The Pulse: 8th Edition Kingdom of Saudi Arabia Healthcare ...

20

Kingdom of Saudi Arabia Healthcare Overview 2018 The Pulse: 8 th Edition

Transcript of The Pulse: 8th Edition Kingdom of Saudi Arabia Healthcare ...

Kingdom of Saudi Arabia Healthcare Overview 2018

The Pulse: 8th Edition

We are seeking to introduce recognised Long-term Care and Rehabilitation providers to reputable investors in Cairo, Muscat, Abu Dhabi, Riyadh and Jeddah.

> Management Agreement> Joint Venture > Long-term Lease of Land

and/or Property

LONG TERM CARE & REHABILITATION CENTERS

We have a number of opportunities for healthcare service providers. Market entry is possible by way of management agreement, Joint Venture and Long-term Lease of Land and/or Property.

> Muscat

> Riyadh

> Jeddah

> Cairo

> Dubai

> Abu Dhabi

> Sharjah

> Ajman

> Fujairah

GENERAL HOSPITALS We are seeking investors to partner with a recognized healthcare operator to establish Clinics in:

> Riyadh > Jeddah> Abu Dhabi > Muscat> Cairo

Possible modes of market entry include:

> Management Agreement> Joint Venture > Long-term Lease of Land and/or Property

CLINICS

The opportunities are available in:

> Riyadh> Cairo> Dubai> Abu Dhabi> Sharjah

> Ajman> Fujairah> Muscat> Jeddah

The Specialties are:

> Ophthalmology> Pediatric > Maternity> IVF> Orthopedic> Beauty & Cosmetics> Wellness

An established and recognized healthcare provider is seeking to setup centers of excellence through management agreement, joint venture or long term lease.

CENTERS OF EXCELLENCE

Providers and Investors Seeking to Expand

in the Middle East and North Africa

Opportunities for Healthcare

Service The opportunities are available in:

The Kingdom of Saudi Arabia with a current estimated population of approximately 32.6 million is the largest country in the GCC. Under Vision 2030, the country is going through fundamental structural changes in all the sectors including the healthcare sector.

The Healthcare sector in KSA is undergoing evolution on the back of rapid advancements in technology, research and development (R&D) in line with the global and regional trends. However, healthcare providers and professionals are grappling with several challenges concurrently, such as patients becoming customers and the patientcare transitioning from “fee for quality” rather than “fee for service”. This coupled with new compliance requirements that aim at wellness and prevention plus ensuring better coordination, efficiencies, add depth and complexity to an increasingly competitive marketplace.

Mansoor AhmedDirector | MENA

Development Solutions | Healthcare | Education & PPP

Imad DamrahManaging Director

Kingdom of Saudi Arabia [email protected]

Ian AlbertRegional Director | MENA

Valuation & Advisory [email protected]

3Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

Recent trends and industry dynamics require operators in the healthcare sector to make challenging decisions. Whilst the healthcare system has improved across the region including Saudi Arabia the sector offers opportunities for investors/operators. Key factors that make KSA’s healthcare market attractive are:

> KSA’s Healthcare Sector is structured to provide a basic platform of healthcare services to all, with specialised treatment facilities offered at some private and public hospitals.

> KSA has an estimated population of 32.6 million in 2018, which is expected to double, reaching 77.2 million by 2050, growing at 2.65% per annum. Assuming a more conservative 1.02% average annual growth, as suggested by World bank, KSA population would still reach 45.1 million by 2050. This increase in population is expected to fuel the demand for healthcare services in the kingdom. Concurrently, the healthcare system needs to treat emerging Lifestyle Diseases and Illnesses associated with modern and urban lifestyle, partially due to the growing middle-income population.

> The government is encouraging private sector participation in the healthcare sector as the public sector’s role is gradually transitioned to becoming more of a regulator rather than as a provider of healthcare facilities, as highlighted in the National Transformation Plan (NTP) and the privatisation plan. In 2017, Saudi Arabian General Investment Authority (SAGIA) announced that foreign investors can have 100% ownership in health and education sectors, once implemented this is expected to boost private sector investment in healthcare in KSA.

> Government commitment to healthcare is evident as the government continues its efforts in developing various medical cities, however, many of these facilities are expected to be operated in conjunction with the private sector investment using various Public Private Partnership (PPP) models.

> The healthcare and social services sector has been allocated 15% (SAR 147 million) of the total KSA’s 2018 budgeted expenditures, up from actual spend of SAR 133 million during 2017. This 10.5% increase in the allocation reflects a strong indication of potential demand as well as the Government’s willingness to augment growth and improvement within the sector.

Colliers International KSA Healthcare Overview 2018 (the 8th in The Pulse series) provides an in-depth analysis of the key factors impacting the Saudi Healthcare sector and its future outlook and identify opportunities and challenges to operators and investors.

4 Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

COMMITMENT PASSION INTELLIGENCEKNOWLEDGEEXPERIENCE

USP

Colliers International Healthcare Advisory & Valuation Services team is solely focused on healthcare related business (OpCo) and real estate (PropCo), from complex medical business related operational advisory to real estate related advisory.

Our group has the experience and knowledge essential to providing forward thinking solutions to any challenging healthcare related decisions where success is measured in high quality care delivered in a cost effective way.

