The Rise and Rise of London’s Luxury Quarter · London Luxury Quarter ... The global appetite for...

24

Retail Intelligence The Rise and Rise of London’s Luxury Quarter

Transcript of The Rise and Rise of London’s Luxury Quarter · London Luxury Quarter ... The global appetite for...

Retail Intelligence

The Rise and Rise of London’s Luxury Quarter

02 | Jones Lang LaSalle

London Luxury Quarter | 01

IntroductionThe global appetite for luxury retailing is growing and London is at the forefront of this growth. Mayfair, St James’s and the surrounding streets have seen a rapid expansion of the luxury offering in recent years, cementing their role as the leading destination for luxury retailing in the Capital. New West End Company and Heart of London Business Alliance, which together represent over 1,000 businesses, recognised this growth and as a result two years ago created the London Luxury Quarter to transform the area into a valuable entity that can be marketed globally.

Jones Lang LaSalle has been commissioned by the New West End Company and Heart of London Business Alliance to define the boundary of the London Luxury Quarter and to identify and understand its make-up and future growth prospects.

02 | Jones Lang LaSalle

A resilient and growing sector…The global luxury market has remained relatively sheltered from the economic crisis. Despite a short period of slower sales in 2009, it bounced back in 2010 and continued to flourish throughout 2011 and into 2012. Whilst economic uncertainty has deterred most global middle-income shoppers, affluent Western shoppers have flocked back to the premium brands, which together with economic growth in the BRIC nations and an insatiable appetite for luxury goods in the Far East, has driven growth in the luxury goods market globally.

According to retail expert Verdict, the global luxury goods market witnessed strong growth to 2010, and is currently valued at $320bn. Verdicts recent forecasts suggest that this expansionary trend is set to continue with estimates valuing the market at around $500bn by 2015.

Europe remains the largest luxury goods market with over $117bn being spent on luxury branded products in 2010 however, Asia Pacific is the only market not to have suffered a drop in luxury sales in 2009 and is set to experience unprecedented growth over the next five years, rapidly closing in on Europe’s number one position. By 2015 Asia Pacific’s luxury goods market is expected to be valued at $144bn, up 92% on today’s valuation. The growing wealth creation in the Asia Pacific region, most notably throughout China, and the sheer volume and size of its densely populated cities, has made it a very attractive destination for luxury retailers.

The global luxury retail market

London Luxury Quarter | 03

57.6 74.7 110.8

2005 2010 2015

Americas

82.8 117

175.6

2005 2010 2015

Europe

10 17.6 29.4

2005 2010 2015

Middle East & Others

33.7 75 144.1

2005 2010 2015

Asia Pacific(excl. Japan)

38.1 36.2

39.4

2005 2010 2015

Japan

Year Total ($bn)

2005 222

2010 320

2015 499

Map 1 – Global expenditure on luxury branded products by region 2005 – 2015(f) ($bn)

Source: Verdict Research

As a result, the Global Luxury Houses have emerged from the financial crisis much faster and stronger than most businesses. Burberry, Gucci Group, Hermes, LVMH, Polo Ralph Lauren and Richemont have all revealed strong sales growth, with some recording record sales in the last year. Expanding store networks has driven growth, particularly across the Asia Pacific region, where retail operations typically outperform the rest of the business elsewhere in the world. Despite this rapidly expanding region, London and the West remains a core, mature and key market for international luxury retail.

04 | Jones Lang LaSalle

A leading global city with destination appeal…London ranks number one in the world in terms of international visitors, with close to 17 million expected in 2012, up 1.1% on 2011 (Mastercard Global Destination Cities Index, 2012). In Jones Lang LaSalle’s ‘Global 300’ ranking, which ranks global cities based on population GDP, connectivity, corporate presence, office stock and real estate investment volumes, it comes in third, just behind New York and Tokyo but ahead of its European counterparts Paris and Madrid.

London’s diverse DNA is undoubtedly its unique selling point. Investors, retailers and shoppers are not only attracted to the city because of its position as a top global financial powerhouse, but also because it is steeped in history and has a strong heritage.

As a retail destination, London ranks alongside the best leading global cities, including New York, Paris, Milan, Hong Kong and Shanghai. Its diverse offer has global retail appeal and it is often the first port of call for international brands when looking to expand into Europe. According to Jones Lang LaSalle’s 2011 Cross Border Retail report, London ranks number one in Europe, boasting the largest number of international brands when compared to 55 other leading European cities.

There are a whole host of drivers that make London attractive and successful, but understanding its make-up is crucial for anyone looking to invest in the city, be it a retailer looking to open a flagship store, or an international investor looking for investment opportunities.

Jones Lang LaSalle has identified 12 key components that make London stand out ahead of its global competitors for visitors, retailers and real estate investors alike:

Global Financial Centre – London’s position as a top financial centre brings with it real estate that is fit for purpose for global occupiers with strong covenants. While London’s exposure to financial & business services increases market volatility, its top ranking position undoubtedly channels global capital and attracts leading global enterprise.

Liquidity – even in the worst market conditions, there is an exit strategy for investors. London is perceived as a mature and transparent market, making it an attractive investor destination.

Stock – London is the biggest market in Europe – there is quality real estate stock readily available, with new leases to high calibre occupiers.

Lease Lengths – the institutional nature of UK real estate has created an investment market geared towards the investor. Leases are typically longer than for the rest of the UK, and in many cases secured on a better quality of building than in other global markets.

Tenure – the guarantee of title may be taken for granted by domestic investors, but not by overseas investors. Freehold is the most desired tenure for many, but more experienced overseas investors are embracing the leasehold structure.

Transparency – independent research, data and industry scrutiny from the press, advisors and equity analysts all serve to create a very transparent and comprehensible market. The Jones Lang LaSalle Transparency index ranks the UK as the 3rd most transparent real estate market globally (retail adjusted) after the US and the Netherlands.

Professional Advice – the law firms and surveying practices operating in London often come with a platform which enables a consistent level of advice across the globe. In such a competitive market it is also a source of comfort that there is no monopolistic practice.

