTB) market

from 8:00 to 22:10 CET. The base value of the DJ Euro Stoxx 50 index was 1000 when it was born on the

31st of December, 1991. This index uses the free float to determine the market capitalization of its

components.

2.2.5. The Nikkei 225 Index.

This is the leading index of the Japanese market, and it is composed by the 225 largest and most liquid

Japanese equities traded in the Tokyo Stock Exchange (TSE). It is not a market capitalization index, but a

price-weighted index whose components are reviewed once a year. A price-weighted index is similar to a

simple average but the divisor is adjusted to maintain continuity and to reduce the effect of external factors

not directly related to the market. The denominator is, for example, adjusted by splits.

The Nikkei index reached its all-time high on the 29th

of December, 1989, and from this top it has dropped

down more than 80%. This top index level was achieved due to an impressive real estate bubble. This index

is used as the underlying for futures and options in Osaka, and in the Chicago Mercantile Exchange (CME).

2.2.6. The Hang Seng Index (HSI).

This is the leading index of the Stock Exchange of Hong Kong (SEHK). This index was born on the 24th

of

November, 1969, and Hang Seng futures trade in the Hong Kong Futures Exchange since 1986, with a

multiplier of HKD 50 per index point, while mini contracts have a multiplier of HKD 10.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 117/420 CFA, CMT, CAIA, FRM, EFA, CFTe

2.2.7. The uptick rule in the U.S. equity markets.

The uptick rule, a regulation prohibiting equity short sales following downticks, was created after the 1929

stock market crash in order to increase downward momentum in bear markets. The rule tries to avoid sharp

declines requiring every short sale to be executed only on a higher price than a previous trade (uptick). This

rule was in effect from 1929 to 2007 (78 years), when the Securities and Exchange Commission (SEC)

removed it.

2.2.8. The Dollar Index.

This index indicates the international value of the U.S. Dollar in terms of its more relevant partners, by

averaging the exchange rates between the USD and six major world currencies: EUR, JPY, GBP, CAD, SEK,

and CHF, according to a geometric weighted average, in which the power of each currency represents its

weight into the final value, and each currency is expressed in U.S. dollars (USD). Therefore, the Dollar Index

represents the value of the USD against a basket of six currencies. The constant of this equation

(50.14348112) was introduced when the index was born in order to start with a 100 base value in 1973, when

the world’s major trading nations abandoned the 25-year-old Bretton Woods agreement to fix their currency

rates:

( 2.17)

where,

USDI = US Dollar Index

EUR = Euro (57.6%).

JPY = Japanese Yen (13.6%).

GBP = Great Britain Pound (11.9%).

CAD = Canadian Dollar (9.1%).

SEK = Swedish Krona (4.2%).

CHF = Swiss franc (3.6%).

0.576 + 0.136 + 0.119 + 0.091 + 0.042 + 0.036 = 1.00

If we want to express the JPY, the CAD, the SEK, and the CHF in their more familiar format in JPY per

USD, in CAD per USD, in SEK per USD, and in CHF per USD, we just have to change the sign of the

exponents.

( 2.18)

Dollar Index derivatives started trading in the NYBOT (New York Board of Trade), and this exchange was

then bought by the Intercontinental Exchange or ICE. The future multiplier is $1,000 per index point. The

Dollar Index is a crucial element when intermarket relationships (currencies, fixed income, equities,

commodities, etc) are analyzed, because the U.S. Dollar plays a key role in the current configuration of

international financial markets. According to Markos Katsanos, the more relevant factors affecting the Dollar

Index are:

The U.S. trade deficit.

The U.S., Japanese, Canadian, and European interest rate and bond yields.

CPI inflation.

Quarterly Gross Domestic Product (GDP).

Non-farm payroll.

2.2.9. Oil indices: XOI and OIX.

In the last decades, oil has become a predominant commodity, such as gold or natural gas. The never-ending

increasing demand, especially by China and India has caused oil price to rise dramatically, and some analysts

try to determine when the world crude productivity will start to decline, leading us to a permanent oil shock

era.

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 118/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

The most popular indices to measure oil prices are the AMEX oil index (XOI) and the CBOE oil index

(OIX). According to Markos Katsanos, XOI is slightly preferred to OIX. Both indices are price weighted and

based on a basket of widely-held corporations (e.g., Apache, Exxon Mobil, Total, British Petroleum, etc)

involved in the exploration, production, and development of petroleum.

XOI was established with a base value of 125 on the 27th

of August, 1984, and it is made up of 12 component

companies, with a great range of market capitalizations, and this is cause of its main disadvantage. As each

price-weighted index (e.g., DJIA, DJUA, DJTA, etc), shares with the higher prices are over-weighted, while

shares with lower prices are under-weighted, independently of their market capitalization (true value). It is

worth noting that share prices are meaningless, and a company of any size can have whatever share price

range it wants by splitting or reverse-splitting its stock.

