E THIOPIA : T HINGS W HICH H INDER D EVELOPMENT Mr D Boland.

MANAGEMENT AGENCYMulti Donor Trust Fund

EthiopiaSocialAccountabilityProgramPhase 2

EthiopiaProtection of Basic Services

Social AccountabilityProgram

Social AccountabilityGuide

First edition

Chapter 10 of 13

www.esap2.org.et2 / 239

Contents

0. Contents

0. Introduction to the Social Accountability guide ................... 6

0.1. Introduction ................................................................................................6

0.2. Target Group ...............................................................................................6

0.3. Definitions and Concepts used .....................................................................7

0.4. Capacity Development Rationale ................................................................ 8

0.4.1. Overall Objective ...........................................................................................................................8

0.4.2. Specific Objective ..........................................................................................................................8

0.4.3. Results ...........................................................................................................................................8

0.5. Rationale of the Social Accountability Tools ................................................9

0.6. Approach ...................................................................................................10

0.6.1. The Three-Staged Approach and a Modular Framework .......................................................... 10

0.6.2. Training Programme for the Orientation ....................................................................................11

0.6.3. Training Programme for the Rolling-Out .................................................................................. 13

0.6.4. Monitoring and Tailored Support .............................................................................................. 14

0.7. How to Use This Document ........................................................................ 14

0.7.1. Session Overview ......................................................................................................................... 15

0.7.2. Hand-outs ................................................................................................................................... 15

0.7.3. Trainer Notes .............................................................................................................................. 16

0.8. The Social Accountability Training Tool Kit ............................................... 17

1. Introduction to Social Accountability ..................................19

1.1. Session overview ........................................................................................ 19

1.2. Hand-outs .................................................................................................. 19

1.2.1. Primer Social Accountability .......................................................................................................20

1.2.2. Exercise on Citizens’ Role in Basic Service Delivery ..................................................................23

1.2.3. Exercise on Citizen-led Social Accountability in Practice .......................................................... 25

1.3. Trainer notes .............................................................................................33

1.4. Slides .........................................................................................................38

2. Roles and Responsibilities in Social Accountability ...........40

2.1. Session overview ....................................................................................... 40

2.2. Hand-outs ................................................................................................. 40

2.2.1. Primer on Regional and Woreda Responsibilities in Service Delivery ...................................... 41

2.2.2. Exercise on Service Standards and Social Accountability .........................................................43

2.2.3. Action Plan Matrix ......................................................................................................................45

2.3. Trainer notes .............................................................................................46

2.4. Slides .........................................................................................................50

www.esap2.org.et3 / 239

3. Vulnerability and Social Inclusion ..................................... 52

3.1. Session overview ........................................................................................52

3.2. Hand-outs ..................................................................................................52

3.2.1. Primer on Social Vulnerability and Social Inclusion .................................................................. 53

3.2.2. Role-play Social Vulnerability and Social Inclusion ..................................................................54

3.2.3. Exercise on Vulnerable Groups .................................................................................................. 57

3.3. Trainer Notes .............................................................................................59

3.4. Slides .........................................................................................................64

4. Overview of the Regional and Woreda Budget Processes ... 66

4.1. Session overview ........................................................................................66

4.2. Hand-outs ..................................................................................................66

4.2.1. Primer on the Regional and Woreda Budget Process ................................................................ 67

4.2.2. Exercise on a Household Budget ............................................................................................... 72

4.3. Trainer Notes.............................................................................................74

4.4. Slides .........................................................................................................81

5. Social Accountability Tools - Community Score Cards ........ 83

5.1. Session Overview .......................................................................................83

5.2. Hand-outs ..................................................................................................83

5.2.1. Primer Community Score Card ...................................................................................................84

5.2.2. Input Tracking Form ...................................................................................................................97

5.2.3. Issues and Priorities Form ..........................................................................................................98

5.2.4. Scoring Matrix Form ...................................................................................................................99

5.3. Trainer Notes ........................................................................................... 101

5.4. Slides ....................................................................................................... 107

6. Social Accountability Tools - Citizens’ Report Cards ......... 110

6.1. Session Overview ..................................................................................... 110

6.2. Hand-outs ................................................................................................ 110

6.2.1. Primer Citizens’ Report Cards.................................................................................................... 111

6.2.2. Sample Questionnaire ...............................................................................................................119

6.2.3. Agriculture Sector Stakeholders Exercise ................................................................................ 122

