Third quarter 2016 - Microsoft · Agenda 2 1 Third quarter 2016 results 2 Hafslund’s role in the...

52

Third quarter 2016 Finn Bjørn Ruyter Oslo, 25 October 2016 Presentation to analysts

Transcript of Third quarter 2016 - Microsoft · Agenda 2 1 Third quarter 2016 results 2 Hafslund’s role in the...

Third quarter 2016

Finn Bjørn Ruyter

Oslo, 25 October 2016

Presentation to analysts

Agenda

2

1 Third quarter 2016 results

2 Hafslund’s role in the green shift

3 Appendix

Third quarter 2016 highlights

• Historically high year-to-date profit after tax for the third quarter of NOK

1,019 million – up NOK 19 million on the same quarter the previous

year.

• EBITDA of NOK 659 million on a par with the previous year.

• Networks' result up NOK 61 million on the same quarter in 2015.

• Energy production and demand slightly lower than the third quarter of

2015 due to lower water flow and mild weather towards the end of the

quarter.

• Power price for Oslo area (NO1) of 0.21 NOK/kWh up 0.11 NOK/kWh,

from historical low level in the comparative prior-year quarter.

• Introduction of automatic power meters (AMS) and construction of new

generator at Vamma proceeding according to plan.

3

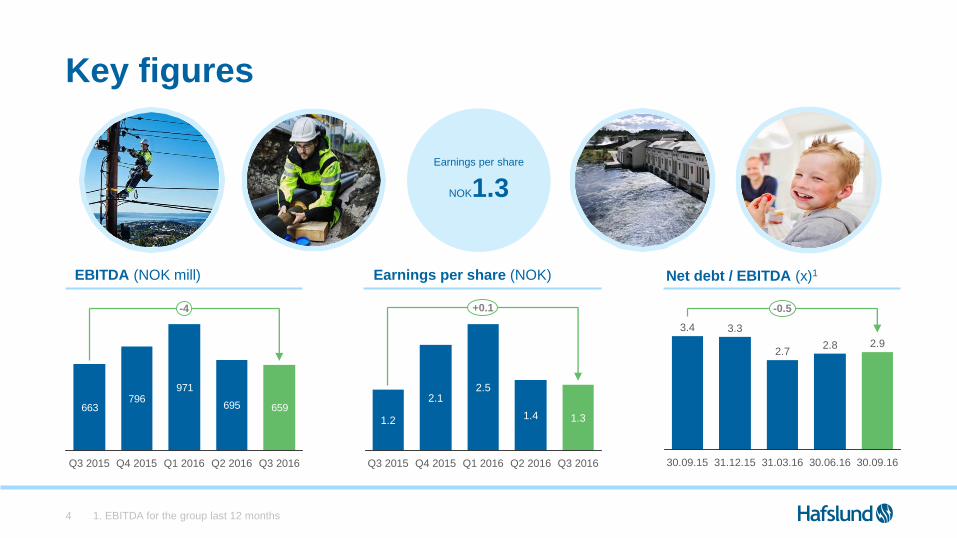

Key figures

1. EBITDA for the group last 12 months4

2.7

-0.5

30.09.16

2.92.8

31.12.15 30.06.1631.03.16

3.3

30.09.15

3.4

EBITDA (NOK mill) Earnings per share (NOK)

Earnings per share

NOK1.3

Net debt / EBITDA (x)1

663796

971

695 659

Q2 2016Q1 2016 Q3 2016

-4

Q3 2015 Q4 2015

1.4

+0.1

1.3

2.5

Q1 2016Q4 2015 Q3 2016Q2 2016

2.1

Q3 2015

1.2

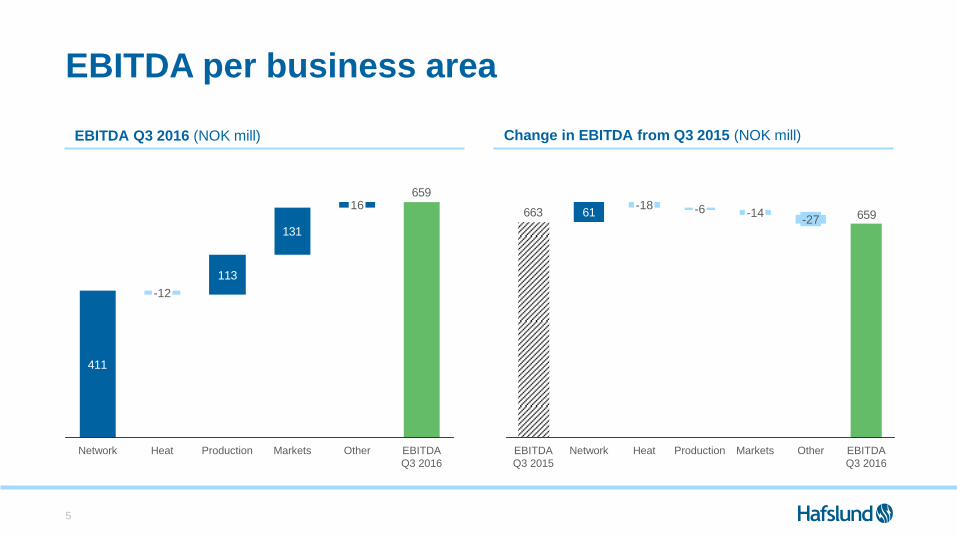

EBITDA per business area

5

411

113

131

659

Markets

16

OtherProduction EBITDA

Q3 2016

-12

Network Heat

65961663

EBITDA

Q3 2015

-27

EBITDA

Q3 2016

-14

Heat

-18

Production

-6

Markets OtherNetwork

EBITDA Q3 2016 (NOK mill) Change in EBITDA from Q3 2015 (NOK mill)

Somewhat higher number of less serious injuries since the previous report. A strong focus on

competence building and monitoring of injuries to prevent recurrence.

