The Shape of Things to Come for P/C Insurance Markets … Shape of Things to Come for P/C Insurance...

73

The Shape of Things to Come for P/C Insurance Markets and the American Workplace Robert P. Hartwig, Ph.D., CPCU, President & Economist Insurance Information Institute 110 William Street New York, NY 10038 Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org NCCI Annual Issues Symposium Orlando, FL May 5, 2016 Download at www.iii.org/presentations

-

Upload

truongtuong -

Category

Documents

-

view

217 -

download

0

Transcript of The Shape of Things to Come for P/C Insurance Markets … Shape of Things to Come for P/C Insurance...

The Shape of Things to Come for P/C Insurance Markets and the

American Workplace

Robert P. Hartwig, Ph.D., CPCU, President & EconomistInsurance Information Institute 110 William Street New York, NY 10038

Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

NCCI Annual Issues SymposiumOrlando, FLMay 5, 2016

Download at www.iii.org/presentations

2

P/C Insurance Industry Financial Overview

2015: Second-Best Year in the Post-Crisis Era & Carbon Copy of 2014

Modest CATs, Reserve ReleasesWorkers Comp Helped Too

2

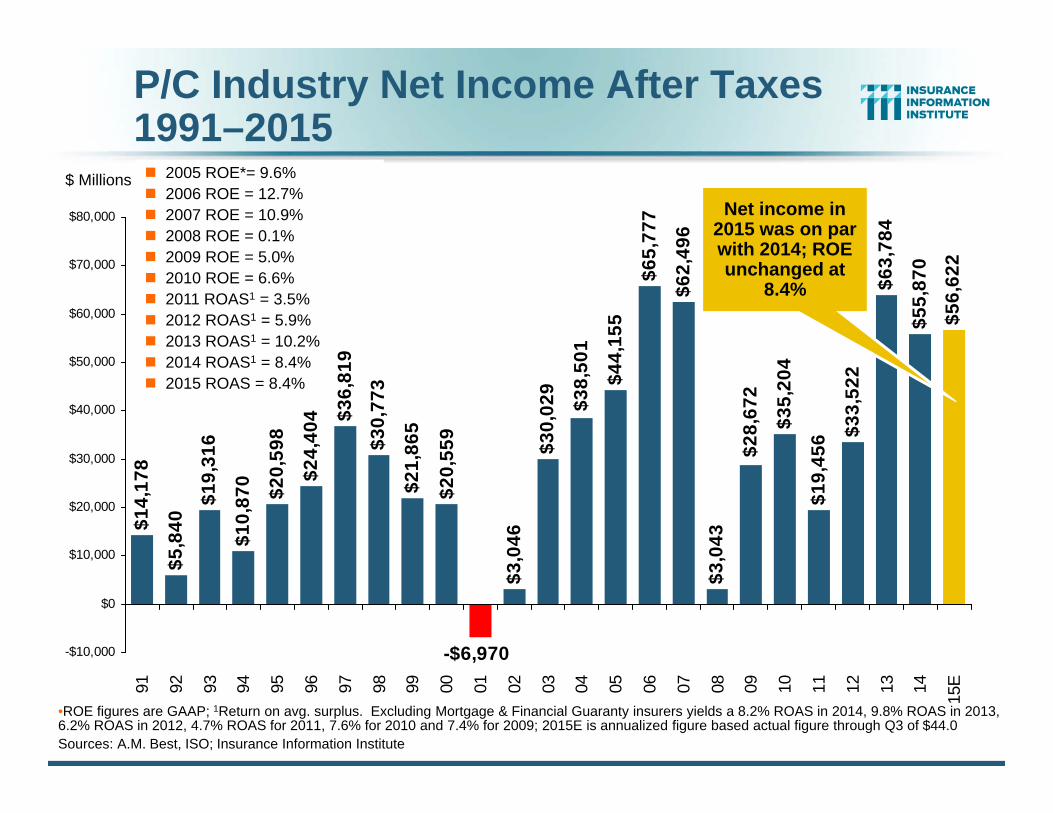

P/C Industry Net Income After Taxes1991–2015 2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.1% 2009 ROE = 5.0% 2010 ROE = 6.6% 2011 ROAS1 = 3.5% 2012 ROAS1 = 5.9% 2013 ROAS1 = 10.2% 2014 ROAS1 = 8.4% 2015 ROAS = 8.4%

•ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 8.2% ROAS in 2014, 9.8% ROAS in 2013, 6.2% ROAS in 2012, 4.7% ROAS for 2011, 7.6% for 2010 and 7.4% for 2009; 2015E is annualized figure based actual figure through Q3 of $44.0Sources: A.M. Best, ISO; Insurance Information Institute

$14,

178

$5,8

40$1

9,31

6

$10,

870 $20,

598

$24,

404 $3

6,81

9$3

0,77

3

$21,

865

$3,0

46$3

0,02

9

$62,

496

$3,0

43

$35,

204

$19,

456 $3

3,52

2$6

3,78

4

$55,

870

$56,

622

$38,

501

$20,

559

$44,

155

$65,

777

-$6,970

$28,

672

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15E

Net income in 2015 was on par with 2014; ROE unchanged at

8.4%

$ Millions

-5%

0%

5%

10%

15%

20%

25%

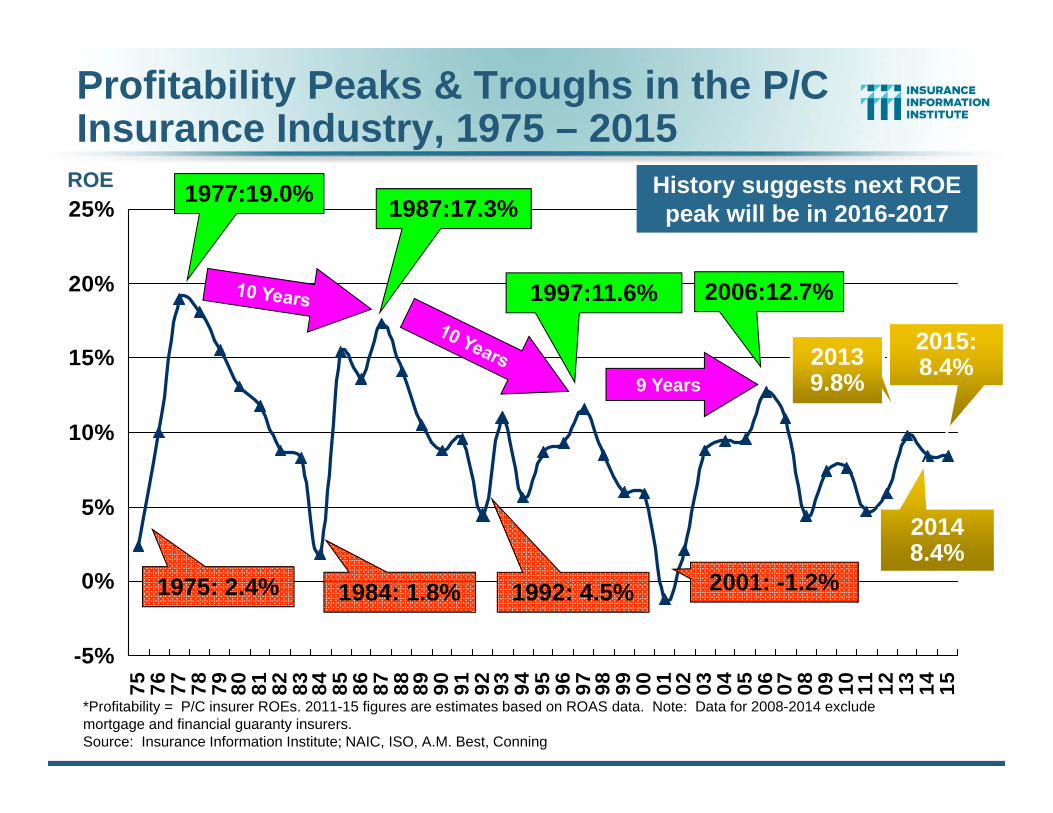

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2015

*Profitability = P/C insurer ROEs. 2011-15 figures are estimates based on ROAS data. Note: Data for 2008-2014 exclude mortgage and financial guaranty insurers.Source: Insurance Information Institute; NAIC, ISO, A.M. Best, Conning

1977:19.0% 1987:17.3%

1997:11.6% 2006:12.7%

1984: 1.8% 1992: 4.5% 2001: -1.2%

9 Years

History suggests next ROE peak will be in 2016-2017

ROE

1975: 2.4%

2013 9.8%

2014 8.4%

2015: 8.4%

5

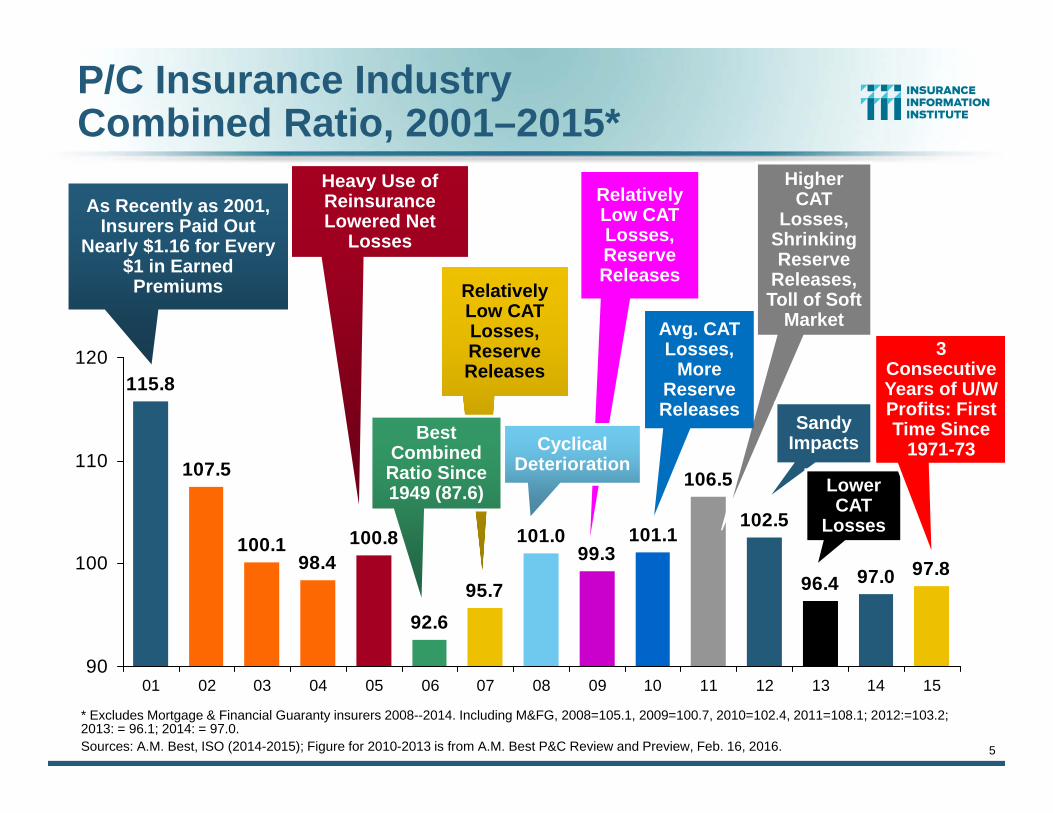

P/C Insurance Industry Combined Ratio, 2001–2015*

* Excludes Mortgage & Financial Guaranty insurers 2008--2014. Including M&FG, 2008=105.1, 2009=100.7, 2010=102.4, 2011=108.1; 2012:=103.2; 2013: = 96.1; 2014: = 97.0. Sources: A.M. Best, ISO (2014-2015); Figure for 2010-2013 is from A.M. Best P&C Review and Preview, Feb. 16, 2016.

95.7

99.3101.1

106.5

102.5

96.4 97.0 97.8101.0

92.6

100.898.4

100.1

107.5

115.8

90

100

110

120

01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

As Recently as 2001, Insurers Paid Out

Nearly $1.16 for Every $1 in Earned Premiums Relatively

Low CAT Losses, Reserve Releases

Heavy Use of Reinsurance Lowered Net

Losses

Relatively Low CAT Losses, Reserve Releases

Higher CAT

Losses, Shrinking Reserve

Releases, Toll of Soft

Market

Cyclical Deterioration

Sandy Impacts

Lower CAT

Losses

Best Combined

Ratio Since 1949 (87.6)

Avg. CAT Losses,

More Reserve Releases

3 Consecutive Years of U/W Profits: First Time Since

1971-73

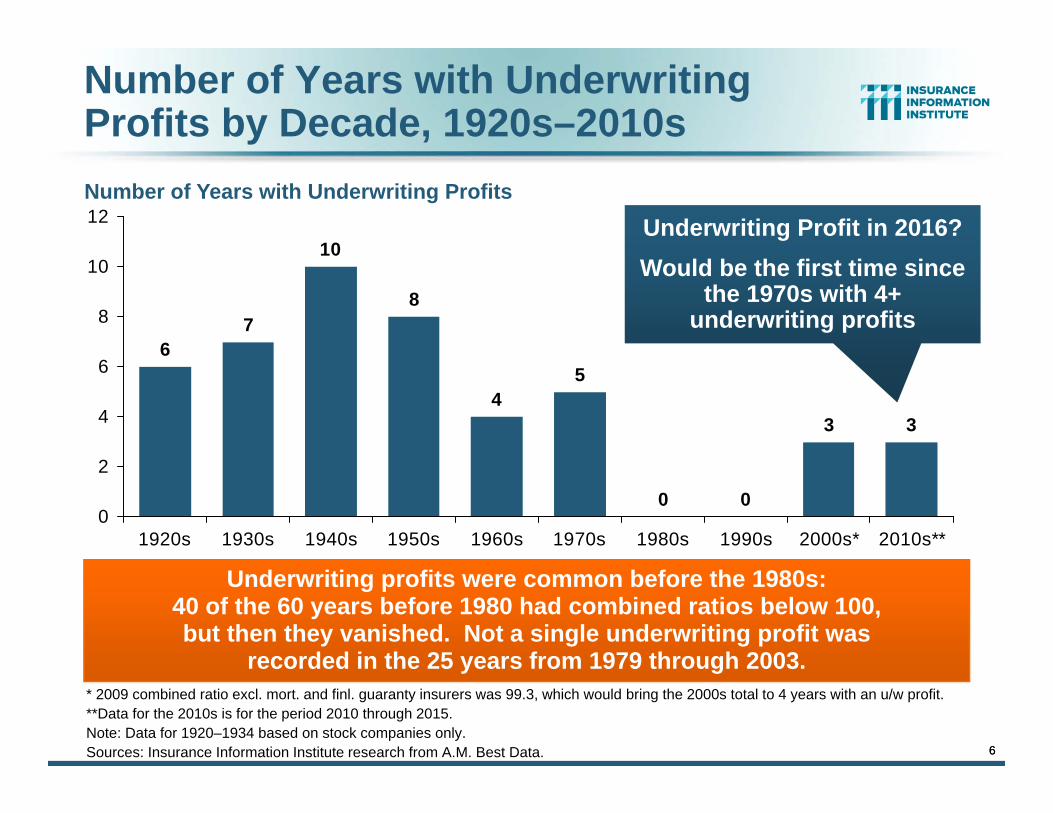

6

Number of Years with Underwriting Profits by Decade, 1920s–2010s

0 0

3 3

54

8

10

76

0

2

4

6

8

10

12

1920s 1930s 1940s 1950s 1960s 1970s 1980s 1990s 2000s* 2010s**

* 2009 combined ratio excl. mort. and finl. guaranty insurers was 99.3, which would bring the 2000s total to 4 years with an u/w profit.**Data for the 2010s is for the period 2010 through 2015.Note: Data for 1920–1934 based on stock companies only.Sources: Insurance Information Institute research from A.M. Best Data.

Number of Years with Underwriting Profits

Underwriting profits were common before the 1980s:40 of the 60 years before 1980 had combined ratios below 100, but then they vanished. Not a single underwriting profit was

recorded in the 25 years from 1979 through 2003.

6

Underwriting Profit in 2016?Would be the first time since

the 1970s with 4+ underwriting profits

Source: A.M. Best; Barclays research for estimates.

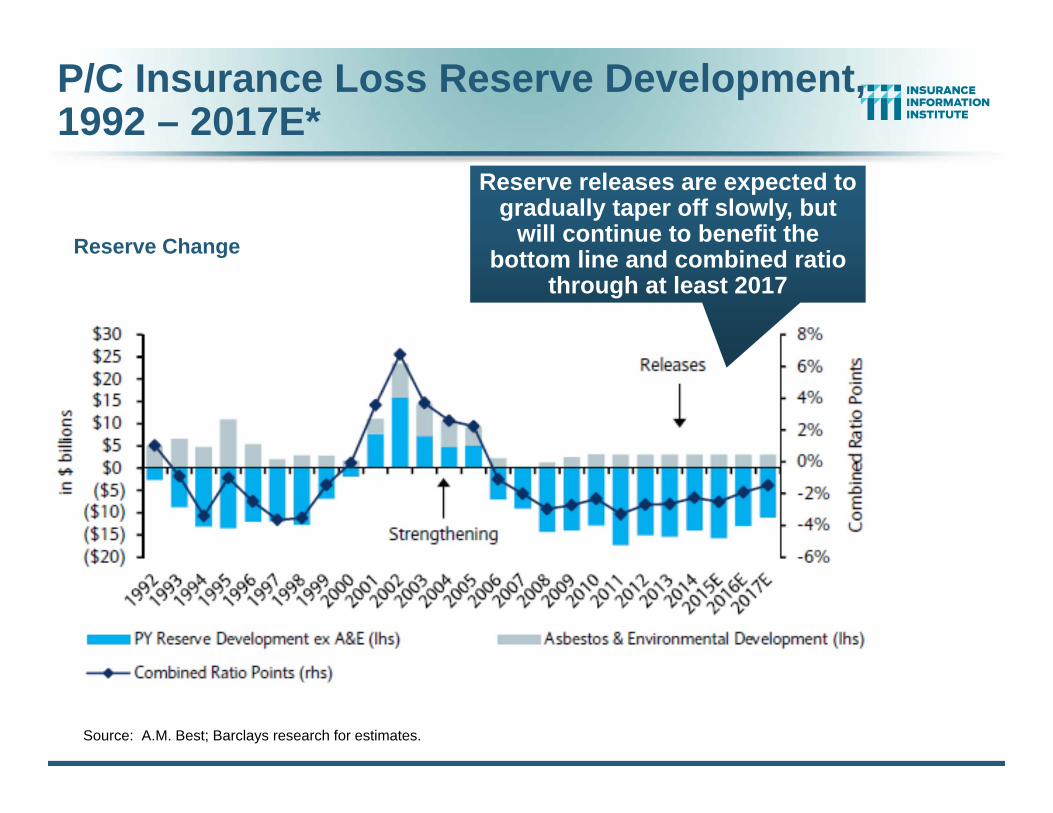

Reserve Change

P/C Insurance Loss Reserve Development, 1992 – 2017E*

Reserve releases are expected to gradually taper off slowly, but

will continue to benefit the bottom line and combined ratio

through at least 2017

8

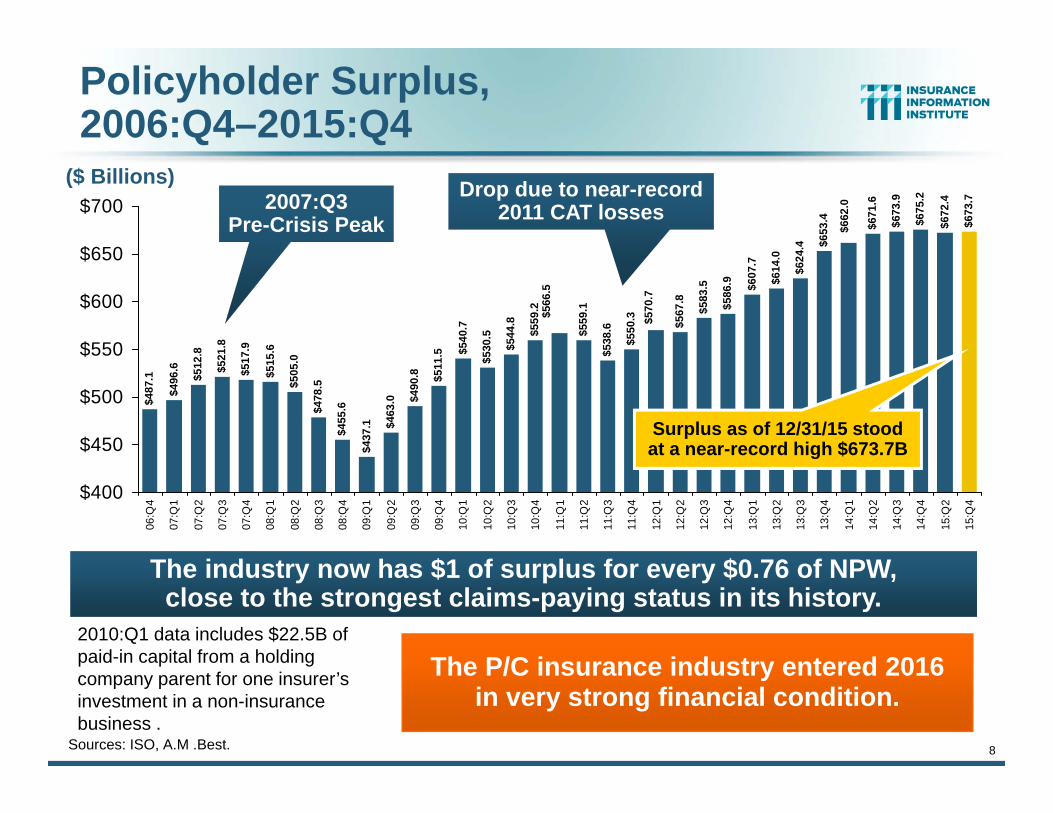

Policyholder Surplus, 2006:Q4–2015:Q4

Sources: ISO, A.M .Best.

($ Billions)$4

87.1

$496

.6

$512

.8

$521

.8

$478

.5

$455

.6

$437

.1 $463

.0 $490

.8 $511

.5 $540

.7

$530

.5

$544

.8

$559

.2

$559

.1

$538

.6

$550

.3 $567

.8

$583

.5

$586

.9 $607

.7

$614

.0

$624

.4 $653

.4 $671

.6

$673

.9

$675

.2

$672

.4

$673

.7

$662

.0

$570

.7

$566

.5

$505

.0

$515

.6

$517

.9

$400

$450

$500

$550

$600

$650

$700

06:Q

4

07:Q

1

07:Q

2

07:Q

3

07:Q

4

08:Q

1

08:Q

2

08:Q

3

08:Q

4

09:Q

1

09:Q

2

09:Q

3

09:Q

4

10:Q

1

10:Q

2

10:Q

3

10:Q

4

11:Q

1

11:Q

2

11:Q

3

11:Q

4

12:Q

1

12:Q

2

12:Q

3

12:Q

4

13:Q

1

13:Q

2

13:Q

3

13:Q

4

14:Q

1

14:Q

2

14:Q

3

14:Q

4

15:Q

2

15:Q

4

2007:Q3Pre-Crisis Peak

Surplus as of 12/31/15 stood at a near-record high $673.7B

2010:Q1 data includes $22.5B of paid-in capital from a holding company parent for one insurer’s investment in a non-insurance business .

The industry now has $1 of surplus for every $0.76 of NPW,close to the strongest claims-paying status in its history.

Drop due to near-record 2011 CAT losses

The P/C insurance industry entered 2016in very strong financial condition.

