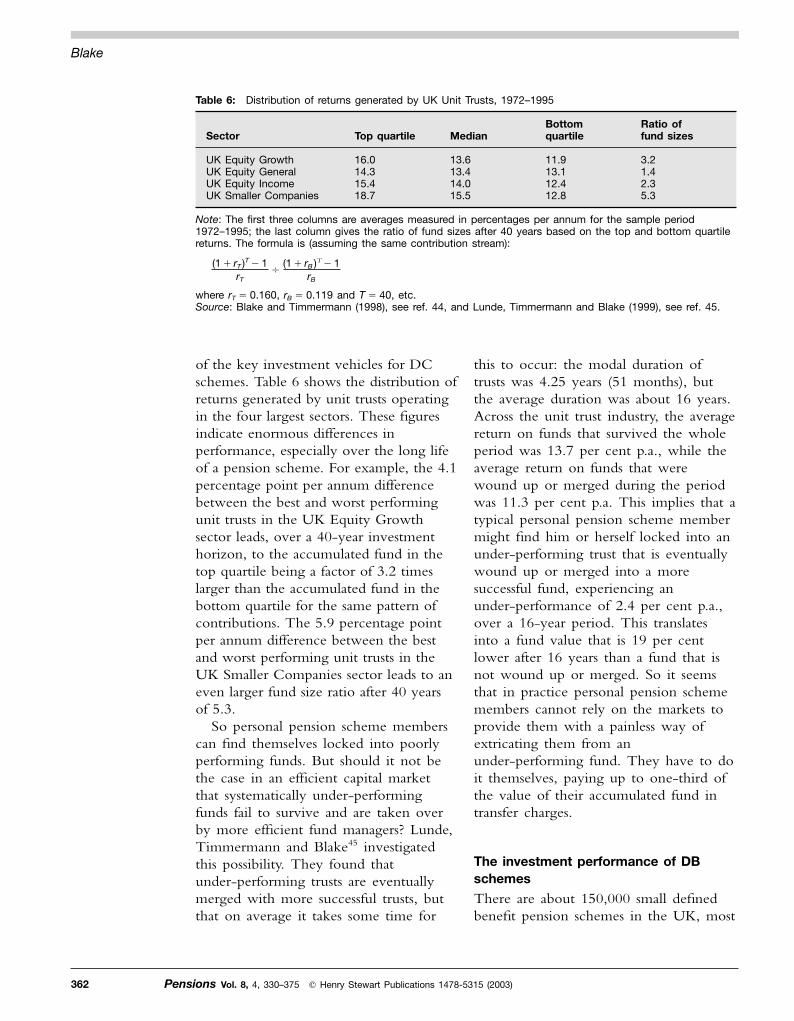

The UK pension system: Key issues - Springer [email protected]. scheme or to a personal or...

46

elsewhere in Europe and its governments have taken measures to prevent a pension crisis developing. These measures have involved making systematic cuts in unfunded state pension provision, and increasingly transferring the burden of providing pensions to the funded private sector. The UK is not entitled to be complacent, however, since there remain some serious and unresolved problems with the different types of private sector provision. The current system of pension provision A flat-rate first-tier pension is provided by the state and is known as the basic state pension (BSP). Second-tier or Introduction The UK was one of the first countries in the world to develop formal private pension arrangements (beginning in the 18th century) and was also one of the first to begin the process of reducing systematically unfunded state provision in favour of funded private provision (beginning in 1980). This explains why the UK is one of the few countries in Europe that is not facing a serious pensions crisis. The reasons for this are straightforward: state pensions (both in terms of the replacement ratio and as a proportion of average earnings) are among the lowest in Europe, the UK has a long-standing funded private pension sector, its population is ageing less rapidly than 330 Pensions Vol. 8, 4, 330–375 Henry Stewart Publications 1478-5315 (2003) The UK pension system: Key issues Received (in revised form): 9th April, 2003 David Blake is Professor of Financial Economics at Birkbeck College in the University of London and Chairman of Square Mile Consultants, a training and research consultancy. He is Senior Research Associate, Financial Markets Group, London School of Economics; Senior Consultant, UBS Pensions Research Centre, London School of Economics; Research Associate, Centre for Risk & Insurance Studies, University of Nottingham Business School; formerly Director of the Securities Industry Programme at City University Business School and Research Fellow at both the London Business School and the London School of Economics. He was a student at the London School of Economics in the 1970s and early 1980s, gaining his PhD on UK pension fund investment behaviour in 1986. In June 1996, he established the Pensions Institute at Birkbeck College (www.pensions-institute.org). Abstract This paper examines the key issues relating to the UK pension system. It reviews the current system of pension provision, describes and analyses the reforms since 1980; examines the legal, regulatory, and accounting framework for occupational pension schemes; assesses the different types of risks and returns from membership of defined benefit and defined contribution pension schemes; and investigates the management and investment performance of pension fund assets. The paper ends with a discussion of the review of institutional investment in the UK conducted by Paul Myners and published in March 2001. Keywords: UK pension system; pension reforms; state pensions; private pensions; defined benefit; defined contribution; pension fund management; investment performance; Myners review of institutional investment David Blake Pensions Institute, Birkbeck College, University of London, Gresse St, London W1T 1LL, UK. Tel: 44 (0)20 7631 6410; Fax: 44 (0)20 7631 6403; E-mail: [email protected]

Transcript of The UK pension system: Key issues - Springer [email protected]. scheme or to a personal or...

elsewhere in Europe and its governmentshave taken measures to prevent apension crisis developing. These measureshave involved making systematic cuts inunfunded state pension provision, andincreasingly transferring the burden ofproviding pensions to the funded privatesector. The UK is not entitled to becomplacent, however, since there remainsome serious and unresolved problemswith the different types of private sectorprovision.

The current system of pensionprovisionA flat-rate first-tier pension is providedby the state and is known as the basicstate pension (BSP). Second-tier or

IntroductionThe UK was one of the first countries inthe world to develop formal privatepension arrangements (beginning in the18th century) and was also one of thefirst to begin the process of reducingsystematically unfunded state provision infavour of funded private provision(beginning in 1980).

This explains why the UK is one ofthe few countries in Europe that is notfacing a serious pensions crisis. Thereasons for this are straightforward: statepensions (both in terms of thereplacement ratio and as a proportion ofaverage earnings) are among the lowestin Europe, the UK has a long-standingfunded private pension sector, itspopulation is ageing less rapidly than

330 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

The UK pension system:Key issuesReceived (in revised form): 9th April, 2003

David Blakeis Professor of Financial Economics at Birkbeck College in the University of London and Chairman of Square MileConsultants, a training and research consultancy. He is Senior Research Associate, Financial Markets Group, London Schoolof Economics; Senior Consultant, UBS Pensions Research Centre, London School of Economics; Research Associate, Centrefor Risk & Insurance Studies, University of Nottingham Business School; formerly Director of the Securities IndustryProgramme at City University Business School and Research Fellow at both the London Business School and the LondonSchool of Economics. He was a student at the London School of Economics in the 1970s and early 1980s, gaining his PhDon UK pension fund investment behaviour in 1986. In June 1996, he established the Pensions Institute at Birkbeck College(www.pensions-institute.org).

Abstract This paper examines the key issues relating to the UK pension system. Itreviews the current system of pension provision, describes and analyses the reformssince 1980; examines the legal, regulatory, and accounting framework for occupationalpension schemes; assesses the different types of risks and returns from membership ofdefined benefit and defined contribution pension schemes; and investigates themanagement and investment performance of pension fund assets. The paper ends witha discussion of the review of institutional investment in the UK conducted by PaulMyners and published in March 2001.

Keywords: UK pension system; pension reforms; state pensions; private pensions;defined benefit; defined contribution; pension fund management; investmentperformance; Myners review of institutional investment

David BlakePensions Institute,Birkbeck College,University of London,Gresse St,London W1T 1LL,UK.

Tel: �44 (0)20 7631 6410;Fax: �44 (0)20 7631 6403;E-mail: [email protected]

scheme or to a personal or stakeholderpension scheme that has been contractedout of S2P. In such cases both theindividual and the employer contractingout receive a rebate on their NICs (1.6per cent of earnings for the employeeand 3.5 per cent for the employer, unlessit operates a contracted-outmoney-purchase scheme (COMPS), inwhich case the employer rebate is 1.0per cent)6 and the individual foregoes theright to receive a S2P pension. However,there is no obligation on employers tooperate their own pension scheme, nor,since 1988, is there any contractualrequirement for an employee to join theemployer’s scheme if it has one.

