TIJARA PROVINCIAL ECONOMIC GROWTH PROGRAMpdf.usaid.gov/pdf_docs/PNADS987.pdf · USAID Tijara...

95

TELECOMMUNICATION SERVICES IN IRAQ AND GATS NEGOTIATIONS RECOMMENDATIONS AND IMPACT TIJARA PROVINCIAL ECONOMIC GROWTH PROGRAM May 2009 This report was produced for review by the U.S. Agency for International Development (USAID). It was prepared by The Louis Berger Group, Inc./AECOM International Development Joint Venture. Contract No. 267-C-00-08-0050-00

-

Upload

hoangthuan -

Category

Documents

-

view

217 -

download

3

Transcript of TIJARA PROVINCIAL ECONOMIC GROWTH PROGRAMpdf.usaid.gov/pdf_docs/PNADS987.pdf · USAID Tijara...

TELECOMMUNICATION SERVICES IN IRAQ AND

GATS NEGOTIATIONS RECOMMENDATIONS AND IMPACT

TIJARA PROVINCIAL ECONOMIC GROWTH

PROGRAM

May 2009 This report was produced for review by the U.S. Agency for International Development (USAID). It was prepared by The Louis Berger Group, Inc./AECOM International Development Joint Venture. Contract No. 267-C-00-08-0050-00

USAID TIJARA PROVINCIAL ECONOMIC GROWTH PROGRAM MAY 2009 TELECOMMUNICATION SERVICES IN IRAQ AND GATS NEGOTIATIONS

RECOMMENDATIONS AND IMPACT

DISCLAIMER The author’s views expressed in this publication do not necessarily reflect the views of the United States Agency for International Development or the United States Government.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 i

Table of Contents

1. INTRODUCTION AND METHODOLOGY .......................................... 1

2. SUB-SECTOR CONTEXT IN GATS .................................................. 3

2.1 WTO DEFINITION AND FRAMEWORK .......................................................................3 2.1.1 Content of the Annex on Telecommunications ...............................................................3 2.1.2 Definition of Basic Telecommunication Services ............................................................5 2.1.3 Scope and Coverage of the Fourth Protocol ..................................................................5 2.1.4 Reference Paper on Telecommunications .....................................................................5 2.1.5 WTO Classification ......................................................................................................11 2.1.6 Four Modes of Supply ..................................................................................................12

2.2 WTO MEMBERS AND THE AGREEMENT ON TELECOMMUNICATION SERVICES ......................................................................................................................12

3. THE TELECOMMUNICATIONS SECTOR....................................... 13

3.1 DEFINITIONS. ................................................................................................................13 3.2 TELECOMS IN THE WORLD ECONOMY AND AT THE WTO ...............................14

3.2.1 Telecommunications Data............................................................................................14 3.2.2 Telecommunications Market Trends ............................................................................19 3.2.3 Role of Telecoms in Economic Development...............................................................21 3.2.4 Linkages between Telecommunication Services and Other Sectors ............................22 3.2.5 WTO versus Liberalization/ Privatization of Telecommunication Services....................22 3.2.6 Regulation and Its Importance: Elements to Consider .................................................23 3.2.7 Infrastructures ..............................................................................................................27

3.3 EXAMPLES OF WTO MEMBERS ...............................................................................28 3.3.1 1st Sub-Sector: Voice Telephone Services (A) ............................................................28 3.3.2 2nd Sub-Sector: Packet-Switched Data Transmission Services (B).............................29 3.3.3 3rd Sub-Sector: Circuit Switched Data Transmission Services (C) ..............................30 3.3.4 4th Sub-Sector: Telex Services (D)..............................................................................31 3.3.5 5th Sub-Sector: Telegraph Services (E).......................................................................31 3.3.6 6th Sub-Sector: Facsimile Services (F) ........................................................................31 3.3.7 7th Sub-Sector: Private Leased Circuit Services (G)....................................................31 3.3.8 8th Sub-Sector: Electronic Mail (H) ..............................................................................31 3.3.9 9th Sub-Sector: Voice Mail (I) ......................................................................................32 3.3.10 10th Sub-Sector: Online Information and Database Retrieval (J) .................................33 3.3.11 11th Sub-Sector: Electronic Data Interchange (EDI) (K) ..............................................33 3.3.12 12th Sub-Sector: Enhanced/Value-Added Facsimile Services

(Incl. Store and Forward, Store and Retrieve (L)..........................................................33 3.3.13 13th Sub-Sector: Code and Protocol Conversion (M) ..................................................33 3.3.14 14th Sub-Sector: Online Information and/or Data Processing

(Incl. Transaction Processing) (N)................................................................................33 3.3.15 15th Sub-Sector: Other (O) ..........................................................................................33 3.3.16 State of Play of the Telecommunication Sector in the Benchmarked Countries ...........35 3.3.17 GATS Commitments on Telecoms vs. Services Efficiency...........................................41

4. THE IRAQI TELECOMMUNICATIONS SECTOR ............................ 42

4.1 ECONOMIC, SOCIAL AND REGULATORY ENVIRONMENT ............................. 42 4.2 THE IRAQI TELECOMMUNICATIONS SECTOR................................................. 42

4.2.1 Background..................................................................................................................42 4.2.2 Legal Framework .........................................................................................................43 4.2.3 Communications and Media Commission of Iraq .........................................................43 4.2.4 Equipments and Networks in Iraq ................................................................................44

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 ii

4.2.5 The Iraqi Telecommunications Market .........................................................................44 4.2.6 Role of the Iraq’s Private Sector...................................................................................47

5. RECOMMENDATIONS ON IRAQI POSITIONS ON GATS / TELECOMMUNICATIONS SERVICES NEGOTIATIONS................ 48

5.1 RECOMMENDATIONS ON TELECOMMUNICATION SECTOR UNDER GATS..48

5.2 TELECOMMUNICATIONS SERVICES: REFERENCE PAPER ..............................54

5.3 PRECONDITIONS TO TELECOMMUNICATIONS LIBERALIZATION ...................57

6. IMPACT OF GATS / TELECOMMUNICATION SERVICES IN IRAQ……………………………………………………………………..59

6.1 ECONOMIC IMPACT.....................................................................................................59 6.2 SOCIAL IMPACT............................................................................................................60 6.3 ENVIRONMENTAL IMPACT ........................................................................................61

BIBLIOGRAPHY………………………………………………………………………………….…62 ANNEX: NATIONAL COMMITMENTS OF BENCHMARKED COUNTRIES ………………..64

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 iii

ACRONYMS ADSL Asymmetric Digital Subscriber Line ASCCI American Standard Code of Information Interchange CMC Communications and Media Commission CSD Circuit Switched Data COSIT Central Organization for Statistics and Information Technology CPA Coalition Provisional Agency CW Continuous Wave EDI Electronic Data Interchange EU European Union FDI Foreign Direct Investment FOG Fiber Optic Gulf GATS General Agreement on Trade in Services GATT General Agreement on Trade and Tariffs GDP Gross Domestic Product GOI Government of Iraq HSPA High Speed Packet Access ICT Information and Communication Technologies IMF International Monetary Fund IQR Iraqi Dinar ISP Internet Services Provider IT Information technologies ITPC Iraqi Telecommunication and Post Company ITU International Telecommunications Union KRG Kurdistan Regional Government LTE Long Term Evolution MFN Most Favored Nation MENA Middle East and North Africa MoU Memorandum of Understanding MVNO Mobile Virtual Network Operators NRA National Regulatory Agency OECD Organization for Economic Co-operation and Development PCN Personal Communication Systems PSTN Public Switched Telephone Network PTN Public Telecommunications Network PTO Public Telecommunications Operator RIO Reference Interconnection Offer SME Small and Medium Enterprise TDMA Time Division Mobile Access TRIPS Trade Related Intellectual Property Rights UAE United Arab Emirates UK United Kingdom UNCTAD United Conference on Trade and Development USAID United States Agency for International Development USD US Dollar VoIP Voice over Internet Protocol VSAT Very Small Aperture Terminal WCDMA Wide band Code Division Multiple Access WLL Wireless Local Loop WTO World Trade Organization

