Today’s Uncertain Economy: Implications for Public Entities and P/C Insurance

65

Today’s Uncertain Economy: Implications for Public Entities and P/C Insurance April 10, 2013 Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information Institute 110 William Street New York, NY 10038

-

Upload

avalbane-dargan -

Category

Documents

-

view

29 -

download

0

description

Today’s Uncertain Economy: Implications for Public Entities and P/C Insurance. April 10, 2013. Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief Economist Insurance Information Institute 110 William Street New York, NY 10038 - PowerPoint PPT Presentation

Transcript of Today’s Uncertain Economy: Implications for Public Entities and P/C Insurance

Today’s Uncertain Economy: Implications for Public Entities

and P/C InsuranceApril 10, 2013

Steven N. Weisbart, Ph.D., CLU, Senior Vice President & Chief EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: 212.346.5540 Cell: 917.494.5945 [email protected] www.iii.org

The Strength of the Economy Will Influence P/C Insurer

Growth Opportunities

2

Growth Will Expandthe Insurer Exposure Base

Across Most Lines

2

3

A Continued Weak Recovery is Forecast:Real GDP Growth, Yearly, 1970-2014F

Forecasts from Blue Chip Economic Indicators, 3/2013 issue, median of range of 52 forecasts.Sources: (GDP) U.S. Department of Commerce at http://www.bea.gov/national/xls/gdpchg.xls.

-4.5%

-3.0%

-1.5%

0.0%

1.5%

3.0%

4.5%

6.0%

7.5%

Real GDP Growth (%)

The median forecast is for several more years of real yearly GDP growth under 3% -- weaker than after most recent recessions

In recoveries, real yearly GDP growth is often 4% or more

4

March 2013 Forecasts of Quarterly US Real GDP for 2013-14

2.0% 2.1% 2.2%

2.8% 2.9% 3.0%

3.6% 3.7% 3.7%

1.7%1.6% 1.7%

1.1%

2.6%

2.0%2.5%

2.7%

3.4%3.6%3.5%

2.9%

0%

1%

2%

3%

4%

13:Q2 13:Q3 13:Q4 14:Q1 14:Q2 14:Q3 14:Q4

10 Most Pessimistic

Median

10 Most Optimistic

Sources: Blue Chip Economic Indicators (3/13); Insurance Information Institute

Real GDP Growth Rate

Despite the sequester and other challenges to the U.S. economy,virtually every forecast in the Blue Chip universe in early March sees

improvement ahead

If it lasts, the sequester will have greatest effect here

State-by-State Leading Indicatorsthrough 2013:Q2

Sources: Federal Reserve Bank of Philadelphia at www.philadelphiafed.org/index.cfm; Insurance Information Institute.Next release is April 4, 2013 5

Near-term growth forecasts vary

widely by state. Strongest growth

= dark green; weakest = beige

6

State & Local Government Contribution to Change* in Real US GDP, Quarterly, 2009-2012

*seasonally adjusted at annual ratesSources: (GDP) U.S. Department of Commerce at http://www.bea.gov/national/xls/gdpchg.xls.; I.I.I.

-0.75%

-0.50%

-0.25%

0.00%

0.25%

0.50%

0.75%

1.00%

Real GDP Growth (%) The drag on the

economy from state & local governments is

diminishing.

Cutbacks by state and local governments have hampered the economy’s recovery from

the recession

8

Y-o-Y Percentage Change in the Value of Public Construction Put in Place, by Segment, Feb. 2013*

2.4%

-1.7% -2.9%-9.9%-10.4% -12.5%-12.9%

-22.2%

-12.3%

-3.8%

-13.8%

20.5%16.3%

2.9%

-30%

-20%

-10%

0%

10%

20%

30%

To

tal P

ub

licC

on

stru

ctio

n

Res

iden

tial

Po

wer

Tra

nsp

ort

atio

n

Co

nse

rvat

ion

& D

evel

op

.

Hig

hw

ay &

Str

eet

Wat

er S

up

ply

Hea

lth C

are

Ed

uca

tion

al

Am

use

men

t &R

ec.

Pu

blic

Saf

ety

Co

mm

erci

al

Sew

age

&W

aste

Dis

po

sal

Off

ice

With strained state and local government budgets, public construction activity declined in many segments; will the sequester crimp 2013?

Growth (%)

*seasonally adjusted; data published April 1, 2013Source: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

Transportation and Power projects lead public sector

construction

9

Labor Market Trends

Steady Job Gains in the Private SectorOffset Steady Job Losses in the

Public Sector

9

10

Unemployment and Underemployment Rates: Stubbornly High in 2012, But Falling

3.5

5.0

6.5

8.0

9.5

11.0

12.5

14.0

15.5

17.0

18.5

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Jan11

Jan12

Jan13

"Headline" Unemployment Rate U-3

Unemployment + Underemployment Rate U-6

Unemployment “Headline”

unemployment stood at 7.6% in

Mar. 2013.

The Federal Reserve’s target for ending “easy money” is 6.5%

(assuming inflation remains

within its 2% target).

Source: US Bureau of Labor Statistics; Insurance Information Institute.

U-6 went from 8.0% in March

2007 to 17.5% in October 2009; Stood at 13.8%

in Mar. 2013

January 2000 through Mar. 2013, Seasonally Adjusted (%)

Stubbornly high unemployment and underemployment constrain overall economic growth, but the job market is now clearly improving.

10

Nov. 12

11

State Government EmploymentMonthly, 1990–2013*

*As of February 2013 (Jan 2013 and Feb 2013 are preliminary); Seasonally adjustedNote: Recessions indicated by gray shaded columns.Sources: US Bureau of Labor Statistics; National Bureau of Economic Research (recession dates); Insurance Information Institutes.

Millions

4.00

4.25

4.50

4.75

5.00

5.25

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Latest was 5.02 million, down 3.7% from peak (Aug 2008)

State government employment rises in recessions, shrinks

after them(for a while)

State government employment rises in recessions, shrinks

after them (for a while)

State government employment

rises in recessions,

shrinks after them (for a while)

12

Local Government EmploymentMonthly, 1990–2013*

*As of February 2013 (Jan 2013 and Feb 2013 are preliminary); Seasonally adjustedNote: Recessions indicated by gray shaded columns.Sources: US Bureau of Labor Statistics; National Bureau of Economic Research (recession dates); Insurance Information Institutes.

