The Taylor Wessing Technology Barometer · PDF fileThe Taylor Wessing Technology Barometer ......

13

The Taylor Wessing Technology Barometer Tracking the temperature of the UK technology sector > April 2015 Powered by:

Transcript of The Taylor Wessing Technology Barometer · PDF fileThe Taylor Wessing Technology Barometer ......

The Taylor Wessing Technology Barometer

Tracking the temperature of the UK technology sector

>April 2015

Powered by:

Contents

Taylor Wessing View .....................................................3

Corporate activity continues ....................................4

Trading and confidence ..........................................7

Sub-sector trends .................................................. 8

M&A and fundraising ............................................ 10

About Taylor Wessing .............................................. 12

All share prices quoted in this document are as at the close of business on 31 March 2015

Taylor Wessing view

#(MBTW)All-Share The Megabuyte Taylor Wessing All-Share continues to out perform the FTSE All-Share in the first quarter of 2015.

#Boardroomconfidence Increased positivity with 46% of respondents feeling more confident about the sector.

#PrivateEquity Visible North American investor interest in the UK tech scene.

#Deals 5 Private Equity deals, valued at £706m.

#CapitalMarkets Capital market fundraising restricted to follow up offerings with no IPOs having taken place.

Your #guide to the top takeaways from this quarter’s Technology Barometer:

Technology Barometer | 3

4 | Technology Barometer

Corporate activity continues

Source: Megabuyte, Capital IQ

Chart 1: Megabuyte Index Series – Q1 2015

In another corporate activity enriched period, the Megabuyte Taylor Wessing (MBTW) All-Share continued to outperform the FTSE All-Share in the first quarter of 2015. This quarter’s performance was helped by Lexmark’s $11 per share bid for Kofax, as well as Bond International’s announcement that it is to put itself up for sale, as part of a strategic review.

Overall, the MBTW All-Share returned 5% in the three months ended March, marginally outperforming the FTSE All-Share, which rose 4% over the same period. The variation in performance is more significant on a 12-month horizon, where an 8% uplift for the MBTW All-Share compares to a return of just 2% for the wider market. The corporate activity in the first quarter follows the recent delistings of Allocate Software, Advanced Computer Software, Incadea and Daisy, which have been acquired by HgCapital, Vista Equity Partners, Dealertrack and a consortium of investors respectively.

From a sector perspective, the latest quarterly performance was similar for Software and ICT Services, up 4% and 5% respectively. However, whilst the Software sector index has risen 12% over the last 12 months, the ICT Services sector is up by just 4%.

The Software sector’s quarterly return was driven by the Accounting & Enterprise Software, Security & Infrastructure Software and Specialist Applications peer groups, which rose 6%, 5% and 7% respectively. The latter was helped by a 13% recovery for AVEVA, whilst the Accounting & Enterprise Software group was strengthened by a 62% rise for Kofax and a 53% uplift for Bond International. Holding back the sector was a 5% decline for the Banking & Insurance Software, with the Innovation Group, Fidessa and First Derivatives all down between 6% and 9%.

The clear outperforming peer group within the ICT Services sector was Data Centre & Hosting Services (+11%), due to a

900

950

1000

1050

1100

1150

06-Jan-15 26-Jan-15 15-Feb-15 07-Mar-15 27-Mar-15

inde

x

MBTW All-Share Software ICT Services

Technology Barometer | 5

Chart 2: Megabuyte Index Series – since inception

Source: Megabuyte, Capital IQ

800

1300

1800

2300

2800

Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14

inde

x

MBTW All-Share Software ICT Services

strong performance by Iomart (+20%). Meanwhile, InternetQ (+29%) and Inmarsat (+16%) helped the Mobile Wireless & Satellite group also post a respectable return of 8%. Returns for the sector’s other peer groups were more modest, with Infrastructure Services and Telecoms & Networks rising 3% and 1%, whilst Consulting & Systems Integration ended the period 2% lower.

Valuations edge higher

The MBTW All-Share PE multiple continued to tick up higher in the first quarter of 2015, reaching 21.0x at the period end. However, whilst this is 8% ahead of where the multiple started the quarter, it remains 3% lower than one year ago. On an EV/EBITDA basis, the MBTW All-Share continues to trade below January 2014 highs of 12.6x EV/EBITDA, but did creep 3% higher over the last three months to end the quarter at 11.0x.

Despite the corporate activity in the Software sector, it was a 14% increase for the ICT Services sector’s PE multiple to 22.9x that drove the MBTW All-Share multiple higher. By contrast, the Software sector multiple was up by just 1% to 18.9x. Similarly, a 7% increase for the ICT Services sector’s EV/EBITDA multiple to 10.5x compared to a marginal decrease for the Software sector to 11.5x.

