TIK WORKING PAPERS on Innovation Studies No. 20180524 · foundations e.g. in terms of regulations...

35

TIK WORKING PAPERS on Innovation Studies No. 20180524 http://ideas.repec.org/s/tik/inowpp.html Senter for teknologi, innovasjon og kultur Universitetet i Oslo TIK Centre for technology, innovation and culture P.O. BOX 1108 Blindern N-0317 OSLO Norway Eilert Sundts House, 5th floor Moltke Moesvei 31 Phone: +47 22 84 16 00 Fax: +47 22 84 16 01 http://www.sv.uio.no/tik/ [email protected]

Transcript of TIK WORKING PAPERS on Innovation Studies No. 20180524 · foundations e.g. in terms of regulations...

TIK WORKING PAPERS

on Innovation Studies

No. 20180524 http://ideas.repec.org/s/tik/inowpp.html

Senter for teknologi, innovasjon og kultur Universitetet i Oslo

TIK

Centre for technology, innovation and culture P.O. BOX 1108 Blindern

N-0317 OSLO Norway

Eilert Sundts House, 5th floor

Moltke Moesvei 31

Phone: +47 22 84 16 00 Fax: +47 22 84 16 01

http://www.sv.uio.no/tik/

1

The green flings: market fluctuations and incumbent energy industries’ engagement in renewable energy

Tuukka Mäkitie, Håkon E. Normann, Taran M. Thune, and Jakoba Sraml Gonzalez

Centre for Technology, Innovation and Culture, University of Oslo, Norway

Abstract

Reorientation of fossil fuel industries towards renewable energies, and the role of market

changes underlying such processes, have not featured strongly in the study of sustainable

energy transitions. We contribute to this important policy issue with a case study of

diversification of Norwegian oil and gas industry in offshore wind power. We study how the

engagement in diversification has changed during 2007-2016, and whether these changes

correspond with developments in the industry’s task and institutional environments. By using

news, statistical and survey data, our study reveals that despite continuous growth in offshore

wind market, the industry engaged more in offshore wind during two market downturn

periods in the oil and gas market, and less during an oil and gas boom period. Our results

therefore draw attention to the importance of market changes in reorientation of fossil fuel

industries towards renewable energies. We conclude by discussing the role of market changes

in influencing reorientations towards renewable energies, and implications of results for

policies which seek to support sustainable energy transitions.

Keywords Sustainable energy transition; Task environment; Oil and gas industry; Offshore wind power;

Norway

2

1. Introduction

The current hydrocarbon energy system rests on a large incumbent industry that has dominated the

energy system of the world for more than a century. This industry, consisting of e.g. large oil and service

firms, has stakes in established value chains, technologies and business models. Oil and gas (O&G)

industry is therefore often seen to defend the current socio-technical energy system based on fossil fuels

against a transition towards sustainability and renewable energy.

Some recent studies, however, have shown that such incumbent industries are also able to transform and

adapt to transition processes, and even drive innovation in renewable energy (Bergek et al., 2013; Steen

& Weaver, 2017). For instance, oil companies have played a role in the development and

commercialization of solar PV technology (Pinkse & van den Buuse, 2012). In Norway, diversification

of the O&G industry to offshore wind power has had an impact on the development of an innovation

system around offshore wind power in the country (Hansen & Steen, 2015; Mäkitie et al., 2018). For

example the national oil company Statoil has made significant investments in renewable energy projects,

seeking to grow a new “green path” alongside its on-going O&G operations (Nilsen, 2017). In countries

with strong fossil fuel industries, such reorientations of incumbent energy industry towards renewable

energy have high relevance for energy and industrial policy, as it creates potential for utilization of

capabilities and experience of these industries in new markets. Renewable energy can therefore present

an opportunity to create jobs on the basis of oil and gas experiences, which can have political importance

in O&G countries in supporting ambitions to carry out a sustainable energy transition.

The environment of firms has been suggested as an important source of pressures driving incumbent

industry reorientation towards sustainability (Geels, 2014; Penna & Geels, 2015). However, the role of

market changes underlying such reorientations has this far received relatively little attention, even

though economic pressures have been reported to be effective in destabilizing fossil fuel paths (e.g.

Turnheim & Geels, 2012). We argue that the economic perspective (e.g. markets and value creation) is

3

also particularly important because changes in markets are likely to cause a relatively fast reaction in

industries, as firms seek to secure their revenue production by reorganizing their activities to fit market

conditions. Hence, market changes have the potential to cause more urgent reorientation than e.g.

institutional changes, which are likely to take longer (cf. Penna & Geels, 2015). Such understanding

can, for instance, be useful in creation of policy mixes which simultaneously incentivize market

developments of sustainable technologies while also reduce support and destabilize unsustainable

technologies (cf. Kivimaa & Kern, 2016).

In this paper, we analyse the reorientation of an incumbent energy industry towards renewable energy

as influenced by changing pressures and incentives in their environment. Our perspective draws

attention to three potentially important and often over-looked issues related to understanding energy

industries in sustainable energy transitions. First, the central role of the economic environment for firm

behaviour; second, the possible intermittency of engagement in transitions; and third, the redeployability

of firm resources between fossil fuel and renewable energy markets. The empirical context we address

is the O&G in Norway and its engagement in diversification to offshore wind power (OWP) during

2007-2016. We apply the analytical framework of task and institutional environments of organizations

(Scott, 2003) and draw upon a range of data sources such as news data, statistics, and documentary and

survey data. Our research questions are: How has the engagement of oil and gas industry in offshore

wind power changed over time, and have the changes in engagement been consistent with the changing

conditions in the environment of the industry?

We continue the paper in section two by discussing theoretical perspectives for understanding how

environment of fossil fuel industries can influence their reorientation to renewable energy markets. In

section three, we introduce our case study topic, data and methods. In section four, we present our study

of Norwegian O&G industry’s engagement in diversification in OWP. We discuss our results in section

five in light of existing literature and outline the implications of the results for policy targeting

sustainable energy transitions.

4

2. Theoretical perspectives

Previous literature has shown that pressures and incentives from environment can act as incetives and

pressures for industries to transform (Tushman & Anderson, 1986; Geels, 2014). In order to inform our

analysis, we draw on literature from institutional theory regarding organization-environment interaction.

Moreover, we complement this literature with insights from management literature regarding the role

of market changes for resource redeployment across related markets. Finally, we synthesize these

perspectives into a framework which we apply in our analysis.

2.1. Organizational environment and industrial change

Firms rely on their environment for inputs, such as resources and legitimacy, and for outputs, such as

markets for their products. Their actions are also influenced by surrounding institutions, such as

regulations, norms and culture (Scott, 2014). Analytically, the environment of firms can therefore be

divided into (economic) task environment and institutional environment, which both can exert different

pressures and incentives for change (Scott, 2003).

Task environment consists of elements directly relevant for firms to execute their main task, i.e. revenue

and value creation. The task environment consists of inputs (resources and materials) and outputs

(markets), as well as the competitive and collaborative landscape with other actors. Therefore, task

environment has high importance for firms, and they seek to control this interface by arranging and

coordinating firm activities to fit the prevailing conditions exerted by their task environment (Scott,

2003). Examples of such measures are e.g. securing crucial resources (physical materials, financial and

human capital etc.) and adapting firm strategy to ensure a favourable position in the marketplace.

Task environment is external to firms, and therefore beyond their direct control. Changes to elements of

task environment, e.g. rapid growth or drop in demand for the products of the firm, or availability of

qualified human capital, causes changes and uncertainty for firms (Suarez & Oliva, 2005). Therefore,

5

changes in task environment shape the activities of firms by posing pressures and incentives regarding

competitiveness, efficiency and financial performance (Scott, 2003).

