This supplement updates and amends certain - RiverSource

88

May 1, 2021 RiverSource ® Variable Universal Life 5 RiverSource ® Variable Universal Life 5 – Estate Series This wrapper contains a prospectus. Choose e-delivery. Too much mail? Visit ameriprise.com/e-delivery today to see which documents you can receive online. Issued by: RiverSource Life Insurance Company S-6542 CH (5/21)

Transcript of This supplement updates and amends certain - RiverSource

May 1, 2021

RiverSource® Variable Universal Life 5RiverSource® Variable Universal Life 5 –Estate Series

This wrapper contains a prospectus.

Choose e-delivery.Too much mail?

Visit ameriprise.com/e-delivery today to seewhich documents you can receive online.

Issued by: RiverSource Life Insurance CompanyS-6542 CH (5/21)

This page left blank intentionally

��������������� ������� �������

������������������� �����

���������� ����� �� �������

�� !"#$%"&!'�!(�"!)!*(+, �-$"./"�/01!+**%�(234/*,5

#67899:;<=>?@=A/2BCD>>?

�� !"#$%"&!'�+.+<+&&!--'./"�/01!+**%�(2;EFF!"!,F$"&$*("/&(/GG1�&/(�$*--�H*!,$*$"/F(!"I%*!DDCD>D>@

#6795<JK;<=DB@=A/2BCD>DB #6798>JK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�!(�"!)!*(+, �-$"+, /*(/H!L1%-./"�/01!+**%�(2=�� !"#$%"&!'�!(�"!)!*(+, �-$"#!1!&(L1%-./"�/01!+**%�(2

#67D95JK;<=DB@=A/2BCD>DB #6757DJK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�!(�"!)!*(+, �-$"8+, /*(/H!'./"�/01!+**%�(2=�� !"#$%"&!'�!(�"!)!*(+, �-$"#!1!&(./"�/01!+**%�(2=�� !"#$%"&!'

�!(�"!)!*(+, �-$"+&&!--./"�/01!+**%�(2

#67<>5JK;<=DB@=A/2BCD>DB #67<>8JK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�+.+<+, /*(/H!'./"�/01!+**%�(2;EFF!"!,F$"&$*("/&(/GG1�&/(�$*--�H*!,$*$"/F(!"+G"�1D?CD>B?@

#679D>JK;<=DB@=A/2BCD>DB #679D<JK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�+.+<JM$�&!#A./"�/01!+**%�(2

#679B>JK;<=DB@=A/2BCD>DB #679B<JK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�+.+<+, /*(/H!'./"�/01!+**%�(2;EFF!"!,F$"&$*("/&(/GG1�&/(�$*--�H*!,G"�$"($+G"�15>CD>BD@=�� !"#$%"&!'�+.+<#!1!&('./"�/01!+**%�(2=�� !"#$%"&!�+.+<+&&!--'

./"�/01!+**%�(2

B8>875JK;<=DB@=A/2BCD>DB B8>878JK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�+.+<+, /*(/H!'./"�/01!+**%�(2;EFF!"!,F$"&$*("/&(/GG1�&/(�$*--�H*!,$*$"/F(!"+G"�15>CD>BD0%(G"�$"($+G"�1D?CD>B5@=�� !"#$%"&!'

�+.+<#!1!&('./"�/01!+**%�(2=�� !"#$%"&!'�+.+<+&&!--'./"�/01!+**%�(2

#67<B<JK;<=DB@=A/2BCD>DB #67<B9JK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�+.+<+, /*(/H!'./"�/01!+**%�(2;EFF!"!,F$"&$*("/&(/GG1�&/(�$*--�H*!,$*$"/F(!"+G"�1D?CD>B50%(G"�$"($+G"�1D?CD>B?@=�� !"#$%"&!'

�+.+<#!1!&('./"�/01!+**%�(2;EFF!"!,F$"&$*("/&(/GG1�&/(�$*--�H*!,$*$"/F(!"+G"�1D?CD>B50%(G"�$"($#!G(NBOCD>B9@=�� !"#$%"&!'�+.+<+&&!--'

./"�/01!+**%�(2;EFF!"!,F$"&$*("/&(/GG1�&/(�$*--�H*!,$*$"/F(!"+G"�1D?CD>B5@

#67<?8JK;<=DB@=A/2BCD>DB #67<?<JK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�!(�"!)!*(P"$%G+**%�(2J$*("/&(Q

#677BBJK;<=DB@=A/2BCD>DB

�� !"#$%"&!'�!(�"!)!*(P"$%G+**%�(2J$*("/&(QQ

#677BDJK;<=DB@=A/2BCD>DB

B

��������������� ������� �������

������������������� �����

���������� ����� �� �������

�� !"#$%"&!'�!(�"!)!*(+, �-$"+, .*(./!0."�.12!+**%�(345.*,6

789:;<=>9?@>A.3BCD99?

�� !"#$%"&!'�!(�"!)!*(+, �-$"0."�.12!+**%�(3

#E787:FG<=>DB@>A.3BCD9DB #E78:B�<8>B6@>+H"�2D?CD9B6

�� !"#$%"&!'�!(�"!)!*(+, �-$"+, .*(./!0."�.12!+**%�(3>�� !"#$%"&!'�!(�"!)!*(+, �-$"#!2!&(0."�.12!+**%�(3

#E7897FG<=>DB@>A.3BCD9DB #E78B9I<8>B6@>+H"�2D?CD9B6

�� !"#$%"&!'0."�.12!#!&$*,EJ$EK�!L�M!N*-%".*&!

#E7B?7O<=>9P@>A.3BCD99P #E7BP=�<=>9P@>A.3BCD99P

�� !"#$%"&!#%&&!--�$*#!2!&('0."�.12!L�M!N*-%".*&!

#E7D96FQ<8>B?@>+H"�2D?CD9B? #E7D96FQ<8>B?@>+H"�2D?CD9B?

RSTUVWXYVZU'0."�.12![*� !"-.2L�M!=>RSTUVWXYVZU'0."�.12![*� !"-.2L�M!=4\-(.(!#!"�!-

#E7=8DFG<=>DB@>A.3BCD9DB #E7=86FQ<8>B?@>+H"�2D?CD9B?

�� !"#$%"&!'0."�.12![*� !"-.2L�M!N0>�� !"#$%"&!'0."�.12![*� !"-.2L�M!N04\-(.(!#!"�!-

#E78BPFG<=>DB@>A.3BCD9DB #E78B?FQ<8>B?@>+H"�2D?CD9B?

�� !"#$%"&!'0."�.12![*� !"-.2L�M!N*-%".*&!NNN

#E7BP?FG<=>DB@>A.3BCD9DB #E7DBBL<9=>9?@>A.3BCD99?

RSTUVWXYVZU]0."�.12![*� !"-.2L�M!N*-%".*&!

#E7B?8FG<=>DB@>A.3BCD9DB #E7B:BFQ<8>B?@>+H"�2D?CD9B?

�� !"#$%"&!'#�*/2!̂ "!)�%)0."�.12!L�M!N*-%".*&!

#E7B??;<9=>9P@>A.3BCD99P

�� !"#$%"&!'0."�.12![*� !"-.2L�M!7N*-%".*&!

#E7:99FQ<8>B?@ #E7:9=FQ<8>B?@

_̀UaXbbXcSdeSdaXVfghSXdiUjZVSkUjZ̀gdeUjhXZUVhgSdSdTUjhfUdhXlhSXdjXaaUVUiYdiUVZUVhgSdTgVSgkbUgddYShmZXdhVgZhjgdiTgVSgkbUbSaUSdjYVgdZUlXbSZSUjbSjhUigkXTUnobUgjUVUhgSdh̀SjjYllbUfUdhcSh̀mXYVbghUjhlVSdhUilVXjlUZhYjaXVaYhYVUVUaUVUdZUnpqZUlhgjfXiSaSUiSdh̀SjjYllbUfUdhrgbbXh̀UVhUVfjgdiSdaXVfghSXdZXdhgSdUiSdh̀UlVXjlUZhYjVUfgSdSdUaaUZhgdiYdZ̀gdeUin

Js!5$.",$MK�"!&($"-$M(s!52.&t�$&t0."�.12!#!"�!-Q%*,-CN*&u$*1!s.2M$M(s!52.&t�$&tv2$1.2+22$&.(�$*0uNuQ%*,<(s!wQ%*,x@<�*&2%,�*/F2.--N.*,F2.--NNN-s."!-$M(s!Q%*,@C.HH"$ !,(s!.HH$�*()!*($M52.&t�$&t<#�*/.H$"!@L�)�(!,<w5�#[email protected]%1E., �-!"$M(s!Q%*,CH%"-%.*(($.-%1E., �-$"3./"!!)!*(1!(y!!*5�#.*,52.&t�$&t+, �-$"-CLLFy�(s"!-H!&(($(s!Q%*,u

5�#�-.,,!,.-.-%1E., �-!"($(s!Q%*,!MM!&(� !A.3D:CD9DBu

z{�|������ }� |������� ������������{����� �� ��~���������� � �{������� �{������ �����z{�� ������z{������������� �� ��{�� ��������� ��|�{�����������

� ����� }� � ������ ����������� ��������� � ������ ��������

52.&t�$&tv2$1.2+22$&.(�$*0uNuQ%*, #!!t-s�/s($(.2�* !-()!*("!(%"*u 52.&t�$&t+, �-$"-CLLFC., �-!"�52.&t�$&t<#�*/.H$"!@L�)�(!,C-%1E., �-!"u

z����������z����������������z����������z�������������

����������������

D

[This Page Intentionally Left Blank]

S-6720-14 A (06/21)

John R. WoernerPresident andGeneral Manager –InsuranceRiverSource LifeInsurance Company

From the PresidentThank you for taking an important step and turning to RiverSource Life Insurance Company foryour insurance protection needs. Having appropriate financial protection in place can bring youa feeling of added confidence. We are proud of our 125-year heritage honoring ourcommitments to clients and look forward to continuing this tradition with you.