2.2.10. The CRB (Commodity Research Bureau) Index.

This is an index based on a basket of commodities, so it is ideal to follow commodity prices as an asset class.

Since its creation, as the commodity markets evolved, it has changed its composition and its name

periodically. Let us show the evolution of this well-known commodity index.

The CRB was created by the Commodity Research Bureau in 1957, taking the prices of 28 commodities. In

1987, the basket was reduced to 21 items. In 1995, the basket was again reduced to 17 items. From the

original 28 items included in 1957, the commodities eliminated were those that lost its relevance, such as

onions, rye or potatoes. In 2005 three new commodities were added: unleaded gas, aluminum, and nickel,

and the calculation methodology also changed from a geometric average to a weighting arithmetic average in

order to better reflect the commodity prices in a more volatile environment. By its very mathematical nature,

geometric averaging continually rebalanced the index, decreasing exposure to rising commodities and

increasing exposure to declining commodities. As an example of the different weights, the weight of crude

oil is 23 times larger than orange juice or hogs, and 4.6 times larger than sugar’s weight. When this reading

assignment was published, the RJ/CRB Index has the following composition:

Metals: 20%.

Energy: 39%.

Tropicals: 21%.

Meats: 7%.

Grains: 13%.

In relation to its name, in 2001 it was changed from CRB Index to Reuters CRB Index, and it changed again,

in 2001, to Reuters/Jefferies CRB Index (RJ/CRB). This index is truly relevant because commodities are

excellent to diversify a traditional fixed-income or equity portfolio.

From an individual perspective, a long- position in commodities provides hedging against inflation and dollar

depreciation, and it also provides additional returns from commodity price appreciation. From a portfolio

perspective, commodities help to achieve desirable long-term results, and to reduce the overall volatility of

their portfolio. In order to help traders and portfolio managers to hold a position in this index, the NYBOT

(New York Board of Trade) offers a future contract with a price multiplier of $200 per index point.

Finally, to conclude this section it is worth noting that Reuters/Jefferies CRB Index has been recognized as

the most relevant barometer for commodity prices, and it is now accepted globally as a standard for tracking

commodity future prices.

2.2.11. The GSCI (Goldman Sachs Commodity Index).

This is another commodity index, created by Goldman Sachs in 1991, and it is composed by 24 items. The

principal difference between GSCI and CRB is that GSCI is heavily weighted in energy futures contracts,

with a 72.5% compared with only 39% in the CRB Index. This overweight in energy, especially crude oil,

explains the exponential growth of GSCI when comparing both commodity indices, as we do in Figure 2-12.

Take note that having an excessive weight in a predetermined sector is not necessarily an advantage, because

it limits the diversification into other commodities which is especially beneficial in periods of declining oil

prices.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 119/420 CFA, CMT, CAIA, FRM, EFA, CFTe

Source: StocksCharts.com Figure 2-12

2.2.12. The XAU and HUI Indices.

The Philadelphia Exchange (PHLX) Gold and Silver Sector (XAU) Index is a capitalization-weighted index,

composed by 16 companies involved in the gold and silver mining industry, while the AMEX Gold BUGS

Index (HUI) is a modified equal-dollar weighted index, composed of 15 unhedged gold mining stocks. The

term BUGS is an acronym standing for Basket of Unhedged Gold Stocks.

2.2.13. The CBOE Volatility Index (VIX).

Volatility is one of the most relevant figures traders and investors use to analyze stock markets. Volatility can

be measured in different ways but the most common calculation is based on the standard deviation.

According to this statistical calculation, volatility is a measure of how prices oscillate around its mean. It

refers to both up and down oscillations, so it has not been devised to detect trends.

Because volatility expresses the price oscillations around its mean, it is mean reverting by nature, so it can be

used to gauge the fear and greed of the uninformed market players, according to the following rule: a high

volatility is a warning about stress, emotion, fear and nervousness, so we should interpret this is a warning

for a market bottom. Remember that sentiment indicators based on uninformed market players are contrary

by nature. On the other hand, a low volatility measure shows a moment of relax and calm, so a potential

market top is around the corner. Therefore, volatility is a figure that helps traders to determine extremes of

market emotion.

Volatility can be historical or implied. Historical volatility is just the standard deviation of prices, so it has

little predictive power, while implied volatility is a way to measure market participants’ anxiousness about

the future, so we will prefer implied volatility as a sentiment indicator.

The implied volatility of an option contract is that value of the volatility of the underlying instrument which,

when input in an option pricing model (such as Black–Scholes) will return a theoretical value equal to the

current market price of the option. A way to measure implied volatility is through the VIX figure. VIX is the

exchange symbol for an indicator of volatility in the trading of S&P-500’s options. Volatility in the trading

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 120/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

options of the NASDAQ composite and the S&P-100 Index are represented by VXN and VXO, respectively.