Hospitals

Daycare / Surgery Centers

Medical Clinics

Health / Medical Parks

Laboratories

Market Research | Market Entry & Expansion | Equity & Debt Fund RaisingHighest & Best Use Study | Market & Financial Feasibility Study

Operator Search and Selection | Land, Property & Business Valuations

Long Term Care / Rehab Centers

5Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

KSA is divided into 13 provinces, of which Makkah and Riyadh are the most populated provinces in which approximately 16.3 million or 51.4% of the total population reside. These two provinces have the highest concentration of expatriates (non-Saudi Nationals) with 46.7% and 42.8% respectively.

Demographic analysis

Hail 2.%

Najran 1.8%

Al Jouf 1.6%

Al Bahah 1.5%

Northern Borders 1.1%

Makkah26.2%

Riyadh25.2%

Eastern 15.1%

Aseer 6.8%Madinah 6.6%

Jazan 4.8%

Al Qassem 4.8%Tabouk 2.8%

Others 8.1%

Population Density of KSA (P/km2)

15.1

32.6 M

Population of KSA(2018 estimated)

RiyadhMadinah

Al-Qassim

Ha’ilTabuk

Al-JawfNorthern Borders

Eastern Province

Najran

Jizan

Al-Bahah

Makkah

Asir

1-45-2425-240

Population Density by Governorate

Persons/Sq km

KSA’s population by province, 2016

Population growth, 2010 - 2050

Male

Saudi

57%Female

Non Saudi

43%

63%37%

6 Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

HISTORICAL

PROJECTED

2010 2011 2012 2013 2014 2015 2016 2017 2018 2020 2030 2040 2050

80

60

40

20

0

Popu

latio

n M

CAGR 1.03%CAGR 2.65%

Pessimistic Optimistic

Curr

ent

Between 2010 and 2016, population grew at 2.65% CAGR. Assuming the same level of growth until 2050, the Kingdom’s population is expected to reach 77.2 million. However, based on a conservative estimate of 1.02% as suggested by World Bank, KSA’s population is expected to reach 45.1 million by 2050.

Expanding population coupled with rising income levels are expected to fuel demand for healthcare as well as infrastructure, energy, water, telecoms, technology, housing, education, financial services etc.

The population pyramid in KSA has significantly changed between 1980 and 2015, and it will further change by 2050 this will have a significant impact on healthcare demand in terms of quality, quantity and type of healthcare facilities.

During 2015-2050 approximately 19 million babies will be born in KSA, creating demand for facilities and services, relating to mother and childcare (obstetrics, gynecology, pediatrics, etc.) along with the more common prevailing communicable and some non-communicable diseases.

The age group between 20-39 years is very important for future healthcare planning, as it is common that there is the development of chronic diseases; cardiovascular, irritable bowel syndrome, chronic obstructive pulmonary disease and some types of cancer. These have a long term impact on demand for healthcare. With 12 million population in this age group there is considerable demand not only for curative but also preventative facilities.

Over the next three decades, we envisage a sharp rise in healthcare demand as approximately 80.0% of an individual healthcare requirements typically occur post the 40-50 age range. This is primarily due to an increase in lifestyle related diseases, such as diabetes, coronary and other obesity-related illnesses.

An increase in life expectancy in KSA is expected to extend from the current level of 73.1 years and 76.1 years for males and females respectively to 78.4 and 81.3 by 2050. This is expected to create demand on long- term care (LTC) facilities, focusing on geriatric related care, rehabilitation and home healthcare services.

Based on current international benchmarks of 4-6 beds per 1,000 population above 65 years, KSA currently needs from 6,400 to 9,600 beds dedicated for LTC, this is expected to reach 41,200 – 61,800 LTC beds by 2050.

0-20

20-39

40-59

60+

7Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

Changing Population Profile

80+

75-79

70-74

65-69

60-64

55-59

50-54

45-49

40-44

35-39

30-34

25-29

20-24

15-19

10-14

05-09

00-04

2.5M 2M 1M 0 1M 2M 2.5M 2.5M 2M 1M 0 1M 2M 2.5M

2015 31.5 M 2050 45.1 M1400K 700K 0 700K 1400K

1980 9.7 M

0.09M0.9%

0.4M3.8%

1.2M12.8%

2.9M29.5%

5.2M53.0%

0.3M1.0%

1.3M4.2%

7.5M23.8%

11.9M37.6%

0.5M33.4%

2.9M6.4%

7.4M16.5%

12.0M26.6%

12.7M28.1%

10.1M22.4%

1980 2015 2050

5.2 M

10.5 M 10.1

M

1980 2015 2050

2.9 M

11.9 M

12.7 M

1980 2015 2050

1.2 M

7.5 M

12.0 M

1980 2015 2050

0.49 M1.6 M

10.3 M

In many regional and international markets among the keys to successful second homes and resort developments, especially targeting the affluent customers, is yearlong destination conceptual planning. To achieve this developers have to go beyond spa packages to include health driven wellness offerings; beauty and cosmetic, weight loss and packages relating to lifestyle disease. These increase absorption, occupancy levels within the development and enhance price premiums

HEALTH & WELLNESS

Destination-based fitness camps are gaining popularity especially within the younger generation Y and Z (age range of 20 to 40 years). Destination healthcare retreats comprise two primary components ; retreats that promote lifestyle changes and academies focused on enhancing group skill techniques. The fitness industry is upgrading with fitness slimming getaway programs in holiday locations. With obesity levels increasing across the region, the KSA holiday home market can benefit by applying these new trends which will enhance the absorption / occupancy of new developments and price premiums.

