To Company A · • Origin Energy 37.5% ConocoPhillips 37.5% Sinopec 25.0%. Off-take Agreements:...

27

Origin Energy L GPO Box 5376, To Company From Subject Please find Regards Helen Har Company S 02 8345 5023 Limited ACN 000 0 , Sydney NSW 200 Company A ASX Limite Helen Hard Australia P d attached a dy Secretary 3 – helen.hardy@ 051 696 • Lvl 45 A 01 • Telephone (02 Announceme d dy Pacific LNG – a presentatio @originenergy.c Australia Square, 2 2) 8345 5000 • Fac nts Office FID2 Investo on to be mad com.au 264-278 George S csimile (02) 9252 or Presentati de to investo Street, Sydney NSW 1566 • www.orig Facsimile 1 Date 4 Pages 2 ion ors and medi W 2000 inenergy.com.au 1300 135 638 4 July 2012 27 a today. 8 For personal use only

Transcript of To Company A · • Origin Energy 37.5% ConocoPhillips 37.5% Sinopec 25.0%. Off-take Agreements:...

Origin Energy LGPO Box 5376,

To

Company

From

Subject

Please find Regards

Helen HarCompany S 02 8345 5023

Limited ACN 000 0, Sydney NSW 200

Company A

ASX Limite

Helen Hard

Australia P

d attached a

dy Secretary

3 – helen.hardy@

051 696 • Lvl 45 A01 • Telephone (02

Announceme

d

dy

Pacific LNG –

a presentatio

@originenergy.c

Australia Square, 22) 8345 5000 • Fac

nts Office

FID2 Investo

on to be mad

com.au

264-278 George Scsimile (02) 9252

or Presentati

de to investo

Street, Sydney NSW 1566 • www.orig

Facsimile 1

Date 4

Pages 2

ion

ors and medi

W 2000 inenergy.com.au

1300 135 638

4 July 2012

27

a today.

8

For

per

sona

l use

onl

y

Australia Pacific LNG – FID2 Final Investment Decision on Train 2

Grant King, Managing Director

4 July 2012

For

per

sona

l use

onl

y

Important Notice This presentation does not constitute investment advice, or an inducement or recommendation to acquire or dispose of any securities in Origin, in any jurisdiction (including the USA). This presentation is for information purposes only, is in a summary form, and does not purport to be complete. This presentation does not take into account the investment objectives, financial situation or particular needs of any investor, potential investor or any other person. No investment decision should be made in reliance on this presentation. Independent financial and taxation advice should be sought before making any investment decision.

Any statements in this presentation in the nature of forward looking statements, including statements of current intention, statements of opinion and predictions as to possible future events are not statements of fact and there can be no certainty of outcome in relation to the matters to which the statements relate. These forward looking statements involve known and unknown risks, uncertainties, assumptions and other important factors that could cause the actual outcomes to be materially different from the events or results expressed or implied by such statements. Those risks, uncertainties, assumptions and other important factors are not all within the control of Origin and cannot be predicted by Origin and include changes in circumstances or events that may cause objectives to change as well as risks, circumstances and events specific to the industry, countries and markets in which Origin and its related bodies corporate, joint ventures and associated undertakings operate. They also include general economic conditions, exchange rates, interest rates, the regulatory environment, competitive pressures, selling price, market demand and conditions in the financial markets which may cause objectives to change or may cause outcomes not to be realised. None of Origin or any of its respective subsidiaries, affiliates and associated companies (or any of their respective officers, employees or agents) (the "Relevant Persons") makes any representation, assurance or guarantee as to the accuracy or likelihood of fulfilment of any forward looking statement or any outcomes expressed or implied in any forward looking statements. The forward looking statements in this presentation reflect views held only at the date of this presentation. In addition, statements about past performance are not necessarily indicative of future performance. Subject to any continuing obligations under law or the ASX Listing Rules, Origin and the Relevant Persons disclaim any obligation or undertaking to disseminate after the date of this presentation any updates or revisions to any forward looking statements to reflect any change in expectations in relation to any forward looking statements or any change in events, conditions or circumstances on which such statements are based. No representation or warranty, express or implied, is or will be made in relation to the accuracy or completeness of the information in this presentation and no responsibility or liability is or will be accepted by Origin or any of the Relevant Persons in relation to it. In particular, Origin does not endorse, and is not responsible for, the accuracy or reliability of any information in this presentation relating to a third party. All references to "$" are references to Australian dollars unless otherwise specified. All references to debt refer to interest-bearing debt. A reference to Australia Pacific LNG or APLNG is a reference to Australia Pacific LNG Pty Limited, an incorporated joint venture in which Origin currently holds a 42.5% shareholding but which is expected to be diluted to 37.5% as described in this presentation. A reference to FID1 is a reference to the Final Investment Decision on the first train including infrastructure for the second train of APLNG’s two train CSG to LNG project taken on 28 July 2011. A reference to FID2 is a reference to a Final Investment Decision on the remainder of the second train of APLNG’s two train CSG to LNG project, as announced in this presentation.