9

-5%

0%

5%

10%

15%

20%

25%

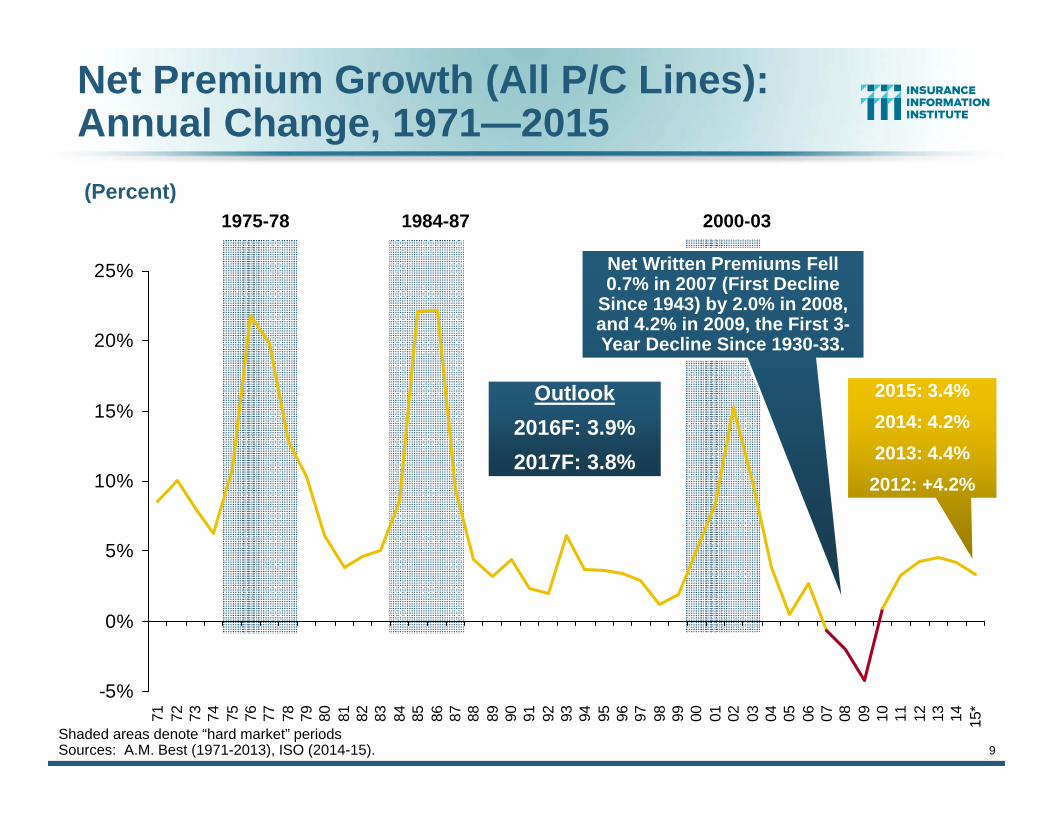

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15*

Net Premium Growth (All P/C Lines): Annual Change, 1971—2015(Percent)

1975-78 1984-87 2000-03

Shaded areas denote “hard market” periodsSources: A.M. Best (1971-2013), ISO (2014-15).

Net Written Premiums Fell 0.7% in 2007 (First Decline

Since 1943) by 2.0% in 2008, and 4.2% in 2009, the First 3-Year Decline Since 1930-33.

2015: 3.4%2014: 4.2%2013: 4.4%

2012: +4.2%

Outlook2016F: 3.9%2017F: 3.8%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

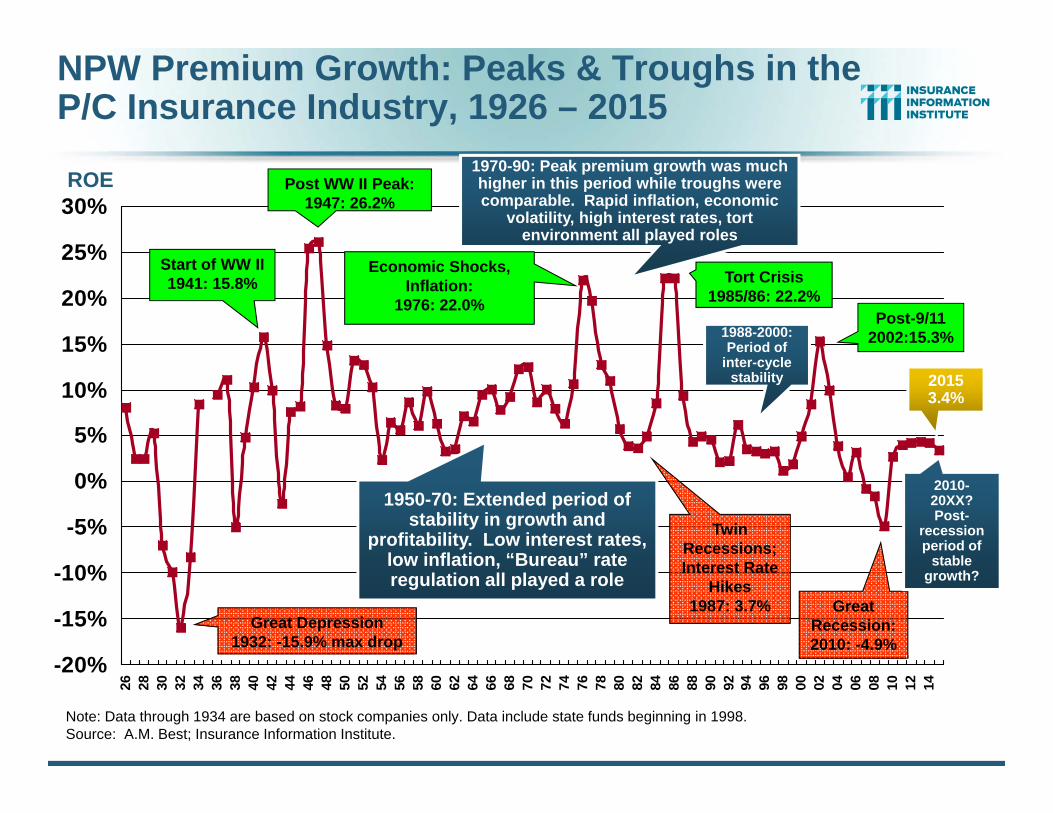

26 28 30 32 34 36 38 40 42 44 46 48 50 52 54 56 58 60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12 14

Note: Data through 1934 are based on stock companies only. Data include state funds beginning in 1998.Source: A.M. Best; Insurance Information Institute.

Economic Shocks, Inflation:

1976: 22.0%

Tort Crisis1985/86: 22.2%

Post-9/112002:15.3%

Twin Recessions; Interest Rate

Hikes1987: 3.7% Great

Recession:2010: -4.9%

ROE

2015 3.4%

NPW Premium Growth: Peaks & Troughs in the P/C Insurance Industry, 1926 – 2015

Great Depression1932: -15.9% max drop

Post WW II Peak:1947: 26.2%

Start of WW II1941: 15.8%

1950-70: Extended period of stability in growth and

profitability. Low interest rates, low inflation, “Bureau” rate regulation all played a role

1970-90: Peak premium growth was much higher in this period while troughs were comparable. Rapid inflation, economic

volatility, high interest rates, tort environment all played roles

1988-2000: Period of

inter-cycle stability

2010-20XX? Post-

recession period of

stable growth?

11

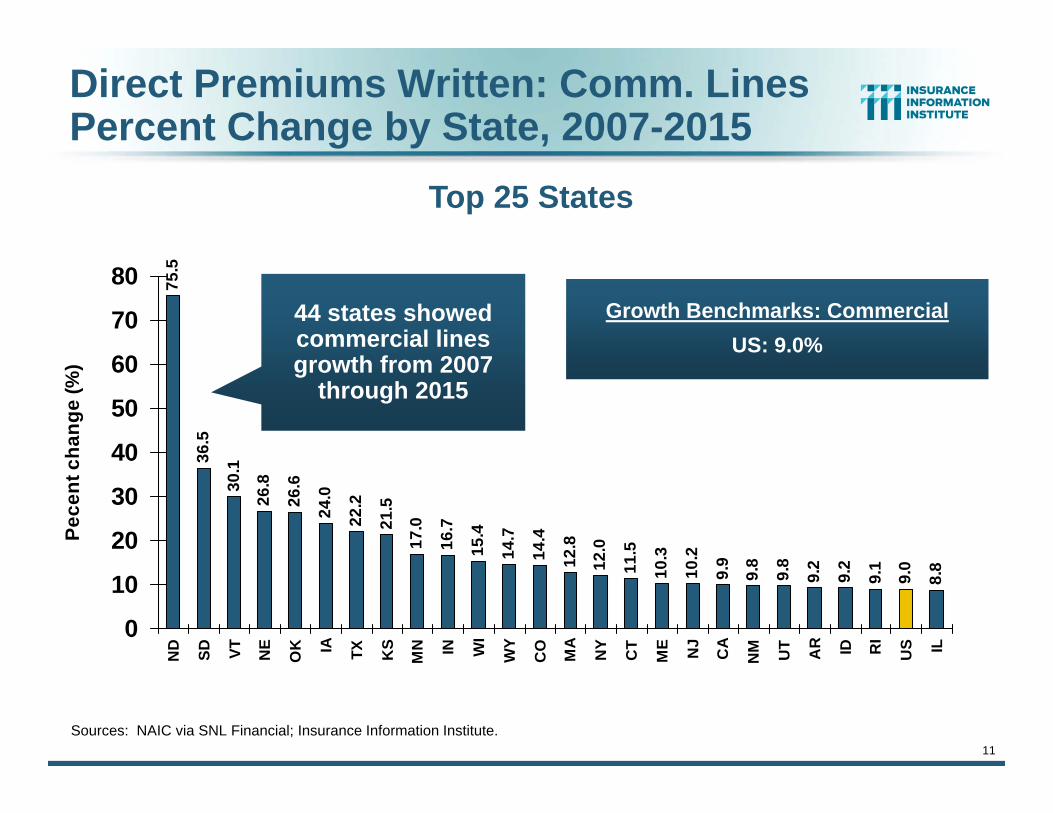

Direct Premiums Written: Comm. LinesPercent Change by State, 2007-2015

75.5

36.5

30.1

26.8

26.6

24.0

22.2

21.5

17.0

16.7

15.4

14.7

14.4

12.8

12.0

11.5

10.3

10.2

9.9

9.8

9.8

9.2

9.2

9.1

9.0

8.8

0

10

20

30

40

50

60

70

80

ND SD VT NE

OK IA TX KS

MN IN WI

WY

CO MA

NY

CT

ME NJ

CA

NM UT AR ID RI

US IL

Pece

nt c

hang

e (%

)

Sources: NAIC via SNL Financial; Insurance Information Institute.

Top 25 States

44 states showed commercial lines growth from 2007

through 2015

Growth Benchmarks: CommercialUS: 9.0%

12

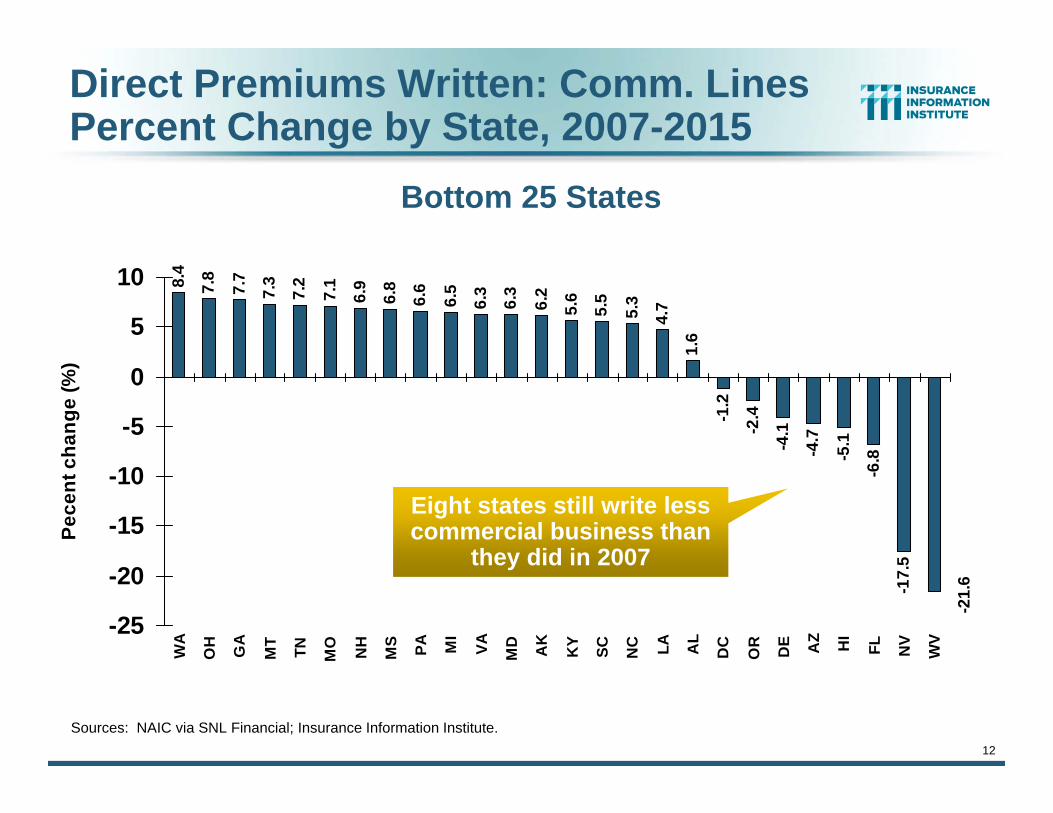

Direct Premiums Written: Comm. LinesPercent Change by State, 2007-2015

8.4

7.8

7.7

7.3

7.2

7.1

6.9

6.8

6.6

6.5

6.3

6.3

6.2

5.6

5.5

5.3

4.7

1.6

-1.2

-2.4

-4.1

-4.7

-5.1

-6.8

-17.

5

-21.

6

-25

-20

-15

-10

-5

0

5

10

WA

OH GA

MT

TN MO NH

MS PA MI

VA MD AK

KY

SC NC LA AL

DC

OR DE AZ HI

FL NV

WV

Pece

nt c

hang

e (%

)

Bottom 25 States

Sources: NAIC via SNL Financial; Insurance Information Institute.

Eight states still write less commercial business than

they did in 2007

13

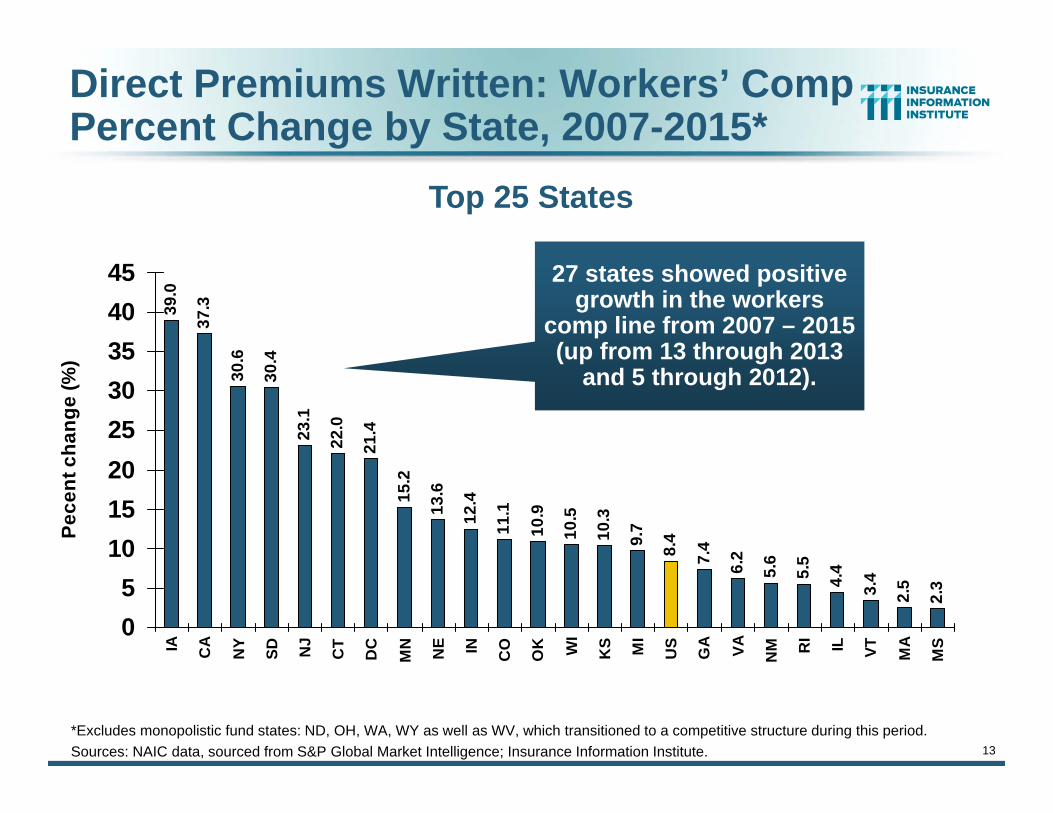

Direct Premiums Written: Workers’ CompPercent Change by State, 2007-2015*

39.0

37.3

30.6

30.4

23.1

22.0

21.4

15.2

13.6

12.4

11.1

10.9

10.5

10.3

9.7

8.4

7.4

6.2

5.6

5.5

4.4

3.4

2.5

2.3

05

1015202530354045

IA CA

NY

SD NJ

CT

DC

MN NE IN CO

OK WI

KS MI

US

GA VA NM R

I IL VT MA

MS

Pece

nt c

hang

e (%

)

*Excludes monopolistic fund states: ND, OH, WA, WY as well as WV, which transitioned to a competitive structure during this period.Sources: NAIC data, sourced from S&P Global Market Intelligence; Insurance Information Institute.

Top 25 States

27 states showed positive growth in the workers

comp line from 2007 – 2015 (up from 13 through 2013

and 5 through 2012).

14

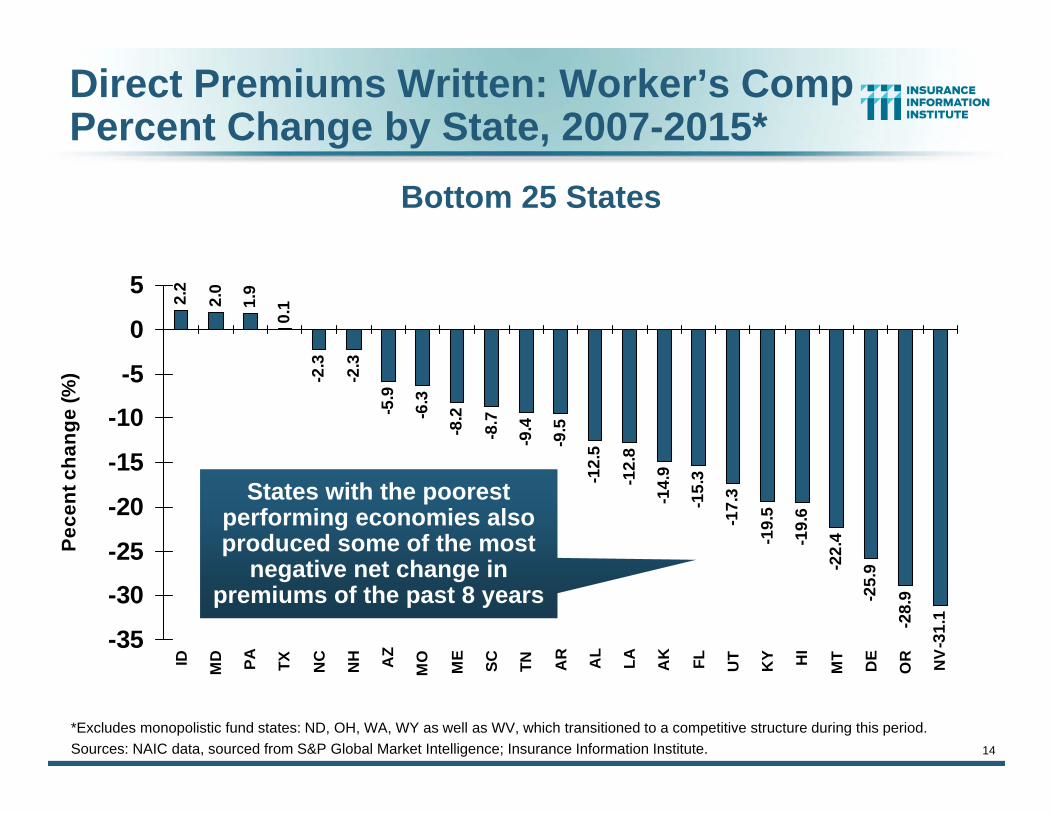

Direct Premiums Written: Worker’s CompPercent Change by State, 2007-2015*

2.2

2.0

1.9

0.1

-2.3

-2.3

-5.9

-6.3

-8.2

-8.7

-9.4

-9.5

-12.

5

-12.

8

-14.

9

-15.

3

-17.

3

-19.

5

-19.

6

-22.

4

-25.

9

-28.

9

-31.

1

-35

-30

-25

-20

-15

-10

-5

0

5

ID MD PA TX NC

NH AZ

MO

ME

SC TN AR AL

LA AK FL UT

KY HI

MT

DE

OR NV

Pece

nt c

hang

e (%

)

Bottom 25 States

*Excludes monopolistic fund states: ND, OH, WA, WY as well as WV, which transitioned to a competitive structure during this period.Sources: NAIC data, sourced from S&P Global Market Intelligence; Insurance Information Institute.

States with the poorest performing economies also produced some of the most

negative net change in premiums of the past 8 years

15

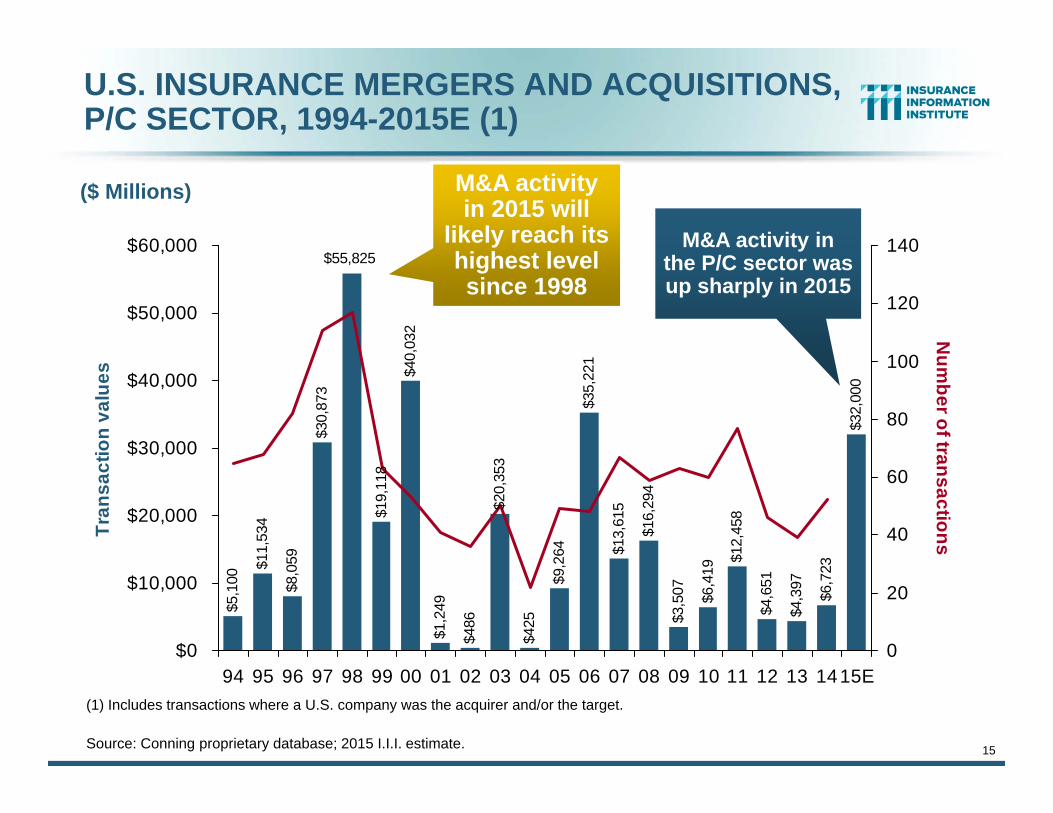

U.S. INSURANCE MERGERS AND ACQUISITIONS,P/C SECTOR, 1994-2015E (1)

$5,1

00

$11,

534

$8,0

59

$30,

873

$19,

118

$40,

032

$1,2

49

$486

$20,

353

$425

$9,2

64

$35,

221

$13,

615

$16,

294

$3,5

07 $6,4

19

$12,

458

$4,6

51

$4,3

97

$6,7

23

$32,

000

$55,825

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 1415E

Tran

sact

ion

valu

es

0

20

40

60

80

100

120

140

Num

ber of transactions

($ Millions)

(1) Includes transactions where a U.S. company was the acquirer and/or the target.