Institutional environment consist of regulative, normative and cultural-cognitive elements, which

promote and sustain desirable conduct of firms (Scott, 2014). First, regulative features of institutional

environment refer to “rules of the game” and governance systems. In order to avoid penalties from

authorities, firms tend to comply with relevant rules and laws. Second, normative features stand for the

perceived appropriateness of firm behaviour and the commitment in following the common values of

the society. Firms are therefore socially obliged to follow expectations of “moral” behaviour in their

relevant surroundings. Third, cultural-cognitive features refer to shared symbolic systems, meanings

and beliefs, which guide the behaviour of firms consciously or unconsciously. Such cultural-cognitive

elements lead firms to mimic “orthodox” behaviour, which derives from taken-for-granted

understanding of what is beneficial for the organization.

The respective institutional environment of firms defines them, as it creates the social meaning of firms

vis-à-vis the broader context of the society (Scott, 2003, 2014). To stay legitimate, firms seek to conform

to surrounding institutions, and changes taking place in institutional environment often lead to changes

also in firms (Mahon & Waddock, 1992). Institutional environment of firms is enacted for instance by

governmental authorities, professional groups and society at large. Governmental organizations, for

instance, can introduce policies designed to either encourage or hinder certain kind of firm behaviour

(Scott, 2003).

In practice, the division between task and institutional environments is not clear-cut. For instance,

technologies are shaped by social intentions and concerns, while markets are embedded in institutional

foundations e.g. in terms of regulations and practices (Pinch & Bijker, 1987; Fligstein & Mara-Drita,

1996). Moreover, governing institutions have co-evolved with certain types of socio-technical systems,

creating strong legitimacy for them, which is one of the reasons for e.g. lock-in to environmentally

harmful energy systems (Unruh, 2000). Hence, the division between task and institutional environments

serves analytical purposes, but does not suggest as simple division in the real world.

6

2.2. Industries and diversification

We understand the O&G industry as an organizational field consisting of firms along a value chain of

extracting oil and gas. These firms consist of various resources related to these operations, such as know-

how, production facilities, customer relations, and production and management capabilities (Penrose,

1959; Barney, 1991; Eisenhardt & Martin, 2000). Firms apply these resources in the industry to create

value and revenue, but they also offer the basis for diversification to new markets.

Generally speaking, firms are more likely to engage in related markets where they can redeploy their

existing resources e.g. in terms of technology (Breschi et al., 2003), suppliers and customers (Nayyar &

Kazanjian, 1993) or manufacturing (Carroll et al., 1996). This offers firms possibilities to realize

synergies and complementarities between their operations in different markets (Tanriverdi &

Venkatraman, 2005), but also a smoother entry and exit of the markets through possibilities to redeploy

resources between markets (Lieberman et al., 2017).

Besides offering new business opportunities, diversification can also act as an opportunity to reduce

dependence on a single market, and enable firms to distribute resources between markets in different

market situations. Bergh and Lawless (1998) suggest that large firms with low levels of diversification

(i.e. firms focused on a single market) tend to invest in other markets when uncertainty in their core

market grows. In other words, such firms often adapt to uncertainty caused by e.g. downturns in demand

by looking into other markets to secure revenue production. Moreover, they are likely to exit from such

alternative markets and refocus back to their core market if uncertainty diminishes and opportunities

there reappear (Bergh, 1998). Hence, changes in the task environment of firms, such as in demand, can

incentivize and/or pressure firms to redeploy resources between markets because the relative

attractiveness of markets can shift over time. High demand in the core market can incentivize firms to

deploy resources into that market; while during downturns there can be pressures to seek opportunities

in other related markets (Helfat & Eisenhardt, 2004; Wu, 2013).

7

Such movement between markets is possible due to ease of resource redeployability between markets

that have similarities e.g. in terms of technology and value chains. Engagement in related markets carry

relatively small transaction costs, as there is limited need to retrain or hire new staff and to reconfigure

equipment to the needs of the new market. This helps the entry to a market, but also enables firms to

reverse their engagement, and refocus back on their core market (Sakhartov & Folta, 2015; Lieberman

et al., 2017). Diversification to alternative markets can therefore act as a relatively easy reorientation

strategy for firms facing uncertainty and diminishing opportunities in their core market.

2.3. Analytical framework

Based on above theoretical perspectives, we present our analytical framework in Figure 1. Our

framework suggests that changes in task and institutional environments of an industry cause pressures

and incentives for incumbent energy industry to respond to new prevailing conditions (cf. Geels, 2014;

Mignon & Bergek, 2016). We focus on one type of response to changes in environment: diversifying to

a related market by redeploying resources to renewable energy market. We also acknowledge that firms

can choose to refocus back to their core market if the pressures and incentives for diversification

disappear (Bergh & Lawless, 1998; Lieberman et al., 2017). Such redeployment behaviour is likely to

be amplified in the case of the energy industries market, where periods of high commodity prices in

hydrocarbons can offer lucrative market opportunities in comparison to renewable energy markets,

characterized with lower profit margins.

8

Figure 1 Analytical framework

3. Methodology

3.1. Case study

Upstream O&G industry in Norway is a complex industrial sector oriented towards identification,

extraction and production of hydrocarbons in offshore conditions, especially in the Norwegian

Continental Shelf (NCS). Extraction of offshore petroleum resources requires high investments of

capital, equipment and knowledge. Key companies are the operators (such as Shell, BP and Statoil)

which are responsible for extracting oil and natural gas from underground repositories. The industry is

disintegrated, meaning that sub-contractors of operators perform most of the activities. Consequently,

there is a substantial network of supplier and service companies that deliver products and services along

the value chain of the industry. In 2014, 1500-2000 Norwegian companies and around 300 000

employees, directly or indirectly, belonged to this industry (Blomgren et al., 2015). Only a small

minority of companies were operators while the rest were various supply and service companies.

9

As a natural resource-based industry that does little refinement of products, the activities and investment

in O&G industry fluctuates considerably with commodity prices. The price for crude oil and gas

influences the revenue of petroleum companies and investments to develop new fields. The relationship

between oil prices and activities is pro-cyclical, which leads to intermittent up and downturns in the

industry. In periods of low oil price, the oil companies (operators) tend to restructure and reduce costs

to keep the productivity and profitability of oil extraction (Grant, 2003). In periods of high oil prices,

the companies often invest in exploration and development activities to maximize the long-term

profitability (Baaij et al., 2011). A drop in oil prices below a given level triggers lower investments

(Tvedt, 2002). Nevertheless, the cyclical nature of the oil industry has this far given relative certainty to

the supply chain that there will be a next upturn (Mohn & Misund, 2009).

3.2. Research design

We investigated the engagement of O&G industry in diversification to OWP during 2007-2016. We did

this by tracing the activities of O&G industry firms over time, to see whether the level of engagement

in diversification followed changes in the task and institutional environment of the industry. In order to

analyse such context dependent processes (Yin, 2009), our empirical work comprised of a case study of

an incumbent industry in its national context, which, however, operates in international markets.

Therefore, we focused our analysis on processes taking place in the domestic environment, but also were

mindful of important developments taking place abroad.

We adopted a qualitative process study approach (Langley, 1999; Van de Ven, 2007). We used our data

material to describe incidents of O&G industry´s engagement in diversification to OWP and parallel

developments in its environment, and analysed them as sequences of events taking place over our study

period (Van de Ven, 1992). Incidents were therefore the basic unit of analysis, and each incident

contained information about firm specific activities in OWP market, answering to questions such as who

did what, and when incidents happened.

10

We used three codes to specify the type of OWP engagement “incidents” that occurred over time: 1)

statements, 2) investments, and 3) contracts in OWP. This way we could track down the “depth” of

engagement in diversification. “Statements” were incidents where the firm had made e.g. a public

statement regarding their interest and entry to the OWP market. Because such statements did not

necessarily entail concrete commitments, we saw these as the ‘weakest’ form of incidents.

“Investments” code stood for investments in future capabilities in OWP market, such as R&D projects,

facilities or specialized OWP companies. “Contracts” were the ´deepest´ form of engagement in OWP,

and were used for all incidents where firms had sold their services and products in the OWP market.

