The Role of Depositary Receipts - · PDF fileThe Role of Depositary Receipts ... DRs are...

12

GLOBAL TRANSACTION SERVICES INDUSTRY INSIGHT Asia Pacific The Role of Depositary Receipts For Corporate and Institutional Clients

Transcript of The Role of Depositary Receipts - · PDF fileThe Role of Depositary Receipts ... DRs are...

GLOBAL TRANSACTION SERVICES

IND

US

TR

Y I

NS

IGH

T

Asia Pacific

The Role of Depositary ReceiptsFor Corporate and Institutional Clients

2

The role of depositary receiptsValentina Chuang, Depositary Receipt Services, Citi

3

A depositary receipt (DR) program is an effective option for non-UScompanies seeking to undertake global equity offerings. DRs havelong been a popular instrument in worldwide capital markets,particularly where the elimination of custody and cross-border safe-keeping charges are a key concern.

3

25A guide for Chinese companies to listing on the US securities markets

The role of depositary receipts

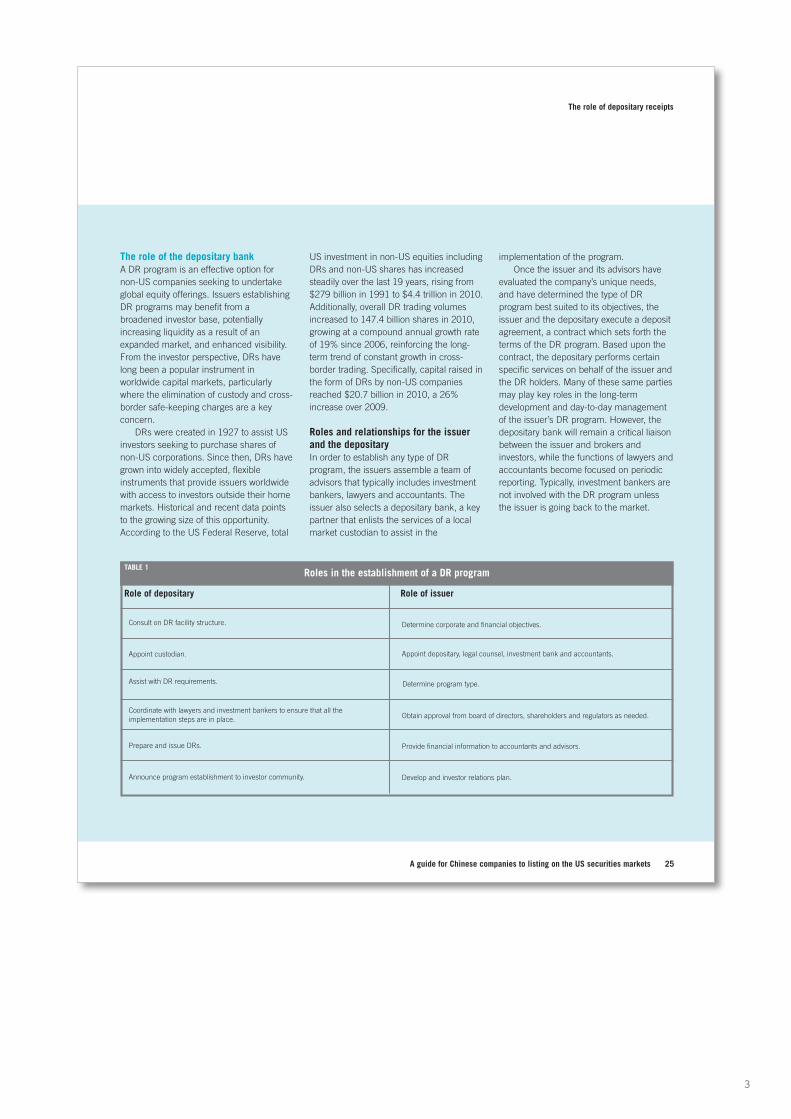

The role of the depositary bankA DR program is an effective option fornon-US companies seeking to undertakeglobal equity offerings. Issuers establishingDR programs may benefit from abroadened investor base, potentiallyincreasing liquidity as a result of anexpanded market, and enhanced visibility.From the investor perspective, DRs havelong been a popular instrument inworldwide capital markets, particularlywhere the elimination of custody and cross-border safe-keeping charges are a keyconcern.

DRs were created in 1927 to assist USinvestors seeking to purchase shares ofnon-US corporations. Since then, DRs havegrown into widely accepted, flexibleinstruments that provide issuers worldwidewith access to investors outside their homemarkets. Historical and recent data pointsto the growing size of this opportunity.According to the US Federal Reserve, total

US investment in non-US equities includingDRs and non-US shares has increasedsteadily over the last 19 years, rising from$279 billion in 1991 to $4.4 trillion in 2010.Additionally, overall DR trading volumesincreased to 147.4 billion shares in 2010,growing at a compound annual growth rateof 19% since 2006, reinforcing the long-term trend of constant growth in cross-border trading. Specifically, capital raised inthe form of DRs by non-US companiesreached $20.7 billion in 2010, a 26%increase over 2009.