6.3. Trainer Notes........................................................................................... 123

6.4. Slides ........................................................................................................131

www.esap2.org.et4 / 239

7. Social Accountability Tools - Community Mapping ............133

7.1. Session overview ...................................................................................... 133

7.2. Hand-outs ................................................................................................ 133

7.2.1. Primer community mapping ..................................................................................................... 134

7.2.2. Example of a Community Map ..................................................................................................137

7.2.3. Example of Community Mapping Exercise in Tanzania .......................................................... 138

7.2.4. Sample Enumeration Form ...................................................................................................... 139

7.2.5. Sample of a Record Book .......................................................................................................... 140

7.2.6. Nine Steps to Conducting an Interface Meeting .......................................................................141

7.3. Trainer Notes ........................................................................................... 143

7.4. Slides ....................................................................................................... 150

8. Social Accountability Tools - Participatory Planning and Budgeting ...................................................................152

8.1. Session overview ...................................................................................... 152

8.2. Hand-outs ................................................................................................ 152

8.2.1. Primer Participatory Planning and Budgeting ......................................................................... 153

8.2.2. Case Studies of Participatory Planning and Budgeting ............................................................157

8.2.3. Fictional Woreda Budget (only in five sectors) ........................................................................ 163

8.2.4. Kebele Fictional Budget ............................................................................................................ 164

8.3. Trainer Notes .......................................................................................... 165

8.4. Slides ....................................................................................................... 172

9. Social Accountability Tools - Gender Responsive Budgeting ........................................................................174

9.1. Session Overview ..................................................................................... 174

9.2. Hand-outs ................................................................................................ 174

9.2.1. Primer Gender Responsive Budgeting .......................................................................................175

9.2.2. Exercise on the Prioritization of Private Household Expenditures ......................................... 186

9.3. Trainer Notes........................................................................................... 187

9.4. Slides ....................................................................................................... 194

10. Social Accountability Tools - Social Auditing ...................197

10.1. Session overview .................................................................................... 197

10.2. Hand-outs .............................................................................................. 197

10.2.1. Primer Social Auditing ............................................................................................................ 198

10.2.2. Case studies of Social Auditing ............................................................................................... 201

10.3. Trainer notes .........................................................................................205

10.4. Slides ..................................................................................................... 212

www.esap2.org.et5 / 239

11. Capacity Development Results Framework ......................214

11.1. Session overview ..................................................................................... 214

11.2. Hand-outs ............................................................................................... 214

11.2.1. Primer Capacity Development Results Framework ................................................................ 214

11.3. Trainer notes .......................................................................................... 217

11.4. Slides ......................................................................................................222

12. Participants’ Capacity Development Action Plans ........... 224

12.1. Session overview ....................................................................................224

12.2. Hand-outs ..............................................................................................224

12.3. Trainer notes ..........................................................................................225

12.4. Slides .....................................................................................................228

13. Delivering the Training................................................... 230

13.1. Preparation of the Training ....................................................................230

13.1.1. Development of the training programme ................................................................................230

13.1.2. Preparing the training materials ............................................................................................. 231

13.1.3. Arranging for the training venue and preparing the training room. ......................................232

13.1.4. The Social Accountability Tool Box .........................................................................................232

13.2. Conduct of the Training ..........................................................................233

13.2.1. The Start of the Training .........................................................................................................233

13.2.2. Time Management ..................................................................................................................233

13.2.3. Absenteeism ............................................................................................................................234

13.2.4. Ice Breakers and Energizers ....................................................................................................234

13.3. Training Approaches ..............................................................................234

13.3.1. The Role of the Trainer ............................................................................................................234

13.3.2. Stimulating Participants .........................................................................................................237

13.4. Monitoring and Tailored Support at Woreda Level ................................238

13.4.1. Gender and Women’s Participation ........................................................................................238

13.4.2. Authority Roles ........................................................................................................................238

13.4.3. Practical Issues ........................................................................................................................238

www.esap2.org.et197 / 239

Session 10: Social Accountability Tools – Social Auditing

10. Social Accountability Tools - Social Auditing

10.1. Session overview

Aim of sessionIntroduce participants to Social Auditing and its potential use in the Ethiopian context

Learning Outcomes

At the end of the session, participants will understand: • The purpose of Social Auditing • The principles and approach of Social Auditing• The steps involved in conducting a Social Auditing• How to design and implement a Social Auditing plan

Additional results Hand-outs

Orientation training: Field level:Case studies of Social Auditing An overview of Social Auditing

Time allocationOrientation: 2 x 90 minutesIn field: 4 x 90 minutes

Work formPlenary discussions, group discussions and exercises, PowerPoint Presentation.