2 |

For

per

sona

l use

onl

y

Important Notice (continued)

All comparative data is in relation to either the year ended 30 June 2011 or the 6 months ended 31 December 2010 as indicated, unless otherwise stated. Certain comparative amounts may have been reclassified to conform with the current year’s presentation.

Reserves The statements in this document relating to reserves and resources have been compiled by Andrew Mayers, a full-time employee of Origin, based on the information provided in the December 2011 assessment of Australia Pacific LNG’s CSG reserves and resources, which were prepared by internationally recognised petroleum consultant Netherland, Sewell & Associates, Inc. (NSAI) as per their report dated 20 February 2012, compiled by Mr John G. Hattner, a full-time employee of NSAI. Andrew Mayers is qualified in accordance with ASX Listing Rule 5.11 and has consented to the form and context in which these statements appear. Reserves quoted here have been compiled in a manner consistent with the Petroleum Resources Management System 2007 published by Society of Petroleum Engineers (SPE). This document may be found at the SPE website. Further information regarding the formulation of Origin’s reserves may be found in Origin’s Management Discussion and Analysis released to the ASX on 23 February 2012 and its Annual Reserves Report released to the ASX on 28 July 2011, including information on the calculation of reserves and the existence of reversion rights in some areas.

3 |

For

per

sona

l use

onl

y

Australia Pacific LNG has approved a Final Investment Decision on the second train of its CSG to LNG project …

• FID taken on the second train of the Australia Pacific LNG project (FID2)

• Marketing complete for two-train project

• Shareholdings following completion of Sinopec’s additional equity subscription: Origin 37.5%, ConocoPhillips 37.5%, Sinopec 25%

• Since FID1 in July 2011, there has been no significant change in the estimated US$20 billion project costs other than as a result of movements in foreign exchange rates, which at the time converted to A$23 billion

• The project is estimated to cost A$23 billion from FID1 to first gas from the second train

• Robust project economics

• On schedule and budget to deliver first LNG in mid-2015

• Origin and ConocoPhillips are commencing a joint process to further dilute their interests in Australia Pacific LNG

4 |

Artist’s impression of the LNG facility on Curtis Island

Origin and Australia Pacific LNG exploration and production permits in the Surat and Bowen basins

… marking a major milestone for the project, and for the growth of Origin

For

per

sona

l use

onl

y

Project description:

• CSG-to-LNG export project - two LNG trains approved, each with a 4.5 mtpa nameplate capacity

Shareholdings(1): • Origin Energy 37.5% ConocoPhillips 37.5% Sinopec 25.0%

Off-take Agreements:

• 7.6 mtpa LNG supply for 20 years to Sinopec(2)

• ~1.0 mtpa LNG supply for 20 years to The Kansai Electric Company

Project cost: • A$23 billion from July 2011 until start-up of Train 2 in early 2016, in line with the US dollar cost estimates announced at FID1

APLNG economics: • US$35/bbl breakeven oil price(3) to cover estimated project costs and project finance debt service obligations

• US$50/bbl breakeven oil price(3) for Origin to recover its weighted average cost of capital on its estimated cash injection into Australia Pacific LNG

APLNG reserves(4)

(at 31 December 2011): • 2P: 12,810 PJ 3P: 16,022 PJ • Additional 4,240 PJ (2C) or 10,614 PJ (3C) of contingent resources

Timing: • First LNG: Train 1 expected mid-2015, Train 2 expected early-2016

APLNG’s value to Origin is demonstrated by a breakeven oil price of US$35/bbl to cover project costs and project finance debt service obligations …

(1) Percentages shown assume completion of Sinopec’s 25% equity subscription. (2) Refer to note 2 on slide 7. (3) Real oil price; from FID1 (July 2011) over the estimated life of the project. (4) Refer to Reserves disclosure in Important Notices on slide 3. Australia Pacific LNG reserves are calculated on a forward view of commodity

prices. Some of APLNG’s CSG reserves and resources are subject to reversionary rights.

