The State of Agricultural Commodity Markets

55

2004 The State of Agricultural Commodity Markets

Transcript of The State of Agricultural Commodity Markets

2004

The State of Agricultural Commodity Markets

Copies of FAO publications can be requested from:

SALES AND MARKETING GROUP

Information DivisionFood and Agriculture Organization of the United NationsViale delle Terme di Caracalla00100 Rome, Italy

E-mail: [email protected]: (+39) 06 57053360Web site: http://www.fao.org

2004

The State of Agricultural Commodity Markets

Produced by theEditorial Production and Design GroupPublishing Management ServiceFAO

The designations employed and the presentation ofmaterial in this information product do not imply the expression of any opinion whatsoever on the partof the Food and Agriculture Organization of the United Nations concerning the legal or developmentstatus of any country, territory, city or area or of itsauthorities, or concerning the delimitation of itsfrontiers or boundaries.

ISBN 92-5-105133-X

All rights reserved. Reproduction and disseminationof material in this information product for educationalor other non-commercial purposes are authorizedwithout any prior written permission from thecopyright holders provided the source is fullyacknowledged. Reproduction of material in thisinformation product for resale or other commercialpurposes is prohibited without written permission ofthe copyright holders. Applications for such permission should beaddressed to: ChiefPublishing Management ServiceInformation Division FAO Viale delle Terme di Caracalla, 00100 Rome, Italy

or by e-mail to: [email protected]

© FAO 2004

Photographs:FAO/18350/P. Cenini, FAO/18191/H. Wagner,FAO/19174/M.Marzot, FAO/17720/A. Conti,FAO/20831/R. Messori

4 About this report

6 Foreword

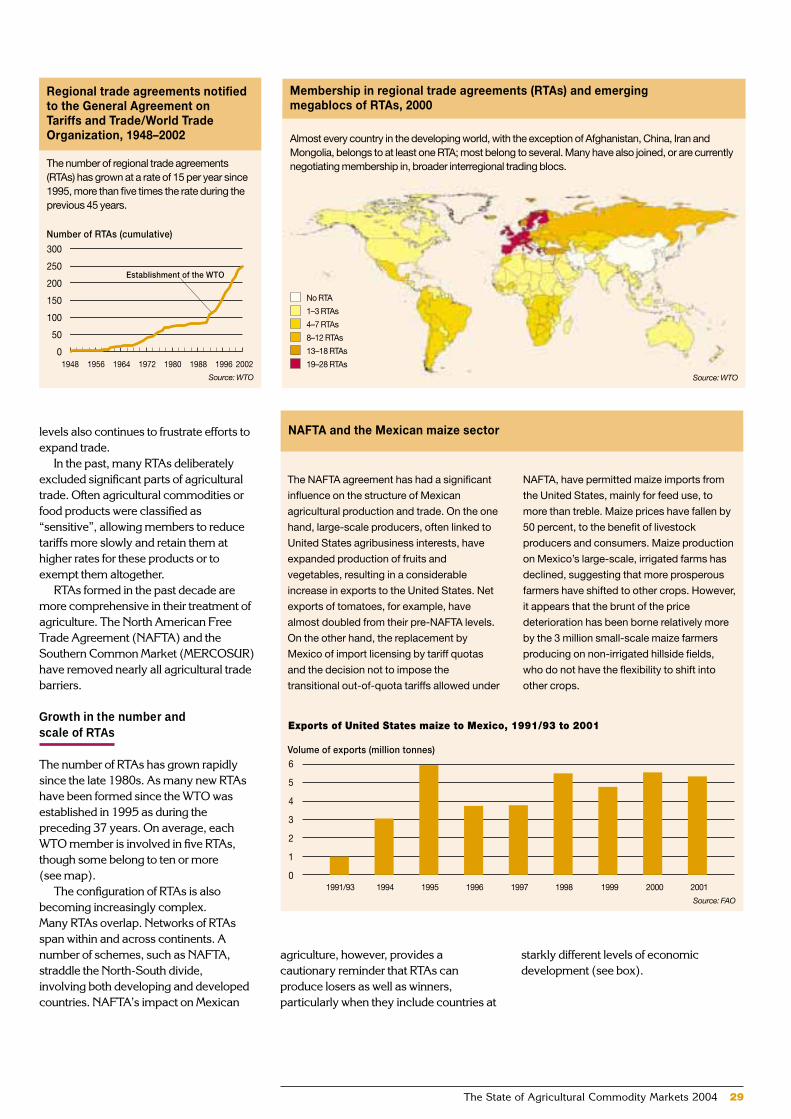

8 Recent developments and long-term trends

8 Current conditions and recent developments on agricultural commodity markets10 Long-term trends reveal structural changes 12 Changing terms of trade for agricultural commodities

14 Food import bills

14 Changing consumption patterns and international trade16 Food import bills strain economies18 Sources of variation in food import bills of least developed countries

20 Agricultural export earnings

20 The risks of dependency on commodity exports22 Barriers to trade in developed countries – tariffs, tariff escalation and producer

support

26 Changing patterns of agricultural trade

26 The evolution of trade in primary and processed agricultural products 28 Commodity trade and regional integration among developing countries30 Market concentration and vertically integrated food chains

