Topic 1 accounting_for_leases

59

BKAF3063 – A141 1 Topic 1 Accounting for Leases (MFRS 117)

-

Upload

kim-rae-ki -

Category

Education

-

view

93 -

download

0

Transcript of Topic 1 accounting_for_leases

BKAF3063 – A1411

Topic 1Accounting for

Leases(MFRS 117)

Chapter Outl ine

BKAF3063 – A1412

Nature and classification of leases.

Accounting by lessee:

operating lease

finance lease

Accounting by lessor:

operating lease

direct financing lease

Sales and leaseback transactions.

Disclosure requirement.

Learning outcomes:

BKAF3063 – A1413

Define what is lease & differentiate between operating & finance lease

Record the leases transactions in the book of lessor and lessee

Define and record sales and leaseback transantions

Definition of Lease

BKAF3063 – A1414

MFRS 117 (Para 4):

An agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of time.

MFRS 117 (Para 4):

An agreement whereby the lessor conveys to the lessee in return for a payment or series of payments the right to use an asset for an agreed period of time.

Advantages of Lease

BKAF3063 – A1415

1) 100% financing at fixed rates – without requiring any down

payment, lease payments often remain fixed.

2) Protection against obsolescence – reduce risk of

obsolescence.

3) Flexibility – less restrictive provision than other debt

agreements.

4) Less costly financing.

5) Off-Balance-Sheet financing – specifically on operating

lease.

� Finance Lease if it transfers

substantially all the risks and rewards incidental to ownership.

DMart

� Operating Lease if it does not transfer

substantially all the risks and rewards incidental to ownership.

Classif ication of Lease

BKAF3063 – A1416

Classif ication of Lease …cont.

BKAF3063 – A1417

Risks include the possibilities of losses from

idle capacity or technological obsolescence and of variations in return due to changing economic

conditions

Rewards may be represented by the expectation of profitable operation over the asset’s economic life and of gain from appreciation in value or realization of a residual value.

Ownership Transfer

BKAF3063 – A1418

Legal form:- Title remains with the lessor for all types of lease.

Accounting view: “Substance over form” A lease that transfers substantially all of the benefits and

risks incidental to the ownership of property should be accounted for as acquisition of an asset and the incurrence of an obligation by the lessee.

“practically how the asset treated/used…” vs. “legally who own the asset…”

Conclusion: The ownership rights differs according to type of the lease.

Classification of Lease: Para 10 - depends on the substance of the transaction rather than the form of the contract.

BKAF3063 – A1419

Operating Lease

NO

NO

NO

NO

NO

YES

YES

YES

YES

YES

Ownership transfers at the end of the lease?

Bargain Purchase Option?

Lease term is for majority of economic life?75% or more

PV of MLP equals at least substantially all of FV of the leased asset? 90% or more

Leased asset(s) specialised?

Finance Lease

Finance Lease

Finance Lease

Finance Lease

Finance Lease

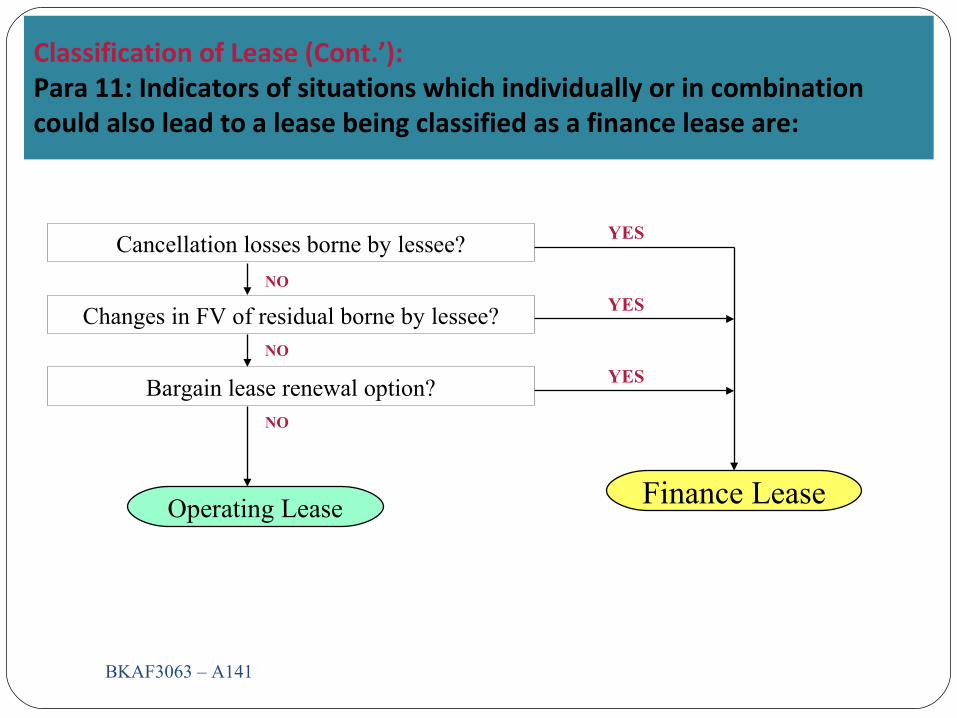

Classification of Lease (Cont.’):Para 11: Indicators of situations which individually or in combination could also lead to a lease being classified as a finance lease are:

BKAF3063 – A14110

Operating Lease Finance Lease

NO

NO

NO

YES

YES

YES

Cancellation losses borne by lessee?

Changes in FV of residual borne by lessee?

Bargain lease renewal option?

Terms

BKAF3063 – A14111

☺ Lease Term - Non-cancellable period for which lessee has contracted to lease. - Commencement of lease term = when recognition takes place.

☺ Inception date - the earlier of the date of the lease agreement and the date of commitment by the parties to the principle provision of the lease. - Inception of the lease = when leases are classified.

☺ Bargain purchase option (BPO) - option to purchase the asset at a price lower than fair value at the date of the option become exercisable.

