The Regulation of Director General of Taxation (“DGT”) No ... · -Unofficial English...

12

-Unofficial English translation- The Regulation of Director General of Taxation (“DGT”) No. Per-61/PJ./2009 regarding Procedures for Implementing Double Tax Avoidance Agreements Considering : a. based on Article 32A Law No.7/1983 regarding Income Tax as amended lastly by Law No.36/2008 stipulate that the Indonesia Government has authority to make an agreement with the government of other countries in purpose to avoid double taxation and prevent tax evasion; b. based on Double Tax Avoidance Agreements between the Indonesia Government and other countries, one of them stipulated about the Indonesia Government taxation right of specific income that obtained or earned by non resident tax payer according to the prevailing regulations; c. need a guidance to give legal security in applying prevention of misuse of Double Tax Avoidance Agreements; Remembering : 1. Law No.6/1983 regarding The General Tax Provisions and Procedures Law (Pages of Indonesia Republic Country Law No.49/1983, Additional Pages of Indonesia Republic Country No. 3262) as amended lastly by Law No16/2009 (Pages of Indonesia Republic Country Law No. 62/2009, Additional Pages of Indonesia Republic Country No.4999) 2. Law No.7/1983 regarding Income Tax (Pages of Indonesia Republic Country No.50/1983, Additional Pages of Indonesia Republic Country No.3263) as amended lastly by Law No.36/2008 (Pages of Indonesia Republic Country No.133/2008, Additional Pages of Indonesia Republic Country No.4893) Deciding Stabilizing : Directorate General of Taxation (“DGT”) Regulation Regarding Procedures for Implementing Double Tax Avoidance Agreements Article 1 In this Regulation of the Director General of Taxation, the meaning of: 1. Persetujuan Penghindaran Pajak Berganda (Double tax avoidance agreements), further will be referred to as P3B (Tax Treaty), is the agreement between the Indonesian Government and the governments of other countries made in order to avoid double taxation and prevent tax evasion. 2. Wajib Pajak Luar Negeri (Non Indonesian tax resident), further will be referred to as WPLN, is a non resident tax subject , as defined by Law No.7/1983 regarding Income Tax Law as amended lastly by Law No.36/2008, either individual or entity, who obtains and/or earns income sourced from Indonesia or receives and/or earns income sourced from Indonesia through a Permanent Establishment (“PE”) in Indonesia. 3. A tax withholder is a government entity, resident taxpayer, event organizer, PE, or other representative of an overseas company which is obliged to withhold tax on income received or earned by WPLN according to the prevailing regulations. 4. Surat Keterangan Domisili (Certificate of Domicile), further will be referred to as SKD (“CoD”), is a form issued by the DGT which has been completed and signed by the WPLN, and has been certified by the tax authority in the Tax Treaty partner countries.

-

Upload

truongxuyen -

Category

Documents

-

view

224 -

download

0

Transcript of The Regulation of Director General of Taxation (“DGT”) No ... · -Unofficial English...

-Unofficial English translation-

The Regulation of Director General of Taxation (“DGT”)No. Per-61/PJ./2009

regardingProcedures for Implementing Double Tax Avoidance Agreements

Considering : a. based on Article 32A Law No.7/1983 regarding Income Tax as amendedlastly by Law No.36/2008 stipulate that the Indonesia Government hasauthority to make an agreement with the government of other countries inpurpose to avoid double taxation and prevent tax evasion;

b. based on Double Tax Avoidance Agreements between the IndonesiaGovernment and other countries, one of them stipulated about theIndonesia Government taxation right of specific income that obtained orearned by non resident tax payer according to the prevailing regulations;

c. need a guidance to give legal security in applying prevention of misuse ofDouble Tax Avoidance Agreements;

Remembering : 1. Law No.6/1983 regarding The General Tax Provisions and ProceduresLaw (Pages of Indonesia Republic Country Law No.49/1983, AdditionalPages of Indonesia Republic Country No. 3262) as amended lastly byLaw No16/2009 (Pages of Indonesia Republic Country Law No. 62/2009,Additional Pages of Indonesia Republic Country No.4999)

2. Law No.7/1983 regarding Income Tax (Pages of Indonesia RepublicCountry No.50/1983, Additional Pages of Indonesia Republic CountryNo.3263) as amended lastly by Law No.36/2008 (Pages of IndonesiaRepublic Country No.133/2008, Additional Pages of Indonesia RepublicCountry No.4893)

Deciding

Stabilizing : Directorate General of Taxation (“DGT”) Regulation Regarding Procedures forImplementing Double Tax Avoidance Agreements

Article 1

In this Regulation of the Director General of Taxation, the meaning of:

1. Persetujuan Penghindaran Pajak Berganda (Double tax avoidance agreements), further willbe referred to as P3B (Tax Treaty), is the agreement between the Indonesian Governmentand the governments of other countries made in order to avoid double taxation and preventtax evasion.

