The Ram Fund Presentation Spring, 2013 - NKD Group · The Ram Fund Presentation Spring, 2013 I....

73

The Ram Fund Presentation Spring, 2013 I. Introduction II. Performance III. Investment Approach IV. Companies Analyzed V. Portfolio Composition VI. Class Highlights VII. Questions From The Audience

Transcript of The Ram Fund Presentation Spring, 2013 - NKD Group · The Ram Fund Presentation Spring, 2013 I....

The Ram Fund Presentation Spring, 2013

I. Introduction II. Performance

III. Investment Approach

IV. Companies Analyzed

V. Portfolio Composition

VI. Class Highlights

VII. Questions From The Audience

Welcome As the faculty advisor for the Ram Fund (the University of Rhode Island’s Student-Managed Investment Fund), I get to have a number of great experiences each and every semester. First, I get to work with a class populated by our very best students. Second, I get to observe them make an incredible amount of progress in a relatively short time. They enter the class with excellent academic backgrounds but little or no practical experience: While they know the basics of security valuation from their previous classes, their exposure is limited to “book learning”, where all the examples and problems are neat, clear, and well-defined. However, by the end of a relatively short semester, they have learned not only that real-world financial data is complicated, ambiguous, and messy, but also how to organize and analyze these data and use them to value firms. They have also learned how to succinctly and clearly present their findings, and how to function in a team environment where they must both give and respond to peers’ criticism. Finally, because much of their analysis and questions take place outside of the regular one-hour class time, I get to spend a significant amount of time with these exceptional students outside the regular classroom at almost any hour of the day. The fund has had another very good semester and year. The fund hit a high-water mark of $223,000 at the end of March, and finished the semester at slightly over $216,000 - up 10.9% year to date, and 15.11% over the last 12 months (since 4/30/2011). Its performance shined, whether compared to the S&P 500, the S&P 400 or the S&P 600. The following pages present the results of their labors for the Spring, 2013 Ram Fund. I hope you find them and their work as impressive as I do. Peter J. DaDalt Ph.D Ram Fund Faculty Advisor The College of Business The University of Rhode Island Voice: 401.932.7004 Email: [email protected]

Ram Fund Management Team Name Sector Covered

Mark Albanese Consumer Staples

Michael Giancaspro Basic Materials

Stephen Gross Services

Park Guo Technology

Peter Hathaway Consumer Discretionary

John Kashmanian Industrials

Benjamin Kupa Healthcare

Jared Moreau Utilities

Bryan Poston Financial Services

Luis Rondon Energy

Ram Fund Portfolio Holdings

(All figures as of 4/19/2013)

Ticker Sector Shares Price Value

ARLP Alliance Resource Partners 75 66.01 4,950.75 AVGO Avago Technologies LTD 400 31.26 12,504.00 CHE Chemed Corp 150 78.70 11,805.00 CPK Chesapeake Utilities Corp 200 50.82 10,164.00 STZ Constellation Brands Inc 250 48.52 12,130.00 CLB Core Laboratories NV 100 139.50 13,950.00 XRAY Dentsply International 225 41.56 9,351.00 DSX Diana Shipping Inc. 600 9.34 5,604.00 HLF Herbalife Ltd. 250 35.78 8,945.00 IJJ iShares S&P Midcap Value Index Fund 150 97.39 14,608.50 IJS iShares S&PSmallcap Value Index Fund 150 78.93 11,839.50 IPGP IGP Photonics Corp.* 200 62.29 12,458.00 KEYN Keynote Systems Inc 500 11.08 5,540.00 PEZ Powershares Dynamic Cons. Discr ETF 350 32.86 11,501.00 PWR Quanta Services LTD. 100 27.31 2,731.00 RS Reliance Steel and Aluminum Corp* 200 65.69 13,138.00 SWX Southwest Gas Corp 250 49.47 12,367.50 UAL United Continental Holdings 400 30.60 12,240.00 URS URS Corp 200 44.90 8,980.00 WPP Wasau Paper Corp. 800 10.19 8,152.00

Cash 11,909.99 Total 216,061.74 Change last presentation (11/30/2012) 23,311.15

4/21/2013

1

Spring, 2013

• Mark Albanesea ba ese• Michael Giancaspro• Stephen Gross• Park Guo• Peter Hathaway• John Kashmanian• Benjamin Kupa• Jared Moreau• Bryan Poston• Luis Rondon

4/21/2013

2

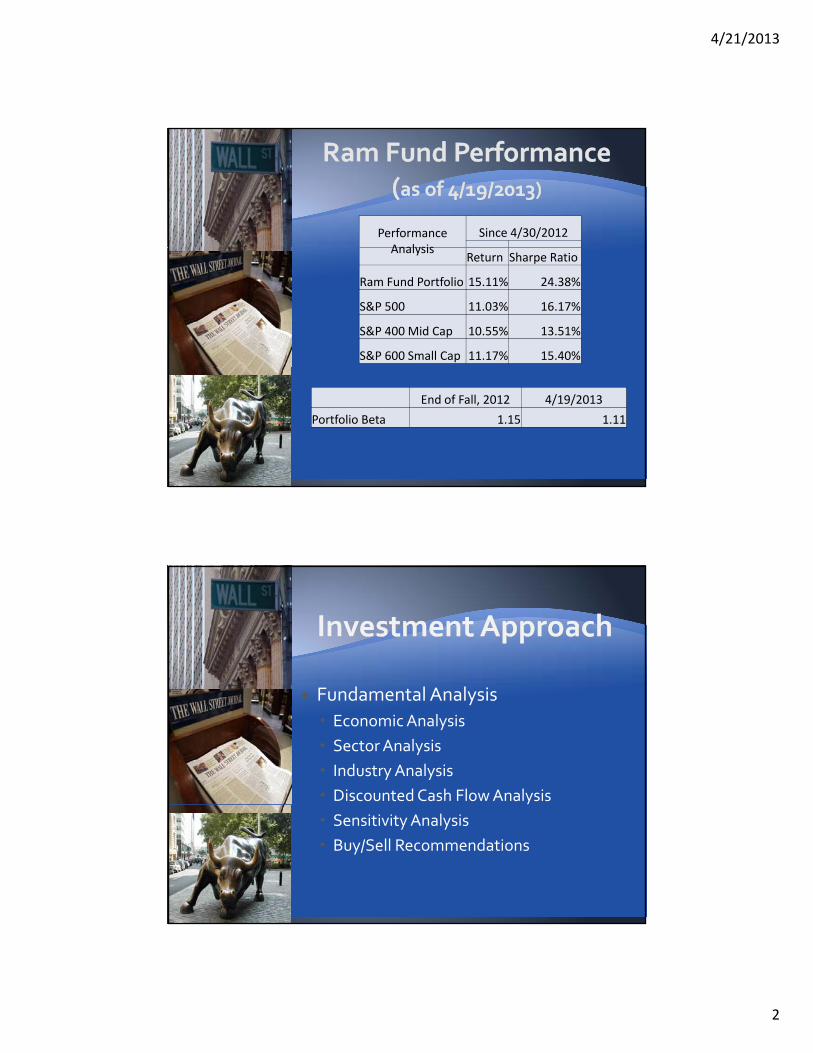

Performance Analysis

Since 4/30/2012Analysis

Return Sharpe Ratio

Ram Fund Portfolio 15.11% 24.38%

S&P 500 11.03% 16.17%

S&P 400 Mid Cap 10.55% 13.51%

S&P 600 Small Cap 11.17% 15.40%

End of Fall, 2012 4/19/2013

Portfolio Beta 1.15 1.11

Fundamental Analysis

Economic Analysis

Sector Analysis

Industry Analysis

Discounted Cash Flow Analysisy

Sensitivity Analysis

Buy/Sell Recommendations

4/21/2013

3

Ratio Analysis Ratio Analysis

Valuation and Profitability

Competitive Environment

Porter’s 5 Forces

Major risk and profitability drivers

Profitability & Relative Valuation

Discounted Cash Flow Analysis

Sensitivity Analysis

4/21/2013

4

S&P’s Research Insight

Multiples

Fi i l R ti Financial Ratios

4/21/2013

5

4/21/2013

6

Household Applience

Construction & Farm Equip. Industrials

Consumer Goods

AGCOCO.

iRobots Corp.

Staples:

Processed & pkg. Omega Protein

Corp

Electronic Equipment,

Instruments, & Components

IPG Photonics Corporation

Technology

SectorCompany Selection

IndustrySector

Company SelectionIndustry

Economy

GoodsCorp.

Bio TechUnited

TherapeuticsHealthcare

Education &

Basic MaterialsPaper & Paper

Products Orient Paper Inc.

ServicesEducation & Training

DeVry Inc.

EnergyOil & Gas Drilling

Rowan Companies Plc.

Financial Services

Specialized Finance KKR Financials

UtilitiesAtmos Energy

Corp Gas Utilities

Target Price: $59.69

Manufacture and distribute variety of agricultural products

and replacement parts worldwide

Offer a comprehensive line of tractors, combines, sprayers,

implements and hay toolsimplements and hay tools

Strong global presence with factories around the world and

2,600 independent dealers and distributors in 140

countries

4/21/2013

7

Market to Book: 1.536ROI: 13 135

2012 Revenue: $9962 million

+13 5%ROI: 13.135Beta: 2.16

+13.5%

2012 Net Income: $600 million

+11.1%

T t P i $ 8 Target Price: $49.82

Segments: Natural Gas Distribution, Regulated

Transmission & Storage, Non‐regulated

Nation’s largest natural gas provider

h l b d h f d Geographical breadth of operations provides

diversity

4/21/2013

8

Price to Book: 1.60ROI: 4 38%

2012 Revenue: $2114 million

2012 Net Income: $217 millionROI: 4.38%Beta: .5

2012 Net Income: $217 million

Annual Dividend Yield: 3.4%

For‐Profit College Of Secondary Education And o o t Co egeO Seco da y ducat o dTraining Medical/Healthcare/Health Sciences Business/Management Engineering Accounting and Finance Training

8 % G th R t F Th N t Y 8.95% Growth Rate For The Next 5 Years

Risks: Regulations

4/21/2013

9

Key Statistics Price (11/26/2012) – 32 81

Recent Acquisitions

ATC International (2011) Price (11/26/2012) – 32.81

Market Cap – 2.07B

52 Week Range – 18.15 – 3.32

EPS (ttm) – 2.39

Beta – 1.6

Multiples

ATC International (2011) A Subsidiary Of Becker

Professional Education

Professional Finance And Accounting Training

American University Of The Caribbean (2011)

d l h lMultiples P/E = 13.73 P/B = 1.47 P/S = 1.01

Medical School

Devry Brasil (2009) & Fanor Expanding Business

4/21/2013

10

Global manufacturer of fiber lasers, fiber amplifiers, and d d ldiode lasers Cheaper, smaller, more powerful, more efficient Fully vertically integrated

Highest quarterly revenue growth amongst direct

competitors (17.4%)

Highest ROE & ROA in industry (small/mid‐cap)g y ( / p)

Highest gross margin amongst competitors

#2 in Boston Globe 100 in 2012

2012 Net Income: $147.7 million 22% Growth

2011 R&D: $31.4 million 33% of op. exp.

ROE: IPGP: 23.97% Industry: 6.05%

EPS (ttm): IPGP: $2.81 Industry: $0.05

Op. Margin: IPGP: 37% Industry: 7%

4/21/2013

11

Target Price $24 47 Current Price $24 31Target Price $24.47 ‐Current Price $24.31

Recommendation: Strong Hold

Company & Industry Information

iRobot is in the Household Appliance industry and builds advanced robots.

Contract products: Used by Military and police for bomb detection and donationUsed by Military and police for bomb detection and donation.

Household products:Robotic household cleaning devices, such as vacuums, floor cleaners, etc. Recently iRobot has moved into the medical robotics field.

4/21/2013

12

IRBT• Gross Margin: 40%• P/S: 1.56• Beta: 1.38• ROA: 5.02%• ROE: 6.07%• ROI: 6.53%

Industry • Gross Margin: 20%• P/S: 1.24• Beta: 1.05• ROA: 2.58%• ROE: 4.36%• ROI: 3.48%

• iRobot has been working to change its business focus recently, moving from primarily government contract revenue to consumer products.

The chart above compares iRobot Corporation to the S&P 500 and the Appliance Companies over the past six months

H ld ti T t P i f $ Hold rating –Target Price of $7.72

Specialty finance company

Investment portfolio composed of high yield

securities and commercial real estate

Recent acquisition of Colonie Center, a 1.3 million

square foot regional mall

4/21/2013

13

Key Statistics

Price (04/19/2013) – $10.18

Market Cap 1 81B

P/E (ttm) ‐ 5.45

P/B ‐ .98 Market Cap – 1.81B

52 Week Range ‐ $7.95 ‐ 11.93

Beta – 1.12

/ 9 P/S = 3.6

EPS (ttm) – $1.87

Omega Protein is a vertically integrated producer of omega‐3 fish oil and specialty fish meal

d d i i l i di products, and nutritional ingredient company.