Source: Conning proprietary database; 2015 I.I.I. estimate.

M&A activity in the P/C sector was up sharply in 2015

M&A activity in 2015 will

likely reach its highest level since 1998

16

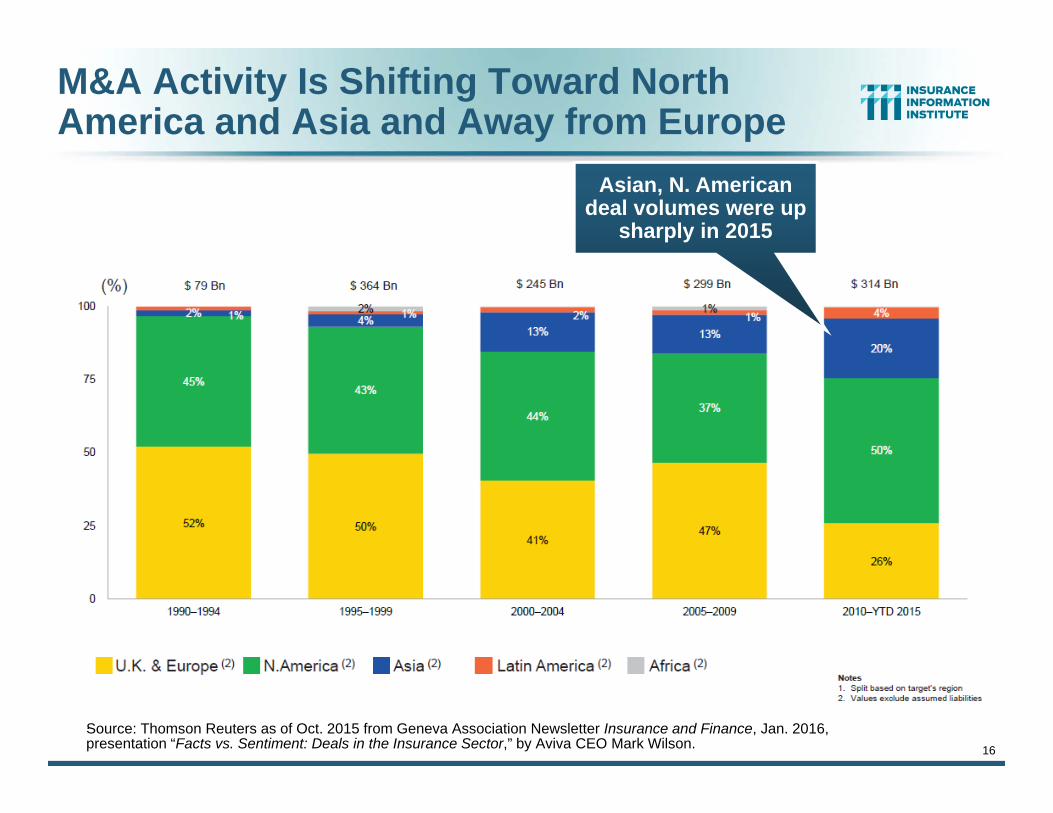

M&A Activity Is Shifting Toward North America and Asia and Away from Europe

.Source: Thomson Reuters as of Oct. 2015 from Geneva Association Newsletter Insurance and Finance, Jan. 2016, presentation “Facts vs. Sentiment: Deals in the Insurance Sector,” by Aviva CEO Mark Wilson.

Asian, N. American deal volumes were up

sharply in 2015

INVESTMENTS: THE NEW REALITY

17

Investment Performance is a Key Driver of Profitability

Depressed Yields Will Necessarily Influence Underwriting & Pricing

17

Property/Casualty Insurance Industry Investment Income: 2000–20151

$38.9$37.1 $36.7

$38.7

$54.6

$51.2

$47.1 $47.6$49.2

$48.0 $47.3 $46.4 $47.2

$39.6

$49.5$52.3

$30

$40

$50

$60

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15

Due to persistently low interest rates, investment income fell in 2012, 2013 and 2014 but showed a small (1.9%) increase in 2015—

a trend that may continue.

1 Investment gains consist primarily of interest and stock dividends. Sources: ISO; Insurance Information Institute.

($ Billions) Investment earnings are still below their 2007 pre-crisis peak

19

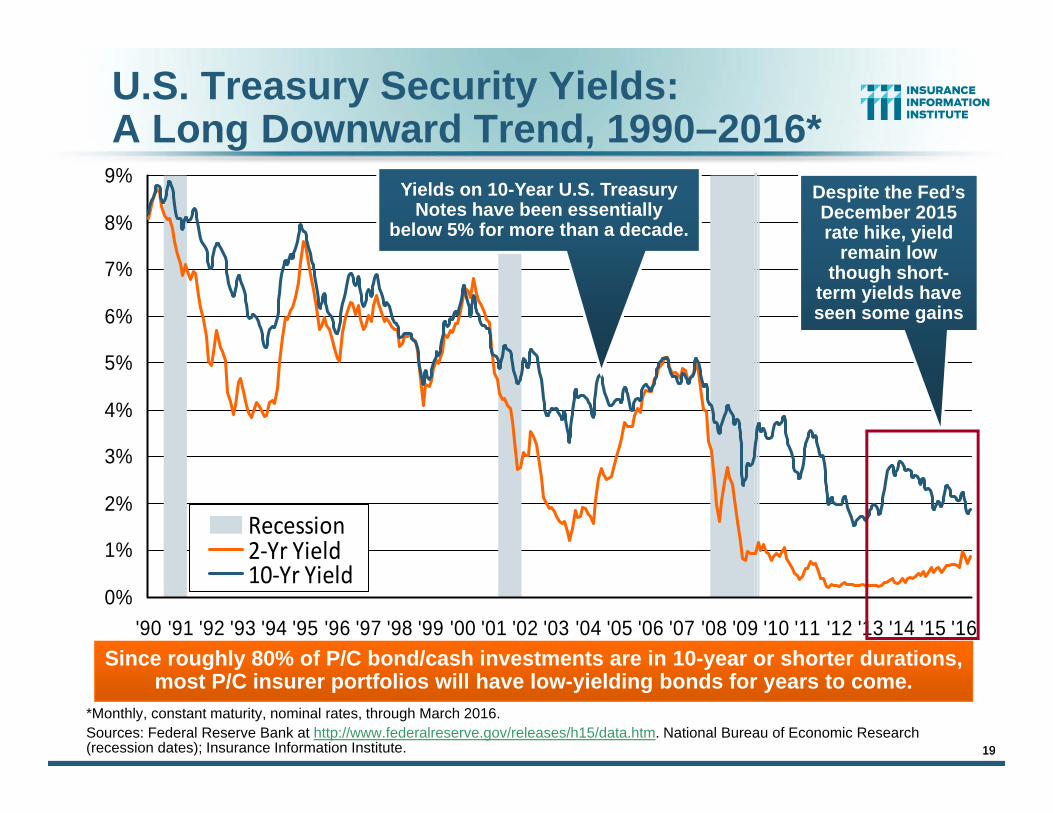

U.S. Treasury Security Yields:A Long Downward Trend, 1990–2016*

*Monthly, constant maturity, nominal rates, through March 2016.Sources: Federal Reserve Bank at http://www.federalreserve.gov/releases/h15/data.htm. National Bureau of Economic Research (recession dates); Insurance Information Institute.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

'90 '91 '92 '93 '94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Recession2‐Yr Yield10‐Yr Yield

Yields on 10-Year U.S. Treasury Notes have been essentially

below 5% for more than a decade.

Since roughly 80% of P/C bond/cash investments are in 10-year or shorter durations, most P/C insurer portfolios will have low-yielding bonds for years to come.

Despite the Fed’s December 2015 rate hike, yield

remain low though short-

term yields have seen some gains

19

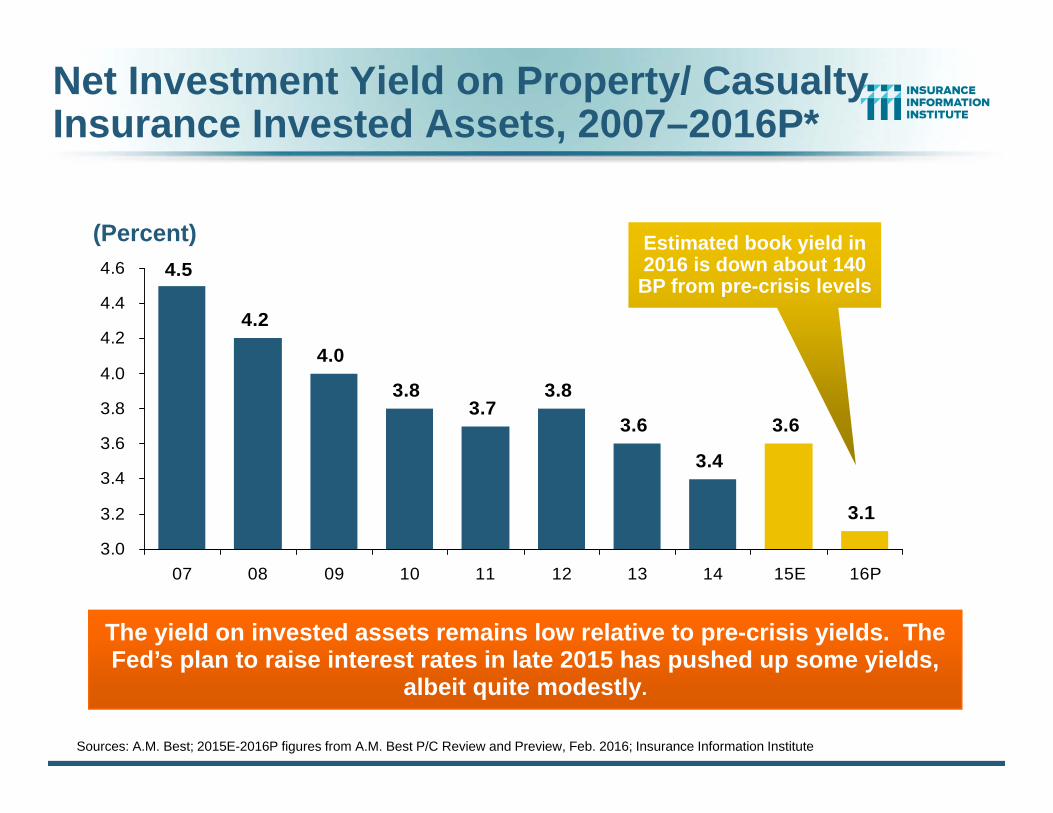

Net Investment Yield on Property/ Casualty Insurance Invested Assets, 2007–2016P*

4.5

4.2

4.0

3.8

3.4

3.6

3.1

3.73.8

3.6

3.0

3.2

3.4

3.6

3.8

4.0

4.2

4.4

4.6

07 08 09 10 11 12 13 14 15E 16P

The yield on invested assets remains low relative to pre-crisis yields. The Fed’s plan to raise interest rates in late 2015 has pushed up some yields,

albeit quite modestly.

Sources: A.M. Best; 2015E-2016P figures from A.M. Best P/C Review and Preview, Feb. 2016; Insurance Information Institute

(Percent) Estimated book yield in 2016 is down about 140 BP from pre-crisis levels

21

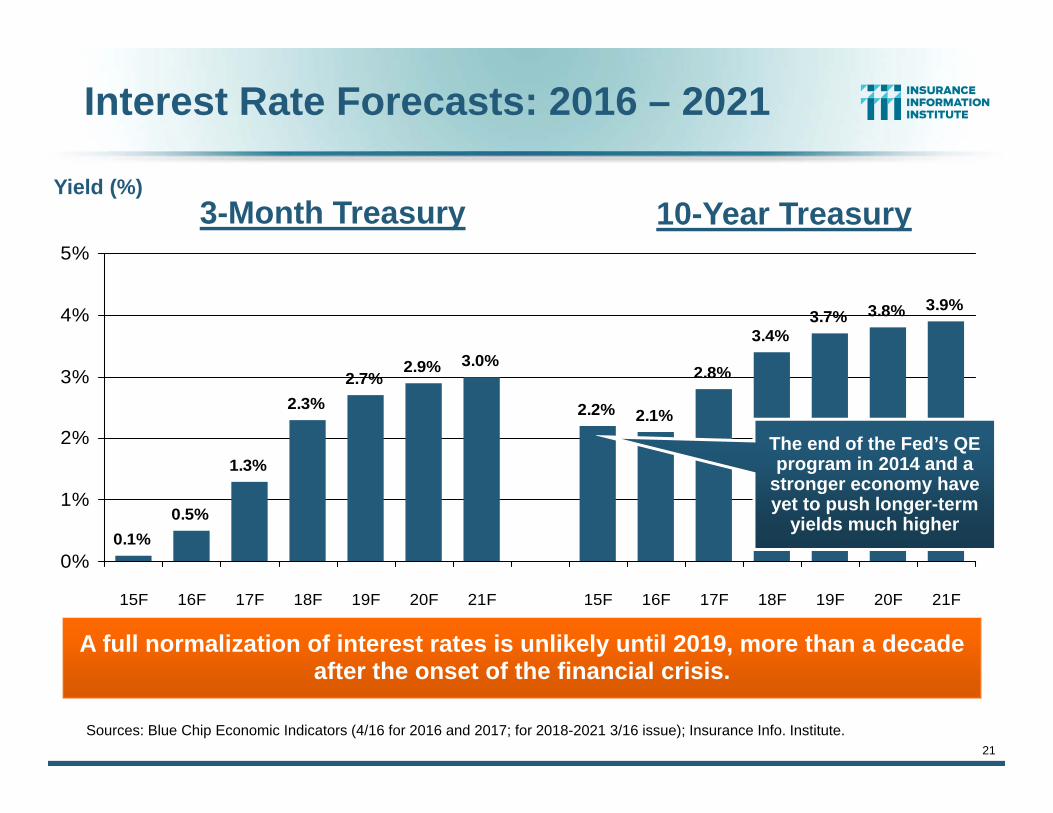

Interest Rate Forecasts: 2016 – 2021

3.0%

2.2% 2.1%

2.8%

3.4%3.7% 3.8% 3.9%

0.1%0.5%

1.3%

2.3%2.7%

2.9%

0%

1%

2%

3%

4%

5%

15F 16F 17F 18F 19F 20F 21F 15F 16F 17F 18F 19F 20F 21F

A full normalization of interest rates is unlikely until 2019, more than a decade after the onset of the financial crisis.

Yield (%)

Sources: Blue Chip Economic Indicators (4/16 for 2016 and 2017; for 2018-2021 3/16 issue); Insurance Info. Institute.

3-Month Treasury 10-Year Treasury

The end of the Fed’s QE program in 2014 and a

stronger economy have yet to push longer-term

yields much higher

Profitability & Politics

2222

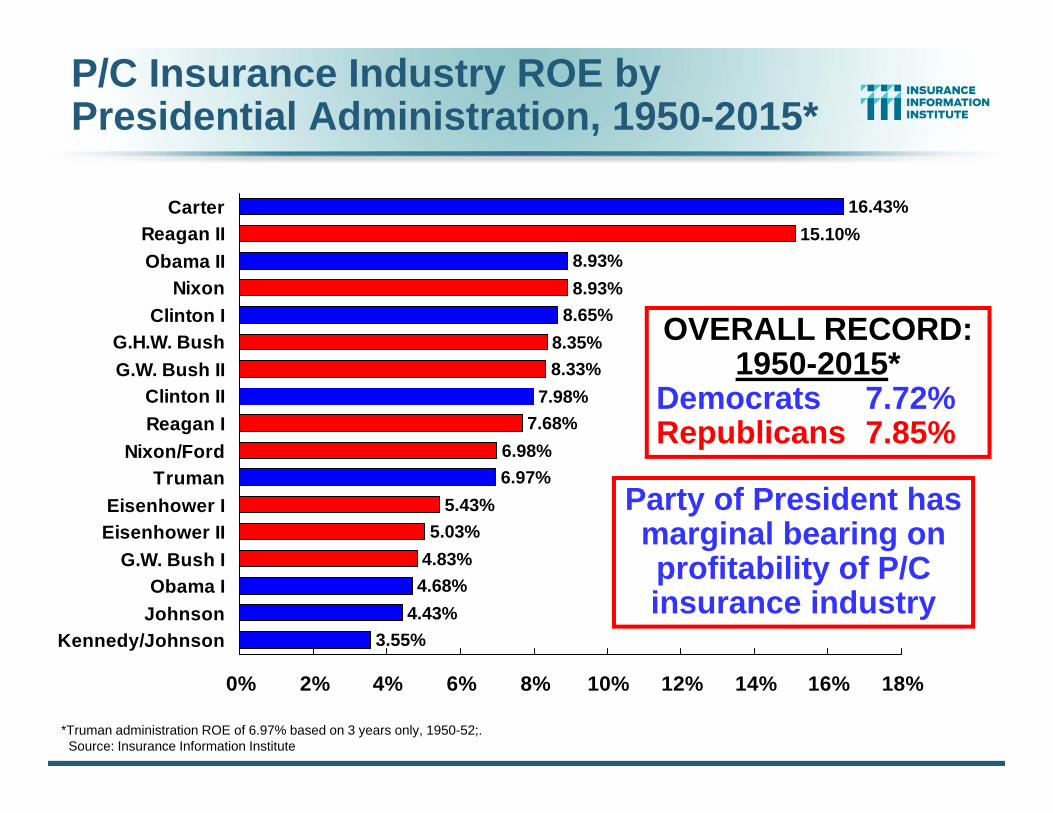

How Is Profitability Affected by the President’s Political Party?

15.10%8.93%8.93%

8.65%8.35%8.33%

7.98%7.68%

6.98%6.97%

5.43%5.03%

4.83%4.68%

4.43%3.55%

16.43%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

CarterReagan IIObama II

NixonClinton I

G.H.W. BushG.W. Bush II

Clinton IIReagan I

Nixon/FordTruman

Eisenhower IEisenhower II

G.W. Bush IObama I

JohnsonKennedy/Johnson

*Truman administration ROE of 6.97% based on 3 years only, 1950-52;.Source: Insurance Information Institute

OVERALL RECORD: 1950-2015*

Democrats 7.72%Republicans 7.85%

Party of President has marginal bearing on profitability of P/C insurance industry

P/C Insurance Industry ROE by Presidential Administration, 1950-2015*

24

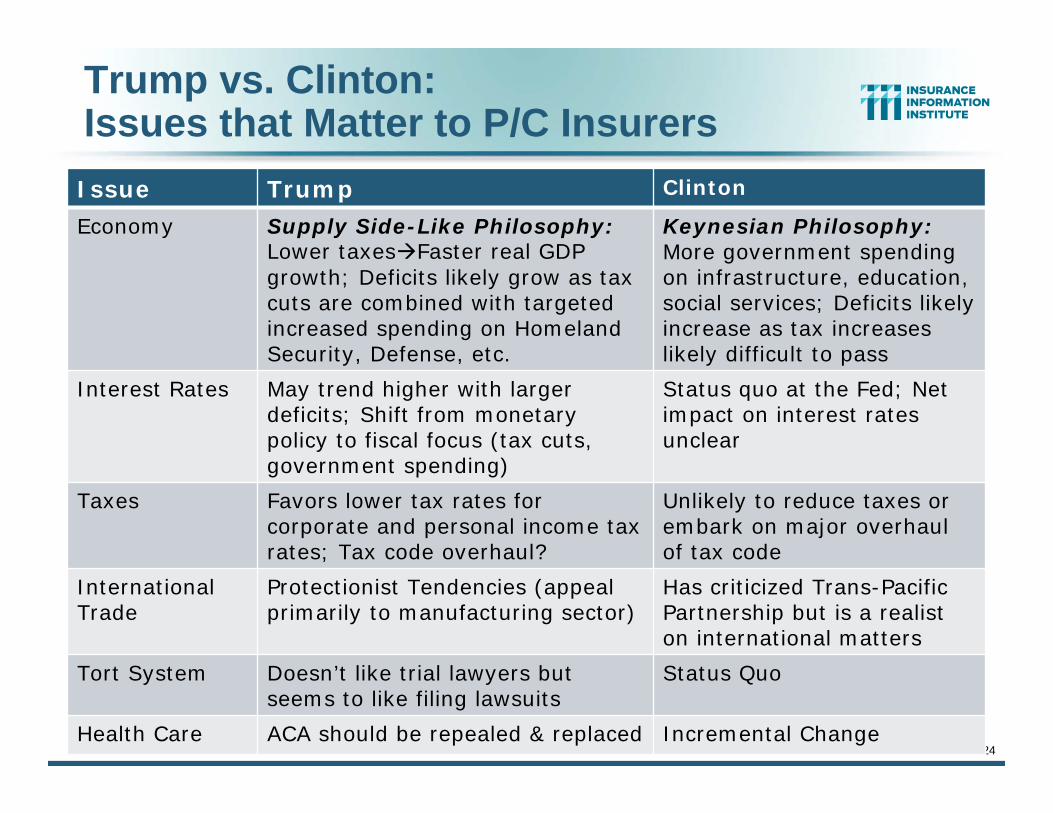

Trump vs. Clinton:Issues that Matter to P/C Insurers

Issue Trump Clinton

Economy Supply Side-Like Philosophy:Lower taxesFaster real GDP growth; Deficits likely grow as tax cuts are combined with targeted increased spending on Homeland Security, Defense, etc.

Keynesian Philosophy: More government spending on infrastructure, education, social services; Deficits likely increase as tax increases likely difficult to pass

Interest Rates May trend higher with larger deficits; Shift from monetary policy to fiscal focus (tax cuts, government spending)

Status quo at the Fed; Net impact on interest rates unclear

Taxes Favors lower tax rates for corporate and personal income tax rates; Tax code overhaul?

Unlikely to reduce taxes or embark on major overhaul of tax code

International Trade

Protectionist Tendencies (appeal primarily to manufacturing sector)

Has criticized Trans-PacificPartnership but is a realist on international matters

Tort System Doesn’t like trial lawyers butseems to like filing lawsuits

Status Quo

Health Care ACA should be repealed & replaced Incremental Change

Source: James Madison Institute, February 2008.