There is a wide range of private sectorpension schemes open to individuals.They can join their employer’soccupational pension scheme (if it hasone), which can be any one of thefollowing:

— contracted-in salary-related scheme(CISRS)

— contracted-in money-purchase scheme(CIMPS)

— contracted-out salary-related scheme(COSRS)

— contracted-out money-purchasescheme (COMPS)

— contracted-out mixed-benefit scheme(COMBS)

— contracted-out hybrid scheme(COHS).

A CISRS is a defined benefit (DB)scheme that has not been contracted outof S2P and so provides a salary-relatedpension in addition to the S2P pension.A CIMPS provides a definedcontribution supplement to the S2Ppension. A COSRS must satisfy a‘reference scheme test’ in order tocontract out of S2P, namely provide apension for life from age 65 which isindexed to inflation up to a maximum of

supplementary pensions are provided bythe state, employers and private sectorfinancial institutions, the so-called threepillars of support in old age. The mainchoices are between: a state system thatoffers a pension that is low relative toaverage earnings, but which is fullyindexed to prices after retirement; anoccupational system that offers arelatively high level of pension (partiallyindexed to prices after retirement up to amaximum of 5 per cent p.a.), but, as aresult of poor transfer values betweenschemes on changing jobs, only toworkers who spend most of theirworking lives with the same company;and a personal pension system that offersfully portable (and partially indexed)pensions, but these are based onuncertain investment returns and aresubject to very high set-up andadministration charges, ofteninappropriate sales tactics, and very lowpaid-up values if contributions into theplans lapse prematurely.

Employees in the UK in receipt ofearnings subject to National Insurancecontributions (NICs) will build upentitlement1 both to the BSP2 and, on‘band earnings’ between the lowerearnings limit (LEL) and the upperearnings limit (UEL),3 to the pensionprovided by the State Second PensionScheme (S2P); S2P was introduced inApril 2002, and replaced theState-Earnings-Related Pension Scheme(SERPS), which was introduced in 1978.These pensions are paid by theDepartment of Work and Pensions(DWP) (formerly the Department ofSocial Security (DSS))4 from StatePension Age which is 65 for men and 60for women.5 The self-employed are alsoentitled to a BSP, but not to a S2Ppension. Employees with earnings inexcess of the LEL will automatically bemembers of S2P, unless they belong toan employer’s occupational pension

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 331

The UK pension system: Key issues

schemes, but with lower unit costsbecause of the savings on up-frontmarketing and administration costs. ASPS is a low-cost PPS with chargescapped at 1 per cent p.a. of the fundvalue and into which contributions of upto £3,600 p.a. can be made irrespectiveof whether the SPS member has madeany net relevant earnings during theyear.7

In 1996, the UK workforce totalled28.5m people, of whom 3.3m wereself-employed.8 The pension arrangementsof these people were as follows:9

— 7.5m employees in SERPS (now S2P)— 1.2m employees in 110,000

contracted-in occupational schemes— 9.3m employees in 40,000

contracted-out occupational schemes(85 per cent of such schemes aresalary-related, although 85 per cent ofnew schemes started in 1998 weremoney purchase or hybrid)

— 5.5m employees in personal pensionschemes

— 1.7m employees without a pensionscheme apart from the BSP

— 1.5m self-employed in personalpension schemes

— 1.8m self-employed without a pensionscheme apart from the BSP.

These figures indicate that 72 per cent ofsupplementary pension scheme membersin 1996 were in SERPS or anoccupational scheme and 28 per centwere in PPSs.10

Table 1 shows the sources ofretirement income in 1997-98. A singleperson had total retirement incomeaveraging 43 per cent of national averageearnings (NAE). Nearly two-thirds ofthis came from state benefits and anotherquarter came from occupational pensions:personal pensions provided only about 5per cent of total retirement income forthe average person.11

5 per cent p.a. where the startingpension is calculated by taking aminimum of 1/80th of the average salaryover the three years prior to retirementfor each year of service in the scheme upto a maximum of 40 years’ service. ACOMPS must have contributions nolower than the contracted-out rebate. ACOMBS can use a mixture of thereference scheme test and the minimumcontributions test to contract out of S2P,while a COHS can provide pensionsusing a combination of salary-related andmoney purchase elements. Individualscan also top up their schemes withadditional voluntary contributions (AVCs)or free-standing additional voluntarycontributions (FSAVCs) up to limitspermitted by the Inland Revenue.

As an alternative, individuals have thefollowing individual pension choices thatare independent of the employer’sscheme:

— personal pension scheme (PPS)— group personal pension scheme

(GPPS)— stakeholder pension scheme (SPS).

A PPS is divided into two components.The first is an appropriate personalpension scheme (APPS) which iscontracted out of S2P and provides‘protected rights’ benefits that stand inplace of S2P benefits: they are alsoknown as minimum contribution orrebate-only schemes since the onlycontributions permitted are the combinedrebate on NICs with the employee’sshare of the rebate grossed up for basicrate tax relief (at 22 per cent). Thesecond is an additional scheme, alsocontracted out, that receives anyadditional contributions up to InlandRevenue limits. A GPPS is a schemethat has been arranged by a smallemployer with only a few employees: itis essentially a collection of individual

332 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

(b) the spouse’s pension was cut from100 per cent of the member’spension to 50 per cent fromOctober 2001 (Social Security Act1986);

(c) the revaluation factor for bandearnings was reduced by about 2per cent p.a. (Pensions Act 1995);the combined effect of all thesechanges was to reduce the value ofSERPS benefits by aroundtwo-thirds.

4 Provided a ‘special bonus’ in the formof an extra 2 per cent NationalInsurance rebate for all PPSscontracting out of SERPS betweenApril 1988 and April 1993 (SocialSecurity Act 1986); provided anincentive between April 1993 andApril 1997 in the form of a 1 per centage-related National Insurance rebateto members of contracted-out PPSsaged 30 or more to discourage themfrom recontracting back into SERPS;age-related National Insurance rebatescontinued in a revised form after April1997 (Social Security Act 1993).

5 Relaxed the restriction on PPSs thatan annuity had to be purchased on theretirement date, by introducing anincome drawdown facility whichenabled an income (of between 35 and100 per cent of a single life annuity)to be drawn from the pension fund

The reforms since 1980

Thatcher-Major reforms to the pensionsystem

The Thatcher Conservative Governmentthat came into power in 1979 becamethe first government in the developedworld to confront head on the potentialcrisis in state pension provision. Thereforms were continued by thesucceeding Major Government. TheseGovernments introduced measures whichdid the following.

1 Linked the growth rate in statepensions to prices rather than NAE,thereby saving about 2 per cent p.a.(Social Security Act 1980).

2 Raised the state pension age from 60to 65 for women over a ten-yearperiod beginning in 2010, therebyreducing the cost of state pensions by£3bn p.a. (Pensions Act 1995).

3 Reduced the benefits accruing underSERPS (which had only been set upin 1978) in a number of ways:

(a) the pension was to be reduced(over a ten-year transitional periodbeginning in April 1999) from 25per cent of average revalued bandearnings over the best 20 years to20 per cent of average revaluedband earnings over the full career(Social Security Act 1986);

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 333

The UK pension system: Key issues

Table 1: Sources of retirement income in 1997–1998

Source

Single person Married couples

£per week % of total % of NAE £per week % of total % of NAE

State benefitsa

Occupational pensionsInvestment incomeb

Earningsc

Total

9533147

149

642295

100

271042

43

133904833

304

44301611

100

3826149

87

Notes: aIncludes incapacity benefit, housing benefit, council tax benefit etc; bIncludes income from personalpensions; cWomen in the age range 60-65 and men in the age range 65–70.Source: Department of Social Security (2000), see ref. 9.

Defects in the Thatcher-Major reforms

The main defects of the Thatcher-Majorreforms were as follows.

1 Removing the requirement thatmembership of an occupationalpension scheme could be made acondition of employment. Membershipwas made voluntary and newemployees had to take the activedecision of joining their employer’sscheme: barely more than 50 per centof them did so.