FITNESS/SKILL RETREATS

With approximately 1.6 million of Saudi population above the age of 60 in 2015, which is expected to increase to more than 10 million by 2050, Colliers expects an increasing demand for retirement homes. There is an established pattern across international markets for developing retirement communities that provide the look and feel of vacation homes. There is a potential for the Saudi developers to look at capitalizing on such concepts within their developments.

RETIREMENT COMMUNITIES

With a decline of the nursing home model of care and the growth in more assisted living options, long-term rehabilitation centers have become common across international markets. Developers can integrate new real estate products, targeting retirees as well as those looking for long-term care and immediately accessible amenities.

REHABILITATION CENTRES

Creating Healthcare & Wellness HUBThe NEOM City which will cost $500 billion and was announced in October 2017 will be located on the Red Sea Coast promising a new lifestyle that does not currently exist in Saudi Arabia. The new city is planned to span over a total area of 10,000 square miles (25,900 square kilometers) linking KSA to Egypt and Jordan, creating new markets for many sectors, including healthcare and biotech.

The biotech sector will focus on next-generation gene therapy, genomics, stem cell research, nanobiology, bioengineering plus attracting the talent to research, develop and apply the new knowledge, NEOM will be a new nexus for this vital activity.

The Demand for Second HomesIn last few decades alongside the demand for primary accommodation, a second-tier demand for second homes within the residential market has emerged, especially in the Eastern Province. With the development of NEOM city, Colliers expects that the second homes market flourish in the red sea area not only as secondary homes but also as an investment product supported and driven by leisure, healthcare and wellness

Sustaining high occupancy levels all year round in second home destinations can be challenging. Colliers has witnessed and advised on these challenges in a number of countries. Often they can be addressed through introducing healthcare and wellness driven resorts, long-term care and rehabilitation facilities. These facilities can have a positive impact on occupancy levels by attracting not only vacationers but also retired households and those seeking longer holidays within proximity to healthcare facilities.

While seasonality is part of the story, it can also be due to the lack of destination pull factors. Complex destination components, alongside leisure and environment including proximity of hospitals, clinics, long-term rehabilitation centers, wellness retreats, fitness/ skill retreats and retirement homes.

There is an opportunity within the holiday home market for developers to create destinations by providing essential community infrastructure.

Long beaches, valleys and deserts cradled by mountains all located in north-western Saudi Arabia with breathtakingly diverse terrain, this unique geographical location enjoys a temperate climate. Cool winds from the Red Sea create the most desirable temperatures for future residents – on average around 10°C cooler than surrounding areas and the rest of the GCC.

8 Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

9Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

30

25

20

15

10

5

0

30

25

20

15

10

5

0

> Alzheimer’s disease > atherosclerosis > asthma > some kinds of cancer > chronic liver disease or cirrhosis, Chronic Obstructive Pulmonary Disease,

> type 2 diabetes > heart disease > metabolic syndrome

> chronic renal failure

> osteoporosis > stroke

Common diseases of longevity

Lifestyle diseases

USA UK

Japa

n

Switz

erla

nd

Chin

a

Swed

en

Germ

any

Turk

ey

Leba

non

Jord

an

UAE

Bahr

ain

Qata

r

KSA

Kuw

ait

Oman

Egyp

t

Analyzing the demographic trends, it is estimated that KSA’s population will change from Baby Boomers to Generation X, Y & Z. This shift would impact disease patterns and in turn the type of healthcare services required.

Lifestyle diseases (also sometimes called diseases of longevity or diseases of civilization) are diseases that appear to increase in frequency as countries become more industrialized and life expectancy increases due to urbanization and rising disposable income. A more sedentary, consumption of processed food often leads to increased chronic diseases (diabetes, coronary problems and obesity-related illnesses).

Diabetes: The rate of diabetes related illnesses has witnessed an unprecedented increase across the MENA Region. Based on latest figures available for 2014, there were over 422 million people diagnosed with diabetes in the world and MENA’s contribution was 38.7 million diabetic patients in 2017, which is expected to increase to over 70 million by 2024. In KSA during 2017, the diabetes prevalence rate was 17.75% for age group 20-79 years, totaling to over 3.8 million cases.

Obesity: In 2016, KSA’s obesity prevalence rate among adults was 35.4%,also one of the highest in the MENA region.

Hypertension: The prevalence of hypertension among adults in 2015 in KSA stood at 23.3% alsoone of highest in the GCC region.

Hypertension prevalence (% of population above 18) in 2015

Obesity prevalence (% of population above 18) in 2016

19.5

37.936.235.535.435.132.1

32.032.031.729.827.8

27.0

22.320.3

6.24.3

Japa

n

Chin

a

Switz

erla

nd

Swed

en

Germ

any

Oman UK

Bahr

ain

UAE

Egyp

t

Leba

non

Turk

ey

Qata

r

KSA

Jord

an

USA

Kuw

ait

Diabetes prevalence (% of population ages 20 to 79) in 2017

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

20

18

16

14

12

10

8

6

4

2

0

KSA

Egyp

t

UAE

Qata

r

Bahr

ain

Kuw

ait

Leba

non

Oman

Turk

ey

Jord

an

USA

Chin

a

Germ

any

Japa

n

Switz

erla

nd

Swed

en UK

Source: World bank WHO,, Colliers International Research 2018

10,000

8,000

6,000

4,000

2,000

0

USD

As a

% o

f KSA

Per

Cap

ita E

xp.900%

800%

700%

600%

500%

400%

300%

200%

100%

0

Switz

erla

nd

USA

Norw

ay

Luxe

mbo

urg

Swed

en

Denm

ark

Aust

ralia

Irela

nd

Neth

erla

nds

Germ

any

Aust

ria

Cana

da

Icel

and

UK

Ando

rra

Qata

r

UAE

Saud

i Ara

bia

Bahr

ain

Kuw

ait

Leba

non

Oman

Turk

ey

Jord

an

Egyp

t

Healthcare expenditure per capita – 2015

10 Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

USD Per Capita

As a % of KSA Per Capita Exp

Introduction of Mandatory Health Insurance for Expatriates working in Private Sector

