The Test of Entrepreneurship -...

25

1 | © 2013 EFL Global Ltd. All Rights Reserved The Test of Entrepreneurship REVOLUTIONIZING MSME FINANCE

Transcript of The Test of Entrepreneurship -...

1 | © 2013 EFL Global Ltd. All Rights Reserved

The Test of Entrepreneurship REVOLUTIONIZING MSME FINANCE

2 | © 2013 EFL Global Ltd. All Rights Reserved

What we do

EFL provides knowledge for financial institutions

about individuals

using psychometrics

enabling them to expand portfolios

and improve control over risk

3 | © 2013 EFL Global Ltd. All Rights Reserved

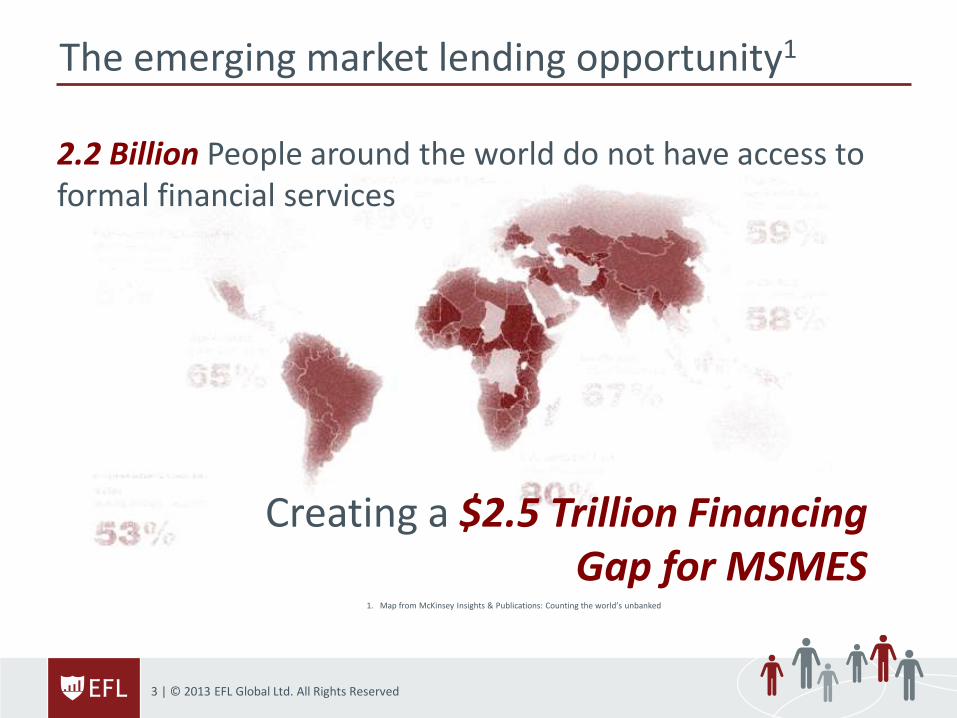

The emerging market lending opportunity1

1. Map from McKinsey Insights & Publications: Counting the world’s unbanked

Creating a $2.5 Trillion Financing Gap for MSMES

2.2 Billion People around the world do not have access to formal financial services

4 | © 2013 EFL Global Ltd. All Rights Reserved

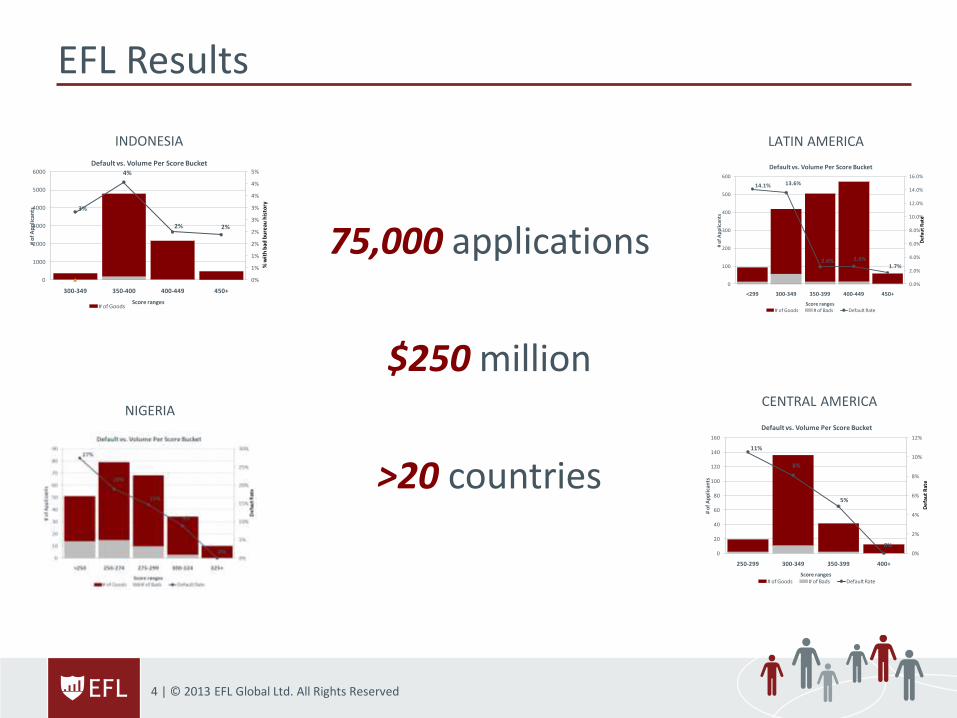

EFL Results

11%

8%

5%

0%0%

2%

4%

6%

8%

10%

12%

0

20

40

60

80

100

120

140

160

250-299 300-349 350-399 400+

# o

f A

pp

lica

nts

Score ranges

Default vs. Volume Per Score Bucket

# of Goods # of Bads Default Rate

De

fau

tR

ate

3%

4%

2% 2%

0%

1%

1%

2%

2%

3%

3%

4%

4%

5%

0

1000

2000

3000

4000

5000

6000

300-349 350-400 400-449 450+

# o

f A