32 Conclusions, challenges and policy responses

36 References

38 Annex

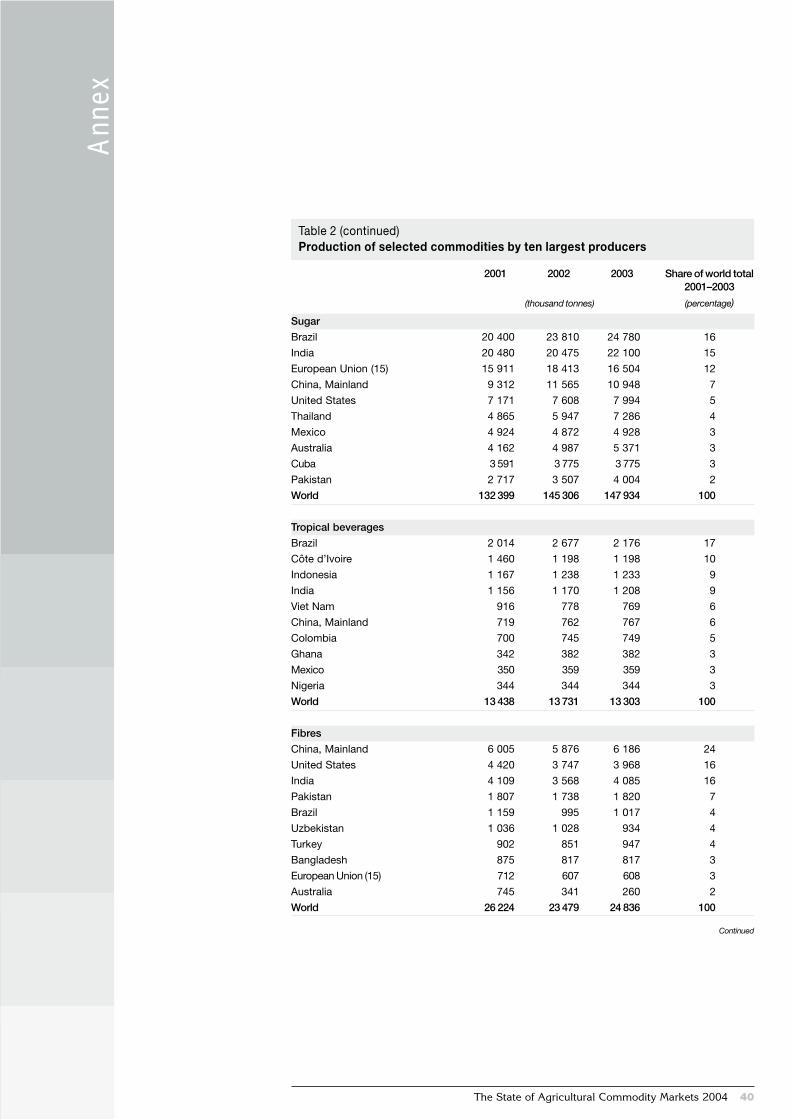

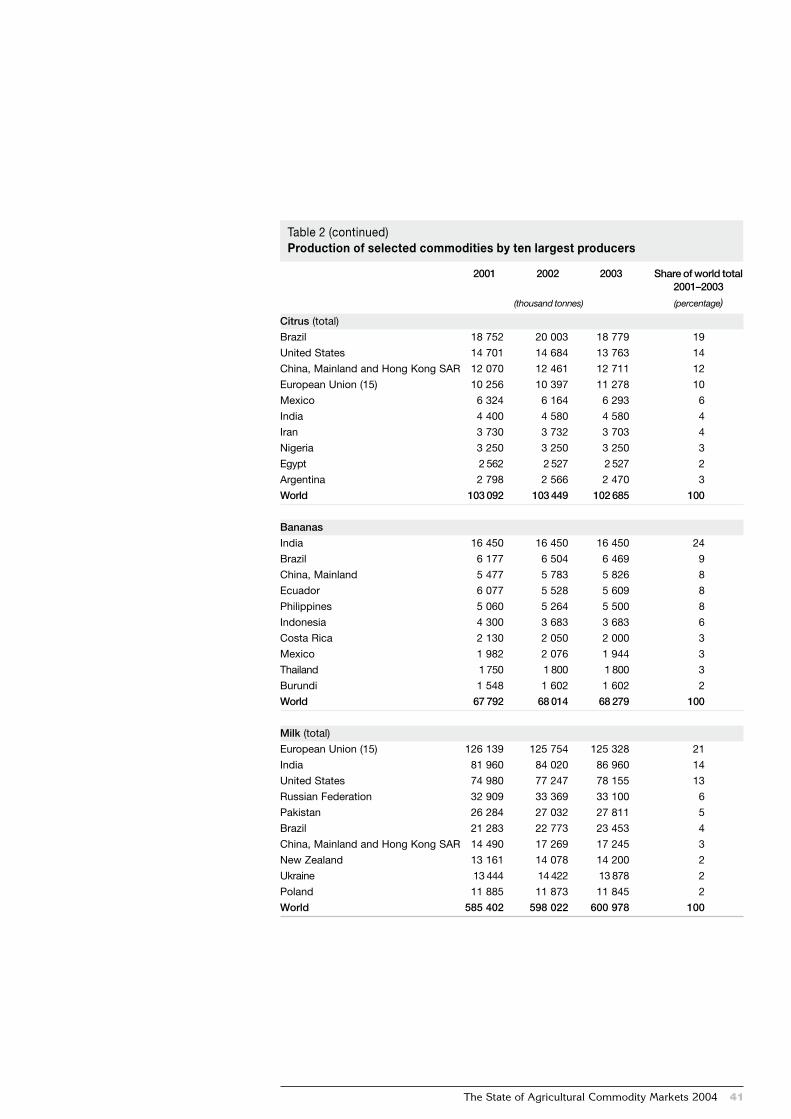

38 Table 1. Commodity prices in real terms 39 Table 2. Production of selected commodities by ten largest producers42 Table 3. Exports of selected commodities by ten largest exporters45 Table 4. Imports of selected commodities by ten largest importers48 Table 5. Terms of trade in agriculture and versus manufactures49 Table 6. Shares of individual commodity groups in total agricultural exports and

imports in each country group50 Table 7. Growth rates in export and import unit values, by country group51 Table 8. Variability in nominal export and import unit values

52 FAO Commodities and Trade Division publications, 2003–04

The State of Agricultural Commodity Markets 2004 3

Contents

The State of Agricultural CommodityMarkets 2004 is the first issue of anew biennial publication that is

intended to expand FAO’s existing series of“State of …” reports. While the findings andconclusions presented rely on technicalanalysis by FAO commodity and tradespecialists, this is not a technical report.Rather, it aims to present commoditymarket issues in an objective, transparentand accessible way to the attention of awider public, including policy-makers,commodity market observers and all thoseinterested in commodity marketdevelopments and their impact ondeveloping countries.

A particular goal is to raise awareness ofthe impact that developments oncommodity markets have on thelivelihoods and food security of hundreds ofmillions of people in the developing world,as well as on the economies of dozens ofdeveloping countries that depend oncommodity exports for a substantialportion of their export earnings.

The report is divided into four mainsections, supplemented by tables thatprovide basic data on current conditionsand historical trends for commodity pricesand terms of trade.

The first section, Recent developmentsand long-term trends, considers trends andvolatility in agricultural commodity pricesand discusses current conditions andrecent developments against thisbackground.

The second section focuses on Foodimport bills. It looks at the changing patternof food imports as developing countrieshave shifted from being net exporters to netimporters of food and other agriculturalproducts. The section also examines theimpact of international food pricemovements on the food import bills ofdeveloping countries in general and theleast developed countries in particular.

The third section, Agricultural exportearnings, looks at the continuingimportance of agricultural exports for theeconomies of many developing countries.

This section examines the implications ofdeclining commodity prices and pricevolatility for commodity-dependentcountries and investigates how tariffs andsubsidies have impeded growth inagricultural exports from developingcountries.

The fourth and final section exploresChanging patterns of agricultural trade,with particular attention to theirimplications for commodity-dependentfarmers and countries in the developingworld. Issues addressed in this sectioninclude the shift in trade from primary toprocessed agricultural products, thegrowing importance and potential forcommodity trade and regional tradeagreements among developing countries,and the impact of increasing marketconcentration as agricultural commoditychains are increasingly dominated by a fewtransnational trading, processing anddistribution companies.

About this report

The State of Agricultural Commodity Markets 2004 4

The State of Agricultural Commodity Markets 2004 5

Acknowledgements

The State of Agricultural CommodityMarkets 2004 was prepared by a team fromthe Commodities and Trade Division ofFAO, led by Alexander Sarris and DavidHallam, and under the general guidance ofHartwig de Haen, Assistant DirectorGeneral, Economic and Social Departmentof FAO.

Material for Section 1 on Recentdevelopments and long-term trends wasprovided by commodity specialists in theCommodities and Trade Division:Abdolreza Abbassian, Pedro Arias,Boubaker BenBelhassen, Concha Calpe,Kaison Chang, Merritt Cluff, Michael Griffin,Ali Gurkan, David Hallam, Pascal Liu,Shakib Mbabaali, Brian Moir, NancyMorgan, Paul Pilkauskas, Adam Prakash,George Rapsomanikis, Shangnan Shui,and Peter Thoenes. The statistical dataunderlying the analyses and many of thegraphics were compiled by the statisticalclerks in the Division: Gianni Borgianelli,Laura Cattaneo, Claudio Cerquiglini,Daniela Citti, Julie Claro, Dino Forzinetti,John Heine, Massimo Iafrate, DanielaMargheriti, Patrizia Masciana, VincenzoMazzucca, Marco Milo, Mauro Pace andBarbara Senfter.

The annex tables providing supportingdata were assembled by Pedro Arias andJulie Claro.

Material for Section 2 on Food importbills was drafted by Ali Gurkan, MerrittCluff, Adam Prakash, and Piero Conforti.

Section 3 on Agricultural exportearnings was prepared by Pedro Arias,Shakib Mbabaali, George Rapsomanikisand David Hallam.

Material for Section 4 on Changingpatterns of agricultural trade was providedby Nasredin Elamin, Hansdeep Khaira andHarmon Thomas.

All of the above reviewed andcommented on draft material. Furtherhelpful comments on earlier drafts werereceived from a number of other FAOprofessionals in the Economic and SocialDepartment, in particular: Jelle Bruinsma,Deep Ford, Ted Gillin, Haluk Kasnakoglu,Panos Konandreas, Ramesh Sharma,Prakash Shetty, Josef Schmidhuber, JacobSkoet and Randy Stringer.

The report was edited by David Hallamwith assistance from Pedro Arias andAndrew Marx.

Long-term trends and short-termshocks on agricultural commoditymarkets affect us all. They have a

direct impact not only on the prices of thefood we eat and the clothes we wear but onthe economic well-being of households,communities and entire nations thatdepend on commodity exports. Lessdirectly but just as inexorably, they affectthe viability of rural communities andlifestyles, the pace of migration to urbanareas and the prospects for sustainabledevelopment.

The impact is greatest on hundreds ofmillions of people and on many of thepoorest countries in the developing world.An estimated 2.5 billion people in thedeveloping world depend on agriculture fortheir livelihoods. For many of them, the saleof agricultural commodities or employmentin producing and processing commoditiesfor export represent their only sources ofcash income. More than 50 developingcountries, including a majority of the leastdeveloped countries (LDCs), depend onexports of three or fewer agriculturalcommodities, typically tropical products,for between 20 and 90 percent of theirforeign exchange earnings. However, manyLDCs are also net food importers, spendingmore than half their export earnings oncommodity markets purchasing foodimports to make up for shortfalls indomestic production. For these people andcountries, developments on internationalcommodity markets may literally spell thedifference between feast and famine.

Declining prices, distorted markets

The long-term trend in real prices foragricultural commodities has beendownwards but prices have also shownmarked variability around that trend. In the second half of the1990s, prices of a number of commodities exported bydeveloping countries fell to their lowestlevels since the Great Depression of the1930s. The price of coffee plummeted 70

percent between 1997 and 2001,threatening the livelihoods of an estimated25 million people who depend on coffeeand triggering food emergencies in severalcountries in Africa and Central America.On the other hand, the lower prices forbasic foods enabled many poorconsumers, especially in urban areas, tomeet their food needs at lower cost and togain access to more nutritious diets.

Although commodity markets haverebounded in recent months, anddramatically so in the case of cereals, realprices in general continue their long-termdownward trend. Many farmers andexporting countries still find themselvestrapped by their dependency – producingand exporting more but earning less thanthey did in the past. At the same time, food-importing countries have benefited from thedownward trend, but are concerned by thevariability and short-term increases ininternational food prices.

Many reasons can be cited for the long-term decline and short-term volatility of realcommodity prices. Much of the steadydownward trend appears to be structural,reflecting the basic forces of supply anddemand that drive markets: global supplieshave grown more rapidly than demand,fuelled by increased productivity and theemergence of major new producers.