RiverSource® variable life insurance is a product solution that can serve multiple purposes.First, it provides a death benefit that is an income-tax-free way to transfer wealth from onegeneration to the next. Second, it can also provide a source of potentially income-tax-freeretirement income through cash value accumulation. Consult with your financial advisorperiodically to help ensure your coverage continues to provide the benefits you need as your lifechanges.

At RiverSource Life Insurance Company, we also want to help make your life insurance assimple and convenient as possible. That’s why we’re pleased to offer electronic delivery(e-delivery) for many of your financial documents, including this prospectus. When you choosee-delivery, Ameriprise will:

• Mail you less paper

• Securely organize and store your documents

• Help protect your financial documents from fraud, fire and other unexpected events

Using less paper is also a simple, yet meaningful way to help conserve natural resources.

If you are not yet enjoying the benefits of e-delivery, you can learn more or sign up when youvisit ameriprise.com/e-delivery.

Thank you for your business. We at RiverSource Life Insurance Company look forward tocontinuing to help meet your financial needs.

Sincerely,

John R. WoernerPresident and General Manager – InsuranceRiverSource Life Insurance Company

Variable life insurance is a complex investment vehicle that is subject to market risk, including the potential loss of principal invested.

Accessing policy cash value through loans and surrenders may cause a permanent reduction of policy cash values and death benefit, and negate anyguarantees against lapse. Surrender charges may apply to the policy and loans may be subject to interest charges. Although loans are generally nottaxable, there may be tax consequences if the policy lapses, or is surrendered or exchanged with an outstanding loan. Taxable income could exceedthe amount of proceeds actually available. Surrenders are generally taxable to the extent they exceed the remaining investment in the policy. If thepolicy is a modified endowment contract (MEC), pre-death distributions, including loans from the policy, are taxed on an income-first basis, and theremay be a 10% federal income tax penalty for distributions of earnings prior to age 59-1/2.

Neither RiverSource Life Insurance Company, nor its affiliates or representatives, offer tax or legal advice. Consult with your tax adviser or attorneyregarding your specific situation.

RiverSource Distributors, Inc. (Distributor), Member FINRA. Issued by RiverSource Life Insurance Company, Minneapolis, Minnesota. Affiliated withAmeriprise Financial Services, LLC.

© 2021 RiverSource Life Insurance Company. All rights reserved.

This page is not part of the prospectus

This page left blank intentionally

Prospectus

May 1, 2021

RiverSource®

Variable Universal Life 5Variable Universal Life 5 – Estate SeriesINDIVIDUAL FLEXIBLE PREMIUM VARIABLE LIFE INSURANCE POLICIES

New policies are not currently being offered.

Issued by: RiverSource Life Insurance Company (RiverSource Life)70100 Ameriprise Financial CenterMinneapolis, MN 55474Telephone: 1-800-862-7919(Service Center)Website address: riversource.com/lifeinsuranceRiverSource Variable Life Separate Account

This prospectus contains information that you should know before investing in RiverSource Variable Universal Life 5(VUL 5) or RiverSource Variable Universal Life 5 – Estate Series (VUL 5 – ES). VUL 5 – ES is a life insurance policy withan initial Specified Amount of $1,000,000.00 or more. We reserve the right to offer the Estate Series at a lowerSpecified Amount on a promotional basis and/or to certain groups of individuals such as current or retired employeesand financial advisors of Ameriprise Financial, Inc. or its subsidiaries, and their spouses or domestic partners, wheresuch promotion or group offering is expected to result in overall cost reductions to RiverSource Life.

All other policies are VUL 5 policies. The information in this prospectus applies to both VUL 5 – ES and VUL 5 unlessstated otherwise.

The purpose of each policy is to provide life insurance protection on the life of the Insured and to potentially build PolicyValue. Each policy is a long-term investment that provides a death benefit that we pay to the Beneficiary upon theInsured’s death. You may direct your Net Premiums or transfers to:• A Fixed Account to which we credit interest.

• Subaccounts that invest in underlying Funds.

Prospectuses are available for the Funds that are investment options under these policies. Please read allprospectuses carefully and keep them for future reference.

RiverSource Life has not authorized any person to give any information or to make any representations regarding thepolicy other than those contained in this prospectus or the Fund prospectuses. Do not rely on any such information orrepresentations. All material state variations are disclosed in the prospectus.

Please note that your investments in a policy and its underlying Funds:• Are NOT deposits or obligations of a bank or financial institution;

• Are NOT insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency; and

• Are subject to risks including loss of the amount you invested and the policy ending without value.

The Securities and Exchange Commission (SEC) has not approved or disapproved these securities or passed uponthe accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Variable life insurance is a complex vehicle that is subject to market risk, including the potential loss of principalinvested. Before you invest, be sure to ask your sales representative about the policy’s features, benefits, risks andfees, and whether it is appropriate for you based upon your financial situation and objectives. Your sales representativemay or may not be authorized to offer you several different variable life insurance policies in addition to the policydescribed in this prospectus. Each policy has different features or benefits that may be appropriate for you based onyour financial situation and needs, your age and how you intend to use the policy. The different features and benefitsmay include investment and fund manager options, variations in interest rate amounts and guarantees and surrendercharge schedules. The fees and charges may also be different among the policies. Be sure to ask your salesrepresentative about all the options that are available to you.

For your convenience, we have defined certain words and phrases used in this prospectus in the “Key Terms” section.

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 1

Effects of COVID-19 Pandemic

The coronavirus disease 2019 (“COVID-19”) public health crisis presents ongoing significant economic and societaldisruption, and has driven significant volatility in the equity and interest rate markets. Any periods of continued highmarket volatility, and your individual circumstances (e.g., your selected allocations and the timing of any purchasepayments, transfers, or withdrawals), will affect values under your policy. As part of how we maintain our strong financialstrength and claims-paying ability, we continue to reserve amounts for our contractual obligations in accordance withsignificant state solvency regulations. The extent to which the COVID-19 pandemic may impact financial markets,investment performance under your policy, and our financial strength and claims-paying ability will depend on futuredevelopments, which are highly uncertain and cannot be estimated, including the scope and duration of the pandemicand actions taken by governmental authorities, market participants, and other third parties in response to thepandemic.

We have implemented comprehensive strategies to address the operating environment spurred by the pandemic. Topromote the safety and security of our employees and to assure the continuity of our business operations, we haveimplemented a work from home protocol for virtually all of our employee population, restricted business travel, andprovided resources for complying with the guidance from the World Health Organization, the U.S. Centers for DiseaseControl and government authorities. We have been satisfying elevated customer service volumes and our operationsteams have continued to operate successfully and without disruptions in service. Our pandemic strategy is flexible andscalable and takes into consideration that a pandemic could be widespread and may occur in multiple waves, affectingdifferent communities at different times with varying levels of severity. We cannot, however, predict the impact thatnatural or man-made disasters and catastrophes, including the COVID-19 pandemic, may have over near- or longer-termperiods.

2 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

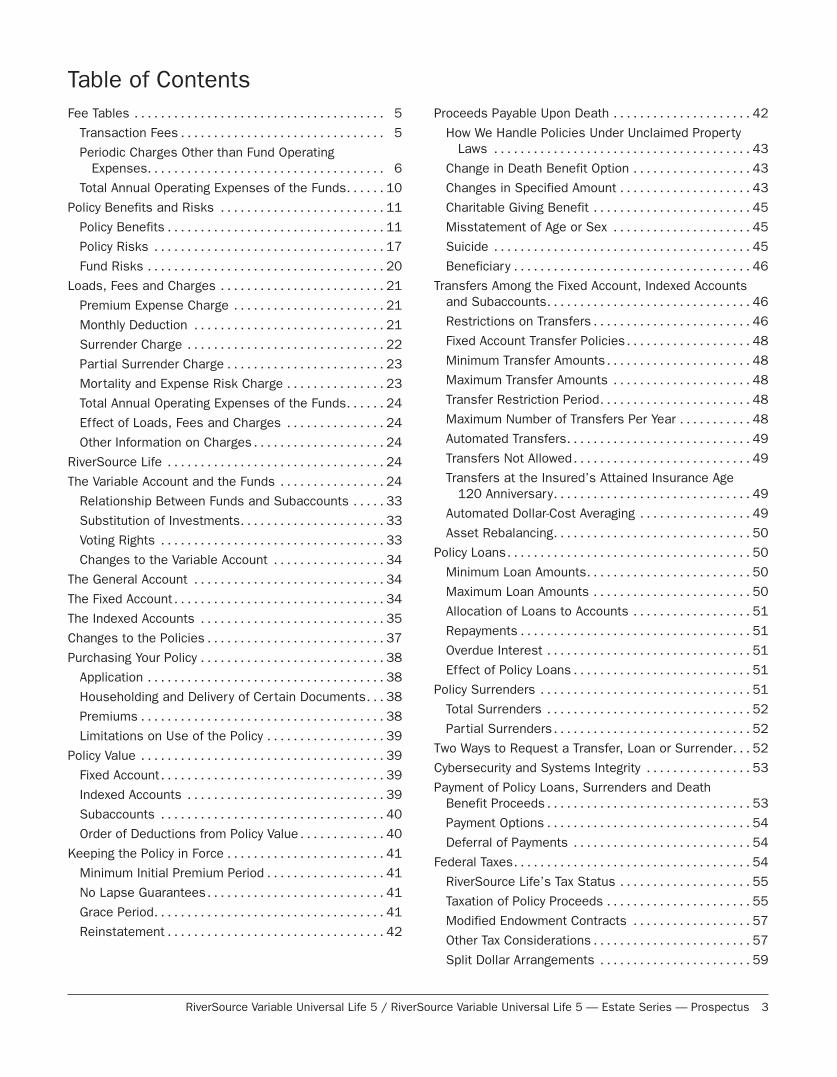

Fee Tables . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Transaction Fees . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