Introduction of Mandatory Health Insurance for Saudi working in the Private Sector

Introduction of Mandatory Health Insurance for Dependents of Expatriates

Introduction of Mandatory Health Insurance for all Visitors

Introduction of Unified Health Insurance Policy for all Saudi employees and their Dependents working in the Private Sector

Health Insurance Key Milestones

SAR 15.3 billion

claim paid to healthcare

providers in 2017 SAR 18.9 billion total health

insurance premiums subscribed

in 2017 Utilization rate per Issued Member 77%

13.4% of Saudi Insured

68.0% of

Expatriates Insured

Claim rejection

ratio appox. 25%

2006 20132010 2014

2016

Average Premium Per

Person SAR 1,759

Health Insurance Loss Ratio

88%

Health Insurance Indicators 1,027,833 Total Primary Saudis

1,719,634 Total Dependent Saudis

6,185,809 Total Primary Non Saudis

2,009,456 Total Dependent Non Saudis

10,942,732 Total Beneficiaries

27 Total Insurance Companies

10 Tital TPA Companies

5,026 Total Health Care Providers

Healthcare expenditure per capitaCurrently, the healthcare market in KSA is driven by public expenditure at 74.2% (2016) and 25.8% by private sector, which is expected to increase to 28.1% by 2025.

The graph below shows the top 15 countries in the world per capita healthcare spending 3 times to 8 times more than KSA.

Beds

Hospitals

274 58.3%

152 32.3%

44 9.4%

41,853 59.1%

17,428 16.3%

11,581 16.3%

MOH Sector Quasi Govt Sector Private Sector

11Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

14.0

12.0

10.0

8.0

6.0

4.0

2.0

0.0

Germany France UK Canada USA Japan KSA Kuwait Oman UAE Qatar Bahrain

4.1

13.3

8.1

3.3

9.9

6.1

2.8

7.9

2.6

2.7

9.9

2.6

2.6

11.3

2.8

2.4

11.0

13.2

2.8

5.7

2.2 2.6

6.3

1.9 2.2

4.8

1.6 1.93.

81.3

1.96.

11.3 1.5

4.3

2.0

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

12 817 22.1%

17 428 24.6%

10 939 18.8%

11 581 16.3%

34 370 59.1%

41 835 59.1%

CAGR 3.3%

CAGR 1.0%

CAGR 5.3%

MOH (Beds) Quasi Govt (Beds) Private (Beds)

Physicians

Nurses

Beds

Ministry of Health (MoH)

Ministry of Health (MoH) is the regulator for all healthcare related activities and services within the country. MoH has played a dominant role in providing healthcare services in KSA. In 2016, MoH contributed 58.3% of the total hospitals and 59.1% of the total beds supply. The primary aim of these facilities is to provide care for free to Saudi nationals. However, in areas where private hospitals are not available or under certain emergency circumstances or in case of specialized treatments that are not available in local private hospitals, expats can access MoH facilities.

The Quasi-Government healthcare facilities are hospitals and health centers operated by the MoH and predominantly catering to employees of the government organizations. Some of the Quasi-Government Facilities include: National Guard, Ministry of Defence and Aviation, Ministry of Interior, Royal Commission, ARAMCO, etc.

Private sector facilities are accessed by expatriates as they do not have access to public facilities and at times Saudi nationals also visit private facilities to avoid the waiting time at public facilities and benefit from the higher quality of care. Private sector operated approximately 32.2% of hospitals carrying 24.6% of the overall bed supply.

Quasi-Government

Private Sector

Hospitals & Bed Capacity by sectorsThe healthcare sector in KSA is represented by 3 healthcare players:

Growth in Beds

2010 2016

Key healthcare indicators per 1,000 population - 2015

Between 2010 and 2016 the number of doctors per 1,000 population increased from 2.4 in 2010 to 2.8. The ratio of nurses improved from 4.8 to 5.7 and number of beds per 1,000 population increased from 2.1 to 2.2. However, even then it remains low compared to other developed countries and even world average of 2.7 beds. Yet, it is far too simplistic to look only at bed ratios when looking at the Saudi healthcare market. Population demographics, disease profiles, medical procedural advances, insurance costs, government / private sector involvement and affordability levels all have significant impacts on bed and hospital demand numbers.

Note: data for Japan and Canada for 2014

Composition of hospitals and beds by sector, 2016

12 Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

Outpatient encounters in KSA, 2010-2016*As the key healthcare provider in KSA, MoH hospitals are the main providers of treatments to outpatients with approximately 64.3 million of the outpatient encounters in 2016. However, during 2010 – 2016, the volume of outpatient encounters in MoH decreased from 51.1% to 46.6%, while private sector encounters increased from 31.1% to 36.7%, with private sector experiencing a CAGR of 4.6%, with total volume of outpatients increasing from 40.5 to 50.7 million, compared to a decline of 2.0 million outpatients in the MoH facilities. This trend can be explained by the increasing number of insured expatriates and the increasing popularity of the private sector among Saudi nationals.