Advances in agricultural productivitythrough improved technology potentiallybenefit both producers and consumers. Theformer stand to gain from lower costs andimproved competitiveness, and the latterfrom lower prices. But it has mainly beenproducers in better-endowed and more-developed regions that have been able totake advantage of productivity gains tostrengthen their position on world markets.The LDCs have seen their share of worldagricultural trade shrink, even as theirdependency on it has remained far higherthan that of other developing countries.

The main beneficiaries of lower foodprices have been consumers in developedcountries and in urban areas of developingcountries. However, for the vast majority of

Foreword

The State of Agricultural Commodity Markets 2004 6

the world’s poor and hungry people wholive in rural areas of developing countriesand depend on agriculture, losses in incomeand employment caused by declines in theprices of the products they market generallyoutweigh the benefits of lower food priceswhen commodity prices fall.

The problem of oversupply has beenexacerbated by government policies in bothdeveloped and developing countries thathave severely distorted agriculturalmarkets.

Tariffs on agricultural imports indeveloped and developing countries haveimpeded growth in agricultural exports fromdeveloping countries. Tariff escalation,where higher tariffs apply to goods exportedat more advanced stages of processing, hasreduced opportunities for developingcountries to export higher-value processedgoods whose prices have beenconsiderably more stable than those forbasic commodities.

In addition to tariffs, farmers indeveloping countries must contend withcompetition from highly subsidized andhighly mechanized producers in theindustrialized countries. Producer support tofarmers in developed countries currentlyadds up to more than US$230 billion peryear, almost 30 times the amount providedas aid for agricultural development todeveloping countries.

Tariffs and other barriers have alsoslowed the growth of trade amongdeveloping countries. South–south tradecould expand rapidly, particularly whereincome growth is high and consumptionlevels remain low. But tariff barriers amongdeveloping countries can be higher thanthose imposed on imports by developedcountries.

Another development in agriculturalcommodity markets has been theincreasing concentration of market powerin the hands of a few transnationalcorporations. Just three companies nowcontrol almost half the coffee roasting in theworld, for example, and the 30 largestsupermarket chains control almost one-third of grocery sales worldwide.

Such transnational enterprises havehelped some smallholders integrate into theglobal market and have helped in thetransfer of modern production anddistribution technology. However, it is amatter of concern that marketconcentration has left others with littlemarket power: FAO’s Panel of Eminent

Experts on Ethics in Food and Agriculturewarned four years ago that “there areserious power imbalances arising from theconcentration of economic power in thehands of a few”.

Making commodity markets work for all

Agricultural commodity prices have shownsigns of recovery in recent months.However, that recovery does not appear tobe secure and the long-term prospects forcommodity-dependent farmers andcountries in the developing world are notbright. On the other hand, further short-term commodity price rises for basic foodsare likely, and may threaten livelihoods inmany low-income food-deficit countries.

Agricultural commodity prices remainhighly volatile, and the tendency for growthin the supply of agricultural commodities tooutpace growth in demand at given pricespersists. High tariffs and subsidies indeveloped countries still hamper marketaccess and depress prices. While tradeamong developing countries is growingfaster than trade between developing anddeveloped countries, opportunities forincreased trade among developingcountries are still undermined by tradebarriers. For some commodities, trade,processing and retailing have becomedominated by a small number oftransnational corporations, and the marketpower of farmers and exporting countrieshas become relatively limited. Concern hasbeen expressed at the apparently smallshare of developing country producers inthe final value of their production.

The commodity market crisis of the1990s has focused attention on all of theseproblem areas and has highlighted the needfor new approaches to resolving many ofthem.

Take the example of price volatility. Pastefforts to deal with the problem emphasizedmeasures to stabilize prices or revenuesdirectly, by managing buffer stocks orproviding compensation to countries thatsuffered from unforeseen shortfalls inexport earnings. For the most part and for avariety of reasons, these measures failed.New approaches aim less at preventingprice swings than at helping farmers andconsumers protect themselves against theirimpact through schemes such as market-based price insurance or forward-pricingsystems.

Efforts to address the long-term problemof excess production of traditional exportcrops must focus both on increasingdemand and controlling supplies of somecommodities and on reducing thevulnerability of farmers and countries thatdepend on these commodities.Diversification strategies that would allowfarmers to shift to growing higher-valuecrops or to producing and trading value-added processed goods can contribute toreducing both supplies and dependency.

Action must also be taken to improveour understanding of the impact thatincreasing concentration in commoditychains has had on competition, prices andthe share of final retail value that goes tofarmers and exporters of agriculturalproducts. Careful monitoring and furtheranalysis are urgently needed, along withsupport for efforts by exporters to increasetheir collective market power. Analysismust also be devoted to understanding howdeclining world prices of basic foodcommodities, as well as the changingmarket structures, affect the food security of the poor in both rural and urban areas.

With the launch of The State ofAgricultural Commodity Markets, FAOhopes to contribute to informed discussionand decisive action in all of these areas. This report will provide a biennial review ofimportant trends in commodity marketsand will highlight major policy issues andoptions for action.

Given the significant role that agriculturalcommodities play in all of our lives and theirvital importance for millions of the world’shardest working and most vulnerablepeople, increased attention and concertedaction are long overdue.

Jacques DioufFAO Director-General

The State of Agricultural Commodity Markets 2004 7

After a steep and prolonged declinein the prices of many agriculturalcommodities to historic lows from

the late 1990s through 2001, prices onworld markets have rebounded, or at leastlevelled off, over the past two years.

The recent recovery reflects reducedsupplies of some commodities andstronger demand for others, as marketshave responded to chronic oversupply andfalling prices caused by changes intechnology, consumer preferences, andmarket structures, policies and institutions.A variety of short-term factors have alsocontributed to the recovery, including theweaker exchange rate for the United Statesdollar, which is used to denominate manycommodity prices.

Fragile recovery for tropical beverages and sugar

Between 1997 and 2001, coffee prices fellby almost 70 percent, plummeting belowthe cost of production in many countries.This steep decline left coffee prices lowerthan they had been 30 years earlier, even in nominal terms, and precipitated foodemergencies in several countries in Africaand Central America that depend heavilyon coffee exports. Coffee prices havestrengthened gradually over the past twoyears as producers, especially in LatinAmerica, have responded to falling pricesby reducing supplies.

Cocoa prices followed a similar trend but rallied earlier, starting in 2000. Therecovery in cocoa prices began to falter bylate 2003, however, as supplies started torise again. The market has been weakenedfurther by competition from “cocoa butterequivalent”, as the European Union (EU)relaxed its regulations on the use of fatsderived from other sources to replace someof the cocoa butter in chocolates.

Tea prices have also been under pressure,as production ran ahead of demandgrowth, reaching record levels in 2003.

Record production and surplus stockshave also continued to pressure world

sugar prices in the second half of the2003/04 crop year.

Horticultural product prices remain sensitive to market balance

Increased supplies from Latin America andsluggish demand depressed banana pricesin 2003. Frozen concentrated orange juiceprices were similarly influenced, althoughfresh fruit prices were shored up byreduced production. While demand growthhas been significant for tropical fruits, pricelevels remain sensitive to market balance.

Fibres and raw materials rebound

Shifts in the price trends for mostagricultural raw materials have been lessdramatic and there has been morevariation among individual commodities.Nevertheless, a broadly similar pattern ofrecovery has emerged in most cases.

Cotton, rubber, jute, sisal and abacaprices have all benefited recently fromstronger demand and slower supplygrowth. Prices for hides and skins, on theother hand, declined through 2003 inresponse to weak demand and increasedsupply.

Cereals and oilcrops register gains

International prices for most cereals surgedduring the second half of 2003, reflectingtight market conditions. In the case of rice,the tightness was exacerbated by theimposition of restrictions on exports inIndia and Myanmar. For wheat, reductionsin exportable supplies in the EU and theCommonwealth of Independent Statesfuelled the price rise. Coarse grain pricescontinued to receive underlying supportfrom sharply reduced exports by China,near-record low stocks in the United Statesand continuing increases in soybeanprices.

The picture for oilseeds is ratherdifferent. In the past few years, prices haveimproved steadily from the low levels

Current conditions and recent developments on agricultural commodity markets

Rec

ent d

evel

opm

ents

and

long

-ter

m tr

ends

The State of Agricultural Commodity Markets 2004 8

recorded in 1999–2000 and producershave responded with a robust increase inproduction. The increase in prices wastriggered mainly by a sustained growth indemand that outstripped the expansion insupplies.

With demand firm and stocks atrelatively low levels, both global output and

prices for oilcrop products are expected tocontinue to rise in the short term.

Dairy prices strong but animal diseasesdisrupt the market for meat

Market balance is also currently favourableto dairy product prices. International prices

have been bolstered in recent months bylimited export supplies and sustainedimport demand. Higher prices areexpected to be maintained during 2004.