pp

lica

nts

Score ranges

Default vs. Volume Per Score Bucket

# of Goods

% w

ith

bad

bu

reau

his

tory

INDONESIA

NIGERIA

14.1% 13.6%

2.6% 2.6%1.7%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

0

100

200

300

400

500

600

<299 300-349 350-399 400-449 450+

# o

f A

pp

lica

nts

Score ranges

Default vs. Volume Per Score Bucket

# of Goods # of Bads Default Rate

De

fau

tR

ate

LATIN AMERICA

CENTRAL AMERICA

75,000 applications

$250 million

>20 countries

5 | © 2013 EFL Global Ltd. All Rights Reserved

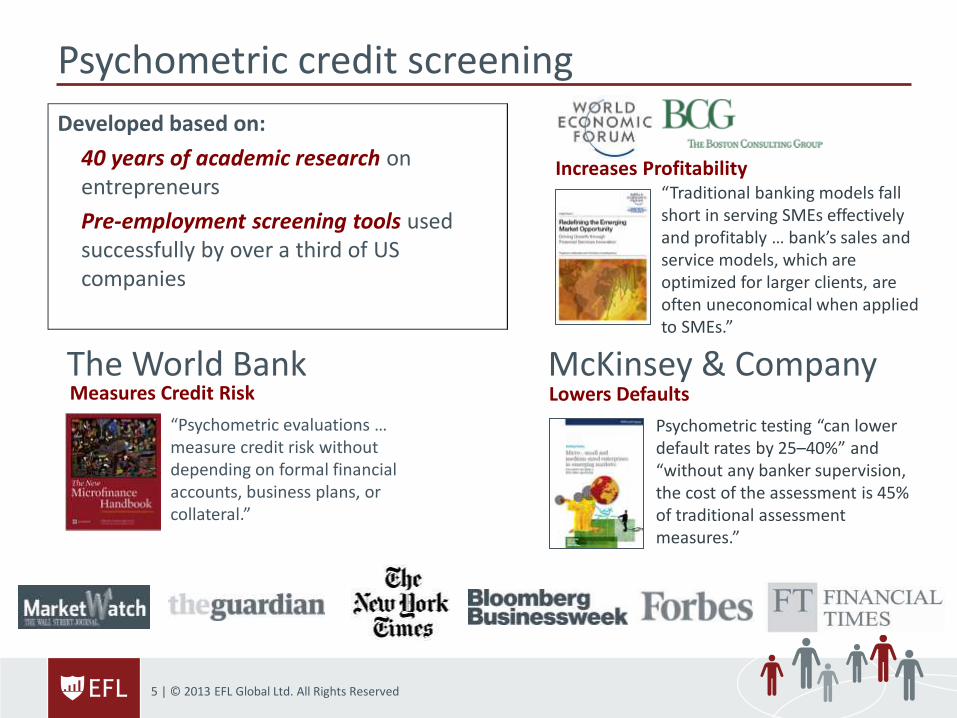

Psychometric credit screening

Developed based on:

40 years of academic research on entrepreneurs

Pre-employment screening tools used successfully by over a third of US companies

Psychometric testing “can lower default rates by 25–40%” and “without any banker supervision, the cost of the assessment is 45% of traditional assessment measures.”

McKinsey & Company Lowers Defaults Measures Credit Risk

“Psychometric evaluations … measure credit risk without depending on formal financial accounts, business plans, or collateral.”

The World Bank

“Traditional banking models fall short in serving SMEs effectively and profitably … bank’s sales and service models, which are optimized for larger clients, are often uneconomical when applied to SMEs.”

