THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Susan Horky, LCSW.

36

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Susan Horky, LCSW

-

Upload

bryan-wiggins -

Category

Documents

-

view

218 -

download

1

Transcript of THE PATIENT PROTECTION AND AFFORDABLE CARE ACT Susan Horky, LCSW.

THE PATIENT PROTECTION AND AFFORDABLE CARE ACT

Susan Horky, LCSW

Components

Patient-related Ensuring coverage Increasing access Fairness/transparency/getting value Increasing quality

Systems efforts Supporting prevention Decreasing costs Workforce development Additional systemic changes

Ensuring insurance

No annual or lifetime caps

Can’t be kicked off insurance if sick or made mistakes on application

Can’t be denied coverage due to pre-existing condition

Ensuring insurance

Dependents remain on parents’ insurance till 26

Can’t be made to wait more than 90 days for coverage

Ensuring Insurance

People with insurance can keep their current insurance (or choose not to)

If you’re uninsured you can: Obtain insurance through employer Go to an exchange [Obtain Medicaid]

Tax credits available for people < 400% FPL = $94,200 for a family of four

Tax credit

Generally available only for people who buy individual/family policies through an exchange

Available for people who have employer based health insurance IF

The employees’ part of the premium is more than 9.5% of household income or

If the plan covers less than 60% of medical costs

Ensuring insurance

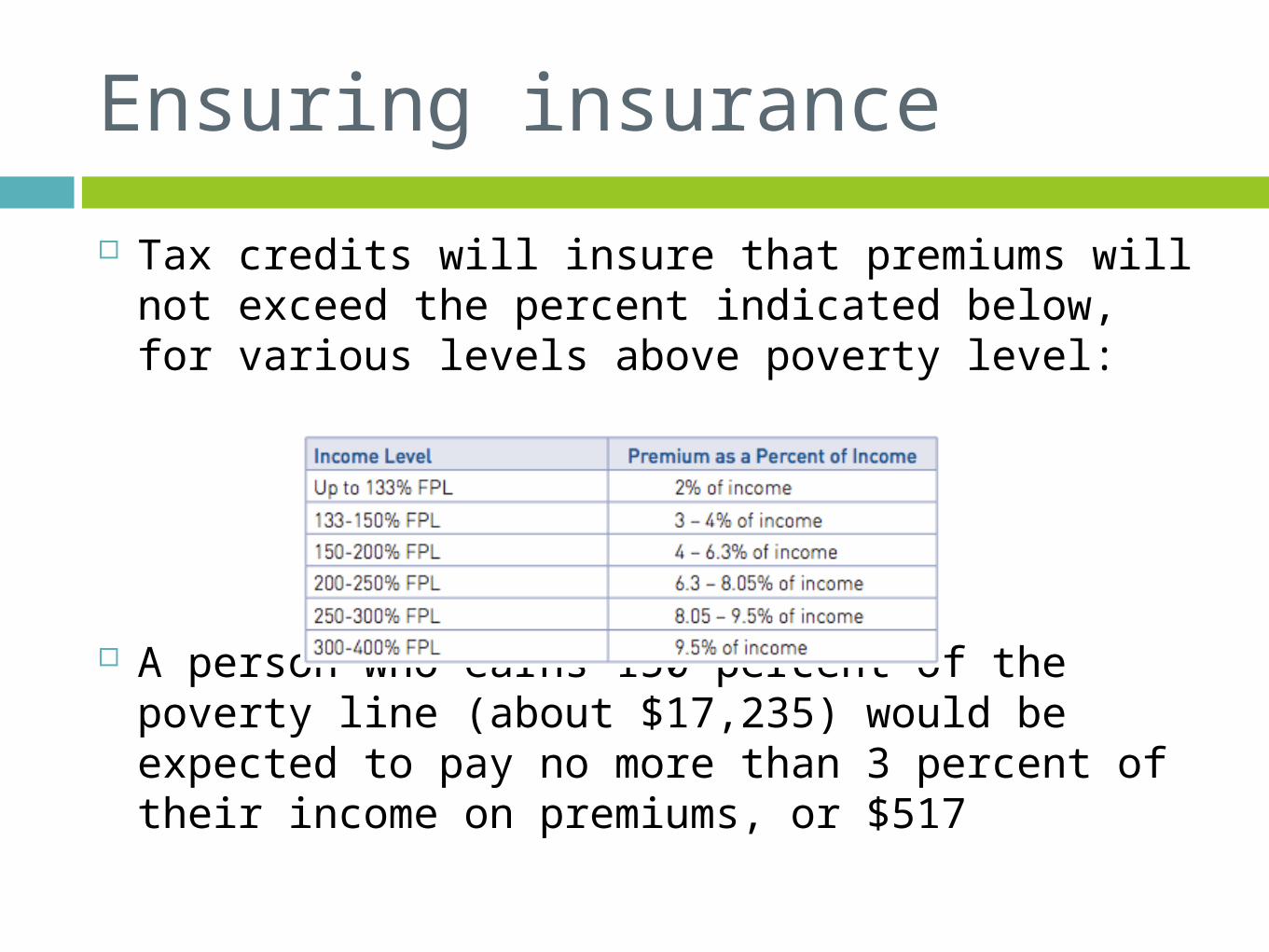

Tax credits will insure that premiums will not exceed the percent indicated below, for various levels above poverty level:

A person who earns 150 percent of the poverty line (about $17,235) would be expected to pay no more than 3 percent of their income on premiums, or $517

Ensuring Insurance: Affordability Sets limits to how much families must

pay out of pocket

2013 limits are $6,250 for an individual and $12,500 for family

These amounts are indexed annually for inflation

Ensuring Insurance: Exchanges Similar to buying car insurance, but

online

Choose from different options, clearly laid out

Users won’t know if exchange is set up by state or federal government

Ensuring Insurance: Exchanges

Ensuring Insurance

“Navigators” will assist patients in navigating the insurance and healthcare systems

Navigator grants available to states, agencies, universities

Penalties for no coverage

Some people who choose not to have coverage will be required to pay a penalty

This is NOT the case if: Your share of premiums (after federal subsidies