The international market for meats, onthe other hand, continues to be disruptedby animal disease outbreaks. During thefirst half of 2004, approximately one-thirdof global meat exports were affected byoutbreaks of avian flu or by identified casesof bovine spongiform encephalopathy(BSE). Import bans on poultry and beeffrom disease-affected countries are leadingto higher prices for products originatingfrom disease-free zones. Constrainedexport supplies of meat are also pushingup prices for other animal protein products.

Long-term decline continues

In general, it appears that the balancebetween supply and demand of agriculturalcommodities has improved, and with it theprospects for commodity prices after thesharp and persistent decline during the late1990s. In spite of the recent strengthening,however, agricultural commodity pricesgenerally remain close to historicallydepressed levels – and their longer-termdecline relative to the prices ofmanufactured goods continues.

This secular downward trend is analysedfurther in the following sections of thisreport. For the latest informationconcerning commodity prices and trade,readers are referred to the Commoditiesand Trade Division pages on the FAO Website at http://www.fao.org/es/ESC/en/index.html.

The State of Agricultural Commodity Markets 2004 9

Recent trends in world prices of selected commodities, 1991–2003

Tropical beverages

US$/tonne3 500

3 000

2 500

2 000

1 500

1 000

500

Meat and meat products

4 0003 5003 0002 5002 0001 5001 000

500

Oilseeds, oils/fats and cakes/meals

Index (1990–92 = 100)200

175

150

125

100

75

50

Fibres

US$/tonne2 500

2 000

1 500

1 000

500

0

Sugar

US$/tonne

1991 1993 1995 1997 1999 2001 2003 1991 1993 1995 1997 1999 2001 2003

1991 1993 1995 1997 1999 2001 2003 1991 1993 1995 1997 1999 2001 2003

1991 1993 1995 1997 1999 2001 2003 1991 1993 1995 1997 1999 2001 2003

Cereals

40035030025020015010050

300

250

200

150

100

CoffeeTeaCocoa

US$/tonne US$/tonneMaizeWheatRice

LambPork

BeefChicken

SeedsOils/FatsCakes/Meals

Dairy

US$/tonne2 500

2 000

1 500

1 000

Fruits

US$/tonne2 500

2 000

1 500

1 000

5001991 1993 1995 1997 1999 2001 2003 1991 1993 1995 1997 1999 2001 2003

ButterSkim milkproducts

BananasCitrus

Source: FAO

CottonAbacaSisalJute

Movements in commodity prices onworld markets provide abarometric reading on supply and

demand conditions. Spikes or sharp dropsin prices highlight the impact of shocks thataffect the markets. Long-term trends incommodity prices, on the other hand,reflect the influence of changes intechnology, consumer preferences, andmarket structures, policies and institutions.

A graph of agricultural commodityprices over the past 40 years revealsseveral striking features:■ Real prices of agricultural commodities,

relative to prices of all manufacturedgoods, have declined significantly, evenas nominal prices have risen.

■ Real prices have fluctuated considerablyaround the long-term downward trend.

■ Both the fluctuations and the long-termdecline have been less pronouncedsince the mid-1980s.Over the past four decades, real prices

for agricultural commodities declined byabout 2 percent per year. Several factorshave contributed to this long-term decline.

Prices of agricultural commodities canbe expected to decline relative to industrialproducts as technological advances reducecosts and make it possible, at given prices,to expand production at a rate thatoutstrips both population growth andincreases in demand spurred by risingincomes.

Prices of some commodities have alsobeen driven lower by oversupply, fuelled byintense global competition in production,reduced transportation costs and newtechnologies that have increasedproductivity and introduced syntheticalternatives to some commodities. In somecases, the emergence of major newproducers has also affected marketbalance: between 1985 and 2001, forexample, Viet Nam increased its coffeeexports from less than 10 000 tonnes tomore than 900 000 tonnes, becoming theworld’s second largest exporter, andcontinued to expand production even whenprices plunged between 1995 and 2001.

Export subsidies and subsidies toproducers in some developed countrieshave pushed down world prices for manyagricultural products grown in temperatezones, reducing the export earnings ofdeveloping countries that exportcommodities such as cotton, sugar andrice.

Trends for real commodity prices reveala distinct “breakpoint”. Prior to the mid-1980s, prices fluctuated widely while theoverall trend declined steeply. Since thattime, both the fluctuations and the trendhave flattened out considerably.

This change in the trend of realagricultural commodity prices is explainedin part by a slowdown in the formerly rapidgrowth of prices for manufactured goodsrelative to commodities that had eroded thepurchasing power of revenues fromcommodity exports in the past.

A number of global factors helped slow the rise in nominal prices for all traded goods, including trade policyreforms and increased trade inmanufactured goods, whose prices havetended to fall more quickly as a result oftechnological advances and highproductivity growth. One key factor wasincreased production and trade ofmanufactured goods by developingcountries. Between 1980 and 2000,developing countries almost tripled theirshare of global manufacturing exports,which rose from 11 to 27 percent.

Trade liberalization and technologicalchange have also played a part indiminishing price variability, by reducingthe incidence of supply-side shocks. Trade liberalization has permitted a widerrange of countries to participate in worldcommodity markets, reducing the relative importance of the supply situationin any one country, while technologicaladvances have reduced the vulnerability of some crops to climatic influences.The low price levels reached in recent years have themselves limited the scopefor extensive variability, at leastdownwards.

Long-term trends reveal structural changesR

ecen

t dev

elop

men

ts a

ndlo

ng-t

erm

tren

ds

The State of Agricultural Commodity Markets 2004 10

Impacts differ for both commodities and countries

Although real prices for all agriculturalcommodities have declined over the past40 years, the rate of decline has variedfrom one commodity to another. Rawmaterials, tropical beverages, oilcrops, and cereals have experienced the steepestdeclines. The fall in real prices has beenleast severe for horticultural products, meat and dairy. Some developingcountries have managed to take advantageof these trends by shifting production andtrade into these higher-value sectors. Bydoing so, they have reduced theirdependence on products whose prices

have fallen more sharply and remainedhighly erratic.

For the most part, it has been the moreadvanced and prosperous developingcountries that have managed to do this.Developing countries other than LDCshave more than doubled the share ofhorticultural, meat and dairy products intheir agricultural exports. At the same time,they reduced their reliance on tropicalbeverages and raw materials, bringing theshare of these products in their totalagricultural exports down from more than55 percent in the early 1960s to around 30percent in 1999–2001. But in the LDCs,dependence on these products for theiragricultural export earnings actually

increased from 59 percent to 72 percentduring the same period.

Many LDCs rely heavily on a fewcommodities whose prices not only havefallen sharply but have been highly erratic,further complicating economic planning anddevelopment. Over the past 40 years, priceshave been most volatile for tropicalbeverages and raw materials – the samecommodity groups that have experiencedsome of the steepest long-term declines.Overall, variability from trend levels has beenhighest for agricultural commodities tradedby LDCs and other developing countries andhas been lowest for agricultural productstraded by developed countries, both forexports and for imports.

The State of Agricultural Commodity Markets 2004 11

Agricultural commodity prices, 1961–2002

200

150

100

50

01961 1966 1971 1976 1981 1986 1991 1996 2002

* Real prices deflated by export unit values of all merchandise exports** MUV = Manufactures export unit value

Real prices* for agricultural commodities have declined by almost 50percent over the past 40 years, even though nominal prices have risen.Both trends have slowed significantly since the 1980s.

Index (1991–92 = 100)

Nominal prices

Real prices*

Real price trend

MUV**

Real prices* for agricultural commodity groups, 1961–2002

Source: FAO

1961 1966 1971 1976 1981 1986 1991 1996 2002* Agricultural commodity prices on world markets deflated by

export unit values of all merchandise exports

Index (1991–92 = 100)

SugarHorticultureTropical beveragesRaw materials

CerealsOilcropsMeatDairy

350

300

250

200

150

100

50

0

Changing composition of commodity groups in total agricultural exports, by country grouping

Variability of commodity trade unitvalues, 1961–2001

Price volatility has been greatest for agriculturalcommodities traded by developing countries.

30

25

20

15

10

5

0

Varia

tion

arou

nd tr

endl

ine

(per

cent

)

Exports ImportsSource: FAO

Least developed countries

Other developing countries

Developed countries

More advanced developing countries have been able to reduce theirreliance on tropical beverages, raw materials and sugar, the prices of which have suffered steep declines on world markets. But least developed countries have become more dependent on thesecommodities.

Source: FAO

Percentage of total agricultural exports

50

40

30

20

10

0

1961–63

1999–2001

LDCs ODCsMeat

LDCs ODCsHorticulture

LDCs ODCsSugar

LDCs ODCsTropical

beverages

LDCs ODCsRaw

materials

Source: FAOLDCs = least developed countries; ODCs = other developing countries

For developing countries that dependheavily on commodity exports forforeign exchange, the cash price is

analytically less revealing than is thepurchasing power it provides. Thatpurchasing power is reflected by the“barter” terms of trade – the ratio of pricesof exported goods to the prices of imports.As this ratio diminishes, the quantity ofimports that can be purchased from agiven quantity of exports also shrinks.