VIX, VXN and VXO are traded on the CBOE. Additionally, the VXD tracks the volatility of the DJIA (Dow

Jones Industrial Average).

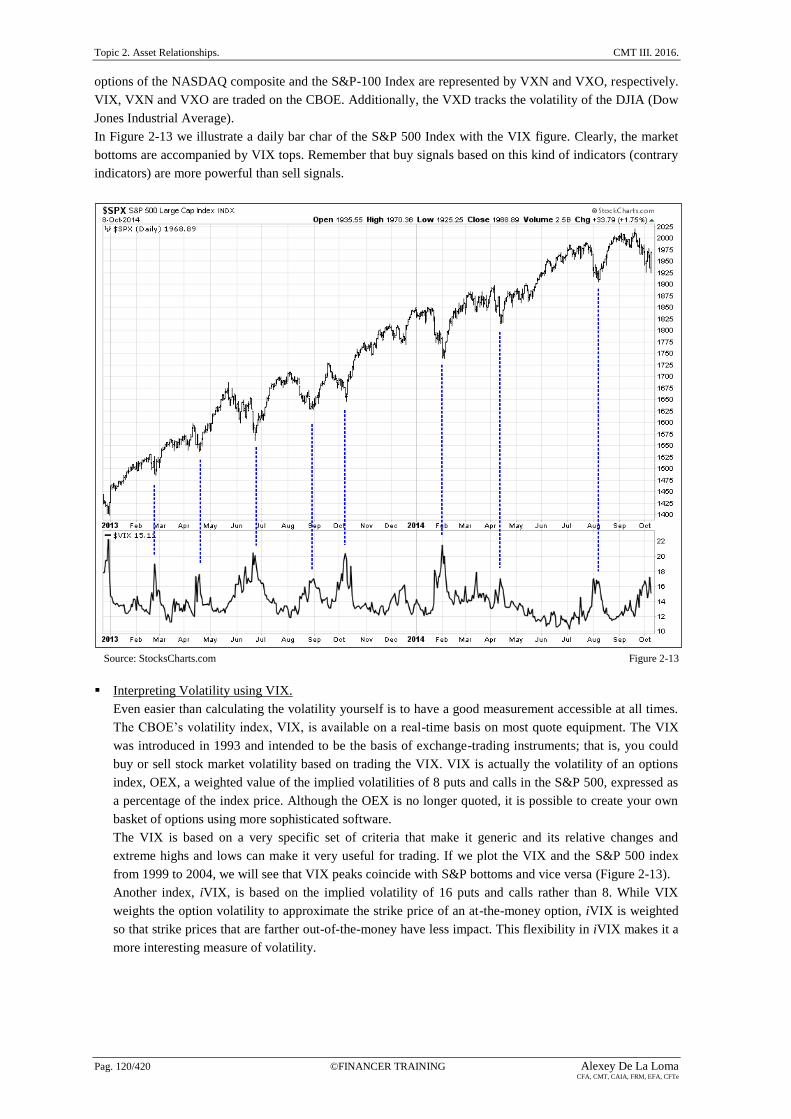

In Figure 2-13 we illustrate a daily bar char of the S&P 500 Index with the VIX figure. Clearly, the market

bottoms are accompanied by VIX tops. Remember that buy signals based on this kind of indicators (contrary

indicators) are more powerful than sell signals.

Source: StocksCharts.com Figure 2-13

Interpreting Volatility using VIX.

Even easier than calculating the volatility yourself is to have a good measurement accessible at all times.

The CBOE’s volatility index, VIX, is available on a real-time basis on most quote equipment. The VIX

was introduced in 1993 and intended to be the basis of exchange-trading instruments; that is, you could

buy or sell stock market volatility based on trading the VIX. VIX is actually the volatility of an options

index, OEX, a weighted value of the implied volatilities of 8 puts and calls in the S&P 500, expressed as

a percentage of the index price. Although the OEX is no longer quoted, it is possible to create your own

basket of options using more sophisticated software.

The VIX is based on a very specific set of criteria that make it generic and its relative changes and

extreme highs and lows can make it very useful for trading. If we plot the VIX and the S&P 500 index

from 1999 to 2004, we will see that VIX peaks coincide with S&P bottoms and vice versa (Figure 2-13).

Another index, iVIX, is based on the implied volatility of 16 puts and calls rather than 8. While VIX

weights the option volatility to approximate the strike price of an at-the-money option, iVIX is weighted

so that strike prices that are farther out-of-the-money have less impact. This flexibility in iVIX makes it a

more interesting measure of volatility.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 121/420 CFA, CMT, CAIA, FRM, EFA, CFTe

2.3. The S&P 500.

In this chapter, Markos Katsanos starts to study intermarket analysis using the most relevant U.S. equity

index, that is, the S&P 500. Evidently, intermarket analysis relies on the premise that previous relationships

will not suffer a severe change in the future, so before making any conclusion it is necessary to determine

whether the correlation coefficient is stable over time. Markets may decouple and a strategy based on a false

assumption might produce a considerable drawdown.