2. Wajib Pajak Luar Negeri (Non Indonesian tax resident), further will be referred to as WPLN,is a non resident tax subject, as defined by Law No.7/1983 regarding Income Tax Law asamended lastly by Law No.36/2008, either individual or entity, who obtains and/or earnsincome sourced from Indonesia or receives and/or earns income sourced from Indonesiathrough a Permanent Establishment (“PE”) in Indonesia.

3. A tax withholder is a government entity, resident taxpayer, event organizer, PE, or otherrepresentative of an overseas company which is obliged to withhold tax on income receivedor earned by WPLN according to the prevailing regulations.

4. Surat Keterangan Domisili (Certificate of Domicile), further will be referred to as SKD (“CoD”),is a form issued by the DGT which has been completed and signed by the WPLN, and hasbeen certified by the tax authority in the Tax Treaty partner countries.

5. Surat Pemberitahuan Masa (monthly tax return), further will be referred to as SPT Masa(“monthly tax return”) is the tax return used by the tax withholder to report the settlement ofthe tax withheld in a certain period according to the prevailing regulations.

Article 2

Tax withholder obliged to withholds the tax payable on the income received or earned by WPLN inaccordance with Law No.7/1983 regarding Income Tax as amended lastly by Law No.36/2008.

Article 3

1. A tax withholder shall withhold the tax in accordance with the regulations stipulated in theTax Treaty, in the following case:a. the income recipient is not an Indonesian tax resident,b. the administrative requirements to implement the regulations stipulated in the Tax

Treaty have been fulfilled, andc. there is no tax treaty abuse by the WPLN as defined in the regulation regarding the

prevention of misuse of a Tax Treaty.

2. In the case that the regulation in point 1 above is not fulfilled, the tax withholder is obliged towithhold the tax payable in accordance with the regulations stipulated in Law No.7/1983 asamended lastly by Law No.36/2008.