HSE

1 last 12 months, the total number of injuries per million manhours on own employees and suppliers in our facilities in Hafslund Group excl. Market

2 Industry average for total injuries acc. To Energy Norway's statistics for 2014, for companies in the energy industry, incl. the contractors, but without suppliers6

0injuries

Goal

9.0Injuries per million

hours (H2)

10.9Injuries per million

hours (H2)

Industry average 2Last 12 months per

30.09.2016 1

Lower production than last year due to reduced water flow, and warmer weather at the end of the

quarter reduced the energy demand

Production and distribution

7

Heat and Production (GWh)

1 050

681 618

930821

151

511 722262

136

Q3 2015 Q1 2016 Q2 2016

-244

Q4 2015 Q3 2016

ProductionHeat

Network (GWh)

Q1 2016

3.856

5.498

Q3 2015

3.302

Q2 2016

-118

6.602

Q4 2015 Q3 2016

3.184

Network

Power price development NO1

Source NordPool Spot, and Nasdaq OMX Commodities per

30.09.20168

0.15

0.10

0.05

0.20

0.30

0.25

0.00Jan JulApr JunMar May SepFeb Aug Nov DecOct

NOK/kWh

2015

2016

Rising power prices have reduced the effect hedging activity has on company results

Developments in forward prices and hedge trading

Source Nasdaq OMX Commodities, Bloomberg. Per 10.10.20169

Forward prices for 2017 (YR-17) Results from hedging activity (NOK mill)

10

15

20

25

30

35

Jan-17Jul-16Jul-12 Jan-14 Jan-16Jul-14Jan-13Jan-12 Jul-15Jan-15Jul-13

øre/kWh

Forward price

25

86

163

1513

201520142013 Ytd 20162012

Results per business area

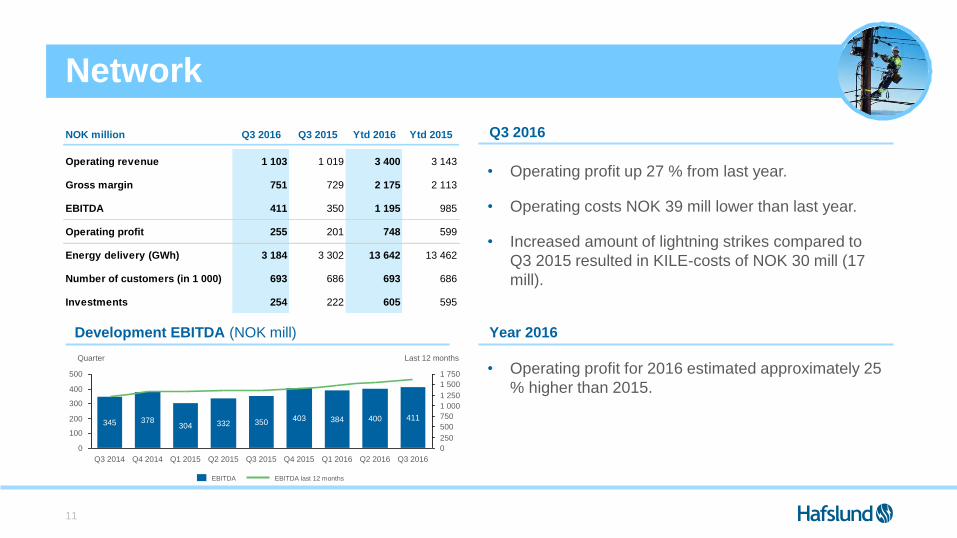

10

NETWORK HEAT PRODUCTION MARKETS

11

• Operating profit up 27 % from last year.

• Operating costs NOK 39 mill lower than last year.

• Increased amount of lightning strikes compared to

Q3 2015 resulted in KILE-costs of NOK 30 mill (17

mill).

0

1 250

1 000300

750

500200

250

1 750

1 500

100

0

500

400

Q1 2015Q4 2014 Q3 2016

345

Last 12 months

411400

Q3 2015

350

Q2 2015 Q2 2016Q1 2016

384

Q4 2015

Quarter

403304

378 332

Q3 2014

• Operating profit for 2016 estimated approximately 25

% higher than 2015.

Development EBITDA (NOK mill)

Q3 2016

Year 2016

Network

EBITDA last 12 monthsEBITDA

NOK million Q3 2016 Q3 2015 Ytd 2016 Ytd 2015

Operating revenue 1 103 1 019 3 400 3 143

Gross margin 751 729 2 175 2 113

EBITDA 411 350 1 195 985

Operating profit 255 201 748 599

Energy delivery (GWh) 3 184 3 302 13 642 13 462

Number of customers (in 1 000) 693 686 693 686

Investments 254 222 605 595

* Given normal energy demand the rest of the year, current network tariffs and forward power prices12

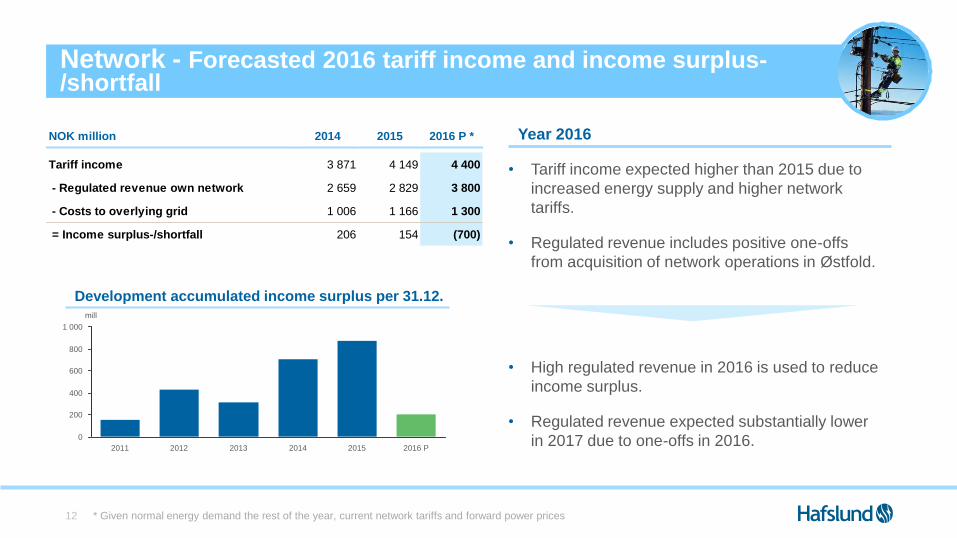

Year 2016

• Tariff income expected higher than 2015 due to

increased energy supply and higher network

tariffs.

• Regulated revenue includes positive one-offs

from acquisition of network operations in Østfold.

• High regulated revenue in 2016 is used to reduce

income surplus.

• Regulated revenue expected substantially lower

in 2017 due to one-offs in 2016.

Network - Forecasted 2016 tariff income and income surplus-/shortfall

800

600

400

200

0

1 000

mill

2016 P20152014201320122011

Development accumulated income surplus per 31.12.

NOK million 2014 2015 2016 P *

Tariff income 3 871 4 149 4 400

- Regulated revenue own network 2 659 2 829 3 800

- Costs to overlying grid 1 006 1 166 1 300

= Income surplus-/shortfall 206 154 (700)

Network - status AMS

13

Roll-out phase

700 000 total

power meters

August

16

• Full scale roll-out of power meters started in August.

• Accumulated investments of NOK 454 mill per

30.09.16 against total project estimate of NOK 2.4

billion.