OVERVIEW

5 |

… or US$50/bbl to cover Origin’s weighted average cost of capital on its estimated cash injection into Australia Pacific LNG

For

per

sona

l use

onl

y

Australia Pacific LNG has made significant progress over the last four years …

6 |

… in the development of one of Australia’s largest LNG export projects

Milestones Timing (CY)

Origin and ConocoPhillips form APLNG incorporated JV Q4 2008

Initial Advice Statement submitted Q1 2009

Curtis Island site selected Q3 2009

Commenced FEED work Q4 2009

Environmental approvals Q1 2011

Sinopec – 4.3 mtpa foundation customer Q2 2011

Issued major project contracts Q2 2011

FID1 announced Q3 2011

Kansai – 1.0 mtpa LNG offtake heads of agreement Q4 2011

Sinopec – 3.3 mtpa LNG offtake - marketing completed Q1 2012

FID2 announced mid-2012

First LNG, Train 1 mid-2015

First LNG, Train 2 early-2016

For

per

sona

l use

onl

y

Australia Pacific LNG is a strong and aligned incorporated joint venture, combining Origin’s Australian CSG experience with ConocoPhillips’ extensive LNG and CSG capabilities …

• Australia’s largest integrated energy company

• Listed in S&P/ASX 20 index

• Integrated energy company with global operations

• One of world’s largest CSG operators with over 25 years’ experience

• Integrated energy and chemical company • One of China’s largest petroleum products

suppliers and crude oil and natural gas producers

• 7.6 mtpa LNG off-take agreement for 20 years(2)

• 1 mtpa LNG off-take agreement for 20 years

Developer of CSG to LNG project based on Australia’s largest CSG 2P Reserves base

UPSTREAM DOWNSTREAM

• Domestic contracts

37.5%(1) 37.5%(1) 25%(1)

(1) Percentages shown assume completion of Sinopec’s 25% equity subscription. (2) In calendar year 2015, it is expected cargoes will be delivered at a pro rata rate of 2.5 mtpa. The additional 3.3 mtpa offtake agreement

extends from early 2016 to 2035. In calendar year 2016, it is expected cargoes will be delivered at a pro rata rate of 4.3 mtpa prior to the start of the second train, following which the rate will increase by a pro rata rate of 3.3 mtpa.

… to supply two of Asia’s leading energy companies, Sinopec and Kansai

7 |

For

per

sona

l use

onl

y

8 |

FID2 is the final condition precedent for Sinopec’s equity subscription in Australia Pacific LNG to increase to 25 per cent

(1) Assumes Origin has a 37.5% shareholding in APLNG; assumes AUD/USD exchange rate parity for subscription proceeds of US$110 per % and includes US$1.765 billion of Sinopec subscription monies paid to APLNG in August 2011 for first 15% shareholding; capital expenditure since 1 January 2011 assumes foreign exchange rates on date of shareholder cash calls and assumes 1.086 billion Origin shares on issue.

Sinopec’s additional equity subscription would value APLNG at approximately A$6.20 per Origin share(1) using a look-through valuation

• With the taking of FID2, Sinopec’s agreement to increase its shareholding in APLNG from 15% to 25% is now unconditional with completion due to occur shortly

• Origin and ConocoPhillips holdings will then each be diluted from 42.5% to 37.5%

• Shareholdings at completion: Origin (37.5%); ConocoPhillips (37.5%); Sinopec (25%)

• Sinopec’s additional equity subscription and share of capital expenditure since 1 January 2011 will result in Sinopec injecting an estimated US$2.1 billion into APLNG

• Reinforces that the export project is overseen by a strong and experienced group of shareholders in Australia Pacific LNG

For

per

sona

l use

onl

y

Australia Pacific LNG marketing is complete with contracts in place for 8.6 mpta of LNG