Within the Software sector, the Banking & Insurance Software PE multiple contracted roughly in line with the share price index to 21.0x, although the group remained the most highly valued software segment on this metric. However, on an EV/EBITDA basis, only the Media & Telecoms Software (9.4x) group is valued below Banking & Insurance Software (10.0x). On this metric, Accounting & Enterprise Software is by far the most highly valued group, on 13.0x EV/EBITDA, helped by the recent corporate activity in this part of the market.

6 | Technology Barometer

Peer Group Weighted average current year valuation

EV/Sales EV/EBITDA PE ratio

Accounting & Enterprise Software 3.6x 13.0x 20.1x

Banking & Insurance software 2.0x 10.0x 21.0x

Media & Telecoms software 2.3x 9.4x 18.7x

Security & Infrastructure Software 3.8x 10.2x 14.6x

Specialist Applications 3.4x 11.5x 18.5x

All Software 3.3x 11.5x 18.9x

Consulting & Systems Integration 2.5x 12.3x 18.0x

Datacentre Hosting Services 5.2x 11.1x 21.2x

Infrastructure Services 0.3x 5.6x 12.5x

Mobile, Wireless & Satellite 5.4x 11.2x 30.1x

Telecoms & Networks 1.8x 10.7x 21.1x

All ICT Services 3.3x 10.5x 22.9x

Megabuyte All Share 3.3x 11.0x 21.0x

Table 1: Peer Group valuations

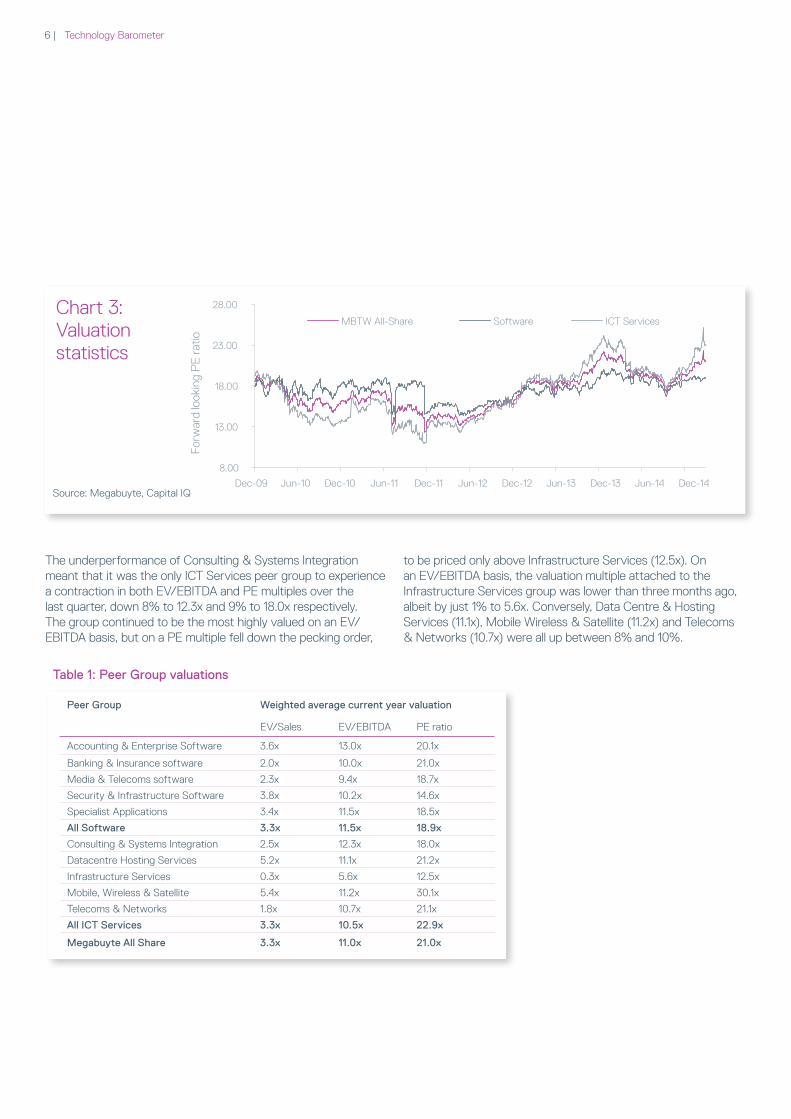

Chart 3: Valuation statistics

8.00

13.00

18.00

23.00

28.00

Dec-09 Jun-10 Dec-10 Jun-11 Dec-11 Jun-12 Dec-12 Jun-13 Dec-13 Jun-14 Dec-14

Forw

ard

look

ing

PE

rat

io

MBTW All-Share Software ICT Services

The underperformance of Consulting & Systems Integration meant that it was the only ICT Services peer group to experience a contraction in both EV/EBITDA and PE multiples over the last quarter, down 8% to 12.3x and 9% to 18.0x respectively. The group continued to be the most highly valued on an EV/EBITDA basis, but on a PE multiple fell down the pecking order,

to be priced only above Infrastructure Services (12.5x). On an EV/EBITDA basis, the valuation multiple attached to the Infrastructure Services group was lower than three months ago, albeit by just 1% to 5.6x. Conversely, Data Centre & Hosting Services (11.1x), Mobile Wireless & Satellite (11.2x) and Telecoms & Networks (10.7x) were all up between 8% and 10%.