Periodic Charges Other than Fund OperatingExpenses. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

Total Annual Operating Expenses of the Funds. . . . . . 10

Policy Benefits and Risks . . . . . . . . . . . . . . . . . . . . . . . . . 11

Policy Benefits . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

Policy Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Fund Risks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 20

Loads, Fees and Charges . . . . . . . . . . . . . . . . . . . . . . . . . 21

Premium Expense Charge . . . . . . . . . . . . . . . . . . . . . . . 21

Monthly Deduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

Surrender Charge . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 22

Partial Surrender Charge . . . . . . . . . . . . . . . . . . . . . . . . 23

Mortality and Expense Risk Charge . . . . . . . . . . . . . . . 23

Total Annual Operating Expenses of the Funds. . . . . . 24

Effect of Loads, Fees and Charges . . . . . . . . . . . . . . . 24

Other Information on Charges . . . . . . . . . . . . . . . . . . . . 24

RiverSource Life . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 24

The Variable Account and the Funds . . . . . . . . . . . . . . . . 24

Relationship Between Funds and Subaccounts . . . . . 33

Substitution of Investments. . . . . . . . . . . . . . . . . . . . . . 33

Voting Rights . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 33

Changes to the Variable Account . . . . . . . . . . . . . . . . . 34

The General Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

The Fixed Account . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

The Indexed Accounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . 35

Changes to the Policies . . . . . . . . . . . . . . . . . . . . . . . . . . . 37

Purchasing Your Policy . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Application . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Householding and Delivery of Certain Documents. . . 38

Premiums . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 38

Limitations on Use of the Policy . . . . . . . . . . . . . . . . . . 39

Policy Value . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Fixed Account. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Indexed Accounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

Subaccounts . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 40

Order of Deductions from Policy Value . . . . . . . . . . . . . 40

Keeping the Policy in Force . . . . . . . . . . . . . . . . . . . . . . . . 41

Minimum Initial Premium Period . . . . . . . . . . . . . . . . . . 41

No Lapse Guarantees. . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Grace Period. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

Reinstatement . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 42

Proceeds Payable Upon Death . . . . . . . . . . . . . . . . . . . . . 42

How We Handle Policies Under Unclaimed PropertyLaws . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

Change in Death Benefit Option . . . . . . . . . . . . . . . . . . 43

Changes in Specified Amount . . . . . . . . . . . . . . . . . . . . 43

Charitable Giving Benefit . . . . . . . . . . . . . . . . . . . . . . . . 45

Misstatement of Age or Sex . . . . . . . . . . . . . . . . . . . . . 45

Suicide . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 45

Beneficiary . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Transfers Among the Fixed Account, Indexed Accountsand Subaccounts. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 46

Restrictions on Transfers . . . . . . . . . . . . . . . . . . . . . . . . 46

Fixed Account Transfer Policies. . . . . . . . . . . . . . . . . . . 48

Minimum Transfer Amounts. . . . . . . . . . . . . . . . . . . . . . 48

Maximum Transfer Amounts . . . . . . . . . . . . . . . . . . . . . 48

Transfer Restriction Period. . . . . . . . . . . . . . . . . . . . . . . 48

Maximum Number of Transfers Per Year . . . . . . . . . . . 48

Automated Transfers. . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Transfers Not Allowed. . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Transfers at the Insured’s Attained Insurance Age120 Anniversary. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 49

Automated Dollar-Cost Averaging . . . . . . . . . . . . . . . . . 49

Asset Rebalancing. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Policy Loans. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 50

Minimum Loan Amounts. . . . . . . . . . . . . . . . . . . . . . . . . 50

Maximum Loan Amounts . . . . . . . . . . . . . . . . . . . . . . . . 50

Allocation of Loans to Accounts . . . . . . . . . . . . . . . . . . 51

Repayments . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Overdue Interest . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Effect of Policy Loans . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Policy Surrenders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 51

Total Surrenders . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Partial Surrenders. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 52

Two Ways to Request a Transfer, Loan or Surrender. . . 52

Cybersecurity and Systems Integrity . . . . . . . . . . . . . . . . 53

Payment of Policy Loans, Surrenders and DeathBenefit Proceeds . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 53

Payment Options . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Deferral of Payments . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

Federal Taxes. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 54

RiverSource Life’s Tax Status . . . . . . . . . . . . . . . . . . . . 55

Taxation of Policy Proceeds . . . . . . . . . . . . . . . . . . . . . . 55

Modified Endowment Contracts . . . . . . . . . . . . . . . . . . 57

Other Tax Considerations . . . . . . . . . . . . . . . . . . . . . . . . 57

Split Dollar Arrangements . . . . . . . . . . . . . . . . . . . . . . . 59

Table of Contents

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 3

Distribution of the Policy . . . . . . . . . . . . . . . . . . . . . . . . . . 61

Legal Proceedings. . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 62

Key Terms . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

Financial Statements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 68

Appendix A: Policy Availability by Jurisdiction . . . . . . . . . 69

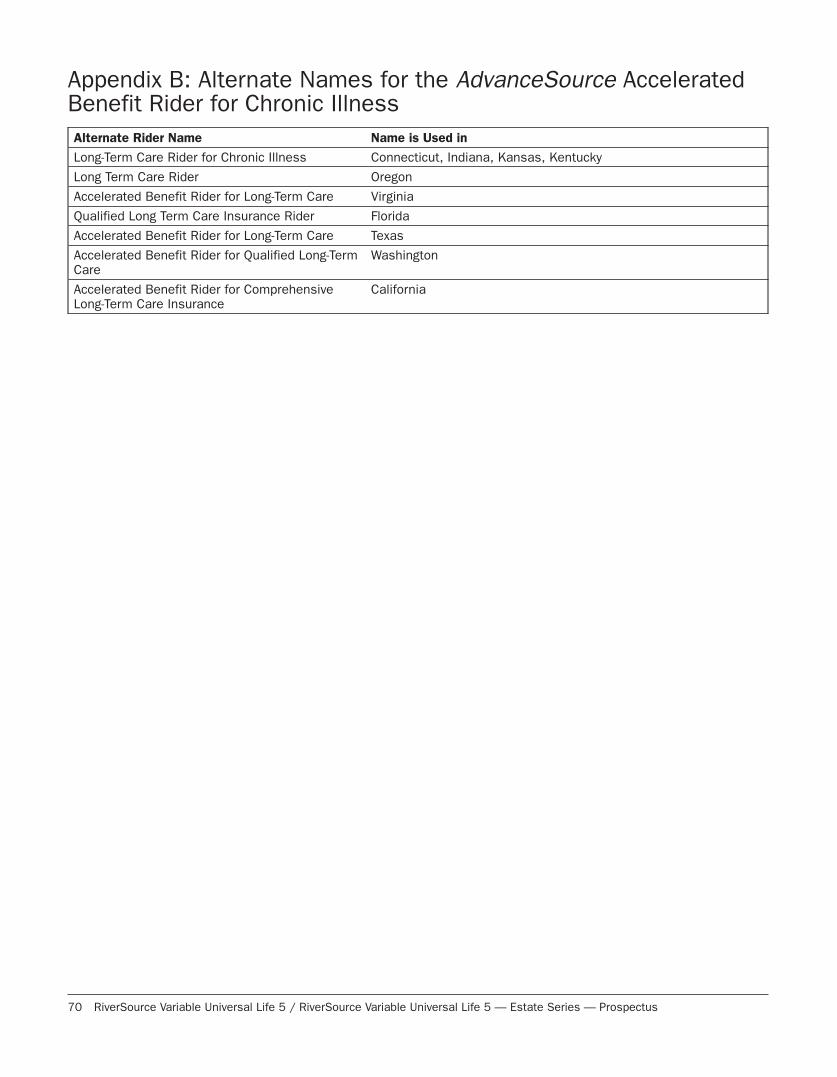

Appendix B: Alternate Names for the AdvanceSourceAccelerated Benefit Rider for Chronic Illness . . . . . . . 70

Appendix C: S&P Disclaimer . . . . . . . . . . . . . . . . . . . . . . . 71

Table of Contents

4 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

Fee TablesThe following tables describe the fees and expenses that you will pay when buying, owning and surrendering thepolicy. The first table describes the fees and expenses that you will pay at the time that you buy the policy orsurrender the policy.

Transaction FeesAMOUNT DEDUCTED

CHARGE WHEN CHARGE IS DEDUCTED VUL 5 VUL 5 – ES

Premium ExpenseCharge

When you pay premium. 4% of each premiumpayment.

4% of each premiumpayment.

State Premium Taxes When you pay premium. Deducted from each premiumpayment. See discussionunder “Premium ExpenseCharge.”

Deducted from each premiumpayment. See discussionunder “Premium ExpenseCharge.”

Surrender Charge(a) When you urrender your policyfor its full Cash SurrenderValue, or the policy Lapses,during the first ten years andfor ten years after requestingan increase in the SpecifiedAmount. All the rates shownto the right are the initialSurrender Charge. Theserates grade down over10 years to zero.

Rate per $1,000 of initialSpecified Amount:

Rate per $1,000 of initialSpecified Amount:

Minimum: $11.92 — Female,Standard Nontobacco, Age 0.

Minimum: $11.92 — Female,Standard Nontobacco, Age 0.

Maximum: $57.00 — Male,Standard Tobacco, Age 60.

Maximum: $57.00 — Male,Standard Tobacco, Age 60.

Representative Insured:20.95 — Male, PreferredNontobacco, Age 35.

Representative Insured:23.82 — Male, PreferredNontobacco, Age 40.

Partial Surrender Fee When you surrender part ofthe value of your policy.

The lesser of: The lesser of:

• $25; or • $25; or

• 2% of the amountsurrendered.

• 2% of the amountsurrendered.

Accelerated BenefitRider for Terminal IllnessCharge (ABRTI)

Upon payment of AcceleratedBenefit.