Roles and relationships for the issuerand the depositaryIn order to establish any type of DRprogram, the issuers assemble a team ofadvisors that typically includes investmentbankers, lawyers and accountants. Theissuer also selects a depositary bank, a keypartner that enlists the services of a localmarket custodian to assist in the

implementation of the program. Once the issuer and its advisors have

evaluated the company’s unique needs,and have determined the type of DRprogram best suited to its objectives, theissuer and the depositary execute a depositagreement, a contract which sets forth theterms of the DR program. Based upon thecontract, the depositary performs certainspecific services on behalf of the issuer andthe DR holders. Many of these same partiesmay play key roles in the long-termdevelopment and day-to-day managementof the issuer’s DR program. However, thedepositary bank will remain a critical liaisonbetween the issuer and brokers andinvestors, while the functions of lawyers andaccountants become focused on periodicreporting. Typically, investment bankers arenot involved with the DR program unlessthe issuer is going back to the market.

Role of depositary Role of issuer

Roles in the establishment of a DR program

Consult on DR facility structure. Determine corporate and financial objectives.

Appoint custodian. Appoint depositary, legal counsel, investment bank and accountants.

Assist with DR requirements. Determine program type.

Coordinate with lawyers and investment bankers to ensure that all theimplementation steps are in place. Obtain approval from board of directors, shareholders and regulators as needed.

Provide financial information to accountants and advisors.Prepare and issue DRs.

Develop and investor relations plan.Announce program establishment to investor community.

TABLE 1

4

26 A guide for Chinese companies to listing on the US securities markets

The role of depositary receipts

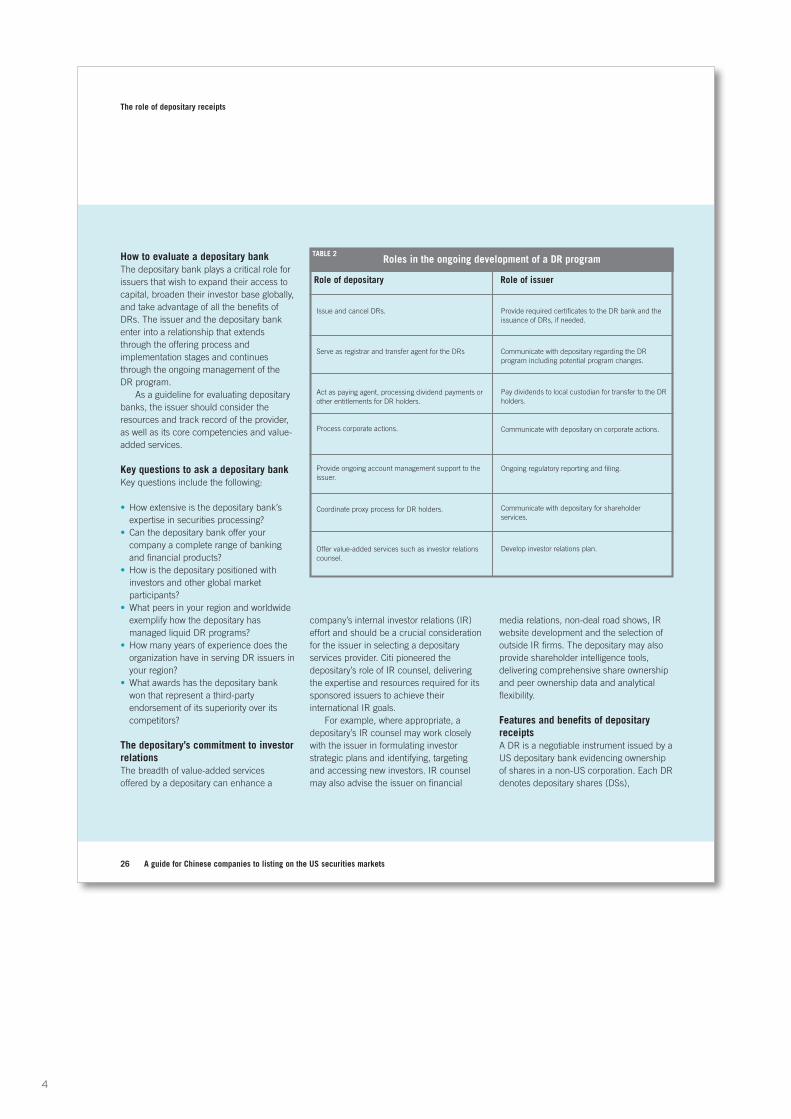

How to evaluate a depositary bankThe depositary bank plays a critical role forissuers that wish to expand their access tocapital, broaden their investor base globally,and take advantage of all the benefits ofDRs. The issuer and the depositary bankenter into a relationship that extendsthrough the offering process andimplementation stages and continuesthrough the ongoing management of theDR program.