For countries where agricultural tradeaccounts for a large proportion of totaltrade, movements in the terms of trade ofagriculture can have importantimplications for the affordability of foodimports and for food security. This isparticularly true for LDCs and some otherdeveloping countries. During thecommodity price boom of the mid-1970sand early 1980s, the prices of agriculturalexports of developing countries increasedmore quickly than the prices of theiragricultural (mainly food) imports. Sincethe mid-1980s, this trend has reversed.Many of these countries have sufferedsevere losses from deteriorating terms oftrade, both between agricultural exportsand imports and between the agriculturalcommodities they export and themanufactured goods they import.

At the aggregate level, terms of tradewithin the agriculture sector worldwideneither rose nor fell significantly between1961 and 2002. However, looking at termsof trade separately for countries in differentincome groups reveals that developingcountries experienced large and persistentfluctuations.

From the mid-1980s to the present,terms of trade for both the LDCs and forother developing countries havedeteriorated significantly. For the LDCs, for example, agricultural terms of trade fell by half from a peak in 1986 to a low in 2001. Because many of these countriesdepend on commodity exports to finance food imports, a decline in terms of trade for agriculture threatens foodsecurity.

For developed countries, on the otherhand, there has been no long-term trend interms of trade in agriculture, and onlyminor fluctuations have occurred duringthe past 40 years.

Changing barter terms of trade betweenagriculture and manufactures

If deteriorating terms of trade in agriculturehave hurt the balance of payments andincreased the debt burden of manydeveloping countries, the fall in terms oftrade between agricultural commoditiesand manufactured imports has been evenmore persistent and more damaging.Between 1961 and 2001, the averageprices of agricultural commodities sold byLDCs fell by almost 70 percent relative tothe price of manufactured goodspurchased from developed countries.

A decline over time in the barter terms oftrade between primary goods andmanufactured goods, with a consequenttransfer of income from developing todeveloped countries, was noted some 50years ago by economists Raul Prebisch andHans Singer. They explained this in termsof the tendencies for economic growth toincrease the demand for manufacturedgoods more than for primary products, andfor productivity to increase more rapidly forprimary products, thus driving the prices ofprimary products lower relative to those ofmanufactured goods. One recent studyfound that productivity increased 20percent faster in agriculture than inmanufacturing worldwide, and more than100 percent faster in developing countriesthan in developed countries.

Most data do indicate a long-termdecline in the barter terms of trade.However, the rate of decline varies and,depending on the time period chosen,fluctuations in the data can make it difficultto distinguish trends from shorter-termvariability. While there is a clear decliningtrend in the terms of trade for agricultureversus manufactures over the wholeperiod, the nature of the trend clearly

Changing terms of trade for agriculturalcommodities

Rec

ent d

evel

opm

ents

and

long

-ter

m tr

ends

The State of Agricultural Commodity Markets 2004 12

changes in the mid-to-late 1980s, and forthe 1990s no significant downward trend isapparent.

Impact of declining terms of trade on developing countries

Although it may be difficult to confirm andquantify a long-term global trend usingstatistical data, there is no doubt that termsof trade for agricultural exports from manydeveloping countries have declinedsignificantly. The decline has been mostpronounced for the countries that canafford it least. Even during the 1990s, whilethe terms of trade for developed and otherdeveloping countries remained relativelystable, they plummeted by 25 percent forthe LDCs.

A decline in the agricultural terms oftrade can be counteracted by increases inthe quantity produced and exported so asto maintain or increase the real value ofexport earnings. In fact, for developingcountries as a group, increases in thequantity of agricultural exports have morethan offset the effect of declining realexport prices, such that the real value oftheir export earnings has risen by nearly 30percent in the last two decades. In otherwords, their “agricultural income terms oftrade” have increased. However, theevolution of the income terms of tradevaried considerably among LDCs andother developing countries. For LDCs,export earnings failed to increase, andrising import prices further eroded theirpurchasing power. Real agricultural exportearnings of LDCs fell by more than 30percent over the same period. Over the last

40 years their income terms of trade havefallen by half.

The region that has suffered most fromdeclining terms of trade is sub-SaharanAfrica. Since the 1970s, their deteriorationhas led to a substantial reduction in thepurchasing power of all African commodity

exports. World Bank estimates suggest thatbetween 1970 and 1997 declining terms oftrade cost non-oil-exporting countries inAfrica the equivalent of 119 percent of theircombined annual gross domestic product(GDP) in lost revenues. Export quantitieshave not grown sufficiently to cover the loss.

The State of Agricultural Commodity Markets 2004 13

Barter terms of trade in agriculture: ratio of export toimport unit values

Source: FAO

Income terms of trade for agriculture

Source: FAO

Barter terms of trade for agriculture versus manufactures:indexed ratios of agricultural export unit values tomanufacturing export unit values of developed countries

300

250

200

150

100

50

Index (1990–91 = 100)

Least developed countries

Other developing countries

Developed countries

Decline in African agriculturalcommodity terms of trade, 1960–2000

Index (1990 = 100)

200

150

100

50

Source: UNCTAD

Terms of trade by commodity group,1975–2000

150

100

50

0

Source: UNCTAD

1975 1980 1985 1990 1995 2000

1961 1966 1971 1976 1981 1986 1991 1996 2002

300

250

200

150

100

50

Index (1990–91 = 100)

Least developed countries

Other developing countries

Developed countries

1961 1966 1971 1976 1981 1986 1991 1996 2002Source: FAO

Index (1970 = 100)

Oilseeds

Raw materials

Tropical beverages

1960

1965

1970

1975

1980

1985

1990

1995

1998

1999

2000

Least developed countries(billion US$)

Other developing and developed countries (billion US$)

1961 1966 1971 1976 1981 1986 1991 1996 2002

109876543210

200180160140120100806040200

LDCs

Other developing countries

Developed countries

Over the course of the past 40 years,the net flow of agriculturalcommodities between developed

and developing countries has reverseddirection. In the early 1960s, developingcountries had an overall agricultural tradesurplus of almost US$7 billion per year. Bythe end of the 1980s, however, this surplushad disappeared. During most of the 1990sand early 2000s, developing countrieswere net importers of agricultural products.FAO has projected that this agriculturaltrade deficit is likely to widen markedly.

The change has been even morepronounced for the LDCs, which over thesame period have changed from being netexporters to significant net importers ofagricultural commodities. By the end of the1990s, imports by the LDCs were morethan double their exports.

Food imports grow rapidly

Global trade in foodstuffs has grown rapidlyand changed radically over recent decades.Between 1970 and 2001, gross world foodimports, measured in terms of calorieequivalents, rose by almost 60 percent. Butthis growth differed markedly among bothcountry and commodity groups.

Gross imports of food by developingcountries grew by 115 percent over thisperiod. Imports by developed countries,which already import a higher proportionof their food, grew by 45 percent. A closerlook at the data reveals that food importsby developing countries increased rapidlyduring the 1970s, grew more slowly duringthe 1980s and accelerated again over the1990s. This pattern holds true both for thevolume of food imports and for the ratio offood imports to availability forconsumption per capita. The expansion offood imports meant that the food tradesurplus of US$1 billion of developingcountries was transformed into a deficit ofmore than US$11 billion during this period.Moreover, this trend is expected tocontinue: according to FAO projections, bythe year 2030, the net food trade deficit ofdeveloping countries is expected to swell tomore than US$50 billion in constant1997–99 US$.

Despite substantial differences in thetrade and dietary profiles of developed anddeveloping countries, imports of particularcommodities appear to be evolving in asimilar manner.

Among the five broad food commoditygroups – cereals, edible oils, animal

Changing consumption patterns and international trade

Food

impo

rt b

ills

The State of Agricultural Commodity Markets 2004 14

Agricultural trade balance of least developed countries, 1961–2002

10 0009 0008 0007 0006 0005 0004 0003 0002 0001 000

0

Since the late 1980s, the least developed countries have become major net importers of agriculturalproducts.

Mill

ion

US

$

Net surplus

Net deficit

Source: FAO

Agricultural imports Agricultural exports

1961 1966 1971 1976 1981 1986 1991 1996 2002

products, sugar, and fruit and vegetables – cereal foodstuffs once dominatedinternational trade. Now, however, theshare of cereals in total agricultural importshas fallen below 50 percent in developingcountries and below one-third in developedcountries. While the share of cereal importshas declined, both developed anddeveloping countries are importing greaterquantities of higher-value and processedfoods, particularly edible oils, livestockproducts and fruits and vegetables.

The falling relative importance of cerealtrade has masked divergent trends amongdifferent grains. Trade shares of the“premium” cereals – wheat and rice – haveregistered strong growth, but caloriedependence on traded coarse grains hasdecreased sharply.

The relative importance of importedsugar also has been in long-term decline.With expanded production and use of non-cane sugar and other sweeteners, sugarimports by developed countries have fallen.

Changing diets, changing trade

Changes in patterns of production,advances in technology and changes indomestic and trade policies play animportant role in determining the structureof international trade. However, the dietsand preferences of consumers and thedemands of an increasingly concentratedfood industry have driven many of the shiftsin trade among commodities. These havebeen further influenced by globalization and

the spreading presence of the fast-foodindustry in developing countries.

