The Philippines: The New Tiger of Asia - PANA · The Philippines: The New Tiger of Asia ... CARAGA...

20

The Philippines: The New Tiger of Asia Dr. Bernardo M. Villegas Ph.D. (Harvard) University Professor, University of Asia and the Pacific Manila, Philippines

Transcript of The Philippines: The New Tiger of Asia - PANA · The Philippines: The New Tiger of Asia ... CARAGA...

The Philippines: The New Tiger of Asia

Dr. Bernardo M. Villegas

Ph.D. (Harvard)

University Professor, University of Asia and the Pacific

Manila, Philippines

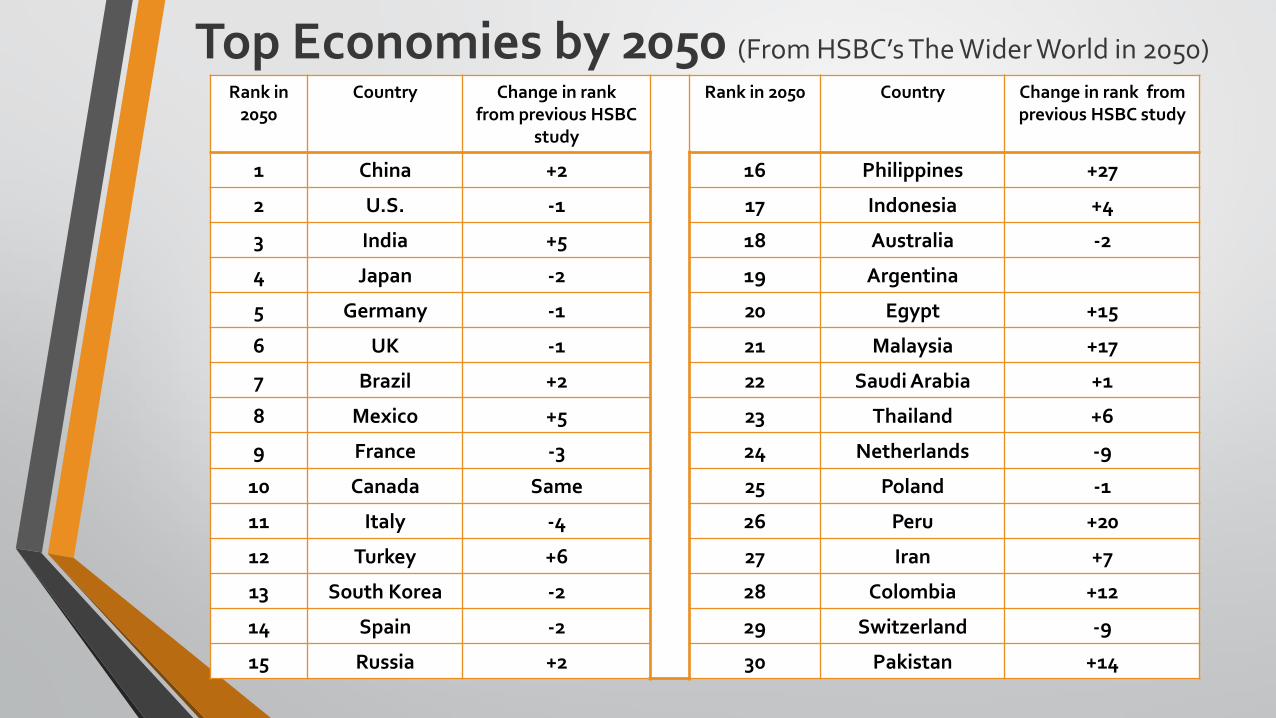

The Philippine Economy: Reaching the Tipping Point

•Growth Rates of 7-10% possible in the next 10 years

• Result of over 25 years of slow and painful reforms

•Will be the 16th largest economy in 2050

(The Wider World in 2050 Report, HSBC)

Top Economies by 2050 (From HSBC’s The Wider World in 2050)