Key topicsSocial Auditing, Auditing Plan, Auditor General, Audit Committees Social Auditing, and Bureaus of Auditors.

10.2. Hand-outsThe following hand-outs for distribution to participants are provided on the following pages:

10.2.1 Primer Social Auditing

10.2.2 Case studies of Social Auditing

www.esap2.org.et198 / 239

Session 10: Social Accountability Tools – Social Auditing

10.2.1. Primer Social Auditing

Key message

Social Auditing can be used as a Social Accountability tool to assess service delivery processes, demonstrate the social, economic and environmental benefits of the services and indicate potentials for process improvements

Estimated reading time

15 minutes

RemarksAdapted from “Social Audit: A toolkit: a guide for performance improvement and outcome measurement”, 2005, Centre for Good Governance

What is Auditing?

The general definition of an audit is an evaluation of a person, organization, system, process, enterprise, project or product. The term most commonly refers to audits in accounting, but similar concepts also exist in project management, quality management, water management, and energy conservation.

Audits are performed to ascertain the validity and reliability of information, also to provide an assessment of a system’s internal control. The goal of an audit is to create an overall qualitative evaluation of the person, organization, system, etc., in question, on a test basis.

What is a Social Audit?

A Social audit is an independent evaluation of the performance of an organization and its at-tainment of social goals. It enables an organization to assess and demonstrate its social, eco-nomic and environmental impact and benefits. A social audit will not only examine the finan-cial status and performance of an organization but also the contribution it has made to the lives of the people it is supposed to serve.

How Different is a Social Audit Compared to other Audits?

Financial audits are focused on the verification, reliability and integrity of financial informa-tion. An operational audit focuses on establishing standards of operation, measuring perfor-mance against standards, examining and analysing deviations, taking corrective action and reappraising standards based on experience. A Social Audit provides an assessment of the im-pact of a department’s non-financial objectives through systematic and regular monitoring on the basis of the views of its stakeholders.

What are the Benefits of Social Auditing for Government Officials?

• The information from a Social Audit can provide crucial information about the depart-ments’ ethical performance and how stakeholders perceive the services offered by the government.

www.esap2.org.et199 / 239

Session 10: Social Accountability Tools – Social Auditing

• Social Auditing helps managers to understand and anticipate stakeholder concerns as it provides information about the interests, perspectives and expectations of service users.

• Social Auditing identifies specific organizational improvement goals and highlights prog-ress on their implementation and completeness.

• Social Auditing requires openness and this can further enhance accountability through the sharing of public information with the general public.

• Social Auditing is also useful in helping departments re-align their priorities with the ex-pectations of citizens.

What are the Benefits of Social Auditing for Citizens?

• The process can increase public awareness of service delivery gaps and concerns.

• It can assist in building trust between citizens and service providers.

• It can contribute to improved accountability of public officials towards citizens.

Steps to Social Auditing in Ethiopia

Step 1: Defining Objectives

In this step, the actors are involved in identifying the objectives, the various stakeholders to be involved, the projects or services to be audited, the time-frame of the audit and the factors or indicators that will be audited.

Step 2: Identifying Stakeholders

It is important to identify a wide variety of stakeholders that should include the government at different sectors or levels, service providers or private contractors, representatives of civil soci-ety organizations, beneficiaries and service provider staff members. It is important to include socially excluded groups as part of the stakeholders as well.

Step 3: Collecting and Analysing Data

Social Audits generally collect information through interviews, focus groups, surveys, quality tests, compilations of statistics, case studies, participant observations and evaluation panels. Any of these methods can be used in a blended approach. The choice of methods is depen-dent on the context, sector and objectives. Official government records are often used to track service delivery performance, but the challenge in this is often officials do not want to share such records, or the records are kept in a way that is not user-friendly. It is important to have government support early on to ensure access to essential information. Government officials should be convinced of the potential benefits of the process.

www.esap2.org.et200 / 239

Session 10: Social Accountability Tools – Social Auditing

Step 4: Dissemination of Information

After the data is collected, the findings are shared with the various stakeholders for feedback. It is important to involve the citizens who were involved in the collection of information. The citi-zens can verify the information by indicating whether services were delivered as it was stated in government official records. Where a Social Audit has been implemented stakeholders have used various methods from songs, street plays and banners to explain the process and publi-cize the Social Audit.