Pilots

Sept

16

Ultimo

18

30 000

installed power

meters

Roll-out plan

H2 2016

H1 2017

H2 2017

H1 2018

H2 2018

Not Hafslund

14

300

300

250

150

200 450

100

50

0

-50

150

600

0

-12

Quarter

Q3 2015Q4 2014

116

Q3 2014 Q1 2016

5

Last 12 months

Q2 2016

285

Q4 2015

157

6

Q1 2015

201

-9 19

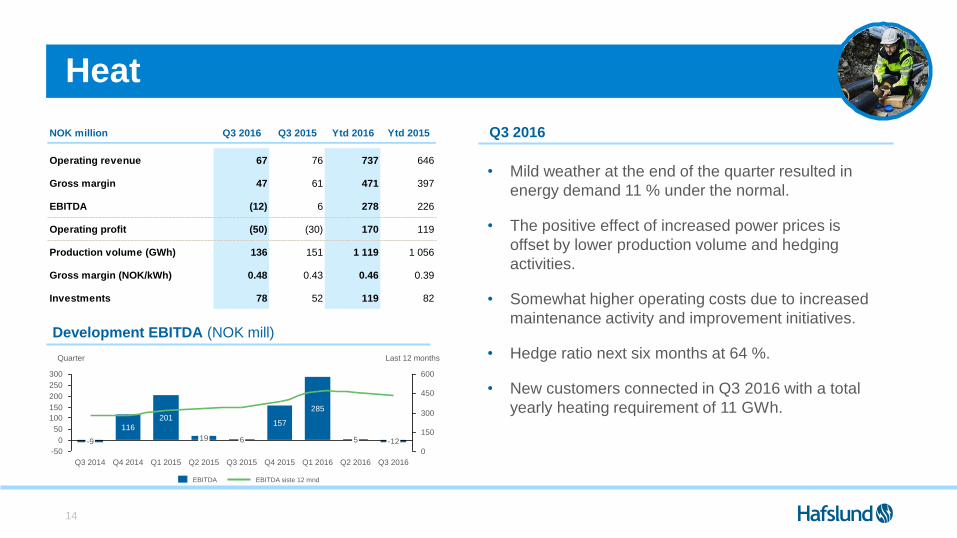

Q2 2015 Q3 2016

• Mild weather at the end of the quarter resulted in

energy demand 11 % under the normal.

• The positive effect of increased power prices is

offset by lower production volume and hedging

activities.

• Somewhat higher operating costs due to increased

maintenance activity and improvement initiatives.

• Hedge ratio next six months at 64 %.

• New customers connected in Q3 2016 with a total

yearly heating requirement of 11 GWh.

Development EBITDA (NOK mill)

Q3 2016

Heat

EBITDA EBITDA siste 12 mnd

NOK million Q3 2016 Q3 2015 Ytd 2016 Ytd 2015

Operating revenue 67 76 737 646

Gross margin 47 61 471 397

EBITDA (12) 6 278 226

Operating profit (50) (30) 170 119

Production volume (GWh) 136 151 1 119 1 056

Gross margin (NOK/kWh) 0.48 0.43 0.46 0.39

Investments 78 52 119 82

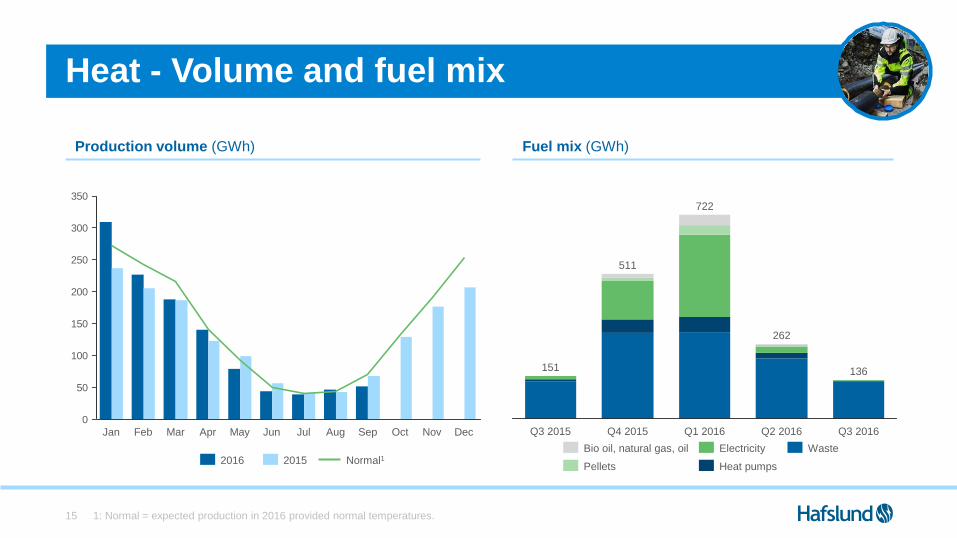

Heat - Volume and fuel mix

1: Normal = expected production in 2016 provided normal temperatures.15

0

50

100

150

200

250

300

350

JunJan NovOctAprMar May DecSepAugJulFeb

20152016 Normal1

Production volume (GWh) Fuel mix (GWh)

Q3 2016

136

722

Q3 2015 Q4 2015

511

151

Q1 2016 Q2 2016

262

Bio oil, natural gas, oil

Pellets Heat pumps

WasteElectricity

1 Normal levels for Q4 is ~690 GWh.16

150

0

120

40

300

450

80

600

0

160

147

Last 12 months

Q1 2016

95

Q4 2015

91

Q3 2015

119

Q3 2016

113

Q2 2016Q2 2015

129

65

117

Q1 2015

153

Q4 2014Q3 2014

Quarter

Development EBITDA (NOK mill)

• Production volume is 22 % below last year and 11 %

below the normal.

• Revenue (NOK/kWh) of 0.20 is NOK 0.03 higher

than last year and slightly below power price NO1.

• Hedge ratio next six months at 35 %.

• Estimated production in Q4 slightly below normal

levels1.

Q3 2016

Production

EBITDA EBITDA last 12 months

NOK million Q3 2016 Q3 2015 Ytd 2016 Ytd 2015

Operating revenue 167 176 519 503

EBITDA 113 119 355 300

Operating profit 101 107 322 266

Revenue (NOK/kWh) 0.20 0.17 0.22 0.19

Production volume (GWh) 821 1 050 2 369 2 609

Investments 52 4 179 20

Production and water flow

1: Normal production = 3100 GWh based on 10 years data adjusted for efficiency improvements.

