THE RELATIONSHIP BETWEEN CAPITAL INFLOWS AND THE REAL EXCHANGE RATE IN VIETNAM Nguyen Thi Vu Ha, PhD...

40

THE RELATIONSHIP BETWEEN CAPITAL INFLOWS AND THE REAL EXCHANGE RATE IN VIETNAM Nguyen Thi Vu Ha, PhD Student - VNU Supervisors: Prof. Nguyen Hong Son, Dr. Nguyen Manh Hung

-

Upload

mireya-burnap -

Category

Documents

-

view

245 -

download

8

Transcript of THE RELATIONSHIP BETWEEN CAPITAL INFLOWS AND THE REAL EXCHANGE RATE IN VIETNAM Nguyen Thi Vu Ha, PhD...

THE RELATIONSHIP BETWEEN CAPITAL INFLOWS

AND THE REAL EXCHANGE RATE IN VIETNAM

Nguyen Thi Vu Ha, PhD Student - VNU

Supervisors: Prof. Nguyen Hong Son,

Dr. Nguyen Manh Hung

Outline

Introduction

Brief Review of Literature

Overview of Capital Inflows to Vietnam

Overview of Foreign Exchange Market in Viet Nam

Capital Inflows to Vietnam and the real exchange rate

Preliminary Results

Conclusion

Introduction

Definition

• Capital inflows are defined as the increase in net international indebtedness of

the private and the public sectors during a given period of time

Two types of inflows

• Inflows that are driven by fundamental economic factors expected to be stable

• Inflows that are not driven by fundamental economic factors may be unstable

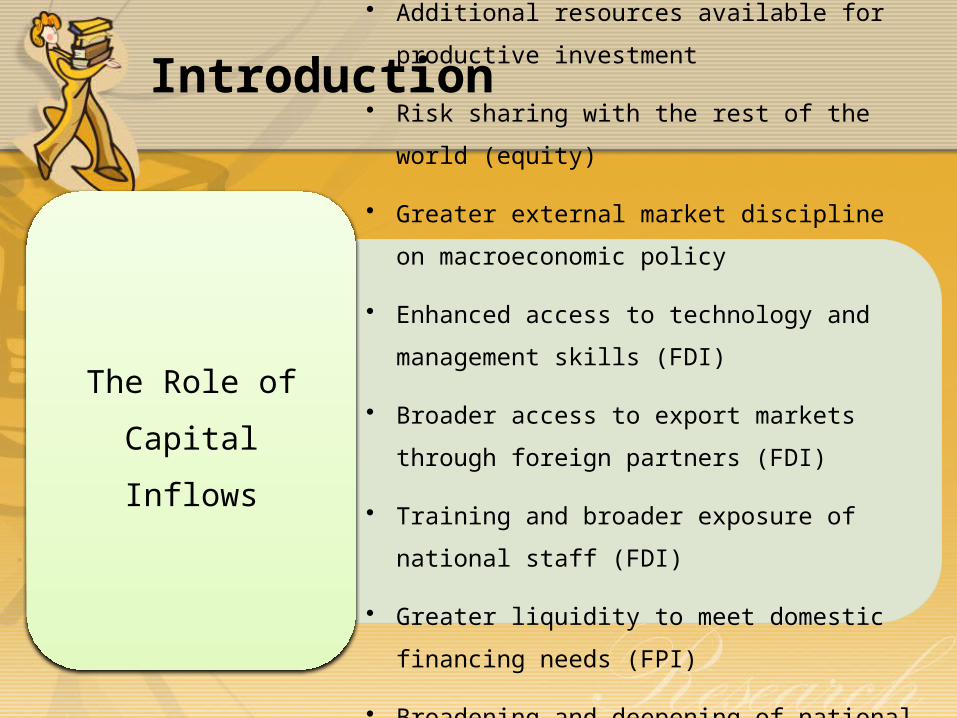

Introduction• Additional resources available for productive

investment

• Risk sharing with the rest of the world (equity)

• Greater external market discipline on

macroeconomic policy

• Enhanced access to technology and

management skills (FDI)

• Broader access to export markets through

foreign partners (FDI)

• Training and broader exposure of national staff

(FDI)

• Greater liquidity to meet domestic financing

needs (FPI)

• Broadening and deepening of national capital

markets (FPI)

• Improvement of financial sector skills (FPI)

The Role of Capital

Inflows

Introduction

But, capital inflows creates the pressure to push up the domestic

currency’s value against the foreign currencies such as the

United States (US) dollar

IntroductionIn Viet Nam, capital control

policies are applied to

change the scale and

structure of the capital

inflows to encourage long-

term capital sources,

especially when much

capital has been poured into

the financial investment and

real estate sector after Viet

Nam became the WTO

member.

The government should

carefully analyze the

impacts of the capital control

policy frameworks. The

failure to alter inappropriate

control policies may result in

the fall of GDP growth rate

and undermine price

stability.

Introduction

Research questions:

• How has capital inflow impacted the real effective

exchange rate in Viet Nam? and

• What are the effective measures to cushion the

effects of capital inflow on exchange rate?

Brief Review of Literature

An increased foreign capital inflow helps the host countries to achieve high economic growth but at the same time it creates problems:

• inflation pressures, high real exchange rate (with adverse effects on exports), loss of control over monetary policy, high dollarization (Greenville, 2008; Kwan, 1998);

• lower domestic saving, and fall in the domestic interest rate or the cost of capital (World Bank, 1996).

The impact depends on the volume of flows, the macroeconomic policy framework, the microstructure of the flows and the incentives in the financial sector (World Bank, 1996).

Brief Review of Literature

Capital inflows can create financial instability

(Kawai and Takagi, 2008).

• Capital inflows affect the financial system by pushing up equity and other

asset prices (the asset price inflation), reduce the quality of assets and

negatively affect the balance sheets of the banks or finance companies

because capital inflow often comes through financial sector.

• Recent experience suggests that the impact of capital inflows on asset

prices has been particularly significant (Greenville, 2008; andSchadler,

2008).

Brief Review of Literature

Measures to manage capital inflows are often

examined in different ways and different

dimensions.

• Some authors have looked at direct and indirect measures (Kwan, 1998)

while others concentrated in macroeconomic and structural measures

(Fernandez-Arias and Montiel, 1995; Grenville, 2008; and Schadler,

2008).

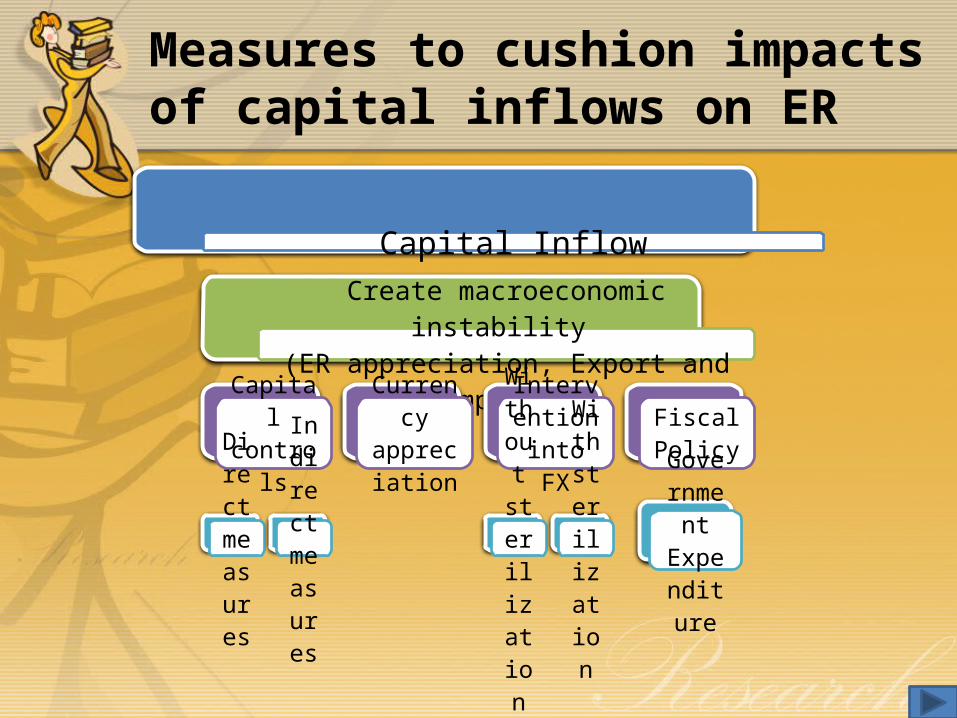

Measures to cushion impacts of capital inflows on ER

Capital Inflow

Create macroeconomic instability (ER appreciation, Export and Import)

