(Thinking About) Hedging Municipal Portfolios with...

23

(Thinking About) Hedging Municipal Portfolios with Derivatives Cadmus Hicks February 20, 2003 2003 by Nuveen Investments

Transcript of (Thinking About) Hedging Municipal Portfolios with...

(Thinking About) Hedging Municipal Portfolios

with DerivativesCadmus Hicks

February 20, 2003

2003 by Nuveen Investments

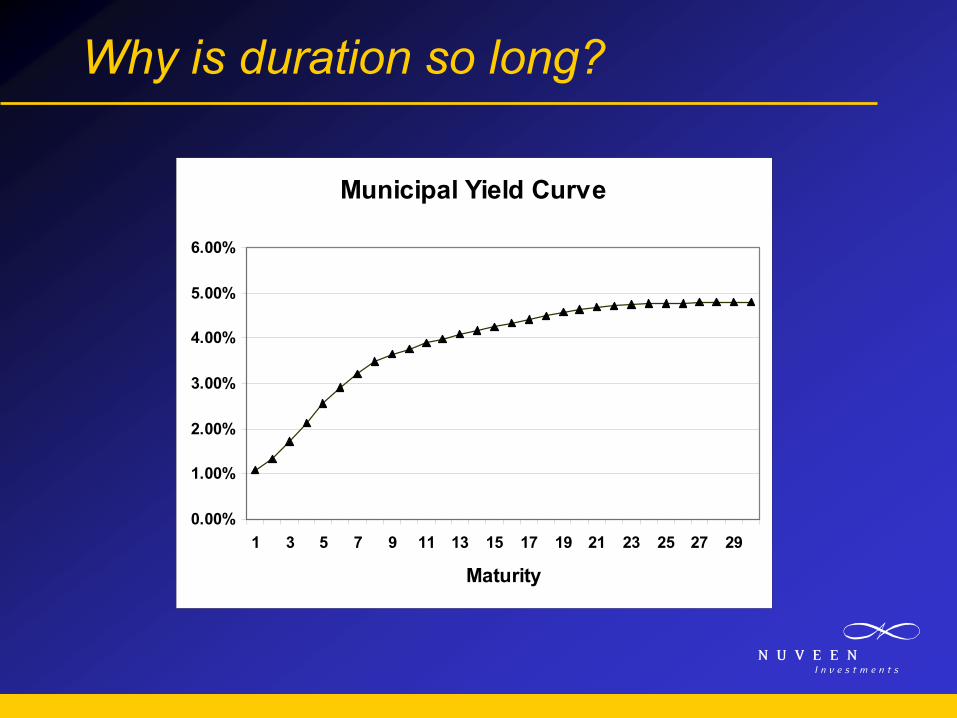

Why is duration so long?

Municipal Yield Curve

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

1 3 5 7 9 11 13 15 17 19 21 23 25 27 29

Maturity

Why is duration so long?

Municipal Yield Curve

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

0.00 2.00 4.00 6.00 8.00 10.00 12.00 14.00 16.00 18.00

Duration

The Challenge

• To reduce the price volatility of a fund to match that of a benchmark.