Rank in 2050

Country Change in rank from previous HSBC

study

Rank in 2050 Country Change in rank from previous HSBC study

1 China +2 16 Philippines +27

2 U.S. -1 17 Indonesia +4

3 India +5 18 Australia -2

4 Japan -2 19 Argentina

5 Germany -1 20 Egypt +15

6 UK -1 21 Malaysia +17

7 Brazil +2 22 Saudi Arabia +1

8 Mexico +5 23 Thailand +6

9 France -3 24 Netherlands -9

10 Canada Same 25 Poland -1

11 Italy -4 26 Peru +20

12 Turkey +6 27 Iran +7

13 South Korea -2 28 Colombia +12

14 Spain -2 29 Switzerland -9

15 Russia +2 30 Pakistan +14

The Global Competitiveness Index 2014-2015 rankings

Source: http://www.weforum.org/reports/global-competitiveness-report-2014-2015

GCI 2014-2015 GCI 2013-2014

Country/Economy Rank (out of 144) Score Rank (out of 148) Switzerland 1 5.70 1

Singapore 2 5.65 2

United States 3 5.54 5

Germany 5 5.49 4

Japan 6 5.47 9

Hong Kong SAR 7 5.46 7

Taiwan, China 14 5.25 12

Malaysia 20 5.16 24

Korea, Rep. 26 4.96 25

China 28 4.89 29

Thailand 31 4.66 37

Indonesia 34 4.57 38

Philippines 52 4.40 59

South Africa 56 4.35 53

Brazil 57 4.34 56

Vietnam 68 4.23 70

India 71 4.21 60

Lao PDR 93 3.91 81

Cambodia 95 3.89 88

Myanmar 134 3.24 139

5.9

5.9

5.5

5.1

4.7

4.1

3.6

3.1

2.7

2.4

2

1.7

1.1

0.8

0.6

0.4

0.2

0.1

0.1

0.3

0.4

0.7

1

1.5

1.9

2.3

2.7

3.1

3.6

4.2

4.8

5.3

5.8

6.2

6.2

8 7 6 5 4 3 2 1 1 2 3 4 5 6 7 8

Philippines 102 million

Source: United Nations, Department of Economic and Social Affairs, Population Division (2011). World Population Prospects: The 2010 Revision.

Percent of total population

25-29

50-54

40-44

30-34

15-19

4-9

55-59

45-49

35-39

20-24

10-14

0-5

60-64 65-69

Working age population:

50.5% (51M)

Male

Female

Young dependents: 46%

(47M)

Aged dependents: 3.5%

Main Source of Competitive Advantage: Young and Growing Population

Philippine IT-BPM industry size

2006–2012; US$ billion x% YoY Growth

1Philippines IT-BPM market as percentage of global offshore services market, in revenue terms *Cited from the Presentation of Mr. Bong Borja, EGS President and Country Head Sources: BPAP, ACPI, CCAP, GDAP, HIMOAP, PSIA

# FTEs

(~‘000) 236 383 424 527

Global

share1 5% 6% 6% 7% 8%

3.44.5

6.17.1

8.9

11.0

13.2

2006 2007 2008 2009 2010 2011 2012

34% 17%

25%

24%

Copyright ©2012: BPAP. All rights reserved.

FTEs Revenue

(US$M)

Rev % inc.

