The U.S. Housing Confidence Index™

24

The U.S. Housing Confidence Survey™ and The U.S. Housing Confidence Index™ Overview www.pulsenomics.com ©2014-2018 Pulsenomics LLC Pulsenomics®, Housing Confidence Survey™, and Housing Confidence Index™ are trademarks of Pulsenomics LLC. "Over the last three decades, we have learned a great deal about the dynamics of home prices. Our research shows that real estate values have enormous wealth effects, but the markets are inefficient, and are propelled by expectations of market participants. These housing confidence data are critical inputs to our understanding of consumer behavior, and where real estate markets and the economy may be heading." Karl “Chip” Case (1946 – 2016) “This survey and these indices will add immeasurably to our understanding of housing markets, with unprecedented detailed information through time and across geographical areas. We have always been mostly in the dark about fundamental drivers of home prices–now that will change.” Robert Shiller Yale Professor, Nobel Laureate and Pulsenomics Honorary Adviser

Transcript of The U.S. Housing Confidence Index™

TheU.S.HousingConfidenceSurvey™

and

TheU.S.HousingConfidenceIndex™

Overview

www.pulsenomics.com ©2014-2018PulsenomicsLLC

Pulsenomics®,HousingConfidenceSurvey™,andHousingConfidenceIndex™aretrademarksofPulsenomicsLLC.

"Overthelastthreedecades,wehavelearnedagreatdealaboutthedynamicsofhomeprices.Ourresearchshowsthatrealestatevalueshaveenormouswealtheffects,butthemarketsareinefficient,andarepropelledbyexpectationsofmarketparticipants.Thesehousingconfidencedataarecriticalinputstoourunderstandingofconsumerbehavior,andwhererealestatemarketsandtheeconomymaybeheading."

Karl“Chip”Case(1946–2016)

“Thissurveyandtheseindiceswilladdimmeasurablytoourunderstandingofhousingmarkets,withunprecedenteddetailedinformationthroughtimeandacrossgeographicalareas.Wehavealwaysbeenmostlyinthedarkaboutfundamentaldriversofhomeprices–nowthatwillchange.”

RobertShillerYaleProfessor,NobelLaureateandPulsenomicsHonoraryAdviser

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|2

TableofContents

Part1: TheU.S.HousingConfidenceSurvey™(HCS)

• Overview 3

• SampleSizes 4

• NationalandMetropolitanAreaSamples;OnlineSurveyMode 5• SamplingApproach;QualityControlMeasures 7

• SurveyAccuracy 8

• OtherSelectedHousingSurveys,ConfidenceSurveysandRelatedIndices 10

Part2: TheU.S.HousingConfidenceIndex™(HCI)

• DefinitionandPurpose 13 • HCIMethodologyOverview;Coverage 14

• InterpretingHCIValues 15• Context 16

Part3: WhyTheU.S.HousingConfidenceSurvey™and

TheU.S.HousingConfidenceIndex™areImportant 18

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|3

ProductionandManagement

HCSandHCIweredevelopedandareadministeredbyexpertswithestablishedtrackrecordsforproducingauthoritativesurveyresearchandU.S.housingindices.TheyareproducedbyPulsenomicsLLCunderthedirectionofitsfounder,TerryLoebs.Pulsenomics®isanindependentresearchandconsultingfirmwithuniqueexpertiseconcerningtheU.S.housingmarketthatspecializesindataanalytics,newproductandindexdevelopmentforinstitutionalclientsinthefinancialandrealestatearenas.

Loebshasmorethan30yearsofexperienceinthecapitalmarketsandindevelopinginnovativeproductsandservicesdrivenbyU.S.housingdata.Formorethanadecade,heledthecommercialdevelopmentoftheCase-ShillerIndexes®andthesuccessfulefforttoestablishtheirworld-widereputationasthepremierhomepriceperformancebenchmark.LoebswasacentralfigureinthelaunchoftheS&P/Case-ShillerHomePriceIndices,andacatalystindevelopingnewfinancialproductsandmarketinfrastructureforU.S.homepriceriskmanagement,includingtheCMEHomePriceFuturesandOptionsmarket,andthefirststockexchange-tradedhomeprice-linkedsecurities.HeistheauthorandmanagerofHCSandHCI,aswellasTheZillow®HomePriceExpectationsSurvey™(HPES),whichPulsenomicsadministerseachquartertoanexpertpanelcomprisedof150leadingeconomists,portfoliomanagers,strategists,andrealestatemarketanalysts.

“Inthemostrecentboom,payinghighpricesrequiredanoptimisticassessmentoffuturepricegrowth.Risingpricesaremoststronglyassociatedwithoptimisticexpectations,andcreditmarketconditions…playedasupportingrole.”

(Excerptfrom“ANationofGamblers”,byEdwardGlaeser,NBER,January2013)

TheU.S.HousingConfidenceSurvey™

“Lettheinfluxofmoneybeeversogreat,iftherebenoconfidence,propertywillsinkinvalue,andtherewillbenoinducementoremulationtoindustry.Thecirculationofconfidenceisbetterthanthecirculationofmoney…Theestablishmentofconfidencewillraisethevalueofproperty,andrelievethosewhoaresounhappyastobeinvolvedindebts.”

ExcerptfromJamesMadison’sspeechatCommonwealthofVirginiaConvention,June20,1788

________________________________________________________________________________________________________________________________________________________________________________________________________________________

Overview

TheU.S.HousingConfidenceSurvey™(HCS)isthefirsthouseholdsurveydevelopedtofacilitatesystematicmeasurementandreportingofconsumerconfidenceintheU.S.housingmarket.HCSisuniqueamongconsumerandeconomicconfidencesurveys.AstheinstrumentforcollectingthemarketintelligenceusedtoproduceTheU.S.HousingConfidenceIndex™(HCI),HCSiscomprisedofarobustdatasetthat:

• Systematicallymeasureshousingconfidencenationallyandinindividualmetropolitanareamarkets.

• Gaugesattitudesconcerninghomeownershipandprevailingmarketconditionsamongallhouseholdtypes,andseparately,forhomeownersandrenters.

• Measureshomevalueexpectationsforbothshort-termandlong-termhorizons.

• Quantifies,analyzes,andtracksimportanthouseholdattitudesbytenurecategoryandkeydemographicvariables.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|4

HonoraryAdvisers

Karl“Chip”CaseandRobertShillerwerenamedPulsenomicsHonoraryAdvisersin2013.ThedevelopmenteffortforHCSandHCIwasinspired,inpart,bytheirencouragement,input,andmorethan85collectiveyearsofpioneeringresearchconcerninghomepricesandwealtheffects,homebuyerexpectations,financialmarkets,andbehavioraleconomics.

ChipCase(1946-2016)wasaProfessorofEconomicsatWellesleyCollege,whereheheldtheComanandHepburnChairinEconomics,andtaughtfor34years.HewasaseniorfellowoftheJointCenterforHousingStudiesatHarvardUniversityandPresidentoftheBostonEconomicsClub.ChipalsoservedasamemberoftheboardsofdirectorsoftheAmericanRealEstateandUrbanEconomicsAssociation,theMortgageGuaranteeInsuranceCorporation(MGIC),theDepositor'sInsuranceFundofMassachusetts,CenturyBank,theLincolnInstituteofLandPolicy,andtheRapportInstituteforGreaterBoston.Hewasauthororco-authoroffivebooksincludingPrinciplesofEconomics,presentlyinitseleventhedition.

RobertShillerisSterlingProfessorofEconomicsatYaleUniversity,andProfessorofFinanceandFellowattheInternationalCenterforFinance,YaleSchoolofManagement.Bobhaswrittenextensivelyaboutfinancialmarkets,financialinnovation,behavioraleconomics,macroeconomics,realestate,statisticalmethods,andonpublicattitudes,opinions,andmoraljudgmentsregardingmarkets.Hehasbeenresearchassociate,NationalBureauofEconomicResearchsince1980,andhasbeenco-organizerofNBERworkshops:onbehavioralfinancewithRichardThalersince1991,andonmacroeconomicsandindividualdecisionmaking(behavioralmacroeconomics)withGeorgeAkerlofsince1994.Hewritesaregularcolumn"Financeinthe21stCentury"forProjectSyndicate,whichpublishesaroundtheworld,and"EconomicView"forTheNewYorkTimes.InOctober2013,BobwasawardedtheNobelPrizeinEconomicSciences,andwaselected2016PresidentoftheAmericanEconomicAssociation.

HCSdeploysasurveyinstrumentdevelopedforaspecificpurpose:togatherconcrete,measurableconsumerattitudesconcerninghomeownershipandlocalrealestatemarketconditionsthatenableproductionofHCI.Incollaborationwithitsprojectadvisersandpartners,andwithaviewtowardselicitingaccurateanswers,PulsenomicsdesignedtheHCSinstrumenttobeengaging,relevantandcomprehensibletobothhomeownerandrenterrespondents.

TheHCSquestionnairewascraftedbysubjectmatterexpertsandthoroughlytestedinthefield.Theinstrumentisadministeredtoadultrespondentswhoarethesoleorjointdecision-makerconcerninghouseholdfinancialmatters.1

Inadditiontoresponsedataconcerninghousingmarketconditions,expectations,andhomeownershipaspirations,keydemographicinformationiscollectedfromeachrespondenttoenablepost-stratificationweighting.ThesamplebalancingweightsarecalculatedandappliedattheindividualmetropolitanarealevelsothatHCSresultsandHCIlevelsreflecttheuniquepopulationattributesofeachgeographicmarketstudied.2

HCSisadministeredinauniformandsystematicmanner,andinaccordancewithapplicableStatelaws,Federallaws,andcodesofprofessionalconduct(e.g.,thoseoftheAmericanAssociationforPublicOpinionResearch,theNationalCouncilonPublicPolls,andtheInsightsAssociation).AdherencetothesecodesensurethatHCSisdeployedusingthehighestprofessionalstandardsofsurveyadministration,andenablePulsenomicstoproduceHCIthatareauthoritativeandbasedonconsistentlyreliabledata.