2.3.1. Correlation between the S&P 500 and the international indices.

Before applying a correlation or a regression analysis to two markets, it is necessary to determine the

timeframe of both price series: intraday, daily, weekly, monthly, quarterly, or even annually. The use of

long-term timeframes has the advantage of avoiding windowing error and daily noise (remember that in any

financial time series, the shorter the timeframe the higher the noise). In the empirical tests conducted by

Markos Katsanos in this chapter, correlations rise relevantly when weekly returns replace daily data. The

author conducts nonparametric (Spearman) price correlations between a set of international indices (e.g.,

DJIA, DAX, CAC, Hang-Seng, FTSE, TSX, etc) and the S&P 500 using daily prices and daily percentages

from CSI Data. A different number of years is considered to compare the evolution of the correlation

measure (e.g., 2, 4, 5, 10 and 15 years), so both short-term and long-term relationships are analyzed by

Katsanos.

It is worth noting that a correlation matrix among international indices should be analyzed with extraordinary

care, especially the long-term price correlations, because some of the relationships could be nonlinear.

Because of this, Markos Katsanos always recommends to check a scatterplot or a chart of the related index

before making any significant investment decision based on the figures included in a correlation matrix. An

example of a scatterplot can be found in Figure 2-3.

In order to analyze the evolution of correlations over time, the correlations are calculated, yearly, taking daily

time series from CSI Data. Therefore, if a 16-year period (1992-2007) is analyzed, we have 16 correlations to

see how relationships evolve. Then, Katsanos calculate the average, mean, standard deviation and the

maximum range (highest minus lowest correlation value over each time span) to have a better understanding

of this evolution. However, the standard deviation may not be the best measure of variance as most value

were concentrated at the far right of the histogram (negative skew) making the correlation distribution to

deviate from the Normal or Gaussian distribution. In order to solve this limitation, Markos Katsanos divided

the yearly correlations in percentiles, so, for example, if the 10% percentile of the correlations between the

S&P 500 and the DJIA is 0.61 it means that only 10% of the yearly correlations were below 0.61.

Conclusions about the S&P 500 versus international indices correlation:

The correlation is more stable with high capitalization indices, such as the DJIA or the FTSE, and less

stable with small capitalization indices, such as the Russell 2000.

The correlation is less volatile with European indices, than it is with U.S. indices

The correlations are highly erratic when yearly time segments, over the 16-year study, are considered.

The most and the less unstable correlations correspond to the Nikkei and the FTSE indices,

respectively.

The impact of globalization and free money flow across national borders has caused an increase in

correlations, and this is illustrated in the higher numbers shown in short-term periods (e.g., last 2 years

or last 4 years) when compared to longer-term periods (e.g. last 10 years or last 15 years).

Correlations among the S&P 500 and all non-US indices decrease when using daily percentage yields

instead of prices, and this is partially caused by differences in time zones. This is also a problem when

calculating actual real-time correlations.

How to estimate future correlations?

Instead of taking the historical value of a correlation as a way to predict future correlations, Marko

Katsanos recommends adjusting the correlation coefficient by the trend or rate of change of the

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 122/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

correlation during the most recent 5-year period. The goal of this adjustment is to take into account the

most recent trend.

2.3.2. Interest rates, commodities, Forex, and the VIX index.

Technical analysts and traders have always used interest rates as a relevant factor in equity markets

evolution. One way to estimate future correlation is just based on taking historical correlations. However, in

terms of interest rates, this method has experienced some empirical problems. During the 20th

century,

interest rates and stock prices experienced negative correlation, and this was illustrated by the old saying

“Don’t fight the Fed”. This maxim suggests buying (selling) stocks when the Fed starts to lower (raise)

interest rates. However, an investor who followed this analysis and bought stocks when the Fed started

lowering interest rates in 2001, and again in August 2007, would have suffered severe losses. Figure 2-14

illustrates the comparison between the S&P 500 index (solid thick line) and the 10 year T-Note yield (solid

thin line) weekly time series, and it also shows the 18-week correlation (bottom chart) between both series. In

this figure we can see how the correlation coefficient changed with the new century, from negative to

positive values (this is illustrated with two ovals, one before 2000, and the other after 2000).

Source: StocksCharts.com Figure 2-14

When searching for factors that affect price correlations, we might look for market corrections, uncertainties

or perceived risks. This is illustrated in Figure 2-14 when the 1987 crash, the 1997 Asian financial crisis, and

the 1999 LTCM financial crisis produced sharp declines in stock prices and subsequent rallies in bonds, as

investors fled to safety. These extreme events (shaded in grey) resulted in negative correlation between

stocks and bonds, that is, positive correlation between stock prices and bond yields. Additionally to

recessions or price shocks, inflation expectations or rising commodity prices also cause correlation reversals

because rising inflation is negative for bonds and therefore positive for yields. This fluctuation of correlations

can also be seen when comparing the S&P 500 index with currencies (JPY) and commodities (CRB Index).