In AL, if the AcceleratedBenefit payment is $25,000or greater, the fee will be$250. For Accelerated Benefitpayments less than $25,000,the fee will be 1% of theAccelerated Benefit payment.In FL, the fee is $100 perAccelerated Benefit payment.For all other states, the feewill be $250. The maximumaggregate charge for allAccelerated Benefitsadvanced is $500.

In AL, if the AcceleratedBenefit payment is $25,000or greater, the fee will be$250. For Accelerated Benefitpayments less than $25,000,the fee will be 1% of theAccelerated Benefit payment.In FL, the fee is $100 perAccelerated Benefit payment.For all other states, the feewill be $250. The maximumaggregate charge for allAccelerated Benefitsadvanced is $500.

Fees for Express Mailand Electronic FundTransfers of Loan orSurrender Proceeds

When you take a loan orsurrender and proceeds aresent by express mail orelectronic fund transfer.

• $25 — United States. • $25 — United States.

• $35 — International. • $35 — International.

(a) This charge varies based on individual characteristics. The charges shown in the table may not be representative of the charge you will pay.For information about the charge you would pay, contact your sales representative or RiverSource Life at the address or telephone numbershown on the first page of this prospectus.

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 5

The next table describes the fees and expenses that you will pay periodically during the time that you own the policy,not including Fund fees and expenses.

Periodic Charges Other than Fund Operating ExpensesAMOUNT DEDUCTED

CHARGE WHEN CHARGE IS DEDUCTED VUL 5 VUL 5 – ES

Cost of InsuranceCharge(a)

Monthly. Monthly rate per $1,000 ofNet Amount at Risk:

Monthly rate per $1,000 ofNet Amount at Risk:

Minimum: $.015 — Female,Standard Nontobacco, Age 3:Duration 1.

Minimum: $.015 — Female,Standard Nontobacco, Age 3:Duration 1.

Maximum: $83.333 — Male,Standard Tobacco, Age 112.Duration 1.

Maximum: $83.333 — Male,Standard Tobacco, Age 112.Duration 1.

Representative Insured:$0.09 — Male, PreferredNontobacco, Age 35:Duration 1.

Representative Insured:$0.12 — Male, PreferredNontobacco, Age 40:Duration 1.

Policy Fee Monthly. Guaranteed: $15.00 permonth.

Guaranteed: $15.00 permonth.

Current: $10.00 per monthfor initial Specified Amountsbelow $100,000; and

Current: $7.50 per month.

$7.50 per month for initialSpecified Amounts of$100,000 and above.

Administrative Charge Monthly. Monthly rate per $1,000 ofinitial Specified Amount:

Monthly rate per $1,000 ofinitial Specified Amount:

Minimum: $.063 — Female,Standard Nontobacco, Age 0.

Minimum: $.063 — Female,Standard Nontobacco, Age 0.

Maximum: $4.827 — Male,Standard Nontobacco,Age 96.

Maximum: $4.827 — Male,Standard Nontobacco,Age 96.

Representative Insured:Male, Preferred Nontobacco,Age 35:

Representative Insured:Male, Preferred Nontobacco,Age 40:

Current: $0.11 per month,years 1-10; $0 per month,years 11+.

Current: $0.161 per month,years 1-10; $0 per month,years 11+.

Guaranteed: $0.137 permonth, all Durations.

Guaranteed: $0.202 permonth, years 1-20; $0.171per month, years 21+.

Mortality and ExpenseRisk Charge

Monthly. Guaranteed: Annual rate of0.60% applied monthly to theVariable Account Value.

Guaranteed: Annual rate of0.60% applied monthly to theVariable Account Value.

Current: 0% Current: 0%

(a) This charge varies based on individual characteristics. The charges shown in the table may not be representative of the charge you will pay. Forinformation about the charge you would pay, contact your sales representative or RiverSource Life at the address or telephone number shown onthe first page of this prospectus.

6 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

Periodic Charges Other than Fund Operating Expenses (continued)

AMOUNT DEDUCTED

CHARGE WHEN CHARGE IS DEDUCTED VUL 5 VUL 5 – ES

Indexed AccountCharge(a)

Monthly. Guaranteed: Annual rate of0.60% applied monthly.

Guaranteed: Annual rate of0.60% applied monthly.

Current: 0.60% Current: 0.60%

Interest Rate on Loans Charged daily and due at theend of the policy year.

Guaranteed:4% per year.

Guaranteed:4% per year.

Current: Current:• 4% for policy years 1-10; • 4% for policy years 1-10;

• 2% for policy years 11+. • 2% for policy years 11+.

Interest Rate onPayments underAccelerated BenefitRider for Terminal Illness(ABRTI)

Annually, payable at the endof each policy year.

Guaranteed:• For that part of the accelerated benefit which does not

exceed Policy Value available for policy loans when anaccelerated benefit is requested, we will charge thepolicy’s Guaranteed Loan Interest Rate shown under PolicyData.

• For that part of the accelerated benefit which exceedsPolicy Value available for policy loans when theaccelerated benefit is requested, the greatest of:

• the current yield on 90-day Treasury bills, or

• the current maximum statutory adjustable policy loaninterest rate, or

• the policy’s Guaranteed Loan Interest Rate shown underPolicy Data.

Accidental Death BenefitRider (ADB)(b)

Monthly. Monthly rate per $1,000 ofaccidental death benefitamount:

Monthly rate per $1,000 ofaccidental death benefitamount:

Minimum: $.04 — Female,Age 5.

Minimum: $.04 — Female,Age 5.

Maximum: $.16 — Male,Age 69.

Maximum: $.16 — Male,Age 69.

Representative Insured:$0.08 — Male, PreferredNontobacco, Age 35.

Representative Insured:$0.08 — Male, PreferredNontobacco, Age 40.

Automatic IncreaseBenefit Rider (AIBR)

No charge. No charge for this rider,however, the additionalinsurance added by the rideris subject to monthly cost ofinsurance charges.

No charge for this rider,however, the additionalinsurance added by the rideris subject to monthly cost ofinsurance charges.

Children’s InsuranceRider (CIR)

Monthly. Monthly rate per $1,000 ofCIR Specified Amount:$.58.

Monthly rate per $1,000 ofCIR Specified Amount:$.58.

(a) The Indexed Account charge is equal to the sum of the charges for all Indexed Accounts. The charge for an Indexed Account is equal to thecurrent Indexed Account charge for that Indexed Account multiplied by the sum of the Segment Values corresponding to that Indexed Account asof the Monthly Date. The Indexed Account charge will be taken out of Policy Value as part of the monthly deduction.

(b) This charge varies based on individual characteristics. The charges shown in the table may not be representative of the charge you will pay. Forinformation about the charge you would pay, contact your sales representative or RiverSource Life at the address or telephone number shown onthe first page of this prospectus.

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 7

Periodic Charges Other than Fund Operating Expenses (continued)

AMOUNT DEDUCTED

CHARGE WHEN CHARGE IS DEDUCTED VUL 5 VUL 5 – ES

Overloan ProtectionBenefit (OPB)

Upon exercise of the Benefit. 3% of the Policy Value. 3% of the Policy Value.

Waiver of MonthlyDeduction Rider(WMD)(a)

Monthly. Monthly rate per $1,000 ofnet amount risk:

Monthly rate per $1,000 ofnet amount of risk:

Minimum: $.00692 —Female, Nontobacco, Age 20.

Minimum: $.00692 —Female, Nontobacco, Age 20.

Maximum: $.34212 — Male,Standard Tobacco, Age 59.

Maximum: $.34212 — Male,Standard Tobacco, Age 59.

Representative Insured:$0.01340 — Male, PreferredNontobacco, Age 35.

Representative Insured:$0.01899 — Male, PreferredNontobacco, Age 40.

Waiver of Premium Rider(WP)(a)(b)

Monthly. Monthly rate multiplied by thegreater of themonthly-specified premiumselected for the rider or themonthly deduction for thepolicy and any other ridersattached to the policy.

Monthly rate multiplied by thegreater of themonthly-specified premiumselected for the rider or themonthly deduction for thepolicy and any other ridersattached to the policy.

Minimum: $.03206 — Male,Nontobacco, Age 20.

Minimum: $.03206 — Male,Nontobacco, Age 20.

Maximum: $.40219 —Female, Standard Tobacco,Age 59.

Maximum: $.40219 —Female, Standard Tobacco,Age 59.

Representative Insured:$0.04009 — Male, PreferredNontobacco, Age 35.

Representative Insured:$0.04649 — Male, PreferredNontobacco, Age 40.

(a) This charge varies based on individual characteristics. The charges shown in the table may not be representative of the charge you will pay. Forinformation about the charge you would pay, contact your sales representative or RiverSource Life at the address or telephone number shown onthe first page of this prospectus.

(b) States in which the WP does not include waiver for involuntary unemployment include FL and MT.

8 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

Periodic Charges Other than Fund Operating Expenses (continued)

AMOUNT DEDUCTED

CHARGE WHEN CHARGE IS DEDUCTED VUL 5 VUL 5 – ES

AdvanceSource®

Accelerated BenefitRider for Chronic Illness(ASR)(a)(b)(c)(d)

Monthly (while the rider is ineffect)

Monthly rate per $1,000 ofthe rider Specified Amount:

Monthly rate per $1,000 ofthe rider Specified Amount:

Minimum: $0.0025, Male,Age 20, Super PreferredNon-Tobacco, Duration 1, 1%Monthly Benefit Percent.

Minimum: $0.0025, Male,Age 20, Super PreferredNon-Tobacco, Duration 1, 1%Monthly Benefit Percent.

Maximum: $24.41, Female,Age 20, Standard Tobacco,Duration 80, 3% MonthlyBenefit Percent.

Maximum: $24.41, Female,Age 20, Standard Tobacco,Duration 80, 3% MonthlyBenefit Percent.

