the Role of Contingent Convertible Bond in Capital...

71

the Role of Contingent Convertible Bond in Capital Structure Decisions A master thesis by Weikeng Chen [401248] MSc. Finance and International Business Supervisor: Peter Løchte Jørgensen Department of Economics and Business Summer 2012 Aarhus University Business and Social Science

Transcript of the Role of Contingent Convertible Bond in Capital...

the Role of Contingent Convertible Bond

in Capital Structure Decisions

A master thesis by

Weikeng Chen [401248]MSc. Finance and International Business

Supervisor: Peter Løchte JørgensenDepartment of Economics and Business

Summer 2012Aarhus University

Business and Social Science

The Role of Contingent Convertible Bond

in Capital Structure Decisions

Weikeng ChenAarhus University

Abstract

The financial crisis has exposed flaws in the regulation of capital positionsof large financial institutions. When they get financially distressed, governmentregulators are implicitly forced to provide extensive amount of liquidity infu-sion, which usually causes a lot of public controversy. This paper develops anew derivative security, Contingent Convertible Bond, which is a debt instru-ment that automatically converts to equity if the issuing institution reaches apre-specified level of financial distress. This kind of “debt-to-equity swap” or au-tomatic bail-in is highly advantageous to the institution when it gets distressed,since raising new equity at this time has very high cost and makes it unfeasible.In this paper, we derive close-form formula for the market value of this securi-ty when the institution’s assets are modeled as a Geometric Brownian Motionprocess and its conversion trigger is set as a threshold of asset value. Our calibra-tion results show that, the introduction of Contingent Convertible Bond into thecapital structure can reduce the institution’s default probability and effectivelymitigate the management’s risk shifting motivation.

Keywords: Contingent Convertible Bond, Capital Structure, FinancialStability, Structural Model, Close-form Solution

CONTENTS i

Contents

1 Introduction 1

2 Literatures 32.1 Conversion trigger of contingent capital . . . . . . . . . . . . . . . . . 32.2 Existing research on contingent capital . . . . . . . . . . . . . . . . . . 52.3 Comparison between CoCo Bond Models with asset trigger . . . . . . 6

2.3.1 Similarities across 3 models . . . . . . . . . . . . . . . . . . . . 72.3.2 Differences across 3 models . . . . . . . . . . . . . . . . . . . . 8

3 Models 113.1 Asset Dynamics . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11

3.1.1 Girsanov Theorem . . . . . . . . . . . . . . . . . . . . . . . . . 113.1.2 Real World and Risk-Neutral World . . . . . . . . . . . . . . . 133.1.3 Absence of Arbitrage and Asset Equation . . . . . . . . . . . . 143.1.4 Definition of variables, functions and expectations . . . . . . . 15

3.2 Benchmark Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 173.2.1 Security Design and Assumptions . . . . . . . . . . . . . . . . . 173.2.2 Asset Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . 183.2.3 Valuation of claims . . . . . . . . . . . . . . . . . . . . . . . . . 19

3.3 Debt-Equity Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 203.3.1 Security Design and Assumptions . . . . . . . . . . . . . . . . . 203.3.2 Asset Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . 223.3.3 Valuation of claims . . . . . . . . . . . . . . . . . . . . . . . . . 22

3.4 Subordinate Debt Model . . . . . . . . . . . . . . . . . . . . . . . . . . 273.4.1 Security Design and Assumptions . . . . . . . . . . . . . . . . . 273.4.2 Asset Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . 283.4.3 Valuation of claims . . . . . . . . . . . . . . . . . . . . . . . . . 29

3.5 CoCo Bond Model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 353.5.1 Security Design and Assumptions . . . . . . . . . . . . . . . . . 363.5.2 Asset Equation . . . . . . . . . . . . . . . . . . . . . . . . . . . 373.5.3 Valuation of claims . . . . . . . . . . . . . . . . . . . . . . . . . 38

4 Calibration 434.1 Default Probability . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 43

4.1.1 Mathematical derivation . . . . . . . . . . . . . . . . . . . . . . 444.1.2 Calibrating the models . . . . . . . . . . . . . . . . . . . . . . . 49

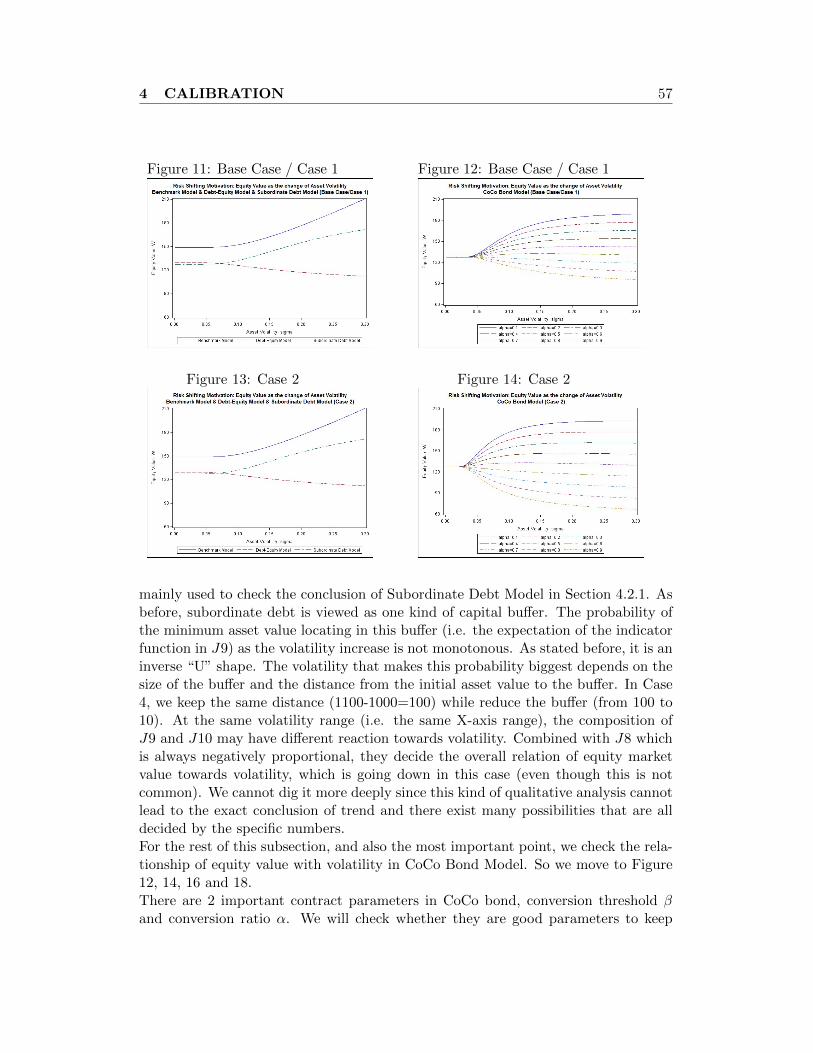

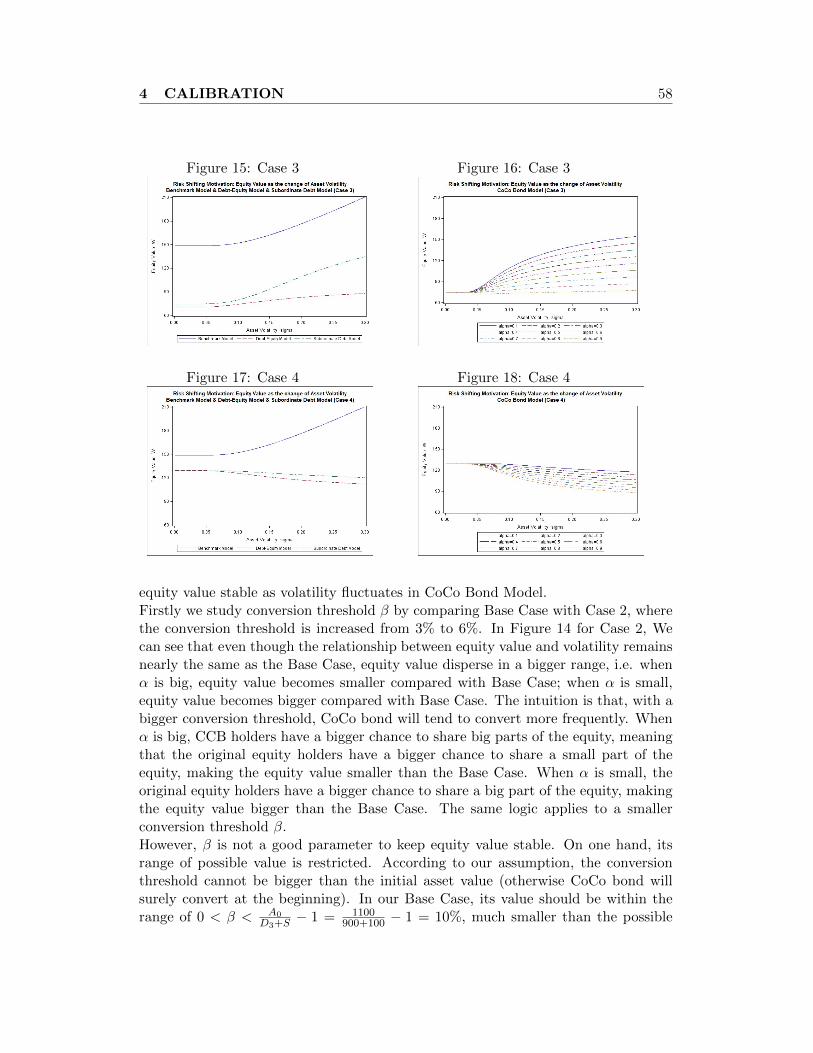

4.2 Risk Shifting Motivation . . . . . . . . . . . . . . . . . . . . . . . . . . 524.2.1 Mathematical derivation . . . . . . . . . . . . . . . . . . . . . . 534.2.2 Calibrating the models . . . . . . . . . . . . . . . . . . . . . . . 55

5 Extensions 605.1 Endogenous coupon rates . . . . . . . . . . . . . . . . . . . . . . . . . 605.2 Endogenous value paid-out rate . . . . . . . . . . . . . . . . . . . . . . 62

