TIPS DEVELOPMENT DIALOGUE SEMINAR South Africa and the Credit Crunch Ben Smit Bureau for Economic...

23

TIPS DEVELOPMENT DIALOGUE SEMINAR South Africa and the Credit Crunch Ben Smit Bureau for Economic Research University of Stellenbosch 15 May 2009

-

Upload

gregory-blaise-adams -

Category

Documents

-

view

213 -

download

0

Transcript of TIPS DEVELOPMENT DIALOGUE SEMINAR South Africa and the Credit Crunch Ben Smit Bureau for Economic...

TIPS DEVELOPMENT DIALOGUE SEMINAR

South Africa and the Credit Crunch

TIPS DEVELOPMENT DIALOGUE SEMINAR

South Africa and the Credit Crunch

Ben Smit

Bureau for Economic Research

University of Stellenbosch

15 May 2009

OutlineOutline

SA already in cyclical slowdown when

crisis struck

Financial indicators

Real indicators

Overall expected impact

SA cyclical slowdown: GDP growth rateSA cyclical slowdown: GDP growth rate

-5

-3

-1

1

3

5

7

1980 1985 1990 1995 2000 2005

y-o

-y %

ch

an

ge Ave 1985-94:

0.8% pa

Ave 1995-04:3.1% pa

4Q08 =-1.8% (SAAR)

RMB/ BER BCI

0

20

40

60

80

100

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008

SA cyclical slowdown: RMB/BER BCISA cyclical slowdown: RMB/BER BCI

2009Q1

•Business confidence declined from 33 in 08Q4 to 27 in 09Q1

•Manufacturing 31 16

•Building 42 33

•New vehicles 0 5

•Retail 49 52

•Wholesale 44 31

Financial impact: Portfolio capital flowsFinancial impact: Portfolio capital flows

-60000

-50000

-40000

-30000

-20000

-10000

0

10000

20000

30000

40000

2002 2003 2004 2005 2006 2007 2008 2009

Ran

d (

mill

ion

s)