2: Normal = Median water flow last 10 years.17

0

100

200

300

400

DecJun OctSepFebJan Aug NovMayMar Apr Jul

2016 Normal 12015

Production (GWh)

0

500

1 000

1 500

2 000

aprjan novjulmai aug desfeb jun oktmar sep

Normal 2 Max. capacity utilization20152016

Water flow and capacity utilization (m3/sec)

Q3

18

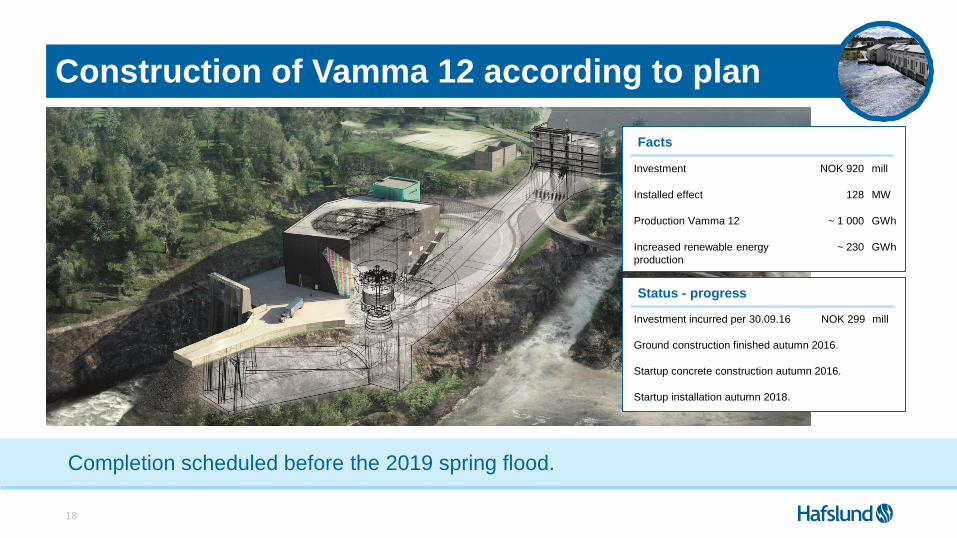

Facts

Investment NOK 920 mill

Installed effect 128 MW

Production Vamma 12 ~ 1 000 GWh

Increased renewable energy

production

~ 230 GWh

Completion scheduled before the 2019 spring flood.

Construction of Vamma 12 according to plan

Status - progress

Investment incurred per 30.09.16 NOK 299 mill

Ground construction finished autumn 2016.

Startup concrete construction autumn 2016.

Startup installation autumn 2018.

19

80

160

40

0

120

240 600

450

300

150

0

200

Quarter Last 12 months

Q3 2015

92

Q1 2016

208

137

Q1 2015

85

Q3 2016

153

Q4 2014 Q2 2016

131124

Q4 2015

145186

Q3 2014 Q2 2015

• Satisfying results in a quarter with low energy

demand.

• Increased volume due to 39,000 additional

customers than in Q3 2015.

• The result reflects costs related to increased

marketing activities and somewhat lower margins.

• 1,084,000 customers at the end of Q3, where

365,000 customers are outside Norway.Development EBITDA (NOK mill)

Q3 2016

Markets

EBITDA last 12 monthsEBITDA

NOK million Q3 2016 Q3 2015 Ytd 2016 Ytd 2015

Operating revenues 1 273 887 4 995 4 235

Gross margin 392 390 1 257 1 165

EBITDA 131 145 462 468

Operating profit 111 125 396 407

Number of customers (in 1 000) 1 084 1 045 1 084 1 045

Sold volume (GWh) 3 156 3 017 13 774 12 689

NETWORK HEAT PRODUCTION MARKETS

Group summary

20

Change in EBITDA, and profit after tax

21

659663

Operating

expenses

9

Gross marginEBITDA

Q3 2015

3

Gain/loss

financial items

10

EBITDA

Q3 2016

234

42

127

255

659

DepreciationEBITDA

Q3 2016

Financial

expenses

Profit after

tax Q3 2016

Tax

Earnings per

share NOK 1.31

Profit after tax Q3 2016 (NOK mill)Change in EBITDA from Q3 2015 (NOK mill)

Investments

22

Investments, excluding acquisitions (NOK bn.) Growth investments towards 2020

Vamma 12

NOK 920 mill.

+230 GWh

District heating

+260 GWh

Markets

Organic customer

growth2014

0.9

20152013

1.5

1.3

2018 P2017 P2016P

0.8

Annual investments Periodical avg. Investments

Network

AMS NOK 2.4 bn.

~10 000 new customers

annually

Average 2017P-2018P:

NOK 2.1 billion

Hafslund’s goal is to maintain a rating equivalent to BBB+

Change in net interest bearing debt

1: EBITDA for for the group last 12 months23

633

392266

659

9 045

Paid interest

and tax

Net debt

30.09.16

Investments Freed

capital

49

EBITDA Change in

working

capital etc

Net debt

30.09.16

8 896

2.7

3.3

30.06.16

3.4

30.09.15 31.12.15 31.03.16

2.8

30.09.16

2.9

36%

30.09.16

37%

30.06.1631.12.15

33% 34%

31.03.16

35%

30.09.15

Equity ratio (%)

Net debt / EBITDA (x)1Change in net debt in the quarter (NOK mill)

Outlook

• Operating profit 2016 for Network estimated about 25 % higher than for 2015.

• Profit after tax for Q4 is expected somewhat lower than last year due to positive one-offs in

2015, while 2016 as a whole is expected better than 2015.

• Increased level of investment driven by AMS and Vamma 12. Average annual investment of

NOK 2.1 billion over the next two years compared to an average of NOK 1.0 billion (ex.

acquisitions) for the previous three years and NOK 1.5 billion in 2016.

• Q4 and Q1 with seasonal high energy demand for Heat and Markets.

24

Agenda

25

1 Third quarter 2016 results

2 Hafslund’s role in the green shift

3 Appendix

Hafslund’s role in thegreen shift

For Hafslund, it is a strategic priority to offer green and renewable energy solutions

Hafslund has had a strong focus on green and

renewable solutions for many years

27

1898

Renewable

run-of-river

hydropower

production for

more than 100

years

2010 2011

Oil-fired and electric

boiler at Rodeløkka

replaced with

environmentally

friendly bioenergy

boiler (100 MW)

2013

More environmentally friendly

district heating with new

wood-pellet boiler (56 MW)

20152006

Oslo network upgraded

to supply power to

growing population with

increased electrification

Close to target of

100% renewable

district heating

New Vamma

generator (128 MW)

New Kykkelsrud

generator (40 MW)

Hafslund is green in all business areas

28

Vision:

The energy solutions of the future –

for you and for the environment

MARKETS

HEAT

PRODUCTION

Renewable energy

Renewable thermal energy

NETWORKS

Electrification

Renewable power

production

Renewable heating

Electrification

Efficient energy use

10,000 new

customers

per year

29

The electricity network will have the capacity to handle the growth in population and the

increasing demand for power as a result of increased electrification

Network: A robust electricity network is the key to electrification

30

• Within Hafslund’s grid area, 168 main

transformers supply a total of 19 TWh

of renewable energy per year.