Tax – UK investment offers an investor-friendly regulatory framework and tax regime to overseas investors, with no barriers to real estate ownership and to the transfer of funds in and out of the country.

Currency – the devaluation of Sterling after the 2008 global economic crisis made the price of UK real estate even more competitive, and divesting out of “riskier” currencies into Sterling has emerged as a contemporary defensive play. With recent uncertainty in the Eurozone, Sterling has increased its appeal to many global investors.

Why London?

London Luxury Quarter | 05

Familiarity – a “soft” factor maybe, but a very important one. Investors naturally prefer to invest in areas which they are familiar with. In London, this has sometimes rather patronisingly been described as a “monopoly board mentality”, but in reality it derives from investors already having strong cultural (or even colonial) links with London, as well as a working knowledge of assets and strategy, either directly or from contemporaries.

Schooling & Education – home to globally recognised schools and universities, for higher net worth investors, schooling of relatives has provided familiarity and an opportunity to purchase residential property. This fosters an understanding of London real estate practice which migrates into the commercial sector. The escalation in tuition fees has already driven more overseas students into our universities at the expense of domestic students. According to UCAS there were 1.8 million full time undergraduate students in higher education last year, of which 5.7% were international.

Heritage, Culture & Language – multi-cultural London (reports suggest one in three Londoners are from an ethnic minority group), heritage, quality of life (especially for higher net worths) and the English language make London an attractive place to invest, work and live.

Each of the 12 factors above play their part in contributing to London’s global appeal and success. History has demonstrated that should temporary competitiveness be lost in some areas, London has a strong and broad based DNA that more than compensates, and helps it retain its strong, leading global position.

06 | Jones Lang LaSalle

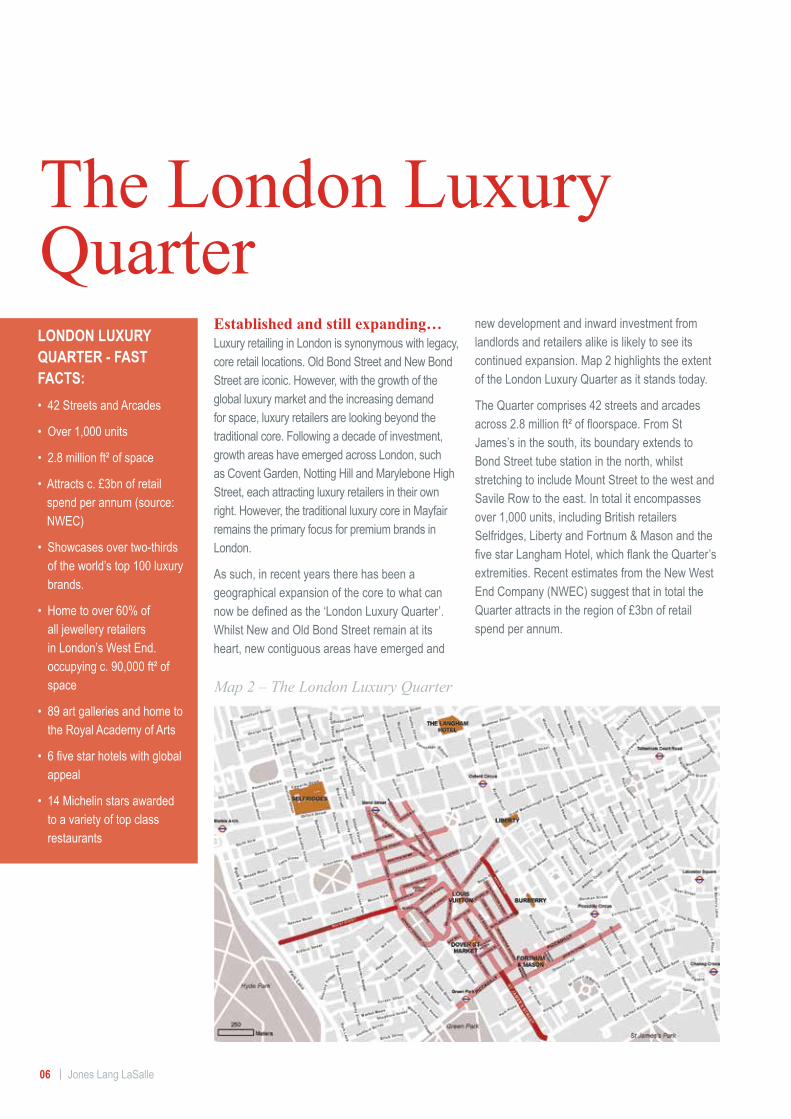

Established and still expanding…Luxury retailing in London is synonymous with legacy, core retail locations. Old Bond Street and New Bond Street are iconic. However, with the growth of the global luxury market and the increasing demand for space, luxury retailers are looking beyond the traditional core. Following a decade of investment, growth areas have emerged across London, such as Covent Garden, Notting Hill and Marylebone High Street, each attracting luxury retailers in their own right. However, the traditional luxury core in Mayfair remains the primary focus for premium brands in London.

As such, in recent years there has been a geographical expansion of the core to what can now be defined as the ‘London Luxury Quarter’. Whilst New and Old Bond Street remain at its heart, new contiguous areas have emerged and

new development and inward investment from landlords and retailers alike is likely to see its continued expansion. Map 2 highlights the extent of the London Luxury Quarter as it stands today.

The Quarter comprises 42 streets and arcades across 2.8 million ft² of floorspace. From St James’s in the south, its boundary extends to Bond Street tube station in the north, whilst stretching to include Mount Street to the west and Savile Row to the east. In total it encompasses over 1,000 units, including British retailers Selfridges, Liberty and Fortnum & Mason and the five star Langham Hotel, which flank the Quarter’s extremities. Recent estimates from the New West End Company (NWEC) suggest that in total the Quarter attracts in the region of £3bn of retail spend per annum.