Oct ‘08

Financial impact: Exchange ratesFinancial impact: Exchange rates

4

5

6

7

8

9

10

11

12

13

14

2002 2003 2004 2005 2006 2007 2008 2009

Rand/ euro Rand/ $

Oct ‘08

100

10100

20100

30100

40100

50100

60100

70100

80100

Jan-99 Jan-00 Jan-01 Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

100

5100

10100

15100

20100

25100

30100

35100

Resources (lhs) All Share

Financial impact: JSE share pricesFinancial impact: JSE share prices

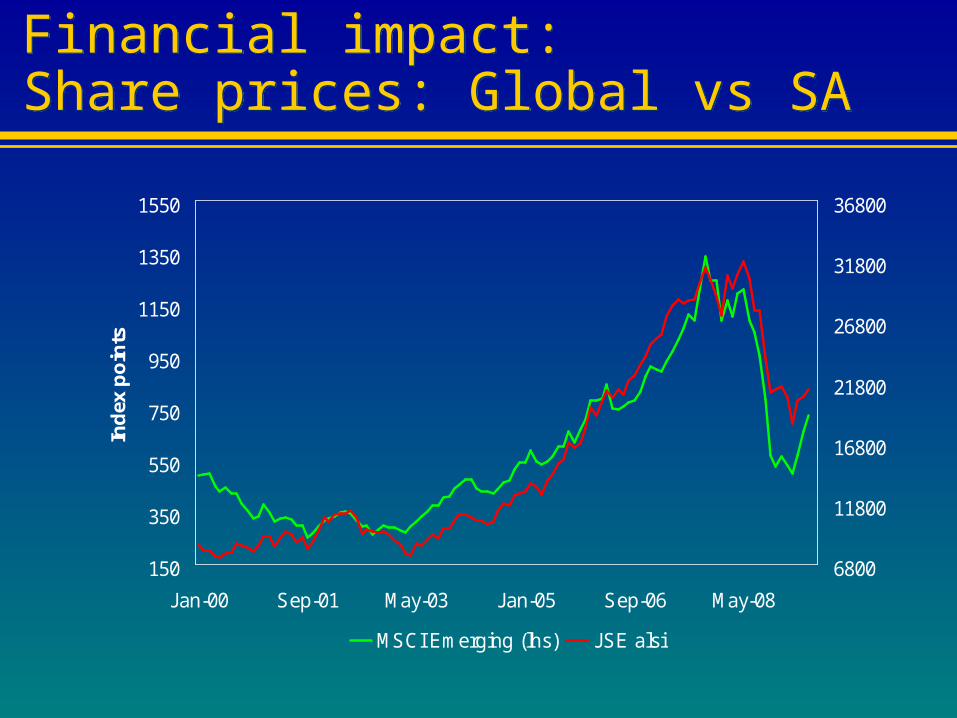

Financial impact: Share prices: Global vs SAFinancial impact: Share prices: Global vs SA

150

350

550

750

950

1150

1350

1550

Jan-00 Sep-01 May-03 Jan-05 Sep-06 May-08

Ind

ex p

oin

ts

6800

11800

16800

21800

26800

31800

36800

MSCI Emerging (lhs) JSE alsi

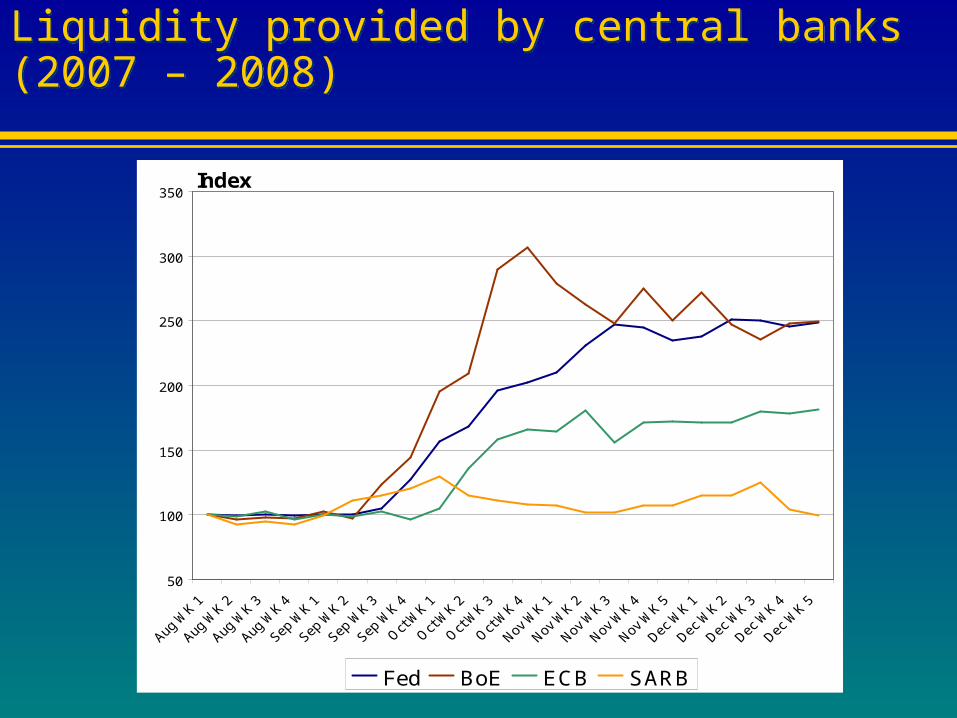

Liquidity provided by central banks (2007 – 2008)Liquidity provided by central banks (2007 – 2008)