Article 4

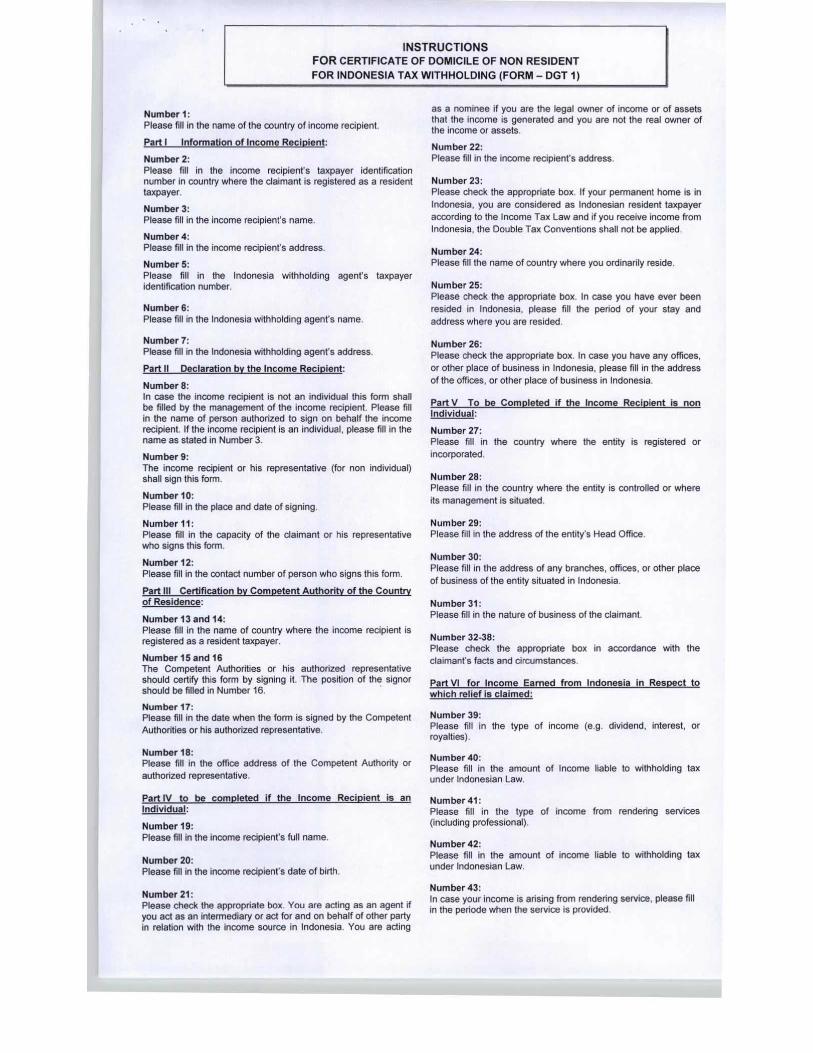

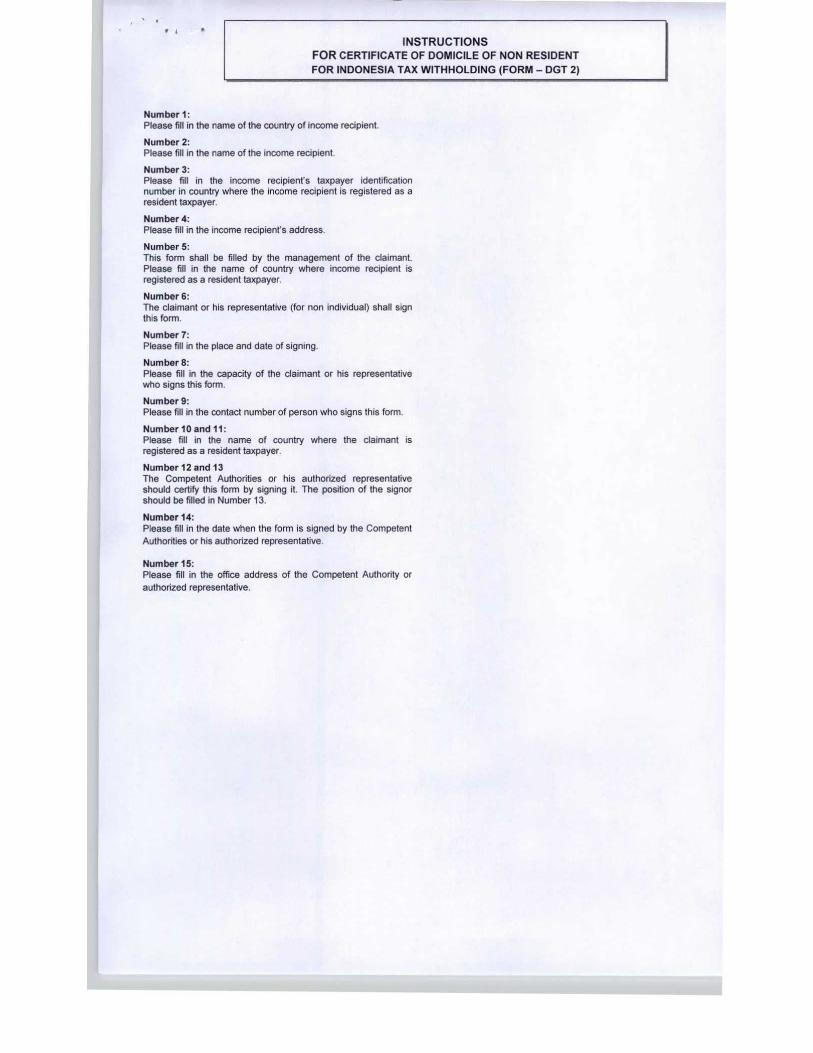

1. The CoD document as intended in this regulation is the form as stipulated in Attachment II(Form-DGT1) or Attachment III (Form-DGT2) of this DGT Regulation.

2. The CoD document as intended in Attachment III (Form-DGT2) of the DGT Regulation isused in the case of:a. the WPLN receiving or earning income through a custodian relating to the income from

the share transfer transaction or obligations which are traded or listed in theIndonesian Stock Exchange, except interest and dividend; or

b. WPLN banks.