SampleSizes

EachtimeHCSisfielded,atleast500completedHCSquestionnairesarecompletedbyheadsofhouseholdwithineachof25majormetropolitanareas,andseparately,3,000arecompletedbyheadsofhouseholdacrossall50statesinproportiontothenationalhouseholdpopulation.ForeacheditionofHCS,Pulsenomicscompilesmorethan700,000responsedatapointsthatarerecordedfromaminimumof15,500completedquestionnaires.31HCSfieldworkisexecutedbyPulsenomicsstrategicpartner,SurveyUSAofClifton,NewJersey.TheHCSinstrumentincludesapproximately45questions,althoughtheactualnumberofquestionspresentedtoHCSrespondentsisdependentonseveralfactors,suchaseachrespondent’stenureprofileandanswerpattern.Forexample,certainsurveyquestionsarespecifictoowner-occupantsorrenter-occupants;therespondent’sanswerpatterncantriggerquestion-branchinglogicwithinHCSthatdetermineswhetherafollow-upquestionisnecessary,andifso,whatversionofafollow-upquestionisappropriatetopresent.TheHCSquestionnaireisavailableathttps://pulsenomics.com/Housing_Confidence_Survey.html2Post-stratificationweightsforeachmetroareaarederivedfromtheU.S.Censusdata,andappliedforkeydemographiccharacteristics(i.e.,age,gender,race/ethnicity)andhouseholdtenureprofile(i.e.,owner-occupied,renter-occupiedhomes).Forthenationalsample,thebalancingweightsreflectthedemographiccharacteristicsandtenureprofileofallU.S.households.3Over-samplingmaybeemployedtoensurethathard-to-reachpopulationsegmentsarenotunder-represented;thus,theactualnumberofcompletedquestionnairescollectedforeachmetroareatypicallyexceeds15,500.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|5

NationalandMetropolitanAreaSamples

Inadditiontoanation-widestudy,HCSresearchisconductedin25majorU.S.metropolitanareas:

Atlanta Denver LosAngeles Philadelphia SanFrancisco

Boston Detroit Miami Phoenix SanJose

Chicago Houston Minneapolis St.Louis Seattle

Columbus Indianapolis Orlando SanAntonio Tampa

Dallas LasVegas NewYork SanDiego WashingtonD.C.

OnlineSurveyMode

HCSusesdatacollectedelectronicallyfromlargesamplesofinternetusers.SurveyrespondentscompletetheHCSquestionnaireviatheinternetontheirsmartphone,tablet,desktopcomputer,orotherelectronicdevice.Anadultage18oroverwhoisthesoledecision-makerorajointdecision-makerconcerninghouseholdfinancialmattersisselectedbyasystematicprocedurethatprovidesabalanceofsurveyrespondentsbygender,age,race/ethnicity,andhouseholdtenure.4

Fortheforeseeablefuture,untilanentirelynewcommunicationsparadigmisinvented,Pulsenomicsexpectsinternet-usersamplestobethebestoptionforgatheringHCSrespondentdata--notbecausesuchnon-probabilitysamplesare4HCSnationalsamplesalsousegeographicregionasabalancingfactor.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|6

ideal,preferredorperfect--butbecausetheyarenowsuperiortoolder,datedmethodologieswhichyieldless(andcostmore)thantheyusedto.Pulsenomicsbelievesthattheuseofinternet-usersamplesandcollectionofrespondentdataonlineachievethebestpossiblebalancebetweenkeyHCSgoals:mitigatingtotalsurveyerror(TSE),optimizinggeographiccoverageandexecutionefficiency.5

Thereliabilityofmid-20thcenturysurveymethods(e.g.,thosethatrelyontheU.S.mailandlandlinetelephones)havebeencompromisedbyacombinationofsocietalandtechnologicalchangesthathaveunfoldedinrecentdecades.6Profoundlifestylechanges,largernumbersofmultiple-earnerhouseholds,longeraveragecommutetimes,theproliferationofmobile“smart”phones,theinternet,andotherdigitalcommunicationstechnologiesarejustsomeofthefactorsthathavefundamentallyalteredconsumerpreferencesandbehaviorsthataffectsurveysamplingandresponseratesinthe21stcentury.

Whilesurveyresearchersroutinelybalancerespondentdatatomatchkeycharacteristicsofthetargetpopulation,relativetothepast,thosewhogatherfeedbackfromtelephonerespondentstodaymustapplylargerweightstothedatatheycompileinordertoneutralizetheill-effectsofnon-coverageandnon-responsebiases.Alas,adjustmentsintendedtoaddressnon-participationratesintelephonesurveyscancompromisetotalsurveyaccuracyinimmeasurableways.

5HCSusedamulti-modal,blended-sampleapproach(alandlinesampleframewasusedtoaugmentaninternetcellphoneusersample)throughJuly2016.6Notlongago,themajorityofprivately-fundedconsumerresearchstudieswerebaseduponlandlinesampleframes,withrespondentstypicallyselectedproportionatetoeachmetropolitanarea’spopulationthroughtheRandomDigitDialing(RDD)method.RDDisdesignedtogivealllistedandunlistedlandlinetelephonenumbersanequal,non-zerochanceofbeingcalledandinterviewed.Althoughmosttelephonesurveystodayincludesomepercentageofcell-phonerespondents,neitherthephysicallocationnorplaceofresidenceofmobilephoneuserscanbeascertained;comprehensivedatabasescomprisedoftheuniverseofcellphoneusersdonotexist,anditisillegalforresearchersto“auto-dial”cellphonenumbers.

Theproliferationofmarketing“junkmail”,andthepublic’sgrowingrelianceonelectronicmessaging(emails,texts)forwrittencommunications,andgrowinguseofdigitalpaymentsforbillremittancesarejustafewfactorsthathavecontributedtolowresponseratestosurveysdisseminatedviaU.S.mail.

Theubiquityofvoicemail,caller-IDandothercall-screeningtechnologieshasimpededtheabilitytoreachsurveyrespondentstelephonically.Unsurprisingly,responseratesfortelephonesurveyshaveplummetedoverthepasttwodecades(andhaveneverbeenlower);thedegreeoftelephonicnonresponseencounteredbyopinionresearcherstodayischallengingfundamentalassumptionslong-heldamongthepublicandmedia(i.e.,thatasamplerepresentativeofthestudypopulationisassuredbyrandomlyselectingtelephonenumbersand/ordialingacombinationofcellphoneandlandlinerespondenttargets).

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|7

SamplingApproach

HCSemploysastratifiedquotasampling.Thismethodisdesignedtocapturekeypopulationcharacteristicsthatareproportionaltothoseintheoverallpopulation,andentailsdividingapopulationintosmallergroups,orstrata,formedaccordingtogroupmembers'sharedattributesorcharacteristics.

Todiversifythesurveyrespondentpoolandenhancerepresentativeness,HCSsamplesaredrawnfromanetworkofsuppliers.7Thecompositionandqualityofeachsample,andeachsampleprovider,areproactivelymonitoredtoensureHCSdataintegrityandconsistency.QualityControlMeasures

HCSincorporatesmultiplelayersofqualitycontroltoenhancethereliabilityofrespondentdata.

SurveyTopicBlinding

Tomitigateselectionbias,HCSrespondentsareblindedtothesurveysubjectmatterbeforeagreeingtocompleteit,andnoresearchsponsorname(s)arepresented.In-surveyandpost-surveyQC

• Multiplein-surveyrespondentintegritytestsidentifyillogicalandunrealisticresponses.ThesesafeguardsensurethatrespondentsarereadingHCSquestionscarefully,andansweringthemthoughtfully.8

• Digitalfingerprintingtechniquesareemployedtoterminatebots,preventduplicaterespondents,andflagout-of-marketrespondents.9

• Atwo-wayspeedfilterisappliedtoallrespondentswhocompleteHCS.10SampleproviderQC

• AnyHCSsampleproviderthatusesemailrecruitmentmustcomplywithindustry-standarddoubleopt-inproceduresformarketresearch.11

• EachproviderusedasasourceforHCSsamplesismonitoredonanongoingbasisforthequalityofsamplestheyprovide,andareactivelyreviewedviaasystematicbenchmarkingprocess.12

7Relianceonasingle-sourceofonlinesamplecanincreasebias(e.g.,non-coverage).ThecombinationsofsamplesuppliersusedtoconductHCSaretrackedforeachofthe25metro-areasamplesandthenationalsampleeachtimeHCSisfielded,andaremanagedovertimewithaviewtowardspreservingdataqualityandconsistency.8HCSisimmediatelyterminatedwhenarespondentfailsanyoneofthesein-surveyqualitychecks,andalldatareceivedfromsuchrespondentspriortoterminationarediscarded.9Responsesfromout-of-marketrespondents(e.g.,thosecompletingHCSviaanIPaddressthatisinconsistentwiththeirrecordedplaceofresidence)arediscarded.10AlldatareceivedfromrespondentswhocompleteHCSmorequickly(ormoreslowly)thanthresholdratesareautomaticallydiscarded.11Theopt-inprocessindicatestherespondents’relationshipwiththesampleprovider.Doubleopt-inreferstoaprocessthatrequiresproactiveconfirmationfromthepersonjoininganonlinepanelthats/hewishestobeapanelmemberandunderstandswhatpanelmembershipandsurveyparticipationentails.12Onceperquarter,abrieftestinstrumentdesignedtomeasurerespondentattentiveness,timespent,answerconsistency,andresponsequalityisadministeredtoarepresentativesampleofeachprovider’sonlinerespondentpanel.Oncecollected,thetestdataarecomparedtocorrespondingperformancebenchmarkstoassesssamplequality.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|8

Samplingerrorisonlyoneofseveraltypesoferrorthatsurveyresearchersmustmanage.Othersourcesofsurveyerrorinclude:

• Thesequenceandorderingofquestions

• Theaccuracyandconsistencyofthesurveyquestions(iftheyarespoken)andresponses(iftherespondentdataaremanuallyrecorded)