ME

NH

MA

CT

PA

WVVA

NC

LATX

OK

NE

ND

MN

MI

IL

IA

ID

WA

OR

AZ

HI

NJRI C+

DE

AL

VT

NY

MD

SC

GA

TN

AL

FL

MS

ARNM

KYMOKS

SD WI

INOH

MT

CA

NV

UT

WY

CO

AK

= A= B= C= D= F= NG

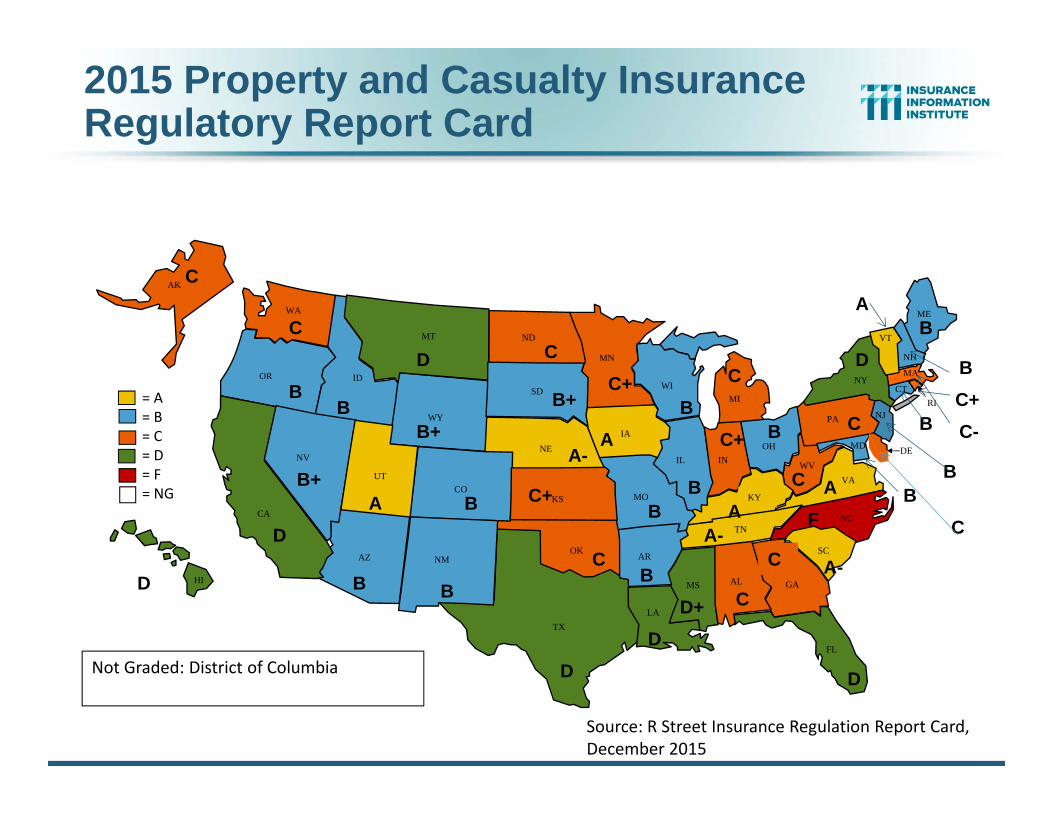

Source: R Street Insurance Regulation Report Card, December 2015

B+ A

B

A-

B+

B

A

A-

CC

BB

D

F

C

C+

A C-

B

D

C

C

BC

A

B

B

A

B

B

C+

B

B

B+

C

B

B

A-

C+

C

C

CDB

D+D

D D

D

2015 Property and Casualty InsuranceRegulatory Report Card

Not Graded: District of Columbia

26

Labor Markets Trends:Recovery Continues in 2016

2015Largest Job Gains in Many Years

Unemployment Rate Fell to Lowest Level Since 2008

Payrolls Expanded to Record High26

27

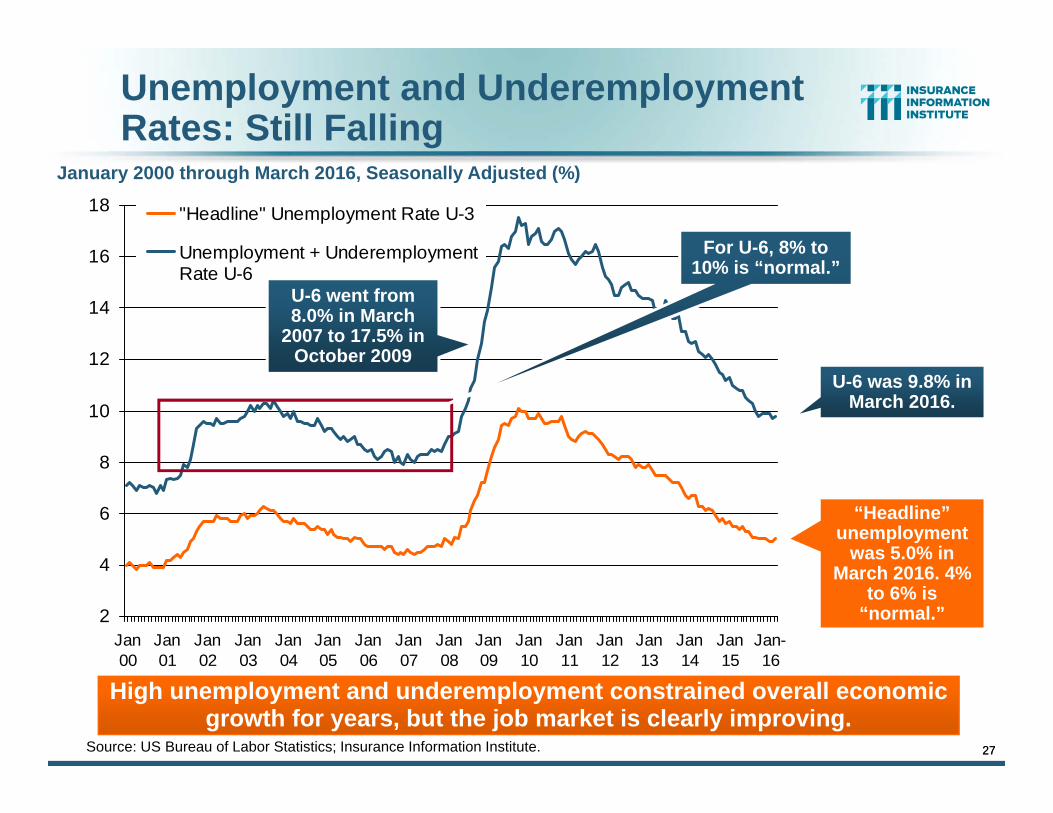

Unemployment and Underemployment Rates: Still Falling

2

4

6

8

10

12

14

16

18

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Jan11

Jan12

Jan13

Jan14

Jan15

Jan-16

"Headline" Unemployment Rate U-3

Unemployment + UnderemploymentRate U-6

“Headline” unemployment

was 5.0% in March 2016. 4%

to 6% is “normal.”

Source: US Bureau of Labor Statistics; Insurance Information Institute.

U-6 was 9.8% in March 2016.

January 2000 through March 2016, Seasonally Adjusted (%)

High unemployment and underemployment constrained overall economic growth for years, but the job market is clearly improving.

27

U-6 went from 8.0% in March

2007 to 17.5% in October 2009

For U-6, 8% to 10% is “normal.”

28

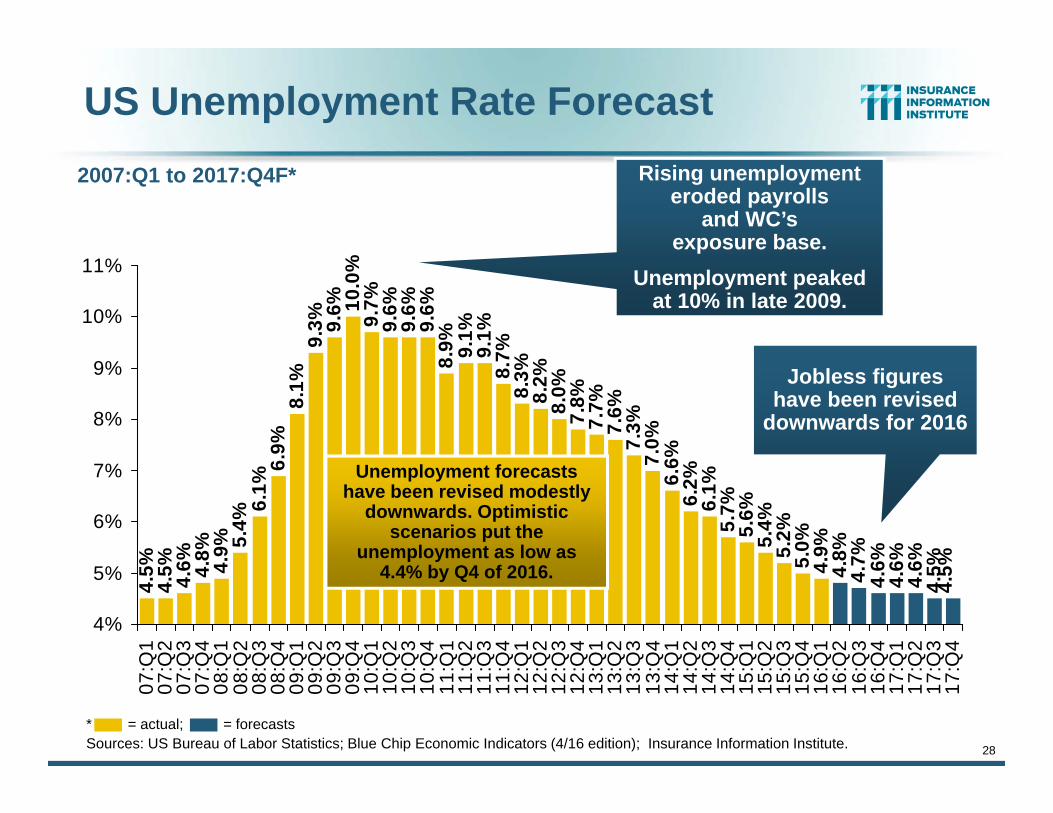

US Unemployment Rate Forecast4.

5%4.

5% 4.6% 4.8% 4.9% 5.

4%6.

1%6.

9%8.

1%9.

3% 9.6% 10

.0%

9.7%

9.6%

9.6%

8.9% 9.1%

9.1%

8.7%

8.3%

8.2%

8.0%

7.8%

7.7%

7.6%

7.3%

7.0%

6.6%

6.2%

6.1%

5.7%

5.6%

5.4%

5.2%

5.0%

4.9%

4.8%

4.7%

4.6%

4.6%

4.6%

4.5%

4.5%

9.6%

4%

5%

6%

7%

8%

9%

10%

11%

07:Q

107

:Q2

07:Q

307

:Q4

08:Q

108

:Q2

08:Q

308

:Q4

09:Q

109

:Q2

09:Q

309

:Q4

10:Q

110

:Q2

10:Q

310

:Q4

11:Q

111

:Q2

11:Q

311

:Q4

12:Q

112

:Q2

12:Q

312

:Q4

13:Q

113

:Q2

13:Q

313

:Q4

14:Q

114

:Q2

14:Q

314

:Q4

15:Q

115

:Q2

15:Q

315

:Q4

16:Q

116

:Q2

16:Q

316

:Q4

17:Q

117

:Q2

17:Q

317

:Q4

Rising unemployment eroded payrolls

and WC’s exposure base.

Unemployment peaked at 10% in late 2009.

* = actual; = forecastsSources: US Bureau of Labor Statistics; Blue Chip Economic Indicators (4/16 edition); Insurance Information Institute.

2007:Q1 to 2017:Q4F*

Unemployment forecasts have been revised modestly

downwards. Optimistic scenarios put the

unemployment as low as 4.4% by Q4 of 2016.

Jobless figures have been revised

downwards for 2016

29

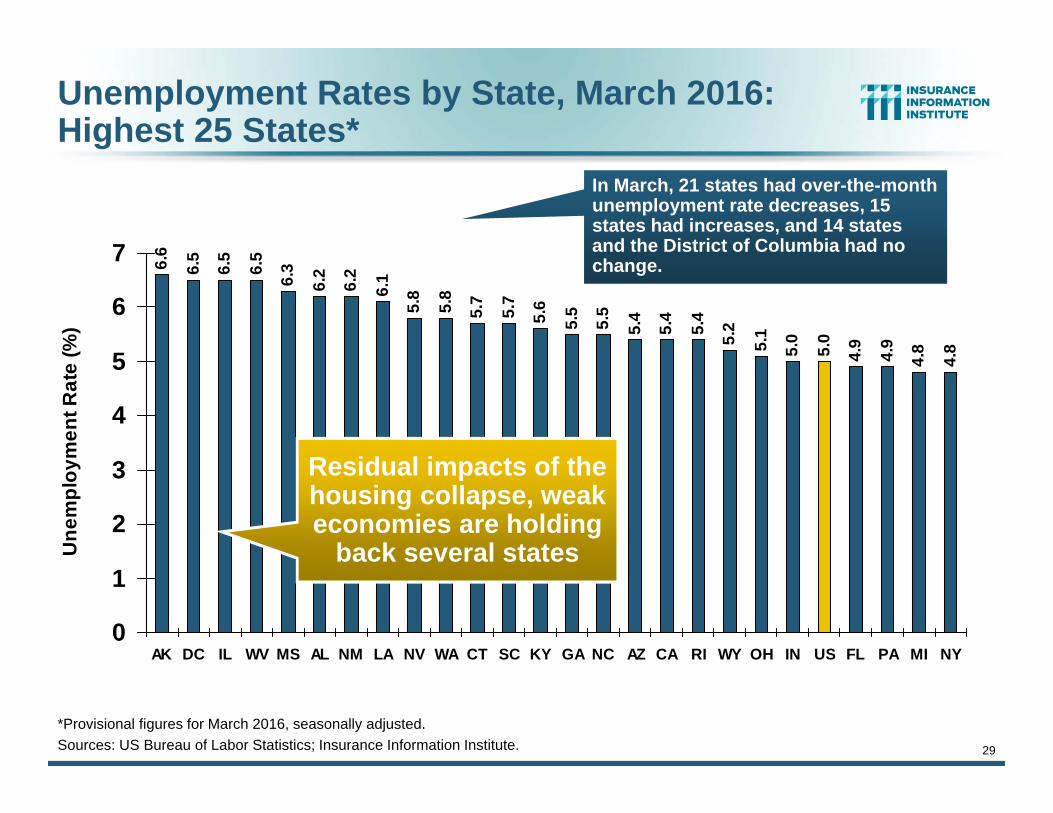

Unemployment Rates by State, March 2016:Highest 25 States*

6.6

6.5

6.5

6.5

6.3

6.2

6.2

6.1

5.8

5.8

5.7

5.7

5.6

5.5

5.5

5.4

5.4

5.4

5.2

5.1

5.0

5.0

4.9

4.9

4.8

4.8

0

1

2

3

4

5

6

7

AK DC IL WV MS AL NM LA NV WA CT SC KY GA NC AZ CA RI WY OH IN US FL PA MI NY

Une

mpl

oym

ent R

ate

(%)

*Provisional figures for March 2016, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

In March, 21 states had over-the-month unemployment rate decreases, 15 states had increases, and 14 states and the District of Columbia had no change.

Residual impacts of the housing collapse, weak economies are holding

back several states

30

4.7

4.5

4.5

4.5

4.4

4.4

4.4

4.4

4.3

4.3

4.2

4.0

4.0

3.9

3.8

3.8

3.7

3.5

3.4

3.3

3.1

3.1

3.0

2.9

2.6

2.5

0

1

2

3

4

5

MD OR TN WI DE MA NJ OK MT TX MO AR VA KS IA ID MN UT ME VT HI ND NE CO NH SD

Une

mpl

oym

ent R

ate

(%)

Unemployment Rates by State, March 2016: Lowest 25 States*

*Provisional figures for March 2016, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

In March, 21 states had over-the-month unemployment rate decreases, 15 states had increases, and 14 states and the District of Columbia had no change.

Strength in Energy, Agricultural States-most also avoided

housing bust

31

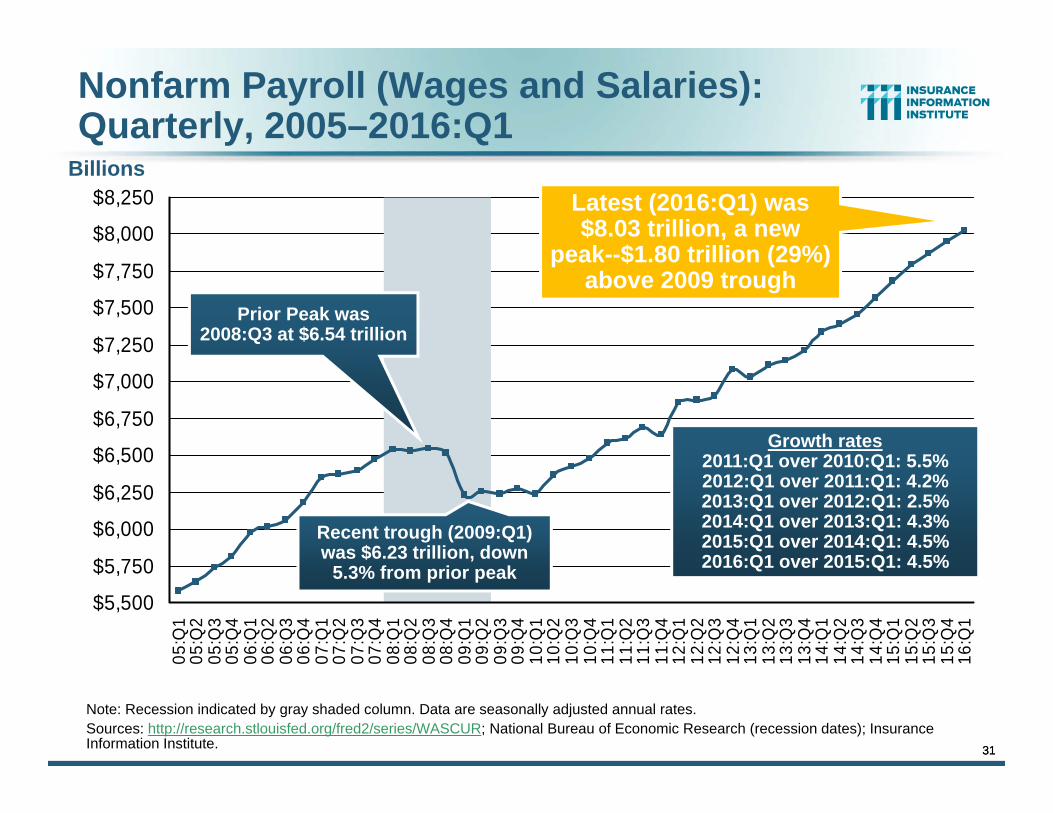

Nonfarm Payroll (Wages and Salaries):Quarterly, 2005–2016:Q1

Note: Recession indicated by gray shaded column. Data are seasonally adjusted annual rates.Sources: http://research.stlouisfed.org/fred2/series/WASCUR; National Bureau of Economic Research (recession dates); Insurance Information Institute.

Billions

$5,500

$5,750

$6,000

$6,250

$6,500

$6,750

$7,000

$7,250

$7,500

$7,750

$8,000

$8,25005

:Q1

05:Q

205

:Q3

05:Q

406

:Q1

06:Q

206

:Q3

06:Q

407

:Q1

07:Q

207

:Q3

07:Q

408

:Q1

08:Q

208

:Q3

08:Q

409

:Q1

09:Q

209

:Q3

09:Q

410

:Q1

10:Q

210

:Q3

10:Q

411

:Q1

11:Q

211

:Q3

11:Q

412

:Q1

12:Q

212

:Q3

12:Q

413

:Q1

13:Q

213

:Q3

13:Q

414

:Q1

14:Q

214

:Q3

14:Q

415

:Q1

15:Q

215

:Q3

15:Q

416

:Q1

Prior Peak was 2008:Q3 at $6.54 trillion

Recent trough (2009:Q1) was $6.23 trillion, down

5.3% from prior peak

Growth rates2011:Q1 over 2010:Q1: 5.5%2012:Q1 over 2011:Q1: 4.2%2013:Q1 over 2012:Q1: 2.5%2014:Q1 over 2013:Q1: 4.3% 2015:Q1 over 2014:Q1: 4.5%2016:Q1 over 2015:Q1: 4.5%

31

Latest (2016:Q1) was $8.03 trillion, a new

peak--$1.80 trillion (29%) above 2009 trough

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15$25

$30

$35

$40

$45

$50Wage & Salary DisbursementsWC NPW

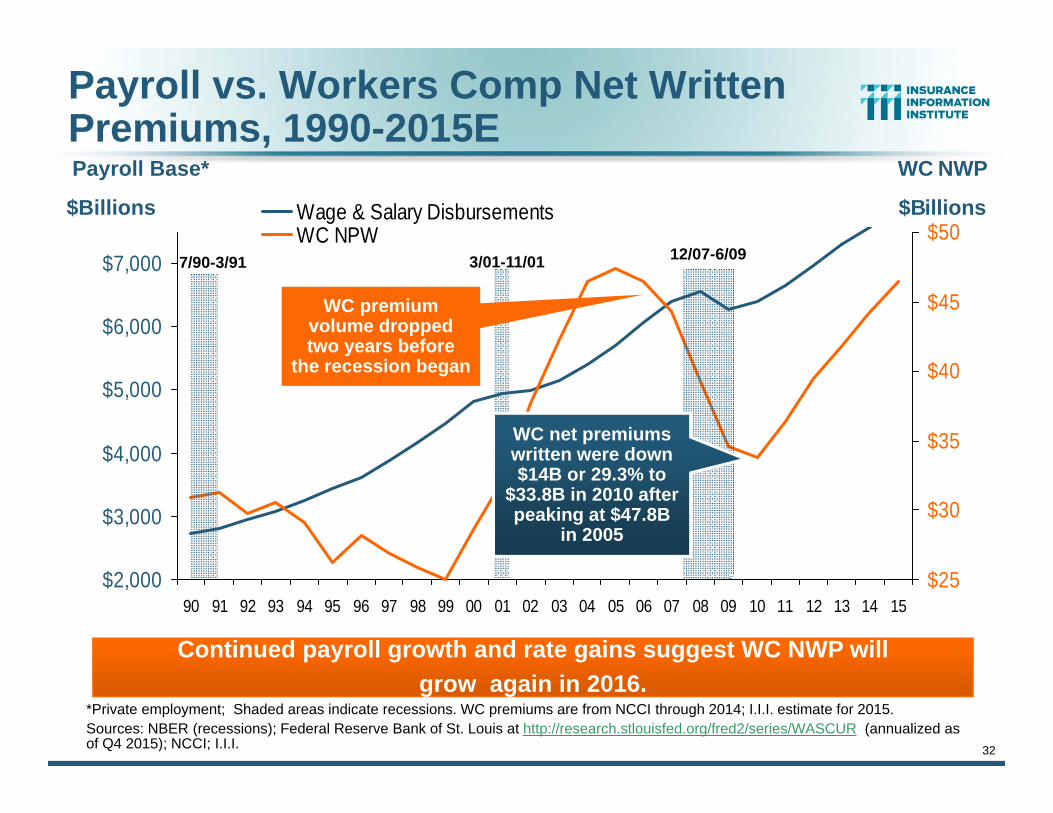

32

Payroll Base* WC NWP

Payroll vs. Workers Comp Net Written Premiums, 1990-2015E

*Private employment; Shaded areas indicate recessions. WC premiums are from NCCI through 2014; I.I.I. estimate for 2015.Sources: NBER (recessions); Federal Reserve Bank of St. Louis at http://research.stlouisfed.org/fred2/series/WASCUR (annualized as of Q4 2015); NCCI; I.I.I.