The London Luxury QuarterLONDON LUXURY QUARTER - FAST FACTS:• 42 Streets and Arcades

• Over 1,000 units

• 2.8 million ft² of space

• Attracts c. £3bn of retail spend per annum (source: NWEC)

• Showcases over two-thirds of the world’s top 100 luxury brands.

• Home to over 60% of all jewellery retailers in London’s West End. occupying c. 90,000 ft² of space

• 89 art galleries and home to the Royal Academy of Arts

• 6 five star hotels with global appeal

• 14 Michelin stars awarded to a variety of top class restaurants

Map 2 – The London Luxury Quarter

London Luxury Quarter | 07

Best of British…Set within the heart of London, and surrounded by the heritage and culture of Mayfair, the Quarter showcases some of the best of British luxury retailers. From the Mulberry and Alexander McQueen flagships stores on Bond Street, to the Stella McCartney and Matthew Williamson stores on Bruton Street, it is the go-to destination in London for those seeking the latest British trends. Savile Row, famed all over the world for its traditional men’s bespoke tailoring, is anchored by Gieves & Hawkes, a brand internationally recognised for its quintessentially British style and craftsmanship. British jeweller Asprey, a brand synonymous with refinement and luxury, and menswear retailer Alfred Dunhill also have stores within the boundaries of the Quarter. High-end British fashion brands Belstaff and Burberry are continuing to embrace their roots by reaffirming their commitment to the area with new flagship stores. But competition for space is fierce; Belstaff recently agreed a record rent for a store in the traditional core.

Leading the way for International brands…The Quarter also has a strong presence from international luxury brands, highlighting its global appeal. French fashion houses Hermes and Chanel have resided in the Quarter for over 30 years, and later this year Chanel will open a second store which will more than quadruple its floorspace in the area. Louis Vuitton cemented its presence in 2010 when it opened a new flagship store, and earlier this year Italian shoe and accessories retailer Salvatore Ferragamo extended the lease and size of its New Bond Street store. Missoni has revealed plans to open a second store in the Quarter, and Swiss jeweller Piaget has secured a central pitch.

More recent international arrivals include Fendi, which has agreed a deal to open a flagship and European HQ in the former Mallet unit on New Bond Street, whilst Celine, owned by LMVH, and leading fashion designer Oscar de la Renta, have recently agreed deals to open on Mount Street.

There has been interest in the Quarter from more aspirational premium brands that wish to trade alongside the luxury brands. Chinese apparel retailer Bosideng recently opened on South Molton Street and US chain Victoria Secret’s has opened a UK flagship on New Bond Street.

In total, more than two thirds of the world’s Top 100 Luxury Brands, as defined by Jones Lang LaSalle, are located within the boundaries of the London Luxury Quarter. This figure reflects a 42% increase on 2005, showing the growth in the sector and the attractiveness of the Quarter to global luxury brands. The strength of trade in the area has resulted in some luxury brands now being multi-sited. Jimmy Choo, Cartier, Burberry, Ralph Lauren and Vivienne Westwood are just a few notable retailers that have representation from more than one store.

The powerhouse luxury brands dominate much of the Quarter, particularly in the traditional core. However, the growth of the area has not only been driven by the big luxury houses, but also by demand from smaller luxury brands looking for space alongside the well-known premium brands. South Molton Street’s proximity to the core has recently attracted French boutique chains Maje and Aubade, whilst Orelar Brown, a tailored men’s beach and swimwear boutique has opened on Vigo Street, hoping to take advantage of its location adjacent to Savile Row. In addition, British designer Alice Temperley has recently agreed terms to open a store on Bruton Street alongside her UK fashion counterparts Stella McCartney and Matthew Williamson. Hay Hill and Grafton Street have also attracted the attention of the acquisitive smaller luxury brands. High end fashion brand Vanessa Bruno and luxury interior designer Anna Casa have recently taken spots in these locations.

Attracting new, niche and specialist…The opening of Dover Street Market in 2004 was also significant as it provided new and upcoming ‘discovery brands’ with the opportunity to trade under the same roof as more established brands. It has become an important destination in its own right for shoppers looking for a new and unique shopping experience.

The Quarter is also home to over 60% of all jewellery retailers found in London’s West End. Research from the New West End Company claims this is one of the largest concentrations of jewellery in the world given the mix of brands and collections on offer. World renowned jewellers such as Bulgari, Cartier, Graff, Harry Winston, Tiffany’s and Piaget all have flagship stores in the Quarter, whilst more specialist jewellers have presence in some of the Quarter’s historic arcades. In total, over 90,000 ft² of space is dedicated to the sector.

08 | Jones Lang LaSalle

KEY NEW LUXURY ENTRANTS TO THE QUARTER IN 2012:• Alice Temperley

• Annoushka

• Belstaff

• Celine

• Fendi

• Isabel Marant

• Oscar de la Renta

Beyond Retail and the development of the social sceneWhat differentiates the London Luxury Quarter from any other global luxury destination in the world is the depth and choice of offer, which extends beyond traditional retailing. The key components of the Quarter that are ‘beyond retail’ can be summarised as follows:

Business: Leading Office Accommodation• Set within a leading business district, the

Quarter contains over 715,000 ft² of boutique office space, which accommodates global institutions and niche financial expertise (Hedge Funds, Private Offices).

• The prestigious location, surroundings and ancillary cultural and leisure facilities make it a sought after location for financial expertise, in particular for high net worth individuals.

• Its proximity to key clients and leisure amenities, and associated benefits to brand image, only add to its attractiveness as a location.

Living: High End Residential• Proximity to commerce, retail, restaurants, clubs,

theatres, heritage and culture attracts a global appetite for living in the Quarter, which is home to some of London’s most sought after addresses.

• Prime residential values have remained resilient throughout recent years, buoyed by demand from international investors, and values in the Quarter are some of the highest in Central London.

• Demand continues - there are six new residential developments within the boundaries of the Quarter that have been granted planning permission. They include the Grafton Street / Bruton Lane development which will comprise of 11 self-contained private flats and the redevelopment of 27 Albermale Street by Bremantel International which plans six new apartments.

