The Third Arrow of Abenomics: How Far Will It Reach? Ito... · · 2015-09-29The Third Arrow of...

35

The Third Arrow of Abenomics: How Far Will It Reach? Takatoshi Ito* University of Tokyo October 24, 2013 * In addition to teaching career at Minnesota, Harvard, Hitotsubashi and Tokyo, the author has been Senior Advisor at Research Department, IMF (1994-1997); Deputy Vice Minister, Ministry of Finance (1999-2001); and Member, Prime Minister’s Council on Economic and Fiscal Policy (2006-2008) under PM Abe and PM Fukuda. Currently, a chair of council of experts to reform GPIF. Zadankai at CJEB, Columbia University

-

Upload

nguyenliem -

Category

Documents

-

view

215 -

download

1

Transcript of The Third Arrow of Abenomics: How Far Will It Reach? Ito... · · 2015-09-29The Third Arrow of...

The Third Arrow of Abenomics: How Far Will It Reach?

Takatoshi Ito* University of Tokyo October 24, 2013

* In addition to teaching career at Minnesota, Harvard, Hitotsubashi and Tokyo, the author has been Senior Advisor at Research Department, IMF (1994-1997); Deputy Vice Minister, Ministry of Finance (1999-2001); and Member, Prime Minister’s Council on Economic and Fiscal Policy (2006-2008) under PM Abe and PM Fukuda. Currently, a chair of council of experts to reform GPIF.

Zadankai at CJEB, Columbia University

Takeaways • (0) Three arrows: Abenomics is a package of 3 arrows:

• (1) 1st Arrow: Aggressive Monetary Policy, Early success

– QQE by new BOJ Governor Kuroda, April 4 – Yen depreciation (by 25%) and Stock prices increases (by 50%)

• (2) 2nd Arrow: Flexible Fiscal Policy, now on track – Short-run success. 2013Q2 growth rate was high. – Consumption tax will rise to 8% in April 2014 as scheduled

• (3) 3rd Arrow: Growth Strategy, yet to be released – Most critical element. Many candidate areas: e.g., – Agriculture; health care; female labor force promo; energy

• All combined:

– A Jump from a bad (deflation) to a good (normal) equilibrium

October 24, 2013 (c) Takatoshi ITO 2

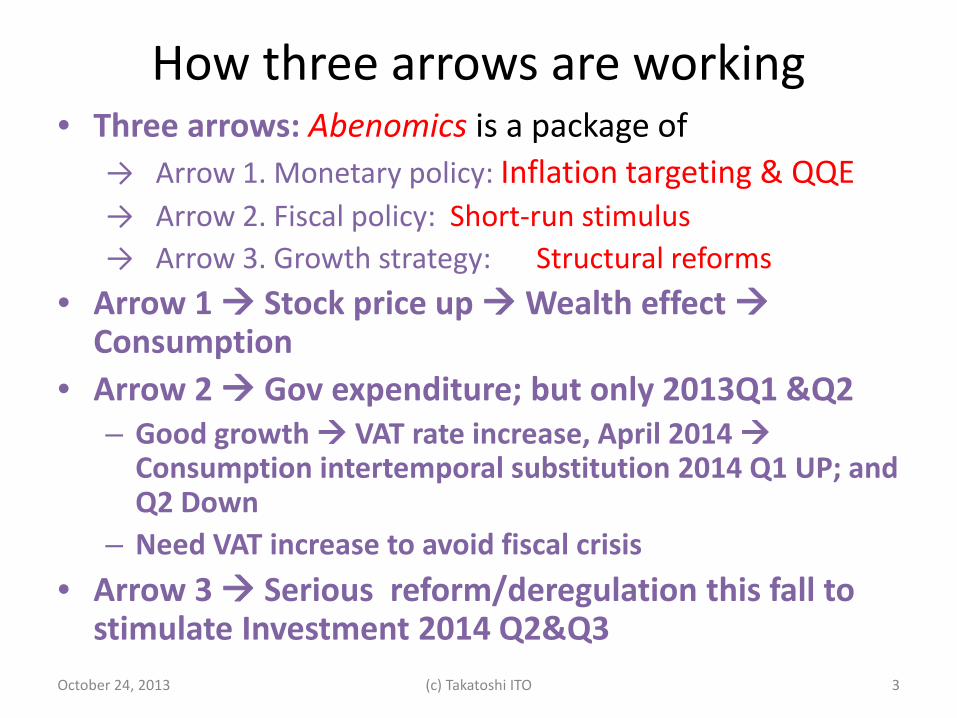

How three arrows are working • Three arrows: Abenomics is a package of

→ Arrow 1. Monetary policy: Inflation targeting & QQE → Arrow 2. Fiscal policy: Short-run stimulus → Arrow 3. Growth strategy: Structural reforms