Step 5: Holding a Public Meeting

The findings of a Social Audit are shared at a public meeting organized and facilitated by a neu-tral party, often a local civil society organization . If the Social Audit was conducted district-wide or at a national level, it is important to host several hearings to ensure that every citizen is able to participate in this forum. The rules of conduct during the meeting should be explained up front and everyone should adhere to it. The citizens should firstly share their findings of the Social Audit, and then the public officials or service providers should respond to the findings and commentary from the citizens. The meeting should be concluded with public officials or service providers indicating their commitments to take up the issues raised by the citizens.

Step 6: Follow-up and Reporting

After the public hearing, the final Social Audit will be compiled. The report should be dis-seminated as widely as possible to government, media and other stakeholders. The report should include recommendations for government officials to address the issues identified in the report that can be used for advocacy with government to address issues of corruption and mismanagement.

Step 7: The Role of the Office of the Auditor-General

Develop and strengthen the overall audit system of Ethiopia to ensure there is access to neces-sary information for the proper management and administration of the government’s plans and budget.

Determine if all public funds of the government have been collected and used appropriately according to the law, regulations and budget.

Undertake financial and performance audits of government offices and institutions.

Submit reports to the Finance and Budgetary Affairs Standing Committee of Parliament. Au-dited entities are required to report back to the committee on what they have done in response to the recommendations made by the Auditor-General and the Committee.

www.esap2.org.et201 / 239

Session 10: Social Accountability Tools – Social Auditing

10.2.2. Case studies of Social Auditing

Key message

These cases will present the experiences and lessons of stakeholders who have undertaken Social Auditing. The participants will be able to learn from these experiences and challenges and critically think about the applicability of Social Auditing to their own context.

Estimated reading time

10 minutes per case study

Remarks Each group will receive only one case study out of the three.

Case 1: Parivartan’s Social Auditing in Delhi, India

Parivartan began in June 2000 as an organization helping citizens to gain access to govern-ment services without resorting to bribery and extortion. Its objective evolved into empower-ing the people to fight for their rights and to force systemic changes.

The passage of the Delhi Right to Information Act of 2001 allows citizens to access govern-ment held information. Parivartan’s work began by raising awareness on the Information Act and how it could be used by the general public, especially as it links to issues of access to information.

Parivartan first obtained documents through the Delhi Right to Information Act on public works in the communities: Sundernagari and New Seemapuri. Parivartan then started an awareness campaign in these areas. The field workers held street meetings, sang songs and enlightened the people about public works that should have been built.

Through this process, there was exposure of the lapses in contracts as based on the views of citizens. This roused the community to demand a public hearing, which was organized in De-cember 2001 through Parivartan and the MKSS. It was well attended, covering 1,000 people including the residents, media and other personalities. The various contracts were read out, and the residents testified as to whether or not the public works or services had been pro-vided as indicated in the contracts. Of the 68 contracts read aloud, 64 were to have irregular appropriations.

Local residents participated by going on site visits and providing testimonies to the validity of the contracts read out. They also prompted the government to realize corrective action on these lapsed public works. Several tangible results came out of the Social Auditing and Public Hearing Processes:

• On each public works site a notice board now displays all the relevant information.

• A list of all completed works within the last quarter is prominently displayed on the notice boards of all division offices.

• A list of all works carried out in a locality within the last year is painted on a wall in the area.

www.esap2.org.et202 / 239

Session 10: Social Accountability Tools – Social Auditing

• Copies of contracts for all on-going works are displayed on the walls of the local public works branch office.

• The Chief Secretary of Delhi issued an order that all government departments should con-duct their own public hearings and if these are found to be poorly implemented by the departments then the people should respond by demanding full implementation.

The greatest lasting impact of the Social Audit was that citizens realized how it was possible to hold their government accountable. This resulted in local area committees being formed in different communities. These committees would monitor the public works being conducted in their areas, demand redress where discrepancies were happening and recommend priority is-sues and areas in need of immediate attention.

The process has also ensured a more transparent and open civil service who are responsive to the needs of citizens.

Case 2: CCAGG’s Social Audit in Abra province, Philippines

The Concerned Citizens of Abra for Good Government (CCAGG) was formed in 1987 to moni-tor public spending and raise political awareness in the communities of Abra province. CCAGG began when a news article in a local newspaper listed 20 completed public infrastructure proj-ects in the region. They decided to verify the information, and in the process, they exposed discrepancies and anomalies in the government’s reports. Their report eventually led to the suspension of 11 government engineers. The CCAGG’s work has since focused on infrastruc-ture monitoring and participatory audits.