As a guideline for evaluating depositarybanks, the issuer should consider theresources and track record of the provider,as well as its core competencies and value-added services.

Key questions to ask a depositary bankKey questions include the following:

• How extensive is the depositary bank’sexpertise in securities processing?

• Can the depositary bank offer yourcompany a complete range of bankingand financial products?

• How is the depositary positioned withinvestors and other global marketparticipants?

• What peers in your region and worldwideexemplify how the depositary hasmanaged liquid DR programs?

• How many years of experience does theorganization have in serving DR issuers inyour region?

• What awards has the depositary bankwon that represent a third-partyendorsement of its superiority over itscompetitors?

The depositary’s commitment to investorrelationsThe breadth of value-added servicesoffered by a depositary can enhance a

company’s internal investor relations (IR)effort and should be a crucial considerationfor the issuer in selecting a depositaryservices provider. Citi pioneered thedepositary’s role of IR counsel, deliveringthe expertise and resources required for itssponsored issuers to achieve theirinternational IR goals.

For example, where appropriate, adepositary’s IR counsel may work closelywith the issuer in formulating investorstrategic plans and identifying, targetingand accessing new investors. IR counselmay also advise the issuer on financial

media relations, non-deal road shows, IRwebsite development and the selection ofoutside IR firms. The depositary may alsoprovide shareholder intelligence tools,delivering comprehensive share ownershipand peer ownership data and analyticalflexibility.

Features and benefits of depositaryreceiptsA DR is a negotiable instrument issued by aUS depositary bank evidencing ownershipof shares in a non-US corporation. Each DRdenotes depositary shares (DSs),

Role of depositary Role of issuer

Roles in the ongoing development of a DR program

Issue and cancel DRs. Provide required certificates to the DR bank and theissuance of DRs, if needed.

Serve as registrar and transfer agent for the DRs Communicate with depositary regarding the DRprogram including potential program changes.

Pay dividends to local custodian for transfer to the DRholders.

Communicate with depositary on corporate actions.

Ongoing regulatory reporting and filing.

Communicate with depositary for shareholderservices.

Develop investor relations plan.

Act as paying agent, processing dividend payments orother entitlements for DR holders.

Process corporate actions.

Provide ongoing account management support to theissuer.

Coordinate proxy process for DR holders.

Offer value-added services such as investor relationscounsel.

TABLE 2

5

27A guide for Chinese companies to listing on the US securities markets

The role of depositary receipts

representing a specific number ofunderlying shares on deposit with acustodian in the issuer’s home market. Theterm “DR” is commonly used to mean boththe physical certificate and the securityitself.

DRs are generally subject to the tradingand settlement procedures of the market inwhich they trade. The different types of DRare frequently identified by the markets inwhich they are available, or the rules andregulations associated with the structures.For example:

• American depositary receipts (ADRs) areDRs that are publicly available toinvestors in the United States; and

• Global depositary receipts (GDRs) areDRs that may be offered to investors intwo or more markets outside the issuer’shome country, usually pursuant to Rule144A and Regulation S (Reg S) under theUS Securities Act of 1933.

DRs can be publicly offered, privatelyplaced or issued pursuant to aninternational offering. The structure of theDR program typically defines the segmentof investors that can purchase thesecurities. In the United States, publiclyoffered securities are available to thebroadest spectrum of investors and tradeeither on a national stock exchange (eg,NASDAQ or the New York Stock Exchange(NYSE)) or in the over-the-counter (OTC)market. GDRs are usually offered toinstitutional investors through a privateoffering, in reliance on exemptions fromregistration under the US Securities Act of1933. These exemptions are Reg S for non-US investors and Rule 144A for USinvestors that are Qualified InstitutionalBuyers (QIBs). QIBs in the United States

include institutions that own and invest atleast $100 million in securities of non-affiliates and registered broker-dealers thatown or invest on a discretionary basis atleast $10 million in securities of non-affiliates. A GDR offering often has a Rule144A component as well as a placement tonon-US investors pursuant to Reg S.

Benefits of a DR program specific toissuers and investors are highlighted inTable 3.

DRs can play a critical role in othertypes of cross-border transaction, such asprivatizations and mergers and acquisitions.

PrivatizationsThe privatization of state-owned assets is animportant undertaking for governmentsworldwide, as countries seek to restructuretheir economies and reduce fiscal deficits.Infrastructure and service enterprises suchas telecommunications, utilities, airlinesand petrochemicals are among thosecommonly targeted for privatization.

DRs have been used successfully bygovernments seeking to privatize state-owned enterprises. Privatizations require asuccessful offering of securities to investors,and DRs provide an effective mechanism

DRs enable issuers to: DRs aid investors by:

Benefits of a DR programTABLE 3

Access capital outside the issuer’s home market. Facilitating diversification into non-US securities.

Build company visibility in the United States and/orinternationally.

Trading, clearing, and settling in accordance with thepractices of the investor’s home market.

Broaden and diversify their shareholder base. Eliminating cross-border custody safe-keeping charges.