This is illustrated in Figure 2-15 and in Figure 2-16, where the S&P 500 index (solid thick line) is compared

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 123/420 CFA, CMT, CAIA, FRM, EFA, CFTe

to the JPYUSD and to the CRB Index, both in solid thin line. The timeframe is weekly, and the fluctuations

of correlation are represented with a vertical line.

Source: StocksCharts.com Figure 2-15

Source: StocksCharts.com Figure 2-16

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 124/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

2.4. European Indices.

2.4.1. The DAX-30.

Correlation with international indices, especially U.S. equity indices.

Trading DAX futures has now become very popular among US and Australian traders due to the

following three advantages: (1) it is a liquid market, (2) it adds currency diversification, and (3) it offers a

wider range of trading times. The German futures market (Eurex) is open 14 hours a day from 8:00 to

22:00 CET (02:00 – 16:00 US). When analyzing a correlation matrix between DAX and major

international indices, forex, and commodities, the highest values correspond to the Euro Stoxx 50 in first

place, and the CAC 40 index in second place. The DAX and the Euro Stoxx 50 share some stocks so their

correlation is not a big surprise. If we are interested in comparing American indices with the DAX index,

in order to predict the DAX movements, we have two options: (1) we can shift back one day the

American indices because all American exchanges close four and a half hours later than DAX, or (2) we

can correlate the DAX opening price with the previous day’s closing price of the corresponding American

index. Both alternatives can also be applied to other international indices (American, European or Asian

indices).

Correlation with U.S. stocks.

When correlations are applied to individual U.S. stocks, the analysis concludes that the DAX-30 index

shows the highest positive correlation with interest rate sensitive groups, such as Utilities, Financials, and

Building Material stocks.

Correlation with European Futures.

European indices futures trade long after the closing of equity trading in their corresponding exchanges

(cash indices), so a more realistic correlation should be established between the European index future

with the corresponding U.S. future, instead of using the indices. For example, the correlation between the

DAX and the S&P index increased from 0.13 to 0.55, when the future of the S&P 500 was used instead of

the cash index.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 125/420 CFA, CMT, CAIA, FRM, EFA, CFTe

2.4.2. The time factor.

According to the correlations matrix among international indices, the correlation of weekly percentage yields

is stronger than the corresponding daily one; but what about higher timeframes? Markos Katsanos calculates

the Pearson’s correlation coefficient of percentage yields for time intervals ranging from 1 to 100 days

between DAX and S&P e-mini futures and plots the results. The graphical representation shows an

exponential movement for the first 5-day period. Then it makes a short-term peak at the 10-day increment,

decreases slightly, and then increases very slightly to level off at 75 days. Therefore a time increment of five

to ten days, when dealing with percentage differences, might be the optimum to use when creating a

intermarket trading strategy for the short and medium term. Figure 2-17 shows the correlation variation for

time intervals ranging from 1 to 100 days of percent yields between DAX and S&P futures for the 5-year

period from the 1st of July, 2002 to the 30

th of June, 2007.

According to Markos Katsanos, the correlation of intraday percentage changes follows a similar pattern to the

daily yields of Figure 2-17. For example, the correlation between the DAX and the Euro Stoxx 50 improved

exponentially for the first 10-min period, made a short-term peak at the 75-min increment, making only

marginal improvements for the next 200 minutes.

Source: Markos Katsanos Figure 2-17

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 126/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

2.5. Gold.

Gold as a commodity has experienced an incredible bull market from to 2002 to 2012 (Figure 2-18) and one

of the reasons of this exponential movement is that gold is much more accessible for ordinary investors. In

previous decades the minimum amount needed to buy a gold bullion was $1 million. Additionally, buying

gold coins or jewelry were not the solution because of the storing and reselling inconveniences. Although

gold futures can be traded on the New York Commodities Exchange (COMEX), futures are not a popular

security among ordinary investors. The popularity of gold as an investment changed with the arrival of

exchange-traded funds (ETFs). Investors can buy and sell shares of SPDR Gold Trust (ETF), each share

represents one-tenth of an ounce of gold, and the shares are highly liquid.

Generally, Gold has a good performance in times of increasing inflation, a weak dollar or financial

turbulences. However, is it a good long-term investment? As we can see in Figure 2-18 (monthly line chart

from 1980 to 2015 showing Gold in a solid thick line and the S&P 500 in solid thin line), Gold peaked in

1980 and it was in a continuous bear market until 2002, and that is a long-term trend of more than 20 years.