Culture: The Arts• The Quarter is home to the world renowned

Royal Academy of Arts. In early 2012, the David Hockney exhibition was held there and

generated a buzz in the art world that provoked interest in the art galleries in the nearby vicinity of the Quarter.

• Berkeley Square hosts a variety of cultural events including PAD - London’s leading fair for 20th Century art and design. The event offers visitors a place to discover and purchase iconic works from prominent international galleries.

• In total there are 89 art galleries and dealers within the boundary which together occupy over 160,000 ft² of space. They include the Halcyon Gallery, one of Europe’s leading contemporary art galleries, and the Fine Art Society, which specialises in British 19th and 20th Century art and design.

Tourism: Globally Recognised Leading Hotels• The Quarter boasts a number of luxury hotels,

six of which are internationally renowned five star venues: Browns, The Connaught, Claridges, The Ritz London, The Langham and The Westbury

Dining: World Renowned Restaurants• The number of restaurants located in the Quarter

has risen in recent years. At present there are 59 open across 155,000 ft² of space – this reflects a 17% rise in floorspace since 2005.

• Recent entrants include Hakkasan on Bruton Street, which has already been awarded a Michelin star, Aubaine on Dover Street, Novikov on Berkeley Street and Aurelia on Cork Street.

• There are a total of 14 Michelin stars in the area with Hibiscus, The Square and Helen Darroze at the Connaught each holding two. Other prestigious restaurants include The Wolseley and Nobu.

Leisure: Exclusive Private Member Clubs and Casinos• A growing number of exclusive new era private

member clubs, easily accessible to the high net worth clientele who visit, live and/or work in the area, are present within the Quarter. These include, but not limited to: Annabels, Dunhill, Mortons, Mark’s Club and George.

London Luxury Quarter | 09

• The Arts Club on Dover Street, originally founded in 1863, underwent a complete renovation in 2011. It was totally transformed into a truly world class establishment for those involved in art, literature or science to meet, exchange ideas, entertain and relax.

• The Ritz Club, featuring an exclusive casino and private gaming room, sits within The Ritz London hotel, attracting high net worth gamers.

Other: Various • Auction Houses – the Quarter is home to Sotheby’s, Bohams and

Christies, three of the most distinguished leaders in the auction world.

• Motoring – a number of luxury car brand showrooms are located within the confines of the Quarter, from Bentley, Bugatti and Rolls Royce to Jaguar and Porsche.

• Yachting – Grafton Street is home to Camper & Nicholson, the global leader in all luxury yachting activities. Princess and Sunseeker also provide yachting services within the Quarter.

• Sport –British gun-maker Holland and Holland trades on Bruton Street, selling bespoke sporting rifles and shotguns and Berretta, one of the oldest firearms manufacturers in the world, is located on St James’s Street. Purdy’s and William & Son are close by in Mount Street.

• Specialist – and last but not least, the Quarter is home to a variety of small independent retailers that are specialists in their respective fields. There are a number of renowned wine merchants, including Jeroboams on Davies Street, Berry Brothers on St James’s and the Hedonism Wines on Davies Street, in addition to specialist butchers (Allens of Mayfair on Mount Street), cheese-mongers (Paxton and Whitfield on Jermyn Street), barbers, perfumers and chemists trading in the Quarter.

This diverse offer beyond core retail is key to attracting people to the Quarter. The complementary mix of retail, leisure, services and tourism has positive spin-off effects for all. The ability to shop, work, live and socialise in the Quarter contributes to it being a truly sustainable and unique location.

Who shops in the LLQLocal, European and Global shopper appeal…The location of the London Luxury Quarter results in a very diverse consumer base.

The resident and local catchment population is dominated by affluent demographic groups. According to the CACI Acorn classification, prosperous and well educated residents are on the Quarter’s doorstep in abundance. Perhaps unsurprisingly, within 1km of Bond Street, 86% of residents are from the most affluent urban groups in the country.

10 | Jones Lang LaSalle

The number one international consumer group, outside of the Eurozone, is the Middle East. In total it accounts for 26% of total international sales. However, the most significant growth has been from the Far East. Average spend from Thailand has surged 18% year-on-year, and from Malaysia it has increased 16%. China, the second largest non-European shopper group, saw 11% year on-on-year growth over the same period.

Drilling down a level, map 4 highlights where international sales specific to London’s West End and locations across the Quarter are coming from.

China is still the largest international consumer group in both the West End and on Bond Street, accounting for 16% and 28% of sales respectively. However, consumers from Russia are significant across all locations, contributing the highest proportion of international sales to retailers in Mayfair. Jermyn Street generates 16% of its international sales from the US.

US9% ➔

6

Brazil-1%

➔

9

Nigeria7% ➔

4

MiddleEast9% ➔

1

RussiaFed

1% ➔

3 HongKong13% ➔

8

India-2%

➔

10 Malaysia16% ➔

7

Thailand18% ➔

5

China11% ➔

2

% change year-on-yearJan-Jul 2011-12

Ranking (sales)

Bond StreetChina 28%

Russia Fed 8%

MayfairRussia Fed 8%

US 9% Jermyn StUS 16%

Nigeria 15%Russia Fed 10%

West EndChina 16%Kuwait 7%

Russia Fed 8%

Map 3 - % change in year-on-year International average spend in the UK and ranking by total contribution to sales

Map 4 – Origin of International Sales to London and the Quarter

In addition to the affluent local resident population, London and the Quarter has significant international appeal, which in recent years has been boosted by the depreciation of Sterling. Map 3 shows where the year-on-year growth in international spend (outside of Europe) is coming from, and ranks each market in terms of contribution to total UK sales.

Source: Global Blue, July 2012

Source: Global Blue, May 2012

London Luxury Quarter | 11

In Mayfair, sales from Indonesia and Qatar more than doubled in the period between January and May 2012 compared to the previous year. Bond Street has also benefited from these visitors, with sales from Qatar up 79% and Indonesia up 65%.