Increase opportunities to increase local share prices asa result of global demand/trading.

Enhancing accessibility of research, and of price andtrading information.

Enlarge the market for the company’s shares, potentiallyincreasing liquidity.

Allowing easy comparison to securities of similarcompanies trading in the investor’s home market.

Adjust share price levels to those of peers through a DRratio.

Permitting dividend payments in US dollars andcorporate action processing.

Utilize DRs to facilitate M&A activity through use asacquisition currency.

Enabling uniform proxy and corporate actionprocessing.

Develop stock option plans and stock purchase plansfor employees outside the issuer’s home market.

Providing oppurtunities to move between markets.

6

28 A guide for Chinese companies to listing on the US securities markets

both to increase private ownership and toraise capital overseas.

M&ADRs can enhance the ease of trading andsettlement related to cross-border mergersand acquisitions; they also can facilitate theexecution of corporate actions such aspayments of dividends, structuring of rightsofferings and solicitation of votes. DRsenable issuers to address investor demandswithout the need to build an independentUS shareholder support infrastructure, or tomodify the equity issuance and tradingpatterns of the home market. Types of M&Atransaction that have made successful useof DRs include:

• spin-offs of non-US subsidiaries;• equity-based acquisitions of US business

entities; and • equity-based acquisitions of non-US

business entities.

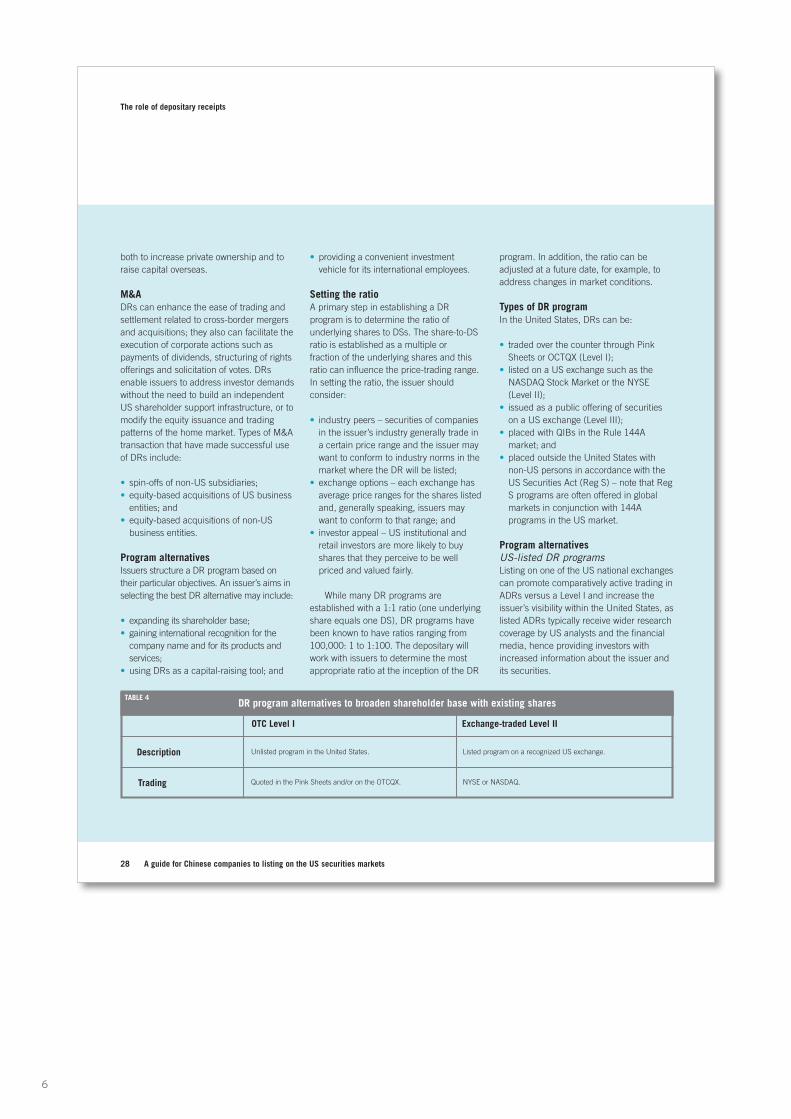

Program alternativesIssuers structure a DR program based ontheir particular objectives. An issuer’s aims inselecting the best DR alternative may include:

• expanding its shareholder base;• gaining international recognition for the

company name and for its products andservices;

• using DRs as a capital-raising tool; and

• providing a convenient investmentvehicle for its international employees.

Setting the ratioA primary step in establishing a DRprogram is to determine the ratio ofunderlying shares to DSs. The share-to-DSratio is established as a multiple or fraction of the underlying shares and thisratio can influence the price-trading range.In setting the ratio, the issuer shouldconsider:

• industry peers – securities of companiesin the issuer’s industry generally trade ina certain price range and the issuer maywant to conform to industry norms in themarket where the DR will be listed;

• exchange options – each exchange hasaverage price ranges for the shares listedand, generally speaking, issuers maywant to conform to that range; and

• investor appeal – US institutional andretail investors are more likely to buyshares that they perceive to be wellpriced and valued fairly.

