The Oregon Grape and Wine Industry AAWE Conference 15 August, 2008.

12

The Oregon Grape and Wine Industry AAWE Conference 15 August, 2008

-

Upload

xander-newbold -

Category

Documents

-

view

216 -

download

2

Transcript of The Oregon Grape and Wine Industry AAWE Conference 15 August, 2008.

The Oregon Grape and Wine Industry

AAWE Conference

15 August, 2008

2

About Us

3

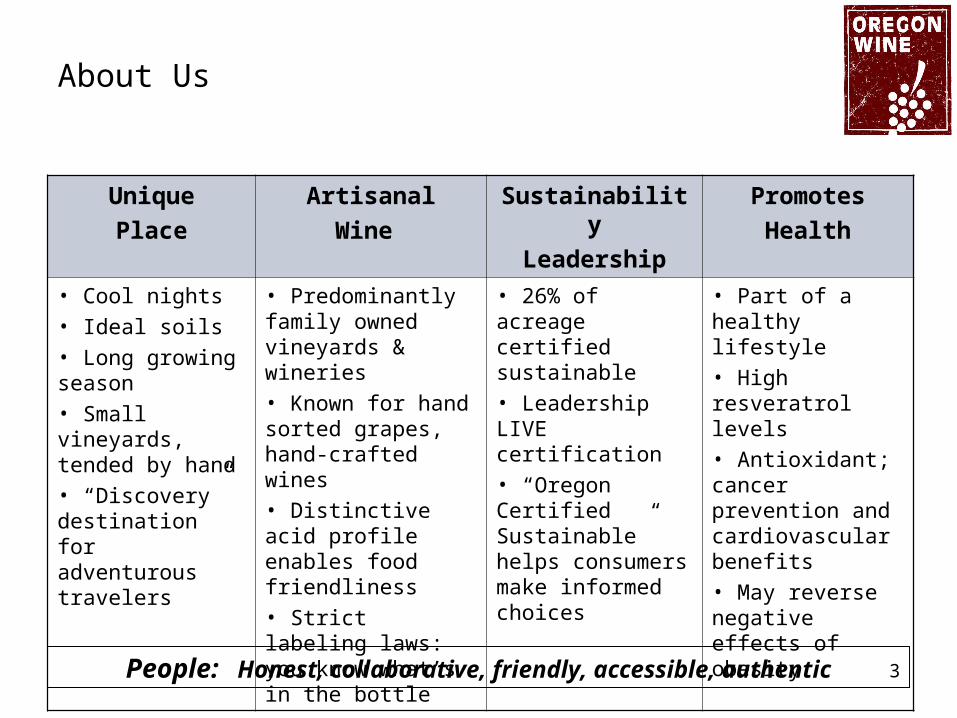

Unique

Place

Artisanal

Wine

Sustainability

Leadership

Promotes

Health

• Cool nights• Ideal soils • Long growing season• Small vineyards, tended by hand• “Discovery” destination for adventurous travelers

• Predominantly family owned vineyards & wineries• Known for hand sorted grapes, hand-crafted wines• Distinctive acid profile enables food friendliness• Strict labeling laws: you know what’s in the bottle

• 26% of acreage certified sustainable • Leadership LIVE certification • “Oregon Certified Sustainable” helps consumers make informed choices

• Part of a healthy lifestyle• High resveratrol levels• Antioxidant; cancer prevention and cardiovascular benefits• May reverse negative effects of obesity