Sinopec

• 7.6 mpta LNG supply for 20 years

• Largest LNG supply agreement in Australian history by annual volume

• Commencing 2015 for 4.3 mtpa and 2016 for additional 3.3 mtpa

9 |

Kansai

• 1.0 mtpa LNG supply for 20 years

• Commencing 2016

For

per

sona

l use

onl

y

The project is underpinned by a large, high quality reserves base with strong, experienced operators in CSG and LNG developments

Quality of the CSG resource

• APLNG holds prime acreage in both of the Queensland’s CSG “sweet spots” – Spring Gully/Fairview and the Undulla Nose

Australia’s largest 2P reserves base

• Large CSG reserves position

• Well developed resource base

-

5,000

10,000

15,000

20,000

25,000

30,000

PJ

Ramp and Tail Gas Train 2 Train 1

3C 2C 3P 2P

Estimated Requirements

QCLNG GSA Domestic Gas Origin Contract

Bowen Basin

Undulla Nose

Spring Gully / Fairview

Note: Some of APLNG’s CSG reserves and resources are subject to reversionary rights. For further information, refer to Origin’s Management Discussion & Analysis for the half year ended 31 December 2011 released to the ASX on 23 February 2012. This reserve and resource data has been prepared to be consistent with the Petroleum Resources Management System 2007 guidelines published by the Society of Petroleum Engineers. 10 |

APLNG permits

Surat Basin

For

per

sona

l use

onl

y

Australia Pacific LNG has world leading operators

UPSTREAM • Operated by Origin

• Over 15 years’ CSG production experience in Australia

• Complemented by ConocoPhillips’ 25 years of CSG experience

DOWNSTREAM • Operated by ConocoPhillips

• Over 40 years’ LNG production experience

• Using ConocoPhillips’ Optimised Cascade® technology licence, Bechtel has delivered 8 LNG trains globally

11 |

Drilling Gathering Gas & water facilities

Electrification Water disposal/ treatment

Pipelines

LNG Plant, Tanks and LNG Terminal

For

per

sona

l use

onl

y

Upstream is on budget and schedule for Train 1 start-up in mid-2015

12 |

Milestones Date (CY)

EPC pipeline contract awarded to MCJV July 2011

First Savanna hybrid coil drill rig operational July 2011

Pipeline manufacture 2011 and 2012

Second Savanna hybrid coil drill rig operational early 2012

Powerlink switchyard contractor mobilised to Condabri North May 2012

Condabri construction camp occupied June 2012

First compressor train arrived and two gas processing modules shipped from Thailand

mid-2012

Pipeline welding commences* Q3 2012

3rd and 4th drill rigs mobilised end 2012

Mechanical completion of first gas processing plant mid-2013

Main pipeline completion early 2014

Narrows Crossing pipeline completion mid-2014

Train 1 electrification complete mid-2014

Train 1 gas processing plants complete late 2014

First gas to LNG Train 1 early 2015

* Schedule updated. There has been no change to the critical path as a result of this schedule change.

For

per

sona

l use

onl

y

13 |

The drilling rate will increase as 3rd and 4th rigs are mobilised over the coming months

(1) Excludes domestic gas sales and pre-start up LNG sales to BG. (2) Exploration & Appraisal wells and Spring Gully development wells take longer than Phase 1 Development wells due to different well

design. Above table excludes injection bores, water bores & water rigs.

• Around 1,100 operated wells to be drilled by APLNG to support ramp requirements for two trains (Phase 1)

• The key areas for drilling these Phase 1 operated wells are Talinga, Spring Gully, Condabri and Combabula

• Land access managed with 6-12 months of access agreements in place ahead of drilling

• Non-operated gas comprises around 200 TJ/day(1) (or 15%) of the estimated 1,400 TJ/day(1) gas required for a two-train project

• Current operated well deliverability is over 1 TJ per well per day on average across the Talinga and Spring Gully developments

• Phase 1 average drilling rate to date is 5.2 days/well

• The drilling activity is expected to increase as additional rigs are mobilised and commissioning is completed over coming months. A third hybrid coil drilling rig will be mobilised in Q3 CY2012 and a fourth rig is due to be mobilised before the CY 2012 year end