Continued payroll growth and rate gains suggest WC NWP will grow again in 2016.

7/90-3/91 3/01-11/01 12/07-6/09

$Billions $Billions

WC premium volume dropped two years before

the recession began

WC net premiums written were down $14B or 29.3% to

$33.8B in 2010 after peaking at $47.8B

in 2005

33

POSITIVE LABOR MARKET DEVELOPMENTS

Key Factors Driving Workers Compensation Exposure

33

34

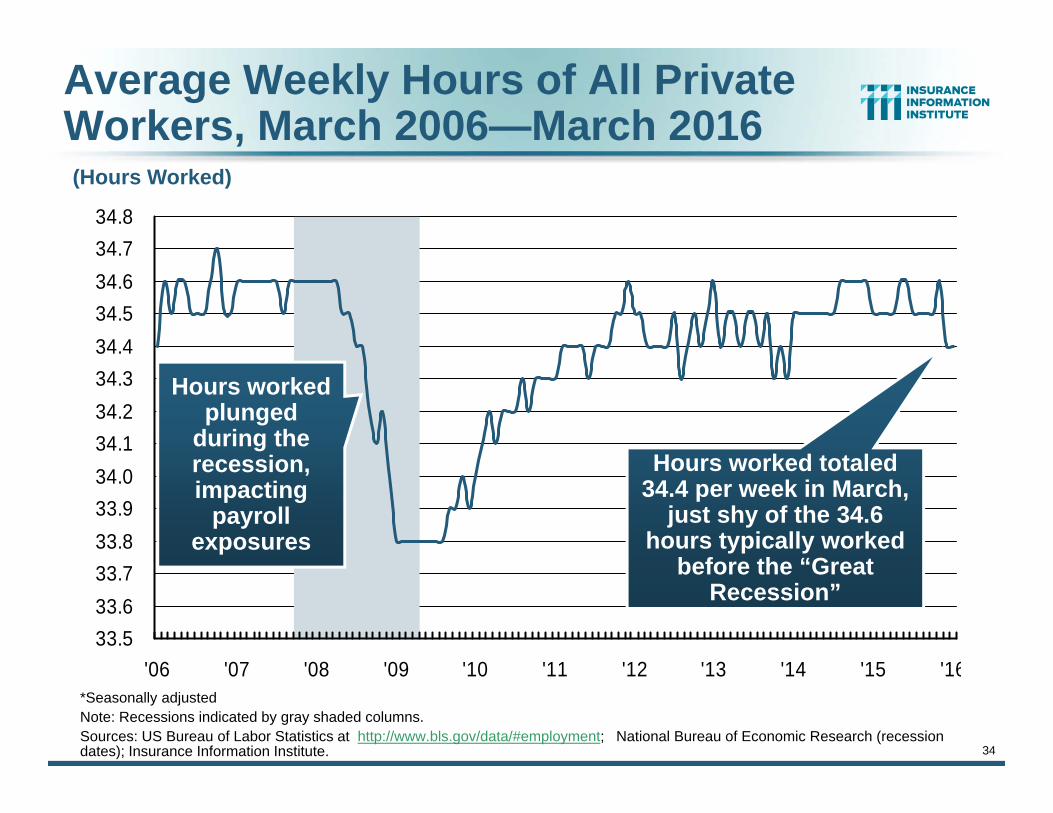

Average Weekly Hours of All Private Workers, March 2006—March 2016

*Seasonally adjustedNote: Recessions indicated by gray shaded columns.Sources: US Bureau of Labor Statistics at http://www.bls.gov/data/#employment; National Bureau of Economic Research (recession dates); Insurance Information Institute.

33.533.633.733.833.934.034.134.234.334.434.534.634.734.8

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Hours worked totaled 34.4 per week in March,

just shy of the 34.6 hours typically worked

before the “Great Recession”

Hours worked plunged

during the recession, impacting

payroll exposures

(Hours Worked)

35

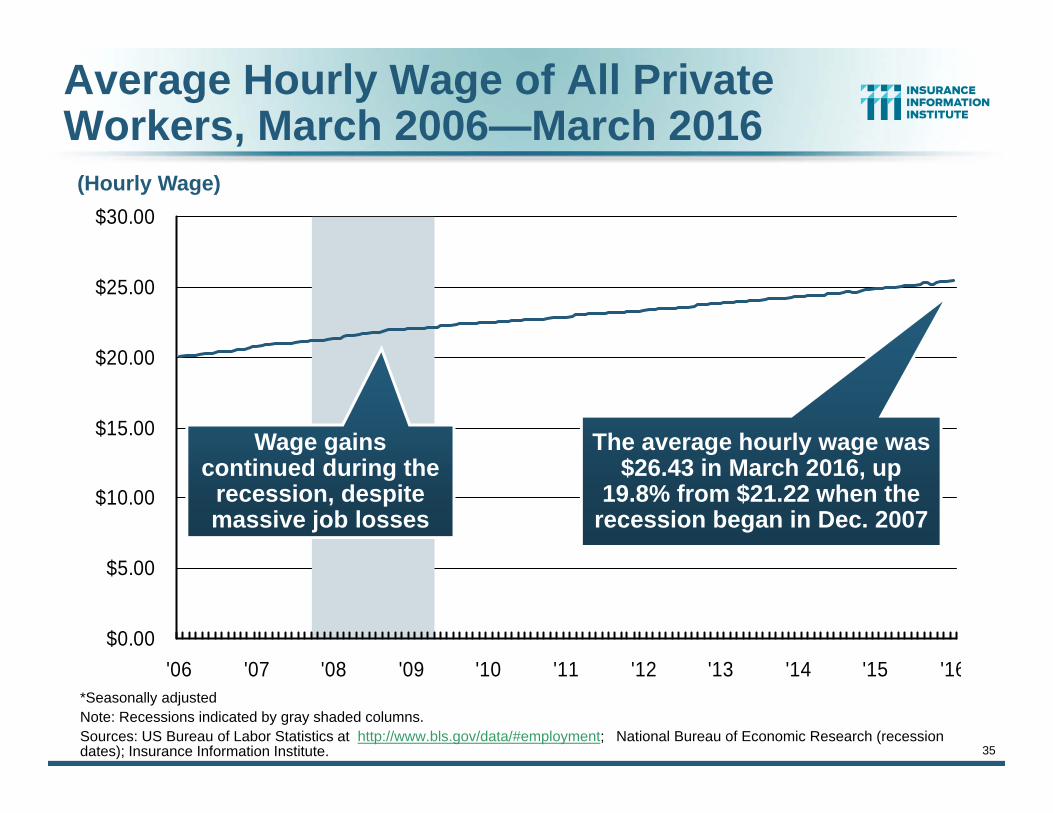

Average Hourly Wage of All Private Workers, March 2006—March 2016

*Seasonally adjustedNote: Recessions indicated by gray shaded columns.Sources: US Bureau of Labor Statistics at http://www.bls.gov/data/#employment; National Bureau of Economic Research (recession dates); Insurance Information Institute.

$0.00

$5.00

$10.00

$15.00

$20.00

$25.00

$30.00

'06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

The average hourly wage was $26.43 in March 2016, up

19.8% from $21.22 when the recession began in Dec. 2007

Wage gains continued during the

recession, despite massive job losses

(Hourly Wage)

36

ADVERSE LONG-TERMLABOR MARKET DEVELOPMENTS

Key Factors Harming Workers Compensation Exposure and the

Overall Economy

36

37

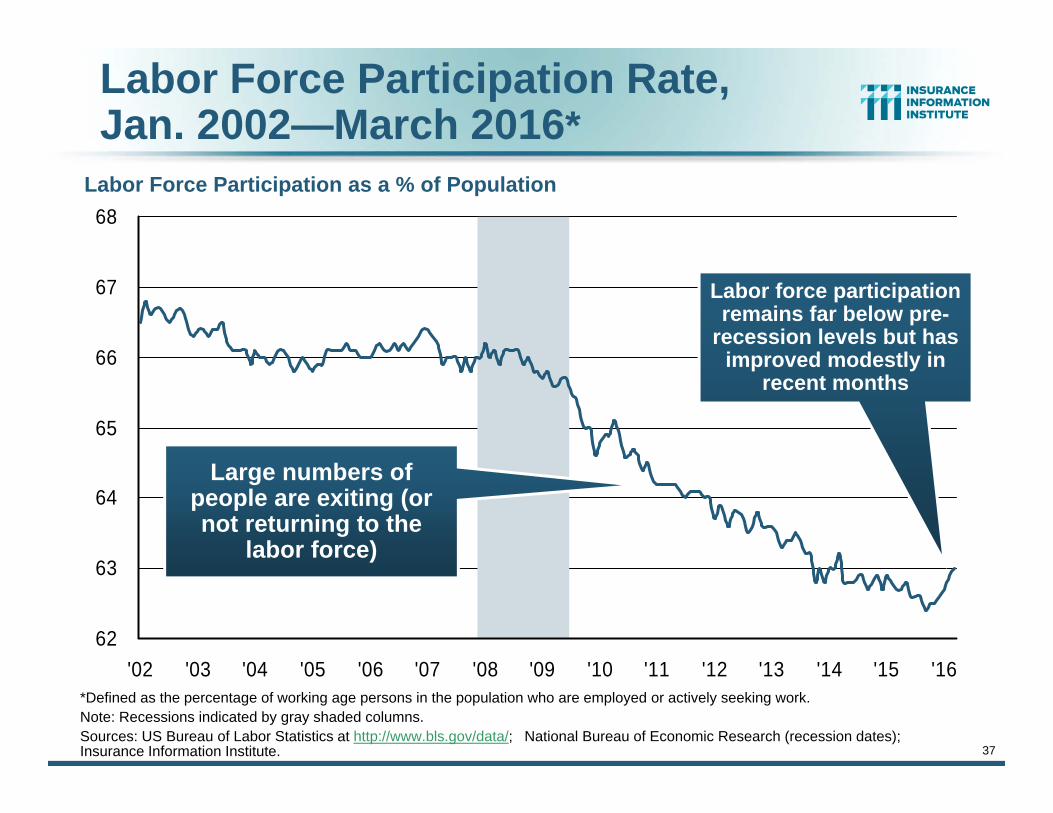

Labor Force Participation Rate,Jan. 2002—March 2016*

*Defined as the percentage of working age persons in the population who are employed or actively seeking work.Note: Recessions indicated by gray shaded columns.Sources: US Bureau of Labor Statistics at http://www.bls.gov/data/; National Bureau of Economic Research (recession dates); Insurance Information Institute.

62

63

64

65

66

67

68

'02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

Large numbers of people are exiting (or not returning to the

labor force)

Labor force participation remains far below pre-

recession levels but has improved modestly in

recent months

Labor Force Participation as a % of Population

38

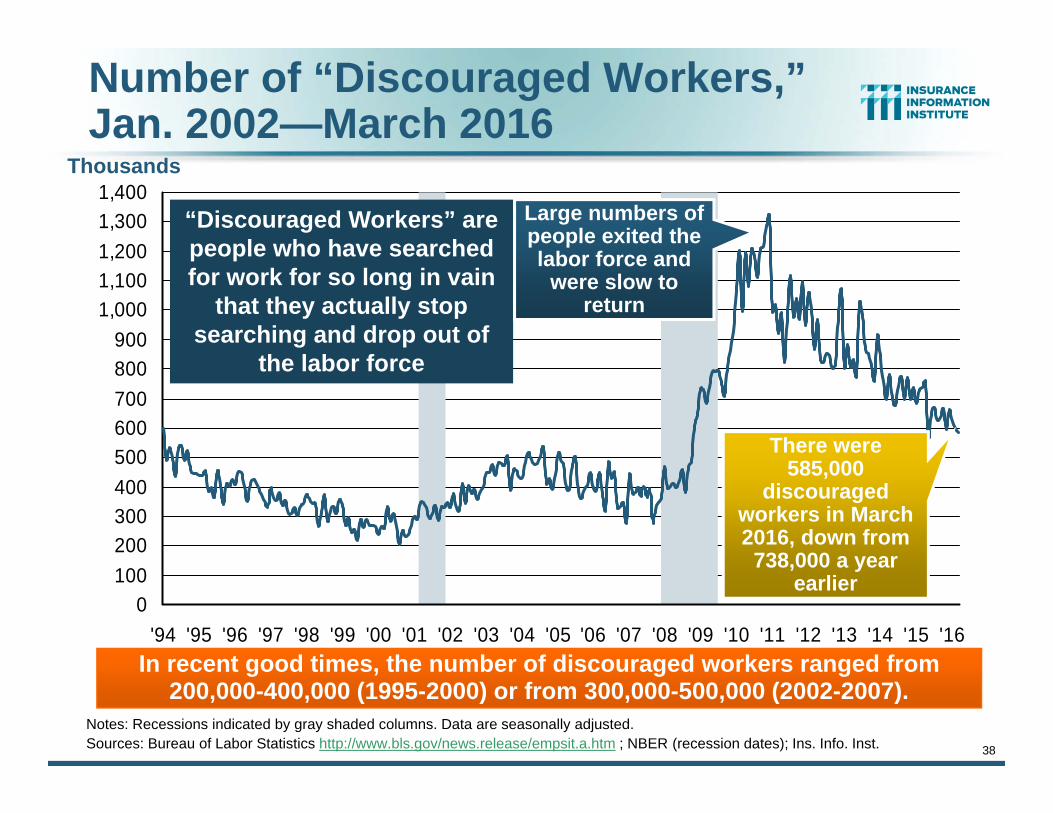

Notes: Recessions indicated by gray shaded columns. Data are seasonally adjusted.Sources: Bureau of Labor Statistics http://www.bls.gov/news.release/empsit.a.htm ; NBER (recession dates); Ins. Info. Inst.

0100200300400500600700800900

1,0001,1001,2001,3001,400

'94 '95 '96 '97 '98 '99 '00 '01 '02 '03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16In recent good times, the number of discouraged workers ranged from

200,000-400,000 (1995-2000) or from 300,000-500,000 (2002-2007).

There were 585,000

discouraged workers in March 2016, down from

738,000 a year earlier

Thousands

“Discouraged Workers” are people who have searched for work for so long in vain

that they actually stop searching and drop out of

the labor force

Number of “Discouraged Workers,”Jan. 2002—March 2016

Large numbers of people exited the labor force and

were slow to return

CONSTRUCTION INDUSTRY OVERVIEW & OUTLOOK

39

The Construction Sector Is Critical to the Economy and the P/C Insurance Industry

39

40

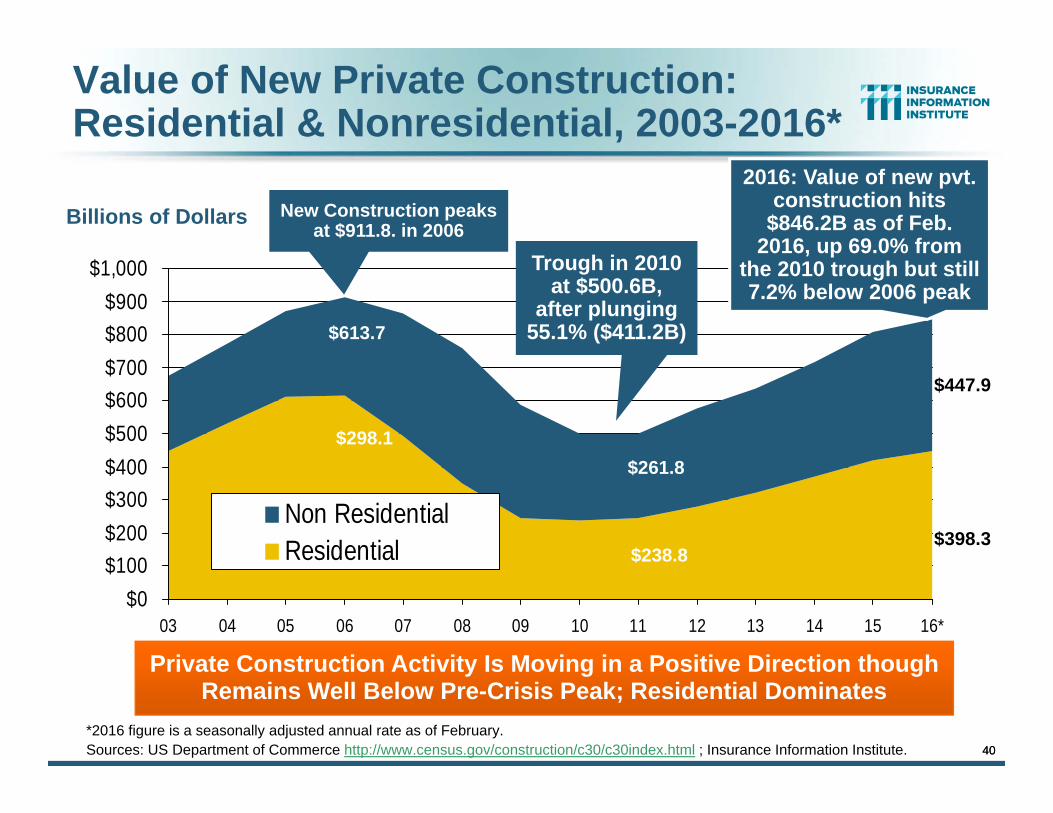

Value of New Private Construction: Residential & Nonresidential, 2003-2016*

Billions of Dollars

$0$100$200$300$400$500$600$700$800$900

$1,000

03 04 05 06 07 08 09 10 11 12 13 14 15 16*

Non ResidentialResidential

Private Construction Activity Is Moving in a Positive Direction though Remains Well Below Pre-Crisis Peak; Residential Dominates

$298.1

$613.7

New Construction peaks at $911.8. in 2006

Trough in 2010 at $500.6B,

after plunging 55.1% ($411.2B)

2016: Value of new pvt. construction hits

$846.2B as of Feb. 2016, up 69.0% from

the 2010 trough but still 7.2% below 2006 peak

40

$261.8

$238.8

$447.9

$398.3

*2016 figure is a seasonally adjusted annual rate as of February.Sources: US Department of Commerce http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

41

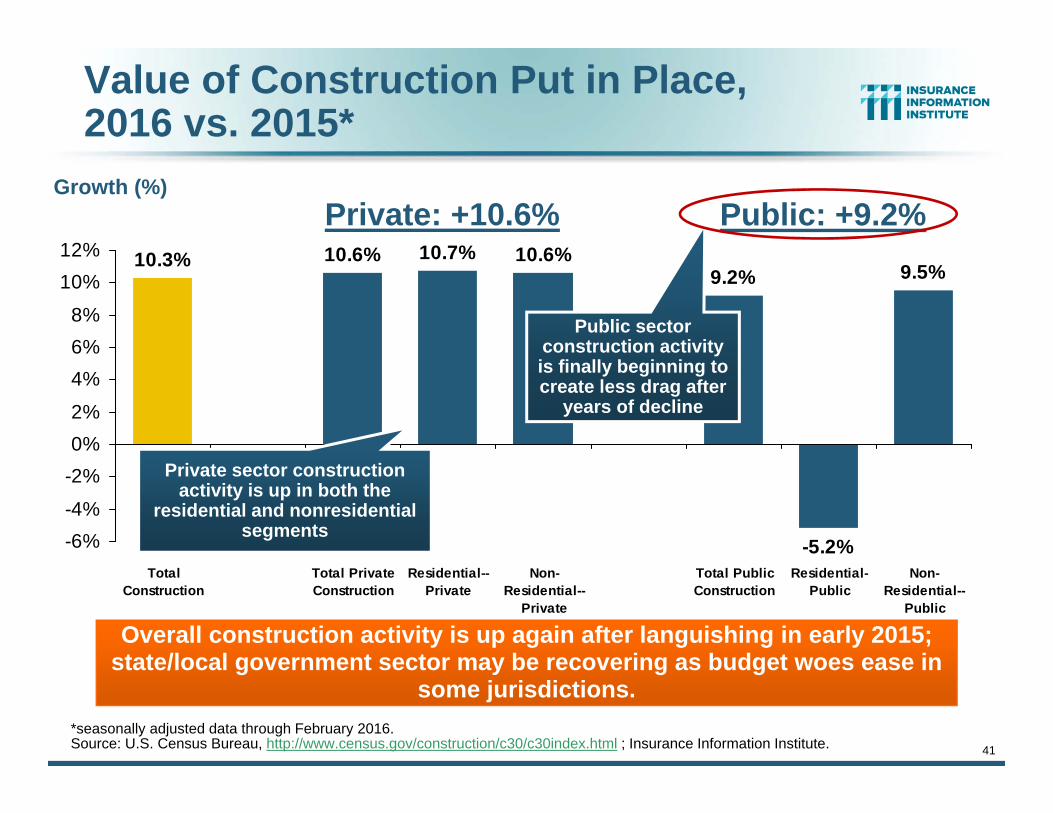

Value of Construction Put in Place, 2016 vs. 2015*

9.2%

-5.2%

9.5%10.3% 10.6% 10.7% 10.6%

-6%-4%

-2%0%2%

4%6%8%

10%12%

TotalConstruction

Total PrivateConstruction

Residential--Private

Non-Residential--

Private

Total PublicConstruction

Residential-Public

Non-Residential--

Public

Overall construction activity is up again after languishing in early 2015; state/local government sector may be recovering as budget woes ease in

some jurisdictions.

Growth (%)

Private sector construction activity is up in both the

residential and nonresidential segments

*seasonally adjusted data through February 2016.Source: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

Private: +10.6% Public: +9.2%

Public sector construction activity is finally beginning to create less drag after

years of decline

42

(Millions of Units)

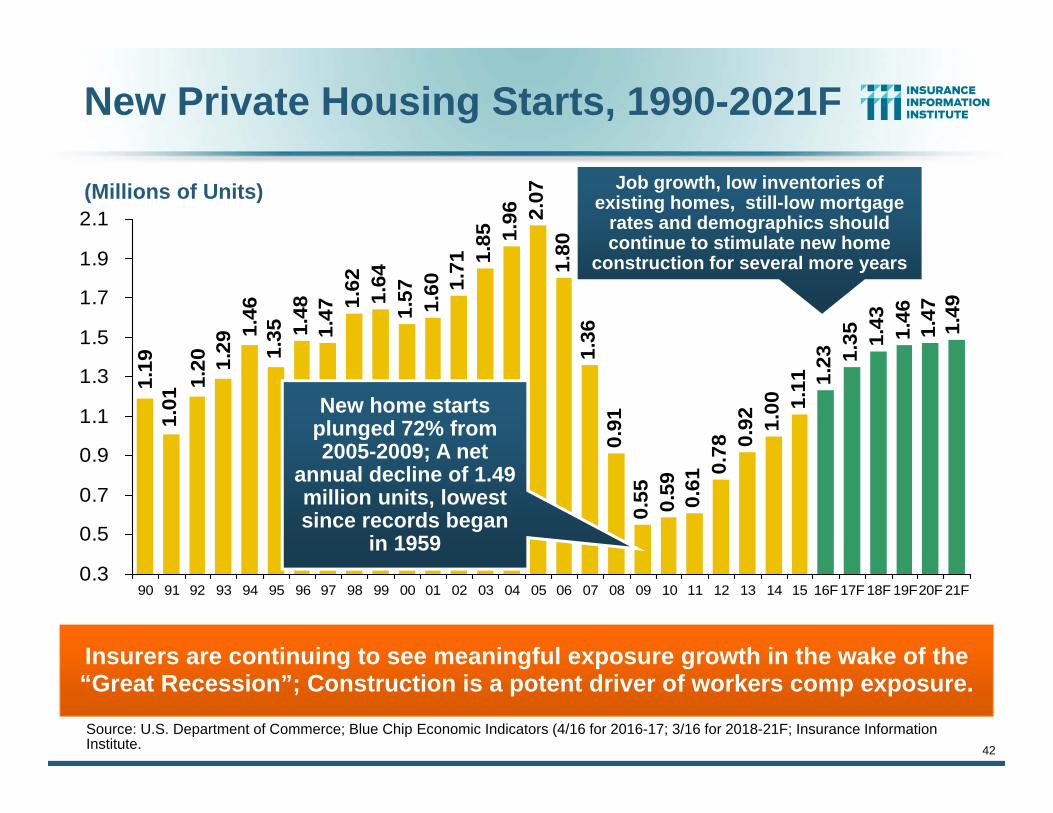

New Private Housing Starts, 1990-2021F

1.48

1.47 1.