• Arrow 1 Stock price up Wealth effect Consumption

• Arrow 2 Gov expenditure; but only 2013Q1 &Q2 – Good growth VAT rate increase, April 2014

Consumption intertemporal substitution 2014 Q1 UP; and Q2 Down

– Need VAT increase to avoid fiscal crisis • Arrow 3 Serious reform/deregulation this fall to

stimulate Investment 2014 Q2&Q3 October 24, 2013 (c) Takatoshi ITO 3

• Objective. To break “deflationary expectation” – The real interest rate (= nominal rate – πe) will decline, & – Investment and Consumption will be stimulated

• Is it credible? – Credible as the BOJ under Gov. Kuroda is committed to QE

• (Skeptic) Does QE work? – (Answer) It worked in FRB, BOE, ECB preventing deflation. – (Answer) Timing and communication is important

• BOJ, important developments – 2% Inflation targeting on January 22, 2013, under Gov. Shirakawa – April 4, 2013: Quantitative and Qualitative Easing (QQE) under Gov.

Kuroda – April 24, 2013: Outlook, forecast of 1.9% by 2015

• See also, Takatoshi Ito, “Abenomics: Early Success and Prospects” Spotlight, September/October 2013, pp. 4-7

October 24, 2013 (c) Takatoshi ITO 4

Targeting Inflation

Early Success (mid-Nov, 2012 to end-April 2013)

• Yen depreciation and stock price rise, mid-Nov to April – The USD/JPY moved from 78 yen to 98 yen/$

• 20% depreciation – Stock prices (Nikkei 225): 8660 13,800

• 50% increases

• PM Abe’s approval rating has increased – Emphasis on the economy is working

• This is NEW, compared to Episode I (2006-07) – Strong leadership (e.g., inflation targeting); No wobbling – Politically controversial issues are shelved

• Patriotic education • Constitution reform: status for Self-Defense Force (SDF) • Also Chinese aggression is helping Abe’s popularity so far

(c) Takatoshi ITO 5 October 24, 2013

October 24, 2013 (c) Takatoshi ITO 6

Yen/USD (2012/1/1/- 2013/10/10)

October 24, 2013 (c) Takatoshi ITO 7

Nikkei 225(2012/1/1/- 2013/10/10)

October 24, 2013 (c) Takatoshi ITO 8

• Quick fix: a short-run stimulus to raise the growth rate, 2013Q2 – To win the upper house election in July – Important data for a decision of “a go” or “a no-go” for consumption

tax increases will be decided in October 2013 – In concerted efforts with BOJ to raise π – Supplementary budget will be spent by end-June

• But controversial – Contents. Public works reminds of “Old style LDP (pre-Koizumi)” – But, that is an only way to disburse quickly

• (Skeptic) Could this hasten an eventual fiscal bust? – (A) Mostly maintenance and repair of infrastructure – But, yes, fiscal consolidation is needed in medium-term – In the medium term, growth policy will work to replace fiscal stimulus

• Important: Short-term stimulus and Medium-term consolidation

October 24, 2013 (c) Takatoshi ITO 9

Stimulus Fiscal

Fiscal sustainability • Fiscal situation is very bad—unsustainable

– Debt-GDP ratio much worse than fiscal crisis counties in the Euro zone. Worst among OECD.