• Hafslund’s investments in upgrading the

network is approaching NOK 1 billion

per year to supply electricity to a

growing population and increasing

electrification.

The network supplies renewable

electricity, 100% emission-free, to Oslo,

Akershus and Østfold

The network is dimensioned to handle increased electrification

Hafslund has modernised and upgraded capacity throughout the grid area

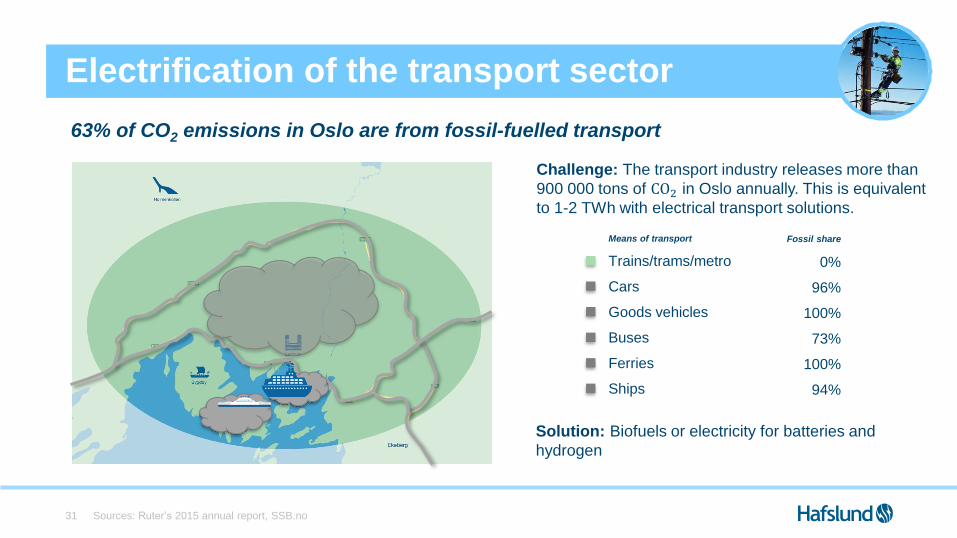

Sources: Ruter’s 2015 annual report, SSB.no 31

Fossil share

0%

96%

100%

73%

100%

94%

Electrification of the transport sector

63% of CO2 emissions in Oslo are from fossil-fuelled transport

Means of transport

Trains/trams/metro

Cars

Goods vehicles

Buses

Ferries

Ships

Solution: Biofuels or electricity for batteries and

hydrogen

Challenge: The transport industry releases more than

900 000 tons of CO2 in Oslo annually. This is equivalent

to 1-2 TWh with electrical transport solutions.

Digitalisation of the network will improve the quality of electricity supply and contribute to increased energy saving

AMS meters digitalise the network

32

700,000 meters provide 35 billion readings per year

Home

Power outage

Ground fault

Voltage

Consumption vs. production Substation

Power outage

Ground Fault

Voltage

Power out vs. in

Transformer station Operations center

Before AMS

With AMS

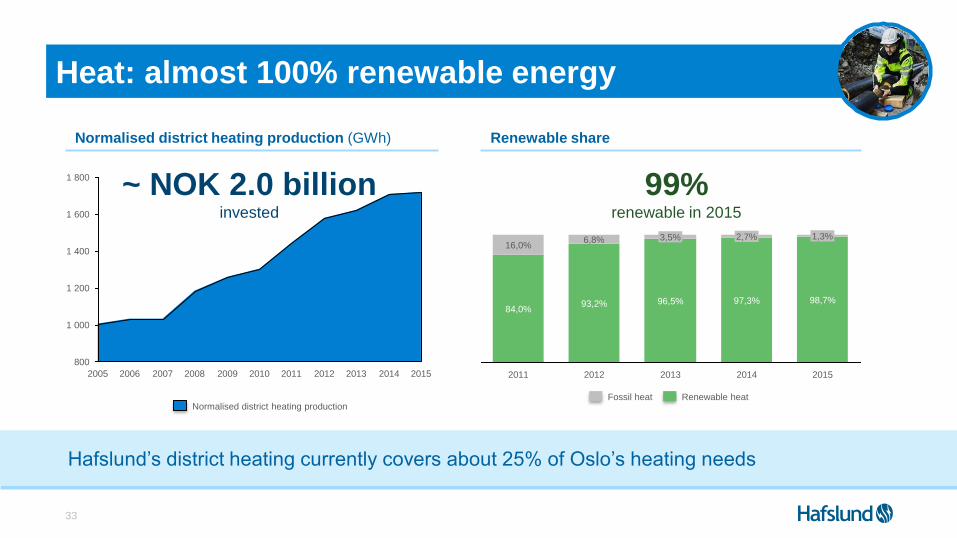

Hafslund’s district heating currently covers about 25% of Oslo’s heating needs

33

Heat: almost 100% renewable energy

800

1 000

1 800

1 400

1 600

1 200

20132012 20152011200920082006 2010 201420072005

Normalised district heating production

Renewable share

97,3%

3,5%6,8% 2,7% 1,3%

20142012 2013

93,2% 96,5% 98,7%

2011

16,0%

84,0%

2015

Fossil heat Renewable heat

Normalised district heating production (GWh)

99% renewable in 2015

~ NOK 2.0 billioninvested

34

Heating makes use of waste heat that is otherwise lost

Time in service by heating source – aiming for high share of renewable Opportunity: Heat-based ventilation cooling

Illustration: Munthers

• District heating is used to dry air, which is then

added to water molecules and cooled

• Increased utilisation of heat from waste

incineration, which would otherwise go to waste

during the summer

900

600

300

Installed

power

[MW]1,050

+2 °C

-10 °C

Price-

dependent use

Waste 161 MW

Bio-oil 259 MW

Wood pellets 56 MW

Natural gas 100 MW

Biodiesel 152 MW

Heat pumps 30 MW

Electricity 233 MW

Time in service [Hours/year]

20% of CO2 emissions relate to buildings

Sources: City of Oslo: Climate and energy strategy 201535

Renewable thermal energy replaces oil-fired heating

20% of CO2 emissions in Oslo are from fossil-fueled heating

+260 GWhnew district

heating

+240 GWhelectric heating

Challenge: 500 GWh fossil heating left in

Oslo, equivalent to roughly 270 000 tons of

CO2 emmisions.