and employer contributions) would total more than 8 percent of your income

Your income is below the income tax filing threshold, and so you’re not required to file taxes

You were uninsured for less than three months of the year (If over three, the penalty is pro-rated)

You choose not to get insurance for religious reasons

Penalties for no coverage

The Urban Institute estimates that approximately 6% of the population (roughly 18 million Americans) will even have to consider the question of whether to get insurance or pay a penalty

Penalty in 2015 will be $95.00 Proof will be filed with income tax Penalty will be deducted from

income

Ensuring Insurance

Small businesses (<50 employees) are specifically exempted from having to provide insurance

Large employers do have to have to provide insurance or pay a penalty, as then the cost of providing coverage to their employees is covered by tax payers

Small businesses-Incentives

Very small businesses (< 25 employees) can get tax credits to help with insurance if they choose to offer it

Small businesses with up to 100 employees will have access to state-based Small Business Health Options Program (SHOP) Exchanges

SHOP exchanges are estimated to reduce by 4% the costs small businesses pay in premiums

Grandfathered Insurance Policies

Grandfathered plans are those in existence prior to 2014 who apply for grandfathered status (partial ACA exemption)

Grandfathered plans lose their status if they significantly raise premiums, copays etc

Grandfathered plans

Get rid of lifetime insurance caps

Offer dependent coverage for young adults until age 26

Keep people on their insurance even if they made mistakes on application (rescission)

Provide preventive care without cost-sharing

Offer “essential health benefits" for individual and small group plans

Refrain from imposing annual dollar limits (for individual policies only)

Provide coverage to children under 19 if they have a pre-existing conditions (for individual policies only)

Do have to Don’t have to

Essential health benefits (Required for individual and small group plans only) Ambulatory patient

services

Emergency services

Hospitalization

Maternity and newborn care

Mental health and substance use disorder services including behavioral health treatment

Prescription drugs

Rehabilitative and habilitative services and devices

Laboratory services

Preventive and wellness services and chronic disease management

Pediatric services, including oral and vision care..