Representative Insured:$0.0025, Male, PreferredNon-Tobacco, Age 35:Duration 1, 2% MonthlyBenefit Percent.

Representative Insured:$0.0025, Male, PreferredNon-Tobacco, Age 40:Duration 1, 2% MonthlyBenefit Percent.

Accounting ValueIncrease Rider(a)

Monthly. Monthly rate per $1,000 ofnet amount risk:

Monthly rate per $1,000 ofnet amount of risk:

Minimum: $.0325 — Male,Nontobacco, Age 85.

Minimum: $.0325 — Female,Nontobacco, Age 85.

Maximum: $.0629 —Female, Tobacco, Age 35-55.

Maximum: $.0629 —Female, Tobacco, Age 35-55.

Representative Insured: $0.5— Male, Nontobacco,Age 35.

Representative Insured: $0.5— Male, Nontobacco,Age 40.

(a) This charge varies based on individual characteristics. The charges shown in the table may not be representative of the charge you will pay. Forinformation about the charge you would pay, contact your sales representative or RiverSource Life at the address or telephone number shown onthe first page of this prospectus.

(b) The monthly cost of insurance rate is based on the Accelerated benefit Insured’s sex (except in Montana), Risk Classification, issue age, Durationand the Monthly Benefit Percent shown in the “Policy Data” section of the policy. The cost of insurance rates for this rider will not exceed theguaranteed maximum monthly cost of insurance rates for this rider shown in the “Policy Data” section of the policy.

(c) This rider is only available for policies purchased under the Option 1 death benefit. This rider has a different name in some jurisdictions. (SeeAppendix B.)

(d) In Colorado, Florida, Hawaii, North Carolina, Ohio, Tennessee and Vermont, the minimum, maximum and representative Insured rates for the riderare 0.025 for Male, Age 25, Super Preferred Non-Tobacco, 1% Monthly Benefit; 4.3575, Female, Age 79, Standard Tobacco, 3% Monthly BenefitPercent; and 0.0575, Male, Age 35, Preferred Non-Tobacco, 2% Monthly Benefit for VUL 5, respectively and 0.025 for Male, Age 25, SuperPreferred Non-Tobacco, 1% Monthly Benefit; 4.3575, Female, Age 79, Standard Tobacco, 3% Monthly Benefit Percent; and 0.0725, Male, Age 40,Preferred Non-Tobacco, 2% Monthly Benefit for VUL 5 – ES.

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 9

Total Annual Operating Expenses of the FundsThe next table provides the minimum and maximum total operating expenses charged by the underlying Funds thatyou may pay periodically during the time that you own the policy. The minimum and maximum expenses listed beloware based on expenses for the Funds’ fiscal year ended December 31, 2020, unless otherwise noted, without takinginto account fee waivers and/or expense reimbursements that may apply. More detail concerning each underlyingFund’s fees and expenses is contained in each Fund’s prospectus.

Minimum and maximum annual operating expenses for the Funds(Including management fees, distribution and /or service (12b-1) fees and other expenses)(1)

Minimum(%) Maximum(%)

Total expenses before fee waivers and/or expense reimbursements 0.39 2.60

(1) Total annual Fund operating expenses are deducted from amounts that are allocated to the Fund. They include management fees and otherexpenses and may include distribution (12b-1) fees. Other expenses may include service fees that may be used to compensate serviceproviders, including us and our affiliates, for administrative and policy Owner services provided on behalf of the Fund. The amount of thesepayments will vary by Fund and may be significant. See “The Variable Account and the Funds” for additional information, including potentialconflicts of interest these payments may create. Distribution (12b-1) fees are used to finance any activity that is primarily intended to result inthe sale of Fund shares. Because 12b-1 fees are paid out of Fund assets on an on going basis, you may pay more if you select Subaccountsinvesting in Funds that have adopted 12b-1 plans than if you select Subaccounts investing in Funds that have not adopted 12b-1 plans. For amore complete description of each Fund’s fees and expenses and important disclosure regarding payments the Fund and/or its affiliatesmake, please review the Fund’s prospectus and the Statement of Additional Information (“SAI”).

10 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

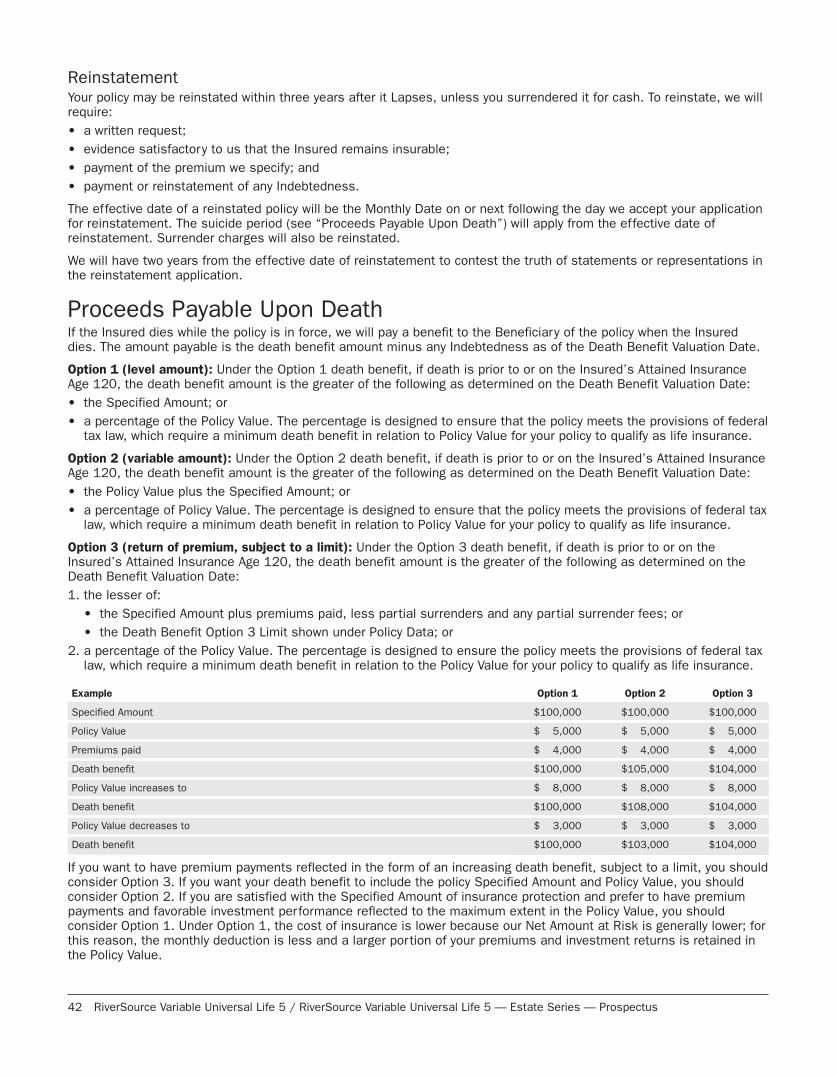

Policy Benefits and RisksThis summary describes the policy’s important benefits and risks. The sections in the prospectus following thissummary discuss the policy’s benefits, risks and other provisions in more detail.

Policy BenefitsPOLICY BENEFIT WHAT IT MEANS HOW IT WORKS

Death Benefit We will pay a benefit to theBeneficiary of the policywhen the Insured dies. Yourpolicy’s death benefit cannever be less than theSpecified Amount unlessyou change that amount oryour policy has outstandingIndebtedness.

The amount payable is the death benefit amount minus anyIndebtedness as of the Death Benefit Valuation Date. Youmay choose either of the following death benefit options:Option 1 (level amount): If death is prior to or on theInsured’s Attained Insurance Age 120, the death benefitamount is the greater of the following as determined on theDeath Benefit Valuation Date:• the Specified Amount; or• a percentage of the Policy Value.This percentage is shown in the Death Benefit PercentageTable under Policy Data.Option 2 (variable amount): If death is prior to or on theInsured’s Attained Insurance Age 120, the death benefitamount is the greater of the following as determined on theDeath Benefit Valuation Date:• the Policy Value plus the Specified Amount; or• a percentage of the Policy Value.You may change the death benefit option or Specified Amountwithin certain limits, but doing so generally will affect policycharges. We reserve the right to limit any decrease to theextent necessary to qualify the policy as life insurance underthe Internal Revenue Code of 1986, as amended (Code).This percentage is shown in the Death Benefit PercentageTable under Policy Data.Option 3 (return of premium, subject to a limit): If death isprior to or on the Insured’s Attained Insurance Age 120, thedeath benefit amount is the greater of the following asdetermined on the Death Benefit Valuation Date:1. the lesser of:

• the Specified Amount plus premiums paid, less partialsurrenders and any partial surrender fees; or

• the Death Benefit Option 3 Limit shown under PolicyData; or

2. a percentage of the Policy Value.You may change the death benefit option or Specified Amountwithin certain limits, but doing so generally will affect policycharges. We reserve the right to decline to make any deathbenefit option change that we determine would cause thepolicy to fail to qualify as life insurance under applicable taxlaws.Death Benefit after the Insured’s Attained InsuranceAge 120 anniversary:Under all Death Benefit Options, the death benefit upondeath of the Insured after the Insured’s Attained InsuranceAge 120 anniversary will be the greater of:• the death benefit on the Insured’s Attained Insurance

Age 120 anniversary, minus any partial surrenders andpartial surrender fees occurring after the Insured’sAttained Insurance Age 120 anniversary; or

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 11

Policy Benefits (continued)

POLICY BENEFIT WHAT IT MEANS HOW IT WORKS

Death Benefit (continued) • the Policy Value on the date of death.This percentage is shown in the Death Benefit PercentageTable under Policy Data.

Charitable Giving Benefit For VUL 5 – ES only, youmay name an organizationdescribed in Section 170(c)of the Code to receive anamount equal to 1% of thepolicy’s Proceeds payableupon death, with amaximum charitable giftamount of $100,000.Proceeds payable upondeath do not includeamounts paid under anyoptional insurance benefitsdescribed below. Thisbenefit is not available inall states.