50

100

150

200

250

300

350Index

Fed BoE ECB SARB

Real sector: Exports decline sharplyReal sector: Exports decline sharply

Jan/Feb ’09 vs Jan/Feb

‘08

Jan/Feb ’09 vs Nov/Dec

‘08

Contribution to ’08 total

exports

Vehicle and Transport Equipment -7.65% -47.90% 10.3%

Machinery, Mechanical Appliances & Electrical Equipment

-27.06% -28.68% 9.8%

Mineral Products (Total) 36.37% 16.66% 18.0%

Mineral Products (Coal only) 59.23% -25.10% 5.9%

Diamonds -63.21% -25.85% 2.3%

Gold 25.94% -13.42% 6.9%

Platinum -38.26% -20.88% 12.1%

Base Metals & Articles thereof -32.91% -19.20% 17.3%

Chemical Products -5.03% -26.33% 7.1%

Food & Agricultural Categories 48.41% 11.76% 7.2%

Total Exports -5.03% -26.33%

Source of basic data: Customs & Excise

Real sector:Manufacturing: Investec PMI vs Prod VolReal sector:Manufacturing: Investec PMI vs Prod Vol

35

40

45

50

55

60

65

Jan-02 Jan-03 Jan-04 Jan-05 Jan-06 Jan-07 Jan-08 Jan-09

index

-15

-10

-5

0

5

10

15

2 m

onth

s sm

ooth

ed

Investec PMI Mnfr Prod 2mm

April2009

l

30

35

40

45

50

55

60

65

Jan-98 Oct-99 Dec-00 02-Feb 03-Apr 04-Jun 05-Aug 06-Oct 07-Dec Feb-09

Ind

ex p

oin

ts

SA PMI Global PMI

Real Sector:

Manufacturing PMI: SA vs Global

Expansion

Contraction

-60

-40

-20

0

20

40

60

92 94 96 98 00 02 04 06 08

Net

bala

nce

Real sector:BER Manufacturing Survey: Export volumes changes

Real sector:BER Manufacturing Survey: Export volumes changes

Expected

-54

-80

-60

-40

-20

0

20

40

60

80

100

74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

Net

bala

nce

Real sector:BER manufacturing survey:Domestic sales volume changes

Real sector:BER manufacturing survey:Domestic sales volume changes

Expected

-65

-80

-60

-40

-20

0

20

40

60

80

100

74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08

Net

bala

nce

Real sector:BER manufacturing survey:Production volume changes

Real sector:BER manufacturing survey:Production volume changes

Expected

-63

-30

-20

-10

0

10

20

30

40

92 94 96 98 00 02 04 06 08

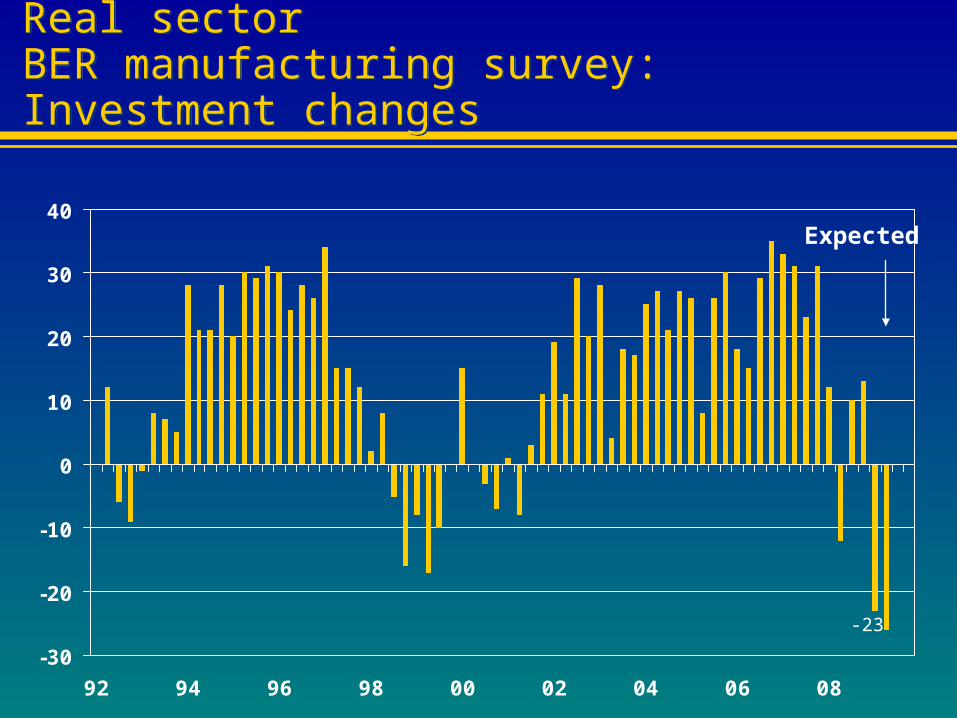

Real sectorBER manufacturing survey:Investment changes

Real sectorBER manufacturing survey:Investment changes

Expected

-23

Real sector:BER manufacturing survey:Expected total fixed investment in 12 months time

Real sector:BER manufacturing survey:Expected total fixed investment in 12 months time