62 1.64

1.57 1.60 1.

71 1.85 1.

96 2.07

1.80

1.36

0.91

0.55 0.59 0.61

0.78 0.

92 1.00 1.

11 1.23 1.

35 1.43 1.46

1.47 1.49

1.351.

461.

291.

201.

011.

19

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16F 17F 18F 19F20F 21F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (4/16 for 2016-17; 3/16 for 2018-21F; Insurance Information Institute.

Insurers are continuing to see meaningful exposure growth in the wake of the “Great Recession”; Construction is a potent driver of workers comp exposure.

New home starts plunged 72% from 2005-2009; A net

annual decline of 1.49 million units, lowest since records began

in 1959

Job growth, low inventories of existing homes, still-low mortgage

rates and demographics should continue to stimulate new home

construction for several more years

43

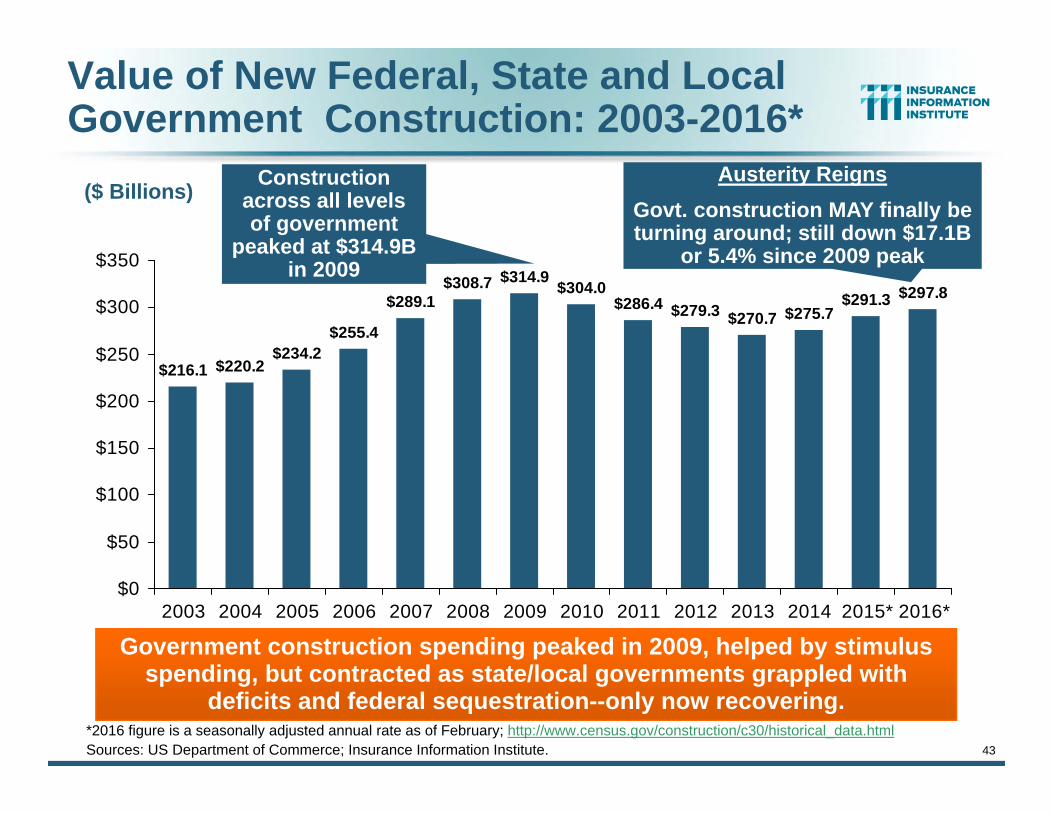

$314.9 $304.0$286.4 $279.3 $270.7 $275.7

$291.3 $297.8

$216.1 $220.2$234.2

$255.4

$289.1$308.7

$0

$50

$100

$150

$200

$250

$300

$350

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015* 2016*

($ Billions)

Government construction spending peaked in 2009, helped by stimulus spending, but contracted as state/local governments grappled with

deficits and federal sequestration--only now recovering.

Value of New Federal, State and Local Government Construction: 2003-2016*

*2016 figure is a seasonally adjusted annual rate as of February; http://www.census.gov/construction/c30/historical_data.htmlSources: US Department of Commerce; Insurance Information Institute.

Construction across all levels of government

peaked at $314.9B in 2009

Austerity ReignsGovt. construction MAY finally be turning around; still down $17.1B

or 5.4% since 2009 peak

44

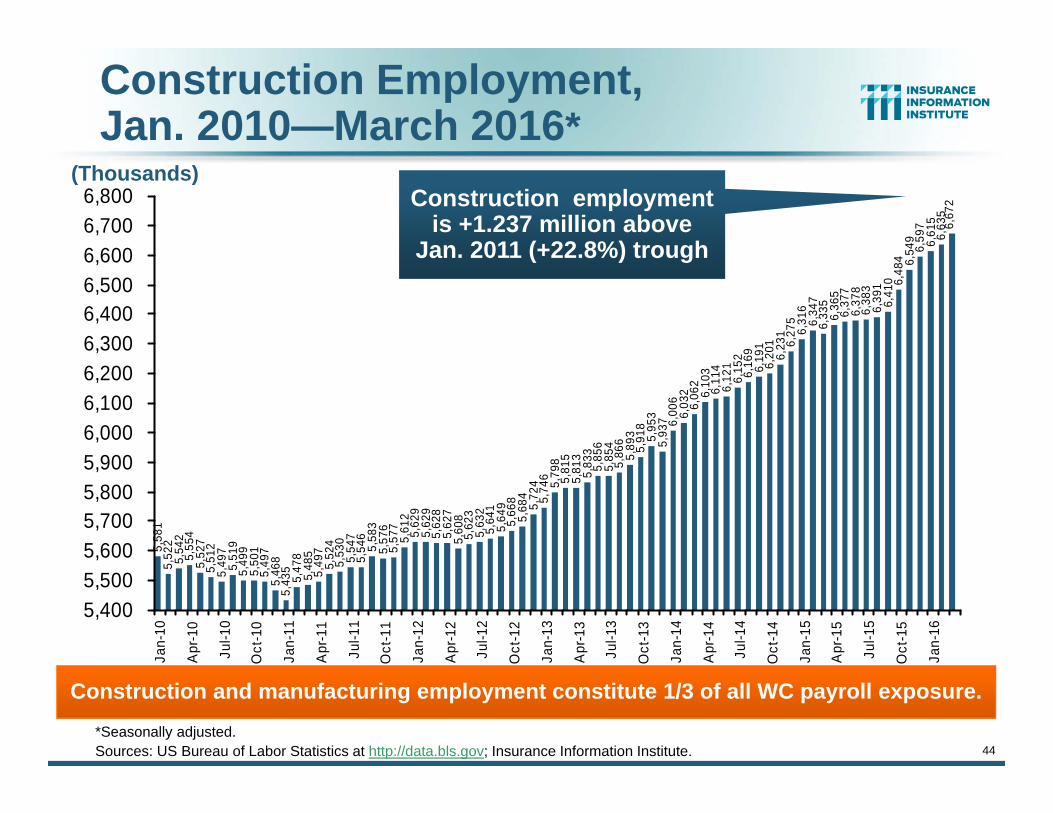

Construction Employment,Jan. 2010—March 2016*

*Seasonally adjusted.Sources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

5,58

15,

522

5,54

25,

554

5,52

75,

512

5,49

75,

519

5,49

95,

501

5,49

75,

468

5,43

55,

478

5,48

55,

497

5,52

45,

530

5,54

75,

546

5,58

35,

576

5,57

75,

612

5,62

95,

629

5,62

85,

627

5,60

85,

623

5,63

25,

641

5,64

95,

668

5,68

45,

724

5,74

6 5,79

85,

815

5,81

35,

833

5,85

65,

854

5,86

65,

893

5,91

85,

953

5,93

7 6,00

66,

032

6,06

26,

103

6,11

46,

121

6,15

26,

169

6,19

16,

201

6,23

16,

275

6,31

66,

347

6,33

56,

365

6,37

76,

378

6,38

36,

391

6,41

0 6,48

4 6,54

96,

597

6,61

56,

635

6,67

2

5,4005,5005,6005,7005,8005,9006,0006,1006,2006,3006,4006,5006,6006,7006,800

Jan-

10

Apr

-10

Jul-1

0

Oct

-10

Jan-

11

Apr

-11

Jul-1

1

Oct

-11

Jan-

12

Apr

-12

Jul-1

2

Oct

-12

Jan-

13

Apr

-13

Jul-1

3

Oct

-13

Jan-

14

Apr

-14

Jul-1

4

Oct

-14

Jan-

15

Apr

-15

Jul-1

5

Oct

-15

Jan-

16

Construction employment is +1.237 million above

Jan. 2011 (+22.8%) trough

(Thousands)

Construction and manufacturing employment constitute 1/3 of all WC payroll exposure.

45

Construction Employment, Jan. 2003–March 2016

Note: Recession indicated by gray shaded column.Sources: U.S. Bureau of Labor Statistics; Insurance Information Institute.

5,000

5,500

6,000

6,500

7,000

7,500

8,000

'03 '04 '05 '06 '07 '08 '09 '10 '11 '12 '13 '14 '15 '16

The “Great Recession” and housing bust destroyed 2.3 million constructions jobs

The construction sector was a growth leader in 2014-16 as the housing market, private investment, and govt. spending recover. WC insurers continue to benefit.

Construction employment troughed at 5.435 million in

Jan. 2011, after a loss of 2.291 million jobs, a 29.7% plunge

from the April 2006 peak

45

Construction employment

peaked at 7.726 million in April 2006

(Thousands) Construction employment as of March 2016 totaled

6.672 million, an increase of 1.237MM jobs or 22.8% from

the Jan. 2011 trough

Gap between pre-recession

construction peak and today: 1.05 million jobs

MANUFACTURING & ENERGY SECTOR OVERVIEW & OUTLOOK

46

The U.S. Manufacturing and Energy Sectors Are Being Buffeted by a

High Dollar, Weak Export Markets and Plunging Oil Prices

46

47

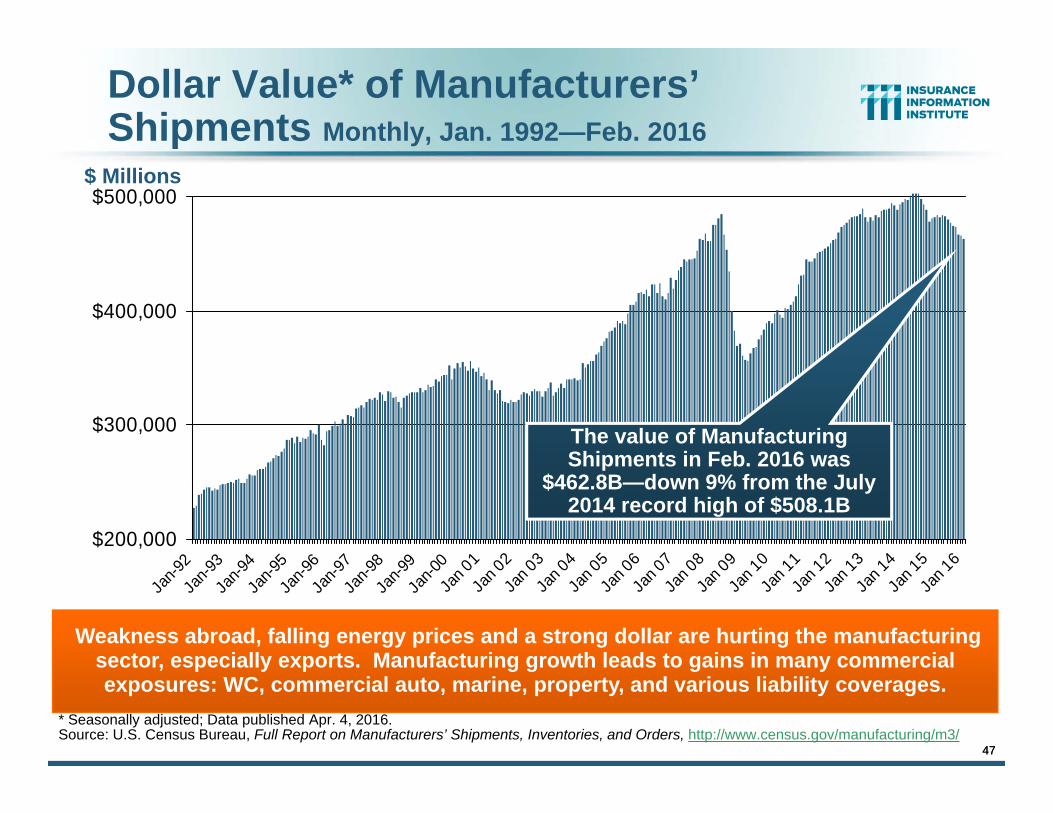

$200,000

$300,000

$400,000

$500,000

Jan-9

2Ja

n-93

Jan-9

4Ja

n-95

Jan-9

6Ja

n-97

Jan-9

8Ja

n-99

Jan-0

0Ja

n 01

Jan 0

2Ja

n 03

Jan 0

4Ja

n 05

Jan 0

6Ja

n 07

Jan 0

8Ja

n 09

Jan 1

0Ja

n 11

Jan 1

2Ja

n 13

Jan 1

4Ja

n 15

Jan 1

6Dollar Value* of Manufacturers’ Shipments Monthly, Jan. 1992—Feb. 2016

* Seasonally adjusted; Data published Apr. 4, 2016.Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Weakness abroad, falling energy prices and a strong dollar are hurting the manufacturing sector, especially exports. Manufacturing growth leads to gains in many commercial exposures: WC, commercial auto, marine, property, and various liability coverages.

$ Millions

47

The value of Manufacturing Shipments in Feb. 2016 was

$462.8B—down 9% from the July 2014 record high of $508.1B

58.3

57.1

60.4

59.6

57.8

55.3

55.1

55.2

55.3 56

.9 58.2

58.5

60.8 61.4

59.7

59.7

54.2 55

.851

.4 52.5

52.5

51.8 52.2 53

.1 54.1

51.9 53

.3 54.1

52.5

50.2

50.5

50.7 51

.651

.749

.950

.253

.1 54.2

50.7

49.0

50.9

55.4

55.7 56.2

56.4 57

.056

.551

.353

.2 53.7 54

.9 55.4

55.3 57

.159

.056

.659

.058

.755

.553

.553

.352

.351

.6 53.1

53.1

51.9

51.0

50.0

49.4

48.4

48.0

48.2 49

.551

.850

.851.3

40

45

50

55

60

65

Jan-

10Fe

b-10

Mar

-10

Apr

-10

May

-10

Jun-

10Ju

l-10

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11Fe

b-11

Mar

-11

Apr

-11

May

-11

Jun-

11Ju

l-11

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12Fe

b-12

Mar

-12

Apr

-12

May

-12

Jun-

12Ju

l-12

Aug

-12

Sep

-12

Oct

-12

Nov

-12

Dec

-12

Jan-

13Fe

b-13

Mar

-13

Apr

-13

May

-13

Jun-

13Ju

l-13

Aug

-13

Sep

-13

Oct

-13

Nov

-13

Dec

-13

Jan-

14Fe

b-14

Mar

-14

Apr

-14

May

-14

Jun-

14Ju

l-14

Aug

-14

Sep

-14

Oct

-14

Nov

-14

Dec

-14

Jan-

15Fe

b-15

Mar

-15

Apr

-15

May

-15

Jun-

15Ju

l-15

Aug

-15

Sep

-15

Oct

-15

Nov

-15

Dec

-15

Jan-

16Fe

b-16

Mar

-16

Apr

-16

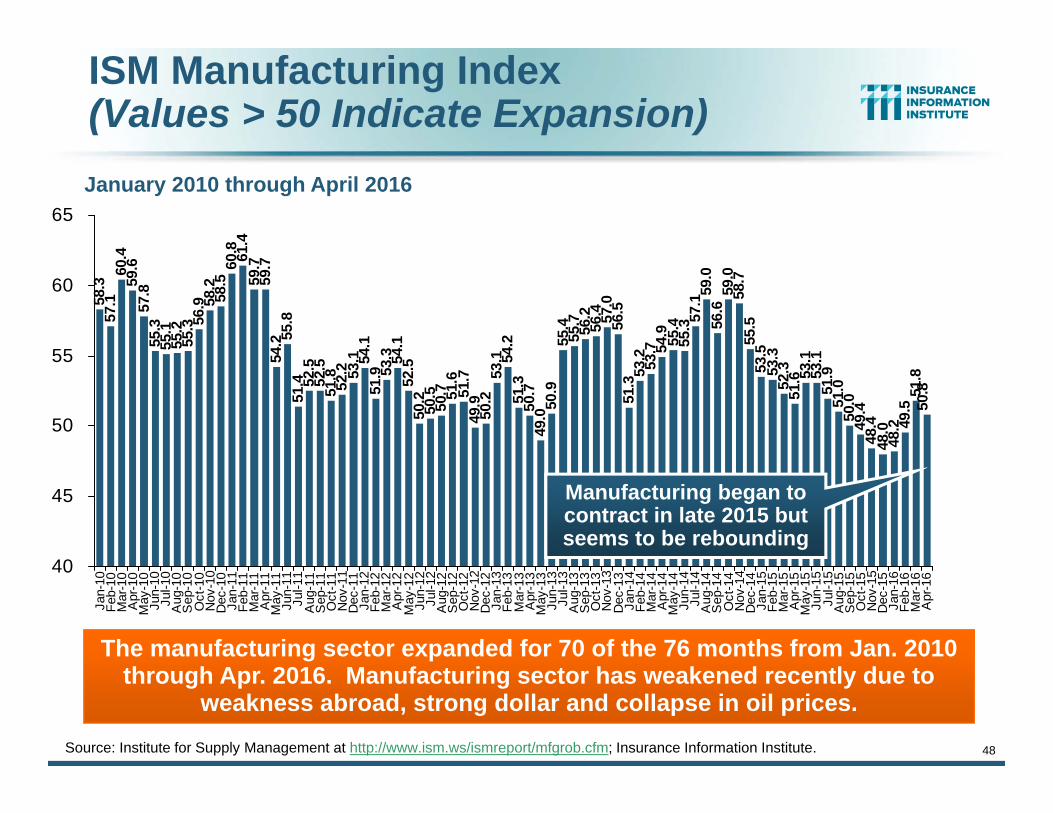

ISM Manufacturing Index(Values > 50 Indicate Expansion)January 2010 through April 2016

The manufacturing sector expanded for 70 of the 76 months from Jan. 2010 through Apr. 2016. Manufacturing sector has weakened recently due to

weakness abroad, strong dollar and collapse in oil prices.Source: Institute for Supply Management at http://www.ism.ws/ismreport/mfgrob.cfm; Insurance Information Institute.

Manufacturing began to contract in late 2015 but seems to be rebounding

48

49

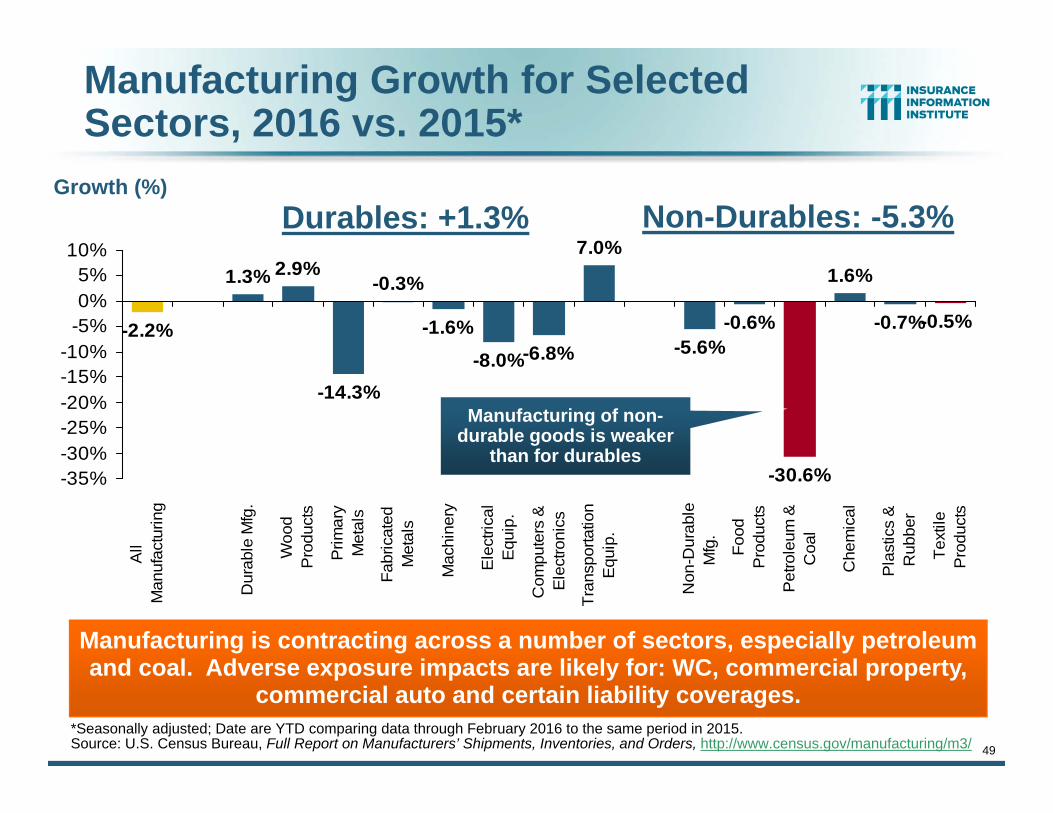

Manufacturing Growth for Selected Sectors, 2016 vs. 2015*

-1.6%-8.0%-6.8%

7.0%

-5.6%-0.6%

-30.6%

1.6%

-0.7%-0.5%-2.2%

1.3% 2.9%

-14.3%

-0.3%

-35%-30%-25%-20%-15%-10%

-5%0%5%

10%

All

Man

ufac

turin

g

Dur

able

Mfg

.

Woo

dP

rodu

cts

Prim

ary

Met

als

Fabr

icat

edM

etal

s

Mac

hine

ry

Ele

ctric

alE

quip

.

Com

pute

rs &

Ele

ctro

nics

Tran

spor

tatio

nE

quip

.

Non

-Dur

able

Mfg

.

Food

Pro

duct

s

Pet

role

um &

Coa

l

Che

mic

al

Pla

stic

s &

Rub

ber

Text

ileP

rodu

cts

Manufacturing is contracting across a number of sectors, especially petroleum and coal. Adverse exposure impacts are likely for: WC, commercial property,

commercial auto and certain liability coverages.