2 No requirement to ensure thattransferring from an occupational to apersonal pension scheme was in thebest interests of the employee, leadingdirectly to the personal pensionsmis-selling scandal that erupted inDecember 1993. Between 1988 and1993, 500,000 members ofoccupational pension schemes hadtransferred their assets to personalpension schemes following highpressure sales tactics by agents of PPSproviders. As many as 90 per cent ofthose who transferred had been giveninappropriate advice. Miners, teachers,nurses and police officers were amongthe main targets of the sales agents.Many of these people remainedworking for the same employer, butthey switched from a goodoccupational pension scheme offeringan index-linked pension into a PPStowards which the employer did notcontribute and which took 25 percent of the transfer value incommissions and administrationcharges. An example reported in thepress concerned a miner whotransferred to a PPS in 1989 andretired in 1994 aged 60. He receiveda lump sum of £2,576 and a pensionof £734 by his new scheme. Had heremained in his occupational scheme,he would have received a lump sumof £5,125 and a pension of £1,791.

(which otherwise remains invested inearning assets) and delaying theobligation to purchase an annuity untilage 75 (Finance Act 1995).

6 Enabled members of occupationalpension schemes to join personalpension schemes (Social Security Act1986).

7 Simplified the arrangements foroccupational schemes to contract outof SERPS by abolishing therequirement for occupational schemesto provide guaranteed minimumpensions (GMPs): since April 1997,COSRSs had to demonstrate only thatthey satisfy the reference scheme test(Pensions Act 1995).

8 Ended its commitment to pay for partof the inflation indexation ofoccupational schemes (Pensions Act1995). Until April 1997, COSRSs hadto index the GMP up to an inflationlevel of 3 per cent p.a. and anyadditional pension above the GMP upto an inflation level of 5 per cent p.a.Since the GMP replaced the SERPSpension which was itself fully indexedto inflation, the Government increasedan individual’s state pension tocompensate for any inflation on theGMP above 3 per cent p.a. But the1995 Act abolished the GMPaltogether and required COSRSs toindex the whole of the pension thatthey pay up to a maximum of 5 percent p.a. (this is known as limitedprice indexation).

9 Improved the security of the assets inprivate sector schemes through thecreation of the Occupational PensionsRegulatory Authority (Opra), acompensation fund operated by thePension Compensation Board (PCB), aminimum funding requirement (MFR)and a Statement of InvestmentPrinciples (SIP) (Pensions Act 1995);Opra, the PCB and the MFR areexamined in more detail below.

334 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

pensions’ (December 1998) turned out tobe much less radical than initiallyanticipated, but nevertheless continuedwith the Thatcher Government’s agendaof attempting to reduce the cost to thestate of public pension provision, and oftransferring the burden of provision to theprivate sector through the introduction ofSPSs.

Nevertheless, there was much greateremphasis on redistributing resources topoorer members of society than was thecase with the Conservatives. Shortly afterthe publication of the Green Paper, theTreasury issued a consultation documenton the type of investment vehicles inwhich stakeholder pension contributionsmight be invested. These proposals willbe examined in turn.

The DSS proposals

The key objectives of the DSS GreenPaper were as follows:

1 Reduce the complexity of the UKpension system, by abolishing SERPS.

2 Introduce a minimum incomeguarantee in retirement linked toincreases in national average earningson the grounds that people who workall their lives should not have to relyon means-tested benefits in retirement;the first-tier BSP will remain indexedto prices, however, and over time willbecome a relatively unimportantcomponent of most people’s pensions.

3 Provide more state help for those whocannot save for retirement, eg thelow-paid (those on less than halfmedian earnings), carers and thedisabled, via the unfunded state system.

4 Encourage those who are able to savewhat they can for retirement, viaaffordable and secure second pillarpensions:

— provided by the state for those onmodest incomes (via a new

As a result of a public outcry, PPSproviders have had to compensatethose who had been giveninappropriate advice to the tune of£13.5bn.

3 No restriction on the charges thatcould be imposed in personal pensionplans, hoping that market forces alonewould ensure that PPSs werecompetitively provided.

4 Giving personal pension schememembers the right to recontract backinto SERPS. This option has turnedout to be extremely expensive for theGovernment because of theback-loading of benefits in DB pensionschemes such as SERPS: benefits accruemore heavily in the later years than theearlier years.12 Despite the financialincentives given to contract out ofSERPS into PPSs, it turned out to beadvantageous for men over 42 andwomen over 34 to contract back intoSERPS once the period of the specialbonus had ended in 1993. Todiscourage this from happening thegovernment has been forced to offeradditional age-related rebates to PPSmembers since 1993. Far from savingthe Government money, the net cost ofPPSs during the first ten years wasestimated by the National Audit Officeto be about £10bn.

The Blair reforms to the pension system

The Blair New Labour Government cameinto power in 1997 with a radical agendafor reforming the welfare state. In theevent, Frank Field, appointed the firstMinister for Welfare Reform at theDepartment of Social Security (DSS) andcharged with the objective of ‘thinkingthe unthinkable’, proved to be too radicalfor the traditional Old Labour wing of theLabour Party and was soon replaced. Theeventual DSS Green Paper proposals ‘Anew contract for welfare: Partnership in

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 335

The UK pension system: Key issues

— modernise the system, by abolishingthe weekly means-test, and movingmore into line with the tax systemwhich is based on an annual cycle,thus paving the way for further taxand benefit integration in the future.

SERPS was replaced by a new S2P inApril 2002: the S2P was initiallyearnings-related but from April 2007becomes a flat-rate benefit, even thoughcontributions are earnings-related, afeature that is intended to provide strongincentives for middle- and high-incomeearners to contract out. The S2P:

— ensures that everyone with acomplete work record receivescombined pensions above the MIG

— gives the low paid earning below£9,500 p.a. twice the SERPS pensionat £9,500 p.a. (implying that theaccrual rate is 40 per cent of £9,500rather than the 20 per cent underSERPS)

— gives a higher benefit than SERPSbetween £9,500 and £21,600 p.a.(average earnings in 1999)

— leaves those earning over £21,600p.a. unaffected (with an accrual rate of20 per cent)

— uprates these thresholds in line withnational average earnings

— provides credits for carers (includingparents with children under 5) andthe disabled.

Stakeholder pensions

New SPSs were introduced in April2001, but are principally intended formiddle-income earners(£9,500–£21,600) with no existingprivate pension provision. They can beused to contract out of S2P.

They are collective arrangements,provided by:

— an employer

unfunded state second pension), and— provided by the private sector for

middle- and high-income earners,with the option of new low-costdefined contribution stakeholderpensions which are likely to replacehigh-cost personal pensions. Butthere will be no extra compulsionto save for retirement at the secondpillar and no additional incentivesover those already existing at thesecond pillar.

The Green Paper proposals formed thebasis of the Welfare Reform and PensionsAct which received the Royal Assent inNovember 1999. The Act deals withfollowing issues.

State pensions

A minimum income guarantee (MIG) of£75 per week was introduced forpensioners in April 1999: it ismeans-tested on a weekly basis (andtapers off if the claimant’s capital exceedsa specified limit) and is indexed toearnings. The MIG significantly increasedthe benefit income of the poorestpensioners, creating a new, higherincome threshold below whichpensioners with no or little savingsshould not fall.

In October 2003, the Governmentintroduced the pension credit (PC),13 theaim of which is not just to end thepenalty on savings, but, for the first time,to reward savings. The PC, which isuntaxed, is designed to make up thedifference between the income apensioner receives from all existingsources (including private pensions andsavings) and the MIG. The PC will:

— reward work and savings inretirement, by abolishing the capitallimits and introducing a cash rewardfor modest savings, earnings orsecond-tier pensions;

336 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

occupational DC plans will attract taxrelief on contributions up to a maximumof 17.5 per cent of earnings (below age36), rising to 40 per cent (above age 61).But contributions up to £3,600 p.a. canbe made into any DC plan regardless ofthe size of net relevant earnings.Contributions in excess of £3,600 p.a.may continue for up to 5 years afterrelevant earnings have ceased. Thereafter,contributions may not exceed £3,600p.a. All contributions into DC plans willbe made net of basic rate tax, withproviders recovering the tax from theInland Revenue and with higher ratetax, if any, being recovered in theself-assessment tax return.

Occupational pensions

Occupational schemes can contract outof the S2P. Employers can again makemembership of an occupational scheme acondition of employment, and employeesare only allowed to opt out if they havesigned a statement of rights being givenup, certified that they have adequatealternative provision, and have takenadvice that confirms that the alternativeis at least as good as the S2P.