Source: Megabuyte, Capital IQ

Technology Barometer | 7

Trading and confidence

Election distractions

Overall Boardroom confidence increased in the first quarter of 2015, although some CXOs view the UK general election as a short term distraction and others believe that the result could have more significant longer term impacts. Nevertheless 46% of the survey’s CXO respondents highlighted that that they are feeling more confident about their company’s prospects than three months ago. The proportion that answered less confident did, however, increase slightly on the previous quarter to 8%, whilst the remaining 46% noted that confidence levels remained unchanged from three months ago.

Interestingly, for the first time in the survey’s history, 100% of Boardrooms were either positive or very positive regarding the prospects of their business over the next 12 months. The fact that there was a 75% and 25% split between ‘positive’ and ‘very positive’ suggests that the CXOs that feel less confident than three months ago were those that had been some of the most bullish in previous surveys. Conversely, those previously feeling ‘negative’ or ‘cautious’ about the outlook, now look to be more optimistic for what lies ahead.

As indicated above, the majority of this quarter’s qualitative responses revolved around the upcoming UK general election. One respondent highlighted that the election is expected to be a major distraction in government circles over the next three months. Meanwhile, another suggested that the result could have a significant impact on the business economy.

Chart 4: CXO change in confidence in Q1 2015

Chart 5: CXO level of confidence over next 12 months

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0%

Very Cautious

Cautious

Neutral

Positive

Very positive

Mar-15 Dec-14 Sep-14 Jun -14

80.0%

Source: Megabuyte

Source: Megabuyte

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0%

No change

More

Mar 15 Dec-14 Sept-14 Jun-14

Technology Barometer | 7

Technology Barometer | 98 | Technology Barometer

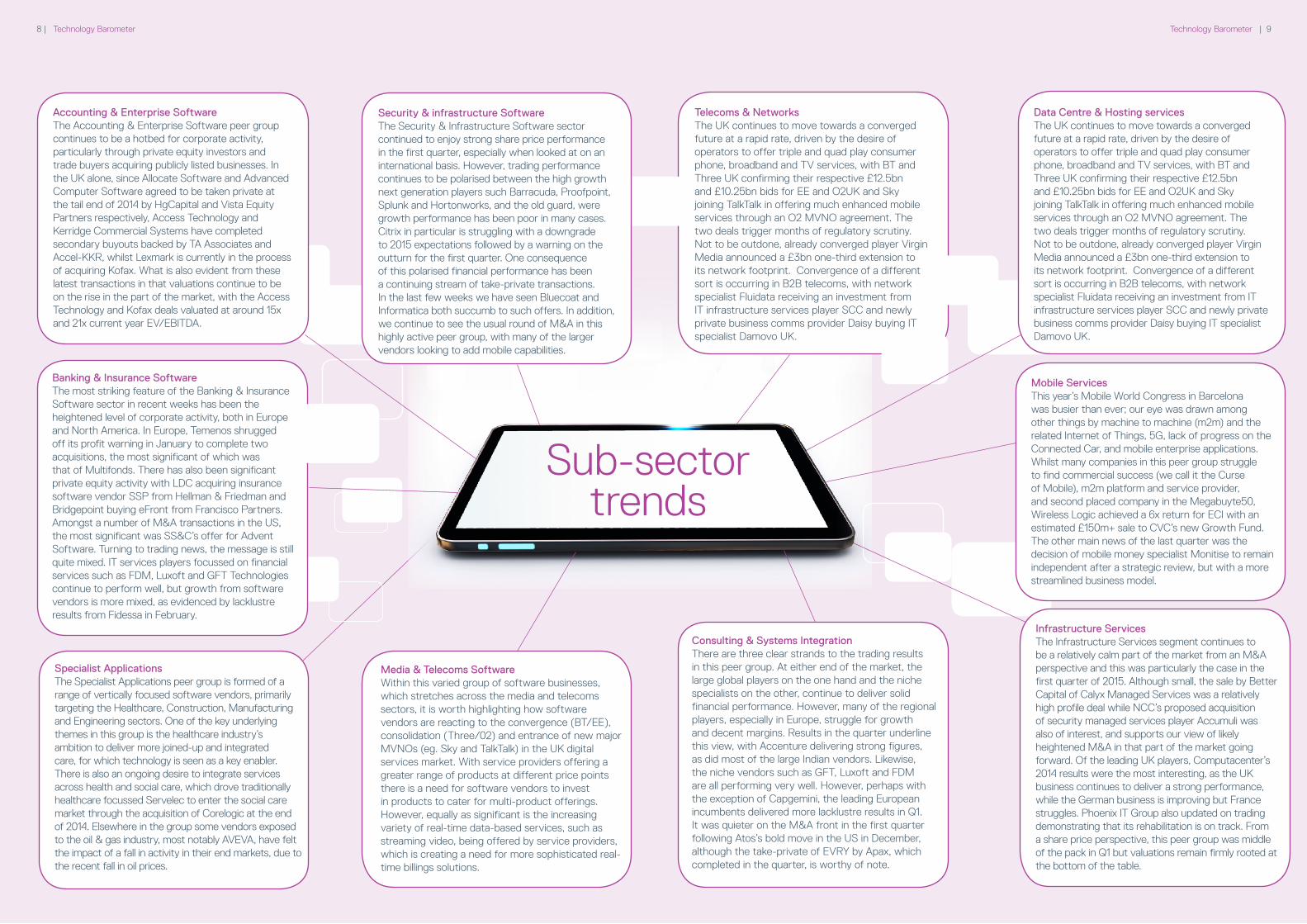

Banking & Insurance SoftwareThe most striking feature of the Banking & Insurance Software sector in recent weeks has been the heightened level of corporate activity, both in Europe and North America. In Europe, Temenos shrugged off its profit warning in January to complete two acquisitions, the most significant of which was that of Multifonds. There has also been significant private equity activity with LDC acquiring insurance software vendor SSP from Hellman & Friedman and Bridgepoint buying eFront from Francisco Partners. Amongst a number of M&A transactions in the US, the most significant was SS&C’s offer for Advent Software. Turning to trading news, the message is still quite mixed. IT services players focussed on financial services such as FDM, Luxoft and GFT Technologies continue to perform well, but growth from software vendors is more mixed, as evidenced by lacklustre results from Fidessa in February.

Telecoms & Networks The UK continues to move towards a converged future at a rapid rate, driven by the desire of operators to offer triple and quad play consumer phone, broadband and TV services, with BT and Three UK confirming their respective £12.5bn and £10.25bn bids for EE and O2UK and Sky joining TalkTalk in offering much enhanced mobile services through an O2 MVNO agreement. The two deals trigger months of regulatory scrutiny. Not to be outdone, already converged player Virgin Media announced a £3bn one-third extension to its network footprint. Convergence of a different sort is occurring in B2B telecoms, with network specialist Fluidata receiving an investment from IT infrastructure services player SCC and newly private business comms provider Daisy buying IT specialist Damovo UK.