Fish oil is directly approved by the FDA as the only marine source of long‐chain Omega‐3’s.

Recent human nutrition acquisitions, which produce dietary & health supplements.

4/21/2013

14

Omega Protein

Valuation

Price to Book = .92

Price to Sales = .81

Profitability

Industry

Valuation

Price to Book = 1.39

Price to Sales = 1.09

Profitability

ROI = 1.6%

EBIT = 5.36%

NPM = 1.72%

ROI = 2.86%

EBIT = 7.69%

NPM = 6.93%

4/21/2013

15

Target price $41.20

Global Offshore Contract Drilling Company

L di i Hi h S ifi ti J k il Ri Leading in High‐Specification Jack‐up oil Rigs

Currently operates 31 rigs

Key Statistics Price (04/19/2013) – 31 24 Price (04/19/2013) – 31.24

Market Cap ‐ 3.88B

52 Week Range – 28.62‐39.40

EPS (ttm) – 1.46

Beta – 1.77

Debt to equity‐44.35

Multiples P/E = 21.44 P/B = 0.94 P/S = 2.79

4/21/2013

16

Recommendation: Hold

Address the unmet needs of patients with chronic

and life‐threatening conditions

Offers 3 products that treat pulmonary arterial Offers 3 products that treat pulmonary arterial

hypertension

Market Cap of 3.02B – Larger Biotech Firm

UTHR: Industry:

P/B: 2.76 16.2

P/E 10.55 86.30

Net Profit: 34.15% 10.10%

ROE: 14.73% 8.8%

Debt/Equity: 25.37 103.6

4/21/2013

17

35.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Ram Fund

S&P 400

S&P 600

0.00%

5.00%

Real Estate

Consumer Defensive

Healthcare

Utilities

Communication Services

Energy

Industrials

Technology

Dow Jones US Total Market

Portfolio

0 5 10 15 20

Basic Materials

Consumer Cyclical

Financial Services

4/21/2013

18

Practical applications Practical applications

Access to large scale financial databases

Team orientationTeam orientation

Exposure to & preparation for the CFA exam

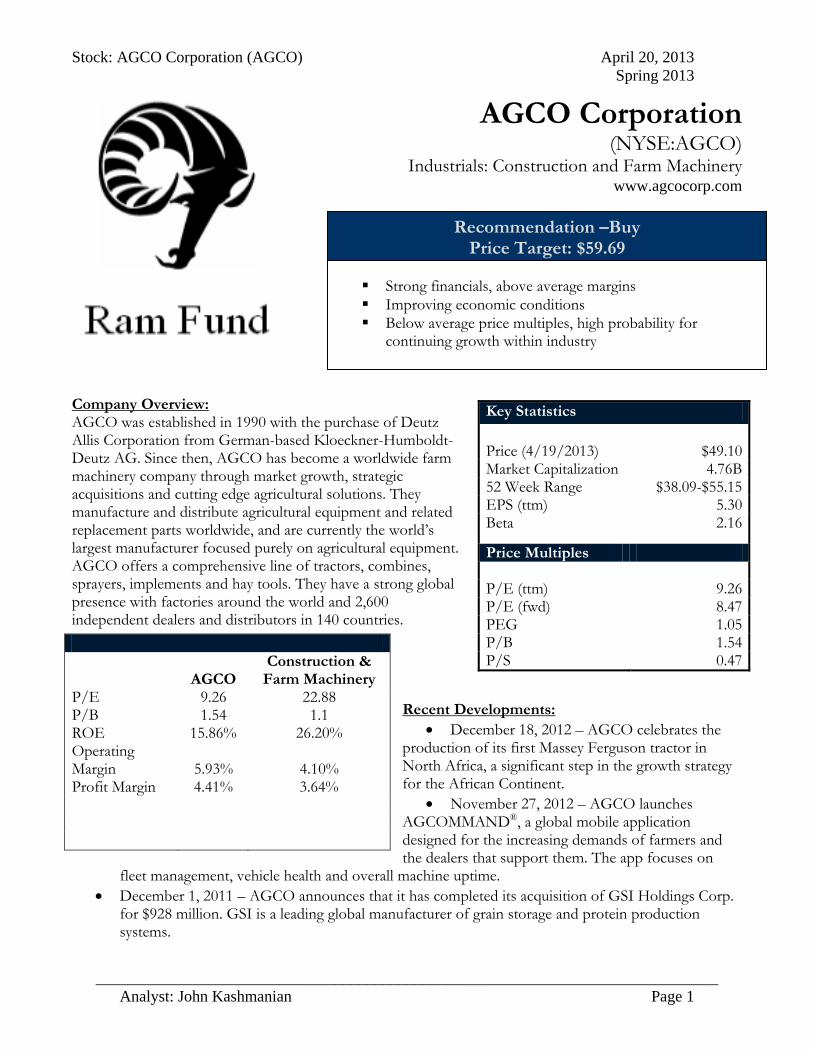

Stock: AGCO Corporation (AGCO) April 20, 2013 Spring 2013

______________________________________________________________________________ Analyst: John Kashmanian Page 1

AGCO Corporation (NYSE:AGCO)

Industrials: Construction and Farm Machinery www.agcocorp.com

Company Overview: AGCO was established in 1990 with the purchase of Deutz Allis Corporation from German-based Kloeckner-Humboldt-Deutz AG. Since then, AGCO has become a worldwide farm machinery company through market growth, strategic acquisitions and cutting edge agricultural solutions. They manufacture and distribute agricultural equipment and related replacement parts worldwide, and are currently the world’s largest manufacturer focused purely on agricultural equipment. AGCO offers a comprehensive line of tractors, combines, sprayers, implements and hay tools. They have a strong global presence with factories around the world and 2,600 independent dealers and distributors in 140 countries.

Recent Developments:

• December 18, 2012 – AGCO celebrates the production of its first Massey Ferguson tractor in North Africa, a significant step in the growth strategy for the African Continent.

• November 27, 2012 – AGCO launches AGCOMMAND®, a global mobile application designed for the increasing demands of farmers and the dealers that support them. The app focuses on

fleet management, vehicle health and overall machine uptime. • December 1, 2011 – AGCO announces that it has completed its acquisition of GSI Holdings Corp.

for $928 million. GSI is a leading global manufacturer of grain storage and protein production systems.

Key Statistics Price (4/19/2013) $49.10 Market Capitalization 4.76B 52 Week Range $38.09-$55.15 EPS (ttm) 5.30 Beta 2.16

Price Multiples P/E (ttm) 9.26 P/E (fwd) 8.47 PEG 1.05 P/B 1.54 P/S 0.47

AGCO

Construction & Farm Machinery

P/E 9.26 22.88 P/B 1.54 1.1 ROE 15.86% 26.20% Operating Margin Profit Margin

5.93%

4.41%

4.10%

3.64%

Recommendation –Buy Price Target: $59.69

Strong financials, above average margins Improving economic conditions Below average price multiples, high probability for

continuing growth within industry

Stock: AGCO Corporation (AGCO) April 20, 2013 Spring 2013

______________________________________________________________________________ Analyst: John Kashmanian Page 2

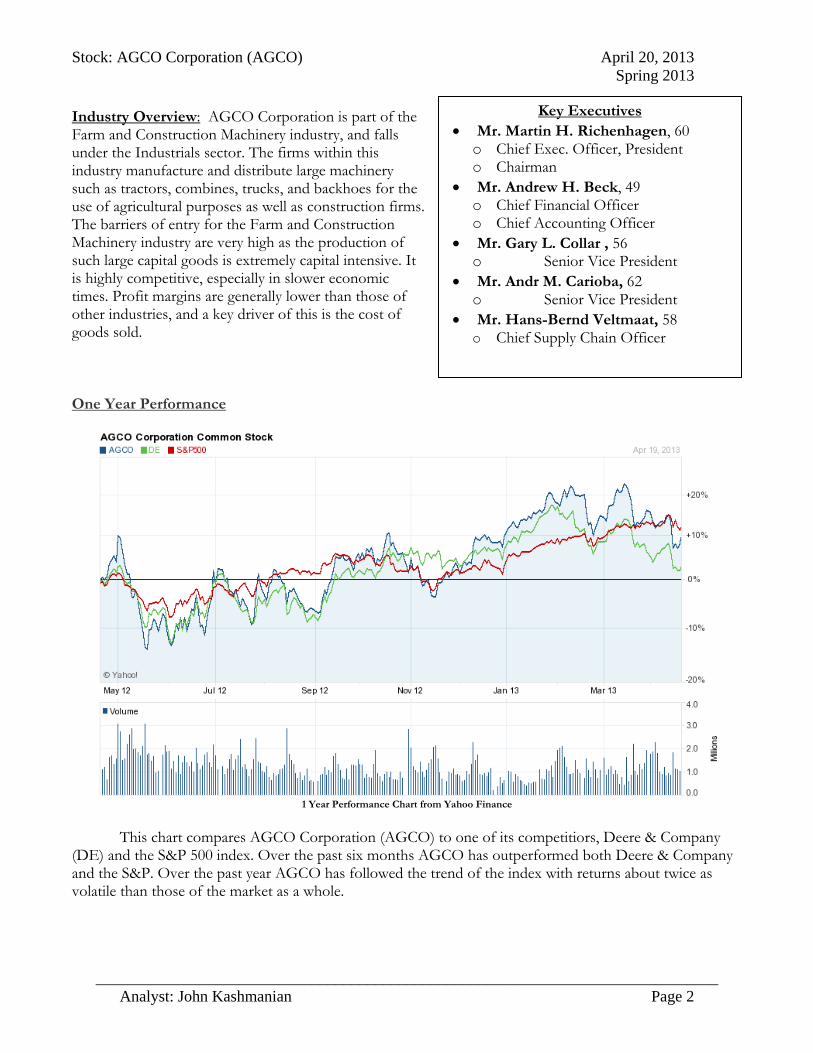

Industry Overview: AGCO Corporation is part of the Farm and Construction Machinery industry, and falls under the Industrials sector. The firms within this industry manufacture and distribute large machinery such as tractors, combines, trucks, and backhoes for the use of agricultural purposes as well as construction firms. The barriers of entry for the Farm and Construction Machinery industry are very high as the production of such large capital goods is extremely capital intensive. It is highly competitive, especially in slower economic times. Profit margins are generally lower than those of other industries, and a key driver of this is the cost of goods sold. One Year Performance

1 Year Performance Chart from Yahoo Finance

This chart compares AGCO Corporation (AGCO) to one of its competitiors, Deere & Company

(DE) and the S&P 500 index. Over the past six months AGCO has outperformed both Deere & Company and the S&P. Over the past year AGCO has followed the trend of the index with returns about twice as volatile than those of the market as a whole.

Key Executives • Mr. Martin H. Richenhagen, 60 o Chief Exec. Officer, President o Chairman

• Mr. Andrew H. Beck, 49 o Chief Financial Officer o Chief Accounting Officer

• Mr. Gary L. Collar , 56 o Senior Vice President

• Mr. Andr M. Carioba, 62 o Senior Vice President

• Mr. Hans-Bernd Veltmaat, 58 o Chief Supply Chain Officer

Stock: AGCO Corporation (AGCO) April 20, 2013 Spring 2013

______________________________________________________________________________ Analyst: John Kashmanian Page 3

Factors that Affect the Industry: The major driver of the Farm and Construction industry is the overall health of the economy.