Capital controlsDirect measures

Indirect

measures

Currency

appreciation

Intervention into

FXWithout sterilization

With sterilization

Fiscal PolicyGovernmen

t Expenditur

e

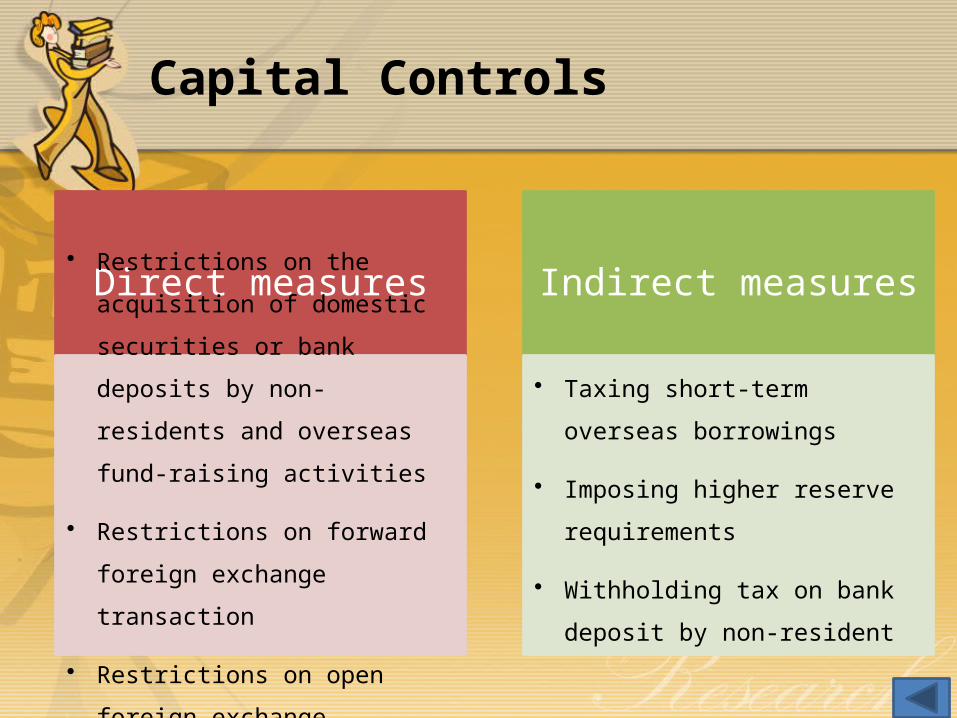

Capital Controls

Direct measures

• Restrictions on the acquisition of

domestic securities or bank

deposits by non-residents and

overseas fund-raising activities

• Restrictions on forward foreign

exchange transaction

• Restrictions on open foreign

exchange positions of banks

Indirect measures

• Taxing short-term overseas

borrowings

• Imposing higher reserve

requirements

• Withholding tax on bank deposit

by non-resident

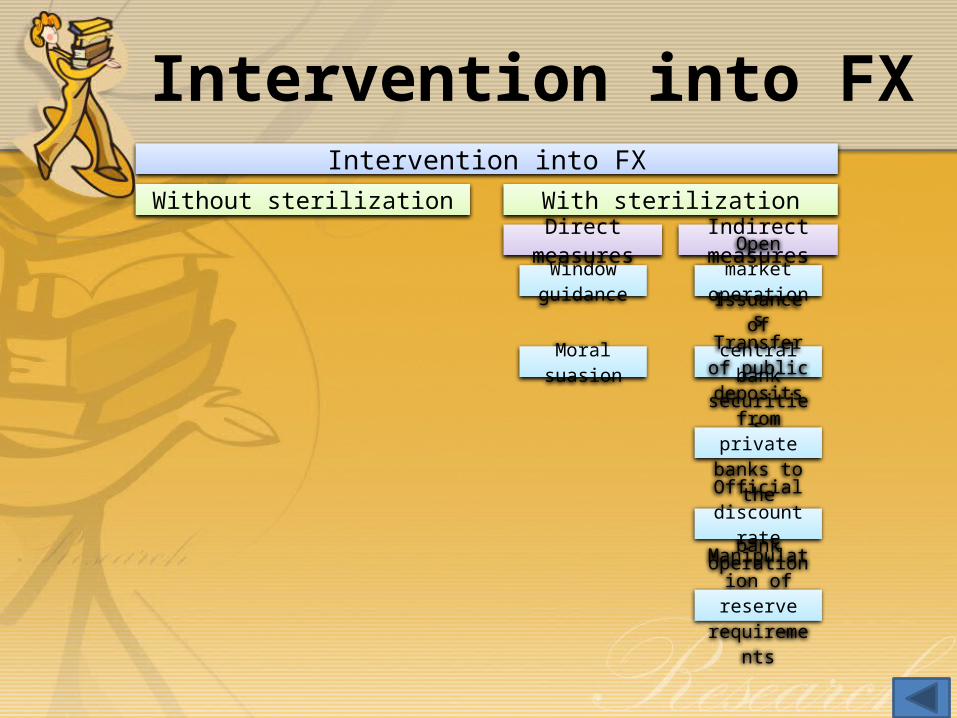

Intervention into FXIntervention into FX

Without sterilization With sterilizationDirect

measuresWindow guidance

Moral suasion

Indirect measures

Open market operations

Issuance of central bank

securitiesTransfer of public

deposits from private banks to the central bankOfficial discount rate

operation

Manipulation of reserve

requirements

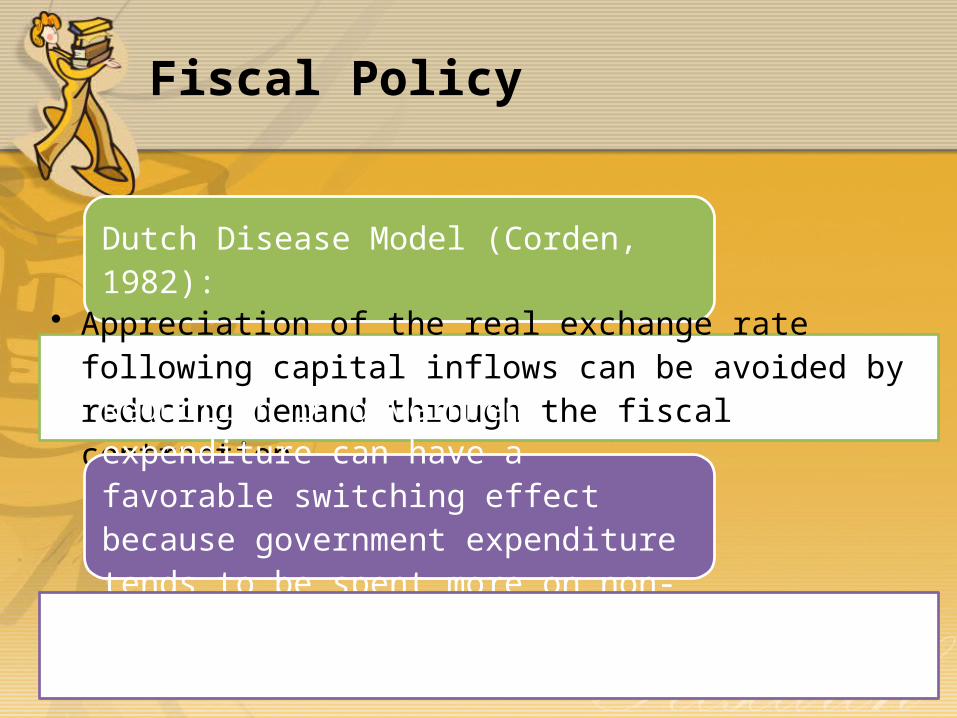

Fiscal Policy

Dutch Disease Model (Corden, 1982):

• Appreciation of the real exchange rate following capital inflows can be avoided by reducing demand through the fiscal contraction.