Finally, we used these codes to define significant events taking place in the time series by identifying

patterns and linkages between individual incidents. Each activity or incident could be part of one or

more codes/events (Van de Ven & Poole, 1990).

Due to technological similarities between the markets in some parts of the value chain (see more in

Mäkitie et al., 2018), we assumed that firms are able to redeploy resources between O&G and OWP

markets relatively easily. We also assumed that negative developments in the core O&G market, such

as reduced demand caused by decreasing oil price, translated to fewer market opportunities and thereby

more uncertainty in the task environment. Positive developments (e.g. increasing demand and rising oil

price), on the other hand, meant improved market conditions and lower uncertainty. We also outlined

the key market developments in OWP, where growth in demand acted as an incentive for entry to OWP.

Moreover, we analysed developments in the institutional environment in terms of possible changes in

public legitimacy of O&G and OWP. Due to our interest in sustainability transitions, we focused

especially on legitimacy issues of O&G industry related to climate change. Increase in attention to

climate change and transition perspectives of the O&G industry was therefore assumed as an indication

of weakening public legitimacy of the industry. These indications were compared with attention to

economic factors of O&G industry in relation to employment and social welfare, which are commonly

used by the Norwegian O&G industry in legitimizing itself in public debate (cf. Ihlen & Nitz, 2008).

The economic perspective is therefore used as indication of strengthening public legitimacy.

11

Similarly to e.g. Penna and Geels (2015), we divided the analysis of incidents and events into a sequence

of phases. We defined the phases by identifying significant changes in our three key quantitative data

sources: the number of OWP engagement incidents, Brent oil price and O&G investments in NCS (see

more in the next sub-section). We normalized the different data sources by defining significant change

as 40% of overall range of the respective data series values. We then identified years that had a

significant change from the previous year in one or more indicators: these years were 2009, 2011 and

2015, resulting in four phases. We named the phases based on the analysis of our data on OWP

engagement incidents (see section 4).

3.3. Data

We collected a database of the engagement of 75 Norwegian O&G industry firms1 in OWP market. As

the primary source of data for collecting the OWP engagement incidents of these firms, we used the

media database Atekst/Retriever to search for news from five major Norwegian news media reporting

on O&G industry2. In total, we analysed 698 news articles. We also searched through press releases on

firm websites and analysed annual reports of firms when these were available for the whole study period.

Moreover, we used survey data regarding decisions and timing of entry in the OWP market (more details

in Normann & Hanson, 2015). We collected the name of the company, year, type of engagement

(statement, investment or contract) and described the incident qualitatively. In total, we identified 241

unique incidents of OWP engagement during 2007-2016.

We used two main indicators to describe the task environment developments in the O&G market. First,

average annual price for North Sea oil barrel (Brent), which influences the operator’s decisions to invest.

Second, the total investments in NCS by operators signify the size of the market and demand in O&G

industry. These annual statistics were retrieved from the Norwegian Statistical Agency (SSB) and the

1 Slightly more than 100 O&G industry firms in total have diversified to OWP in Norway. 2 These media outlets were Dagens Næringsliv, Teknisk Ukebladet, Sysla, Offshore, and Petro. We performed individual searches with all 75 firm names and five synonyms for OWP in Norwegian.

12

Petroleum Directorate. To enable comparison of our task environment indicators with the engagement

incidents, we normalized the datasets by calculating the z-score of each variable (x) by using population

mean (µ) and standard deviation (σ).

Additionally, we used data of Wind Europe regarding installed capacity and investments in OWP in

Europe. Finally, to measure changes in institutional environment, we tracked public discussion

surrounding climate change, economy, transitions and O&G industry in Norway by using the

Atekst/Retriever tool3. Moreover, we used prior literature to describe task and institutional environments

for O&G and OWP. We summarize the key concepts, indicators and data in Table 1.

Table 1 Concepts, indicators and data

Definition Indicator(s) Data sources

Task

environment

Material-resource environment

consisting of inputs (resources) and

outputs (markets) of O&G industry

Brent oil price

Investment levels in O&G

in NCS

OWP market in Europe

Statistics Norway

Petroleum Directorate

Wind Europe

Prior studies

Institutional

environment

Regulative, normative and cultural-

cognitive environment of O&G

industry

Legitimacy of O&G

industry

News data (six newspapers)

Prior studies

Engagement in

diversification

The degree of activities of O&G

industry firms in OWP

Engagement incidents of

O&G industry firms in

OWP (3 categories)

News data (5 industry medias)

Annual reports

Firm news

3 We searched news articles in six Norwegian newspapers: Aftenposten, VG, Adresseavisen, Dagbladet, Morgenbladet and Klassekampen. We searched Norwegian equivalent of the words “climate change”, ”jobs”, “employment”, “welfare”, “transition”, “phasing out” and “after oil” together with 16 Norwegian synonyms for O&G industry during 2005-2016.

13

4. Results

The four identified phases in the engagement of O&G industry in OWP were 1) The build-up phase in

2007-2008, 2) First wave of engagement in 2009-2010, 3) Stagnation during 2011-2014 and 4) Second

wave of engagement in 2015-2016. In this section, we present our results in two steps. First, in section

4.1 we put forth an overview of our data, presenting the key variables in our analysis. Second, in section

4.2 we present a more detailed qualitative analysis of our data.

4.1. Overview of results

Figure 2 presents the level of diversification engagement incidents of O&G industry in OWP over time.

The figure illustrates two peaks, in 2009-2010 and 2015-2016, which we call as the first and second

waves of engagement. These two phases are separated by the stagnation period in engagement in 2011-

2014 when the level of engagement remained did not grow.

Figure 2 Engagement of oil and gas industry firms in offshore wind power

8 8

20

35

23 23

15 23

46

34

0

5

10

15

20

25

30

35

40

45

50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Num

ber

of in

cide

nts

2nd wave of engagement

1st wave of engage-ment

Build-up Stagnation

14

Figure 3 outlines key developments in the task environment of O&G industry: Brent oil price and level

of investments in NCS, which are important indicators of the development in the Norwegian O&G

market.

Figure 3 Task environment of firms: oil and gas market (SSB, EIA)