Development rigs and days/well

Max Wells per year(2)

Max new wells by mid-2015

3 rigs at 5.2 days/well 210 630

4 rigs at 5.2 days/well 280 842

4 rigs at 4.6 days/well 320 952

4 rigs at 4.0 days/well 365 1,100

4 rigs at 3.5 days/well 420 1,250

5 rigs at 4.6 days/well 400 1,200

5 rigs at 3.5 days/well 525 1,575

Average well production

TJ/day Q1 CY2012

Talinga 1.5 TJ/day

Spring Gully* 0.7 TJ/day

* Spring Gully production currently limited whilst recovering from water capacity restrictions during recent flooding events. The quarterly average per well production rate was approximately 1 TJ/d prior to capacity restrictions

For

per

sona

l use

onl

y

The gathering construction camp at Condabri is now occupied by contractors

Condabri Gathering Camp

Gathering

• Leighton Contractors and East Coast Pipelines contracted to deliver gathering system

• Gathering construction camp is now occupied by contractors, as scheduled

Gazebo at Condabri Gathering Camp

14 |

For

per

sona

l use

onl

y

APLNG’s gas and water facilities are simple and repeatable

15 |

Gas processing facilities

• 7 new gas processing facilities required for project

• Modularisation and improved design has significantly reduced footprint

• Fabrication of gas plant modules is well underway

• >90% offsite fabricated/pre-assembled, by tonnage

• First compressor train arrived and two gas processing modules shipped from Thailand in mid-2012, as scheduled

• Laing O’Rourke contracted to construct the facilities

• Site preparation works have commenced

Water – brine treatment skid

Construction of the new gas processing and water treatment facilities is on track to commence in mid-2012

85 TJ/day Gas Processing Facility Train

Water treatment plants

• 2 new water treatment facilities required for project

• Leighton Contractors to construct the facilities

• Site preparation works have commenced

For

per

sona

l use

onl

y

16 |

Pipeline welding is due to commence in the September 2012 quarter …

Pipelines

• EPC pipeline contract awarded to McConnell Dowell, Consolidated Contracting Co. joint venture (MCJV) in July 2011

• Line pipe awarded to MetalOne in Japan; first delivery made in January 2012

• Pipeline land access arrangements progressing on schedule

• Pipeline materials are currently held at Callide storage yard with welding to commence in September Quarter 2012

• APLNG and QCLNG collaboration on Narrows Crossing behind schedule, but no impact to critical path

The Narrows Crossing (QCLNG site)

Electrification

• Train 1 electrification contracts awarded to Powerlink and on schedule

• Powerlink to deliver electrification to water treatment facilities and gas processing plants

• Mobilisation of contractors to site and early preparation works are underway

• The Central and Orana regions electrification connections continue to progress on schedule

