The Travel & Tourism Competitiveness Report 2009

525

The Travel & Tourism Competitiveness Report 2009 Managing in a Time of Turbulence Jennifer Blanke, World Economic Forum Thea Chiesa, World Economic Forum Editors World Economic Forum Geneva, Switzerland 2009 The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

Transcript of The Travel & Tourism Competitiveness Report 2009

The Travel & TourismCompetitiveness Report 2009Managing in a Time of Turbulence

Jennifer Blanke, World Economic Forum

Thea Chiesa, World Economic Forum

Editors

World Economic ForumGeneva, Switzerland 2009

part1.r2 2/26/09 11:58 AM Page i

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

The Travel & Tourism CompetitivenessReport 2009 is published by the WorldEconomic Forum within the framework of theGlobal Competitiveness Network and theIndustry Partnership Programme for Aviation,Travel and Tourism.

Professor Klaus Schwab, Executive Chairman

EDITORS

Jennifer Blanke, Director, Senior Economist, Head of Global Competitiveness Network

Thea Chiesa, Associate Director, Head of Aviation, Travel and Tourism

GLOBAL COMPETITIVENESS NETWORK

Fiona Paua, Senior Director, Head of Strategic Insight Teams

Ciara Browne, Senior Community ManagerAgustina Ciocia, Community ManagerMargareta Drzeniek Hanouz, Director, Senior EconomistThierry Geiger, Economist, Global Leadership FellowIrene Mia, Director, Senior EconomistPearl Samandari, Team CoordinatorEva Trujillo Herrera, Research Assistant

We thank Hope Steele for her superb editingwork and Ha Nguyen for her excellent graph-ic design and layout.

The terms country and nation as used in this report do not in all cases refer to a territorial entity that is a state as understoodby international law and practice. The terms cover well-defined, geographically self-contained economic areas that may not be states but for which statistical data are maintained on a separate and independent basis.

World Economic ForumGeneva

Copyright © 2009by the World Economic Forum

Published by World Economic Forumwww.weforum.org

All rights reserved. No part of this publicationmay be reproduced, stored in a retrieval sys-tem, or transmitted, in any form or by anymeans, electronic, mechanical, photocopying,or otherwise without the prior permission ofthe World Economic Forum.

ISBN-13: 978-92-95044-18-0

part1.r2 2/26/09 11:58 AM Page ii

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

Contents

Partner Institutes v

Preface xiby Klaus Schwab, World Economic Forum

Executive Summary xiiiby Jennifer Blanke and Thea Chiesa, World Economic Forum

Part 1: Selected Issues of T&T Competitiveness 1

1.1 The Travel & Tourism Competitiveness Index 2009: 3Measuring Sectoral Drivers in a Downturnby Jennifer Blanke, Thea Chiesa, and Eva Trujillo Herrera, World Economic Forum

1.2 Endangered Growth: How the Price of Oil 39Challenges International Travel & Tourism Growthby Jürgen Ringbeck, Amit Gautam, and Timm Pietsch, Booz & Company

1.3 The Importance of Public-Private Partnership 49in the Current Downturnby Amir Girgis and Ufi Ibrahim, World Travel & Tourism Council (WTTC)

1.4 How Well Does the Travel & Tourism 55Competitiveness Index Explain Differences in Travel Intensity Among Countries?by Selim Ach and Brian Pearce, International Air TransportAssociation (IATA)

1.5 Capturing the Visitor Economy: 65A Framework for Successby Alex Kyriakidis, Heather Hancock, Simon Oaten, and Rashid Bashir, Deloitte

1.6 Tourism Price Competitiveness 77by Peter Forsyth, Monash University, and Larry Dwyer, University of New South Wales

1.7 National Competitiveness Council: 91Setting Up the Egyptian Travel & Tourism Competitiveness Councilby Ashraf Ibrahim, Egyptian Travel & Tourism Competitiveness Council (T&TCC) and Heba Ali Zayed, Egyptian National Competitiveness Council (ENCC)

1.8 Navigating Yet Another Perfect Storm: 97The Promise of Sustainable Travel & Tourismby Thea Chiesa, World Economic Forum

1.9 Strengthening the Travel & Tourism 107Competitiveness Indexby Geoffrey Lipman and John Kester, United Nations World Travel Organization (UNWTO)

Part 2: Country/Economy Profiles and Data 109Presentation

2.1 Country/Economy Profiles 111How to Read the Country/Economy Profiles .............................113List of Countries/Economies......................................................115Country/Economy Profiles..........................................................116

2.2 Data Tables 383How to Read the Data Tables ....................................................385Index of Data Tables...................................................................387Data Tables.................................................................................389

Technical Notes and Sources 483

About the Authors 489

Acknowledgments 493

iii

part1.r2 2/26/09 11:58 AM Page iii

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

part1.r2 2/26/09 11:58 AM Page iv

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

The World Economic Forum’s Global CompetitivenessNetwork is pleased to acknowledge and thank the following organizations as our valued Partner Institutes,without whom the realization of the Travel & TourismCompetitiveness Report 2009 would not have been feasible:

Albania

Institute for Contemporary Studies (ISB)Artan Hoxha, PresidentElira Jorgoni, Senior Expert and Project ManagerDenalada Kuzumi, Researcher

Algeria

Centre de Recherche en Economie Appliquée pour le Développement (CREAD)

Youcef Benabdallah, Assistant ProfessorYassine Ferfera, Director

Argentina

IAE—Universidad AustralMaría Elina Gigaglia, Project ManagerEduardo Luis Fracchia, Professor

Armenia

Economy and Values Research CenterManuk Hergnyan, ChairmanSevak Hovhannisyan, Board Member and Senior AssociateGohar Malumyan, Research Associate

Australia

Australian Industry GroupNicholas James, EconomistTony Pensabene, Associate Director, Economics & ResearchHeather Ridout, Chief Executive

Austria

Austrian Institute of Economic Research (WIFO)Karl Aiginger, DirectorGerhard Schwarz, Coordinator, Survey Department

Azerbaijan

Azerbaijan Marketing SocietyFuad Aliyev, Executive DirectorAshraf Hajiyev, Project CoordinatorSaida Talibova, Consultant

Bahrain

Bahrain Competitiveness Council, Bahrain Economic Development Board

Nada Azmi, Business Intelligence Specialist, Research Services Unit

Jawad Habib, Senior Partner, BDO Jawad HabibRima Al Kilani, Director, International Marketing

Bangladesh

Centre for Policy Dialogue (CPD)Khondaker Golam Moazzem, Senior Research FellowKazi Mahmudur Rahman, Senior Research AssociateMustafizur Rahman, Executive Director

Barbados

Arthur Lewis Institute for Social and Economic Studies, University of West Indies (UWI)

Andrew Downes, Director

Belgium

Vlerick Leuven Gent Management SchoolLutgart Van den Berghe, Professor, Executive Director

and Chairman, Competence Centre Entrepreneurship,Governance and Strategy

Bieke Dewulf, Associate, Competence Centre Entrepreneurship,Governance and Strategy

Wim Moesen, Professor

Benin

Micro Impacts of Macroeconomic Adjustment Policies (MIMAP)Benin

Epiphane Adjovi, Business CoordinatorMaria-Odile Attanasso, Deputy CoordinatorFructueux Deguenonvo, Researcher

Bosnia and Herzegovina

MIT Center, School of Economics and Business in Sarajevo,University of Sarajevo

Zlatko LagumdÏija, ProfessorZeljko Sain, Executive DirectorJasmina Selimovic, Assistant Director

Botswana

Botswana National Productivity CentreDabilani Buthali, Manager, Information and Research Services

DepartmentThembo Lebang, Executive DirectorOmphemetse David Matlhape, Research Consultant

Brazil

Fundação Dom CabralMarina Araújo, ResearcherCarlos Arruda, Professor and Coordinator of Competitiveness

and Innovation CenterJuan Rios, Research Assistant

Movimento Brasil Competitivo (MBC)Cláudio Leite Gastal, Director PresidentLucas Tadeu Melo Câmara, Director

Brunei Darussalam

Ministry of Industry and Primary ResourcesPehin Dato Dr. Hj Ahmad Hj Jumat, MinisterDato Paduka Hj Hamdillah Hj Abd Wahab, Deputy MinisterDato Paduka Hamid Hj Mohd Jaafar, Permanent Secretary

Bulgaria

Center for Economic DevelopmentAnelia Damianova, Senior Expert

Burkina Faso

Société d’Etudes et de Recherche Formation pour leDéveloppement (SERF)

Abdoulaye Tarnagda, Director General

Burundi

University Research Centre for Economic and Social Development (CURDES), National University of Burundi

Richard Ndereyahaga, Head of CURDESGilbert Niyongabo, Dean, Faculty of Economics & Management

v

Part

ner

Inst

itute

s

Partner Institutes

part1.r2 2/26/09 11:58 AM Page v

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

Cambodia

Economic Institute of CambodiaSok Hach, DirectorTuy Chak Riya, Research AssociateHang Sambopisith, Researcher

Cameroon

Comité de Compétitivité (Competitiveness Committee)Lucien Sanzouango, Permanent Secretary

Canada

Institute for Competitiveness and ProsperityLance Bialas, ResearcherRoger Martin, Chairman and Dean of the Rotman School

of Management, University of TorontoJames Milway, Executive Director

Chad

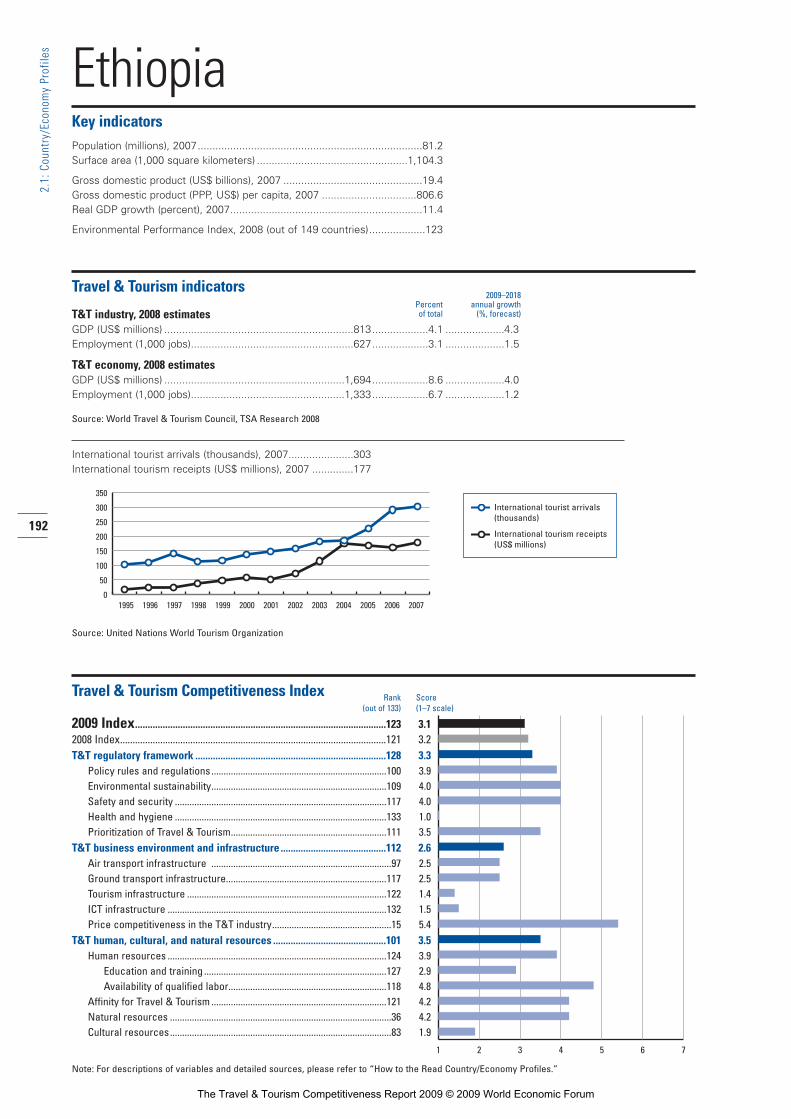

Groupe de Recherches Alternatives et de Monitoring du Projet Pétrole-Tchad-Cameroun (GRAMP-TC)