The following is the sequence of events covering the first CCAGG expenditure monitoring ex-ercise. The sequence has been repeated in subsequent projects. The group first received copies of documents pertaining to the pump-priming infrastructure plan of the Community Enhance-ment and Development Program (CEDP). The organized monitoring teams, with the help of the National Economic and Development Authority (NEDA), and the Department of Budget and Management (DBM) NEDA gave training sessions on monitoring, as well as lists and pro-files of the projects in Abra. DBM provided total project costs and the schedule of fund releases for the projects.

CCAGG organized the project’s beneficiaries and transferred the monitoring technology to them. The movement was able to expose anomalies such as ghost projects and incomplete public works.

In partnership with the United Nations Development Program (UNDP), CCAGG conduct-ed the first Participatory Audit. The regular audits would stress compliance with rules and regulations but this Participatory Audit added the concept of value for money to the audits. This means that residents themselves could assess the actual benefits derived from the public expenditures.

www.esap2.org.et203 / 239

Session 10: Social Accountability Tools – Social Auditing

The media were crucial in disseminating the results of CCAGG investigations and in help-ing to influence public opinion. CCAGG engages the local media primarily as they realized it was more important to empower people to demand good governance rather than making the CCAGG do the work for them. They disseminated information on public work projects via the local radio stations that had the largest media reach in the province.

The government audit teams investigated CCAGG’s first complaints and filed administrative cases against 11 public works engineers. Politicians tried to step in and intervene on their be-half but other civil society organizations supported the cause while the cases were prosecuted. Eventually, the accused were found guilty.

The Sinalang Detour Bride Bridge was completed in 1996 at a cost of 8.26 million pesos. It was rushed and ended up never being used due to errors in the engineering design. Overpricing of materials was also discovered. And in 1997 a flash flood destroyed the bridge unleashing a public outcry.

The CCAGG pushed for government agencies to investigate this and NEDA, Public Works and the Commission on Audit (COA) sent in their respective teams. CCAGG was not satisfied with the response from Public Works. The COA then recommended the prosecution of certain pub-lic works personnel.

Case 3: CIET Social Auditing in Islamabad, Pakistan

The Community Information and Epidemiological Technologies (CIET) International under-took a baseline study in 10 districts with over 10,000 households on devolved public services and local governance. The results of this baseline survey were released to the public and subse-quently a 5 year Social Audit of Pakistan was conducted annually to track and prove this. The devolution helped to broaden the information policy in the sectors of health, education, water, judiciary and police services.

The CIET International’s Social Audit allows for analysis of factors behind the state of public services. It strengthens the community voice not only by reflecting their views but also through formal mechanisms of participation. Ordinary folk help analyse data and develop solutions. Through the Social Audit, capacities at local and national levels are built, both in the communi-ties that use the services and in the agencies that provide them.

In the first phase of design and data collection the strategic focus is clarified, and the instru-ments are designed and pilot-tested. Information is collected from households and from key informants on a panel of representative communities.

In the second phase, the data is gathered from households and is then linked with information from public services. On this basis an analysis is drawn up with a view towards future action. These results are then brought back to the communities to stimulate their ideas for improving the services. Finally, community representatives are brought face to face with service providers and planners to discuss the evidence and find solutions.

www.esap2.org.et204 / 239

Session 10: Social Accountability Tools – Social Auditing

In the third phase, there is a process of socialization of evidence for public accountability, through a workshop where a communications plan is developed. Evidence-based training for planners and service providers is prepared, the training of media to improve reporting stan-dards is planned and the creation of partnerships with civil society organizations is prioritized.

The pilot revealed only 23 per cent of households across the country were satisfied with the government’s health services. While 45 per cent of households said they were dissatisfied with the available services while 32 per cent said they had no access at all to the government’s public health services. These results and others are used to inform government policy in health and other sectors. This is one of the first feedback mechanisms employed in Pakistan for govern-ment planners to understand the views of citizens and the areas of service delivery they can improve on.

www.esap2.org.et205 / 239

Session 10: Social Accountability Tools – Social Auditing

10.3. Trainer notesThis session is compulsory for the orientation training, and elective for the rolling-out trainings. These training notes are based on a time-frame of 360 minutes. The trainer of the 180 minute orientation training has to adjust the session accordingly.