Millions

10.0

10.5

11.0

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Latest was 14.03 million,

down 3.9% from peak (Jun 2009)

Recession proof? Local government employment

rose through this and the prior recession

First significant drop in local government employment in over

three decades(-4.2% in 1980-82)

13

Unemployment Rates Vary Widelyby State and Region*

9.6%

9.4%

8.6%

8.6%

7.9%

7.8%

7.7%

7.3%

7.2%

7.2%

6.0%

5.6%

9.3%

8.4%

8.1%

7.2%

6.6%

9.4%

8.0%

7.3%

6.5%

5.8%

4.4%

6.5%

5.2%

0%

3%

6%

9%

12%

MS

NC

SC

GA KY

TN FL WV AR AL

LA VA NJ

NY

PA DE

MD RI

CT

ME

MA

NH VT

AK HI

Une

mpl

oym

ent R

ate

(%)

*Provisional figures for February 2013, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

Southeast Mid-Atlantic New England

14

Unemployment Rates Vary Widelyby State and Region* (cont’d)

9.6%

9.5%

5.0%

4.4%

3.8%

3.3%

7.5%

8.4%

9.6%

7.2%

7.0%

5.5%

8.7%

5.5%

6.7%

8.8%

6.2%

4.9%5.2%5.

6%

7.2%

6.8%

6.4%

5.0%

7.9%

0%

3%

6%

9%

12%

AZ

NM TX OK

CO ID MT

UT

WY

CA

NV

OR

WA IL MI

IN WI

OH

MO

MN

KS IA SD NE

ND

Une

mpl

oym

ent R

ate

(%)

*Provisional figures for February 2013, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute

Southwest MountainFar West

Great PlainsGreat Lakes

The Aging Workforce

19

Number of Workers Age 65-69, 70-74,and 75+, Quarterly, 1998-2012

2327

2312 2404

2406

2393 2530

2498 2559 2627

25702632

2627

2562 2674 2859

2896

2723 2842

28723127

2951 3079

3047 3218

3201 3330

3344

3351

33643396

3334 342634803505

35063547 3764

3775

3626 3833 4074

4138

41054213

1027

1022

10261069

1037 1129

1094

1090

1115

1139

11421181

1215

1160

1182

1177

1135

1162

1138

1141

1177

1182

1183

1213

11931244

1250

1314 1375

126213141356

1385

1397

1385

1367

1370 1452

1442

1407

1389 1530

1524

14301495 15801633

15051550

1498 1598

1564

1584 16821726

171917791835

1842

624

636

641686

668718773

758

789

780

775

801

779

792

762815

790

774

802

765 863926

811 919

928

947

969

1039

9741055

1018 1076

1057

1085

1085

1072 1171

1152

1133

11511210

1224

1258

1256

11431190

1206

1198

1166 1279

1243

1185 1267

1280

1302

1311

1301

12841381

2473

20432067

20432083

20192051

2014 2106 22182251

22422283

223422652304

1250

986

500

1000

1500

2000

2500

3000

3500

4000

4500

1998.1

1998.3

1999.1

1999.3

2000.1

2000.3

2001.1

2001.3

2002.1

2002.3

2003.1

2003.3

2004.1

2004.3

2005.1

2005.3

2006.1

2006.3

2007.1

2007.3

2008.1

2008.3

2009.1

2009.3

2010.1

2010.3

2011.1

2011.3

2012.1

2012.3

Age 65-69 Age 70-74 Age 75 & over

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

There are now over 7.4 million senior workers. This is double the number in 1998. Over the next decade it will

probably double again.

(Thousands)

This is the leading edge of the older half of the

“baby boom” generation

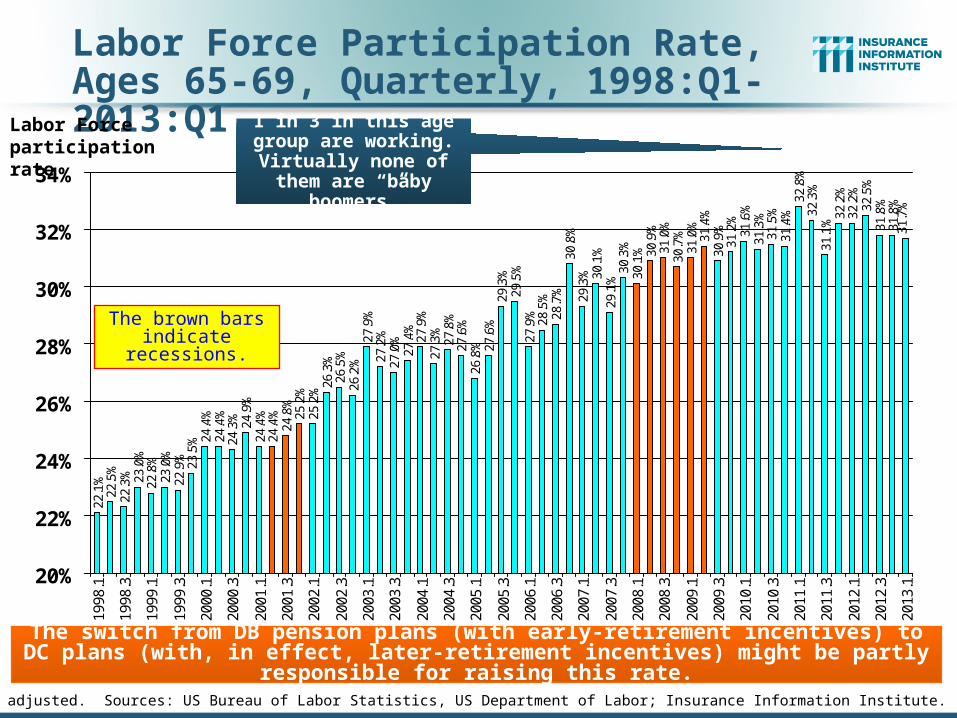

Labor Force Participation Rate, Ages 65-69, Quarterly, 1998:Q1-2013:Q1

25.2%

25.2%26.3%

26.5%

26.2%

27.9%

27.2%

27.4%27.9%

27.3%27.8%

27.6%

26.8% 27.6%

29.3%

29.5%

27.9% 28.5%

28.7%

30.8%

29.3% 30.1%

29.1%30.3%

30.1% 30.9%

31.0%

30.7%

31.0%

31.4%

30.9%

31.2%

31.6%

31.3%

31.5%

31.4%32.8%

32.3%

31.1%32.2%

32.2%

32.5%

31.8%

31.8%

31.7%

27.0%

22.9%

23.0%

22.8%

23.0%

22.3%

22.5%

22.1%

23.5% 24.4%

24.4%

24.3% 24.9%

24.4%

24.4%

24.8%

20%

22%

24%

26%

28%

30%

32%

34%

1998.1

1998.3

1999.1

1999.3

2000.1

2000.3

2001.1

2001.3

2002.1

2002.3

2003.1

2003.3

2004.1

2004.3

2005.1

2005.3

2006.1

2006.3

2007.1

2007.3

2008.1

2008.3

2009.1

2009.3

2010.1

2010.3

2011.1

2011.3

2012.1

2012.3

2013.1

Not seasonally adjusted. Sources: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

The brown bars indicate recessions.