While many DR programs areestablished with a 1:1 ratio (one underlyingshare equals one DS), DR programs havebeen known to have ratios ranging from100,000: 1 to 1:100. The depositary willwork with issuers to determine the mostappropriate ratio at the inception of the DR

program. In addition, the ratio can beadjusted at a future date, for example, toaddress changes in market conditions.

Types of DR programIn the United States, DRs can be:

• traded over the counter through PinkSheets or OCTQX (Level I);

• listed on a US exchange such as theNASDAQ Stock Market or the NYSE(Level II);

• issued as a public offering of securitieson a US exchange (Level III);

• placed with QIBs in the Rule 144Amarket; and

• placed outside the United States withnon-US persons in accordance with theUS Securities Act (Reg S) – note that RegS programs are often offered in globalmarkets in conjunction with 144Aprograms in the US market.

Program alternativesUS-listed DR programsListing on one of the US national exchangescan promote comparatively active trading inADRs versus a Level I and increase theissuer’s visibility within the United States, aslisted ADRs typically receive wider researchcoverage by US analysts and the financialmedia, hence providing investors withincreased information about the issuer andits securities.

The role of depositary receipts

OTC Level I Exchange-traded Level II

DR program alternatives to broaden shareholder base with existing sharesTABLE 4

Unlisted program in the United States. Listed program on a recognized US exchange.

Quoted in the Pink Sheets and/or on the OTCQX.

Description

Trading NYSE or NASDAQ.

7

29A guide for Chinese companies to listing on the US securities markets

Issuers can also use ADRs to accessinstitutional investors that may beprohibited or limited by their respectivecharters, or by regulation, from investing innon-US securities purchased in the issuer’shome market. US investors may prefer topurchase ADRs rather than shares in theissuer’s home market as the DR securitiestrade, clear and settle according to USmarket conventions.

To list its ADRs in the United States, theissuer must comply with the requirementsof the relevant stock exchange. The issuermust register under the Securities Act andthe Securities Exchange Act of 1934 andfile an initial registration statement andperiodic financial reports. Non-US issuersthat are listing their securities mustreconcile all financial statements to USgenerally accepted accounting principles(US GAAP) or international financialreporting standards (IFRS), as published bythe International Accounting StandardsBoard. Financial reporting for individualbusiness segments need not be reconciledto US GAAP or IFRS. Listing securitiesexempts non-US issuers from complyingwith various state securities regulations.

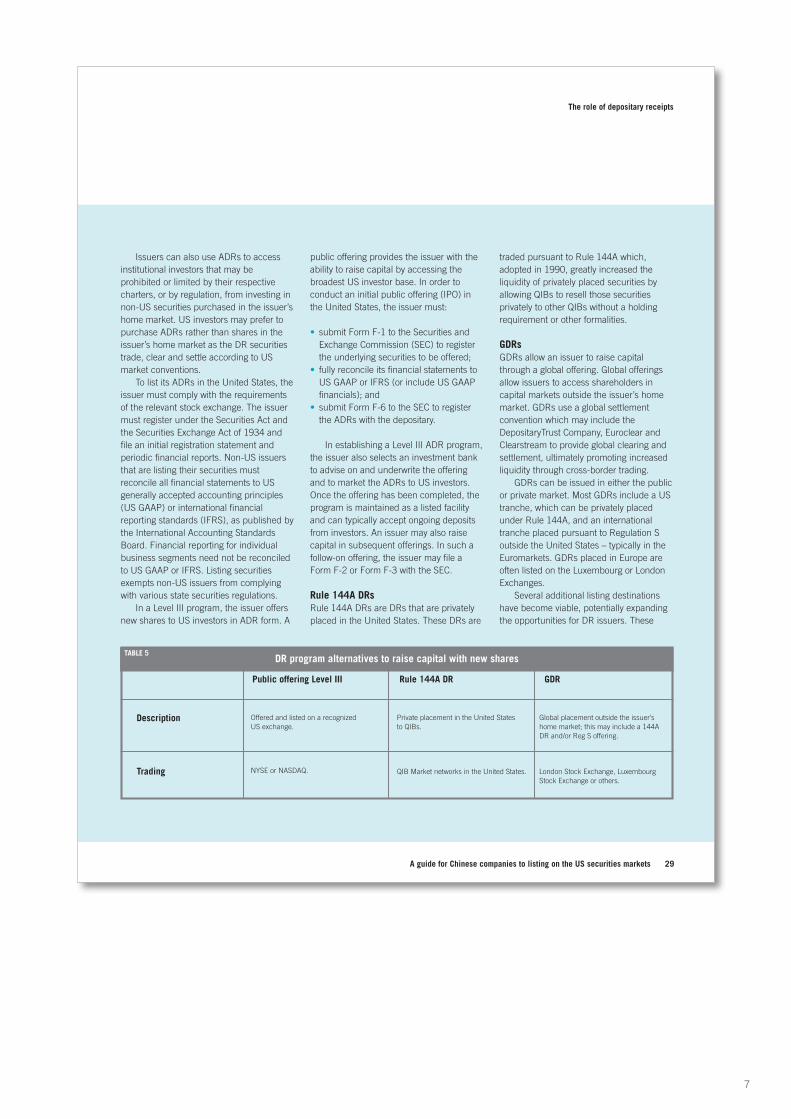

In a Level III program, the issuer offersnew shares to US investors in ADR form. A

