tma compliance bulletin - The Mortgage Alliance · tma compliance bulletin {REDEFINING THE MORTGAGE...

10

tma compliance bulletin PRIVATE AND CONFIDENTIAL {REDEFINING THE MORTGAGE CLUB} 8th Edition 2017 our experience is vast. our knowledge is great. we’ve been around for a long time and we will share all we know with you.

Transcript of tma compliance bulletin - The Mortgage Alliance · tma compliance bulletin {REDEFINING THE MORTGAGE...

tmacompliancebulletin

PRIVATE AND CONFIDENTIALREDEFINING THE MORTGAGE CLUB

8th Edition 2017

our experience is vastour knowledge is great wersquove been around fora long time and we willshare all we know with you

comp

lianc

e

REDEFINING THE MORTGAGE CLUB

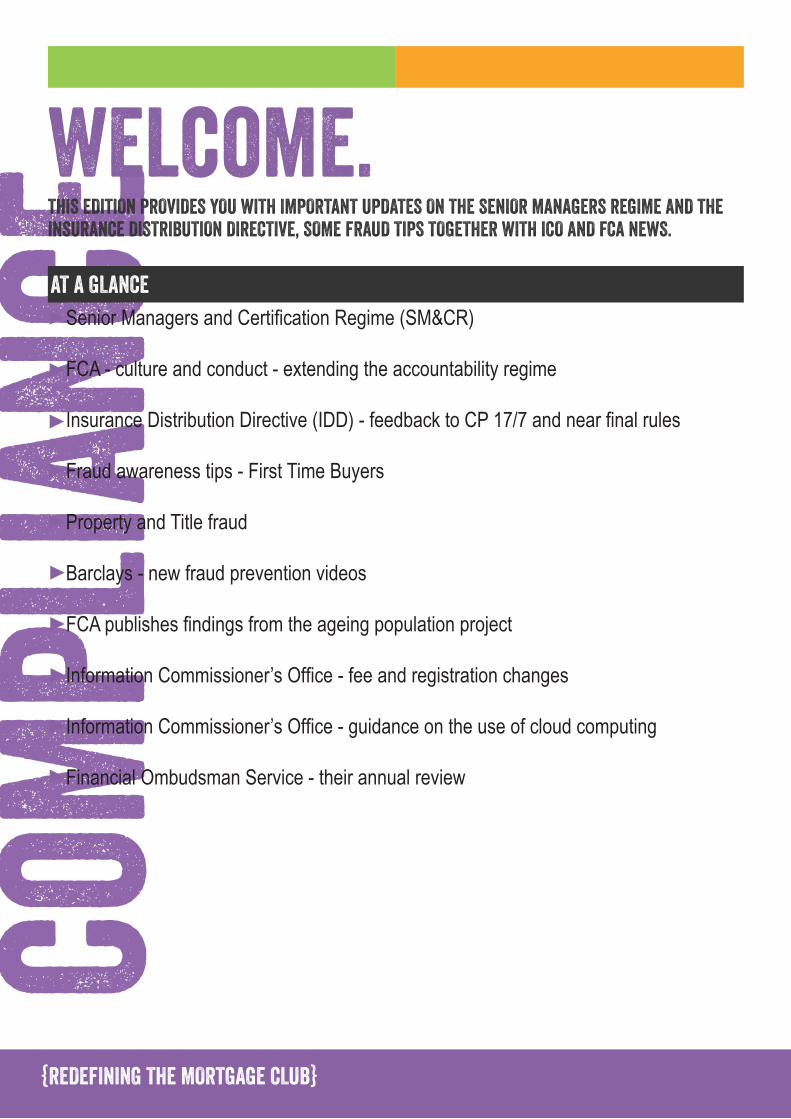

THIS EDITION PROVIDES YOU WITH IMPORTANT UPDATES ON THE SENIOR MANAGERS REGIME AND THE INSURANCE DISTRIBUTION DIRECTIVE SOME FRAUD TIPS TOGETHER WITH ICO AND FCA NEWS

welcomeAT A GLANCE

Senior Managers and Certification Regime (SMampCR)

FCA - culture and conduct - extending the accountability regime

Insurance Distribution Directive (IDD) - feedback to CP 177 and near final rules

Fraud awareness tips - First Time Buyers

Property and Title fraud

Barclays - new fraud prevention videos

FCA publishes findings from the ageing population project

Information Commissionerrsquos Office - fee and registration changes

Information Commissionerrsquos Office - guidance on the use of cloud computing

Financial Ombudsman Service - their annual review

PRIVATE AND CONFIDENTIAL

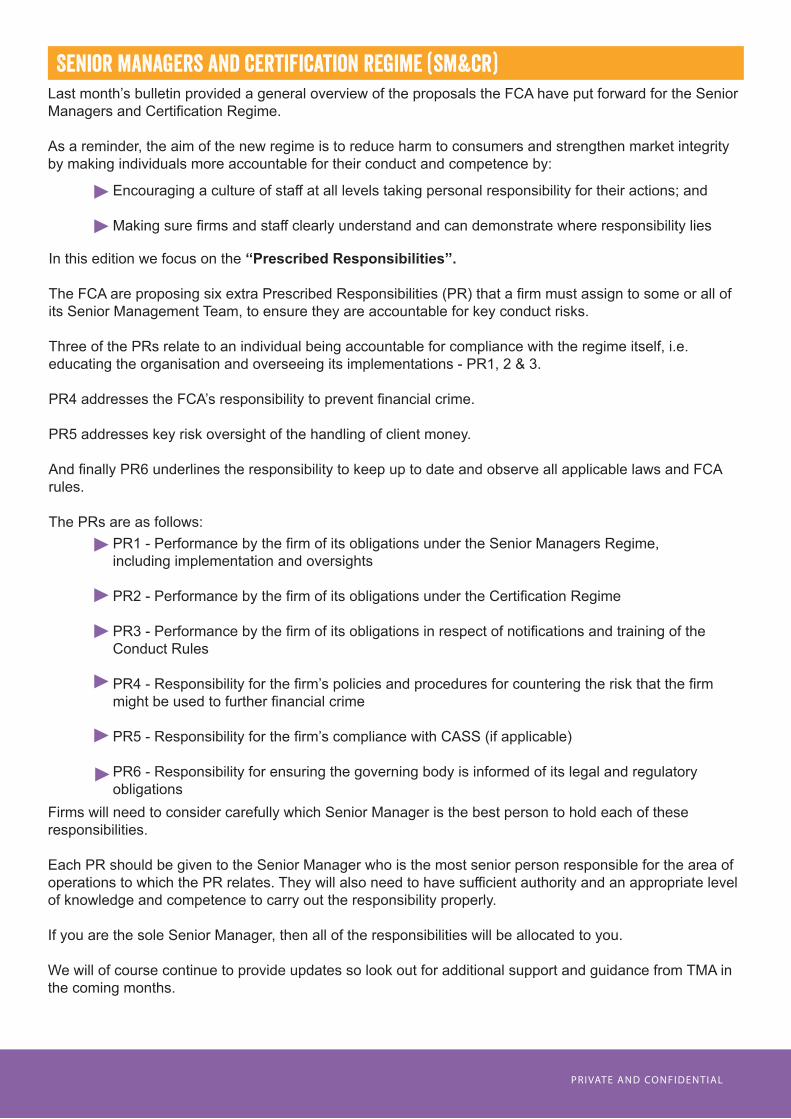

Senior managers and certification regime (smampcr) Last monthrsquos bulletin provided a general overview of the proposals the FCA have put forward for the Senior Managers and Certification Regime

As a reminder the aim of the new regime is to reduce harm to consumers and strengthen market integrity by making individuals more accountable for their conduct and competence by

Encouraging a culture of staff at all levels taking personal responsibility for their actions and

Making sure firms and staff clearly understand and can demonstrate where responsibility lies