CONTENTS ii

6 Summary 65

7 Reference 66

8 Appendix 688.1 Prove the basic properties of GBM . . . . . . . . . . . . . . . . . . . . 688.2 Derive the explicit formula of H function . . . . . . . . . . . . . . . . . 698.3 Derive an intermediate formula (40) . . . . . . . . . . . . . . . . . . . 738.4 Valuation of European call option . . . . . . . . . . . . . . . . . . . . . 748.5 Prove Equation (68) . . . . . . . . . . . . . . . . . . . . . . . . . . . . 758.6 Valuation of decompositions in Debt-Equity Model . . . . . . . . . . . 778.7 Valuation of down-and-in call barrier option . . . . . . . . . . . . . . . 788.8 Valuation of decompositions in Subordinate Debt Model . . . . . . . . 818.9 Valuation of decompositions in CoCo Bond Model . . . . . . . . . . . 82

1 INTRODUCTION 1

1 Introduction

The 2007-2009 financial crisis exposed flaws in the regulation of capital positions oflarge financial institutions (LFIs), especially big banks. The architecture governingthe financial insolvency of banks and other financial institutions needs a particularexamination. The insolvency and bankruptcy of these institutions might cause social-ly vital disruptions in the overall financial system. In order to prevent the possibleconsequence, the government regulators are forced to provide extensive amount ofimplicit guarantees when they get financially distressed, which usually take the formof outright infusion of taxpayer money to enrich their capital position. This is the socalled “Too Big To Fail” (TBTF) problem and the need for government bailout bringsa huge social cost. Facing this problem, government regulators need to put forwardsome strict proposals to improve the prudential bank regulation. However, moreimportantly, banks themselves should ensure that they have enough loss-absorbingcapital as buffer and they can internalize the losses when they get financially dis-tressed, in order to preclude a big dependence on the public bailout.To solve this problem, enhancing the bank’s financial stability by optimizing itscapital structure would be a good perspective. Some innovative and well-designedderivative securities could help to internalize the bank’s possible losses during thefinancial crisis. Among the possible choices, Contingent Convertible Bond (CoCobond, CCB), one kind of contingent capitals, would be a good derivative securitythat is potentially beneficial to the enhancement of the financial stability.Contingent Convertible Bond is a debt instrument that automatically converts toequity if the issuing bank reaches a pre-specified level of financial distress (calledconversion trigger). This derivative is issued as debt and it can enjoy the debt ben-efit of tax deduction before conversion. When a distress-related trigger is breached(usually due to the depletion of capital during a financial crisis), CoCo bond willmandatorily convert into common equity to enrich its capital position. This kind of“debt-to-equity swap” or automatic bail-in is highly advantageous to the bank whenit gets distressed, because raising new equity to enrich its capital position, anotherbail-in procedure instead, has very high cost in distress times and makes it unfeasible.So CoCo bond can be viewed as another type of capital buffer for big banks withdefault risk. It precludes the need of external government bail-out, which usuallycauses a lot of public controversy.This innovative derivative security was proposed by Flannery (2005) and the follow-ing researches extend the analysis and construct financial models for quantitativevaluation. However, regarding CoCo bond’s conversion design, equilibrium pricingand possible influence on bank’s capital structure, it still remains at an early researchstage and seems far from reaching a consensus. There are already some attempts inreal financial world. For example, Lloyd’s bank issued the first £7 billion ($11.6 bil-lion) CoCo bonds in 2009. However, as a newly emerging security, the number of realworld cases is very limited and thus the real world data is far from sufficient to testthe theoretical model. Facing this kind of data restriction, usually researchers willcalibrate the model with some well approximated parameters to see its application

1 INTRODUCTION 2

in the capital structure decision, which is also what we conduct in our empirical partafter introducing the models.Undoubtedly, different designs of the underlying assets and the contractual terms ofCoCo bond would lead to totally different models with different valuation methods,sometimes even with slightly different conclusions. In this paper, we construct a Co-Co Bond Model and present a close-form solution for the CoCo price and all otherbank claims (senior debt, subordinate debt, equity). It utilizes the outcomes fromsome of the existing models as well as makes some important improvements in thedesign of contractual terms. The existing research and our improvements will beexplained more in detail in Section 2.For a brief description of our CoCo Bond Model, the asset dynamics follow the com-mon Geometric Brownian Motion (GBM) process. We assume both the corporatesenior debt and CoCo bond have continuous coupon payment and finite maturity, adesign character that makes CoCo bond feasible and implementable in real financialmarket. The market values of all claims in our model have been successfully derivedwith close-form formula. Some other model elements such as dividend payment,possible bankruptcy cost, default probability, risk shifting motivation, etc. are alsocovered in this paper.The derivation of close-form formula is very important in derivative valuation. With-out explicit solutions, the common data simulation methods (such as Monte Carlosimulation) have very low efficiency in converging to the real number if the derivativeis complicatedly designed. Besides, close-form formula makes our comparative staticanalysis much easier and time-efficient.Models construction is the core of this paper. We begin from a Benchmark Model, theclassic Black-Scholes-Merton model of debt and equity valuation. The model frame-work and research methodology inspire us to construct other models, either by addinganother security into the capital structure, or by loosening some strict assumptions.Besides, conclusion from Benchmark Model, especially the equity-volatility relation-ship, is where the traditional and classical theory comes from and thus it is worthour attention.In order to see the role of CoCo bond in enhancing the financial stability, under theframework of Benchmark Model, we construct another 2 supporting models. Debt-Equity Model considers a capital structure with corporate debt and equity, the sameas Benchmark Model. However, many assumptions from the Benchmark Model havebeen loosened. This model is the template and basis for models with more securitiesin the capital structure. Its conclusion can be used to compare with our core model,CoCo Bond Model, to see whether it is beneficial to add CoCo bond into the capitalstructure. Another supporting model is Subordinate Debt Model. Also for compar-ison purpose, we construct this model with another debt instrument, subordinatedebt, which is used to directly “compete” with CoCo bond. So there are 4 modelsin total in our paper, 3 supporting models and a core model, CoCo Bond Model.Quantitative analysis by data calibration is performed for all 4 models, and the roleof CoCo bond is clearly displayed after the comparison.The rest of this paper is organized as follows. Section 2 examines the recent research

2 LITERATURES 3

findings and compares our CoCo Bond Model with models in 2 published papers.Section 3 presents our 4 models, each beginning from the security assumptions, thenthe valuation of all claims, and ending with the mathematical formulas. Section 4tests the advantage of CoCo bond quantitatively from 2 perspectives, default proba-bility and risk shifting motivation, by data calibration. Some extensions for the CoCoBond Model are provided in Section 5. It provides more choices and inspiring whendesigning CoCo bond in real world. Section 6 summarizes. Detailed calculationsleading to our valuation formulas are deferred to Appendix.

2 Literatures

2.1 Conversion trigger of contingent capital

Regarding the design of contingent capital, there exist a list of issues that need to besettled before implementation. Detailed proposals can refer to Flannery (2009) andMcDonald (2010). Here we just provide the most important design characteristic ofthe contingent capital: the setting of distress-related conversion trigger.Conversion trigger is widely discussed in the literatures of contingent capital. Typeof conversion trigger should be clearly determined no later than the issuance of con-tingent capital. When the trigger is reached, the conversion should be conductedmandatorily and automatically. Until now, it does not have a consensus regardingwhich should be chose as conversion trigger. For different considerations, there existdifferent types of triggers.We briefly list the conversion triggers that have been discussed and utilized in ex-isting literatures. We will not give a detailed explanation about the advantage anddisadvantage for each type of trigger as many papers have covered. Interested readerscan refer to the corresponding literatures for a deeper study.Conversion triggers in the current research can be classified into 3 types:

1. A systemic event which will make a big influence on the banking system as awhole, for example, the financial crisis which can be observed and measured bysome kind of market index, some big changes of banking supervision regulation,etc. Related research can refer to Kashyap, Rajan and Stein (2008).

2. The trigger related to the individual LFI. This is the most common type inliterature. This type of trigger includes the following financial indicators.

- Capital ratio of LFI. This is one of the most important risk ratios of LFI.It can take the form of either equity to debt value, or equity to assetvalue. Debt value and asset value are both unique; however we have 2choices for equity value: book value of equity and market value of equity.Accordingly, there exist both book capital ratio and market capital ratio.Their advantages and disadvantages will be analyzed more in detail below.In literature, for example, Flannery (2005) suggested a capital ratio basedon the market value of the bank’s equity. However, Glasserman and Nouri(2010) developed a model with a capital-ratio trigger based on book value.

2 LITERATURES 4

- Underlying asset value of LFI. Utilizing this trigger will make the analysistractable and remove the possibility of multiple equilibriums. Relatedresearch can refer to Raviv and Hilscher (2011) and Albul, Jaffee andTchitsyi (2010). In our paper, we also choose it as the conversion trigger.

- Share price of LFI. Obviously this is another market value indicator. Re-lated research can refer to Glasserman and Wang (2009).

3. The combination of 2 or more indicators. One example is a trigger based on thehealth of both an individual bank and the financial system, suggested by SquamLake Working Group (2009). Another example can be referred to McDonald(2010).

As above, according to which kind of equity value we use, there are 2 types of capitalratios for LFI: book capital ratio and market capital ratio. Market value of equityis based on the market price of the LFI’s stock. Book value of equity is based onregulatory accounting measures of debt and capital. It is also called regulatory value,or accounting value. In research, it will be the residual of asset value after deductingthe value of all kinds of debt.In current literatures, there are many discussions regarding the advantage and dis-advantage of using the book value or market value indicators. Since the discussionappears in many literatures, here we just list the general points in the literatureswithout detailedly pointing out their origin. Note that, the disadvantage of one typeof indicator may construct part of the reason why we may use the other type, viceversa.Using the book value indicators:

- Advantage: Existing regulatory capital requirements for LFIs are based pri-marily on book values.

- Advantage: Existing issuances of contingent capital to date all use triggersbased on regulatory values rather than market prices.

Using the market value indicators:

- Advantage: It is continuously updated with the newest information and reactssensitively to any market shock.

- Advantage: It is forward-looking and thus it can reveal any potential shock andshow the market and the investors’ expectation.

- Disadvantage: Market values could potentially be manipulated to trigger con-version.

- Disadvantage: Market value indicators may result in multiple solutions or nosolution for the market price of the contingent capital. This leads to the problemof the viability of contracts designed with market-based triggers. Sundaresanand Wang (2010) have a wonderful explanation for this point.

