The Use of Decision Criteria in Selecting Information ... · Criteria in Selecting Information...

19

Justifying IT Investments The Use of Decision Criteria in Selecting Information Systems/Technology Investments By: C. James Bacon Senior Lecturer in Information Systems University of Canterbury Christchurch, New Zealand Abstract In a competitive environment, selecting and ef- fectively pursuing the right information systems/technology (IST) investments can be key factor in sustaining corporate viability and prosperity.This study examines the criteria used by 80 organizations in allocating strategic IST resources. Seniorexecutives were asked to in- dicate which of 15 criteria they usein deciding among competing projects. They also identified how frequently the criteria are used and ranked them by importance. Theresults indicate that criteria such as the support of explicit business objectives andresponse to competitive systems are now important in selecting IST investments. Although financial criteria are usedby most organizations, the extentof analysis and applica- tion appears to leave room for improvement. Keywords: Projectselection, information tech- nology investments, systems spend- ing, project evaluation and approval ACM Category: K.6 Introduction How are investment decisions made for new systems development, packagedsoftware, machine upgrades, improved networks, emerg- ing technologies, andother information systems & technology (IST) projects? Are such decisions effective in supporting strategic business goals, targeting the use of information systems & technology,andmaximizing overall returns? Making effective investment decisionsfor IST projects hasbecome critical to the organization. Theamount of money being spent on IST is now about half of all durable equipment spending, ac- cording to U.S. Government figures (Loveman, 1991). Overall, IST spending is running at about 2.7 percent of U.S. corporate revenues (Maglit- ta andSullivan-Trainor, 1991). However, even these figures may not includewhat is suspected to be a large amount of decentralized IST spend- ing (Davis, 1989).These figures also do not in- clude the total organizational costs associated with IST investments (Keen, 1991). At the same time, increasing economic andcom- petitive pressures are compelling companies to scrutinizetheir IST operating and capital budgets verycarefully (Wilder and Hildebrand, 1992). With decreasing margins and limited capital resources, companies must ensure these resources are allocatedjudiciously among competing projects. Thus, carefuland correct IST investment (or proj- ect selection)decisions are becoming more of an economic andcompetitive necessity. There is no uniform definition of what constitutes an IST investment, and not all investment in in- formation systems and/or technology is of a capital nature.The current cost of processing and operations is clearly not. Neitheris "routine" systems maintenance. But outlays for computer hardware, network facilities, andexternally developed software products are clearly capital expenditures. In addition, in-house development projects involving new systems andsignificant enhancements would also seem to represent capital expenditures. AnIST capital investment is therefore defined as: Any acquisition of computer hardware, net- work facilities, or pre-developed software, or any "in-house" systems development project, that is expected to add to or enhance an organization’s information MIS Quarterly~September 1992 335

Transcript of The Use of Decision Criteria in Selecting Information ... · Criteria in Selecting Information...

Justifying IT Investments

The Use of DecisionCriteria in SelectingInformationSystems/TechnologyInvestments

By: C. James BaconSenior Lecturer in Information

SystemsUniversity of CanterburyChristchurch, New Zealand

AbstractIn a competitive environment, selecting and ef-fectively pursuing the right informationsystems/technology (IST) investments can be key factor in sustaining corporate viability andprosperity. This study examines the criteria usedby 80 organizations in allocating strategic ISTresources. Senior executives were asked to in-dicate which of 15 criteria they use in decidingamong competing projects. They also identifiedhow frequently the criteria are used and rankedthem by importance. The results indicate thatcriteria such as the support of explicit businessobjectives and response to competitive systemsare now important in selecting IST investments.Although financial criteria are used by mostorganizations, the extent of analysis and applica-tion appears to leave room for improvement.

Keywords:Project selection, information tech-nology investments, systems spend-ing, project evaluation and approval

ACM Category: K.6

IntroductionHow are investment decisions made for newsystems development, packaged software,machine upgrades, improved networks, emerg-ing technologies, and other information systems& technology (IST) projects? Are such decisionseffective in supporting strategic business goals,targeting the use of information systems &technology, and maximizing overall returns?

Making effective investment decisions for ISTprojects has become critical to the organization.The amount of money being spent on IST is nowabout half of all durable equipment spending, ac-cording to U.S. Government figures (Loveman,1991). Overall, IST spending is running at about2.7 percent of U.S. corporate revenues (Maglit-ta and Sullivan-Trainor, 1991). However, eventhese figures may not include what is suspectedto be a large amount of decentralized IST spend-ing (Davis, 1989). These figures also do not in-clude the total organizational costs associatedwith IST investments (Keen, 1991).At the same time, increasing economic and com-petitive pressures are compelling companies toscrutinize their IST operating and capital budgetsvery carefully (Wilder and Hildebrand, 1992). Withdecreasing margins and limited capital resources,companies must ensure these resources areallocated judiciously among competing projects.Thus, careful and correct IST investment (or proj-ect selection) decisions are becoming more of aneconomic and competitive necessity.

There is no uniform definition of what constitutesan IST investment, and not all investment in in-formation systems and/or technology is of acapital nature. The current cost of processing andoperations is clearly not. Neither is "routine"systems maintenance. But outlays for computerhardware, network facilities, and externallydeveloped software products are clearly capitalexpenditures. In addition, in-house developmentprojects involving new systems and significantenhancements would also seem to representcapital expenditures.

An IST capital investment is therefore defined as:

Any acquisition of computer hardware, net-work facilities, or pre-developed software,or any "in-house" systems developmentproject, that is expected to add to orenhance an organization’s information

MIS Quarterly~September 1992 335

Justifying IT Investments

systems capabilities and produce benefitsbeyond the short term.

This definition may vary from a general definitionof capital expenditure that refers to "long-livedassets" (International Federation of Accountants,1989). Considering the rapid rate of developmentand change in information systems & technolo-gy, there may be few IST investments that couldbe classified as "long-lived." Therefore, thedefinition of a capital investment for iST purposesincludes any investment that looks beyond theshort term, that is, anything beyond one year.

Capital budgeting is the process of planning forand deciding upon capital investments. It focuseson the evaluation of cash flows, based on thetime-value of money, using discounted cash flow(DCF) techniques. DCF techniques reduce allestimated cash outflows and inflows associatedwith a given investment or project back to thepresent, so as to express everything in presentdollar terms. Cash flows in different periods andin different projects therefore have a commonbasis of comparison. There are also non-DCFtechniques that ignore the time valueof money.These are the Payback Method (PBK) and the Ac-counting Rate of Return Method (ARR). PBKevaluates a project on the basis of how quicklyit takes to pay for itself, whereas ARR divides theaverage annual income from a project by its in-itial capital investment. These non-DCF tech-niques are frequently used as "yardsticks" inconjunction with DCF techniques.

There are two basic DCF techniques:

Net Present Value (NPV), which discountsall estimated cash flows for a project topresent value, using a required rate ofreturn or "hurdle-rate." It may also bereferred to as Expected Present Value(EPV), to reflect the incorporation of prob-ability and expected value estimates(’rhompson and Thuesen, 1987). If thepresent value of the cash inflows exceedsthe present value of the cash outflows, in-cluding the initial capital investment, thiswill give a positive net present value and,thus, encourage project acceptance.

Internal Rate of Return (IRR), which aimsto find the discount rate that would equatethe present value of estimated cash out-flows with the present value of inflows. If

this rate is greater than the required rateof return, the project may be accepted.

A third technique, the Profitability Index Method,is an extension of the two basic discounted cashflow techniques. It provides comparative profit-ability among different investments by dividingthe present value of future cash flows by a proj-ect’s initial investment.

A limitation with current capital budgeting theory,insofar as it relates to ’investments in informationsystems & technology, is that its starting pointis the cash flows as given; it essentially assumesthat those cash flows are known. Even riskanalysis only provides for the estimation of cashflows after the underlying flows have been deter-mined. Therefore, capital budgeting provides littleinsight into the quantification of benefits andestimation of cash flows (Weaver, et al., 1989).