fr ’11

Voice BPO 497,000 8,697 18%

Non-voice

BPO/KPO

154,380 2,470 20%

ITO 57,078 1,160 17%

Health Info Mgt &

Care

45,000 460 66%

Engineering

Services

10,836 206 20%

Animation 9,000 132 3%

Game

Development

3,500 50 251%

TOTAL FTEs 776,794 13,174 19%

19%

284 640

9.5%

777

Philippines 2012 Performance*

31% 45%

9.9%

2016 Projections

US$ 25 Billion IT-BPM Revenue

1.3 Million Direct Employment

Overseas Filipino Workers, 2011

Sources: Commission on Filipinos Overseas

Americas and Trust Territories

4,326,059 41%

Middle East 2,987,923

29%

East and South Asia 1,449,373

14%

Europe 808,779

8%

Oceania 451,042

4%

Africa 63,508

1% Sea-based workers

369,104 3%

Total = 10,455,788

Positive Trends

• Stable democracy

• Improving governance

• Strong macroeconomic fundamentals

• Labor peace

• Educated, young, and English-speaking labor force

• Strategic geographic location: launching pad for AEC

• Renaissance of manufacturing

• High rate of savings due to OFW remittances

• Low rate of dependence on petroleum

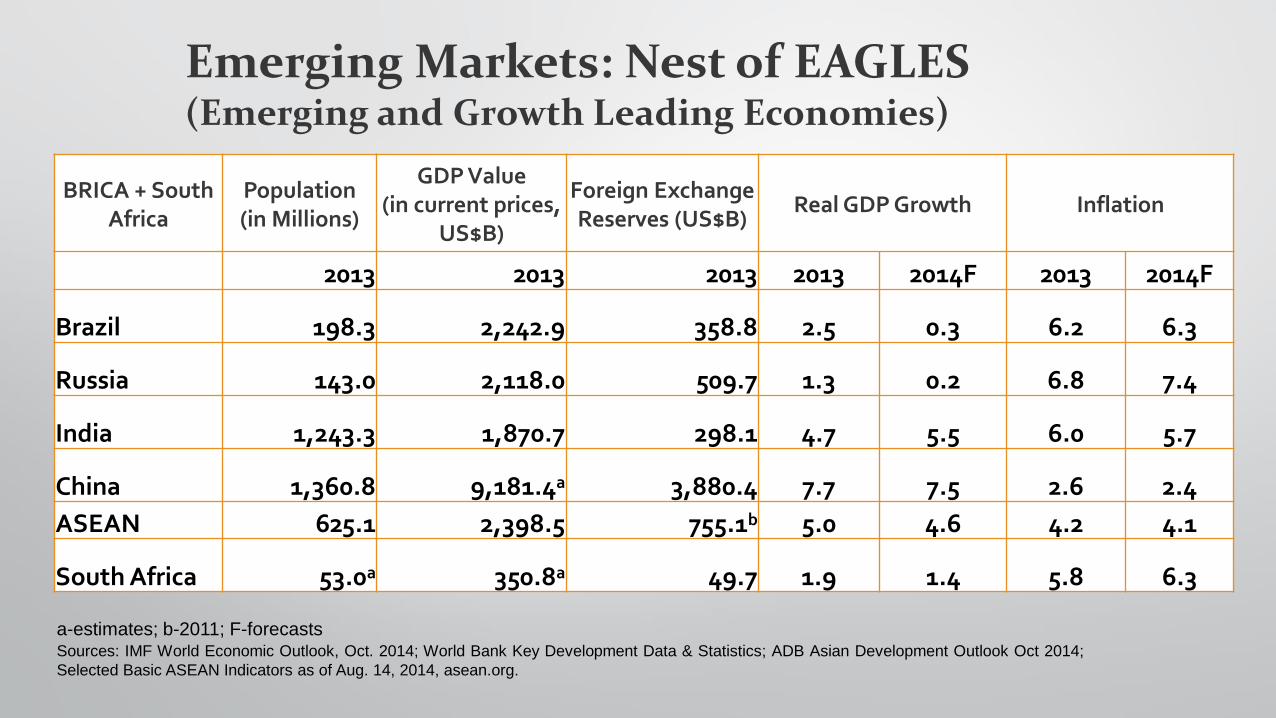

• One of the emerging markets

BRICA + South Africa

Population (in Millions)

GDP Value (in current prices,

US$B)

Foreign Exchange Reserves (US$B)

Real GDP Growth Inflation

2013 2013 2013 2013 2014F 2013 2014F

Brazil 198.3 2,242.9 358.8 2.5 0.3 6.2 6.3

Russia 143.0 2,118.0 509.7 1.3 0.2 6.8 7.4

India 1,243.3 1,870.7 298.1 4.7 5.5 6.0 5.7

China 1,360.8 9,181.4a 3,880.4 7.7 7.5 2.6 2.4

ASEAN 625.1 2,398.5 755.1b 5.0 4.6 4.2 4.1

South Africa 53.0a 350.8a 49.7 1.9 1.4 5.8 6.3

Emerging Markets: Nest of EAGLES (Emerging and Growth Leading Economies)

a-estimates; b-2011; F-forecasts Sources: IMF World Economic Outlook, Oct. 2014; World Bank Key Development Data & Statistics; ADB Asian Development Outlook Oct 2014;

Selected Basic ASEAN Indicators as of Aug. 14, 2014, asean.org.