Solution: Half can be replaced with

renewable district heating close to

Hafslund’s infrastructure, while the rest is

based on heat produced with electricity, e.g.

heat pumps

Hafslund supplies infrastructure to facilitate the

removal of fossil fuel use

36

Solutions from electrification:

- Electricity for chargers

- Electricity for hydrogen

stations

- Electricity for heating

- Electricity for heat pumps

- Shorepower to ships

Solutions from district heating:

- District heating for heating

- District heating for cooling

- District cooling

37

Production: Renewable run-of-river hydropower in Glomma

Grid area

Heat, Oslo

Power stations

Hafslund head

office

Kykkelsrud

Vamma

Sarpsborg power station area

River basin to

Hafslund’s power plant

38

New renewable energy under construction

Facts

Investment 920 MNOK

Installed capacity 128 MW

Production Vamma 12 1,000 GWh

Increased renewable production 230 GWh

Estimated completion spring 2019

39

Markets offer customer solutions for efficient energy use

20132007 2020+

Hafslund

Markets today

Big in the Nordic region

National leader

Regional player

Grønt Valg

(Green Choice)

Hafslund OnlineActive

environmental

option

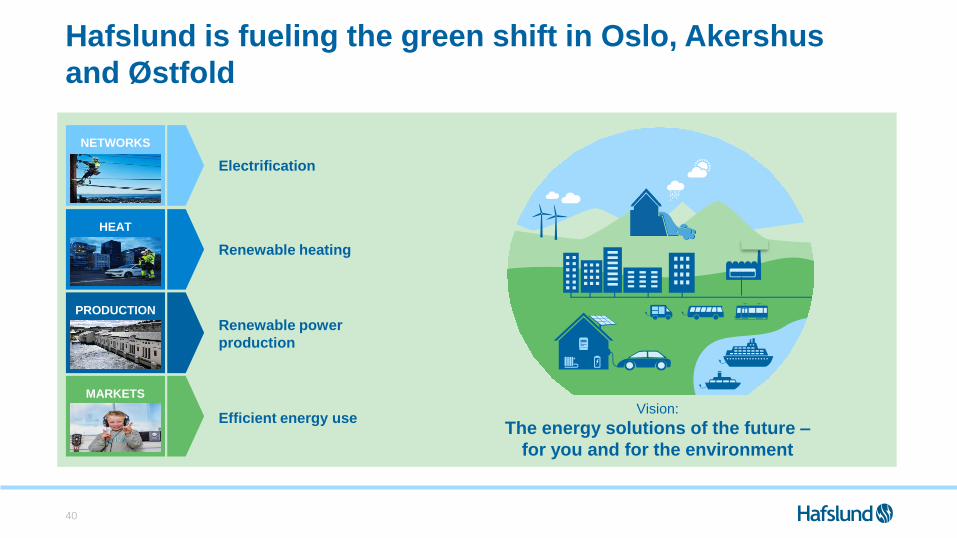

Hafslund is fueling the green shift in Oslo, Akershus

and Østfold

40

Vision:

The energy solutions of the future –

for you and for the environment

MARKETS

HEAT

PRODUCTION

Renewable energy

Renewable thermal energy

NETWORKS

Electrification

Renewable power

production

Renewable heating

Electrification

Efficient energy use

Agenda

41

1 Third quarter 2016 results

2 Hafslund’s role in the green shift

3 Appendix

Oslo price (NO1) historic and forward

Source: NordPool Spot, Nasdaq OMX

Prices per 30.09.201642

0.40

0.00

0.20

0.10

0.30

0.50

20192016 2020201520102009 2017 2018201420022000 2006200520031999 2001 2004

NOK/kWh

2007 2011 20122008 2013

Period averagePower price - Oslo price

0.21 NOK/kWh

Group profit and loss account

43

NOK million Q3 2016 Q3 2015 Ytd 2016 Ytd 2015

Operating revenue 2 580 2 158 422 9 581 8 545

Cost of energy (1 268) (836) (432) (5 310) (4 441)

Gross margin 1 312 1 322 (10) 4 271 4 104

Gain/loss financial items 28 19 9 107 78

Operating expenses (681) (678) (3) (2 054) (2 058)

EBITDA 659 663 (4) 2 324 2 124

Depreciation and write-downs (234) (236) 2 (688) (672)

Operating profit 425 427 (2) 1 636 1 452

Interest expences etc (72) (123) 51 (214) (300)

Market value change loan portfolio 30 44 (14) 57 105

Financial expenses (42) (79) 37 (157) (195)

Pre-tax profit 383 348 35 1 479 1 256

Tax (127) (111) (16) (460) (383)

Profit after tax 255 237 19 1 019 873

Earnings per share (EPS) in NOK 1,31 1,21 0,10 5,22 4,47

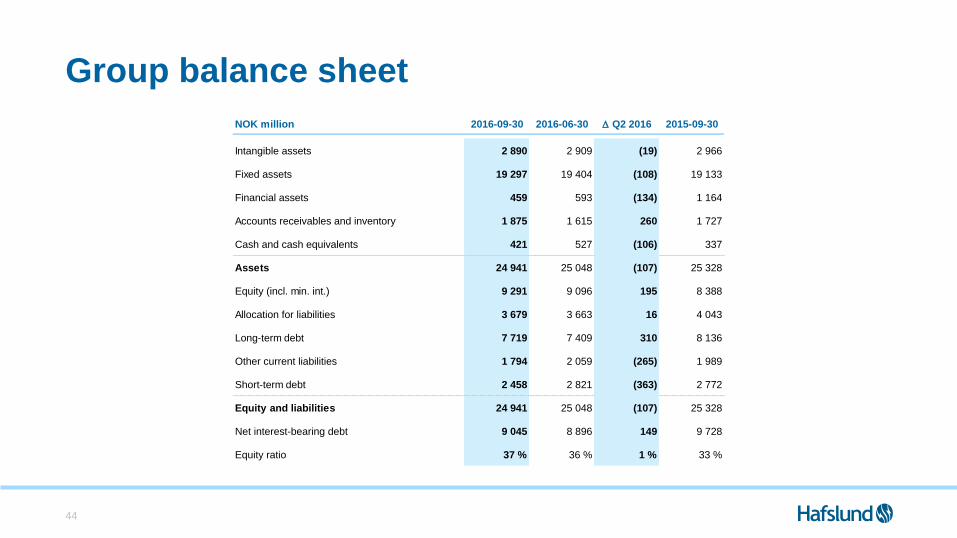

Group balance sheet

44

NOK million 2016-09-30 2016-06-30 Q2 2016 2015-09-30

Intangible assets 2 890 2 909 (19) 2 966

Fixed assets 19 297 19 404 (108) 19 133

Financial assets 459 593 (134) 1 164

Accounts receivables and inventory 1 875 1 615 260 1 727

Cash and cash equivalents 421 527 (106) 337

Assets 24 941 25 048 (107) 25 328

Equity (incl. min. int.) 9 291 9 096 195 8 388

Allocation for liabilities 3 679 3 663 16 4 043

Long-term debt 7 719 7 409 310 8 136

Other current liabilities 1 794 2 059 (265) 1 989

Short-term debt 2 458 2 821 (363) 2 772

Equity and liabilities 24 941 25 048 (107) 25 328

Net interest-bearing debt 9 045 8 896 149 9 728

Equity ratio 37 % 36 % 1 % 33 %

Group cash flow

45

NOK million Q3 2016 Q3 2015 Ytd 2016 Ytd 2015

EBITDA 659 663 (4) 2 324 2 124

Paid interests (49) (53) 4 (277) (331)