In this edition we focus on the lsquolsquoPrescribed Responsibilitiesrsquorsquo

The FCA are proposing six extra Prescribed Responsibilities (PR) that a firm must assign to some or all of its Senior Management Team to ensure they are accountable for key conduct risks

Three of the PRs relate to an individual being accountable for compliance with the regime itself ie educating the organisation and overseeing its implementations - PR1 2 amp 3

PR4 addresses the FCArsquos responsibility to prevent financial crime

PR5 addresses key risk oversight of the handling of client money

And finally PR6 underlines the responsibility to keep up to date and observe all applicable laws and FCA rules

The PRs are as followsPR1 - Performance by the firm of its obligations under the Senior Managers Regime including implementation and oversights

PR2 - Performance by the firm of its obligations under the Certification Regime

PR3 - Performance by the firm of its obligations in respect of notifications and training of the Conduct Rules

PR4 - Responsibility for the firmrsquos policies and procedures for countering the risk that the firm might be used to further financial crime

PR5 - Responsibility for the firmrsquos compliance with CASS (if applicable)

PR6 - Responsibility for ensuring the governing body is informed of its legal and regulatory obligations

Firms will need to consider carefully which Senior Manager is the best person to hold each of these responsibilities

Each PR should be given to the Senior Manager who is the most senior person responsible for the area of operations to which the PR relates They will also need to have sufficient authority and an appropriate level of knowledge and competence to carry out the responsibility properly

If you are the sole Senior Manager then all of the responsibilities will be allocated to you

We will of course continue to provide updates so look out for additional support and guidance from TMA in the coming months

REDEFINING THE MORTGAGE CLUB

comp

lianc

efca - culture and conflict - extending and accountability regime

insurance distribution directive (IDD)-feedback to cp 177 and near final rules

It is our understanding that a new technical paper will follow soon detailing timescales and templates that will be of relevance to the new regime

The deadline for feedback to the FCA has now passed (3 November 2017) but firms should still read the Consultation Paper here

Following on from the opening article Jonathan Davidson who is Director of Supervision at the FCA delivered a speech in London recently - he was there to talk about culture and conduct in financial services through the lens of the Senior Managers and Certification Regime or as he likes to call it the lsquolsquoaccountability regimersquorsquo

The speech focused on why culture is so important and why they are introducing the accountability regime

Here are the key points

Cultural change requires individual engagement and accountability

Culture may not be measurable but if it is manageable for example through incentives and governance

They want consumers to understand the FCArsquos expectations around culture in firms and feel able to speak up when standards arenrsquot met

An ethical culture can be more powerful than one based solely on financial incentives

Please read the speech in full here

This Policy Statement (PS) sets out the FCArsquos response to the feedback they received for the first of three Consultation Papers on the IDD

The UK is required to comply with the IDD by 23 February 2018 This will require changes to your advice process procedures and policies - for all insurance sales

Some key changes are summarised below

The IDD requires all insurance distributors and their employees to have the appropriate knowledge and ability to perform their roles This must be supported by a minimum of fifteen hours of continuing professional training or development (CPD) in each twelve months This will be extended to insurance intermediaries and they will need to maintain records of employee competence and CPD

The IDD makes a number of changes to the pre contract disclosures ie what firms might know as lsquolsquoinitial disclosurersquorsquo that firms are required to make such as disclosing whether they are an insurer or an intermediary whether or not they provide advice and whether they act for the customer or insurer

The IDD makes a number of changes for advised sales ie

There is a new explicit requirement that all contracts proposed must be consistent with customerrsquos demands and needs - this includes both advised and non-advised sales and

There is a requirement that firms who advise must provide a personalised recommendation explaining why the product recommended best meets the customerrsquos needs

PRIVATE AND CONFIDENTIALPRIVATE AND CONFIDENTIAL

Whilst these new rules build on pre-existing provisions in ICOBS firms should take the opportunity to re visit their sales process in particular the demands and needs assessment and the extent to which recommendations are made relate back to established customer needs

The IDD requires changes to the existing disclosures covering conflicts of interest for an intermediary - it will also introduce new requirements to disclose information concerning the firms remuneration ie intermediaries must disclose the nature of their remuneration in relation to the insurance contract and whether they work on the basis of fee commission or a combination of both

To clarify these are lsquolsquonear finalrsquorsquo rules simply because they are still under discussion at the European Commission and as the FCA need time to prepare this is their best guess of what the rules will currently look like

Final rules are likely to be made in January 2018 in time for firms to comply by 23 February 2018

Next steps

Start to review your existing processes and assess whether they will fit in with the new regime

Firms should read the third Consultation Paper and any feedback must be with the FCA by 25 November 2017

As usual please look out for support and guidance from TMA in the coming months

fraud awareness tips - first time buyersAs an adviser you will be aware of the need to be diligent in the fight against financial crime Failure to do so is not only contrary to FCA expectations (see also our earlier comments on the specific responsibility PR4 under the SMampCR) but your livelihood could be placed at risk

To help mitigate the possibility that your business is used to conduct mortgage fraud we have created a short summary guide that specifically focuses on First Time Buyers and the risks that they may represent Analysis shows that this customer group presents the highest chance of fraud being perpetrated via your business

The guide contains tips and suggestions of the types of the basic checks that you can make when processing a mortgage application for this client type

For more information on Fraud awareness for first time buyers click here

property and title fraudRecorded incidents of fraud are rising with fraudsters continuing to target the properties of both individuals and companies These attacks often include the presentation of forged registration or identity documents as part of HM Land Registry applications HM Land Registry and the Law Society wish to bring these matters to the attention of the public and raise awareness

This joint Law Society and HM Land Registry document provides a practical guide for solicitors on some of the indicators of potential fraud in land transactions and registration of title It is intended as a reference point for the legal profession to be of assistance in recognising potential fraud but not to set a regulatory framework

In view of the rapidly evolving nature of title fraud it should be recognised that this document cannot cover all fraud scenarios and types of fraud threat affecting title to land

Whilst it is aimed at solicitors contained within are several case examples which will be of interest eg

REDEFINING THE MORTGAGE CLUB

comp

lianc

eA criminal gang targeted high value residential properties in the London area being marketed for rent The landlord only had one notification address (that is their address for service) recorded on the proprietorship register and that address was the rental property as opposed to an address where they lived or worked

The landlord let the property to the fraudsters and received six monthsrsquo rent in advance which gave the fraudsters possession of the property and time to commit the fraud

The organised fraud gang successfully sold the property for pound13m although the purchase was not registered by HM Land Registry The registered title fraud was prevented because of certain fraud indicators In this case indicators were

The owner

Was a sole owner

Had one address for service which was the rental property

Was long established having owned the property for over 20 years

The property was vulnerable because it was

Unmortgaged

Of high value

Not lived in or not occupied by the owner

Please click here for the full paper

barclays - new fraud prevention videosHave you ever wondered how valuable your social media data is to a fraudster Or how someone might try to relieve you of your account pin number

With the kind permission of Barclays we have collated a collection of video links which briefly explain the tricks used by fraudsters to try and obtain personal data which could later be used in an identity fraud

Please take time to view them (remembering to turn on your sound) - they may help you not to becone a victim of fraud

View some of the collection here - the links will take you to YouTube and are usually no more than a minute long

Digital safety - PIN protection

Digital safety - personal data

Digital safety - hacked emails

Digital safety - passwords

The phone scam

Cyber crime

PRIVATE AND CONFIDENTIAL

fca publishes findings from the ageing population projectThe FCA has recently published an lsquolsquoOccasional Paperrsquorsquo outlining the findings from a project that explored how the ageing population would impact the Financial Services industry

The FCA launched the Ageing Population Project in February 2016 to explore how older people use financial services and products The paper reviews the public policy implications of having a population which is getting older and the resulting impact on financial services The document also includes actions which the FCA and industry could take to better support older people

This publication is the first of a series of documents which the FCA will publish as part of their focus on consumers including an overarching strategy lsquoApproach to Consumersrsquo which will be published later this Autumn