A further limitation is that capital budgeting theoryin textbooks on the subject concentrates almostexclusively on the financial criteria (Brealey andMyers, 1988; Brigham and Gapenski, 1991; VanHorne, 1986; Weston and Brigham, 1987). Whileit might be said that every business decisioneventually comes down to financial criteria, thereare other criteria that should be, and in practiceare, considered by the managerial decisionmaker. This applies particularly to investmentsin IST.

A third limitation is that current capital budgetingtheory does little to address the organizationaland behavioral factors involved in the practice ofcapital budgeting (Hellings, 1985; Kennedy,1986).

Significance of ISTInvestment CriteriaThere seems to be a greater need to define andenhance the way in which capital expendituredecisions are carried out in practice. In particular,there is an increasing need to subject invest-ments in IST to more rigorous analysis andjustification, comparable to that undertaken forother investments (Silk, 1990). This is especiallyimportant because some studies suggest that in-vestments in IST do not necessarily provide ahigh return but may, in fact, result in costs thatcontribute to a loss in competitive capability(Loveman, 1991; Strassman, 1985).

336 MIS Quarter/y/September 1992

Justifying IT Investments

Improvement in IST capital investment decisionsshould lead to more effective and efficient useof IST resources. The expectation is that therewill be an improved targeting and more strategicuse of IST resources with resulting positive im-pact, either directly or indirectly, on the overallprofitability of the organization.

The basic question that might therefore be askedis:

How do organizations decide on their in-formation systems and technology (IST) in-vestments, and how should they decide?

This question might be dealt with in the follow-ing terms:

(a) the process in arriving at the IST capitalexpenditure decision, and (b) the criteriaor methods used.

The process is concerned with the formal and in-formal organizational dynamics involved, startingwith the initiation of an IST project or investmentand culminating in review and approval. Itanswers the question: how was the investmentdecision made? In some organizations it is ahighly political process where the informaldynamics predominate (Weill and Olson, 1989).In others, the process may be more structured(Doll and Torkzadeh, 1987; McKeen andGuimaraes, 1985).

The criteria are concerned with the financial andnon-financial justification used in proposing,evaluating, and deciding upon the project or in-vestment. They answer the question: why was theinvestment decision made?

There has been discussion on whether financialcriteria alone should be applied to IST invest-ments, given the intangible and strategic natureof some of the benefits (Badiru, 1990; Davenport,1989). There has also been some work on cashflow estimation and cost/benefit analysis methods(Due, 1989; Pohlman, et al., 1988). And since theearly days of information systems, work has beendone on the value of information (Boyd andKrasnow, 1963). There has also been compara-ble work in the related field of R&D project selec-tion (Hall and Nauda, 1990; Kim and Kang, 1989).A significant work is Parker and Benson’s (1988)book Information Economics, which considersIST investment benefits based on six classes ofvalue: return on investment, strategic match,

competitive advantage, management informationsupport, competitive response, and strategic ISarchitecture. Also, Keen’s (1991) book Shapingthe Future: Business Design Through Informa-tion Technology contains important material onmanaging the economics of information capital.

However, little empirical work has been done onthe financial and other criteria actually used inpractice in deciding on project selection andcapital investments in IST. Yet this informationwould seem to be important as a platform forseeking enhancements in the way organizationsdecide on their investments in informationsystems & technology.

The criteria used in making the decision on ISTinvestments have significance for a number ofreasons. First, the criteria used or not used, andthe way in which they are applied or not applied,significantly impact the effectiveness with whichIST investment decisions are made. They deter-mine whether the "right" projects are selected.

Second, the criteria are significant for theorganization’s finance and management account-ing function in terms of their role in maximizingreturn on investment and their involvement in thecost vs. benefit analysis that may precede an ISTcapital investment decision.

A final reason why the criteria used in IST in-vestments have significance concerns the right"balance" in the use of criteria. There are essen-tially two opposing views in considering cost vs.benefit analysis for the purpose of evaluating andselecting IST projects/investments. One view isthat cost vs. benefit analysis, beyond an intuitiveassessment, is neither feasible nor useful, espe-cially when the numbers seem to be stretchedto fit the need. This is reinforced by the belief that,even if the projected benefits are realized, it isdifficult to prove that they are attributable to theIST investment. Neither is it always easy to quan-tify the "soft" or indirect organizational costs in-volved, which may be greater than the hard/directcosts (Hochstrasser, 1990; Keen, 1991). It hasalso been suggested that ROI analysis is ap-plicable to transaction-oriented systems or tothose undertaken for strategic, market-orientedpurposes (Weill and Olson, 1989). All of this hassome truth, and the quantification implicit in costvs. benefit analysis may not always be feasible.In fact it may even turn into a "numbers game"that displaces real analysis. Nonetheless, quan-tification should always be attempted, and pro-

MIS Quarterly/September 1992 337

Justifying IT Investments

cedures should be put in place to ensureevaluation, screening, and benefit-tracking (In-ternational Federation of Accountants, 1989).Otherwise, there may be an absence of disci-plined analysis, no real basis of objectivemeasurement, and limited awareness of the truecosts and benefits of IST investments (Hoch-strasser, 1990; McKinnon and Kallman, 1987;Silk, 1990).

The other view imposes a universal requirementfor a clear, measurable, and reliable return oninvestment over two to three years or less. It isoriented to traditional, cost-saving, productivity-oriented projects, and it tends to screen out thoseproviding better customer service, improved deci-sion support, enhanced communication, and sim-ilar strategic payoffs. It denies the reality ofintangible benefits, ignores any beneficial "rip-ple" effects, and dismisses any associated cashinflows due to the difficulty of measuring such in-flows (Downing, 1989; Parker and Benson, 1988).The problem with this view is that the traditionalproject often fails to produce the expected costsavings and productivity improvements (Econo-mist, 1990; Strassman, 1985).

In summary, the criteria actually used tend to in-dicate whether there is an appropriate balancein utilizing both quantitative and qualitative formsof evaluation in selecting information systems &technology investments.

Methodology, Criteria,and Survey SampleIn an effort to gain some answers on the ISTcapital investment (project selection) decisioncriteria used in practice, a survey was undertakenin 1990 of 80 American, British, Australian, andNew Zealand companies. A one-page surveyform was developed with the aim of making it aseasy as possible to provide the data requested.The form provided 15 possible IST investmentcriteria, a means of indicating whether they areused or not, the percentage of projects to whicheach criterion is applied, and an overall rankingin terms of total project value for each criterion.The criteria are defined in Appendix A and listedin Table 1.

The criteria are categorized into financial,management, and development criteria. They

Table 1. Criteria Used in the Survey of ISTProject Selection (Investment) Decisions

Financial Criteria

Discounted Cash Flow (DCF)1. Net Present Value2. Internal Rate of Return3. Profitability Index Method

Other Financial4. Average/Accounting Rate of Return5. Payback Method6. Budgetary Constraint

Management Criteria7. Support Explicit Business Objectives8. Support Implicit Business Objectives9. Response to Competitve Systems10. Support Management Decision Making11. Probability of Achieving Benefits12. Legal/Government Requirements

Development Criteria13. Technical/System Requirements14. Introduce/Learn New Technology15. Probability of Project Completion

were developed, first, through interviews with 20chief information officers (CIOs) in Britain and theUnited States. These CIOs were questioned onwhat criteria their organizations use in selectingIST investment projects, with the aim of develop-ing a full list of the criteria used in practice.Second, the criteria and the form were tested andrefined in a pilot study with 12 companies. Thefinalized survey form is shown in Appendix B,which demonstrates how a typical form wouldhave been filled in.

The criteria used in the survey and listed in Table1 are primary.level criteria. That is, they areoriented to the basic IST project selection andinvestment decisionmthe basic reason for the in-vestment. This distinguishes them from second-ary-level criteria, such as functionality or viabilityof hardware or software, that might be used inselecting a particular IST vendor. For example,the criterion Technical/System Requirements isnot a secondary-level, vendor-oriented criterion.As indicated in Appendix A, it applies when hard-ware or software requirements are a major fac-tor or need behind the investment decision.