Strong health will generally translate into higher corporate and government spending, both a necessity for the growth and sustainability of the industry. It has been hit by slow economic growth following the global financial crisis, which took a particular toll on global construction activity. Things seem to be finally turning around for the industry though, as an improving global economy and rising food prices are allowing farmers to spend more money on machinery. Company Outlook: AGCO Corporation is continually growing with expanding operations in North America, South America, Europe, Asia and Australia. They are also finally breaking ground in Africa in which there are tremendous growth possibilities. The population of Africa is expected to grow to 2 billion by 2050 which translates into enormous future agricultural needs. With frequent acquisitions AGCO is also proving that is can expand into different specialized markets with growing market share. With healthy financials, positive growth potential and a bullish stance on the overall economy the future outlook for AGCO is bright. Current valuation puts AGCO at an intrinsic value of $59.69 per share, about 20% higher than current market value. This indicates a recommendation of strong buy. Free Cash Flow Projections:

Shares Outstanding 96.04 Initial Growth 8.70% Terminal Growth 2.5% Expected P/E 9.0 Req. Rate of Return 12% Debt Ratio 55% Depreciation/Sales 1.8% CapEx/Sales 5.6% NWC/Sales 18.0%

Year

2012 2013 2014 2015 2016 2017 Net Income

$809.45 $938.73 $1,084.37 $1,248.25 $1,432.44

Depreciation

$194.92 $211.88 $230.31 $250.35 $272.13 CAP. Expenditures

$606.42 $659.18 $716.53 $778.86 $846.62

NWC

$1,741.10 $1,949.20 $2,118.78 $2,303.12 $2,503.49 $2,721.29 Change In NWC

$208.10 $169.58 $184.33 $200.37 $217.80

Free Cash Flow

$637.83 $321.85 $413.82 $519.37 $640.14 Terminal Value

$6,906.79

Total Cash Flow

$637.83 $321.85 $413.82 $519.37 $7,546.93 Discount Factor

1.12 1.25 1.40 1.57 1.76

PV of CF

$569.49 $256.57 $294.55 $330.07 $4,282.33 Intrinsic Value $5,733.02

Value Per share $59.69

Stock: AGCO Corporation (AGCO) April 20, 2013 Spring 2013

______________________________________________________________________________ Analyst: John Kashmanian Page 4

Terminal Growth

59.69 2.0% 2.5% 3.0% 3.5% 4.0% 4.5% Initial

Growth 6% 56.64 58.81 61.21 63.89 66.91 70.34

7% 56.99 59.18 61.61 64.33 67.38 70.85

8% 57.29 59.50 61.96 64.71 67.80 71.30

9% 57.53 59.77 62.25 65.03 68.16 71.70

10% 57.73 59.99 62.50 65.30 68.45 72.02

11% 57.87 60.15 62.68 65.50 68.68 72.28

12% 57.96 60.25 62.79 65.64 68.84 72.47

13% 57.98 60.29 62.85 65.71 68.93 72.57

14% 57.94 60.26 62.83 65.70 68.94 72.60

15% 57.84 60.16 62.74 65.62 68.86 72.54

16% 57.66 59.99 62.57 65.46 68.71 72.39

17% 57.41 59.74 62.32 65.21 68.46 72.15

18% 57.08 59.40 61.99 64.87 68.12 71.80

19% 56.67 58.99 61.57 64.45 67.69 71.36

20% 56.18 58.48 61.05 63.92 67.14 70.80

Stock: AGCO Corporation (AGCO) April 20, 2013 Spring 2013

______________________________________________________________________________ Analyst: John Kashmanian Page 5

Analysts Recommendations:

Stock: Atmos Energy Corp (ATO) April 19th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Jared Moreau Page 1

Atmos Energy Corp. (NYSE:ATO)

Utilities: Gas Utilities

http://atmosenergy.com/

Company Overview: Headquartered in Dallas, Texas, Atmos Energy Corp. is the nation’s largest natural gas provider with 3 million customers in 12 states. Atmos operates in three segments: Natural Gas Distribution, Regulated Transmission & Storage, and Non-regulated, which provides natural gas management and marketing services to municipalites, local gas distribution companies, and industrial customers.

Recent Developments: April 2nd – Robert W. Best, who was serving as executive chairman, retired form the company effective April 1, 2013. Best joined the company in March 1997 and served as chairman, president and chairman and CEO from October 2008 to October 2010.

March 31st —Despite natural gas charges falling, Atmos upped its monthly customer charge from $7.50 to $17, a 136% increase. Money is needed to help cover cost of $400 million in capital projects.

Key Statistics Price (04/19/2013) $43.176 Market Cap. $3.95B 52 Week Range $31.56-43.86 EPS (ttm) 2.50 Beta 0.5

Price Multiples P/E (ttm) 17.48 P/E (fwd) 16.61 PEG 2.93 P/B 1.60 P/S 1.15 P/CF 5.56

Key Ratios

ATO Industry Gross Margin 31.59% 41.44% Op. Profit Margin 13.8% 14.24%

ROA 3.74% 3.09% ROI 4.38% 5.61% ROE 8.83% 9.80% Current Ratio 0.71 0.95 Debt/Equity 114.99 55.1 EBITDA (millions) $713.4M $371.36M

Recommendation – Hold Price Target: $49.82

Geographical breadth of operations provide diversity in

economic conditions, weather patterns, gas supplies, and regulatory climates

Highest annual dividend yield in utilities sector, 3.4% Non-regulated operations ranked as one of leading domestic

natural gas marketers

Stock: Atmos Energy Corp (ATO) April 19th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Jared Moreau Page 2

Industry Overview:

Atmos Energy Corp. is part of the natural gas industry in the utilities sector. The industry includes domestic companies that provide distribution service to residential, commercial, and industrial customers. Wide variations in weather and swings in the economy have an impact on performance. The capital-intensive businesses are subject to federal, state, and sometimes local regulations; which determine maximum rates of return they may earn. Investors look for high dividend yield from these mature, low-growth companies with relatively stable and consistent returns. The utilities sector generally tends to outperform when the economy is weak and underperform when the economy is rallying. Investors look to this defensive sector to combat decreasing portfolio values in weak times.

The chart above shows 1-year returns for Atmos Energy Corp. (ATO), the S&P 500, and rival companies Oneok Inc. (OKE) and Xcel Energy Inc. (XEL). Over the past year Atmos has outperformed the S&P 500 and has beaten both competitors with strong earnings. In the past two months, Atmos has begun to separate itself as its returns have gained more rapidly than competitors. Company Outlook:

Atmos’ yearly revenues have been steadily decreasing at a constant rate, but its net income has not suffered. Analysts estimate growth over the next 5 years to be 6%. Atmos continues to fund new projects for expansion every year, to maintain this growth. Their geographic breadth renders the firm less exposure to certain risks relative to competitors who may operate in small segments. A sizeable portion of Atmos’ customer base has no other option for energy supply, eliciting the firm a competitive advantage of customer loyalty.

Stock: Atmos Energy Corp (ATO) April 19th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Jared Moreau Page 3

Appendix A: Discounted Cash Flow Results

2013E 2014E 2015E 2016E 2017E EBIT $259,899.15 $272,894.11 $286,538.81 $300,865.75 $315,909.04 Depreciation $15,593.95 $16,373.65 $17,192.33 $18,051.95 $18,954.54 Cap Ex $23,390.92 $24,560.47 $25,788.49 $27,077.92 $28,431.81

Net Working Capital $15,593.95 $16,373.65 $17,192.33 $18,051.95 $18,954.54 Change in NWC $306,480.95 $779.70 $818.68 $859.62 $902.60 Free Cash Flow $67,673.82 $273,303.45 $286,968.62 $301,317.05 $316,382.90

NPV Shares Share Price Constant Growth $5,397,274 90,500 $ 59.64

P/E $4,509,120 90,500 $ 49.82

Sensitivity Analysis

Appendix B: Analyst Coverage

Price Initial Growth 49.82 3.00% 4.00% 5.00% 6.00% 7.00% 8.00% 9.00% 10.00% 12.50 36.92 38.59 40.32 42.12 43.97 45.90 47.89 49.95 13.50 39.08 40.85 42.70 44.61 46.59 48.63 50.76 52.95 14.50 41.23 43.12 45.07 47.10 49.20 51.37 53.62 55.95 15.50 43.39 45.38 47.45 49.59 51.81 54.10 56.48 58.95 16.50 45.55 47.65 49.82 52.08 54.42 56.84 59.35 61.95 17.50 47.71 49.91 52.20 54.57 57.03 59.58 62.21 64.94 18.50 49.87 52.18 54.58 57.06 59.64 62.31 65.08 67.94 19.50 52.02 54.44 56.95 59.55 62.25 65.05 67.94 70.94 20.50 54.18 56.71 59.33 62.04 64.86 67.78 70.80 73.94 21.50 56.34 58.97 61.70 64.54 67.47 70.52 73.67 76.94 22.50 58.50 61.24 64.08 67.03 70.08 73.25 76.53 79.93

P/E

Stock: Atmos Energy Corp (ATO) April 19th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Jared Moreau Page 4

Via NASDAQ

Analyst Firms Making Recommendations

BANK OF AMERICA ML ARGUS RESEARCH

BARCLAYS CAPITAL EDWAR JONES J.J.B. HILLIARD

US CAPITAL ADV UBS

GOLDMAN SACHS

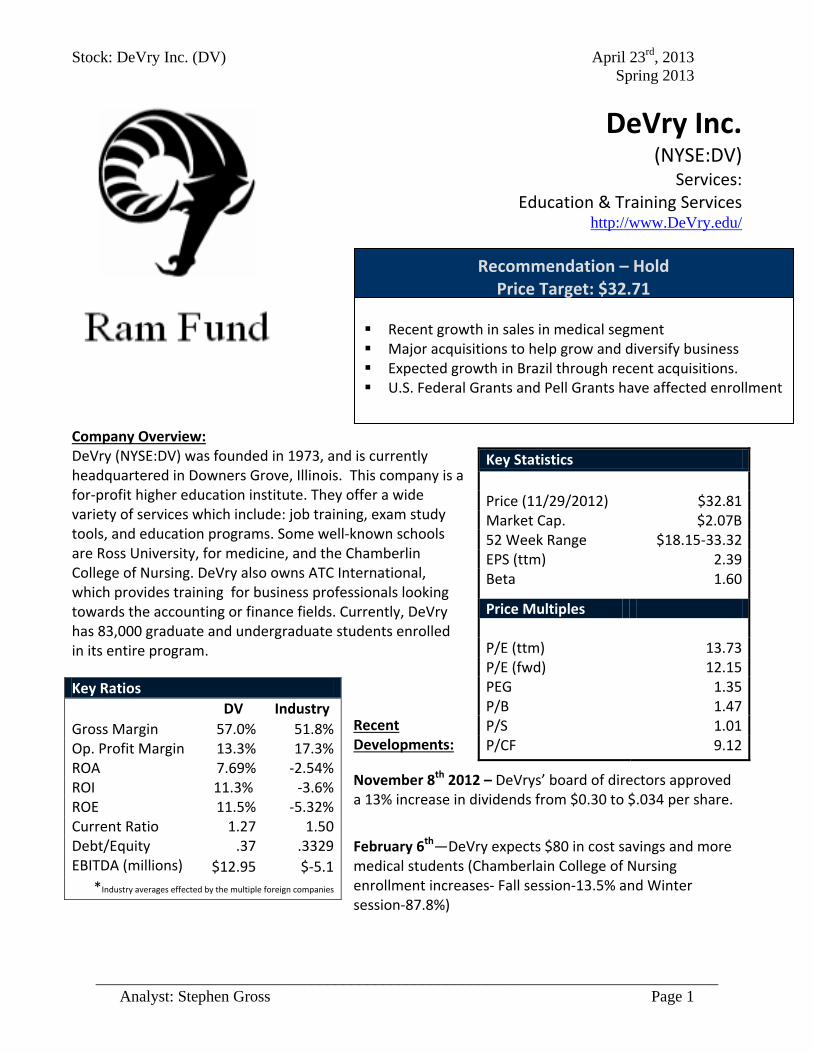

Stock: DeVry Inc. (DV) April 23rd, 2013 Spring 2013

______________________________________________________________________________ Analyst: Stephen Gross Page 1

DeVry Inc. (NYSE:DV)

Services: Education & Training Services

http://www.DeVry.edu/

Company Overview: DeVry (NYSE:DV) was founded in 1973, and is currently headquartered in Downers Grove, Illinois. This company is a for-profit higher education institute. They offer a wide variety of services which include: job training, exam study tools, and education programs. Some well-known schools are Ross University, for medicine, and the Chamberlin College of Nursing. DeVry also owns ATC International, which provides training for business professionals looking towards the accounting or finance fields. Currently, DeVry has 83,000 graduate and undergraduate students enrolled in its entire program.

Recent Developments:

November 8th 2012 – DeVrys’ board of directors approved a 13% increase in dividends from $0.30 to $.034 per share.

February 6th—DeVry expects $80 in cost savings and more medical students (Chamberlain College of Nursing enrollment increases- Fall session-13.5% and Winter session-87.8%)

Key Statistics Price (11/29/2012) $32.81 Market Cap. $2.07B 52 Week Range $18.15-33.32 EPS (ttm) 2.39 Beta 1.60

Price Multiples P/E (ttm) 13.73 P/E (fwd) 12.15 PEG 1.35 P/B 1.47 P/S 1.01 P/CF 9.12

Key Ratios

DV Industry Gross Margin 57.0% 51.8% Op. Profit Margin 13.3% 17.3% ROA 7.69% -2.54% ROI 11.3% -3.6% ROE 11.5% -5.32% Current Ratio 1.27 1.50 Debt/Equity .37 .3329 EBITDA (millions) $12.95 $-5.1

*Industry averages effected by the multiple foreign companies

Recommendation – Hold Price Target: $32.71

Recent growth in sales in medical segment Major acquisitions to help grow and diversify business Expected growth in Brazil through recent acquisitions. U.S. Federal Grants and Pell Grants have affected enrollment

Stock: DeVry Inc. (DV) April 23rd, 2013 Spring 2013

______________________________________________________________________________ Analyst: Stephen Gross Page 2

Industry Overview:

DeVry is in the education and training services industry which is considered a part of the service sector. These companies are considered For-Profit education entities. The markets for these services are extremely dependent on government regulation because of federal grant and student financial assistance programs. According to Yahoo! Finance, this industry is made up of roughly 39 companies with a market cap of $48.7 billion. It has performed well as of late due to new product launches and recent acquisitions made by the leading performers. Also, with President Obama remaining in the White House, companies in this industry should benefit from his Affordable Health Care Act as more Americans will be insured.