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 1

1. INTRODUCTION AND METHODOLOGY The purpose of this series of documents on various sub-sectors under services is to prepare the Government of Iraq (GOI) for the submission of the services chapter to the World Trade Organization (WTO). It also seeks to assist the GOI to better understand the context in which each sub-sector operates in the economy. WTO accession is hardly an end in itself. Instead, WTO Accession is the beginning of a process of serious economic reform. Accession to the “club” of WTO requires serious commitments to liberalization, as well as an understanding of the impact of these commitments on the economy at large and its broader benefits. Each of the sub-sector reports is broken into five parts:

1. Introduction and methodology – the key analytical elements applicable to the sub-sector;

2. Sub-Sector Context within the General Agreement on Trade in Services (GATS) and Value Chain Development – the sub-sector in the context of GATS, international best practices, and value chain development of the sub-sector;

3. Iraq and the role of the specific sub-sector, including the regulatory environment, data, and the role of the private sector in WTO negotiations;

4. Recommendations for Iraq in the negotiations of the sub-sector;

5. A general discussion of the impact of the proposed liberalization commitments on Iraq in the sub-sector.

Section 2 describes the framework, or the “lens” through which the Iraqi Government Services Committee should consider in the analysis of their sector. The WTO framework, its modes, horizontal commitments and value chain underpin the essence of preparation, and are the main content of impact analysis. Sections 3-5 provide a more detailed analysis of the sub-sector itself and its role and overall impact on the Iraqi economy. There are five key methodological tools and concepts used to analyze the role of services in Iraq. These include:

a. WTO framework (definition of “modes”);

b. International best practices;

c. Regulation;

d. Mode analysis;

e. Most Favored Nation (MFN) status, National Treatment and Market Access. In each case we need to make sure that the GOI clearly understands the framework and context of the sub-sector analyzed and its relationship to the Four Modes contained in GATS. Iraq applied for WTO accession in December 2004 and submitted a Memorandum on the Foreign Trade Regime in September 2005. The Working Party met for a second time in April 2008 to continue the examination of Iraq’s foreign trade regime, however Services negotiations did not commence.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 2

This study has been prepared as a background paper supporting Iraq’s accession to the WTO. As part of the WTO accession process, Iraq must negotiate offers/commitments for Trade in Goods and for Trade in Services. The Iraqi Services sector is likely to be of particular interest to WTO members, due to its significant economic potential. An extensive consultation process underpins this study, which involved attending relevant meetings to make presentations and exchange information, meeting with experts in the government and civil society, and undertaking dialogue in an electronic discussion. This study will be presented at various meetings of the GOI Services Committee. In addition to this paper, there are several lengthy presentation materials prepared by the Trade Division that will discuss various aspects of this paper in greater detail. Working Committee meetings will include members of civil society, as well as trade negotiators from Iraq. In the writing of this paper, consultation was undertaken in the form of face-to-face meetings with a range of stakeholders representing national and regional organizations.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 3

2. SUB-SECTOR CONTEXT IN GATS 2.1 WTO DEFINITION AND FRAMEWORK

The telecommunications sector presents a unique case in GATS negotiations, due to its dual role as both a backbone for other services and as a service in itself. WTO Negotiations on telecommunications have started in 1986 and lasted for 11 years until 1997. During the Uruguay Round, the telecommunications sector became one of four services sectors where an agreement has not been reached by the Round’s closing deadline in 1994. The WTO members reached only an ‘in principle’ agreement for freer market access and liberalization of basic telecommunication services. A number of individual commitments were made in the supply of value-added or enhanced services, but only a few members, such as the United States, were willing to make specific commitments in basic telecommunications services.1 Extended negotiations on basic telecommunications services continued in 1994-1997, primarily through the specially created Negotiating Group on Basic Telecommunications, Since then, new commitments have been made either by new WTO members upon accession, or in a unilateral fashion by existing Members. The following three documents currently comprise the core texts relating to trade in telecommunications services: 1. The Annex on Telecommunications2 – signed April 1994, at the conclusion of the

Uruguay Round. This annex deals with specific issues pertaining to trade in telecom services – most importantly with access to public networks. It provides a guarantee that a supplier of any service would have the right to use public telecommunications networks and services within a given member country. (See section 2.1.1 for discussion.)

2. The Fourth Protocol to the General Agreement on Trade in Services3 – signed on April 30, 1996 and entered into force on February 5, 1998. This document provides the legal basis for the annexation of new basic telecommunications schedules to the Uruguay Round services schedules. (See section 2.1.3 for discussion.)

3. The Reference Paper on Telecommunications4 – adopted during the negotiations of the Fourth Protocol in 1996. The paper provides a set of regulatory principles and commits Members to market policies that promote competition.

2.1.1 Content of the Annex on Telecommunications

The key aim of the Annex on Telecommunications is to establish the right of a service supplier to use telecommunications networks and services. The Annex guarantees that suppliers of all liberalized commercial services – financial, professional, or any others falling 1 Within GATS, telecommunications services are broken into two categories. “Basic services” are understood to include all telecommunication services, both public and private, that involve end-to-end transmission of customer and supplier information. “Value-added services” are understood to denote telecommunications for which the supplier “adds value” to the customer's information by enhancing its form or content, or by providing for its storage and retrieval. Examples of value-added services include: e-mail; voice mail; facsimile and database retrieval, electronic data interchange; enhanced facsimile services (including store and forward, store and retrieve fax); code and protocol conversion; online information and/or data processing (including transaction processing). 2 More information available at: www.wto.org/english/tratop e/serv e/12-tel e.htm 3 More information available at: www.wto.org/english/tratop e/serv e/4prote e.htm 4 More information available at: www.wto.org/english/tratop e/serv e/telecom e/tel23 e.htm

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 4

within the GATS ambit – have reasonable and nondiscriminatory access to public telecommunication networks within the borders of WTO Members that made telecommunications commitments. The access is guaranteed for all communications and commercial purposes.5 This guarantee translates into the ability of a foreign service provider to enter the country and connect to its public network for the purpose of offering a service to consumers in that market. The Annex is a document balancing user rights and regulatory rights. Access to telecommunication networks is guaranteed regardless of whether the networks are privately or publicly owned and regardless of whether they are monopolies. Access is conditioned in certain prudential circumstances, such as for the purposes of protecting the public operator, restraining companies from illegal competition or preserving network integrity.6

• Obligations

The Annex broadens the scope of the obligations required from GATS members, with regard specifically to telecommunications. It includes commitments regarding transparency, access to public networks, and treatment of developing countries. However, by the terms of the Annex, these obligations apply only to services for which Members have scheduled a market access commitment.

• The transparency provision outlines what telecommunications information should be made publicly available: all tariff and non-tariff conditions of service, licensing requirements, conditions for interconnection, technical interconnection specifications, and standards affecting access and use of public networks.

• The provision on access to public telecommunications networks involves the right to buy and use equipment needed to connect to the network, to connect private circuits with the public system or with other circuits, and to use the public network to transmit information, including information from computerized databases, both within the country concerned and to or from any other WTO member. Such access should be granted on the basis of the Most Favored Nation (MFN) and national treatment.

• Other provisions call for Members with more developed telecommunications systems to share technical information and use special consideration with developing countries.

• Exceptions

In line with a government’s right to regulate its domestic basic telecommunications market, it may need to put certain limitations on its obligations so that it is able to ensure the security and confidentiality of message content, to protect the technical integrity of the public network, to provide or continue to provide universal services, and to maintain efficient technical operations.

• Relation to International Organizations

The Members recognize that there are several international organizations that set telecommunications standards. Most of the standard-setting is regulatory in nature,

5 The Annex offers a definition which essentially incorporates access to the public telecom infrastructure which permits services offered to the public, generally e.g. telegraph, telephone, telex and data services 6 Rights under the Annex apply to all available public services such as telephone, telegraph, telex and data transmission, but do not apply to measures affecting the cable or broadcast distribution of radio or programming television.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 5

addressing the need for interconnectability among different types of information, such as voice, video and data, and over different types of networks, such as land-line, satellite and radio. For instance, the International Telecommunication Union (ITU)7 sets standards for shared telecommunications resources such as radio frequencies and the geostationary stationary orbit for satellites. Additionally, the Members “recognize the role played by intergovernmental and non-governmental organizations and agreements in ensuring the efficient operation of domestic and global telecommunications services, in particular the International Telecommunication Union.”