2 LITERATURES 5

2.2 Existing research on contingent capital

Before the model section, we provide a brief overview of the literatures on contingentcapital until now.The original proposal and idea of contingent capital was pioneered by Flannery.Flannery (2005) proposed a new financial security for LFIs, called reverse convertibledebentures. It is a form of debt that converts to equity if the institution’s capitalratio falls below a threshold. His proposal utilized a capital ratio based on the marketvalue of the bank’s equity, a feature that may cause multiple equilibriums or even noequilibrium, proved later by Sundaresan and Wang (2010). Flannery (2009) extentthis proposal and considered how it could be implemented in real financial market.In this proposal, he renamed it as Contingent Capital Certificates (CCC). Kashyap,Rajan and Stein (2008) proposed a custodial account, i.e. a “lock box” to hold bankfunds that would be released if an event, usually, one kind of crisis, happens overthe life of the policy. It would resemble an investment in a defaultable “catastro-phe” bond. The trigger is a systemic event, rather than the risk of the individualinstitution. Instead, the Squam Lake Working Group (2009) recommended a triggerthat based on the risk condition of both an individual bank and the banking systemas a whole. Glasserman and Wang (2009) studied the convertible securities designedby the US Treasury for its Capital Assistance Program. They suggested this kindof security can be viewed as a type of contingent capital in which banks hold theoption to convert preferred shares to common equity and the trigger can be set astheir share price.Other literatures regarding the design of contingent capital lead to model construc-tion and quantitative valuation. Some models can achieve close-form solution, i.e.explicit formula for the pricing of contingent capital and other banking claims, whileothers need to utilize some kinds of data simulation to do the valuation. McDonald(2010) got the value of contingent capital with a dual trigger through joint simulationof a bank’s share price and one kind of market index. Pennacchi (2010) developed astructural credit risk model of a bank that issued fixed or floating coupon bonds inthe form of contingent capital. The return on the bank’s assets is simulated to followa jump-diffusion process, and default-free interest rates are stochastic. Raviv andHilscher (2011) obtained closed-form pricing formula under the assumption that theconversion trigger is set by a threshold level of assets and both debts take the form ofzero-coupon deposit. They priced each banking claim by replicating its payoff usinga combination of different barrier options that all have closed form solution. Albul,Jaffee and Tchitsyi (2010) also used an asset-level trigger and obtained closed-formformula by assuming that all debts have infinite maturity. Glasserman and Nouri(2010) developed a model with a capital-ratio trigger based on book value of equi-ty. Different from the conversion process in other literatures, which is one-time andcomplete conversion, their model suggested a conversion mechanism that convertsjust enough contingent capital to meet the capital requirement each time a bank’scapital ratio reaches the threshold. Sundaresan and Wang (2010) proved that settingthe conversion trigger at a level of share price may lead to multiple solutions or no

2 LITERATURES 6

solution for the market price of contingent capital, raising questions about the fea-sibility of contracts designed with market-based triggers. Their research cast doubton the proposal suggested by Flannery, who recommended a capital ratio based onthe market value of the bank’s equity.Remaining researches proposed other methods to improve LFI’s capital position dur-ing a financial crisis. Those proposals usually take the form of either some guidingregulations, or suggestions of some innovative securities or security combination. Forexample, Duffie (2010) proposed the mandatory offering of new equity by banks whenthey face financial crisis and their capital position deteriorates. As opposed to theconversion of debt to equity, a mandatory rights offering provides new cash that mayreduce the risk of a liquidity crisis. Hart and Zingales (2010) designed a new, imple-mentable capital requirement for LFIs which ensures that LFIs are always solvent,while preserving some of the disciplinary effects of debt. Their mechanism requiredthat LFIs should maintain a sufficiently large equity cushion. If the CDS (Credit De-fault Swap) price goes above the threshold, the LFI regulator forces the LFI to issueequity until the CDS price moves back down. Pennacchi, Vermaelen and Wolff (2010)proposed a new security, the Call Option Enhanced Reverse Convertible (COERC).The security is a form of contingent capital, but at the same time, equity holdershave the option to buy back the shares from the bondholders at the conversion price.Compared to other forms of contingent capital proposed in the literature, the COER-C is less risky in a world where bank assets can experience sudden and large declinesin value.Among the existing literatures, our paper can be categorized into the type of litera-tures which lead to model construction and quantitative valuation. Similar to Ravivand Hilscher (2011) and Albul, Jaffee and Tchitsyi (2010), the conversion trigger inour model is also set as a threshold level of asset value. We make improvements byloosening some calculation-simplified assumptions in the above models, which makesthe security more implementable in real financial world. Our model also leads toclose-form solution for the valuation of each claim. In the next subsection, we willintroduce the similarities and differences between our model and the above 2 modelsmore in detail, from each model’s security design, the reason why they design in thisway, to the logic of mathematical derivation under each model. The comparison alsoguides the readers into our model construction gradually and implicitly explains whywe design the model in this way and its significance.

2.3 Comparison between CoCo Bond Models with asset trigger

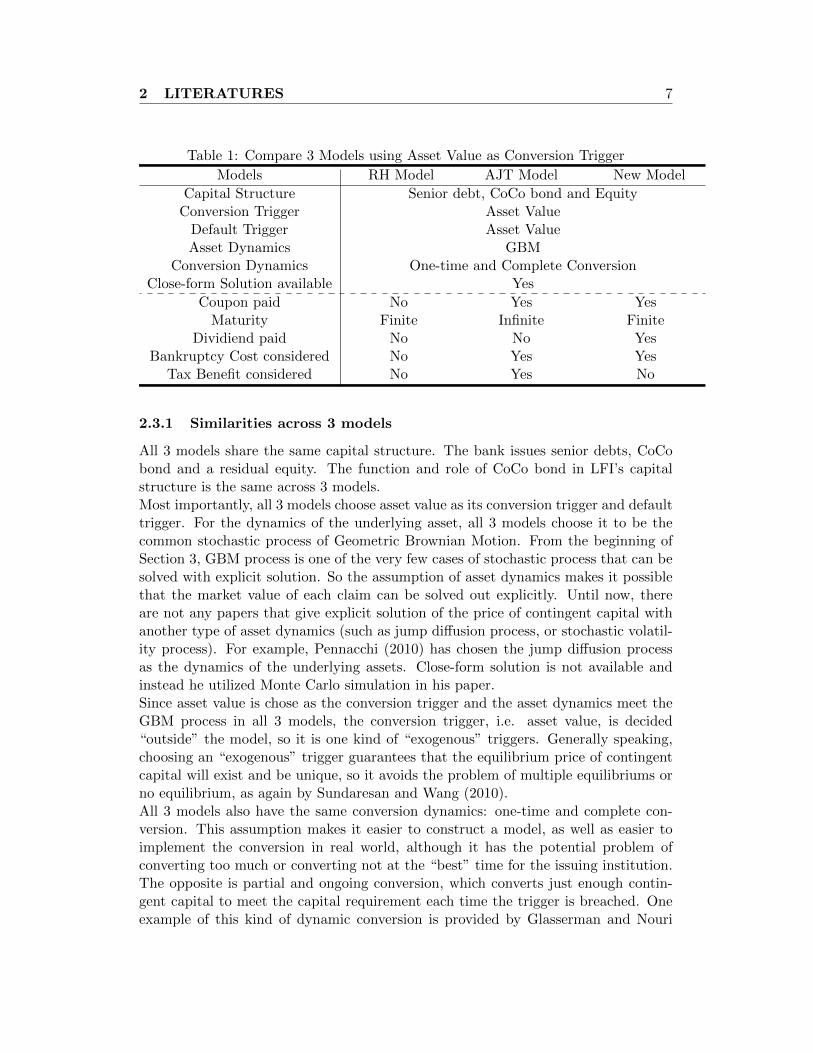

To introduce our model gradually, we describe and compare 2 CoCo Bond Modelswith our model. 3 models all choose the asset value as conversion trigger. As isexplained before, using asset value as conversion trigger makes the analysis tractableand removes the possibility of multiple equilibriums. The comparison of 3 modelscan be clearly shown in Table 1.

2 LITERATURES 7

Table 1: Compare 3 Models using Asset Value as Conversion Trigger

Models RH Model AJT Model New Model

Capital Structure Senior debt, CoCo bond and EquityConversion Trigger Asset Value

Default Trigger Asset ValueAsset Dynamics GBM

Conversion Dynamics One-time and Complete ConversionClose-form Solution available Yes

Coupon paid No Yes YesMaturity Finite Infinite Finite

Dividiend paid No No YesBankruptcy Cost considered No Yes Yes

Tax Benefit considered No Yes No

2.3.1 Similarities across 3 models

All 3 models share the same capital structure. The bank issues senior debts, CoCobond and a residual equity. The function and role of CoCo bond in LFI’s capitalstructure is the same across 3 models.Most importantly, all 3 models choose asset value as its conversion trigger and defaulttrigger. For the dynamics of the underlying asset, all 3 models choose it to be thecommon stochastic process of Geometric Brownian Motion. From the beginning ofSection 3, GBM process is one of the very few cases of stochastic process that can besolved with explicit solution. So the assumption of asset dynamics makes it possiblethat the market value of each claim can be solved out explicitly. Until now, thereare not any papers that give explicit solution of the price of contingent capital withanother type of asset dynamics (such as jump diffusion process, or stochastic volatil-ity process). For example, Pennacchi (2010) has chosen the jump diffusion processas the dynamics of the underlying assets. Close-form solution is not available andinstead he utilized Monte Carlo simulation in his paper.Since asset value is chose as the conversion trigger and the asset dynamics meet theGBM process in all 3 models, the conversion trigger, i.e. asset value, is decided“outside” the model, so it is one kind of “exogenous” triggers. Generally speaking,choosing an “exogenous” trigger guarantees that the equilibrium price of contingentcapital will exist and be unique, so it avoids the problem of multiple equilibriums orno equilibrium, as again by Sundaresan and Wang (2010).All 3 models also have the same conversion dynamics: one-time and complete con-version. This assumption makes it easier to construct a model, as well as easier toimplement the conversion in real world, although it has the potential problem ofconverting too much or converting not at the “best” time for the issuing institution.The opposite is partial and ongoing conversion, which converts just enough contin-gent capital to meet the capital requirement each time the trigger is breached. Oneexample of this kind of dynamic conversion is provided by Glasserman and Nouri

2 LITERATURES 8

(2010).Different from the attempt of “using other stochastic process than GBM process”,which makes it nearly impossible to get a close-form solution, the assumption of“partly conversion” can lead to close-form solution after a slightly more complicatedcalculation. The model by Glasserman and Nouri has successfully done it.