The chart above compares DeVry (DV) to the S&P 500 and rival companies Apollo Group (APOL) and Lincoln Educations Services (LINC). Over the past year DeVry has underperformed the S&P 500 and outperformed competitors. In July 2011, there was a sharp drop in enrollment for For-Profit colleges. Also, in July 2012 there was a sharp decline due to a change in Q4 2012 Guidance estimates. Company Outlook:

DeVry has had a main focus on cost savings. DeVry has seen enrollment totals decrease overall. As there student service and administrative expenses have increased over the last 5 years, DeVry has looked for cost saving measures. This is expected to cut costs by one-third to around $80 million a year. Enrollments at the company’s medical and healthcare colleges have seen strong growth (Ross University, Chamberlain College). This part of the company is expected to continue to grow. The acquisitions of ATC International, which provides accounting and finance training, and the recent acquisition of American University of the Caribbean, a medical school based in St. Maarten. Lastly, DeVry has continued to expand its operation in Brazil through DeVry Brasil. DeVry Brasil is located in the country’s northeast and has seen solid growth.

Stock: DeVry Inc. (DV) April 23rd, 2013 Spring 2013

______________________________________________________________________________ Analyst: Stephen Gross Page 3

Appendix A: Discounted Cash Flow Results

Assumptions

Sales Growth 8.95% Debt 12% NWC % 8%

P/E 13.4 Terminal Sales Growth 0% CapEx % 6%

P/S .78

Free Cash Flow (000’s) 2012 2013 2014 2015 2016 2017 Net Income 152,007 165,612 180,434 196,583 214,177

+ Depreciation 68,499 74,629 81,309 88,586 96,514 ∆ NWC 46,031 182,145 198,447 216,208 235,559 256,642 + Depreciation 136,114 16,302 17,761 19,351 21,083

- Capital Expenditures 145,984 159,050 173,285 188,793 205,691 Free Cash Flow*(1-Debt

Ratio=12%) 145,984 159,050 173,285 188,793 205,691

Sensitivity Analysis

Price Initial Growth

$

32.71 5% 6% 7% 8% 9% 10% 11% 12%

P/E 8 18.09 18.83 19.61 20.41 21.20 22.10 22.99 23.91

9 19.86 20.70 21.56 22.45 23.33 24.34 25.33 26.36

10 21.64 22.56 23.51 24.50 25.47 26.58 27.68 28.81

11 23.41 24.42 25.46 26.54 27.61 28.82 30.02 31.27

12 25.19 26.28 27.41 28.59 29.74 31.06 32.37 33.72

13 26.97 28.14 29.37 30.63 31.88 33.30 34.71 36.17

14 28.74 30.01 31.32 32.68 34.01 35.55 37.06 38.62

15 30.52 31.87 33.27 34.72 36.15 37.79 39.40 41.07

16 32.29 33.73 35.22 36.77 38.29 40.03 41.75 43.53

17 34.07 35.59 37.17 38.81 40.42 42.27 44.09 45.98

18 35.85 37.46 39.12 40.86 42.56 44.51 46.44 48.43

19 37.62 39.32 41.08 42.90 44.70 46.75 48.78 50.88

20 39.40 41.18 43.03 44.95 46.83 48.99 51.13 53.34

Stock: DeVry Inc. (DV) April 23rd, 2013 Spring 2013

______________________________________________________________________________ Analyst: Stephen Gross Page 4

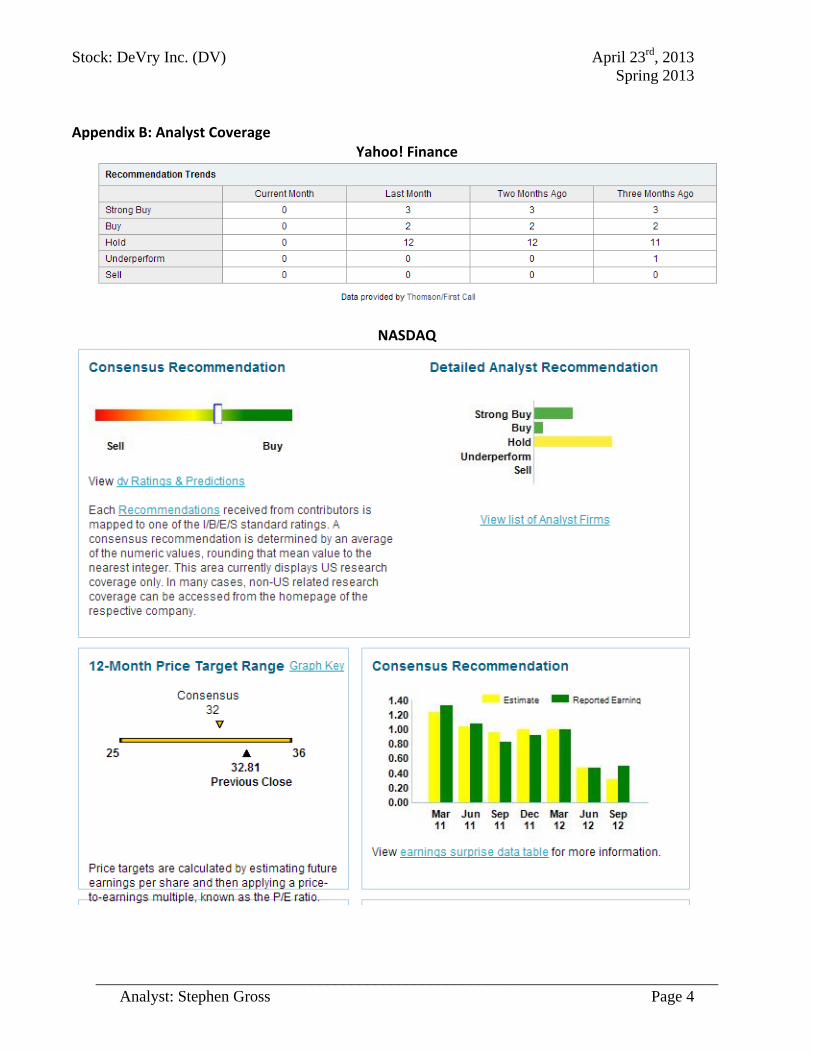

Appendix B: Analyst Coverage

Yahoo! Finance

NASDAQ

Stock: IPG Photonics Corporation April 23, 2013 Spring 2013

______________________________________________________________________________ Analyst: Park Guo Page 1

IPG Photonics Corporation (Nasdaq:IPGP) Technology: Semiconductor-Integrated Circuits

http://www.ipgphotonics.com/

Company Overview: Founded in 1990 in Russia, IPG Photonics is a leading provider in fiber lasers and fiber amplifiers. The company is currently headquartered in Oxford, Massachusetts and operates internationally with a wide range of customers. It now has sales offices in thirteen countries including the United States, China, and Russia as well as seven materials processing application centers. As of 2012, IPGP had over 1,900 customers worldwide and no one customer represents more than 7% of their total sales. IPGP maintains a strong market presence by selling do diverse customer base. Materials processing represents a large portion of their income and includes titanium air frame welding in the aerospace sector to credit card marking for consumers. IPGP has been increasing expenditures in acquiring businesses and facilities to expand its business even more.

Recent Developments • 04/17/2013- Michael Klosof IPGP became board member for Mi-Light, a non-profit organization in Michigan for supporting and promoting the growth of photonics in the US • 04/09/2013- New US patent has been issued to IPGP for “Wavelength stabilized light emitter and system for protecting emitter from backreflected light.” • 09/04/2012- Expanded integrated laser systems offerings with the acquisition of JP Sercel Associates Inc.

Key Statistics Price (04/18/2013) $61.60 Market Capitalization

3.18 B

52 Week Range $37.58-70.11 EPS (ttm) 2.81 Beta 1.67

Price Multiples Price/Earnings (ttm) 22.04 Price/Earnings (fwd) 16.96 PEG Ratio 0.92 Price/Book 4.28 Price/Sales 5.66

Key Ratios

IPGP Industry

Net Profit Margin 25.78% 11.8% ROA (ttm) 19.65% 2.74% ROE 23.97% 10.6% Current Ratio 5.3 2.56 Debt/Equity P/E Ratio

2.3 22.17

33.24 39.33

Recommendation –Hold Fair Value: $72.69

• Capital expenditures increased approximately 28% during 2012

• Increasing growth in sales and reduction of cost of sales

• Increased diverse customer base by 11.7% to 1,900 worldwide

customers

Stock: IPG Photonics Corporation April 23, 2013 Spring 2013

______________________________________________________________________________ Analyst: Park Guo Page 2

Industry Overview: The semiconductor industry can be viewed as the backbone of all modern day technology. Within the technology sector, semiconductors are further divided into broad line, integrated circuits, specialized, equipment and materials, and memory chips. Each individual division provides the essential foundation for the technology we have today. The focus of this analysis is based on the integrated circuits of the semiconductor industry. The growth of this industry is dependent on the capital expenditure of customers, especially manufacturers in the materials processing market. Revenues are generated through the sales of its products, primarily fiber lasers, to various end-users. The industry is subject to risks such as environmental regulations, certificate requirements, seasonal reduction in business activities, etc. During the past year, the economy has improved marginally and the improvement will lead to increased consumer spending. Increased spending will cause manufacturers to invest in capital expenditures in order to preserve and improve their efficiency.

The chart above compares the performance of IPG Photonics (IPGP)totwo close competitors as

identified by Yahoo! Finance: Coherent, Inc. (COHR)and FANUC Corporation (FANUY), as well as the S&P 500(^GSPC)market index over thepast five years. Company Outlook: Since the economic slowdown, IPG Photonics has been steadily increasing their sales and driving up their share price. Acquisitions of bright startup companies as well as vertically integrating their manufacturing processes makes them the top performing firm within the industry. Capital expenditures have also been increasing in recent years which show the desire to expand their reach to even more countries. Their expertise in the field of fiber lasers coupled with the expansion facilities allows IPG Photonics to expand their business into more diverse market segments.

Stock: IPG Photonics Corporation April 23, 2013 Spring 2013

______________________________________________________________________________ Analyst: Park Guo Page 3

Appendix A: Discounted Cash Flow Results and Sensitivity(Dollar figures in thousands)

Stock: IPG Photonics Corporation April 23, 2013 Spring 2013

______________________________________________________________________________ Analyst: Park Guo Page 4

Appendix B: Analyst Coverage Via NASDAQ

`

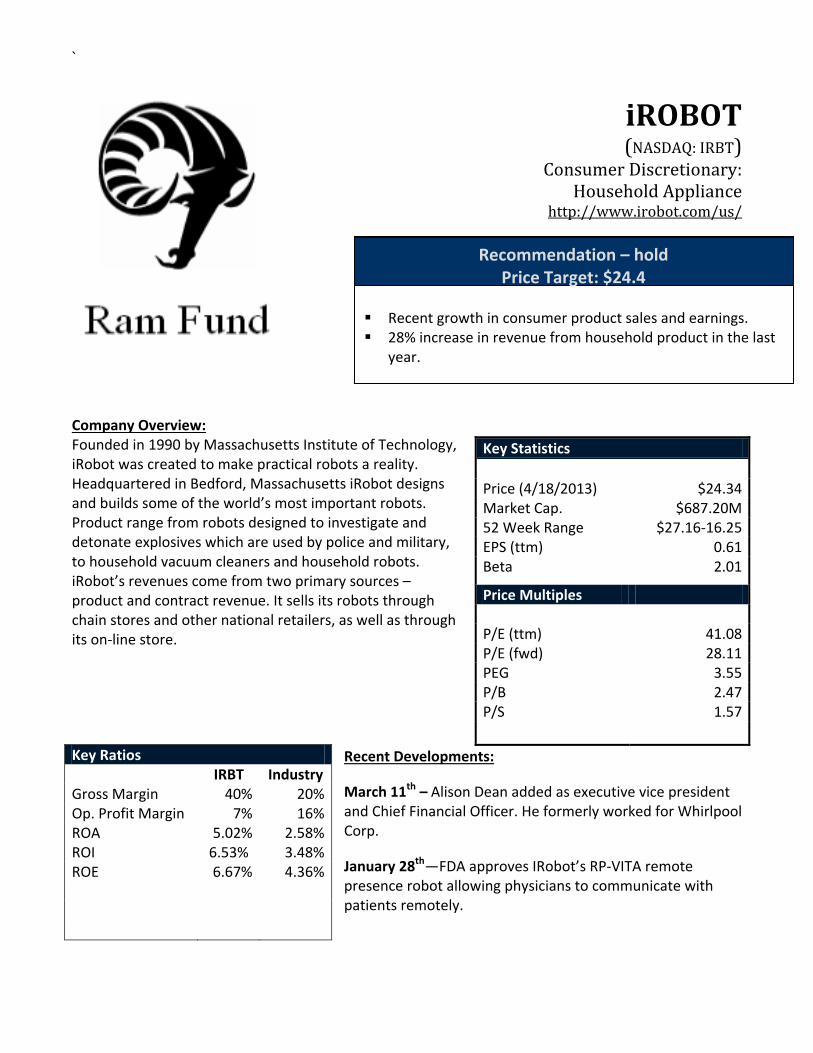

iROBOT (NASDAQ: IRBT)

Consumer Discretionary: Household Appliance

http://www.irobot.com/us/

Company Overview: Founded in 1990 by Massachusetts Institute of Technology, iRobot was created to make practical robots a reality. Headquartered in Bedford, Massachusetts iRobot designs and builds some of the world’s most important robots. Product range from robots designed to investigate and detonate explosives which are used by police and military, to household vacuum cleaners and household robots. iRobot’s revenues come from two primary sources – product and contract revenue. It sells its robots through chain stores and other national retailers, as well as through its on-line store.