Income growth, relative price changes,urbanization and shifts in consumerpreference have altered dietary patterns inboth the developed and developingcountries. When people have more moneyto spend, they add more variety and moreexpensive and high-value foods to theirdiets. These changes are reflected in boththe volume and the composition of worldtrade in agricultural commodities.

Expenditures on foodstuffs andresponses to income changes differbetween developing and developedcountries. In the latter, most consumerscan already afford the foods they prefer.When their incomes rise, changes in theirdiets and food purchases are thereforerelatively small.

In developing countries, on the otherhand, rising incomes have an immediateand pronounced impact on diets andconsequently on trade in both commoditiesand processed foods, as people adjust theirbudgets to include higher-value food items.Similarly, declining real food prices haveallowed poor consumers access toimproved diets at existing income levels.

Since the mid-1970s, for example, percapita meat consumption in developingcountries has more than doubled. Over thesame period, these countries havechanged from being net exporters of morethan 500 000 tonnes of meat to netimporters of more than 1.2 million tonnes.FAO has estimated that over the next 30

years people in the developing world willincrease the quantity of meat, dairyproducts and oils in their diets by 30percent or more. Per capita consumption ofcereals in these countries is not expected tochange, although total cereal use perperson may continue to rise owing to thegrowing use of coarse grains as feed.

In addition to rising incomes, rapidurbanization has contributed to changes inlifestyles, food preferences and the structureof commodity trade. As their numbers andpurchasing power have grown, city-dwellers have increased demand not onlyfor more dietary diversity, but also forproducts that require less time to prepare.Imports of high-value and processed foodproducts have risen to meet this demand. A growing problem of overnutrition andobesity in both developed and developingcountries has appeared alongside theexisting problem of undernutrition.

According to United Nations estimates,the world’s urban population is expected toincrease by 70 percent over the next threedecades. Most of this growth will take placein developing countries, particularly inAfrica and Asia. As recently as 1985,almost 70 percent of the population indeveloping countries lived in rural areas; by the year 2020, more than half of these 6 billion people are expected to live incities. Their higher incomes and urbanlifestyles are likely to bring about furtherchanges in the structure of global imports,accelerating the trend towards higher-valueand processed foodstuffs.

The State of Agricultural Commodity Markets 2004 15

Changes in per capita foodconsumption in developing countries

80

70

60

50

40

30

20

10

0

Consumption of meat, oils, and dairy productshas increased rapidly. Cereal consumption hasnot.

Percentage change

Source: FAO

* Projected

1975–85 1985–98 1998–2015*

Cereals

Sugar

Oilseeds

Meat

Dairy

Urbanization in developingcountries, 1960–2030

By the year 2020, a majority of the more than 6 billion people in the developing world will livein cities.

Source: United Nations

Rural

Urban

4.5

4

3.5

3

2.5

2

1.5

1

0.5

0

Food import bills by country group,1990–2000

120

100

80

60

40

20

0

During the 1990s, developing countriesincreased their nominal food imports by 43 percent and low-income food-deficitcountries by 54 percent.

Billion US$

Source: FAO

* LIFDCs = low-income food-deficit countries;LDCs = least developed countries

Developed Developing LIFDCs* LDCs*countries countries

1995–2000

1990–94

Projected

1960 1970 1980 1990 2000 2010 2020 2030

Billion people

Recent increases in food importshave been particularly significantamong many of the countries that

are most vulnerable to food insecurity. For developing countries as a whole, thevolume of gross food imports grew at anannual rate of 5.6 percent – far higher thanthe 1.9 percent annual growth in developedcountries.

The economic performance ofindividual developing countries played animportant part in determining how quicklythey increased their food imports duringthe 1990s. Countries that recorded strongoverall economic growth, as measured byper capita GDP, increased food importsmore quickly. Rapid growth in theagriculture sector had the opposite effect.Where agricultural value added per capitagrew more quickly, food imports generallydid not.

Neither of these effects is surprising.Food production responds relatively slowlyto changes in demand, as it takes sometime for farmers to increase plantings,harvests or herd sizes. Expansion ofdomestic production can also be hindered

by inherent weaknesses in domestic foodproduction and distribution systems.Examples of such weaknesses include lowproductivity, inefficiencies in supply chainsand marketing systems needed to reachurban consumers, and lack ofcompetitiveness with imported supplies – especially where the latter may havebenefited from developed countrysubsidies. Thus, when incomes anddemand rise rapidly, imports can scale upmore quickly than domestic production.More rapid growth in the agriculture sector,on the other hand, often increases theavailability of domestic foods, reducing thedemand for imports.

Paying for food imports can strain theresources of countries where economicgrowth lags and foreign exchange earningsare limited. Examining how large a slicefood import bills take out of GDP andexport earnings (total merchandiseexports) provides a way of gauging thelevel of “stress” food imports mayrepresent.

Over the past three decades, the shareof gross food import bills in GDP more than

Food import bills strain economiesFo

od im

port

bills

The State of Agricultural Commodity Markets 2004 16

Share of gross food imports (excluding food aid) in total apparent food consumption, 1970–2001

Since 1970, the proportion of imported food in total food consumption (in kcal terms) has increased indeveloping countries.

Percentage

1970 1975 1980 1985 1990 1995 2000

25

20

15

10

5

0

Other developing countries

Low-income food-deficit countries

Least developed countries

Source: FAO

doubled for an average developing country.The increase was most pronounced for theLDCs, where the value of food imports rosefrom about 1 percent of their GDP to over 4 percent. This means that the growth ofgross food import bills has outstrippedoverall economic growth in developingcountries, straining their economicresources.

Comparing the cost of gross foodimports with export earnings reveals thestrain food bills may place on foreignexchange. It also reveals that over the past30 years the countries most vulnerable tofood insecurity (the LDCs) have spent, on average, an increasing share of theirlimited foreign exchange earnings toimport food. In the early 1970s, they spentaround 43 percent of their export earningson commercial food imports, with the otherdeveloping countries spending around 36 percent. Since that time, however, theaverage share for the LDCs increased to 54 percent but declined to 24 percent forthe other developing countries.

Food imports and food aid

In addition to spending an increasing shareof their GDP and foreign exchangeearnings on food imports, LDCs are alsomajor recipients of food aid. When lessfood aid flows to countries that suffer from food shortages, it might be expectedthat commercial food imports would

increase – and the data tend to confirm thatthis is the case.

When the value of food aid increased asa share of total food imports during theearly 1980s, LDCs spent a significantlysmaller share of their GDP and exportearnings on commercial food imports.Since the mid-1980s, however, this trendhas reversed. The value of food aid hasdeclined significantly compared with the

total value of food imports. LDCs appear tohave compensated by dedicating a largershare of domestic resources to boostingcommercial food imports and maintainingnational food security.

The State of Agricultural Commodity Markets 2004 17

Share of food imports in GDP in developing countries, 1970–2001

Since 1970, the share of GDP spent on food imports has increased sharply in developing countries.Among the least developed countries the share has almost tripled.

Percentage

6

5

4

3

2

1

0

Least developed countries

Other developing countries

Share of food import bills in total value of merchandise exports, 1970–2001

Percentage

Source: FAO

1970 1975 1980 1985 1990 1995 2000

1970 1975 1980 1985 1990 1995 2000

90

80

70

60

50

40

30

20

10

0

Least developed countries

Other developing countries

Share of food aid in total value offood imports by least developedcountries, 1970–2001

Food aid accounted for an increasing share oftotal food imports in least developed countriesthrough the mid-1980s, but has declined sincethen.

1970 1975 1980 1985 1990 1995 2000

30

25

20

15

10

5

0

Source: FAO

Percentage

Source: FAO

Since 1990, least developed countries have spent between 50 and 80 percent of the foreign exchangeearned from exports to import food.

Variations in food import bills resultfrom variations in both the pricesand the quantities of food imported.

Import price variation is largely the result ofinternational market volatility. Increasingprices reduce the demand for importedfoods and, if import demand is inelastic,lead to higher import bills at a lowerquantity of imports, with negativeconsequences for food security. Theopposite occurs where import prices fall.Import quantity variation is affected notonly by price, as demand adjusts to pricechanges, but also by other importantfactors, including exogenous changes indomestic production and demand.Analysing the contribution of changes inprices and quantities of food imports tochanges in the food import bills of LDCscould shed some light on the types ofpolicy that would be appropriate forreducing market risks and uncertaintiesfaced by vulnerable developing countries atthe national level.