When reviewing the treatment of older people the FCA found that there are risks that their financial services needs are not being fully met which can result in exclusion poor customer outcomes and potential harm The issues appear to be driven by a range of interrelated causes These include policies and controls that are not designed around consumer needs and unintended consequences of product and service design

While older consumers are not necessarily vulnerable they are more likely than other groups to experience vulnerability at some point (whether temporarily or permanently)

This is particularly the case for those aged over 75 In line with the aims of the FCArsquos Mission this paper has focused on the issues where regulation and financial services firms can play a role and make a difference

There is scope for financial services firms to do more The FCA has set out some ideas for firms to consider in ways that fit their business models such as looking at product and service design customer support and reviewing and adapting strategies

The paper also explores a range of issues including older consumersrsquo engagement with retail banking third party access and planning ahead later life lending and long term care

These issues will require action from multiple parties to address over time In many cases solutions do not lie within the remit of any one party - including the FCA or the regulated firms that it supervises

The FCA has considered who might be best placed to address the gaps to improve financial markets for older people including other bodies who might be better placed to take forward topics outside the FCArsquos remit

The FCA anticipates a further review in three to five years of how the financial services industry is adapting to meet the needs of older consumers

The full paper can be found here

information commissionerrsquos office - fee and registration changesAs we count down to the General Data Protection Regulation (GDPR) taking effect next May the ICO wanted to clarify how the fees that lsquolsquodata controllersrsquorsquo have to pay to them are changing

Under the current Data Protection Act (DPA) organisations that process personal information are required to notify with the ICO as data controllers

This involves explaining what personal data you collect and what you do with it You are also required to pay a notification fee based on your size of either pound35 or pound500 These fees are used to fund most of the ICOrsquos work

comp

lianc

e

REDEFINING THE MORTGAGE CLUB

When the new data protection legislation comes into effect next year there will no longer be a requirement to notify the ICO in the same way However a provision in the Digital Economy Act means it will remain a legal requirement for data controllers to pay the ICO a data protection fee These fees will be used to fund the ICOrsquos data protection work As now any money the ICO receives in fines will be passed directly back to the Government

how much will data controllers have to payThe Digital Economy Act paves the way for a new funding system for the ICO The amount of the data protection fee is being developed by the ICOrsquos sponsoring department the Department for Digital Culture Media and Sport (DCMS) in consultation with the ICO and representatives of those likely to be affected by the change

The final fees will be approved by Parliament

The new system will aim to make sure the fees are fair and reflect the relative risk of the organisationrsquos processing of personal data The size of the data protection fee will still be based on the organisationrsquos size and turnover and will also take into account the amount of personal data it is processing

The current draft proposal is a three tier system which will differentiate between small and big organisations and also how much personal data an organisation is processing The aim is to keep the system as simple as possible so that organisations will easily be able to categorise themselves

They expect to know more by the end of the year and will communicate to data controllers once they do

When will the new data protection fee system start

The new model will go live on 1 April 2018

Irsquom due to renew shortly should I still go ahead with this

Organisations should continue to renew their notification as usual and it is still a criminal offence to not notify if an organisation needs to Once they know more about the new fees they will be telling all organisations about the changes and what they need to do

So until the news fees come in it is very much business as usual - so no excuses for not notifying

information commissionerrsquos office - guidance on the use of cloud computingDoes your organisation process personal data in the cloud If so the ICO has produced some useful cloud computing guidance here

financial ombudsman service - their annual reviewThe Financial Ombudsman Service were set up by Parliament to resolve individual complaints between financial businesses and their customers - fairly reasonably quickly and as informally as possible They can look into problems involving most types of money matters - from payday loans to pensions pet insurance to PPI If a business and their customer canrsquot resolve a problem themselves they can step in to sort things out Independent and unbiased theyrsquoll get to the heart of whatrsquos happened - and reach a fair pragmatic answer that helps both sides move on

If they think the business has acted fairly - or therersquos just been a misunderstanding - theyrsquoll explain how things stand But if someonersquos been treated unfairly theyrsquoll use their powers to put things right

That could mean telling a business to do anything from amending a credit file to reducing loan repayments or from settling an insurance claim to correcting a pension

PRIVATE AND CONFIDENTIAL

Since they were set up theyrsquove seen the real impact of financial concerns complaints and disputes on people from all sorts of backgrounds and livelihoods Theyrsquore committed to sharing their insight and experience to encourage fairness and confidence in financial services

Their annual review is always an opportunity to look forward as well as back and this one is no exception

The full review can be found here

Thank you for taking the time to read this bulletinWe hope you found it useful

Wersquod really appreciate any feedback you haveEmail hellotmaclubcom

Would you like to try a new Compliance PackageFor more details email hellotmaclubcom or click here to see our compliance

proposition

Want to receive our compliance bulletins by emailEmail marketingtmaclubcom

tell us your thoughts

you have to learn the rules of the gamethen play better than anyone elserdquoalbert einstein

ldquo

comp

lianc

e

REDEFINING THE MORTGAGE CLUB

THIS EDITION PROVIDES YOU WITH IMPORTANT UPDATES ON THE SENIOR MANAGERS REGIME AND THE INSURANCE DISTRIBUTION DIRECTIVE SOME FRAUD TIPS TOGETHER WITH ICO AND FCA NEWS

welcomeAT A GLANCE

Senior Managers and Certification Regime (SMampCR)

FCA - culture and conduct - extending the accountability regime

Insurance Distribution Directive (IDD) - feedback to CP 177 and near final rules

Fraud awareness tips - First Time Buyers

Property and Title fraud

Barclays - new fraud prevention videos

FCA publishes findings from the ageing population project

Information Commissionerrsquos Office - fee and registration changes

Information Commissionerrsquos Office - guidance on the use of cloud computing

Financial Ombudsman Service - their annual review

PRIVATE AND CONFIDENTIAL

Senior managers and certification regime (smampcr) Last monthrsquos bulletin provided a general overview of the proposals the FCA have put forward for the Senior Managers and Certification Regime

As a reminder the aim of the new regime is to reduce harm to consumers and strengthen market integrity by making individuals more accountable for their conduct and competence by

Encouraging a culture of staff at all levels taking personal responsibility for their actions and

Making sure firms and staff clearly understand and can demonstrate where responsibility lies

In this edition we focus on the lsquolsquoPrescribed Responsibilitiesrsquorsquo

The FCA are proposing six extra Prescribed Responsibilities (PR) that a firm must assign to some or all of its Senior Management Team to ensure they are accountable for key conduct risks

Three of the PRs relate to an individual being accountable for compliance with the regime itself ie educating the organisation and overseeing its implementations - PR1 2 amp 3

PR4 addresses the FCArsquos responsibility to prevent financial crime

PR5 addresses key risk oversight of the handling of client money

And finally PR6 underlines the responsibility to keep up to date and observe all applicable laws and FCA rules

The PRs are as followsPR1 - Performance by the firm of its obligations under the Senior Managers Regime including implementation and oversights

PR2 - Performance by the firm of its obligations under the Certification Regime

PR3 - Performance by the firm of its obligations in respect of notifications and training of the Conduct Rules

PR4 - Responsibility for the firmrsquos policies and procedures for countering the risk that the firm might be used to further financial crime

PR5 - Responsibility for the firmrsquos compliance with CASS (if applicable)

PR6 - Responsibility for ensuring the governing body is informed of its legal and regulatory obligations

Firms will need to consider carefully which Senior Manager is the best person to hold each of these responsibilities

Each PR should be given to the Senior Manager who is the most senior person responsible for the area of operations to which the PR relates They will also need to have sufficient authority and an appropriate level of knowledge and competence to carry out the responsibility properly

If you are the sole Senior Manager then all of the responsibilities will be allocated to you

We will of course continue to provide updates so look out for additional support and guidance from TMA in the coming months