2.1.2 Definition of Basic Telecommunication Services

After the Uruguay Round, negotiations on telecommunications continued, with a focus on basic telecommunication services. These negotiations led to the adoption of the Fourth Protocol in April 1996 (in force February 1998). Basic telecommunication services include all telecommunication services, both public and private, that involve end-to-end transmission of customer and supplier information. They are defined as “voice and non-voice services consisting of the transmission of information between points specified by a user in which the information delivered by the telecommunications agency to the recipient is identical in form and content to the information received by the telecommunications agency from the user.” Examples of such services include voice telephone services, packet switched data transmission services, circuit-switched data transmission services, telex services, telegraph services, facsimile services, privately leased circuit services, or mobile services.

2.1.3 Scope and Coverage of the Fourth Protocol

Schedules of Specific Commitments and Lists of Exemptions from Article II of the GATS concerning basic telecommunications are annexed as the Fourth Protocol (also known as the Basic Telecommunications Agreement.) The Fourth Protocol encompasses members’ commitments on basic telecommunication services in three areas: • Provided through cross-border supply, • Provided through the establishment of foreign firms, or • Provided through commercial presence, including the ability to own and operate

independent telecom network infrastructure.

2.1.4 Reference Paper on Telecommunications

The key goal of the Reference Paper on Telecommunications, adopted simultaneously with the Fourth Protocol in 1996, is to ensure that Members adopt policies that permit competition. The signing of the Reference Paper was a response to Members’ concern during the Uruguay Round that commitments to competitive telecommunications market will be hard to enforce when monopolistic national telecommunications providers (generally government-owned) are dominant. Adopting the Reference Paper was an attempt by the Members to address some of the specific domestic barriers most frequently faced by service providers when they attempt to access the network of domestic Public Telecommunications Operators8. 7 See the International Telecommunication Union website: www.itu.int. 8 Taunya L. McLarty: “Liberalized Telecommunications Trade at the WTO: Implications for Universal Service Policy,“Federal Communications Law Journal, Vol. 51, 1998.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 6

The Reference Paper, which could be added onto a Member’s schedule, allowed the member to adopt “additional commitments” to competitive regulatory principles. This approach is very flexible, allowing each country the option to freely undertake additional commitments. The Reference Paper is a short document with 3 main characteristics: 1. It does not have any legal status and is not considered a binding agreement. Its primary

purpose is to provide WTO members with a framework for defining additional commitments on regulations. However, additional commitments made by members as part of services schedule become part of the national commitment lists and are binding.

2. The document is general: it contains principles on sector regulation but no detailed rules. 3. It describes results to obtain but not the means to be implemented. By doing so, it

provides some flexibility in its implementation. The Reference paper includes some definitions and principles on key issues on telecommunication regulation: • Competitive safeguards, meaning disposals to prevent abuse of dominant position • Interconnection to public networks • Universal service • Licenses delivery • Independence of the regulator • Allocation of scarce resources • Transparency

A comprehensive approach to regulatory reform was needed, in part, because laws and regulations covering telecommunications in most countries tend to be anticompetitive in nature, due to the fact that the telecommunications market has historically been monopolized by the state. Additionally, telecommunications services are different from goods that require little interaction between the provider and the country’s regulators beyond the country’s borders. In the case of telecommunications, the service provider continues to have significant interaction with regulators once inside the borders of a country. Over 75 countries that have signed the WTO agreement also accepted the “Reference Paper” on regulatory principles in February 1997.9 Some of the Members adopted the Reference Paper in whole, while others specified certain exceptions to elements of the Paper, which were also attached in their schedules.

• Competitive safeguards

To avoid anticompetitive effects, the Members are to ensure competitive safeguards, by preventing the dominant supplier from (1) engaging in anticompetitive cross-subsidization; (2) using information with anticompetitive results; and (3) withholding technical information that is necessary for an entrant to compete. Nondiscrimination safeguards are supposed to be implemented by Members. Safeguards are rules that prevent the dominant carrier from abusing its market power against potential entrants. Abusive actions would include: the cross-subsidization of competitive service with revenues from noncompetitive public network services; the overcharging of competitors for

9 Patrick XAVIER, Swinbure University of Technologies, Melbourne: International Benchmarking in the context of WTO Commitments, ITU Workshop, February 2008

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 7

access to the Public Telecommunications Network (PTN); and discrimination in giving access to or information about the PTN. Additionally, interconnection regulations control the access to the network for the origination or termination of telecommunications services. Interconnection may be network-to-network or network-to-service provider. If the terms of interconnection are subject to private party negotiations, the interconnection policies must force the dominant carrier to negotiate in an open, economical, and cost-based manner. Some countries are taking a sector-by-sector approach for these commitments. The Reference Paper sets out the general prohibition on cross-sector subsidization, but it does not set the specific initiatives that have to be taken in order to ensure competition. However, a fully competitive policy would require service providers to keep separate accounts and would allow tariff rebalancing.

• Interconnection to public networks

Facilities competition exists when new entrants, who can meet a reasonable and objective set of standards, are allowed to interconnect to the public network and provide services to end users in competition with Public Telecommunication Operators. To have full facilities competition, however, new entrants must be given interconnection rights broader in scope than simply interconnection to the public networks. Optimal market access depends on multiple options: interconnecting to private and public networks, leasing available circuits, sharing leased circuits, interconnecting between leased and switched networks, and reselling transmission capacity. Additionally, the terms of interconnection must provide adequate technical interface, provide adequate usage and supply conditions, and be based on competitive tariffs. These liberalized interconnection rules are especially important to the international cellular market, which has had an appreciable impact on communications technology. Cellular service providers, which provide radio-based services, depend heavily on local exchange carriers and interexchange carriers to connect the land line system with the cellular system. The Reference Paper sets the interconnection framework. Interconnection is a mixture of legal and technical rights and obligations. The Reference Paper deals with the fundamental interconnection matters that should be included in telecommunications legislation and sets forth some details for a legal model of legislation in the area. Interconnection must be done on nationally-based MFN principles. Interconnection with a major supplier will be ensured at any technically feasible point in the network. Such interconnection is provided as follows:

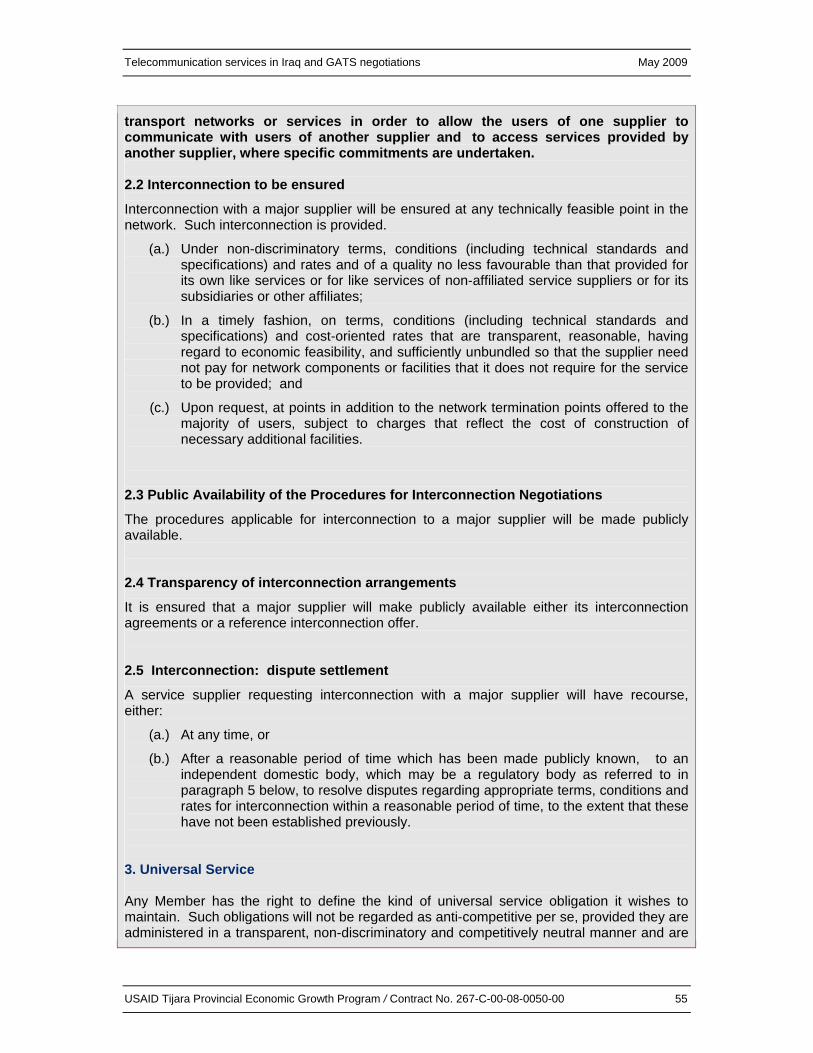

• On a non-discriminatory basis and at cost-based rates. The quality of interconnection provided to third parties should be no less favorable than that provided by the operator for the country’s own similar services, or for similar services of non-affiliated service suppliers, or for its subsidiaries or other affiliates;