• Theclarityandconsistencyofinterviewervoices

• Theinabilitytocontactsomemembersofthepopulation• Therefusalofsomemembersofthepopulationtoparticipate

• Thedifficultyoftranslatingeachquestionnaireintoallpossiblelanguagesanddialects

• Theextenttowhichresponsedataareweightedandweightingmethodology(“designeffects”)

SurveyAccuracy

TheoverarchingaccuracygoalofHCSismitigatingtotalsurveyerror(TSE).Consistentwiththisgoal,theHCSsurveyinstrumentdesignincorporatestheinputandfeedbackfromsubjectmatterexperts,learningfromiterativefieldtesting,andthecontinuousscrutinyofrespondentdata.Severalfactorsimpactthereliabilityofsurveyresearch.Although“totalsurveyerror”(TSE)canbemanaged,itisimpossibletomeasurewithprecision;non-samplingerrorscannotberoutinelyquantified,andoftencannotbequantifiedatall.TheonecomponentofTSEthatcouldbequantifiedinthepast—samplingerror—isincreasinglydifficulttoisolatetoday.• MarginofSamplingError—“MOE”

Fordecades,journalistswereconditionedtolookforamarginofsamplingerrorwhenexaminingresearchresults.Whileresearchpractitionersknewthatsamplingerrorwasonlyoneofmanydifferentpossiblesourcesoferrorintheexecutionofanopinionresearchproject,general-assignmentreportersondeadlinescannedthepollsters’memoforthe“MOE”andhavingfoundit,theyincludeditintheirstories.Today,researchscientistsaregraduallyreplacingamarginofsamplingerrorwithadifferentkindofmeasure--thecredibilityinterval--becauseMOEismeaningfulonlyforprobabilitysamples.13• CredibilityIntervals

Inanevolvingopinionresearchworldwhereamajorityofstudiesarecompletedusinganon-probabilitysample,statisticiansandresearchtradeassociationsstillneedtoexpresstojournalistsandotherconsumersofsurveydatahowmuchofabrackettoplacearoundagivensurveyfinding,wheresuchbracketisolatestheerrorthatmightbeattributabletosamplingalone.ToaccomplishthisobjectiveforHCS,Pulsenomicshasadoptedthecredibilityintervalbecauseitisausefulgaugeofsamplingerrorwhennoteverypotentialrespondenthasaknown,non-zerochanceofinclusioninasurvey.

Acredibilityintervalisanestimateofanintervalaroundameasuredpercentagewithinwhichthetruepercentage,ifalleligiblerespondentsweretobeinterviewed,wouldhaveanx%chanceoffalling.Forsufficientlylargesamplesizesandintheabsenceofpriordata,thecredibilityintervalwillbesimilartothetwostandard-deviationconfidenceintervalthatwouldbeobtainedfromaprobabilitysample,afterestimatinganeffectivesamplesizebasedontherespondentweightsusingaformuladevelopedbyLeslieKish(squareofsumofweightsoversumofsquaresofweights).14

Bywayofillustration:if70percentofHCSrespondentsindicatethat“nowisagoodtimetobuyahome”,andifthecredibilityintervalis3percentagepoints,thentheintervalbetween67%and73%mightbedisplayedastherangeofcredibleoutcomes(usingtheindustryshorthandof70%,“+/-3percentagepoints.”).Thesedatacouldthenbe

13Aprobabilitysampleisoneforwhicheverymemberofthetargetpopulationhasanequal,known,andnon-zerochanceofselection.Random-digitdialing(RDD)oflandlinetelephonenumberswasembraceddecadesagobytheopinionresearchcommunityasameanstoreliablycreateprobabilitysamples.Comprehensive,reasonablyaccuratedatabasesoflandlinetelephonenumbersstillexistandarereadilyaccessiblebysurveyresearchers;databasesofcellphonenumbersandinternetaddressesarelessreliablebecausetheycanbeincompleteanderror-prone.14Bayesiancredibilityintervalsrepresentuncertaintyasasubjectiveprobabilityestimate,whichshouldnotbeinterpretedasafrequency.Fora95%credibilitylevel,thereisnocollectionofalternativeresearchoutcomeswhichwouldfallwithintheinterval19timesoutof20followingabell-curvedistribution.Acredibilityintervalrepresentsa“degreeofbelief”inaproposition.Foramorethoroughoverviewofcredibilityintervals,see“TheEvolutionfromMarginofSamplingErrortoCredibilityInterval”.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|9

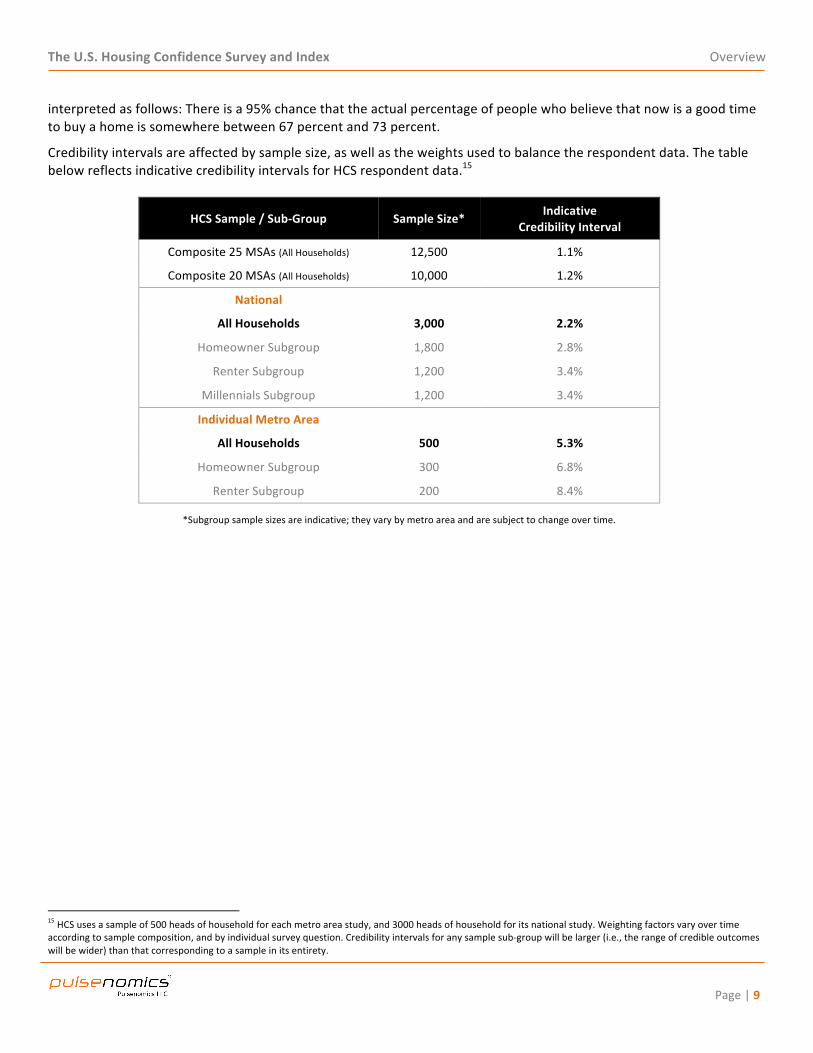

interpretedasfollows:Thereisa95%chancethattheactualpercentageofpeoplewhobelievethatnowisagoodtimetobuyahomeissomewherebetween67percentand73percent.

Credibilityintervalsareaffectedbysamplesize,aswellastheweightsusedtobalancetherespondentdata.ThetablebelowreflectsindicativecredibilityintervalsforHCSrespondentdata.15

HCSSample/Sub-Group SampleSize* IndicativeCredibilityInterval

Composite25MSAs(AllHouseholds) 12,500 1.1%

Composite20MSAs(AllHouseholds) 10,000 1.2%

National

AllHouseholds 3,000 2.2%

HomeownerSubgroup 1,800 2.8%

RenterSubgroup 1,200 3.4%

MillennialsSubgroup 1,200 3.4%

IndividualMetroArea

AllHouseholds 500 5.3%

HomeownerSubgroup 300 6.8%

RenterSubgroup 200 8.4%

*Subgroupsamplesizesareindicative;theyvarybymetroareaandaresubjecttochangeovertime.

15HCSusesasampleof500headsofhouseholdforeachmetroareastudy,and3000headsofhouseholdforitsnationalstudy.Weightingfactorsvaryovertimeaccordingtosamplecomposition,andbyindividualsurveyquestion.Credibilityintervalsforanysamplesub-groupwillbelarger(i.e.,therangeofcredibleoutcomeswillbewider)thanthatcorrespondingtoasampleinitsentirety.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|10

CaseandShillerbeganasurveyofrecenthomebuyersin1988,andithasbeenconductedannuallysince2003.Withinthesesurveys,consumersinfourcitieshavereportedtheirone-yearandten-yearexpectationsforhomevalues.InawhitepaperpreparedfortheFall2012BrookingsPanelonEconomicActivity,acumulativeanalysisofthesurveydata,comprisedofnearly5,000completedmailsurveys,waspresentedbyCase,ShillerandThompson.Overtheyears,conclusionsmadebytheauthorsinconnectionwiththisresearchthatarepertinenttoHCSandHCIinclude:

“Weseea[housing]marketlargelydrivenbyexpectations.”“Webelievethatoneaspectof[theU.S.housingbubbleandbust]hasnotreceivedtheattentionitdeserves:theroleofexpectations.”“Bothkindsofexpectations[one-yearandten-year]areimportant.Homesellerswillhaveanincentivetowaitanotheryearifone-yearexpectationsarehigh,whilebuyershaveanincentivetobuynowratherthannextyear.But,inmakingageneraldecisionwhethertobuyatallornot,andforjudgingtheoveralllong-terminvestmentreturn…thelonger-termexpectationsarelikelytobemoreimportant.”“Thelong-termexpectationalsomattersimportantlyfordemandforhousing,andthelong-termexpectationisimportanttothewaythatpeoplejudgewhethertobuyahome.”“Moreoftherootcausesofthebubblecanbeseenin[homebuyers’]long-term,ten-yearhomepriceexpectations.”“Thedataalsoshowthat[home]buyerswere,ifanything,outinfrontofshort-term[homevalue]changesthatwereoccurring…”“Itisfromthesenebulousandrelativelyslow-moving[ten-year]expectationsthatthebubbletookmuchofitsimpetus,andthatfuturehomepricemovementswillaswell.”“Therearereasonstosuspectthatthe[home]pricechangesweactuallyseearerelatedtoswingsinpublicopinionsratherthanfundamentals.”(RobertShillercommentingonaMargaretHwangSmithandGarySmithpaperpresentedatBrookingsinMarch2006).