You may designate the charitable Beneficiary at any time andchange the charitable Beneficiary once each policy year bywritten request. There is no additional charge for thecharitable giving benefit. RiverSource Life pays the charitablegiving benefit from its assets; it is not deducted from thepolicy Proceeds and it is not paid by the Insured. There is nocharitable deduction associated with payment of premiumsinto a life insurance policy. In addition, you will not receive atax deduction for the charitable giving benefit we pay. As withall tax matters you should consult a tax advisor.

Minimum Initial PremiumGuarantee and No LapseGuarantee (NLG)

Your policy will not Lapse(end without value) if theMinimum Initial Premiumguarantee or the NLGoption is in effect, even ifthe Cash Surrender Value isless than the amountneeded to pay the monthlydeduction.

Minimum Initial Premium Guarantee : A period of the firstpolicy year during which you may choose to pay the MinimumInitial Premium as long as the Policy Value minusIndebtedness equals or exceeds the monthly deduction.No Lapse Guarantee: Each policy has the following NLGoption which remains in effect if you meet certain premiumrequirements and Indebtedness does not exceed the PolicyValue minus Surrender Charges:• No Lapse Guarantee To Age 75 (NLG-75) guarantees the

policy will not Lapse before the Insured’s AttainedInsurance Age 75 (or 10 years, if later).

Flexible Premiums You choose when to paypremiums and how muchpremium to pay.

When you apply for your policy, you state how much youintend to pay and whether you will pay monthly, quarterly,semiannually or annually. You may also make additional,unscheduled premium payments subject to certain limits.You cannot make premium payments on or after theInsured’s Attained Insurance Age 120. We reserve the rightto refuse premiums to the extent necessary to qualify thepolicy as life insurance under the Code. Although you haveflexibility in paying premiums, the amount and frequency ofyour payments will affect the Policy Value, Cash SurrenderValue and the length of time your policy will remain in forceas well as affect whether any of the NLG options remain ineffect.

12 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

Policy Benefits (continued)

POLICY BENEFIT WHAT IT MEANS HOW IT WORKS

Right to Examine YourPolicy (“Free Look”)

You may return your policyfor any reason and receivea full refund of allpremiums paid.

If you exercise your right to examine your policy underthe “Free Look” provision of the policy, you will receive a fullrefund of all premiums paid.You may mail or deliver the policy to our Service Center or toyour sales representative with a written request forcancellation by the 10th day after you receive it (20th day inNorth Dakota). On the date your request is postmarked orreceived, the policy will immediately be considered void fromthe start.Under our current administrative practice, your request tocancel the policy under the “Free Look” provision will behonored if received at our Service Center within 30 days fromthe latest of the following dates:• The date we mail the policy from our Service Center.• The Policy Date (only if the policy is issued in force).• The date your sales representative delivers the policy to

you as evidenced by our policy delivery receipt, which youmust sign and date.

We reserve the right to change or discontinue thisadministrative practice at any time.

Investment Choices You may direct your NetPremiums or transfer yourPolicy’s Value to:• The Variable Account,

which consists ofSubaccounts, each ofwhich invests in a Fundwith a particularinvestment objective.

• Under the Variable Account your policy’s value mayincrease or decrease daily, depending on the investmentreturn. No minimum amount is guaranteed.

• The Fixed Account,which is part of ourgeneral investmentaccount.

• The Fixed Account earns interest rates that we adjustperiodically. This rate will never be lower than 2%.

• The Indexed Accounts,which are part of ourgeneral investmentaccount.

• The Indexed Accounts earn interest based on a change inthe value of one or more designated index(es), subject toa Segment Growth Cap, Segment Floor and SegmentParticipation Rate. Indexed interest will never be lowerthan 0% for the 1-year Indexed Account or 1% for the2-year Indexed Account.

Policy Value Credit We may periodically apply apolicy value credit to yourPolicy Value. Therequirements that must bemet to receive any policyvalue credit are shownunder Policy Data.

How it works: The amount of the policy value credit isdetermined by multiplying the policy value credit percentagetimes the Policy Value minus any Indebtedness at the timethe calculation is made.We reserve the right to calculate and apply any policy valuecredit annually, quarterly or monthly.Any policy value credit will be allocated according to yourpremium allocation percentages in effect. Any policy valuecredit is nonforfeitable, except indirectly due to anyapplicable Surrender Charge.We reserve the right to change the policy value creditpercentage based on our expectations of future investmentearnings, persistency, expenses, and/or federal and statetax assumptions. However, it will never be less than zero.

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 13

Policy Benefits (continued)

POLICY BENEFIT WHAT IT MEANS HOW IT WORKS

Surrenders You may cancel the policywhile it is in force andreceive its Cash SurrenderValue or take a partialsurrender out of your policy.

The Cash Surrender Value is the Policy Value minusIndebtedness minus any applicable Surrender Charges.Partial surrenders are available within certain limits for a fee.

Loans You may borrow againstyour policy’s CashSurrender Value.

Generally, you may access your policy’s Cash SurrenderValue through policy loans without incurring taxes orSurrender Charges associated with withdrawals. Seediscussion under “Policy Loans” and “Federal Taxes.”

Transfers You may transfer yourPolicy’s Value.

You may transfer Policy Value from one Subaccount toanother or between Subaccounts and the Fixed Account. Youcan also arrange for automated transfers among the FixedAccount and Subaccounts. Certain restrictions may apply.

Optional InsuranceBenefits

When you purchase yourpolicy, you may add optionalbenefits to your policy at anadditional cost, in the formof riders (if you meetcertain requirements).Generally, the amounts ofthese benefits do not varywith investment experienceof the Variable Account.Certain restrictions andconditions apply and areclearly described in theapplicable rider. TheOverloan Protection benefitis only available when thereis an outstanding loan onyour policy.

Available riders you may add:• Accelerated Benefit Rider for Terminal Illness (ABRTI): If

the Insured is terminally ill and death is expected to occurwithin six months (in AZ, AR, CT, DC, DE, MT, ND and SD)or within twelve months (in all other states), the riderprovides that you can withdraw a portion of the deathbenefit prior to death.

• Accidental Death Benefit Rider (ADB): ADB provides anadditional death benefit if the Insured’s death is causedby accidental injury.

• Automatic Increase Benefit Rider (AIBR): AIBR providesan increase in the Specified Amount at a designatedpercentage on each Policy Anniversary until the earliest ofthe Insured’s Attained Insurance Age 65 or the occurrenceof certain other events, as described in the rider.

• Children’s Insurance Rider (CIR): CIR provides level termcoverage on each eligible child.

• Overloan Protection Benefit (OPB): Protects the policyfrom lapsing as a result of the loan balance exceeding thePolicy Value.

• Waiver of Monthly Deduction Rider (WMD): Under WMD,we will waive the monthly deduction if the Insuredbecomes totally disabled before Attained InsuranceAge 60.

In addition:• If total disability begins on or after Attained Insurance

Age 60 but before Attained Insurance Age 65, themonthly deduction will be waived only for a limitedperiod of time; and

• WMD also includes a waiver for involuntaryunemployment benefit where monthly deductions maybe waived up to 12 months. WMD for involuntaryunemployment is not available in Florida or Montana.Ask your sales representative about the terms of theWMD.

14 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

Policy Benefits (continued)

POLICY BENEFIT WHAT IT MEANS HOW IT WORKS

Optional InsuranceBenefits (continued)

• Waiver of Premium Rider (WP): Under WP, if totaldisability begins before Attained Insurance Age 60, prior toAttained Insurance Age 65 we will add the specifiedpremium shown under Policy Data in the policy to thePolicy Value or waive the monthly deduction if higher. On orafter Attained Insurance Age 65, we will waive the monthlydeduction.In addition:• If total disability begins on or after Attained Insurance

Age 60 but before Attained Insurance Age 65, themonthly deduction will be waived for a limited period oftime; and

• WP also includes a waiver for involuntary unemploymentbenefit where monthly deductions may be waived up to12 months. WP for involuntary unemployment is notavailable in Florida or Montana. Ask your salesrepresentative about the terms of the WP.

• AdvanceSource Accelerated Benefit Rider for ChronicIllness (ASR): ASR provides a rider payment to theAccelerated Benefit Insured, as an acceleration of thepolicy’s death benefit, if the Accelerated Benefit Insuredbecomes a Chronically Ill Individual who receives QualifiedLong-term Care Services. Please note the following aboutthe ASR:

• This rider is only available for policies purchased under theOption 1 death benefit .

• This rider has a different name in some jurisdictions. (SeeAppendix B.)

• At the request of you or the Accelerated Benefit Insuredthe accelerated benefit under this rider will be paid eachmonth, limited by the maximum monthly benefit to theAccelerated Benefit Insured or to any individual authorizedto act on behalf of the Accelerated Benefit Insured.

• These payments are subject to certain limitations andsatisfaction of eligibility requirements which include thefollowing: 1) A current written eligibility certification from aLicensed Health Care Practitioner that certifies theAccelerated Benefit Insured is a Chronically Ill Individual;and 2) Proof that the Accelerated Benefit Insured receivedor is receiving Qualified Long-term Care Services pursuantto a Plan of Care; and 3) Proof that the Elimination Periodhas been satisfied; and 4) Written Notice of Claim andProof of Loss, as described in the “Claim Provisions”section of the policy, in a form satisfactory to us.

• We will begin Monthly Benefit Payments under this riderwhen the Eligibility for the Payment of Benefits Conditionsare met and a claim for benefits has been approved by us.The ASR does not include inflation protection coverageand therefore the benefit level will not increase over time.Because the costs of long-term care services will likelyincrease over time, you should consider whether and howthe benefits of the ASR may be adjusted.

• Monthly Benefit Payments paid will also change othervalues of the life insurance policy as provided in the ridersuch as Policy Value less Indebtedness, SurrenderCharges and monthly No-Lapse Guarantee premiums.