Recent Developments:

March 11th – Alison Dean added as executive vice president and Chief Financial Officer. He formerly worked for Whirlpool Corp.

January 28th—FDA approves IRobot’s RP-VITA remote presence robot allowing physicians to communicate with patients remotely.

Key Statistics Price (4/18/2013) $24.34 Market Cap. $687.20M 52 Week Range $27.16-16.25 EPS (ttm) 0.61 Beta 2.01

Price Multiples P/E (ttm) 41.08 P/E (fwd) 28.11 PEG 3.55 P/B 2.47 P/S 1.57

Key Ratios

IRBT Industry Gross Margin 40% 20% Op. Profit Margin 7% 16% ROA 5.02% 2.58% ROI 6.53% 3.48% ROE 6.67% 4.36%

Recommendation – hold Price Target: $24.4

Recent growth in consumer product sales and earnings. 28% increase in revenue from household product in the last

year.

`

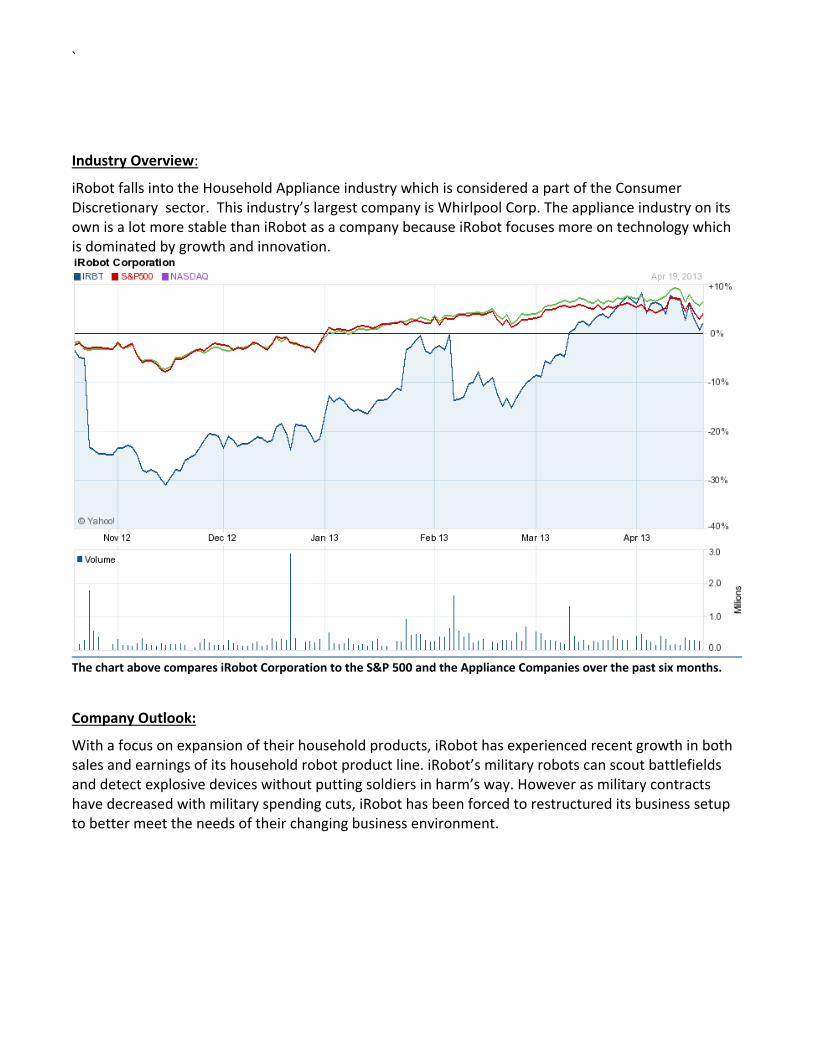

Industry Overview:

iRobot falls into the Household Appliance industry which is considered a part of the Consumer Discretionary sector. This industry’s largest company is Whirlpool Corp. The appliance industry on its own is a lot more stable than iRobot as a company because iRobot focuses more on technology which is dominated by growth and innovation.

The chart above compares iRobot Corporation to the S&P 500 and the Appliance Companies over the past six months. Company Outlook:

With a focus on expansion of their household products, iRobot has experienced recent growth in both sales and earnings of its household robot product line. iRobot’s military robots can scout battlefields and detect explosive devices without putting soldiers in harm’s way. However as military contracts have decreased with military spending cuts, iRobot has been forced to restructured its business setup to better meet the needs of their changing business environment.

`

Appendix A: Discounted Cash Flow Results

Discounted Cash Flow Results:Debt Ratio 23%CapX/Sales 3%DEPREC/SALES 3%NWC/Sales 40.0%Sales Growth 12.0%PE 40.0RROR 12.0%Shares Outstanding 27.9

Year 2012 2013E 2014E 2015E 2016E 2017ENet income 18939 21186 23699 26509 29653Depreciation 12703.43 14228 15935 17847 19989.1Net Working Cap 160,395 195437.3 218890 245157 274575 307524Change in NWC 35,042 23,452 26,267 29,419 32,949Cap EX 14657.8 16417 18387 20593 23064.3FCF -6626.66 4714.5 5250.6 5847.4 6512.02Year for PV calculations: 1 2 3 4 5Terminal Value (PE) 1186129Total CF -6626.66 4714.5 5250.6 5847.4 1192641Discount Factor 1.12 1.2544 1.4049 1.5735 1.76234PV of CF -5916.66 3758.4 3737.2 3716.2 676737Intrinsic Value 682031.7725Value per Share 24.47$

Growth

Terminal P/E 24.47 0.08 0.09 0.1 0.11 0.12 0.13 0.14 0.1535 22.41 22.18 21.95 21.70 21.45 21.19 20.93 20.6536 23.01 22.79 22.55 22.31 22.06 21.80 21.53 21.2537 23.62 23.39 23.15 22.91 22.66 22.40 22.13 21.8638 24.22 23.99 23.76 23.52 23.26 23.00 22.74 22.4639 24.82 24.60 24.36 24.12 23.87 23.61 23.34 23.0640 25.43 25.20 24.97 24.72 24.47 24.21 23.94 23.6741 26.03 25.80 25.57 25.33 25.08 24.82 24.55 24.2742 26.64 26.41 26.17 25.93 25.68 25.42 25.15 24.8743 27.24 27.01 26.78 26.53 26.28 26.02 25.76 25.4844 27.84 27.62 27.38 27.14 26.89 26.63 26.36 26.0845 28.45 28.22 27.98 27.74 27.49 27.23 26.96 26.6946 29.05 28.82 28.59 28.35 28.09 27.83 27.57 27.2947 29.65 29.43 29.19 28.95 28.70 28.44 28.17 27.8948 30.26 30.03 29.80 29.55 29.30 29.04 28.77 28.50

P/E

Stock: KKR Financial Holdings LLC (KFN) April 2013 Spring 2013

______________________________________________________________________________ Analyst: Bryan Poston Page 1

KKR Financial Holdings LLC (NYSE:KFN) Specialized Finance

Company Overview: KKR Financial Holdings LLC is a specialized finance company founded in 2004 in San Francisco, California. KKR typically invests in a large range of financial assets. These assets range anywhere from high yield bonds to corporate loans to other debt securities. Just recently, KKR has begun to invest in the retail real estate market, acquiring a few shopping malls across the United States in partnership with some other investment firms. In these types of investments, KKR usually works as the majority owner of the commercial real estate, working as both owner and general manager of the asoociated property. KKR Financial also has a Natural Resources segment, which invests in both oil and natural gas properties, mostly located in the continental United States.

Current Developments • Earnings call May 1, 2013 • March 11, 2013 - Dividends/share of $.05 paid • Diluted Earnings per share of $1.87 • Enterprise Value of 8.01B

Key Statistics Price (04/19/2012) 10.18 Market Capitalization 1.81B 52 Week Range 7.95 - 11.93 EPS (ttm) 1.87 Beta 1.12 Price Multiples P/E (ttm) 5.45 P/B 0.98 P/S 3.6 P/CF 6.93

Key Ratios (04/19/2013)

KFN Industry ROA

3.68%

0.93%

ROE (ttm) 18.98% 8.21% ROI P/E (ttm)

3.76% 7.05

4.58% 18.18

P/B 0.98 1.46 Dividend Yield 5.95% 3.06%

Recommendation – Hold Price Target: $7.72

• Diverse portfolio of financial assets • Recent entry into commercial real estate • Inconsistent cash flows and investment related income • High yield investments

Stock: KKR Financial Holdings LLC (KFN) April 2013 Spring 2013

______________________________________________________________________________ Analyst: Bryan Poston Page 2

Industry Overview: Specialty finance companies typically invest in a broad range of financial assets. This includes but is not limited to bonds, loans, debt securities, equity related investments, and real estate. The executive management of each firm determines an investment strategy for analysts and investors to follow. Due to the high diversity of investment options that are available for firms to pick from, each firm is highly unique within its industry. Many firms are categorized further based on the nature of their major investments. In context, KKR Financial Holdings LLC is now considered a mortgage investment firm more than anything else. This categorization is available largely to aid in comparison between companies in the industry.

6 Month Performance Chart from Google Finance

The above chart provides a comparison of KKR Financial Holdings LLC (KFN) to the S&P 500 and a competitor, Prospect Capital Corporation. KKR has largely outpaced both the S&P and Prospect Capital Corporation since last September.