2.3.2 Differences across 3 models

More importantly, we need to overview the different designs across 3 models, whichshow the improvements we have made in our model. In brief, the improvement workfocuses mainly on the loosening of 2 assumptions of bond design, zero-coupon as-sumption for RH Model and infinite maturity assumption for AJT Model. Naturally,coupon payment and bond maturity will be the concentration of the following anal-ysis.

RH ModelWe call the CoCo Bond Model developed by Raviv and Hilscher (2011) as RH Modelfor short. In RH Model, the senior debt takes the form of zero-coupon deposit. Nodividend is distributed to the equity holder during the maturity. This means thatthere are no cash outflows before the maturity. If we use Expression (13) in Section3 to describe the dynamics of underlying assets under Q-measure, in this model wehave δ = 0 and the drift of the underlying assets is equal to the risk free interest rater.Without coupon payment, the only way for senior debt holder (deposit holder here)to realize value from their investment is the payment at maturity, so in this model,the maturity should be finite. Otherwise the senior debt holders get nothing if theirlife span is smaller than infinite.Without coupon payment, it is not possible to consider the tax-saving benefit. Taxbenefit takes a form of tax saving for the debt interest the banks pay out during theyear. In RH Model, banks do not pay out any coupons during the maturity, so thereis no tax benefit and thus it is not considered.In RH Model, bankruptcy cost is also not covered. This simplification does not inline with most structural models in literature, and we will make the correction in ourmodel.Because of the assumption of no coupon payment and no bankruptcy cost, the valu-ation of 3 banking claims (senior debts, CoCo bond and equity) is simplified. Theyprice each claim by replicating its payoff using a combination of different barrier op-tions that all have closed form solution. So the close-form solution of each claim iseasily calculated. Note that all the barrier options they use to replicate the bankingclaims are the type of “down” barrier option (down-and-in option or down-and-outoption), because by assuming the initial asset value larger than the conversion trig-ger, the CoCo bond will converse only when the asset value falls down and hits thetrigger.To save space, we will not list their pricing formulas here. It is easily checked in their

2 LITERATURES 9

paper.

AJT ModelWe call the CoCo Bond Model developed by Albul, Jaffee and Tchitsyi (2010) as AJTModel for short. AJT Model calls senior debt as straight bond or straight debt. It isjust a matter of denomination and its role is exactly the same as senior debt in ouranalysis. In AJT Model, both straight bond and CoCo bond are consol type, meaningthey are annuities with infinitive maturity. Straight bond pays coupon continuallyin time until default. At default, fraction α of the bank’s assets is lost. CoCo bondpays coupon continually in time until it hits the conversion trigger. The amounts ofboth coupon payments are constants and they are decided exogenously.Since both bonds pay coupon continuously in time before the maturity, it is possibleto assume that the bonds’ maturity is infinite (not necessarily though, such as ourmodel), i.e. one kind of annuities. The payoffs of both bonds are taking the formof continuously paying coupons. They have a final payment only when it defaults orconverses.Although not common in real world, this assumption also simplifies the pricing cal-culation. To calculate the present value of coupon payment, it is always easier whenthe maturity is infinite. As in Section 3, both stopping times (conversion time anddefault time) are always finite (P(τ = +∞) = 0). So when the maturity is infinite,CoCo bond will always covert before the maturity, and the bank will always defaultbefore the maturity, meaning that there is just one possibility to be considered in thevaluation. If the maturity is finite as in our model, we need to figure out differentpossibilities regarding the comparison of stopping time and maturity. The calculationof the present value of coupon payment with infinite maturity is somewhat similar towhat we calculate for the present value of the annuity (interest paid out each perioddivided by interest rate).Besides, we always need to consider the final payment when default or conversionhappens, which is a certain event because the maturity is infinite. This kind of u-nique possibility also simplifies the calculation.Because of the payment of continuous coupon, the parameter of cash outflow δ is notequal to 0 in this model, meaning that the drift of underlying assets under Q-measurewill be smaller than r (it will be r−δ). They call it µ in their paper. The exact valueof δ (and thus µ) is needed because it decides both stopping times. In AJT Model,its value is exogenously decided. In their paper, they do not consider dividend ofequity.Different from RH Model, AJT Model considers bankruptcy cost. As in the generalliterature, it is set as a constant proposition of the asset value when it hits the defaulttrigger. In their model, bankruptcy cost will always be positive because, as before,default trigger will always be reached with an infinite maturity.Besides, they also consider tax benefit in their model. As before, tax benefit is thetax deduction for paid debt interest during the year. In general literature, it is alwaysset as a constant fraction of the coupon paid out (it is the exogenously decided θ intheir paper). So the amount of tax benefit is easily got after the valuation of both

2 LITERATURES 10

coupons is calculated.From the above analysis, we can get the conclusion that, in order to get the close-form solution, both models have made some strict assumptions. In RH Model, theyassume that the senior debt takes the form of zero-coupon deposit. However, ingeneral structural models, we always assume the bonds pay coupons, continuouslyor discreetly. Actually, coupon payment is one important element of the design ofbonds and its amount will greatly affect the value of bonds. In AJT Model, eventhough coupon payment is considered, they assume that both bonds are consol type,meaning they are annuities with infinitive maturity. This simplification assumptionis also not in line with most cases of bonds in real financial world. In one word, bothdesigns make CoCo bond easier for theoretical valuation, but not implementable inreal financial market.What about a new model to loosen both assumptions, making the design of CoCobond more realistic and implementable even though the valuation may be a bit morecomplicated? This is our motivation and inspiration to design a new CoCo BondModel.

New ModelThe biggest difference in our model is the loose of some assumptions of both bonds.We assume that both bonds have continuously coupon payment, with finite maturity.The assumption is more in compliance with the general assumption of bonds inliterature, as well as the feasible design of real world bonds. So our correction willbe an improvement for the existing CoCo Bond Models which use asset level as itsconversion trigger.A positive coupon payment, different from RH Model’s zero-coupon deposit, meansthe bank will have cash outflow before the maturity. As in AJT Model, the drift ofunderlying asset under Q-measure will be smaller than r (we set it as r − δ in ourmodel).A finite maturity, different from AJT Model, means that both stopping times can beeither before or after the maturity. Now we need to consider both possibilities whenwe do the valuation for each claim.In other aspects of the model design, there also exist some differences. In AJT Model,value paid-out rate δ is decided exogenously (via µ). In the main content of thispaper, δ is exogenously decided when dividend payment is included. In the Extensionsection, δ is endogenously decided when dividend payment is not considered. Besides,regarding the amount of coupon payment, our model is slightly different from thatof AJT Model. In their model, the amounts of both coupon payments are constantsand they are decided exogenously. In our paper, coupon payment is a constantfraction (we call it coupon rate) of the face value of bond. Usually the face value ofbond is decided at the initial time when the bond is issued. So if the coupon rateis decided exogenously, the coupon design will actually be the same as AJT Model(both kinds are constant). This is the case in our main content. However, in one ofour extensions, we also consider the case of endogenously coupon rates. So at thissetting, the coupon payment is still fixed continuously across the maturity, however

3 MODELS 11

it is decided endogenously.Bankruptcy cost is also considered in our model. The setting is the same as AJTModel, which is in line with most literatures. Different from their model, we do notconsider the tax benefit. As before, this claim is easy to get because it is just aconstant fraction of the coupon payment. About the dividend payment, we take itinto consideration in our main model, but do not consider it in our Extension. Asis shown in the model section, this makes a big difference about the setting of valuepaid out rate δ.In conclusion, our models make some improvements about the design of CoCo bond(also the normal senior debt) by loosening some calculation-orientation assumptions.It makes the calculation a little more complicated, but its advantage in theoreticaldesign and practical application overwhelms. More detail of the design of our modelis provided in the model section.In the following model section, 3 supporting models are introduced before our coremodel, the CoCo Bond Model. We begin from a Benchmark Model, the classicBlack-Scholes-Merton model of debt and equity valuation. Based on the frameworkof Benchmark Model, we construct Debt-Equity Model in which many assumptionsof Benchmark Model have been loosened. Subordinate Debt Model adds subordinatedebt, another debt instrument, into the bank’s capital structure, which is used todirectly “compete” with CoCo bond in our analysis. Finally, CoCo Bond Model willbe introduced.

3 Models

3.1 Asset Dynamics

All of our models utilize standard option pricing method, which is based on a longline of research on capital structure that includes Black and Scholes (1973), Merton(1973; 1974), Black and Cox (1976), Leland (1994; 1996), and numerous subsequentpapers. This approach starts by modeling the dynamics of a firm’s assets and thenprices debt and equity as claims on those assets. We will begin with the dynamicsanalysis of the firm’s underlying assets. Before our model, we will introduce GirsanovTheorem briefly since it is frequently applied in our paper.