REDEFINING THE MORTGAGE CLUB

comp

lianc

efca - culture and conflict - extending and accountability regime

insurance distribution directive (IDD)-feedback to cp 177 and near final rules

It is our understanding that a new technical paper will follow soon detailing timescales and templates that will be of relevance to the new regime

The deadline for feedback to the FCA has now passed (3 November 2017) but firms should still read the Consultation Paper here

Following on from the opening article Jonathan Davidson who is Director of Supervision at the FCA delivered a speech in London recently - he was there to talk about culture and conduct in financial services through the lens of the Senior Managers and Certification Regime or as he likes to call it the lsquolsquoaccountability regimersquorsquo

The speech focused on why culture is so important and why they are introducing the accountability regime

Here are the key points

Cultural change requires individual engagement and accountability

Culture may not be measurable but if it is manageable for example through incentives and governance

They want consumers to understand the FCArsquos expectations around culture in firms and feel able to speak up when standards arenrsquot met

An ethical culture can be more powerful than one based solely on financial incentives

Please read the speech in full here

This Policy Statement (PS) sets out the FCArsquos response to the feedback they received for the first of three Consultation Papers on the IDD

The UK is required to comply with the IDD by 23 February 2018 This will require changes to your advice process procedures and policies - for all insurance sales

Some key changes are summarised below

The IDD requires all insurance distributors and their employees to have the appropriate knowledge and ability to perform their roles This must be supported by a minimum of fifteen hours of continuing professional training or development (CPD) in each twelve months This will be extended to insurance intermediaries and they will need to maintain records of employee competence and CPD

The IDD makes a number of changes to the pre contract disclosures ie what firms might know as lsquolsquoinitial disclosurersquorsquo that firms are required to make such as disclosing whether they are an insurer or an intermediary whether or not they provide advice and whether they act for the customer or insurer

The IDD makes a number of changes for advised sales ie

There is a new explicit requirement that all contracts proposed must be consistent with customerrsquos demands and needs - this includes both advised and non-advised sales and

There is a requirement that firms who advise must provide a personalised recommendation explaining why the product recommended best meets the customerrsquos needs

PRIVATE AND CONFIDENTIALPRIVATE AND CONFIDENTIAL

Whilst these new rules build on pre-existing provisions in ICOBS firms should take the opportunity to re visit their sales process in particular the demands and needs assessment and the extent to which recommendations are made relate back to established customer needs

The IDD requires changes to the existing disclosures covering conflicts of interest for an intermediary - it will also introduce new requirements to disclose information concerning the firms remuneration ie intermediaries must disclose the nature of their remuneration in relation to the insurance contract and whether they work on the basis of fee commission or a combination of both

To clarify these are lsquolsquonear finalrsquorsquo rules simply because they are still under discussion at the European Commission and as the FCA need time to prepare this is their best guess of what the rules will currently look like

Final rules are likely to be made in January 2018 in time for firms to comply by 23 February 2018

Next steps

Start to review your existing processes and assess whether they will fit in with the new regime

Firms should read the third Consultation Paper and any feedback must be with the FCA by 25 November 2017

As usual please look out for support and guidance from TMA in the coming months

fraud awareness tips - first time buyersAs an adviser you will be aware of the need to be diligent in the fight against financial crime Failure to do so is not only contrary to FCA expectations (see also our earlier comments on the specific responsibility PR4 under the SMampCR) but your livelihood could be placed at risk

To help mitigate the possibility that your business is used to conduct mortgage fraud we have created a short summary guide that specifically focuses on First Time Buyers and the risks that they may represent Analysis shows that this customer group presents the highest chance of fraud being perpetrated via your business

The guide contains tips and suggestions of the types of the basic checks that you can make when processing a mortgage application for this client type

For more information on Fraud awareness for first time buyers click here

property and title fraudRecorded incidents of fraud are rising with fraudsters continuing to target the properties of both individuals and companies These attacks often include the presentation of forged registration or identity documents as part of HM Land Registry applications HM Land Registry and the Law Society wish to bring these matters to the attention of the public and raise awareness

This joint Law Society and HM Land Registry document provides a practical guide for solicitors on some of the indicators of potential fraud in land transactions and registration of title It is intended as a reference point for the legal profession to be of assistance in recognising potential fraud but not to set a regulatory framework

In view of the rapidly evolving nature of title fraud it should be recognised that this document cannot cover all fraud scenarios and types of fraud threat affecting title to land

Whilst it is aimed at solicitors contained within are several case examples which will be of interest eg

REDEFINING THE MORTGAGE CLUB

comp

lianc

eA criminal gang targeted high value residential properties in the London area being marketed for rent The landlord only had one notification address (that is their address for service) recorded on the proprietorship register and that address was the rental property as opposed to an address where they lived or worked

The landlord let the property to the fraudsters and received six monthsrsquo rent in advance which gave the fraudsters possession of the property and time to commit the fraud

The organised fraud gang successfully sold the property for pound13m although the purchase was not registered by HM Land Registry The registered title fraud was prevented because of certain fraud indicators In this case indicators were

The owner

Was a sole owner

Had one address for service which was the rental property

Was long established having owned the property for over 20 years

The property was vulnerable because it was

Unmortgaged

Of high value

Not lived in or not occupied by the owner

Please click here for the full paper

barclays - new fraud prevention videosHave you ever wondered how valuable your social media data is to a fraudster Or how someone might try to relieve you of your account pin number

With the kind permission of Barclays we have collated a collection of video links which briefly explain the tricks used by fraudsters to try and obtain personal data which could later be used in an identity fraud

Please take time to view them (remembering to turn on your sound) - they may help you not to becone a victim of fraud

View some of the collection here - the links will take you to YouTube and are usually no more than a minute long

Digital safety - PIN protection

Digital safety - personal data

Digital safety - hacked emails

Digital safety - passwords

The phone scam

Cyber crime

PRIVATE AND CONFIDENTIAL

fca publishes findings from the ageing population projectThe FCA has recently published an lsquolsquoOccasional Paperrsquorsquo outlining the findings from a project that explored how the ageing population would impact the Financial Services industry

The FCA launched the Ageing Population Project in February 2016 to explore how older people use financial services and products The paper reviews the public policy implications of having a population which is getting older and the resulting impact on financial services The document also includes actions which the FCA and industry could take to better support older people

This publication is the first of a series of documents which the FCA will publish as part of their focus on consumers including an overarching strategy lsquoApproach to Consumersrsquo which will be published later this Autumn

When reviewing the treatment of older people the FCA found that there are risks that their financial services needs are not being fully met which can result in exclusion poor customer outcomes and potential harm The issues appear to be driven by a range of interrelated causes These include policies and controls that are not designed around consumer needs and unintended consequences of product and service design

While older consumers are not necessarily vulnerable they are more likely than other groups to experience vulnerability at some point (whether temporarily or permanently)

This is particularly the case for those aged over 75 In line with the aims of the FCArsquos Mission this paper has focused on the issues where regulation and financial services firms can play a role and make a difference

There is scope for financial services firms to do more The FCA has set out some ideas for firms to consider in ways that fit their business models such as looking at product and service design customer support and reviewing and adapting strategies

The paper also explores a range of issues including older consumersrsquo engagement with retail banking third party access and planning ahead later life lending and long term care

These issues will require action from multiple parties to address over time In many cases solutions do not lie within the remit of any one party - including the FCA or the regulated firms that it supervises

The FCA has considered who might be best placed to address the gaps to improve financial markets for older people including other bodies who might be better placed to take forward topics outside the FCArsquos remit

The FCA anticipates a further review in three to five years of how the financial services industry is adapting to meet the needs of older consumers

The full paper can be found here

information commissionerrsquos office - fee and registration changesAs we count down to the General Data Protection Regulation (GDPR) taking effect next May the ICO wanted to clarify how the fees that lsquolsquodata controllersrsquorsquo have to pay to them are changing