Key messages

• Social Auditing can assist citizens and local officials to determine if public funds spent at the local level reflects the budgeted allocation of money

• Social Auditing can improve the verification processes of audits that often rely only on financial data and not on the performance of local authorities

Timing

Part 1: Introduction to Social Auditing: 45 minutesPart 2: Group exercise on case studies: 45 minutesPart 3: Group exercise on Social Auditing Plan: 60 minutesPart 4: Plenary discussions on Social Auditing Plan: 30 minutesPart 5: Group exercise on interface meetings: 60 minutesPart 6: Plenary discussions on interface meetings: 30 minutesPart 7: Group exercise on monitoring, follow-up and communication: 45 minutesPart 8: Plenary discussions on monitoring, follow-up and communication: 45 minutesTotal: 360 minutes

Work formPowerPoint presentation, group discussions and exercises, plenary discussions

Hand-outs10.2.1 Case studies of Social Auditing 10.2.2 An Overview of Social Auditing

Preparations

• Pre-prepared flip chart or PowerPoint on Social Auditing • Flip chart paper• Markers• Flip chart stand • PowerPoint projector

Remarks Distribute slides after presentation

30 minutes, PowerPoint presentation

Slide 1: Session 10: Social Auditing

Introduce theme

www.esap2.org.et206 / 239

Session 10: Social Accountability Tools – Social Auditing

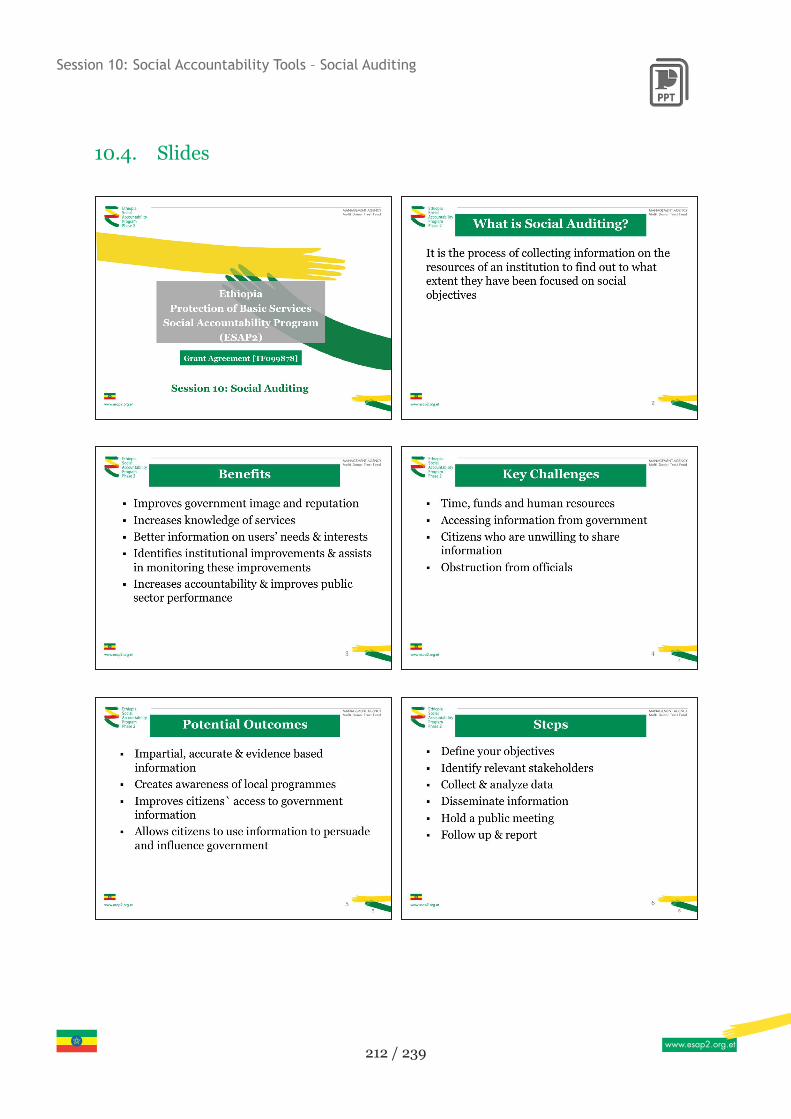

Slide 2: What is Social Auditing?

This is a process of collecting information on the resources of an institution and how it has been used for social objectives. For example, to verify whether the woreda budget has actu-ally built 20 toilets in the rural community in the previous financial year as it is stated in the regional and woreda budget expenditure reports and audit books.