OtherSelectedHousingSurveys,ConfidenceSurveysandRelatedIndicesCase-ShillerHomebuyerSurveys

Oneofthemostdurableofallhousing-focused,consumerattitudinalsurveystodateisaresearcheffortinitiatedbyKarlCaseandRobertShiller.Thisprojectbeganin1988,andhasfocusedontheattitudesandexpectationsofrecenthomebuyersinfourcities.16ThesurveyisadministeredannuallyusingaquestionnairethatissenttoseveralhundredrecipientsviaU.S.mail.

16Asofthiswriting,themostrecentwhitepaperconcerningthisresearchwaspresentedtoTheBrookingsInstitutionin2012.See“WhatHaveTheyBeenThinking?HomeBuyerBehaviorinHotandColdMarkets”,byKarlE.Case,RobertJ.ShillerandAnneThompson.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|11

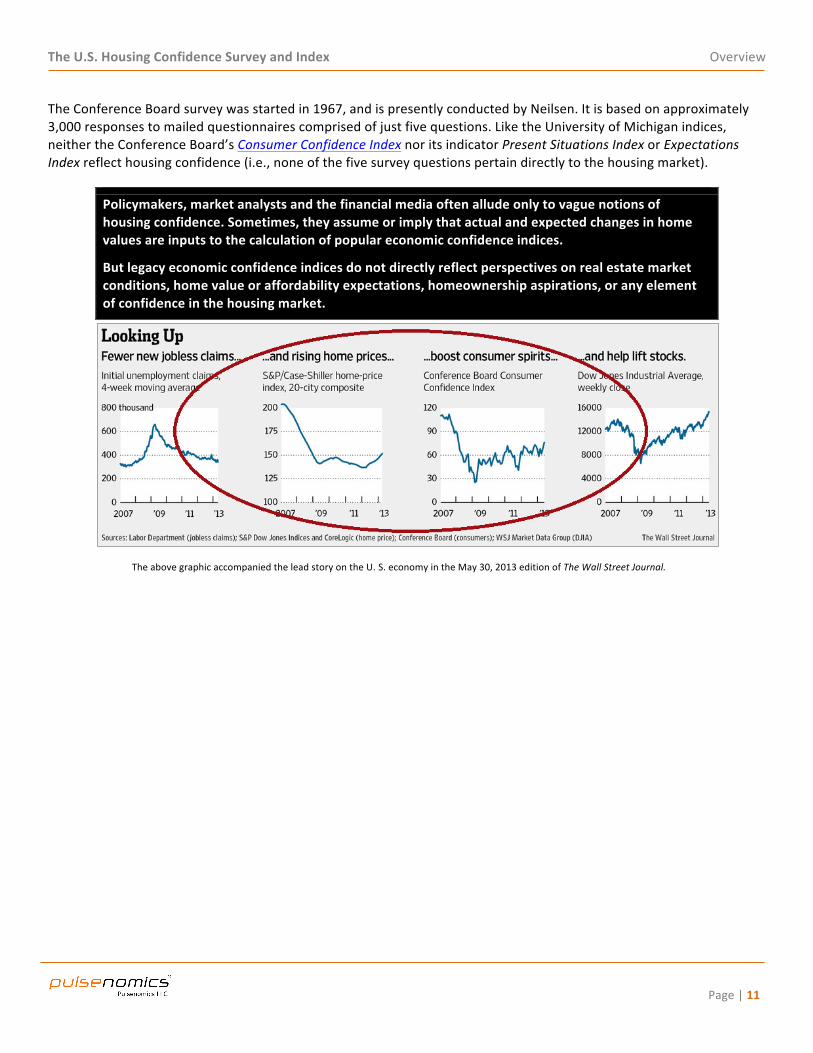

TheConferenceBoardsurveywasstartedin1967,andispresentlyconductedbyNeilsen.Itisbasedonapproximately3,000responsestomailedquestionnairescomprisedofjustfivequestions.LiketheUniversityofMichiganindices,neithertheConferenceBoard’sConsumerConfidenceIndexnoritsindicatorPresentSituationsIndexorExpectationsIndexreflecthousingconfidence(i.e.,noneofthefivesurveyquestionspertaindirectlytothehousingmarket).

TheabovegraphicaccompaniedtheleadstoryontheU.S.economyintheMay30,2013editionofTheWallStreetJournal.

Policymakers,marketanalystsandthefinancialmediaoftenalludeonlytovaguenotionsofhousingconfidence.Sometimes,theyassumeorimplythatactualandexpectedchangesinhomevaluesareinputstothecalculationofpopulareconomicconfidenceindices.

Butlegacyeconomicconfidenceindicesdonotdirectlyreflectperspectivesonrealestatemarketconditions,homevalueoraffordabilityexpectations,homeownershipaspirations,oranyelementofconfidenceinthehousingmarket.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|12

(continuedfromprecedingpage)

Policymakers,marketanalystsandthefinancialmediaoftenalludeonlytovaguenotionsofhousingconfidence.Sometimes,theyassumeorimplythatactualandexpectedchangesinhomevaluesareinputstothecalculationofpopulareconomicconfidenceindices.

Butlegacyeconomicconfidenceindicesdonotdirectlyreflectperspectivesonrealestatemarketconditions,homevalueoraffordabilityexpectations,homeownershipaspirations,oranyelementofconfidenceinthehousingmarket.

“Astronghousingmarkethasbuoyedtheeconomicrecoverybyimprovingconfidenceamongconsumers,encouraginghouseholdspendingandgeneratingconstructionjobs.”(TheWallStreetJournal,9/19/2013)

“Jobgains,alongwiththestrengtheninghousingmarket,haveinturncontributedtoincreasesinconsumerconfidenceandsupportedhouseholdspending.”(BenBernanke,OpeningRemarks,6/19/2013PressConference)

“Thebroad-basedhousingimprovementsappeartobebuoyingconsumerconfidenceandspending.”(TheNewYorkTimes,5/29/2013)

“RisinghomepricesshouldhelpbuoyconsumerconfidenceandthebroadereconomybecausehousesrepresentthelargestfinancialassetformanyAmericans.”(TheWallStreetJournal,5/29/2013)

“…anumberoffactorshavehelpedconfidence,fromfallinggasolinepricestoarisingstockmarkettoarecoveringhousingmarket.”(MarketWatch,5/17/2013)

“ConsumerConfidenceJumpsasU.S.HomeValuesClimb”(BloombergNewsreportheadline,4/30/2013)

“ManycreditrecoveringhomevaluesforhelpingboostApril’s[ConsumerConfidenceIndex]number.”(U.S.News&WorldReport,4/30/2013)

"U.S.businessesandconsumershaveshownsurprisingmuscleinrecentweeks…confidencehasbeenbuoyedbyrisinghomevalues…”(TheWallStreetJournal,3/22/2013)

"ConsumerconfidencereboundedinFebruary…itispossiblethatconfidencewilldropbackinthecomingmonths…However,thecontinuingrecoveryinthehousingmarketmayfurtherboostthatconfidence.”(CBSMoneyWatch,2/26/2013)

“However,depressedhomepriceshavecontinuedtobeastructuralheadwindtogrowthbykeepingalidonconfidenceandcloggingupkeytransmissionchannelsofmonetarypolicy.”(SocieteGeneraleCrossAssetResearch,2/21/2013)

”Improvementinthe[housing]sectorcouldhelpbroadtractsoftheeconomybycreatingjobs,improvingconsumerconfidenceandboostingproperty-taxreceiptsformunicipalities.”(TheWallStreetJournal,1/27/2013)

“HouseholdwealthintheU.S.climbedinthethirdquarter,reflectingincreasesinstockvaluesandhomepricesthatarehelpingboostconsumerconfidence.”(BloombergNews,12/6/2012)

“Animprovinghousingmarketisbuoyingconsumers’spiritsandspurringspending…Theconfidenceeffects[ofU.S.housing]aremassive.”(TheWallStreetJournal,11/27/2012)

“Still,otherhome-valueandhome-priceindicatorssuggestpricegainshavecontinued–apossibleexplanationforwhyconsumersentiment,thoughlowbyhistoricalstandards,continuestoimprove.”(TheWallStreetJournal,10/31/2012)

“Betternewsonrealestatecouldexplainwhysurveysofconsumerconfidencepostedbetter-than-expectedreadingsinSeptember–evenasotherdataforthismonth…remainweak.”(TheWallStreetJournal,9/25/2012)

“Rising[house]pricesalsocouldhelpturnaroundconsumer’fragilepsychology,anunpredictablebutimportantfactorthatcanfuelmoresales.”(TheWallStreetJournal,9/10/2012)

“Consumersseemtosharehispessimism[forhomeprices].AconsumerconfidencesurveyreleasedbyTheConferenceBoard…felltoafour-monthlow.”(TheWallStreetJournal,5/29/2012)

“[…homepricechangesexplain]agreatdealofthedepthanddurationofthedeclineinconsumerconfidenceduringtheGreatRecessionanditsaftermath.Thisvariablehasbecomemoreimportantsince2000,asthevalueofhousingappreciatedatarapidrateandthencollapsedafter2007asthehousingmarketimploded.The30percentnationaldeclineinhousingpricessincethepeakexplainsmuchofthecrateringofconsumerconfidence.”(“ConsumerSentimentandSpending”,TheMilkenInstitute,Sept2011)

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|13

TheU.S.HousingConfidenceSurvey™(HCS)isalarge-scalehouseholdresearchsurveythatispresentlyconductedtwiceannuallynationally,andwithineachof25ofthelargestU.S.metropolitanareas.