Under the current Data Protection Act (DPA) organisations that process personal information are required to notify with the ICO as data controllers

This involves explaining what personal data you collect and what you do with it You are also required to pay a notification fee based on your size of either pound35 or pound500 These fees are used to fund most of the ICOrsquos work

comp

lianc

e

REDEFINING THE MORTGAGE CLUB

When the new data protection legislation comes into effect next year there will no longer be a requirement to notify the ICO in the same way However a provision in the Digital Economy Act means it will remain a legal requirement for data controllers to pay the ICO a data protection fee These fees will be used to fund the ICOrsquos data protection work As now any money the ICO receives in fines will be passed directly back to the Government

how much will data controllers have to payThe Digital Economy Act paves the way for a new funding system for the ICO The amount of the data protection fee is being developed by the ICOrsquos sponsoring department the Department for Digital Culture Media and Sport (DCMS) in consultation with the ICO and representatives of those likely to be affected by the change

The final fees will be approved by Parliament

The new system will aim to make sure the fees are fair and reflect the relative risk of the organisationrsquos processing of personal data The size of the data protection fee will still be based on the organisationrsquos size and turnover and will also take into account the amount of personal data it is processing

The current draft proposal is a three tier system which will differentiate between small and big organisations and also how much personal data an organisation is processing The aim is to keep the system as simple as possible so that organisations will easily be able to categorise themselves

They expect to know more by the end of the year and will communicate to data controllers once they do

When will the new data protection fee system start

The new model will go live on 1 April 2018

Irsquom due to renew shortly should I still go ahead with this

Organisations should continue to renew their notification as usual and it is still a criminal offence to not notify if an organisation needs to Once they know more about the new fees they will be telling all organisations about the changes and what they need to do

So until the news fees come in it is very much business as usual - so no excuses for not notifying

information commissionerrsquos office - guidance on the use of cloud computingDoes your organisation process personal data in the cloud If so the ICO has produced some useful cloud computing guidance here

financial ombudsman service - their annual reviewThe Financial Ombudsman Service were set up by Parliament to resolve individual complaints between financial businesses and their customers - fairly reasonably quickly and as informally as possible They can look into problems involving most types of money matters - from payday loans to pensions pet insurance to PPI If a business and their customer canrsquot resolve a problem themselves they can step in to sort things out Independent and unbiased theyrsquoll get to the heart of whatrsquos happened - and reach a fair pragmatic answer that helps both sides move on

If they think the business has acted fairly - or therersquos just been a misunderstanding - theyrsquoll explain how things stand But if someonersquos been treated unfairly theyrsquoll use their powers to put things right

That could mean telling a business to do anything from amending a credit file to reducing loan repayments or from settling an insurance claim to correcting a pension

PRIVATE AND CONFIDENTIAL

Since they were set up theyrsquove seen the real impact of financial concerns complaints and disputes on people from all sorts of backgrounds and livelihoods Theyrsquore committed to sharing their insight and experience to encourage fairness and confidence in financial services

Their annual review is always an opportunity to look forward as well as back and this one is no exception

The full review can be found here

Thank you for taking the time to read this bulletinWe hope you found it useful

Wersquod really appreciate any feedback you haveEmail hellotmaclubcom

Would you like to try a new Compliance PackageFor more details email hellotmaclubcom or click here to see our compliance

proposition

Want to receive our compliance bulletins by emailEmail marketingtmaclubcom

tell us your thoughts

you have to learn the rules of the gamethen play better than anyone elserdquoalbert einstein

ldquo

PRIVATE AND CONFIDENTIAL

Senior managers and certification regime (smampcr) Last monthrsquos bulletin provided a general overview of the proposals the FCA have put forward for the Senior Managers and Certification Regime

As a reminder the aim of the new regime is to reduce harm to consumers and strengthen market integrity by making individuals more accountable for their conduct and competence by

Encouraging a culture of staff at all levels taking personal responsibility for their actions and

Making sure firms and staff clearly understand and can demonstrate where responsibility lies

In this edition we focus on the lsquolsquoPrescribed Responsibilitiesrsquorsquo

The FCA are proposing six extra Prescribed Responsibilities (PR) that a firm must assign to some or all of its Senior Management Team to ensure they are accountable for key conduct risks

Three of the PRs relate to an individual being accountable for compliance with the regime itself ie educating the organisation and overseeing its implementations - PR1 2 amp 3

PR4 addresses the FCArsquos responsibility to prevent financial crime

PR5 addresses key risk oversight of the handling of client money

And finally PR6 underlines the responsibility to keep up to date and observe all applicable laws and FCA rules

The PRs are as followsPR1 - Performance by the firm of its obligations under the Senior Managers Regime including implementation and oversights

PR2 - Performance by the firm of its obligations under the Certification Regime

PR3 - Performance by the firm of its obligations in respect of notifications and training of the Conduct Rules

PR4 - Responsibility for the firmrsquos policies and procedures for countering the risk that the firm might be used to further financial crime

PR5 - Responsibility for the firmrsquos compliance with CASS (if applicable)

PR6 - Responsibility for ensuring the governing body is informed of its legal and regulatory obligations

Firms will need to consider carefully which Senior Manager is the best person to hold each of these responsibilities

Each PR should be given to the Senior Manager who is the most senior person responsible for the area of operations to which the PR relates They will also need to have sufficient authority and an appropriate level of knowledge and competence to carry out the responsibility properly

If you are the sole Senior Manager then all of the responsibilities will be allocated to you

We will of course continue to provide updates so look out for additional support and guidance from TMA in the coming months

REDEFINING THE MORTGAGE CLUB

comp

lianc

efca - culture and conflict - extending and accountability regime

insurance distribution directive (IDD)-feedback to cp 177 and near final rules

It is our understanding that a new technical paper will follow soon detailing timescales and templates that will be of relevance to the new regime

The deadline for feedback to the FCA has now passed (3 November 2017) but firms should still read the Consultation Paper here

Following on from the opening article Jonathan Davidson who is Director of Supervision at the FCA delivered a speech in London recently - he was there to talk about culture and conduct in financial services through the lens of the Senior Managers and Certification Regime or as he likes to call it the lsquolsquoaccountability regimersquorsquo

The speech focused on why culture is so important and why they are introducing the accountability regime

Here are the key points

Cultural change requires individual engagement and accountability

Culture may not be measurable but if it is manageable for example through incentives and governance

They want consumers to understand the FCArsquos expectations around culture in firms and feel able to speak up when standards arenrsquot met

An ethical culture can be more powerful than one based solely on financial incentives

Please read the speech in full here

This Policy Statement (PS) sets out the FCArsquos response to the feedback they received for the first of three Consultation Papers on the IDD

The UK is required to comply with the IDD by 23 February 2018 This will require changes to your advice process procedures and policies - for all insurance sales

Some key changes are summarised below

The IDD requires all insurance distributors and their employees to have the appropriate knowledge and ability to perform their roles This must be supported by a minimum of fifteen hours of continuing professional training or development (CPD) in each twelve months This will be extended to insurance intermediaries and they will need to maintain records of employee competence and CPD

The IDD makes a number of changes to the pre contract disclosures ie what firms might know as lsquolsquoinitial disclosurersquorsquo that firms are required to make such as disclosing whether they are an insurer or an intermediary whether or not they provide advice and whether they act for the customer or insurer

The IDD makes a number of changes for advised sales ie

There is a new explicit requirement that all contracts proposed must be consistent with customerrsquos demands and needs - this includes both advised and non-advised sales and

There is a requirement that firms who advise must provide a personalised recommendation explaining why the product recommended best meets the customerrsquos needs

PRIVATE AND CONFIDENTIALPRIVATE AND CONFIDENTIAL

Whilst these new rules build on pre-existing provisions in ICOBS firms should take the opportunity to re visit their sales process in particular the demands and needs assessment and the extent to which recommendations are made relate back to established customer needs