Antoine Doudjidingao, ResearcherGilbert Maoundonodji, DirectorCeline Nénodji Mbaipeur, Program Officer

Chile

Universidad Adolfo IbáñezIgnacio Briones, Associate Professor of Economics,

School of GovernmentLeonidas Montes, Dean, School of Government

China

Institute of Economic System and ManagementNational Development and Reform CommissionZhou Haichun, Deputy Director and ProfessorChen Wei, Research FellowDong Ying, Professor

China Center for Economic Statistics Research, Tianjin Universityof Finance and Economics

Lu Dong, ProfessorXiao Hongye, ProfessorJian Wang, Associate ProfessorBojuan Zhao, ProfessorHuazhang Zheng, Associate Professor

Colombia

National Planning DepartmentOrlando Gracia Fajardo, Entrepreneurial Development DirectorCarolina Rentería Rodríguez, General DirectorMauricio Torres Velásquez, Advisor

Côte d’Ivoire

Chambre de Commerce et d’Industrie de Côte d’IvoireMamadou Sarr, General Director

Croatia

National Competitiveness CouncilMartina Hatlak, Research AssistantMira Lenardic, General Secretary

Cyprus

European University CyprusBambos Papageorgiou, Head of Socioeconomic and

Academic Research

The Cyprus Development BankMaria Markidou-Georgiadou, Manager, International

Banking Services Unit and Business Development

Czech Republic

CMC Graduate School of BusinessDagmar Glückaufová, Academic DeanFilip Hrnãífi, President

Denmark

Copenhagen Business School, Department of InternationalEconomics and Management

Lise Peitersen, Administrative DirectorOle Risager, Professor

Ecuador

Escuela de Postgrado en Administración de Empresas (ESPAE)Escuela Superior Politécnica del Litoral (ESPOL)Elizabeth Arteaga, Project AssistantVirginia Lasio, Acting DirectorSara Wong, Professor

Egypt

The Egyptian Center for Economic StudiesHanaa Kheir-El-Din, Executive Director and Director of Research

Estonia

Estonian Institute of Economic ResearchEvelin Ahermaa, Head of Economic Research SectorMarje Josing, Director

Estonian Development FundKitty Kubo, Head of ForesightOtt Pärna, Chief Executive Officer

Ethiopia

African Institute of Management, Development and GovernanceTegegne Teka, General Manager

Finland

ETLA—The Research Institute of the Finnish EconomyPetri Rouvinen, Research DirectorPasi Sorjonen, Head of the Forecasting GroupPekka Ylä-Anttila, Managing Director

France

HEC School of Management, ParisBertrand Moingeon, Professor, Deputy DeanBernard Ramanantsoa, Professor, Dean of HEC School of

Management

Gambia, The

Gambia Economic and Social Development Research Institute(GESDRI)

Makaireh A. Njie, Director

Georgia

Business Initiative for Reforms in GeorgiaGiga Makharadze, Founding Member of the Board of DirectorsTamar Tchintcharauli, Executive DirectorMamuka Tsereteli, Founding Member of the Board of Directors

Germany

WHU—Otto Beisheim School of Management, VallendarRalf Fendel, Professor of Monetary EconomicsMichael Frenkel, Professor, Chair of Macroeconomics and

International Economics

Ghana

Association of Ghana Industries (AGI)Carlo Hey, Project ManagerCletus Kosiba, Executive DirectorTony Oteng-Gyasi, President

Greece

SEV Hellenic Federation of EnterprisesMichael Mitsopoulos, Coordinator, Research and AnalysisThanasis Printsipas, Economist, Research and Analysis

Guatemala

FUNDESAEdgar A. Heinemann, President of the Board of DirectorsPablo Schneider, Economic DirectorJuan Carlos Zapata, General Manager

Guyana

Institute of Development Studies, University of GuyanaKaren Pratt, Research AssociateClive Thomas, Director

vi

Part

ner

Inst

itute

s

part1.r2 2/26/09 11:58 AM Page vi

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

Hong Kong SAR

Hong Kong General Chamber of CommerceDavid O’Rear, Chief Economist

Federation of Hong Kong IndustriesAlexandra Poon, Director

Hungary

KOPINT-TÁRKI Economic Research Ltd.Ágnes Nagy, Project ManagerÉva Palócz, Chief Executive Officer

Iceland

Innovation Center IcelandKarl Fridriksson, Managing Director of Human Resources and

ServicesRosa Signy Gisladottir, Manager, Marketing and Media RelationsThorsteinn I. Sigfusson, Director

India

Confederation of Indian IndustryChandrajit Banerjee, Director-GeneralTarun Das, Chief MentorT S Vishwanath, Senior Director and Head, International

Trade Policy

Indonesia

Kadin IndonesiaM.S. Hidayat, ChairmanTulus Tambunan, Director

Ireland

Competitiveness Survey Group, Department of Economics,University College Cork

Eleanor Doyle, Professor, Department of EconomicsNiall O’SullivanBernadette Power

National Competitiveness CouncilAdrian Devitt, ManagerCaoimhe Gavin, Policy AdvisorGráinne Greehy, Graduate Trainee

Israel

Manufacturers’ Association of Israel (MAI)Shraga Brosh, PresidentDan Catarivas, DirectorYehuda Segev, Managing Director

Italy

SDA Bocconi School of ManagementSecchi Carlo, Full Professor of Economic Policy, Bocconi UniversityPaola Dubini, Associate Professor, Bocconi UniversityFrancesco A. Saviozzi, SDA Assistant Professor, Strategic and

Entrepreneurial Management Department

Jamaica

Mona School of Business (MSB), University of the West IndiesPatricia Douce, Survey CoordinatorMichelle Tomlinson, Survey CoordinatorNeville Ying, Executive Director and Professor

Japan

Hitotsubashi University, Graduate School of International Corporate Strategy (ICS)

in cooperation with Keizai Doyukai (Japan Association of Corporate Executives)

Yoko Ishikura, ProfessorKiyohiko Ito, Vice-President and General Manager for Policy

Studies, Keizai Doyukai

Jordan

Ministry of Planning & International CooperationJordan National Competitiveness TeamRafat Al-Rawabdeh, Senior Researcher

Kazakhstan

Corporation for Export Development and PromotionVakhit Mamatayev, ConsultantGaziz Myltykbayev, Deputy Chairman of the BoardKassen Pernebayev, Director, Analytical Department

Kenya

Institute for Development Studies, University of NairobiMohamud Jama, Director and Associate ProfessorPaul Kamau, Research FellowDorothy McCormick, Associate Professor

Korea, Republic of

Korea Advanced Institute of Science and Technology—KAISTMyungchul Shin, Head, School AdministrationBae Soonhoon, Vice President and Professor, Graduate School of

ManagementYoujin Sung, Manager, Exchange Program

Kuwait

Economics Department, Kuwait UniversityAbdullah Alsalman, Assistant ProfessorMohammed El-Sakka, ProfessorReyadh Faras, Assistant Professor

Kyrgyz Republic

Economic Policy Institute “Bishkek Consensus”Lola Abduhametova, Program CoordinatorMarat Tazabekov, Chairman

Latvia

Institute of Economics, Latvian Academy of Sciences, RigaRaita Karnite, Director

Lesotho

Mohloli Chamber of BusinessRefiloe Kepa, General Manager

Libya

National Economic Development BoardEntisar Elbahi, Executive Office Manager

Lithuania

Statistics LithuaniaOna Grigiene, Head, Economical Survey DivisionAlgirdas Semeta, Director General

Luxembourg

Chamber of Commerce of the Grand Duchy of LuxembourgFrançois-Xavier Borsi, Attaché, Economic DepartmentPhilippe Courtin, Attaché, Economic DepartmentCarlo Thelen, Chief Economist, Member of the Managing Board

Macedonia, FYR

National Entrepreneurship and Competitiveness Council (NECC)Dejan Janevski, Project CoordinatorZoran Stavreski, President of the Managing BoardSaso Trajkoski, Executive Director

Madagascar

Centre of Economic Studies, University of AntananarivoPépé Andrianomanana, DirectorRazato Raharijaona Simo, Executive Secretary

Malawi

Malawi Confederation of Chambers of Commerce and IndustryChancellor L. Kaferapanjira, Chief Executive Officer

Malaysia

Institute of Strategic and International Studies (ISIS)Tan Sri Mohamed Jawhar Hassan, Chairman and Chief Executive

OfficerMahani Zainal Abidin, Director-GeneralSteven C.M. Wong, Assistant Director-General

Malaysia Productivity Corporation (MPC)Dato’ Nik Zainiah Nik Abdul Rahman, Director GeneralChan Kum Siew, Director, International Competitiveness Division

vii

Part

ner

Inst

itute

s

part1.r2 2/26/09 11:58 AM Page vii

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

Mali

Groupe de Recherche en Economie Appliquée et Théorique(GREAT)

Massa Coulibaly, Coordinator

Malta

Competitive Malta—Foundation for National CompetitivenessMargrith Lutschg-Emmenegger, Vice PresidentAdrian Said, Chief CoordinatorCaroline Sciortino, Research Coordinator

Mauritania

Centre d’Information Mauritanien pour le DéveloppementEconomique et Technique (CIMDET/CCIAM)

Lô Abdoul, Consultant and AnalystKhira Mint Cheikhnani, DirectorHabib Sy, Analyst

Mauritius

Joint Economic Council of MauritiusRaj Makoond, Director

Board of Investment, InvestmauritiusDev Chamroo, Director, Planning & PolicyManisha Dookhony, Manager, Planning & PolicyRaju Jaddoo, Managing Director

Mexico

Center for Intellectual Capital and CompetitivenessErika Ruiz Manzur, Executive DirectorRené Villarreal Arrambide, President and Chief Executive OfficerJesús Zurita González, General Director

Instituto Mexicano Para la Competitividad (IMCO)Gabriela Alarcon Esteva, EconomistManuel J. Molano Ruiz, Deputy General DirectorRoberto Newell Garcia, General Director

PROMEXICO Trade & InvestmentJose Gustavo Hernandez Rodriguez, Business Intelligence UnitLisette Jimenez del Rio, Business Intelligence UnitBernardo von Raesfeld Porras, Business Intelligence Unit

Moldova

Center for Strategic Territorial DevelopmentRuslan Codreanu, Executive DirectorRoman Smolnitchi, Program Coordinator

Mongolia

Open Society Forum (OSF)Munkhsoyol Baatarjav, Manager of Economic PolicyErdenejargal Perenlei, Executive Director

Montenegro

Institute for Strategic Studies and Prognoses (ISSP)Maja Drakic, Project ManagerPetar Ivanovic, Chief Executive OfficerVeselin Vukotic, President

Morocco

Université Hassan IIFouzi Mourji, Professor of Economics

Mozambique

EconPolicy Research Group, Lda.Peter Coughlin, DirectorDonaldo Miguel Soares, ResearcherEma Marta Soares, Assistant

Namibia

Namibian Economic Policy Research Unit (NEPRU)Joel Hinaunye Eita, Senior ResearcherLameck Odada, Research AssistantKlaus Schade, Acting Director

Nepal

Centre for Economic Development and Administration (CEDA)Ramesh Chandra Chitrakar, Executive DirectorMenaka Rajbhandari Shrestha, ResearcherSantosh Kumar Upadhyaya, Researcher

Netherlands

Erasmus Strategic Renewal Center, Erasmus University RotterdamFrans A. J. Van den Bosch, ProfessorHenk W. Volberda, Professor

New Zealand

Business New ZealandMarcia Dunnett, Manager, Sector GroupsPhil O’Reilly, Chief Executive

The New Zealand InstituteDavid Skilling, Chief Executive Officer

Nigeria

Nigerian Economic Summit Group (NESG)Felix Ogbera, Associate Director, ResearchChris Okpoko, Senior Consultant, Research

Norway

BI Norwegian School of ManagementEskil Goldeng, ResearcherTorger Reve, Professor

HSH, The Federation of Norwegian Commercial and ServiceEnterprises

Vibeke H. Madsen, Chief Executive Officer

Oman

The International Research FoundationAzzan Al Busaidi, Chief Executive OfficerSalem Ben Nasser Al-Ismaily, Chairman