Labor Force participation rate

The switch from DB pension plans (with early-retirement incentives) to DC plans (with, in effect, later-retirement incentives) might be partly responsible for raising this rate.

1 in 3 in this age group are working. Virtually

none of them are “baby boomers”

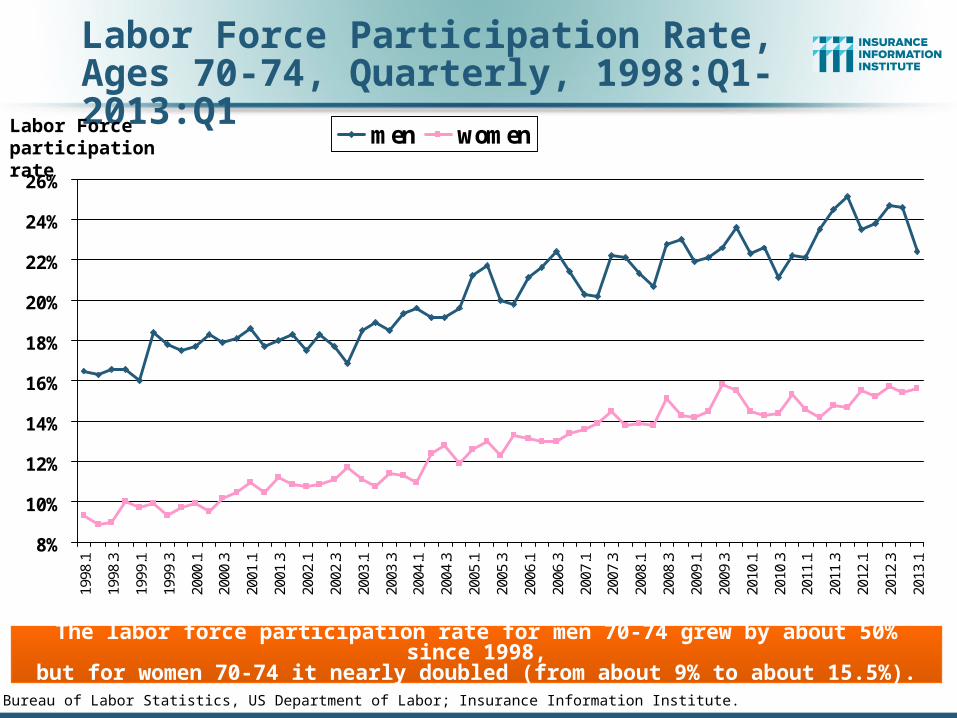

Labor Force Participation Rate,Ages 70-74, Quarterly, 1998:Q1-2013:Q1

14.2%

13.8%14.2%

14.0%

14.0%14.4%

14.4% 14.9%

14.9% 15.4%

15.6%

15.3%16.4% 17.0%

15.8%16.2% 16.7%

16.9%

17.2%

17.0%

16.7%

16.8%18.0%

17.5%

17.3%

16.9%

18.6%

18.2%

17.7%

17.9%18.9%

19.2%

18.0%

18.1%

17.4%18.4%

18.0%18.4% 19.3%19.5%

19.2%

19.1% 19.9%

19.6%

18.8%

14.6%

13.1%13.6%

12.4%12.9%

12.4%

12.2%

12.5% 13.1%

13.3%

13.5%

13.6%

13.8% 14.4%

13.7% 14.2%

9%

12%

15%

18%

21%

1998

.1

1998

.3

1999

.1

1999

.3

2000

.1

2000

.3

2001

.1

2001

.3

2002

.1

2002

.3

2003

.1

2003

.3

2004

.1

2004

.3

2005

.1

2005

.3

2006

.1

2006

.3

2007

.1

2007

.3

2008

.1

2008

.3

2009

.1

2009

.3

2010

.1

2010

.3

2011

.1

2011

.3

2012

.1

2012

.3

2013

.1

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

Labor Force participation rate

The labor force participation rate for workers 70-74 grew by about 50% since 1998.Growth stalled during and after the Great Recession but has since resumed.

Nearly 1 in 5 in this age group is working.

15 years ago it was 1 in 8.

Labor Force Participation Rate,Ages 70-74, Quarterly, 1998:Q1-2013:Q1

8%

10%

12%

14%

16%

18%

20%

22%

24%

26%

1998

.1

1998

.3

1999

.1

1999

.3

2000

.1

2000

.3

2001

.1

2001

.3

2002

.1

2002

.3

2003

.1

2003

.3

2004

.1

2004

.3

2005

.1

2005

.3

2006

.1

2006

.3

2007

.1

2007

.3

2008

.1

2008

.3

2009

.1

2009

.3

2010

.1

2010

.3

2011

.1

2011

.3

2012

.1

2012

.3

2013

.1

men women

Source: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

Labor Force participation rate

The labor force participation rate for men 70-74 grew by about 50% since 1998,but for women 70-74 it nearly doubled (from about 9% to about 15.5%).

Labor Force Participation Rate, Quarterly Ages 75 and over, 1998-2013:Q1

5.4%

5.1%5.1% 5.2%

5.0%

5.5%5.9%

5.8% 5.9% 6.0% 6.1%6.5%

6.1%

6.6%

6.3%6.7%

6.4% 6.6%

6.0%

6.5%6.5%

7.1%

7.0%

6.9%6.9%7.2% 7.4% 7.6%7.6%

7.0% 7.2%7.3%7.3%

6.9%

7.7%

7.5%

7.1%7.5% 7.6% 7.7%

7.6%7.6%

7.4%7.8%

8.6%

5.8%

5.4%

5.1%

4.8%5.0%

4.6%4.6%

4.5%

5.2% 5.4%

5.3%

5.2% 5.3%

5.2%5.2%

5.1%

3%

5%

7%

9%

1998.1

1998.2

1998.3

1998.4

1999.1

1999.2

1999.3

1999.4

2000.1

2000.2

2000.3

2000.4

2001.1

2001.2

2001.3

2001.4

2002.1

2002.2

2002.3

2002.4

2003.1

2003.2

2003.3

2003.4

2004.1

2004.2

2004.3

2004.4

2005.1

2005.2

2005.3

2005.4

2006.1

2006.2

2006.3

2006.4

2007.1

2007.2

2007.3

2007.4

2008.1

2008.2

2008.3

2008.4

2009.1

2009.2

2009.3

2009.4

2010.1

2010.2

2010.3

2010.4

2011.1

2011.2

2011.3

2011.4

2012.1

2012.2

2012.3

2012.4

2013.1

Sources: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

In the last 14 years, the labor force participation rate for workers 75 and over grew from 4.5% to 8.6%. So 91.4% of these people are retired.