People: Honest, collaborative, friendly, accessible, authentic

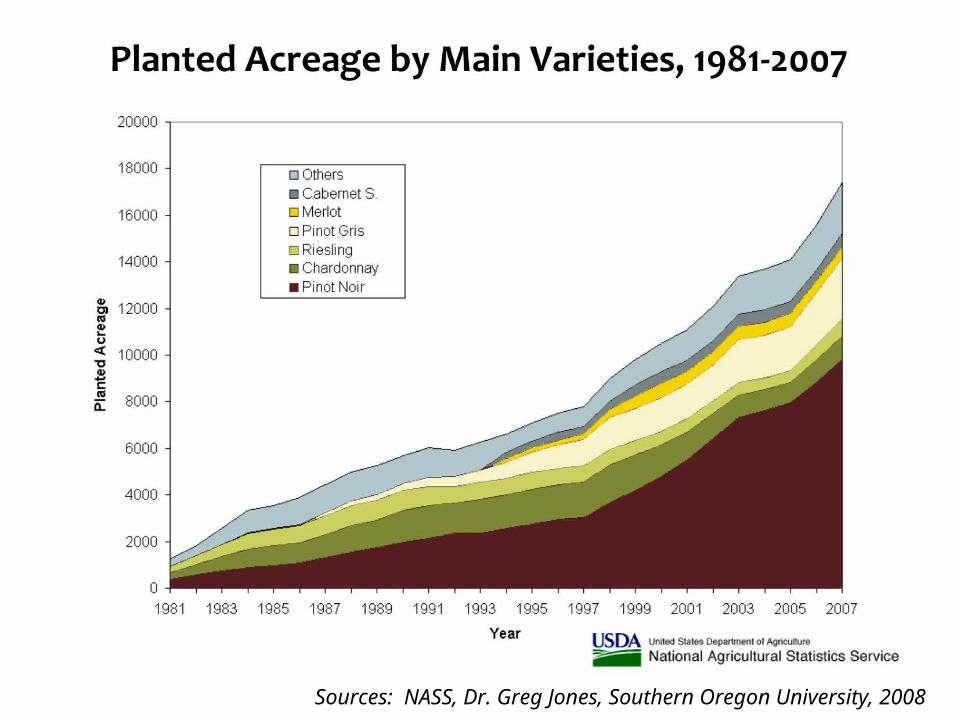

Sources: NASS, Dr. Greg Jones, Southern Oregon University, 2008Sources: NASS, Dr. Greg Jones, Southern Oregon University, 2008