• Powerlink’s switchyard contractor mobilised to Condabri North in mid-May 2012

… and Powerlink continues to progress electrification activities

For

per

sona

l use

onl

y

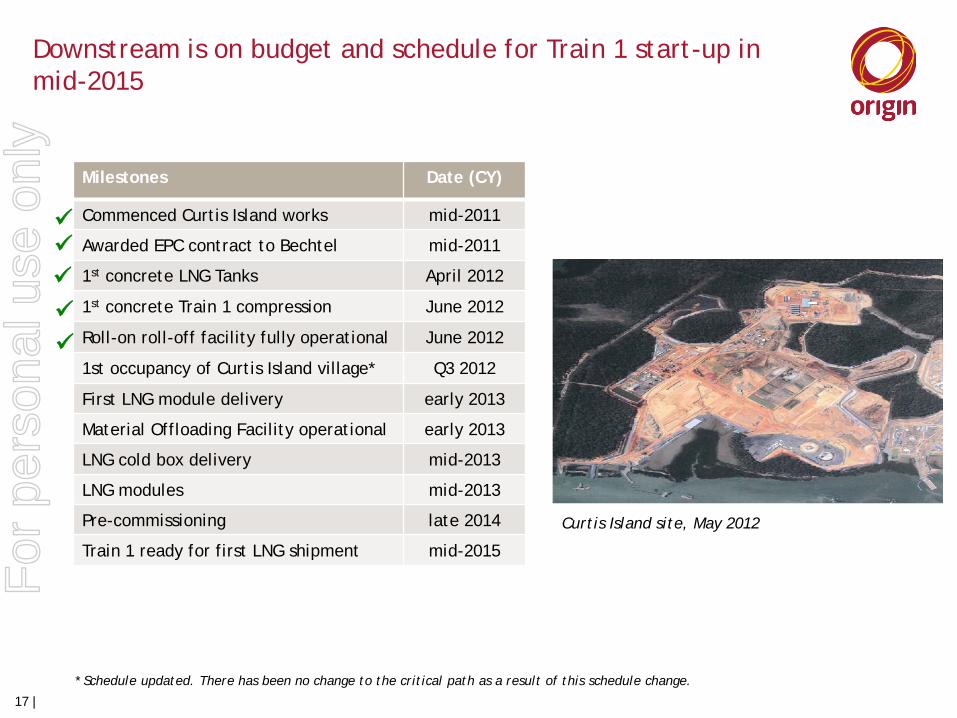

Downstream is on budget and schedule for Train 1 start-up in mid-2015

Milestones Date (CY)

Commenced Curtis Island works mid-2011

Awarded EPC contract to Bechtel mid-2011

1st concrete LNG Tanks April 2012

1st concrete Train 1 compression June 2012

Roll-on roll-off facility fully operational June 2012

1st occupancy of Curtis Island village* Q3 2012

First LNG module delivery early 2013

Material Offloading Facility operational early 2013

LNG cold box delivery mid-2013

LNG modules mid-2013

Pre-commissioning late 2014

Train 1 ready for first LNG shipment mid-2015

17 |

Curtis Island site, May 2012

* Schedule updated. There has been no change to the critical path as a result of this schedule change.

For

per

sona

l use

onl

y

Downstream operations on the mainland and Curtis Island are progressing as planned

April 2012

LNG tank foundations Curtis Island Camp

Mainland – temporary materials offloading facility

Mainland – aggregate loading onto barge

Curtis Island – Material Offloading Facility marine works

Curtis Island – cement batch plant 18 |

For

per

sona

l use

onl

y

Bechtel is responsible for all activity on Curtis Island (engineering, procurement, construction) under a fixed price contract … Engineering and Procurement

• Engineering and procurement remain on schedule

• The module yard is being prepared for receiving material in Indonesia (first deliveries were received in June 2012) with the module site management team mobilised in June 2012

• Delivery of the compressors, which is a critical path item, is on schedule

April 2012

LNG tank foundations Curtis Island Camp

Construction

• Pouring of the Train 1 foundations commenced in June 2012

• Construction of both LNG tanks are underway and the tank sub-contractor is progressing on schedule

• Roll-On Roll-Off facilities on the Fisherman Landing and Curtis Island sites are complete and now fully operational

• Material Off-loading Facility construction is progressing as planned to support delivery of compressors and other components in early 2013

… and remains on track to deliver the downstream scope of the project 19 |

For

per

sona

l use

onl

y

Australia Pacific LNG is making a significant economic contribution to Queensland and creating thousands of new jobs …

• Currently creating employment for around 4,000 Queenslanders and will create 6,000 construction jobs and a further 1,000 jobs for ongoing operations

• More than 650 land access agreements in place across exploration, development and pipeline permits

• Independently chaired community consultative committees operating in regional centres

• Skills Queensland program to enable farmers to support CSG infrastructure on their land

• Program to address housing affordability in regional communities commenced

• Development drilling using Australian first minimal disturbance lease construction

… while remaining committed to community engagement, education and limiting environmental impacts

20 |

For

per

sona

l use

onl

y

Risk mitigation plans and controls are in place …

21 |

… to minimise financial and operational risks to the project

• Project operators are world class operators in their fields • Industry leaders engaged for all key contracts and services of the project • Integration and interfacing team established to drive alignment between

different project components • Significant front-end loading conducted prior to FID

Execution risk

• Key contracts for upstream pipeline and downstream LNG plant are predominantly fixed price, lump sum

• All major contracts are awarded • Offshore pre-fabrication & modularisation to reduce field construction hours • Appropriate contingency built into cost schedules • Dedicated commissioning team on Curtis Island

Project cost overruns & delays

• Key downstream and pipeline contracts are predominantly fixed price with labour risk passed on to the contractor