Increases Profitability

6 | © 2013 EFL Global Ltd. All Rights Reserved

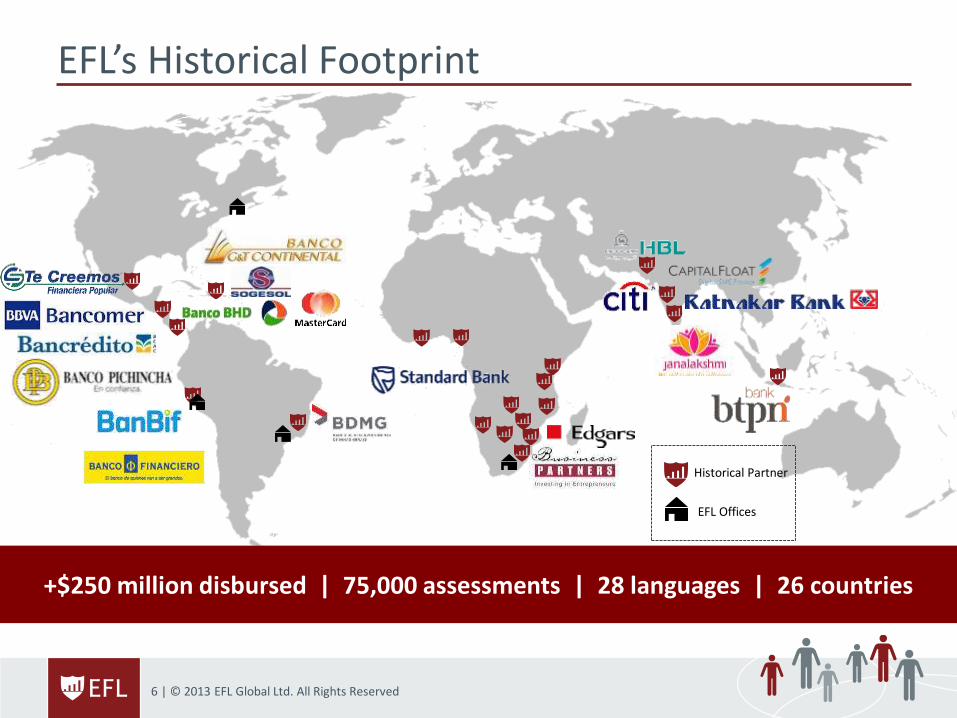

EFL’s Historical Footprint

Historical Partner

EFL Offices

+$250 million disbursed | 75,000 assessments | 28 languages | 26 countries

7 | © 2013 EFL Global Ltd. All Rights Reserved

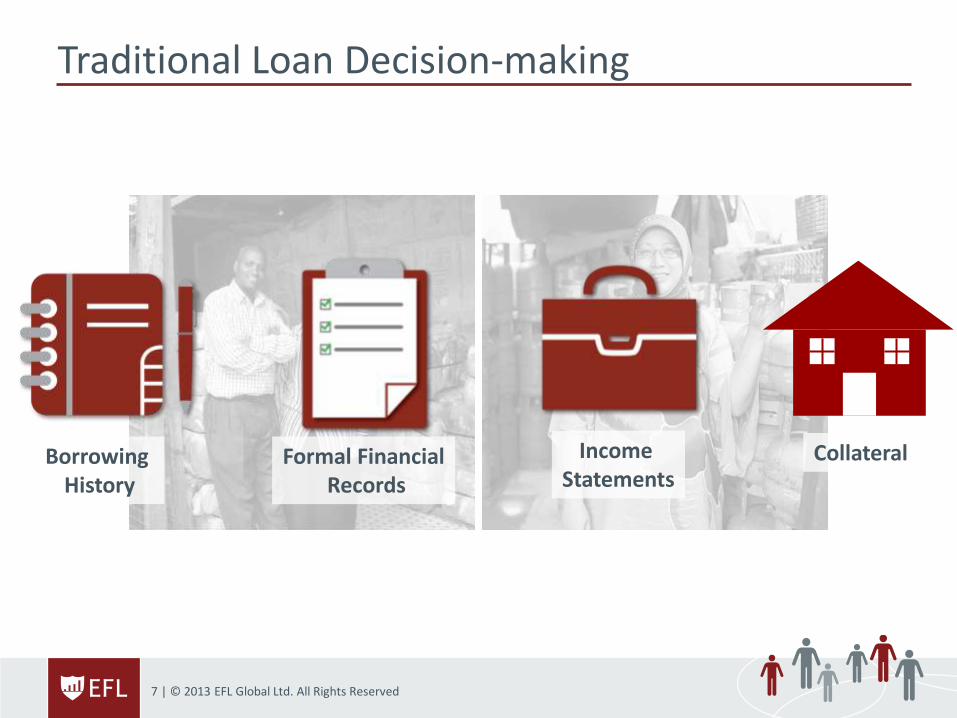

Traditional Loan Decision-making

Income Statements

Collateral Borrowing History

Formal Financial Records

8 | © 2013 EFL Global Ltd. All Rights Reserved

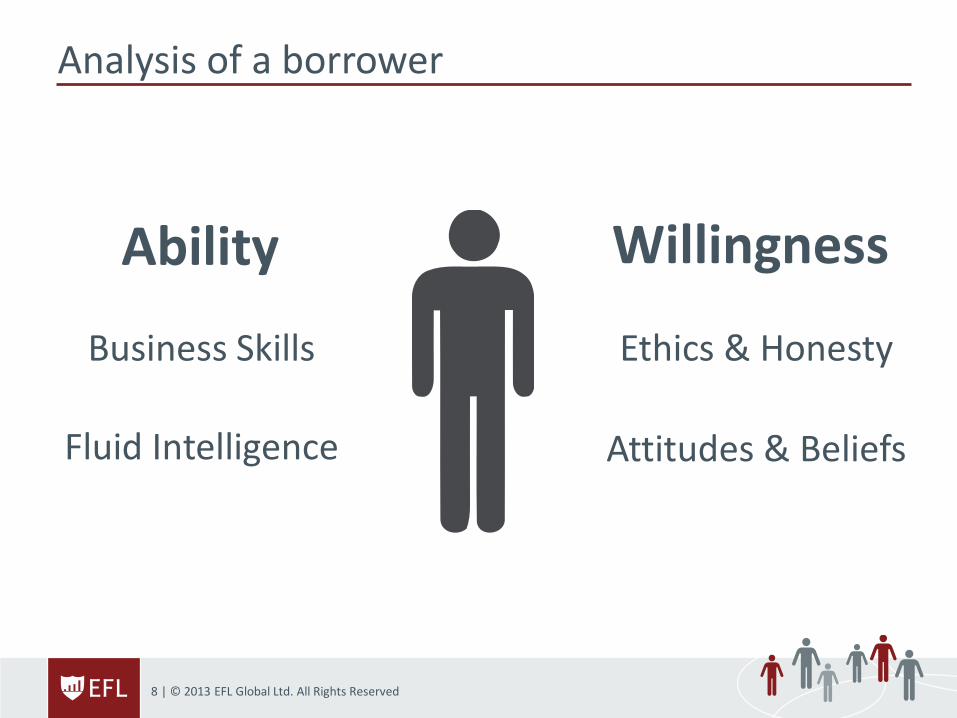

Analysis of a borrower

Attitudes & Beliefs

Ethics & Honesty

Fluid Intelligence

Business Skills

Willingness Ability

9 | © 2013 EFL Global Ltd. All Rights Reserved

EFL’s software

10 | © 2013 EFL Global Ltd. All Rights Reserved

Partner applications

Thin File Clients Existing Customers

Current Approvals No File Clients

The EFL Score can be used as a stand-alone or supplementary tool for a variety of different borrower profiles

11 | © 2013 EFL Global Ltd. All Rights Reserved

3 Case Studies

1. Large, low risk microfinance in India

2. Credit bureau partnership in Peru

3. New product and market entry in Kenya

12 | © 2013 EFL Global Ltd. All Rights Reserved

EFL Case Study: Indian MFI

13 | © 2013 EFL Global Ltd. All Rights Reserved

India Case Study: Project Overview • Leading Indian Microfinance Bank engaged EFL’s credit scoring

methodology to control risk in low-information borrowing population.