The Next 11: Emerging Engines of Growth

Source: IMF, World Economic Outlook, Database April 2014

Country Population 2013 GDP 2013

(in millions) (current US$ B)

Bangladesh 156.3 141.28

Egypt 84.2 271.43

Indonesia 248.0 870.27

Iran 77.1 366.26

Mexico 118.4 1,258.54

Nigeria 169.3 286.47

Pakistan 182.6 238.74

Philippines 97.5 272.02

South Korea 50.2 1,221.80

Turkey 76.5 827.21

Vietnam 89.7 170.57

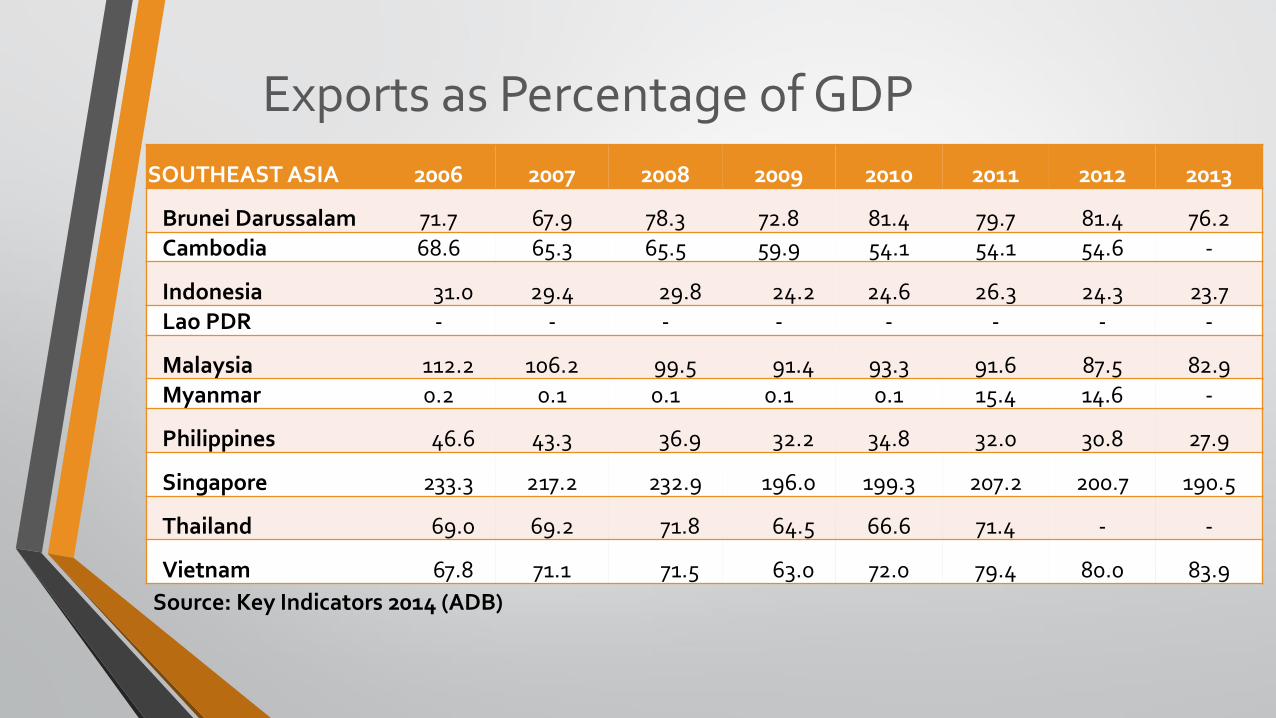

Exports as Percentage of GDP

Source: Key Indicators 2014 (ADB)