3. The administrative requirements as mentioned in Article 3(1) b for the CoD which is to begiven by the WPLN to the tax withholder are:a. the form stipulated in Attachment II or Attachment III of this DGT Regulation has been

used;b. it has been fully filled out by the WPLN;c. it has been signed by the WPLN;d. it has been certified by the tax authority in the Tax Treaty partner countries; ande. it has been provided before the end of the deadline to submit tax returns for tax

payable.

4. The custodian as mentioned in paragraph 2 (a) is the party who provides custody servicesfor shares and other assets relating to shares and other services, including receivingdividends, interests and other rights, finishing shares transactions, and acting on behalf ofan account holder who is his/her client.

5. An institution which has been named explicitly in the Tax Treaty or which has already beenagreed upon by the authorities in Indonesia and the Tax Treaty partner countries does notneed to submit a CoD.

Article 5

1. A CoD, which uses the form as mentioned in Attachment II (Form-DGT1) which is providedto the tax withholder after the deadline to submit the monthly tax return for the tax payable

period, cannot be considered as a basis on which to implement the regulations stipulated inthe Tax Treaty.

2. The form as intended in Attachment III (Form-DGT2), which passes the requirements asmentioned in Article 4(2), is used as the basis for implementing the regulations as stipulatedin the Tax Treaty, starting on the date on which the CoD was certified by the tax authority ofthe Tax Treaty partner countries and remains in effect for 12 months.

Article 6

WPLN may apply a refund for the tax overpayment which should not have been payable inaccordance with the prevailing regulations in the case of the benefits in the Tax Treaty not havingbeen provided due to the administrative requirements as stipulated in Article 3(1)(b) not havingbeen fulfilled, but the WPLN is of the view that the tax withholding is not in accordance with theregulations stipulated in the Tax Treaty.

Article 7

The procedures to implement the Tax Treaty by the tax withholder are stipulated in Attachment I ofthis DGT Regulation.

Article 8

1. A withholding tax slip has to be prepared by the tax withholder in accordance with theprevailing regulations and procedures.

2. In the case that there is an income received or earned by a WPLN but no tax to bewithholding in Indonesia according to the regulations stipulated in the Tax Treaty, the taxwithholder is still obliged to prepare a withholding tax slip.

Article 9

1. A tax withholder is obliged to provide a photocopy of the CoD received by the WPLN as anattachment to the monthly tax return.

2. The head of the Tax Office has to carry out an investigation on the correctness of thereporting of the amount of tax withheld and record the CoD and the withholding tax slipreported by the tax withholder.

3. The head of the Tax Office has to carry out an investigation on whether the WPLN has a PEin Indonesia as in accordance with the regulations stipulated in the Tax Treaty.

4. In the case that there is an indication that the WPLN carries out activities or business inIndonesia through a PE as intended in point 3 and has not been registered as a taxpayer,the Tax Office informs the Tax Office where the PE is registered to send a reminder letter(Surat Himbauan) in accordance with the prevailing regulations.

Article 10

When this DGT Regulation is effective:

1. The DGT Circular Letter No.SE-03/PJ.101/1996 dated 29 March 1996 regarding theImplementation of the Tax Treaty;

2. The DGT Circular Letter No. SE-04/PJ.101/1996 dated 28 May 1996 regarding theTransitional Period for Implementing SE-03/PJ.101/1996;

are revoked and become non effective.

Article 11

This DGT regulation is in effect starting 1 January 2010.

Stipulated in Jakarta5 November 2009

Director of DGT

Mochamad Tjiptardjo

Attachment 1

Procedures in implementing the Tax Treaty

A. Regulations for Tax Withholder and Custodian

1. A tax withholder withholds tax on all income received or earned by a WPLN in accordance withthe regulations stipulated in the Law No.7/1983 as amended lastly by Law No.36/2008(Income Tax Law (“ITL”).

2. Tax withholder

3. A tax withholder must prepare a withholding tax slip in accordance with the prevailingregulations. The withholding tax slip has to be provided to the WPLN.

4. Even if there is no tax to be withheld, the tax withholder is still obliged to prepare a withholdingtax slip by filling in the gross income amount, and filling in “Nil” in the Income Tax Withheldcolumn. The relevant withholding tax slip is not obliged to be provided to the WPLN.