The IDD requires changes to the existing disclosures covering conflicts of interest for an intermediary - it will also introduce new requirements to disclose information concerning the firms remuneration ie intermediaries must disclose the nature of their remuneration in relation to the insurance contract and whether they work on the basis of fee commission or a combination of both

To clarify these are lsquolsquonear finalrsquorsquo rules simply because they are still under discussion at the European Commission and as the FCA need time to prepare this is their best guess of what the rules will currently look like

Final rules are likely to be made in January 2018 in time for firms to comply by 23 February 2018

Next steps

Start to review your existing processes and assess whether they will fit in with the new regime

Firms should read the third Consultation Paper and any feedback must be with the FCA by 25 November 2017

As usual please look out for support and guidance from TMA in the coming months

fraud awareness tips - first time buyersAs an adviser you will be aware of the need to be diligent in the fight against financial crime Failure to do so is not only contrary to FCA expectations (see also our earlier comments on the specific responsibility PR4 under the SMampCR) but your livelihood could be placed at risk

To help mitigate the possibility that your business is used to conduct mortgage fraud we have created a short summary guide that specifically focuses on First Time Buyers and the risks that they may represent Analysis shows that this customer group presents the highest chance of fraud being perpetrated via your business

The guide contains tips and suggestions of the types of the basic checks that you can make when processing a mortgage application for this client type

For more information on Fraud awareness for first time buyers click here

property and title fraudRecorded incidents of fraud are rising with fraudsters continuing to target the properties of both individuals and companies These attacks often include the presentation of forged registration or identity documents as part of HM Land Registry applications HM Land Registry and the Law Society wish to bring these matters to the attention of the public and raise awareness

This joint Law Society and HM Land Registry document provides a practical guide for solicitors on some of the indicators of potential fraud in land transactions and registration of title It is intended as a reference point for the legal profession to be of assistance in recognising potential fraud but not to set a regulatory framework

In view of the rapidly evolving nature of title fraud it should be recognised that this document cannot cover all fraud scenarios and types of fraud threat affecting title to land

Whilst it is aimed at solicitors contained within are several case examples which will be of interest eg

REDEFINING THE MORTGAGE CLUB

comp

lianc

eA criminal gang targeted high value residential properties in the London area being marketed for rent The landlord only had one notification address (that is their address for service) recorded on the proprietorship register and that address was the rental property as opposed to an address where they lived or worked

The landlord let the property to the fraudsters and received six monthsrsquo rent in advance which gave the fraudsters possession of the property and time to commit the fraud

The organised fraud gang successfully sold the property for pound13m although the purchase was not registered by HM Land Registry The registered title fraud was prevented because of certain fraud indicators In this case indicators were

The owner

Was a sole owner

Had one address for service which was the rental property

Was long established having owned the property for over 20 years

The property was vulnerable because it was

Unmortgaged

Of high value

Not lived in or not occupied by the owner

Please click here for the full paper

barclays - new fraud prevention videosHave you ever wondered how valuable your social media data is to a fraudster Or how someone might try to relieve you of your account pin number

With the kind permission of Barclays we have collated a collection of video links which briefly explain the tricks used by fraudsters to try and obtain personal data which could later be used in an identity fraud

Please take time to view them (remembering to turn on your sound) - they may help you not to becone a victim of fraud

View some of the collection here - the links will take you to YouTube and are usually no more than a minute long

Digital safety - PIN protection

Digital safety - personal data

Digital safety - hacked emails

Digital safety - passwords

The phone scam

Cyber crime

PRIVATE AND CONFIDENTIAL

fca publishes findings from the ageing population projectThe FCA has recently published an lsquolsquoOccasional Paperrsquorsquo outlining the findings from a project that explored how the ageing population would impact the Financial Services industry

The FCA launched the Ageing Population Project in February 2016 to explore how older people use financial services and products The paper reviews the public policy implications of having a population which is getting older and the resulting impact on financial services The document also includes actions which the FCA and industry could take to better support older people

This publication is the first of a series of documents which the FCA will publish as part of their focus on consumers including an overarching strategy lsquoApproach to Consumersrsquo which will be published later this Autumn

When reviewing the treatment of older people the FCA found that there are risks that their financial services needs are not being fully met which can result in exclusion poor customer outcomes and potential harm The issues appear to be driven by a range of interrelated causes These include policies and controls that are not designed around consumer needs and unintended consequences of product and service design

While older consumers are not necessarily vulnerable they are more likely than other groups to experience vulnerability at some point (whether temporarily or permanently)

This is particularly the case for those aged over 75 In line with the aims of the FCArsquos Mission this paper has focused on the issues where regulation and financial services firms can play a role and make a difference

There is scope for financial services firms to do more The FCA has set out some ideas for firms to consider in ways that fit their business models such as looking at product and service design customer support and reviewing and adapting strategies

The paper also explores a range of issues including older consumersrsquo engagement with retail banking third party access and planning ahead later life lending and long term care

These issues will require action from multiple parties to address over time In many cases solutions do not lie within the remit of any one party - including the FCA or the regulated firms that it supervises

The FCA has considered who might be best placed to address the gaps to improve financial markets for older people including other bodies who might be better placed to take forward topics outside the FCArsquos remit

The FCA anticipates a further review in three to five years of how the financial services industry is adapting to meet the needs of older consumers

The full paper can be found here

information commissionerrsquos office - fee and registration changesAs we count down to the General Data Protection Regulation (GDPR) taking effect next May the ICO wanted to clarify how the fees that lsquolsquodata controllersrsquorsquo have to pay to them are changing

Under the current Data Protection Act (DPA) organisations that process personal information are required to notify with the ICO as data controllers

This involves explaining what personal data you collect and what you do with it You are also required to pay a notification fee based on your size of either pound35 or pound500 These fees are used to fund most of the ICOrsquos work

comp

lianc

e

REDEFINING THE MORTGAGE CLUB

When the new data protection legislation comes into effect next year there will no longer be a requirement to notify the ICO in the same way However a provision in the Digital Economy Act means it will remain a legal requirement for data controllers to pay the ICO a data protection fee These fees will be used to fund the ICOrsquos data protection work As now any money the ICO receives in fines will be passed directly back to the Government

how much will data controllers have to payThe Digital Economy Act paves the way for a new funding system for the ICO The amount of the data protection fee is being developed by the ICOrsquos sponsoring department the Department for Digital Culture Media and Sport (DCMS) in consultation with the ICO and representatives of those likely to be affected by the change

The final fees will be approved by Parliament

The new system will aim to make sure the fees are fair and reflect the relative risk of the organisationrsquos processing of personal data The size of the data protection fee will still be based on the organisationrsquos size and turnover and will also take into account the amount of personal data it is processing

The current draft proposal is a three tier system which will differentiate between small and big organisations and also how much personal data an organisation is processing The aim is to keep the system as simple as possible so that organisations will easily be able to categorise themselves

They expect to know more by the end of the year and will communicate to data controllers once they do

When will the new data protection fee system start

The new model will go live on 1 April 2018

Irsquom due to renew shortly should I still go ahead with this

Organisations should continue to renew their notification as usual and it is still a criminal offence to not notify if an organisation needs to Once they know more about the new fees they will be telling all organisations about the changes and what they need to do

So until the news fees come in it is very much business as usual - so no excuses for not notifying

information commissionerrsquos office - guidance on the use of cloud computingDoes your organisation process personal data in the cloud If so the ICO has produced some useful cloud computing guidance here

financial ombudsman service - their annual reviewThe Financial Ombudsman Service were set up by Parliament to resolve individual complaints between financial businesses and their customers - fairly reasonably quickly and as informally as possible They can look into problems involving most types of money matters - from payday loans to pensions pet insurance to PPI If a business and their customer canrsquot resolve a problem themselves they can step in to sort things out Independent and unbiased theyrsquoll get to the heart of whatrsquos happened - and reach a fair pragmatic answer that helps both sides move on