The compensation scheme establishedby the 1995 Pensions Act was extendedto cover 100 per cent of the liabilities ofpensioners and those within ten years ofnormal pension age (NPA).

Personal pensions

PPSs can contract out of the S2P. Theyreceive protection in cases of thebankruptcy of the member.

HM Treasury proposals

The Treasury proposals were containedin ‘Helping to Deliver StakeholderPensions: Flexibility in PensionInvestment’ (February 1999). They calledfor the introduction of more flexibleinvestment vehicles for managing pensioncontributions, not only those in the new

— a representative or membership oraffinity organisation, or

— a financial services company.

They are defined contribution (DC)schemes, with the same restrictions as forpersonal pensions, namely that on theretirement date up to 25 per cent of theaccumulated fund may be taken as atax-free lump sum, the remaining fundmay be used to buy an annuity or toprovide a pension income by way of adrawdown facility until age 75 when anannuity must be purchased with theremaining assets.

They have to meet minimumstandards, known as CAT marks (forcharges-access-terms) concerning:

— the charging structure and level ofcharges (a maximum of 1 per cent offund value)

— levels of contractual minimumcontributions (£20)

— contribution flexibility andtransferability (no penalties ifcontributions cease temporarily (up tofive years) or if the fund is transferredto another provider).

The main provisions of the Pensions Act1995 apply to SPSs, covering the annualreport and accounts, the appointment ofprofessional advisers and the Statement ofInvestment Principles.

They are regulated principally byOpra, although the selling of schemesand the supervision of their investmentmanagers is regulated by the FinancialServices Authority (FSA), with thePensions Ombudsman for redress.Employers without an occupationalscheme and with at least five staff mustoffer access to one ‘nominated’ SPS andto provide a payroll deduction facility.

There is a new integrated tax regimefor all defined contribution pension plans.SPSs, personal pension plans and

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 337

The UK pension system: Key issues

to earnings. Now the Governmentexplicitly rejected this on the grounds ofboth cost14 and the fact that it wouldbenefit the high-paid as well as thelow-paid, whereas the Government’semphasis was on helping the low-paid.But the problem with keeping the BSPlinked to prices rather than to earnings isthat it will continue to fall relentlessly asa proportion of NAE: it is currently just17 per cent of NAE and will fall to wellbelow 10 per cent by 2025. While theGovernment admits that this will savesubstantial sums of money, it implies theGovernment is effectively abandoning thefirst pillar of support in old age andobliging everyone to rely on the secondand third pillars. The Green Paper talkedabout building on the BSP, but thisimplies building on a sinking ship.

If the Government is genuinelyconcerned about security at theminimum level for all, it should considerfunding the first pillar appropriately byestablishing an explicit fund (like theSocial Security Trust Fund (SSTF) in theUSA) into which it places the NICs ofthose who are in work, while theGovernment itself funds the contributionsof the low-paid, carers and thedisabled.15 The contribution rate couldbe actuarially set to deliver the MIG forall when they retire. It could be ahypothecated part of NICs. In otherwords, the contributions would accrue‘interest’ equal to the growth rate inNAE. The state could explicitly issueNAE-indexed bonds which the SSTFwould buy. This is the only honest wayboth of preserving the value of andhonouring the promises under the firstpillar. The second and third pillars couldthen be formally integrated with the firstpillar, ie the second pillar is used todeliver the tranche of pension betweenthe MIG and the Inland Revenue limits,while the third pillar is used forvoluntary arrangements above the Inland

stakeholder pension schemes, but alsothose in occupational and personalpension schemes. These investmentvehicles were given the name individualpension accounts (IPAs). The main IPAsare authorised unit trusts (AUTs oropen-ended mutual funds), investmenttrust companies (ITCs or closed-endedmutual funds), and open-endedinvestment companies (OEICs).

In comparison with the individualarrangements of existing personal pensionschemes and the poor transferability ofoccupational pension schemes, IPAs offer:

— lower charges: since collectiveinvestment vehicles have much loweroverheads than individual investments;

— greater flexibility: since IPAs are easyto value and transfer betweendifferent stakeholder, personal andoccupational pension schemes,allowing employees to move jobswithout having to change pensionschemes, thereby encouraging greaterlabour market flexibility.

Assessment of the Blair reforms

The Welfare Reform and Pensions Act,while containing some significantimprovements on the existing system,does not fully meet the Green Paper’sown objectives.

Reforms to state pensions

While the abolition of SERPS helped tosimplify the UK’s extremely complexpension system, the proposal to have aMIG (of £75 per week) that differedfrom the BSP (£67.50 per week at thetime) reintroduced substantial complexityat the starting point for state pensionprovision, especially when the differencebetween the two amounts (£7.50 perweek) was initially so small. It wouldhave been far simpler to set the MIGequal to the BSP and to link the latter

338 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

per cent p.a. and rose to as much as 2.2per cent p.a. of fund value for 25-yearpolicies18 are much higher than the 1 percent p.a. CAT-marked limit on SPSs.There may be a range of providers ofSPS to begin with, but the only way fora provider to survive in the long runwill be if it operates at low unit cost ona large scale. This will inevitably lead tomergers among providers and a finalequilibrium with a small number of verylarge providers.

Existing personal pension providersand distribution channels face thesechallenges:

— APPSs face massive competition fromSPSs for future NIC rebates

— SPSs could be better than PPSs formiddle-income groups, leaving PPSsas a choice only for those on highincomes who require and are willingto pay for a bespoke product

— new affinity-based SPSs with gatewayorganisations linking up with pensionproviders (eg AmalgamatedEngineering & Electrical Union with720,000 members and FriendsProvident)

— the Treasury’s proposed PPIs providea low-cost alternative investmentvehicle to the high-cost managedfunds of most PPSs

— Individual savings accounts (ISAs),introduced by the Treasury in April1999 to encourage greater personalsector savings, also provide animportant alternative to PPSs.Contributions into ISAs of up to£5,000 per annum are permitted, andthe investment returns are free fromincome and capital gains tax. Whilenot intended as pension savingsvehicles (they do not attract tax reliefon contributions, for example, unlikestandard pension savings products),ISAs can be used in retirementincome planning, since they enjoy the

Revenue limits. If the first pillar remainsunfunded, there is nothing to preventfuture generations reneging on anagreement which they are expected tokeep but did not voluntarily enter into.

The fact that membership of pensionschemes at the second pillar remainsvoluntary, is highly worrying for reasonsof myopia and moral hazard.Compulsory contributions are seen asone way of dealing with individualmyopia and the problem of moralhazard. Myopia arises because individualsdo not recognise the need to makeadequate provision for retirement whenthey are young, but regret this whenthey are old, by which time it is too lateto do anything about it. Moral hazardarises when individuals deliberately avoidsaving for retirement when they areyoung because they calculate that thestate will feel obliged not to let themlive in dire poverty in retirement.Inevitably, this will lead to substantialmeans testing in retirement.

In short, while the Welfare Reformand Pensions Act has some good points,it fails three tests set by Frank Field for agood state pension system: it is notmandatory, it is not funded and itremains means-tested.16,17

Reforms to private pensions

The Government’s proposal to have amaximum charge of 1 per cent of fundvalue on SPSs will have two dramaticeffects on private sector pensionprovision, especially PPSs.

The first is that it will help to forceeconomies of scale in DC pensionprovision. This is because stakeholderpensions will be a retail product withwholesale charges. To deliver thisproduct effectively, providers will need toexploit massive economies of scale.Charges for personal pension schemeswhich prior to the introduction ofstakeholder pension schemes averaged 1.4

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 339

The UK pension system: Key issues

SERPS was an incredibly complexpension system that very few pensionsprofessionals fully understood, let alonemembers of the general public. Whilethere was comment in the media at thetime of these changes to SERPS, verylittle of this seems to have permeated theconsciousness of the mass of thepopulation and the extent of the changeswas little understood. Thirdly, thechanges were introduced with a time lagof 15 to 20 years, so it was easy foreveryone to forget about them.

Even when changes were introducedimmediately, such as the switch in theuprating of the state pension fromearnings to prices, the immediatedifference was relatively small and mostpeople failed to realise how smalldifferences can compound into largeamounts over time.19

A final explanation lies in the fact thatstate pension provision is much lessimportant for most people in the UKthan on the continent, and those forwhom it is important, namely thelow-paid, have little political influence.