• In a timely fashion, on terms, conditions (including technical standards and specifications) and cost-oriented rates that are transparent, reasonable, having regard to economic feasibility, and sufficiently unbundled so that the supplier need not pay for network components or facilities that it does not require for the service to be provided; and

• Upon request, at points in addition to the network termination points offered to the majority of users, subject to charges that reflect the cost of construction of necessary additional facilities.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 8

The procedures applicable for interconnection to a major supplier will be made publicly available. It is ensured that a major supplier will make publicly available either its interconnection agreements or a reference interconnection offer (RIO). The interconnection regime should also provide a right of arbitration to the regulatory authority to resolve disputes regarding interconnection, with the right to appeal to ordinary courts against the decisions of the regulator. On dispute settlements, a service supplier requesting interconnection with a major supplier will have recourse, either (a) at any time, or (b) after a reasonable period of time (which has been made publicly known), to an independent domestic body (which may be a regulatory body) to resolve the disputes regarding appropriate terms, conditions and rates for interconnection within a reasonable period of time, to the extent that these have not been established previously. Finally, important but often overlooked provisions in a national telecommunications law, which is key for realizing interconnection, are provisions regarding inter-operability.

• Universal service

A common reason cited for failure to liberalize the telecommunications sector is that some goals of universal service, such as providing basic telephone services to rural or low-income areas, would not be met in a fully competitive environment. Under the Reference Paper, each country can define its own objectives for universal service. Conceivably, steps taken to implement an aggressive universal service program that has the government taking the lead role could run contrary to most of the commitments in the Reference Paper, including licensing, interconnection, allocation of spectrum, and independence of the regulatory body. The Member can take action, however, to implement such a program and the action will not be considered anticompetitive per se, as long as it is administered in a neutral manner and is “not more burdensome than necessary.” If necessary is interpreted in the same way it has been interpreted for the GATT, Article XX exceptions, then the universal service exception will rarely be used successfully. Under GATT’s Article XX test of necessary, the means of implementing a domestic universal service policy could not be inconsistent with the underlying GATS principles of MFN treatment, transparency, national treatment, and market access. Presumably, though, the strict GATT test would apply only to the restrictive trade measures inconsistent with a general obligation of GATS that has not been exempted in a Schedule or with a specific commitment that has been included in a Schedule. Universal service is one of the most significant issues driving domestic basic telecommunications policy. It is an especially pressing goal for developing countries. One of the most significant challenges faced by developing and emerging countries is their lack of comprehensive infrastructure that will provide, at a minimum, basic services. There are traditional ways of addressing this hurdle, namely, maintaining government operation of the infrastructure or subsidization of the services. Alternatively, there are some newly emerging ways to address the need for basic services, such as encouraging multinational conglomerates to finance telecommunications projects in developing countries or allowing revenue from liberalized international trade in services to finance the developing country’s domestic market need for telecommunications infrastructure. Countries are essentially on their own when they keep policies in place that make the government the sole provider of basic telecommunications services. In order to implement a universal service program domestically, a government could take a variety of approaches, but most of these will not be consistent with the spirit of GATS or the 1997

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 9

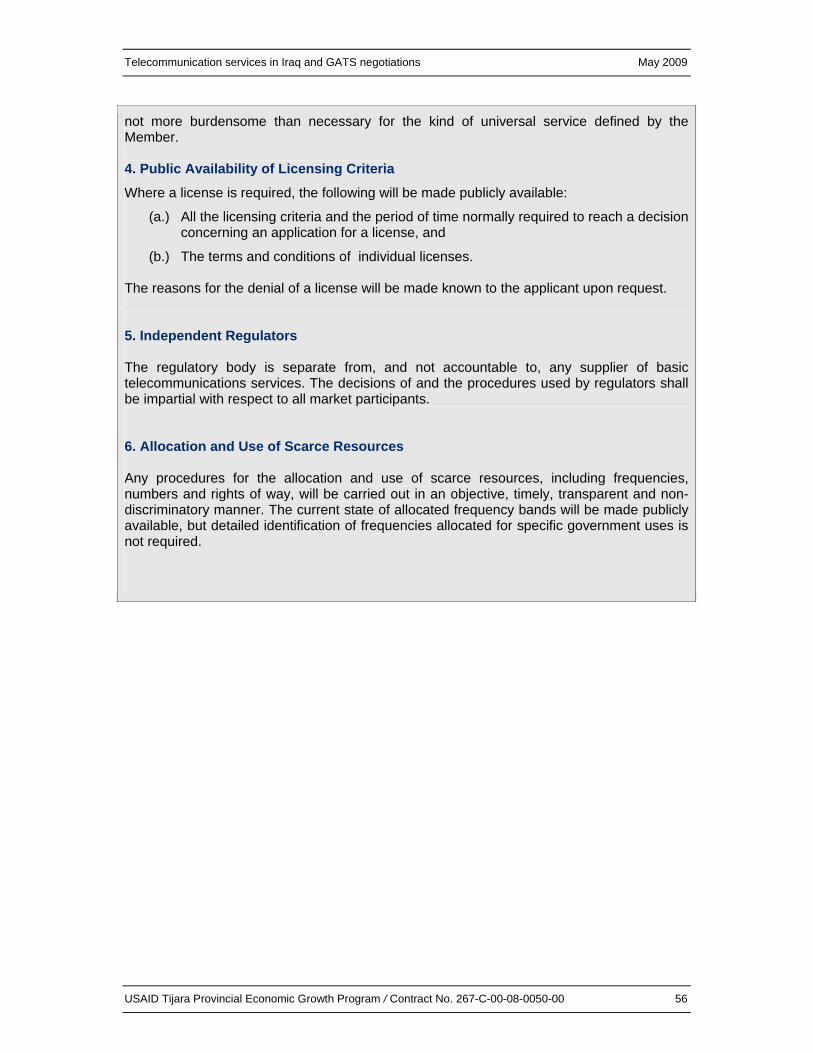

Telecommunications Commitments. For instance, owning the telecommunications infrastructure and cross-subsidizing the economically disadvantaged classes in society is not consistent with the Reference Paper, and socializing a private market through tax-funded subsidies may not be consistent with future negotiations on subsidies under GATS. Another option is for foreign conglomerates to finance the infrastructure costs. To address the financial hurdle faced by such projects, the International Telecommunication Union10, in partnership with the private sector, established WorldTel11. WorldTel functions much like an international development bank that finances telecommunications and information technology projects. Equity partners of the bank are other financial organizations, the private sector, and institutional investors. However, these resources are not widely available to the majority of countries, and WorldTel projects will not set the stage for a comprehensive telecommunications policy to meet consumer demands for basic and enhanced services. A third option is to deregulate the market domestically, while negotiating market access and nondiscrimination internationally. Essentially, counting on market supply to meet the broad spectrum of technical and social demands will result in more universal service of basic telecommunications by promoting economic efficiency and technological advancement. Generally speaking, universal service will be provided by a designated operator. That operator will have, as part of its license, an obligation to provide universal service as defined by the government. Usually the obligation to provide universal service is funded through a common fund to which all operators who offer “a public service” contribute. The method by which those other operators contribute to the fund should be set forth in the law. The amounts contributed to the universal service fund may not be the same from each operator, as long as any terms of contributing to the fund by each operator are fairly applied and are transparent. It could be expected that newly-formed regulators will need training in the area of basic accounting in order to manage the universal service fund. While this is not addressed specifically by the Reference Paper, it is an important feature for the successful provision of universal service.