If they think the business has acted fairly - or therersquos just been a misunderstanding - theyrsquoll explain how things stand But if someonersquos been treated unfairly theyrsquoll use their powers to put things right

That could mean telling a business to do anything from amending a credit file to reducing loan repayments or from settling an insurance claim to correcting a pension

PRIVATE AND CONFIDENTIAL

Since they were set up theyrsquove seen the real impact of financial concerns complaints and disputes on people from all sorts of backgrounds and livelihoods Theyrsquore committed to sharing their insight and experience to encourage fairness and confidence in financial services

Their annual review is always an opportunity to look forward as well as back and this one is no exception

The full review can be found here

Thank you for taking the time to read this bulletinWe hope you found it useful

Wersquod really appreciate any feedback you haveEmail hellotmaclubcom

Would you like to try a new Compliance PackageFor more details email hellotmaclubcom or click here to see our compliance

proposition

Want to receive our compliance bulletins by emailEmail marketingtmaclubcom

tell us your thoughts

you have to learn the rules of the gamethen play better than anyone elserdquoalbert einstein

ldquo

REDEFINING THE MORTGAGE CLUB

comp

lianc

efca - culture and conflict - extending and accountability regime

insurance distribution directive (IDD)-feedback to cp 177 and near final rules

It is our understanding that a new technical paper will follow soon detailing timescales and templates that will be of relevance to the new regime

The deadline for feedback to the FCA has now passed (3 November 2017) but firms should still read the Consultation Paper here

Following on from the opening article Jonathan Davidson who is Director of Supervision at the FCA delivered a speech in London recently - he was there to talk about culture and conduct in financial services through the lens of the Senior Managers and Certification Regime or as he likes to call it the lsquolsquoaccountability regimersquorsquo

The speech focused on why culture is so important and why they are introducing the accountability regime

Here are the key points

Cultural change requires individual engagement and accountability

Culture may not be measurable but if it is manageable for example through incentives and governance

They want consumers to understand the FCArsquos expectations around culture in firms and feel able to speak up when standards arenrsquot met

An ethical culture can be more powerful than one based solely on financial incentives

Please read the speech in full here

This Policy Statement (PS) sets out the FCArsquos response to the feedback they received for the first of three Consultation Papers on the IDD

The UK is required to comply with the IDD by 23 February 2018 This will require changes to your advice process procedures and policies - for all insurance sales

Some key changes are summarised below

The IDD requires all insurance distributors and their employees to have the appropriate knowledge and ability to perform their roles This must be supported by a minimum of fifteen hours of continuing professional training or development (CPD) in each twelve months This will be extended to insurance intermediaries and they will need to maintain records of employee competence and CPD

The IDD makes a number of changes to the pre contract disclosures ie what firms might know as lsquolsquoinitial disclosurersquorsquo that firms are required to make such as disclosing whether they are an insurer or an intermediary whether or not they provide advice and whether they act for the customer or insurer

The IDD makes a number of changes for advised sales ie

There is a new explicit requirement that all contracts proposed must be consistent with customerrsquos demands and needs - this includes both advised and non-advised sales and

There is a requirement that firms who advise must provide a personalised recommendation explaining why the product recommended best meets the customerrsquos needs

PRIVATE AND CONFIDENTIALPRIVATE AND CONFIDENTIAL

Whilst these new rules build on pre-existing provisions in ICOBS firms should take the opportunity to re visit their sales process in particular the demands and needs assessment and the extent to which recommendations are made relate back to established customer needs

The IDD requires changes to the existing disclosures covering conflicts of interest for an intermediary - it will also introduce new requirements to disclose information concerning the firms remuneration ie intermediaries must disclose the nature of their remuneration in relation to the insurance contract and whether they work on the basis of fee commission or a combination of both

To clarify these are lsquolsquonear finalrsquorsquo rules simply because they are still under discussion at the European Commission and as the FCA need time to prepare this is their best guess of what the rules will currently look like

Final rules are likely to be made in January 2018 in time for firms to comply by 23 February 2018

Next steps

Start to review your existing processes and assess whether they will fit in with the new regime

Firms should read the third Consultation Paper and any feedback must be with the FCA by 25 November 2017

As usual please look out for support and guidance from TMA in the coming months

fraud awareness tips - first time buyersAs an adviser you will be aware of the need to be diligent in the fight against financial crime Failure to do so is not only contrary to FCA expectations (see also our earlier comments on the specific responsibility PR4 under the SMampCR) but your livelihood could be placed at risk

To help mitigate the possibility that your business is used to conduct mortgage fraud we have created a short summary guide that specifically focuses on First Time Buyers and the risks that they may represent Analysis shows that this customer group presents the highest chance of fraud being perpetrated via your business

The guide contains tips and suggestions of the types of the basic checks that you can make when processing a mortgage application for this client type

For more information on Fraud awareness for first time buyers click here

property and title fraudRecorded incidents of fraud are rising with fraudsters continuing to target the properties of both individuals and companies These attacks often include the presentation of forged registration or identity documents as part of HM Land Registry applications HM Land Registry and the Law Society wish to bring these matters to the attention of the public and raise awareness

This joint Law Society and HM Land Registry document provides a practical guide for solicitors on some of the indicators of potential fraud in land transactions and registration of title It is intended as a reference point for the legal profession to be of assistance in recognising potential fraud but not to set a regulatory framework

In view of the rapidly evolving nature of title fraud it should be recognised that this document cannot cover all fraud scenarios and types of fraud threat affecting title to land

Whilst it is aimed at solicitors contained within are several case examples which will be of interest eg

REDEFINING THE MORTGAGE CLUB

comp

lianc

eA criminal gang targeted high value residential properties in the London area being marketed for rent The landlord only had one notification address (that is their address for service) recorded on the proprietorship register and that address was the rental property as opposed to an address where they lived or worked

The landlord let the property to the fraudsters and received six monthsrsquo rent in advance which gave the fraudsters possession of the property and time to commit the fraud

The organised fraud gang successfully sold the property for pound13m although the purchase was not registered by HM Land Registry The registered title fraud was prevented because of certain fraud indicators In this case indicators were

The owner

Was a sole owner

Had one address for service which was the rental property

Was long established having owned the property for over 20 years

The property was vulnerable because it was

Unmortgaged

Of high value

Not lived in or not occupied by the owner

Please click here for the full paper

barclays - new fraud prevention videosHave you ever wondered how valuable your social media data is to a fraudster Or how someone might try to relieve you of your account pin number

With the kind permission of Barclays we have collated a collection of video links which briefly explain the tricks used by fraudsters to try and obtain personal data which could later be used in an identity fraud

Please take time to view them (remembering to turn on your sound) - they may help you not to becone a victim of fraud

View some of the collection here - the links will take you to YouTube and are usually no more than a minute long

Digital safety - PIN protection

Digital safety - personal data

Digital safety - hacked emails

Digital safety - passwords

The phone scam

Cyber crime

PRIVATE AND CONFIDENTIAL

fca publishes findings from the ageing population projectThe FCA has recently published an lsquolsquoOccasional Paperrsquorsquo outlining the findings from a project that explored how the ageing population would impact the Financial Services industry

The FCA launched the Ageing Population Project in February 2016 to explore how older people use financial services and products The paper reviews the public policy implications of having a population which is getting older and the resulting impact on financial services The document also includes actions which the FCA and industry could take to better support older people

This publication is the first of a series of documents which the FCA will publish as part of their focus on consumers including an overarching strategy lsquoApproach to Consumersrsquo which will be published later this Autumn

When reviewing the treatment of older people the FCA found that there are risks that their financial services needs are not being fully met which can result in exclusion poor customer outcomes and potential harm The issues appear to be driven by a range of interrelated causes These include policies and controls that are not designed around consumer needs and unintended consequences of product and service design

While older consumers are not necessarily vulnerable they are more likely than other groups to experience vulnerability at some point (whether temporarily or permanently)