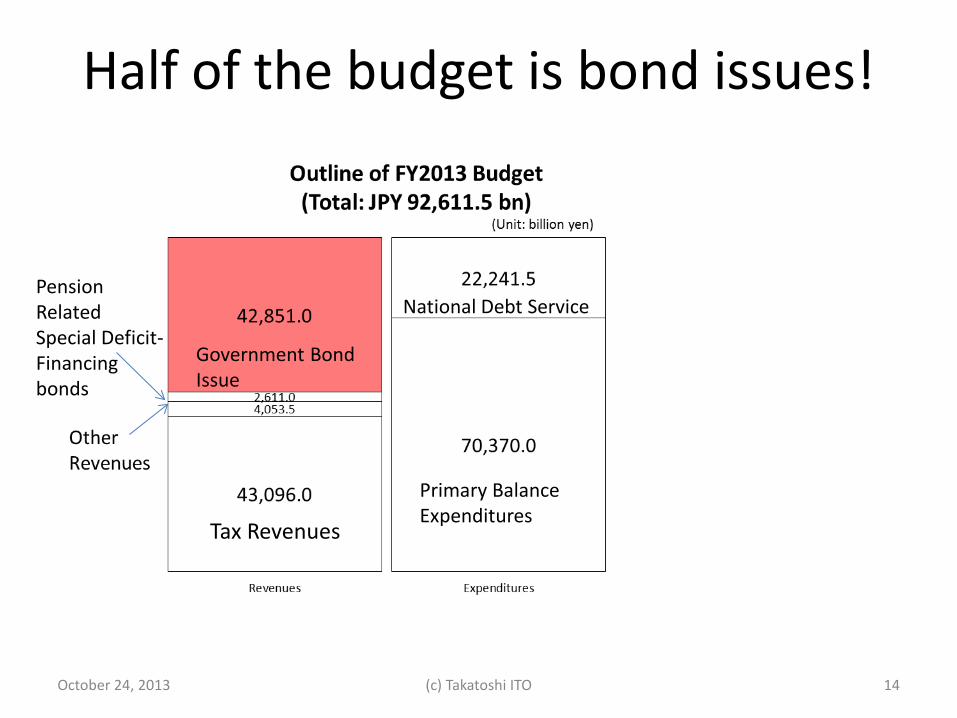

– In the general account budget, half of expenditures are financed by new bond issues

• Total budget 2013 is about • Tax revenues are less than half of total expenditure

• Correction – Raise tax rates: consumption; income; corporate – Cut expenditure Japan is lowest in Gov ex/GDP; social

security related expenditures are rising rapidly – Economic growth Even with very high growth rate, it

would not be enough • Best option is to raise consumption tax rate

October 24, 2013 (c) Takatoshi ITO 10

October 24, 2013 (c) Takatoshi ITO 11

October 24, 2013 (c) Takatoshi ITO 12

October 24, 2013 (c) Takatoshi ITO 13

Half of the budget is bond issues!

October 24, 2013 (c) Takatoshi ITO 14

Pension Related Special Deficit-Financing bonds

National Debt Service

Primary Balance Expenditures

Tax Revenues

Government Bond Issue

Fiscal Policy: Defying Gravity Medium-term consolidation needed

• Takeo Hoshi and Takatoshi Ito, “Defying Gravity: How Long Will Japanese Government Bond Prices Remain High?” NBER wp. 18287, August 2012.

• Take-away – Japanese financial institutions buy most JGBs

• Domestic holding, more than 90% • They are extremely risk-averse

– Household saving is flat and will be declining – An increase in corporate saving goes into saving – A ceiling of stable JGB increases is the sum of Private Sector

(Household and Corporate) saving (mostly bank deposits) – Simulation exercises show that the ceiling will be hit by 2021 – A crisis will happen before that date

October 24, 2013 (c) Takatoshi ITO 15

Controversy: consumption tax hike “As scheduled” vs. “Delay”

• Legislation (August 2012)—agreed by 3 major parties – April 2014: 5% 8%; October 2015: 8% 10%

• Objections – Prof. Hamada and Mr. Honda – special advisers to Cabinet—argued for delay

in tax hike – The “as scheduled” vs. “Delay” became a huge political issue in August 2013

• Interviews of 60 experts from August 26 to 31 – Group interviews, 7 groups – Interviewers: Ministers Aso and Amari; Governor Kuroda, and 4 private-sector

members of CEFP – More than 42 people supported “as scheduled”.

• See pros and cons in the following slides, and also – Takatoshi Ito, “Japan Must be brave—it is time to put up taxes,” Financial

Times, September 9, 2013 – Takatoshi Ito, “Consumption tax fears risk stalling Abe’s ‘three arrows’ East

Asian Forum, September 8, 2013

October 24, 2013 (c) Takatoshi ITO 16

“Delay” “as scheduled” • Economy is fragile;