• Bechtel is managing three projects on Curtis Island and should be well placed to manage resources between projects to control costs

• Existing workforce and new infrastructure to support a growing population • Large degree of modularisation reducing construction workforce • Established upstream contractors selected with existing labour capability

Insufficient labour for project execution

• Extensive community engagement to provide accurate facts and counter misinformation in the current public debate on CSG

• Working closely and collaboratively with landowners and farmers • Strong government support on environmental and land access issues

Environment & community concerns

Risk Response

For

per

sona

l use

onl

y

Project capital costs remain in line with FID1 estimates …

• Estimated capital expenditure (project and non-project costs) from July 2011 until start of up Train 2 in early 2016 includes: - A$23 billion(1) project costs – in line with US dollar estimates at FID1(2) - non-project related costs(3), which will be substantially offset by revenues from future early

gas sales including domestic sales and sales to other LNG projects • Of the A$23 billion estimated project costs:

- over two thirds are denominated in AUD, with the balance primarily in USD - two thirds are fixed or unit rate contracts, the balance includes some floating rate

contracts and owners costs • A$18 billion of contracts have been awarded by APLNG to date • APLNG cost estimates announced in July 2011 already allowed headroom for cost increases in

the period to first LNG in respect of specific non-operated upstream gas fields. As a result, the recent cost increases announced by other LNG project participants are not expected to materially impact APLNG’s existing cost estimates for its two-train project assessed against information currently available from the other projects - non-operated costs are approximately 12% of APLNG’s total expenditure

(1) Based on Bloomberg forward foreign exchange rates as at 21 June 2012. (2) US$20 billion (which included US$2.5 billion of contingency) equivalent to A$23 billion at FID1 in July 2011, based on Bloomberg forward

exchange rates as at 1 December 2010. (3) Non-project costs include costs associated with the domestic operations, pre-LNG operating and maintenance costs and costs associated with

the supply of gas to third party LNG projects. (4) AUD movement not evident due to rounding to the nearest AUD billion.

… with movements in foreign exchange rates decreasing the cost quoted in AUD(4), and increasing the cost quoted in USD

22 |

For

per

sona

l use

onl

y

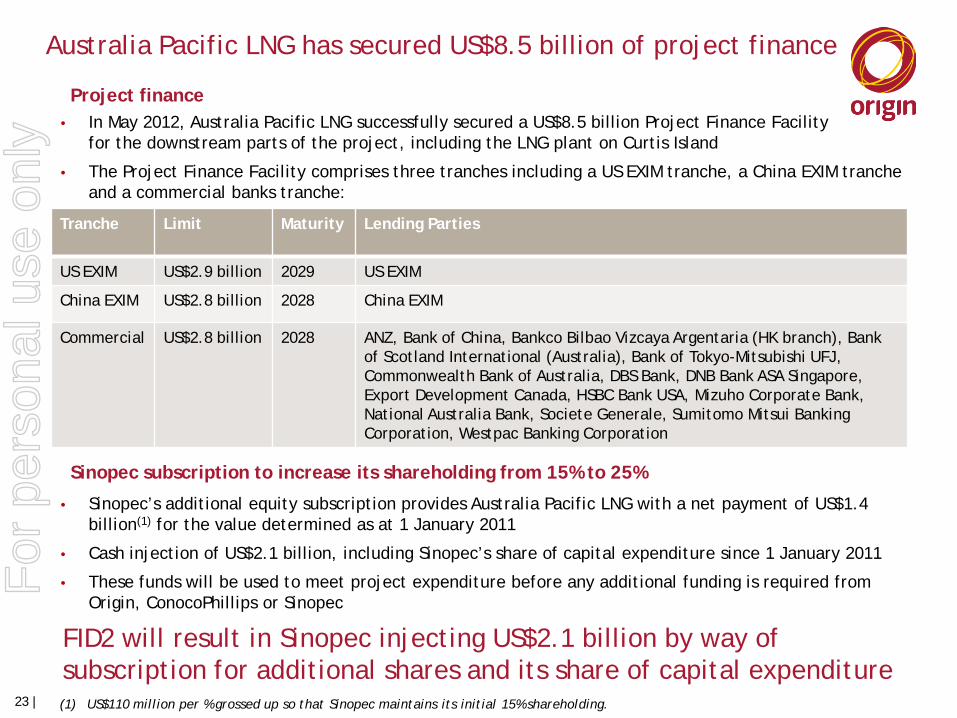

Australia Pacific LNG has secured US$8.5 billion of project finance

• In May 2012, Australia Pacific LNG successfully secured a US$8.5 billion Project Finance Facility for the downstream parts of the project, including the LNG plant on Curtis Island