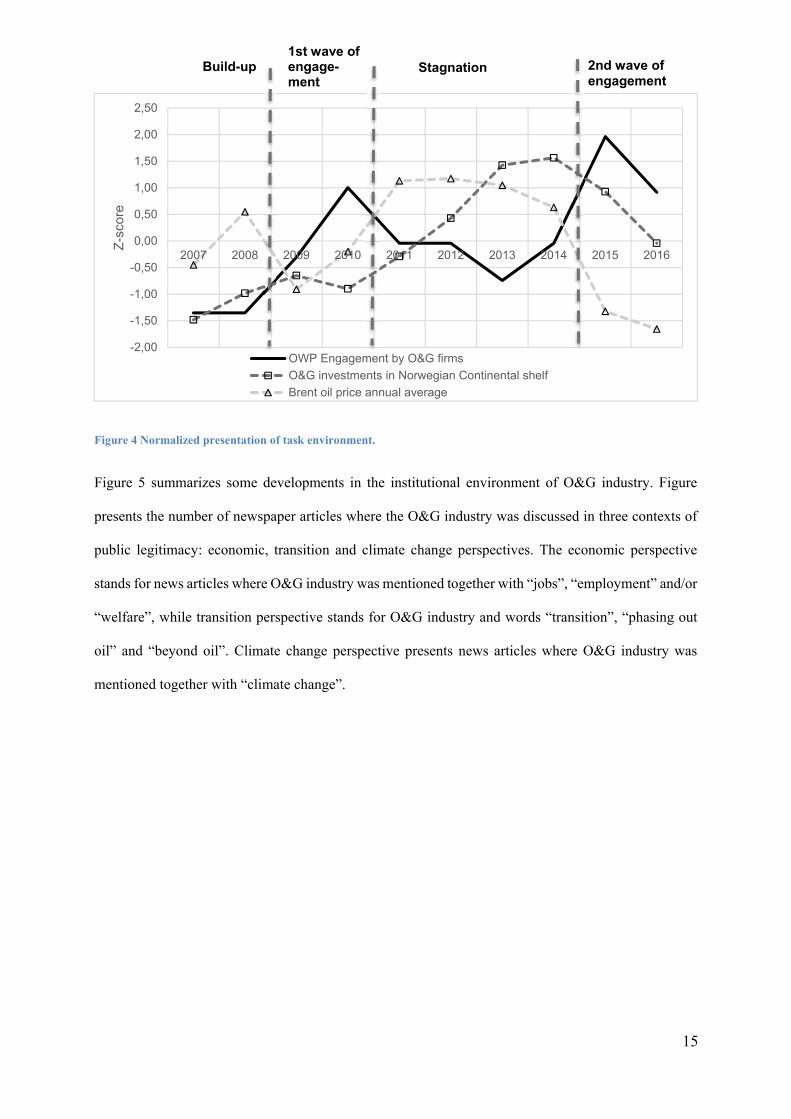

To enable comparison over different scales, we illustrate engagement incidents and task environment

developments in Figure 4 by normalizing changes in variables between 0 and 1. All indicators saw major

fluctuation. During 2009-2010 and 2015-2016, OWP engagement was relatively high with positive z-

scores. As was seen Figure 3, these periods corresponded with downturn in oil price and investment

levels. During Stagnation phase of 2011-2014, the O&G market was booming, while OWP engagement

was relatively low. Hence, higher engagement in diversification in OWP took place when the core O&G

market was declining, while the engagement diminished during O&G boom period.

8192

110

128

140

131

153

179

215 220

197

162

5565

73

97

62

79

111 112

10999

5244

20

40

60

80

100

120

70

90

110

130

150

170

190

210

230

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

US

D (

nom

inal

)

Bill

ions

of

NO

Ks

(nom

inal

)

O&G investments in Norwegian Continental shelf Brent oil price annual average

2nd wave of engagement

1st wave of engage-ment

Build-up Stagnation

15

Figure 4 Normalized presentation of task environment.

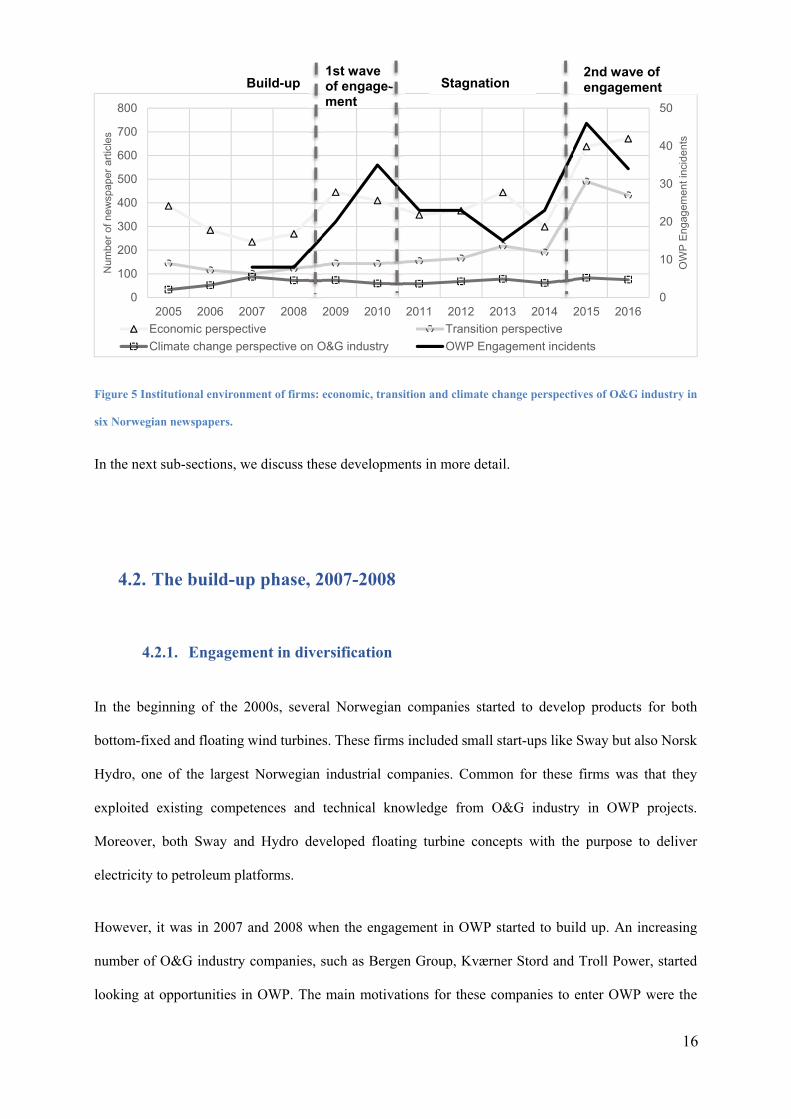

Figure 5 summarizes some developments in the institutional environment of O&G industry. Figure

presents the number of newspaper articles where the O&G industry was discussed in three contexts of

public legitimacy: economic, transition and climate change perspectives. The economic perspective

stands for news articles where O&G industry was mentioned together with “jobs”, “employment” and/or

“welfare”, while transition perspective stands for O&G industry and words “transition”, “phasing out

oil” and “beyond oil”. Climate change perspective presents news articles where O&G industry was

mentioned together with “climate change”.

-2,00

-1,50

-1,00

-0,50

0,00

0,50

1,00

1,50

2,00

2,50

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Z-s

core

OWP Engagement by O&G firms

O&G investments in Norwegian Continental shelf

Brent oil price annual average

2nd wave of engagement

1st wave of engage-ment

Build-up Stagnation

16

Figure 5 Institutional environment of firms: economic, transition and climate change perspectives of O&G industry in

six Norwegian newspapers.

In the next sub-sections, we discuss these developments in more detail.

4.2. The build-up phase, 2007-2008

4.2.1. Engagement in diversification

In the beginning of the 2000s, several Norwegian companies started to develop products for both

bottom-fixed and floating wind turbines. These firms included small start-ups like Sway but also Norsk

Hydro, one of the largest Norwegian industrial companies. Common for these firms was that they

exploited existing competences and technical knowledge from O&G industry in OWP projects.

Moreover, both Sway and Hydro developed floating turbine concepts with the purpose to deliver

electricity to petroleum platforms.

However, it was in 2007 and 2008 when the engagement in OWP started to build up. An increasing

number of O&G industry companies, such as Bergen Group, Kværner Stord and Troll Power, started

looking at opportunities in OWP. The main motivations for these companies to enter OWP were the

0

10

20

30

40

50

0

100

200

300

400

500

600

700

800

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

OW

P E

ngag

emen

t in

cide

nts

Num

ber

of n

ewsp

aper

art

icle

s

Economic perspective Transition perspective

Climate change perspective on O&G industry OWP Engagement incidents

2nd wave of engagement

1st wave of engage-ment

Build-up Stagnation

17

expectations for an international market for OWP, as a slump in the O&G industry and the opportunities

to exploit existing competences in new markets. The build-up phase was characterized especially by

R&D in floating wind power concepts (i.e. deep water OWP turbines) of Hywind and Sway. In 2007,

Hywind, inherited by Statoil from merger with Norsk Hydro, received NOK 59 Million funding from

Enova, a public research agency. Also, Sway raised NOK 150 Million in private investment. In 2008,

Statoil made its first significant breakthrough in their effort to establish itself as an OWP park operator,

and was consented its first park, the Sheringham Shoal in UK.