Sub-sector trends

Media & Telecoms SoftwareWithin this varied group of software businesses, which stretches across the media and telecoms sectors, it is worth highlighting how software vendors are reacting to the convergence (BT/EE), consolidation (Three/02) and entrance of new major MVNOs (eg. Sky and TalkTalk) in the UK digital services market. With service providers offering a greater range of products at different price points there is a need for software vendors to invest in products to cater for multi-product offerings. However, equally as significant is the increasing variety of real-time data-based services, such as streaming video, being offered by service providers, which is creating a need for more sophisticated real-time billings solutions.

Consulting & Systems IntegrationThere are three clear strands to the trading results in this peer group. At either end of the market, the large global players on the one hand and the niche specialists on the other, continue to deliver solid financial performance. However, many of the regional players, especially in Europe, struggle for growth and decent margins. Results in the quarter underline this view, with Accenture delivering strong figures, as did most of the large Indian vendors. Likewise, the niche vendors such as GFT, Luxoft and FDM are all performing very well. However, perhaps with the exception of Capgemini, the leading European incumbents delivered more lacklustre results in Q1. It was quieter on the M&A front in the first quarter following Atos’s bold move in the US in December, although the take-private of EVRY by Apax, which completed in the quarter, is worthy of note.

Specialist ApplicationsThe Specialist Applications peer group is formed of a range of vertically focused software vendors, primarily targeting the Healthcare, Construction, Manufacturing and Engineering sectors. One of the key underlying themes in this group is the healthcare industry’s ambition to deliver more joined-up and integrated care, for which technology is seen as a key enabler. There is also an ongoing desire to integrate services across health and social care, which drove traditionally healthcare focussed Servelec to enter the social care market through the acquisition of Corelogic at the end of 2014. Elsewhere in the group some vendors exposed to the oil & gas industry, most notably AVEVA, have felt the impact of a fall in activity in their end markets, due to the recent fall in oil prices.

Data Centre & Hosting services The UK continues to move towards a converged future at a rapid rate, driven by the desire of operators to offer triple and quad play consumer phone, broadband and TV services, with BT and Three UK confirming their respective £12.5bn and £10.25bn bids for EE and O2UK and Sky joining TalkTalk in offering much enhanced mobile services through an O2 MVNO agreement. The two deals trigger months of regulatory scrutiny. Not to be outdone, already converged player Virgin Media announced a £3bn one-third extension to its network footprint. Convergence of a different sort is occurring in B2B telecoms, with network specialist Fluidata receiving an investment from IT infrastructure services player SCC and newly private business comms provider Daisy buying IT specialist Damovo UK.