Systems/Back-end Aspects of ACA

Increasing access

Making healthcare choices more understandable

Choosing own PCP

No ER prior authorization required

Encouraging cultural competence Workforce diversity grants Health care professionals training for diversity

Increasing access

Significant focus on (and funding for) Federally Qualified Health Centers Community Health Centers which serve a

variety of Federally designated Medically Underserved Area/Populations (MUA or MUP).

Migrant Health Centers which provide culturally-competent and primary preventive medical care to migrant and seasonal agricultural workers,

Health Care for the Homeless Programs which reach out to homeless individuals and families and provide primary and preventive care and substance abuse services, and

Public Housing Primary Care Programs that serve residents of public housing and are located in or adjacent to the communities they serve.

Increasing access

School based health centers

Co-locating primary and specialty care in community-based mental health settings

Extension of family-to-family health information centers

Removing barriers and improving access to wellness for individuals with disabilities

Counting resident time in non provider settings.

Fairness/Value/Transparency Low salaried individuals must have same

insurance options as high salaried individuals

All people must be charged the same premiums for the same coverage except for:

Individual vs. family coverage The insurance rating area in which the person lives The age of the person (but cannot vary more than 3:1) Whether or not the person uses tobacco (but cannot

vary more than 1.5:1)

Fairness/Value/Transparency All approved health insurance plans must

have same components (within Silver, Gold and/or Platinum)

Amount patient pays of own healthcare costs (through deductibles and copays) Bronze plan: 40% Silver plan: 30% Gold plan: 20% Platinum plan: 10%

Fairness/Value/Transparency 80%-85% of premium incomes must be

spent on healthcare

If insurance company spends more than 15%-20% premium incomes on administrative costs or profits, they must send rebates to the insured

Fairness/Value/Transparency Each hospital must

make public a list of the hospital's standard charges for items and services it provides

Each health insurance plan must have a clear plan for appealing their coverage decisions and standardized complaint forms

Nursing home compare Medicare website

Quality

Payments to hospitals will be linked to quality measures, including Readmissions Hospital acquired infections Patient perceptions of care Health outcomes Patient safety/medical errors Implementation of wellness programs

Quality

Technical assistance will be available to hospitals, to help improve quality

Healthcare professionals and hospitals will get bonuses for quality reporting

They will also be penalized for not doing quality reporting

Quality

Significant funding available to create innovative programs that improve quality:

Aging and disability resources centers Medical Home projects Integrated care around hospitalizations MCH Home visiting projects Research into postpartum depression Train health professionals in quality

initiatives and patient safety

Quality

Health care delivery system research

Medication management services in treatment of chronic disease.

Design and implementation of regionalized systems for emergency care

Trauma care centers and service availability

Program to facilitate shared decision-making

Presentation of prescription drug benefit and risk information

Patient navigator program

Improving women’s health

Community Health Teams

Quality

Funding for innovative programs, continued Research into health disparities Childhood Obesity Demonstration Project Demonstration project concerning

individualized wellness plan Community transformation grants Patient-Centered Outcomes Research

Prevention

Rebates on premiums if person uses employer-based fitness plan

No cost-sharing on preventive coverage for individual or group insurance purchased through exchanges

Clinical and community preventive services; Community education and outreach campaign about prevention

Nutrition labeling of standard menu items at chain restaurants.

No co-pays on ACIP recommended Immunizations

Prevention

Incentives for prevention of chronic diseases in patients with Medicaid

Coverage of comprehensive tobacco cessation services for pregnant women with Medicaid

Improving access to preventive services for eligible adults in Medicaid Providers will be paid at Medicare rates for

preventive services for Medicaid patients

Cultural competency, prevention, and public health and individuals with disabilities training

Workforce development National health care workforce commission;

Health care workforce assessment

Public health workforce recruitment and retention programs

State health care workforce development grants

Federally supported student loans

Nursing student loan program; Nurse education, practice, and retention grants; Advanced nursing education grants

Health care workforce loan repayment programs

Workforce Development

Mental and behavioral health education and training grants

Training opportunities for direct care workers

Training in family medicine, general internal medicine, general pediatrics, and physician assistants

Nurse-managed health clinics

National Health Service Corps

Allied health workforce recruitment and retention programs; Grants to promote the community health workforce

Additional Systems changes

Funding for innovative pilot programs that change how providers bill (thus reducing costs)

Decrease in DSH payments