Bond Street1. Qatar - ➔79%2. Indonesia - ➔65%3. Japan - ➔58%

Mayfair

Jermyn St

West End

1. Indonesia - ➔148%2. Qatar - ➔102%3. UAE - ➔99%

1. China - ➔108%2. Pakistan - ➔74%3. India - ➔20%

1. Qatar - ➔78%2. China - ➔50%3. Malaysia - ➔35%

Map 5 – Top 3 international markets fuelling growth across London and the Quarter (year-on-year)

The global appeal of London is soaring, particularly in the Far East. Map 5 ranks the top three markets that are fuelling the growth in international sales across the same geography.

Economic growth in China is still a key driver of international sales in the West End, up 50% May 2012 on last year. The boom in Far Eastern sales in Jermyn Street shows that international shoppers are willing to shop outside the traditional retail core and explore new areas. This is positive news for the Quarter and its future growth prospects, especially when considering Grosvenor’s development plans in north Mayfair and The Crown Estate’s plans for investing in St James’s.

Source: Global Blue, May 2012

12 | Jones Lang LaSalle

Increasing need for serviceWhile the luxury sector has proved itself adept at nurturing customers, despite the continuing global uncertainty over economies and the growth of on-line shopping, there remain real challenges. Retailers continually need to offer something more.

Luxury retailers have historically benefited from shoppers wanting to touch and feel a product before they spend their hard-earned cash. However, with the rise and success of websites such as net-à-porter, which is dedicated to the luxury shopper, retailers need to consider what more they can do – use of mobile technology for instance to drive footfall and provide information to potential customers. They need to focus even more on service and the in-store experience to become entertainers, comperes, theatre producers, masters of ceremonies, butlers, concierges, pamperers, flatterers, psychologists, social workers and more, in order to compete.

The diverse consumer base that the Quarter attracts adds another dimension for retailers to consider. From the discreet European shopper, to the more conspicuous Far Eastern consumers, retailers need to tailor their services to the varying cultural demands. A chauffeur driven service to the store entrance may be a luxurious service for the more ostentatious shopper, but a back door entrance with private dressing area may be favoured by other more private individuals.

In a bid to provide an unrivalled service, retailers in the Quarter need to adapt to and keep up with the changing and sometimes challenging demands and needs of its shoppers. Not only do consumers want an experience, but they also want to know everything about a product before they buy. As such, specialist knowledge is key. Competition for the best employees is intense, with retailers wanting only the top employees with expert product knowledge and language skills.

There is already evidence of retailers in the Quarter adapting to this changing retail environment. The new Chanel store, due to open in the Quarter later this year, will feature a private VIP area on its second floor. This follows in the footsteps of the Louis Vuitton store which incorporated this service into its 2010 redevelopment. Graff, Cartier and many of the high end jewellers frequently provide parking outside their stores to meet the needs of their clientele, who like to arrive safely in chauffeur driven cars. Stella McCartney on Bruton Street has a back entrance that offers its customers privacy from the general public. Likewise, the new Temperley store set to open on the same street will have discreet rear access.

London Luxury Quarter | 13

Retail investment and development in the QuarterRetail investment goes from strength to strength… The London Luxury Quarter is an attractive market for investors thanks to constrained supply, sustained demand and the rise in rents and values over recent years. As such, retail investment activity has been on a general upward trend over the last 10 years. Fig 1 – Total Value of Retail Transactions in the Quarter from 2002 - 2011

Table 1 – Top Investment Deal in the Quarter 2002 – 2011

In total, $2.9 bn worth of deals was transacted in the Quarter between 2002 and 2011. 2011 saw a significant increase in the total value of retail investment transactions, up almost 50% on 2010 to just shy of $650 mn. The sale of 17-20 New Bond Street for over $255 mn to LVMH (the largest deal of the last 10 years in terms of total value) significantly boosted this figure.

The increasing value of property in the Quarter is clear. In 2011 there was just one more transaction recorded than 2002; however the total value of deals transacted was more than three times as much.

As table 1 demonstrates, with the exception of 2007, when a deal on Berkeley Street topped the table, the most expensive investment deal in each year over the last decade was for properties located on Bond Street. This highlights the street’s continued appeal to investors looking for secure assets that offer a safe haven against the global economic uncertainty. However, with continued investment, and the Quarter’s boundaries extending beyond the core of Bond Street, investors are beginning to look for assets located on the neighbouring streets.