-20

-10

0

10

20

30

40

50

60

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

Net

bal

ance

-8

-80

-60

-40

-20

0

20

40

60

80

100

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009

Manufacturing Retail B&C

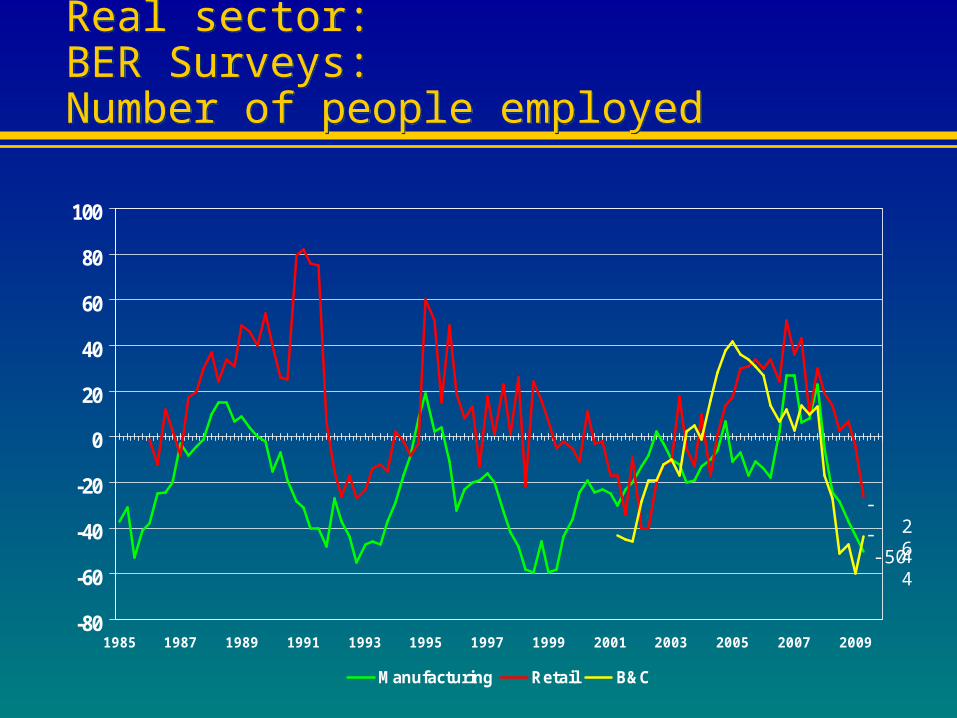

Real sector:BER Surveys:Number of people employed

Real sector:BER Surveys:Number of people employed

-26

-50-44

Real sector:BER manufacturing survey:Numbers employed vs hours worked

Real sector:BER manufacturing survey:Numbers employed vs hours worked

-80

-60

-40

-20

0

20

40

Mar-70 Jun-76 Sep-82 Dec-88 Mar-95 Jun-01 Sep-07

BE

R n

et b

alan

ce

Number of factory workers Average hours worked

-67

-43

0

1

2

3

4

5

6

7

8

9

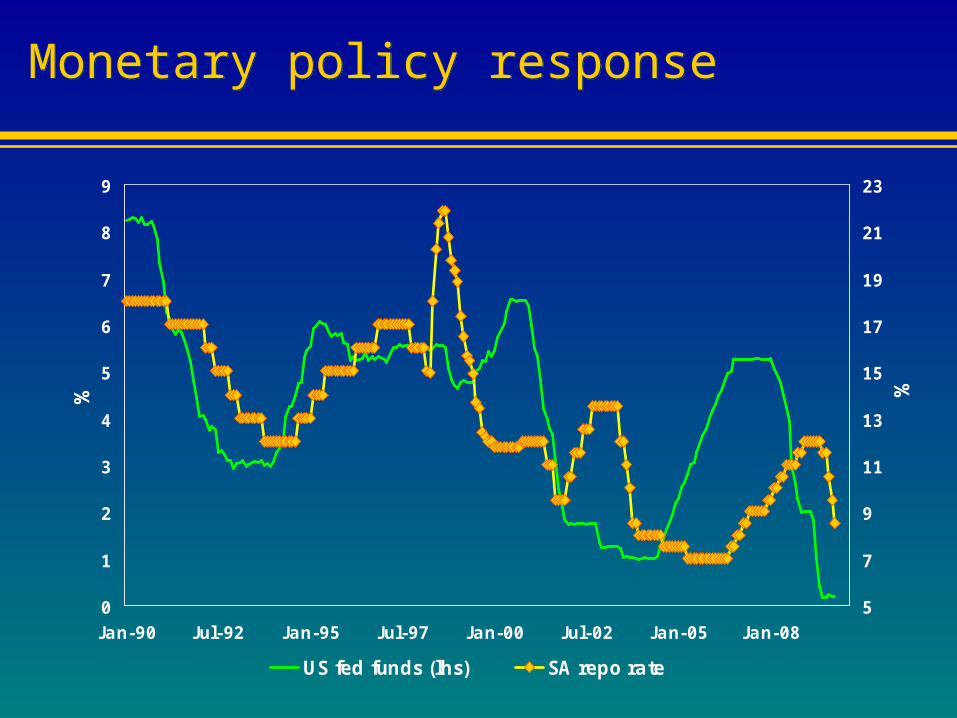

Jan-90 Jul-92 Jan-95 Jul-97 Jan-00 Jul-02 Jan-05 Jan-08

%

5

7

9

11

13

15

17

19

21

23

%

US fed funds (lhs) SA repo rate

Monetary policy responseMonetary policy response

Fiscal Policy responseFiscal Policy response

Budget more expansive than expected, unlikely to prevent sharp growth slowdown

Budget may benefit SA focused construction companies, non-durable retailers (social grant increases, 45% of personal tax relief for people with taxable income below R150k p.a.)

Extension of child support grant to 15 – research being done of feasibility of further extension to 18 years of ago

Massive public sector investment (R787 over MTEF) key growth support, but also risks (offshore funding constrained in current environment) – Acsa already hinted may spend less

-6

-4

-2

0

2

4

6

8

10

1994 1997 2000 2003 2006 2009

% o

f G

DP

Budget balance Public sector borrowing requirement

Overall SA impact of the global crisis/recession in 2009Overall SA impact of the global crisis/recession in 2009

08Q3 09Q2

South Africa***

- GDP growth 3.2 -0.8

- Export growth 6.7 -9.1

Global GDP growth

- World

- IMF** 3.0 -1.3

- JPM* 2.3 -2.6

- Advanced countries

- IMF** 0.5 -3.8

- JPM* 1.4 -3.4

- Emerging markets

- IMF** 6.1 1.6

- JPM* 6.0 0.2*Aug ’08 vs May ’09

**Oct ’08 vs April ’09

*** BER forecast

Bureau for Economic Research

Economic information that works for you

Bureau for Economic Research

Economic information that works for you

Website: www.ber.sun.ac.za

E-mail: [email protected]

Tel No: 021-887 2810