The results of a study of a sample ofimportant food commodities – wheat,coarse grains, rice, sugar, chicken, skimmilk, soybeans and palm oil – revealconsistent differences among commoditiesin the relative importance of price andquantity variation in determining changes infood import bills. The contributions of the

variations in import prices to import billsranges from around 35 percent to nearly 70 percent. The contribution of pricevariations is significantly (in statisticalterms) lower for basic staples (such assugar, rice, coarse grains and wheat) thanfor those products with higher price andincome elasticities (such as chicken andpalm oil). This implies that food import billsfor staple foods in LDCs are moreinfluenced by variations in domesticproduction that prompt adjustments inimports to satisfy domestic basic foodconsumption needs. For instance, a largenegative shock to domestic staple foodproduction, given the high self-sufficiency in

Sources of variation in food import bills of leastdeveloped countries

Food

impo

rt b

ills

The State of Agricultural Commodity Markets 2004 18

Distribution of the incidence of import price spikes for selected basic foodcommodities faced by least developed countries, 1970–2000

Wheat Coarse grains Rice Sugar Chicken Skim milk Soybeans Palm oil

60

50

40

30

20

10

0

Percentage

Contribution of price variations tovariations in import bills forselected basic food commoditiesfor least developed countries

0 10 20 30 40 50 60 70

ChickenPalm oil

SoybeansSkim milk

WheatCoarse grains

RiceSugar

Percentage

The frequency of spikes in prices for basic food commodities has diminished since the 1970s for allthe commodities surveyed.

1970s 1980s 1990s

Source: FAO

Source: FAO

basic foods of most LDCs, translates into alarge increase in demand for imports. Giventhe inelastic food-security consumptionneeds of LDCs, such large increases inimport demand are not influenced greatlyby international prices. From a policyperspective, these findings suggest thatmeasures designed to address instability indomestic markets for basic food staplesmay play a relatively greater role inreducing instability in their food import bills.

However, measures to cope with theeffects of international price instability maystill be an important component of anoverall strategy to address the uncertaintythat is inherent in food import bills. Importprice changes have a strong influence onLDC food import bills and, with so much oftheir limited foreign exchange earningsbeing spent on food imports, LDCs areparticularly vulnerable to unexpected pricespikes and instability in international foodmarkets. A price spike is defined as anunpredictable extreme price increasebeyond what could be expected as anormal response to the evolution of pricesand quantities. Spikes in internationalprices for basic foods can impose seriousstrains on foreign exchange reserves,especially when they occur simultaneouslywith negative shocks in domestic foodproduction.

Although the number of price spikes hasdiminished for many basic foodcommodities since the 1970s, many LDCshave suffered from extreme price volatility,with a large number of spikes in the pricesof basic food commodities they mustimport to ensure the food security of theirpopulation.

Most of these spikes coincided withmajor events that affected food productionand markets worldwide, such as the “globalfood crisis” of 1974–75. Others, however,coincided with important policy decisions inmajor industrialized regions, such aschanges in domestic support policies in theUnited States and the EU that exacerbatedprice changes in international marketsresulting from normal supply and demandvariations.

Over the past 30 years, the food importbills of LDCs have grown much faster thanboth their overall economies and theirexport earnings. LDCs have alsoexperienced much greater volatility in theirfood import bills, particularly in relation totheir overall economic growth and exportearnings. The combination of high and

unpredictable food import bills undoubtedlystrains the ability of some LDCs to ensurefood security at a national level.

Sudden changes in the markets triggeredby major policy decisions appear to havehad a measurable and potentially damagingimpact on these vulnerable countries.Analysis of these price spikes and theirrelation to decisions on agricultural andtrade policies taken by developed countries highlights the need to assess the

potential impacts of the latter on LDCsduring international policy deliberations,such as those in the World TradeOrganization (WTO), and to plan measuresto mitigate them. In addition, steps should betaken to reduce the vulnerability of LDCsand ensure their access to a steady supply of food on international markets byaddressing problems of short-term worldprice volatility.

The State of Agricultural Commodity Markets 2004 19

Food imports, economic development and food security

Source: FAO

Percentage

0 5 10 15 20 25 30

* Averages for countries grouped by prevalence of undernourishment

Food imports as a share of merchandise exports

Food aid as a share of food imports

Food imports as a share ofapparent consumption

Food insecure(prevalence ofundernourishment > 15 percent)

Relatively food secure(prevalence ofundernourishment < 15 percent)

Average value of food-trade-related variables for least developed countries grouped by prevalence of undernourishment, 1999–2001*

Developing countries that suffer from

widespread hunger tend to depend heavily

on agriculture for employment and incomes

and on exports of agricultural commodities

for foreign exchange revenues. Even though

their populations tend to be predominantly

rural and their economies agricultural,

these countries also rely increasingly on

food imports and spend a high proportion

of their foreign exchange earnings to

purchase them.

Analysis of a wide range of variables

related to economic and agricultural

development, food imports and food

insecurity suggests that the nature and

degree of involvement in international trade

by developing countries are associated with

levels of hunger and food insecurity in

developing countries.

The relationships between food imports,

involvement in international trade and food

security can be demonstrated by dividing

developing countries into two broad groups,

based on the proportion of their population

that is chronically hungry. Countries where

more than 15 percent of the population is

undernourished are classified as food

insecure. Those where the prevalence of

undernourishment is less than 15 percent are

considered to be relatively food secure.

Statistical analysis reveals that food

insecurity is highly correlated with a composite

index based on three indicators related to the

structure of their international trade – the

share of food imports in total merchandise

exports, the share of food aid in food imports

and the share of total food imports in calories

available for consumption.

It appears that countries where hunger is

widespread spend a far higher proportion of

their export earnings on food imports.

Despite this heavy expenditure of limited

foreign exchange, however, these food-

insecure countries cover a smaller share of

their apparent consumption from food

imports. This suggests that food-insecure

countries might import even more food to

cover shortfalls in domestic production and

ensure food security if they were not

constrained by limited export earnings. It also

suggests that the need to expend such a high

proportion of foreign exchange resources on

food imports may reduce the ability of these

food-insecure countries to invest in other

areas that would stimulate development and

reduce their long-term vulnerability.

Many developing countries dependon exports of a small number ofagricultural commodities, even a

single commodity, for a large share of theirexport revenues. This concentration leavessuch countries highly vulnerable tounfavourable market or climaticconditions. A drought or a drop in prices onthe international markets can quickly draintheir foreign exchange reserves, stifle theirability to pay for essential imports andplunge them into debt.

As many as 43 developing countriesdepend on a single commodity for morethan 20 percent of their total revenues frommerchandise exports. Most of thesecountries are in sub-Saharan Africa or LatinAmerica and the Caribbean and depend onexports of sugar, coffee, cotton lint orbananas. Most suffer from widespreadpoverty. More than three-quarters of these43 countries are classified as LDCs, where per capita GDP is less than US$900per year.

Furthermore, recent data show that fewof the countries concerned are reducingtheir commodity dependency. In 14 of thecountries, dependency on a singleagricultural commodity actually increased

between 1986–88 and 1997–99, and onlyseven countries succeeded in reducingtheir reliance on a single commodity. Overthe past 20 years, real prices for many ofthe commodities these countries dependupon have fluctuated widely and fallensignificantly overall (see page 11).

Declines and fluctuations in exportearnings have battered income, investmentand employment in these countries and leftmany of them deeply in debt. TheInternational Monetary Fund (IMF) andWorld Bank have classified 42 countries asHeavily Indebted Poor Countries (HIPCs).Thirty-seven of these rely on primarycommodities for more than half of theirmerchandise export earnings. More thanhalf the world’s cocoa and more than aquarter of its coffee are produced incountries classified as HIPCs.

The high cost of declining prices

Most agricultural commodities haveexperienced a downward trend in realprices, and the long-term forecasts are notencouraging. According to World Bankestimates for 2015, although real prices of

The risks of dependency on commodity exports A

gric

ultu

ral e

xpor

t ear

ning

s

The State of Agricultural Commodity Markets 2004 20

Exporting more coffee, earning less

Source: FAO

1985 1990 1995 2001

Export volume Export value1985 1990 1995 2001

1501209060300

Since coffee prices peaked in the mid-1980s,countries that depend on coffee for more than20 percent of their export earnings haveincreased the volume of coffee they trade by26 percent. But their income from coffeeexports has fallen by almost a third.

Cotton exports grow but income lags

Source: FAO

1985 1990 1995 2001

Export volume Export value

1985 1990 1995 2001

1501209060300

During the 1990s, countries that depend oncotton exports for more than 20 percent oftheir trade revenues increased the volume ofexports by over 40 percent. But theirrevenues fell by 4 percent following a steepdrop in cotton prices.

Index (1989–91 = 100) Index (1989–91 = 100)

Dependence on agricultural export earnings from a single commodity, 1997/99

Forty-three developing countries depend on exports of a single agricultural commodity for more than 20 percent of their total revenues from merchandiseexports. Most of them suffer from widespread poverty, with more than three-quarters classified as least developed countries. Most common among thecommodities they depend upon are coffee, cocoa, cotton, sugar and bananas.

most agricultural commodities areprojected to rise above current levels, theywould still remain below their mid-1990speaks.

For some developing countries, thecollapse of commodity prices wastraumatic, triggering rising ruralunemployment and a steep decline inexport earnings. Lower income fromexports has jeopardized their ability to payfor food imports, particularly in countrieswhere food import bills account for a highshare of the GDP.

If prices for the ten most important (in terms of export values) agriculturalcommodities exported by developingcountries had risen in line with inflationsince 1980, these exporters would havereceived around US$112 billion more in2002 than they actually did. This is morethan twice the total amount of aiddistributed worldwide.