20020 0

100,000,000

200,000,000

300,000,000

400,000,000

500,000,000

600,000,000

700,000,000

2

4

6

8

10

12

No. o

f Tra

nsac

tions

Total

Valu

e $

2003 2004 2005 2006 2007 2008 2009 2010 2011

Year Address Price in $ (‘000) Purchaser

2002 25 Old Bond Street 43,000 Tiffany & Co

2003 39-42 New Bond Street 54,300 David Daly

2004 Burlington Arcade 128,300 Bermudan Trust Fund

2005 167 New Bond St 75,160 Quinlan Private

2006 105-106 New Bond St 47,500 Winrunner Ltd

2007 15 Berkeley St 63,600Invista Real Estate Investment Management

2008 17-20 New Bond St 119,200 David Daly

2009 167 New Bond St 114,000 Hermes

2010 6-8 Old Bond Street 107,000 Giuseppe DeLonghi

2011 17-20 New Bond St 255,300 LVMH

Source: Real Capital Analytics, June 2012

Source: Real Capital Analytics, June 2012

14 | Jones Lang LaSalle

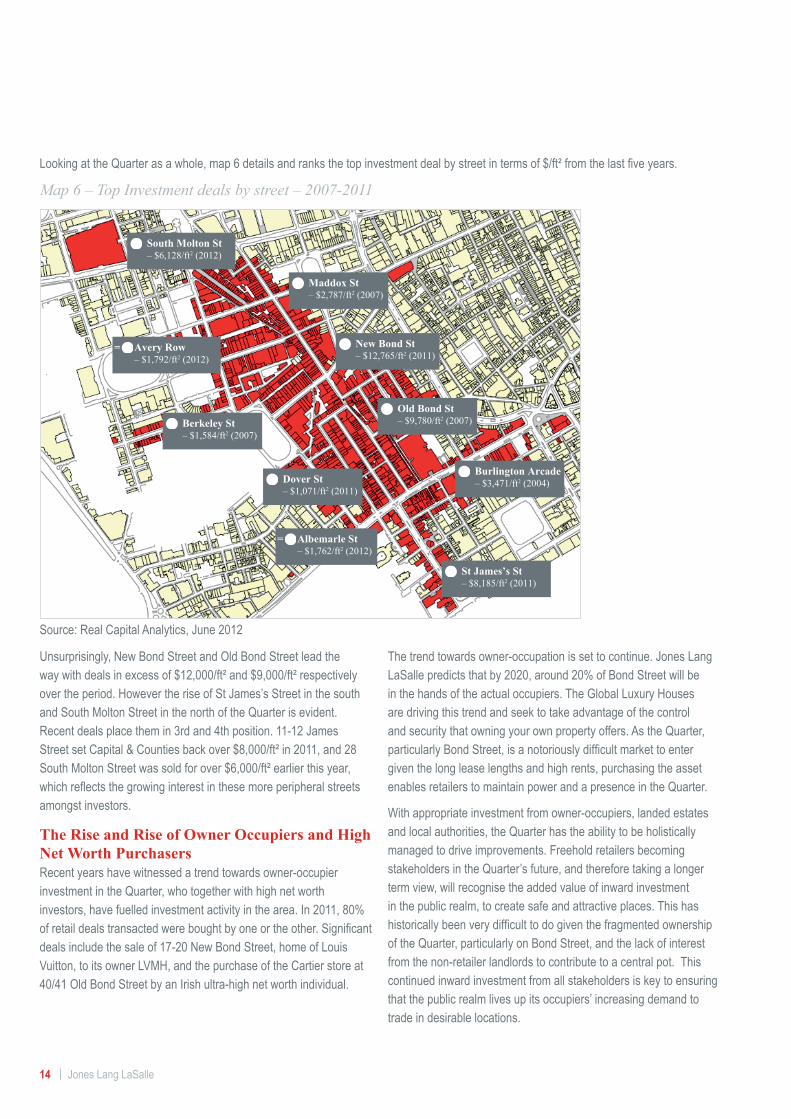

Looking at the Quarter as a whole, map 6 details and ranks the top investment deal by street in terms of $/ft² from the last five years.

South Molton St– $6,128/ft2 (2012)

6

Dover St– $1,071/ft2 (2011)

9

Berkeley St– $1,584/ft2 (2007)

8

Avery Row– $1,792/ft2 (2012)

= 7

Albemarle St– $1,762/ft2 (2012)

= 7

Old Bond St– $9,780/ft2 (2007)

2

New Bond St– $12,765/ft2 (2011)

1

Maddox St– $2,787/ft2 (2007)

6

Burlington Arcade– $3,471/ft2 (2004)

5

St James’s St– $8,185/ft2 (2011)

3

Map 6 – Top Investment deals by street – 2007-2011

Unsurprisingly, New Bond Street and Old Bond Street lead the way with deals in excess of $12,000/ft² and $9,000/ft² respectively over the period. However the rise of St James’s Street in the south and South Molton Street in the north of the Quarter is evident. Recent deals place them in 3rd and 4th position. 11-12 James Street set Capital & Counties back over $8,000/ft² in 2011, and 28 South Molton Street was sold for over $6,000/ft² earlier this year, which reflects the growing interest in these more peripheral streets amongst investors.

The Rise and Rise of Owner Occupiers and High Net Worth PurchasersRecent years have witnessed a trend towards owner-occupier investment in the Quarter, who together with high net worth investors, have fuelled investment activity in the area. In 2011, 80% of retail deals transacted were bought by one or the other. Significant deals include the sale of 17-20 New Bond Street, home of Louis Vuitton, to its owner LVMH, and the purchase of the Cartier store at 40/41 Old Bond Street by an Irish ultra-high net worth individual.

The trend towards owner-occupation is set to continue. Jones Lang LaSalle predicts that by 2020, around 20% of Bond Street will be in the hands of the actual occupiers. The Global Luxury Houses are driving this trend and seek to take advantage of the control and security that owning your own property offers. As the Quarter, particularly Bond Street, is a notoriously difficult market to enter given the long lease lengths and high rents, purchasing the asset enables retailers to maintain power and a presence in the Quarter.

With appropriate investment from owner-occupiers, landed estates and local authorities, the Quarter has the ability to be holistically managed to drive improvements. Freehold retailers becoming stakeholders in the Quarter’s future, and therefore taking a longer term view, will recognise the added value of inward investment in the public realm, to create safe and attractive places. This has historically been very difficult to do given the fragmented ownership of the Quarter, particularly on Bond Street, and the lack of interest from the non-retailer landlords to contribute to a central pot. This continued inward investment from all stakeholders is key to ensuring that the public realm lives up its occupiers’ increasing demand to trade in desirable locations.

Source: Real Capital Analytics, June 2012

London Luxury Quarter | 15

Map 7 – Major developments across the Quarter

Table 2 – Details of Major Developments in the Quarter

Map Number

Address Size (ft²)

Details Stage

1 28 South Molton Street 14,000 Retail & Office Development - Bosideng

Opened August 2012

2 101 New Bond Street 50,000 Office Development Pre-planning

3 111-115 New Bond Street

16,500 Retail Development - Victoria’s Secret

Opened September 2012

4 135-137 New Bond Street

25,000 Retail Development - Belstaff

Under construction

5 8-10 Grafton Street 60,500 4,500 ft² retail & 56,000 ft² office space

Pre-planning

6 49 – 51 Conduit Street & 24 Savile Row

31,500 9,000 ft² retail & 22,500 ft² office space

Due summer 2013

7 Crossrail, 64 – 72 Bond Street

291,000 44,000 ft² retail & 247,000 ft² office space

Construction strart 2015

8 34 – 36 Bruton Street 20,000 7,500 ft² retail & 12,500 ft² office space

Construction strart 2013

9 158 – 159 New Bond Street

40,000 Retail Development Chanel

Due December 2012

10 Burlington Arcade 37,500 Retail Development Pre-application

11 St James’ Gateway 100,000 23,000 ft² retail, 57,000 ft² office & 18,000 ft² residential

Due 2013

12 121 Regent Street 20,000 Retail Development - Burberry

Opened September 2012

Major Retail DevelopmentsThe retail property market in London has enjoyed a period of strong growth, driven by retailers competing for space. However, the demand and supply imbalance means that future development is essential to sustain growth and provide new retailers with the opportunity to enter the market. At present there are 12 key developments, either under construction or in the pipeline, that are shaping the future of the Quarter.