• Eacheditionofthesurveyisadministeredto15,500U.S.adultheadsofhousehold:dataarecompiledfrom25separatemetroareasamplesof500residents,andanationwidesampleof3,000residents.

• TheHCSinstrument–whichhasbeendesignedandvettedbysubjectmatterexpertsandthoroughlytestedinthefield–isdeployedviatheinternet,andforeachofthemetropolitanareassurveyed,respondentdataarebalanced(weighted)accordingtoitsuniquepopulationattributes(i.e.,gender,age,race/ethnicity)andhouseholdtenureprofile(i.e.,owner-occupied,renter-occupied).

• TerryLoebs,founderofPulsenomicsLLC,istheauthorandmanagerofHCSandHCI.KarlCaseandRobertShillerwerenamedHonoraryAdvisersin2013;thedevelopmenteffortforthisprojectwasinspired,inpart,bytheirencouragement,input,andmorethan80collectiveyearsofpioneeringresearchconcerninghousingwealtheffects,homebuyerexpectations,andbehavioraleconomics.

TheU.S.HousingConfidenceIndex™

DefinitionandPurpose

TheU.S.HousingConfidenceIndex™(HCI)wascreatedbyPulsenomicstoeffectivelymonitorandconciselycommunicatethepulseoftheU.S.residentialrealestatemarketnationallyandforindividualmetropolitanareas.17The768uniquetimeseriesthatcompriseHCIarebaseduponresponsedatacollectedfromTheU.S.HousingConfidenceSurvey™(seesidebar).TheHCIdatasetincludesthreefactorsub-indexesthatprovideinsightintothedriversofconsumers’overallhousingconfidence:• TheHousingMarketConditionsIndex™Reflectsconsumersentimentconcerningprevailingmarketconditionswithinlocalhousingmarkets.

• TheHousingExpectationsIndex™Quantifieshouseholdexpectationsregardinghousingaffordability,localhomevalueappreciationinthenear-termandlongrun,andmore.

• TheHomeownershipAspirationsIndex™Revealsandtrackskeyconsumerattitudesconcerningtheiroverarchinghomeownershipgoals.

ForeveryindividualmetropolitanmarkettrackedbyHCI,foreachofthefourU.S.CensusRegions,andforthenationasawhole,Pulsenomicsalsoproducestenuresub-indexesthattrackhousingconfidencebyhouseholdtype(i.e.,TheRenterConfidenceIndex™andTheHomeownerConfidenceIndex™).TheMillennialHousingConfidenceIndex™(MHCI)serieswaslaunchedin2018toseparatelytrackhousingmarketsentimentamonghouseholdsheadedbymembersofthemillennialgeneration.18TheuniquecompositionofHCIprovidesvaluable,uncommoninsightintotheU.S.housingmarket,andcomplementslegacymeasuresofmacroeconomichealth.Importantly,theconsumerattitudesthatarequantifiedandtrackedbyHCIcanhaveoutsizedinfluenceoneconomicdecision-makingbyhouseholds,andsignificantperiod-to-periodchangesinHCImayforeshadowimportantshiftsinlocalhousingmarketdynamicsandmacroeconomicactivity.HCIcanenhanceeconomicanalysis,policy-making,decision-making,andriskmanagementprotocolspertainingtokeyU.S.housingmarkets,localeconomies,andthenationaleconomybysystematicallyquantifyingandmonitoringchangesinhousingconfidenceovertime.

17PulsenomicsLLCistheindexcalculationagent,andtheownerofallintellectualpropertyrelatedtoHCSandHCI.18Thethreefactorsub-indexesarealsoproducedinconjunctionwitheverytenure-specificHCIandMHCI.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|14

HCIMethodologyOverview19

HCIiscomputedusingaweighteddiffusionindexmethodology.Diffusionindicesmeasurethedegreethatdataarediffused(dispersed)withinasample.LeadingU.S.economicdataseriesarecommonlysummarizedorindexedusingthisapproach.20EachHousingConfidenceIndex(HCI)21isaweightedcompositemeasureofthreeunderlyingfactorsub-indexes,eachofwhichquantifyauniquedimensionofconfidenceinthehousingmarket:

• TheHousingMarketConditionsIndex(HMCI)• TheHousingExpectationsIndex(HEI)• TheHomeownershipAspirationsIndex(HAI)

PulsenomicscalculatesaheadlineHCIandthethreeunderlyingsub-indexesattheindividualU.S.metropolitanmarketlevelusingmorethan700,000individualconsumerresponsesgatheredfromeacheditionofTheU.S.HousingConfidenceSurvey™(HCS)22.HCICoverage

InadditiontothefourHCIsproducedforthetotalofallsurveyedhouseholdsineachmetromarket,Pulsenomicscalculatestenure-specificsub-indicesforeachcity,i.e.,headlineandindicatorHCIsfor(a)thesubsetofrespondentswhoarehomeownersand(b)thesubsetofrespondentswhoarerenters.Pulsenomicsalsocalculatesheadlineindicesandsub-indicesforhouseholdsheadedbymembersofthemillennialgeneration.EacheditionofHCIiscomprisedof768indexvalues.23

19ThecompleteHCIMethodologydocumentisavailableathttps://pulsenomics.com/Housing_Confidence_Index.html20Afewexamples:TheWellsFargoHomebuilderConfidenceIndex;TheInstituteofSupplyManagement’s(ISM)PurchasingManagers’Index;TheConferenceBoard’sConsumerConfidenceIndex,PresentSituationsIndex,andExpectationsIndex;andTheUniversityofMichigan’sIndexofConsumerSentiment,IndexofCurrentEconomicConditionsandIndexofConsumerExpectations.21Pulsenomics®,HousingConfidenceIndex™,andHousingConfidenceSurvey™,aretrademarksofPulsenomicsLLC.22Presently,HCIsarecalculatedforeachof25ofthelargestU.S.metropolitanstatisticalareas,selectedcombinationsofthoseMSAs(CompositeHCIs),foreachofthefourmajorU.S.geographicRegions,andforthenationasawhole(U.S.HCI).CompositeHCIsarecalculatedbycombiningandbalancingselectedmetro-levelHCIsaccordingtotheweightingfactorsprovidedwithinthetablespresentedonpages7-9.23Priorto2018,Pulsenomicspublished252indexseries.In2018,withtheadditionoffivenewmetro-areasamplesandalargenationwidesample,thetotalnumberofHCSrespondentsincreased55%,andPulsenomicsexpandedHCIproductionwithnewly-addedmetro-levelHCIs,nationalHCIs,regionalHCIs,andmillennialHCIs.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|15

Numberofmarkets: 32[1National,4Regional,25Metro-level,2Metrocomposites]

HCIs: x4[1HeadlineHCI,3indicatorindices(HMCI,HEI,HAI)]

TenureCategories: x3[AllHouseholds,HomeownerHouseholds,RenterHouseholds]

GenerationCategories: _x2_[AllGenerations,MillennialGeneration] 768

InterpretingHCIvalues

HCIvaluesaresetonanumericscaleof0to100.Themaximumindexvalueof100wouldindicatemaximumconfidence(i.e.,uniformlypositiveanswerstorelevantquestionswithinTheU.S.HousingConfidenceSurvey™(HCS)wereprovidedbyrespondents);theminimumindexvalueof0wouldindicatenoconfidence(i.e.,uniformlynegativeanswerstorelevantquestionswithinHCSwereprovidedbyrespondents).

Foranyindexreportingperiod:

• Anindexvalueexceeding50designatesapositivedegreeofconfidence

• Anindexvalueequalto50indicatesaneutraldegreeofconfidence

• Anindexvalueslessthan50indicatesanegativedegreeofconfidence.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|16

“[…homepricechangesexplain]agreatdealofthedepthanddurationofthedeclineinconsumerconfidenceduringtheGreatRecessionanditsaftermath.Thisvariablehasbecomemoreimportantsince2000,asthevalueofhousingappreciatedatarapidrateandthencollapsedafter2007asthehousingmarketimploded.The30percentnationaldeclineinhousingpricessincethepeakexplainsmuchofthecrateringofconsumerconfidence.”(“ConsumerSentimentandSpending”,TheMilkenInstitute,September2011)

“Housingactivityandpricesseemlikelytorecover…butitwillbeimportanttomonitordevelopmentsinthissectorcarefully.”

(FederalReserveChairmanBenBernanke,July17,2013)

“Peoplearefeelingbetterabouttheirhomes…andthat’sdrivingthemtospendmore…[but]consumers’psychecanchange.”