• Licenses delivery

In the licensing process, new entrants often face both technical and procedural barriers. The technical barriers are loosely addressed in GATS. Article VI requires Members to ensure that “measures of general application affecting trade in services are administered in a reasonable, objective and impartial manner”; to ensure that licensing schemes or other such qualification requirements are administered in a manner that is fair to the applicants and are based on standards that do not nullify specific sectoral commitments; and to put in place, when practicable, a mechanism for review of administrative decisions that affect a provider’s ability to supply services. The Recognition provision of GATS, Article VII, says that the domestic body with the authority to review a license application should not use technical or nontechnical criteria as a “disguised restriction” on trade in services. The Reference Paper further requires the domestic regulatory body to provide the criteria, terms and conditions, and reasons for the denial of a license application. 10 http://www.itu.int 11 http://www.world-tel.com

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 10

This GATS Article on “recognition” distinguishes between the substance of the criteria and the procedure by which the criteria are implemented. Article VII does not attempt to dictate what the specific criteria or standards for operation must be, so it is less strict than the technical barriers to trade limits under the GATT. The Article allows Members to impose autonomously their standards and criteria for denying certifications or licenses. Thus, the substance of the policies can be discriminatory if the discriminatory policies are included in the Member’s Schedule. After ten years, when these discriminatory practices are to be phased out, the discriminatory policies potentially could be refashioned into a statement of “technical integrity” for the Members’ services. Article VII encourages Members to recognize as sufficient the criteria already met by a service supplier under another Member’s standards. Preferably, Members should agree, in a multilateral forum, to use internationally recognized criteria for licensing. However, where this option is not practical, Members may enter into bilateral arrangements for mutual recognition criteria, or a Member may continue to set its standards unilaterally. Procedurally, however, the criteria for the licensing or certification of a service supplier cannot be applied in such a way that would discriminate between countries or that would constitute a disguised restriction on trade.

• Independence of the regulator

There needs to be independence between the telecommunications regulators and the telecommunications service providers. While the rules must be accessible to the private sector, the regulators must be detached, that is, have no economic or political interest in the outcome of making rules, granting and renewing licenses, reviewing supplier agreements, resolving disputes, and applying sanctions. The Reference Paper further requires “the regulatory body [to be] separate from, and not accountable to, any supplier of basic telecommunications services.” GATS requires the Members to “maintain or institute as soon as practicable judicial, arbitral or administrative tribunals or procedures which provide, at the request of an affected service supplier, for the prompt review of, and where justified, appropriate remedies for, administrative decisions affecting trade in services.” The Reference Paper requires that an effective appeal procedure be in place and that the decisions be “impartial with respect to all market participants.”12

• Allocation of scarce resources

In many cases, newly formed regulatory bodies have little if any experience in the area of frequency management. While the responsibilities of the regulator regarding frequency are well known, and include spectrum planning (including liberating and allocating specialty services, licensing of spectrum and monitoring compliance with spectrum use), new regulatory agencies may not necessarily have the capacity, either in terms of knowledge or experience, to meet these demands. While it may not be necessarily included in a telecommunications law, an important factor regarding frequency management is ensuring the technical capacity of the regulator in order for it to meet its mandate. This provision is intended for allocations of resources such as radio spectrum. The commitments of the Reference Paper, including licensing and interconnection, apply to all sectors, including spectrum management, but this paragraph will allow Parties to make their initial decisions about spectrum allocation apart from the underlying principles of GATS, that is, they can be discriminatory.

12 Patrick XAVIER, International Benchmarking in the context of WTO commitments, ITU workshop

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 11

Thus, the management of scarce public resources, such as the radio spectrum, public rights of way, poles and masts, numbers, domain names, facility sights, and co-location premises must be:

• Non-discriminatory, • Transparent, and • Provided in objective and timely manner.

• Transparency

Members must make available to the public:

• Laws, regulations and administrative guidance

• All licensing criteria

• Information concerning access to and use of the public telecommunication network (including relevant license or concession provisions)

• Tariffs and all terms and conditions of service

• Conditions regarding attachment of terminal equipment

2.1.5 WTO Classification

Telecommunication services are addressed in a GATS Chapter named “Communication Services”, which also includes Postal and Courier services as well as Audiovisual services. The classification system used in the GATS by WTO members divides Telecommunication Services (2C) into the following categories: C. Telecommunication services

a. Voice telephone services b. Packet-switched data transmission services c. Circuit-switched data transmission services d. Telex services e. Telegraph services f. Facsimile services g. Private leased circuit services h. Electronic email i. Voice mail j. On-line information and data base retrieval k. Electronic data interchange (EDI) l. Enhanced / value added facsimile services, incl. store and forward, store and retrieve m. Code and protocol conversion n. On-line information and /or data processing (incl. transaction processing) o. Other

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 12

2.1.6 Four Modes of Supply

Trade in services is defined by reference to four modes of supply, as follows:

• Mode 1: Cross-border supply. The service but not the service supplier crosses the national border (e.g., international calls)

• Mode 2: Consumption abroad. The service is consumed abroad (e.g., US resident uses his/her domestic phone while traveling in Iraq)

• Mode 3: Commercial presence. A supplier from one country establishes commercial presence in the jurisdiction of another country. (E.g., a foreign company establishes an agency, branch or subsidiary in Iraq to supply telecommunication services in Iraq.)

• Mode 4: Presence of natural persons. The services are supplied by providers through the (temporary) presence of natural persons. (E.g., telecommunication executives or managers travel from the parent telecommunication company in the United States to the company’s branch or subsidiary in Iraq.)

2.2 WTO MEMBERS AND THE AGREEMENT ON TELECOMMUNICATION SERVICES

The Basic Telecommunications Agreement was negotiated among 69 countries – both developed and developing – that account for over 99% of the total revenues from telecommunications for all WTO Members. To date, over 100 countries took commitments on telecommunications. The range of services and technologies covered by this Agreement is very broad, spanning technologies from submarine cables to satellites, from wide-band networks to cellular phones, and from business intranets to fixed wireless for rural and underserved regions. For market access, many Members did not list limitations for cross-border supply and consumption abroad. However, some Members, especially developing countries, did include phase-in periods for their commitments. Most of the Members included limitations on commercial presence by limiting foreign investment levels. By the conclusion of the negotiations, 47 countries had committed to at least phase-in authorization for 100% foreign ownership or control of most telecommunications services and facilities; 10 countries opened up to foreign investment in certain sectors; and another 10 countries would not permit foreign control. As in the 1994 Schedule of Commitments on enhanced services, the basic services commitments on market access for presence of natural persons are generally unbound except as stated in the horizontal section. There are very few limitations on national treatment for the four modes of supply. A few countries, however, require board members of public telecommunications operators (PTOs) to have a domestic nationality for commercial presence and reference the horizontal commitments for presence of natural persons. Additional commitments for basic telecommunications are substantial. Most Members made a commitment to undertake the obligations contained in the “Reference Paper,” which they attached to their Schedules without reservation. A number of WTO members have registered exemptions to the Most Favored Nation treatment principle in the telecommunications sector: there are a number of exemptions in particular as regards satellite services and accounting rates. It may be argued that the first ones are not only allowing unfair discrimination, but that they actually prevent the most efficient development of cross-border telecommunications. Full liberalization of telecommunications markets should solve this issue.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 13

3. THE TELECOMMUNICATIONS SECTOR 3.1 DEFINITIONS

Telecommunication is the assisted transmission of signals over a distance for the purpose of communication. The public switched telephone network (PSTN) is the network of the world’s public circuit-switched telephone networks – a function similar to that of the Internet, which is the network of the world's public IP-based packet-switched networks. Originally a network of fixed-line analog telephone systems, the PSTN is now almost entirely digital, and includes mobile as well as fixed telephones.