Reduction in government expenditure can have a favorable switching effect because government expenditure tends to be spent more on non-tradable goods (Athukorala, 2003)

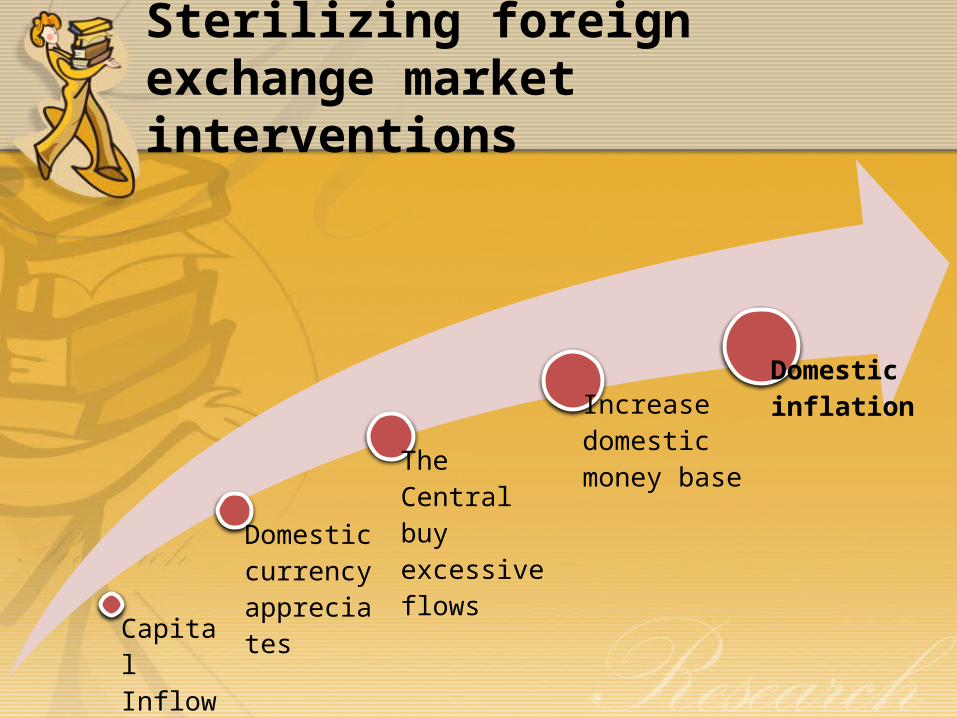

Sterilizing foreign exchange market interventions

Capital Inflows

Domestic currency appreciates

The Central buy excessive flows

Increase domestic money base

Domestic inflation

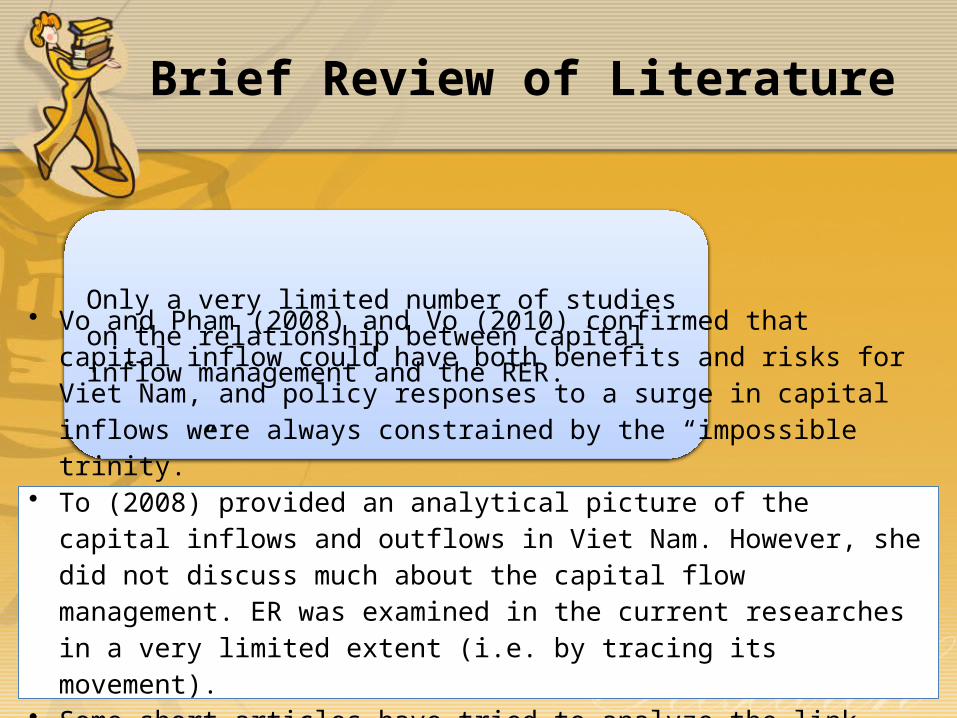

Brief Review of Literature

Only a very limited number of studies on the relationship between capital inflow management and the RER.

• Vo and Pham (2008) and Vo (2010) confirmed that capital inflow could have both benefits and risks for Viet Nam, and policy responses to a surge in capital inflows were always constrained by the “impossible trinity.”

• To (2008) provided an analytical picture of the capital inflows and outflows in Viet Nam. However, she did not discuss much about the capital flow management. ER was examined in the current researches in a very limited extent (i.e. by tracing its movement).

• Some short articles have tried to analyze the link between exchange rate and some specific components of capital inflows (e.g. FDI, and FPI) but only for a short period of time and based on qualitative analysis.

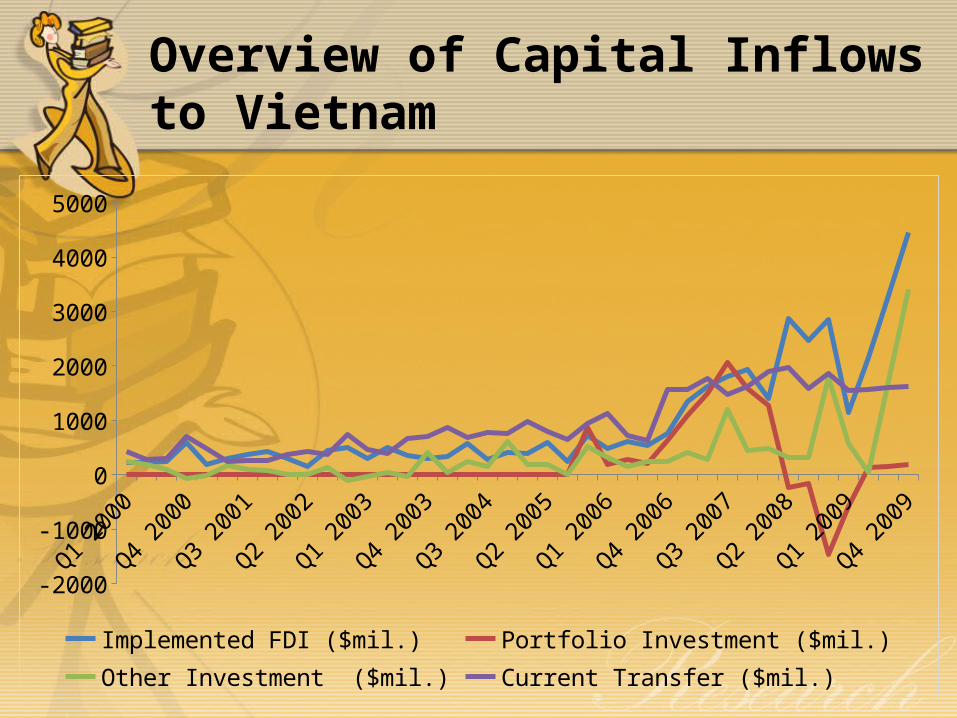

Overview of Capital Inflows to Vietnam

Q1

2000

Q3

2000

Q1

2001

Q3

2001

Q1

2002

Q3

2002

Q1

2003

Q3

2003

Q1

2004

Q3

2004

Q1

2005

Q3

2005

Q1

2006

Q3

2006

Q1

2007

Q3

2007

Q1

2008

Q3

2008

Q1

2009

Q3

2009

-2000

-1000

0

1000

2000

3000

4000

5000

Implemented FDI ($mil.) Portfolio Investment ($mil.)Other Investment ($mil.) Current Transfer ($mil.)