Terms… (cont)

BKAF3063 – A14112

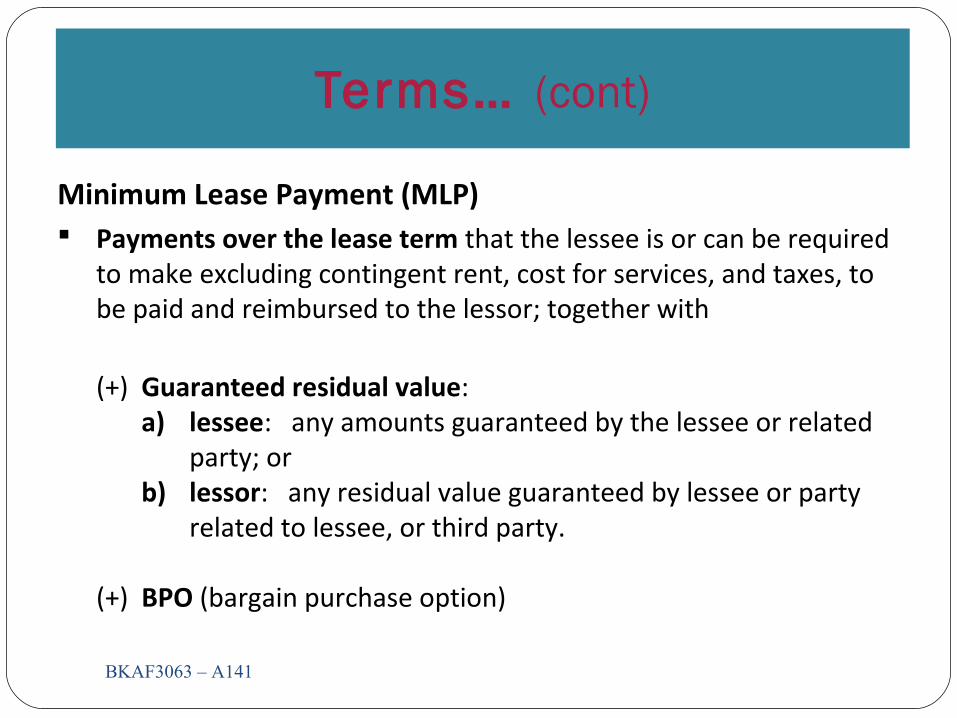

Minimum Lease Payment (MLP) Payments over the lease term that the lessee is or can be required

to make excluding contingent rent, cost for services, and taxes, to be paid and reimbursed to the lessor; together with

(+) Guaranteed residual value:a) lessee: any amounts guaranteed by the lessee or related

party; orb) lessor: any residual value guaranteed by lessee or party

related to lessee, or third party.

(+) BPO (bargain purchase option)

Terms …(cont.)

BKAF3063 – A14113

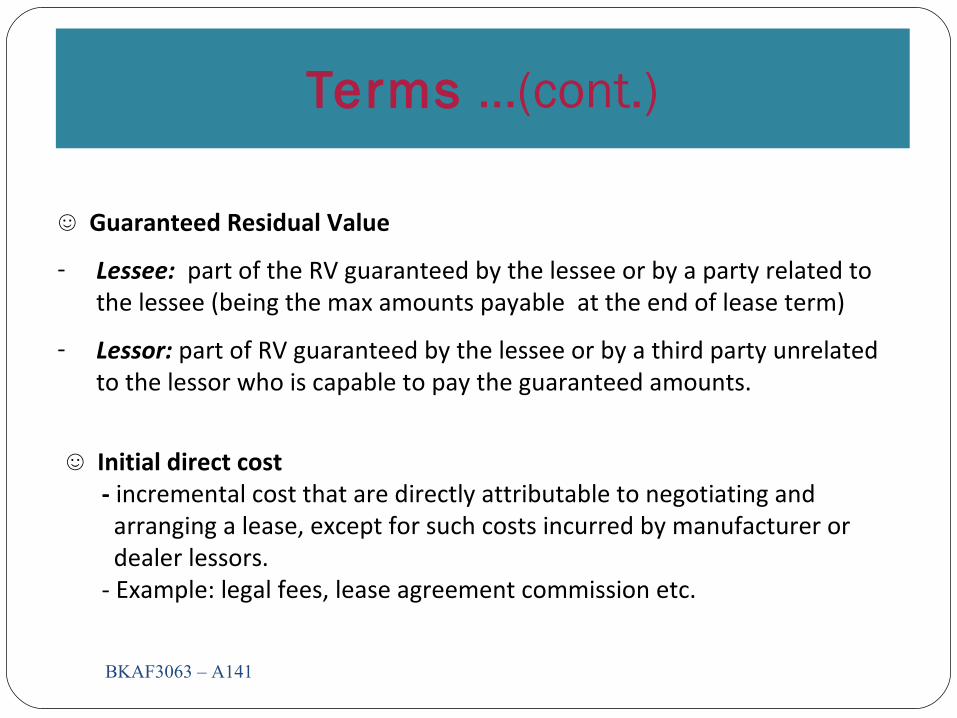

☺ Guaranteed Residual Value

- Lessee: part of the RV guaranteed by the lessee or by a party related to the lessee (being the max amounts payable at the end of lease term)

- Lessor: part of RV guaranteed by the lessee or by a third party unrelated to the lessor who is capable to pay the guaranteed amounts.

☺ Initial direct cost - incremental cost that are directly attributable to negotiating and arranging a lease, except for such costs incurred by manufacturer or dealer lessors. - Example: legal fees, lease agreement commission etc.

Terms …(cont.)

BKAF3063 – A14114

☺ Gross Investment

a) the MLP receivable by the lessor under a finance lease, and

b) any unguaranteed residual value accruing to the lessor.

☺ Net Investment- the gross investment in the lease discounted at the interest rate

implicit in the lease.

Classif ication of Lease…cont.

BKAF3063 – A14115

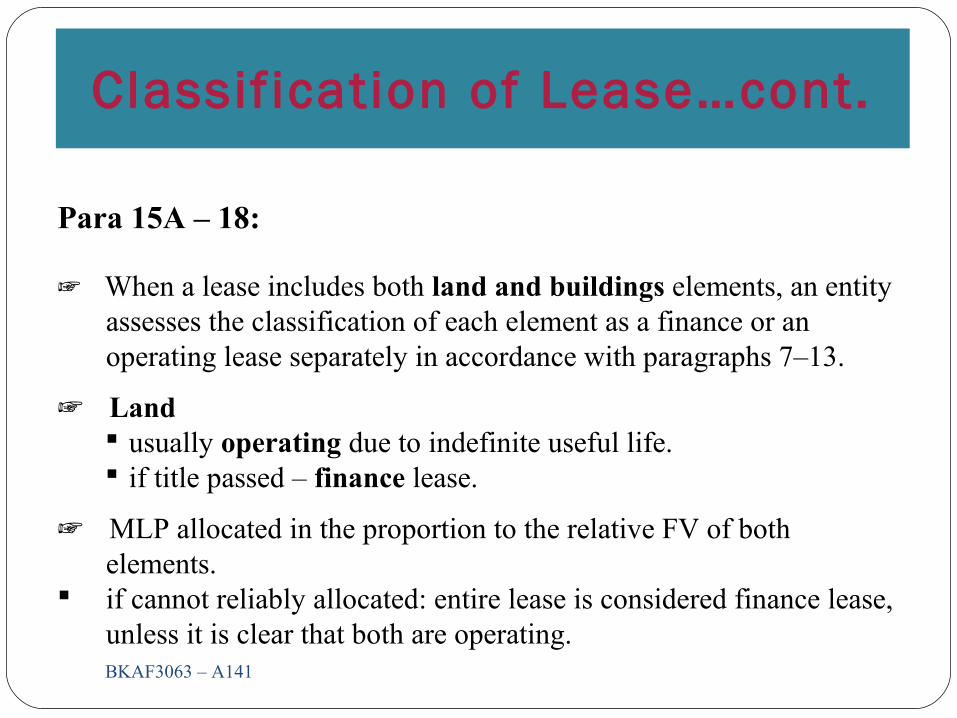

Para 15A – 18:

☞ When a lease includes both land and buildings elements, an entity assesses the classification of each element as a finance or an operating lease separately in accordance with paragraphs 7–13.