338 MIS Quarterly~September 1992

Justifying iT Investments

None of the criteria is dependent upon another,but some are related. For example, Response toCompetitive Systems (#9) might be associatedwith Support Explicit Business Objectives (#7).Also, Probability of Achieving Benefits (#11)might be associated with the Net Present Valuecriterion, by way of systematic risk assessment.Other criteria, such as Budgetary Constraint (#6),might apply across the board to most projects.However, interviews with the 20 CIOs concernedshowed that each criterion was of sufficient im-portance to be treated as a separate and distinctcriterion for the purpose of the survey.

An important finding in developing the criteriawas the need to distinguish between those ISTprojects undertaken in support of implicitbusiness objectives, as opposed to those in sup-port of explicit business objectives. In the pro-totype list of criteria, no distinction was made.However, it soon became evident that virtuallyall projects and investments in IST are, directlyor indirectly, undertaken in support of implicitbusiness objectives. For example, a significantmachine upgrade might be undertaken due tovolume constraints with existing hardware, andthere may or may not be specific objectives at-tached to the upgrade. Essentially, it is aresponse to a problem. Presumably however, theproject also provides support for basic businessobjectives (strictly speaking, aims or goals), suchas profitability, increase in sales, etc. On the otherhand, there may be investment in new or addi-tional hardware as part of a specific plan and ex-plicit business objectives. Thus, there is a basicdifference between those IST projects or invest-ments undertaken in support of implicit businessobjectives as opposed to those undertaken insupport of explicit business objectives.

Another important finding was the need toseparate into two parts the probability (and risk)of success (or non-success) relating to an ISTproject. Some organizations engaging in R&Drecognize technical success, i.e., meeting allspecifications and tests, as distinct frommarketing success, i.e., the finished product sell-ing well (Gaynor, 1990). In the field of informa-tion systems & technology, this is equivalent toProbability of Project Completion and Probabili-ty of Achieving Benefits. Probability of ProjectCompletion concerns the probability of the proj-ect being completed according to time, cost, andquality requirements. Probability of AchievingBenefits relates to the probability and risk

attached to the desired revenue flows andbusiness effects. Such risk may be included inadjusting expected cash flows for risk. However,a number of companies indicated this as a riskthat needs to be separately considered in today’sturbulent business environment.

Lastly, the competitive environment is having anincreasing impact on the selection of IST pro-jects/investments, such that Response to Com-petitive Systems has become a further importantcriterion. Thus, an IST project may be undertakento achieve a competitive advantage for theorganization, or it may be undertaken in responseto other organizations trying to do the same thing.

A letter inviting participation in the survey, withthe survey form enclosed, was sent to 72 public-ly listed companies in Britain, 67 in the UnitedStates, 24 in Australia, and 40 in New Zealandfor a total gross sample of 203 companies. Thenet total of usable replies (three were unusable)was 80, for a response rate (achieved after follow-up) of just under 40 percent. Of the 80 companiesproviding a usable reply, 25 were American, 23British, 11 Australian, and 21 were New Zealandcompanies. The reason for using these four coun-tries was to obtain a wide experience of practicewithin a relatively common business environment.

There were originally 250 companies randomlyselected from a library of around 2,500 currentannual reports. A number of these companieswere screened out because they were too smallor because they did not appear to have, by thenature of their business, a significant investmentin information systems & technology. Thisscreening process reduced the number of com-panies to 203, to which the letter was sent. Interms of size, the 80 sample companies that pro-vided a usable response to the survey are largeorganizations in which the IST investment deci-sion (project selection) process and the criteriaused are generally more structured than in smallorganizations (Doll and Torkzadeh, 1987). Thebreakdown of the sample by company size, interms of annual sales, is shown in Table 2.

The industries in the sample represented a broadmix of different types of businesses. These areshown in Table 3, which uses the Datamation in-dustry categories (Davis, 1989).

Each of the 203 annual reports was studied toobtain, where possible, the name of the mostpropriate senior management person able to pro-

MIS Quarterly/September 1992 339

Justifying IT Investments

Table 2. Number of Survey Responsesby Company Size (Annual Sales)

Annual Sales No. of(in millions of U.S. Dollars) Companies

0 - 99 11100 - 499 11500 - 2,499 172,500 - 9,999 3010,000 plus 11

Total 80

Table 3. Survey Responses by Industry

Industry or No. ofType of Company Companies

Food and Beverage 11Industrial and Automotive 10Banking and Finance 8Electronics 6Insurance 5Retail 5Petroleum 4Metal and Metal Products 3Transportation 2Telecommunications 2Process Industries 24

Total 80

vide or arrange the provision of the informationrequested on the survey form. In some cases thiswas the chief information officer, in others it wasthe chief financial officer. Where them was uncer-tainty, the letter and attached survey form wassent to the chief executive officer (CEO). The ac-tual respondents by job title am shown in Table 4.

Completion of column 2 on the survey sheetanswered the second question in. the survey,which was:

What is your estimate of the number ofprojects to which a given criterion appliesas a pementage of the total number ofprojects?

The survey results in answer to these two ques-tions provided: (1) the percent of companies thatuse a given IST project selection (investment)criterion, and (2) the average percent of projectsto which a given criterion is applied for thosecompanies using the criterion. This is shown inTable 5.

For example, 68 pement of the companies in-dicated that they use budgetary constraint (on atleast some of their projects) as one of their criteriain deciding on IST projects/invastments. As a fur-ther example, 16 percent of the companies saidthat they use Average/Accounting Rate of Returnas a criterion in selecting (at least some of) theirIST projects. :

In response to the second question the resultsindicate, for example, that those companies us-ing Net Present Value as a decision criterion ap-ply it, on average, to 58 percent of their projects.

The percent application of a given criterion foraft projects in aft companies in the sample, in-cluding those companies not using the criterion,can be determined by multiplying the criterionusage percent in Table 5 by the application per-cent. For example, the Net Present Value methodis applied to only 28 percent (0.49 x 0.58), of allprojects across all companies in the sample. Sup-port of Explicit Business Objectives is applied to50 percent (0.88 x 0.57) of all projects. Also, the

Table 4. Survey Responses by Job Title

No. ofJob Title Responses

Chief Information Officer 29Information Systems (IS)

Manager 20IS Planning Manager 12Chief Financial Officer 10IS Controller 7Chief Executive Officer 2

Total 80

Survey ResultsCompletion of column 1 on the survey sheetanswered the first question in the survey, whichwas:

Excluding routine maintenance work,which of the following criteria do you usein making the basic go-ahead decision onsystems development projects and com-puter hardware or software facilities?

340 MIS Quarterly~September 1992

Justifying IT Investments

Table 5. Usage and Application of a Given IST Investment (Project Selection) Criterion

% of CompaniesCriteria Using the Criterion

% of Projectsto Which Applied

by Companies Using

Financial CriteriaDiscounted Cash Flow (DCF)

1. Net Present Value 49 582. Internal Rate of Return 54 543. Profitability Index Method 8 47

Other Financial4. Average/Accounting Rate of Return5. PaybackMethod6. Budgetary Constraint

Management Criteria7. Support Explicit Business Objectives8. Support Implicit Business Objectives9. Response to Competitive Systems

10. Support Management Decision Making11. Probability of Achieving Benefits12. Legal/Government Requirements

Development Criteria13. Technical/System Requirements14. Introduce/Learn New Technology15. Probability of Project Completion

16 4761 5168 64

88 5769 4461 2888 2946 6371 13

79 2560 1331 62

data show that only 40 percent of all projects inall the companies are subjected to some type ofDCF method.

Completion of column 3 on the survey sheetanswered the third question in the survey, whichwas:

What ranking would you give to eachcriterion in terms of the overall value ofprojects to which it applies?