The situation on the continent israther different. State pensions provide amuch higher replacement ratio than inthe UK and social solidarity appears tobe a more important objective than it isin the UK. As a consequence, it is muchharder to alter pension arrangements onthe continent, even if the political willto do so is strong, which it clearly isnot.

The legal structure of andregulatory framework foroccupational pension schemes

The trust fund

Most occupational pension schemes inthe UK have been set up as pensiontrust funds. A trust is a legal relationshipbetween individuals and assets, by which

big advantage that they can be cashedin tax free at any time, therebyavoiding the need to purchase apension annuity on the retirementdate.

The second benefit is that it willeffectively force stakeholder pensionfunds to be passively managed, sinceactive management would result in acharge higher than 1 per cent. Asdemonstrated below, active fundmanagers have not demonstrated thatthey can systematically deliver thesuperior investment performance thatjustifies their higher charges. Furtherpassively-managed mutual funds in theUSA, such as Vanguard (which aresimilar investment vehicles to PPIs), havecharges below 0.3 per cent.

The political economy of pension reform

How has it been possible for UKGovernments to reduce the size of statepension provision without significantpolitical protest when similar attempts todo so on the continent have led to streetprotests and strikes (eg in Italy inNovember 1994 and France inNovember 1995)?

Consider the SERPS pension. Whenit was first introduced in 1978, it offereda pension of 25 per cent of the best 20years of band earnings revalued to theretirement date by increases in nationalaverage earnings, with a 100 per centspouse’s pension. Within a quarter of acentury, the value of these benefits hadbeen reduced by two thirds before thescheme was abandoned altogether. Howhas this been achieved so peaceably?There are three main explanations. First,SERPS had only been established a fewyears before changes to it started beingmade, so very few people were drawingthe pension and little loyalty for thescheme had accumulated. Secondly,

340 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

pension scheme must be establishedunder irrevocable trust, with theemployee being a beneficiary under thetrust, and the employer being acontributor. However, the word‘irrevocable’ is not crucial, since the trustdeed can provide for the alteration andwinding-up of the scheme. But the solepurpose of the scheme must be toprovide ‘relevant benefits’ in respect ofservice as an employee, where benefitsare defined as pensions and lump sumspayable on or in anticipation ofretirement or on death. The benefitsmust be made available to the memberor widow/er, children, or dependants.Most trusts have limitations on theirdurations under the 1963 Perpetuitiesand Accumulations Act. However,occupational pension schemes areexempted from these limitations wherethey have received exempt approval fromthe Inland Revenue (under section 163of the 1993 Pensions Schemes Act).

The pension scheme must also appointan administrator to manage the scheme.Under the 1970 Finance Act, theadministrator must be a resident of theUK. Typically the trustees, so long asthey are resident in the UK, areappointed as administrator to the scheme.

The Occupational Pensions RegulatoryAuthority

The 1995 Pensions Act established theOccupational Pensions RegulatoryAuthority (Opra) as the regulatoryauthority for the pensions industry. It isfinanced by an annual levy on pensionschemes. Opra took over most of theresponsibilities of the OccupationalPensions Board (OPB) which had beenset up under the 1973 Social SecurityAct to monitor scheme rules on thepreservation of benefits for early leavers,equal access and contracting-outrequirements. The 1995 Act transferred

assets provided by one individual (thesettlor) are held by another group ofindividuals (trustees) for the benefit of athird group of individuals (thebeneficiaries). The interests of thebeneficiaries are set out in the trust deed.If the trust is a discretionary trust, thetrustees have the freedom of action todispose the income and capital of thetrust as they see fit. The trust servesthree functions: it is the primary sourceof payment of pension entitlements; it isa security for payment; and it is a vehiclefor the collective protection andenforcement of the rights of individualscheme members. The first scheme toadopt this legal vehicle was that ofColmans, the mustard manufacturer, in1900.

There are several reasons why a trustfund came to be preferred to a statutoryfund, its main alternative. A trust fundwas much cheaper to set up than astatutory fund. It was also much moreflexible: the trust deed could be drawnup in virtually any way that suited theemployer, and the employer could ensureeffective control of the fund through hisappointment of the trustees.Nevertheless, a trust is also a usefulvehicle for protecting pension benefits.This is because a trust is a means ofattaching to assets the interests of a wideclass of beneficiaries, including those notyet born. The presence of a trust alsoseparates the assets of the trust fromthose of the employer, a valuable featurein the case of default.

Since trust law had not originally beenestablished to validate pension schemes, itsoon became necessary to put thearrangements on a formal basis. This wasdone in the Superannuation and OtherTrust Funds (Validation) Act of 1927,which permitted the formal validation oftrust funds.

In order to receive exempt approvedstatus from the Inland Revenue, a

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 341

The UK pension system: Key issues

— apply for a court injunction toprevent the misuse ormisappropriation of scheme assets;

— apply for a court order requiring therestitution of scheme assets where it issatisfied that they have beenmisappropriated, eg where schemeassets have been loaned to theemployer in contravention of legalrequirements;

— direct trustees to pay members’benefits, eg where an employerdeducts pension contributions fromearnings but does not pass them on tothe scheme;

— require the production of anydocument relating to a particularpension scheme from a trustee,manager, professional adviser oremployer;

— enter premises where schememembers are employed, or wheredocuments relating to schememembers are kept, or where theadministration of a pension scheme iscarried out, and to question anyperson on those premises who may beable to provide relevant information.

The Pensions Act requires every pensionscheme to appoint an auditor and anactuary. The Act imposes a specificobligation on the auditor and actuary toreport to Opra if they have ‘reasonablecause’ to believe that there has been abreach of duty relevant to the scheme’sadministration by the employer, trustees,administrator or a professional adviser.The auditor and actuary are protectedfrom any claim of breach of privilege ifthey ‘blow the whistle’ but face civilpenalties or even disqualification if theyfail to meet these requirements. The Actalso requires the appointment of aprofessional fund manager where ascheme has investments regulated by the1986 Financial Services Act. The auditor,actuary and fund manager are classified as

the contracting-out arrangements to theNational Insurance Contributions Office(NICO) of the Inland Revenue anddisbanded the OPB.

Opra has extensive powers, includingthe power to:

— remove or suspend a trustee wherethere has been a ‘serious or persistentbreach’ of his or her duties, whereproceedings have been commencedagainst him or her for an offenceinvolving dishonesty or deception,where a bankruptcy petition has beenpresented against him or her, orwhere an application has been madeto disqualify him/her as a companydirector;

— appoint a new trustee if an existingtrustee has been removed ordisqualified under the Pensions Act,or in order to secure ‘the properadministration of the scheme’ or ‘theproper use or application of the assetsof the scheme’;

— wind-up schemes if it is satisfied thatthe scheme ought to be replaced by adifferent scheme, that the scheme isno longer required, or that awinding-up is necessary to protect theinterests of the generality of thescheme members;

— modify schemes to enable a schemeto reduce or eliminate a statutorysurplus, to enable surplus assets to bedistributed to the employer in thecase where a scheme is beingwound-up, or to enable a scheme tobe contracted out during a prescribedperiod;

— impose civil penalties for misconduct,eg making a payment to theemployer from the scheme assetscontrary to s. 37, or failure to obtainan actuarial valuation and certificate inaccordance with s. 57, or failure tomaintain a payment schedule or makea statement of investment principles;

342 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

beneficiaries and to act impartiallybetween the interests of different classesof beneficiaries. They have to act inaccordance with the trust deed and rulesof the scheme, within the framework oftrust law and the statutory regulations ofOpra. They also have to act prudently,conscientiously, honestly, and with theutmost good faith. But there are nospecific rules on the number of trusteesor for the scheme to have anindependent trustee. There is also norequirement for a trustee to have anyspecial training or to meet anyprofessional standard. It is possible for thetrustee to be a limited company: indeedmore than half of existing pensionschemes have corporate trustees (althoughmost of these are not independent of theemployer).

Trustees have a fiduciary duty underthe 1961 Trustee Investments Act topreserve the trust capital and to apply thecapital and its income according to thetrust deed. This means that trustees areultimately responsible for the safe custodyof scheme assets and for ensuring thatthe benefits provided under scheme rulesare duly delivered to scheme members.Trustees generally have wide investmentpowers, including powers to borrow.Indeed, the failure to invest, or at leastplace funds on deposit, might maketrustees liable to make up the lostincome. Scheme members can sue forcompensation if they suffer loss as aresult of negligence by trustees under the1925 Trustee Act.