FDI

From 1991 to 2009, Viet Nam received 11,995 FDI projects with the total registered capital of $191.2 billion, 35% of which were implemented.

• After peaking in 1996, FDI inflows into Viet Nam had declined following the Asian crisis.

• However, since 2004, it has increased rapidly, reaching more than $12.0 billion in 2006 and $21.3 billion in 2007 in terms of committed inflow.

• FDI inflow reached its peak again in 2008 with the total registered capital of $71.7 billion. In 2010, the implemented FDI reached $11.0 billion, increasing by 10% compared to 2009

• The surge of FDI in the last three years reflects investors’ confidence in Viet Nam’s economic reform and development prospect as well as the shift of FDI in labor-intensive industries such as outsourcing logistics, electronics, garments and manufacturing from China to Vietnam

FDI

The registered FDI has been allocated mainly in manufacturing industry, real estate, hotels and restaurants, construction and communications and telecom.

• In the 1990s, FDI was concentrated in import substitution industries. • Since 2000, it has been shifted to export manufacturing sector and

services sector. • From 2008 until now, FDI was poured into real estate businesses,

creating a boom in real estate.

FDI

The foreign invested enterprises play an increasingly significant role in Viet Nam’s economy.

• In 1995, these enterprises employed 220 thousand workers and accounted for 6.3% of the GDP.

• In 2007, they employed almost 1,3 million workers and accounted for 16.2% of the GDP. The growth rate of the foreign invested sector is usually higher than other sectors in Vietnam.

• The foreign invested sector is currently a dynamic force for Viet Nam’s exports and the development of various manufacturing industries

FPI

Since 2001, FPI began to flow into Viet Nam with several funds having an average capital of $5.0-20.0 million each

FPI inflows in Viet Nam increased rapidly in 2006, thanks to investments on the stock market by international financial groups and funds.

Foreign investment funds brought in $2.0 billion of FPI into Viet Nam at the end of 2006.

Foreign portfolio inflows accounted for 2.2% and 10.4% of the GDP in 2006 and 2007, respectively.

After a sharp fall in 2008 due to the impact of the global financial crisis, the FPI inflow has recovered since the beginning of 2009. As of August 2010, Viet Nam’s stock market accounts for 40.0% of the GDP

Overview of Foreign Exchange Market in Viet Nam

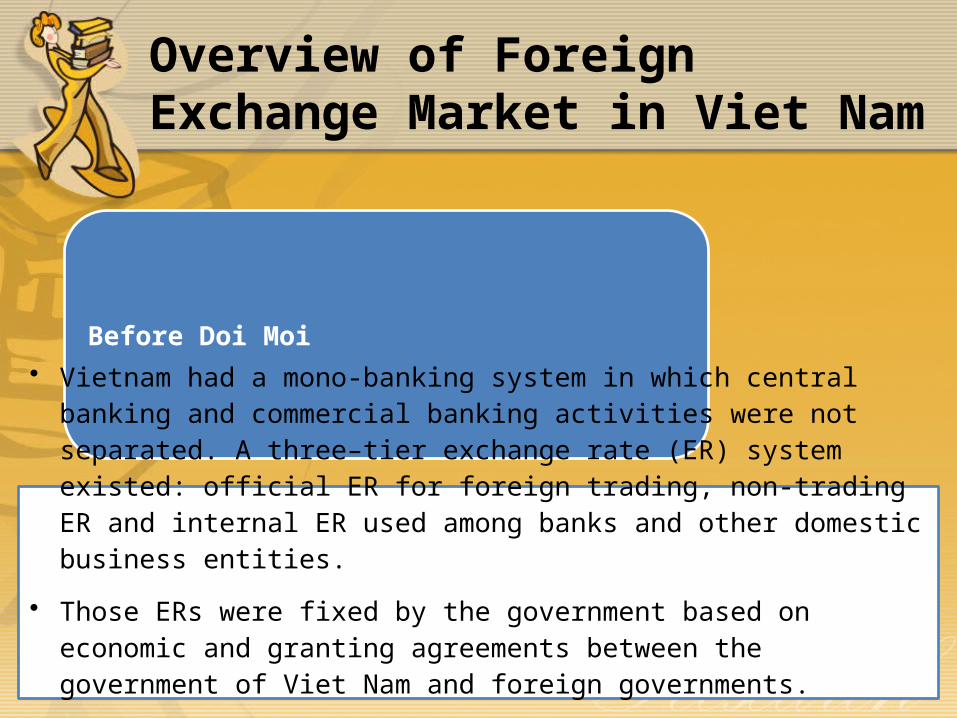

Before Doi Moi

• Vietnam had a mono-banking system in which central banking and commercial banking activities were not separated. A three–tier exchange rate (ER) system existed: official ER for foreign trading, non-trading ER and internal ER used among banks and other domestic business entities.

• Those ERs were fixed by the government based on economic and granting agreements between the government of Viet Nam and foreign governments.

• However, there was a paralleled informal/free foreign exchange market with higher ERs than those set by the government.

Overview of Foreign Exchange Market in Viet Nam

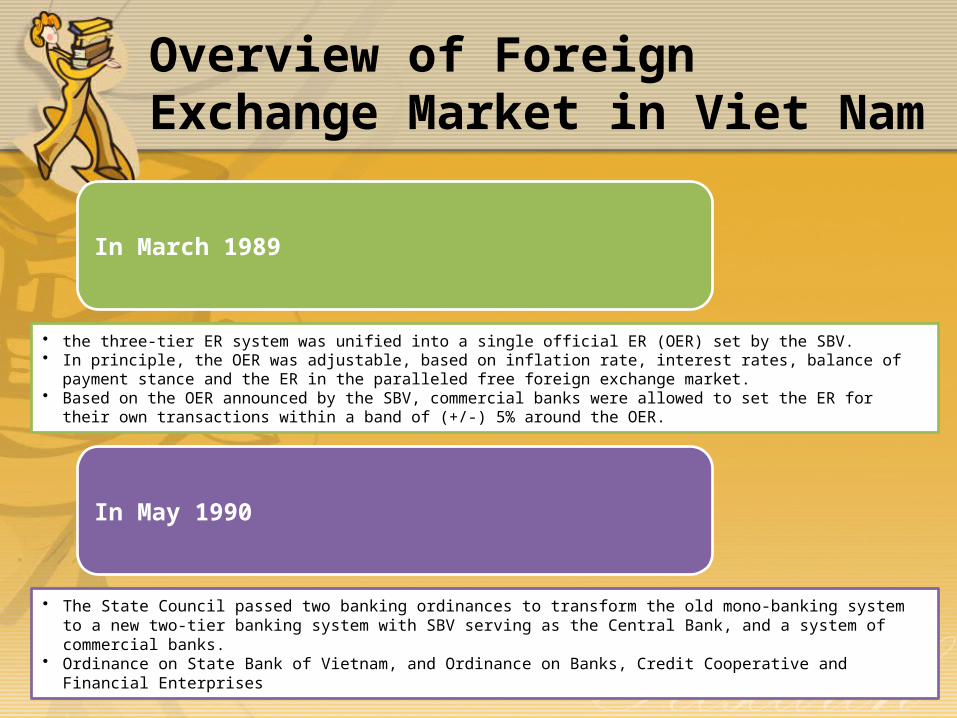

In March 1989

• the three-tier ER system was unified into a single official ER (OER) set by the SBV.• In principle, the OER was adjustable, based on inflation rate, interest rates, balance of payment stance and the ER in

the paralleled free foreign exchange market. • Based on the OER announced by the SBV, commercial banks were allowed to set the ER for their own transactions

within a band of (+/-) 5% around the OER.