• The PSTN is largely governed by technical standards created by the ITU. The Internet is a global system of interconnected computer networks that interchange data by packet switching using the standardized Internet Protocol Suite (TCP/IP). It is a "network of networks" that consists of millions of private and public, academic, business, and government networks of local to global scope that are linked by copper wires, fiber-optic cables, wireless connections, and other technologies. Conventional cellular radio and landline telephony use circuit switching. Services like Cellular Digital Packet Data or CDPD, by contrast, employ packet switching. General Packet Radio Service GRPS, Bluetooth, and some aspects of 3G, also use packet switching. Circuit switching dominates the Public Switched Telephone Network or PSTN. Network resources set up calls over the most efficient route. Circuit Switched Data (CSD) is the original form of data transmission developed for the time division multiple access (TDMA)-based mobile phone systems like Global System for Mobile Communications (GSM). CSD uses a single radio time slot to deliver 9.6 kbit/s data transmission to the GSM Network and Switching Subsystem where it can be connected through the equivalent of a normal modem to the PSTN, allowing direct calls to any dial-up service. Mobile phone handsets must be made to operate on one of two dominant types of mobile phone frequency networks. The most common type of air link technology is the Global System for Mobiles (GSM) network, which was developed by the European Group Special Mobile (the original source of the network’s acronym) in the early 1990s to replace the different national standards and unify the continent in one Europe-wide system. Today, the GSM network has expanded around the world and currently serves over 75% of mobile phone users, or approximately two billion people in 50 countries. But some countries, like Japan, do not have a GSM network and instead operate on a Code Division Multiple Access (CDMA) network or Wide-band CDMA (WCDMA). CDMA technology is used in approximately 14% of mobile phones. However, the industry’s leading companies are beginning to produce third generation (3G) systems, such as Universal Mobile Telecommunications Systems (UMTS), that can operate on either frequency network and are making older technologies obsolete. The next big innovation in handset technology, fourth generation (4G), is expected to produce phones for the market in 201213. 4G mobile communications will have higher data transmission rates than 3G (20 megabits per second for 4G compared to 300 kilobits/second for 3G).

13 Datamonitor, “Global Mobile Phones: Industry Profile,” December 2005

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 14

Telex remains one of the most reliable, universally available forms of electronic data communication, with approximately one million users worldwide. By operating within its own physical network, Telex provides a legal and secure transmission standard, regardless of origin or destination. Still leading the way in the Global Telex market are the Finance, Shipping, Oil and Gas industries.

Telegraphy is the long-distance transmission of written messages without physical transport of letters. Radiotelegraphy or wireless telegraphy transmits messages using radio. Telegraphy includes recent forms of data transmission such as fax, email, and computer networks in general. A telegraph is a machine for transmitting and receiving messages over long distances, i.e., for telegraphy. The word telegraph alone now generally refers to an electrical telegraph. Wireless telegraphy is also known as CW, for continuous wave (a carrier modulated by on-off keying).

Private leased circuit service is the service of providing permanent transmission connection between two customer premises for the exclusive use by a customer. This service may be provided by facilities owned or operated by an operator or by transmission capacity sold or leased by a non-facilities-based telecommunications provider, or reseller, and may use terrestrial or satellite facilities. It generally does not involve central office switching operations.

Electronic mail, often abbreviated to email is any method of creating, transmitting, or storing primarily text-based human communications with digital communications systems. Historically, a variety of electronic mail system designs evolved that were often incompatible or not interoperable.

Voicemail (sometimes called messagebank) is a centralized system of managing telephone messages for a large group of people. The term is also used more broadly, to denote any system of conveying voice message, including the answering machine.

Electronic Data Interchange (EDI) refers to the structured transmission of data between organizations by electronic means. It is more than mere E-mail; for instance, organizations might replace bills of lading and even checks with appropriate EDI messages. It also refers specifically to a family of standards, including the X12 series. However, EDI also exhibits its pre-Internet roots, and the standards tend to focus on ASCII (American Standard Code for Information Interchange) -formatted single messages rather than the whole sequence of conditions and exchanges that make up an inter-organization business process. EDI can be formally defined as 'the transfer of structured data, by agreed message standards, from one computer system to another without human intervention'. Most other definitions used are variations on this theme. Even in this era of technologies such as XML web services, the Internet and the World Wide Web, EDI is still the data format used by the vast majority of electronic commerce transactions in the world.

3.2 TELECOMS IN THE WORLD ECONOMY AND AT THE WTO

3.2.1 Telecommunications Data

Telecommunication is an important part of the world economy. The contribution of the telecommunication industry was estimated to be USD 1.2 trillion in 2006. The dynamic nature of the global telecommunications market is widely attributed to rapid technological development and an increasingly liberal policy environment.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 15

Fixed-line market penetration remains comparatively low in most developing countries, at an average of 13% at the end of 2007, even though the developing world accounted for 58% of the world’s 1.3 billion fixed-telephone lines in that year. This segment of the market showed a decline in developed countries and just a slight increase in some developing countries. On the whole, fixed-line penetration worldwide stagnated in 200714. Mobile penetration, however, continued to show high growth rates and reached an estimated 61% of the world’s population (or 2.67 billion subscriptions) at the end of 2008. More than 70% of the world’s mobile subscribers were in developing countries at the beginning of 2008. Africa remains the region with the highest growth rate (32% between 2006 and 2007). Its mobile penetration of 28% is comparable with the 37% in Asia, 72% in the Americas, and 110% in Europe at the end of 2007. Despite high growth rates in the mobile sector, major differences in mobile penetration rates still exist between regions and within countries, particularly between urban and rural areas. The impressive growth in the number of mobile subscribers is mainly due to developments in some of the world’s largest markets. The so-called BRIC countries – Brazil, the Russian Federation, India and China – are expected to have an important impact in terms of population, resources and global share of GDP. These countries alone accounted for over 1.3 billion mobile subscribers at the end of 2008. Nearly 90% of the population of Western Europe has access to a mobile phone. Growth in fixed lines, mobile cellular subscribers and internet users, in billions, world, 1996-2006

0

1

2

3

4

5

6

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006

Internet usersMobile suscribersFixed lines

Source: ITU World Telecommunication/ ICT indicators database

14 ITU World Telecommunication/ ICT indicators, November 2008

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 16

Worldwide mobile subscribers 2000-2008

61%

48%41%

34%28%23%

19%16%12%

0%

10%

20%

30%

40%

50%

60%

70%

2000 2001 2002 2003 2004 2005 2006 2007 2008est

Source: ITU World Telecommunication/ ICT indicators database Mobile subscribers per 100 people, 2007

28

37

49

72

78

110

0 20 40 60 80 100 120

Africa

Asia

World

Americas

Oceania

Europe

Source: ITU World Telecommunication/ ICT indicators database ITU’s Internet and broadband data suggest that more and more countries are going high-speed. By the end of 2007, more than 50% of all Internet subscribers had a high-speed connection. Dial-up is being replaced by broadband across developed and developing countries. Already, in Chile, Senegal and Turkey, over 90% of all Internet subscribers have broadband. However, major differences in penetration levels remain. While fixed broadband penetration stood at less than 1% in Africa, it had reached much higher levels in Europe (16%) and the Americas (10%) by the end of 2007. The difference is also reflected in the regional distribution of total broadband subscribers.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 17

Number of economies with broadband commercially available

81

113

133

145

166

0 20 40 60 80 100 120 140 160 180

2002

2003

2004

2005

2006

Source: ITU/ UNCTAD/ KADO Digital Opportunity Platform The number of mobile broadband subscribers reached 167 million at the end of 2007, driven by 18% growth since 2006. There is intense competition among technologies, such as 2.5G and 3G, as well as the emerging high-speed packet access (HSPA), WiMAX, and long-term evolution (LTE). Recent estimates indicate that HSPA subscribers worldwide have topped the 50 million mark, rising from just 11 million in 2007. Equipping customers with functional and affordable handsets will help boost the adoption of mobile broadband. For example, Apple's introduction of the 3G iPhone has shown that consumer habits and expectations are shifting, and a new generation of customers has emerged for whom always-on, high-bandwidth connectivity is the norm. From simple Internet browsing and e-mail to mobile banking, mobile shopping, mobile VoIP and mobile television – broadband applications are likely to revolutionize the mobile marketplace. The rise of voice-over-Internet-protocol (VoIP) services is probably the best example of the move to an “all-IP” environment. VoIP services have continued to grow strongly over the past two years, although at a slower growth rate than in 2005. More importantly, it is steadily replacing traditional public switched telephone network (PSTN) lines in many developed, and in some developing, countries. The global number of VoIP subscribers reached 80 million in 2008, of whom business users constitute an increasing share. The regional distribution of subscribers varies, depending on the cost of traditional fixed-line communications as well as the regulatory treatment of VoIP and of the international gateway for PSTN long-distance calls. Skype, the most frequently cited example of a global VoIP provider, had 196 million registered users in March 2007, up from 95 million in 2006. On World predicts that by 2011, there will be 100 million mobile VoIP users. And Skype is expected to have 25% of the world’s VoIP market. Regulatory tools are needed to help fine-tune market conditions so that VoIP can grow to its full potential. Some of the issues which regulators and policy-makers can address include peering arrangements among VoIP providers, interconnection agreements with other voice service providers, numbering reform (including number portability) and legalizing both VoIP provision and use where these are banned.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 18