Top 7 regions in terms of the highest number of outpatients included Riyadh (23.5%), Eastern (13.2%), Madinah (7.4%), Jeddah (7.0%), Jazan (6.9%), Makkah (6.8%) and Al-Ahsa (6.0%).

Outpatient Encounters by Specialty in MOH hospitals in 2015**

Number of outpatients in KSA (millions), 2010 - 2016

Key Causes of Death in KSANon-communicable diseases accounted for 68% of all deaths in the KSA which is significant improvement. The overall decline in communicable diseases can be explained by the improvement in sanitation systems, nutrition, hygiene awareness and invention of more effective medicine.

As a result of urbanization, rise in life expectancy and disposable income, an increase of chronic/lifestyle diseases, such as diabetes, coronary problems and other obesity-related illnesses, is increasing in KSA.

45.6%

45.6%5%

9.2%

11%

4.5%

18%

11.4%

5.9%

10%

9%

3%2%

2%2%

6%

6%

5.9%

6.6%

Ophtalmology Obs/Gyn Musculo-Skeletal ENT Oral and Dental Skin and Subcutaneous Tissue

Digestive System Others

Cardiovascular disease Injuries DIabetes, urogenital, blood and endocrine diseases

Cancer Common infectious diseases

Neonatal disorders Chronic respiratory Disease

Neurological disorders Digestive diseases Mental and behavioral disorders

140

120

100

80

60

40

20

0

4031.1%

51

23 17.1%

23

66 51.1%

64

CAGR 0.0%

CAGR -0.5%

CAGR 4.6%

Ministry Of Health Quasi Govt Private Sector

2010 2016

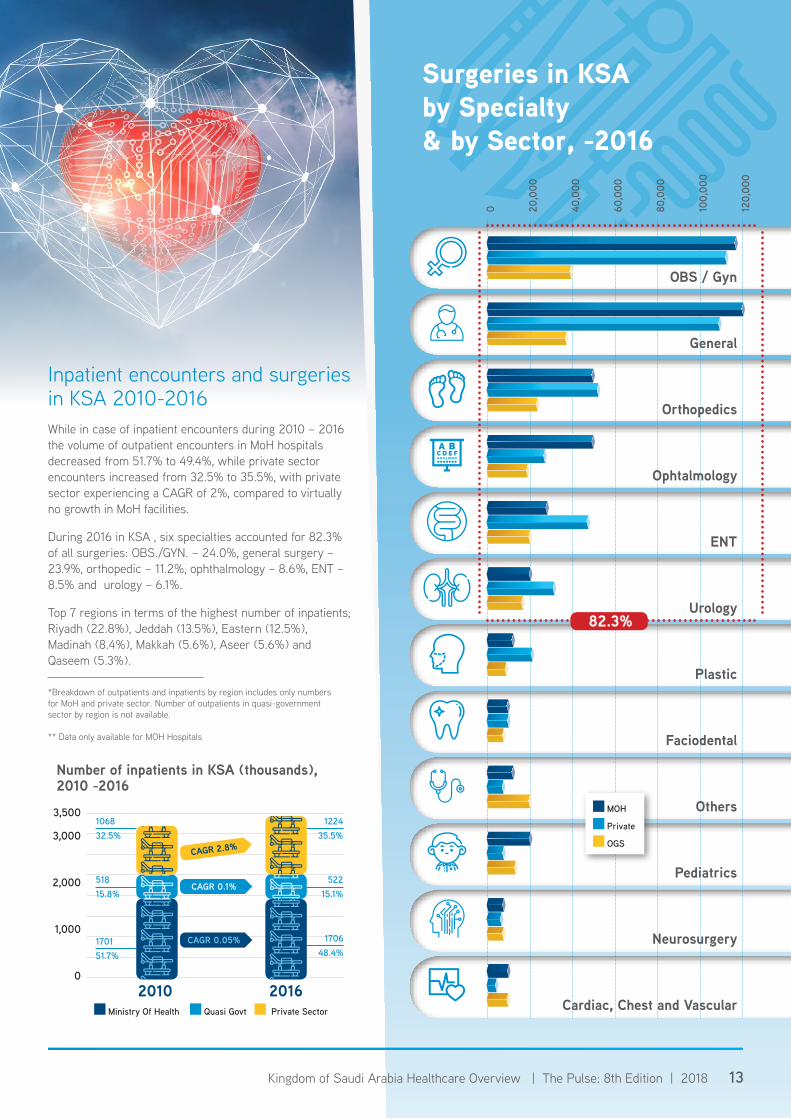

Surgeries in KSA by Specialty & by Sector, -2016

13Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

0 20,0

00

40,0

00

60,0

00

80,0

00

100,

000

120,

000

Inpatient encounters and surgeries in KSA 2010-2016While in case of inpatient encounters during 2010 – 2016 the volume of outpatient encounters in MoH hospitals decreased from 51.7% to 49.4%, while private sector encounters increased from 32.5% to 35.5%, with private sector experiencing a CAGR of 2%, compared to virtually no growth in MoH facilities.

During 2016 in KSA , six specialties accounted for 82.3% of all surgeries: OBS./GYN. – 24.0%, general surgery – 23.9%, orthopedic – 11.2%, ophthalmology – 8.6%, ENT – 8.5% and urology – 6.1%.