In May 1990

• The State Council passed two banking ordinances to transform the old mono-banking system to a new two-tier banking system with SBV serving as the Central Bank, and a system of commercial banks.

• Ordinance on State Bank of Vietnam, and Ordinance on Banks, Credit Cooperative and Financial Enterprises

Overview of Foreign Exchange Market in Viet Nam

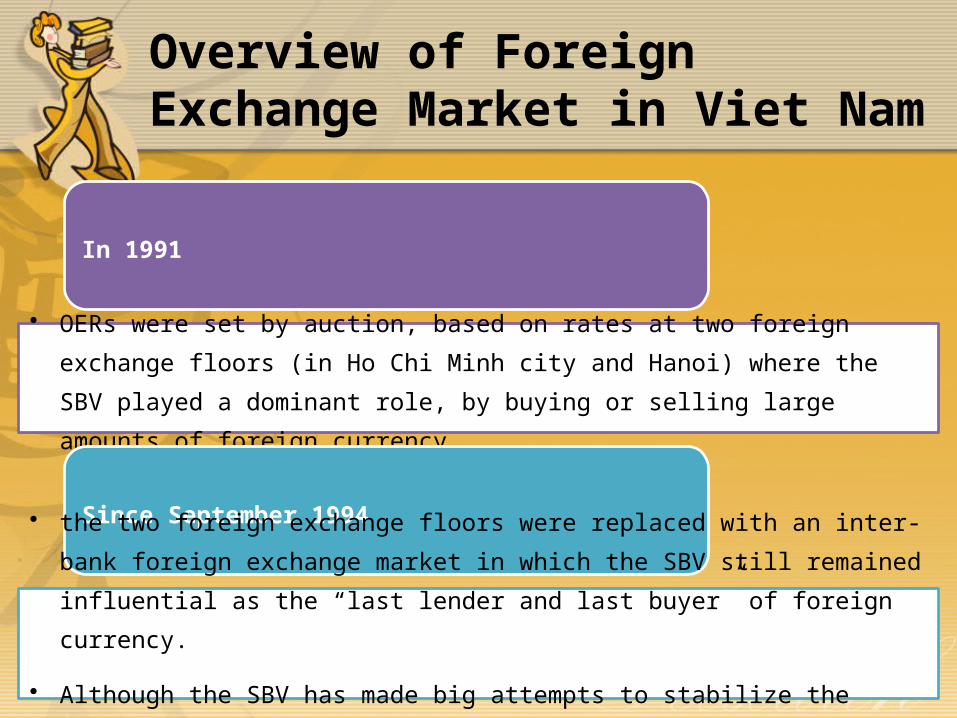

In 1991

• OERs were set by auction, based on rates at two foreign exchange floors (in Ho Chi Minh city and Hanoi) where the SBV played a dominant role, by buying or selling large amounts of foreign currency.

Since September 1994

• the two foreign exchange floors were replaced with an inter-bank foreign exchange market in which the SBV still remained influential as the “last lender and last buyer” of foreign currency.

• Although the SBV has made big attempts to stabilize the exchange rates, under the market pressure, since the mid-1990s, the ER band has been widened continuously.

Overview of Foreign Exchange Market in Viet Nam

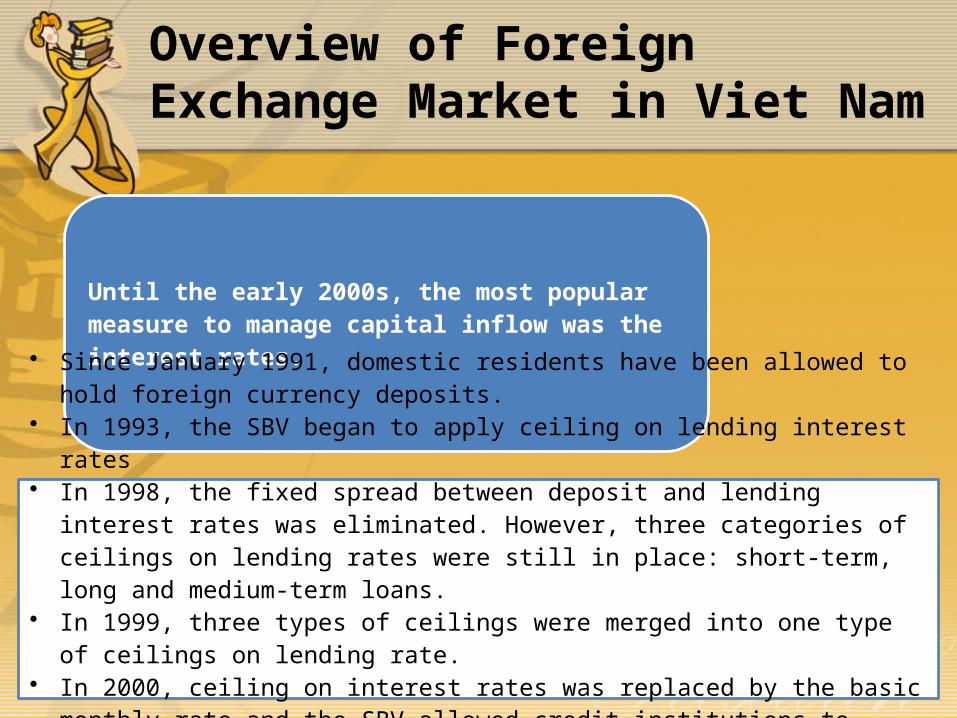

Until the early 2000s, the most popular measure to manage capital inflow was the interest rates.

• Since January 1991, domestic residents have been allowed to hold foreign currency deposits.

• In 1993, the SBV began to apply ceiling on lending interest rates• In 1998, the fixed spread between deposit and lending interest rates was

eliminated. However, three categories of ceilings on lending rates were still in place: short-term, long and medium-term loans.

• In 1999, three types of ceilings were merged into one type of ceilings on lending rate.

• In 2000, ceiling on interest rates was replaced by the basic monthly rate and the SBV allowed credit institutions to determine the foreign currency lending rates by the Singapore Inter-bank market rates.

• Since June 2002, the interest rate has been liberalized

Overview of Foreign Exchange Market in Viet Nam

• Massive inflows of capital into Viet Nam

over the past years have loaded

mounting pressure on the ER of dong

against the dollar, and consequently on

the exchange rate policy to stabilize the

foreign exchange market.

Overview of Foreign Exchange Market in Viet Nam

12000

13000

14000

15000

16000

17000

18000

19000

The NER has been consistently increasing since the mid-2000s, experiencing a sharp rise during the 2007-2009 periods.

• Massive inflows of capital into Viet Nam over the past years

have loaded mounting pressure on the ER of dong against

the dollar, and consequently on the exchange rate policy to

stabilize the foreign exchange market.

Overview of Foreign Exchange Market in Viet Nam

More market-oriented instruments (e.g. sterilization, gradual adjustment of ER band) have been employed by

the SBV in combination with administrative measures

However, the instability of the exchange rates is rooted in chronicle macro-economic weaknesses (e.g.

trade deficit, fiscal deficit) which cannot be addressed within a few

days.