Growth (%)

Manufacturing of non-durable goods is weaker

than for durables

*Seasonally adjusted; Date are YTD comparing data through February 2016 to the same period in 2015.Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Durables: +1.3% Non-Durables: -5.3%

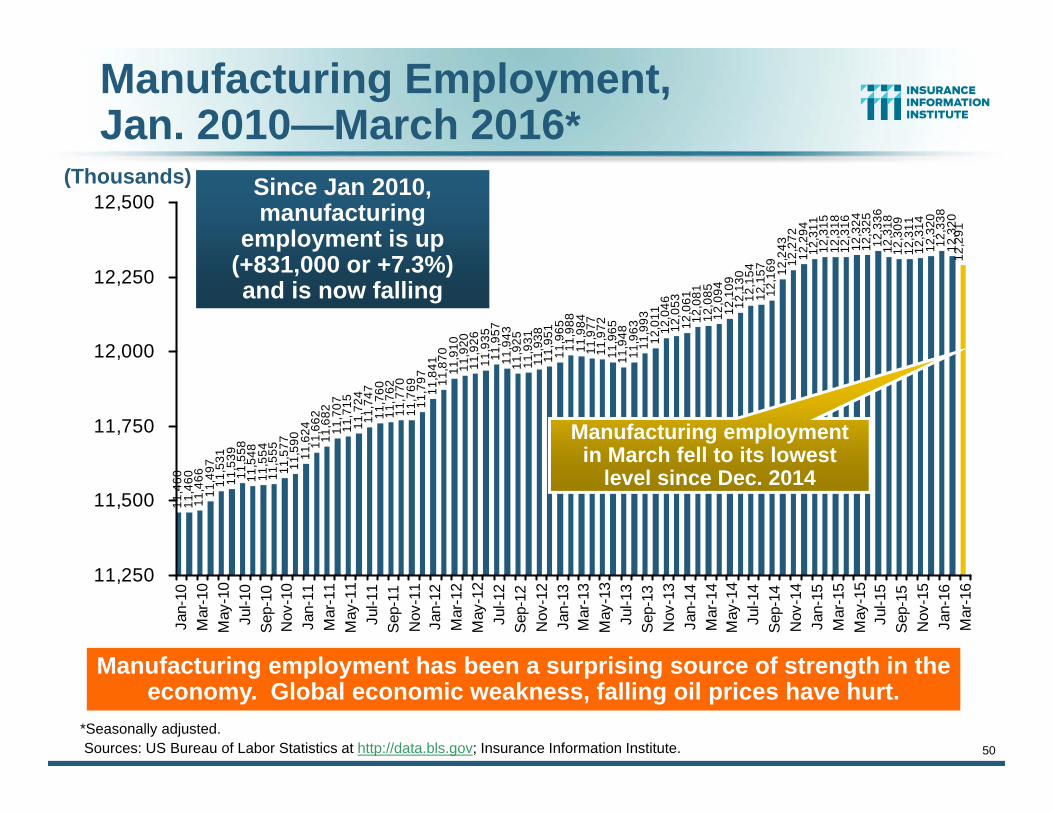

50

Manufacturing Employment,Jan. 2010—March 2016*

11,4

6011

,460

11,4

6611

,497

11,5

3111

,539

11,5

5811

,548

11,5

5411

,555

11,5

7711

,590

11,6

2411

,662

11,6

8211

,707

11,7

1511

,724

11,7

4711

,760

11,7

6211

,770

11,7

6911

,797

11,8

4111

,870

11,9

1011

,920

11,9

2611

,935

11,9

5711

,943

11,9

2511

,931

11,9

3811

,951

11,9

6511

,988

11,9

8411

,977

11,9

7211

,965

11,9

4811

,963

11,9

9312

,011

12,0

4612

,053

12,0

6112

,081

12,0

8512

,094

12,1

0912

,130

12,1

5412

,157

12,1

69 12,2

4312

,272

12,2

9412

,311

12,3

1512

,318

12,3

1612

,324

12,3

2512

,336

12,3

1812

,309

12,3

1112

,314

12,3

2012

,338

12,3

2012

,291

11,250

11,500

11,750

12,000

12,250

12,500Ja

n-10

Mar

-10

May

-10

Jul-1

0S

ep-1

0N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-1

1S

ep-1

1N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-1

2S

ep-1

2N

ov-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3S

ep-1

3N

ov-1

3Ja

n-14

Mar

-14

May

-14

Jul-1

4S

ep-1

4N

ov-1

4Ja

n-15

Mar

-15

May

-15

Jul-1

5S

ep-1

5N

ov-1

5Ja

n-16

Mar

-16

Manufacturing employment has been a surprising source of strength in the economy. Global economic weakness, falling oil prices have hurt.

*Seasonally adjusted.Sources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

(Thousands) Since Jan 2010, manufacturing

employment is up (+831,000 or +7.3%)and is now falling

Manufacturing employment in March fell to its lowest

level since Dec. 2014

51

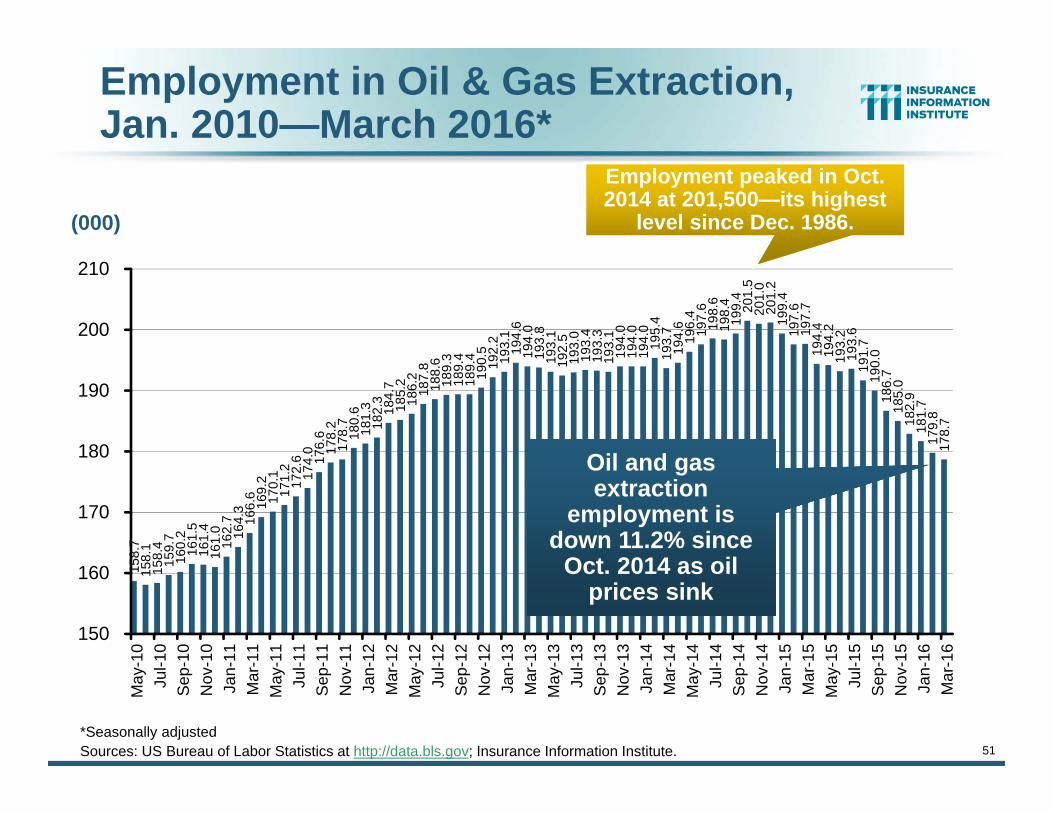

Employment in Oil & Gas Extraction,Jan. 2010—March 2016*

*Seasonally adjustedSources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

158.

715

8.1

158.

415

9.7

160.

216

1.5

161.

416

1.0

162.

716

4.3

166.

616

9.2

170.

117

1.2

172.

617

4.0

176.

617

8.2

178.

718

0.6

181.

318

2.3

184.

718

5.2

186.

218

7.8

188.

618

9.3

189.

418

9.4

190.

519

2.2

193.

119

4.6

194.

019

3.8

193.

119

2.5

193.

019

3.4

193.

319

3.1

194.

019

4.0

194.

019

5.4

193.

719

4.6

196.

419

7.6

198.

619

8.4

199.

420

1.5

201.

020

1.2

199.

419

7.6

197.

719

4.4

194.

219

3.2

193.

619

1.7

190.

018

6.7

185.

018

2.9

181.

717

9.8

178.

7

150

160

170

180

190

200

210

May

-10

Jul-1

0S

ep-1

0N

ov-1

0Ja

n-11

Mar

-11

May

-11

Jul-1

1S

ep-1

1N

ov-1

1Ja

n-12

Mar

-12

May

-12

Jul-1

2S

ep-1

2N

ov-1

2Ja

n-13

Mar

-13

May

-13

Jul-1

3S

ep-1

3N

ov-1

3Ja

n-14

Mar

-14

May

-14

Jul-1

4S

ep-1

4N

ov-1

4Ja

n-15

Mar

-15

May

-15

Jul-1

5S

ep-1

5N

ov-1

5Ja

n-16

Mar

-16

Oil and gas extraction

employment is down 11.2% since

Oct. 2014 as oil prices sink

(000)

Employment peaked in Oct. 2014 at 201,500—its highest

level since Dec. 1986.

The Sharing Economy: An Update

The On-Demand Economy Will Transform the American

Workforce and the P/C Insurance Industry Too

52

53

The Sharing Economy Has Grown—And Attracted Political Scrutiny

54

Political Skepticism About the‘Gig’ Economy

"Many Americans are making extra money renting out a spare room, designing a website ... even driving their own car. This on demand or so called 'gig' economy is creating exciting opportunities and unleashing innovation, but it's also raising hard questions about workplace protections and what a good job will look like in the future."

--Hillary Clinton, July 13, 2015

55

Regulatory Issues Abound as Well, With Implications for Insurance Coverages

A driver for Uber is an employee, not a contractor, according to a California Ruling that eventually could push up costs ‘for the smartphone-based ride hailing service and hurt the closely watched start-up's valuation.

The California Labor Commissioner's decision could ripple through the burgeoning industry of providing services via smartphones, with potential implications for other “crowdsourced” services such as Uber rival Lyft, chore service Task Rabbit, and cleaning service Home joy.

--Reuters, June 18, 2015

56

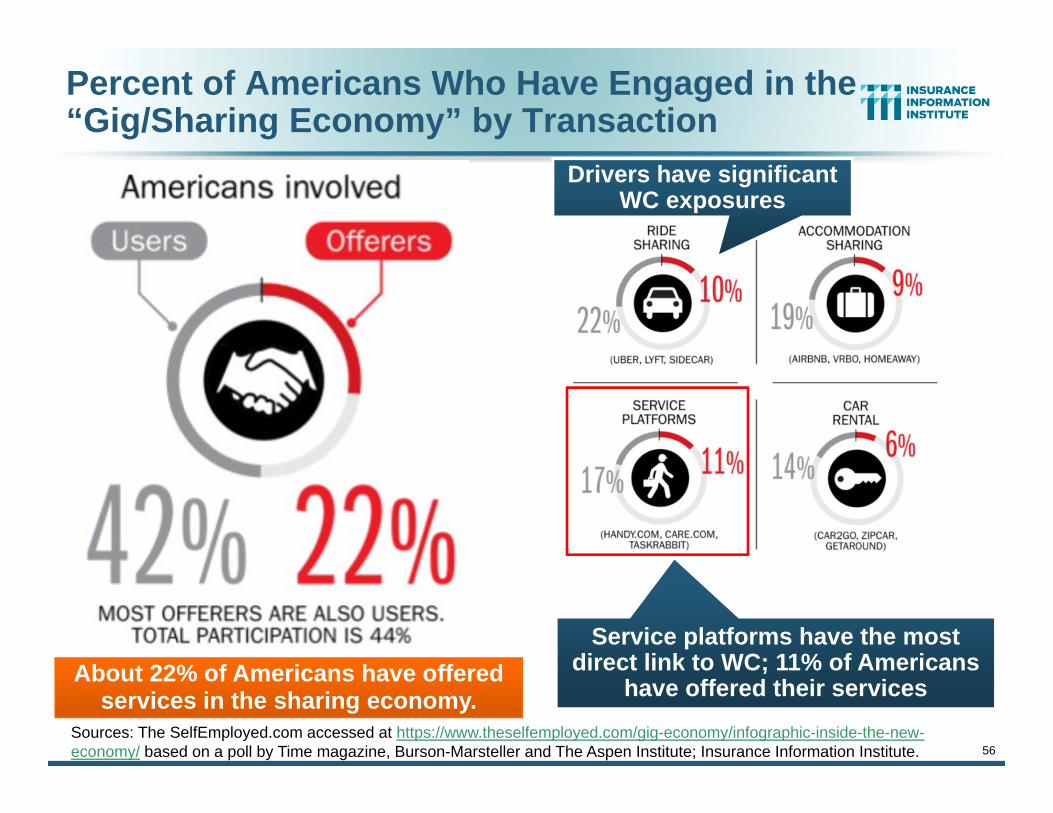

Percent of Americans Who Have Engaged in the “Gig/Sharing Economy” by Transaction

Sources: The SelfEmployed.com accessed at https://www.theselfemployed.com/gig-economy/infographic-inside-the-new-economy/ based on a poll by Time magazine, Burson-Marsteller and The Aspen Institute; Insurance Information Institute.

About 22% of Americans have offered services in the sharing economy.

Service platforms have the most direct link to WC; 11% of Americans

have offered their services

Drivers have significant WC exposures

57

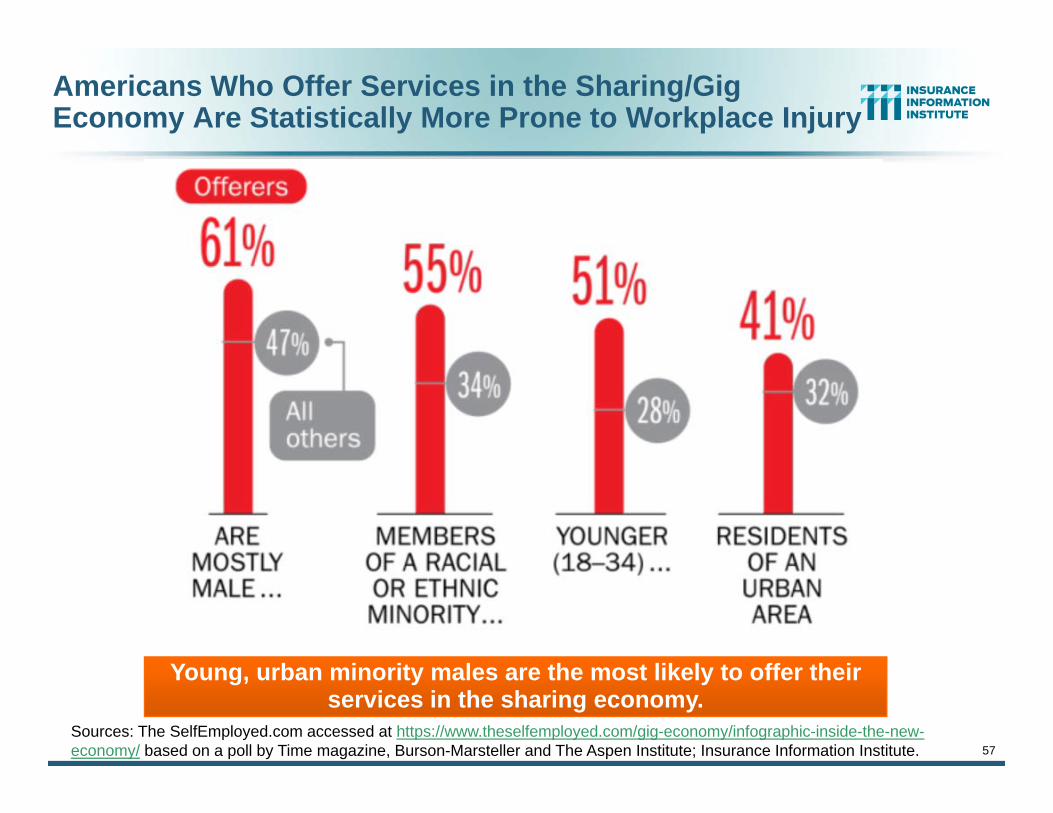

Americans Who Offer Services in the Sharing/Gig Economy Are Statistically More Prone to Workplace Injury

Sources: The SelfEmployed.com accessed at https://www.theselfemployed.com/gig-economy/infographic-inside-the-new-economy/ based on a poll by Time magazine, Burson-Marsteller and The Aspen Institute; Insurance Information Institute.

Young, urban minority males are the most likely to offer their services in the sharing economy.

58

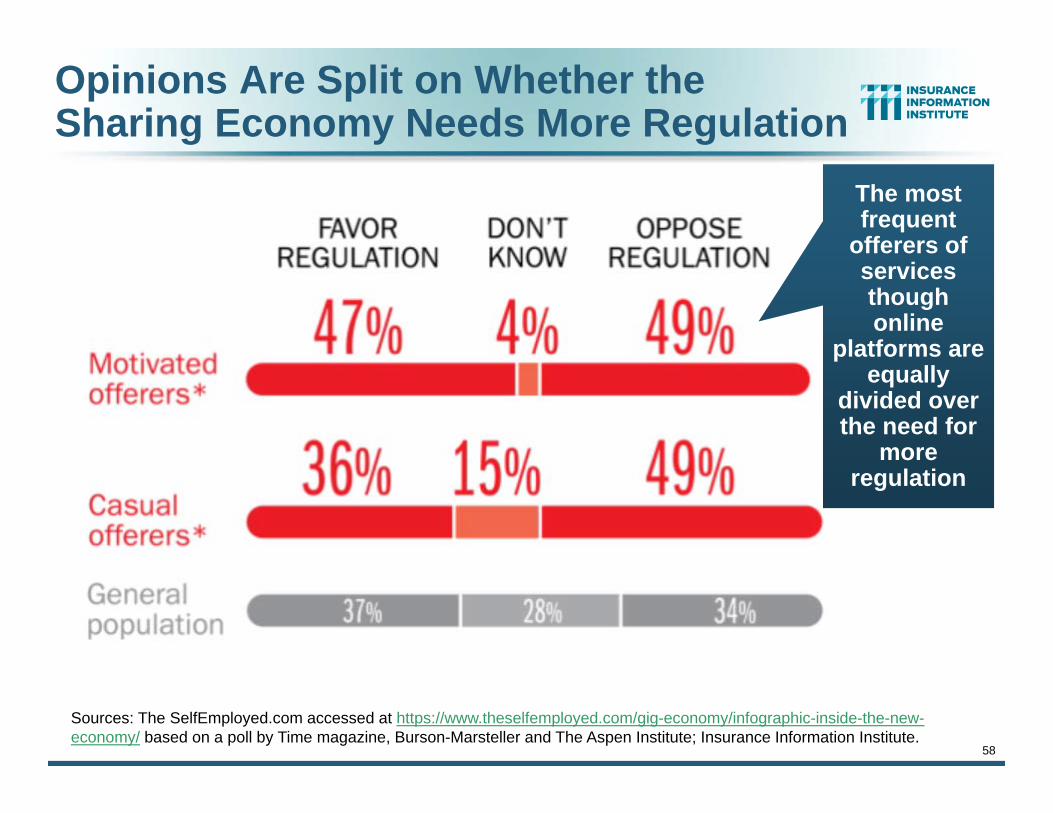

Opinions Are Split on Whether the Sharing Economy Needs More Regulation

Sources: The SelfEmployed.com accessed at https://www.theselfemployed.com/gig-economy/infographic-inside-the-new-economy/ based on a poll by Time magazine, Burson-Marsteller and The Aspen Institute; Insurance Information Institute.

The most frequent

offerers of services though online

platforms are equally

divided over the need for

more regulation

59

THE ‘INTERNET OF THINGS’

Capturing Economic Value Amid a Shifting Insurer Value Chain

60

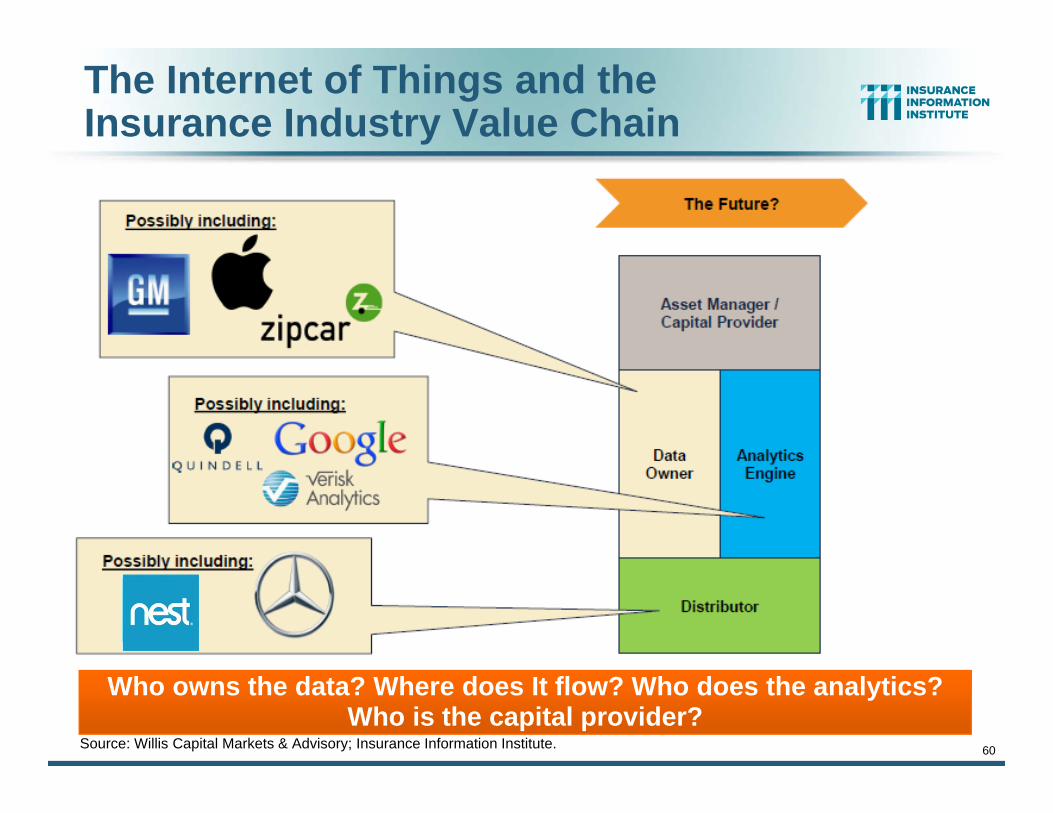

The Internet of Things and the Insurance Industry Value Chain

Source: Willis Capital Markets & Advisory; Insurance Information Institute.

Who owns the data? Where does It flow? Who does the analytics? Who is the capital provider?