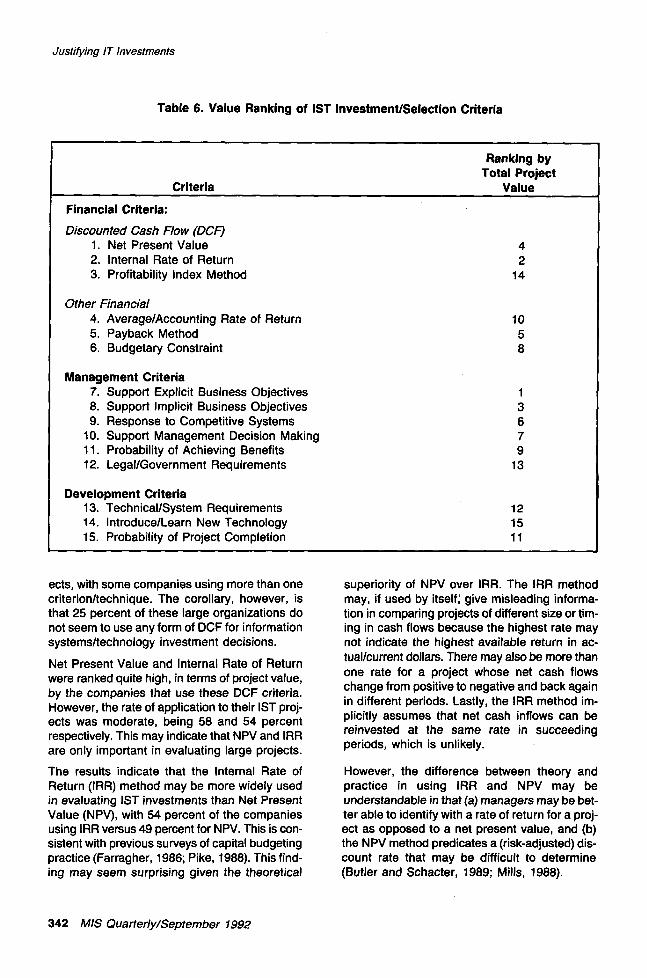

The survey results in answer to the third ques-tion enabled a determination of the average rank-ing of each criterion based on the total value ofprojects to which the criterion is applied (for thosecompanies using the criterion). This ranking isshown in Table 6.

For example, the resuits indicate that those com-panies using Net Present Value as a decisio~criterion ranked it fourth in importance (onaverage) in terms of the total value of projects

to which it is applied. Support of Explicit BusinessObjectives was ranked #1.

Thus, the survey results show the percent of com-panies using a given criterion, the percentage ofprojects to which it is actually applied by thosecompanies using it, and the ranking of eachcriterion in terms of total project value to whichit is applied.

Financial criteriaPrevious surveys on capital budgeting havefound that discounted cash flow (DCF) tech-niques appear to improve the quality of capitalbudgeting decisions (Pike, 1988). An initial ques-tion in scrutinizing the survey results was,therefore, how many organizations use someform of DCF? The data showed that 75 percentuse some form of DCF in selecting their IST proj-

MIS Quarterly~September 1992 341

Justifying IT Investments

Table 6. Value Ranking of IST Investment/Selection Criteria

Criteria

Ranking byTotal Project

Value

Financial Criteria:

Discounted Cash Flow (OCF)1. Net Present Value2. Internal Rate of Return3. Profitability Index Method

Other Financial4. AveragelAccounting Rate of Return5. Payback Method6. Budgetary Constraint

Management Criteria7. Support Explicit Business Objectives8. Support Implicit Business Objectives9. Response to Competitive Systems

10. Support Management Decision Making11. Probability of Achieving Benefits12. Legal/Government Requirements

Development Criteria13. Technical/System Requirements14. Introduce/Learn New Technology15. Probability of Project Completion

42

14

1058

13679

13

121511

ects, with some companies using more than onecriterion/technique. The corollary, however, isthat 25 percent of these large organizations donot seem to use any form of DCF for informationsystems/technology investment decisions.

Net Present Value and Internal Rate of Returnwere ranked quite high, in terms of project value,by the companies that use these DCF criteria.However, the rate of application to their IST proj-ects was moderate, being 58 and 54 percentrespectively. This may indicate that NPV and IFIRare only important in evaluating large projects.

The results indicate that the Internal Rate ofReturn (IRR) method may be more widely usedin evaluating IST investments than Net PresentValue (NPV), with 54 percent of the companiesusing IRR versus 49 percent for NPV. This is con-sistent with previous surveys of capital budgetingpractice (Farragher, 1986; Pike, 1988). This find-ing may seem surprising given the theoretical

superiority of NPV over IRR. The IRR methodmay, if used by itself; give misleading informa-tion in comparing projects of different size or tim-ing in cash flows because the highest rate maynot indicate the highest available return in ac-tual/current dollars. There may also be more thanone rate for a project whose net cash flowschange from positive to negative and back againin different periods. Lastly, the IRR method im-plicitly assumes that net cash inflows can bereinvested at the same rate in succeedingperiods, which is unlikely.

However, the difference between theory andpractice in using IRR and NPV may beunderstandable in that (a) managers may be bet-ter able to identify with a rate of return for a proj-ect as opposed to a net present value, and (b)the NPV method predicates a (risk-adjusted) dis-count rate that may be difficult to determine(Butler and Schacter, 1989; Mills, 1988).

342 MIS Quarter/y/September 1992

Justifying IT Investments

The Profitability Index Method (PIM), sometimesknown as the Project Selection Index, is the leastused of all criteria, being used by only 8 percent(i.e., six out of 80), of the companies surveyed.These few companies apply the criterion as asupplementary benchmark to NPV.

Overall, the moderate use of DCF techniquesraises questions as to the extent of quantifica-tion in support of selection decisions on IST proj-ects (even though quantification need not alwaysbe in financial terms). Quantification of estimatedrevenue flows or cash savings will not always befeasible. For example, it may be difficult to givereliable estimates of the added revenue thatwould accrue from improved customer servicethrough a new online system. And quantified DCFbenefits may be transcended by other criteria,such as the need to make quicker decisions ormeet the level of service provided by competitors.However, the moderate use of DCF methods sug-gests that there may be some question as towhether quantification of cost vs. benefit, whichis a basic aim of DCF, is being effectively attainedin IST investment decisions.

Such techniques as Expected Value Analysis,Excess Tangible Cost, and Backfitting may be ofsome value in providing the numbers for quan-tification of cost vs. benefits (Rivard and Kaiser,1989). Also, quantification becomes more feasi-ble when there is an effective chargebeck systemin operation for the use of IST resources (Henry,1990; McKinnon and Kallman, 1987). It becomes

even more feasible when there is a benefit-tracking program in operation for IST projects,because there can then be feedback of cost andbenefit information from prior to prospectivesystems investments. This process is shown inFigure 1.

For example, if a new system or technology im-provement were thought to have a positive effectupon such an intangible as employee morale, thisbenefit might be broken down into quantifiedestimates of lower employee turnover, reducedabsenteeism, reduced accidents, reducedwastage, higher quality, and repeat sales throughimproved customer service. In the case of im-proved customer service, variables such aswaiting time, in-stock response, and frequencyof sales~service calls might be quantified. In ad-dition, the extent to which a new system/technology supports specific customer objectivesand/or resource life cycle needs might be iden-tified (Ives and Learmonth, 1984). The revenueestimates and associated costs might then bemonitored, and future estimates could benefitthrough the data captured and learning gainedfrom such prior projects. However, as illustratedin Figure 1, the process begins with specificationof business objectives and concomitant quan-tification so there is something against which totrack benefits and costs.

But even if quantification is considered feasible,management might not consider the effort worththe time and cost involved. This could be the case

specification I

of BusinessObjectives

%~1 I n fS°;s~:tmis° n .

I

l Specification!