Capital Inflows to Vietnam and the real exchange rate

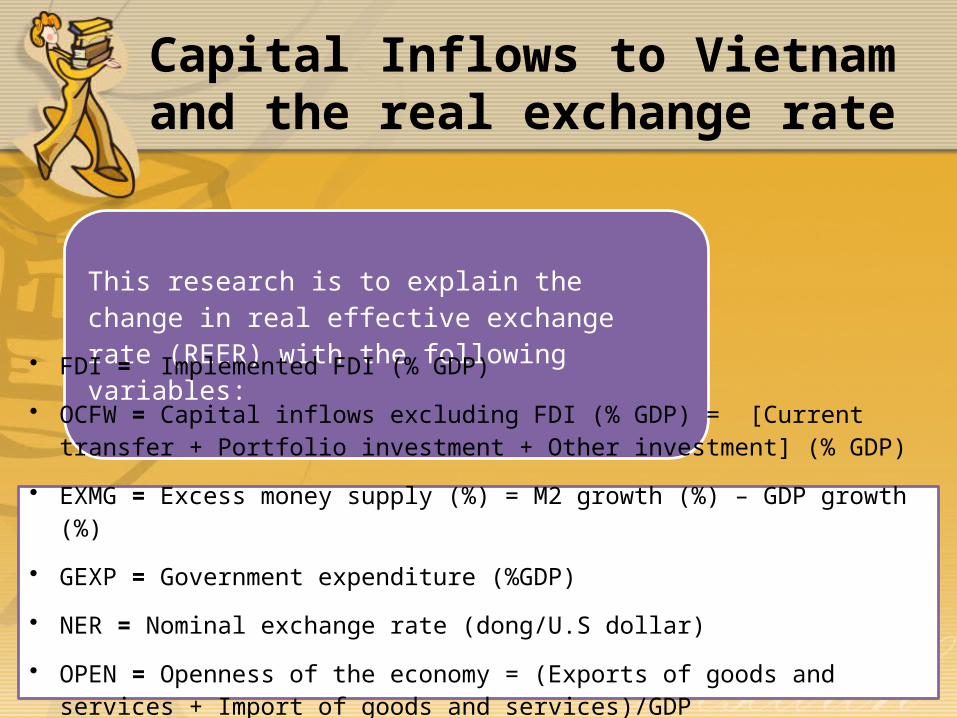

This research is to explain the change in real effective exchange rate (REER) with the following variables:

• FDI = Implemented FDI (% GDP)

• OCFW = Capital inflows excluding FDI (% GDP) = [Current transfer + Portfolio investment + Other investment] (% GDP)

• EXMG = Excess money supply (%) = M2 growth (%) – GDP growth (%)

• GEXP = Government expenditure (%GDP)

• NER = Nominal exchange rate (dong/U.S dollar)

• OPEN = Openness of the economy = (Exports of goods and services + Import of goods and services)/GDP

• GEXP, OPEN, EXMG and NER represent the current policy responses to the impact of capital inflows on real effective exchange rate.

Capital Inflows to Vietnam and the real exchange rate

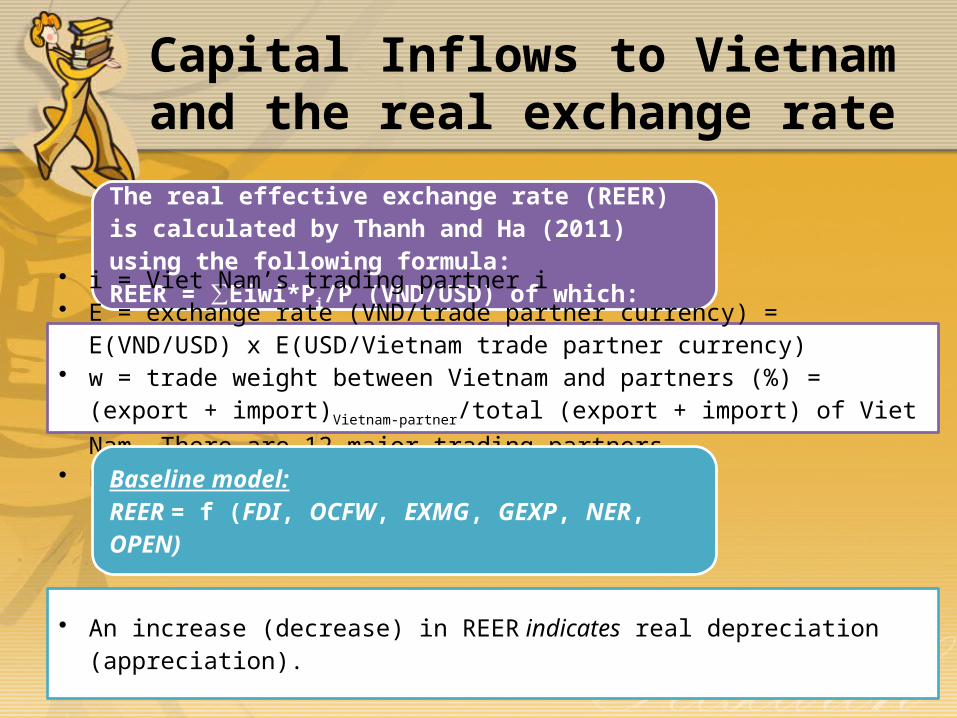

The real effective exchange rate (REER) is calculated by Thanh and Ha (2011) using the following formula: REER = ∑Eiwi*Pi/P (VND/USD) of which:

• i = Viet Nam’s trading partner i• E = exchange rate (VND/trade partner currency) = E(VND/USD) x

E(USD/Vietnam trade partner currency)• w = trade weight between Vietnam and partners (%) = (export + import)Vietnam-

partner/total (export + import) of Viet Nam. There are 12 major trading partners. • P = the price index.

Baseline model: REER = f (FDI, OCFW, EXMG, GEXP, NER, OPEN)

• An increase (decrease) in REER indicates real depreciation (appreciation).

Capital Inflows to Vietnam and the real exchange rate

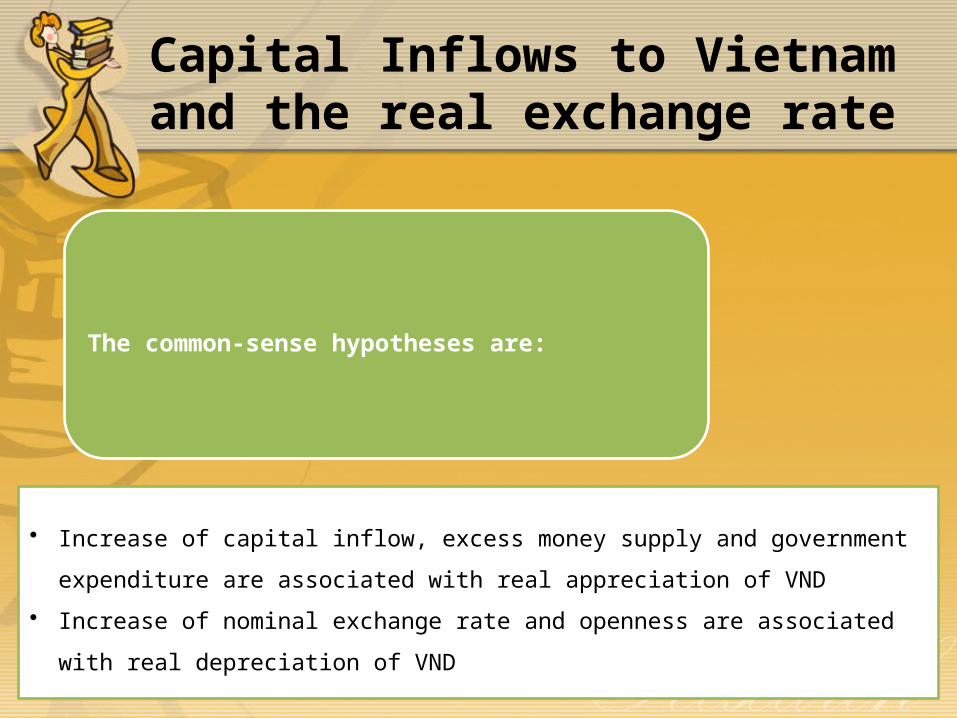

The common-sense hypotheses are:

• Increase of capital inflow, excess money supply and government expenditure are

associated with real appreciation of VND

• Increase of nominal exchange rate and openness are associated with real

depreciation of VND

Capital Inflows to Vietnam and the real exchange rate

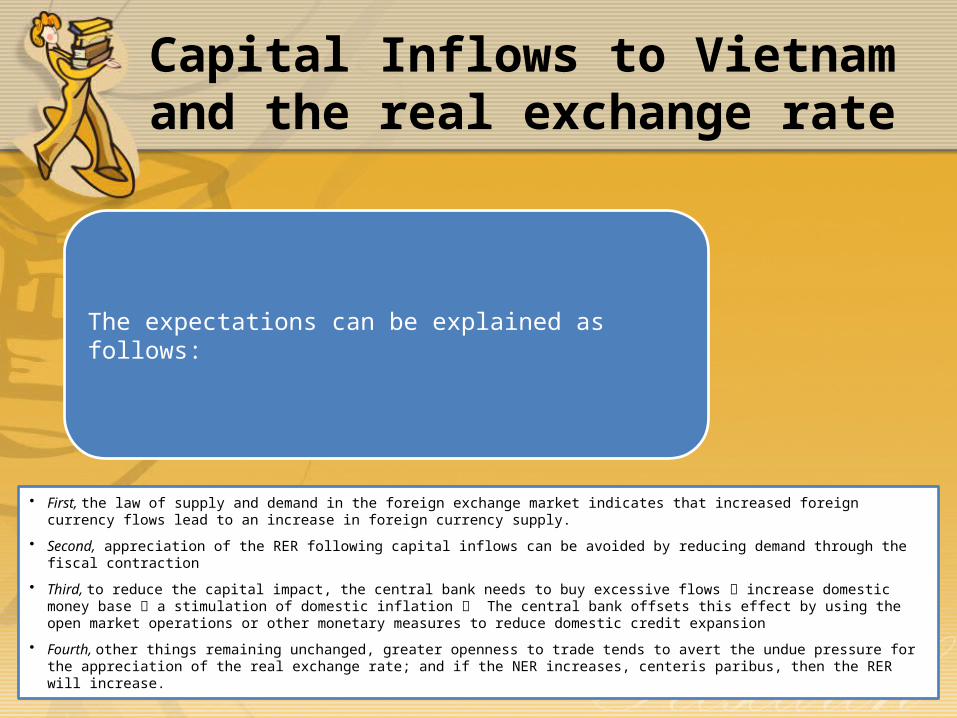

The expectations can be explained as follows:

• First, the law of supply and demand in the foreign exchange market indicates that increased foreign currency flows lead to an increase in foreign currency supply.

• Second, appreciation of the RER following capital inflows can be avoided by reducing demand through the fiscal contraction

• Third, to reduce the capital impact, the central bank needs to buy excessive flows increase domestic money base a stimulation of domestic inflation The central bank offsets this effect by using the open market operations or other monetary measures to reduce domestic credit expansion

• Fourth, other things remaining unchanged, greater openness to trade tends to avert the undue pressure for the appreciation of the real exchange rate; and if the NER increases, centeris paribus, then the RER will increase.

Capital Inflows to Vietnam and the real exchange rate

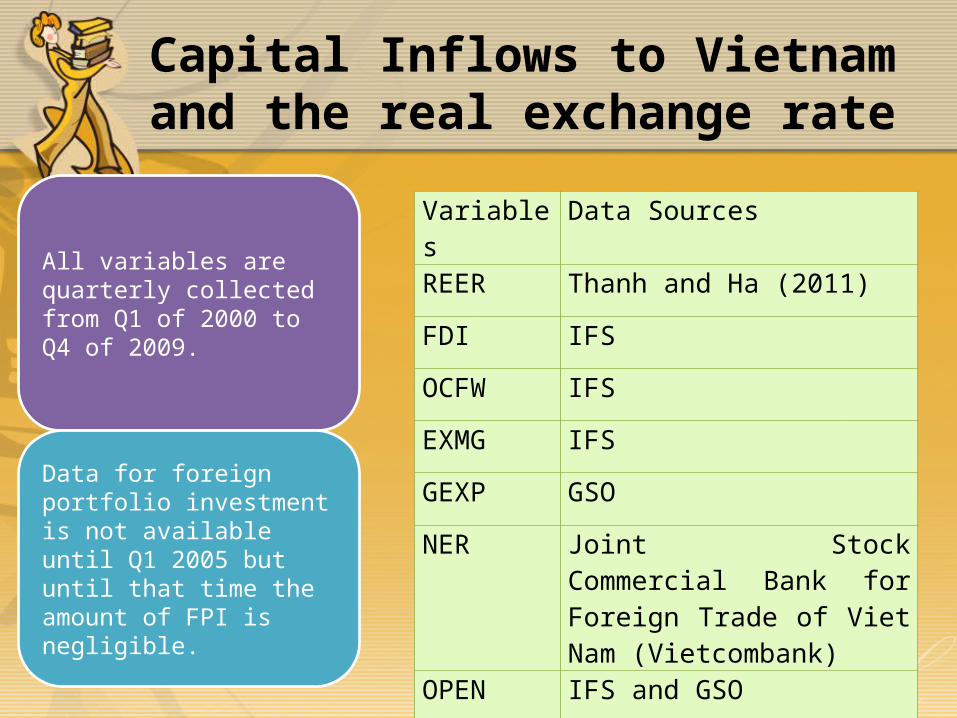

All variables are quarterly collected from Q1 of 2000 to Q4 of 2009.

Data for foreign portfolio investment is not available until Q1 2005 but until that time the amount of FPI is negligible.

Variables Data Sources

REER Thanh and Ha (2011)

FDI IFS

OCFW IFS

EXMG IFS

GEXP GSO

NER Joint Stock Commercial Bank for Foreign Trade of Viet Nam (Vietcombank)