Slide 3: What are the Benefits of Social Auditing?

A boost to a government’s image and reputation, and provides citizens with better knowledge of services available.

Project managers get access to information on users’ interests, needs and expectations.

Helps identify priority areas for institutional improvement and assists in tracking progress.

Increases accountability and overall improvement of public-sector performance.

Slide 4: The Challenges with Social Auditing

The process needs time, money and organizational efforts. This will require making use of local community volunteers to help undertake the verification fieldwork process.

Accessing info from government agencies can be obstructive or unreliable info may be shared. Information like woreda expenditure reports could be difficult to access when there is not a culture of sharing information in the civil service.

Citizens might be unwilling to share information due to fear of intimidation by leaders. When citizens are asked about their views of services that are related to powerful leaders in their community, they might not be forthcoming to participate and share their views on the status of service delivery. The relationship between citizens and leaders/officials needs to be considered before undertaking any Social Auditing.

Beneficiaries of corruption might want to keep the status quo and manipulate findings or in-timidate citizens. Beneficiaries of corruption could interfere in this context.

Slide 5: Potential Outcomes of Social Auditing

Information that is evidence-based, accurate and impartial: This is powerful to per-suade government officials to find corrective measures to improve service delivery.

Creates awareness among service users and providers regarding local pro-grammes: This will assist both service users and providers to be more vigilant about the local programme design, procurement processes and monitoring of the implementation of services.

www.esap2.org.et207 / 239

Session 10: Social Accountability Tools – Social Auditing

Improve citizens’ access to government held information that can expose mis-management and corruption: This information will assist citizens to effectively monitor and start creating a culture of information sharing between service users and providers.

Permits stakeholders to use information to influence government and monitor progress.

Slide 6: Steps towards Conducting a Social Audit

Step 1: Defining Objectives

In this step, the actors are involved in identifying the objectives, the various stakeholders to be involved, the projects or services to be audited, the time-frame of the audit and the factors or indicators that will be audited.

Step 2: Identifying Stakeholders

It is important to identify a wide variety of stakeholders that should include government from different sectors or levels, service providers or private contractors, representatives of civil soci-ety organizations, beneficiaries and service provider staff members. It is important to include socially excluded groups as part of the stakeholders as well.

Step 3: Collecting and Analysing data

Social Audits generally collect information through several methods that include: interviews, focus groups, surveys, quality tests, compilation of statistics, case studies, participant obser-vations and evaluation panels. Any of these methods can be used in a blended approach. The choice of methods is dependent on the context, sector and objectives. Official government re-cords are often used to track service delivery performance, but the challenge in this is that too often officials do not want to share such records or the records are kept in a way that is not user-friendly or accessible. This is why it is important to inspire government support early on to ensure access to essential information. Government officials should be convinced of the po-tential benefits of the process.

Step 4: Dissemination of Information

After the data is collected, the findings are shared with the various stakeholders for feedback. It is important to involve the citizens who were involved in the collection of information. The citizens can verify the information by indicating whether services were delivered as stated in government official records. Where a Social Audit has been implemented stakeholders have used various methods from songs, street plays and banners to explain the process and publi-cize the social audit.

www.esap2.org.et208 / 239

Session 10: Social Accountability Tools – Social Auditing

Step 5: Holding of a Public Meeting

The findings of the Social Audit are shared at a public meeting organized and facilitated by a neutral party, often a local civil society organization. If the Social Audit was conducted district-wide or at a national level, it is important to host several hearings to ensure that every citizen is able to participate in this forum. The rules of conduct during the meeting should be explained and everyone should adhere to them. The citizens should share their findings of the Social Audit first and then the public officials or service providers should respond to the findings and commentary of the citizens. The meeting should be concluded with public officials or service providers indicating their commitments to take up the issues raised by the citizens.

Step 6: Follow-up and Reporting

After the public hearing, the final Social Audit will be compiled. The report should be dissemi-nated as widely as possible to government, media and other stakeholders. The report should include recommendations for government officials to address the issues identified in the re-port. These can be used for advocacy work with the government to address issues of corruption and mismanagement.

After the PowerPoint presentation hold a discussion on the information presented and the questions that participants might have.

Slide 7: The role of the Office of the Auditor-General

• Develop and strengthen the overall audit system of Ethiopia to ensure access to necessary information for the proper management and administration of the plans and budget of the government.

• Determine if all public funds of the government have been collected and used appropriately according to the law, regulations and budget.

• Undertake financial and performance audits of government offices and institutions.