Security & infrastructure SoftwareThe Security & Infrastructure Software sector continued to enjoy strong share price performance in the first quarter, especially when looked at on an international basis. However, trading performance continues to be polarised between the high growth next generation players such Barracuda, Proofpoint, Splunk and Hortonworks, and the old guard, were growth performance has been poor in many cases. Citrix in particular is struggling with a downgrade to 2015 expectations followed by a warning on the outturn for the first quarter. One consequence of this polarised financial performance has been a continuing stream of take-private transactions. In the last few weeks we have seen Bluecoat and Informatica both succumb to such offers. In addition, we continue to see the usual round of M&A in this highly active peer group, with many of the larger vendors looking to add mobile capabilities.

Accounting & Enterprise SoftwareThe Accounting & Enterprise Software peer group continues to be a hotbed for corporate activity, particularly through private equity investors and trade buyers acquiring publicly listed businesses. In the UK alone, since Allocate Software and Advanced Computer Software agreed to be taken private at the tail end of 2014 by HgCapital and Vista Equity Partners respectively, Access Technology and Kerridge Commercial Systems have completed secondary buyouts backed by TA Associates and Accel-KKR, whilst Lexmark is currently in the process of acquiring Kofax. What is also evident from these latest transactions in that valuations continue to be on the rise in the part of the market, with the Access Technology and Kofax deals valuated at around 15x and 21x current year EV/EBITDA.

8 | Technology Barometer Technology Barometer | 9

Mobile ServicesThis year’s Mobile World Congress in Barcelona was busier than ever; our eye was drawn among other things by machine to machine (m2m) and the related Internet of Things, 5G, lack of progress on the Connected Car, and mobile enterprise applications. Whilst many companies in this peer group struggle to find commercial success (we call it the Curse of Mobile), m2m platform and service provider, and second placed company in the Megabuyte50, Wireless Logic achieved a 6x return for ECI with an estimated £150m+ sale to CVC’s new Growth Fund. The other main news of the last quarter was the decision of mobile money specialist Monitise to remain independent after a strategic review, but with a more streamlined business model.

Infrastructure ServicesThe Infrastructure Services segment continues to be a relatively calm part of the market from an M&A perspective and this was particularly the case in the first quarter of 2015. Although small, the sale by Better Capital of Calyx Managed Services was a relatively high profile deal while NCC’s proposed acquisition of security managed services player Accumuli was also of interest, and supports our view of likely heightened M&A in that part of the market going forward. Of the leading UK players, Computacenter’s 2014 results were the most interesting, as the UK business continues to deliver a strong performance, while the German business is improving but France struggles. Phoenix IT Group also updated on trading demonstrating that its rehabilitation is on track. From a share price perspective, this peer group was middle of the pack in Q1 but valuations remain firmly rooted at the bottom of the table.