• The Project Finance Facility comprises three tranches including a US EXIM tranche, a China EXIM tranche and a commercial banks tranche:

Tranche Limit Maturity Lending Parties

US EXIM US$2.9 billion 2029 US EXIM

China EXIM US$2.8 billion 2028 China EXIM

Commercial US$2.8 billion 2028 ANZ, Bank of China, Bankco Bilbao Vizcaya Argentaria (HK branch), Bank of Scotland International (Australia), Bank of Tokyo-Mitsubishi UFJ, Commonwealth Bank of Australia, DBS Bank, DNB Bank ASA Singapore, Export Development Canada, HSBC Bank USA, Mizuho Corporate Bank, National Australia Bank, Societe Generale, Sumitomo Mitsui Banking Corporation, Westpac Banking Corporation

• Sinopec’s additional equity subscription provides Australia Pacific LNG with a net payment of US$1.4 billion(1) for the value determined as at 1 January 2011

• Cash injection of US$2.1 billion, including Sinopec’s share of capital expenditure since 1 January 2011

• These funds will be used to meet project expenditure before any additional funding is required from Origin, ConocoPhillips or Sinopec

Project finance

Sinopec subscription to increase its shareholding from 15% to 25%

FID2 will result in Sinopec injecting US$2.1 billion by way of subscription for additional shares and its share of capital expenditure

23 | (1) US$110 million per % grossed up so that Sinopec maintains its initial 15% shareholding.

For

per

sona

l use

onl

y

Origin has sufficient liquidity to fund its share of APLNG

• Origin's remaining funding requirement(1) for its 37.5% share of APLNG for the period from 1 July 2012 to first production of both LNG trains is approximately A$3.6 billion

• Origin has around A$4.6 billion(2) of undrawn debt facilities and cash, which is more than sufficient to fund its commitments to APLNG, meet short-term maturing debt obligations and maintain a prudent liquidity buffer

• Some of Origin’s debt facilities mature within the period to first gas from the second train and will be replaced as required

• Any dilution of Origin’s interest in APLNG below 37.5% will improve this funding position

• Origin and ConocoPhillips will commence a joint process to dilute their current 37.5% respective interests in APLNG

• Origin is looking to retain around a 30% stake in APLNG over the longer term

(1) After US$8.5 billion of project finance and payment of Sinopec’s additional equity subscription monies to APLNG. 37.5% interest assumes Sinopec’s 25% subscription completes.

(2) As at 31 May 2012.

0

500

1,000

1,500

2,000

2,500

FY20

12

FY20

13

FY20

14

FY20

15

FY20

16

FY20

17

FY20

18

FY20

19

FY20

20

FY20

21

FY20

22

FY20

22+

A$ m

illio

n

Origin Debt & Bank Guarantee Maturity Profile as at 31 May 2012

Loan & Bank Guarantees - UndrawnLoans & Bank Guarantees - DrawnUSPP & Hybrids

The export project is now further de-risked, supporting further dilution of Origin’s equity interest in APLNG

24 |

For

per

sona

l use

onl

y

… delivering significant value to Origin shareholders

Australia Pacific LNG is on track to deliver first LNG by 2015 …

Commercialisation of Australia’s largest 2P CSG reserves at international oil-linked prices

Strong and aligned shareholder group each with strong funding capacity

ConocoPhillips-Bechtel experience in developing LNG facilities using Optimised Cascade® Process

Marketing completed on full two-train project leveraging strong growth in Asian energy markets

Appropriate and effective risk mitigation plans

Successful history of working sustainably with communities

25 |

For

per

sona

l use

onl

y

Thank you

For more information

Kylie Springall Group Manager, Investor Relations Email: [email protected] Office: +61 2 8345 5288 Mobile: + 61 400 477 393 www.originenergy.com.au

26 |

For

per

sona

l use

onl

y