3.1.1 Girsanov Theorem

Let Ztt>0 be a standard Brownian motion, defined on a probability space (Ω,F ,P),and let Ftt>0 be the associated Brownian filtration. Let θtt>0 be an adapted pro-cess satisfying the hypotheses of Novikov’s Proposition:

E[exp

(∫ t

0θ2s ds

)]< +∞ ∀t > 0 (1)

Define

Mt = exp

(∫ t

0θs dZs −

1

2

∫ t

0θ2s ds

)(2)

3 MODELS 12

Now we can define a new probability measure Q on the measurable space (Ω,F) asfollows.For each T > 0 and any event F ∈ FT ,

Q(F ) = EP[MT1F

](3)

If we define

Zt = Zt −∫ t

0θs ds , t ∈ [0, T ] (4)

Under the probability measure Q, the stochastic process Zt06t6T is a standardBrownian motion.This is the famous Girsanov Theorem. It is commonly used for the transformationof probability measures in stochastic process.Now we move to a special application of Girsanov Theorem.If we set θt = θ ∈ R ∀t > 0, it simplifies to the Cameron-Martin Theorem, which isviewed as the most important special case of Girsanov Theorem.When θt = θ, the hypotheses of Novikov’s Proposition (1) is easily met. We can write(2) as:

Mt(θ) = exp

(∫ t

0θ dZs −

1

2

∫ t

0θ2 ds

)= eθZt−θ

2t/2 (5)

As before, Ztt>0 is a standard Brownian motion under the probability measure P(we also write it as P0, with the corresponding expectation operator E0). We candefine a new probability measure Q (we also write it as Pθ, with the correspondingexpectation operator Eθ) on (Ω,F) as follows.For each T > 0 and any event F ∈ FT ,

Pθ(F ) = E0

[MT (θ)1F

]or P0(F ) = Eθ

[MT (θ)−11F

](6)

For each T > 0 and any nonnegative random variable Y ,

Eθ[Y ] = E0 [MT (θ)Y ] or E0[Y ] = Eθ[MT (θ)−1Y

](7)

Similar to (4), if we define

Zt = Zt −∫ t

0θ ds = Zt − θt , t ∈ [0, T ] (8)

Under the probability measure Q = Pθ, the stochastic process Zt06t6T is a standardBrownian motion.From Cameron-Martin Theorem, we know that Zt06t6T is a Brownian motion withdrift θ under the probability measure Q = Pθ.Cameron-Martin Theorem deals only with special probability measures under whichpaths are distributed as Brownian motion with constant drift. However, GirsanovTheorem applies to nearly all probability measures. For the mathematical derivationin this paper, we need to transform the Brownian motion (with or without drift) underP-measure into another Brownian motion (with or without drift) under Q-measure.So Cameron-Martin Theorem is well enough for our calculation.

3 MODELS 13

3.1.2 Real World and Risk-Neutral World

The stochastic process of asset dynamics is the same for all the models we develop inour paper. So we display it at the beginning of all models and will refer to it everytime we begin a new model.We suppose that the firm’s future cash flows have a total market value at time tgiven by At. We always refer to At as the assets of the firm. In order to justifythis valuation of the firm, we could assume that there is some other security whosemarket value at any time t is At.Assume that we have a real world probability measure P (P-measure for short) definedon the measurable space (Ω,F), then we have a real world probability space (Ω,F ,P).Let ZPt t>0 be a standard Brownian motion under (Ω,F ,P). For the dynamics ofassets in real world, we assume that At meets a general Geometric Brownian Motion(GBM) process. It satisfies:

dAt = (ϕ− δ)At dt+ σAt dZPt (9)

where ϕ is the real world rate of return of assets, δ is the constant fraction of valuepaid out to security holders continuously, σ is the diffusion coefficient, and ZPt is astandard Brownian motion under P-measure. 1 The initial market value of assets isset to be A0, and maturity is T .For the valuation, the most important part in our paper, we will utilize the RiskNeutral Valuation Method, which values the market price of all claims under therisk-neutral world. We define a new probability measure Q (Q-measure for short) forthe risk neutral world and thus have a new probability space (Ω,F ,Q). In order toapply Girsanov Theorem, as before we write it as P , P0 and Q , Pθ. 2

For Q-measure to be a risk-neutral measure, we should set

θ = −ϕ− rσ

(10)

Where r is the risk free interest rate. From Girsanov Theorem, we can get a newstochastic process ZQt t>0 which is a standard Brownian motion under Q-measure.

ZQt = ZPt − θt = ZPt +ϕ− rσ

t (11)

From (11), we can get its differential form:

dZQt = dZPt +ϕ− rσ

dt (12)

From (9) and (12), we can get the dynamics of At under the risk-neutral world (Q-measure):

dAt = (r − δ)At dt+ σAt dZQt (13)

1Parameters ϕ, δ, σ and r have already been annualized.2θ has the same definition as in Section 3.1.1.

3 MODELS 14

So we can see that, under the risk-neutral world, the dynamics of assets follow a GBMprocess with drift (r− δ) and diffusion coefficient σ. For the pricing and valuation inthe rest of our paper, except for some explicit notes, all the calculation and derivationis under the risk-neutral world.For the convenience of the mathematic derivation, we can set:

µ = r − δ − σ2

2⇐⇒ drift = r − δ = µ+

σ2

2(14)

From the basic property of GBM and the lognormal distribution of At3, we have:

At = A0e(r−δ−σ2/2)t+σZQt = A0e

µt+σZQt (15)

EQ[At] = A0e(r−δ)t = A0e

(µ+σ2

2)t (16)

logAt ∼ N (logA0 + µt, σ2t) (under Q-measure) (17)

PQ(At < m) = Φ

(logm− (logA0 + µt)

σ√t

), for m > 0 (18)

where Φ(·) is the Cumulative Distribution Function (CDF) of standard normal dis-tribution. 4

3.1.3 Absence of Arbitrage and Asset Equation

Market values of securities are viewed as the claims on the asset A. The absence ofwell-behaved arbitrage implies that at any time t ∈ [0, T ], the market value of assetsAt is equal to the market values of all claims. It consists of all the securities, aswell as other claims on asset value such as bankruptcy cost, etc. Then we have thefollowing asset equation.

At =∑t

the market value of each claim, t ∈ [0, T ] (19)

Usually, we define the firm value as the market value of all securities. Then we have:

Ft =∑t

the market value of each security, t ∈ [0, T ] (20)

Then the asset equation can also be written as:

At = Ft +∑t

the market value of other claim than security, t ∈ [0, T ] (21)

3Note that, because of the continuous path property of Brownian Motion and Geometric BrownianMotion, for related variables all across this paper, inequality relation “less than (<)” and “less orequal to (6)” can be regarded as the same. The same logic applys to the inequality realtion of“greater than (>)” and “greater or equal to (>)”.

4A detailed derivation for (15)-(18) is provided in Appendix Section 8.1.

3 MODELS 15

Especially, at time t = 0, the sum of the initial market value of all claims is equal tothe initial asset value A0.Asset Equation is the most important equality relationship in our paper. It will beverified in every model we develop. The fulfillment of asset equation guarantees thatour models are internally consistent. Besides, it can also be used to verify whetherour close-form solution is correctly derived.

3.1.4 Definition of variables, functions and expectations

For the valuation of the securities in the following models, we need to define somevariables, functions and expectations. All the definition and description below isunder the risk-neutral world (Q-measure).Let’s define:

Wt = logAtA0

(22)

From (15), we haveWt = µt+ σZQt (23)

Since ZQt is a standard Brownian motion and meets the normal distribution with

ZQt ∼ N (0, t), Wt is a general Brownian motion and meets the normal distributionwith Wt ∼ N (µt, σ2t).Let’s also define:

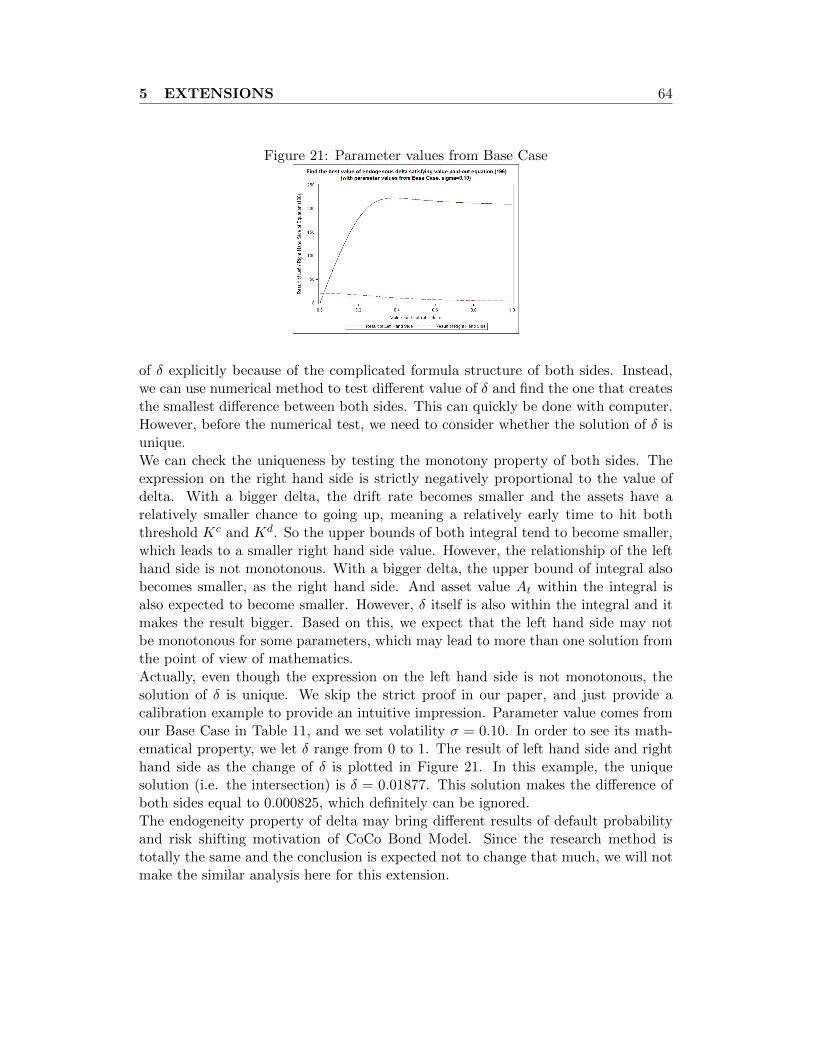

mt = min06s6t

Ws (24)

We can see that for a specific t > 0, mt is the minimum value of general Brownianmotion until time t.We can get the CDF of mt as below. 5

PQ(mt 6 m) = Φ

(m− µtσ√t

)+ exp

(2µm

σ2

)Φ

(m+ µt

σ√t

), for m 6 0 (25)

As before, Φ(·) is the CDF of standard normal distribution. For a special case, wehave PQ(mt 6 0) = 1.We set a threshold K(K < A0) and define the time τ as the first time that the assetvalue drops and hits K. Obviously τ is one kind of stopping time. 6

τ = infs : As 6 K (26)

With maturity T , we have the following relationship. They are mutually derivableand thus equivalent.

τ 6 T ⇐⇒ min06s6T

As 6 K ⇐⇒ A0emT 6 K ⇐⇒ mT 6 log

K

A0(27)

5We provide the proof in Step 3, Appendix Section 8.2.6Stopping time τ is an important random time in stochastic process, meaning that the decision

about when to stop is based solely on information available up to time τ . A formal definition canrefer to any textbook of stochastic process, such as Protter (1990) or Duffie (2001).