public offering provides the issuer with theability to raise capital by accessing thebroadest US investor base. In order toconduct an initial public offering (IPO) inthe United States, the issuer must:

• submit Form F-1 to the Securities andExchange Commission (SEC) to registerthe underlying securities to be offered;

• fully reconcile its financial statements toUS GAAP or IFRS (or include US GAAPfinancials); and

• submit Form F-6 to the SEC to registerthe ADRs with the depositary.

In establishing a Level III ADR program,the issuer also selects an investment bankto advise on and underwrite the offeringand to market the ADRs to US investors.Once the offering has been completed, theprogram is maintained as a listed facilityand can typically accept ongoing depositsfrom investors. An issuer may also raisecapital in subsequent offerings. In such afollow-on offering, the issuer may file aForm F-2 or Form F-3 with the SEC.

Rule 144A DRsRule 144A DRs are DRs that are privatelyplaced in the United States. These DRs are

traded pursuant to Rule 144A which,adopted in 1990, greatly increased theliquidity of privately placed securities byallowing QIBs to resell those securitiesprivately to other QIBs without a holdingrequirement or other formalities.

GDRsGDRs allow an issuer to raise capitalthrough a global offering. Global offeringsallow issuers to access shareholders incapital markets outside the issuer’s homemarket. GDRs use a global settlementconvention which may include theDepositaryTrust Company, Euroclear andClearstream to provide global clearing andsettlement, ultimately promoting increasedliquidity through cross-border trading.

GDRs can be issued in either the publicor private market. Most GDRs include a UStranche, which can be privately placedunder Rule 144A, and an internationaltranche placed pursuant to Regulation Soutside the United States – typically in theEuromarkets. GDRs placed in Europe areoften listed on the Luxembourg or LondonExchanges.

Several additional listing destinationshave become viable, potentially expandingthe opportunities for DR issuers. These

The role of depositary receipts

Public offering Level III Rule 144A DR GDR

DR program alternatives to raise capital with new sharesTABLE 5

Offered and listed on a recognized US exchange.

Private placement in the United States to QIBs.

Global placement outside the issuer’shome market; this may include a 144ADR and/or Reg S offering.

NYSE or NASDAQ. QIB Market networks in the United States. London Stock Exchange, LuxembourgStock Exchange or others.

Description

Trading

8

30 A guide for Chinese companies to listing on the US securities markets

include the Singapore Exchange Limitedand the Dubai International FinancialExchange.

The evolution of regionally specific DRsis evidence of the flexibility of the GDR,allowing issuers to select the investor basethey wish to access and broaden theirshareholder base into new markets. Forexample, an issuer could establish a GDRprogram that targets European, Asianand/or Latin American investors and doesnot offer shares in the United States. Overtime, the GDR program could be enhancedto reach additional markets and investors.

Upgrading a GDR to a publicly listedprogramA non-US company may decide to list itsDRs subsequent to its global Rule 144Aand Regulation S offering. Upgrading froma GDR to a US-listed ADR program is aviable option for companies wishing toachieve greater global reach and visibility.Although the Regulation S tranche easilymay be moved to a listed facility 40 daysafter the Regulation S offer, generally a Rule144A tranche is slightly more challenging.A Rule 144A facility cannot actively coexistwith a US-listed program. In order toupgrade the Rule 144A facility to a listedprogram, the issuer will typically first needto file a Form F-4 registration statementpursuant to the Securities Act. After the F-4registration statement has been filed, aregistered exchange offer with the QIBsmay be undertaken. Under certaincircumstances, and if the Rule 144Aprogram is “seasoned,” the issuer may optfor a private exchange using a certificationprocess rather than a registered exchangeunder the Securities Act.

Issuance and cancellation of DRsBased upon availability and marketconditions, an investor may acquire a DReither by purchasing existing DRs or byconverting shares purchased in the issuer’shome market to DRs. New DRs are issuedsubsequent to the deposit by an investor orbroker of shares with the depositary’s localmarket custodian. The depositary thenissues DRs, which represent the shares ondeposit, to the investor or broker. This isreferred to as an issuance of DRs.

Conversely, an investor may cancel theDRs and sell the underlying ordinary sharesin the relevant home market upon deliveryof the DRs and of cancellation instructionsto the depositary, which in turn cancels theDRs and notifies its custodian to release theunderlying shares according to theinvestor’s instructions. The broker may theneither safe keep or sell the ordinary sharesin the local market.