Trustees (and their investment advisers)also have to abide by the FinancialServices Act 1986. It is a criminaloffence to carry on investment businessin the UK unless either authorised to doso or exempted from the provisions ofthe Act. Pension fund managers areregulated by the Financial ServicesAuthority (FSA) (formerly IMRO — theInvestment Managers Regulatory

‘professional advisers’ under the PensionsAct and will have to be members of arecognised professional body. There is norequirement under the Act to appoint alegal adviser. However, legal advisers to apension scheme are exempt from therequirement to blow the whistle on thetraditional grounds of legal professionalprivilege, except where there is reason tobelieve that the pension scheme is beingused for money laundering purposes.

The Act also established the PensionsCompensation Board (PCB) to administera compensation scheme. Certainconditions will need to be met before thecompensation provisions apply:

— the scheme must be established undertrust

— the employer must be insolvent— the value of the scheme assets must

have been reduced as a result of anillegal act and, in the case of asalary-related scheme, to less than 90per cent of the value of the liabilities.

The amount of any compensation isdetermined by regulations, but will notexceed 90 per cent of the loss at theapplication date and, in the case of asalary-related scheme, will be limited towhatever is necessary to restore thescheme to a 90 per cent solvency level.The PCB has power to make drip-feedpayments to a defrauded scheme in anemergency situation where it accepts thatthere are grounds for compensation andwhere the trustees would not otherwisebe able to make pension payments. Thescheme will be financed by a special levyon occupational pension schemesimposed after the compensatable eventhas taken place.

Trustees

The role of the trustees is to operate thepension scheme in the best interests of its

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 343

The UK pension system: Key issues

company director. The assets of thescheme cannot be used to pay a fineimposed on a trustee; previously schemeassets could be used to indemnify atrustee who inadvertently committed abreach of trust.

Thirdly, the Act allows for theappointment of member-nominatedtrustees (MNTs) unless schememembers have specifically voted againstthis. Once appointed, MNTs can onlybe removed with the agreement of allother trustees; previously, the employerhad the exclusive power to appointand remove trustees. Where theappointment of MNTs has beenapproved, the scheme’s membership isentitled to elect one-third of the totalnumber of trustees, with a minimumof two MNTs for large schemes andone in schemes with fewer than 100members. The MNT does not have tobe a scheme member, although theemployer has the power to block theappointment of a non-scheme memberof whom he does not approve;however, the employer cannot blockthe appointment of a scheme memberwho has been elected. A schememember includes any ‘active, deferred,or pensioner member’ of the scheme.MNTs have the same fiduciaryresponsibilities as other trustees to actin the best interests of all members.

Fourthly, the Act imposes on trustees aduty of care to invest the assets of thefund in an orderly and correct manner.Section 33 prohibits the trust deed orrules from restricting a trustee’s liabilitywhere that duty of care is not properlyobserved. Section 34 gives pensiontrustees a general power to makeinvestments ‘of any kind as if they wereabsolutely entitled to the assets of thescheme’. Trustees are, however,permitted to delegate authority to a fundmanager. In the case of a discretionaryfund manager, with powers to make

Organisation). Under s. 19 of the Act,trustees who are not involved in dailyinvestment decision-taking for theirschemes do not have to be regulatedunder the Act. However, the FSA makesregular inspection visits to occupationalpension schemes. In general, it finds thatmost schemes are well-run, althoughsome schemes have been criticised forinadequate record-keeping and failing toensure that administrative staff areproperly trained.

Trustees have substantial discretionover who benefits in the event of amember dying, especially if the memberwas unmarried or had no one who wasfinancially dependent on him or her. If,for example, a man was married (even ifthe wife was financially independent) orhad parents, or children up to the age of18 who were financially dependent onhim, the case would be clear-cut: theywould receive a widow’s or dependant’spension. If the man had a financiallyindependent common-law wife, the caseis also clear-cut: the common-law wifewould not receive a widow’s pension. If,however, the common-law wife wasfinancially dependent, she might receivea pension at the trustees’ discretion.

There is no restriction on whoreceives the tax-free lump sum in theevent of death in service. It can go towhoever is nominated by the member. Ifno one is nominated and there are nodependent relatives, it will go into themember’s estate and be taxed.

The 1995 Pensions Act had a majorimpact on trustees. First, it placed alltrustees under the supervision of Opra.Secondly, it specified who could notserve as a trustee. For example, a schemeauditor or actuary cannot serve as atrustee. Neither can ‘unsuitable persons’such as anyone who has been convictedof an offence involving dishonesty ordeception, an undischarged bankrupt, orany person disqualified from acting as a

344 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

one-size-fits-all structure and in March2001, the government announced that itwould replace the MFR with a fundingstandard that was scheme-specific. Eachof these funding standards will beconsidered in turn.

The MFR

The MFR came into effect in April1997. It applied to all occupationalschemes except occupational moneypurchase schemes, public service schemesestablished by statute, local governmentschemes, schemes with a governmentguarantee and unapproved schemes. Itobliged schemes subject to MFR toensure that ‘the value of the assets of thescheme are not less than the amount ofthe liabilities of the scheme’. Theprocedure for doing this were set out inthe Occupational Pension Schemes(Minimum Funding Requirement andActuarial Valuations Regulations) 1996(SI 1996/1536) and Guidance Note 27from the Institute and Faculty ofActuaries.

Trustees subject to MFR were obligedto prepare and maintain a schedule ofcontributions indicating the rate of bothemployer and member contributions andthe dates on which the contributions hadto be paid into the fund. The actuaryhad to give an opinion on whether thecontributions were ‘adequate for thepurpose of securing that the minimumfunding requirement will continue to bemet throughout the prescribed period[the next five years] or, if it appears tohim that it is not met, will be met bythe end of that period’.

A ‘serious underprovision’ arose in thecase where the scheme’s assets were lessthan 90 per cent of its liabilities. Theemployer was required to make up thedifference to 90 per cent through a cashinjection or other means such as a bankletter of credit for the amount of shortfalland for the life of the schedule of

day-to-day investment decisions, thetrustees will not normally be heldresponsible for any act or default of thefund manager, as long as they have takenall reasonable steps to satisfy themselvesthat the manager ‘has the appropriateknowledge and experience for managingthe investments of the scheme’. In thecase of other types of fund manager, thetrustees will normally be held responsiblefor any act or default by them.

Fifthly, the Act requires trustees toprepare and maintain a Statement ofInvestment Principles (SIP). The SIPspecifies the strategic objectives of thepension fund and must cover thefollowing issues:

— the kinds of investments held— the balance between different kinds of

investments— risk and the need for the

diversification of investments— expected return on investments— the realisation of investments.

In preparing the SIP, the trustees arerequired to take written advice from ‘aperson who is reasonably believed by thetrustees to be qualified by his ability inand practical experience of financialmatters and to have the appropriateknowledge and experience of themanagement of the investment of suchschemes’.

Finally, trustees are required tointroduce arrangements for resolvinginternal disputes between schemeadministrators and scheme members.

The minimum funding requirement andscheme-specific funding standard

The minimum funding requirement(MFR) was introduced by the 1995Pensions Act in response to the Maxwellscandal.20 However, there was almostimmediate criticism of its inflexible,

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 345

The UK pension system: Key issues

proposals were recommended by the2001 Myners review of institutionalinvestment.20 The new standard isexpected to come into force in 2005.

Trustees and their advisers will berequired to take a view on the appropriatefunding and investment of the scheme inthe light of the scheme’s specificcircumstances and those of the sponsoringemployer. Associated with this will be astrong regime of transparency anddisclosure. The trustees and advisers ofeach scheme will be required to publish ascheme-specific funding statement which‘sets out in a clear and straightforwardway how it sees its liabilities growing overtime and how, through contributions tothe fund and growth in the value of theassets through investment returns, itproposes to meet its liabilities’. Thefunding statement will specify:

— the funding objectives for the scheme— the fund’s investment policy and

projected returns on its assets— assumptions for projecting its

liabilities, including the range ofeconomic scenarios considered

— a contribution schedule agreed by thetrustees and the employer.