• EFL survey administered alongside existing application materials to determine predictive power in pilot phase.

• Partner bank administered more than 6,000 EFL surveys and disbursed more than 3,000 loans, allowing EFL to track and evaluate the performance of the EFL tool in the Indian microfinance segment.

14 | © 2013 EFL Global Ltd. All Rights Reserved

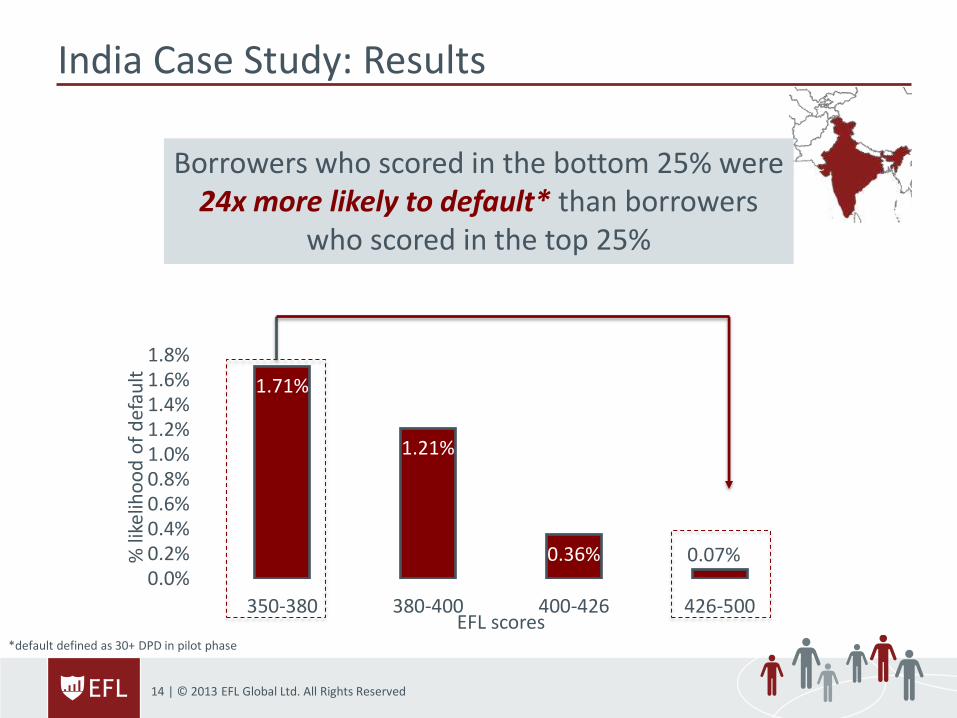

India Case Study: Results

Borrowers who scored in the bottom 25% were 24x more likely to default* than borrowers