Evidently, if inflation is considered, results are even worse, especially if we compare an investment in gold

with an investment in U.S. equities (S&P-500)

Therefore, investing in stocks is usually a better hedge against inflation over the long term because

companies raise prices when inflation goes up, and growing productivity also helps stock prices keep ahead

of inflation, and this is not the case with gold. Another reason for this limited gold long-term performance is

based on the fundamental law of supply and demand. Commodities that are used in industry should be

continuously replenished, and this is not the case with gold, that stays in the market.

Positive factors affecting the price of gold: expansionary policy, the USD, negative interest rates in the

US, inflation, and high commodity prices.

Negative factors affecting the price of gold: central Bank selling which can affect gold in the short term.

Source: StockCharts.com Figure 2-18

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 127/420 CFA, CMT, CAIA, FRM, EFA, CFTe

2.5.1. Correlations with equities and commodities.

A visual inspection of Figure 2-18 shows that gold and equities are usually uncorrelated, except for relatively

short periods (2003-2008 or 2009-2012). Take note that more than 35 years are illustrated in this figure, so a

5-year period can be considered as relatively short. According to Markos Katsanos, the positive correlation

that started in 2003 was due to external reasons, such as the heavy decline of the dollar, a raising inflation,

and the bull market in the rest of the commodities. So this positive correlation only happened by chance, and

we should expect both markets to be uncorrelated, as it is the case in the last 4 years (2011-2015).

Gold and Silver have always been positively correlated markets, so their prices move in the same direction.

Because they have the same fundamentals, the price of one does not move in a particular direction because

the other market is moving the same way. Although they move in the same direction, short-term market

inefficiencies can be found and exploited between these two metals.

Another important factor explaining the gold behavior is the U.S. dollar. As this commodity is denominated

in the U.S. currency, gold is affected by the Fed monetary policy. As an example, because of the

expansionary monetary policy followed by the Fed in 2004, gold broke out from historical prices to develop a

new 10-year top. It is worth noting that gold, unlike paper money, cannot be printed.

Another example of the close relationship between gold and US dollar is represented when comparing gold

denominated in USD with gold denominated in euros from 2002 to 2005. In this period, the first experienced

a strong uptrend, while the second moved in a sideways range. The gold in US dollars experienced an

uptrend caused by the USD bear market, not because of a real bull market in gold. This is represented in

Figure 2-19. As a little review of the correlation coefficients showed by Markos Katsanos, gold is positively

correlated with the CRB Index ( = 0.63), with silver ( = 0.82), and with crude oil ( = 0.41), and

negatively correlated with the Dollar Index ( = -0.55).

Source: StockCharts.com Figure 2-19

To conclude with this session, do not forget that all commodities are subject to seasonal changes, and gold is

not an exception. Demand for gold is driven principally by the jewellery industry, and this demand is

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 128/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

especially strong from September to December, prior to the Christmas time. This recurrence in ups and

downs repeat regularly except when external factors, such as the weakness of the dollar (Figure 2-19).

2.5.2. Leading or lagging?

In this section Markos Katsanos introduces an interesting discussion about whether gold prices are leading or

lagging other related commodities. A visual inspection of charts is not enough to make a clear conclusion.

Looking at the charts reveals that gold sometimes lead and sometimes lag other correlated commodities. In

order to solve this question, Markos Katsanos shift gold yields one to ten days forward and up (positive

values) to ten days back in time (negative values). This is done to infer which commodities have stronger

leading or lagging correlations with gold, with the final goal of predicting future movements. Keep in mind

that this analysis is only appropriate for the short term (10 days or less).

The Philadelphia Exchange (PHLX) Gold and Silver Sector (XAU) Index.

According to the lag analysis, the XAU is leading gold for both weekly and daily yields. The weekly

yield weighted average of 10-day leading correlations was 0.29, while the lagging correlation was 0.15.

This study showed a strong positive correlation between the XAU and gold for both weekly ( =0.68) and

daily ( =0.62) yields. John Murphy also mentions a long-term lead of gold stocks over gold bullion in

his book Trading with Intermarket Analysis.

The Dollar Index.

There is a weak negative correlation when daily percent differences (yields) were used, while this

negative correlation increased when raw prices were used. It seems evident that, as gold is denominated

in US dollars, it should lag the dollar. However, this initial impression was only confirmed by the first

two days of the lag, and then gold took the lead.

Silver.

This commodity had the second best correlation of weekly and daily yields, the first correlation

corresponds to the XAU. Silver moves more or less coincidentally with gold.

Canada’s Venture Index.

This index had the best coincident correlation based on raw prices ( =0.965). The Venture Index leads

gold prices.

The CRB Index.

This commodity index had the worst positive coincident correlation for both weekly and daily yields, so

no significant lead or lag was detected.

According to this analysis, gold prices either lag or move with other commodities. Therefore, the best way to

trade this relationship is using related markets to forecast gold prices, and not the other way around.