Economy may fall back to stagnation and deflation if tax hike

October 24, 2013 (c) Takatoshi ITO 17

• Economy is firmly expanding – Q1: 3.8% &Q2: 4.1% – Expected to continue

positive growth – Even with tax hike, BOJ

expects CPI inflation rate will become close to 2% in 2015

Announcement Date 2012 Q2 2012 Q3 2012 Q4 2013 Q1 2013 Q2

2013/5/16 -0.9 -3.5 1 3.52013/6/10 -0.6 -3.6 1.2 4.12013/8/12 -0.9 -3.6 1 3.8 2.62013/9/9 -1.2 -3.5 1.1 4.1 3.8

“Delay” “as scheduled” • Lesson of 1997: tax

rate hike from 3% to 5% produced a negative growth in 1998

October 24, 2013 (c) Takatoshi ITO 18

• Recession in 1998 was due to Asian financial crisis and Japanese banking crisis

• True lesson of 1997: has to address a major problem early, NPL in the 1990s and fiscal unsustainability in 2000s

“Delay” “as scheduled” • (silence)

October 24, 2013 (c) Takatoshi ITO 19

• Amending the rate hike requires a new law – Takes time and political capital delay in the third arrow

– The market would react negatively; stock price decline

• Suspension leads foreign investors to believe that PM Abe is weak and Abenomics will fail; they unwind positions – Yen will appreciate – Stock prices will fall – 1st arrow will be broken

What are the forecasts (as of August 2013) telling us?

• Up and down (intertemporal substitution) in consumption will realize – A big “rush-to-buy” boom (4%, QtoQ, annualized

growth rate) in 2014:1st quarter. – A big decline (minus 5%, QtoQ annualized growth

rate) in 2014:2nd quarter • This up-and-down (mini business cycle) can be

smoothed by counter-cyclical government expenditures (15 month budget is desirable)

• A permanent decline due to a decline in purchasing power of consumers

October 24, 2013 (c) Takatoshi ITO 20

GDP forecasts with and without consumption tax rate hike

October 24, 2013 (c) Takatoshi ITO 21 Author’s calculation

• In the medium- to long-run, the economy needs – Consumption and Investment increases – Productivity gains & Wage increases – Growth without fiscal stimulus

• But which industries? – Backward Industries due to lots of regulations are the

hopefuls • Health and medical care • Agriculture

– FTA and TPP – Capital Markets and the Public Pension fund reform

• See T. Ito, “Abe should aim his third arrow at Japan’s farmers” Financial Times, June 2013.

October 24, 2013 (c) Takatoshi ITO 22

Strategy Growth

TPP (Trans-Pacific Partnership) • TPP is a big deal for Japan

– A chance to recover from a late start and implementation in FTAs with large trading partners.

– A chance to do domestic reform in the name of external liberalization (gai-atsu)

• Japan has mentioned 5 sensitive areas (“sacred areas”) : Rice, Wheat, Beef and Pork, Dairy Products, and Sugar

• But, PM Abe has been clever in not giving a clear language of protection October 24, 2013 (c) Takatoshi ITO 23

FTA/EPA in the past

• Japan has been lagging behind Korea and China, not to mention Australia and Singapore, in concluding FTAs

• Japan’s existing FTAs do not cover important trading partners – Not having FTAs are disadvantage for Japanese

exporters such as • “Agriculture” is the stumbling bloc in negotiating

FTAs with US, Australia and NZ •

October 24, 2013 (c) Takatoshi ITO 24

Japan’s FTA

October 24, 2013 (c) Takatoshi ITO 25

Comments: Important trading partners are missing: US, EU, and China Those concluded are countries with little threat of importing agricultural products The so-called “liberalization ratio” is below 90% for Japan

Source: Ministry of Foreign Affairs

What does Japan have to do in conclusion of TPP?

• Liberalization more than 96% … • Japan’s tariff lines: 9018 • Of which , 5 “Sacred Areas” have 586 (6.5% of all tariff

lines) – Rice: 58 – Wheat: 109 – Beef and pork: 100 – Dairy products: 188 – Sugar: 131

• Currently rumored to “protect” only 366 (4.1%) – Other 200 some items are mostly (semi-)processed products – Would that be enough to conclude TPP? – Would that be acceptable domestically?

October 24, 2013 (c) Takatoshi ITO 26

Agricultural Coop has prevented productivity increases

• Agricultural coop, JA, has been a strong political lobby • JA’s instinct

– Maximize its membership • Against policies to push scale economies • Strong area should be sacrificed to help the weakest

– Cut production when demand decreases (due to population declines and taste changes)

• Not interested in exports – Keeping high tariffs protects Japanese farmers who are

disadvantaged by small arable land • Japanese agricultural economists are mostly Marxists

October 24, 2013 (c) Takatoshi ITO 27

The dairy industry as an example

• Raw milk drinking milk Dairy products (cheese; butter; LL milk; etc)

• Should the industry be protected by high tariff?