(HomeDepotCFOCarolTome,August20,2013)

Context

ThehistoricU.S.homepriceboomandbusthaveremindedusthat,despitetheirenormityandimportance,housingmarketsareincompleteandinefficient.TheunprecedentedscaleandpersistenceofgovernmentsupportfortheresidentialrealestatesectorinthewakeofthebustunderscorethathealthyhousingmarketsarevitaltotheprosperityoftheUnitedStateseconomyandoursociety.ConcernsabouttheinevitablereductioningovernmentsupportarepalpableandsuggestthatvolatilityinU.S.residentialrealestatemarkets–broughttoextraordinarylevelsduringtheboomandbust–islikelytoremainelevatedforyearstocome.TheU.S.housingexperienceofthepastdecade–alongwithevolveddemographics,rapidlychangingconsumerattitudes,andunpredictablegovernmentpolicies–allsuggestthat,goingforward,newandmoreproactiveformsofrealestatemarketintelligencewillbenecessarytodetectandmonitoremergenthousingriskseffectively.Confidenceinourhousingmarketsisaprerequisiteforstablerealestateassetvaluesandahealthyeconomy.Housingconfidencecaninfluenceindividualbehavior,homeprices,andeconomicconsumption.Inthedigitalage,theincreasedvelocityandheightenedvolatilityofconsumerattitudechangessuggestthathousingconfidenceshouldbemeasuredandmonitoredinasystematicfashion.24

HCIrepresentsatimely,ground-breakingefforttodojustthat:systematicallyquantifyandeffectivelymonitorhousingconfidencenationallyandwithinmajormetropolitanmarketsacrosstheUnitedStates.25HCIisconstructedusingdatacollectedfromHCS,alarge-scalehouseholdsurveythatgaugeshousingmarketsentimentand

expectationsbycollectingrelevantdatafromconsumersacrosstheUnitedStates.TheHCSinstrumentwasdevelopedbyPulsenomicstogatheraccurateandtimelyassessmentsofprevailinghousingmarketconditions,homeownershipaspirations,andhomevalueexpectationsamongtheadultpopulation–bothhomeownersandrenters–livingindifferentmetropolitanareasacrossthecountry.HCIreflectsthedegreeofconfidenceamongbothrentersandhomeownerswithinspecifichousingmarkets,in“realtime”(incontrasttomostinformationsets,priceindices,andresearchpertainingtoU.S.housingmarkets,whicharetypicallyderivedfrompropertytransactiondata–whichinmanycases,areseveralmonthsoldatthetimetheyarecompiledandreported).HCIrepresentsthecurrentattitudesofallmarketstakeholders–notjustthoseofhouseholderswhohappentohavebeeninvolvedinarecentrealestatetransaction.26

24Residentialrealestatehaspowerful,two-wayconsumerwealtheffectsanda“confidencemultiplier”.Theconfidencemultiplierinrealestatemanifestsitselfthroughbothprice-to-priceandprice-to-GDP-to-pricefeedbackcycles,anditcanbemagnifiedbyculturalandinstitutionalforces.(GeorgeA.AkerlofandRobertJ.Shiller.2009.AnimalSpirits:HowHumanPsychologyDrivesTheEconomy,AndWhyItMattersForGlobalCapitalism.PrincetonandOxford:PrincetonUniversityPress,pp.16-17,153-156.)25Patentpending.26Forexample,lessthanonepercentofallU.S.householdsareinvolvedinahomepurchaseorsalecontractinatypicalmonth.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|17

“Higherpricesofhousesandotherassets…haveincreasedhouseholdwealthandconsumerconfidence,spurringconsumerspendingandcontributingtogainsinproductionandemployment.”

(FederalReserveChairmanBenBernanke,May22,2013)

““It’sprettyclearthathousingisrecovering.That’sapositiveforgrowth.Itboostswealthandconfidence.”

(JimO’Sullivan,chiefU.S.economistatHighFrequencyEconomicsLtd.,April30,2013)

“Aresurgenthousingmarkethasaidedtheslow-growingU.S.economy,helpinggenerateconfidenceamongconsumers,boostinghouseholdspendingandcreatingconstructionjobs.”(TheWallStreetJournal,August22,2013)

HCIisrelevanttomillionsofindividualsandthousandsofinstitutionsaroundtheworldwithastakeinthe$28trillionU.S.housingmarket.27HCIcanprovideearlysignalsofimpendingchangestohousingmarkethealthbysystematicallymeasuringpertinentconsumerattitudesandexpectationsthatcaninfluencelocalmarketpricesforresidentialrealestate.Recentyears’eventshaveillustratedthatchangingperspectivesregardingthehealthofU.S.housingmarketscanhaveprofoundeffectsoneconomicconsumption,homeownershiprates,houseprices,investorpsychology,andfinancialmarketliquidity.Unlikemostotherlargemarketsandmajorassetclasses,U.S.housingisgeographicallyfragmentedandlacksefficientpricediscoveryandothersignalsofimpendingvaluechangesduetotherelativeilliquidityofresidentialrealestateassetsandtheinherentinefficienciesoftheirmarkets.

However,justlikethoseofotherassetclasses,futurelevelsoftransactionvolumeandpricesinresidentialrealestatemarketsaredependentonthesentimentsandexpectationsofcurrentandprospectivemarketstakeholders.28BoldpolicyactionsinrecentyearsbyTheWhiteHouseandTheFederalReservehaveunderscoredtheprofoundimpactthatthe

housingmarketcanhaveonbothconsumerconfidenceandmacroeconomichealth.29Theseunprecedentedfederalinitiatives,ongoingpolicydebates,andgrowinginterestinhomepriceexpectationsamongpolicymakersalso:

• Suggestthattraditional,laggingindicatorsofhousingmarketconditions(e.g.,homepriceindicesandrealestatetransactionvolumes)areincompletegaugesofmarketrisk,and

• Implythatthesentimentsandexpectationsofhousingmarketstakeholdersareveryimportant,impactfulandwarrantcarefulmonitoring

Ofcourse,prevailingconditions,expectationsandaspirationswithinhousingmarkets–housingconfidence–mustfirstbemeasuredeffectivelyandcommunicatedcomprehensiblyinordertoappreciatetheirfundamentalimportance.Thedifferencesinthesefactorsacrossindividualmarkets,andtheirdegreeofchangeovertimemustbequantifiedinordertounderstandandmonitorhowvariancesinhousingconfidenceforeshadowmarketturningpointsandfuturelevelsofeconomicactivity.HCIistheonlymetricdesignedtoreflect,systematicallyquantifyandmonitorhousing-relatedsentimentsandexpectationsforspecificrealestatemarkets;assuch,theyarepositionedtoevolveintoauthoritativebellwethersoffuturehomevaluechangesandmacroeconomicactivity.

27Thelatestavailablerealestatevaluefigureis$27.8trillionasofthiswriting(TableB.101,BalanceSheetofHouseholdsandNonprofitOrganizations,FourthQuarter2017FlowofFundsAccountsoftheUnitedStates,BoardofGovernorsoftheFederalReserveSystem,March8,2018).28Althougheffortstodevelopmodern,morecompleteandliquidmarketsforU.S.housingriskareongoing(e.g.,TheCMEHomePriceFuturesandOptions),tradingvolumetodatehasbeensporadicandthin.Pricediscoveryinthehousingmarketisreceivedbypolicymakersandthegeneralpubliclargelyviapasttransactionsdataandpubliclyavailablepriceindices;however,thesedataareinherentlybackward-looking.29Asdescribedinsomedetailonpages9-11),noneoftoday’sheadlineconsumerconfidenceindicesreflectanydirectassessmentofprevailingconditionsintherealestatemarket,expectationsforhomevalues,orothersentimentconcerningthehousingmarket.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|18

WhyTheU.S.HousingConfidenceSurveyandHousingConfidenceIndexareImportant

ThenumberofU.S.housingmarketstakeholdersisenormous;individualstakesaretypicallyverylarge,andhavepractical,economicandemotionaldimensions

• Over130millionhousingunitssheltertheU.S.population,andthevalueofresidentialrealestateintheU.S.heldby

individualsandnonprofitorganizationsisapproaching$30trillion.EvenafterthehistoricU.S.housingbustandrecentgainsinfinancialassets,forthevastmajorityofAmericanhomeowners,residentialrealestateremainstheirsinglelargestasset.30

• Formanyhomeowners,theirhouseisnotonlyashelterandstoreofwealth,itisasourceoffamilyesteemandcivicpride.Formillionsofpeoplewhodonotownthehomethattheylivein,attaininghomeownerstatusremainsahallmarkofachieving“TheAmericanDream”.

• GovernmentsandprivatefinancialinstitutionsaroundtheworldareexposedtotheU.S.housingmarketvia$10.5trillioninmortgageandhomeequitysecurities.31TheU.S.federalgovernmentisthesinglelargeststakeholderinthehousingmarket,anditsstakehasgrownsignificantlysince2008.Thus,currentandfutureU.S.taxpayers–regardlessofhomeownershipstatusorgeographiclocation–haveanindirectbuttangiblestakeinthehealthofhousingmarketsacrossthecountry.

• TheintensityandpersistenceofnovelgovernmentpolicyinitiativesinthewakeofthehistoricU.S.housingbustunderscorethecriticaleconomicimportanceofhealthyhousingmarkets,andtheyhighlighttheneedtomorecarefullymonitortheirconditionandstability.Newinformation,moremodern,proactiveandcompleteriskmanagementinstitutionswillbekeyelementsof21stcenturysolutionsthatmakehousingandmortgagemarketslessvulnerabletofailureandpervasiveemergencygovernmentinterventionsdowntheroad.Systematicmonitorsofhousingconfidencearejustoneinnovationthatcanhelp.

HousingisakeydriveroftheU.S.economy

• HousingcontributessignificantlytoU.S.GDPthroughprivateresidentialinvestment(i.e.,constructionofsingle-familyandmultifamilystructures,manufacturedhomeproduction,residentialremodeling,realestatebrokerfees)andconsumptionspendingonhousingservices(i.e.,grossrentsandutilitiespaidbyrenterhouseholds,andhomeowners'imputedrentsandutilitypayments).Inrecentyears,asapercentageofGDP,thesecomponentshaveaveraged3-5%and12-13%,respectively,foracombinedaverageof15-18%.32

• Morethan12millionprivatesectorjobsaredirectlyorindirectlytiedtotheU.S.housingmarketthroughouttheconstruction,manufacturing,retailtrade,financialandotherserviceindustries.Thisrepresentsalmost9%ofthetotalU.S.laborforce.33

30In2011,TheUnitedStatesCensusBureaureportedaninventoryof132.3millionhousingunitsintheU.S.Thisfigurereflectsbothdetachedandattachedsingle-familyhouses,individualapartmentsinmultifamilystructuresandmobilehomes,occupiedaswellasvacanthomes.TheCensusBureau’s2017AnnualSupplementtoTheCurrentPopulationSurveyestimatesthat126.2millionU.S.householdscomprisearesidentpopulationof325.7millionpeople.ThelatestreadingofaggregateU.S.residentialrealestatevalueis$27.8trillionasofthiswriting(TableB.101,BalanceSheetofHouseholdsandNonprofitOrganizations,FourthQuarter2017FlowofFundsAccountsoftheUnitedStates,BoardofGovernorsoftheFederalReserveSystem,March8,2018).Forcomparison,accordingtotheWorldFederationofExchanges,theaggregatemarketcapitalizationofallU.S.-listedequitieswas$32.1trillionatyear-end2017.31SecuritiesIndustryandFinancialMarketsAssociation(SIFMA)FirstHalf2017SecuritizationReport.The$10.5trillionfigureincludessomeoverlap,assomemortgage-backedsecuritiescollateralizeotherMBS(i.e.,CMOs)andCDOs.32Datathrough2016fromTheU.S.BureauofEconomicAnalysisandTheNationalAssociationofHomeBuilders.332016BureauofLaborStatisticsemploymentdatafortheconstructionindustry,therealestatesubsector,manufacturers(i.e.,furniture,woodproducts,electricalequipmentandappliances),andretailtrade(i.e.,furniture,buildingequipment,gardensupply,electronicsandappliancestores).