ICT per status, 2006, %

0102030405060708090

100

Basic

servi

ces

Lease

d lines

Mobile ce

llular

(2G)

Internet

servi

ces

Wireles

s loca

l loop

VSAT

Cable

TVDSL 3G

Monopoly Competition

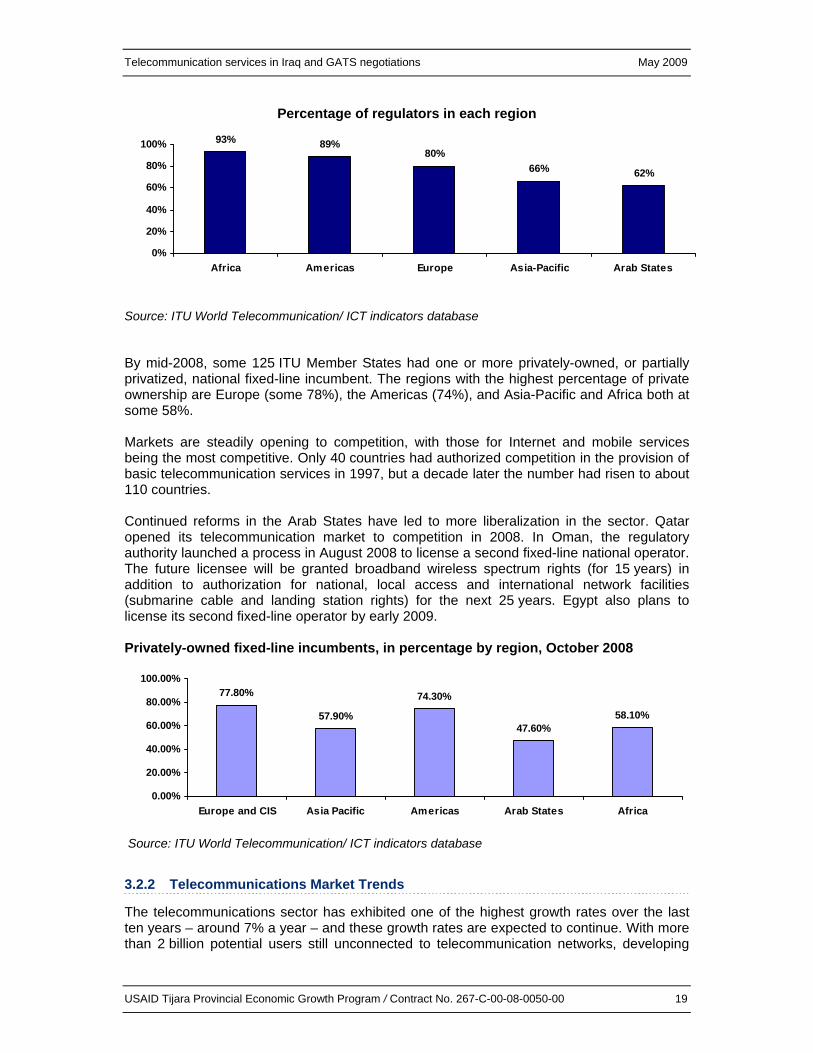

Source: ITU and UNCTAD: World Information Society Report 2007 The first wave of telecommunication reform in developing countries, starting in the late 1990s, aimed to create more transparent and stable legal and regulatory frameworks, with an emphasis on establishing national regulatory authorities and opening certain market segments, such as mobile voice, to competition. The goal was to attract investment and make progress towards universal access to basic telecommunication services. Drastic changes in the sector have since flowed from technological innovation, convergence of services, and growing competition. These changes may now require a further regulatory shift in order to open more market segments to competition, as well as to update licensing and spectrum management practices and foster growth in broadband networks and converged services. A rise in competition and new service providers will also require an enhanced focus on dispute resolution. As of October 2008, 152 countries had created national regulatory authorities for their ICT and telecommunication sectors. Africa now has the highest percentage of countries with a separate sector regulator (93%) followed by the Americas (89%), Europe (80%), Asia-Pacific (66%) and the Arab States (62%). Regulatory agencies, world (cumulative)

14

43

86106

124137

148 152

020406080

100120140160

1990 1995 1998 2000 2002 2004 2006 2008

Source: ITU World Telecommunication/ ICT indicators database

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 19

Percentage of regulators in each region

93% 89%80%

66% 62%

0%

20%

40%

60%

80%

100%

Africa Americas Europe Asia-Pacific Arab States

Source: ITU World Telecommunication/ ICT indicators database By mid-2008, some 125 ITU Member States had one or more privately-owned, or partially privatized, national fixed-line incumbent. The regions with the highest percentage of private ownership are Europe (some 78%), the Americas (74%), and Asia-Pacific and Africa both at some 58%. Markets are steadily opening to competition, with those for Internet and mobile services being the most competitive. Only 40 countries had authorized competition in the provision of basic telecommunication services in 1997, but a decade later the number had risen to about 110 countries. Continued reforms in the Arab States have led to more liberalization in the sector. Qatar opened its telecommunication market to competition in 2008. In Oman, the regulatory authority launched a process in August 2008 to license a second fixed-line national operator. The future licensee will be granted broadband wireless spectrum rights (for 15 years) in addition to authorization for national, local access and international network facilities (submarine cable and landing station rights) for the next 25 years. Egypt also plans to license its second fixed-line operator by early 2009. Privately-owned fixed-line incumbents, in percentage by region, October 2008

77.80%

57.90%

74.30%

47.60%58.10%

0.00%

20.00%

40.00%

60.00%

80.00%

100.00%

Europe and CIS Asia Pacific Americas Arab States Africa

Source: ITU World Telecommunication/ ICT indicators database

3.2.2 Telecommunications Market Trends

The telecommunications sector has exhibited one of the highest growth rates over the last ten years – around 7% a year – and these growth rates are expected to continue. With more than 2 billion potential users still unconnected to telecommunication networks, developing

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 20

and emerging markets are likely to be the main drivers of growth in subscribers and revenues over the next few years. Even if the financial downturn slows down the deployment of new networks and the transition to more advanced technologies, the growth of subscribers is expected to continue15. Global IT spending will continue to outpace global economic growth over the next years16 as companies continue to upgrade their corporate networks worldwide. Primary drivers will include the increased demand from small and medium-sized enterprises, particularly in Asia; continued network equipment and service upgrades across the business sector; and steady demand from both the corporate sector and consumers for innovative, converged electronic devices with Internet access. Sales growth of the PC will slow over the forecast period. From strong double-digit figures of the past few years, global PC shipments will grow by just 4.3% per annum between 2007 and 2011. This growth will be driven by emerging markets and Western Europe where penetration levels are lower. Purchasing and owning a mobile phone will continue to be a worldwide obsession, but the rate of growth will moderate from nearly 10% this year to 5% in 2010. Average revenue per subscriber will decline in the period, as operators compete more aggressively for customers on price. Worldwide demand for broadband internet connections will grow in double-digits the next years for the world's sixty largest economies to 585m subscribers by 2011. Revenues from broadband services will leap from USD137bn in 2007 to USD207bn in 2011, accounting for nearly 40% of total fixed line revenue worldwide. World Telecoms and technology industry (60 countries covered):