Labor Force participation rate The labor force participation

rate for workers 75 and over will probably hit 10% soon. This is close to what the rate was for the 70-74 group a decade ago.

Labor Force Participation Rate, Quarterly Ages 75 and over, 1998-2013:Q1

2%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

13%

1998.1

1998.2

1998.3

1998.4

1999.1

1999.2

1999.3

1999.4

2000.1

2000.2

2000.3

2000.4

2001.1

2001.2

2001.3

2001.4

2002.1

2002.2

2002.3

2002.4

2003.1

2003.2

2003.3

2003.4

2004.1

2004.2

2004.3

2004.4

2005.1

2005.2

2005.3

2005.4

2006.1

2006.2

2006.3

2006.4

2007.1

2007.2

2007.3

2007.4

2008.1

2008.2

2008.3

2008.4

2009.1

2009.2

2009.3

2009.4

2010.1

2010.2

2010.3

2010.4

2011.1

2011.2

2011.3

2011.4

2012.1

2012.2

2012.3

2012.4

2013.1

men women

Sources: US Bureau of Labor Statistics, US Department of Labor; Insurance Information Institute.

In the last 15 years, the labor force participation rate for men 75 and overgrew from 6.9% to 12.6% and for women doubled (from 2.9% to 5.8%).

Labor Force participation rate

26

Fatal Work Injury Rates Improved SlightlySince 2006 but Still Climb Sharply With Age

2.8

2.7 3.

3 3.7 4.

2

5.0

11.2

2.6 3.

0 3.1 3.4 4.

1 4.6

10.2

2.4 2.6 2.7 3.

2 3.7

4.5

12.2

2.5

2.4

2.4 3.

0 3.6 4.

3

12.1

2.8

2.2 2.

7 2.9 3.

6

4.7

11.9

0

2

4

6

8

10

12

14

18-19 20-24 25-34 35-44 45-54 55-64 65+

2006

2007

2008

2009

2010

Source: US Bureau of Labor Statistics, at http://www.bls.gov/iif/oshcfoi1.htm/#2010

The fatality rate for workers 65 and older was 5 times that of workers age 25-34. The workplace of the future will have to

be completely redesigned to accommodate the surge in older workers.

Fatal Work Injury Rate per 100,000 full-time-equivalent workers No improvement in

fatal work injury rate for this age group

27

Older Workers Lose More Daysfrom Work Due to Injury or Illness

56

910

12

15

56

9

1112

13

56

8

10

13

15

56

9

12

14 14

0

2

4

6

8

10

12

14

16

20-24 25-34 35-44 45-54 55-64 65+

2008200920102011

Source: US Bureau of Labor Statistics, Nonfatal Occupational Injuries and Illnesses Requiring Days Away From Work, 2011 (Table 10), released November 8, 2012.

Median Days Away From Work

Youngest baby boomer is age 49 (in 2013)

Median lost time of workers age 65+ is 2-3X that of workers age 25-34. These numbers are pretty stable—they haven’t changed much since 2008.

Oldest baby boomer is age 67 (in 2013)

29

Older Workers Are MuchMore Likely to Break a Bone

3.1 3.7 4.0 4.35.9 6.4

15.313.4

9.9

7.47.86.7

0

2

4

6

8

10

12

14

16

18

20-24 25-34 35-44 45-54 55-64 65+

Fractures Multiple Traumatic Injuries

*per 10,000 full-time-equivalent workersSource: US Bureau of Labor Statistics, US Department of Labor at http://www.bls.gov/news.release/pdf/osh2.pdf Table 14

Incidence Rate* (2011)

30

Older Workers Are More Likely to Slip When Walking, but Less Likely to Overexert Themselves

10

.9 12

.7 17

.0 22

.3

30

.6 35

.1

34

.7 37

.7

44

.3 49

.6

39

.6

23

.8

10

.212

.1

12

.8

11

.4

10

.5

9.9

0

10

20

30

40

50

60

20-24 25-34 35-44 45-54 55-64 65+

Vehicles Floors, Walkways, etc. Overexertion

Source: US Bureau of Labor Statistics, US Department of Labor at http://www.bls.gov/news.release/pdf/osh2.pdf Table 14

Incidence Rate (2011)

Source/Nature of Injury:

Incidence rate for injury caused by vehicles is

about the same for all age groups

Investments: The New Reality

31

Investment Performance is a Key Driver of Profitability

31

32

Insurers Have Not Yet Fully Adapted to a Persistently Low Interest Rate Environment

They Didn’t Expect Rates to bePushed to Such Low LevelsPushed Down so RapidlyHeld to Such Low Levels for So LongSuppressed via Unprecedented Aggressiveness

of the Federal ReserveAbility to Release Prior Reserves Eased UrgencyOFFSETTING FACTORSCapitalization Still SolidEmergence of Sophisticated Price Monitoring

and Underwriting Tools

33

U.S. 10-Year Treasury Note Yields:A Long Downward Trend, 1990–2013

Note: Recessions indicated by gray shaded columns.Sources: Federal Reserve Bank at http://www.federalreserve.gov/releases/h15/data.htm. National Bureau of Economic Research (recession dates); Insurance Information Institutes.

1%

2%

3%

4%

5%

6%

7%

8%

9%

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Yields on 10-Year U.S. Treasury Notes have been essentially below 5% for a full decade.

Since roughly 80% of P/C bond/cash investments are in 10-year or shorter durations, most P/C insurer portfolios will have low-yielding bonds for years to come.

Yields on 10-Year U.S. Treasury Notes recently

plunged to all time record lows

33

34

Distribution of Bond Maturities,P/C Insurance Industry, 2003-2011

16.0%

15.2%

15.7%

16.2%

16.3%

29.8%

29.2%

28.8%

29.5%

30.0%

32.4%

36.2%

39.5%

41.4%

31.3%

32.5%

34.1%

34.1%

33.8%

31.2%

28.7%

26.7%

26.8%

15.4%

15.4%

13.6%

13.1%

12.9%

12.7%

11.7%

11.1%

10.3%

9.2%

7.6%

7.6%

7.4%

8.1%

8.1%

7.3%

6.4%

6.3%15.2%

14.4%

16.0%

15.4%

0% 20% 40% 60% 80% 100%

2003

2004

2005

2006

2007

2008

2009

2010

2011

Under 1 year

1-5 years

5-10 years

10-20 years

over 20 years

Sources: A.M. Best; Insurance Information Institute.

The main shift over these years has been from bonds with longer maturities to bonds with shorter maturities. The industry first trimmed its holdings of over-10-year bonds

(from 24.6% in 2003 to 16.9% in 2011) and then trimmed bonds in the 5-10-year category. Falling average maturity of the P/C industry’s bond portfolio is contributing to a drop in

investment income along with lower yields.