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|19

“Housingpricesareviewedbymanyasanimportanteconomicindicator.Infact,muchoftherecentoptimismregardingtheprospectsforamorevigorousrecoveryoftheeconomyisduetoevidencethatthehousingmarketisfirming.”(“FirstImpressionsCanBeMisleading”,FederalReserveBankofNewYork,LibertyStreetEconomics,March2013)

“TheU.S.housingmarket,whichplungedtheeconomyintorecessionfiveyearsagoandwasapersistentdragontherecovery,isnowakeyeconomicdriveratatimewhenothersectorsareslowing.”(TheWallStreetJournal,11/27/2012)

“AdisappointingreboundinU.S.housingcontinuestotripupthecountry’soveralleconomicrecovery,twoinfluentialFederalReserveofficialssaidonFriday,highlightingacorneroftheeconomythatstillfrustratesmonetarypolicymakers.”(Reuters,10/5/2012)

“ItwashousingthatlefttheU.S.economyinshambles.Nowitmaybehousingthatiskeepingitfrombuckling.”(TheWallStreetJournal,9/26/2012)

“Marketsandgovernmentinstitutionsarevisiblystrugglingtorespondconsistentlytoanunprecedentedrashofcrisesandconflicts.Thesestrugglesdiminishconfidence,whichcompoundstheunderlyingeconomicstressesandlowersexpectations.”(RobertShillercommentingonthedimmingoutlookfornationalhomepricesrevealedintheSeptember2011editionofTheHomePriceExpectationsSurvey)

“SomestrikingcontrastsinexpectationsforcumulativechangeinU.S.homepricesthrough2014continuedinJune,andhavepotentiallyprofoundimplications.Thedirectimpactonourforecastsofconsumerspendingandhousingstarts…wouldbehighlysignificant.TheindirecteffectsonGDP,unemployment,inflation,andhencemonetarypolicywouldalsobegame-changing.”(JoelPrakken,ChairmanofMacroeconomicAdvisers,commentingontheresultsoftheJune2010editionofTheHomePriceExpectationsSurvey)

“Thesesmallfirmsconsistentlycreate60to70percentofnewjobs,yearafteryear,andemploymorethanhalfoftheentireU.S.workforceat27milliondifferentplacesofbusiness.”

(Rep.SamGraves(R-Mo),ChairmanoftheHouseSmallBusinessCommittee,“SmallBusinessesDriveJobCreation,Growth”,TheHill.com,July11,2012)

• Actualandexpectedchangesinhomepriceshavecollateraleffectsonbusinessesandconsumers.Changesinactualorimputedhomeequitylevelsthataccompanyactualandexpectedhomevaluechangesimpactcapitalinvestmentbybusinessesandcreditmarketsviathesecollateraleffects,i.e.,tightercreditconditionscanemergeaslendersreacttothreatstotheircapitalfromdecliningcollateralvalues,andvice-versa.Homeequityloansareatraditionalsourceoffundingforpeoplestartingorexpandingasmallbusiness,andsmallbusinessesarethebiggestjobcreatorsintheUnitedStates.Housingcollateraleffectsaretransitoryinnature,butcouldcompoundpowerfulandlonger-lastinghousingwealtheffects(addressednext).Forexample,theCBOhasreportedthat,“Ariseinhomepricescouldhaveashort-livedeffectonconsumerspending,inadditiontothepermanentwealtheffect,ifhigherhomepriceseaseborrowingconstraints,especiallyforyoungerhouseholds.”34

34Equityextraction,ormortgageequitywithdrawal(“MEW”)hasbeenusedbysomeasaproxyformeasuringthetransitoryimpactofhigherhomevaluesonconsumerspending.“HousingWealthandConsumerSpending”(CongressionalBudgetOfficeBackgroundPaper,January2007)describesastrongnegativecorrelationbetweenMEWandthepersonalsavingrate.FormoreinformationonMEWandwealtheffects,seeAlanGreenspanandJamesKennedy,“SourcesandUsesofEquityExtractedfromHomes,”FinanceandEconomicsDiscussionSeriesNo.2007-20(Washington,D.C.:FederalReserveBoard,March2007).

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|20

“Andperhapsmostimportant,homepricesarefinallyrisinginmuchofthecountry.Thatismakingiteasierforownerstoborrowagainstthevalueoftheirhomesandforsomeformerly"underwater"borrowerstotakeadvantageoflowinterestratesbyrefinancingtheirmortgagestoreducetheirmonthlypayments.Higherhomepricescanalsohaveapsychologicalimpact,makingownersfeelwealthierandthereforemorelikelytospend.”(TheWallStreetJournal,12/9/2012)

“Morethan97%ofpublic-sectorjobcutsaftertherecessioncamefrombudgetreductionsbystateandlocalgovernments,hithardbyfallingtaxrevenuewhenhousingpricescollapsed.Theirbudgetsarestartingtostabilizeasthehousingmarketrecovers,buttheiremploymentcontinuestoshrinkslowly.”

(“GovernmentPayrollsAreFacingNewPressures”,TheWallStreetJournal,3/24/2013)

“Housingalsomayhelpalleviatecliff-relatedweaknessinotherareasoftheeconomyduringthemonthsahead.Thesituationmightbesomewhatanalogousto2001,whenbusinesseslaid-offworkersandcutbackonspending,buthousinggainedground,helpingtobolsterconsumerspendingandmaketherecessionshortandshallow.”

(TheWallStreetJournal,11/28/2012)

• Localgovernmentemployment,spendingandinvestmentplanscanbedirectlyaffectedbyhousingmarkethealth.StateandlocalgovernmentsacrosstheU.S.employatotalof19.4millionworkers,andamongmunicipalities,propertytaxesareavitalrevenuesource,accountingfor$473billion(morethan70percent)ofthe$666billionintotaltaxrevenuecollectedbylocalgovernmentsacrossthecountryin2015.35Sincepropertytaxratesandrevenuesaredependentonprevailingrealestatevalues,fiscalplanning,spendingandinvestmentamonglocalgovernmentscanbesignificantlyimpactedbyactualorexpectedchangesinhomevalues.

Actualandexpectedchangesinhomevalueshavepowerfulwealtheffects

• PersonalconsumptionexpenditurespropeltheU.Seconomy.36Actualandperceivedhomevaluescanhaveabigimpactonconsumerspendingbehavior–andthusoveralleconomicactivity–duetotheirwealtheffects:whenvaluesincrease,orareexpectedtoincrease,homeownersfeelmorecomfortableandsecureabouttheirwealth,causingthemtospendmore.Importantly,researchconfirmsthathousingwealtheffectsarepowerfulandmorepotentthan

thoseofthestockmarket,andshowsthattherelationshipbetweenhousingmarketwealthandconsumptionissymmetrical.37Inotherwords,whenhousingmarketwealthdecreases,householdconsumptiondecreases,justaswhenhousingmarketwealthincreases,householdconsumptionincreases.

• Housingwealthaccountsforapproximatelytwo-thirdsofthetotalwealthofthemedianhousehold.Accordingto

FederalReservedata,28percent($7.1trillion)ofU.S.housingwealthdisappearedfromconsumerbalancesheetsaftertheU.S.housingbubbleburstmorethanadecadeago.Then,duringtheensuingrecovery(throughQ42017),housingwealthincreased53percent($9.5trillion).38

Assumingthattheelasticityofpersonalconsumptionexpendituresis0.10,thedeclineinhomevaluesduringthebustimpliesthatconsumerspendingwasdrivendown2.8percent,or$280billionlowerperyear;usingthesame0.10elasticityassumptionfortherecoveryyears,theriseinhomevaluesafterthebustimpliesthatconsumerspendingwasdrivenup5.3percent,or$636billionhigherperyear.39

35The19.4millionfigureincludesfull-timeandpart-timeemployees(seeTheUnitedStatesCensusBureau,2016AnnualSurveyofPublicEmploymentandPayroll.Forthelocalgovernmentbudgetdata,seeTheUnitedStatesCensusBureau,StateandLocalGovernmentFinancesSummary:2015).36Personalconsumptionexpenditureshaveaccountedforapproximately68percentofGDPoverthepastdecade(BureauofEconomicAnalysisdatathroughJuly2017).37KarlCase,JohnQuigley,andRobertShiller(January2013),“WealthEffectsRevisited:1975-2012”,NBERWorkingPaper,No.18667.38Baseduponthetotalnominalvalueofrealestateheldbyhouseholdsandnon-profitorganizations;includesalltypesofowner-occupiedhousingincludingfarmhousesandmobilehomes,aswellassecondhomesthatarenotrented,vacanthomesforsale,andvacantland.(TableB.101,BalanceSheetofHouseholdsandNonprofitOrganizations,FlowofFundsAccountsoftheUnitedStates,BoardofGovernorsoftheFederalReserveSystem).39Again,seeKarlCase,JohnQuigley,andRobertShiller(January2013),“WealthEffectsRevisited:1975-2012”,NBERWorkingPaper,No.18667.Inthispaper,theauthorsreportthatestimatesofconsumerspendingelasticityrangefrom0.03to0.18,butthosethatareestimatedwithseparatecoefficientsforupmarketsand

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|21

“Nothing’swreakedquitethehavocontheU.S.economy,andindeedthenationalpsyche,asthesix-yearslideinhomeprices.”