10 | Technology Barometer

M&A and fundraising

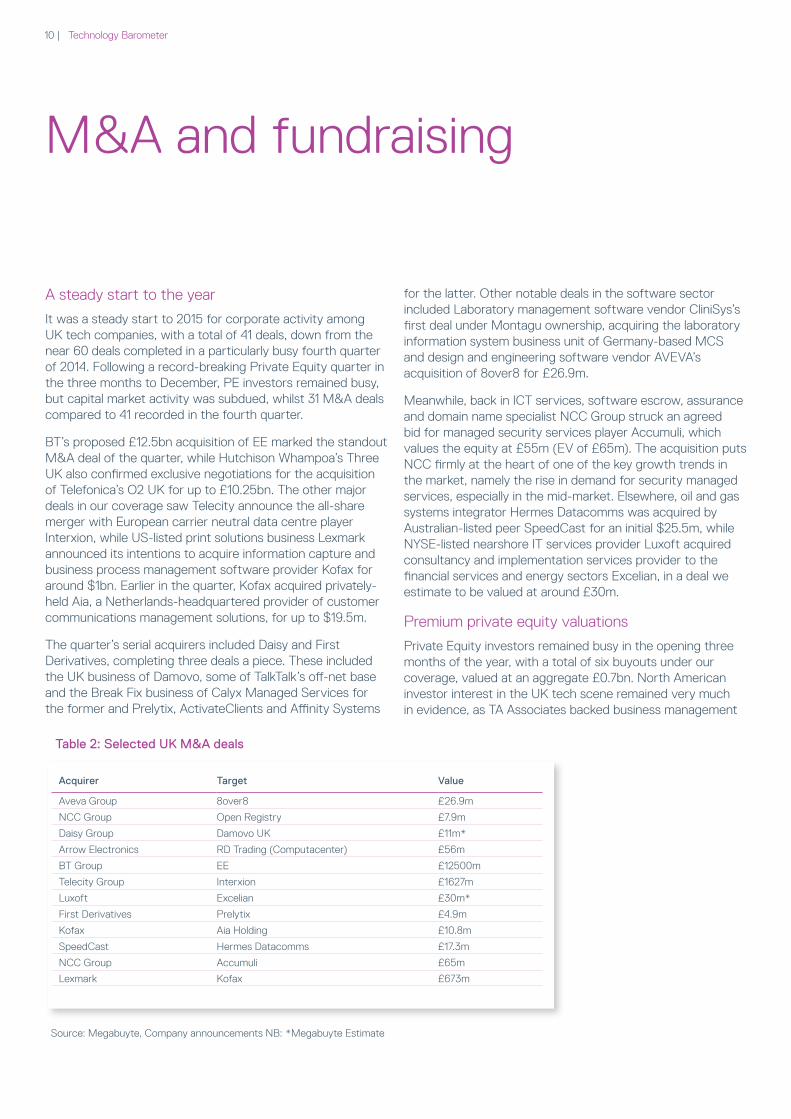

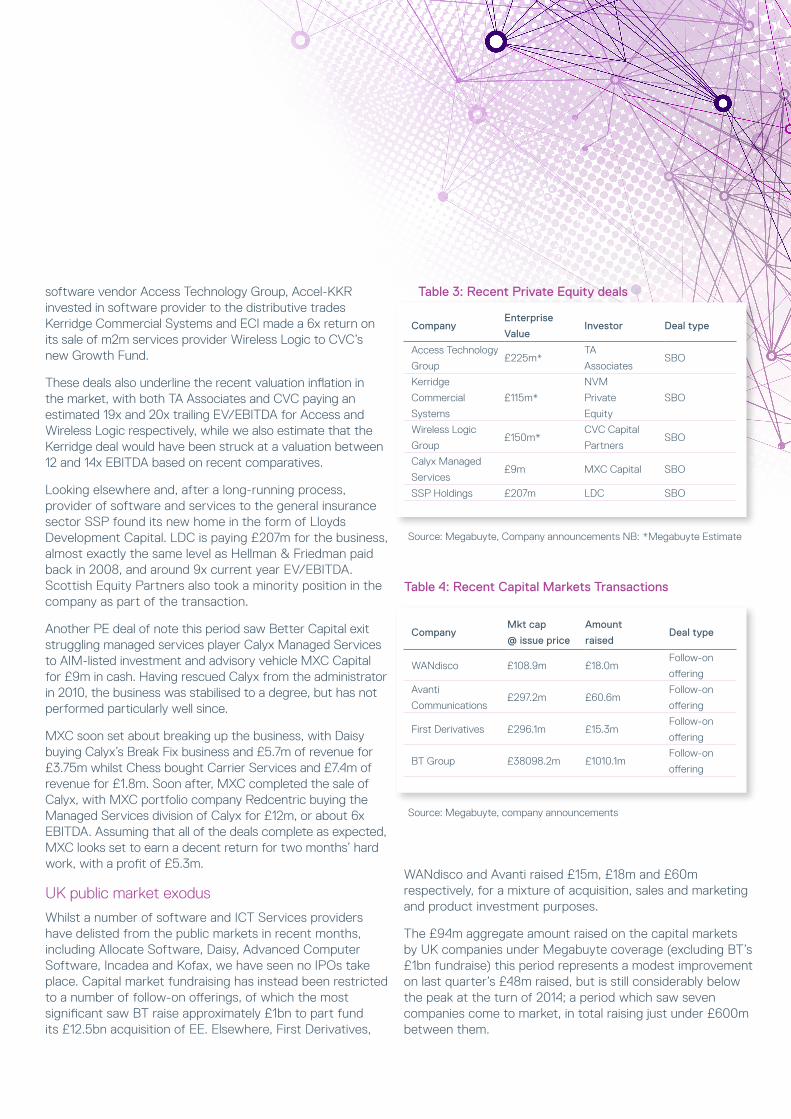

A steady start to the year

It was a steady start to 2015 for corporate activity among UK tech companies, with a total of 41 deals, down from the near 60 deals completed in a particularly busy fourth quarter of 2014. Following a record-breaking Private Equity quarter in the three months to December, PE investors remained busy, but capital market activity was subdued, whilst 31 M&A deals compared to 41 recorded in the fourth quarter.

BT’s proposed £12.5bn acquisition of EE marked the standout M&A deal of the quarter, while Hutchison Whampoa’s Three UK also confirmed exclusive negotiations for the acquisition of Telefonica’s O2 UK for up to £10.25bn. The other major deals in our coverage saw Telecity announce the all-share merger with European carrier neutral data centre player Interxion, while US-listed print solutions business Lexmark announced its intentions to acquire information capture and business process management software provider Kofax for around $1bn. Earlier in the quarter, Kofax acquired privately-held Aia, a Netherlands-headquartered provider of customer communications management solutions, for up to $19.5m.