OPEN IFS and GSO

Preliminary Results

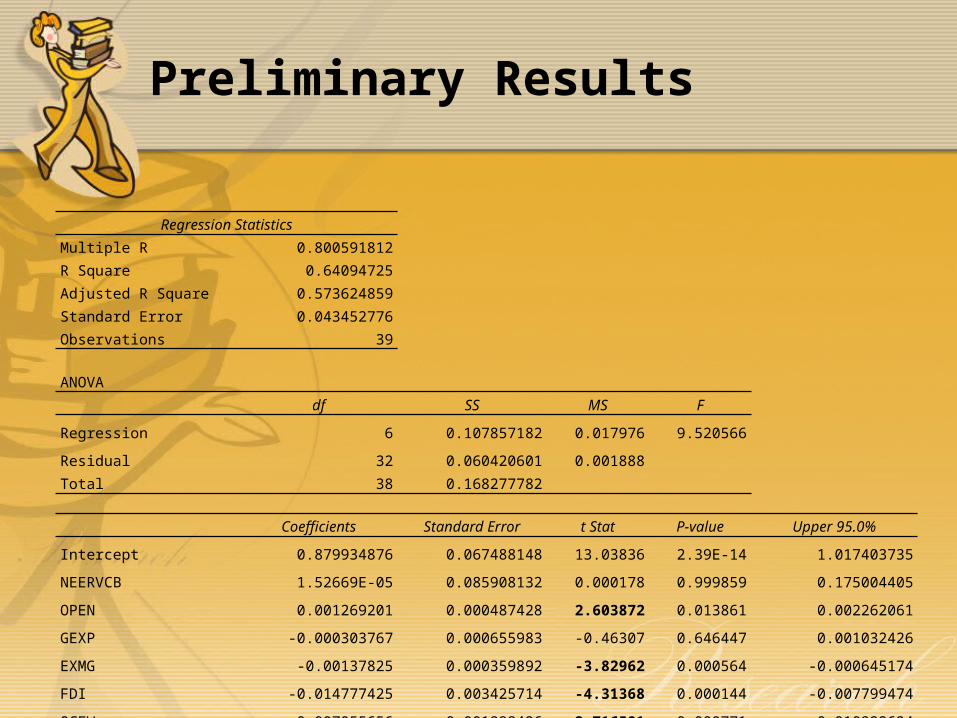

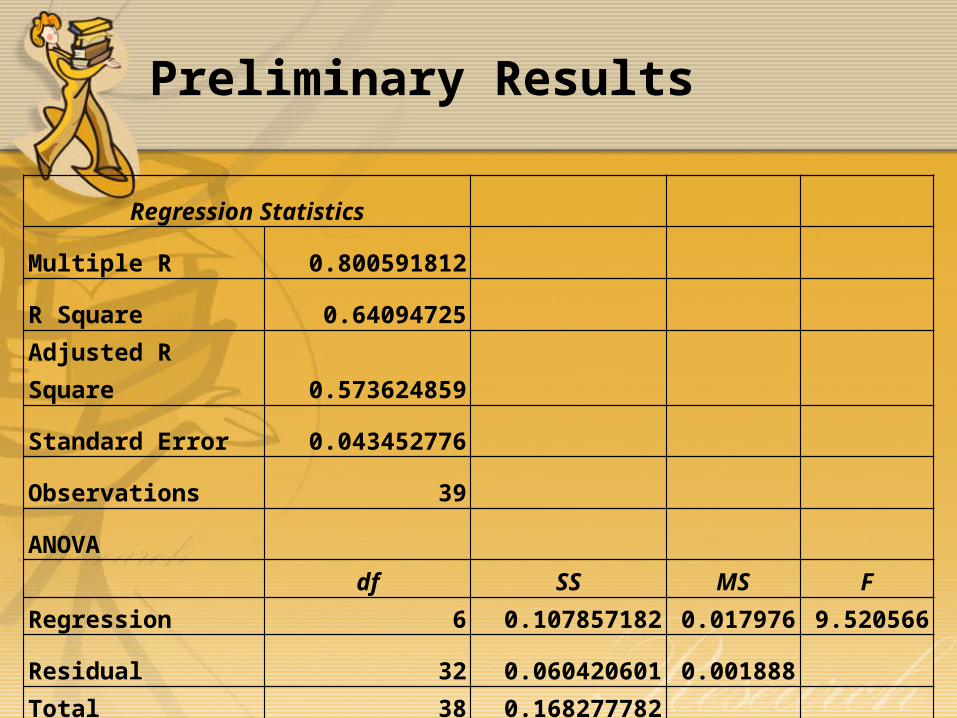

Regression StatisticsMultiple R 0.800591812R Square 0.64094725Adjusted R Square 0.573624859Standard Error 0.043452776Observations 39

ANOVA df SS MS F

Regression 6 0.107857182 0.017976 9.520566

Residual 32 0.060420601 0.001888Total 38 0.168277782

Coefficients Standard Error t Stat P-value Upper 95.0%

Intercept 0.879934876 0.067488148 13.03836 2.39E-14 1.017403735

NEERVCB 1.52669E-05 0.085908132 0.000178 0.999859 0.175004405

OPEN 0.001269201 0.000487428 2.603872 0.013861 0.002262061

GEXP -0.000303767 0.000655983 -0.46307 0.646447 0.001032426

EXMG -0.00137825 0.000359892 -3.82962 0.000564 -0.000645174

FDI -0.014777425 0.003425714 -4.31368 0.000144 -0.007799474

OCFW 0.007055656 0.001898426 3.716581 0.000771 0.010922624

Preliminary Results

Regression Statistics

Multiple R 0.800591812

R Square 0.64094725

Adjusted R Square 0.573624859

Standard Error 0.043452776

Observations 39

ANOVA df SS MS F

Regression 6 0.107857182 0.017976 9.520566

Residual 32 0.060420601 0.001888Total 38 0.168277782

Preliminary Results

Coefficients Standard Error t Stat P-value Upper 95.0%

Intercept 0.879934876 0.067488148 13.03836 2.39E-14 1.017403735

NEERVCB 1.52669E-05 0.085908132 0.000178 0.999859 0.175004405

OPEN 0.001269201 0.000487428 2.603872 0.013861 0.002262061

GEXP -0.000303767 0.000655983 -0.46307 0.646447 0.001032426

EXMG -0.00137825 0.000359892 -3.82962 0.000564 -0.000645174

FDI -0.014777425 0.003425714 -4.31368 0.000144 -0.007799474

OCFW 0.007055656 0.001898426 3.716581 0.000771 0.010922624

Preliminary Results

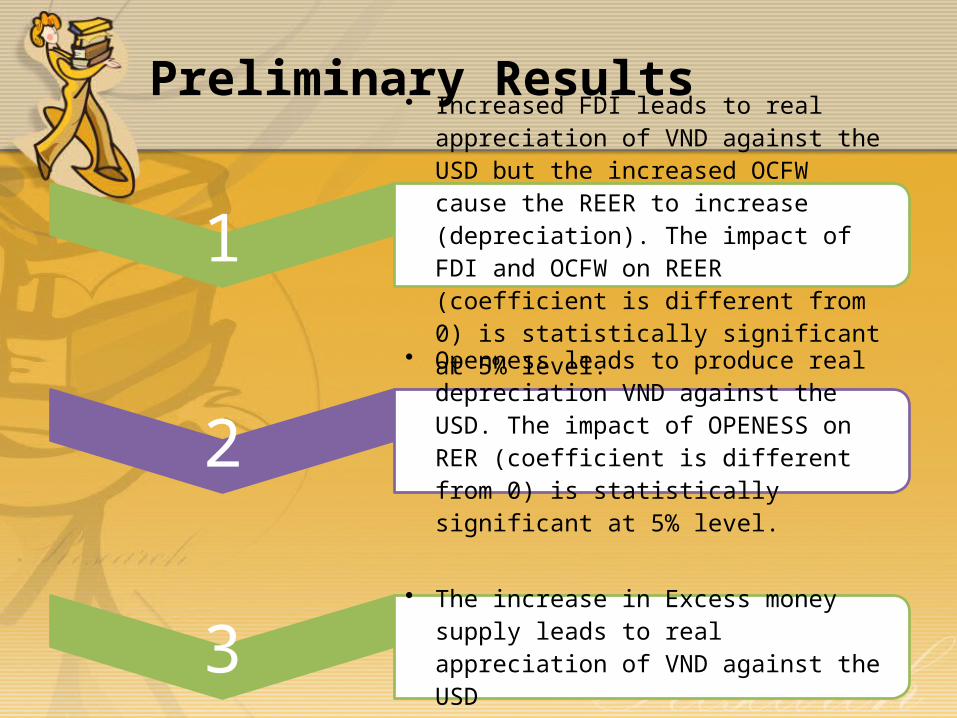

1• Increased FDI leads to real appreciation of

VND against the USD but the increased OCFW cause the REER to increase (depreciation). The impact of FDI and OCFW on REER (coefficient is different from 0) is statistically significant at 5% level.

2• Openness leads to produce real

depreciation VND against the USD. The impact of OPENESS on RER (coefficient is different from 0) is statistically significant at 5% level.

3• The increase in Excess money supply

leads to real appreciation of VND against the USD

Conclusion

In short, capital inflows have significant effects on real effective exchange rate of Viet Nam but two types of capital inflows have different effects on real effective exchange rate.

However, Viet Nam has possessed a limited number of effective policy instruments to neutralize the effect of capital inflows on the real effective exchange rate.

The econometric model shows that money supply currently seems to be the only viable policy option to neutralize the effects of capital inflows on real effective exchange rate.

Increase of capital inflows (FDI) lead to decrease in REER (real appreciation of the dong), and this appreciation effect can be neutralized by a cut in money supply.

Conclusion

This policy may not solve all problems in the long run under the impact of capital inflows.

THANK YOU FOR YOUR LISTENING