• Submit reports to the Finance and Budgetary Affairs Standing Committee of Parliament Audited entities are required to report back to the committee on what they have done in response to the recommendations from the Auditor-General and this committee.

Part 2: 45 minutes, group exercise on case studies

Slide 8: Exercise Case studies

Step 1: Divide participants into four groups. Ask each group to read the selected case study and to answer the questions based on the case study in their groups:

• What is the key lesson for the Ethiopian context of this case study?

• What could have been done differently to apply Social Auditing to the Ethiopian context?

• What are the challenges that need to be overcome to apply Social Auditing at the woreda level?

www.esap2.org.et209 / 239

Session 10: Social Accountability Tools – Social Auditing

Step 2: Ask participants to report back on their answers in plenary.

Please note: The following trainer notes for parts 3 and 4 are only to be used for the orienta-tion training. Further down are provided the trainer notes for parts 3 and 4 for the rolling out training.

Part 3 (orientation training): 45 minutes, group exercise, Social Auditing strategy

Slide 9: Exercise Social Audit

Step 1: Randomly divide participants into groups of five. Ask each group to design a Social Auditing strategy for one woreda and to focus on one sector out of the five ESAP2 sectors. In addition to applying the six steps outlined in the PowerPoint presentation they should also consider:

• What type of information can they access from service facilities and woreda administration offices?

• What type of support would they need from the MA?

Part 4 (orientation training): 45 minutes, plenary discussion, Social Au-diting strategy

Ask each of the five groups to present their Social Auditing strategy with additional questions. Other groups are allowed to ask questions after each presentation. A key focus of the discus-sion should be on the applicability of the Social Auditing tool at the woreda level in the Ethio-pian context.

Please note: The following trainer notes for parts 3 and 4 are only to be used for the rolling out training.

Part 3 (rolling–out training): 60 minutes, group exercise on Social Audit-ing Plan

Slide 9: Exercise Social Audit

Divide participants into different groups and ask them to apply the steps of Social Auditing to design their own plan. This has to be applied to the woreda level. They are free to choose a real woreda or a fictional one.

www.esap2.org.et210 / 239

Session 10: Social Accountability Tools – Social Auditing

Part 4 (rolling-out): 30 minutes, plenary discussion on Social Auditing plan

Slide 10: Exercise on Interface Meeting

Ask each group to present their woreda Social Auditing plan. Hold a discussion on their pre-sentations and ask other participants for their views as well.

Part 5 (rolling-out): 60 minutes, group exercise on interface meetings

Slide 11: Group Exercise on Social Auditing Process

Ask participants to go back to the groups they were in when they designed the Social Auditing plan for their woreda. The task now is to design in more detail the interface meeting they will hold in terms of:

1. Identification and preparation of stakeholders before the interface meeting.

2. The design of the process of the interface meeting.

3. The key messages they would like to communicate to the audience.

4. The outcome of the interface, i.e., an action plan or other activities.

Part 6 (rolling-out): 30 minutes, plenary discussion

Ask each group to present their answers to the questions raised. Hold a discussion based on their responses and ask other participants for their views as well.

Part 7 (rolling-out): 45 minutes, group exercise on monitoring, follow-up and communication

Slide 12: Exercise Social Auditing Process

Ask participants to go back into the groups. The various groups have held their interface meet-ings and now they must design a process of monitoring, follow-up and communication of the Social Auditing process. The groups should consider:

1. What are the mechanisms for monitoring the commitments made during the interface meeting?

2. What are the feedback mechanisms you will use to communicate with the community on the progress of the commitments made during the interface meeting?

3. What steps will you undertake to communicate the Social Auditing results to other stake-holders like the media and regional administrations? How will you involve them in your monitoring and follow up processes?

www.esap2.org.et211 / 239

Session 10: Social Accountability Tools – Social Auditing

4. What are the steps you will employ to create sustainability in the Social Auditing process? Is this going to be a one off activity or do you want to include this as part of the woreda planning and budgeting process?

Part 8 (rolling-out): 45 minutes, plenary discussions

Ask each group to present their answers to the questions. Hold a discussion based on their responses and ask other participants for their views as well. Emphasise with participants that sustainability of their efforts should be considered early in the design of their projects and should be checked at each stage of the process.

www.esap2.org.et212 / 239

Session 10: Social Accountability Tools – Social Auditing

10.4. Slides

www.esap2.org.et213 / 239

Session 10: Social Accountability Tools – Social Auditing