Such events attracted attention in media and industry, and the involvement of a large player like Statoil

created expectations for further growth in OWP. Also, concrete investments and activities in OWP were

starting to emerge. In our data, however, OWP incidents consisted mainly of statements (eight in total)

and investments (five), while actual contracts were few (three).

4.2.2. Task environment

Since the beginning of the 21st century, the oil price had been growing. Even though new oil and gas

discoveries had been relatively small, the level of investments in NCS was increasing because high oil

price made even smaller and “exotic” oil fields profitable to operate. This increased demand in the O&G

industry, making it an attractive market for suppliers. However, this changed when the financial crisis

of 2008 hit, and sent the Brent oil price from USD 132 per barrel in July 2008 to USD 40 by the same

year’s December.

Since the early 2000s, OWP market has developed mainly in the North Sea with Germany, UK,

Denmark and the Netherlands as the leading countries in innovation (Wieczorek et al., 2013). According

to Wind Europe, more than 300 MWs of OWP was installed in both 2007 and 2008, which were new

records in OWP market and signalled growth in the market.

18

4.2.3. Institutional environment

In 2007, there was a heightened attention to climate change globally and in Norway. However, as was

seen in Figure 5, climate change was seldomly discussed in the context of the O&G industry, even

though fossil fuels are a key reason for anthropogenic climate change. Hence, climate change topic

appears to have been largely separated from the cultural-cognitive understanding of the national O&G

industry. Similarly, Ryggvik and Kristoffersen (2015) argue that historically in conflicts regarding the

pace of oil extraction in Norway, economic interests have prevailed over environmental interests.

Instead questioning the legitimacy of O&G market, the awareness of climate change around 2007-2008

resulted in calls for reductions in emissions and increased investments in renewable energy. Together

with the appointment of a renewable enthusiast as the new Minister of Petroleum and Energy in 2007,

this created expectations among firms for government led support for OWP in Norway (Normann 2015).

4.3. First wave of engagement in OWP, 2009-2010

4.3.1. Engagement in diversification

The years of 2009 and 2010 saw rapid increase of OWP incidents. The engagement in diversification in

this phase was characterized by early market entries and statements (26 in total) as well as investments

(16) in competence and capacity building. In April 2009, Statoil, together with Statkraft, confirmed a

joined investment of NOK 10 Billion in the construction of the Sheringham Shoal wind farm in the UK.

Later the same year, the Hywind turbine became the world’s first full-scale floating wind turbine to

come online in October 2009.

Several O&G industry firms entered in competition for contracts in the European OWP market. For

instance, AF and Dr. techn. Olav Olsen invested in an OWP start-up called ViciVentus, CCB opened a

new base to supply OWP parks in the North Sea, and Draka invested in a new cable production facility

19

to power OWP parks. Meanwhile, Fred. Olsen, a pioneer firm in OWP since early 2000s, continued to

establish their position in the market by e.g. seeking and receiving concessions for OWP farms in

Scotland and Ireland.

In 2010 also some of the first major contracts took place. Aker Verdal, having experienced major

cutbacks following the financial crisis and after going through 2009 without any orders from the O&G

industry, signed a contract in 2010 to supply foundations to the Nordsee Ost OWP farm in Germany.

The large engineering, procurement and commissioning company Aibel received, together with ABB,

a NOK 1.7 Billion contract to build one of the converter platforms in the German project Dolwin.

Moreover, maritime companies such as Seaproof Solutions and Parker Maritime received contracts in

installing OWP parks. Also Draka´s earlier investment in a new production unit started to pay off as the

firm received its first OWP cable contract in November 2010.

4.3.2. Task environment

After the financial crisis and crashed oil price, growth in the Norwegian O&G market came to an abrupt

end. During 2009, the oil price remained relatively low, and this stagnation can be visible in 2010’s

diminished level of investments in NCS (Figure 3). This decline in demand caused problems for many

companies in the O&G industry who had expanded their activities alongside the market growth, forcing

companies to lay off people.

In the meantime, the OWP market continued to mature and grow, opening opportunities for diversifiers

from O&G industry with relevant competences. As described by Kern and colleagues (2014), the UK

developed in a few years from a laggard to a leader in OWP deployment, largely stimulated by changes

of the Renewables Obligation in 2009 and 2010, which offered greater public support to more expensive

technologies. Also in Germany the OWP market began to solidify around 2009 with decisions to

implement new projects, despite also being challenged by limited available financial resources after the

20

crisis (Reichardt et al., 2016). In Norway, the domestic OWP market continued to be non-existent

beyond the mentioned Hywind turbine project.

4.3.3. Institutional environment

Amidst the market downturn and lost jobs, the years 2009 and 2010 saw increased attention to the

economic aspects of the O&G industry (Figure 5). Moreover, politicians as well as industry and media

became even more attentive to how opportunities in offshore wind could offset some of the potential

layoffs in the oil and gas industry. There was considerable interest and efforts to lobby for the

development of a small domestic market, but this did not lead to success e.g. due to lack of collective

action from the side of OWP supporters (Normann, 2015).

4.4. Stagnation phase, 2011-2014

4.4.1. Engagement in diversification

The year 2011 saw reduced engagement in OWP from the previous year, and the growing engagement

from previous years turned into stagnation of OWP activities until 2014 (Figure 2). While some firms

continued investing in competence and capacity building, fewer firms decided to enter the OWP market.

Moreover, some OWP projects ran into trouble. While Sway celebrated the installation of a prototype

of its floating turbine, the company struggled to find customers, and eventually declared bankruptcy in

2014. Aker Verdal, on the other hand, experienced financial losses in its Nordsee Ost project, thus

discouraging further activities in OWP.

However, the few firms who decided to enter during this phase seemed to be able to establish a foothold

in the OWP market relatively fast. For instance companies like Simon Møkster and Siem Offshore

21

invested in OWP installation vessels, while Aqualis acquired two firms with capabilities in OWP.

Moreover, a handful of companies, such as Fred. Olsen and Seaproof Solutions secured contracts to

install OWP turbines, while Fjellstrand and Island Offshore were assigned to deliver OWP vessels.

4.4.2. Task environment

The Brent oil price started to recover to its pre-crisis level already in late 2010, and during the following

years the investment level followed suit. This led to an O&G industry boom period in 2011-2014, during

which oil price stabilized to over USD 110 per barrel, and annual investment levels had doubled by 2014

from its 2008 levels (Figure 3). Another important event was the discovery of two major oil fields in

2010-2011 in the Northern part of North Sea and Barents Sea (Johan Sverdrup and Johan Castberg),

which increased expectations for further growth in the market.

Also the European OWP market continued to grow steadily especially with more developments in the

UK, and according to Wind Europe, nearly 1483 MW of OWP was installed in 2014 in comparison to

874 MW in 2011. This took place despite the fact that, unlike solar power and on-shore wind power, in

2008-2013 the cost of OWP increased. This was because of including e.g. high commodity prices (steel)

and increased project size and complexity, which made OWP less attractive for investments.

4.4.3. Institutional environment

Together with the raising oil price and new discoveries, the political interest in a Norwegian offshore

wind industry also faded away. In comparison, the public legitimacy of O&G market remained robust,

and was not significantly challenged by e.g. climate change concerns. This was illustrated in a 2012

study of climate change perceptions of Norwegian public, where 68% of respondents believed climate

change to be anthropogenic, but only 23% agreed that Norway should not begin extraction from new oil

fields because it contributes to climate change (Austgulen, 2012). These notions suggest that climate

22

change issue had not this far significantly challenged the O&G industry’s cultural-cognitive legitimacy

in Norway.

4.5. Second wave of engagement, 2015-2016

4.5.1. Engagement in diversification

The year 2015 was another turning point in engagement in OWP, as the number of incidents doubled

from previous year. More firms than ever before made investments and/or received contracts in OWP

market during this phase. Especially maritime firms were successful in breaking through with several

contracts in the OWP market. Several shipping and offshore firms, such as Fred. Olsen, Siem Offshore

and Simon Møkster who had invested in OWP vessels before, all secured multiple installation and

service contracts in European OWP parks. Fjellstrand even decided to remodel one of their O&G support

vessels into OWP use.