Property/Casualty Insurance Industry Investment Gain: 1994–2012F1

$35.4

$42.8$47.2

$52.3

$44.4

$36.0

$45.3$48.9

$59.4$55.7

$64.0

$31.7

$39.2

$53.4$56.2

$50.8

$58.0

$51.9$56.9

$0

$10

$20

$30

$40

$50

$60

$70

94 95 96 97 98 99 00 01 02 03 04 05* 06 07 08 09 10 11 12F

In 2012 (1st three quarters) both investment income and realized capital gains were lower than in the comparable period in 2011. And because

the Federal Reserve Board aims to keep interest rates exceptionally low through mid-2015, maturing bonds will be re-invested at even lower rates.

1Investment gains consist primarily of interest, stock dividends and realized capital gains and losses.*2005 figure includes special one-time dividend of $3.2B; 2012F figure is I.I.I. estimate based on annualized actual 2012:Q3 result of

$38.089B. Sources: ISO; Insurance Information Institute.

($ Billions)

Investment gains in 2012 are running approximately 20% below their pre-crisis peak

A 100 Combined Ratio Isn’t What ItOnce Was: Investment Impact on ROEs

Combined Ratio / ROE

* 2008 -2012 figures are return on average surplus and exclude mortgage and financial guaranty insurers. 2012:H1 combined ratio including M&FG insurers is 102.2, ROAS = 5.9%; 2011 combined ratio including M&FG insurers is 108.2, ROAS = 3.5%. Source: Insurance Information Institute from A.M. Best and ISO data.

97.5

100.6 100.1 100.8

92.7

101.099.3

100.9 101.1

106.4

95.7

6.2%4.6%

7.6%7.4%4.4%

9.6%

15.9%

14.3%

12.7% 10.9%

8.8%

80

85

90

95

100

105

110

1978 1979 2003 2005 2006 2007 2008 2009 2010 2011 2012:H10%

3%

6%

9%

12%

15%

18%

Combined Ratio ROE*

Combined Ratios Must Be Lower in Today’s DepressedInvestment Environment to Generate Risk Appropriate ROEs

A combined ratio of about 100 generates an ROE of ~7.0% in 2012, ~7.5% ROE in 2009/10,

10% in 2005 and 16% in 1979

Year Ago

2011:H1 = 109.4, 2.3% ROE

38

P/C Insurance Industry Financial Overview

Profit Recovery Was Set Backin 2011 and 2012

by High Catastrophe Losses& Other Factors

38

39

P/C Net Premiums Written: % Change, Quarter vs. Year-Prior Quarter, 2002–2012

Sources: ISO; Insurance Information Institute.

Finally! A sustained period (10 quarters) of growth in net premiums written (vs. same quarter, prior year), and strengthening.

10.2

%15

.1%

16.8

%16

.7%

12.5

%10

.1%

9.7%

7.8%

7.2%

5.6%

2.9%

5.5%

-4.6

%-4

.1%

-5.8

%-1

.6%

10.3

%10

.2% 13

.4%

6.6%

-1.6

%2.

1%0.

0%-1

.9%

0.5%

-1.8

%-0

.7%

-4.4

%-3

.7%

-5.3

%-5

.2%

-1.4

%-1

.3%

1.3% 2.

3%1.

7% 3.5%

1.6% 3.

2% 3.8%

3.1% 4.

2% 5.1%

-10%

-5%

0%

5%

10%

15%

20%

2002

:Q1

2002

:Q2

2002

:Q3

2002

:Q4

2003

:Q1

2003

:Q2

2003

:Q3

2003

:Q4

2004

:Q1

2004

:Q2

2004

:Q3

2004

:Q4

2005

:Q1

2005

:Q2

2005

:Q3

2005

:Q4

2006

:Q1

2006

:Q2

2006

:Q3

2006

:Q4

2007

:Q1

2007

:Q2

2007

:Q3

2007

:Q4

2008

:Q1

2008

:Q2

2008

:Q3

2008

:Q4

2009

:Q1

2009

:Q2

2009

:Q3

2009

:Q4

2010

:Q1

2010

:Q2

2010

:Q3

2010

:Q4

2011

:Q1

2011

:Q2

2011

:Q3

2011

:Q4

2012

:Q1

2012

:Q2

2012

:Q3

This upward trendis likely to continue

as the economy’s recovery strengthens

Most recent “hard market”

42

Commercial Lines Direct Premiums Written:

Pct. Change by State, 2006-2011*

100.

9

60.8

38.9

28.9

27.9

25.6

14.9

8.3

4.0

2.9

2.7

0.9

0.2

0.0

-0.5

-1.5

-2.5

-6.3

-6.4

-6.6

-6.6

-6.7

-7.6

-7.8

-7.9

-20

0

20

40

60

80

100

120N

D

SD

MT IA NE

KS

OK

WY

MN

TX

AK WI

VT IN AR

LA

TN IL

OH

MA

NM

MS

WA

NY

NC

Pe

ce

nt

ch

an

ge

(%

)

Sources: SNL Financial LC.; Insurance Information Institute.

Top 25 States

Only 13 states showed any direct written premium

growth in commercial lines from 2006 to 2011

43

Direct Premiums Written: Comm. LinesPercent Change by State, 2006-2011*

-7.9

-8.0

-8.1

-9.0

-10

.0

-10

.1

-10

.8

-11

.4

-11

.6

-12

.2

-12

.7

-12

.9

-13

.2

-13

.2

-13

.6

-14

.7

-15

.0

-16

.0

-16

.7

-19

.4

-19

.8

-19

.9

-23

.7

-24

.4

-26

.4

-33

.0

-40

-35

-30

-25

-20

-15

-10

-5

0

KY

PA

MO

US

ME

CT

SC AL

VA

GA ID

MD NJ RI

CO

UT

OR MI

DE

CA

NH HI

FL AZ

WV

NV

Pe

ce

nt

ch

an

ge

(%

)

Bottom 25 States

States with the poorest performing economies also producedthe most negative net change in premiums of the past 5 years

Sources: SNL Financial LC.; Insurance Information Institute.

Underwriting Gain (Loss)1975–2012:Q3**

*Includes mortgage and financial guaranty insurers in all years. **through first three quarters of 2012Sources: A.M. Best; ISO; Insurance Information Institute.

Average yearly underwriting loss in the 2008-2011 low-interest-rate environment? $17.8B. With interest rates this low, large persistent

underwriting losses are not a recipe for success.

-$55

-$45

-$35

-$25

-$15

-$5

$5

$15

$25

$35

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

In historical context, 2006-07 underwriting

results were an anomaly

($ Billions) Net underwriting losses in 1st 3 qtrs of 2012 totaled $6.7B

High cat losses in 2011 led to

the worst underwriting

year since 2002

Cumulative underwriting loss since 1975? $500B, averaging $13.2B/year.