☞ Land usually operating due to indefinite useful life. if title passed – finance lease.

☞ MLP allocated in the proportion to the relative FV of both elements.

if cannot reliably allocated: entire lease is considered finance lease, unless it is clear that both are operating.

Classification of LeaseClassification of Lease

BKAF3063 – A14116

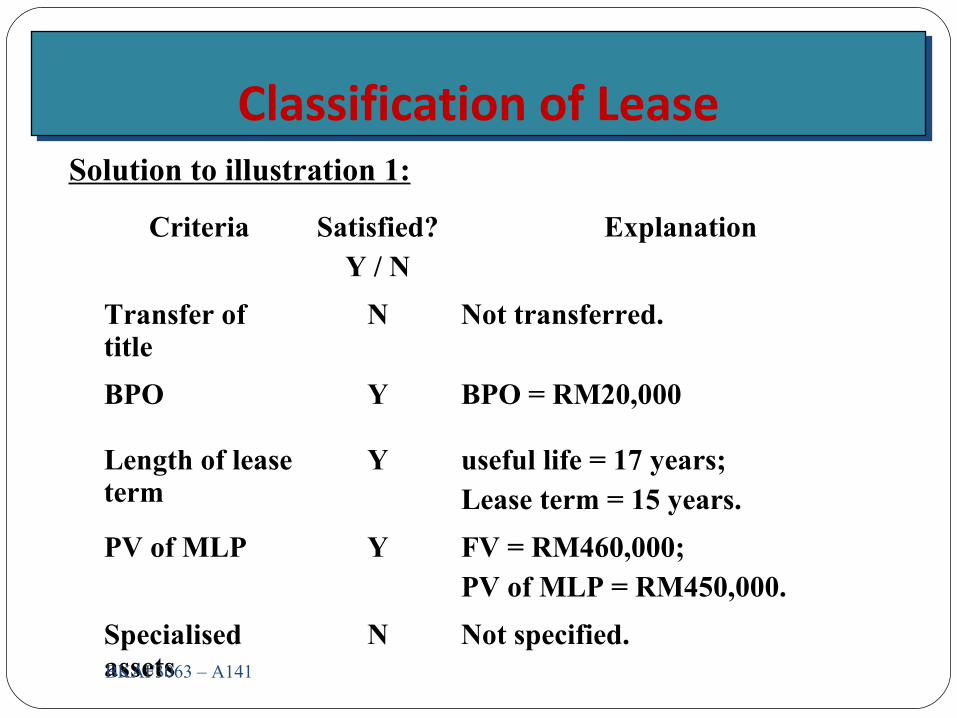

Illustration 1:

Pajakan Co. (Lessor) and Trojan Co. (Lessee) entered into leasing agreement on 1 January 2012. The term of lease is 15 years. The lease agreement is non-cancellable and has minimum lease payments with a present value of RM450,000. The lease involves the use of machinery that has a 17 years estimated useful life and is valued at RM460,000. The lease stated that Trojan has an option to purchase the asset for RM20,000 at the end of leased period.

Classification of LeaseClassification of Lease

Criteria Satisfied? Y / N

Explanation

Transfer of title

N Not transferred.

BPO Y BPO = RM20,000

Length of lease term

Y useful life = 17 years;Lease term = 15 years.

PV of MLP Y FV = RM460,000;PV of MLP = RM450,000.

Specialised assets

N Not specified.BKAF3063 – A14117

Solution to illustration 1:

Finance and operating leases: Differences (Lessee)

Finance Lease Operating Lease

Recognition of PPE and liabilities on the book

Recognition of rental expenses/revenue as incurred/earned

PPE subject to impairment and test

Not applicable

BKAF3063 – A14118

Let’s take a look at Operating Lease in the book of Lessee

BKAF3063 – A14119

Operating Lease:Accounting by Lessee

BKAF3063 – A14120

Para 33 – 34:

☞ Lease payments - should be recognised as an expense in the income statement on a straight-line basis over the lease term.

☞ Lease payments – should exclude costs for services such as insurance and maintenance.

☞ No records on the assets or liability related to the value of the assets (off balance sheet).

Operating Lease:Accounting by Lessee

BKAF3063 – A14121

Illustration 2:

Pajakan Company (lessor) leased an equipment costing RM450,000 to Trojan Company. The economic useful life of the asset is 20 years. The lease is classified as operating lease with the lease term of 5 years starting from 1/1/2011. Payments are made in advance as follows:

1/1/11 RM18,0001/1/12 RM16,0001/1/13 RM14,0001/1/14 RM12,0001/1/15 RM10,000

Asset is used evenly throughout the lease term. The accounting period of both parties ends on 31 December.

Operating Lease :Accounting by Lessee

BKAF3063 – A14122

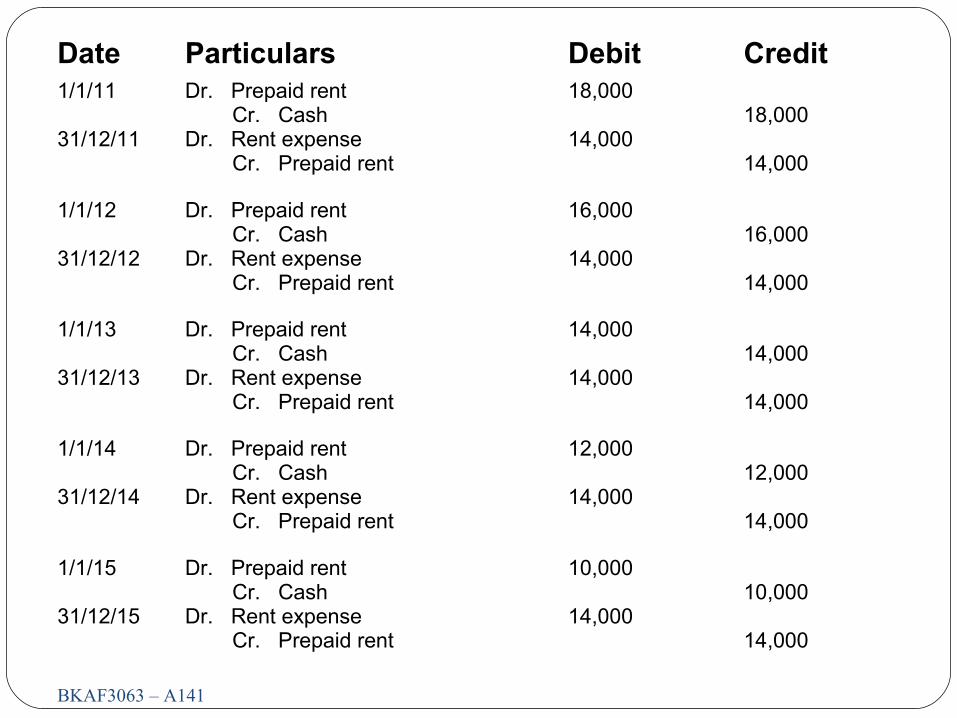

Solution to Illustration 2:

Total payment for the lease period:= RM18,000 +RM16,000 + RM14,000 + RM12,000 + RM10,000)= RM70,000

Expenses recognized per year = RM70,000/5 = RM14,000

Journal entries?