Firms across the value chain continued investments in new technologies and capacity. For instance,

StormGeo and Dr. techn. Olav Olsen announced new R&D projects, while NorSea bought Danish Øer

to seek foothold in the European OWP market. Moreover, Ulstein invested in developing ship design

tailored for OWP use, and also received contracts for delivering OWP vessels. Meanwhile, Statoil raised

its bets by declaring to build the first floating wind power park in the world in Scotland, and increased

its presence in other OWP parks such as in Dogger Bank in UK and Arkona in Germany.

For the first time, a handful of O&G firms engaged also in new OWP markets in North America and

Asia. For instance, OWP pioneer Fred. Olsen managed to secure contracts in the new OWP parks on

the east coast of United States, and Statoil won a lease to explore building an OWP park outside of

New York.

23

4.5.2. Task environment

In late 2014, the oil price crashed once again, which caused a significant downturn in investment levels

in NCS over the next two years. As this downturn lasted longer than in 2009-2010, it had much stronger

impact on the industry, and significant number of companies went bust and numerous jobs were cut.

Moreover, relatively low commodity prices and increasing costs of developing new fields in the Arctic

Sea have put pressure on the business models of the oil companies and led to an industry wide program

for increased cost-saving and efficiency (FT, 2016). In 2016, more than a quarter of the market had

evaporated since the peak year of 2014 (Figure 3).

In terms of OWP, the European market continued to grow. In 2016 the annual investments in OWP were

around EUR 18.2 Billion (Ho & Mbistrova, 2017), for first time exceeding the size of the Norwegian

O&G market. Moreover, the costs of OWP had fallen substantially, and in 2016 developers such as

Dong Energy and Vattenfall promised to build farms at costs well below than what was expected only

some years ago (The Telegraph, 14 September 2016).

However, by 2016, all initiatives aimed at establishing a full-scale OWP demonstration park in Norway

had failed to attract the necessary public support (Normann, 2017). Therefore, the Norwegian strategy

for OWP has been to support the export of products and services to international markets.

4.5.3. Institutional environment

Since the O&G downturn in 2015, there has been some signs of a change in cultural-cognitive perception

of the O&G industry in Norway. Such change was seen in Figure 5 where in 2015 and 2016 there was

increased attention to transitions and “green shifts” in Norwegian economy. According to Ryggvik and

Kristoffersen (2015), further evidence of such change in perception of O&G market include e.g.

increased knowledge of a potential climate crisis, opposition against oil extraction in Lofoten and

Vesterålen areas, and public statements of notable public figures and organizations emphasizing the

24

potential of green jobs while demanding to leave a large part of Norwegian oil and gas in the ground.

Nevertheless, the O&G still continued to enjoy stable regulative support which has been manifested by

new concession rounds for oil exploration in 2015 and 2017.

4.6. Summary

OWP has been cited as one of the opportunities to redeploy the existing competences and resources in

Norwegian O&G industry, and several firms diversified into this emerging market during 2007-2016.

This is unsurprising, as the international market in OWP has been growing rapidly over the last ten

years, asserting an incentive to enter OWP. Despite this steadily growing incentive to diversify, the

engagement of Norwegian O&G firms in OWP has followed a fluctuating pattern. These developments

co-occur with changes in the O&G market. O&G firms showed increased engagement in OWP in 2009

and 2010 – years that were characterized by lower oil price and decreased activities in the Norwegian

O&G market. In 2011-2014 when the oil price recovered to a high level, O&G investments were soaring

and new oil discoveries were announced, the engagement in OWP reduced. Towards the end of 2014,

the oil price collapsed again and demand in O&G market declined, and OWP saw an unprecedented

amount of activities from O&G firms.

OWP has not enjoyed enough public legitimacy and support for implementing a domestic market in

Norway. The guiding principle for climate policy and renewable energy policy throughout this period

has been that measures should be based on cost-efficiency, resulting in weak policy support for more

expensive technologies such as OWP (Wicken, 2011). Meanwhile, the institutional environment for

O&G has remained rather stable. For instance, environmental concerns such as climate change was

relatively seldom discussed together with O&G industry, even though the climate change issue itself

has attracted plenty of attention over the years. Instead, Norwegian government has steadily opened new

areas for O&G exploration with licensing rounds in 2008, 2010, 2012, 2015 and 2017, signalling stable

regulative conditions for the O&G industry. While recent evidence suggests some changes in public

25

debate regarding the future of the O&G industry, seen overall, the institutional environment for O&G

industry has therefore exerted little pressure on the O&G industry to reorientate and diversify.

Hence, our results suggest that the engagement of O&G industry in OWP has had similar patterns as the

task environment, while there is less symmetry with the developments in the institutional environment.

5. Discussion and concluding remarks

Recent literature regarding sustainable energy transitions has investigated the reorientations of

incumbent energy industries in these processes (Bergek et al., 2013; Steen & Weaver, 2017). Pressures

and incentives from industry environment have been suggested to influence such reorientations (Geels,

2014; Mignon & Bergek, 2016). Such questions are relevant for informing policy mixes which seek to

support a sustainable energy transition by complementing the support of renewable energy technology

development with dismantling support for fossil fuel industries (Kivimaa & Kern, 2016). We contributed

to such discussions with our study of the possible role of industry environment in influencing a

reorientation towards renewable energy markets.

Our case study of the engagement of Norwegian oil and gas (O&G) industry in offshore wind power

(OWP) during 2007-2016 showed notable fluctuations over time. While the institutional environment

surrounding the O&G industry remained fairly stable during this period, and the European OWP market

was on a continued growth path, the O&G industry had two peaks of engagement in diversification in

OWP – “green flings” – separated by a period of lower engagement. These “flings” co-occurred with

two periods of major downturns and a boom period in the O&G market. This suggests that reduced

market opportunities in the O&G market pressured to seek a diversification in OWP, while the

subsequent recovery of the O&G market attracted these firms back to their core market. This behaviour

resembles to what previous literature has discussed as redeployment of resources between related

26

markets in reaction to uncertainty and changes in demand (Bergh & Lawless, 1998; Helfat & Eisenhardt,

2004; Wu, 2013; Lieberman et al., 2017).

We are mindful that our study has some shortcomings which need to be addressed in further research.

First, we recognise that also other mechanisms than pressures and incentives from the environment can

explain diversification. For instance in the case of OWP in Norway, socio-political issues such as public

relations opportunities, national politics and other types of pressures and expectations have affected such

decisions (Hansen & Steen, 2015; Normann, 2015). Moreover, firms can diversify to new and even

unrelated markets without significant influence from environment. Therefore, we have not sought to

deliver a full empirical account regarding the relations of O&G and OWP industries in Norway (see

more in Steen & Hansen, 2014; Mäkitie et al., 2018). Rather, we focused on the issue of the environment

of O&G industry in this phenomenon. Also, we have to a large extent relied on news data to track the

engagement in OWP, which poses significant weaknesses. We are dependent on media outlets,

journalists and firms in their decisions to report on the O&G industry’s engagement in OWP, and this

can cause a bias in our data material. Here we have sought to overcome this weakness by using different

data sources in identifying engagement incidents. The most important drawback is that firms are more

likely to report entry decisions, and our dataset therefore has only few observations of exits from OWP.