SOUTHEAST ASIA 2006 2007 2008 2009 2010 2011 2012 2013

Brunei Darussalam 71.7 67.9 78.3 72.8 81.4 79.7 81.4 76.2 Cambodia 68.6 65.3 65.5 59.9 54.1 54.1 54.6 -

Indonesia 31.0 29.4 29.8 24.2 24.6 26.3 24.3 23.7 Lao PDR - - - - - - - -

Malaysia 112.2 106.2 99.5 91.4 93.3 91.6 87.5 82.9 Myanmar 0.2 0.1 0.1 0.1 0.1 15.4 14.6 -

Philippines 46.6 43.3 36.9 32.2 34.8 32.0 30.8 27.9

Singapore 233.3 217.2 232.9 196.0 199.3 207.2 200.7 190.5

Thailand 69.0 69.2 71.8 64.5 66.6 71.4 - -

Vietnam 67.8 71.1 71.5 63.0 72.0 79.4 80.0 83.9

REGION 2010 CAGR 2014e

PHILIPPINES 92,337,852 2.11% 100,387,941

METRO MANILA 11,855,975 1.99% 12,889,589

CORDILLERA 1,616,867 1.90% 1,757,827

ILOCOS 4,748,372 1.37% 5,162,339

CAGAYAN VALLEY 3,229,163 1.54% 3,510,684

CENTRAL LUZON 10,137,737 2.38% 11,021,553

CALABARZON (SOUTHERN TAGALOG) 12,609,803 3.42% 13,709,136

MIMAROPA (SOUTHERN TAGALOG) 2,744,671 1.99% 2,983,954

BICOL 5,420,411 1.63% 5,892,967

WESTERN VISAYAS 7,102,438 1.50% 7,721,634

CENTRAL VISAYAS 6,800,180 1.97% 7,393,025

EASTERN VISAYAS 4,101,322 1.43% 4,458,879

ZAMBOANGA PENINSULA 3,407,353 2.08% 3,704,409

NORTHERN MINDANAO 4,297,323 2.29% 4,671,967

DAVAO REGION 4,468,563 2.19% 4,858,136

SOCCSKSARGEN 4,109,571 2.74% 4,467,847

CARAGA 2,429,224 1.66% 2,641,006

MUSLIM MINDANAO 3,256,140 1.68% 3,540,013

Population: Some regions outpace the average national population growth due to immigration

Source: National Statistics Coordination Board

PER CAPITA GROSS REGIONAL DOMESTIC PRODUCT (at current prices)

Source: National Statistics Coordination Board

Purchasing power: It is because income growths in these recipient regions are faster than the rest

Region / Year 2011 2012 2013

Philippines 102,383 109,494 117,603

NCR METRO MANILA 284,863 309,671 342,170

CAR CORDILLERA 126,477 125,974 133,413

I ILOCOS 61,834 66,722 72,677

II CAGAYAN VALLEY 50,425 56,295 61,800

III CENTRAL LUZON 84,855 90,229 93,745

IVA CALABARZON 125,062 131,602 135,579

IVB MIMAROPA 61,646 63,318 64,137

V BICOL 35,968 38,569 42,206

VI WESTERN VISAYAS 53,488 57,598 61,325

VII CENTRAL VISAYAS 84,769 94,129 101,862

VIII EASTERN VISAYAS 57,549 53,803 58,451

IX ZAMBOANGA PENINSULA 56,473 61,146 63,643

X NORTHERN MINDANAO 85,891 90,793 95,655

XI DAVAO REGION 88,607 90,645 97,037

XII SOCCSKSARGEN 64,321 68,968 75,061

XIII CARAGA 43,688 48,741 51,146

ARMM MUSLIM MINDANAO 26,476 27,690 29,608

Purchasing power: It is because income growths in these recipient regions are faster than the rest