Quantificationof Benefits

CostInformation

,l

ChargebackSystem

ImplementedSystem

Tracking ofBenefits

and Costs

Figure 1. Feedback of Quantified Cost and Benefit InformationFrom Prior to Prospective IST Projects/Investments

MIS Quarterly~September 1992 343

Justifying IT Investments

when a systems project is mandated due totechnical, legal, or competitive requirements. Orthe project may not be considered large enough.Even in these cases, however, it would seem thata ctear evaluation and tracking of cost vs. benefitwould assist the formulation of current and futureIST investment (project selection) policy througha better understanding and identification of IST-related benefits and costs.

However, if cost vs. benefit and DCF evaluationare to become easier and more generally usedin the selection of IST investments, it will takemore than DCF software to do it. There is, itwould seem, a need to develop:

1. Discovery and quantification techniques thatenable improved identification and assess-ment of strategic revenue benefits and costsavings in prospective IST capital projects/investments.

2. A methodology for identifying and quantifyingthe soft/indirect organizational costs.

3. Satisfactory financial evaluation techniques thataddress the rapid change and short-term needsof today’s business and IST environment.

All of this leads to the conclusion, based on theresults of the survey, that there is a need for wideruse of DCF criteria, and greater quantification,in IST investment decisions.

The Payback Method (PBK), a non-DCF method,is used by 61 percent of the companies in thesample (which is more than NPV or IRR). PBKignores the time value of money, as well as anycash flow following the payback period. Also,there is no minimum rate nor any factoring forrisk. However, two companies participating in thesurvey indicated that they use the DiscountedPayback Method, which at least factors in a timevalue for money.

The continued use of the Payback Method andits implicit short-term orientation, notwithstandingits theoretical shortcomings, may have somejustification. To begin with, it is easy to under-stand and use. Second, the complexity and dif-ficulty in making predictions within today’seconomic, political, and technological environ-ments may lead some managers not to trust inlong-term DCF projections; change in any one ofthese three areas could have a material effect onestimated cash flows. Third, in today’s businessenvironment, change occurs so rapidly that time

is compressed. Whereas 10 years was a longtime "yesterday," five years is a long time today.Fourth, in an environment of international cor-porate raiding and unfriendly takeovers, manage-ment may believe that the company’s stockmarket value needs to be kept high through aquick and reliable return on investment, the ob-jective being to keep raiders and takeover mer-chants at bay.

Thus, the short term may well loom larger in theminds of managers than the long term, and thephenomena described may lead to a rapid-returnfocus. Therefore, a management orientation oftwo or three years becomes understandable, andso does the use of Payback as an IST investmentcriterion.

With respect to IST investments in particular, to-day’s technology may be obsolete in two or threeyear’s time. In addition, the general cost of com-puting power continues to decline significantlyyear by year (Horvath and Canham, 1988). Con-sequently, tomorrow’s technology may becheaper than today’s. In such an environment,the use of the Payback Method, oriented to theshort term as it is, may reflect nothing less thanthe "real world."

Lastly, judging by the greater importanceattached to NPV and IRR by those companiesthat use these criteria, it appears that PBK is usedmore as a "yardstick" in complementing NPVand IRR than as a primary measure, particularlyin larger companies.

The Accounting Rate of Return method (ARR),like Payback, does not take into account the timevalue of money. However, it is evidently not usedas widely as Payback (only 16 percent of the com-panies in the sample use it) and, even then, itis used largely as a yardstick measure in conjunc-tion with DCF. Apart from being simple to use andunderstand, it has been said that one of thereasons for its continued use is that managerialbonuses are based on accounting rates of return(Weaver, et al., 1989).

The problem is that when the simple PaybackMethod or Accounting Rate of Return is used asthe only financial criterion apart from BudgetaryConstraint, rather than as a complementary yard-stick to more rigorous DCF criteria, there may begrounds for concern as to whether there is suffi-cient justification and targeting of capital pro-

344 MIS Quarterly/September 1992

Justifying IT Investments

jects/investments in IST (Willcocks and Lester,1991).The financial criterion that figures mostly in ISTproject selection is that of Budgetary Constraint(i.e., "Did we budget for it?"). Of the companiessurveyed, 68 percent use Budgetary Constraintas a project/investment approval criterion. It isapplied by those companies that use it as acriterion to 64 percent of their projects. This isthe highest application of any criteria. Thus, it isnot applied to all projects, and this representsnothing less than the "real world," where it is notalways possible to plan and budget for every ISTcapital expenditure. But such a high rate of ap-plication does seem to argue for the use ofBudgetary Constraint, and the implicit IST capitalbudget, as a norm.

Since budgeting is complementary to the plan-ning and control process, the moderate use ofBudgetary Constraint as a criterion in IST invest-ment projects (with 32 percent of the samplecompanies not using it), may indicate a need forimproved planning and control in the use of ISTresources in some companies. This inference isbased on the observation that a capital expen-diture budget is usually just "part of the picture"in overall (IST) planning (Weaver, et al., 1989).If there is no IST capital budget, there is littlelikelihood of a formalized plan.

On the other hand, Budgetary Constraint isranked eighth in importance/value, out of 15critera, by those companies using the criterion.This may support a general principle of capitalbudgeting theory that all projects contributing toprofitability should be accepted, whether bud-geted or not, unless there is some strategicreason ruling out (current) acceptance. Thus,where a capital budget has been established forIST projects, that budget may be waived if a proj-ect offers a positive and reliable net presentvalue, or if it supports some strategic corporateobjective, or if it is a mandated "must-do" project.

Management and developmentcriteriaOverall, Support of Explicit Business Objectivesis the most important criterion used by companiesin selecting IST investments/projects. Thiscriterion refers to a given IST.project or invest-

ment that supports business objectives specifical-ly indicated in some sort of plan. In comparison,Support Implicit Business Objectives is a deci-sion criterion justifying a project in accordancewith business objectives/aims that are "under-stood," though not necessarily formalized, in anyplan.

Most IST projects implicitly support basicbusiness objectives (or goals). There is thereforea need to distinguish between those projects thatsupport implicit (and generally basic) businessobjectives and those that have been specificallyplanned, or initiated, in response to a plan.

Support of Explicit Business Objectives is usedas an IST investment criterion by 88 percent ofthose companies that participated in the survey.These companies apply it, on average, to 58 per-cent of their projects. It is also the top-rankingcriterion, in terms of project value, in deciding onIST projects. Thus, Support of Explicit BusinessObjectives is clearly considered very importantby those companies in the sample that have theexperience of using it as an IST investmentcriterion.

In a business environment characterized bychange and uncertainty it may not be possibleto anticipate and plan every IST project. It maynot be possible for every one to be initiated infulfillment of one or more explicitly statedbusiness objectives. There will always be a pro-portion of unplanned projects that are virtuallymandated at short notice. However, in an increas-ingly competitive environment, is it necessary toknit together the objectives of the IST functionwith corporate and business-unit strategy in orderto effectively utilize IST resources in sustainingcompetitive goals. As one survey respondent CIOcommented, "If the IS department is in tune withthe business objectives of the organization, thejustification of a system is incorporated into theplanning process, which includes justification ofthe total project expenditure at the macro level."

While it may not always be feasible to quantifythe benefits of a prospective IST investment,such benefits can usually be represented in ex-plicit corporate goals and objectives. If an IST in-vestment is then directed toward the fulfillmentof such goals and objectives, the raison d’etreof the IST function has been satisfied, and quan-tified cost vs. benefit justification no longerdominates. As another survey respondent CIO

MIS Quarterly~September 1992 345

Justifying IT Investments

said, "DCF is dominant, but any project has tovisibly support business strategies and objec-tives. However, where rigorous DCF denies anobvious long-term benefit, then the DCF ap-proach is set aside."

Some projects may neither be supported by aquantified cost vs. benefit analysis nor under-taken in pursuit of explicit (i.e., .planned) cor-porate strategy or objectives. This is almostinevitable in a dynamic, complex business en-vironmnent. However, it would seem that the aimshould be for most projects to satisfy at least oneof these basic criteria.