The high cost of price volatility

Although the extent of volatility has declinedover the last 20 years, prices of manyagricultural commodities remain highlyvolatile. Spikes or drops in prices can betriggered by a drought or a bumper crop.They are prolonged and deepened by thefact that both supply and demand forcommodities, especially perennials,respond slowly to price changes.

When stocks are low and prices high,farmers can increase their planting, but theycannot compress the time it takes for cropsto ripen to harvest. In the case of perennialcrops such as coffee or cocoa, that can takeyears. When farmers eventually do increase

production, prices fall as supplies quicklyoutgrow demand in importing countries,given that demand does not growsignificantly in response to lower prices. The result is a pattern of short-lived boomsfollowed by lingering slumps.

Overall, instability tends to be higher foragricultural raw materials and tropicalbeverages than for temperate-zoneproducts. The former are key commoditiesfor export earnings in developing countries.

Declining prices and price volatility costboth farmers and governments in thedeveloping world dearly. A steep orprolonged slump in commodity prices canmake debt repayment difficult, turning short-term borrowing into long-term debt. A recentIMF/World Bank publication cited a sharpdrop in the prices of key export commoditiesas the main reason why the ratio of debt toexports had worsened dangerously in 15heavily indebted poor countries.

Because exports provide the foreignexchange needed to repay debts, the debt-to-exports ratio is often used togauge whether debts are sustainable. The report noted that the countries inquestion depended on exports of cotton,coffee, cashews, fish and copper, all ofwhich had experienced steep pricereductions.

Some countries have managed to limit,at least temporarily, the adverse effects offalling real prices on export earnings andincomes through productivityimprovements and cost reduction.However, widespread adoption of cost-reducing innovations can add to thedownward pressure on prices for all, whilethose exporters not sharing in productivityincreases (often the LDCs) may findthemselves squeezed between fallingprices and costs that are higher thanaverage.

The State of Agricultural Commodity Markets 2004 21

Percentage share of export earnings in total merchandise exports

0 5 10 15 20 25 30 35 0 10 20 30 40 50 60 70 80 0 10 20 30 40 50 60 0 5 10 15 20 25 30 35 40

MauritiusSwaziland

FijiGuyana

BelizeCuba

Sugar

HondurasGuatemala

RwandaUgandaEthiopiaBurundi

Coffee

Central African Rep.TogoMali

BeninChad

Burkina Faso

Cotton

Costa RicaPanamaEcuador

DominicaSt Vincent

St Lucia

Bananas

Instability of nominal world pricesfor selected commodities, 1986–99

Source: FAO

Beef Coarse Wheat Cocoa Sugar Coffeegrains

25

20

15

10

5

0

Average of annual deviationfrom trend (percent)

Commodities traded by developing countriestend to be more volatile than temperate zoneproducts exported by developed countries.

Decline in nominal prices forselected commodities, 1980–2000

Source: IMF

0

-20

-40

-60

-80

Several of the commodities exported bycommodity-dependent countries haveexperienced steep declines over the past twodecades.

Source: FAO

Bananas Tea Coconut Cotton Coffee Cocoa Sugaroil

Percentage

The high level of agriculturalprotection in both developed anddeveloping countries and the high

level of domestic support in the formerhave impeded growth in agriculturalexports from developing countries. Withthe WTO Agreement on Agriculture, theUruguay Round of trade negotiationsinitiated the process of reducing barriers toagricultural trade. But the level ofprotection remains high.

For Organisation for Economic Co-operation and Development (OECD)countries, the average bound tariff foragricultural products is 60 percent,compared with an average rate of 5percent for industrial goods. Averageapplied tariffs on agricultural imports fromdeveloping countries, are estimated to be12 percent in the United States, 20 percentin the EU, 17.5 percent in Canada and 22percent in Japan. (Of course, theseaverages can only give a broad indicationof relative tariff incidence, and will beinfluenced by the commodity and countrycomposition of trade flows.) At the sametime, preferential trade arrangementsoffered by some developed countries,

particularly for the LDCs, have providedmany opportunities for these countries toexpand and diversify their exports. Thesehave increasingly included duty-free andquota-free access to imports from LDCs asunder the EU’s “Everything but Arms”initiative. However, trade preferences havebeen underutilized in many cases. Tariffsapplied by developing countries can alsobe high and are a constraint on theexpansion of trade among them.

Tariff peaks hit hard

Average tariffs faced by developingcountries may be low, but “tariff peaks” thatare substantially higher than the average areapplied for a number of the commoditiesthey export, such as sugar and horticulturalproducts. For each commodity group, thedeveloped countries have more tariff peaksand higher average peak tariffs than thedeveloping countries. According to theWTO, the highest tariff peaks on agriculturalimports in developed countries are as highas 350 percent for tobacco, 277 percent forchocolate, 171 percent for oilseeds, and 134percent for poultry.

According to FAO estimates, if tariffswere reduced by 40–60 percent indeveloped countries and 25–40 percent indeveloping countries, with tariff peaksbeing subjected to the biggest cuts,

Barriers to trade in developed countries – tariffs, tariff escalation and producer support

Agr

icul

tura

l exp

ort e

arni

ngs

The State of Agricultural Commodity Markets 2004 22

Developed countries’ tariffs onagricultural and non-agriculturalproducts by region, 1997

35302520151050

Tariffs levied by industrial countries on imports from each region (percent)

Developed countries levy much higher tariffson agricultural exports from developingcountries than on those from other developedcountries.

East Latin Middle South Sub- IndustrialAsia America East Asia Saharan

Africa

Source: World Bank

Agricultural products

Non-agricultural products

MFN tariff peaks in developedcountry markets on agriculturalimports from developing countries*

400

300

200

100

0

Percentage

* Ad valorem tariffs only** MFN = most favoured nation

Source: WTO

Poultry Chocolate Oilseeds Tobacco

Average weightedMFN tariff**

MaximumMFN tariff**

agricultural exports of LDCs could increaseby as much as 18 percent.

Tariff escalation deters diversification

Exports from developing countries are alsofaced with tariff escalation, in which highertariffs are levied on goods exported at moreadvanced stages of processing. Tariffescalation is pervasive for manyagricultural commodity chains – thesequences of processing steps throughwhich a basic commodity such as cocoabeans is transformed into a final productsuch as chocolate.

A recent FAO study of 16 commoditychains concluded that 12 suffer from tariffescalation, mostly at the first stage ofprocessing. The study also found that tariffescalation is particularly pronounced incommodity sectors (such as meat, sugar,fruit, coffee, cocoa, and hides and skins)that are important to many of the poorestdeveloping countries.

The food-processing industry includessome of the highest levels of tariff escalationand tariff peaks. Tariffs on fully processedfoods in many cases are more than doublethe tariffs on the basic food commodities.This is seen as one reason for the limitedinvolvement of developing countries inexporting processed products. Anotherrecent study by FAO found that fordeveloping countries about 57 percent ofagricultural export earnings came fromprocessed agricultural products comparedwith 68 percent in developed countries. ForLDCs the share of processed products inagricultural exports amounted to only 20percent. However, tariff escalationdiscourages investment in agriculturalprocessing in developing countries andblunts efforts to reduce dependence onprimary commodities and diversify intomore highly valued products. There are, ofcourse, other reasons, including domesticsupply constraints and entry barriers arisingfrom concentration in international markets,which discourage vertical diversification intothe production of value-added forms ofcommodities by developing countries.

Reducing tariff escalation has beenidentified as one of the most importantmarket access issues in the current WTOnegotiations on agriculture. Thirteen of the45 negotiating proposals that have beensubmitted called for substantial reductionsin tariff escalation, particularly in thedeveloped countries.

Subsidiesin developed countries

While tariffs have generally been falling,other policies that may further limit exportsfrom developing countries have not beensubstantially modified. For example,although the value of such support hasdeclined in both nominal and real terms,export subsidies and domestic support in some developed countries haveremained high and have depressed priceson world markets, eroding the incomes and market share of producers in non-subsidizing developing countries anddraining the foreign exchange reserves ofmany countries that depend heavily oncommodity exports.

Total support to farmers in the OECDcountries adds up to more than US$200billion per year. Support has beenparticularly high for products such as rice,sugar, milk, wheat and meat. As the WorldBank recently observed, “although officialexport subsidies may be small andshrinking, effective export subsidiescreated by domestic support areincreasing”. The extent to which domesticsupport has an impact on world marketprices for agricultural commoditiesobviously depends on the form thatsupport takes and the extent to which it is“decoupled”.

In the case of cotton, while there are noexport subsidies in the United States andthe EU, various forms of direct support

The State of Agricultural Commodity Markets 2004 23

Support to agricultural producers indeveloped countries

250

200

150

100

50

0

Farm support in the developed countries totalsmore than US$200 billion per year and hasdeclined only marginally since the late 1980s.

1986–88

2000–02

EU USA Japan OECD

RiceSugar

MilkWheat

Sheep meatBeef and veal

MaizeOilseedsPig meat