Pakistan

Competitiveness Support FundArthur Bayhan, Chief Executive OfficerAmir Jahangir, Manager, Communications

Paraguay

Centro de Análisis y Difusión de Economia Paraguaya (CADEP)Dionisio Borda, DirectorJaime Escobar, Research MemberFernando Masi, Research Member

Peru

Centro de Desarrollo Industrial (CDI), Sociedad Nacional deIndustrias

Néstor Asto, Project DirectorLuis Tenorio, Executive Director

Philippines

Makati Business ClubAlberto A. Lim, Executive DirectorMichael B. Mundo, Chief EconomistMark P. Opulencia, Deputy Director

Poland

Warsaw School of EconomicsBogdan Radomski, Associate Professor

Portugal

PROFORUM, Associação para o Desenvolvimento da EngenhariaIlídio António de Ayala Serôdio, Vice President of the Board of

Directors

Forum de Administradores de Empresas FAEPedro do Carmo Costa, Member of the Board of DirectorsAdilia Lisboa, General Director

Puerto Rico

Puerto Rico 2000, Inc.Suzette M. Jimenez, PresidentFrancisco Montalvo Fiol, Project Coordinator

Qatar

Qatari Businessmen Association (QBA)Issa Abdul Salam Abu Issa, Secretary-GeneralBassam Ramzi Massouh, General ManagerAhmed El-Shaffee, Economist

viii

Part

ner

Inst

itute

s

part1.r2 2/26/09 11:58 AM Page viii

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

Romania

Group of Applied Economics (GEA)Anca Rusu, Program CoordinatorLiviu Voinea, Executive Director

Russian Federation

Bauman Innovation, Academy of National Economy under the Government of the Russian Federation

Alexei Prazdnitchnykh, Principal, Associate Professor

Stockholm School of Economics, RussiaIgor Dukeov, Research FellowCarl F. Fey, Associate Dean of Research

Saudi Arabia

National Competitiveness Center (NCC)Awwad Al-Awwad, Deputy Governor for InvestmentKhaldon Mahasen, Manager, Investment Performance Assessment

Senegal

Centre de Recherches Economiques Appliquées (CREA),University of DakarAly Mbaye, Director

Serbia

Center for Advanced Economic Studies, CEVESVuk Dokovic, DirectorDusko Vasiljevic, Researcher

Singapore

Economic Development BoardLim Hong Khiang, Director Planning 2Chua Kia Chee, Head, Research and Statistics Unit

Slovak Republic

Business Alliance of Slovakia (PAS)Robert Kicina, Executive Director

Slovenia

Institute for Economic ResearchArt Kovacic, ResearcherPeter Stanovnik, Senior Researcher

University of Ljubljana, Faculty of EconomicsMateja Drnovsek, Assistant ProfessorAles Vahcic, Professor

South Africa

Business Leadership South AfricaConnie Motshumi, DirectorMichael Spicer, Chief Executive Officer

Business Unity South AfricaJerry Vilakazi, Chief Executive OfficerVic Van Vuuren, Chief Operating Officer

Spain

IESE Business School, International Center for Competitiveness,Anselmo Rubiralta Center for Globalization and StrategyEduardo Ballarín, ProfessorMaría Luisa Blázquez, Research AssociateAlmudena Clemente Tiemblo, Research Associate

Sri Lanka

Institute of Policy StudiesIndika Siriwardena, Database Manager

The Ceylon Chamber of CommercePrema Cooray, Secretary General

Suriname

Institute for Development Oriented Studies (IDOS)Ashok Hirschfeld, Qualitative ResearchJohn R. P. Krishnadath, President

Sweden

Center for Strategy and Competitiveness, Stockholm School of Economics

Christian Ketels, Senior Research FellowÖrjan Sölvell, Professor

Switzerland

University of St. Gallen, Executive School of Management,Technology and Law (ES-HSG)

Franz Jaeger, ProfessorBeat Bechtold, Project Manager

Syria

Ministry of Economy and TradeAmer Housni Louitfi, Minister of Economy and Trade

State Planning CommissionTayseer Al-Ridawi, Head of State Planning Commission

UNDP Damascus, “Towards Changing the Mindset forCompetitiveness”

Nuhad Dimashkiyyah, National Project Director

Taiwan, China

Council for Economic Planning and Development, Executive YuanTain-Jy Chen, ChairmanJ. B. Hung, Director, Economic Research DepartmentChung Chung Shieh, Researcher, Economic Research Department

Tajikistan

The Center for Sociological Research “Zerkalo”Qahramon Baqoev, DirectorOl’ga Es’kina, ResearcherAlikul Isoev, Sociologist and Economist

Tanzania

Economic and Social Research FoundationIrene Alenga, Commissioned Studies DepartmentHaidari Amani, Executive Director and ProfessorDennis Rweyemamu, Commissioned Studies Department

Thailand

Sasin Graduate Institute of Business Administration, Chulalongkorn University

Pongsak Hoontrakul, Senior Research FellowToemsakdi Krishnamra, Director of SasinPiyachart Phiromswad, Faculty of Economics

Thailand Development Research Institute (TDRI)Somchai Jitsuchon, Research DirectorChalongphob Sussangkarn, Distinguished FellowYos Vajragupta, Senior Researcher

Trinidad and Tobago

Arthur Lok Jack Graduate School of BusinessKeston Daniel, Research OfficerFaheem Mohammed, Engagement ManagerMark Oakley, Acting Executive Director

Tunisia

Institut Arabe des Chefs d’EntreprisesMajdi Hassen, Executive CounsellorChekib Nouira, President

Turkey

TUSIAD Sabanci University Competitiveness ForumA. Gunduz Ulusoy, Director and ProfessorHande Yegenoglu, Project Specialist

Uganda

Makerere Institute of Social Research, Makerere UniversityRobert Apunyo, Research AssociateDelius Asiimwe, Senior Research FellowCatherine Ssekimpi, Research Associate

Ukraine

CASE Ukraine, Center for Social and Economic ResearchDmytro Boyarchuk, Executive DirectorVladimir Dubrovskiy, Senior Economist

United Arab Emirates

Economic & Policy Research Unit (EPRU), Zayed UniversityJay Squalli, Assistant ProfessorNico Vellinga, Professor

Dubai Competitiveness CouncilAdel Alfalasi, Director

ix

Part

ner

Inst

itute

s

part1.r2 2/26/09 11:58 AM Page ix

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

United States

US Chamber of CommerceScott Eisner, Deputy Chief of StaffCecile Remington, Marketing ManagerJames Robinson, Senior Vice President and Counselor

to the President

Uruguay

Universidad ORTIsidoro Hodara, Professor

Venezuela

CONAPRI—Venezuelan Council for Investment PromotionAna Acosta, Economic AnalystAdolfo Castejón, Investor Services ManagerGiuseppe Rionero, Economic Affairs Manager

Vietnam

Central Institute for Economic Management (CIEM)Dinh Van An, PresidentPhan Thanh Ha, Deputy Director, Department of Macroeconomic

ManagementPham Hoang Ha, Senior Researcher, Department of

Macroeconomic Management

Institute for Economic Research of HCMCNguyen Van Quang, Vice DirectorDu Phuoc Tan, Head, Department of Urban Development StudiesTrieu Thanh Son, Research Fellow

Zambia

Institute of Economic and Social Research (INESOR), University of Zambia

Mutumba M. Bull, DirectorPatricia Funjika, Staff Development FellowJolly Kamwanga, Coordinator

Zimbabwe

Graduate School of Management, University of ZimbabweA. M. Hawkins, Professor

Bolivia, Costa Rica, Dominican Republic, Ecuador, El Salvador,

Honduras, Nicaragua, Panama

INCAE Business School, Latin American Center forCompetitiveness and Sustainable Development

Arturo Condo, RectorMarlene de Estrella, Director of External RelationsLuis Reyes, ManagerRoy Zuñiga, Dean

Latvia, Lithuania

Stockholm School of Economics in RigaKarlis Kreslins, Executive MBA Program DirectorAnders Paalzow, Rector

x

Part

ner

Inst

itute

s

part1.r2 2/26/09 11:58 AM Page x

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

The past year has been a difficult one for the Travel &Tourism (T&T) sector. High oil prices through thesummer of 2008, diminished tourism demand due tothe international economic crisis, and concerns aboutterrorism have raised many challenges for the industry.Yet, despite these difficulties, the T&T sector remains acritical one for the world economy, still accounting for asignificant share of global gross domestic product andemployment, and providing an important opportunityfor developing countries to move up the value chaintoward the production of higher value-added services.In this context, an analysis of the T&T competitivenessof individual countries around the world is particularlypertinent at this time.This is the fundamental objectiveof this third edition of The Travel & TourismCompetitiveness Report (TTCR).

For the past four years, the World Economic Forumhas engaged key industry and thought leaders throughits Aviation,Travel & Tourism Industry PartnershipProgramme to carry out an in-depth analysis of theT&T competitiveness of economies around the world.The goal is to construct a platform for multi-stakehold-er dialogue to ensure the development of strong andsustainable national T&T industries capable of con-tributing effectively to international economic develop-ment.The theme of this third edition of the TTCR,“Managing in a time of turbulence,” reflects the myriadof complexities facing the industry at this time, whichmust be overcome to ensure strong sectoral growthgoing into the future.

At the core of this year’s Report is the third editionof the Travel & Tourism Competitiveness Index (TTCI).The aim of the TTCI, which covers a record 133economies this year, is to provide a comprehensivestrategic tool for measuring “the factors and policies thatmake it attractive to develop the T&T sector in differentcountries.” By providing detailed assessments of theT&T environments in countries worldwide, the resultscan be used by all stakeholders to work together toimprove the industry’s competitiveness in their nationaleconomies, thereby contributing to national growth andprosperity.The same overall index structure used lastyear has been retained, making meaningful inter-yearcomparisons possible and allowing countries to tracktheir progress over time in the various areas measured.

The Report contains detailed profiles for each of the133 economies featured in the study, as well as anextensive section of data tables with global rankings

covering over 70 indicators included in the TTCI. Inaddition, the Report includes insightful contributionsfrom a number of industry experts.These chaptersexplore issues such as the impact of higher oil prices onthe tourism industry, the importance of price competi-tiveness for attracting tourists, and the extent to whichthe TTCI explains differences in travel intensity amongcountries.

The Travel & Tourism Competitiveness Report couldnot have been put together without the distinguishedthinkers who have shared with us their knowledge andexperience.We are grateful to our Strategic DesignPartner, Booz & Company, and our Data PartnersDeloitte, the International Air Transport Association(IATA), the International Union for Conservation ofNature (IUCN), the World Tourism Organization(UNWTO), and the World Travel & Tourism Council(WTTC) for helping us to design and develop theTTCI and for providing much of the industry-relevantdata used in its calculation.We thank our IndustryPartners in this Report—Abercrombie & Kent,Airbus,Bombardier, British Airways, Carlson, Emirates Group,Etihad Airways, Hertz, JetAirways, NetJets Europe,Silversea, Swiss International Airlines, and Rolls-Royce—for their support in this important venture.Our thanks also goes out to our academic advisors onthe Report, Larry Dwyer, Qantas Professor of Travel andTourism Economics in the Australian School of Businessat the University of New South Wales, and PeterForsyth, Professor of Economics at Monash University.

We also wish to thank the editors of the Report,Jennifer Blanke and Thea Chiesa, for their energy andtheir commitment to the project.Appreciation also goesto Fiona Paua, Head of Strategic Insight Teams, and theother members of the competitiveness team: CiaraBrowne,Agustina Ciocia, Margareta Drzeniek Hanouz,Thierry Geiger, Irene Mia, Pearl Samandari, and EvaTrujillo Herrera. Finally, we would like to convey oursincere gratitude to our network of 150 PartnerInstitutes worldwide, without whose enthusiasm andhard work the annual administration of the ExecutiveOpinion Survey and this Report would not be possible.

xi

Pref

ace

PrefaceKLAUS SCHWAB,

Executive Chairman, World Economic Forum

part1.r2 2/26/09 11:58 AM Page xi

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

part1.r2 2/26/09 11:58 AM Page xii

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

The past few years have witnessed many storms in theTravel & Tourism (T&T) industry.These have rangedfrom mounting concerns about terrorism in severalregions to the high cost of fuel and lower tourism-basedspending linked to the current economic downturn. Inthis context, this third edition of The Travel & TourismCompetitiveness Report is being released at a time whenthe industry finds itself at a crossroads with regard tohow to address these diverse and mounting challenges.