Demand for space from powerhouse brands is driving development in the Quarter. British brand Belstaff will anchor a new development at 135-137 New Bond Street, and iconic luxury retailer Burberry has recently opened its largest flagship store on the periphery of the Quarter. Chanel will open a second store on Old Bond Street later this year.

The Crossrail development at 111-115 New Bond Street is the largest development in the pipeline. At just short of 300,000 ft², the majority of the development will be dedicated to office space, but it will feature 44,000 ft² of retail space.

In addition, The Crown Estate’s development of St James’s Gateway, set to complete next year, will add 23,000 ft² of retail space and create a new and vibrant mixed-use district in the south of the Quarter that will attract shoppers, workers and residents alike.

Public Realm Improvements If landlords want to attract the top occupiers and customers globally, then it is essential that they too adapt to the changing retailing environment, and keep up with increased demands. This is particularly true in the Quarter, as shoppers expect a shopping environment that matches the luxury retail offer. Major landlords Grosvenor and The Crown Estate, which own Mount Street and St James’s respectively, have taken advantage of their block ownership and are co-ordinating projects that aim to create ‘places’ that offer more than just retail.

Source: Jones Lang LaSalle, July 2012

16 | Jones Lang LaSalle

Case studyGrosvenor - Mount Street Public Realm Improvements AimTo create a distinctive and vibrant destination for high quality shopping that attracts not only domestic but international high end shoppers and brands to Mount Street.

• improving the street furniture – benches/bins etc.

• better street lighting

• clear pavements, greenery

• enhancing the existing architecture

• improving linkages with other streets

London Luxury Quarter | 17

Opportunities and challengesLondon – A Leading Global CityLondon will continue to be challenged by other global cities. To support future growth of the Quarter, it must maintain its leading position and continue to attract visitors, occupiers and investors alike. Its unique DNA should be nurtured, as the strength of this places it ahead of its competitors and is what will drive future growth.

RetailThe strength of the Quarter as a luxury shopping destination has been underpinned by the diverse mix of brands. From the start-ups to the established, it is a sought after location for luxury retailers across the world. British-born brands have historically provided the backbone to the Quarter, and have played a crucial role in shaping its success to date.

With the increasing influence of the global luxury powerhouses, it is vital that the Quarter continues to provide opportunities for the new and emerging brands in order to maintain the vibrant and unique character that has shaped its evolution. In a location steeped with British heritage, it is also essential that support is given to domestic brands so that the unique charm of the area is not diluted by the arrival of international brands.

A number of major retail destinations across the country now have extended opening hours; in some locations retailers trade until 10pm on a daily basis. Across London’s West End, this is particularly true, however in the Quarter the majority of retailers still only trade between the traditional trading hours of 10am-6pm. This is fast becoming a contentious issue. In a retail market where shoppers demand convenience, there are concerns that the limited shopping hours could have a detrimental effect on trade as consumers choose to shop in other more convenient ways, be it online or in other retail locations.

Beyond Retail & Place MakingAs mentioned, the depth and choice in the Quarter is what differentiates it from any other luxury retail destination across the world. Not only does it showcase an unrivalled mix of retail brands, but also an offer that extends beyond the realms of what is considered ‘traditional retail’. It is this variety that makes it a unique location and allows for place-making.

The challenge facing the development of the ‘beyond retail’ offer across the Quarter comes back to ownership. Landlords can generally generate higher rents from a luxury retailer compared to a restaurant or art gallery occupier, for example, and therefore individual landlords will always strive to get the best deal possible.

In locations where there is block ownership, such as Mount Street, St James’s and Burlington Arcade, the ability to grow the ‘beyond retail’ offer is far easier as the landlord will directly reap the long-term benefits of place-making through a diversified offer. Holistic management of the Quarter is required to ensure the vibrancy and vitality is preserved, be that through landlords working together or through local authority influence.