Nevertheless, our study has drawn attention to three often overlooked issues in the study of sustainable

energy transitions and related policy topics. First, the study of incumbent industries in transitions has

had relatively little focus on the fact that companies are first and foremost concerned with value creation

and “making money”, where short-term profitability play an important role. Therefore, competition and

market forces “here and now” are important for strategy and activities of firms (Porter, 1980). For this

reason, rapid changes in the market can also cause rapid responses. This has been visible in our case

study where some firms in the O&G industry almost immediately increased their engagement in

diversification in OWP when their core market ran into difficult times. Hence, policy measures

addressing the economic environment of incumbent energy industries can have effective and swift

impacts in causing a reorientation towards renewable energy markets. Such findings support the recent

argument made by e.g. Kivimaa and Kern (2016) that destabilizing policy measures (e.g. through

27

regulation) directed towards the market conditions of incumbent energy industries can help to accelerate

sustainable energy transitions.

Second, as noted also by e.g. Geels and Penna (2015), when incumbent reorientation is triggered by

environment, this engagement can also backtrack when the external pressure diminishes. This was

certainly visible in our study when the O&G industry reduced engagement in diversification during a

boom period in O&G market, even though the OWP market also continued to grow in the meantime.

This finding draws attention to the possible reversibility of industry reorientations towards renewable

energy (cf. Pinkse & van den Buuse, 2012). Our results suggested that several firms in the O&G industry

redeployed resources back to O&G when they were no longer pressured to engage in OWP. This notion

is important in reminding that while market opportunities can act as an effective vehicle of causing

industry reorientation towards renewable energy, favourable conditions accentuating such a transition

can also reverse. Therefore, stable and committed policy measures supporting industry reorientations

have central importance, as such “on-off relationships” or “green flings” of incumbent energy industries

are likely to be harmful for committed push for sustainable energy transition.

Third, the relatively fast reorientation of O&G industry towards OWP showed that at least part of the

industry was able use their existing competences and other resources in another market. We therefore

suggest that redeployment of resources is a key factor in enabling reorientation of fossil fuel industries

towards renewable energy. Such opportunities to make use of the vast resources of incumbent energy

industries can be beneficial in speeding up transitions by making use of e.g. financial resources,

engineering capabilities and tacit knowledge related to technologies, and experience in large-scale

project management (Hanson, 2017).

We conclude by calling for further examinations in the field of sustainable energy transitions literature

in to empirically address the above mentioned three key areas. Moreover, we encourage further study

of intermittency in industry reorientations in order to support policy measures seeking to provide stable

framework conditions for sustainable energy transitions. Finally, we call for conceptual development

28

regarding the issue of resource redeployment between “old” and “new” sectors in the context of

sustainable energy transitions.

References

Austgulen, M. H. (2012). Nordmenns holdninger til klimaendringer, medier og politikk. Retrieved

from Oslo:

http://www.hioa.no/extension/hioa/design/hioa/images/sifo/files/file78213_rapport_climate_cr

ossroads_web.pdf

Baaij, M., De Jong, A., & Van Dalen, J. (2011). The dynamics of superior performance among the

largest firms in the global oil industry, 1954–2008. Industrial and Corporate Change, 20(3),

789-824. doi:10.1093/icc/dtq065

Barney, J. (1991). Firm resources and sustained competitive advantage. Journal of Management,

17(1), 99.

Bergek, A., Berggren, C., Magnusson, T., & Hobday, M. (2013). Technological discontinuities and the

challenge for incumbent firms: Destruction, disruption or creative accumulation? Research

Policy, 42(6–7), 1210-1224. doi:http://dx.doi.org/10.1016/j.respol.2013.02.009

Bergh, D. D. (1998). Product-market uncertainty, portfolio restructuring, and performance: An

information-processing and resource-based view. Journal of Management, 24(2), 135-155.

doi:10.1016/S0149-2063(99)80057-9

Bergh, D. D., & Lawless, M. W. (1998). Portfolio Restructuring and Limits to Hierarchical

Governance: The Effects of Environmental Uncertainty and Diversification Strategy.

Organization Science, 9(1), 87-102. Retrieved from http://www.jstor.org/stable/2640423

Blomgren, A., Quale, C., Austnes-Underhaug, R., Harstad, A. M., Fjose, S., Wifstad, K., . . . Erik, H.

S. (2015). Industribyggerne 2015. Retrieved from

29

Breschi, S., Lissoni, F., & Malerba, F. (2003). Knowledge-relatedness in firm technological

diversification. Research Policy, 32(1), 69-87. doi:http://dx.doi.org/10.1016/S0048-

7333(02)00004-5

Carroll, G. R., Bigelow, L. S., Seidel, M.-D. L., & Tsai, L. B. (1996). The fates of de novo and de alio

producers in the American automobile industry 1885-1981. Strategic Management Journal,

17(SUMMER), 117-137.

Eisenhardt, K. M., & Martin, J. A. (2000). Dynamic capabilities: what are they? Strategic

Management Journal, 21(10-11), 1105-1121. doi:10.1002/1097-

0266(200010/11)21:10/11<1105::AID-SMJ133>3.0.CO;2-E

Fligstein, N., & Mara-Drita, I. (1996). How to Make a Market: Reflections on the Attempt to Create a

Single Market in the European Union. American Journal of Sociology, 102(1), 1-33.

Retrieved from http://www.jstor.org/stable/2782186

FT. (2016). Oil majors’ business model under increasing pressure. Retrieved from

https://www.ft.com/content/cbbf5a16-d17d-11e5-92a1-c5e23ef99c77

Geels, F. W. (2014). Reconceptualising the co-evolution of firms-in-industries and their environments:

Developing an inter-disciplinary Triple Embeddedness Framework. Research Policy, 43(2),

261-277. doi:10.1016/j.respol.2013.10.006

Geels, F. W., & Penna, C. C. R. (2015). Societal problems and industry reorientation: Elaborating the

Dialectic Issue LifeCycle (DILC) model and a case study of car safety in the USA (1900–

1995). Research Policy, 44(1), 67-82. doi:http://dx.doi.org/10.1016/j.respol.2014.09.006

Grant, R. M. (2003). Strategic planning in a turbulent environment: evidence from the oil majors.

Strategic Management Journal, 24(6), 491-517.

Hansen, G. H., & Steen, M. (2015). Offshore oil and gas firms’ involvement in offshore wind:

Technological frames and undercurrents. Environmental Innovation and Societal Transitions,

17, 1-14. doi:http://dx.doi.org/10.1016/j.eist.2015.05.001

Hanson, J. (2017). Established industries as foundations for emerging technological innovation

systems: The case of solar photovoltaics in Norway. Environmental Innovation and Societal

Transitions. doi:http://dx.doi.org/10.1016/j.eist.2017.06.001

30

Helfat, C. E., & Eisenhardt, K. M. (2004). Inter-temporal economies of scope, organizational

modularity, and the dynamics of diversification. Strategic Management Journal, 25(13), 1217-

1232. doi:10.1002/smj.427

Ho, A., & Mbistrova, A. (2017). The European offshore wind industry. Key trends and statistics 2016.

Retrieved from https://windeurope.org/wp-content/uploads/files/about-

wind/statistics/WindEurope-Annual-Offshore-Statistics-2016.pdf

Ihlen, Ø., & Nitz, M. (2008). Framing Contests in Environmental Disputes: Paying Attention to Media

and Cultural Master Frames. International Journal of Strategic Communication, 2(1), 1-18.

doi:10.1080/15531180701623478

Kern, F., Smith, A., Shaw, C., Raven, R., & Verhees, B. (2014). From laggard to leader: Explaining

offshore wind developments in the UK. Energy Policy, 69, 635-646.

doi:10.1016/j.enpol.2014.02.031

Kivimaa, P., & Kern, F. (2016). Creative destruction or mere niche support? Innovation policy mixes

for sustainability transitions. Research Policy, 45(1), 205-217.

doi:http://dx.doi.org/10.1016/j.respol.2015.09.008

Langley, A. (1999). Strategies for Theorizing from Process Data. The Academy of Management

Review, 24(4), 691-710. doi:10.2307/259349

Lieberman, M. B., Lee, G. K., & Folta, T. B. (2017). Entry, exit, and the potential for resource

redeployment. Strategic Management Journal, 38(3), 526-544. doi:10.1002/smj.2501

Mahon, J. F., & Waddock, S. A. (1992). Strategic Issues Management: An Integration of Issue Life

Cycle Perspectives. Business & Society, 31(1), 19-32. doi:doi:10.1177/000765039203100103

Mäkitie, T., Andersen, A. D., Hanson, J., Normann, H. E., & Thune, T. M. (2018). Established sectors

expediting clean technology industries? The Norwegian oil and gas sector's influence on

offshore wind power. Journal of Cleaner Production, 177, 813-823.

doi:https://doi.org/10.1016/j.jclepro.2017.12.209

Mignon, I., & Bergek, A. (2016). Investments in renewable electricity production: The importance of

policy revisited. Renewable Energy, 88(Supplement C), 307-316.

doi:https://doi.org/10.1016/j.renene.2015.11.045

31

Mohn, K., & Misund, B. (2009). Investment and uncertainty in the international oil and gas industry.