3 MODELS 16

Oppositely it holds:

τ > T ⇐⇒ mT > logK

A0(28)

Now we define the functions of H(·). We call it H function in the rest of the paper.It is very important because most of the expectations in our paper are calculated insome forms of H function.Let’s define:

Hµ,σ(t, v, k, y) , H(t, v, k, y) = E[exp(vWt + kmt)1mt6y

], t > 0, y 6 0, v, k ∈ (−∞,∞)

(29)1· is an indicator function that is equal to 1 if the condition within the curly bracemeets and otherwise equal to 0. If we set y = 0, the indicator function degenerates toa constant 1 and “disappear” from the expectation operator. Note that H function isbased on the general Brownian motion Wt with drift µ and diffusion σ. For Brownianmotion with other drift or diffusion coefficients, we need to do some transformation(usually by applying the introduced Girsanov Theorem) before using the explicit for-mula of H function.For the convenience of our calculation, based on H function, we also define the func-tion of ∆H i(·):

∆H i(t, v, k) = E[exp(vWt + kmt)1log Kd

A0<mt6log K

i

A0

]= H

(t, v, k, log

Ki

A0

)−H

(t, v, k, log

Kd

A0

)(30)

Kd and Ki are exogenous thresholds and will be defined in the model section. 7

The explicit formula of H function (and thus ∆H function) is available, meaning thatthe right-hand-side expression of (29) and (30) can be achieved explicitly. We showthe result as below. 8

Hµ,σ(t, v, k, y) , H(t, v, k, y) = eµvt+v2σ2t/2hµ,σ(t, k, y) (31)

with

hµ,σ(t, k, y) =2γ

2γ + kσ2eky+2yγ/σ2

Φ

(y + tγ

σ√t

)+

2γ + 2kσ2

2γ + kσ2ekγt+k

2σ2t/2Φ

(y − (γ + kσ2)t

σ√t

)(32)

where γ = µ+ vσ2, and Φ(·) is the CDF of standard normal distribution.The explicit formula of ∆H i(·) can be get from (30) and the result of (31). To savesome space, we do not display it here.From (22) and (24), we have:

At = A0eWt (33)

min06s6t

As = A0emt (34)

7In Section 3, Kd is the default threshold for the last 3 models. Ks (i = s) is the depressionthreshold for Subordinate Debt Model. Kc (i = c) is the conversion threshold for CoCo Bond Model.

8We provide the detailed derivation in Appendix Section 8.2.

3 MODELS 17

mt 6 y ⇐⇒ min06s6t

As 6 A0ey (35)

After some transformation, we can rewrite H(·) and ∆H i(·) as:

H(t, v, k, y) = E

(AtA0

)v ( min06s6t

As

A0

)k1min

06s6tAs 6 A0e

y

(36)

∆H i(t, v, k) = E

(AtA0

)v ( min06s6t

As

A0

)k1Kd < min

06s6tAs 6 Ki

(37)

With the threshold K and stopping time τ defined in (26), it is easy to get thefollowing risk-neutral probabilities:

PQ(τ 6 T ) = P(mT 6 log

K

A0

)= E

[1mT6log K

A0

]= H

(T, 0, 0, log

K

A0

)(38)

PQ(τ > T ) = P(mT > log

K

A0

)= 1− E

[1mT6log K

A0

]= 1−H

(T, 0, 0, log

K

A0

)(39)

We have an important intermediate result, which will be used many times in thefollowing derivation. We display it as below. 9

E[e−rτ1τ6T

]= e−rT

(K

A0

)− θσ

H

(T,θ

σ, 0, log

K

A0

)(40)

where θ = −µσ +

õ2

σ2 + 2r for all the models in our paper.

3.2 Benchmark Model

To begin our models, we outline the classic Black-Scholes-Merton model of debt andequity valuation as our Benchmark Model. It is the first one of our 3 supportingmodels. We suppose that the original owners of the firm choose a capital structureconsisting of debt and equity.

3.2.1 Security Design and Assumptions

For a simple start, we assume that the corporate debt is in the form of a single zero-coupon bond maturing at time T , with face value D. Another security is pure equitywith no dividend. In the event that the total value AT of the firm at maturity isless than the contractual payment D due on the debt, the firm defaults, giving itsfuture cash flows, worth AT , to debt holders. Without default the debt holders willreceive the face value D. At maturity T , equity holders receive the residual after

9The detailed derivation is provided in Appendix Section 8.3.

3 MODELS 18

debt holders.An important assumption is the absence of early default and no bankruptcy cost.The firm will not go bankruptcy before maturity, even when its asset value at sometime before the maturity is less than the face value of the debt D. The only possibledefault time is at maturity T , when its asset value is less than D. Besides, we assumeit does not have any bankruptcy cost when it defaults at the maturity.In order to make it clearer and easier to compare with other models, we will repeatthe security setting and assumptions in Table 2 and Table 3.

Table 2: Security Design of the Benchmark Model

Corporate Debt Equity

Face Value D Dividend div = 0Coupon Rate c1 = 0Maturity TDefault Threshold Kd = DDefault Time τd = T , if AT < DBankruptcy Cost ω = 0

Table 3: Important Assumptions of the Benchmark Model

Assumptions

1. The firm just issues 2 types of securities: corporate debt and equity.2. No coupon payment for debt (c1 = 0)3. No dividend payment for equity (div = 0)4. Absence of early default, i.e. τd /∈ (0, T )5. No bankruptcy cost (ω = 0)

3.2.2 Asset Equation

According to Section 3.1.3, the total market value of debt and equity must be themarket value of the assets at time t ∈ [0, T ]. In this model, both claims are securities(due to the absence of bankruptcy cost), so the firm value is equal to the asset value.

At = Ft = Dt +Wt (41)

Dt and Wt are the market values of corporate debt and equity at time t.Especially, at time t = 0, we have:

A0 = F0 = D0 +W0 (42)

This is what we will verify after we get the market value expressions of both claims.

3 MODELS 19

3.2.3 Valuation of claims

As described in Section 3.1.2, the market values of both claims are calculated underthe risk-neutral world. In order to conduct the valuation in a clear way, we make itinto 4 steps. The analysis by steps will apply across all 4 models.

Valuation FormulaIn this model, since there are no distribution of values before the maturity (neithercoupon nor dividend), the parameter of value paid-out rate δ = 0.For debt holders, at maturity, they will receive the face value D if the firm does notdefault. Otherwise they will take over the firm and receive AT . There is not anycoupon payment. So the market value of debt at time t = 0 is:

D0 = EQ[e−rT min(AT , D)

](43)

For equity holders, they will receive the residual at maturity. There is not anydividend payment. So the market value of equity at time t = 0 is:

W0 = EQ[e−rT max(AT −D, 0)

](44)

Verify Asset EquationWe can easily verify the Asset Equation (42) in this model.

D0 +W0 = e−rTEQ [min(AT , D) + max(AT −D, 0)]

= e−rTEQ [D + min(AT −D, 0) + max(AT −D, 0)]

= e−rTEQ [D + (AT −D) + 0]

= e−rTEQ [AT ]

= A0 (45)

(16) is used when we calculate the expectation of AT .

Explicit FormulaWe begin to derive the explicit valuation formula from equity W0. It is obvious thatthe market value of equity is given by the classical Black-Scholes-Merton Europeancall option pricing formula, regarding the firm’s assets as the underlying and the facevalue of debt as strike. Other option pricing parameters r, σ and T are also definedas before. 10

W0 = A0Φ(d1)− e−rTDΦ(d2) (46)

D0 = A0 −W0 = A0Φ(−d1) + e−rTDΦ(d2) (47)

As before, Φ(·) is the CDF of standard normal distribution, and

d1 =log(A0/D) + (r + σ2/2)T

σ√T

(48)

10The derivation of European call option pricing formula is provided in Appendix Section 8.4.

3 MODELS 20

d2 =log(A0/D) + (r − σ2/2)T

σ√T

= d1 − σ√T (49)

Risk-Neutral ProbabilityWe can get the probability that the firm defaults at maturity. Note that the dynamicsof At is under Q-measure, so what we get is the risk-neutral probability, rather thanthe real world probability.From (17), AT is lognormal distribution with

logAT ∼ N (logA0 + (r − σ2/2)T, σ2T ) (under Q-measure) (50)

We then have:

PQ(AT < D) = Φ

(logD −

[logA0 + (r − σ2/2)T

]σ√T

)= Φ(−d2) = 1− Φ(d2) (51)

Accordingly, the risk-neutral probability that the firm does not default at maturityis:

PQ(AT > D) = 1− PQ(AT < D) = Φ(d2) (52)

3.3 Debt-Equity Model

Now we move to the second supporting model. In this model, we still suppose thatthe original owners of the firm choose a capital structure consisting of just debt andequity. But here, early default and bankruptcy cost will be considered. For a generalcase, we will assume the existence of debt coupon and equity dividend. Other casesof dividend/no coupon, coupon/no dividend and no dividend/no coupon are easy toderive from the general case (for example, for the cases of no coupon payment, justset the coupon rate equal to 0) and they are partly covered in Section 5.2.

3.3.1 Security Design and Assumptions

In this model, we still have corporate debt and equity in the capital structure of thefirm. However, the design of both securities has changed.The biggest change is the consideration of early default. The corporate debt, withface value D, will default when the asset value drops to a default threshold Kd atthe default time τd. It can happen both before the maturity and at maturity. Forsimplicity and more importantly, continuity, we assume the default threshold Kd isthe face value of debt D. Then we have:

τd = infs : As 6 Kd = infs : As 6 D (53)

We can prove that, τd is a stopping time, a very important definition in stochasticprocess.It is obvious that, τd < T means the firm defaults before the maturity. τd = T meansthe firm defaults exactly at maturity. τd > T means the firm does not default duringthe maturity.