Yet, despite the current difficulties, the Travel &Tourism sector remains a critical economic sectorworldwide and one that provides significant potentialfor economic growth and development internationally.A growing national T&T sector contributes to employ-ment, raises national income, and can improve a country’sbalance of payments.The sector is thus an importantdriver of growth and prosperity and, particularly withindeveloping countries, it can play a leading role in povertyreduction.

Given the importance of the T&T sector, four yearsago the World Economic Forum, together with itsIndustry and Data Partners, embarked on a multi-yearresearch effort aimed at exploring various issues relatedto the T&T competitiveness of nations around the world.This year’s Report is published under the theme of“Managing in a time of turbulence,” reflecting the manydifficulties the industry presently faces, which must beovercome to ensure strong sectoral growth going intothe future.This is particularly captured by the topicscovered by the analytical chapters, which will bedescribed below.

The Travel & Tourism Competitiveness IndexDespite the overall importance of developing the T&Tsector, many obstacles at the national level continue tohinder its development. In this light,The Travel &Tourism Competitiveness Index (TTCI) has been devel-oped to measure the many different regulatory and busi-ness-related issues that have been identified as levers forimproving T&T competitiveness in countries around theworld.Through detailed analysis of each pillar and sub-pillar of the Index, businesses and governments canaddress the challenges to the sector’s growth.

The TTCI has been developed within the contextof the World Economic Forum’s Industry PartnershipProgramme for the Aviation,Travel and Tourism sector.

The Index was developed in close collaboration withour Strategic Design Partner Booz & Company and ourData Partners Deloitte, the International Air TransportAssociation (IATA), the International Union forConservation of Nature (IUCN), the World TourismOrganization (UNWTO), and the World Travel &Tourism Council (WTTC).We have also receivedimportant feedback from a number of key companiesthat are Industry Partners in the effort, namelyAbercrombie & Kent,Airbus, Bombardier, BritishAirways, Carlson, Emirates Group, Etihad Airways,Hertz, JetAirways, NetJets Europe, Silversea, SwissInternational Airlines, and Rolls-Royce. Several thoughtleaders from these organizations have also contributedinsightful papers addressing various aspects of T&Tcompetitiveness, which are described below.

The TTCI aims to measure the factors and policiesthat make it attractive to develop the T&T sector in differentcountries. It is based on three broad categories of variablesthat facilitate or drive T&T competitiveness.These categories are summarized into the three subindexes ofthe Index: (1) the T&T regulatory framework subindex;(2) the T&T business environment and infrastructuresubindex; and (3) the T&T human, cultural, and naturalresources subindex.

Each of these three subindexes is composed in turnby a number of pillars of T&T competitiveness, ofwhich there are 14 in all.These are:

1. Policy rules and regulations2. Environmental sustainability3. Safety and security4. Health and hygiene5. Prioritization of Travel & Tourism6. Air transport infrastructure7. Ground transport infrastructure8. Tourism infrastructure9. ICT infrastructure

10. Price competitiveness in the T&T industry11. Human resources12. Affinity for Travel & Tourism13. Natural resources14. Cultural resources

Each of the pillars is, in turn, made up of a numberof individual variables.The dataset includes both harddata and Survey data from the World Economic Forum’s

xiii

Exec

utiv

e Su

mm

ary

Executive SummaryJENNIFER BLANKE

THEA CHIESA

World Economic Forum

part1.r2 2/26/09 11:58 AM Page xiii

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

annual Executive Opinion Survey.The hard data wereobtained from publicly available sources, internationalorganizations, and T&T institutions and experts (forexample, IATA, the IUCN, the UNWTO, the WTTC,UNCTAD, and UNESCO).The Survey is carried outamong CEOs and top business leaders in all economiescovered by our research; these are the people makingthe investment decisions in their respective economies.The Survey provides unique data on many qualitativeinstitutional and business environment issues, as well asspecific issues related to the T&T industry and the qual-ity of the natural environment.The exact methodologyunderlying the construction of the TTCI is described inChapter 1.1.

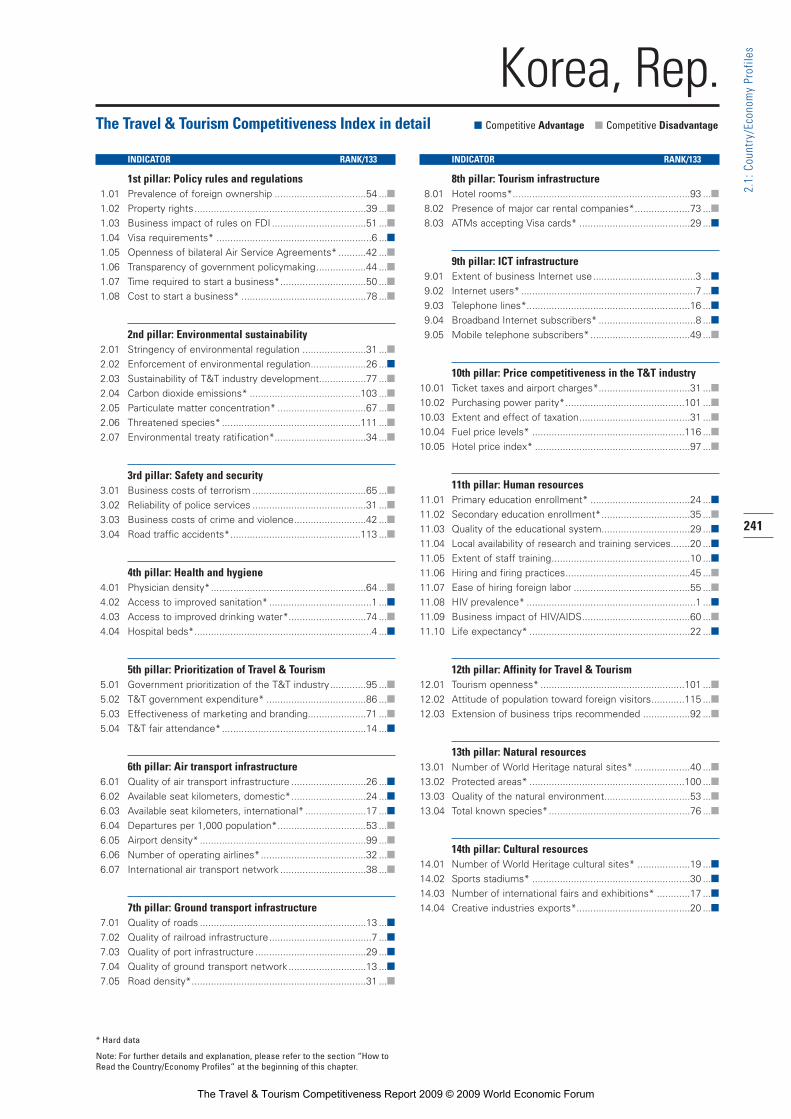

The Travel & Tourism Competitiveness Index rankings2009Table 1 shows the overall ranking for the 133 countriesincluded in this year’s TTCI, comparing this year’s ranking with that of last year, showing all countriesranked together.The table shows that the top threecountries in the overall ranking remain the same as last year, with three European countries—Switzerland,Austria, and Germany—continuing to lead the way inT&T competitiveness.

Tables 2–5 show the rankings in a regional context,grouping countries into the following four regionalgroups: the Americas, Europe, Middle East and Africa,and Asia Pacific (including Central Asia).We discuss aselection of countries from each region to provide asense of the results and how they are interpreted at thenational level. More countries are discussed in detail inChapter 1.1.

EuropeTable 2 shows the rankings for just European countries,with the first column showing the rank within theregion, and the second column showing the overall rankout of all 133 countries included in the index this year.As the table shows, Switzerland is ranked first out of allcountries in the 2009 TTCI, followed by Austria andGermany, the same top three countries for the past threeyears.

Switzerland is a country rich in cultural and natural resources, including an impressive number ofWorld Heritage cultural and natural sites for a countryof its size.A large percentage of the country’s land areais protected (ranked 16th), and the natural environmentis assessed as being among the most pristine in theworld (ranked 9th).This natural heritage is buttressed bya strong national focus on environmental sustainability:Switzerland is ranked 2nd overall on this pillar, based onstrong and well-enforced environmental legislation andwith a particular focus on developing the T&T sectorsustainably.

Switzerland is not only an attractive leisure tourismdestination but is also an important business travel hub,with many international fairs and exhibitions held in the country each year. Staffing of the industry is alsofacilitated by the availability of qualified labor to workin Travel & Tourism (ranked 3rd), perhaps not surprisingin a country with many of the best hotel managementschools.Added to these strengths is Switzerland’s excellentground transport infrastructure (ranked 1st worldwide),with top-quality roads and railroads and an excellentdomestic transport network.Also well assessed is thespecific tourism infrastructure (ranked 7th), with readilyavailable hotel rooms and automated teller machines(ATMs) for cash withdrawals. Such high-quality infra-structure makes a tourist’s stay in the country easy andcomfortable, an experience that is reinforced by thehigh level of general safety and security (ranked 8th).

Austria is ranked 2nd in Europe and out of allcountries in the TTCI, a ranking attributable to its richcultural resources, with eight World Heritage culturalsites and with many fairs and exhibitions catering tobusiness travelers.The natural environment is also wellassessed, along with the country’s focus on environmen-tal sustainability (ranked 9th). In addition,Austrians areperceived as open and welcoming to foreign travelers.Austria’s tourism infrastructure is assessed as second tonone, with abundant car rental facilities, hotel accom-modations, and ATMs. Other strengths include Austria’sassessment as one of the safest countries in the world(ranked 6th) and its excellent health and hygiene levels(ranked 5th).

Germany, ranked 3rd out of all countries, is alsocharacterized by abundant cultural resources, ranked 4thworldwide for its 32 World Heritage cultural sites and2nd for the number of international fairs and exhibitionsheld in the country.The country’s infrastructure isamong the best in the world, ranked 5th for the qualityof its ground transport infrastructure and 7th for its airtransport infrastructure. In addition, Germany getssomewhat better marks than Switzerland and Austria forthe policy rules and regulations affecting the T&Tindustry: it is ranked 17th in this area, with transparentpolicymaking, well-protected property rights, and bilat-eral Air Service Agreements that are assessed as open.