The statement will be drawn upassuming that the employer will continuein existence, that is, on a long-term orongoing basis, and the trustees will berequired to assess and report on thestrength of the employer’s covenant. Theemployer is therefore expected to befully involved in discussions aboutfunding and investment plans, and inagreeing the required contribution rates.Interested parties, such as schememembers, their representatives (such astrade unions and pensioner supportgroups), and the company’s shareholders,can scrutinise the scheme’s funding andinvestment plans and assess whether theyare realistic and appropriate.

contributions. The employer had torestore the scheme’s solvency level to 90per cent within three years of the seriousunderprovision being discovered. Wherethe solvency level was between 90 and100 per cent, it had to be restored to100 per cent and so satisfy the MFR bythe end of the current schedule ofpayments, namely five years.

A number of problems emerged withthe MFR:

— it did not guarantee that the pensionwould be paid in full: a pension fundthat fully meets the MFR might onlyhave funds sufficient to purchasearound 70 per cent of the pensionsdue to active members if the sponsorbecomes insolvent, mainly because theclaims of retired members are metfirst

— it was highly sensitive to the way inwhich pension liabilities were valued

— it restricted pension funds frominvesting in an optimal mix of assets,by encouraging pension fundmanagers to reduce their weighting in‘volatile’ asset categories such asequities.

The Faculty and Institute of Actuaries, inits 2000 publication ‘Review of theMinimum Funding Requirement’,concluded that the MFR ‘cannot bemade to work as a statutory standard’. Itaccepted that there was an ‘inherentconflict between the MFR whichimposes a risk of short-term fluctuationsin funding requirements and thelong-term asset allocation to produce thebest financial results for pension fundmembers’.

A scheme-specific funding standard

In March 2001, the Governmentannounced that it would replace theone-size-fits-all MFR with a long-term,scheme-specific funding standard.21 These

346 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

The Government argues that: ‘Theseproposals will provide protection formembers of all defined benefit schemesand will encourage an intelligent andthought-through approach to planninginvestment and contributions policy.They do not distort investment as theMFR does, because they do not involvethe valuation of liabilities using statutoryreference assets which create artificialincentives for schemes to invest in thoseassets. Employers that wish to go onoffering defined benefit schemes will findit easier to do so under these proposals.At the same time, the proposals willmake it more difficult for those that wishto walk away from the pension promisesthat they have made.’

The accounting framework foroccupational pension schemes

Financial Reporting Statement 17

In November 2000, the AccountingStandards Board (ASB) issued a newFinancial Reporting Standard (‘FinancialReporting Standard 17 — RetirementBenefits’) with the objective of replacingSSAP24, the existing accounting standardfor reporting pension costs in DBpension schemes. The principal changesare that:

— actuarial gains and losses will berecognised fully and immediately(rather than amortised over a periodof up to 15 years)

— scheme assets and liabilities will bevalued by reference to current marketconditions.

The consequence of this could be greatervolatility of pension costs year on yearand greater volatility in the balancesheet.

Prior to the introduction of SSAP24(Accounting for Pension Costs) in 1988,

Each scheme will have to compareitself against the funding statement ona regular basis. If the scheme finds thatit is not adequately funded then it willhave to produce a recovery plan forreturning the fund to full fundingwithin three years. The key objectiveis to ensure that the scheme is fundedto meet the benefits in full in the longterm. The scheme will be required tofile the recovery plan with Opra andreport annually on progress against it.Opra will have some discretion toallow extensions to the deadline forreturning funding to an adequate level,in the light of the specificcircumstances of the scheme.

The trustees, actuaries and auditorswill have whistleblowing duties to reportto Opra if contributions are not paid inaccordance with the recovery plan. Inparticular, the scheme actuary will have astatutory duty of care towards schememembers. This will be particularlyimportant for smaller funds where theremay not be people or organisations withthe required skill or interest to exerciseeffective scrutiny of the scheme’s fundingstatement. The actuary will have anexplicit duty to consider the implicationsof funding plans for the scheme membersand beneficiaries. The actuary will have aduty to report to Opra if contributionsare not being paid according to thefunding statement; if there are any delaysin drawing up a recovery plan in ascheme that is underfunded; and ifcontributions to an underfunded schemeare not being paid in line with therecovery plan.

There will also be an extension of thefraud compensation scheme. The level ofcompensation for fraud will be increasedto cover not simply the MFR liabilitiesas at present, but the full cost of securingmembers’ accrued benefits (or theamount of the loss from fraud,whichever is the lesser).

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 347

The UK pension system: Key issues

of gains and losses in the statement ofrecognised gains and losses, not in theP&L

— the financial statements containadequate disclosures.

FRS17 will have the following effectswhen it is fully in force for year-endsafter 2005.

Scheme assets

Scheme assets will be included at theirfair value on the company’s balance sheetdate. This, in turn, will require anannual update of the scheme’s actuarialvaluation. The expected return onscheme assets will be calculated as theproduct of the expected long term rateof return and the market value (at thestart of the period).

Actuarial liability

The actuarial liability will be calculatedusing the projected unit method and anAA corporate bond discount rate,although the actual discount rate usedcan be based on gilt yields with aconstant risk premium of, say, 1 per cent.This rate will generally be lower thanthat used under SSAP24 which is basedon the assumed returns on the pensionfund assets and so includes an equitycomponent. The discount rate should beof equivalent currency and term as thescheme liability; however, the ASBargues that ‘in theory, different discountrates should be applied to cash flowsarising in different periods, reflecting theterm structure of interest rates. Inpractice, acceptable results may beachieved by discounting all the cashflows at a single weighted averagediscount rate’.23

The AA corporate bond yield waschosen because this was the yield used inthe equivalent US accounting standard,FAS87. FAS87 adopted this particularyield because it matched the asset class

employers accounted for pension schemeson a cash basis. Under SSAP24, theprofit and loss account is charged with‘regular pension cost’ which is designedto be a stable proportion of pensionablepay. Any variations from regular cost arespread forward and charged to profit andloss (P&L) gradually over the averageremaining service lives of the employees.Assets and liabilities are reported atactuarial value rather than fair value.

A number of problems emerged withSSAP24:

— too much flexibility in choosing thevaluation method and in accountingfor the resulting gains and losses

— inadequate disclosure requirementsand lack of transparency

— inconsistency between the pensionassets and liabilities in the company’sbalance sheet and the actual surplus ordeficit in the scheme

— inconsistent with internationalaccounting standards (eg FAS87(Employers’ Accounting for Pensions)and IAS19 (Accounting forRetirement Benefits in the FinancialStatements of Employers)) which hadmoved towards a market basis forvaluing scheme assets.

The objectives of FRS17 are to ensurethat:

— the employer’s financial statementsreflect the assets and liabilities arisingfrom retirement benefit obligationsand any related funding, measured atfair value

— the operating costs of providingretirement benefits are recognised inthe periods the benefits are earned byemployees

— financing costs and any other changesin the value of the assets and liabilitiesare recognised in the periods they arise

— there will be immediate recognition

348 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

most cases, the vesting of suchimprovements is immediate, so the costis charged immediately to the P&Laccount without offset against the surpluseven if it is funded from a surplus.

Profit and loss account

The P&L charge will be split between:

— operating costs: which includescurrent service costs and past servicecosts;

— financing costs: which includesinterest costs (the pension liabilitydiscount) and the expected return onassets.

Any overpaid/unpaid contributions arerepresented as debtor/creditor due withinone year.

Actuarial gains and losses

SSAP24 and IAS19 allow differencesbetween actual and expected outcomesto be spread in the P&L over a numberof years and to defer a hard core (the 10per cent corridor) indefinitely.

FRS17, in a radical departure fromconventional practice, requires immediaterecognition of actuarial gains and lossesthrough a new account, the statement ofrecognised gains and losses (STRGL).The asset returns in the pension fund aredivided into two parts which arerecognised separately in the P&L andSTRGL. The financing item in the P&Lwill show an expected asset return,which is designed to be reasonably stableover time. The differences betweenrealised and expected asset returns areshown in the STRGL, as are changes inactuarial assumptions and differencesbetween these assumptions and actualexperience in respect of the liabilities. Afive-year history of these differences isrequired to enable users of the accountsto assess the accuracy of the forecastreturns.

that a US insurance company, taking onthe liabilities of an insolvent pensionplan, would use to invest the scheme’sremaining assets. The same yield wassubsequently adopted by the InternationalAccounting Standards Committee inIAS19.