who scored in the top 25%

*default defined as 30+ DPD in pilot phase

1.71%

1.21%

0.36% 0.07% 0.0%0.2%0.4%0.6%0.8%1.0%1.2%1.4%1.6%1.8%

350-380 380-400 400-426 426-500

% li

kelih

oo

d o

f d

efau

lt

EFL scores

15 | © 2013 EFL Global Ltd. All Rights Reserved

EFL Case Study: Peruvian Credit Bureau

16 | © 2013 EFL Global Ltd. All Rights Reserved

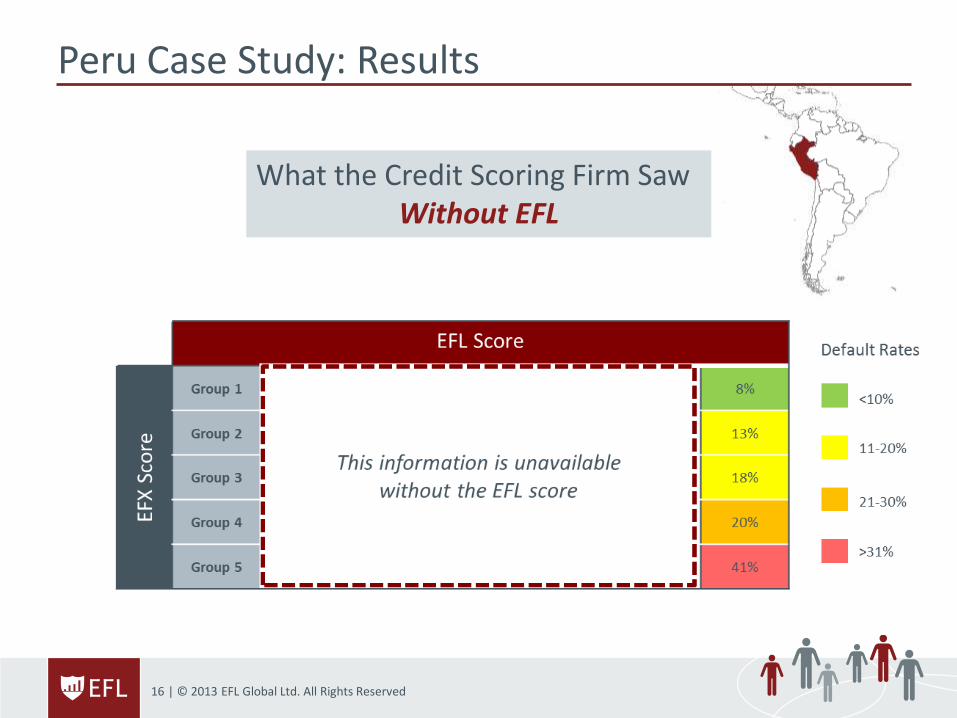

Peru Case Study: Results

What the Credit Scoring Firm Saw Without EFL

17 | © 2013 EFL Global Ltd. All Rights Reserved

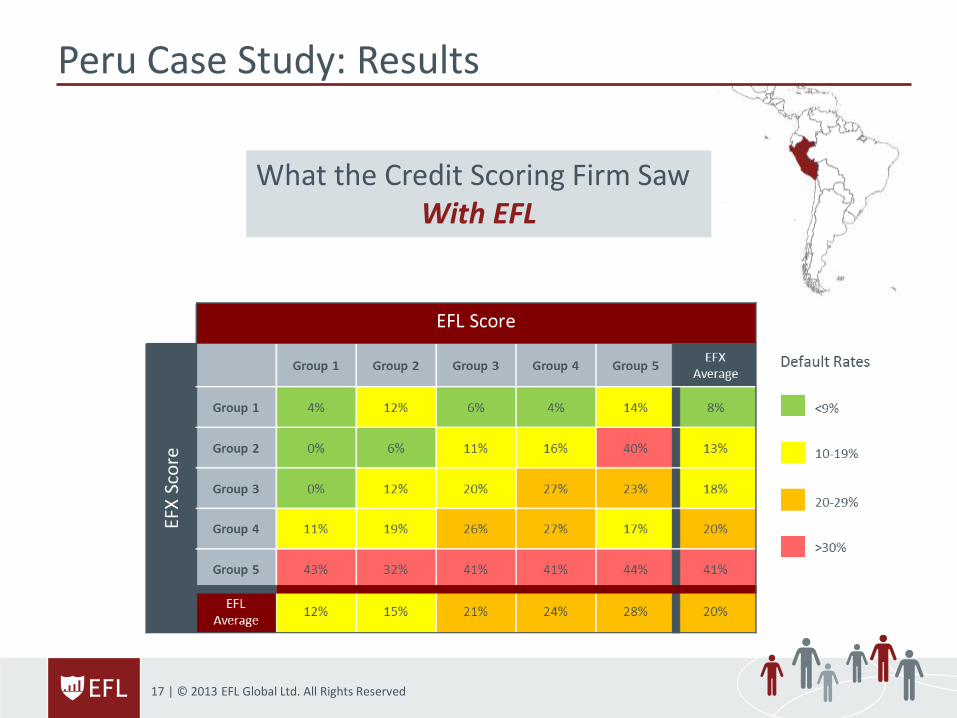

Peru Case Study: Results

What the Credit Scoring Firm Saw With EFL

18 | © 2013 EFL Global Ltd. All Rights Reserved

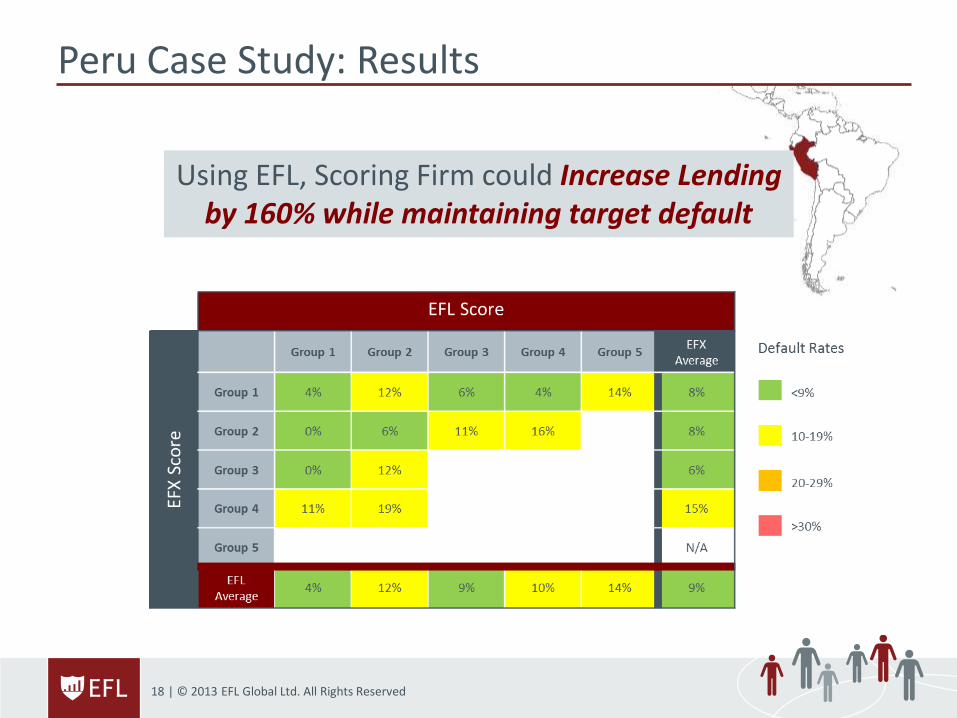

Peru Case Study: Results

20%

52%

8% 9%

EFX EFX + EFL

Acceptance Rate Default Rate

Using EFL, Scoring Firm could Increase Lending by 160% while maintaining target default