5. The investigation on the CoD (Form in Attachment II) to confirm that the income recipient isnot an Indonesian tax subject has to be carried out by the tax withholder. In the case that theincome recipient is a domestic tax subject, the tax withholder is obliged to withhold tax inaccordance with the prevailing regulations stipulated in ITL. The existence of a domestic taxobject is to be determined in the case that the CoD:

a. Part IV point 4 mentions the WPLN’s address in Indonesia; orb. Part IV point 5 mentions that the WPLN has a permanent address in Indonesia; orc. Part IV point 6 mentions the home address of the WPLN in Indonesia; ord. Part V points 1, 2, and 3 mention that the place of establishment, place of residency,

or head office addresses of the WPLN is in Indonesia.

6. In the case that the administrative requirements cannot be fulfilled by the WPLN, the taxwithholder is not allowed to implement the regulations stipulated in the Tax Treaty and mustwithhold tax in accordance with the regulations stipulated in the ITL.

7. In order to be able to implement the Tax Treaty to the WPLN, the tax withholder carries outinvestigation procedures for whether the CoD gives the answers:

a. “No” in point 3 of Part IV; orb. “Yes” in point 6 of Part V; orc. “Yes” for all the questions from point 7 to point 13 in Part V.

The Tax Treaty does not apply if any one of the answers of WPLN who receives the incomeis not in accordance with point a, b, or c above.

8. In the case that the WPLN who receives income is an institution whose name is mentionedexplicitly in the Tax Treaty or has been agreed by the authority in Indonesia and the TaxTreaty partner countries, the tax withholder may implement the regulations as stipulated in theTax Treaty without a CoD.

9. The tax withholder must report the monthly tax return by attaching a photocopy of the CoD andthe withholding tax slip to the Tax Office.

10. For withholding tax on income derived from the shares transfer transactions, or obligationswhich are traded or listed in the Indonesian Stock Exchange, except for interests anddividends, which are received or earned by the WPLN through a custodian:

a. the CoD form as intended in Attachment III has to be filled in completely and signed bythe WPLN who receives the income and certified by the authority of the Tax Treatypartner countries;

b. the original CoD is provided to the custodian by the WPLN who receives the income;c. the custodian must provide the original CoD received from the WPLN which is still

valid to the tax withholder;d. in the case that the WPLN receives incomes from several sources, the custodian can

make copies of the CoD and have them legalized by the Head of the Tax Office wherethe custodian is registered as a taxpayer;

e. the Head of the Tax Office who legalizes the photocopied CoDs must keep the originalCoD;

f. the tax withholder must withhold tax in accordance to with the regulations stipulated inthe Tax Treaty by referring to the original CoD which is still valid, or a photocopy of theCoD which has been legalized and provided by the custodian and keep thephotocopied CoD;

g. the tax withholder must prepare the withholding tax slip and provide it to the WPLNthrough the custodian.

11. For withholding tax on income received or earned by a WPLN bank:a. the CoD form as intended in Attachment III has to be filled in completely and signed by

the WPLN bank and legalized by the authority of the Tax Treaty partner countries; andb. the original CoD is should be provided to the tax withholder.

12. The CoD must be kept by the tax withholder for 10 years in accordance with Article 28(11) ofLaw No.6/1983 regarding the General Tax Regulation and Procedures as amended lastly byLaw No.28/2007.

B. Administration of CoDs by the Tax Office

1. When accepting the tax return, the official who accepts the tax return must investigate thecompleteness of the monthly tax return, at least attaching the withholding tax slip and aphotocopy of the CoD.

2. The review of the correctness of the reporting of the amount withheld by comparing thephotocopy of the CoD with the name of the WPLN mentioned in the withholding tax slip is tobe carried out by the Head of the Tax Office c.q. Head of Supervision and ConsultationSection.

3. In the case that the tax withholder has not carried out his/her obligations in accordance withthis DGT Regulation, the Head of the Tax Office sends a reminder letter (Surat Himbauan) inaccordance with the prevailing regulations.

4. In the case that the information mentioned in the CoD indicates that there is a PE presence inIndonesia for the WPLN, the Tax Office sends the information to the related Tax Office toinvestigate its presence and prepare the reminder letter (Surat Himbauan) in accordance withthe prevailing regulations.

5. The recording of the CoD and withholding tax slip reported by the tax withholder is carried outby the Data Information Processing Section.