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Telephone, main lines (m*) 931.4 980.7 1,028.6 1,073.0 1,114.1 1,150.1 1,174.5 1,186.7 1,200.4 1,217.0

per 100 people 19.5 20.4 21.1 21.8 22.5 23.0 23.2 23.3 23.3 23.5

Mobile subscribers (m) 1,071.2 1,289.0 1,587.6 1,954 2,247.3 2,482.6 2,668.0 2,824.8 2,970,1 3,113.9

per 100 people 22.5 26.8 32.6 39.8 45.3 49.6 52.8 55.4 57.8 60.0

Internet users (m) 543.1 648.5 762.8 841.1 926.2 1,030.6 1,143.1 1,258.2 1,376.8 1,503.0

per 100 people 11.4 13.5 15.7 17.1 18.7 20.6 22.6 24.7 26.8 29.0

Broadband subscriber lines (m) 68.5 107.8 159.9 217.1 284.3 351.3 415.0 475.3 532.6 585.9

per 100 people 1.4 2.2 3.3 4.4 5.7 7.0 8.2 9.3 10.4 11.3

Personal computers (per 1000 people) 126.2 144.4 159.5 175.1 198.3 212.1 225.7 239.5 252.9 265.7

Source: Economist Intelligence Unit * m - millions

15 International Telecommunication Union: A snapshot of the ICT market 16 Global Technology Forum: World telecoms and IT Outlook, Always on. July 2007.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 21

Personal computers (stock per 1000 people)

0100200300400500600700800900

1000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

NorthAmericaWesternEuropeAsia andAustralia LatinAmericaMiddle Eastand AfricaWorld

Source: Economist Intelligence Unit Broadband subscribers (per 100 people)

05

10152025303540

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

NorthAmericaWesternEuropeAsia andAustralia LatinAmericaMiddle Eastand AfricaWorld

Source: Economist Intelligence Unit

3.2.3 Role of Telecoms in Economic Development

Telecommunications infrastructures, as the backbone for other sectors, have important economic, societal, and national security implications. Telecommunications infrastructures are as significant to the competitiveness of services today as the railroads were to manufacturing during the industrial age. Telecommunications infrastructures are also key to the maintenance of a technologically advanced military; thus, the national security implications of trade in telecommunications are higher than in many other services. Additionally, the importance of telecommunications infrastructures is compounded by technology upgrades that affect the reliability and scope of their use. A competitive telecommunications market brings many benefits to businesses and consumers including lower costs, efficient and innovative services, and expanded opportunities and choices. Network expansion has been a key driver of economic growth for many countries, and private investment has been the main catalyst for such expansion;

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 22

much of it in the developing world. According to the World Bank, the private sector invested USD 230 billion in telecommunications infrastructure in the developing world between 1993 and 2003, with the greatest investment in those countries that were open to competition. Indeed as more markets become competitive, expansion into other markets will become essential. Thus, all countries seeking to benefit from the gains of a competitive global telecommunications market have a stake in seeing market opening commitments in this sector17. Deloitte undertook a regression analysis using a cross-section of developing countries18. The analysis estimated that a 10% increase in telecoms penetration could increase the GDP growth rate of a country by 1.2%.

3.2.4 Linkages between Telecommunication Services and Other Sectors

The competitiveness of telecommunication impacts all sectors, as the use of a phone is very much needed by any economic sector. The same can be said for Internet tools. Many sub sectors are relevant to and affected by the liberalization of telecoms:

• Customer sits down at computer – computer services

• Logs onto Internet – communications services

• Goes to website with ads – advertising services

• Orders a product – distribution services

• Pays for the product – financial services

• Downloads product or has it delivered – delivery services Telecoms are also linked to intellectual property rights and data protection (related to TRIPS).

3.2.5 WTO versus Liberalization/ Privatization of Telecommunication Services

To take GATS commitments means to open up market to competition and to liberalize a sector. Privatization is a process of state intervention that literally sells a state enterprise such as a state telephony company. Privatization takes many forms, depending on the percentage of shares to be sold off, the extent to which any foreign ownership is permitted, the length, if any, of a phase-in period, and the specific form of ongoing state ownership. Two main approaches to privatization/liberalization emerge:

1. Privatization with full competition. Both developed and developing countries have followed this model.

2. Privatization with phase-in competition. In this model, privatization of national carriers is accompanied by a sustained period of exclusivity rights or limited competition. Two main reasons can be cited for opting for this model: • Governments want to maximize the sale of value of their national carrier; • Countries want to retain market share and accumulate income prior to sale.

17 Office of the United States Trade Representative, Services Facts www.ustr.gov. Trade in Services Policy Brief – March 2006. 18 Harriet E. Berg, “Economic Contribution of Mobile Communications”, WTO Symposium on Telecommunications, February 2008.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 23

GATS model does not distinguish between liberalization and privatization, as these processes have taken place in tandem globally, with liberalization facilitating the process of privatization. Liberalization was introduced to increase the rapid entry of other competitors in the market and has often consisted of the privatization of the incumbent operator in the sector. Three issues related to privatization are noteworthy: 1. Competition is a key economic force and should be managed by regulation. 2. An independent regulator is needed to enforce competition, reduce monopolies and

promote private and foreign investment. The regulator should be an independent arbitrator.

3. Privatization creates the change of ownership from government entities (partially of fully) to private business entities.

This raises the question: does the kind of ownership – public or private – makes a difference? What about the Universal Service obligations? Liberalization in itself seeks to increase the number of participants in the market. In telecoms markets, liberalization often occurs when the telecommunication framework is based on a monopoly system. The aim of government intervention is to expand the number of communication service providers or lower the entry barriers to all or part of the market, through policy amendments. However, liberalization is the slowest form of introducing reforms, as competition is allowed in slow increments starting often with the introduction of new entrants in the mobile services, such as cellular and paging.

3.2.6 Regulation and Its Importance: Elements to Consider

Key regulatory policies vital in these reforms include:

1. Introduction of competition

2. Privatization of incumbent operator

3. Establishment of an independent regulator Telecommunications liberalization is a complex and relatively new process for developing countries. Choices have to be made regarding the privatization of state-owned telecommunications operators, the introduction of competition, the opening of markets to foreign investment and the establishment of pro-competitive regulations. While there is growing consensus that each of these elements is desirable, it is rare for countries to simultaneously go all the way on all fronts19. Telecom regulations call for the issuance of additional detailed administrative rules, catalogues and notices required to implement the general principles set forth in the regulations. The regulations also provide some clues to several critical administrative areas, including a licensing system that distinguishes between value-added and basic telecom operations, rules to govern the interconnection of telecom networks, and telecom rates.

19 Carsten Fink, Aaditya Mattoo and Randeep Rathindran: An Assessment of Telecommunications Reform in Developing Countries. The World Bank Development Research Group, October 2002.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 24

• Key regulatory issues

Among key regulatory issues, the World Bank20 recommends that regulators should consider the following:

• Licensing: Who can do what? • Competition (especially interconnection): Who can reach subscribers and distribute

content? • Spectrum management: Which bands of spectrum can be used for what service, and

under what conditions? • Universal service: Who pays, for what, and subsidizes whom? • A related issue is the institutional framework: are we seeing more ‘converged

regulators’? • Other issues relate to numbering, market dominance, content regulation,

accessibility, privacy and piracy.

• Regulator’s objectives

To be successful, the Regulator’s function21 should be based on a well-defined set of objectives, which typically would include:

• Attracting investment • Infrastructure planning and development • Sector efficiency improvement • Quality of service improvement • Encouragement of competition • Eliminating barriers to market entry for new operators • Protection and empowerment of the consumers and promotion of the general socio-

economic well being The functions of an independent regulator include, for example:

• Issuing and compliance monitoring of licenses • Setting minimum interconnection terms • Arbitrating disputes between operators or between operators and customers • Designing and monitoring compliance with a national numbering plan • Monitoring the fairness of infrastructure sharing as provided in the law • Regulating tariffs • Managing frequencies, and • Generally enforcing rules and regulations of the sector.

• Adequate funding

Without adequate funding a regulatory body cannot be effective. 20 World Bank: CITEL Doc. STE-356/07 21 Ernest C. Ndukwe, Chief Executive Officer, Nigerian Communications Commission: Lessons from implementation of market reform and competition, WTO Telecoms Symposium, February 2008.

Telecommunication services in Iraq and GATS negotiations May 2009

USAID Tijara Provincial Economic Growth Program / Contract No. 267-C-00-08-0050-00 25

Some National Regulatory Agencies (NRAs) are starved of basic funds essential for operational effectiveness, training and manpower development.