LiquidityFor many DR market participants, liquidity– the consistent breadth and depth oftrading activity – is considered the bestmeasure for long-term success of a DRprogram. Without the ability to move intoand out of positions of sufficient size,institutions are often reluctant to add thesecurity to their managed portfolios.Likewise, brokers prefer to deal in liquidissues, and both sell-side and buy-sideanalysts prefer to cover liquid securitieswith high standards of financial disclosureproviding an important added protection.Once established liquidity can be facilitatedand maintained through a strong investorIR effort and the resources of the depositarybank and other partners.

The findings of Citi’s “The LiquidityPremium” study (published in 2007 by the

Rutgers University School of Law BusinessLaw Journal) built upon academic researchshowing that firms cross-listed on a USexchange, such as the NYSE or NASDAQ,benefit from, on average, a sustainablevaluation premium of 33% over companiesthat do not cross-list. The Citi studydemonstrated that, on average, companieswith liquid DRs, whether cross-listed ordirect listed, had higher valuations, asmeasured by their price-to-book-valueratios, than those with fewer liquid DRs.

Limited two-way marketSome countries maintain restrictions on there-issuance of DRs. In this limited two-waymarket environment, after withdrawal andsale of ordinary shares from the DR facility,the shares are subject to limitations onredeposit into the DR facility. Deposits may,for example, occur only up to a certainlimit. Once that limit has been reached, theDR facility may be closed for re-issuancepending receipt or required permissions. Incontrast, most countries have an unlimitedor free two-way market, where foreigninvestors may purchase at any time,outstanding ordinary shares in the localmarket for deposit into the DR facility.

Relaxed restrictions may benefit issuersthrough:

• increased possibility for immediateissuance of DRs;

• enhanced liquidity over time – the abilityto issue and cancel the company’s DRspotentially enhances trading activity. Theassociated advantages are higher investordemand and higher valuation;

• decreased risk resulting from lower shareprice volatility – due to larger pool of acompany’s stock, changes in supply and

The role of depositary receipts

9

31A guide for Chinese companies to listing on the US securities markets

demand yield smaller price changes; and • broadened opportunity for non-US

investment in the local market.

A DR premium is the differentialbetween the ordinary share price in thelocal currency and the price of the DR.Historically, when the US marketoutperforms the non-US market, thepremium grows. When the local marketoutperforms the US market, the premiumtypically shrinks. The limited two-waymarket promotes cross-border liquidity upto a point; however, it may not significantlyreduce the size of the DR premium ascompared to an unlimited and two-waymarket.

US securities regulations and DRsIssuers of DRs must comply with theregulations of the markets in which theirDRs are issued. In the United States, theSEC was created as an independent agencyof the US government to enforce federalsecurities laws governing securitiesofferings, trading practices and personsdealing in the securities markets. The SECprotects US investors and US markets byrequiring disclosure of material factsconcerning issuers making public offeringsof securities. The SEC is empowered toissue regulations and enforce provisions ofboth federal securities laws and its ownregulations.

Two key US securities laws with whichDR issuers must comply are the:

• Securities Act of 1933; and• Securities Exchange Act of 1934.

The primary intention of the SecuritiesAct is to provide investors with full and fair

disclosure of material information regardingan issuer in connection with the offer andsale of its securities. The Securities ExchangeAct is different in that its primary intention isto provide investors trading securities in thesecondary market with access to full and fairdisclosure of material information about anissuer on an ongoing basis.

With the arrival of the more stringentregulatory climate in the United States,some DR issuers initially felt a need toreassess the costs compared to the benefitsof their US listings. Many did not see theUS regulatory climate as an obstacle, giventhat most countries have tightened theircompliance rules in recent years. In fact,many equities markets outside the UnitedStates are known to have equally strict, andperhaps even stricter, corporate governancerequirements. Some IR experts argue thatmore stringent standards represent anopportunity for companies to differentiatethemselves. When investors calculate therisk/reward equation, there is a greater“comfort factor” with companies known tohave cleared certain regulatory hurdles.

The SEC noted issuer concernsregarding some of the burdens caused byrecent corporate governance legislation. Forexample, the SEC has applied and iscontinuing to evaluate certain exemptions fornon-US companies from provisions of theSarbanes-Oxley Act. In addition, a series ofreforms came into effect in December 2005impacting the securities offering process inthe United States. These measures areexpected to simplify access to the US capitalmarkets for both US and non-UScompanies, including those issuing DRs.

ConclusionDRs are a winning proposition for globalfinancial markets, benefiting non-USissuers and international investors alike. Forissuers, a DR program can serve tobroaden and diversify a company’sshareholder base, enlarging the market forits shares and potentially increasingliquidity. DRs are attractive to investorsworldwide who are looking to eliminatecross-border custody safe-keeping chargesand enhance the accessibility of researchand price and trading information.