46

P/C Insurance Industry Combined Ratio, 2001–2012:Q3*

* Excludes Mortgage & Financial Guaranty insurers 2008--2012. Including M&FG, 2008=105.1, 2009=100.7, 2010=102.4, 2011=108.2; 2012:Q3=100.9. Sources: A.M. Best; ISO.

95.7

99.3100.8

106.4

100.0101.0

92.6

100.898.4

100.1

107.5

115.8

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011* 2012:Q3

Best Combined

Ratio Since 1949 (87.6)

As Recently as 2001, Insurers Paid Out

Nearly $1.16 for Every $1 in Earned

Premiums

Relatively Low CAT Losses, Reserve Releases

Heavy Use of Reinsurance Lowered Net

Losses

Relatively Low CAT Losses, Reserve Releases

Avg. CAT Losses,

More Reserve Releases

Higher CAT

Losses, Shrinking Reserve

Releases, Toll of Soft

Market

Cyclical Deterioration

Lower CAT

Losses Before Sandy

109.4110.2

118.8

109.5

112.5

110.2

107.6

104.1

109.7 110.2

102.5

105.4

91.1

93.6

104.2

98.9

102.1

106.7

109.0

102.9102.0

111.1112.3

122.3

90

95

100

105

110

115

120

125

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

F

13

F

Co

mm

erc

ial L

ine

s C

om

bin

ed

Ra

tio

*2007-2013F figures exclude mortgage and financial guaranty segments.Sources: A.M. Best; Insurance Information Institute

Commercial Lines Combined Ratio, 1990-2013F*

Commercial lines underwriting

performance in 2012 was the worst since 2002 due

to heavy impact from Sandy

47

Commercial Auto Combined Ratio: 1993–2014F

11

2.1

11

2.0

11

3.0 11

5.9

10

2.7

95

.2

92

.9

92

.1

92

.4 94

.3 96

.8 99

.4

98

.0

10

4.6

10

7.1

10

3.6

10

1.2

11

8.1

11

5.7

11

6.2

85

90

95

100

105

110

115

120

125

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12F 13F 14F

Commercial Auto is Expected to Improve as Rate Gains Outpace Any Adverse Frequency and Severity Trends

48Sources: A.M. Best (1990-2013F);Conning (2014F); Insurance Information Institute.

Commercial Multi-Peril Combined Ratio: 1995–2013F

80

90

100

110

120

130

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12E 13F

CMP-Liability CMP-Non-Liability

Commercial Multi-Peril Underwriting Performance is Expected to Improve in 2013 Assuming Normal Catastrophe Loss Activity

*2012-2013 figures are A.M. Best estimate/forecast for the combined liability and non-liability components.Sources: A.M. Best; Insurance Information Institute. 49

General Liability Combined Ratio: 2005–2014F

112.9

95.1

99.0

94.2

100.7

103.3 103.7

107.1

110.8

99.6

90

95

100

105

110

115

05 06 07 08 09 10 11 12F 13F 14F

Commercial General Liability Underwriting Performance Has Been Volatile in Recent Years

Source: Conning Research and Consulting. 50

Inland Marine Combined Ratio: 1999–2014F

101.9

92.8

100.2

83.8

77.379.5

93.3

89.3

86.2

97.7 97.7

89.7 89.7

80.882.5

89.9

75

80

85

90

95

100

105

99 00 01 02 03 04 05 06 07 08 09 10 11 12F 13F 14F

Inland Marine is Expected to Remain Among the Most Profitable of All Lines

Sources: A.M. Best (1999-2011); Insurance Information Institute (2012F); Conning (2013F-2014F) 51

Surety Bonds Combined Ratio,2002–2011

116.9122.0 119.5

101.8

79.5

70.5 72.5

81.6

70.466.6

50

75

100

125

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Source: A.M. Best Aggregates & Averages, 2012, p. 376. 52

Workers Compensation Combined Ratio: 1994–2014F

102.

0

97.0

100.

0

101.

0

112.

6

108.

6

105.

1

102.

7

98.5

103.

5

104.

5

110.

6

116.

8

116.

9

117.

3

115.

0

111.

0

121.

7

107.

0

115.

3

118.

2

90

100

110

120

130

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12E 13F 14F

Workers Comp underwriting results are expected to begin improving in 2013. They deteriorated markedly since 2007 and in

2012 are estimated to have hit their worst level in a decade.

Sources: A.M. Best (1994-2013F); Insurance Information Institute (2014F). 53

P/C Net Income After Taxes1991–2012:Q3 ($ Millions)

$1

4,1

78

$5

,84

0

$1

9,3

16

$1

0,8

70

$2

0,5

98

$2

4,4

04 $

36

,81

9

$3

0,7

73

$2

1,8

65

$3

,04

6

$3

0,0

29

$6

2,4

96

$3

,04

3

$3

5,2

04

$1

9,1

50

$2

6,9

81

$2

8,6

72

-$6,970

$6

5,7

77

$4

4,1

55

$2

0,5

59

$3

8,5

01

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12:Q3

2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.1% 2009 ROE = 5.0% 2010 ROE = 6.6% 2011 ROAS1 = 3.5% 2012:Q3 ROAS1 = 6.3%

Through the first three quarters of 2012, P/C

Industry profits were up 222% from the comparable period in 2011, mainly due

to lower CAT losses in 2012:Q2 and Q3

* ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 6.2% ROAS for 2012:H1, 4.6% ROAS for 2011, 7.6% for 2010 and 7.4% for 2009.Sources: A.M. Best; ISO; Insurance Information Institute.

-5%

0%

5%

10%

15%

20%

25%

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

*1

2:

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2012:Q3*

*Profitability = P/C insurer ROEs. 2012 is an estimate based on ROAS data. Note: Data for 2008-2012 exclude mortgage and financial guaranty insurers. 2012:H1 ROAS = 5.9% including M&FG.Sources: Insurance Information Institute; NAIC; ISO; A.M. Best.

1977:19.0% 1987:17.3%

1997:11.6%2006:12.7%

1984: 1.8% 1992: 4.5% 2001: -1.2%

10 Years

10 Years9 Years

2011:4.6%*

History suggests next ROE peak will be in 2016-2017

ROE

1975: 2.4%

2012:Q3: 6.3%

59

Policyholder Surplus, 2006:Q4–2012:Q3

Sources: ISO; A.M .Best.