Date Particulars Debit Credit1/1/11

31/12/11

Dr. Prepaid rent Cr. CashDr. Rent expense Cr. Prepaid rent

18,000

14,00018,000

14,000

1/1/12

31/12/12

Dr. Prepaid rent Cr. CashDr. Rent expense Cr. Prepaid rent

16,000

14,00016,000

14,000

1/1/13

31/12/13

Dr. Prepaid rent Cr. CashDr. Rent expense Cr. Prepaid rent

14,000

14,00014,000

14,000

1/1/14

31/12/14

Dr. Prepaid rent Cr. CashDr. Rent expense Cr. Prepaid rent

12,000

14,00012,000

14,000

1/1/15

31/12/15

Dr. Prepaid rent Cr. CashDr. Rent expense Cr. Prepaid rent

10,000

14,00010,000

14,000

BKAF3063 – A14123

Let’s take a look at Operating Lease

in the book of Lessor

BKAF3063 – A14124

Operating Lease:Accounting by Lessor

BKAF3063 – A14125

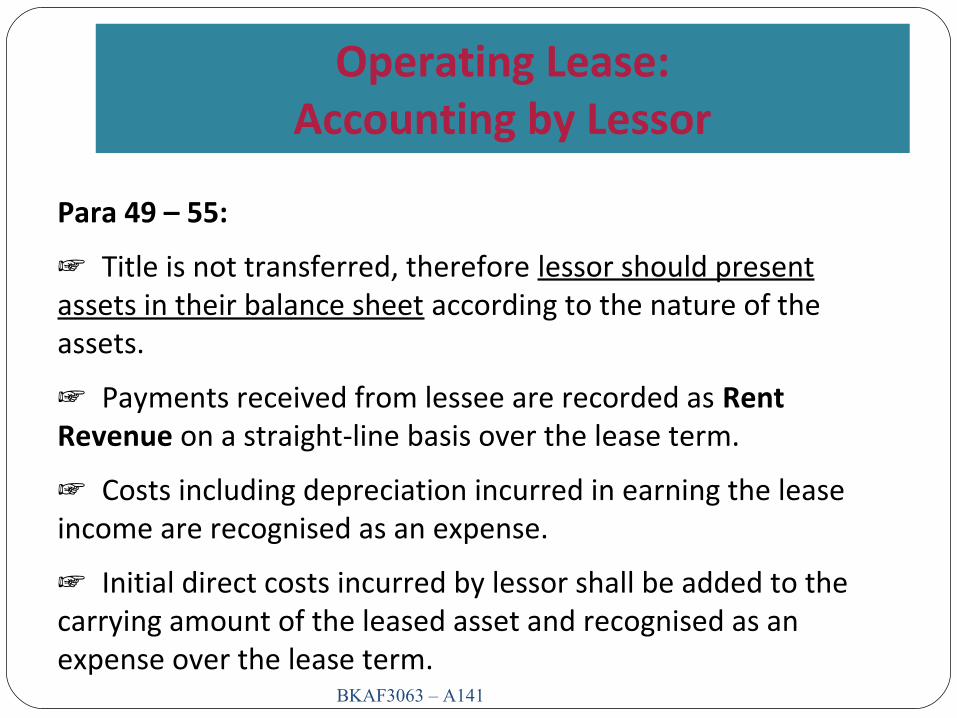

Para 49 – 55:

☞ Title is not transferred, therefore lessor should present assets in their balance sheet according to the nature of the assets.

☞ Payments received from lessee are recorded as Rent Revenue on a straight-line basis over the lease term.

☞ Costs including depreciation incurred in earning the lease income are recognised as an expense.

☞ Initial direct costs incurred by lessor shall be added to the carrying amount of the leased asset and recognised as an expense over the lease term.

Operating Lease:Accounting by Lessor

Operating Lease:Accounting by Lessor

BKAF3063 – A14126

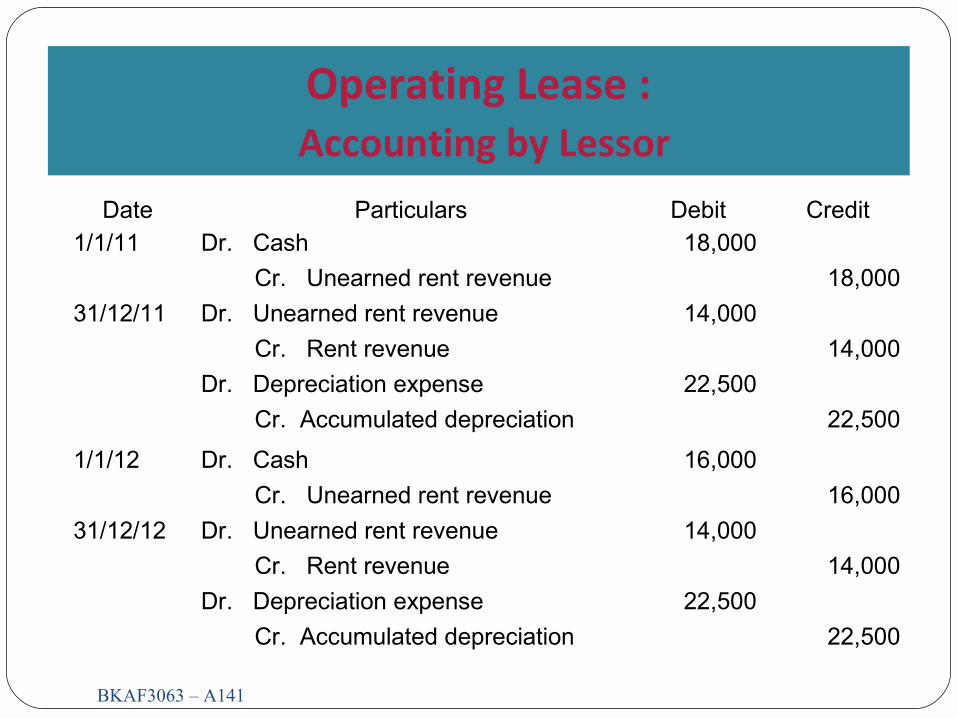

Refer to Illustration 2:

Total payment for the lease period:= RM18,000 +RM16,000 + RM14,000 + RM12,000 + RM10,000= RM70,000

Expenses recognized per year = RM70,000/5 = RM14,000

Depreciation expense recognized per year = RM450,000/20= RM22,500

Journal entries?