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 15

Policy Benefits (continued)

POLICY BENEFIT WHAT IT MEANS HOW IT WORKS

Optional InsuranceBenefits (continued)

• Accounting Value Increase Rider (AVIR): If the policy isfully surrendered while the rider is in force and prior to theexpiration date of the rider, we will waive a portion of theSurrender Charge.

• The amount waived is a percentage of the SurrenderCharge that would apply to the initial Specified Amount.

• The waiver does not apply to any Surrender Charge due toincreases in Specified Amount, or to partial surrenders.

• Surrender Charges will not be waived if the policy is beingsurrendered in exchange for a new insurance policy orcontract.

16 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

Policy RisksPOLICY RISK WHAT IT MEANS WHAT CAN HAPPEN

Investment Risk You direct your NetPremiums or transfer yourPolicy’s Value to aSubaccount that drops invalue.

• You can lose cash values due to adverse investmentexperience. There is no minimum guaranteed cash valueunder the Subaccounts of the Variable Account.

• Your death benefit under Option 2 may be lower due toadverse investment experience.

• Your policy could Lapse due to adverse investmentexperience if neither the Minimum Initial Premium Periodnor the NLG is in effect and you do not pay the premiumsneeded to maintain coverage.

You transfer your Policy’sValue betweenSubaccounts.

• The value of the Subaccount from which you transferredcould increase.

• The value of the Subaccount to which you transferredcould decrease.

Market Risk Variable life insurance is acomplex vehicle that issubject to market risk,including the potential lossof principal invested.

• You may experience loss in Policy Value due to factors thataffect the overall performance of the financial markets.

Risk of Limited PolicyValues in Early Years

The policy is not suitable asa short-term investment.

• If you are unable to afford the premiums needed to keepthe policy in force, your policy could Lapse with no value.

Your policy has little or noCash Surrender Value in theearly policy years.

• Surrender Charges apply to this policy for the first tenyears. Surrender Charges can significantly reduce PolicyValues. Poor investment performance can alsosignificantly reduce Policy Values. During early policy yearsthe Cash Surrender Value may be less than the premiumsyou pay for the policy.

Your ability to take partialsurrenders is limited.

• You cannot take partial surrenders during the first policyyear.

Lapse Risk You do not pay thepremiums needed tomaintain coverage.

• We will not pay a death benefit if your policy Lapses.• Also, the Lapse may have adverse tax consequences.

(See “Tax Risk.”)

Your policy may Lapse dueto Surrender Charges.

• Surrender Charges affect the surrender value, which is ameasure we use to determine whether your policy willenter a grace period (and possibly Lapse, which may haveadverse tax consequences, see “Tax Risk”). A partialsurrender will reduce the Policy Value and the deathbenefit, and may terminate the NLG. Additionally, forOption 1 policies, a partial surrender will reduce theSpecified Amount.

You take a loan againstyour policy.

• Taking a loan increases the risk of:— policy Lapse (which may have adverse tax

consequences, see “Tax Risk”);— a permanent reduction of Policy Value;— reducing the death benefit.

• Taking a loan may also terminate the NLG.

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 17

Policy Risks (continued)

POLICY RISK WHAT IT MEANS WHAT CAN HAPPEN

Lapse Risk (continued) Your policy can Lapse dueto poor investmentperformance.

• Your policy could Lapse due to adverse investmentexperience if neither the Minimum Initial Premium Periodnor the NLG is in effect and you do not pay the premiumsneeded to maintain coverage.

• The Lapse may have adverse tax consequences (See “TaxRisk”).

Exchange/ReplacementRisk

You exchange or replaceanother policy to buy thisone.

• You may pay Surrender Charges on the old policy.• The new policy has Surrender Charges, which may extend

beyond those in the old policy.• You may be subject to new incontestability and suicide

periods on the new policy.• You may be in a higher insurance risk rating category in

the new policy which may increase the cost of the policy.• If a partial surrender is taken prior to the exchange, you

may have adverse tax consequences.• Also, the exchange may have adverse tax consequences.

(See “Tax Risk.”)

You use cash values ordividends from anotherpolicy to buy this one,without fully surrenderingthe other policy.

• If you borrow from another policy to buy this one, the loanreduces the death benefit on the other policy. If you fail torepay the loan and accrued interest, you could lose theother coverage and you may be subject to income tax ifthe policy Lapses or is surrendered with a loan against it.You may have adverse tax consequences. (See “TaxRisk.”)

• If you surrender cash value from another policy to buy thisone, you could lose coverage on the other policy. Also, thesurrender may be subject to income tax. You may haveadverse tax consequences. (See “Tax Risk.”)

Tax Risk A policy may be classifiedas a “modified endowmentcontract” (MEC) for federalincome tax purposes whenissued. If a policy is not aMEC when issued, certainchanges you make to thepolicy may cause it tobecome a MEC.

• Any taxable earnings come out first on surrenders or loansfrom a MEC policy or an assignment or pledge of a MECpolicy. Investment in the policy comes out second. Federalincome tax on these earnings will apply. State and localincome taxes may also apply. If you are under age 59½, a10% penalty tax may also apply to these earnings.

If you exchange or replaceanother policy to buy thisone.

• If you replace the old policy and it is not part of anexchange under Section 1035 of the Code, there may beadverse tax consequences if the total Policy Value (beforereductions for outstanding loans, if any) exceeds yourinvestment in the old policy.

• If you replace the old policy as part of an exchange underSection 1035 of the Code and there is a loan on the oldpolicy, there may be adverse tax consequences if the totalPolicy Value (before reductions for the outstanding loan)exceeds your investment in the old policy.

• The new policy may be or may become a MEC even if theold policy was not a MEC. See discussion under “ModifiedEndowment Contracts”.

18 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

Policy Risks (continued)

POLICY RISK WHAT IT MEANS WHAT CAN HAPPEN

Tax Risk (continued) • The exchange may require a portion of the cash value ofthe old policy to be distributed in order to qualify the newpolicy as a life insurance policy for federal tax purposes.

If your policy Lapses or isfully surrendered with anoutstanding policy loan, youmay experience asignificant tax cost.

• You will be taxed on any earnings in the policy. Generally, apolicy has earnings to the extent the cash value plus anyoutstanding loans exceeds the investment in the contract.

• For non-MEC policies, it could be the case that a policywith a relatively small existing cash value could havesignificant as yet untaxed earnings that will be taxed uponLapse or surrender of the policy.

• For MEC policies, earnings are the remaining earnings(any earnings that have not been previously taxed) in thepolicy, which could be a significant amount depending onthe policy.

You may buy this policy toprovide assets that will beavailable to support yourpromise to pay benefitsunder a nonqualifiedtax-deferred retirementplan.

• Like other general business assets, the policy is subjectto the general creditors of the company and may be usedto pay any expenses of the company. Thus, the policymight not be available to support a business’ obligation tomake payments under a nonqualified deferredcompensation plan. Please consult with your tax advisorregarding potential Code Section 409A implications.

You may buy this policy tofund a qualified tax-deferredretirement plan.

• The policy will not provide any necessary or additional taxdeferral if it is used to fund a qualified tax-deferredretirement plan. See discussion under “QualifiedTax-deferred retirement plans” for additional taxconsiderations.

The investments in theSubaccount are notadequately diversified.

• If a policy fails to qualify as a life insurance policy becauseit is not adequately diversified, the policyholder mustinclude in gross income the “income on the contract” (asdefined in Section 7702(g) of the Code).

Congress may change howa life insurance policy istaxed at any time.The interpretation of currenttax law is subject to changeby the Internal RevenueService (IRS) or the courtsat any time.

• You could lose any or all of the specific federal income taxattributes and benefits of a life insurance policy includingtax-deferred accrual of cash values and income tax freedeath benefits.

• For non-MEC policies you could lose your ability to takenon-taxable distributions or loans from the policy.

• Typically, changes of this type are prospective only, butsome or all of the attributes could be affected.

The IRS may determine thatyou are the Owner of theFund shares held by ourVariable Account.

• You may be taxed on the income of each Subaccount tothe extent of your interest in the Subaccount.

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 19

Fund RisksA comprehensive discussion of the risks of each portfolio in which the Subaccounts invest may be found in each Fund’sprospectus. Please refer to the prospectuses for the Funds for more information. The investment advisers cannotguarantee that the Funds will meet their investment objectives.

20 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

Loads, Fees and ChargesPolicy charges primarily compensate us for:• providing the insurance benefits of the policy;• issuing the policy;• administering the policy;• assuming certain risks in connection with the policy; and• distributing the policy.

We deduct some of these charges from your premium payments. We deduct others periodically from your Policy Value inthe Fixed Account, Indexed Accounts and/or Subaccounts. We may also assess a charge if you surrender your policy orthe policy Lapses. We may profit from one or more of the charges we collect under the policy. We may use these profitsfor any corporate purpose.

Premium Expense ChargeWe deduct this charge from each premium payment. We credit the amount remaining after the deduction, called the NetPremium, to the accounts you have selected. The premium expense charge is 4% of each premium payment. Thepremium expense charge, in part, compensates us for expenses associated with administering and distributing thepolicy, including agents’ commissions, advertising and printing of prospectuses and sales literature. (The SurrenderCharge, discussed under “Surrender Charge” and the administrative charge, discussed under “Administrative charge”below, also may partially compensate us for these expenses.) The premium expense charge also may compensate usfor paying taxes imposed by certain states and governmental subdivisions on premiums received by insurancecompanies. All policies in all states are charged the same premium expense charge even though state premium taxesvary.

Monthly DeductionOn each Monthly Date we deduct from the value of your policy in the Fixed Account, Indexed Accounts and/orSubaccounts an amount equal to the sum of:

1. the cost of insurance for the policy month;

2. the policy fee shown in your policy;

3. the monthly administrative charge;

4. the monthly mortality and expense risk charge;

5. the Indexed Account charge; and

6. charges for any optional insurance benefits provided by rider for the policy month.