($ Billions)

$487.1$496.6

$512.8$521.8

$478.5

$455.6

$437.1

$463.0

$490.8

$511.5

$540.7$530.5

$544.8

$559.2 $559.1

$538.6$550.3

$583.5$570.7$566.5

$505.0$515.6$517.9

$425

$450

$475

$500

$525

$550

$575

$600

06:Q

4

07:Q

1

07:Q

2

07:Q

3

07:Q

4

08:Q

1

08:Q

2

08:Q

3

08:Q

4

09:Q

1

09:Q

2

09:Q

3

09:Q

4

10:Q

1

10:Q

2

10:Q

3

10:Q

4

11:Q

1

11:Q

2

11:Q

3

11:Q

4

12:Q

1

12:Q

3

Surplus as of 9/30/12 was a

new peak

The industry now has $1 of surplus for every $0.80 of NPW, the strongest claims-paying status in its history

Drop due to near-record 2011 CAT losses

60

Inflation and Claims Trends

61

Prices for Hospital Services:12-Month Change,* 1998–2013

*Percentage change from same month in prior year; through January 2013; seasonally adjustedSources: US Bureau of Labor Statistics; National Bureau of Economic Research (recession dates); Insurance Information Institute.

0%

2%

4%

6%

8%

10%

12%

14%

'98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Recession Outpatient Services Inpatient Services

Cyclical peaks in PP Auto tend to occur approximately every 10 years(early 1990s, early 2000s, and possibly the early 2010s)

62

Forces that Drive Car Repair Costs:12-Month Change,* 2001–2013

*Percentage change from same month in prior year; through January 2013; seasonally adjustedSources: US Bureau of Labor Statistics; National Bureau of Economic Research (recession dates); Insurance Information Institute.

0%

2%

4%

6%

8%

10%

12%

14%

'01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13

Recession Auto repair Auto body work

Cyclical peaks in PP Auto tend to occur approximately every 10 years(early 1990s, early 2000s, and possibly the early 2010s)

Catastrophes

6363

Nu

mb

er

Geophysical (earthquake, tsunami, volcanic activity)

Climatological (temperature extremes, drought, wildfire)

Meteorological (storm)

Hydrological (flood, mass movement)

Natural Disasters in the United States, 1980 – 2012Number of Events (Annual Totals 1980 – 2012)

Source: MR NatCatSERVICE 64

41

19

121

3

50

100

150

200

250

300

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010 2012

There were 184 natural disaster events in the

US in 2012

There were over 150 natural disaster events in the US every

year since 2006. That hadn’t happened in any year before.

65

$1

2.6

$1

1.0

$3

.8

$1

4.3

$1

1.6

$6

.1

$3

4.7

$7

.6

$1

6.3

$3

3.7

$7

3.4

$1

0.5

$7

.5

$2

9.2

$1

1.5

$1

4.4

$3

3.1

$3

7.0

$1

4.0

$4

.8

$8

.0

$3

7.8

$8

.8

$2

6.4

$0

$10

$20

$30

$40

$50

$60

$70

$80

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12*

US Insured Catastrophe Losses

*As of 1/2/13. Includes $20B gross loss estimate for Hurricane Sandy.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01 ($25.9B 2011 dollars). Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B ($15.6B in 2011 dollars.) Sources: Property Claims Service/ISO; Insurance Information Institute.

US CAT Losses in 2012 Will Likely Become the 2nd or 3rd Highest in US History on An Inflation-Adjusted Basis (Pvt

Insured). 2011 Losses Were the 5th Highest

2012 CAT losses were down nearly 50% from 2011 until Sandy struck in late October

Record Tornado Losses Caused

2011 CAT Losses to Surge

($ Billions, 2012 Dollars)

65

66

The Dozen Most Costly Hurricanesin U.S. History

Insured Losses, 2012 Dollars, $ Billions

*Estimate as of 12/09/12 based on estimates of catastrophe modeling firms and reported losses as of 1/12/13. Estimates range up to $25B.Sources: PCS; Insurance Information Institute inflation adjustments to 2012 dollars using the CPI.

$9.2 $11.1$13.4

$20.0

$25.6

$48.7

$8.7$7.8$6.7$5.6$5.6$4.4

$0

$10

$20

$30

$40

$50

$60

Irene(2011)

Jeanne(2004)

Frances(2004)

Rita (2005)

Hugo (1989)

Ivan (2004)

Charley(2004)

Wilma(2005)

Ike (2008)

Sandy*(2012)

Andrew(1992)

Katrina(2005)

Sandy will likely become the 3rd costliest hurricane in US insurance history

Irene became the 12th most expensive

hurricane in US history

10 of the 12 most costly hurricanes in insurance history occurred in the past 9 years (2004—2012)

67

If They Hit Today, the Dozen Costliest (to Insurers) Hurricanes in U.S. History

Insured Losses,2012 Dollars, $ Billions

*Estimate as of 12/09/12 based on estimates of catastrophe modeling firms and reported losses as of 1/12/13. Estimates range up to $25B.Sources: Karen Clark & Company, Historical Hurricanes that Would Cause $10 Billion or More of Insured LossesToday, August 2012; I.I.I.

$40$50 $50 $50

$65

$125

$40$35$25$20$20$20

$0

$20

$40

$60

$80

$100

$120

$140

Sandy*(2012)

Betsy(1965)

Hazel(1954)

Donna(1960)

NewEngland(1938)

Katrina(2005)

Galveston(1915)

Andrew(1992)

south-Florida(1947)

Galveston(1900)

mid-Florida(1928)

Miami(1926)

When you adjust for the damage prior storms could have done if they occurred today, Hurricane Katrina slips to a tie for 6th among the most

devastating storms.

Storms that hit long ago had less property and businesses to damage, so simply adjusting their actual claims for inflation doesn’t capture their

destructive power.Karen Clark’s analysis aims to overcome that.

Auto, 230,500 ,

17%

Commercial, 167,500 ,

12%

Homeowner, 982,000 ,

71%

Hurricane Sandy resulted in an

estimated 1.4 million privately insured

claims resulting in an estimated $15 to $25

billion in insured losses. Hurricane

Katrina produced 1.74 million claims and $47.6B in losses

(in 2011 $)

Superstorm Sandy:Number of Claims by Type*

*PCS claim count estimate as of 11/26/12. Loss estimate represents high and low end estimates by risk modelers RMS, Eqecat and AIR. PCS estimate of insured losses as of 11/26/12 $11 billion. All figures exclude losses paid by the NFIP.Source: PCS; AIR, Eqecat, AIR Worldwide; Insurance Information Institute. 68

Sandy is a high frequency, (relatively

low) severity event (avg. severity <50% Katrina)

69

Long Island (NY) Flood-Damaged Structures with & w/o Flood Insurance

Source: Newsday, 1/14/13 from FEMA and Small Business Administration.