Top 7 regions in terms of the highest number of inpatients; Riyadh (22.8%), Jeddah (13.5%), Eastern (12.5%), Madinah (8.4%), Makkah (5.6%), Aseer (5.6%) and Qaseem (5.3%).

Number of inpatients in KSA (thousands), 2010 -2016

OBS / Gyn

General

Orthopedics

Ophtalmology

ENT

Urology

Plastic

Faciodental

Others

Pediatrics

Neurosurgery

Cardiac, Chest and Vascular

*Breakdown of outpatients and inpatients by region includes only numbers for MoH and private sector. Number of outpatients in quasi-government sector by region is not available.

** Data only available for MOH Hospitals

82.3%

MOH

Private

OGS

3,500

3,000

2,000

1,000

0

106832.5%

1224 35.5%

518 15.8%

522 15.1%

170151.7%

1706 48.4%

CAGR 0.1%

CAGR 0.05%

CAGR 2.8%

Ministry Of Health Quasi Govt Private Sector

2010 2016

14 Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

Article 13: Rights of The Private PartyNon-interference by the

Governmental Entity with the business of the Private Party, except as stipulated in the PPP contract and the Kingdom’s laws.> Protection of the property of the Private

Party from nationalization or any other measures.

> The right to freedom of ownership, use and disposal of the investments made in the PPP project in accordance with the PPP contract.

> The freedom of disposition of profits and proceeds received.

> The right to freely dispose of the financial returns from the PPP project, including repatriation.

> The right to recover losses incurred as a result of any change in the Law or unlawful action or the failure of public authorities to take appropriate actions.

Article 28: Duration of the PPP Contract:

The duration of the PPP Contract shall be determined as agreed between the Supervisory Committee and the Private Party provided that the original, renewed or extended, duration of the Contract shall not exceed (30) thirty years from the date of signing the PPP Contract.

Article 49: The Law of Real Estate Ownership and Investment by Non-Saudis

Non-Saudis may own real estate in whole or in part, except for properties located within the boundaries of the cities of Makkah and Medina.Real estate may be leased to the Private Party within the boundaries of the cities of Makkah and Madinah for a period equal to the term of any PPP Contract for the purpose of implementing the PPP Contract for real estate which is the subject of the PPP Contract.

The Saudi Public Private Partnership LawReleased in July 2018 for public debate and comments, it is expected to boost private investment in the Kingdom with the concurrent impact on the Saudi economy.

The Private Public Partnership (PPP) draft bill is the beginnings of the legal framework on which the Saudi government can begin to outsource healthcare provision. The outsourcing is expected to be done through typical PPP projects for a fixed duration and / or selected disposal of government assets. The Saudi government stated aim is to raise US$200 billion by 2030 through privatization.

The features relating to healthcare and education sectors are summarized below:

Article 12: Government Financial Support for PPP Projects

The Government will have established procedures and is expected to provide financial and economic support to PPP project to ensure their success. There are 19 such initiatives highlighted in the document. Some of key initiatives are summarised below;

> Loans at preferential conditions> Bank guarantees.> Contribution to the share of the

PPP Project.> Guarantees on revenues.> Provide support to commercially

not viable but economically desirable projects

> Tariff subsidies.> Provision of the financial resources

for implementation of PPP Project> Tax benefits and/or tax

postponements and/or payment of tax by instalments

> Preferential customs duties > Foreign exchange and interest rate

fluctuation guarantees.> Providing rights, (including the right

to use or occupy), to movable or immovable property

> Assisting in obtaining licenses, permits, approvals;

Article 56: Ownership of Healthcare Companies

The law indicate that non-Saudi nationals will be able to wholly own health institutions, i.e. operating companies (OpCo), that are part of a PPP contract. This seems to be contradiction to the statement issued by governor of the Saudi Arabian General Investment Authority (SAGIA) in August 2017 by the KSA ’s investment authority governor, indicating 100% ownership for foreign investors in the healthcare and education sectors.

Colliers view is that this will boost the foreign investment in the healthcare and education sector, especially from many leading listed and not listed regional operators who are looking to expand into KSA’s lucrative healthcare sector. Additionally we expect that in the final law full ownership will not be limited to PPP projects.

> Providing easements in respect of publicly owned movable or immovable property;

> Right to collect tariffs or user fees and to generate revenues from other types of activities directly or indirectly associated with the implementation of the PPP Project;

> Setting discounted rental payments for use of publicly owned property;

> Granting exclusive rights to engage in the activity in the framework of the concluded PPP Contract.

> On behalf of Governmental Entity providing guarantees relating to• Quality of performance• Delay in their obligations• Termination of the Contract

Article 50: The Labor Law

Subject to approval from the Ministry of Labor and Social Development the PPP projects may enjoy exemption from the Labor Law and the Nitaqat Guide in relation to employment in any PPP with respect to employment of Saudis in the PPP projects.

15Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

Demand Gap BedsIn 2016, KSA had 2.23 beds per 1,000 population, which was quite low compared to world average of 2.7 beds per 1,000 population. Number of doctors per 1,000 population ratios of 2.83 is quite impressive, however, the Kingdom has high dependence on foreign physicians.

Colliers has projected the demand for total number of beds based on the following scenarios:

> Scenario 1 (Beds) – applying KSA’s ratio of beds of 2.23 per 1,000 population,

> Scenario 2 (Beds) - applying world’s ratio of 2.7 beds per 1,000 population.

Each scenario was calculated based on pessimistic and optimistic projections of population growth between 2016 – 2050, namely at a CAGR of 1.02% according to World bank and a CAGR of 2.65% based on historical growth of the country’s population between 2010 – 2016.