The quarter’s serial acquirers included Daisy and First Derivatives, completing three deals a piece. These included the UK business of Damovo, some of TalkTalk’s off-net base and the Break Fix business of Calyx Managed Services for the former and Prelytix, ActivateClients and Affinity Systems

for the latter. Other notable deals in the software sector included Laboratory management software vendor CliniSys’s first deal under Montagu ownership, acquiring the laboratory information system business unit of Germany-based MCS and design and engineering software vendor AVEVA’s acquisition of 8over8 for £26.9m.

Meanwhile, back in ICT services, software escrow, assurance and domain name specialist NCC Group struck an agreed bid for managed security services player Accumuli, which values the equity at £55m (EV of £65m). The acquisition puts NCC firmly at the heart of one of the key growth trends in the market, namely the rise in demand for security managed services, especially in the mid-market. Elsewhere, oil and gas systems integrator Hermes Datacomms was acquired by Australian-listed peer SpeedCast for an initial $25.5m, while NYSE-listed nearshore IT services provider Luxoft acquired consultancy and implementation services provider to the financial services and energy sectors Excelian, in a deal we estimate to be valued at around £30m.

Premium private equity valuations

Private Equity investors remained busy in the opening three months of the year, with a total of six buyouts under our coverage, valued at an aggregate £0.7bn. North American investor interest in the UK tech scene remained very much in evidence, as TA Associates backed business management

Source: Megabuyte, Company announcements NB: *Megabuyte Estimate

Table 2: Selected UK M&A deals

Acquirer Target Value

Aveva Group 8over8 £26.9m

NCC Group Open Registry £7.9m

Daisy Group Damovo UK £11m*

Arrow Electronics RD Trading (Computacenter) £56m

BT Group EE £12500m

Telecity Group Interxion £1627m

Luxoft Excelian £30m*

First Derivatives Prelytix £4.9m

Kofax Aia Holding £10.8m

SpeedCast Hermes Datacomms £17.3m

NCC Group Accumuli £65m

Lexmark Kofax £673m

Technology Barometer | 11

software vendor Access Technology Group, Accel-KKR invested in software provider to the distributive trades Kerridge Commercial Systems and ECI made a 6x return on its sale of m2m services provider Wireless Logic to CVC’s new Growth Fund.

These deals also underline the recent valuation inflation in the market, with both TA Associates and CVC paying an estimated 19x and 20x trailing EV/EBITDA for Access and Wireless Logic respectively, while we also estimate that the Kerridge deal would have been struck at a valuation between 12 and 14x EBITDA based on recent comparatives.

Looking elsewhere and, after a long-running process, provider of software and services to the general insurance sector SSP found its new home in the form of Lloyds Development Capital. LDC is paying £207m for the business, almost exactly the same level as Hellman & Friedman paid back in 2008, and around 9x current year EV/EBITDA. Scottish Equity Partners also took a minority position in the company as part of the transaction.

Another PE deal of note this period saw Better Capital exit struggling managed services player Calyx Managed Services to AIM-listed investment and advisory vehicle MXC Capital for £9m in cash. Having rescued Calyx from the administrator in 2010, the business was stabilised to a degree, but has not performed particularly well since.

MXC soon set about breaking up the business, with Daisy buying Calyx’s Break Fix business and £5.7m of revenue for £3.75m whilst Chess bought Carrier Services and £7.4m of revenue for £1.8m. Soon after, MXC completed the sale of Calyx, with MXC portfolio company Redcentric buying the Managed Services division of Calyx for £12m, or about 6x EBITDA. Assuming that all of the deals complete as expected, MXC looks set to earn a decent return for two months’ hard work, with a profit of £5.3m.

UK public market exodus

Whilst a number of software and ICT Services providers have delisted from the public markets in recent months, including Allocate Software, Daisy, Advanced Computer Software, Incadea and Kofax, we have seen no IPOs take place. Capital market fundraising has instead been restricted to a number of follow-on offerings, of which the most significant saw BT raise approximately £1bn to part fund its £12.5bn acquisition of EE. Elsewhere, First Derivatives,

Source: Megabuyte, Company announcements NB: *Megabuyte Estimate

Source: Megabuyte, company announcements

Table 3: Recent Private Equity deals

Table 4: Recent Capital Markets Transactions

CompanyEnterprise

ValueInvestor Deal type

Access Technology

Group£225m*

TA

AssociatesSBO

Kerridge

Commercial

Systems

£115m*

NVM

Private

Equity

SBO

Wireless Logic

Group£150m*

CVC Capital

PartnersSBO

Calyx Managed

Services£9m MXC Capital SBO

SSP Holdings £207m LDC SBO

CompanyMkt cap

@ issue price

Amount

raisedDeal type

WANdisco £108.9m £18.0mFollow-on

offering

Avanti

Communications£297.2m £60.6m

Follow-on

offering

First Derivatives £296.1m £15.3mFollow-on

offering

BT Group £38098.2m £1010.1mFollow-on

offering

WANdisco and Avanti raised £15m, £18m and £60m respectively, for a mixture of acquisition, sales and marketing and product investment purposes.