3 MODELS 21

Another big change is the consideration of coupon payment. We assume that thedebt will pay continuous coupons until it defaults (if any), at the coupon rate c1.We assume the coupon rate is exogenous. If the debt does not default before thematurity, at maturity T the payment of debt is the same as Benchmark Model.In this model, the equity will pay out dividends continuously. Because of the paymentof coupon and dividend, the paid-out rate δ will be positive. We assume in each timeinterval dt, the dividend will be the residual value after the payment of coupon, thenthe dividend in dt will be (δAt − c1D) dt. At maturity T (if any), the payment ofequity is the residual value after the payment of debt, the same as the BenchmarkModel.If the above difference between paid-out value and debt coupon (δAt − c1D) is neg-ative, the firm is generating insufficient cash to service its debt. As is customary,such as the suggestion from Glasserman and Nouri (2010), we interpret a negativedividend as the issuance of a small amount of new equity, which brings cash into thefirm. This cash is immediately paid out to the debt holders, so the issuance has noimpact on the total amount of capital in the firm. Furthermore, we assume that thenew equity is issued to existing shareholders (as in a rights offering). Thus, the pro-portion of the firm owned by each shareholder is unchanged. So, when this differenceis positive, we call it as dividend; when it is negative, it is actually the cost of raisingequity. We will incorporate this stream of payments into our overall valuation of theequity (and equity from converted CoCo bond in our core model).In order to make it clearer and easier to compare with other models, we will repeat thesecurity setting and assumptions in Table 4 and Table 5. Compared with BenchmarkModel, except Assumption 1, all other 4 assumptions have been changed.

Table 4: Security Design of Debt-Equity Model

Corporate Debt Equity

Face Value D Dividend div = (δAt − c1D) dt (before τd)Coupon Rate c1 > 0 div = 0 (after τd)Maturity TDefault Threshold Kd = DDefault Time τd = infs : As 6 KdBankruptcy Cost ω > 0

Table 5: Important Assumptions of Debt-Equity Model

Assumptions

1. The firm just issues 2 types of securities: corporate debt and equity.2. There is coupon payment for debt (c1 > 0).3. There is dividend payment for equity (positive, 0 or negative).4. Early default can happen before the maturity.5. There is positive bankruptcy cost (ω > 0).

3 MODELS 22

3.3.2 Asset Equation

According to Section 3.1.3, the total market value of all claims must be the marketvalue of the assets. In this model, except 2 securities of debt and equity, bankruptcycost is a deadweight lost and “takes” some value away from the assets. As a result,it is also one claim on the asset value, although it is not included as part of the firmvalue. At time t ∈ [0, T ], we have:

At = Dt +BCt +Wt = Ft +BCt (54)

Dt, Wt and BCt are the market values of corporate debt, equity and bankruptcy costat time t. Especially, at time t = 0, we have:

A0 = D0 +BC0 +W0 = F0 +BC0 (55)

This equation is what we will verify after we get the market value expressions of allclaims.

3.3.3 Valuation of claims

As described in Section 3.1.2, the market values of all claims are calculated underthe risk-neutral world. As before, the valuation process includes 4 steps.

Valuation FormulaValuation in this model is much more complicated than that in the Benchmark Mod-el, because it needs to consider both possibilities of default before maturity and nodefault before maturity. In the valuation formulas, we will utilize indicator functionsto distinguish and reflect each possibility.To make it clearer, we decompose the market value of each banking claim (discountedto time t = 0) into different payments. We then take the expectation of each paymentand sum them up to get the market value of each claim.

- Decomposition of corporate debtIf there is no default during the maturity (τd > T ), debt holders can get afull payment of the face value D at maturity. Besides, they will get continuouscoupon payment until time T. However, if default happens sometime during thematurity (τd 6 T ), debt holders will take over the firm and acquire the residualassets at the default time τd, and part of the assets will be a deadweight lostas bankruptcy cost. Coupon is continuously paid until default. So we candecompose the debt payments as below.Debt coupon:

J1 =

∫ min(τd,T )

0e−rsc1D ds (56)

3 MODELS 23

Debt principal if no default:

J2 = e−rTD 1τd>T (57)

Debt principal if default at maturity or before maturity:

J3 = e−rτd(1− ω)D 1τd6T (58)

So the expectation of the initial market value of debt is:

D0 = EQ[J1 + J2 + J3] (59)

- Decomposition of bankruptcy costThe bankruptcy cost will be positive only when the default happens before thematurity (τd 6 T ). At this time, it takes the form of a deadweight lost as aconstant fraction ω of the residual assets.

J4 = e−rτdωD 1τd6T (60)

So the expectation of the initial market value of bankruptcy cost is:

BC0 = EQ[J4] (61)

- Decomposition of equityIf there is no default during the maturity (τd > T ), equity holders can get theresidual assets after the fulfillment of debt principal at maturity. However, ifdefault happens sometime during the maturity (τd 6 T ), debt holders will takeover the firm and thus equity holders get nothing. Besides, dividend payment,whether positive or negative, will be valid until the firm defaults. So we candecompose the equity payments as below.Residual payment at maturity if no default:

J5 = e−rT (AT −D) 1τd>T (62)

Dividend payment:

J6 =

∫ min(τd,T )

0e−rs(δAs − c1D) ds (63)

So the expectation of the initial market value of equity is:

W0 = EQ[J5 + J6] (64)

Verify Asset EquationNow we will verify the Asset Equation (55). We add it by parts as follows.

EQ[J1 + J6] = EQ[∫ min(τd,T )

0e−rsδAs ds

](65)

3 MODELS 24

EQ[J2 + J5] = e−rTEQ[AT 1τd>T

]= e−rTEQ [AT ]− e−rTEQ

[AT 1τd6T

]= A0e

−δT − EQ[e−rTAT 1τd6T

](66)

EQ[J3 + J4] = EQ[e−rτdD 1τd6T

](67)

To be continued, we need to utilize the following equality relationship. 11

EQ[(e−rτdD − e−rTAT ) 1τd6T

]= EQ

[∫ T

τd

e−rsδAs ds 1τd6T]

(68)

With Equation (68), we can easily have:

EQ[J2 + J3 + J4 + J5] = A0e−δT + EQ

[(e−rτdD − e−rTAT ) 1τd6T

]= A0e

−δT + EQ[∫ T

τd

e−rsδAs ds 1τd6T]

= A0e−δT + EQ

[∫ T

min(τd,T )e−rsδAs ds

]

= A0e−δT + EQ

[∫ T

0e−rsδAs ds

]− EQ

[∫ min(τd,T )

0e−rsδAs ds

]

= A0e−δT +A0 −A0e

−δT − EQ[∫ min(τd,T )

0e−rsδAs ds

]

= A0 − EQ[∫ min(τd,T )

0e−rsδAs ds

](69)

To get the expectation of∫ T0 e−rsδAs ds, we need to apply Fubini Theorem, under

which we can “move” the expectation calculation inside the integral:

EQ[∫ T

0e−rsδAs ds

]=

∫ T

0e−rsδ EQ[As] ds

=

∫ T

0e−rsδ A0e

(r−δ)s ds = δA0

∫ T

0e−δs ds

= −A0e−δs∣∣∣∣T0

= A0 −A0e−δT (70)

11We provide the proof in Appendix Section 8.5.

3 MODELS 25

Based on (65) and (69), we have:

D0 +BC0 +W0 = EQ[J1 + J2 + J3 + J4 + J5 + J6]

= EQ[(J1 + J6) + (J2 + J3 + J4 + J5)]

= EQ[∫ min(τd,T )

0e−rsδAs ds

]+A0 − EQ

[∫ min(τd,T )

0e−rsδAs ds

]= A0 (71)

Now we have verified Asset Equation (55).Note that the present market value of coupon and dividend payment (J1 + J6)is equal to the present value of total cash outflow during the maturity, which is∫ min(τd,T )0 e−rsδAs ds, rather than

∫ T0 e−rsδAs ds. Actually, the difference of these

two terms∫ Tmin(τd,T )

e−rsδAs ds is never produced by the firm because the firm willnot have any cash outflow after it defaults at τd. All the assets are taken over bydebt holders and the firm does not exist after default. But for calculation purpose,this term will appears in our mathematical derivation.

Explicit FormulaAfter some intensive mathematical derivation, we can get the risk-neutral expectationof each decomposition payment. 12 Since we use indicator function to reflect whetherdefault or not during the maturity, H function, containing indicator function as onemultiplier, will be used widely to achieve the explicit formula of the expectation.The definition, property and some basic calculation of functions H(·) are described

in Section 3.1.4. Remember that we have θ = −µσ +

õ2

σ2 + 2r for all the calculationformulas in our paper.

EQ[J1] =c1D

r

1− e−rT[1−H

(T, 0, 0, log

Kd

A0

)]− e−rT

(Kd

A0

)− θσ

H

(T,θ

σ, 0, log

Kd

A0

)(72)

EQ[J2] = e−rTD

[1−H

(T, 0, 0, log

Kd

A0

)](73)

EQ[J3] = e−rT (1− ω)D

(Kd

A0

)− θσ

H

(T,θ

σ, 0, log

Kd

A0

)(74)

EQ[J4] = e−rTωD

(Kd

A0

)− θσ

H

(T,θ

σ, 0, log

Kd

A0

)(75)

12To save space, we just provide the final formulas in the Main Body of this paper. A detailedderivation is deferred to Appendix Section 8.6.

3 MODELS 26

EQ[J5] = e−rT[A0e

(µ+σ2/2)T −A0H

(T, 1, 0, log

Kd

A0

)]− e−rTD

[1−H

(T, 0, 0, log

Kd

A0

)](76)

EQ[J6] = A0 −A0e−δT + e−rTA0H

(T, 1, 0, log

Kd

A0

)− e−rTD

(Kd

A0

)− θσ

H

(T,θ

σ, 0, log

Kd

A0

)

− c1D

r

1− e−rT[1−H

(T, 0, 0, log

Kd

A0

)]− e−rT

(Kd

A0

)− θσ

H

(T,θ

σ, 0, log

Kd

A0

)(77)

According to (59), (61) and (64), we can get the initial market value of debt,bankruptcy cost and equity.Pay attention that, unlike (70) ,

EQ[∫ min(τd,T )

0e−rsδAs ds

]6= EQ

[∫ min(τd,T )

0e−rsδ EQ[As] ds

]

= EQ[−A0e

−δs∣∣∣∣min(τd,T )

0

]= A0 −A0EQ

[e−δmin(τd,T )

](78)

The equation does not hold because the pre-condition of Fubini Theorem is violated13, so the expectation calculation cannot be “moved” inside the integral. Instead, itscorrect formula can be get from (72) and (77):

EQ[∫ min(τd,T )

0e−rsδAs ds

]= EQ[J1 + J6]

= A0−A0e−δT+e−rTA0H

(T, 1, 0, log

Kd

A0

)−e−rTKd

(Kd

A0

)− θσ

H

(T,θ

σ, 0, log

Kd

A0

)(79)

Note that in (79) the threshold is Kd with the corresponding stopping time τd. Ifwe have another threshold Ki with the corresponding stopping time τi, we can easily

calculate the value of EQ[∫ min(τi,T )

0 e−rsδAs ds]. This result will be used in CoCo

Bond Model, where it is the conversion threshold Kc with conversion time τc (i.e.i = c).