The current cost of construction for a Grade A hospital is in the range of US$ 1,900 / sqm to US$ 2,700 / sqm, while the gross area per bed ranges from 90 sqm to 125 sqm with investment in medical fit-outs ranging between US$ 80,000 to US$ 120,000 per bed.

It is far too simplistic too take into consideration only population projections when looking at the Saudi healthcare market, other factors previously mentioned need to be considered. The Saudi government policy seems to be emerging as a regulator and

facilitator encouraging the provide sector to bridge the gap in the healthcare sector in the KSA. In 2017, Saudi Arabian General Investment Authority (SAGIA) announced that foreign investors can have 100% ownership in health and education sectors, once implemented this is expected to boost private sector investment in healthcare in the KSA.

Demand Gap ClinicsFor projections of clinics required till 2050 we also used two scenarios along with the same approach for population projections:

> Scenario 1 (Clinics) – 75% of total doctors working in public or private sector or having their own business run clinics on full time or part time basis.

> Scenario 2 (Clinics) - 50% of total doctors working in public or private sector or having their own business run clinics on full time or part time basis.

Currently a large portion of demand in the clinics market is in residential buildings, offices buildings and retail shops. Colliers has observed a move away from the this historic preference to the development of dedicated healthcare clinics / daycare surgery centers and centers of excellence as one of the main growth opportunity in KSA.

The following exhibits represent the number of additional beds and potential investment in real estate and healthcare business (medical fit-outs, medical equipment etc.), which are required to cater to the demand of the growing population during upcoming years:

Conclusions

16 Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

2020F 2030F 2050F

Investment Required in Real Estate

Billion USD

2020F 2030F 2050F

Investment Required in Medical Fit-outs

Billion USD

2020F 2030F 2050F+

=

TOTAL

Billion USD

2020F 2030F 2050F

Additional Beds

Required

DEMAND FORECAST – Beds & Required Investment in Real Estate & Medical Fit-outs

Pessimistic population growth projections (World Bank – 1.02%)

Optimistic population growth projections (Historic growth – 2.65%)

2020F

2020F

2020F

2020F

2030F

2030F

2030F

2030F

2050F

2050F

2050F

2050F

150

100

50

0

150

100

50

0

4540

30

20

10

0

4540

30

20

10

0

16

15

10

5

0

16

15

10

5

0

60

50

40

30

20

10

0

60

50

40

30

20

10

0

2,90026,000

7.0–12.8

23.6 – 37.3

18,400

77,000

10,850

51,00028,000

110,000

29,300

102,00050,300

178,000

beds /1,000 population beds /1,000 population

2.23 2.7

0.7–1.3 5.7 – 9.04.6–8.4

16.5 – 26.1

2.7–5.0

11.0 – 17.47.3–13.4

22.0 – 34.812.6–23.0

38.2 –60.5

0.5–1.03.6 – 6.33.1–6.2

10.3 – 18.4

1.9–3.7

6.9 – 12.34.8–9.4

14.8 – 26.4

5.0–9.9

13.8 – 24.58.6–17.0

24.0 – 42.7

0.2–0.42.1 – 2.61.5–2.2

6.1 – 7.7

0.9–1.3

4.1 – 5.12.2–3.4

8.8 – 11.0

2.3–3.5

8.2 – 10.2

4.0–6.0

14.2 –17.8

17Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

Clinic Space Required

‘000 sqm

Investment Required

USD Million

2020F 2020F

2020F 2020F

2020F 2020F

2030F 2030F

2030F 2030F

2030F 2030F

2050F 2050F

2050F 2050F

2050F 2050F

5000

4000

3000

2000

1000

0

5000

4000

3000

2000

1000

0

120

100

80

60

40

20

0

200018001600140012001000800600400200

0

200018001600140012001000800600400200

0

DEMAND FORECAST – Clinics & Required

Investment in Real Estate

Additional Doctors Required

50%IF IF75%of DoctorsHaving Own Clinics

of Doctors Having Own Clinics

39.1–55.9103.7–148.2

144.1–205.9

415.8–594.0389.2–555.9

1,347–1,924.8

259.4–370.6

898.2–1283.2

26.1–37.369.1–98.8

96.1–137.3

277.2–396.0

74–93 198–247112–140 296–371

274–343

792–990412–515

1,188–1,485

741-926

2,566–3,208

1,112–1,390

3,850–4,812

Pessimistic population growth projections (World Bank – 1.02%)

Optimistic population growth projections (Historic growth – 2.65%)

9,9003,700

39,600

13,700

128,000

37,000

18 Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

Demand for Private HealthcareYear on year the volume and share of private sector has been increasing. In case of outpatients, between 2010-16 the private sector share increased from 31% (40 million) to 37% (51 million) a CAGR of 4.6%. For inpatient services the share increased from 32% (1.1 million) to 35% (1.3 million) at a CAGR of 2%. This compares to negative growth in MoH facilities, due primarily to the increasing number of insured expatriates and increasing popularity of the private sector among Saudi nationals.

The public sector’s role is also gradually transitioned to becoming more of a regulator rather than as a provider of healthcare facilities.

Daycare Surgical CentresDue to advancements in healthcare technology (for example laparoscopy) a number of daycare surgeries (treatments / procedures) have significantly increased, resulting in higher demand for daycare surgery centers.