The depositary is a key partner for theissuer, both in establishing a DR programand in developing and managing theprogram on an ongoing basis. The role ofthe depositary in a UK programestablishment includes advising on DRfacility structure, and coordinating withlawyers and investment bankers to ensurethat all implementation steps arecompleted. On an ongoing basis, the criticalrole of the depositary includes issuing DRsand providing ongoing accountmanagement and IR support to the issuer.

A crucial consideration for the issuer inselecting its depositary is the depositary’sexperience and a program of value-addedservices, which should be designed tocomplement the company’s IR effort.

The role of depositary receipts

10

32 A guide for Chinese companies to listing on the US securities markets

Citi’s ADR programs for ChinesecompaniesCiti’s Depositary Receipt Services is themarket leader in China, which is reflectedin the largest number of new listingmandates won in recent years on the backof its service quality and dedicated team onthe ground. In 2010, approximately $5.3billion in capital (for both IPOs and follow-on offerings) was raised in China in DRform. Citi led the way in DR IPOs, raisingmore than $1.9 billion in DR form –capturing 47% of the IPO market share inChina. Its team in Asia provides dedicatedservices to issuers before their offeringlisting, as well as ongoing support after theirlisting. This includes its IR services, whichcomprise training and a range of visibilityprograms that help issuers enhancecommunication with relevant investorgroups in the United States.

Citi’s Depositary Receipt Servicesbusiness has been recognized by The Assetmagazine for seven consecutive years. Mostrecently, Citi was named best ADR bank in2011 and best GDR bank in 2010 by themagazine.

About Citi’s Depositary Receipt ServicesDepositary Receipt Services, a businesswithin Citi Global Transaction Services, is aleader in bringing quality issuers to US andglobal capital markets, and in promotingDRs as an effective capital markets tool. Citibegan offering DRs in 1928 and today iswidely recognized for providing non-UScompanies with access to the powerfulglobal platform Citi has to offer. Forinformation about DRs visitwww.citi.com/adr.

About CitiCiti, the leading global financial servicescompany, has approximately 200 millioncustomer accounts and does business inmore than 160 countries and jurisdictions.Citi provides consumers, corporations,governments and institutions with a broadrange of financial products and services,including consumer banking and credit,corporate and investment banking,securities brokerage, transaction services,and wealth management. Additionalinformation may be found atwww.citigroup.com | Twitter: @Citi |YouTube: www.youtube.com/citi | Blog:http://new.citi.com | Facebook:www.facebook.com/citi | LinkedIn:www.linkedin.com/company/citi.

About Citi’s Global Transaction ServicesGlobal Transaction Services, a division ofCiti’s Institutional Clients Group, offersintegrated cash management, trade, andsecurities and fund services to multinationalcorporations, financial institutions andpublic sector organizations around theworld. With a network that spans more than100 countries, Citi’s Global TransactionServices supports more than 65,000clients. As of the fourth quarter of 2010, itheld $353 billion in liability balances, up4% sequentially, and assets under custodygrew 2% to $12.6 trillion.

Global Transaction Serviceswww.transactionservices.citigroup.com

Information herein is being provided solelyfor information purposes by Citibank, NA.At the time of publication, this informationwas believed to be accurate, but Citi makesno representation or warranty as tocorrectness of the information set forth

above. The above information does notconstitute a recommendation, solicitation oroffer by Citi for the purchase or sale of anysecurities, nor shall this material beconstrued in any way as investment or legaladvice or a recommendation, reference orendorsement by Citi.

© 2011 Citibank, NA All rights reserved.Citi and Arc Design are service marks ofCitigroup Inc, or its affiliates, used andregistered throughout the world.

The role of depositary receipts

11

For more information about Citi’s Depositary Receipt Services, please visit www.citi.com/dr.

Valentina ChuangDirector, Regional HeadTel: +852 2868 [email protected]

Geoffrey TangVice President, Sales and Account Manager Head, ASEAN, Hong Kong and KoreaTel: +852 2868 [email protected]

Sophie ZhangSenior Vice President, Sales and Account Manager Head, ChinaTel: +86 21 2896 [email protected]

May ZhangVice President, Sales and Account Manager, ChinaTel: +852 2868 [email protected]

Abhishek AgarwalVice President, Sales and Account Manager, IndiaTel: +91 22 4029 6205 [email protected]

Naomitsu AbeVice President, Sales and Account Manager, JapanTel: +81 3 6270 [email protected]

Terry YangDirector, Sales and Account Manager, TaiwanTel: +886 2 8726 [email protected]

Regional

China

India

Japan

Taiwan

Contact our dedicated team of professionals for all your depositary receipts needs.

Global Transaction Services Asia Pacific — September 2011© 2011 Citibank, N.A. All rights reserved. Citi and Arc Design is a trademark and service mark of Citigroup Inc., used and registered throughout the world.

CTA4019

![[Deutsche Bank] Depositary Receipts Handbook](https://static.fdocuments.net/doc/165x107/577d2f891a28ab4e1eb1fe3f/deutsche-bank-depositary-receipts-handbook.jpg)