19 | © 2013 EFL Global Ltd. All Rights Reserved

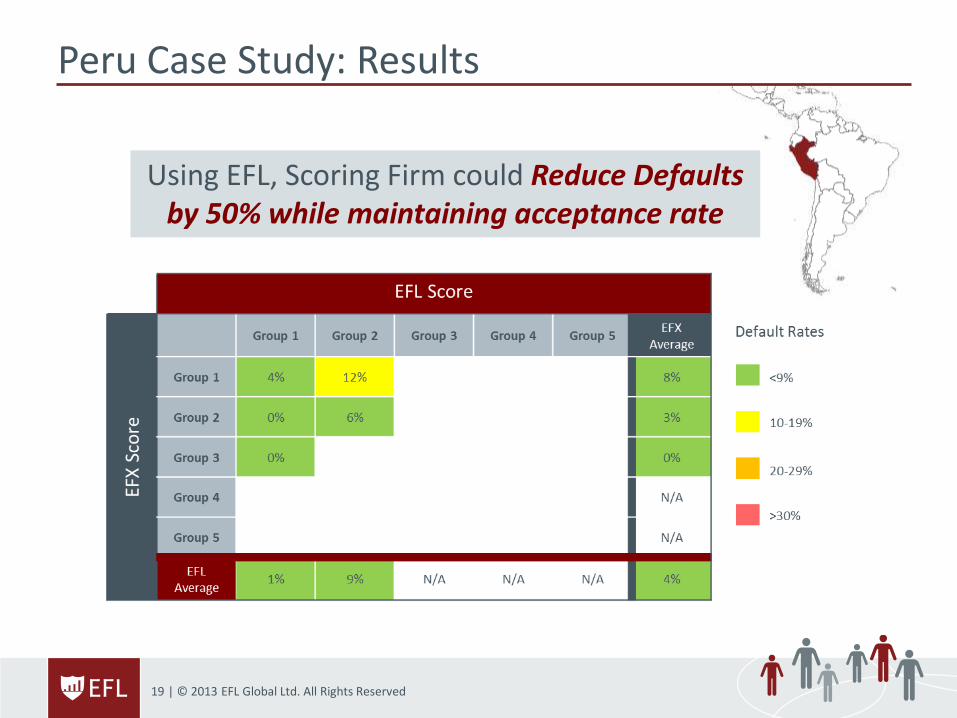

Peru Case Study: Results

Using EFL, Scoring Firm could Reduce Defaults by 50% while maintaining acceptance rate

20% 20%

8%

4%

EFX EFX + EFL

Acceptance Rate Default Rate

20 | © 2013 EFL Global Ltd. All Rights Reserved

EFL Case Study: Kenyan Commercial Bank

21 | © 2013 EFL Global Ltd. All Rights Reserved

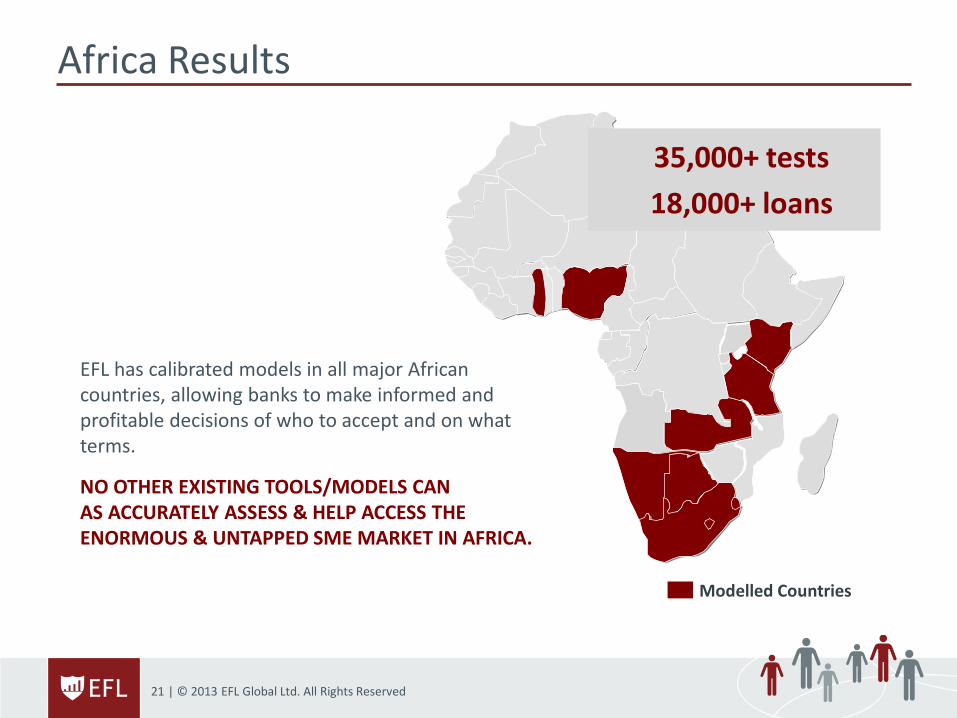

Africa Results

35,000+ tests

18,000+ loans

Modelled Countries

EFL has calibrated models in all major African countries, allowing banks to make informed and profitable decisions of who to accept and on what terms.

NO OTHER EXISTING TOOLS/MODELS CAN AS ACCURATELY ASSESS & HELP ACCESS THE ENORMOUS & UNTAPPED SME MARKET IN AFRICA.