Factors that Affect the Industry: The financial sector is strongly affected by interested rates as well as government regulation. Especially in regards to KKR Financial, financial assets are often acquired using debt or other financial instruments. Due to this factor, firms in this industry have a tendency to alter their investment strategies based on changes in interest rates. On top of that, the government plays a major role in the regulation and management of the industry. Each investment firm encounters a significant amount of cost with respect to staying in line with current regulations. With the high volume of investment related transactions throughout the year, firms must work extremely diligently in order to follow proper reporting procedures. Company Outlook:

Recent Acquisition • Colonie Center (04/9/2013)

o 1.3 million square foot super-regional mall with over 113 stores in Albany, New York

o Made in conjunction with Colonie Pacific

o Rennovated in 2007 attracting L.L. Bean, P.F. Chang's, and The Cheesecake Factory

o Addition of a 13 screen cinema and a Whole Foods location to be completed in 2014

Stock: KKR Financial Holdings LLC (KFN) April 2013 Spring 2013

______________________________________________________________________________ Analyst: Bryan Poston Page 3

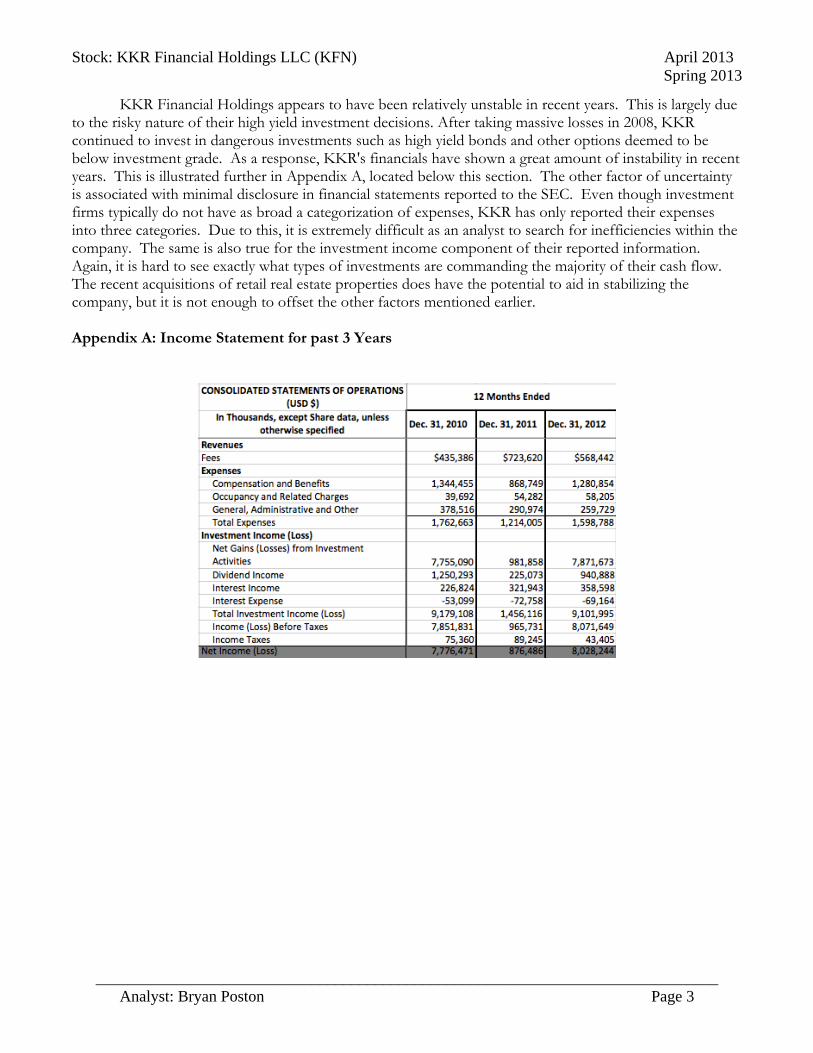

KKR Financial Holdings appears to have been relatively unstable in recent years. This is largely due to the risky nature of their high yield investment decisions. After taking massive losses in 2008, KKR continued to invest in dangerous investments such as high yield bonds and other options deemed to be below investment grade. As a response, KKR's financials have shown a great amount of instability in recent years. This is illustrated further in Appendix A, located below this section. The other factor of uncertainty is associated with minimal disclosure in financial statements reported to the SEC. Even though investment firms typically do not have as broad a categorization of expenses, KKR has only reported their expenses into three categories. Due to this, it is extremely difficult as an analyst to search for inefficiencies within the company. The same is also true for the investment income component of their reported information. Again, it is hard to see exactly what types of investments are commanding the majority of their cash flow. The recent acquisitions of retail real estate properties does have the potential to aid in stabilizing the company, but it is not enough to offset the other factors mentioned earlier. Appendix A: Income Statement for past 3 Years

Stock: KKR Financial Holdings LLC (KFN) April 2013 Spring 2013

______________________________________________________________________________ Analyst: Bryan Poston Page 4

Appendix B: Analyst Coverage

http://www.nasdaq.com/symbol/kfn/analyst-research

Stock: Omega Protein Corp. April 20, 2012 Spring 2013

______________________________________________________________________________ Analyst: Mark Albanese Page 1

Omega Protein Corp. (Nasdaq:OME) Consumer Staples: Processed & Packaged Goods

www.omegaprotein.com

Company Overview: Omega Protein is a vertically integrated producer of omega-3 fish oil and specialty fish meal products, and nutritional ingredient company. The company was founded in 1913 and is headquartered in Houston, Texas. Omega Protein operates in two business segments, Animal Nutrition and Human Nutrition. The Animal Nutrition segment products include fish meal, which is a nutritional animal feed additive, fish solubles, and crude fish oil. Fish solubles are processed into organic fertilizer to aid vegetation growth. Additionally, fish oil products are used in the production of food, animal feed, industrial applications, and dietary supplements. Omega Protein is currently expanding its operations within the Human Nutrition segment. Acquisitions include Cyvex, InCon, and Wisconsin Specialty Protein, which provide ingredients to the nutraceutical industry, concentrate Omega-3 fish oil compounds, and produce whey protein, respectively.

Recent Developments • 02/27/2013: Omega Protein acquires Wisconsin Specialty Protein, a whey protein producer for $27 million. • 12/31/2012: The Company recorded anticipated future legal fees associated with the U.S Attorney’s Office for the Eastern District of Virginia investigation, totaling $7.7 million. • 12/31/2012: The Atlantic States Marine Fisheries Commission voted to reduce the Total Allowable Catch in New Jersey, South Carolina, Texas, and Virginia.

Key Statistics Price (11/27/2012) $9.55 Market Cap. 19.8 M 52 Week Range $5.88-11.21 EPS (ttm) .20 Beta 2.02

Price Multiples Price/Earnings (ttm) 47.23 Price/Earnings (fwd) 9.95 PEG Ratio 1.21 Price/Book .92 Price/Sales .81

Key Ratios

OME Industry

EBIT Margin 5.36 % 7.69 % Net Profit Margin 1.72 % 6.9 3 % ROA 1.42 % 2.09 % ROI 1.6 % 2.86 % ROE 2.02 % 7.26 % Current Ratio 3.8 1.71 Debt/Equity 13.41 121.98

Recommendation – Hold Price Target: 10.99

• Capital expenditures for operations, excluding acquisitions are expected to be between $20 and $22 million in 2013.

• Fish oil yields for 2012 were 29% below the five year average, increasing per unit product costs.

• Received $44.8 million from litigation settlements in 2010 and 2011.

Stock: Omega Protein Corp. April 20, 2012 Spring 2013

______________________________________________________________________________ Analyst: Mark Albanese Page 2

Industry Overview: The Processed & Packaged Goods sub-industry represents a significant portion of the Consumer Goods sector. This sector consists of 351 firms of which 109 firms are categorized under the Processed & Packaged Goods sub-industry. This sub-industry focus is to process foods, and sell these finished goods to retail outlets for distribution. Depending on whether or not the firm has its own warehouse operation, it may or may not incur significant transportation costs. However, the Processed & Packaged sub-industry does benefit from its differentiated products, which unlike commoditized products result in higher gross margins. Growth in this industry is primarily driven by population growth, wealth, consumer preferences, demographics, and supply. Consumer Staples maintain stable demand year to year, because its products are essential for day to day living. As a result, population growth is directly related to demand for food products, which increases sales revenue for Processed & Packaged Goods firms. During the past few years Consumer Staples have experienced higher trading volume due to their defensive nature.

The chart above compares the performance of Omega Protein Corp. (OME) to its closest

competitor, Darling International Inc. (DAR), and the S&P 500 index over the past year.

Factors that Affect the Industry: There are two important drivers that affect the performance of the consumer staples sector. The

first driver that determines the performance of this industry is the state of the economy. In depressed economies interest rates decline and firms are able to finance capital expenditures with debt at a lower cost. Second, sentiment drivers, such as branding allow firms to offset inflationary price increases, raising cost of goods with higher pricing strategies, and maintain sales.

Stock: Omega Protein Corp. April 20, 2012 Spring 2013

______________________________________________________________________________ Analyst: Mark Albanese Page 3

Company Outlook: When evaluating Omega Protein’s previous years’ financial investors will conclude that management is committed to expanding its Human Nutrition segment. Over the past three years the Human Nutrition segment has acquired three new subsidiaries. Management believes that this product mix diversification will allow the company to offset declining fish oil yields. Also, these three acquisitions have experienced higher gross margins than the Animal Nutrition segment. Once these operations have been completely immersed into Omega Protein’s business model, its net profit will have a greater percentage attributable to the Human Nutrition segment than the Animal Nutrition segment. Appendix A: Discounted Cash Flow Results and Sensitivity

Inputs Initial Revenue Growth 0.10 Terminal Revenue Growth 0.04 CapEX % Rev 0.13 Depreciation & Amortization 0.08 Cost of Equity 0.14 P/E Multiple 9.95 P/S Multiple .81 Number of Shares Outstanding 19,827,780

Free Cash Flow 2013 2014 2015 2016 2017 Total Revenue 259,202,900 285,123,190 313,635,509 344,999,060 379,498,966

% Change Revenue 10.00% 10.00% 10.00% 10.00% 10.00%

Net Income 8,879,439 9,767,383 10,744,121 11,818,533 13,000,387

Capital Expenditures 32,400,363 29,937,935 32,931,728 36,224,901 39,847,391

CapEx % Rev 12.50% 10.50% 10.50% 10.50% 10.50%

FCFE 11,180,518 7,651,269 8,416,396 9,258,035 10,183,839

Final Terminal Value(P/S)

307,394,162

Cash Flow 11,180,518 7,651,269 8,416,396 9,258,035 10,183,839

PV Cash Flows 11,180,518 6,704,582 6,462,531 6,229,218 187,242,038

No. of Shares 19,827,780 Stock Price 10.99

P/SInitial Growth 10.99$ 0.11 0.21 0.41 0.61 0.81 1.01 1.21 1.41 1.61 1.81

5% 2.94 3.84 5.62 7.41 9.20 10.99 12.78 14.57 16.36 18.146% 2.97 3.91 5.78 7.66 9.53 11.41 13.28 15.16 17.03 18.917% 3.00 3.98 5.95 7.91 9.88 11.84 13.81 15.77 17.74 19.708% 3.03 4.06 6.11 8.17 10.23 12.29 14.35 16.41 18.47 20.539% 3.06 4.13 6.29 8.45 10.60 12.76 14.92 17.07 19.23 21.38

10% 3.09 4.21 6.47 8.73 10.99 13.24 15.50 17.76 20.01 22.2711% 3.12 4.30 6.66 9.02 11.38 13.74 16.11 18.47 20.83 23.1912% 3.15 4.38 6.85 9.32 11.79 14.26 16.73 19.20 21.67 24.1413% 3.18 4.47 7.05 9.64 12.22 14.80 17.38 19.96 22.55 25.1314% 3.21 4.56 7.26 9.96 12.66 15.36 18.06 20.75 23.45 26.1515% 3.25 4.66 7.48 10.30 13.11 15.93 18.75 21.57 24.39 27.2116% 3.28 4.76 7.70 10.64 13.59 16.53 19.47 22.42 25.36 28.3017% 3.32 4.86 7.93 11.00 14.07 17.15 20.22 23.29 26.36 29.4418% 3.36 4.96 8.16 11.37 14.58 17.78 20.99 24.19 27.40 30.6119% 3.39 5.07 8.41 11.75 15.10 18.44 21.79 25.13 28.47 31.8220% 3.43 5.17 8.66 12.15 15.64 19.12 22.61 26.10 29.58 33.07

Stock: Omega Protein Corp. April 20, 2012 Spring 2013

______________________________________________________________________________ Analyst: Mark Albanese Page 4

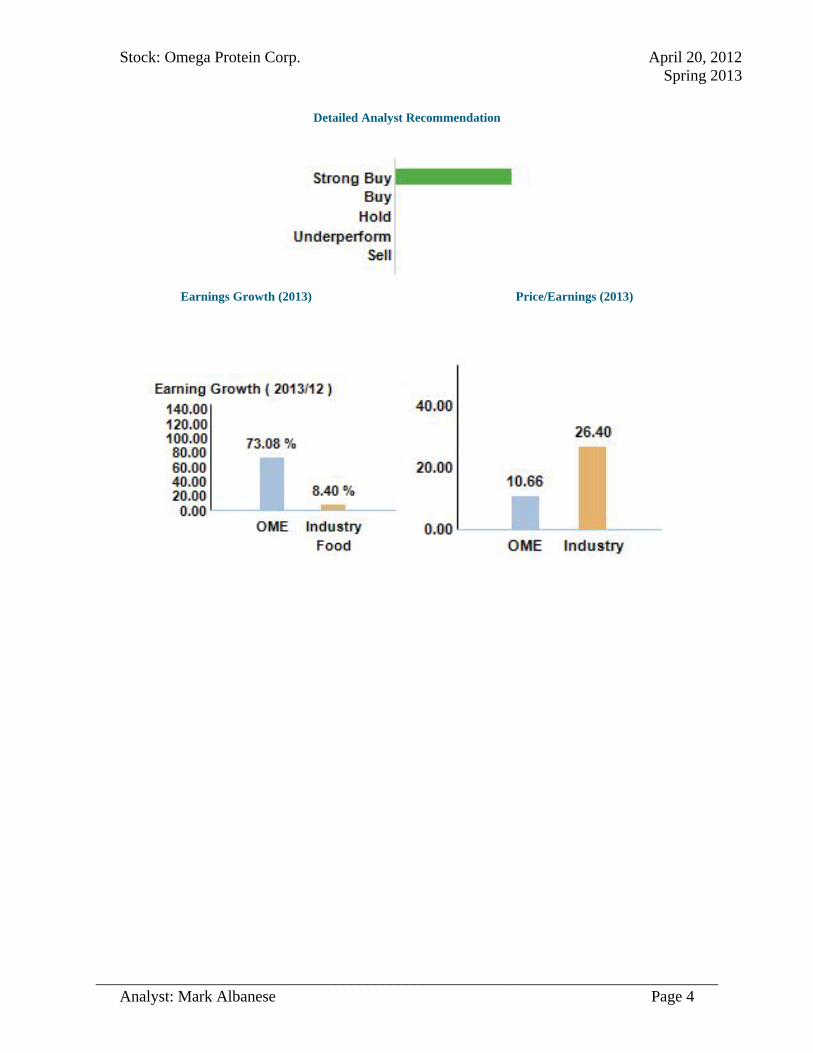

Detailed Analyst Recommendation

Earnings Growth (2013) Price/Earnings (2013)

Stock: Orient Paper, Inc. April 18th, 2013 Spring 2013

Analyst: Michael Robert Giancaspro

Orient Paper, Inc (NYSE:ONP)

Basic Materials: Paper Products

http://www.orientpaperinc.com/

Company Overview: Orient Paper Inc. is a leading paper manufacturer in North China. The Company initially manufactured packaging paper when it was founded in 1996. Since then the Company has expanded its product capacities to include higher quality paper products. In 2003, the Company began producing printing paper with diverse specifications and, beginning in early 2010, the Company began producing digital photo paper. Orient Paper has two locations within Xushui County, Baoding City, Hebei Province and serves over 100 packaging and printing companies and paper products distributors with three types of paper, including packaging paper, printing paper and digital photo paper. In January 2013, the company announced its business expansion plans into tissue paper operations.