2.5.3. Which timeframe should we use to calculate the percentage changes?

When using raw price data to determine statistical metrics, such as correlations or regression, we encounter

two drawbacks:

Financial market prices do not follow a normal or Gaussian distribution.

Relationships between markets are not linear.

In order to sort it out both problems, we have to calculate price differences or percentage changes, but what is

the optimal timeframe to calculate these percentages? Markos Katsanos calculates the Pearson correlation

coefficient between gold and the Dollar Index, and between gold and the XAU Index making the following

conclusion: The pattern is similar for both assets, and a period of 9 days could be used when designing a

short to medium term intermarket trading strategy.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 129/420 CFA, CMT, CAIA, FRM, EFA, CFTe

2.6. Intraday Correlations.

Up until now we have focused on daily and weekly yields to calculate correlation coefficients. However, if

you are a daytrader or a scalper, these timeframes are too long. In order to detect intraday relationships,

Markos Katsanos calculates correlations among the e-min S&P 500 futures and the DAX, Euro Stoxx 50,

and e-mini Dow futures for a wide range of intraday timeframes (from 5min to 1500-min). The results are

illustrated in Table 2-3 and in Figure 2-20, where we can see how correlations increase exponentially up to a

certain increment (about 75-min) when it suddenly starts to move horizontally.

Timeframe (minutes) Euro Stoxx 50 DAX 30 DJIA

5 0.725 0.724 0.614

10 0.750 0.741 0.655

15 0.767 0.754 0.667

20 0.779 0.763 0.679

25 0.783 0.768 0.683

30 0.788 0.774 0.690

35 0.782 0.78 0.694

40 0.776 0.782 0.696

45 0.780 0.787 0.700

50 0.783 0.789 0.703

55 0.787 0.793 0.706

60 0.785 0.797 0.707

65 0.786 0.802 0.724

70 0.788 0.807 0.737

75 0.788 0.810 0.750

80 0.788 0.812 0.761

85 0.788 0.813 0.771

90 0.787 0.814 0.779

95 0.786 0.815 0.787

100 0.785 0.816 0.794

125 0.785 0.823 0.818

150 0.786 0.830 0.830

200 0.783 0.836 0.851

250 0.780 0.842 0.868

375 0.778 0.850 0.889

500 0.786 0.862 0.902

750 0.812 0.884 0.913

1000 0.830 0.897 0.921

1250 0.831 0.900 0.925

1500 0.842 0.910 0.928

Source: Markos Katsanos. Table 2-3

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 130/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

Source: Markos Katsanos Figure 2-20

These are the equations related to the relationship between DAX-30 and the e-mini S&P-500:

( 2.19 )

( 2.20 )

where

ri = Pearson’s intraday correlation coefficient for time interval i.

rj = Pearson’s intraday correlation coefficient for time interval j.

T = time in minutes

For example, the estimation of the 60-min correlation between DAX-30 and the e-mini S&P-500 futures is

based on the first equation:

Additionally, if we are interested in converting correlations between intraday timeframes, that is, if we know

that the 15-min correlation between DAX-30 and the e-mini S&P-500 futures is 0.754, the corresponding

60-min correlation coefficient is based on the second equation:

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 131/420 CFA, CMT, CAIA, FRM, EFA, CFTe

Which timeframe is optimal?.

According to Table 2-3 and to Figure 2-20, Markos Katsanos infer the following conclusions when

choosing the best time span for calculating percentage yields in a trading strategy or indicator:

Surprisingly, the S&P-500 correlated better with the European futures than with the US index (DJIA),

but only for shorter time segments up to 35minutes of yields.

Correlations between the S&P-500 and the European futures peaked between 30- and 35-min yields

and this is probably the best value to use for short-term predictions.

The e-mini S&P-500 correlated better with the Euro Stoxx 50 for very short yields (up to 35 minutes),

with the DAX-30 for medium (40- to 150-min) yields and with DJIA for longer term (over 150-min).

The correlation coefficient between the e-mini S&P-500 and the Euro Stoxx 50 futures improved only

by 7% for longer than 30-min yields, where the correlation with the DJIA futures improved by more

than 30%. Therefore, it a trader is developing a system based on the correlation between the DJIA and

the S&P, it is better to use longer timeframes.

Leading or lagging?

When dealing with a correlation coefficient analysis, the goal of a predictive model is not just predicting

the future prices according to the contemporaneous correlations, but to determine a predictive model that

shows changes and disparities between forecasted and observed values, in an attempt to be ahead of

potential dangers and opportunities. This can only be achieved applying a leading and lagging

methodology which is simply a list of the correlations between values of a time series displaced at

specific time intervals (lags and leads).

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 132/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

2.7. Intermarket Indicators.

Traditional technical indicators, such as moving averages or the RSI (Relative Strength Index), in order to

determine the future trend (short-, medium, or long-term) are based on a unique market time series. However,

intermarket indicators, as those that will be explained in this chapter, are based on more than one time series,

so they benefit from the power of intermarket relationships.