At the end of each accounting year, apension scheme member will have earnedan additional year of service: this currentservice cost is classified as an operatingcost in FRS17. Also by the end of theyear, the member’s pension liability willhave risen because it is one year closer tobeing delivered (this is denoted theinterest cost or pension liability discount),but this will be offset by the expectedreturn generated on the assets backing theliability: the difference is denoted the netfinancing cost in FRS17.

The current service cost will be higherthan the regular cost under SSAP24. Onthe other hand, under FRS17 thediscount rate (and hence the interest costrelating to the liability) is likely to belower than the expected return onscheme assets, so that the net financingcost for the pension scheme is likely tobe a credit.

Surplus or deficit

The net defined benefit pension asset orliability, after attributable deferred tax,will be shown after other net assets inthe balance sheet. FRS17 limits thesurplus recognised by the employer tothe amount that the employer couldrecover through reduced contributionsand agreed refunds.

Past service costs

Past service costs arise whenever animprovement in benefits is backdated (egthe award of a spouse’s pension). UnderSSAP24, they may be set against anysurplus, with any excess cost charged tothe P&L. With FRS17, they are chargedto P&L over the period of vesting. In

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 349

The UK pension system: Key issues

— the balance sheet shows the deficit orrecoverable surplus in the scheme;

— the total profit and loss charge ismore stable than it would be if themarket value fluctuations were spreadforward.

The Association of Chartered CertifiedAccountants (ACCA) argued that thespreading forward of gains/losses overaverage service lives is better thanimmediate recognition because of thelong-term nature of pension costs, theuncertainty over the estimates of keyyields, and the conformity with currentinternational standards (eg IAS19).Although the various components mightbe separately disclosed, the ACCApreferred the pension cost to be chargedas a single item in operating cost.

The FIA argued that, while FRS17will make ‘the respective risks andrewards borne by companies andshareholders more transparent to theshareholders’, there would be ‘adverseimpacts on pension scheme members,because it will introduce new volatilityinto the assessment of pension costs andliabilities’. As a consequence, sponsors ofDB schemes could become morereluctant to improve benefits since thesewould be immediately reflected incompany P&L, even if funded fromsurplus assets.

The long-term effect of FRS17 onasset allocation is not clear. On the onehand, as in the case of the MFR, the useof a specific discount rate for liabilities(such an AA corporate bond yield) mightinduce funds to adopt a morebond-based investment strategy. On theother hand, by excluding the impact ofequity risk on the P&L, FRS17 providescompanies with an incentive to raise theequity component of their pension fundin order to generate higher expectedasset return and profit figures. However,anecdotal evidence suggests that pension

Assessing FRS17

FRS17 will have three major impacts.

— It will reduce the volatility of theP&L but cannot eliminate it, sincechanges in realised market rateseventually flow through to the P&Lvia consequential changes in thelong-term expected returns on bothassets and AA corporate bonds.

— It will increase the volatility of thebalance sheet due to the inclusion ofthe net pension asset or liability andthis may trigger loan covenants orborrowing limits.

— There will be increased complexity ofthe financial statements arising fromnon-cash pension items, eg currentservice cost and amortisation of pastservice costs within operating cost,and the unwinding of the pensionliability discount and the expectedreturn on assets within financing costs.

International accounting standards dealwith this volatility by averaging themarket values over a number of yearsand/or spreading the gains and lossesforward in the accounts over theremaining service lives of the employees.But the consequences are that thebalance sheet does not represent thecurrent surplus or deficit in the schemeand that charges to P&L are infected bygains and losses that arose many yearspreviously.

With FRS17, the P&L shows therelatively stable ongoing service cost,interest cost and expected returns onassets measured on a basis consistent withinternational standards. The effects of thefluctuations in market values, on theother hand, are not part of the operatingresults of the business and are treated inthe same way as revaluations of fixedassets, ie are recognised immediately inthe STRGL. This has two advantagesover the international approach:

350 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

pension benefit that is defined. In theUK, for example, most DB schemes arearranged by companies and are known asoccupational final salary schemes, sincethe pension is some proportion of finalsalary, where the proportion depends onyears of service in the scheme. A typicalscheme in the UK has a benefit formulaof one-sixtieth of final salary for eachyear of service up to a maximum of 40years’ service, implying a maximumpension in retirement of two-thirds offinal salary, and with the pension indexedto inflation up to a maximum of 5 percent per annum (ie limited priceindexation). In contrast with a DCscheme, what is defined is thecontribution rate into the fund, eg 10per cent of earnings. The resultingpension depends solely on the size of thefund accumulated at retirement. Suchschemes are also known as moneypurchase schemes. The accumulated fundmust be used to buy a life annuity froman insurance company (although in theUK, up to 25 per cent of the fund canbe taken as a tax-free lump sum on theretirement date).

DB schemes

DB and DC schemes have different costsand benefits. DB schemes offer anassured (and in many cases a relativelyhigh) income replacement ratio inretirement. People in retirement canexpect to enjoy a standard of living thatis related to their standard of living justprior to retirement. But this is the caseonly for workers who remain with thesame employer for their whole career.Fewer than 5 per cent of workers in theUK do this: the average worker changesjobs about six times in a lifetime.25

Every time workers switch jobs theyexperience a ‘portability loss’ in respectof their pension entitlement. This isbecause DB schemes are generally

funds are increasing rather than reducingtheir weighting in bonds in preparationfor the introduction of FRS17.

Other objections have been putforward:

— the P&L depends on an assessed orexpected figure for asset returns;

— there are potentially two differentvaluation results, the trustees’ fundingvaluation and the company’saccounting valuation; companiesprefer to align the two types ofvaluation, if possible using the weakerfunding basis, thereby reducing thesecurity of benefits;

— despite the greater transparency fromusing market values, there can besubstantially different investmentconditions if companies use differentmeasurement dates, even if these datesare only a short time apart;

— a pension scheme deficit has to bededucted from distributable reserves,thereby lowering dividend cover andpossibly forcing a company to pass adividend payment. Somecommentators have suggested that thisis what should happen if companiesmake a pension promise and do nothave the resources to cover it;

— the use of the projected unit methodto determine pension liabilities isinconsistent with the MFR, eventhough it gives a more realisticmeasure of the true eventual liability;

— unlike the USA, AA bonds are not asignificant investment category in theUK: their weighting was just 7 percent of the total UK bond market inDecember 2000.

The risks and returns in fundedschemesThere are two main types of fundedscheme: the DB scheme and the DCscheme.24 With a DB scheme, it is the

� Henry Stewart Publications 1478-5315 (2003) Vol. 8, 4, 330-375 Pensions 351

The UK pension system: Key issues

leaver valued in terms of their projectedsalary at retirement which is likely to behigher. Long stayers are thereforesubsidised at the expense of early leavers.In the UK, the portability loss is morecommonly known as a ‘cash equivalentloss’.

For a typical worker in the UKchanging jobs six times during theircareer, Table 2 shows that the portabilityloss lies between 25 and 30 per cent ofthe full service pension (ie the pension ofsomeone with the same salary experiencebut who remains in the same scheme alltheir working life). Even someonechanging jobs once in mid-career canlose up to 16 per cent of the full servicepension. It is possible to reduceportability losses by, for example,indexing leaving salaries between the

provided by specific employers and whena worker changes jobs they have tomove to a new employer’s scheme.When they do so, they will either take atransfer value equal to the cashequivalent of their accrued pensionbenefits with them or leave a deferredpension in the scheme that they areleaving. Accrued benefits are valued lessfavourably if someone leaves a schemethan if they remain an active member ofthe scheme. This is because schemeleavers (whether they choose a transfervalue or a deferred pension) have theiryears of service valued in terms of theirleaving salary (although this is upratedannually to the retirement date by thelower of the inflation rate or 5 per cent),whereas continuing members will havethe same years of service as the early

352 Pensions Vol. 8, 4, 330–375 � Henry Stewart Publications 1478-5315 (2003)

Blake

Table 2: Portability losses from defined benefit schemes (percentage of full service pension received atretirement)

Workertype

Job separationassumptions1

Transfervalue2

Deferredpension3

DCpension(employer-run)4

Personalpension(employercontributions)5

Personalpension(no employercontributions)6

Average UK worker(MFR assumptionsrealised)7

Average UKmanual worker

Average UKnon-manualworker

ABC

ABC

ABC

757184

757184

757184

757184

888696

868394

71

78

79

61

66

68

37

45

44

Notes:1 This table presents estimates of the size of the portability losses experienced by three different types of UK