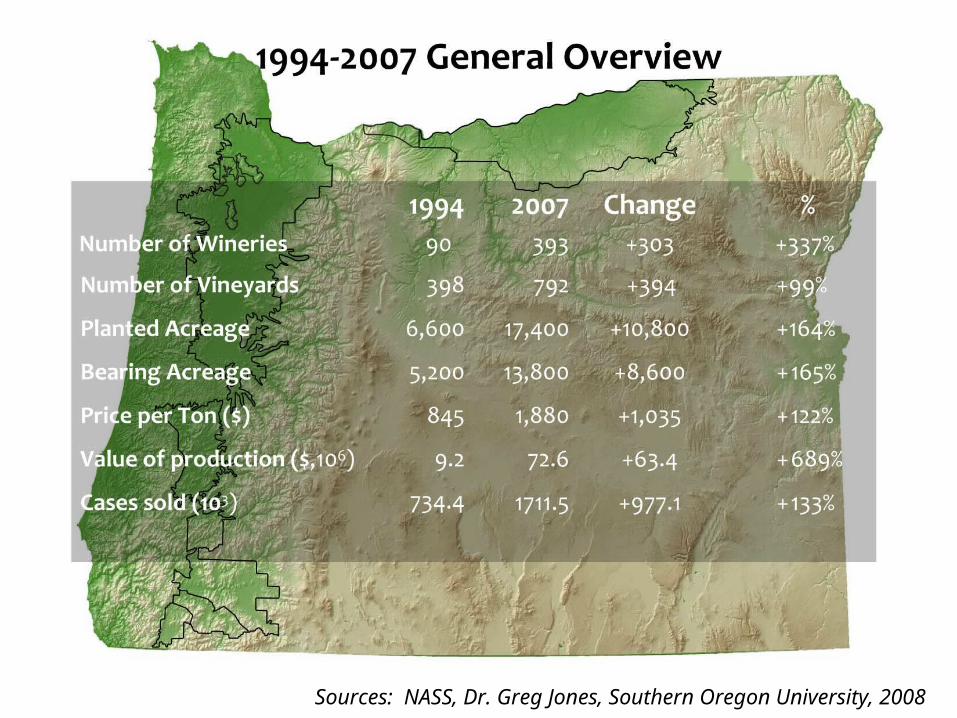

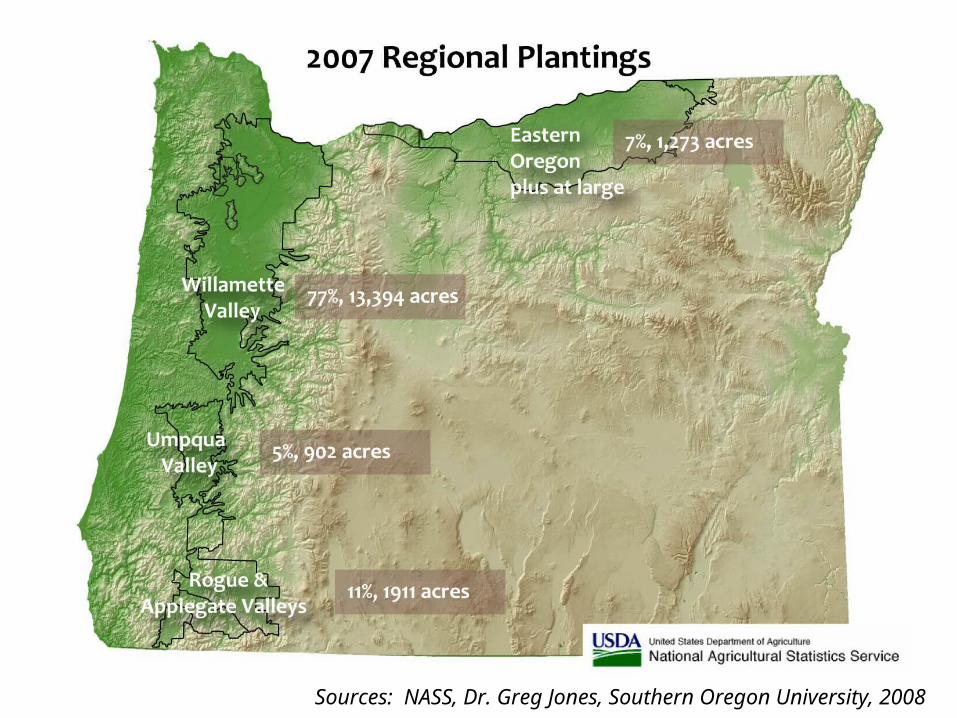

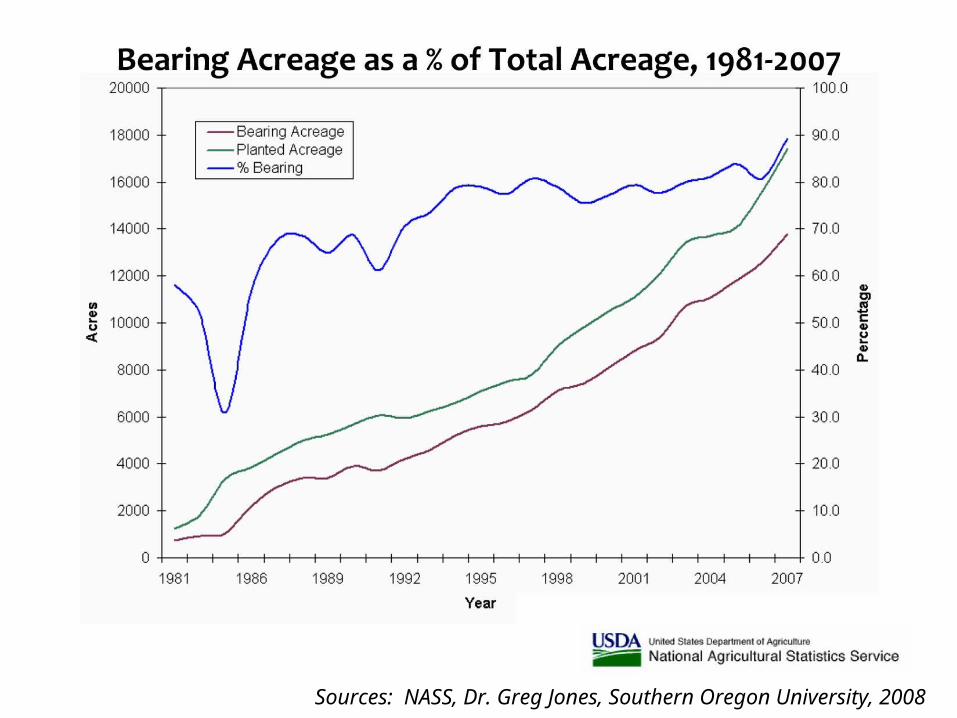

Source: Dr. Greg Jones, Southern Oregon University, 2008Sources: NASS, Dr. Greg Jones, Southern Oregon University, 2008