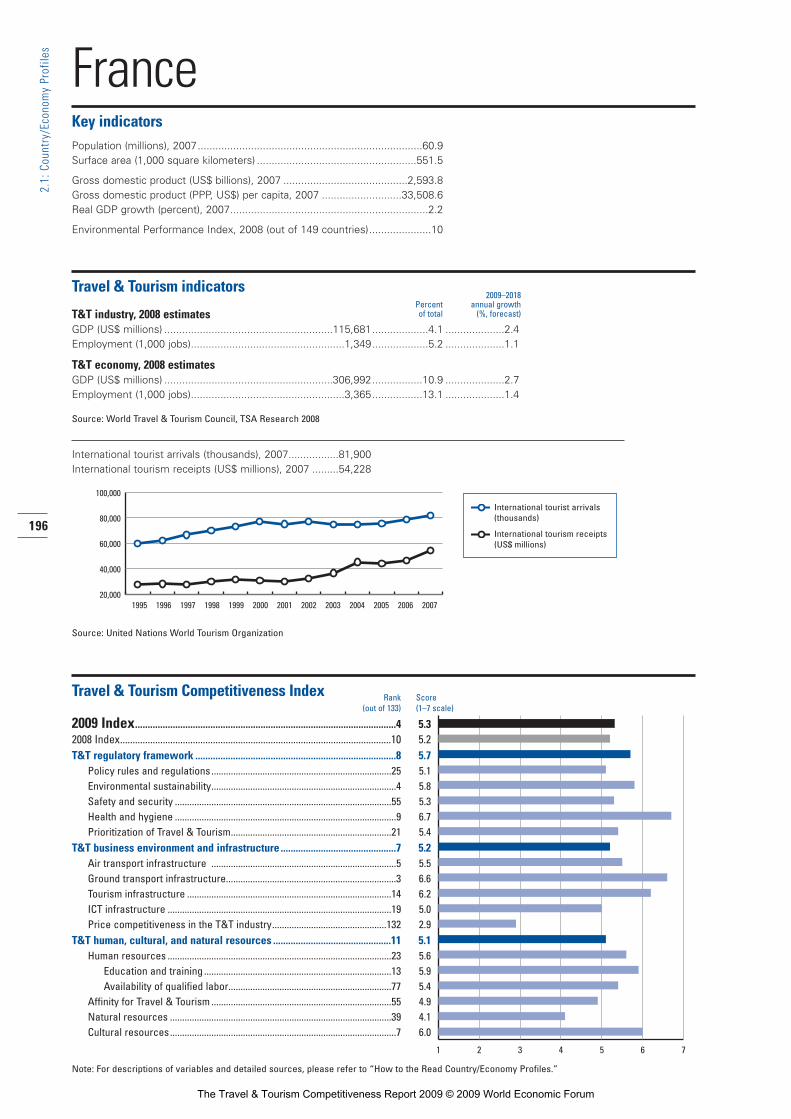

France moves up this year by six places, ranking4th out of all 133 countries. France attracts tourists withits rich cultural heritage (ranked 4th for the number ofWorld Heritage cultural sites and 7th for creative indus-tries).The country also hosts many international fairsand exhibitions (ranked 5th), thereby attracting businesstravelers as well. France’s ground transport infrastructureis among the best in the world (ranked 3rd), with thequality of roads and railroads particularly well assessed, aswell as its air transport infrastructure (ranked 5th).Thecountry’s improvement is in part attributable to astronger perceived prioritization by the government ofthe sector and increased marketing of the country

xiv

Exec

utiv

e Su

mm

ary

part1.r2 2/26/09 11:58 AM Page xiv

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

xv

Exec

utiv

e Su

mm

ary

2009 2008Country/Economy Rank/133 Score Rank/130

Switzerland 1 5.68 1Austria 2 5.46 2Germany 3 5.41 3France 4 5.34 10Canada 5 5.32 9Spain 6 5.29 5Sweden 7 5.28 8United States 8 5.28 7Australia 9 5.24 4Singapore 10 5.24 16United Kingdom 11 5.22 6Hong Kong SAR 12 5.18 14Netherlands 13 5.09 18Denmark 14 5.08 13Finland 15 5.07 12Iceland 16 5.07 11Portugal 17 5.01 15Ireland 18 4.99 21Norway 19 4.97 17New Zealand 20 4.94 19Cyprus 21 4.92 24Belgium 22 4.92 27Luxembourg 23 4.92 20Greece 24 4.91 22Japan 25 4.91 23Czech Republic 26 4.86 30Estonia 27 4.83 26Italy 28 4.78 28Malta 29 4.77 25Barbados 30 4.77 29Korea, Rep. 31 4.72 31Malaysia 32 4.71 32United Arab Emirates 33 4.57 40Croatia 34 4.54 34Slovenia 35 4.53 36Israel 36 4.50 35Qatar 37 4.49 37Hungary 38 4.45 33Thailand 39 4.45 42Mauritius 40 4.43 41Bahrain 41 4.42 48Costa Rica 42 4.42 44Taiwan, China 43 4.40 52Tunisia 44 4.37 39Brazil 45 4.35 49Slovak Republic 46 4.34 38China 47 4.33 62Latvia 48 4.31 45Lithuania 49 4.30 47Bulgaria 50 4.30 43Mexico 51 4.29 55Montenegro 52 4.29 59Puerto Rico 53 4.27 46Jordan 54 4.25 53Panama 55 4.23 50Turkey 56 4.20 54Chile 57 4.18 51Poland 58 4.18 56Russian Federation 59 4.14 64Jamaica 60 4.13 57South Africa 61 4.10 60India 62 4.09 65Uruguay 63 4.09 61Egypt 64 4.09 66Argentina 65 4.08 58Romania 66 4.04 69Dominican Republic 67 4.03 63

(Cont’d.)

2009 2008Country/Economy Rank/133 Score Rank/130

Oman 68 4.01 76Brunei Darussalam 69 3.99 n/aGuatemala 70 3.90 68Saudi Arabia 71 3.89 82Colombia 72 3.89 71Georgia 73 3.89 72Peru 74 3.88 70Morocco 75 3.86 67Azerbaijan 76 3.84 79Ukraine 77 3.84 77Sri Lanka 78 3.82 73Botswana 79 3.81 87Macedonia, FYR 80 3.81 83Indonesia 81 3.79 80Namibia 82 3.77 93Honduras 83 3.77 75Trinidad and Tobago 84 3.75 74Syria 85 3.73 94Philippines 86 3.73 81Gambia, The 87 3.72 84Serbia 88 3.71 78Vietnam 89 3.70 96Albania 90 3.68 92Armenia 91 3.65 89Kazakhstan 92 3.65 91Moldova 93 3.64 98El Salvador 94 3.63 97Kuwait 95 3.63 85Ecuador 96 3.62 86Kenya 97 3.60 101Tanzania 98 3.59 88Suriname 99 3.54 95Zambia 100 3.53 107Senegal 101 3.50 108Guyana 102 3.50 109Nicaragua 103 3.49 99Venezuela 104 3.46 103Mongolia 105 3.46 100Kyrgyz Republic 106 3.45 113Bosnia and Herzegovina 107 3.44 105Cambodia 108 3.43 112Tajikistan 109 3.41 114Ghana 110 3.40 n/aUganda 111 3.38 110Libya 112 3.38 104Pakistan 113 3.33 111Bolivia 114 3.33 106Algeria 115 3.31 102Madagascar 116 3.28 118Malawi 117 3.27 n/aNepal 118 3.25 116Mali 119 3.19 119Benin 120 3.18 120Zimbabwe 121 3.17 117Paraguay 122 3.16 115Ethiopia 123 3.15 121Mozambique 124 3.12 123Cameroon 125 3.09 126Burkina Faso 126 3.08 124Mauritania 127 3.07 122Nigeria 128 3.02 125Bangladesh 129 3.02 127Côte d’Ivoire 130 2.99 n/aBurundi 131 2.98 128Lesotho 132 2.92 129Chad 133 2.52 130

Note that one country covered last year, Uzbekistan, is not included this yearbecause of a lack of Survey data.

Table 1: Travel & Tourism Competitiveness Index 2009 and 2008 comparisons

part1.r2 2/26/09 11:58 AM Page xv

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

through participation in a larger number of internation-al tourism fairs. Ensuring the sustainable development ofthe sector is also a significant priority for the govern-ment, with France ranked a high 4th on this pillar, withstrong and well-enforced environmental legislation.

Spain is ranked just behind France within Europe,at 6th place overall. Spain is ranked 1st out of all coun-tries for the richness of its cultural resources, with manyWorld Heritage sites, a large number of internationalfairs and exhibitions, and significant sports stadium capac-ity. Spain’s tourism infrastructure is ranked 1st interna-tionally, with many hotel rooms, car rental facilities, and

ATMs; its air transport infrastructure also gets goodmarks (ranked 10th).The government prioritizes thesector significantly, and the country makes strong effortsto attract tourists through strong destination-marketingcampaigns and by ensuring Spain’s presence at manyinternational tourism fairs.

Greece is ranked 18th in Europe and 24th overall,with a stable performance compared with last year.The country benefits from rich cultural resources(ranked 23rd), excellent health and hygiene (ranked19th overall), and top-notch tourism infrastructure (5th).Greece is ranked a very high 3rd in terms of the

xvi

Exec

utiv

e Su

mm

ary

Table 2: The Travel & Tourism Competitiveness Index: Europe

SUBINDEXES

T&T business environment T&T human, cultural, OVERALL INDEX T&T regulatory framework and infrastructure and natural resources

Country/Economy Regional rank Overall rank Score Rank Score Rank Score Rank Score

Switzerland 1 1 5.68 1 6.01 1 5.49 2 5.54Austria 2 2 5.46 4 5.91 6 5.22 7 5.24Germany 3 3 5.41 13 5.56 3 5.44 9 5.22France 4 4 5.34 8 5.67 7 5.22 11 5.13Spain 5 6 5.29 29 5.29 8 5.21 5 5.36Sweden 6 7 5.28 12 5.57 14 5.04 8 5.23United Kingdom 7 11 5.22 28 5.29 11 5.07 6 5.30Netherlands 8 13 5.09 22 5.44 9 5.08 17 4.75Denmark 9 14 5.08 10 5.59 10 5.08 28 4.57Finland 10 15 5.07 5 5.82 25 4.69 21 4.71Iceland 11 16 5.07 3 5.92 17 4.93 39 4.37Portugal 12 17 5.01 15 5.52 24 4.74 16 4.78Ireland 13 18 4.99 7 5.73 22 4.79 32 4.45Norway 14 19 4.97 9 5.64 19 4.84 36 4.42Cyprus 15 21 4.92 25 5.35 13 5.05 37 4.38Belgium 16 22 4.92 21 5.45 32 4.56 20 4.73Luxembourg 17 23 4.92 20 5.47 16 4.97 42 4.30Greece 18 24 4.91 18 5.49 27 4.66 27 4.58Czech Republic 19 26 4.86 16 5.50 36 4.41 24 4.67Estonia 20 27 4.83 17 5.50 21 4.81 47 4.19Italy 21 28 4.78 46 4.96 26 4.68 22 4.71Malta 22 29 4.77 11 5.58 31 4.58 52 4.15Croatia 23 34 4.54 43 5.02 37 4.32 43 4.28Slovenia 24 35 4.53 38 5.13 33 4.53 61 3.94Hungary 25 38 4.45 26 5.35 42 4.06 59 3.95Slovak Republic 26 46 4.34 34 5.20 54 3.78 55 4.05Latvia 27 48 4.31 32 5.22 43 4.04 86 3.68Lithuania 28 49 4.30 30 5.27 46 3.98 89 3.65Bulgaria 29 50 4.30 56 4.74 48 3.96 46 4.20Montenegro 30 52 4.29 50 4.86 66 3.57 35 4.43Turkey 31 56 4.20 63 4.60 60 3.73 44 4.28Poland 32 58 4.18 72 4.44 68 3.53 29 4.56Russian Federation 33 59 4.14 79 4.35 61 3.70 38 4.37Romania 34 66 4.04 61 4.68 64 3.61 77 3.83Georgia 35 73 3.89 33 5.20 99 2.84 92 3.64Ukraine 36 77 3.84 62 4.66 72 3.37 103 3.50Macedonia, FYR 37 80 3.81 69 4.46 75 3.29 87 3.67Serbia 38 88 3.71 78 4.35 80 3.20 96 3.57Albania 39 90 3.68 77 4.38 104 2.76 66 3.89Armenia 40 91 3.65 58 4.70 105 2.75 102 3.51Moldova 41 93 3.64 67 4.53 95 2.95 110 3.43Bosnia and Herzegovina 42 107 3.44 96 4.11 93 2.96 124 3.25

part1.r2 2/26/09 11:58 AM Page xvi

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

country’s overall prioritization of Travel & Tourism.Further, there is a strong national affinity for tourismcompared with many other European countries, includ-ing a generally open and positive attitude towardtourists (16th).The country’s overall ranking is heldback, however, by its policy rules and regulations thatare not entirely supportive of the sector’s development(ranked 57th), with stringent rules governing foreigndirect investment (FDI), and with foreign ownershiprestrictions, as well as significant time and cost involvedin starting a new company.Another area of weakness isthe country’s ground transport infrastructure, which isless efficient than in many other European countries(the quality of railroads and ports being of particularconcern).

Italy, despite being endowed with the most WorldHeritage cultural sites in the world, ranks only 21stwithin Europe and 28th overall (the same rank as lastyear).As well as its cultural richness, Italy’s strengths liein areas such as the health and hygiene of the country(27th), its air transport infrastructure (27th), and espe-cially its excellent tourism infrastructure (3rd). However,it faces a number of challenges that bring its overall ratingdown.These include policy rules and regulations, whereItaly ranks 71st (even lower than last year) because of itsvery strong foreign ownership restrictions (ranked106th) and rules governing FDI (122nd). Further, thegovernment is not seen to be prioritizing this sector(107th), which is so important to the overall economy.In addition, ground transport infrastructure requiresupgrading, there is insufficient focus on developing thesector in an environmentally sustainable way, and thereare some safety and security concerns in the country(82nd).