Moving Target, Moving Train

Parallel Shift: Durations of Fund vs. Benchmark

5

6

7

8

9

10

11

12

125i

100i 75

i

50i

25i

Baseli

ne -25i

-50i

-75i

-100i

-125i

paralle l s hift yie ld s ce nario

dura

tion

Benchmark Fund

Moving Target, Moving Train

D ifference in D urations of Fund - B enchmark

0.4

0.9

1.4

1.9

2.4

2.9

3.4

3.9

4.4

125i

100i 75

i

50i

25i

Baseli

ne -25i

-50i

-75i

-100i

-125i

paralle l s hift yie ld s ce nar io

dura

tion

diffe

renc

e

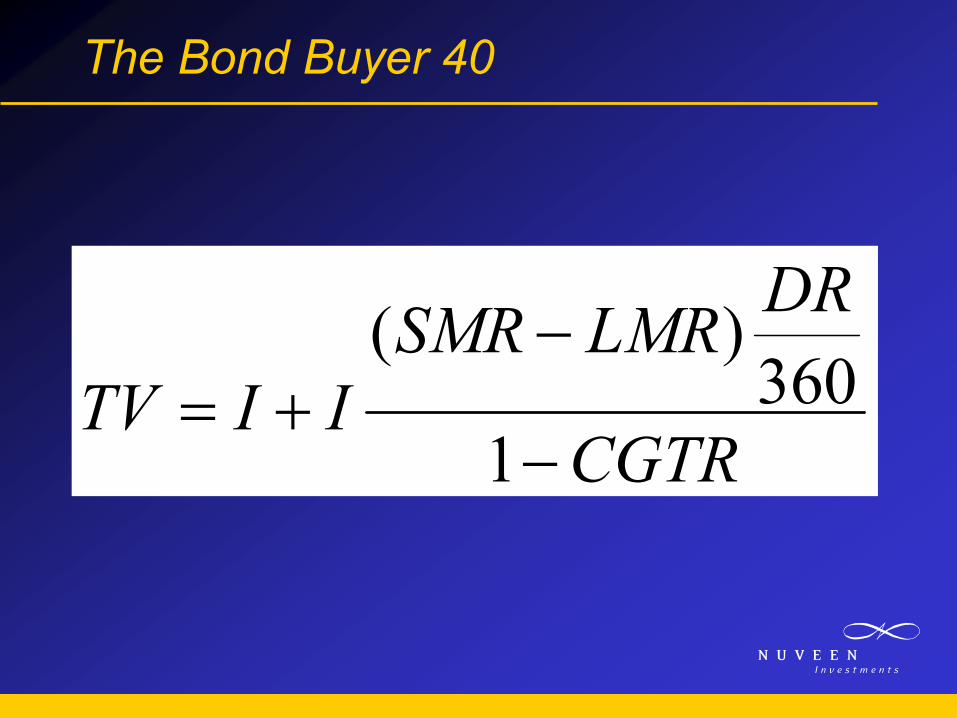

The Bond Buyer 40

TV = Theoretical value of the contract

I = Index valueSMR= Short-term municipal rateLMR = Long-term municipal rateDR = Days remaining until expirationCGTR= Capital gains tax rate

The Bond Buyer 40

CGTR

DRLMRSMRIITV

−

−+=

1360

)(

The Bond Buyer 40

Advantages:In use for many years.No counterparty risk.

Disadvantages:Low trading volume, low liquidity.Underlying Index subject to manipulation.

MMD Rate Locks

• Maturity: 2023 Yield:4.65%

• Value of 1 bp per $1 million: $1,289

• 5 bp spread x DV01/$1MM: $6,443

• Effect of spread on return: 64 bp

• Annualized effect: 258 bp.

MMD Rate Locks

Assume:

Portfolio = $100MM

Average Life = 15 Years

Average Duration = 11 years

DV01 = $110,000

MMD Rate Locks

Assume Target:

Average Life = 10 Years

Average Duration = 8.25 years

DV01/$MM = $825

Target DV01 of Portfolio = $82,500

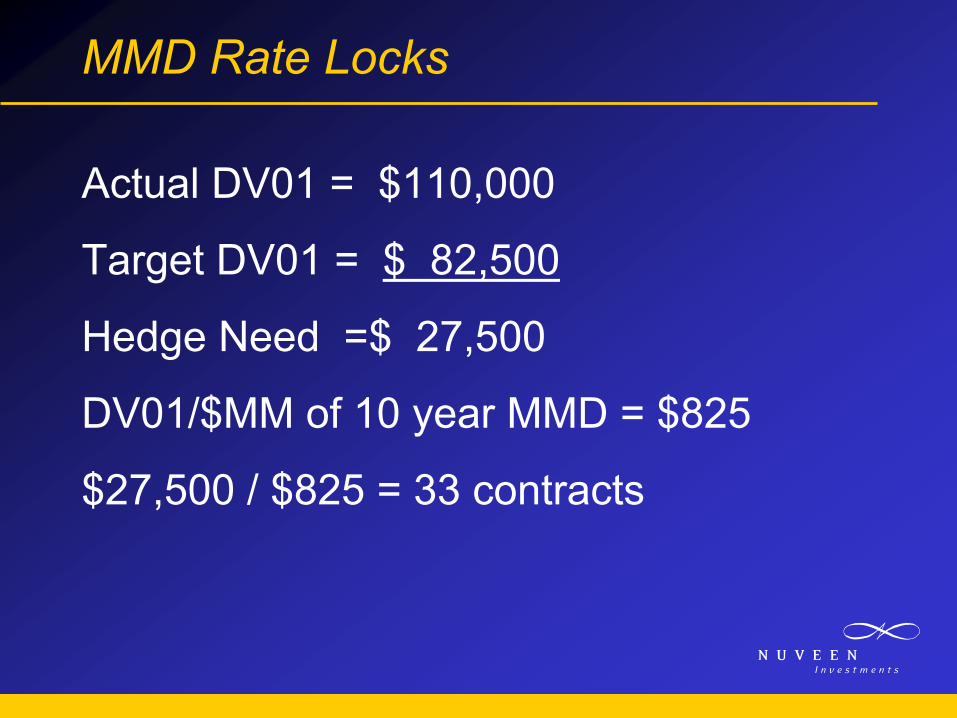

MMD Rate Locks

Actual DV01 = $110,000

Target DV01 = $ 82,500

Hedge Need =$ 27,500

DV01/$MM of 10 year MMD = $825

$27,500 / $825 = 33 contracts

MMD Rate Locks

Hedge Need =$ 27,500

DV01/$MM of 15 year MMD = $1,100

$27,500 / $1,100 = 25 contracts

DV01/$MM of 20 year MMD = $1,300

$27,500 / $1,300 = 21 contracts

Moving Target, Moving Train

Parallel Shift: Durations of Fund vs. Benchmark

5

6

7

8

9

10

11

12

125i

100i 75

i

50i

25i

Baseli

ne -25i

-50i

-75i

-100i

-125i

paralle l s hift yie ld s ce nario

dura

tion

Benchmark Fund

MMD Rate Locks

Advantages:Can take position on specific maturity.Simple to track value.

Disadvantages:Counterparty risk.Large bid/ask spread.

BMA Swaps

Advantages:Can take position on specific maturity.Bid/Ask spread of 3 basis points.

Disadvantages:Counterparty risk.Negative carry lowers tax-exempt income.Less liquid than LIBOR swaps.

Forward Starting BMA Swaps

R1 = 1-year BMA rate = 1.26%R20 = 20-year BMA rate = 4.20%F19 = Rate on 19-year swap that starts in

1 year.

(To simplify, illustration assumes annual compounding.)

Forward Starting BMA Swaps

To simplify, illustration assumes annual compounding

2020

1919

11 )1()1(*)1( RFR +=++

201919

1 042.1)1(*0126.1 =+ F

Forward Starting BMA Swaps

=+

0126.1277.2)1( 19

19F

191

19 0126.1277.2)1(

=+ F

Forward Starting BMA Swaps

0435.1)1( 19 =+ F

%35.419 =F

Forward Starting BMA Swaps

Advantages:Can take position on specific maturity.Capital gains/losses do not affect income.

Disadvantages:Counterparty risk.Less liquid than LIBOR swaps.Forward start costs more.

(Thinking About) Hedging Municipal Portfolios

with DerivativesCadmus Hicks

February 20, 2003

2003 by Nuveen Investments