This is particularly the case for those aged over 75 In line with the aims of the FCArsquos Mission this paper has focused on the issues where regulation and financial services firms can play a role and make a difference

There is scope for financial services firms to do more The FCA has set out some ideas for firms to consider in ways that fit their business models such as looking at product and service design customer support and reviewing and adapting strategies

The paper also explores a range of issues including older consumersrsquo engagement with retail banking third party access and planning ahead later life lending and long term care

These issues will require action from multiple parties to address over time In many cases solutions do not lie within the remit of any one party - including the FCA or the regulated firms that it supervises

The FCA has considered who might be best placed to address the gaps to improve financial markets for older people including other bodies who might be better placed to take forward topics outside the FCArsquos remit

The FCA anticipates a further review in three to five years of how the financial services industry is adapting to meet the needs of older consumers

The full paper can be found here

information commissionerrsquos office - fee and registration changesAs we count down to the General Data Protection Regulation (GDPR) taking effect next May the ICO wanted to clarify how the fees that lsquolsquodata controllersrsquorsquo have to pay to them are changing

Under the current Data Protection Act (DPA) organisations that process personal information are required to notify with the ICO as data controllers

This involves explaining what personal data you collect and what you do with it You are also required to pay a notification fee based on your size of either pound35 or pound500 These fees are used to fund most of the ICOrsquos work

comp

lianc

e

REDEFINING THE MORTGAGE CLUB

When the new data protection legislation comes into effect next year there will no longer be a requirement to notify the ICO in the same way However a provision in the Digital Economy Act means it will remain a legal requirement for data controllers to pay the ICO a data protection fee These fees will be used to fund the ICOrsquos data protection work As now any money the ICO receives in fines will be passed directly back to the Government

how much will data controllers have to payThe Digital Economy Act paves the way for a new funding system for the ICO The amount of the data protection fee is being developed by the ICOrsquos sponsoring department the Department for Digital Culture Media and Sport (DCMS) in consultation with the ICO and representatives of those likely to be affected by the change

The final fees will be approved by Parliament

The new system will aim to make sure the fees are fair and reflect the relative risk of the organisationrsquos processing of personal data The size of the data protection fee will still be based on the organisationrsquos size and turnover and will also take into account the amount of personal data it is processing

The current draft proposal is a three tier system which will differentiate between small and big organisations and also how much personal data an organisation is processing The aim is to keep the system as simple as possible so that organisations will easily be able to categorise themselves

They expect to know more by the end of the year and will communicate to data controllers once they do

When will the new data protection fee system start

The new model will go live on 1 April 2018

Irsquom due to renew shortly should I still go ahead with this

Organisations should continue to renew their notification as usual and it is still a criminal offence to not notify if an organisation needs to Once they know more about the new fees they will be telling all organisations about the changes and what they need to do

So until the news fees come in it is very much business as usual - so no excuses for not notifying

information commissionerrsquos office - guidance on the use of cloud computingDoes your organisation process personal data in the cloud If so the ICO has produced some useful cloud computing guidance here

financial ombudsman service - their annual reviewThe Financial Ombudsman Service were set up by Parliament to resolve individual complaints between financial businesses and their customers - fairly reasonably quickly and as informally as possible They can look into problems involving most types of money matters - from payday loans to pensions pet insurance to PPI If a business and their customer canrsquot resolve a problem themselves they can step in to sort things out Independent and unbiased theyrsquoll get to the heart of whatrsquos happened - and reach a fair pragmatic answer that helps both sides move on

If they think the business has acted fairly - or therersquos just been a misunderstanding - theyrsquoll explain how things stand But if someonersquos been treated unfairly theyrsquoll use their powers to put things right

That could mean telling a business to do anything from amending a credit file to reducing loan repayments or from settling an insurance claim to correcting a pension

PRIVATE AND CONFIDENTIAL

Since they were set up theyrsquove seen the real impact of financial concerns complaints and disputes on people from all sorts of backgrounds and livelihoods Theyrsquore committed to sharing their insight and experience to encourage fairness and confidence in financial services

Their annual review is always an opportunity to look forward as well as back and this one is no exception

The full review can be found here

Thank you for taking the time to read this bulletinWe hope you found it useful

Wersquod really appreciate any feedback you haveEmail hellotmaclubcom

Would you like to try a new Compliance PackageFor more details email hellotmaclubcom or click here to see our compliance

proposition

Want to receive our compliance bulletins by emailEmail marketingtmaclubcom

tell us your thoughts

you have to learn the rules of the gamethen play better than anyone elserdquoalbert einstein

ldquo

PRIVATE AND CONFIDENTIALPRIVATE AND CONFIDENTIAL

Whilst these new rules build on pre-existing provisions in ICOBS firms should take the opportunity to re visit their sales process in particular the demands and needs assessment and the extent to which recommendations are made relate back to established customer needs

The IDD requires changes to the existing disclosures covering conflicts of interest for an intermediary - it will also introduce new requirements to disclose information concerning the firms remuneration ie intermediaries must disclose the nature of their remuneration in relation to the insurance contract and whether they work on the basis of fee commission or a combination of both

To clarify these are lsquolsquonear finalrsquorsquo rules simply because they are still under discussion at the European Commission and as the FCA need time to prepare this is their best guess of what the rules will currently look like

Final rules are likely to be made in January 2018 in time for firms to comply by 23 February 2018

Next steps

Start to review your existing processes and assess whether they will fit in with the new regime

Firms should read the third Consultation Paper and any feedback must be with the FCA by 25 November 2017

As usual please look out for support and guidance from TMA in the coming months

fraud awareness tips - first time buyersAs an adviser you will be aware of the need to be diligent in the fight against financial crime Failure to do so is not only contrary to FCA expectations (see also our earlier comments on the specific responsibility PR4 under the SMampCR) but your livelihood could be placed at risk

To help mitigate the possibility that your business is used to conduct mortgage fraud we have created a short summary guide that specifically focuses on First Time Buyers and the risks that they may represent Analysis shows that this customer group presents the highest chance of fraud being perpetrated via your business

The guide contains tips and suggestions of the types of the basic checks that you can make when processing a mortgage application for this client type

For more information on Fraud awareness for first time buyers click here

property and title fraudRecorded incidents of fraud are rising with fraudsters continuing to target the properties of both individuals and companies These attacks often include the presentation of forged registration or identity documents as part of HM Land Registry applications HM Land Registry and the Law Society wish to bring these matters to the attention of the public and raise awareness

This joint Law Society and HM Land Registry document provides a practical guide for solicitors on some of the indicators of potential fraud in land transactions and registration of title It is intended as a reference point for the legal profession to be of assistance in recognising potential fraud but not to set a regulatory framework

In view of the rapidly evolving nature of title fraud it should be recognised that this document cannot cover all fraud scenarios and types of fraud threat affecting title to land

Whilst it is aimed at solicitors contained within are several case examples which will be of interest eg

REDEFINING THE MORTGAGE CLUB

comp

lianc

eA criminal gang targeted high value residential properties in the London area being marketed for rent The landlord only had one notification address (that is their address for service) recorded on the proprietorship register and that address was the rental property as opposed to an address where they lived or worked

The landlord let the property to the fraudsters and received six monthsrsquo rent in advance which gave the fraudsters possession of the property and time to commit the fraud

The organised fraud gang successfully sold the property for pound13m although the purchase was not registered by HM Land Registry The registered title fraud was prevented because of certain fraud indicators In this case indicators were

The owner

Was a sole owner

Had one address for service which was the rental property

Was long established having owned the property for over 20 years

The property was vulnerable because it was

Unmortgaged

Of high value

Not lived in or not occupied by the owner

Please click here for the full paper

barclays - new fraud prevention videosHave you ever wondered how valuable your social media data is to a fraudster Or how someone might try to relieve you of your account pin number

With the kind permission of Barclays we have collated a collection of video links which briefly explain the tricks used by fraudsters to try and obtain personal data which could later be used in an identity fraud