The AmericasTable 3 shows the regional rankings for the countries inthe Americas.As the table shows, Canada is the high-est-ranked country in the region, ranked 5th out of all133 countries and with an improvement of four placesallowing it to overtake the United States this year forthe top regional spot. Canada’s natural resources consti-tute a key strength, with the country’s nine WorldHeritage natural sites placing it 4th internationally. Itscultural resources are also a strong point, with manyinternational fairs and exhibitions in the country andstrong creative industries in particular. Canada’s air trans-port infrastructure is ranked 1st out of all countries, andit also gets good marks for its tourism and ICT infra-structure, facilitating the online T&T environment.Canada’s policy environment is very conducive to thedevelopment of the sector (ranked 5th, up three placesfrom last year), and the government is seen to be morestrongly prioritizing the sector than last year. For moredetails on Canada’s T&T competitiveness see Box 2 inChapter 1.1.

The United States is ranked 2nd in the Americasand 8th out of all countries, down one position fromlast year.The country places 2nd for the overall businessenvironment and infrastructure and 1st for the country’shuman, cultural, and natural resources. In particular, theUnited States has an excellent air transport infrastructure(ranked 2nd) and high-quality tourism and ICT infra-structure. Its natural resources are ranked 1st out of allcountries, with many nationally protected areas and manyWorld Heritage natural sites, although a perception existsthat the environment is not being sufficiently protected(ranked 106th for environmental sustainability). Safetyand security, ranked 122nd, is also of concern: as well asworries about crime and violence, the country has oneof the highest death rates from road traffic accidents outof all countries covered (ranked 125th).

Barbados is ranked 3rd in the region, at 30thoverall, down one place from last year. Barbados isranked 2nd overall for the country’s affinity for Travel &Tourism, with a positive attitude toward tourists andtoward the value of tourism in the country.The govern-ment is prioritizing the sector to a very high degree(ranked 2nd), spending a high percentage of GDP onthe sector and ensuring effective destination-marketingcampaigns. Further, the country has a regulatory envi-ronment that is quite conducive to the development ofthe sector, requiring few visitors to have visas to enterthe country and with open bilateral Air ServiceAgreements.

Costa Rica is ranked 4th in the region and 42ndoverall, up two places from last year.The country getsexcellent marks for its natural resources (ranked 6th),with several World Heritage sites, a high percentage ofnationally protected areas, and its very diverse fauna.Given the importance of the natural environment forthe county’s tourism industry, it is notable that it ranks ahigh 27th overall for environmental sustainability, anarea of measurable improvement since last year.However, safety and security remains a concern (72nd).Further, although its tourism infrastructure is well devel-oped (33rd), with a strong presence of major car rentalcompanies and abundant hotel rooms, ground transportinfrastructure requires significant upgrading (103rd), par-ticularly roads and ports, making travel in the countrysomewhat difficult.

Brazil is ranked 5th in the Americas and 45thoverall, having seen an improvement of four places sincelast year.The country is ranked 2nd out of all countriesfor its natural resources and 14th for its cultural resources,with many World Heritage sites, a great proportion ofprotected land area, and the most diverse fauna in theworld.This is buttressed by a focus on environmentalsustainability (ranked 33rd). However, the ground trans-port network remains underdeveloped, with the qualityof roads, ports, and railroads ranked 110th, 123rd, and86th, respectively. Safety and security continues to be ofserious concern, ranked 130th overall, just behind South

xvii

Exec

utiv

e Su

mm

ary

part1.r2 2/26/09 11:58 AM Page xvii

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

Africa and Russia.The country also suffers greatly froma lack of price competitiveness (91st), attributable in partto high ticket taxes and airport charges in the country,as well as high prices and high taxation more generally.Further, the overall policy environment is not particular-ly conducive to the development of the sector (ranked95th), with discouraging rules on FDI and much timerequired for starting a business.

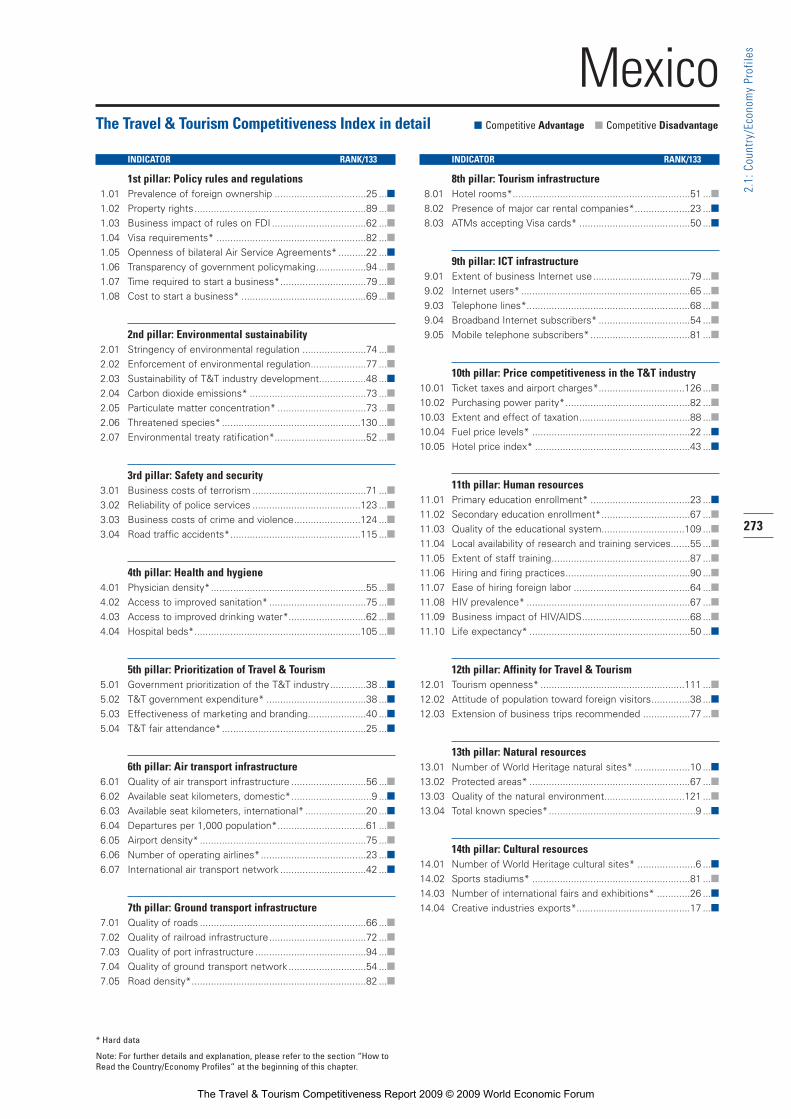

Mexico is ranked just behind Brazil in the regionalranking at 6th place and comes in at 51st place overall,an improvement of four places. Mexico gets quite highmarks for its natural resources (ranked 18th), and this isan area where it has shown an improvement since lastyear, with one more natural World Heritage site addedin the interval.The country’s cultural resources are alsovery rich (20th), with 26 World Heritage cultural sites,several international fairs and exhibitions, and strongcreative industries.These inherent strengths are rein-forced by the overall prioritization of the sector in thecountry (35th), with country-level participation at manyT&T fairs and effective marketing and branding cam-paigns for attracting tourists. Some areas requiring atten-tion are the tourism infrastructure (49th) and, especially,the ground transport infrastructure (84th). In addition,Mexico is ranked a low 77th for its price competitive-ness, due especially to very high ticket taxes and airport

charges (ranked 126th overall). Heath and hygiene issuesremain to be tackled (ranked 74th), and, in particular,safety and security continues to be a major concern,ranked 126th with high levels of crime and violence,a police force that cannot be relied on to provide pro-tection from crime, and many deaths from road trafficaccidents.

Asia PacificTable 4 displays the regional ranking and data for theAsia Pacific region.As the table shows, Australia is thehighest-ranked country from the region, ranked 9thoverall, down five places since last year.Australia isranked 4th for its natural resources, with the most WorldHeritage natural sites worldwide, many known speciesin the country, and a pristine natural environment.Given the importance of the environment for much ofits leisure tourism, it is notable that the stringency andenforcement of its environmental regulations are wellassessed. Given the country’s distance from other conti-nents and the related importance of domestic air travelto overcome the large distances between major sites,its competitiveness is also buttressed by excellent airtransport infrastructure (ranked 3rd) as well as goodgeneral tourism infrastructure (ranked 9th).Australia alsobenefits from the strong government prioritization of

xviii

Exec

utiv

e Su

mm

ary

Table 3: The Travel & Tourism Competitiveness Index: The Americas

SUBINDEXES

T&T business environment T&T human, cultural, OVERALL INDEX T&T regulatory framework and infrastructure and natural resources

Country/Economy Regional rank Overall rank Score Rank Score Rank Score Rank Score

Canada 1 5 5.32 23 5.41 4 5.36 10 5.19United States 2 8 5.28 57 4.70 2 5.47 1 5.67Barbados 3 30 4.77 19 5.47 29 4.62 45 4.21Costa Rica 4 42 4.42 48 4.94 55 3.77 31 4.54Brazil 5 45 4.35 95 4.12 69 3.53 4 5.40Mexico 6 51 4.29 80 4.34 62 3.66 13 4.87Puerto Rico 7 53 4.27 44 4.99 41 4.10 84 3.71Panama 8 55 4.23 53 4.80 56 3.77 53 4.14Chile 9 57 4.18 49 4.87 58 3.76 64 3.92Jamaica 10 60 4.13 51 4.85 57 3.76 80 3.76Uruguay 11 63 4.09 45 4.98 74 3.33 57 3.96Argentina 12 65 4.08 74 4.40 70 3.51 41 4.34Dominican Republic 13 67 4.03 54 4.75 71 3.46 68 3.88Guatemala 14 70 3.90 81 4.32 81 3.20 48 4.17Colombia 15 72 3.89 91 4.18 88 3.08 34 4.43Peru 16 74 3.88 89 4.24 92 2.96 33 4.43Honduras 17 83 3.77 83 4.31 87 3.08 63 3.92Trinidad and Tobago 18 84 3.75 100 4.04 51 3.82 112 3.38El Salvador 19 94 3.63 73 4.42 83 3.19 123 3.28Ecuador 20 96 3.62 103 4.01 97 2.91 62 3.93Suriname 21 99 3.54 110 3.86 91 3.01 79 3.76Guyana 22 102 3.50 94 4.14 111 2.68 88 3.66Nicaragua 23 103 3.49 98 4.05 101 2.79 93 3.63Venezuela 24 104 3.46 122 3.63 86 3.12 91 3.65Bolivia 25 114 3.33 127 3.33 110 2.70 58 3.96Paraguay 26 122 3.16 116 3.74 130 2.44 122 3.30

part1.r2 2/26/09 11:58 AM Page xviii

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

the tourism sector and effective destination-marketingcampaigns.The drop in rank since last year can betraced in large part to a perceived weakening of the prioritization of the sector in the country, a poorerassessment of the ground transport infrastructure, andweakening price competitiveness.

Australia is followed in the regional ranking bySingapore, which is ranked 10th overall, entering thetop 10 this year and up by six places since last year.Singapore benefits from excellent transport infrastructure,with ground transport infrastructure and air transportinfrastructure ranked 4th and 15th, respectively.Singapore also benefits from its top rank out of allcountries for the quality of its human resources to workin the country.With regard to the policy environment, italso ranks 1st, with rules and regulations that areextremely conducive to the development of its T&Tindustries (policies facilitating foreign ownership andFDI, well-protected property rights, few visa restric-tions). Further, it is among the safest countries of allassessed with regard to crime and security. Singapore isranked 2nd for the overall prioritization of Travel &Tourism, an area of improvement since last year.Thecountry’s tourism and ICT infrastructure has also seen ameasurable improvement since last year.