Response to Competitive Systems is used as acriterion by 61 percent of companies and is con-sidered their sixth most important criterion. Thisis a criterion that may not have been relevant inpast years. The fact that it is now indicates thesignificance of IST in today’s competitivebusiness environment. Another CIO commentedthat it is not so much a question of responding,i.e. reacting, as proacting: "We would expressthis criterion as systems to give competitive ad-vantage, i.e., it is more important to keep aheadof the competition than to catch up with it!"

In some cases, Response to CompetitiveSystems may be the underlying criterion wherean organization concludes that "we cannot af-ford not to invest" (as commented by anotherCIO). Without new information technologies theremay be a serious loss in effectiveness and com-petitive standing compared to competitors thatdo invest in them (Johnston and Vitale, 1988).It is not surprising that Support of ManagementDecision Making is used as a criterion by 88 per-cent of the companies that participated in thesurvey. This reflects the importance of systemsin supporting management with requisite infor-mation. What may be surprising is that thesecompanies apply the criterion to only 29 percentof their projects. In terms of project value, it isranked only seventh in importance out of 15criteria. Such ranking may be due to this "almost-traditional" criterion being transcended by othercriteria as organizations mature to other em-phases (such as competitive response) in the useof IST.

The criterion Probability of Achieving Benefits isa risk/probability criterion that is used by less thanhalf (46 percent) of the companies who par-ticipated in the survey. However, it is possible that

it has wider use than this in that it may have im-plicit inclusion in other financial or managementcriteria. Nonetheless, those companies that in-dicated use of the criterion apply it to an average63 percent of their projects, which makes Prob-ability of Achieving Benefits the highest propor-tion of any management criteria, second only toBudgetary Constraint in its percentage applica-tion to IST projects/investments.

Although Probability of Achieving Benefits mightbe implicitly included with other criteria, it maybe a criterion that is best applied separately anddistinctly because: (1) it represents a fundamentalrisk that is inherent in most projects in today’sturbulent business environment, (2) it could pro-vide for a more conscious management focus onand analysis of such risk, and (3) it would facilitatethe learning process relative to this probability/risk.

Technical/System Requirements is a primary-level criterion, not a secondary-level, vendor-oriented criterion. The results show that it is usedas an IST investment or project selection criterionby 79 percent of the companies that participatedin the survey. This in itself is not surprising; suchrequirements are a necessity in most IST proj-ects. For example, an organization may investin an upgraded computer or network because ithas outgrown the present configuration. Or a ma-jor re-write of a system may be required becauseit is no longer maintainable in its present form.

The issue with the Technical/System Re-quirements criterion is the degree to which it isused. In the survey and sample it is shown to ap-ply, on average, to 25 percent of an organizaotion’s IST projects/investments. Where theproportion is significantly more than this average,it may indicate that the IST function and theorganization itself is being driven by techni-cal/system requirements rather than strategic ob-jectives. That is, "the tail is wagging the dog."This may be the case where IST investments areeffectively decided by "technology managers"and not "business managers" (Parker and Ben-son, 1988).

The criterion Introduce or Learn New Technologyis one that, like the criterion Response to Com-petitive Systems, may not have been as relevantin past years. However, it is becoming more ofa justification as information technology con-tinues to grow in its impact upon business organ-

346 MIS Quarterly~September 1992

Justifying IT Investments

izations. Most organizations in the survey (60percent) use it as a criterion, even though it ap-plies to only a small proportion of their projects(13 percent).

Probability of Project Completion is a risk/prob-ability assessment criterion that is used as an in-vestment criterion by just under one-third (31percent), of the organizations that participated inthe survey. This might be considered a low pro-portion of companies given the high rate of fail-ure of IST projects (McComb and Smith, 1991).

Those companies in the sample that do use Prob-ability of Project Completion as a criterion applyit to 63 percent of their projects, which is the third-highest application of any criterion to IST proj-ects. Thus, Probability of Project Completion isconsidered quite important by those companiesthat have the experience of using it in IST invest-ment decisions. This supports research indicatingthat it is a risk/probability factor that needs to bepart of any project evaluation (Spadaro, 1985;Willburn, 1989).

Summary and ConclusionsBusiness competition is global, intense, anddynamic. Information systems & technology (IST)is a key resource in responding to and proactingwith this environment. Consequently, capital in-vestment decisions in selecting systems projectsand hardware/software acquisitions are of acritical nature within the organization’s overallstrategy. The basic question is, therefore, howdo organizations make these investment deci-sions, and how should they?. In responding to thatquestion, this study concentrates on the decisioncriteria, as opposed to the decision process.

Fifteen criteria were used--six financial, sixmanagement, and three development--in asurvey undertaken in 1990 of 80 major com-panies in four countries: the United States, Bri-tain, Australia, and New Zealand. The companieswere asked to indicate which criteria they use,the percentage of projects to which each criterionis applied, and the overall ranking in terms of totalproject value for each criterion.

The results show that discounted cash flow (inthe form of Net Present Value, Internal Rate ofReturn, and/or Profitability Index Method) is used

as an investment criterion for IST projects byabout 75 percent of the Fortune 500-type of com-panies that participated in the survey. Overall,DCF techniques are applied to only 40 percentof all projects in the sample, although it is evi-dent that DCF is important in the evaluation oflarge projects.

Except for Budgetary Constraint, the PaybackMethod is the most widely used financial criterion.Budgetary Constraint itself is used by about two-thirds of the companies in the sample.

The highest-ranked criterion is Support of ExplicitBusiness Objectives, and it is used as an IST in-vestment criterion by nine out of 10 companies.It refers to projects that specifically support andtie in with business objectives articulated in com-pany plans.

Response to Competitive Systems is used as aninvestment criterion by 61 percent of the com-panies in the sample, by whom it is ranked sixthout of 15 in importance. This reflects the increas-ing significance of information systems &technology in today’s competitive businessenvironment.

Somewhat surprisingly, and although it is usedas an investment criterion by nearly all com-panies in the sample, Support of ManagementDecision Making is only applied to about one-quarter of all projects and ranked seventh in im-portance by those companies that use it. Thisrelatively low application and ranking may be dueto Support of Management Decision Making be-ing transcended by other criteria as organizationsmature to other emphases in the use of IST.

There were two probability/risk assessmentcriteria included in the survey, namely Probabilityof Project Completion and Probability of Achiev-ing Benefits. The completion criterion is used byone-third of the companies. The benefits criterionis used by about half of the companies.

The development criterion Technical/System Re-quirements is used by most companies in thesample. The remaining development criterion, In-troduce/Learn New Technology, is used by themajority of companies, though it is only appliedto about 10 percent of their projects.

Some of the general conclusions developed inthe analysis and discussion of the survey resultsare prescriptive in nature. That is, based on thepractice and experience of the 80 major com-

MIS Quarterly~September 1992 347

Justifying IT Investments

panies that participated in the survey, there ap-pear to be a number of proposals that might beconsidered by organizations in making decisionson their IST projects and investments. These areas follows:

1. More accurate quantification of cost vs.benefit and more informed IST investmentdecisions are facilitated where there is effec-tive benefit-tracking and chargeback in place.

2. The ideal is for an IST project or investmentto be undertaken in pursuit of both: (a) quan-tifiable net benefits and (b) explicitly plannedbusiness objectives. Apart from mandatory(must-do) projects, the aim should be for least one of these basic criteria to be involvedin an IST investment decision.

3. The high application rate of Probability ofAchieving Benefits, as an IST investmentcriterion by some companies, indicates thatit may be sufficiently important to be formallyconsidered as a distinct criterion in evaluatingand deciding upon prospective IST capitalinvestments.

4. If an organization wishes to gain access to thepertinent learning curve of new informationtechnology likely to be of benefit, it may benecessary to regularly undertake some R&Dfunding by way of "seed money" for suchprojects and investments.

5. Probability of project completion is a risk/prob-ability criterion that is appropriate to consideras a decision criterion in evaluating anddeciding upon IST projects/investments andis, in any case, an element present in mostof them.

The underlying thrust of the study was and istoward application. The goal is to bridge the gapbetween practice and academia. However, theseresults, together with the analysis and proposalsaccompanying them, are only a beginning, orperhaps just a step along the way, in this key areaof IST management decision making.