Operating Lease : Accounting by Lessor

Date Particulars Debit Credit1/1/11

31/12/11

Dr. Cash

Cr. Unearned rent revenue

Dr. Unearned rent revenue

Cr. Rent revenue

Dr. Depreciation expense

Cr. Accumulated depreciation

18,000

14,000

22,500

18,000

14,000

22,500

1/1/12

31/12/12

Dr. Cash

Cr. Unearned rent revenue

Dr. Unearned rent revenue

Cr. Rent revenue

Dr. Depreciation expense

Cr. Accumulated depreciation

16,000

14,000

22,500

16,000

14,000

22,500

BKAF3063 – A14127

Let’s take a look at Finance Lease in

the book of Lessee

BKAF3063 – A14128

Finance Lease : Accounting by Lessee

BKAF3063 – A14129

Para 20 – 30:

☞ Should be recognized as assets and liabilities (as if the assets being purchased) at amounts equal to the fair value of leased asset or if lower, at the PV of MLP [Para 20].

☞ Cost of assets recorded in lessee’s book:

The lower of:Fair value at inception date.

PV of MLP at inception date.

ORReason: the leasedasset should not berecorded for more thanits fair value.

Finance Lease : Accounting by Lessee

Finance Lease : Accounting by Lessee

BKAF3063 – A14130

Dr. Leased asset xxx *Cr. Lease Liability xxx *

☞ The discount rate (to be used in calculating PV of MLP): implicit in the lease. IF impracticable to determine, use lessee’s incremental

borrowing rate.

☞ MFRS 117 requires the lessee to record the obligation arising from finance lease at then same amount as the leased asset ( para 22)

☞ Journal entries :

* The lower of fair value or PV of MLP

Finance Lease : Accounting by Lessee

Finance Lease : Accounting by Lessee

BKAF3063 – A14131

☞ Interest: MLP − Lease Liabilities/FV of asset :

► Lease payment should be apportioned between the finance charge and the reduction of the outstanding liability.

► Finance charge – allocated to periods during the lease term so as to produce a constant periodic rate of interest on the remaining balance of the liability for each period [ Para 27].

☞ Contingent rents: charged as expense as incurred.

Finance Lease : Accounting by Lessee

Finance Lease : Accounting by Lessee

BKAF3063 – A14132

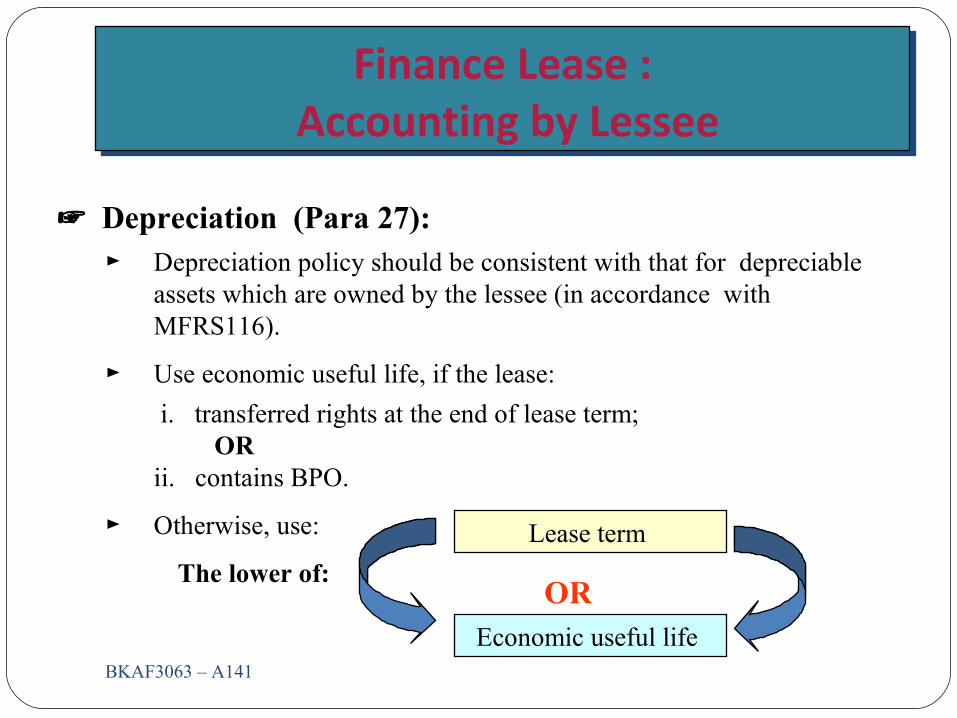

☞ Depreciation (Para 27):► Depreciation policy should be consistent with that for depreciable

assets which are owned by the lessee (in accordance with MFRS116).

► Use economic useful life, if the lease:

i. transferred rights at the end of lease term; OR

ii. contains BPO.

► Otherwise, use:

The lower of:

Lease term

Economic useful life

OR

Finance Lease : Accounting by Lessee

Finance Lease : Accounting by Lessee

BKAF3063 – A14133

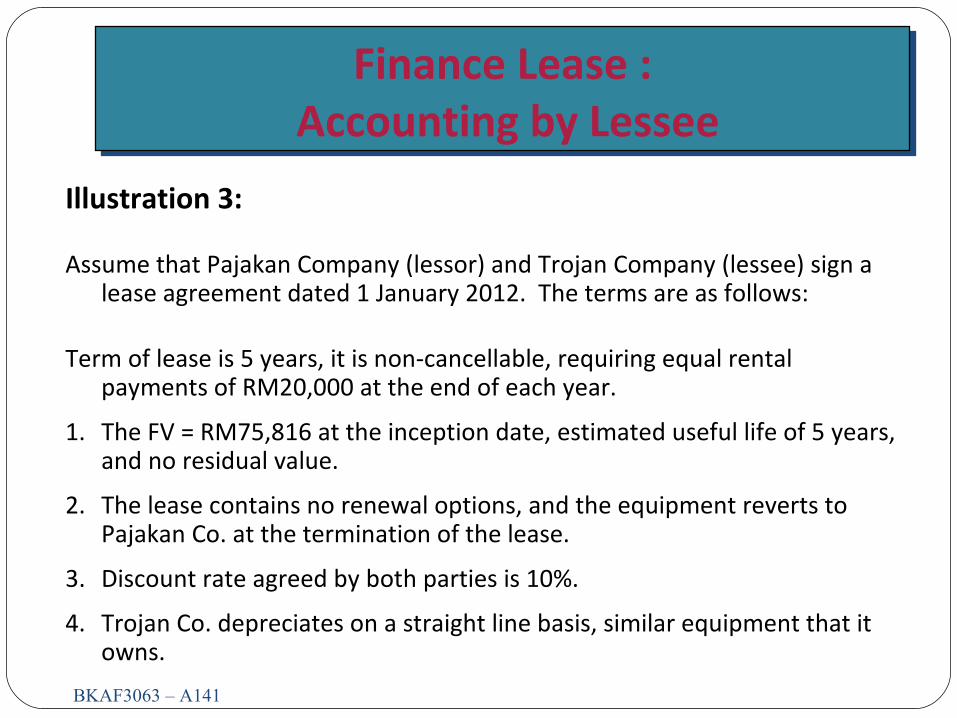

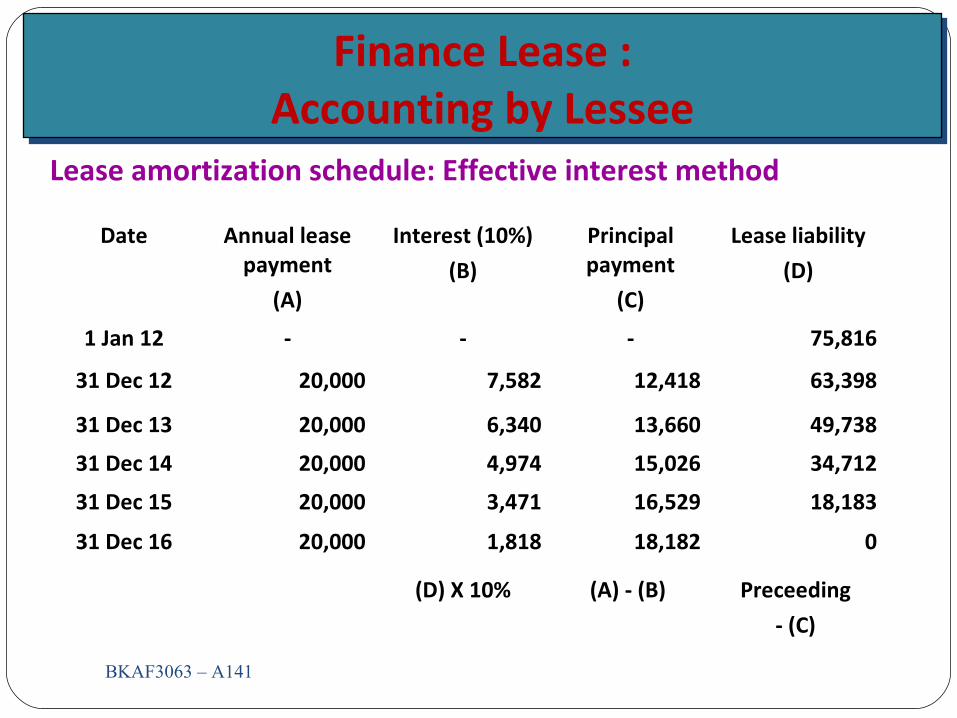

Illustration 3:

Assume that Pajakan Company (lessor) and Trojan Company (lessee) sign a lease agreement dated 1 January 2012. The terms are as follows:

Term of lease is 5 years, it is non-cancellable, requiring equal rental payments of RM20,000 at the end of each year.

1. The FV = RM75,816 at the inception date, estimated useful life of 5 years, and no residual value.

2. The lease contains no renewal options, and the equipment reverts to Pajakan Co. at the termination of the lease.

3. Discount rate agreed by both parties is 10%.

4. Trojan Co. depreciates on a straight line basis, similar equipment that it owns.

Finance Lease :Accounting by Lessee

Finance Lease :Accounting by Lessee

BKAF3063 – A14134

Solution to Illustration 3:

Type of lease: Finance lease

MLP = 20,000 x 5 years = RM100,000

PV of MLP = 20,000 x PVOA(5, 10%)²= 20,000 x 3.7908= 75,816 FV = 75,816.

Journal entry on 1 Jan 2012

Dr. Leased asset 75,816 Cr. Lease Liability 75,816(to recognise the asset leased)

Finance Lease :Accounting by Lessee

Finance Lease :Accounting by Lessee

Date Annual lease payment

(A)

Interest (10%)

(B)

Principal payment

(C)

Lease liability

(D)

1 Jan 12 - - - 75,816

31 Dec 12 20,000 7,582 12,418 63,398

31 Dec 13 20,000 6,340 13,660 49,738

31 Dec 14 20,000 4,974 15,026 34,712

31 Dec 15 20,000 3,471 16,529 18,183

31 Dec 16 20,000 1,818 18,182 0

(D) X 10% (A) - (B) Preceeding

- (C)

BKAF3063 – A14135

Lease amortization schedule: Effective interest method

Finance Lease :Accounting by Lessee

Date Particulars Debit Credit31/12/12 Dr. Lease liability

Interest expense Cr. Cash

Dr. Depreciation expense Cr. Accumulated depreciation

12,4187,582

15,163

20,000

15,16331/12/13 Dr. Lease liability

Interest expense Cr. Cash

Dr. Depreciation expense Cr. Accumulated depreciation

13,6606,340

15,163

20,000

15,163

BKAF3063 – A14136

Journal entries:

Finance Lease :Accounting by Lessee

Date Particulars Debit Credit31/12/14 Dr. Lease liability

Interest expense Cr. Cash

Dr. Depreciation expense Cr. Accumulated depreciation

15,0264,974

15,163

20,000

15,16331/12/15 Dr. Lease liability

Interest expense Cr. Cash

Dr. Depreciation expense Cr. Accumulated depreciation

16,5293,471

15,163

20,000

15,163

BKAF3063 – A14137

Journal entries:

Finance Lease :Accounting by Lessee

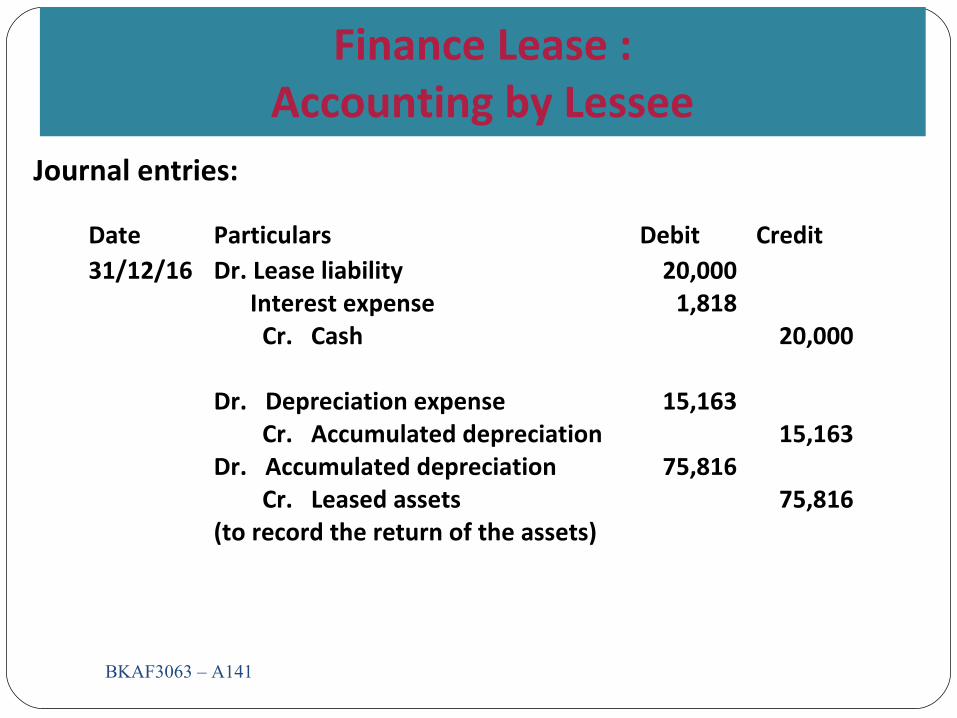

Date Particulars Debit Credit31/12/16 Dr. Lease liability

Interest expense Cr. Cash

Dr. Depreciation expense Cr. Accumulated depreciation

20,0001,818

15,163

20,000

15,163Dr. Accumulated depreciation Cr. Leased assets(to record the return of the assets)