Source: National Statistics Coordination Board

Region / Year 2011-12 2012-13

Philippines 8.8 9.3

NCR METRO MANILA 10.5 12.2 CAR CORDILLERA 1.2 7.5

I ILOCOS 9.1 10.1 II CAGAYAN VALLEY 13.0 11.1 III CENTRAL LUZON 8.5 6.0

IVA CALABARZON 8.3 6.0 IVB MIMAROPA 4.5 3.0

V BICOL 8.7 10.9 VI WESTERN VISAYAS 9.0 7.8 VII CENTRAL VISAYAS 12.8 9.9 VIII EASTERN VISAYAS (5.4) 9.9 IX ZAMBOANGA PENINSULA 10.2 5.9 X NORTHERN MINDANAO 7.7 7.3 XI DAVAO REGION 4.1 8.9 XII SOCCSKSARGEN 9.7 11.3 XIII CARAGA 13.1 6.3

ARMM MUSLIM MINDANAO 6.0 8.3

GROSS REGIONAL DOMESTIC PRODUCT (growth rates at current prices)

Macroeconomic Forecasts

2011 2012 2013 2014f 2015f

Inflation Rate (ave % change) 4.5 3.2 3.0 4.3 3.3

Peso-Dollar Rate (end) 43.93 41.50 44.41 44.80 45-47

Gross Int'l Reserves ($B) 75.4 84.5 83.2 80.0 86.0

GDP Growth Rate 3.9 6.8 7.2 6.3 7.3

Industry Sector 4.1 6.8 9.5 8.0 10.0

Services Sector 5.3 7.6 7.1 6.0 7.2

GDP growth to accelerate due to added reconstruction work and robust private sector

f – Forecasts Sources: NSCB; BSP; Dr. Victor A. Abola, Philippine Economy: Going to Slow Down or Rebound?

2014 Year-end Business Economics Briefing, Nov. 12, 2014, University of Asia and the Pacific, Pasig City

Financial Market Forecasts

2011 2012 2013 2014f 2015f

Inflation Rate (%) 4.7 3.4 3.0 4.3 3.3

Peso-Dollar Rate (P/US$)* 43.9 41.5* 44.4* 44.8* 44-47*

91 day T- bill rate (% p.a.)* 2.0* 1.5* 0.3* 1.3* 2.0*

10-year T-bond rate * (% p.a.)

5.1* 4.7* 3.3* 3.9* 4.4*

PSEi (Level / % change) 4,372 +4.1

5,500 +26.2

6,325 +16.0

7,100 +12.2

8,200 +15.5

*Year-end forecast

Investment environment to remain friendly with low interest rates

f – Forecasts Sources: NSCB; BSP; Dr. Victor A. Abola, Philippine Economy: Going to Slow Down or Rebound?

2014 Year-end Business Economics Briefing, Nov. 12, 2014, University of Asia and the Pacific, Pasig City

Weaknesses and Challenges

• Corruption

• Red tape and Bureaucracy

• High rate of poverty

• Vulnerable to natural calamities such as floods and earthquakes

• Inefficient infrastructures

• Low rates of investments to GDP

• Low Foreign Direct Investments

• Tribal conflicts in Mindanao

Sunrise Industries

Agribusiness

Mining

Triple Ts: Transport, Telecom, and Tourism

Infrastructures

Automobiles

Consumer durables

IT-enabled and IT services

Logistics and retailing

Health care and medical tourism

Education

Construction and real estate

Four Fs: Food, Fashion, Furniture, Fun

Agribusiness

Business Process Outsourcing

Creative Industries

Infrastructures (Airports, Power, Roads and Rail, Seaports, Telecoms, Water)

Manufacturing and Logistics

Mining

Tourism, Medical Travel and Retirement

Source: Arangkada Philippines 2010: A Business Perspective, Joint Foreign Chambers

Seven Key Industries

The Philippines: The New Tiger of Asia

Dr. Bernardo M. Villegas

Ph.D. (Harvard)

University Professor, University of Asia and the Pacific

Manila, Philippines