• Not really – Raw milk imports are unthinkable – Dairy product imports may increase, but really? – Lots of room to increase domestic productivity

October 24, 2013 (c) Takatoshi ITO 28

Should we protect the “dairy” industry?

• No. Agricultural Cooperatives and the Ministry (MAFF) argue – NZ low-price dairy products will kill the Japanese dairy

industry – The current tariffs, e.g., 38.5% for cheese should be

maintained (“sacred area”) • Yes. The gradually lowering tariffs will stimulate

structural reform and the Japanese dairy industry will become a strong industry. Specifically – Production quota – All or nothing rule of raw milk sales to Regional Coop

October 24, 2013 (c) Takatoshi ITO 29

Regulation • Japan is divided into 10 districts • [Production quota] The ministry decides how much to produce and

put quota to Regional JA, and Regional JA to each JA, each JA to each farmer

• There is one regional JA that is a monopoly in distribution of raw milk. The regional JA buys raw milk from farms and sells them to milk and dairy products production companies.

• [ALL or Nothing for each farm] Each dairy farm has to choose either (a) sell all raw milk to the regional JA monopoly or (b) process all raw milk by itself for milk and dairy products

• The regional JA monopoly sells raw milk to dairy product companies • The price of raw milk for “milk” and that of raw milk for “other dairy

products” are different. For milk is higher.

• Basically, this is a socialist “planned economy” – No incentive to “innovate”