22 | © 2013 EFL Global Ltd. All Rights Reserved

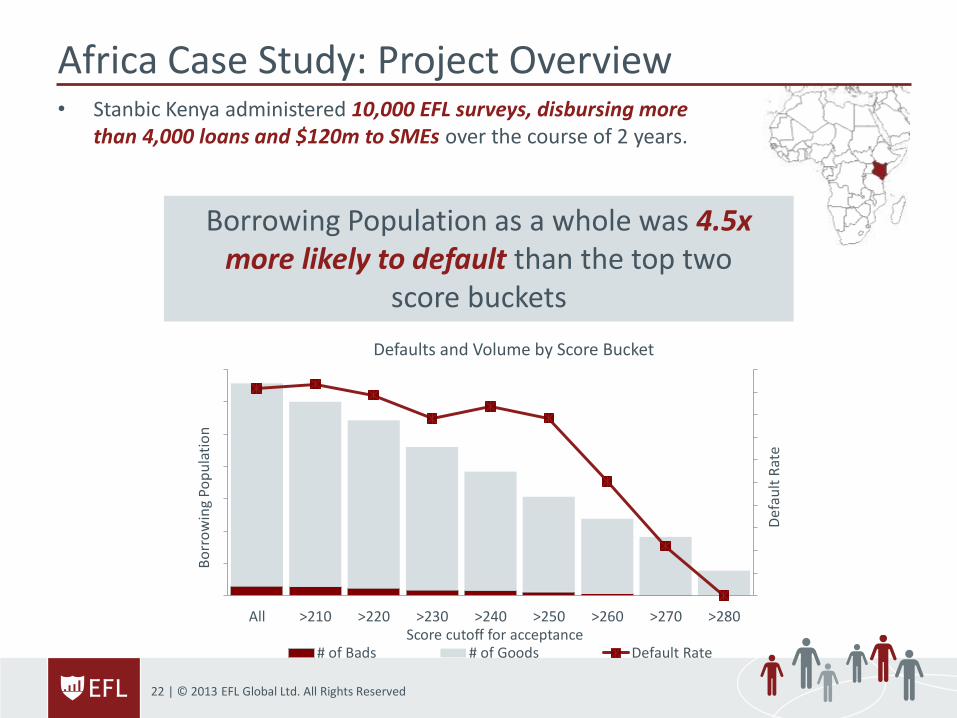

Africa Case Study: Project Overview

0%

1%

1%

2%

2%

3%

3%

4%

4%

5%

5%

0

50

100

150

200

250

300

350

All >210 >220 >230 >240 >250 >260 >270 >280

Bo

rro

win

g Po

pu

lati

on

Score cutoff for acceptance

Defaults and Volume by Score Bucket

# of Bads # of Goods Default Rate

De

fau

lt R

ate

Borrowing Population as a whole was 4.5x more likely to default than the top two

score buckets

• Stanbic Kenya administered 10,000 EFL surveys, disbursing more than 4,000 loans and $120m to SMEs over the course of 2 years.

23 | © 2013 EFL Global Ltd. All Rights Reserved

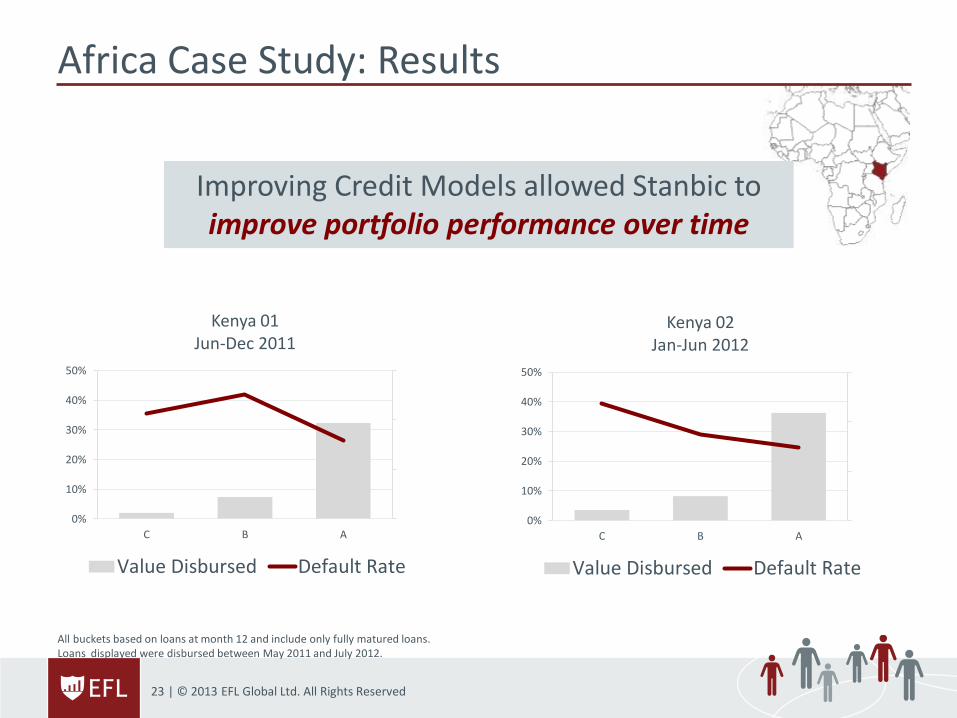

Africa Case Study: Results

All buckets based on loans at month 12 and include only fully matured loans. Loans displayed were disbursed between May 2011 and July 2012.

$-

$1

$2

$3

0%

10%

20%

30%

40%

50%

C B A

Kenya 01 Jun-Dec 2011

Value Disbursed Default Rate

$-

$1

$2

$3

0%

10%

20%

30%

40%

50%

C B A

Kenya 02 Jan-Jun 2012

Value Disbursed Default Rate

Improving Credit Models allowed Stanbic to improve portfolio performance over time