Paid tax 0 (29) 29 (362) (257)

Marketvalue changes and other liquidity adjustments (38) (40) 2 (99) (64)

Change in working capital, etc. (550) (140) (410) 314 606

Total cash flow from operations 22 401 (379) 1 900 2 078

Net operations and expansion investments (392) (296) (96) (942) (772)

Net purchase/sale of shares etc. 266 12 254 394 12

Cash flow from investments activities (126) (284) 158 (548) (760)

Cash flow to down payments and interests (104) 117 (221) 1 352 1 318

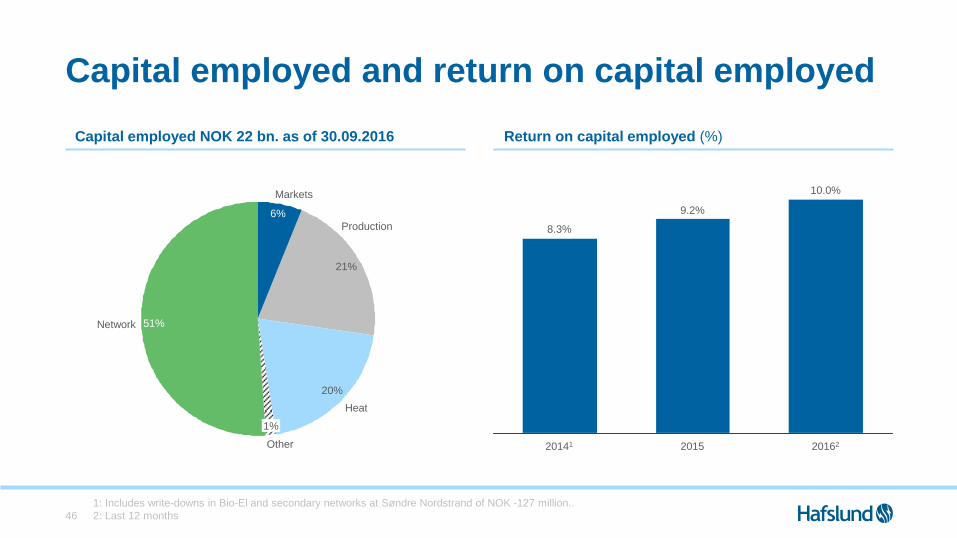

Capital employed and return on capital employed

1: Includes write-downs in Bio-El and secondary networks at Søndre Nordstrand of NOK -127 million..

2: Last 12 months46

20%

Markets

Production

21%

51%

1%

6%

Heat

Network

Other

8.3%

20141 2015 20162

9.2%

10.0%

Capital employed NOK 22 bn. as of 30.09.2016 Return on capital employed (%)

Loans – portfolio data

47

Debt maturity profileNOK million

Loans at maturity next 12 monthsNOK million

3 000

2 000

1 000

0

490

2020

972

470813

20232021

370

20222019

1 706

2018

1 189

2 010

2016

988

2017

350

2025

70

2024 2026+

Other loansBonds

800

0

600

400

200

500

700

600

488

Jul Aug SepNovOct MarFeb MayJan AprDec Jun

Other loansBonds

Q3 16 Q2 16

Bonds 73 % 76 % -3 %

Commercial paper 0 % 0 % 0 %

Other loans 27 % 24 % 3 %

NOK million Q3 16 Q2 16

Nominal value - market value of loans (160) (191) 32

Market value interest rate and fx derivatives* 33 30 3

Average interest incl. derivatives (%) 3.3 % 3.4 % -0.1 %

Loans at maturity next quarter 988 336 652

Unused drawdown facilities 3 717 3 800 (83)

*) incl. currency derivatives under hedge accounting

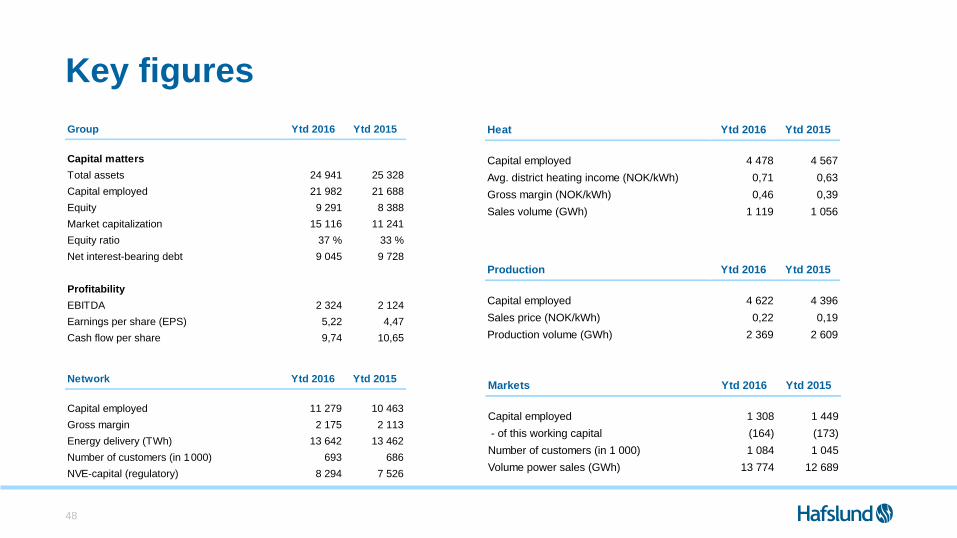

Key figures

48

Group Ytd 2016 Ytd 2015

Capital matters

Total assets 24 941 25 328

Capital employed 21 982 21 688

Equity 9 291 8 388

Market capitalization 15 116 11 241

Equity ratio 37 % 33 %

Net interest-bearing debt 9 045 9 728

Profitability

EBITDA 2 324 2 124

Earnings per share (EPS) 5,22 4,47

Cash flow per share 9,74 10,65

Production Ytd 2016 Ytd 2015

Capital employed 4 622 4 396

Sales price (NOK/kWh) 0,22 0,19

Production volume (GWh) 2 369 2 609

Heat Ytd 2016 Ytd 2015

Capital employed 4 478 4 567

Avg. district heating income (NOK/kWh) 0,71 0,63

Gross margin (NOK/kWh) 0,46 0,39

Sales volume (GWh) 1 119 1 056

Network Ytd 2016 Ytd 2015

Capital employed 11 279 10 463

Gross margin 2 175 2 113

Energy delivery (TWh) 13 642 13 462

Number of customers (in 1 000) 693 686

NVE-capital (regulatory) 8 294 7 526

Markets Ytd 2016 Ytd 2015

Capital employed 1 308 1 449

- of this working capital (164) (173)