October 24, 2013 (c) Takatoshi ITO 30

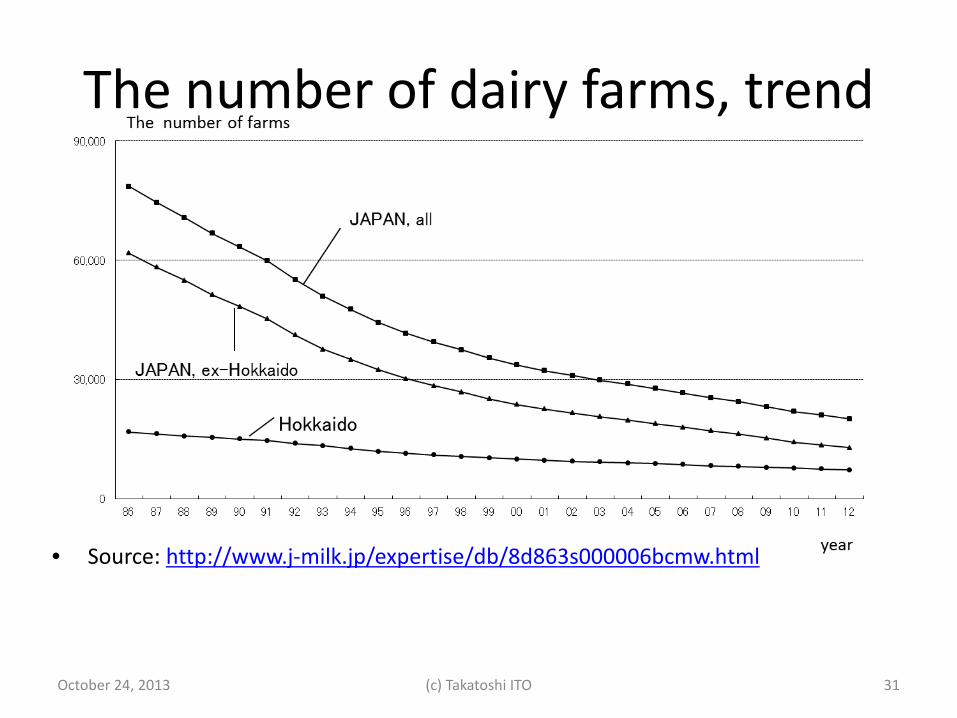

The number of dairy farms, trend

• Source: http://www.j-milk.jp/expertise/db/8d863s000006bcmw.html

October 24, 2013 (c) Takatoshi ITO 31

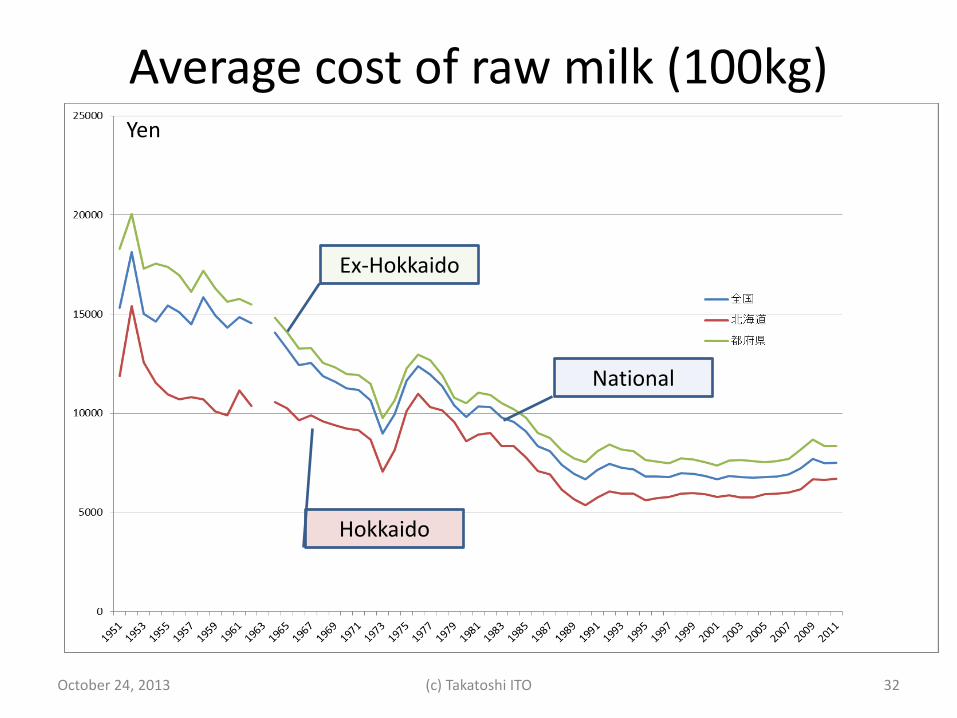

Average cost of raw milk (100kg)

Ex-Hokkaido

Hokkaido

National

October 24, 2013 (c) Takatoshi ITO 32

Yen

Policy implications • Scale economies exist

– By accelerating mergers of farm, costs can be reduced – When large farms become dominant and “brand”

marketing becomes possible, domestic products become competitive

• Hokkaido milk farms are “exploited”—they should be liberated – Farms with lowest costs cannot expand production

(government control, via Shitei Dantai) – Farms with low cost cannot claim high sales prices,

because most raw milk is sold for processed products rather than drinking milk (government control, via Shitei Dantai)

– Domestic distortion should be corrected in parallel with import liberalization

October 24, 2013 (c) Takatoshi ITO 33

Policies backed by growth theory • Measures have been discussed in Episode I (2006-07) • Labor. Policies to increase:

– Raise women participation, age 30-40 (need more nurseries) – More foreign workers (esp. health care workers) – Continue working 65+ workers (delay retirement)

• Capital. Prevent hollowing out – Lower corporate income tax – TPP and FTA (incentive to produce in Japan) – Capital market reform (encourage taking risk)

• Technological Progress – Innovation/deregulation in backward industries – Releasing potentials in agriculture, health care services – Rectify the problem in the energy sector

• Can nuclear power plants be restarted?

October 24, 2013 (c) Takatoshi ITO 34

Conclusion • Abenomics is working fine, so far

– [1st arrow] Monetary policy is right on the target – [2nd arrow] Fiscal stimulus works in the short run – 2013Q1, growth rate (QtoQ) 0.9% (or annualized 3.5%)

• Abenomics, the success means a jump from a bad, deflationary equilibrium to a good, normal equilibrium

• Once in the good equilibrium, fiscal stimulus will not be needed

• [3rd arrow] Growth strategy will be a key to raise growth potential; to erase fiscal debt concern; to raise wages; and to complete the jump

• Risk is too much a distraction to political agenda

October 24, 2013 (c) Takatoshi ITO 35

![English French Portuguese Russian Spanish · English French Portuguese Russian Spanish Abenomics Abenomics [Au pluriel (les Abenomics).] "абэномика" Abeconomía abode lieu](https://static.fdocuments.net/doc/165x107/5f9179c86db9d218e37fedb3/english-french-portuguese-russian-spanish-english-french-portuguese-russian-spanish.jpg)