2.7.1. Relative Strength.

A relative strength indicator is nothing more than a ratio between two securities, or a ratio between a security

and its benchmark. For example the price of gold divided by the CRB Index, the price of Apple divided by

the Nasdaq-100, or the price of the September e-mini S&P future contract divided by the December e-mini

S&P-500 future contract. Relative Strength was popularized by William O’Neil in his classic book How to

Trade Money in Stocks. Markos Katsanos recommends applying a moving average to the relative strength

indicator in order to eliminate the effect of erratic price movements or “noise”. If a stock and its benchmark

are used to determine a relative strength line, we can make the following conclusions:

An up trendline means that the stock is performing better than its benchmark, that is, if both are going up,

the stock is much stronger, while if both are going down, the stock is falling by a smaller percentage.

A down trendline means that the stock is performing worse than its benchmark, that is, if both are going

up, the stock is much weaker, while if both are going down, the stock is falling by a larger percentage.

A trendless line gives us no clue about the relationship between both securities.

In order to determine overbought and oversold levels, Markos Katsanos normalize the relative strength line

from 1 to 100 using the Intermarket Momentum Indicator, which will be explained in a subsequent section in

this chapter. Values over a specific band (e.g. 80) are indicative of an overbought level, while values below

another specific band (e.g., 50) are indicative of an oversold level. Markos Katsanos identifies the following

entry rules: buy when the oscillator crosses its 4-day moving average from below on an oversold market

(<50), and sell when the oscillator crosses its 4-day moving average from above on an overbought market

(>80).

2.7.2. Bollinger Band Divergence Indicator.

This indicator was developed by Markos Katsanos to detect divergences between price and money flow,

although it can also be used to detect divergences between a security and a related market (intermarket

relationship). Let us see how to create this indicator:

First step: Relative position of a security in the Bollinger Bands.

In the first step we determine the relative position of both securities in the Bollinger bands. In this step we

determine variables SEC2BOL’ for the base security, which is the one that you want to predict; and

SEC1BOL’ for the intermarket security. Let us show the calculation for the base security:

( 2.21 )

where

BBB = Bollinger Band Bottom (SMA – 2).

BBT = Bollinger Band Top (SMA + 2).

SEC1BOL’ = Relative position of the base security in the Bollinger bands.

SEC2BOL’ = Relative position of the intermarket security in the Bollinger bands.

SMA = Simple Moving Average.

= Standard deviation.

CMT III. 2016. Topic 2. Asset Relationships.

Alexey De La Loma ©FINANCER TRAINING Pag. 133/420 CFA, CMT, CAIA, FRM, EFA, CFTe

A value of 1 in both SEC1BOL’ and SEC2BOL’ indicates that the security has reached the top band,

while a value of zero indicates that it has reached the bottom band. In order to get rid of negative values

(prices going down below the bottom band), the final value is increased by one:

( 2.22 )

( 2.23 )

Second step: Divergence between a security and its related market..

In the second step we determine the divergence between both securities through a 3-period exponential

moving average (EMA).

( 2.24 )

The indicator value varies from -100 to +100. Values less than zero indicate negative divergence, while

values above zero are indicative of positive divergence. Buy signals are triggered when the indicator reaches

a peak above a predetermined level (usually 10 to 30) and subsequently declines. On the other side, sell

signals are triggered when the indicator reaches a bottom below a predetermined level (usually -10 to -30)

and subsequently rises. According to Markos Katsanos, this indicator has two major drawbacks that are

worth noting:

Because Bollinger bands are based on a standard deviation, it assumes prices follow a Gaussian or normal

distribution.

Because of scaling factors, this indicator does not work properly when markets are negatively correlated.

2.7.3. Intermarket Disparity Indicator.

This indicator was introduced by Steve Nison in his book Beyond Candlestick: New Japanese Charting

Techniques Revealed. Let us see how to create this indicator:

First step: Disparity of the most recent close to a chosen simple moving average for both securities.

In the first step we determine the disparity or difference of the latest close to a chosen moving average for

both securities: the base (1), and the intermarket (2) security.

( 2.25 )

( 2.26 )

where

C1 = Close of the intermarket security.

C2 = Close of the base security, which the one you want to predict.

DS1= Disparity index of security 1.

DS2 = Disparity index of security 2.

SMA = Simple Moving Average.

Second step: Determine the intermarket disparity index.

In the second step, we determine the intermarket disparity index subtracting the disparity index of the

base security from the disparity index of the intermarket security.

( 2.27 )

where

Topic 2. Asset Relationships. CMT III. 2016.

Pag. 134/420 ©FINANCER TRAINING Alexey De La Loma CFA, CMT, CAIA, FRM, EFA, CFTe

c = constant introduced to take into account the sign of the correlation coefficient. It can be +1 if

correlation between securities is positive; and -1 if correlation is negative.