Energy Economics, 31(2), 240-248. doi:10.1016/j.eneco.2008.10.001

Nayyar, P., & Kazanjian, R. (1993). Organizing to attain potential benefits from information

asymmetries and economies of scope in related diversified firms. Academy of Management.

The Academy of Management Review, 18(4), 735.

Nilsen, T. (2017). Innovation from the inside out: Contrasting fossil and renewable energy pathways at

Statoil. Energy Research & Social Science, 28(Supplement C), 50-57.

doi:https://doi.org/10.1016/j.erss.2017.03.015

Normann, H. E. (2015). The role of politics in sustainable transitions: The rise and decline of offshore

wind in Norway. Environmental Innovation and Societal Transitions, 15, 180-193.

doi:10.1016/j.eist.2014.11.002

Normann, H. E. (2017). Policy networks in energy transitions: The cases of carbon capture and storage

and offshore wind in Norway. Technological Forecasting and Social Change, 118, 80-93.

doi:http://dx.doi.org/10.1016/j.techfore.2017.02.004

Normann, H. E., & Hanson, J. (2015). Exploiting global renewable energy growth. Opportunities and

challenges for internationalisation in the Norwegian offshore wind and solar energy

industries. Retrieved from

https://www.ntnu.no/documents/7414984/202064323/Norwegian+OWP+and+PV+report++01

.12.2015.pdf/

Penna, C. C. R., & Geels, F. W. (2015). Climate change and the slow reorientation of the American

car industry (1979–2012): An application and extension of the Dialectic Issue LifeCycle

(DILC) model. Research Policy, 44(5), 1029-1048. doi:10.1016/j.respol.2014.11.010

Penrose, E. (1959). The theory of the growth of the firm. Oxford: Blackwell.

Pinch, T., & Bijker, W. E. (1987). The Social Construction of Facts and Artifacts: Or How the

Sociology of Science and the Sociology of Technology Might Benefit Each Other. In W. E.

Bijker, T. P. Hughes, & T. Pinch (Eds.), The Social Construction of Technological Systems.

New Directions in the Sociology and History of Technology. Cambridge, Massachusetts: The

MIT Press.

32

Pinkse, J., & van den Buuse, D. (2012). The development and commercialization of solar PV

technology in the oil industry. Energy Policy, 40, 11-20. doi:10.1016/j.enpol.2010.09.029

Porter, M. E. (1980). Competitive strategy : techniques for analyzing industries and competitors. New

York: Free Press.

Reichardt, K., Negro, S. O., Rogge, K. S., & Hekkert, M. P. (2016). Analyzing interdependencies

between policy mixes and technological innovation systems: The case of offshore wind in

Germany. Technological Forecasting and Social Change, 106(Supplement C), 11-21.

doi:https://doi.org/10.1016/j.techfore.2016.01.029

Ryggvik, H., & Kristoffersen, B. (2015). Heating Up and Cooling Down the Petrostate: The

Norwegian Experience. In T. Princen, J. P. Manno, & P. L. Martin (Eds.), Ending the Fossil

Fuel Era (pp. 249-275): The MIT Press.

Sakhartov, A. V., & Folta, T. B. (2015). Getting beyond relatedness as a driver of corporate value.

Strategic Management Journal, 36(13), 1939-1959. doi:10.1002/smj.2327

Scott, W. R. (2003). Organizations : rational, natural, and open systems (5th ed. ed.). Upper Saddle

River, N.J: Prentice Hall Pearson Education International.

Scott, W. R. (2014). Institutions and organizations : ideas, interests, and identities (4th ed. ed.).

Thousand Oaks, Calif: Sage.

Steen, M., & Hansen, G. H. (2014). Same Sea, Different Ponds: Cross-Sectorial Knowledge Spillovers

in the North Sea. European Planning Studies, 22(10), 2030-2049.

doi:10.1080/09654313.2013.814622

Steen, M., & Weaver, T. (2017). Incumbents’ diversification and cross-sectorial energy industry

dynamics. Research Policy, 46(6), 1071-1086.

doi:https://doi.org/10.1016/j.respol.2017.04.001

Suarez, F. F., & Oliva, R. (2005). Environmental change and organizational transformation. Industrial

and Corporate Change, 14(6), 1017-1041. doi:10.1093/icc/dth078

Tanriverdi, H., & Venkatraman, N. (2005). Knowledge relatedness and the performance of

multibusiness firms. Strategic Management Journal, 26(2), 97-119. doi:10.1002/smj.435

33

The Telegraph. (14 September 2016). New record for cheapest offshore wind farm Retrieved from

http://www.telegraph.co.uk/business/2016/09/14/new-record-for-cheapest-offshore-wind-

farm/

Turnheim, B., & Geels, F. W. (2012). Regime destabilisation as the flipside of energy transitions:

Lessons from the history of the British coal industry (1913–1997). Energy Policy, 50, 35-49.

doi:https://doi.org/10.1016/j.enpol.2012.04.060

Tushman, M. L., & Anderson, P. (1986). Technological Discontinuities and Organizational

Environments. Administrative Science Quarterly, 31(3), 439-465.

Tvedt, J. (2002). The effect of uncertainty and aggregate investments on crude oil price dynamics.

Energy Economics, 24(6), 615-628.

Unruh, G. C. (2000). Understanding carbon lock-in. Energy Policy, 28(12), 817-830.

doi:http://dx.doi.org/10.1016/S0301-4215(00)00070-7

Van de Ven, A. H. (1992). Suggestions for studying strategy process: A research note. Strategic

Management Journal, 13(S1), 169-188. doi:10.1002/smj.4250131013

Van de Ven, A. H. (2007). Engaged Scholarship. A guide for organizational and social research.

United Kingdom: Oxford University Press.

Van de Ven, A. H., & Poole, M. S. (1990). Methods for Studying Innovation Development in the

Minnesota Innovation Research Program. Organization Science, 1(3), 313-335. Retrieved

from http://www.jstor.org/stable/2635008

Wicken, O. (2011). Marked som begrensning for ny kraft [Markets as a restriction for new power]. In

J. Hanson, S. Kasa, & O. Wicken (Eds.), Energirikdommens paradokser: innovasjon som

klimapolitikk og næringsutvikling (pp. 72-81). Oslo: Universitetsforlaget.

Wieczorek, A. J., Negro, S. O., Harmsen, R., Heimeriks, G. J., Luo, L., & Hekkert, M. P. (2013). A

review of the European offshore wind innovation system. Renewable and Sustainable Energy

Reviews, 26, 294-306. doi:10.1016/j.rser.2013.05.045

Wu, B. (2013). Opportunity costs, industry dynamics, and corporate diversification: Evidence from the

cardiovascular medical device industry, 1976–2004. Strategic Management Journal, 34(11),

1265-1287. doi:10.1002/smj.2069

34

Yin, R. K. (2009). Case study research : design and methods (4th ed. Vol. 5). Thousand Oaks, Calif:

Sage.