We explain each of the six components below.

You specify, in your policy application, what percentage of the monthly deduction from 0% to 100% you want us to takefrom the Fixed Account and from each of the Subaccounts. You may change these percentages for future monthlydeductions by writing to us.

We will take monthly deductions from the Fixed Account and the Subaccounts on a Pro Rata Basis if:• you do not specify the accounts from which you want us to take the monthly deduction; or• the value in the Fixed Account or any Subaccount is insufficient to pay the portion of the monthly deduction you have

specified.

When the Fixed Account, minus any Indebtedness, and the Subaccounts are exhausted, the monthly deduction will betaken from the Indexed Accounts. See “Order of Deductions from Policy Value” for further discussion.

If the Cash Surrender Value of your policy is not enough to cover the monthly deduction on a monthly anniversary, thepolicy may Lapse. However, the policy will not Lapse if the NLG is in effect or the Minimum Initial Premium Period is ineffect and the premium payment requirements have been met. (See “No Lapse Guarantee,” “Minimum Initial PremiumPeriod,” “Grace Period” and “Reinstatement” at the end of this section on policy costs.)

Components of the monthly deduction:1. Cost of Insurance: primarily, this is the cost of providing the death benefit under your policy. It depends on:• the amount of the death benefit;• the Policy Value; and

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 21

• the statistical risk that the Insured will die in a given period.

The cost of insurance for a policy month is calculated as: [a × (b – c)] + d

where:“a” is the monthly cost of insurance rate based on the Insured’s Insurance Age, Duration, sex (unless unisex rates

are required by law), Risk Classification and election of WMD. Generally, the cost of insurance rate will increaseas the insured’s attained insurance age increases.We set the rates based on our expectations of mortality, future investment earnings, persistency and expenses.Our current monthly cost of insurance rates are less than the maximum monthly cost of insurance ratesguaranteed in the policy. We reserve the right to change rates from time to time; any change will apply to allindividuals of the same rate classification. However, rates will not exceed the Guaranteed Maximum Monthly Costof Insurance Rates shown in your policy. All rates are based on the 2001 Commissioners Standard Ordinary(CSO) Smoker and Nonsmoker Mortality Tables, Age Nearest Birthday.

“b” is the death benefit on the Monthly Date divided by 1.0016515813 (which reduces our Net Amount at Risk,solely for computing the cost of insurance, by taking into account assumed monthly earnings at an annual rate of2%).

“c” is the Policy Value on the Monthly Date. At this point, the Policy Value has been reduced by the administrativecharge, mortality and expense risk charge, the policy fee and any charges for optional riders with the exception ofthe WMD as it applies to the base policy.

“d” is any flat extra insurance charges we assess as a result of special underwriting considerations.2. Policy fee: $10.00 per month for initial Specified Amounts below $100,000 and $7.50 per month for initial Specified

Amounts of $100,000 and above. This charge primarily reimburses us for expenses associated with issuing thepolicy, such as processing the application (mostly underwriting) and setting up computer records; and associatedwith administering and distributing the policy, such as processing claims, maintaining records, making policy changesand communicating with Owners. We reserve the right to change the charge in the future, but guarantee that it willnever exceed $15.00 per month.

3. Administrative charge: charged each month prior to the Insured’s Attained Insurance Age 120 anniversary. Thischarge reimburses us, in part, for expenses associated with issuing the policy, such as processing the applicationand underwriting the policy. It also partially reimburses us for commissions or other compensation paid to sellingfirms, advertising and printing of the prospectus and sales literature. We reserve the right to change theadministrative charge based on our expectations of future investment earnings, persistency, expenses and/or federaland state tax assumptions. However, it will never exceed the guaranteed administrative charge shown in the “PolicyData” section of the policy.

4. Mortality and expense risk charge: compensates us for assuming the mortality and expense risks under the policy.Currently, the mortality and expense risk charge is 0% (See “Mortality and Expense Risk Charge” for completediscussion.)

5. Indexed account charge: compensates us for certain administrative, investment and other expenses we assume inmaking available the Indexed Account options. The charge is assessed as an asset-based charge and is based onthe value of the Segments of an Indexed Account on the Monthly Date. Deductions for this charge in excess of theFixed Account Value plus the Variable Account Value will be deducted from the Segments of an Indexed Account. As aresult, the Indexed Interest Rate is effectively reduced by the monthly Indexed Account charge rate. We reserve theright to change this charge in the future, including varying it by Indexed Account; however, it will never exceed theguaranteed Indexed Account charge shown in the Policy Data section of the policy.

6. Optional insurance benefit charges: charges for any optional benefits you add to the policy by rider. (See “FeeTables — Charges Other than Fund Operating Expenses.”)

Note for Montana residents: Please disregard all policy provisions in this prospectus that are based on the sex of theInsured. The policy will be issued on a unisex basis. Also disregard references to mortality tables; the tables will bereplaced with a 70% male, 30% female blend of the 2001 CSO Smoker and Nonsmoker Mortality Tables, Age NearestBirthday.

Surrender ChargeIf you surrender your policy or the policy Lapses during the first ten policy years or in the ten years following an increasein Specified Amount, we will reduce your Policy Value, minus Indebtedness, by the applicable Surrender Charge.

The Surrender Charge primarily reimburses us for costs of issuing the policy, such as processing the application (mostlyunderwriting) and setting up computer records. It also partially pays for commissions, advertising and printing theprospectus and sales literature.

22 RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus

The maximum Surrender Charge for the initial Specified Amount is shown in your policy. It is based on the Insured’sInsurance Age, sex (unless unisex rates are required by law), Risk Classification and initial Specified Amount. Themaximum Surrender Charge for the initial Specified Amount will decrease monthly until it is zero at the end of ten policyyears. If you increase the Specified Amount, an additional maximum Surrender Charge will apply. The additionalmaximum Surrender Charge in a revised policy will be based on the Insured’s Attained Insurance Age, sex (unlessunisex rates are required by law), Risk Classification and the amount of the increase. It will decrease monthly until it iszero at the end of the tenth year following the increase.

The following table illustrates the maximum Surrender Charge for VUL 5 and VUL 5 – ES. For VUL 5, we assume a male,insurance age 35 qualifying for preferred nontobacco rates and the Specified Amount to be $400,000. For VUL 5 – ES,we assume a male, insurance age 40 qualifying for preferred nontobacco rates and the Specified Amount to be$1,500,000.

Lapse or surrenderat beginning of year

Maximum Surrender Charge for:VUL 5 VUL 5 – ES

1 $8,373.27 $35,695.00

2 8,292.47 35,275.00

3 8,211.67 34,855.00

4 8,130.87 34,435.00

5 8,050.07 34,015.00

6 7,843.07 33,069.50

7 6,247.87 26,343.50

8 4,652.67 19,617.50

9 3,057.47 12,891.50

10 1,462.27 6,165.50

11 0.00 0.00

Partial Surrender ChargeIf you surrender part of the value of your policy, we will charge you $25 (or 2% of the amount surrendered, if less). Weguarantee that this charge will not increase for the Duration of your policy.

If you have the AdvanceSource Rider(1) on your policy, once Notice of Claim is received partial surrenders are no longerallowed.

Mortality and Expense Risk ChargeThe mortality and expense risk charge is deducted monthly as part of the monthly deduction. It compensates us forassuming the mortality and expense risks under the policy. It is equal to:

(a) × (b)where:

12

“a” is the Variable Account Value; and“b” is the mortality and expense risk charge shown in the “Charges Other than Fund Operating Expenses” section ofthis prospectus.

The charge primarily compensates us for:• Mortality risk — the risk that the cost of insurance charge will be insufficient to meet actual claims.• Expense risk — the risk that the policy fee and the Surrender Charge (described above) may be insufficient to cover

the cost of administering the policy.

Any profit from the mortality and expense risk charge would be available to us for any proper corporate purposeincluding, among others, payment of sales and distribution expenses, which we do not expect to be covered by thepremium expense charge and Surrender Charges discussed earlier. We will make up any further deficit from our generalassets. We reserve the right to change the mortality and expense risk rate based on our expectations of mortality,reinsurance costs, future investment earnings, persistency, expenses, and/or federal and state tax assumptions.However, it will never exceed the guaranteed mortality and expense risk rate shown in the “Policy Data” section of thepolicy.

(1) This rider has a different name in some jurisdictions. (See Appendix A.)

RiverSource Variable Universal Life 5 / RiverSource Variable Universal Life 5 — Estate Series — Prospectus 23

Total Annual Operating Expenses of the FundsAny applicable management fees12b-1 fees and other expenses of the Funds are deducted from, and paid out of, theassets of the Funds as described in each Fund’s prospectus.

Effect of Loads, Fees and ChargesYour death benefits, Policy Values and Cash Surrender Values may fluctuate due to an increase or decrease in thefollowing charges:• cost of insurance charges;• Surrender Charges;• cost of optional insurance benefits;• policy fees;• administrative charges;• mortality and expense risk charges;• Indexed Account charges; and• annual operating expenses of the Funds, including management fees12b-1 fees and other expenses.

In addition, your death benefits, Policy Values and Cash Surrender Values may change daily as a result of theinvestment experience of the Subaccounts.

Other Information on ChargesWe may reduce or eliminate various fees and charges on a basis that is fair and reasonable and applies to all policyOwners in the same class. We may do this for example when we incur lower sales costs and/or perform feweradministrative services than usual.

RiverSource LifeWe are a stock life insurance company organized under the laws of the State of Minnesota in 1957. Our address is70100 Ameriprise Financial Center, Minneapolis, MN 55474. We are a wholly-owned subsidiary of Ameriprise Financial,Inc.

We conduct a conventional life insurance business. We are licensed to do business in 49 states, the District ofColumbia and American Samoa. Our primary products currently include fixed and variable annuity contracts and lifeinsurance policies.