The demand for daycare surgical centres has also increased regionally and in the KSA, due increase in prevalence of number of lifestyle diseases; diabetes, obesity, depression, strokes, cardiovascular diseases, blood pressure, etc., which does not require treatments in traditional hospital set-ups..

Dedicated purpose built daycare surgery centers and Centers of Excellence can be part of a large office complex and retail centers ; requiring from 3,000 sqm to 5,000 sqm space.

Increased demand for Healthcare QualityKSA’s healthcare facilities in general and Riyadh and Jeddah in particular, are observed to be accredited by international healthcare accreditation bodies such as Joint Commission International (JCI) and Australian Council of Healthcare Standards International (ACHSI).

These accreditations are one of the key factors patients consider while choosing a healthcare facility, as these assure high quality of health standards.

Demand for Maternity and PediatricsNumber of private health facilities, especially in Riyadh and Jeddah are focusing on maternity and pediatrics owing to high demand for these specialties.

Hospitals such as Dallah Hospital, Specialist Medical center and Dr. Sulaiman Al Habib have separate buildings dedicated for mother and child services.

As per Colliers research, throughout the KSA and especially Riyadh and Jeddah there is a high demand for Maternity and Pediatric services supporting a business case for developing stand-alone hospitals or as part of a hospital complex.

Laboratory and Diagnostic CenterStandalone laboratory and diagnostic centers are required in KSA to support the increasing volume of outpatient facilities.

Long Term Care/ RehabilitationWith the changing age profile, KSA requires a large number of LTC facilities. The government is seeking private sector facilities specialized in LTC to refer their patients requiring rehabilitation and/ or long term care.

Increased demand for specialized servicesCenters of excellence focusing on certain specialties such as ophthalmology, cosmetic surgery, IVF and orthopedics (sports medicine) are expected to grow further, especially in Riyadh and Jeddah.

Many General Hospitals also have established dedicated wings to provide highly specialized services in a single specialty this has often been a key factor to the success of these facilities.

Primary CareOwing to the large population in the KSA and high occupancy rates of the hospitals, the country requires more primary care clinics and medical centers to meet the demand of the rising population.

Opportunities

19Kingdom of Saudi Arabia Healthcare Overview | The Pulse: 8th Edition | 2018

The Funding Options > One of the key challenges faced whileestablishing quality hospitals in KSA is thehigh funding requirement.

> Despite the fact that banks and other financialinstitutions actively seek investments withinKSA’s healthcare sector, they often limittheir exposure by only servicing knownmarket paticpents with proven trackrecords. International or regional operatorscontemplating entry into KSA’s market oftenstruggle to secure project finance unlessthere is a recourse to alternative cash flows.

> Further difficulties arise with the termsoffered. Healthcare investments are typicallylong term investments contradicting a bank’srisk appetite which typically extends to atenure that ranges between 5 – 7 years.

> For the first time, entrants to the KSA’smarket, who don’t have enough financialresources or are unable to make significantfinancial commitments due to a variety ofreasons, ultimately end up searching forprivate investors to enter into a licensingand operating agreement, from which theywill extract a management fee. Alternativeoptions include; operators forming andowning the operating company (OpCo)with the investor investing in the land andproperty (PropCo), creating a Joint Venture(JV) with an investor. The various optionsavailable to Operators based on availability offunds are:

• Outright Purchase of the Land;

• Long-term Lease of the Land;

• Land as Equity Investment by the Landlord;

• Long-term Lease of the Land andShell-n-Core Structure fromLandlord/ Investor;

• Creating a JV with the Landlord/ Investorin Equity Partnership;

or

• Signing a Management Agreement withthe Landlord/ Developer/ Investor.

However, each of these options have financial, operational and legal advantages and disadvantages and Operators should seek professional advice before entering into any such arrangement.

The Kingdom is moving towards encouraging more private sector participation in the healthcare sector, however; the extent of investment required is significant.

In Colliers opinion, one way of bridging the required investment is by way of creating more REIT funds. Based on Colliers estimate, REIT funds in the Kingdom can unlock around US$ 7.5 billion to US$ 8.5 billion property value from the private sector, thereby playing a key role in augmenting growth in the healthcare sector.

Colliers is currently working with several market participants through traditional and emerging funding options to assist them in their expansion plans.

For further information, please contact:

Ian AlbertRegional Director | MENAValuation & [email protected]

Mansoor AhmedDirector | MENADevelopment Solutions, Healthcare, Education & [email protected]

Imad DamrahManaging Director Kingdom of Saudi [email protected]

Colliers International | MENA Region

Dubai | United Arab Emirates+971 4 453 7400

Operating from 69 countries on 6 continents

$2.7 billionannual revenue

2 billionsquare feet under management

15,400professionals and staff

Colliers International MENA

Colliers International is a global leader in commercial real estate services, with over 15,400 professionals operating from 69 countries. A subsidiary of First Service Corporation, Colliers International delivers a full range of services to real estate users, owners and investors worldwide, including global corporate solutions, brokerage, property and asset management, hotel investment sales and consulting, valuation, consulting and appraisal services, mortgage banking and insightful research. The latest annual survey by the Lipsey Company ranked Colliers International as the second-most recognized commercial real estate firm in the world.

colliers.com/UAE

Copyright © 2018 Colliers International.

The information contained herein has been obtained from sources deemed reliable. While every reasonable effort has been made to ensure its accuracy, we cannot guarantee it. No responsibility is assumed for any inaccuracies. Readers are encouraged to consult their professional advisors prior to acting on any of the material contained in this report.