Risk-Neutral ProbabilityFrom (38), we can get the risk-neutral probability that the firm will default during

13To apply Fubini Theorem, both integral bounds should be exact numbers (or positive/negativeinfinite). Either one cannot be random number. In this formula, upper bound min(τd, T ) is a randomtime, which violates the pre-condition of Fubini Theorem.

3 MODELS 27

the maturity.

PQ(τd 6 T ) = H

(T, 0, 0, log

Kd

A0

)(80)

Accordingly, from (39), the risk-neutral probability that the firm will not default is:

PQ(τd > T ) = 1−H(T, 0, 0, log

Kd

A0

)(81)

3.4 Subordinate Debt Model

Now we move to the last supporting model. In this model, we will make a change tothe firm’s capital structure by adding another security: subordinate debt.We suppose that the original owners of the firm choose a capital structure consistingof corporate debt, subordinate debt and equity. Early default and bankruptcy costwill also be considered. For a general case, we assume the existence of debt couponand equity dividend as well.In the existence of subordinate debt, corporate debt has a senior payment status ifthe firm defaults. We assume that this kind of senior status is complete, meaning thatsubordinate debt holders will receive nothing if corporate debt holders are not fullyrepaid. So in this model and the model that follows, we can also call the corporatedebt as senior debt, compared with subordinate debt in this model (and CoCo bondin our core model).

3.4.1 Security Design and Assumptions

In this model, we add subordinate debt into the firm’s capital structure. The designof another two securities, senior debt and equity, remains nearly the same as that inthe Debt-Equity Model.Senior debt, with face value D, will default and go bankruptcy when the asset valuefirstly drops to threshold Kd = D at the default time τd. It can happen both beforethe maturity and at maturity. We also assume that senior debt will pay continuouscoupons until its asset value hits Kd (if any), at the exogenously decided coupon ratec1.The new security subordinate debt is issued with face value S and pays continuouscoupons until its asset value hits a threshold Ks (if any), at the coupon rate ofc2, which is also exogenously decided. For simplicity, we assume this threshold isthe sum of the face value of senior debt and subordinate debt, i.e. Ks = D + S.When the asset value firstly drops to Ks at time τs, the firm will continue to exist.However, since its asset value is less than the face value of both debts, the firm willget financially depressed. So we call Ks as the depression threshold. We have:

τs = infs : As 6 Ks = infs : As 6 D + S (82)

Obviously, τs is also a stopping time, the same as τd. Since Ks is strictly larger thanKd, τs is strictly smaller than τd.

3 MODELS 28

After hitting Ks, subordinate debt will not pay coupons any longer even when itsasset value goes up and hit Ks again later. If the asset value is still less than Ks atmaturity, the firm has to declare to default then. So, the firm will default with itsasset value either by hitting Kd before the maturity (early default) or being smallerthan Ks at maturity.Compared with Debt-Equity Model, which just has default threshold, in this modelwe have both depression threshold and (early) default threshold. After hitting de-pression threshold, the firm does not default immediately. It still exists, but stopspaying coupons to the holders of subordinate debt.It is obvious that, τd < T means the firm has early default. τs > T means the firmwill neither default nor get depressed during the maturity. τs 6 T 6 τd means thefirm has no early default (may default at maturity) but will get depressed duringthe maturity. The risk-neutral probabilities of these 3 conditions will be calculatedafter we get the market value of each claim. Among this, T = τd means the firmgets default at maturity when its asset value drops to the face value of senior debt;T = τs means the firm gets depressed at maturity when its asset value drops to theface value of both debts.As in Debt-Equity model, the equity in this model will also pay out dividends con-tinuously. Because of the payment of both coupon and dividend, the paid-out rate δwill be positive. We assume in each time interval dt, the dividend will be the residualvalue after the payment of coupons. So the dividend will be (δAt − c1D− c2S) dt atthe beginning. After it hits the depression threshold Ks (if any), subordinate debtstops paying coupons and the dividend payment will change to (δAt−c1D) dt in eachtime interval until it hits Kd and go bankruptcy (if any). The dividend payment canbe positive as well as negative. 14 At maturity T (if any), the payment of equity isthe residual value after the payment of both debts.In order to make it clearer and easier to compare with other models, we will re-peat the security setting and assumptions in Table 6 and Table 7. Compared withBenchmark Model, all 5 assumptions have been changed.

3.4.2 Asset Equation

According to Section 3.1.3, the total market value of all claims must be the marketvalue of the assets. Compared with Debt-Equity Model, it has one more claim onthe asset value, subordinate debt. It is one kind of security and is included as partof the firm value. At time t ∈ [0, T ], we have:

At = Dt +BCt + St +Wt = Ft +BCt (83)

Dt, St, Wt and BCt are the market values of corporate senior debt, subordinate debt,equity and bankruptcy cost at time t.Especially, at time t = 0, we have:

A0 = D0 +BC0 + S0 +W0 = F0 +BC0 (84)

14The explanation of negative dividend is provided in Section 3.3.1.

3 MODELS 29

Table 6: Security Design of Subordinate Debt Model

Corporate Senior Debt Subordinate Debt

Face Value D Face Value SCoupon Rate c1 > 0 Coupon Rate c2 > 0Maturity T Maturity TDefault Threshold Kd = D Depression Threshold Ks = D + SDefault Time τd = infs : As 6 Kd Depression Time τs = infs : As 6 KsBankruptcy Cost ω > 0 Depression Cost ω′ = 0

Equity

Dividend div = (δAt − c1D − c2S) dt (before τs)div = (δAt − c1D) dt (after τs and before τd)div = 0 (after τd)

Table 7: Important Assumptions of Subordinate Debt Model

Assumptions

1. The firm issues 3 types of securities, including subordinate debt.2. There is coupon payment for both debts (c1 > 0, c2 > 0).3. There is dividend payment for equity (positive, 0 or negative).4. Early default can happen before the maturity.5. There is positive bankruptcy cost (ω > 0).

This equation is what we will verify after we get the market value expressions of allclaims.

3.4.3 Valuation of claims

As before, the market values of all claims are calculated under the risk-neutral world.We conduct the valuation in 4 steps.

Valuation FormulaWe have 2 thresholds in this model, so there exist 3 different conditions. As before,we will utilize indicator functions to distinguish each possibility. We still decomposethe payments of each claim firstly, take the expectation of each payment and thensum them up to get the market value of each claim.The design of corporate debt is totally the same as that in Debt-Equity Model. Itsdynamics and threshold does not change after the introduction of subordinate debt.Its payment at any time in any condition (default or no default) keeps the sameas before. So in this model (also the CoCo Bond Model), the decomposition andvaluation of corporate debt payment is exactly the same as that in the Debt-EquityModel. Since the bankruptcy cost always comes with the corporate debt, its paymentalso keeps the same across the last 3 models. In order to make it complete, we stillrepeat their formulas here, without detailed explanation.

3 MODELS 30

- Decomposition of corporate debtDebt coupon:

J1 =

∫ min(τd,T )

0e−rsc1D ds (85)

Debt principal if no default:

J2 = e−rTD 1τd>T (86)

Debt principal if default at maturity or before maturity:

J3 = e−rτd(1− ω)D 1τd6T (87)

So the expectation of the initial market value of debt is:

D0 = EQ[J1 + J2 + J3] (88)

- Decomposition of bankruptcy costIt exists only when the default happens before the maturity (τd 6 T ).

J4 = e−rτdωD 1τd6T (89)

So the expectation of the initial market value of bankruptcy cost is:

BC0 = EQ[J4] (90)

- Decomposition of subordinate debtIt looks a little more complicated because we have 2 thresholds in this model,which leads to 3 conditions. If there is no depression during the maturity(τs > T ), subordinate debt holders can get the full payment of face value S. Ifthere is early default (τd 6 T ), subordinate debt holders get nothing after thepayment of senior debt holders. In the last condition (τs 6 T < τd), subordinatedebt holders will get their part after the payment of senior debt holders, butbefore the equity holders. Besides, coupon payments will continuously paiduntil it hits the depression threshold. So we can decompose the subordinatedebt payments as below.Debt coupon:

J5 =

∫ min(τs,T )

0e−rsc2S ds (91)

Debt principal if no default or depression:

J6 = e−rTS 1τs>T (92)

3 MODELS 31

Debt principal if depression but no early default:

J7 = e−rT min(AT −D,S) 1τs6T<τd (93)

So the expectation of the initial market value of subordinate debt is:

S0 = EQ[J5 + J6 + J7] (94)

- Decomposition of equityThere are also 3 conditions. Equity holders will always be repaid after thepayment of both kinds of debt holders. Besides, dividend payment will be validuntil the firm defaults, and it will have a big change if the firm gets depressedbecause since then subordinate debt coupon is not paid.Residual payment at maturity if no default or depression:

J8 = e−rT (AT −D − S) 1τs>T (95)

Residual payment at maturity if depression but no early default:

J9 = e−rT max(AT −D − S, 0) 1τs6T<τd (96)

Dividend payment is the sum of the following 3 different conditions:

J10.1 =

∫ T

0e−rs(δAs − c1D − c2S) ds1τs>T (97)

J10.2 =

[∫ τs

0e−rs(δAs − c1D − c2S) ds+

∫ T

τs

e−rs(δAs − c1D) ds

]1τs6T<τd

(98)

J10.3 =

[∫ τs

0e−rs(δAs − c1D − c2S) ds+

∫ τd

τs

e−rs(δAs − c1D) ds

]1τd6T

(99)

J10 = J10.1 + J10.2 + J10.3

=

∫ min(τs,T )

0e−rs(δAs − c1D − c2S) ds+

∫ min(τd,T )

τs

e−rs(δAs − c1D) ds1τs6T(100)

So the expectation of the initial market value of equity is:

W0 = EQ[J8 + J9 + J10] (101)

3 MODELS 32

Verify Asset EquationNow we will verify the Asset Equation (84). We add it by parts as follows.