The £94m aggregate amount raised on the capital markets by UK companies under Megabuyte coverage (excluding BT’s £1bn fundraise) this period represents a modest improvement on last quarter’s £48m raised, but is still considerably below the peak at the turn of 2014; a period which saw seven companies come to market, in total raising just under £600m between them.

12 | Technology Barometer

About Taylor Wessing

Russell HoldenPartner, Head of Corporate Finance+44 (0)20 7300 [email protected]

Mike TurnerPartner, Head of International Technology Group +44 (0)20 7300 4271 [email protected]

Graham HannPartner, Head of UK Technology Group +44 (0)20 7300 4839 [email protected]

Robert FennerPartner, Private Equity+44 (0)20 7300 [email protected]

David MardlePartner, Venture Capital+44 (0)1223 [email protected]

At Taylor Wessing we have a long history of acting for technology companies or those involved more generally in the TMT space. A large portion of our work is providing advice to technology suppliers and users. This means we have a greater familiarity with emerging technologies and business practices than would otherwise be the case.

Our in-depth understanding of the legal issues that can arise in connection with the use of technology is based on specialists who have the requisite experience, both legal and practical, needed to analyse that issue, undertake an informed assessment of the risks and deliver a solution.

We undertake the full range of legal services for our clients in the technology sector including M&A, funding arrangements, intellectual property, commercial contracts, employment and disputes.

Equity Capital Markets

Taylor Wessing has one of the largest dedicated capital markets practices in Europe, with genuine cross-border capability and a strong presence in Asia and the Middle East.

The ECM team advises on transactions involving public companies engaged in European and global securities offerings. As well as having experience advising many technology companies, large and small, we act for listed companies, their sponsors, nominated advisers, brokers and investment banks across all types of European securities offerings.

Our particular expertise in capital markets law and regulation allows us to deal effectively with the increasing disclosure and other ongoing obligations of listed and quoted companies. Our specialist transaction lawyers are highly skilled not only in drafting and negotiating legal documentation, but also in project-managing the transaction process through all stages. This advice includes planning the deal structure and a strategy to complete the transaction, consideration of the tax consequences of the transaction, and how best to mitigate tax.

Private Equity and Venture Capital

Our international private equity practice has really made its mark in the private equity mid-market over the last few years. Our experience in the sector, coupled with our established venture capital and private wealth offerings, allow us to deliver what we believe to be a unique “private capital” model from fund formation and seed investment, through to growth capital and buy-out transactions.

We are flexible in our approach, which is aimed at developing long-term relationships with our clients, and use the existing platform and resources of Taylor Wessing to add value to our clients beyond providing legal services.

Our team works with institutions, individuals and management teams in relation to every aspect of the private equity process.

As a leading firm acting on venture capital transactions, Taylor Wessing is involved in matters ranging from early-stage investments, subsequent funding rounds, convertible debt interim fundings, through to trade sales and IPOs.

Besides our in-depth experience of structuring the corporate and tax aspects of venture capital transactions, we bring our intellectual property expertise to bear as a key component of our advice on investments in all technology-related sectors.

Key Contacts

DisclaimerIS Research Ltd will not accept any liability to any third party who for any reason or by any means obtains access or otherwise relies on this report. IS Research Ltd has itself relied on information provided to it by third parties or which is publicly available in preparing this report. While IS Research Ltd has used reasonable care and skill in preparing this report, IS Research Ltd does not guarantee the completeness or accuracy of the information contained in it and the report solely reflects the opinions of IS Research Ltd.

The information provided by IS Research Ltd should not be regarded as an offer to buy or sell securities and should not be regarded as an offer or solicitation to conduct investment business as defined by The Financial Services and Markets Act 2000 (“the Act”) nor does it constitute a recommendation. Opinions expressed do not constitute investment advice. Any information on the past performance of an investment is not necessarily a guide to future performance. IS Research Ltd operates outside the scope of any regulated activities defined by the Act. If you require investment advice we recommend that you contact an independent adviser who is authorised by the Act to conduct such services. IS Research Ltd does not have any direct investments in any companies contained in the report and has compiled this report on an independent basis.

NB_001570_04.15

© Taylor Wessing LLP 2015 This publication is intended for general public guidance and to highlight issues. It is not intended to apply to specific circumstances or to constitute legal advice. Taylor Wessing’s international offices operate as one firm but are established as distinct legal entities. For further information about our offices and the regulatory regimes that apply to them, please refer to: www.taylorwessing.com/regulatory.html

www.taylorwessing.comEurope > Middle East > Asia