18 | Jones Lang LaSalle

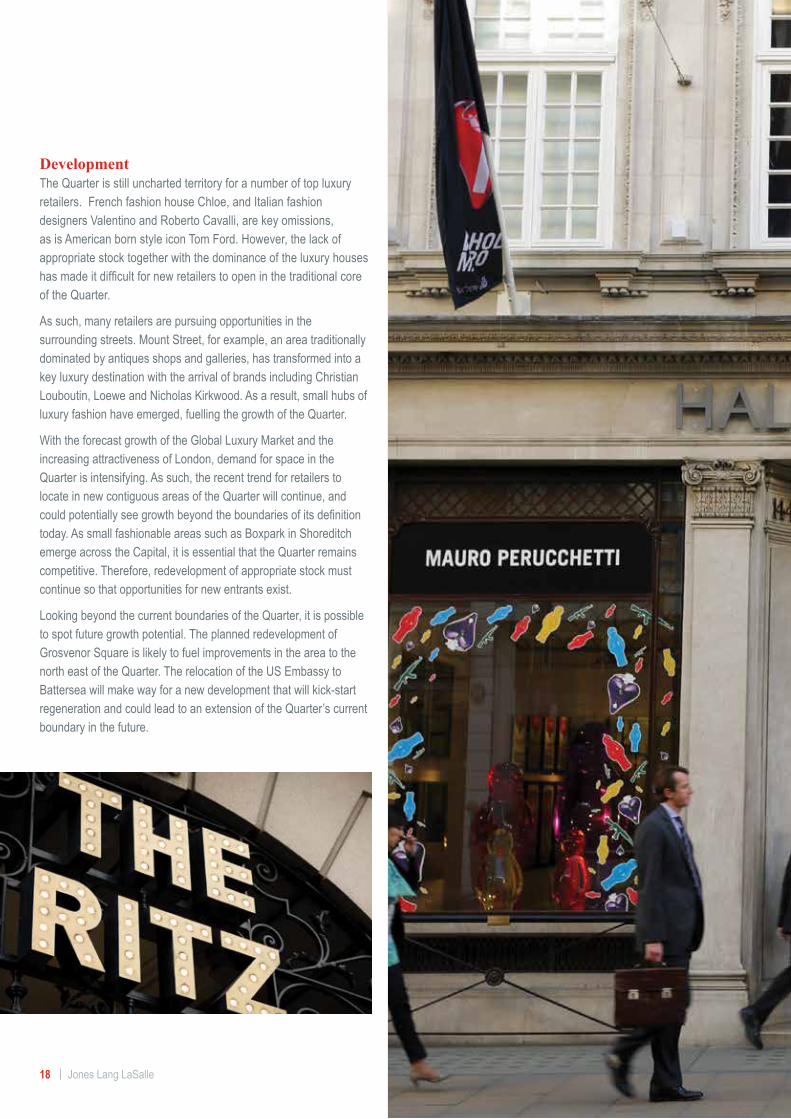

DevelopmentThe Quarter is still uncharted territory for a number of top luxury retailers. French fashion house Chloe, and Italian fashion designers Valentino and Roberto Cavalli, are key omissions, as is American born style icon Tom Ford. However, the lack of appropriate stock together with the dominance of the luxury houses has made it difficult for new retailers to open in the traditional core of the Quarter.

As such, many retailers are pursuing opportunities in the surrounding streets. Mount Street, for example, an area traditionally dominated by antiques shops and galleries, has transformed into a key luxury destination with the arrival of brands including Christian Louboutin, Loewe and Nicholas Kirkwood. As a result, small hubs of luxury fashion have emerged, fuelling the growth of the Quarter.

With the forecast growth of the Global Luxury Market and the increasing attractiveness of London, demand for space in the Quarter is intensifying. As such, the recent trend for retailers to locate in new contiguous areas of the Quarter will continue, and could potentially see growth beyond the boundaries of its definition today. As small fashionable areas such as Boxpark in Shoreditch emerge across the Capital, it is essential that the Quarter remains competitive. Therefore, redevelopment of appropriate stock must continue so that opportunities for new entrants exist.

Looking beyond the current boundaries of the Quarter, it is possible to spot future growth potential. The planned redevelopment of Grosvenor Square is likely to fuel improvements in the area to the north east of the Quarter. The relocation of the US Embassy to Battersea will make way for a new development that will kick-start regeneration and could lead to an extension of the Quarter’s current boundary in the future.

London Luxury Quarter | 19

20 | Jones Lang LaSalle

Travel & ConnectivityLondon’s excellent connectivity with the rest of the world will remain key to its success going forward. Its proximity to international transport hubs, including three major airports (Heathrow, Gatwick and Stansted) and the Eurostar, add to its global appeal.

In terms of passenger numbers, Heathrow is the busiest airport in the world. In order to meet future demand and to maintain the Capital’s future attraction, there are plans in the pipeline to build an additional runway at the airport to increase capacity.

On a more localised scale, the completion of Crossrail in 2018 will improve connectivity domestically across London. With its planned route through Bond Street station, the Quarter is likely to directly benefit from this major transport

development. Predictions from Crossrail estimate that the number of people using the station on a daily basis will increase by over 45% from 155,000 to 255,000. This increase in footfall has the potential to drive significant sales growth in the Quarter.

Heritage & CultureAlthough difficult to quantify, London’s heritage and culture has been fundamental to the city’s development to date. The attraction of the Capital as a place to invest, work and live in has been boosted by its multi-cultural vibrancy, lifestyle and unique character.

London has taken centre stage across the world by hosting the 2012 Olympics. This event has showcased its great diversity to the world and will leave a lasting legacy that will help shape the city’s future development.

London Luxury Quarter | 21

In conclusion…The London Luxury Quarter can deliver. Set within a unique, historic and culturally diverse backdrop, it is a destination with international appeal. Not only does it showcase some of the top global brands, but its assorted mix of retail, office, residential and leisure space sets it apart from any other luxury destination in the world. With projected growth of the global luxury market, there are significant opportunities for the Quarter to grow and extend beyond its current boundary. By building on its existing proposition, it will continue to attract occupiers, investors and shoppers alike.

Copyright © Jones Lang Lasalle IP, Inc. 2012.

This publication is the sole property of Jones Lang LaSalle IP, Inc. and must not be copied, reproduced or transmitted in any form or by any means, either in whole or in part, without the prior written consent of Jones Lang LaSalle IP, Inc. The information contained in this publication has been obtained from sources generally regarded to be reliable. However, no representation is made, or warranty given, in respect of the accuracy of this information. We would like to be informed of any inaccuracies so that we may correct them. Jones Lang LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication.

ContactsJones Lang LaSalle

Guy Grainger Head of UK Retail Tel: +44 (0)207 318 7824 Email: [email protected]

Martin Thomas Director – Central London Retail Tel: +44 (0)207 318 7802 Email: [email protected]

James Brown Head of EMEA Retail Research and Consulting Tel: +44 (0)203 147 1155 Email: [email protected]

Jennie Beattie Senior Retail Research Analyst Tel: +44 (0)207 087 5523 Email: [email protected]

New West End Company

Jace Tyrrell Director of Communications Tel: +44 (0)20 7462 0680 Email: [email protected]

Heart of London Business Alliance

Karen Baines Head of Marketing & Communications Tel: +44 (0)20 7839 3409 Email: [email protected]