Hong Kong is ranked 3rd in the region and 12th overall, up two places since last year. Hong Kong’stransport infrastructure is even better assessed thanSingapore’s, with ground transport and air transportinfrastructures ranked 2nd and 13th, respectively. HongKong gets relatively good marks for cultural resources,with many international fairs and exhibitions held in thecountry and strong creative industries. Hong Kong’spolicy environment is rated second only to Singapore,and shows a strong prioritization of the tourism sector(ranked 8th). Like Singapore, Hong Kong is extremelysafe from crime and violence (ranked 5th), and thecountry is unsurpassed for its quality of health andhygiene, where it ranks first internationally.

New Zealand is ranked 4th in the region and20th overall.The country benefits from its rich naturalresources, with several World Heritage natural sites(ranked 16th) and a very pristine natural environment(ranked 3rd) protected by strong and well-enforcedenvironmental legislation.The overall policy rules andregulations in the country are conducive to the develop-ment of the sector (ranked 10th), with transparent policymaking and among the least time and lowest costrequired to start a business of all countries.Although thecountry’s ground transport network remains somewhatunderdeveloped, the air transport infrastructure gets

xix

Exec

utiv

e Su

mm

ary

Table 4: The Travel & Tourism Competitiveness Index: Asia Pacific

SUBINDEXES

T&T business environment T&T human, cultural, OVERALL INDEX T&T regulatory framework and infrastructure and natural resources

Country/Economy Regional rank Overall rank Score Rank Score Rank Score Rank Score

Australia 1 9 5.24 27 5.31 15 5.01 3 5.42Singapore 2 10 5.24 6 5.77 5 5.25 23 4.69Hong Kong SAR 3 12 5.18 2 5.93 12 5.05 30 4.55New Zealand 4 20 4.94 14 5.55 30 4.62 25 4.65Japan 5 25 4.91 40 5.10 20 4.83 15 4.81Korea, Rep. 6 31 4.72 41 5.06 35 4.45 26 4.64Malaysia 7 32 4.71 42 5.03 38 4.24 14 4.86Thailand 8 39 4.45 70 4.46 40 4.14 19 4.74Taiwan, China 9 43 4.40 75 4.40 18 4.87 65 3.92China 10 47 4.33 88 4.24 59 3.73 12 5.01India 11 62 4.09 107 3.88 63 3.65 18 4.74Brunei Darussalam 12 69 3.99 99 4.04 47 3.96 60 3.95Azerbaijan 13 76 3.84 47 4.95 84 3.19 111 3.40Sri Lanka 14 78 3.82 86 4.27 73 3.34 71 3.85Indonesia 15 81 3.79 113 3.77 79 3.24 40 4.36Philippines 16 86 3.73 85 4.27 89 3.07 70 3.86Vietnam 17 89 3.70 92 4.15 85 3.12 76 3.83Kazakhstan 18 92 3.65 60 4.69 96 2.93 121 3.32Mongolia 19 105 3.46 90 4.19 107 2.72 106 3.48Kyrgyz Republic 20 106 3.45 76 4.39 124 2.49 105 3.48Cambodia 21 108 3.43 111 3.80 113 2.64 74 3.84Tajikistan 22 109 3.41 84 4.30 117 2.58 117 3.37Pakistan 23 113 3.33 124 3.59 94 2.95 108 3.46Nepal 24 118 3.25 119 3.66 120 2.53 97 3.57Bangladesh 25 129 3.02 130 3.16 103 2.78 130 3.11

part1.r2 2/26/09 11:58 AM Page xix

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

excellent marks (ranked 11th), and both the tourism and ICT infrastructures are quite good by internationalstandards. New Zealand also benefits from high-qualityhuman capital (ranked 17th) and a very safe and secureenvironment overall (15th).

Japan is ranked 5th regionally and 25th out of allcountries in the TTCI, with excellent marks for its cul-tural resources (ranked 10th), attributable to its 14 WorldHeritage cultural sites, the many international fairs andexhibitions held in the country, and its rich creativeindustries.The ground transport infrastructure is amongthe best in the world (ranked 8th), especially railroads,and Japan continues to be a leader in the area of educa-tion and training (ranked 12th). However, Japan ranksthird from the bottom for the affinity of the county forTravel & Tourism (131st), and the sector is not perceivedto be a priority for the government (ranked 83rd).

Malaysia is ranked 7th regionally and 32nd overall,with its rich natural resources (ranked 21st) and goodground transport infrastructure (ranked 28th).Thecountry also benefits from excellent price competitive-ness (ranked 4th), with low comparative hotel and fuel prices, low ticket taxes and airport charges, verycompetitive hotel prices, and a favorable tax regime.Malaysia’s policy environment is assessed as highly con-ducive to the development of the sector (ranked 9th),and the country is prioritizing Travel & Tourism; it markets the country at many international tourism fairs(ranked 1st) and also has an excellent evaluation for itsdestination-marketing campaigns (ranked 12th).Withregard to weaknesses, health and hygiene indicators lagbehind those of many other countries in the region,with, in particular, a low physician density (placing thecountry 94th).

Thailand is ranked just behind Malaysia in theregion at 8th place and 39th overall, up three placessince last year. It is endowed with rich natural resourcesand a strong affinity for Travel & Tourism (ranked 24thand 22nd, respectively), with a very friendly attitude ofthe population toward tourists (ranked 13th).This isbuttressed by the sector’s strong prioritization by thegovernment (ranked 12th) with, similar to Malaysia,excellent destination-marketing campaigns and goodprice competitiveness. However, some weaknessesremain: despite the prioritization of the sector by thegovernment, some aspects of the regulatory environment—such as stringent foreign ownership restrictions, visarestrictions for many travelers, and the long timerequired for starting a business in the country—are notparticularly conducive to developing the sector (ranked62nd). In addition, given the importance of the naturalenvironment for the country’s tourism, environmentalsustainability should be a greater priority (ranked 99th).

China, ranked 10th regionally, has seen the largestrank improvement of all countries this year, moving upby a remarkable 15 places to 47th overall. China hasbeen building on a number of clear strengths: it is

ranked 7th for its natural resources, with many WorldHeritage natural sites and fauna that is among the rich-est in the world. It is ranked 15th for its culturalresources, with many World Heritage cultural sites, manyinternational fairs and exhibitions held in the country,and creative industries that are unsurpassed. Moreover,the country is ranked 20th in price competitiveness and28th for the overall prioritization of the sector. In addi-tion, China has a relatively good air transport infrastruc-ture (ranked 34th). However, there are some weaknessespulling the country’s ranking down. China has a policyenvironment that is not conducive for T&T develop-ment (ranked 87th), with strong foreign ownershiprestrictions and visa requirements for most visitors.Furthermore, policies related to environmental sustain-ability get low marks (105th).There are also some safetyand security concerns (116th), as well as issues related tohealth and hygiene (91st), with access to improved sani-tation and drinking water that is low by internationalstandards. Ground transport infrastructure gets middlingmarks (55th), and its tourism infrastructure remainsunderdeveloped (ranked 80th), with few hotel roomsavailable and few ATMs, although on a positive notetourism infrastructure has seen a marked improvementsince last year.

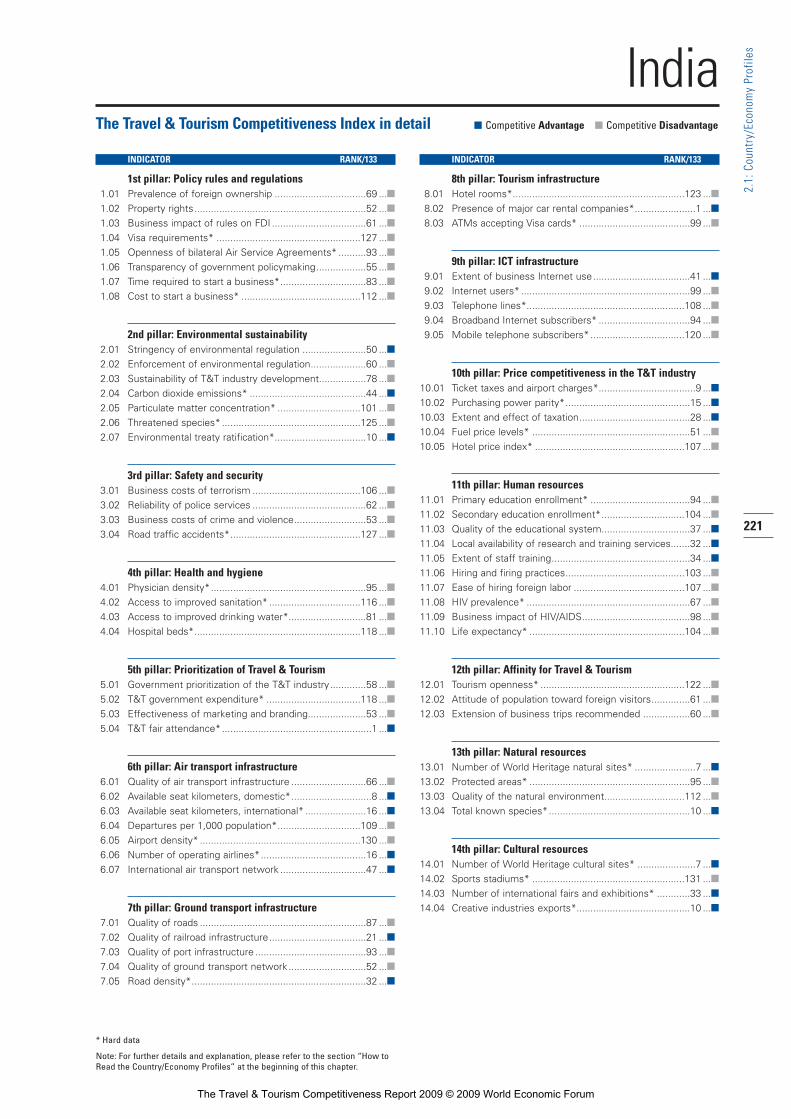

India is ranked 11th in the region and 62nd over-all, up three places since last year.As with China, India iswell assessed for its natural resources (ranked 14th) andcultural resources (24th), with many World Heritagesites, both natural and cultural, rich fauna, and strongcreative industries in the country. India also has quite agood air transport network (ranked 37th), particularlygiven the country’s stage of development, and a reason-able ground transport infrastructure (ranked 49th).However, some aspects of its tourism infrastructureremain somewhat underdeveloped (ranked 73rd), withvery few hotel rooms per capita by international com-parison and low ATM penetration. Further, despite gov-ernment and industry efforts to promote the countryabroad (India is ranked 1st with regard to tourism fairattendance) and the exposure given to recent promo-tional campaigns, the assessment of marketing andbranding to attract tourists remains average (ranked 53rd).Another area of concern is the policy environment,ranked 108th, with much time and cost for starting abusiness, bilateral Air Service Agreements that are notassessed as open, and visas required for most visitors.

Middle East and AfricaTable 5 shows the regional ranking for the Middle Eastand Africa region.As the table shows, The UnitedArab Emirates (UAE) is ranked 1st in the region thisyear, 33rd overall, up seven places since last year, over-taking Israel and Tunisia.While the UAE is not endowedwith rich natural and cultural resources (117th and 84th,respectively), it does very well in several other areas captured by the Index. For example, the country is char-

xx

Exec

utiv

e Su

mm

ary

part1.r2 2/26/09 11:58 AM Page xx

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

acterized by a positive attitude toward foreign travelers(10th) and is also seen as very safe from crime and violence (ranked 14th).The UAE’s infrastructure alsogets good marks, particularly its air transport infrastruc-ture, which is ranked a very high 4th out of all countriesassessed (up one place since last year).The governmentis seen as prioritizing the sector strongly (ranked 3rd),carrying out very effective destination-marketing campaigns (ranked 1st) and ensuring the presence of thecountry at major T&T fairs internationally.An area ofclear improvement since last year is in the rules and regulations, which have been adjusted to better supportthe sector’s development, with the UAE moving upfrom 81st place last year to 53rd this year.