AcknowledgementsThe author would like to thank and acknowledgethe anonymous reviewers and the editors of MISQuarterly for their most helpful input in produc-ing this article.

ReferencesBadiru, A.B. "A Management Guide to Automa-

tion Cost Justification," Industrial Engineer,February 1990, pp. 27-30.

Boyd, D.F. and Krasnow, H.J. "EconomicEvaluation of Management InformationSystems,"lBM Systems Journal (2), 1963, pp.2-23.

Brealey, R.A. and Myers, E. Principles of Cor-porate Finance, 3rd edition, McGraw Hill BookCo., New York, NY, 1988.

Brigham, E.F. and Gapenski, L.C. FinancialManagement: Theory and Practice, 6th edi-tion, The Dryden Press, New York, NY, 1991.

Butler, J.S. and Schacter, B. "The InvestmentDecision: Estimation Risk and Risk AdjustedDiscount Rates," Financial Management(18:4), Winter 1989, pp. 13-19.

Davenport, T.H. "The Case of the Soft SoftwareProposal," Harvard Business Review (89:3),May-June 1989, pp. 12-24.

Davis, D. "U.S. Giants Run a $50 Billion IS Tab,"Datamation, November 15, 1989, pp. 42-44.

Doll, W.J. and Torkzadeh, G. "The Relationshipof MIS Steering Committees to Size of Firmand Formalization of MIS Planning," Com-munications of the ACM (30:11), November1987, pp. 972-978.

Downing, T. "Eight New Ways to EvaluateAutomation," Mechanical Engineering(111:7), July 1989, pp. 82-86.

Due, T. "Determining Economic Feasibility: FourCostlBenefit Analysis Methods," Journal of In-formation Systems Management (6), Fall1989, pp. 14-19.

Economist. "A Lot to Learn," March 3, 1990, pp.70-71.

Farragher, E.J. "Capital Budgeting Practices ofNon-Industrial Firms," The EngineeringEconomist (31:4), Summer 1986, pp. 293-302.

Gaynor, G.H. "Selecting Projects," Research &Technology Management (33:4), July/August1990, pp. 43-45.

Hall, D.L. and Nauda, A. "An Interactive Ap-proach for Selecting R&D Projects," IEEETransactions on Engineering Management(37:2), May 1990, pp. 126-133.

Hellings, J. "Capital Budgeting in the RealWorld," Management Accounting (63), April1985, pp. 38-41.

Henry, B. "Measuring IS for Business Value,"Datamation, April 1, 1990, pp. 89-91.

348 MIS Quarterly~September 1992

Justifying IT Investments

Hochstrasser, B. "Evaluation of IT Investments--Matching Techniques to Projects," Journal ofInformation Technology (5:4), December1990, pp. 215-221.

Horvath, J.L. and Canham, P.J. "Bits and Bytesand Bucks," CA Magazine, August 1988, pp.65-68.

International Federation of Accountants. TheCapita/Expenditure Decision: Statement onInternational Management Accounting Prac-tice 2, Financial and Management AccountingCommittee, 540 Madison Avenue, New York,NY 10022, September/October 1989.

Ives, B. and Learmonth, G. "The InformationSystem as a Competitive Weapon," Com-munications of the ACM (27:12), December1984, pp. 1193-1201.

Johnston, R.H. and Vitale, M.R. "Creating Com-petitve Advantage with InterorganizationalSystems," MIS Quarterly (12:2), June 1988,pp. 153-165.

Keen, P.G.W. Shaping the Future: BusinessDesign Through Information Technology, Har-vard Business School Press, Boston, MA,1991.

Kennedy, J.A. "Ritual and Reality in CapitalBudgeting," Management Accounting (64),February 1986, pp. 34-37.

Kim, S.H. and Kang, K. "R&D Project Selectionin Hong Kong, Korea and Japan," Interna-tional Journal of Technology Management(4:6), 1989, pp. 673-679.

Loveman, G. "Cash Drain, No Gain," Computer-world, November 25, 1991, pp. 69-72.

Maglitta, J. and Sullivan-Trainor, M. "Do theRight Things," Computerworld: The Premier100 (supplement), September 30, 1991, pp.6-13.

McComb,D. and Smith, J.Y. "System ProjectFailure:The Heuristics of Risk," Journal of In-formation Systems Management (8), Winter1991, pp. 25-34.

McKeen, D.J. and Guimaraes, T. "Selecting MISProjects by Steering Committee," Com-munications of the ACM (28:12), December1985, pp. 1344-1352.

McKinnon, W.P. and Kallman, E.A. "MappingChargeback Systems to Organizational En-vironments," MIS Quarterly (11:1), March

1987, pp. 5-20.Mills, R.W. "Capital Budgeting Techniques Used

in the UK and the USA," Management Ac-counting (66), January 1988, pp. 26-27.

Parker, M.M. and Benson, R.J. InformationEconomics, Prentice Hall, Englewood Cliffs,NJ, i988.

Pike, R.H. "An Empirical Study of the Adoptionof Sophisticated Capital Budgeting Practicesand Decision-Making Effectiveness,"Accounting and Business Research (18),Autumn 1988, pp. 341-351.

Pike, R.H. "Do Sophisticated Capital BudgetingApproaches Improve Investment Decision-Making Effectiveness?" The EngineeringEconomist (34:2), Winter 1989, pp. 149-161.

Pohlman, R.A., Santiago, E., and Markel, L.F."Cash Flow Estimation Practices of LargeFirms," Financial Management, Summer1988, pp. 71-79.

Rivard, E. and Kaiser, K. "The Benefit of Quali-ty IS," Datamation, January 15, 1989, pp.53-58.

Silk, D.J. "Managing IS Benefits for the 1990s,"Journal of Information Technology (5:4),December 1990, pp. 185-193.

Spadaro, D. "Project Evaluation Made Simple,"Datamation, November 1, 1985, pp. 121-124.

Strassman, P.A. Information Payoff: TheTransformation of Work in the Electronic Age,Free Press, New York, NY, 1985.

Thompson, R.A. and Thuesen, G.J. "Applica-tions of Dynamic Investment Criteria forCapital Budgeting Decisions," The Engineer-ing Economist (33:1), Fall 1987, pp. 59-86.

Van Horne, J. Financial Management and Policy,7th edition, Prentice Hall, Englewood Cliffs,N J, 1986.

Weaver, S.C., Peters, D., Cason, R., andDaleiden, J. "Panel Discussions on CorporateInvestment: Capital Budgeting," FinancialManagement (18:1), Spring 1989, pp. 10-17.

Weill, P. and Olson, M.H. "Managing Investmentin Information Technology: Mini Case Ex-amples and Implications," MIS Quarterly(13:1), March 1989, pp. 2-16.

Weston, J.F. and Brigham, E.F. Essentials ofManagerial Finance, 8th edition, The DrydenPress, New York, NY, 1987.

MIS Quarterly/September 1992 349

Justifying IT Investments

Wilder, C. and Hildebrand, C. "Faster! Better!Cheaper! Now!" Computerworld, January 2,1992, pp. 2-6.

Willburn, J.A. "Catching Runaway ComputerSystems Before They Bolt," Chief InformationOfficer Journal (2), Fall 1989, pp. 18-22.

Willcocks, L. and Lester, S. "InformationSystems Investments: Evaluation at theFeasibility Stage of Projects," Technovation(11:5), July 1991, pp. 283-302.

About the AuthorC. James Bacon is senior lecturer in informationsystems at the University of Canterbury,Christchurch, New Zealand. He previouslyworked as a systems consultant in London andNew York. His research is in the managementof information systems, with an emphasis on"bridging the gap" between practice andacademia.