75,81675,816

BKAF3063 – A14138

Journal entries:

Let’s take a look at Finance

Lease in the book of Lessor

BKAF3063 – A14139

Finance Lease : Accounting by Lessor

BKAF3063 – A14140

Para 36 – 40:

☞ The receivable to be presented in the Balance Sheet at an amount equal to the net investment in the lease [Para 36], which is defined in para 4 as “the gross investment in the lease less unearned finance income”

☞ Initial direct cost – included in the initial measurement of finance lease receivable and reduce the amount of income recognised over the lease term [para 38].

Finance Lease :Accounting by Lessor

Finance Lease :Accounting by Lessor

BKAF3063 – A14141

Refer to Illustration 3:

Gross investment = 20,000 x 5 years = RM100,000

Net investment = PV of gross investment = 20,000 x PVOA(5, 10%) = 20,000 x 3.7908 = 75,816

Unearned finance income = 100,000 – 75,816 = 24,184

Amortization schedule?

Journal entries?

Finance Lease :Accounting by Lessor

Date Particulars Debit Credit

01/01/05 Dr. Lease receivable Cr. Fixed assets Unearned interest revenue

100,00075,81624,184

31/12/05 Dr. Cash Cr. Lease receivable

Dr. Unearned interest revenue Cr. Interest revenue

20,000

7,582

20,000

7,58231/12/06 Dr. Cash

Cr. Lease receivable

Dr. Unearned interest revenue Cr. Interest revenue

20,000

6,340

20,000

6,340BKAF3063 – A14142

Journal entries:

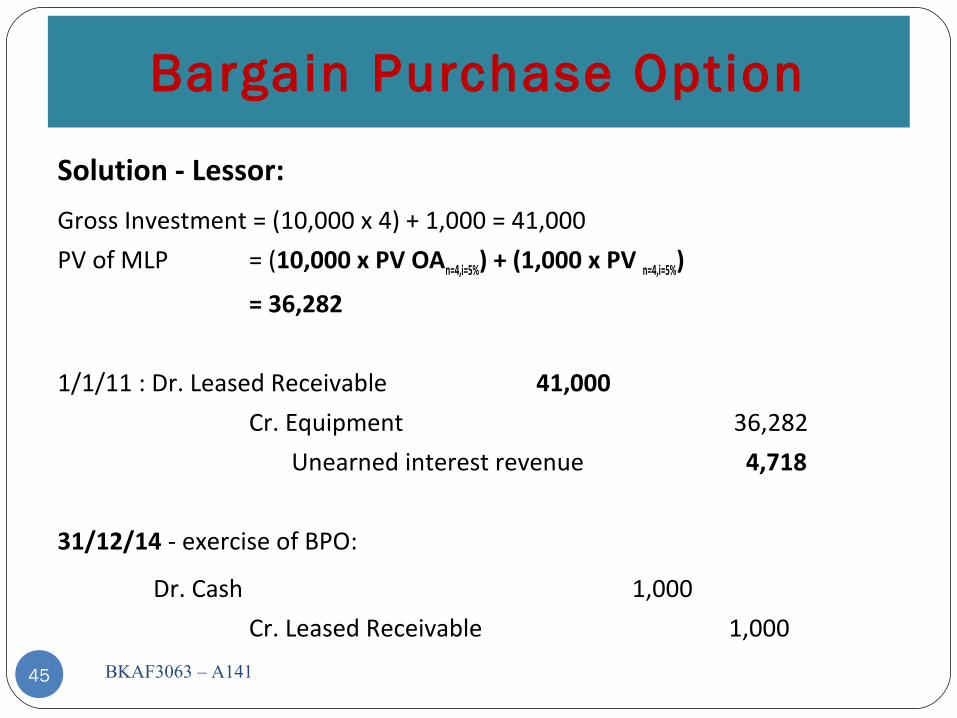

Bargain Purchase Option

MLP will be increased by the exercise price

Useful life will be used as basis for depreciation charge.

Example:

On 1/1/2011, ABC Bhd entered into lease agreement with terms:a) non-cancellable lease term of four years,b) Lease rental of RM10,000 per year to be paid on 31 Dec,

commencing 31/12/2011.c) ABC Bhd has an option to buy the equipment at the end of lease term

for RM1,000. On 1/1/2011, it was estimated tha the fair value of the equipment would be RM5,000 after 4 years’ usage.

The FV of the equipment on 1/1/2011 was RM42,000 and have estimated useful life of 5 years. The implicit rate was 5%.43 BKAF3063 – A141

Bargain Purchase Option

Solution - Lesse:MLP = (10,000 x 4) + 1,000 = 41,000

PV of MLP = (10,000 x PVAn=4,i=5%) + (1,000 x PV n=4,i=5%) = 36,282

1/1/11 : Dr. Leased Equipment 36,282Cr. Lease Payable 36,282

Depreciation exp = 36,282 / 5 = RM7,256.40

31/12/14 - exercise of BPO:Dr. Lease Payable 1,000

Cr. Cash 1,000

44 BKAF3063 – A141

Bargain Purchase Option

Solution - Lessor:

Gross Investment = (10,000 x 4) + 1,000 = 41,000

PV of MLP = (10,000 x PV OAn=4,i=5%) + (1,000 x PV n=4,i=5%)

= 36,282

1/1/11 : Dr. Leased Receivable 41,000

Cr. Equipment 36,282

Unearned interest revenue 4,718

31/12/14 - exercise of BPO:

Dr. Cash 1,000

Cr. Leased Receivable 1,000

45 BKAF3063 – A141

Guaranteed Residual Value

MLP will be increased by GRVGRV will be deducted from the depreciable amount

of leased asset.At the end of lease term,

the lease liability will have a balance equal with GRV If FV of leased asset < GRV , recognise loss (lessee)

46 BKAF3063 – A141

Guaranteed Residual Value

Example:On 1/1/2011, ABC Bhd entered into lease agreement with terms:

a) non-cancellable lease term of four years,

b) Lease rental of RM10,000 per year to be paid on 31 Dec, commencing 31/12/2011.

c) ABC Bhd guaranteed to lessor that the leased asset would have a residual value of RM5,000 at the end of lease term.