61

The ‘Internet of Things’ and ‘The Insurance-Net of Things’

62

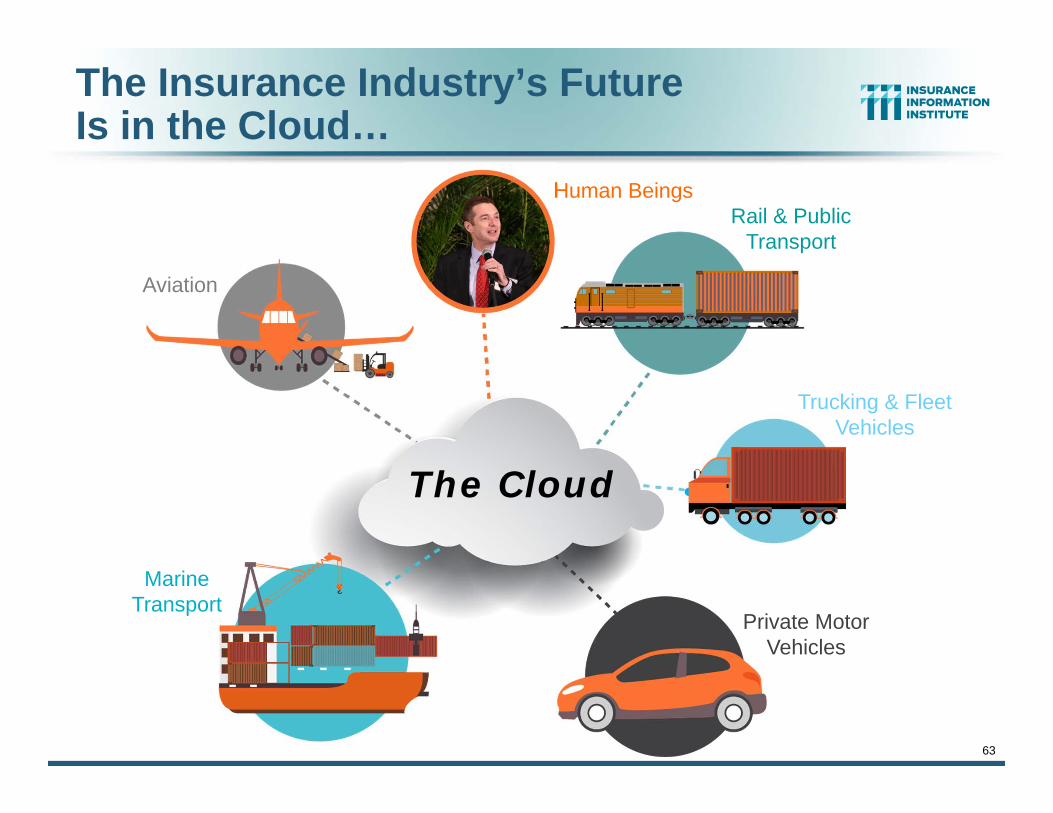

Aviation

Rail & Public Transport

Trucking & Fleet Vehicles

Marine Transport

Private Motor Vehicles

The Insurance Industry’s Future Is in the Cloud…

The Cloud

63

Aviation

Rail & Public Transport

Trucking & Fleet Vehicles

Marine Transport

Private Motor Vehicles

The Cloud

The Insurance Industry’s Future Is in the Cloud…

Human Beings

64

OCCUPATIONAL DEATHS IN TRANSPORTATION:

IS TECHNOLOGY THE SOLUTION?

Technology Promises Safer Vehicles, Highways But How Much of this Is

Silicon Valley Hype?

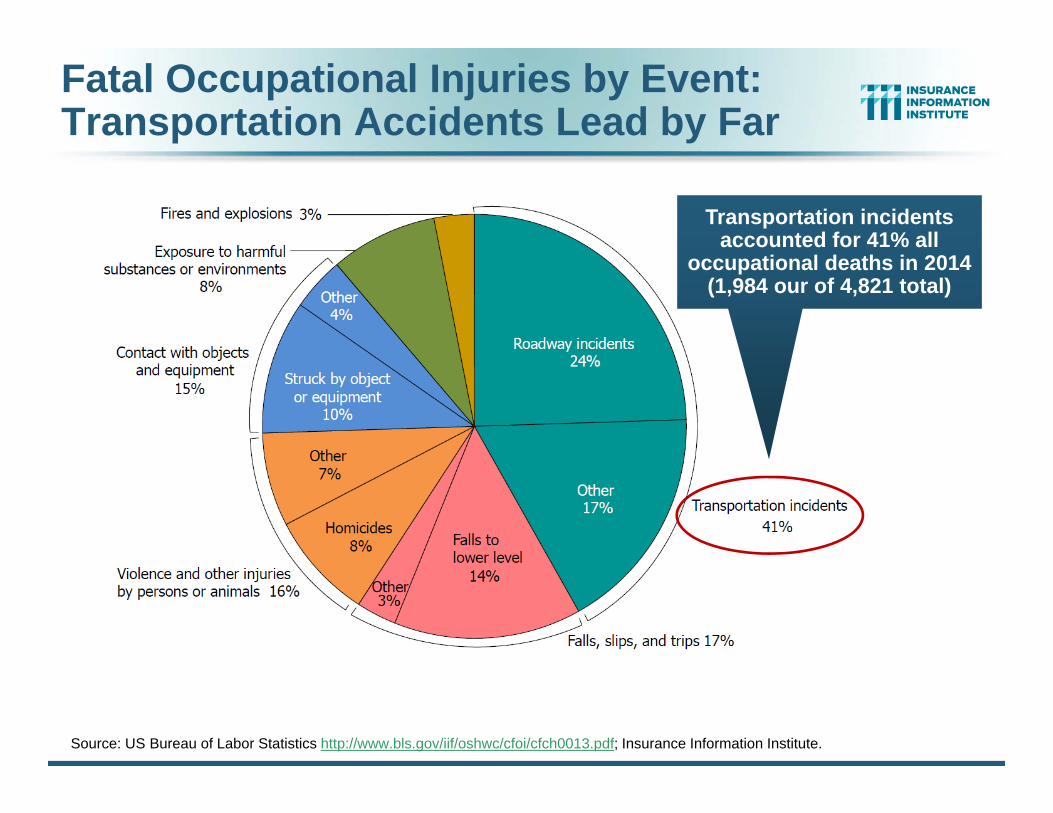

Fatal Occupational Injuries by Event: Transportation Accidents Lead by Far

Transportation incidents accounted for 41% all

occupational deaths in 2014 (1,984 our of 4,821 total)

Source: US Bureau of Labor Statistics http://www.bls.gov/iif/oshwc/cfoi/cfch0013.pdf; Insurance Information Institute.

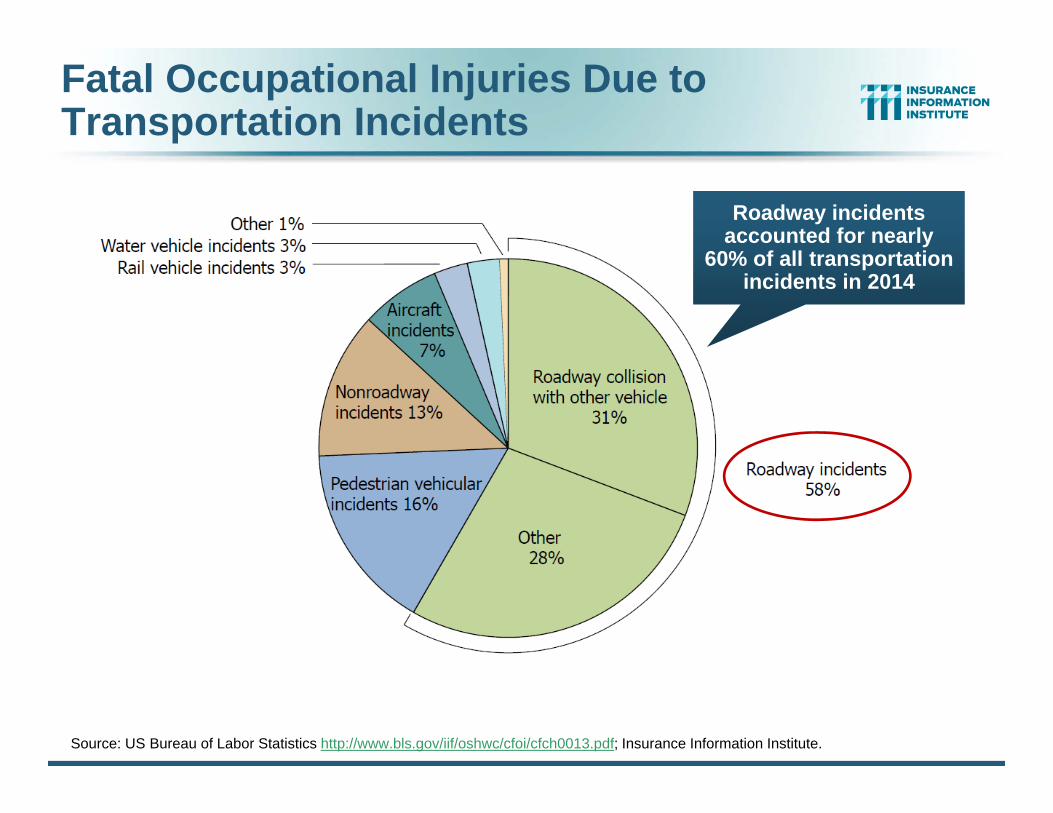

Fatal Occupational Injuries Due to Transportation Incidents

Source: US Bureau of Labor Statistics http://www.bls.gov/iif/oshwc/cfoi/cfch0013.pdf; Insurance Information Institute.

Roadway incidents accounted for nearly

60% of all transportation incidents in 2014

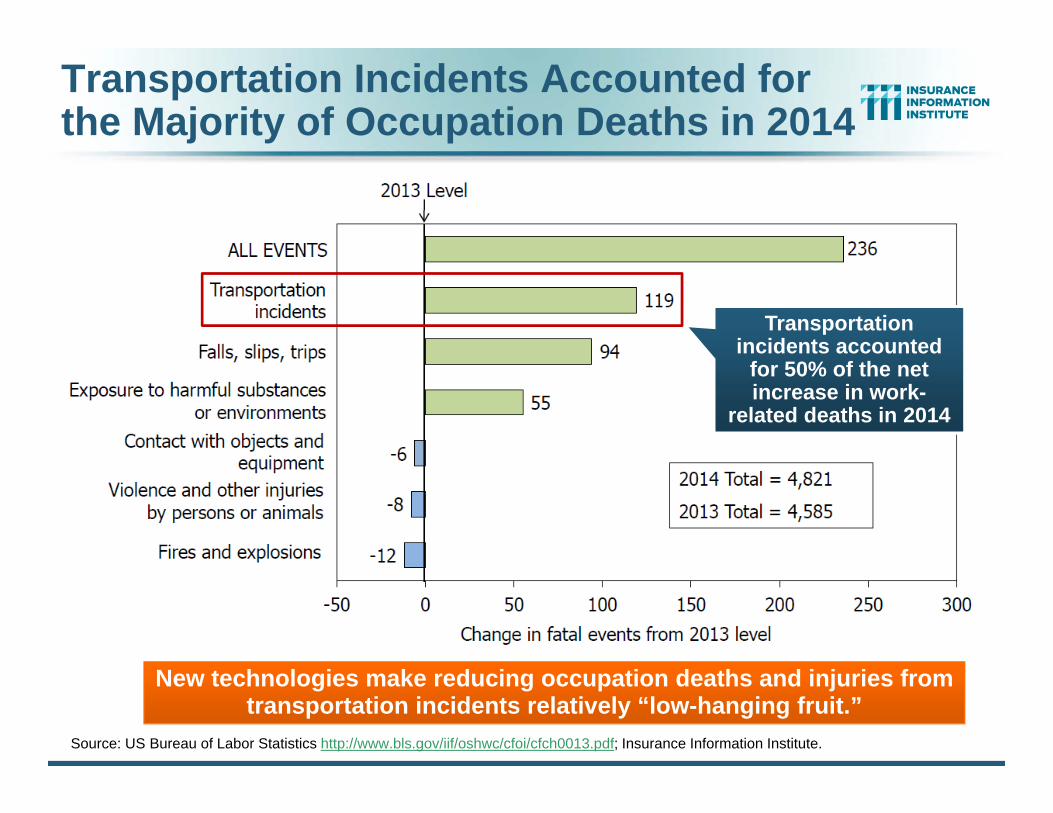

Transportation Incidents Accounted for the Majority of Occupation Deaths in 2014

Source: US Bureau of Labor Statistics http://www.bls.gov/iif/oshwc/cfoi/cfch0013.pdf; Insurance Information Institute.

Transportation incidents accounted

for 50% of the net increase in work-

related deaths in 2014

New technologies make reducing occupation deaths and injuries from transportation incidents relatively “low-hanging fruit.”

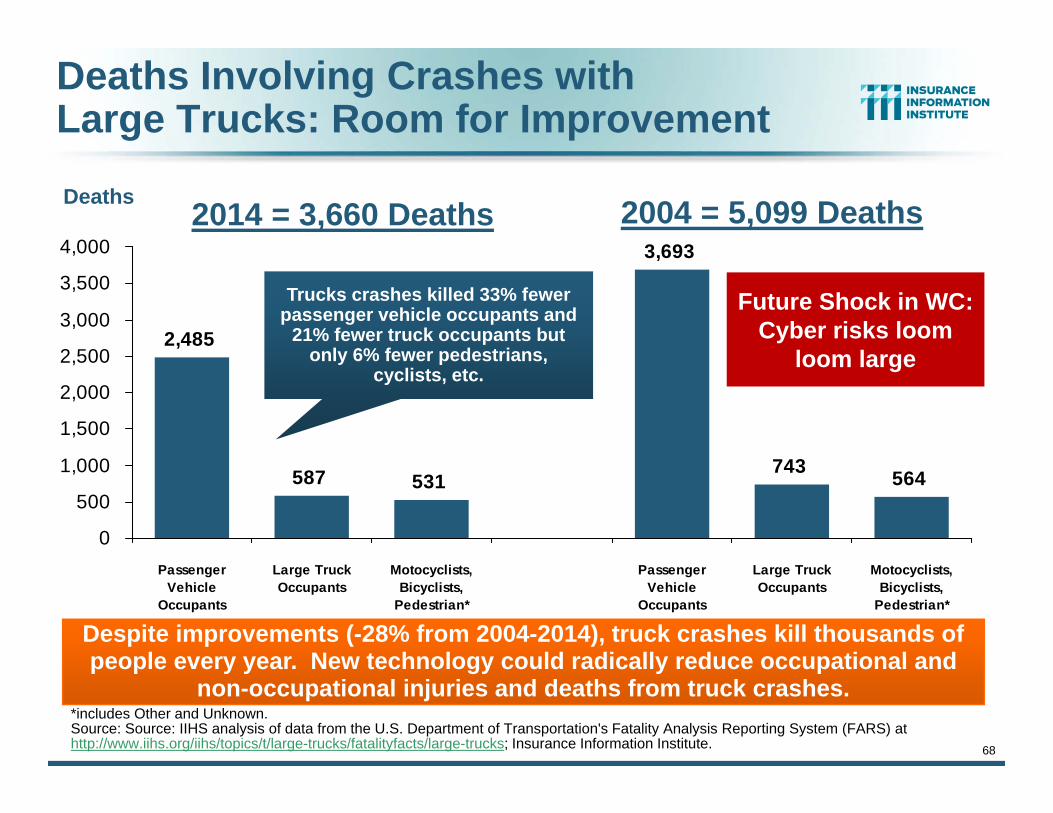

68

Deaths Involving Crashes with Large Trucks: Room for Improvement

564

2,485

587 531

3,693

743

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

PassengerVehicle

Occupants

Large TruckOccupants

Motocyclists,Bicyclists,

Pedestrian*

PassengerVehicle

Occupants

Large TruckOccupants

Motocyclists,Bicyclists,

Pedestrian*

Despite improvements (-28% from 2004-2014), truck crashes kill thousands of people every year. New technology could radically reduce occupational and

non-occupational injuries and deaths from truck crashes.

Deaths

Trucks crashes killed 33% fewer passenger vehicle occupants and

21% fewer truck occupants but only 6% fewer pedestrians,

cyclists, etc.

*includes Other and Unknown.Source: Source: IIHS analysis of data from the U.S. Department of Transportation's Fatality Analysis Reporting System (FARS) at http://www.iihs.org/iihs/topics/t/large-trucks/fatalityfacts/large-trucks; Insurance Information Institute.

2014 = 3,660 Deaths 2004 = 5,099 Deaths

Future Shock in WC:Cyber risks loom

loom large

#RiskyRideSXSWMarch 13, 2016, Austin, TX

70

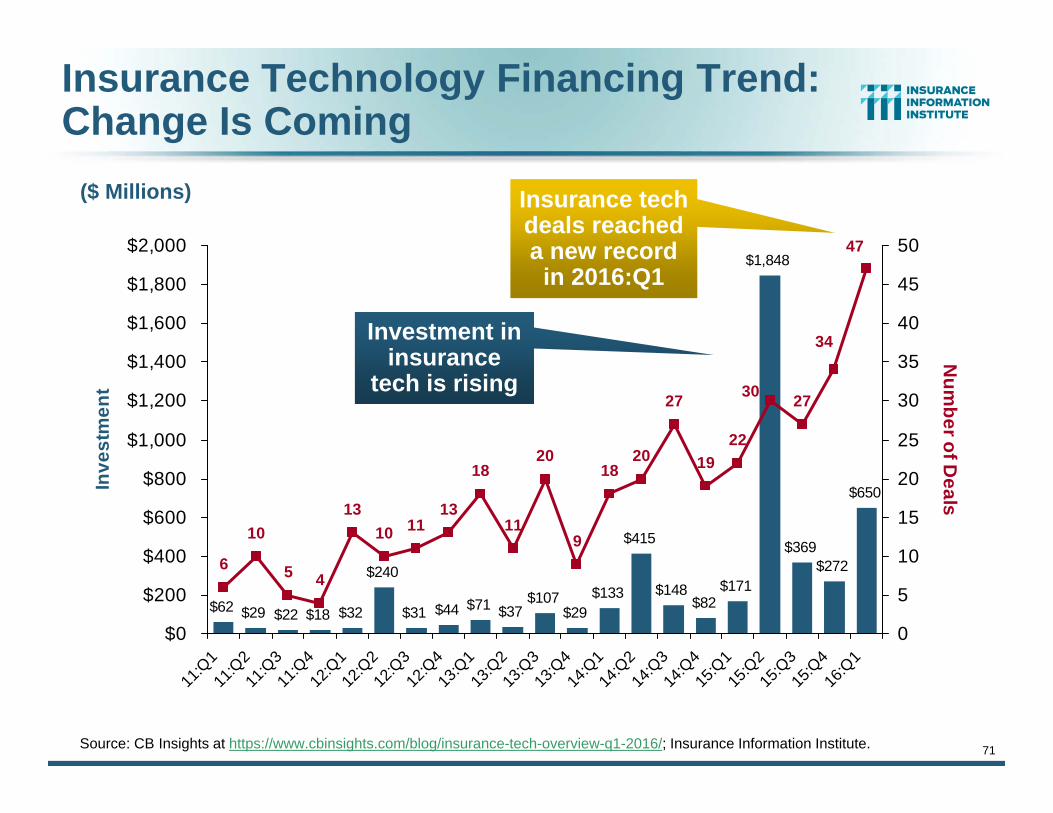

INSURANCE TECHNOLOGY:FIN TECH ZEROES IN

Number and Value of Deals Is Increasing

In Search of the Elusive Insurance ‘Unicorn’

71

$62 $29 $22 $18

$240

$31 $44 $71 $37$107

$29$133

$415

$148$82

$171

$1,848

$369$272

$650

$32

6

10

5 4

1310 11

13

18

11

20

9

1820

27

1922

27

34

30

47

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

$1,600

$1,800

$2,000

11:Q

111

:Q2

11:Q

311

:Q4

12:Q

112

:Q2

12:Q

312

:Q4

13:Q

113

:Q2

13:Q

313

:Q4

14:Q

114

:Q2

14:Q

314

:Q4

15:Q

115

:Q2

15:Q

315

:Q4

16:Q

1

Inve

stm

ent

0

5

10

15

20

25

30

35

40

45

50

Num

ber of Deals

($ Millions)

Investment in insurance

tech is rising

Insurance tech deals reached a new record

in 2016:Q1

Source: CB Insights at https://www.cbinsights.com/blog/insurance-tech-overview-q1-2016/; Insurance Information Institute.

Insurance Technology Financing Trend: Change Is Coming

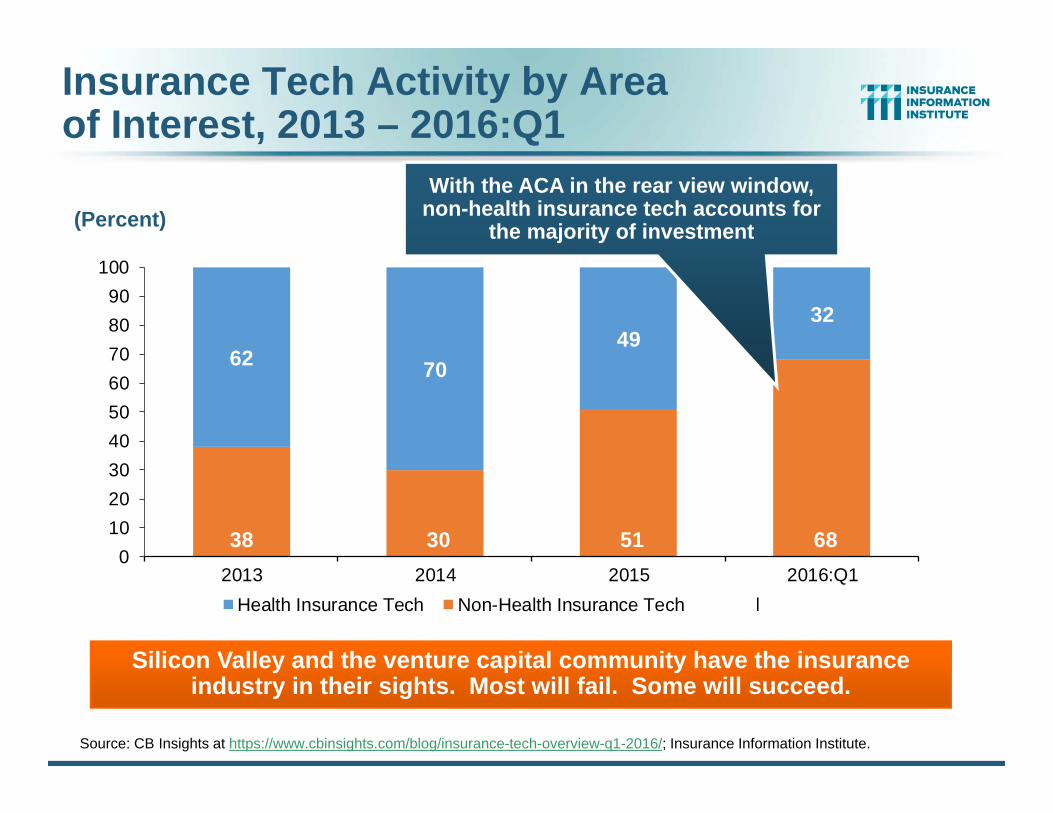

Insurance Tech Activity by Area of Interest, 2013 – 2016:Q1

38 30 51 68

62 7049

32

0102030405060708090

100

2013 2014 2015 2016:Q1Health Insurance Tech Non-Health Insurance Tech Total

Silicon Valley and the venture capital community have the insurance industry in their sights. Most will fail. Some will succeed.

Source: CB Insights at https://www.cbinsights.com/blog/insurance-tech-overview-q1-2016/; Insurance Information Institute.

(Percent)With the ACA in the rear view window,

non-health insurance tech accounts for the majority of investment

www.iii.org

Thank you for your timeand your attention!

Twitter: twitter.com/bob_HartwigDownload at www.iii.org/presentations

Insurance Information Institute Online:

73