Allegations of Fraud: In 2010, Muddy Waters, a short-selling firm run by Carson Block & Sean Reagan published a report, some but not all allegations follow

• Around $30 million has been misappropriated since Oct. 2009 • ONP overstated 2008 revenue by 27x. • ONP overstated 2009 revenue by 40x. • ONP overvalues its assets by at least 10x.

Since the allegations, ONP’s stock price has artificially fallen from as high as $15 in the beginning of 2010 to $1.70 in 2013. Two years later, the company is still a going concern and has taken measures to disprove the allegations through an independent investigation and outright denial of all Carson Block’s claims.

Recommendation – Strong Buy Price Target: $5.79-$6.64 -Recently cleared of all fraud allegations by Deloitte -Expected expansion into tissue paper business -Capacity increased with recent investments in new production lines, Sales growth expected as a result

Key Statistics

Price 4/18/2013 $1.70

Market Cap. $31.00 M

52 Week Range $1.64 - 3.53

EPS .79

Beta 2.97

Dividend Yield %2.90

Price Multiples

P/E 2.08

Earnings Yield 42.98

P/B .299

P/S .287

Key Ratios

ONP Industry

GPM %24.62 %20.82

NPM %14.36 %2.79

ROA 14.93 3.32

ROI 16.25 4.45

ROE 16.97 7.93

Current Ratio 1.964 2.165

EBITDAM %23.12 %13.51

Stock: Orient Paper, Inc. April 18th, 2013 Spring 2013

Analyst: Michael Robert Giancaspro

Orient Paper’s Response to Fraud allegations Orient Paper has taken pains to show the independence of its investigation and noted that the company had not previously hired the involved professionals, who included the law firms Loeb & Loeb and TransAsia Lawyers, as well as the accountants Deloitte & Touche Financial Advisory Services. The financial statements of ONP were validated and cleared of fraud later that year in 2010. Liu Zhenyong, the CEO of ONP, has reiterated this charge on several occasions: that the Muddy Waters researchers had demanded a large sum of money and equity in exchange for a positive report, and had then put out the June sell recommendation when Liu refused. Muddy Waters has denied Liu’s shakedown allegation. However this version of events coincides with an eyewitness account of Rick Pearson, a well-credentialed American analyst who specializes in small-cap Chinese stocks. He toured ONP’s facilities alongside Carson Block and Sean & Reagan. In an article he wrote on 07/01/10 on thestreet.com, he describes their conduct during the tour to be “amateurish”, as they did not ask many questions, and at one point Rick Pearson watched as one of the partners of Muddy Waters “jumped around in the recycled paper piles like a child” when he asked about the presence of his former classmates, the company stated: “The purpose of Carson Block & Sean Reagan’s trip was to pitch a “paid for” research report that would recommend the stock as a strong buy” Muddy Waters held significant short-selling interests, and would profit (and has profited) financially during ONP’s decline in value. Within their report they claimed no responsibility to its accuracy, and those that use it do so at their own risk. Recent Developments: 04/04/13 8:30 AM EDT Orient Paper Declares First Quarter 2013 Dividend of $0.0125 per Share - PR Newswire This is part of a recently instated reoccurring dividend. The company expects the reoccurring dividend to continue well into the future 04/03/13 Orient Paper: A Safe Play For Investors Once Again Seeking Alpha: Orient Paper Inc (ONP) is a name that may seem quite familiar to investors. The leading producer of paper products in northern China was the subject of negative press and fraud reports dating back to 2010… 03/22/13 8:30 AM EDT Orient Paper to Present at the John Tumazos Very Independent Research Metals and Mining Conference in New York - PR Newswire 11/29/10, 4:35 P.M. EDT Audit Committee Clears Orient Paper, http://blogs.barrons.com/stockstowatchtoday/2010/11/29/audit-committee-clears-orient-paper/ Industry Overview:

Stock: Orient Paper, Inc. April 18th, 2013 Spring 2013

Analyst: Michael Robert Giancaspro

Orient Paper, Inc is a Chinese firm that manufactures paper products. According to Research Insight, the Paper Products industry is made up of 24 companies. In the U.S. and other developed markets, the industry is expected to decline. However, overseas the market is just beginning in developing countries like China and India. Paper production and consumption is mostly seen in developed nations like the U.S.A, Japan, and Western Europe who alone make up 70% of worldwide paper production.

The chart above compares Orient Paper, Inc. to the Dow Jones, and rival companies Buckeye Technologies Inc (BKI), and China Paper Holdings (CPPHF). In 2010, there was a sharp decline due to the report of Muddy Waters, a short-selling firm who claimed the company was a fraud. Orient Paper responded to the allegations by outright denying them, and initiating an independent audit, which included the accounting firm Deloitte. The independent audit has since cleared ONP of all fraud allegations, but has yet to even remotely recover the stock price to pre-allegation levels. Company Outlook: Having recently expanded their production capacities and product lines in 2009-2012, Orient Paper expects growth in both sales and earnings. Early in 2013 ONP announced of its planned expansion into the Tissue Paper business. The company’s stock price has yet to recover to pre-fraud-allegation levels and is trading roughly 3x below its intrinsic value. It is one of the most profitable and well run companies in its industry, and is THE leading paper production firm in Northern China. Appendix A: Discounted Cash Flow Results

Stock: Orient Paper, Inc. April 18th, 2013 Spring 2013

Analyst: Michael Robert Giancaspro

Assumptions Expansion reduced Shares Outstanding 18460000 Initial Growth 5% Expected P/E 2 RROR 10% Debt Ratio 12.15% Depreciation to NI 50.42% Capital expenditures decreasing at an average rate (1+-42.84%) NWC / Sales 14.47%

Free Cash Flow

2012 2013ex 2014ex 2015ex 2016EX 2017EX net income 14,672,663 17,138,799 17,995,738 18,895,525 19,840,302 20,832,317 depreciation 8,382,859 8,640,852 9,072,894 9,526,539 10,002,866 10,503,009 net working capital 21,866,644 22,959,976 24,107,975 25,313,374 26,579,042 27,907,995 change in net working capital 10,542,928 1,093,332 1,147,999 1,205,399 1,265,669 1,328,952 Capital expenditures 11,915,693 7,727,564 4,417,149 2,524,885 1,443,248 824,974 Free Cash flow 3,325,218 24,686,318 22,179,550 25,144,943 27,463,336 29,443,063

NPV Shares Share Price

P/E $122,217,135 18460000 $ 6.64

Sensitivity Analysis Initial

Growth

Terminal P/E 6.64 0.03 0.04 0.05 0.06 0.07 0.08 0.09 0.1 1 5.66 5.80 5.94 6.09 6.24 6.39 6.55 6.71 2 6.29 6.46 6.64 6.82 7.01 7.20 7.40 7.60 3 6.93 7.13 7.34 7.56 7.78 8.01 8.24 8.48

4 7.56 7.80 8.04 8.29 8.55 8.81 9.08 9.37 5 8.20 8.47 8.74 9.03 9.32 9.62 9.93 10.25

6 8.84 9.14 9.44 9.76 10.09 10.43 10.77 11.13 7 9.47 9.80 10.14 10.49 10.86 11.23 11.62 12.02 8 10.11 10.47 10.84 11.23 11.63 12.04 12.46 12.90 9 10.75 11.14 11.55 11.96 12.40 12.85 13.31 13.79 10 11.38 11.81 12.25 12.70 13.17 13.65 14.15 14.67 11 12.02 12.48 12.95 13.43 13.94 14.46 15.00 15.56 12 12.66 13.14 13.65 14.17 14.71 15.27 15.84 16.44 13 13.29 13.81 14.35 14.90 15.48 16.07 16.69 17.32 14 13.93 14.48 15.05 15.64 16.25 16.88 17.53 18.21 Appendix B: Discounted Cash Flow Results Assumptions

Stock: Orient Paper, Inc. April 18th, 2013 Spring 2013

Analyst: Michael Robert Giancaspro

Expansion into Tissue Paper Shares Outstanding 18460000 Initial Growth 5% Expected P/E 2 RROR 10% Debt Ratio 12.15% Depreciation to NI 51.42% Capital to sales -4.98% NWC / Sales 14.47%

Free Cash Flow

2012 2013EX 2014EX 2015EX 2016EX 2017EX net income 14,672,663 17,138,799 17,995,738 18,895,525 19,840,302 20,832,317 depreciation 8,382,859 8,640,852 9,072,894 9,526,539 10,002,866 10,503,009 net working capital 21,866,644 22,959,976 24,107,975 25,313,374 26,579,042 27,907,995 change in net working capital 10,542,928 1,093,332 1,147,999 1,205,399 1,265,669 1,328,952 Capital expenditures 11,915,693 7,727,564 4,417,149 2,524,885 1,443,248 824,974 Free Cash flow 3,325,218 24,686,318 22,179,550 25,144943 27,463,336 29,443,063

NPV Shares Share Price

P/E

$$106,972,855 18460000 $ 5.79

Sensitivity Analysis 2

Initial Growth Terminal P/E 5.79 0.03 0.04 0.05 0.06 0.07 0.08 0.09 0.1 1 4.89 4.99 5.09 5.20 5.31 5.43 5.54 5.66 2 5.52 5.66 5.79 5.94 6.08 6.23 6.39 6.54 3 6.16 6.32 6.50 6.67 6.85 7.04 7.23 7.43 4 6.80 6.99 7.20 7.41 7.62 7.85 8.08 8.31 5 7.43 7.66 7.90 8.14 8.39 8.65 8.92 9.20 6 8.07 8.33 8.60 8.88 9.16 9.46 9.76 10.08 7 8.70 9.00 9.30 9.61 9.93 10.27 10.61 10.97 8 9.34 9.66 10.00 10.35 10.70 11.07 11.45 11.85 9 9.98 10.33 10.70 11.08 11.47 11.88 12.30 12.73 10 10.61 11.00 11.40 11.81 12.24 12.69 13.14 13.62 11 11.25 11.67 12.10 12.55 13.01 13.49 13.99 14.50 12 11.89 12.34 12.80 13.28 13.78 14.30 14.83 15.39 13 12.52 13.00 13.50 14.02 14.55 15.11 15.68 16.27 14 13.16 13.67 14.20 14.75 15.32 15.91 16.52 17.15

Stock: Rowan Companies Plc. (RDC) April 24th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Luis Rondon Page 1

Rowan Companies plc (NYSE: RDC)

Energy: Oil & Gas Drilling

www.Rowancompanies.com

Company Overview: Rowan Companies PLC was founded in 1923 by brothers Charlie and Arch Rowan as a contract drilling business. They started with a small land-based steam rig powered by two 45-horsepower boilers. Today Rowan Companies plc is a major provider of global offshore contract drilling service with leading high-specification Jack-up rigs. Currently operating a fleet of 31 Jack-up rigs worldwide, including the North Sea, Gulf of Mexico, Middle East, Trinidad and South East Asia. In 2013 the company will enter the ultra-deepwater market with high-specification drill ships expected to be delivered starting in late 2013.