Number of customers (in 1 000) 1 084 1 045

Volume power sales (GWh) 13 774 12 689

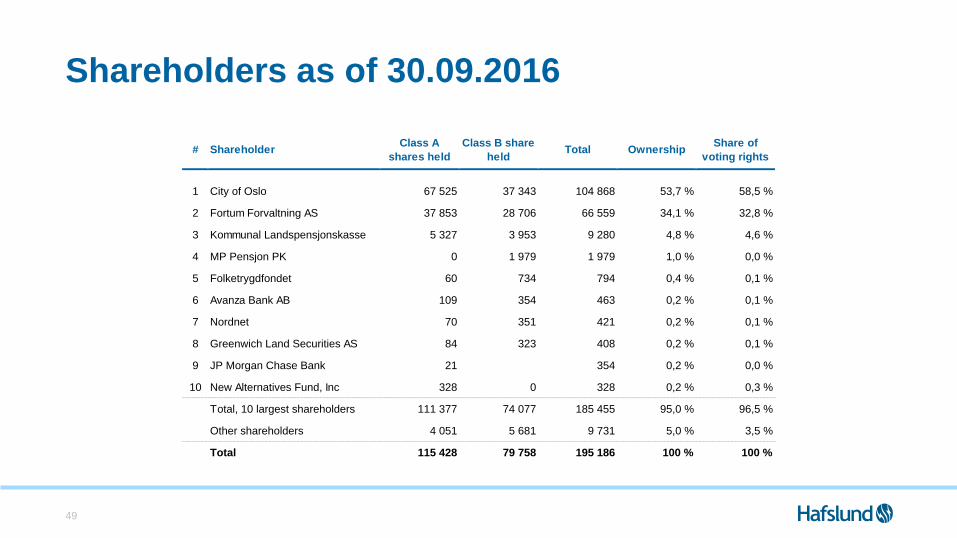

Shareholders as of 30.09.2016

49

# ShareholderClass A

shares held

Class B share

heldTotal Ownership

Share of

voting rights

1 City of Oslo 67 525 37 343 104 868 53,7 % 58,5 %

2 Fortum Forvaltning AS 37 853 28 706 66 559 34,1 % 32,8 %

3 Kommunal Landspensjonskasse 5 327 3 953 9 280 4,8 % 4,6 %

4 MP Pensjon PK 0 1 979 1 979 1,0 % 0,0 %

5 Folketrygdfondet 60 734 794 0,4 % 0,1 %

6 Avanza Bank AB 109 354 463 0,2 % 0,1 %

7 Nordnet 70 351 421 0,2 % 0,1 %

8 Greenwich Land Securities AS 84 323 408 0,2 % 0,1 %

9 JP Morgan Chase Bank 21 333 354 0,2 % 0,0 %

10 New Alternatives Fund, Inc 328 0 328 0,2 % 0,3 %

Total, 10 largest shareholders 111 377 74 077 185 455 95,0 % 96,5 %

Other shareholders 4 051 5 681 9 731 5,0 % 3,5 %

Total 115 428 79 758 195 186 100 % 100 %

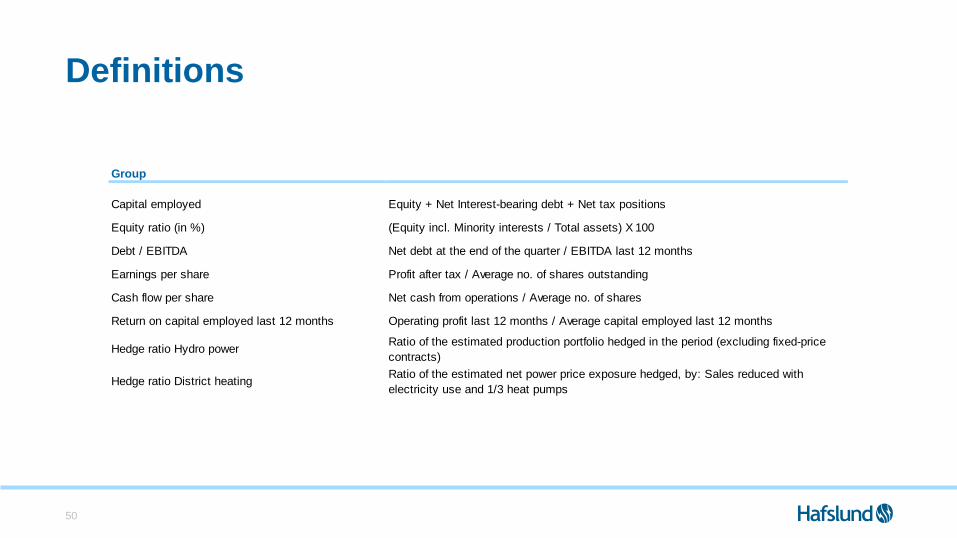

Definitions

50

Group

Capital employed Equity + Net Interest-bearing debt + Net tax positions

Equity ratio (in %) (Equity incl. Minority interests / Total assets) X 100

Debt / EBITDA Net debt at the end of the quarter / EBITDA last 12 months

Earnings per share Profit after tax / Average no. of shares outstanding

Cash flow per share Net cash from operations / Average no. of shares

Return on capital employed last 12 months Operating profit last 12 months / Average capital employed last 12 months

Hedge ratio Hydro powerRatio of the estimated production portfolio hedged in the period (excluding fixed-price

contracts)

Hedge ratio District heatingRatio of the estimated net power price exposure hedged, by: Sales reduced with

electricity use and 1/3 heat pumps

Investor information

• Additional information is available from Hafslund’s website:

– www.hafslund.no

– You can subscribe to Hafslund press releases

• Group CFO, Heidi Ulmo

– Tel: + 47 909 19 325

• Head of Finance and Investor Relations, Martin S. Lundby

– Tel: +47 416 14 448

51

![Fiscal Year ending March 31, 2016 Third Quarter ... · Third Quarter Consolidated Financial Results ... owners of the company [yen] 53.32 58.97 (5.65) ‐9.6% ... 2016 Third Quarter](https://static.fdocuments.net/doc/165x107/5afee97b7f8b9a256b8dba3d/fiscal-year-ending-march-31-2016-third-quarter-quarter-consolidated-financial.jpg)