24 | © 2013 EFL Global Ltd. All Rights Reserved

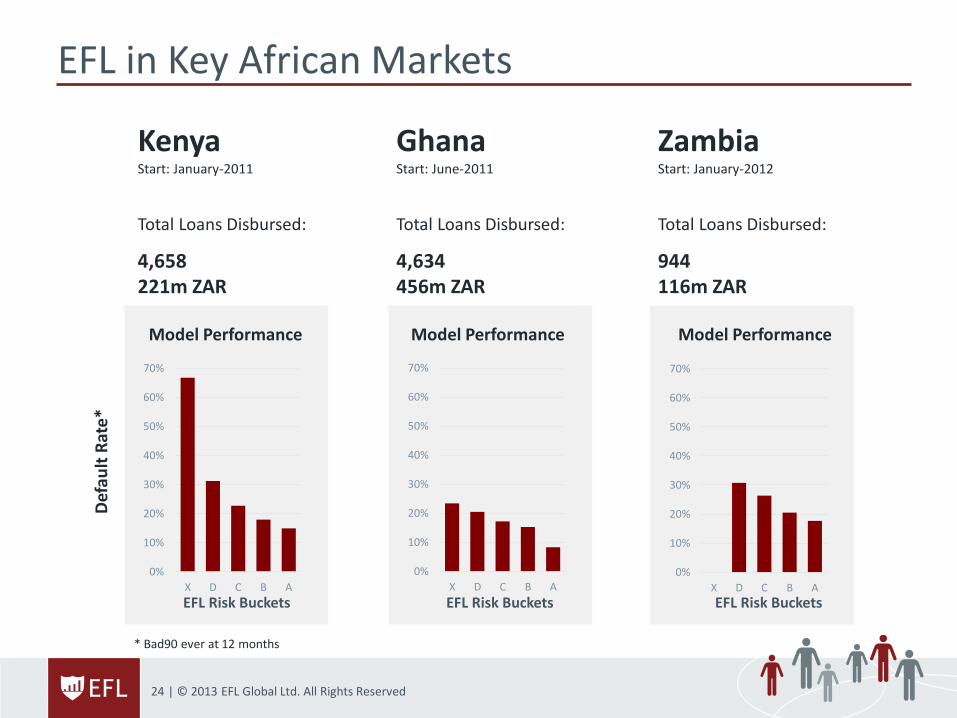

EFL in Key African Markets

Kenya Start: January-2011

Total Loans Disbursed:

4,658 221m ZAR

Ghana Start: June-2011

Total Loans Disbursed:

4,634 456m ZAR

Zambia Start: January-2012

Total Loans Disbursed:

944 116m ZAR

Def

ault

Rat

e*

* Bad90 ever at 12 months

Model Performance Model Performance Model Performance

0%

10%

20%

30%

40%

50%

60%

70%

X D C B A

0%

10%

20%

30%

40%

50%

60%

70%

X D C B A0%

10%

20%

30%

40%

50%

60%

70%

X D C B A

EFL Risk Buckets EFL Risk Buckets EFL Risk Buckets

25 | © 2013 EFL Global Ltd. All Rights Reserved

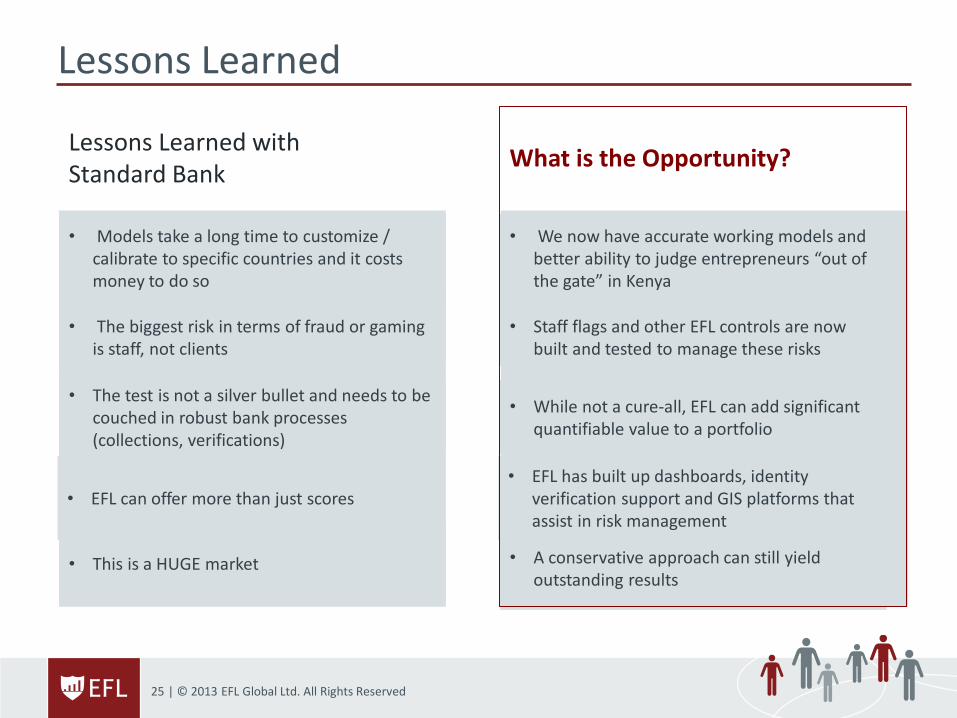

What is the Opportunity?

Lessons Learned

Lessons Learned with Standard Bank

• The biggest risk in terms of fraud or gaming

is staff, not clients

• The test is not a silver bullet and needs to be couched in robust bank processes (collections, verifications)

• This is a HUGE market

• Models take a long time to customize / calibrate to specific countries and it costs money to do so

• Staff flags and other EFL controls are now

built and tested to manage these risks

• While not a cure-all, EFL can add significant quantifiable value to a portfolio

• A conservative approach can still yield outstanding results

• We now have accurate working models and better ability to judge entrepreneurs “out of the gate” in Kenya

• EFL can offer more than just scores • EFL has built up dashboards, identity

verification support and GIS platforms that assist in risk management

![Recapitalisation presentation [xx] [month] 2019 Not for public … · 2019-08-07 · Enormous untapped global resource, particularly in Australia Wave energy available at Australia’s](https://static.fdocuments.net/doc/165x107/5f564772b6549d39ae15fc7d/recapitalisation-presentation-xx-month-2019-not-for-public-2019-08-07-enormous.jpg)