(Barron’s,9/10/2012)

• In2007,TheCongressionalBudgetOffice(CBO)suggestedthatthedecade-longriseinhomepricesfrommid-1997addedasmuchas$460billionperyeartoconsumerspending.40WhilecitingsurveyresearchperformedbyKarlCaseandRobertShillerconcerninglong-termpriceexpectationsamongrecenthomebuyers,inthesamepaper,CBOwrote:

“Thewealtheffectmaybelargerthanthoseestimatesimplyifcurrenthomepricesdonotfullyreflectsomehomeowners’expectationsoffutureprices.Forhomeownerswhoexpect…gainsinthepricesoftheirhomesinthefuture,spendingisincreasednotjustbythetraditionalwealtheffectbutalsobytheimpactofthoseexpectedcapitalgains.Suchhomeownerswillmostlikelyreducetheirspendingiftheexpectedgainsinpricefailtooccur,evenifpricesdonotactuallyfall.”

• Thereis$11.8trillioninU.S.homemortgagedebtoutstandingasofQ32017;withahousingfinancesystembuiltuponalargefoundationoffinancialleverage,homeownernetwealthchanges–andthus,consumptionproclivities–tendtobeamplifiedbyhomevaluechanges.41

downmarketsareconsistentlyabout0.10indownmarkets.Theannualspendingchangeestimatesof$280billionand$636billionwerederivedfromseasonally-adjustedaveragepersonalconsumptionexpendituresfiguresof$10.0trillionduringthebustyears,and$12trillionduringtherecoveryyearsthrough2017,respectively(perTheBureauofEconomicAnalysis).40See“HousingWealthandConsumerSpending,”CongressionalBudgetOfficeBackgroundPaper,January2007.Althoughthereisaconsiderablebodyofresearchconcerninghousingwealtheffects,overtheyears,thestudieshaveyieldedavarietyofconclusionsregardingtheirsizeandtiming.RecentstructuralchangesintheU.S.housingandmortgagefinancemarketswroughtbythehistoricboomandbustinhomepricesislikelytostimulatefurtherstudiesofhousingwealtheffects,includingresearchregardingtheirdegreeofpermanence.41The$11.8trillionfigureincludes$1.3trillionindebtsecuredmymultifamilyhomes.(TableL.217,TotalMortgages,FlowofFundsAccountsoftheUnitedStates,BoardofGovernorsoftheFederalReserveSystem,December7,2017).

“Therecoveryinresidentialconstructionhasbeenhelpful,butnotsufficienttoreversethestructuralheadwindsemanatingfromhousingtothebroadereconomy.However,webelievethatthisisabouttochange.Duringthecourseoflastyear,homepriceshavealsobottomedout,and,moreimportantly,expectationsarenowforfurtherincreases.”

(SocieteGeneraleCrossAssetResearch,2/21/2013)

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|22

“Oneparticipantpointedtoongoingchangesinarangeoffactors—includingdemographics,creditconditions,businessmodels,andconsumerpreferences—thatwerelikelyshiftingbothsupplyanddemandinthehousingsectorandconcludedthattheoutlookforthesectorwasquiteuncertainandpotentiallysubjecttorapidchanges.”

(ExcerptfromMinutesoftheFederalOpenMarketCommittee,March19-20,2013)

TheU.S.housingmarkethasenteredanew,historicallyvolatileera

DemographicshiftsandanunfamiliarconfluenceofmacroeconomicforcesleftinthewakeofthehistoricU.S.housingboomandbustareexacerbatingrealestatemarketvolatility,e.g.,• Increasinglylargenumbersofbabyboomer-homeownersarein,orareapproaching,theirretirementyears.42

• Recordandgrowinglevelsofstudentloandebthaveimpairedtheabilityofyoungadultstosavemoneyforahome

downpayment,impedingnewhouseholdformations.About43millionAmericanscurrentlyowealmost$1.4trillioninfederalstudentdebt,thehighestformofconsumerdebtintheU.S.excludingmortgages.43

• Institutionallandlordshaveaccumulatedmillionsofsingle-familyhomesandconvertedthemtorentalproperties,constrainingthesupplyofhomesthatwouldotherwisebeavailableforsaletofirst-timehomebuyers.44

• Unprecedentedcrisis-eramonetarystimulusprogramsarebeingslowlyunwound,andtheU.S.housingfinancesystemremainssubjecttosignificantreforms.

• Despiterecentpriceincreases,millionsofhomeownersstillowemoreontheirmortgagesthantheirhomesareworth.Somemarketobserversbelievethatthehistorichousingmeltdownandcreditcrisispermanentlyalteredthepsychologyofhomeownersandrentersalike.45

• Whilethe4.1percentnationalunemploymentrateinJanuary2018markeda17-yearlow,at62.7percent,thelaborforceparticipationrateremainsdepressednineyearsintotheeconomicrecovery,andismorethanfourpointslowerthanthehistoricalpeak.46

• The2017overhaulofthefederaltaxcodewillalterhomeownershipincentivesbycurtailingdeductionsformortgageinterestandpropertytaxes.

Theseandotherseminal,post-bustconcernsillustrateemergentdimensionsofhousingmarketriskthattraditionalrealestatedatasetsdonotmeasure,andthatlegacyriskmodelswillstruggletopredict.Theseissuesandthesystemicfailuresthatcontributedtotheepichousingbustandmortgagemarketmeltdownalsounderscorethemeritofevaluatingnewdatasetsandmodelsthatcanbebetter-calibratedtoeffectivelymeasureimportanthousingandmortgagemarketrisksinthe21stcentury.

42Babyboomers–agenerationabout90percentlargerthanGenerationX–areretiringatarecordrate.Inthecomingyears,inordertodownsizeand/orfundtheirretirement,increasingnumbersofboomersmayseektoselltheirhomestomembersofyoungergenerationswhoseviewsofhomeownershipmaybelessfavorableoverallrelativetothoseoftheirparentsandgrandparents.43“U.S.Student-LoanProgramLosingMoneyasBorrowersSeekDebtForgiveness”,TheWallStreetJournal,February2,2018.44Institutionalinvestorsexecuting“buy-to-rent”strategiesfacilitatedareductionofdistressedhomeinventoriesandhelpedtostabilizepricesduringthebust,buttheyalsocrowded-outindividualhomebuyers,especiallyfirst-timersunabletocompetewithaggressiveall-cashbids.Homeportfoliosheldbyinstitutionalinvestorstendtobeconcentratedgeographically,sotheeventualliquidationofthesepropertyportfolioscouldintroducenewhousingmarketrisksandheightenedvolatilityinthefuture.Foracogentoverviewofbusinessinvestorhomepurchaseactivity,itsbenefitsandpotentialrisks,seeFEDSNotes,“BusinessInvestorActivityintheSingle-Family-HousingMarket”,December5,2013.45CoreLogicestimatedthatthetotalnumberofmortgagedresidentialpropertieswithnegativeequitywas2.5millionhomes,or4.9percentofallmortgagedpropertiesasofQ32017.46BureauofLaborStatistics.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|23

“U.S.stocksrosetoarecordhighfollowingstronghousingandconsumer-confidencedata…SurginghousepricesfueledthelargestselloffinU.S.Treasurybondsin10months,signalinggrowinginvestoroptimismabouttheeconomy.”

(TheWallStreetJournal,5/29/2013)“Homepricesjumped10.2%inFebruarycomparedwithayearearlier,thebiggestriseinnearlysevenyears…Thathasgottheattentionofinvestorswhowantinontheaction.”

(“What’stheBestPathtoReal-EstateProfits?”Barron’s,April15,2013)

AuthoritativeU.S.housingandconsumerconfidencedatacanmovefinancialmarkets

Publicaccesstoandmediainterestinhousingdatahaveswelledduringthepastdecade.Formanyofthereasonsdescribedelsewherewithinthisdocument,authoritativeU.S.homedatacanhavesignificantandimmediateeffectsonfinancialmarkets–evensuchdatathatareinherentlybackward-lookingandreportedonalaggedbasis.

Thedegreeofaconsumer’sconfidenceaffectshis/hereconomicdecisions(e.g.,theamountofincometospendandsave),andhaslongbeenconsideredakeyindicatorofmacroeconomichealth.Muchlikeimportanthousingdata,authoritativemeasuresofconsumerconfidenceintheU.S.arewidelyanticipated,closelymonitored,andcangenerateheadlinesfollowingtheirpublicreleaseduetotheirimpactonfinancialmarkets.

TheU.S.HousingConfidenceSurveyandIndex Overview

Page|24

“OnthemorningofMarch15,stocksstumbledonnewsthatakeyreadingofconsumerconfidencewasunexpectedlylow.”

(TheWallStreetJournal,6/13/2013)

“Inthemostrecentboom,payinghighpricesrequiredanoptimisticassessmentoffuturepricegrowth.Risingpricesaremoststronglyassociatedwithoptimisticexpectations,andcreditmarketconditions…playedasupportingrole.”

(Excerptfrom“ANationofGamblers”,byEdwardGlaeser,NBER,January2013)

TheU.S.HousingConfidenceSurveyDeliversUnique,Forward-lookingInsightsHCSandHCIaredifferentinfundamentalwaysfromotherrealestatesurveys,homepriceandeconomicconfidenceindices.HCSisuniqueamongallconsumerhousingandeconomicconfidencesurveysbecauseitistheonlyonethatdoesallofthefollowing:

• Systematicallymeasureshousingconfidencenationallyandinindividualmetropolitanareamarkets.

• Gaugesattitudesconcerninghomeownershipandprevailingmarketconditionsamongallhouseholdtypes,andseparately,forhomeownersandrenters.

• Measureshomevalueexpectationsforbothshort-termandlong-termhorizons.

• Quantifies,analyzes,andtracksimportanthouseholdattitudesbytenurecategoryandkeydemographicvariables.

• ViaHCI,enablesconsistentandconcisereportingofprevailinghouseholdattitudesforeasypublicconsumption,comprehension,andtrackingovertime.

_____________________________________________________________________________________________________