Recent Developments:

• April 4, 2013: RDC announces first quarter earnings beating expectation.

• March 7, 2013: Announces Thomas P. Burke as President

• March 14, 2013: Release Fleet contracts status update

Key Statistics Price (04/19/2013) $31.24 Market Capitalization 3.88B 52 Week Range $28.62 - 39.40 EPS (ttm) 1.46 Beta 1.77

Price Multiples P/E (ttm) 21.44 P/E (fwd) 7.99 PEG .62 P/B .94 P/S 2.76

RDC Oil & Gas Drilling Industry

P/E 21.08 12.1 P/B .94 1.3 Net Profit Margin

14.60% 11.5%

ROE 4.59% 8.7% Div. Yield N/A 2.8%

Recommendation –Hold Price Target: $41.90

Recent growth in contract and earning Improving economic conditions Undervalued shown in discounted cash flow analysis. Improving equipment that are in high demand

Stock: Rowan Companies Plc. (RDC) April 24th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Luis Rondon Page 2

Industry Overview: Rowan Companies plc, falls under the Oil and Gas Drilling industry within the energy sector. Firms in the oil and gas drilling industry own and operate rigs responsible for the exploration and production of gas and oil. The main customers for the oil and gas drilling industry are public and privately owned oil and gas explorers and producers. Oil and gas drilling firms tend to have diverse rig fleets that can fall into one of two classification: land or offshore rigs. Rowan Companies Plc. is classified under the offshore rigs, having 31 Jack-up oil rigs. In recent years Rowan Companies Plc. sold off their land rig side of the business to focus on offshore rigs. Oil and Gas drilling firms’ main business is contract drilling. Firms in the oil and gas drilling industry typically follow one of two growth strategies: organic and through acquisition. Rowan Companies Plc. is currently trying to grow organically by investing on new equipment to be able to meet high demand of ultra-deepwater rigs.

One Year Performance

1 Year Performance Chart from Yahoo Finance

The chart above compares Rowan Companies Plc. (RDC) to the S&P 500 and rival company Transocean Ltd. (RIG). Over the past year RDC has had some month overperforming both the S&P500 and its rival RIG but over the past 6 months it has underperform.

Company Outlook: Rowan Companies Plc. is currently expanding their rig’s fleet. In 2013 they are entering the ultra-deepwater market with the delivery of the first of four high-specification drill ships. They have most of their rigs currently operating under contract for 2013 and 2014. They want to expand into the Southeast Asian market with high-specification oil rigs. This recent quarter EPS was $0.57 beating expectation of $0.44.

Key Executives Chief Executive Officer W. Matt

Ralls President & Chief Operating Officer

Thomas P. Burke

Executive Vice President, Chief Financial Officer & Treasurer

J. Kevin Bartol

Executive Vice President, Legal

John L. Buvens

Stock: Rowan Companies Plc. (RDC) April 24th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Luis Rondon Page 3

Assumptions

Growth 23% Debt

41.14%

NWC % 56.30%

P/E 21.3 Ke 11%

CapEx % 51.30%

Free Cash Flow Projections:

Free Cash Flow 2013 2014 2015 2016 2017 EBIT $251,319 $311,805 $385,805 $478,013 $592,258 ∆ NWC $187,385 $232,170 $287,659 $356,409 $441,591 + Depreciation $350,609 $434,405 $538,228 $666,864 $826,245 "- Capital Expenditures

$883,943 $1,095,205 $1,356,959 $1,681,273 $2,083,097

Free Cash Flow $-28,628 $-581,585 $-720,825 $-892,804 $-1,105,850

Sensitivity Analysis

Stock: Rowan Companies Plc. (RDC) April 24th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Luis Rondon Page 4

Consensus Recommendation

Analyst Firms Making Recommendations

B OF A M L BARCLAYS CAPITA CAP ONE SOUTHCO COWEN SECURITIE CREDIT AGRICOLE DEUTSCHE BK SEC FBR CAP MARKETS GABELLI & COMPA GLOBAL HUNTER S GOLDMAN SACHS J.P. MORGAN JEFFERIES & CO. JOHNSON RICE MACQUARIE CAPIT MORGAN STANLEY RAYMOND JAMES RBC CAPITAL SANFORD BERNSTE SIMMONS & CO. SOCIETE GENERAL STEPHENS INC UBS WELLS FARGO SEC WILLIAMS FINANC

Stock: United Therapeutics (UTHR) April 20th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Benjamin Kupa Page 1

United Therapeutics (NYSE:UTHR)

Healthcare: Biotechnology www.unither.com

Company Overview: Founded in 1996, United Therapeutics Corporation is a biotechnology firm that develops and manufactures drugs for patients that have life-threatening disorders. Currently, UTHR has 3 patented drugs that treat Pulmonary Arterial hypertension; high blood pressure in the arteries of the lungs.

Recent/Upcoming Developments:

April 25th, 2013 – UTHR will announce First Quarter 2013 financial results in a half-hour teleconference.

April 15th, 2013–UTHR gained approval for phase 1 study of Pulmonary Arterial Hypertension treatment using Pluristem Therapeutic’s PLX-PAD cells (Placental Expanded Cells

Key Statistics Price (4/20/2013) $60.26 Market Cap. $3.02B 52 Week Range $41.42-63.11 EPS (ttm) 5.71 Beta 1.4

Price Multiples P/E (ttm) 10.55 P/E (fwd) 8.58 PEG .29 P/B 2.76 P/S 3.28

Key Ratios

UTHR Industry P/E 10.55 86.3 P/B 2.76 16.2 Net Profit Margin 34.15% 10.1%

ROE 14.73% 8.8% Debt/Equity 25.37 103.6

Recommendation –Hold Price Target: $70.66

Growth in revenues and income 3 products in “Phase III” in the pharmaceutical pipeline (2 as

treatment for PAH, 1 for Neuroblastoma)

Stock: United Therapeutics (UTHR) April 20th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Benjamin Kupa Page 2

Industry Overview:

United Therapeutics is a biotechnology firm, a relatively large offshoot of the Healthcare sector. According to data available through Research Insight, the biotechnology industry includes 306 firms, including United Therapeutics. The biotechnology industry has an average market capitalization of $23B, and an average price to book of 16.2. Most recently, the industry has been characterized by the premier biotech firm, Amgen. Much of the success of biotech firms relies upon FDA review panels and introductions of new products for clinical testing.

The Chart above, obtained from Yahoo! Finance displays the one year performance of United Therapeutics Corporation, as well as UTHR’s main competitor Gilead Sciences Inc., and the top performing biotechnology firm, Amgen. While United Therapeutics has been outperformed by Gilead and Amgen recently, it is also a much smaller firm, with a 3.02B market cap, compared to GILD & AMGN’s 80.95B & 83.36B respectively. United Therapeutics Corp. has consistently outperformed the S&P 500 over the past year. In late October, UTHR took a hit when they received an unfavorable response letter from the FDA regarding their oral new drug application, Remodulin. In late March, UTHR received a second unfavorable response from the FDA. Company Outlook:

United Therapeutics has seen recent growth in revenues and profits, from its three patented PAH products. The company has recently begun collaborations with Pluristem Therapeutic, in order to create new products using Pluristem’s PLX-PAD cells. United Therapeutics is focused on creating and acquiring new patents in order to grow, and currently has 9 products at different stages of the pharmaceutical pipeline.

Stock: United Therapeutics (UTHR) April 20th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Benjamin Kupa Page 3

Appendix A: Discounted Cash Flow Results

Sensitivity Analysis

P/E

Growth

Stock: United Therapeutics (UTHR) April 20th, 2013 Spring 2013

______________________________________________________________________________ Analyst: Benjamin Kupa Page 4

Appendix B: Analyst Coverage Via NASDAQ

Mark Albanese 3 Maze Road, Montvale, NJ 07645 | (201) 414-2358| [email protected]

EDUCATION University of Rhode Island Kingston, RI Bachelor of Science in Business Administration: Accounting Expected May 2013

Cumulative GPA: 3.74

Honors: o Honors Program with the College of Business at URI o Frederick & Karen Buchsbaum Scholarship o G & M McKowen Scholarship

o Beta Gamma Sigma o Golden Key National Honor Society

o Dean’s List – Every Semester

PROFESSIONAL EXPERIENCE

International Business Machines Corporation Armonk, NY IBM Global Finance Consolidation Accounting Intern June – August 2012

Valued assets which were either sold or remaining in inventory, aiding the performance of eliminations.

Reconciled general ledger reports for capital lease accounts, such as equipment, depreciation, and indirect costs.

Branded returning lease equipment to various inventory accounts within the Global Asset Recovery System to assist with the process of estimating reserve value.

Analyzed quarterly receivables collected against billings for investment portfolios.

Reclassified cash flow from operations to investments.

Utilized the general ledger to efficiently locate tables containing loan payment structures of individual clients.

Collaborated with leading business professionals to better understand IBM’s leasing practice.

Abercrombie & Fitch Paramus, NJ Sales Associate June – August 2011

Worked part time during the summer assisting with preparation and maintenance of the sales floor.

Upheld a high standard of customer service while assisting customers with purchase decisions.

Became extremely efficient in using database software such as PeopleSoft to operate the cash register.

Reconciled ending cash amount to check for discrepancies.

Was recognized by management staff for my dedication, positive attitude, and quick learning curve.

LEADERSHIP AND EXTRACURRICULARS

Beta Gamma Sigma Student Leadership Forum St. Louis, MO University of Rhode Island Representative November 1 – November 4, 2012

Explored challenging issues, such as ethical decision making and career planning to foster personal growth.

Networked with peers having similar future career goals, and gained new perspectives of successful leadership.

Tau Epsilon Phi Fraternity Kingston, RI Treasurer September 2011 – December 2012

Managed collections of payments from within the fraternity, but also secured funding for events, which included the active brotherhood and elder members.

Organized an online banking account for the organization to manage the budget more efficiently.

Assisted the fraternity in raising funds for philanthropy events to donate to local charities, such as the Rhode Island American Cancer Society.

Habitat for Humanity Birmingham, AL Volunteer March 20 – March 27, 2011

Volunteered with a team of students completing urban renewal field projects during Spring Break.

INTERESTS AND SKILLS Software: Lotus Notes, SQL, Excel, Word, PowerPoint Interests: Swimming, Snowboarding, Reading, Baseball, Hiking, Cooking

5 James Street, Westerly, RI 02891 [email protected]

401.742.3576

Michael R. Giancaspro Education University of Rhode Island, Kingston, RI • Bachelor of Science in Business Administration, December, 2013. • GPA: 3.67/4.00. • Major: Accounting.

Related Coursework Upper Level Business Courses Intermediate Accounting 1&2, Financial Management, Organizational Behavior, Supply Chain Management, Business Law. Notable Accomplishments • Deans list • First Degree Black belt; Shorin-ryu Shorinkan Karate

Work Experience Seafood Haven Westerly RI 05/05-Present Senior Cook: • Investigated theft and notified owner of findings of theft exceeding 1000 dollars • Retrieved change from bank, restaurant deposit box and closed out cash register

• Resolved customer disputes and complaints in a fair and effective manner

• Managed opening and closing shifts which consisted of:

o Stocking all areas of the restaurant

o Inspection and preparation of food – raw and 'ready to eat food'

o Managed 4-5 high school teenagers

o Trained new employees regardless of their position

o Coordinating all kitchen and front end activities

o Performed any necessary job function not being fulfilled on a given day

Janco Company / Burger King Westerly, RI 02/13-Present

Team member:

• Prepared Food according to State/Store health and sanitation policies

• Cleaned the restaurant according to State/Store standards and regulations

• Trained new employees in food preparation and sanitation procedures according to State/Store regulations

Stephen Gross School: 2 Gardenia Lane • Narragansett, RI • 02882

Home: 1646 Rogers Court • Wall, NJ • 07719 [email protected] • [email protected] • 732-272-7311

OBJECTIVE To obtain a position in the accounting field in which I can apply my strong analytical and communication skills.

EDUCATION University of Rhode Island, Kingston, RI

• Masters of Science in Accountancy expected in December 2013 University of Rhode Island, Kingston, RI

• Bachelor of Science in Business Administration, Summa Cum Laude, December 2012 • Major: Accounting GPA: 3.89 • Academic Honors: Centennial Scholarship, Dean’s List (7), Beta Gamma Sigma, Beta Alpha Psi

RELATED EXPERIENCE Aetna Inc., Dental & Vision Finance Summer Associate, Hartford, CT Summer 2012

• Identified and corrected the various weaknesses in the competitive intelligence process • Outlined and streamlined the processes used in creating the financials for the Strategic Plan • Created and implemented multiple Microsoft Access databases to identify and resolve monthly

membership variances • Participated in, and contributed to, a cross functional group capstone project