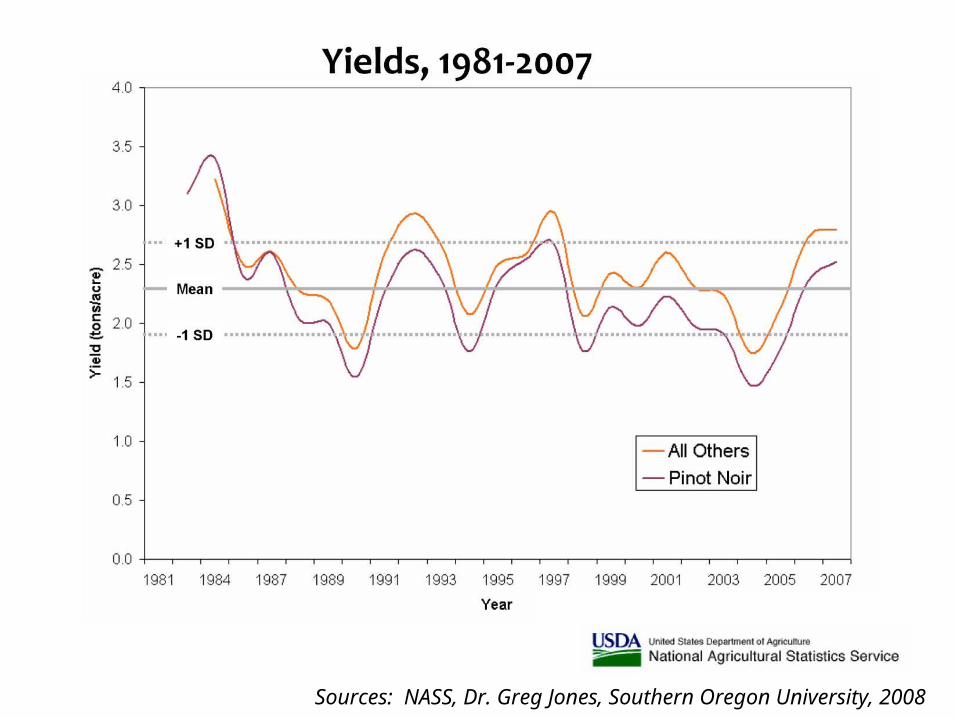

Sources: NASS, Dr. Greg Jones, Southern Oregon University, 2008

Sources: NASS, Dr. Greg Jones, Southern Oregon University, 2008

Sources: NASS, Dr. Greg Jones, Southern Oregon University, 2008

Economic Impact

• Over $1.4B• 8,479 jobs• $203M in wine-related wages• $92M tourism revenue• 1.48M annual winery visits• Wine grapes rank in dollar value within Oregon agriculture: 4th

9Sources: Full Glass Research, OWB, OWA (2005)

Ultra-Premium Focus

• Successfully focused on the higher priced, higher quality segments • Highest average returns per ton • Highest average revenues per case• Despite producing a much smaller volume of wine, OR winery

revenues per capita compare to NY and WA

10

Outlook generally positive

• Demand for PN & PG remains high • Production costs are reasonable for the quality obtained • Market outside NW underexploited, offering solid growth potential • Wine tourism underdeveloped compared to CA wine regions

– ~5% percent of overnight leisure trips involved winery visits• Far lower than Mendocino, San Luis Obispo and Amador counties (10–25%)

• Tourism infrastructure not keeping up with industry growth• However, competition fierce, especially in a softening economy• Market will need to absorb significant increases in the supply of PN

and some other varietals

11

Unique Business Challenges

• No significant economies of scale – no large vineyards possible• Not about cost minimization, but margin optimization• No extraordinarily large player, unlike CA and WA• Limited marketing budgets• Many second career owners not in it for the money

– Not always a rational economic system• Securing effective distribution in 3 tier system• Emphasis on direct distribution – margins vs. efficiency

12