350 MIS Quarterly~September 1992

Justifying IT Investments

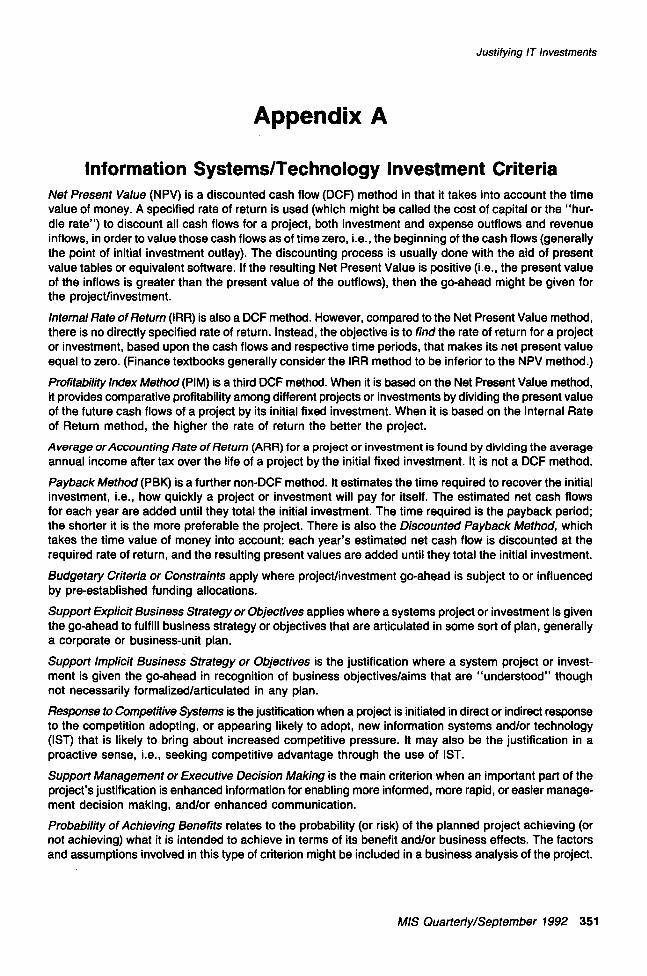

Appendix A

Information Systems/Technology Investment CriteriaNet Present Value (NPV) is a discounted cash flow (DCF) method in that it takes into account the value of money. A specified rate of return is used (which might be called the cost of capital or the "hur-dle rate") to discount all cash flows for a project, both investment and expense outflows and revenueinflows, in order to value those cash flows as of time zero, i.e., the beginning of the cash flows (generallythe point of initial investment outlay). The discounting process is usually done with the aid of presentvalue tables or equivalent software. If the resulting Net Present Value is positive (i.e., the present valueof the inflows is greater than the present value of the outflows), then the go-ahead might be given forthe project/investment.

Internal Rate of Return (IRR) is also a DCF method. However, compared to the Net Present Value method,there is no directly specified rate of return. Instead, the objective is to find the rate of return for a projector investment, based upon the cash flows and respective time periods, that makes its net present valueequal to zero. (Finance textbooks generally consider the IRR method to be inferior to the NPV method.)

Profitability Index Method (PIM) is a third DCF method. When it is based on the Net Present Value method,it provides comparative profitability among different projects or investments by dividing the present valueof the future cash flows of a project by its initial fixed investment. When it is based on the Internal Rateof Return method, the higher the rate of return the better the project.

Average or Accounting Rate of Return (ARR) for a project or investment is found by dividing the averageannual income after tax over the life of a project by the initial fixed investment. It is not a DCF method.

Payback Method (PBK) is a further non-DCF method. It estimates the time required to recover the initialinvestment, i.e., how quickly a project or investment will pay for itself. The estimated net cash flowsfor each year are added until they total the initial investment. The time required is the payback period;the shorter it is the more preferable the project. There is also the Discounted Payback Method, whichtakes the time value of money into account: each year’s estimated net cash flow is discounted at therequired rate of return, and the resulting present values are added until they total the initial investment.

Budgetary Criteria or Constraints apply where project/investment go-ahead is subject to or influencedby pre-established funding allocations.

Support Explicit Business Strategy or Objectives applies where a systems project or investment is giventhe go-ahead to fulfill business strategy or objectives that are articulated in some sort of plan, generallya corporate or business-unit plan.

Support Implicit Business Strategy or Objectives is the justification where a system project or invest-ment is given the go-ahead in recognition of business objectives/aims that are "understood" thoughnot necessarily formalized/articulated in any plan.

Response to Competitive Systems is the justification when a project is initiated in direct or indirect responseto the competition adopting, or appearing likely to adopt, new information systems and/or technology(IST) that is likely to bring about increased competitive pressure. It may also be the justification in proactive sense, i.e., seeking competitive advantage through the use of ISTo

Support Management or Executive Decision Making is the main criterion when an important part of theproject’s justification is enhanced information for enabling more informed, more rapid, or easier manage-ment decision making, and/or enhanced communication.

Probability of Achieving Benefits relates to the probability (or risk) of the planned project achieving (ornot achieving) what it is intended to achieve in terms of its benefit and/or business effects. The factorsand assumptions involved in this type of criterion might be included in a business analysis of the project.

MIS Quarterly/September 1992 351

Justifying IT Investments

Legal or Government Requirements is the justification when a project or hardware/software investmentis undertaken primarily to meet government regulations or legislation, as for example with taxation orreporting requirements.

Technical/System Requirements applies when hardware or software requirements are a major factoror need in going ahead with the project as, for example, with system re-writes or machine conver-sions/upgrades.

Introduce or Learn New Technology applies when an organization introduces some new form of infor-mation technology, or a new concept in systems, for the purpose of gaining experience or expertisein that technology or concept, with a view to its probable use within/by the organization.

Probability of Project Completion is a criterion employed in assessing the probability (or risk) of the proj-ect being completed (or not being completed), according to time, cost, and quality requirements. Thiswould include the following type of factors:

¯ Project size

¯ Technical innovation

¯ Definitional uncertainty

¯ Complex organizational integration requirements

¯ Life-or-death deadline

¯ Experience and ability of personnel

¯ Availability and dependence upon personnel

¯ Senior management support

¯ User participation

The last two factors, namely senior management support and user participation, may not be fully knownin advance, that is, at the point when criteria are being evaluated and exercised.

Appendix BSurvey of Project Decision Methods

Excluding routine maintenance work, which of the following methods, criteria, or justification does yourorganization use in making the basic go-ahead decision on system development projects and computerhardware or software facilities? Please tick them off as applicable in column 1, and please completecolumn 1 before going on to column 2. Also, it may be best to use a pencil in case of changes.

Next, what is your estimate of the number of projects to which a given method applies as a percentageof the total? Indicate this in column 2. Your best estimates will be sufficient.

Lastly, in column 3, what ranking would you give to each method in terms of the overall value of projectsto which it applies? Start with most important = 1, next in importance = 2, etc.

All information from your completed survey sheet will be held strictly confidential, and the overall resultswill be sent to you.

Explanatory Notes giving detailed explanations are attached.

352 MIS Quarterly/September 1992

Justifying IT Investments

Explanatory Notes giving detailed explanation are attached.

Methods/Criteria/Justification Tick

(~’)

Percentof projectsto whichapplied

1. Discounted Cash Flow:(a) Net Present Value I~ ~0 /--)/

(b) Internal Rate of Return ~ ~0

(c) Profitability Index

(d) Other

2. Non-DCF Financial:(a) Average/Accounting Rate of Return

(b) Payback Method V( 5-0

(c) Other

3. Budgetary Criteria/Constraints V~ G~-

4. Support of Business Strategy/Objectives:(a) Explicit ~f ~:~0

(b) Implicit I// j-3"’O

5. Response to Competitive Systems I// "~ 0

6. Support Mgt./Exec. Decision Making I~’ ~ 0 "7

7. Technical/System Requirements ~’ ~--J~ /0

8. Legal or Government Requirements

9. Introduce/Learn New Technology V/ / 0

10. Project Risk or Probabilityof Project Success:

V/ ~.~0(a) Completion of Requirements

(b) Achievement of Benefits

11. Other (please specify):(a)

(b)

(c)

Ranking

MIS Quarterly~September 1992 353