The FV of the equipment on 1/1/2011 was RM42,000 and have estimated useful life of 5 years. The implicit rate was 5%. The estimated residual value at the end of lease term was RM7,000.

47 BKAF3063 – A141

Guaranteed Residual Value

Solution – Lessee:MLP = (10,000 x 4) + 5,000 = 45,000PV of MLP = (10,000 x PV OAn=4,i=5%) + (5,000 x PV n=4,i=5%)

= 39,572

1/1/11 : Dr. Leased Equipment 39,572Cr. Lease Payable 39,572

Depreciation exp = (39,572- 5,000) / 4 = RM8,643

31/12/14, if FV of leased asset is RM3,000,

Dr. Lease Payable 5,000 Accumulated depreciation 34,572

Cr. Leased Equipment 39,572

Dr. Loss on finance lease 2,000Cr. Cash 2,00048 BKAF3063 – A141

Guaranteed Residual Value

Solution – Lessor:

GI = (10,000 x 4) + 7,000 = 47,000PV of GI = (10,000 x PVOA n=4,i=5%) + (7,000 x PV n=4,i=5%)

= 41,218

1/1/11 : Dr. Leased Receivable 47,000 Cr. Equipment 41,218

Unearned interest revenue 5,782

31/12/14, if FV of leased asset is RM3,000,

Dr. Equipment 3,000 Cash 2,000 Loss on finance lease 2,000

Cr. Leased Receivable 7,000

49 BKAF3063 – A141

Sales and LeasebackSales and Leaseback

BKAF3063 – A14150

☞ Transaction in which the owner of the asset (seller, lessee) sells the asset to another and simultaneously leases it back from the new owner.

?In the book of Buyer/lessor:- Same as lessor as discuss before.

In the book of seller/lessee:-To recognize gain from sales of asset: immediate or defer.

Sales and LeasebackSales and Leaseback

BKAF3063 – A14151

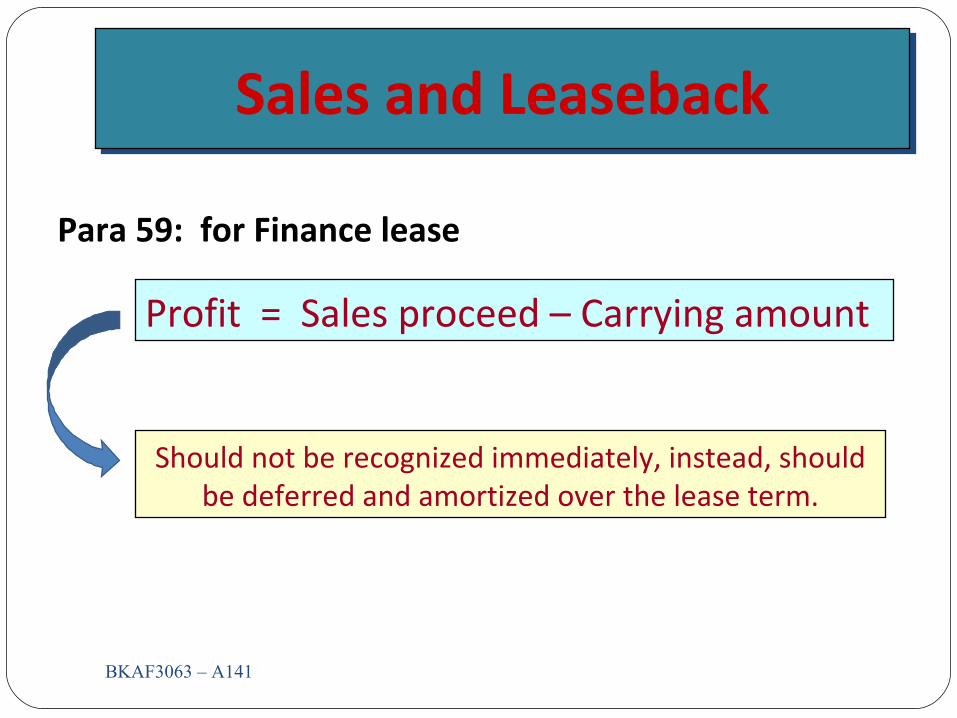

Para 59: for Finance lease

Should not be recognized immediately, instead, should be deferred and amortized over the lease term.

Profit = Sales proceed – Carrying amount

Sales and LeasebackSales and Leaseback

BKAF3063 – A14152

Para 61: for Operating lease.

Should be recognized immediately.

Profit = Sales proceed – Carrying amount

(a) If Selling price = FV

Sales and LeasebackSales and Leaseback

BKAF3063 – A14153

Para 61: for Operating lease

Should be recognized immediately EXCEPT THAT if the loss is compensated by future lease payments at below

market price, it should be deferred and amortized.

Profit = Sales proceed – Carrying amount

(b) If Selling price < FV

Sales and LeasebackSales and Leaseback

BKAF3063 – A14154

Para 61: for Operating lease

deferred and amortized.

Profit = Sales proceed – FV

(c) If Selling price > FV (FV > carrying amount)

recognized immediately.

Profit = FV - Carrying amount

Profit = Sales proceed – Carrying amount

Sales and LeasebackSales and Leaseback

BKAF3063 – A14155

Illustration 5:Chocolate Company sold an equipment to Chips Company and

lease back the asset. The carrying amount (book value) of the asset is RM60,000. The asset has a fair value of RM70,000.

How to recognize profit/loss if the selling price:

1. RM70,0002. RM55,0003. RM50,000 (with lower lease payment)4. RM90,000

Sales and LeasebackSales and Leaseback

BKAF3063 – A14156

Solution to Illustration 11:

1. SP = FV (SP > CA) =

Profit = 70,000 - 60,000 = 10,000

2. SP < FV (SP < CA)

Loss = 55,000 – 60,000 = 5,000 loss

3. SP < FV (SP < CA with lower lease payment)

Loss = 50,000 – 60,000 = 10,000 loss

recognize immediately

recognize immediately

defer & amortize

Sales and LeasebackSales and Leaseback

BKAF3063 – A14157

Solution to Illustration 11:

4. SP > FV =

Profit = 90,000 – 60,000 = 30,000

FV – CA= 70,000 – 60,000= 10,000 recognize immediately

SP – FV= 90,000 – 70,000= 20,000 defer & amortize

Disclosure RequirementsDisclosure Requirements

BKAF3063 – A14158

For Lessee:Para 31: Finance lease. Para 35: Operating lease.

For Lessor:Para 47: Finance lease. Para 56: Operating lease.

End of Topic 1

References:

MFRS 117 Lease

Ng Eng Juan 2012

Lazar & Huang 2012

Zaimah et al. 2009

BKAF3063 – A14159

![Topic 1 ee201[1]](https://static.fdocuments.net/doc/165x107/588103d01a28ab22368b49d1/topic-1-ee2011.jpg)