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

Nassau Suffolk

InsuredUninsured

The Maximum FEMA Grant is $31,900. The Average Grant Award to Homeowners and Renters on Long Island is About $7,300

52,428

$15.0

43,106

$2.2

69

74,736

20,7985,747

Only 37.5% of flood damaged buildings in Nassau County were insured for flood, 62.5% uninsured

27.6% of flood damaged buildings in Suffolk County were insured for

flood, 73.4% uninsured

15,051

Number of buildings

Source: Wharton Center for Risk Management and Decision Processes, Issue Brief, Nov. 2012; Insurance Information Institute.

Residential NFIP Flood Take-Up Rates in NY, CT (2010) & Sandy Storm Surge

70

Flood coverage

penetration rates were

extremely low in many very

vulnerable areas of NY and CT, with take-up rates far below 50% in many areas

71

TERRORISM RISK

The Countdown to TRIA Expiration Begins

Reauthorization Faces an Uphill Battle in Congress

72

I.I.I. Congressional Testimony on the Future of the Terrorism Risk Insurance Program

Issue: Act expires 12/31/14. Insurers still generally regard large-scale terror attacks as fundamentally uninsurable

I.I.I. Input: Testified at first hearing on the issue in DC (on 9/11/12) on trends in terrorist activity in the US and abroad, difficulties in underwriting terror risk; Noted that bin Laden may be dead but war on terror is far from over

Status: New House FS Committee Chair Jeb Hensarling has opposed TRIA in the past; Obama Administration does not seem to support extension; Little institutional memory on insurance subcommittee

Media: Virtually no media coverage yet apart form trade press; WSJ will likely editorialize against it.

Objective: Work with trades, risk management community and others to help build support

Life$1.2 (3%)

Aviation Liability

$4.3 (11%)

Other Liability

$4.9 (12%)

Biz Interruption $13.5 (33%)

Property -WTC 1 & 2*$4.4 (11%) Property -

Other$7.4 (19%)

Aviation Hull$0.6 (2%)

Event Cancellation

$1.2 (3%)Workers Comp

$2.2 (6%)

Total Insured Losses Estimate: $40.0B***Loss total does not include March 2010 New York City settlement of up to $657.5 million to compensate approximately 10,000 Ground Zero workers or any subsequent settlements.

**$32.5 billion in 2001 dollars.

Source: Insurance Information Institute.

Loss Distribution by Type of Insurancefrom Sept. 11 Terrorist Attack ($ 2011)

($ Billions)

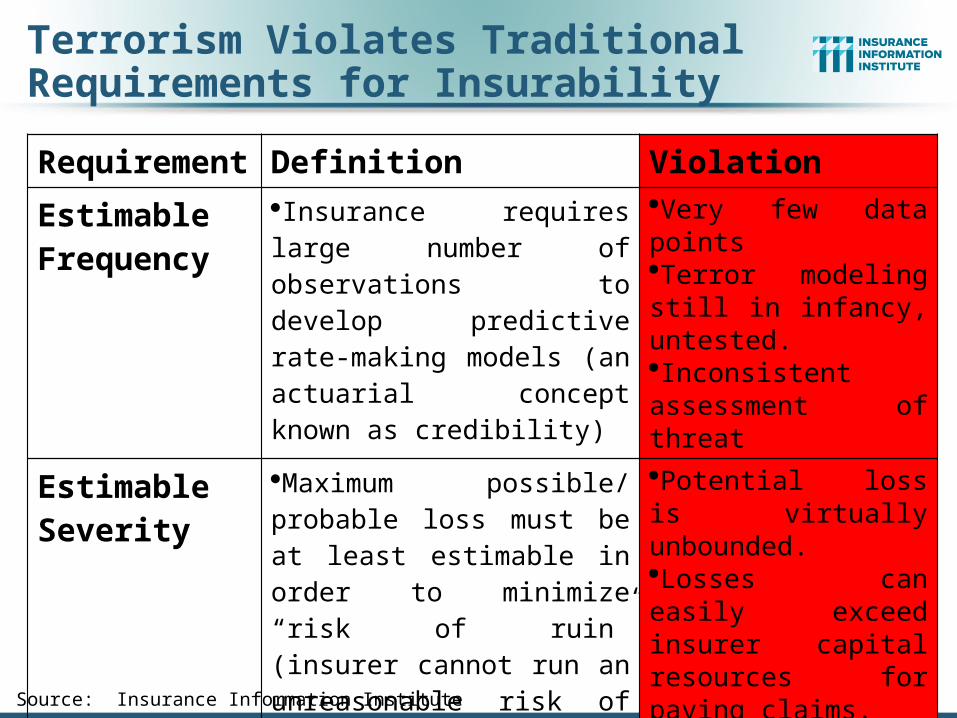

Terrorism Violates Traditional Requirements for Insurability

Requirement Definition Violation

EstimableFrequency

Insurance requires large number of observations to develop predictive rate-making models (an actuarial concept known as credibility)

Very few data pointsTerror modeling still in infancy, untested.Inconsistent assessment of threat

EstimableSeverity

Maximum possible/ probable loss must be at least estimable in order to minimize “risk of ruin” (insurer cannot run an unreasonable risk of insolvency though assumption of the risk)

Potential loss is virtually unbounded.Losses can easily exceed insurer capital resources for paying claims.Extreme risk in workers compensation and statute forbids exclusions.

Source: Insurance Information Institute

Requirement Definition Violation

Diversifiable Risk

Must be able to spread/distribute risk across large number of risks“Law of Large Numbers” helps makes losses manageable and less volatile

Losses likely highly concentrated geographically or by industry (e.g., WTC, power plants)

Random Loss Distribution/Fortuity

Probability of loss occurring must be purely random and fortuitousEvents are individually unpredictable in terms of time, location and magnitude

Terrorism attacks are planned, coordinated and deliberate acts of destructionDynamic target shifting from “hardened targets” to “soft targets”Terrorist adjust tactics to circumvent new security measuresActions of US and foreign govts. may affect likelihood, nature and timing of attack

Source: Insurance Information Institute

Terrorism Violates Traditional Requirements for Insurability (cont’d)

76

Key Takaways

76

77

P/C Insurance Exposures Will Grow With the U.S. Economy Personal and commercial exposure growth is likely in 2013

– But restoration of destroyed exposure will take until mid-decade Wage growth is also positive and could modestly accelerate

P/C Industry Growth in 2013 Will Be Strongest Since 2004 Growth likely to exceed A.M. Best projection of +3.8% for 2012 No traditional “hard market” emerges in 2013

Underwriting Fundamentals Deteriorate Modestly Some pressure from claim frequency, severity in some key lines But WC will be tough to fix

Industry Capacity Hits a New Record by Year-End 2013 (Barring Meg-CAT)

Investment Environment Is/Remains Challenging Interest rates remain low

Takeaways:Insurance Industry Predictions for 2013

www.iii.org

Thank you for your timeand your attention!

Insurance Information Institute