Israel is the second-ranked country in the region,at 36th overall, showing a stable performance since lastyear.The country’s human resources base is well evaluated(29th), providing healthy and well-trained people towork in the T&T sector. Further, its infrastructure isquite well developed compared with those of othercountries in the region, especially its ICT infrastructure.Israel’s rules and regulations, ranked 39th, are conduciveto the development of the sector, with low foreignownership restrictions and visas required from fewcountries, although it requires much time to set up abusiness in the country (ranked 91st). But althoughIsrael gets excellent marks related to health and hygiene(ranked 14th), safety and security continues to be a

xxi

Exec

utiv

e Su

mm

ary

Table 5: The Travel & Tourism Competitiveness Index: Middle East and Africa

SUBINDEXES

T&T business environment T&T human, cultural, OVERALL INDEX T&T regulatory framework and infrastructure and natural resources

Country/Economy Regional rank Overall rank Score Rank Score Rank Score Rank Score

United Arab Emirates 1 33 4.57 39 5.12 23 4.79 78 3.81Israel 2 36 4.50 37 5.13 39 4.21 51 4.16Qatar 3 37 4.49 35 5.16 34 4.48 75 3.83Mauritius 4 40 4.43 24 5.39 44 4.04 69 3.86Bahrain 5 41 4.42 55 4.75 28 4.64 67 3.88Tunisia 6 44 4.37 31 5.26 49 3.87 56 3.97Jordan 7 54 4.25 36 5.15 67 3.55 54 4.05South Africa 8 61 4.10 82 4.31 52 3.81 49 4.17Egypt 9 64 4.09 52 4.84 65 3.59 73 3.84Oman 10 68 4.01 59 4.69 53 3.80 99 3.54Saudi Arabia 11 71 3.89 104 4.01 45 4.02 90 3.65Morocco 12 75 3.86 64 4.59 78 3.27 83 3.73Botswana 13 79 3.81 66 4.55 76 3.29 95 3.60Namibia 14 82 3.77 71 4.45 77 3.27 94 3.60Syria 15 85 3.73 68 4.48 82 3.20 100 3.53Gambia, The 16 87 3.72 65 4.56 90 3.06 98 3.55Kuwait 17 95 3.63 109 3.87 50 3.85 128 3.16Kenya 18 97 3.60 93 4.15 100 2.81 72 3.84Tanzania 19 98 3.59 102 4.03 118 2.56 50 4.17Zambia 20 100 3.53 87 4.26 115 2.64 85 3.69Senegal 21 101 3.50 101 4.03 108 2.71 82 3.75Ghana 22 110 3.40 105 3.94 102 2.78 104 3.49Uganda 23 111 3.38 115 3.75 114 2.64 81 3.76Libya 24 112 3.38 97 4.07 109 2.71 114 3.37Algeria 25 115 3.31 108 3.88 98 2.84 127 3.22Madagascar 26 116 3.28 112 3.79 106 2.74 119 3.32Malawi 27 117 3.27 106 3.91 131 2.43 107 3.47Mali 28 119 3.19 114 3.76 126 2.48 120 3.32Benin 29 120 3.18 117 3.66 121 2.52 116 3.37Zimbabwe 30 121 3.17 125 3.57 125 2.49 109 3.43Ethiopia 31 123 3.15 128 3.27 112 2.65 101 3.52Mozambique 32 124 3.12 120 3.66 129 2.45 125 3.24Cameroon 33 125 3.09 126 3.54 132 2.36 115 3.37Burkina Faso 34 126 3.08 118 3.66 122 2.52 131 3.05Mauritania 35 127 3.07 123 3.61 127 2.47 129 3.14Nigeria 36 128 3.02 132 3.10 116 2.59 113 3.38Côte d’Ivoire 37 130 2.99 131 3.12 123 2.50 118 3.35Burundi 38 131 2.98 129 3.17 119 2.53 126 3.24Lesotho 39 132 2.92 121 3.64 128 2.45 133 2.66Chad 40 133 2.52 133 2.83 133 1.93 132 2.80

part1.r2 2/26/09 11:58 AM Page xxi

The Travel & Tourism Competitiveness Report 2009 © 2009 World Economic Forum

major concern, placing the country at 73rd, primarilyrelated to concerns about terrorism (ranked 129th).

Qatar is ranked 3rd in the region and 37th overall,directly following Israel in the full ranking. Qatar bene-fits from an extremely safe and secure environment(ranked 9th), high-quality human resources in the country (ranked 22nd for human capital), good tourisminfrastructure (28th), and excellent air transport infra-structure (20th), in line with its increasing role as an airtransportation hub. In order to further improve thecountry’s T&T competitiveness, efforts should be madeto upgrade its ground transport infrastructure (ranked59th), more focus should be placed on environmentalsustainability (69th), and further efforts should be madeto improve the policy and regulatory environment(ranked 47th)—in particular, by facilitating more foreigndirect investment and easing visa requirements for enter-ing the country.

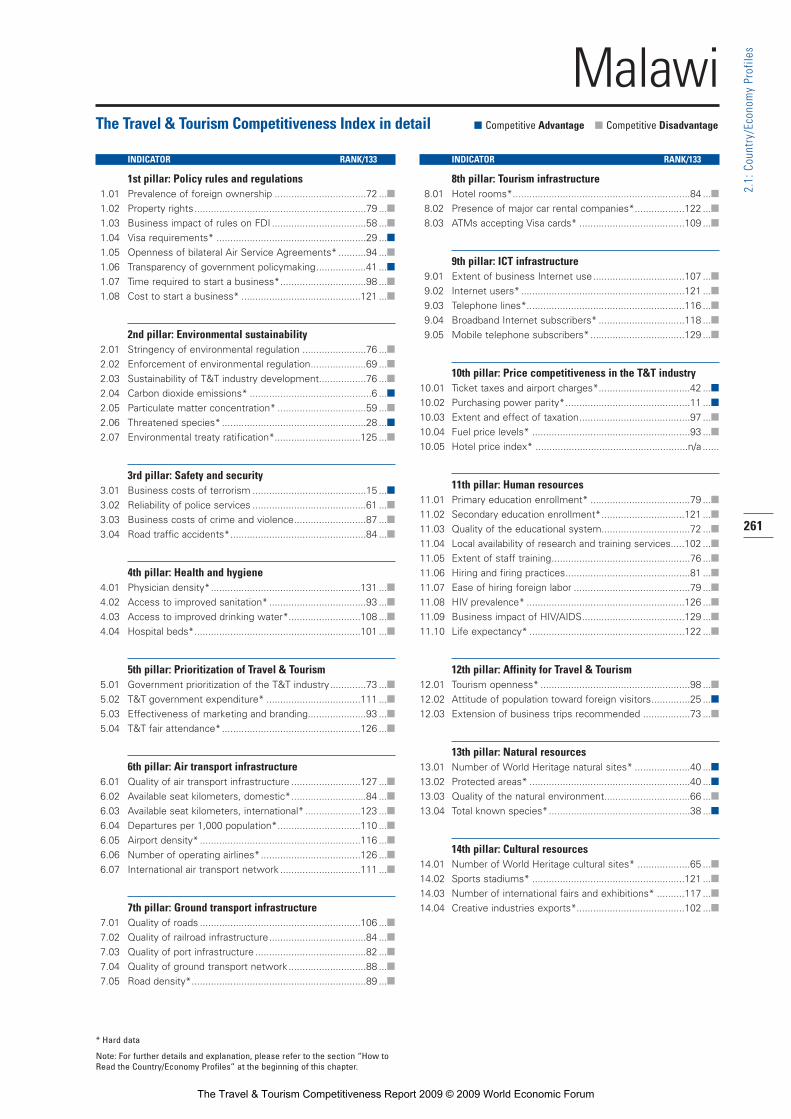

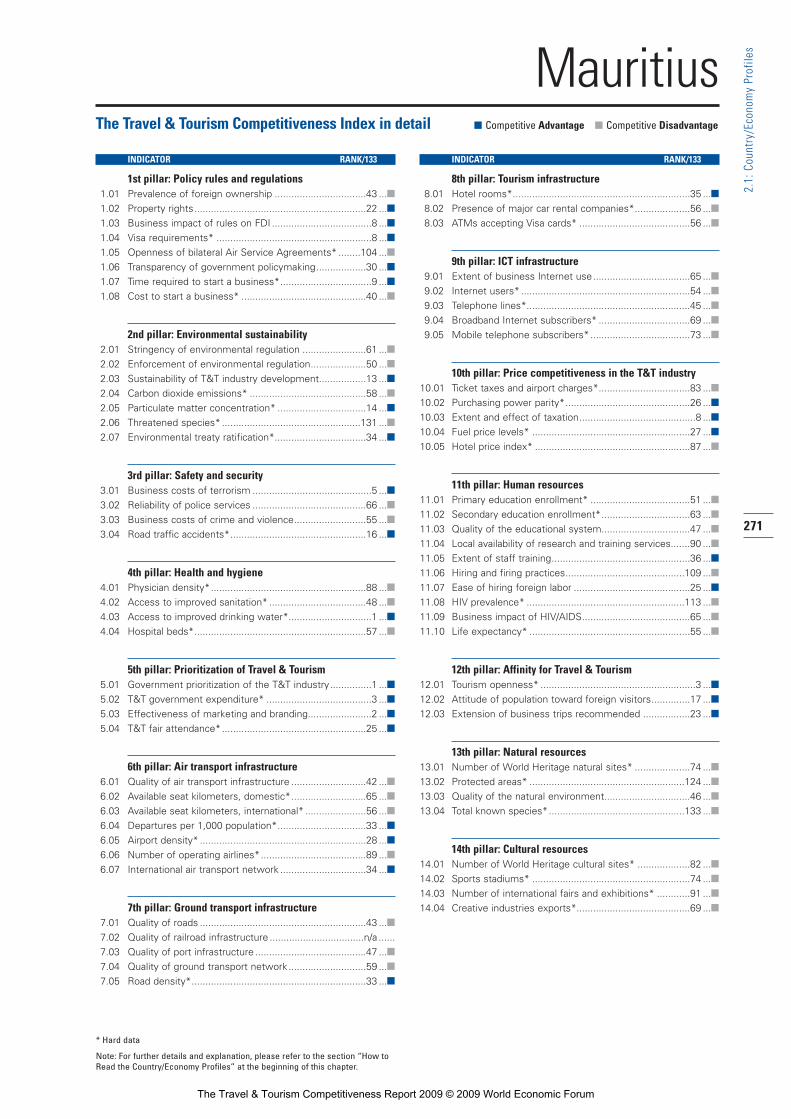

Mauritius is the fourth highest ranked country inthe region, at 40th overall. Mauritius is ranked 1st out ofall countries for the overall prioritization of the sector,with high government spending on the tourism industry(ranked 3rd), ensuring excellent destination-marketingcampaigns to attract tourists (ranked 2nd), and ensuringthe country’s presence at many international tourismfairs.Along similar lines, Mauritius is ranked 3rd for itsoverall affinity for Travel & Tourism, with the sector representing an important part of the economy and thegeneral attitude of the population to foreign travelersbeing extremely welcoming.The country’s tourisminfrastructure is well developed by regional standards,and the policy environment is supportive of the devel-opment of the sector (ranked 13th). Mauritius also ben-efits from price competitiveness (ranked 26th), with rel-atively low prices overall and taxation that is not overlyburdensome, although this would be improved throughlower ticket taxes and airport charges, and more com-petitive hotel prices. Safety and security levels are alsogood by regional standards (ranked 40th), and are on apar with countries such as Germany and Hungary. Interms of challenges, although the government is seen tobe making an effort to develop the industry in a sustain-able way (ranked 13th), this effort could be backed upby more stringent environmental regulations (ranked61st).

Tunisia is ranked 6th among Middle East andAfrican countries and 44th overall, down five placessince last year.Tunisia benefits from a strong assessmentof the prioritization of Travel & Tourism (15th)—similarto top-10 ranked countries such as Austria and Canada—with high government spending on the sector, effec-tive destination-marketing campaigns, and attendance atseveral major international tourism fairs. Further, unlikesome other countries in the region,Tunisia is perceivedas relatively safe from crime and violence (ranked 31st).In addition, price competitiveness is a positive attribute,ranked 7th, with competitive hotel prices, low fuel lev-

els, reasonable taxation, and low prices more generally.On the other hand, health and hygiene remains an areaof concern (75th), with a relatively low physician density and a low concentration of hospital beds.Thecountry’s ICT infrastructure also remains underdevel-oped (ranked 77th).This is an area that has seen a deterioration since last year.