The Oregon Agent Winter 2013

32

-

Upload

blue-water-publishers-llc -

Category

Documents

-

view

215 -

download

1

description

IIABO Winter 2013 mag

Transcript of The Oregon Agent Winter 2013

WashingtonP: 800.562.8095

[email protected] OregonP: 866.528.2918

Looking for Great Local Personal Lines Service? Look no further...

Serving over 2,200 agents throughout Washington and Oregon, and a proud supporter of IIABO.

Brokerage . Commercial Property & Casualty . Earthquake, Flood and Landslide (D.I.C.)Personal Lines . Pollution . Storage Tanks . Environmental Liability

Professional Lines . Surety Bonds . Transportation

} Phone Indications for HO/DF - new! } Online Quoting and Binding } Admitted HO/DF Market - new! } Personal Umbrella } Dwelling Earthquake - new market! } D.I.C. (Earthquake, Flood, Landslide) } Stand-Alone Liabilty (Premises or Personal) } Personal Inland Marine

} Farm & Ranch } Vacant Homes & Vacation Rentals } Course of Construction } Floating Homes/Yachts } Knob/Tube & Post/Pillar } Log Homes (Hand Hewn) } High Value Homes } Protection Class 10

2

We’re proud that our underwriters average more than 15 years of serving you and your Western National clients. You can get more done when your underwriter has a long shelf life. The proof is in the partnership.

What if everything had the same longevity as a Western National

Underwriter?

Untitled-2 1 3/12/2012 11:22:37 AM

Winter 2013 • The Oregon Agent 3

IIABO Office5550 SW Macadam Suite 305

Portland, OR 97239Phone: 503-274-4000Fax: 503-274-0062

Toll Free: 866-774-4226

IIABO Staff DirectoryExecutive Vice President

Vice PresidentMarketing & Communications

Barb [email protected]

Assistant Vice PresidentEducation & Finance

Tyra [email protected]

DirectorAgency Products & Services

Abby [email protected]

IIABO LobbyistRoger Beyer

For more information on advertising,contact Jim Aitkins

Blue Water Publishers22727 - 161st Avenue SE

Monroe, WA 98272360-805-6474 fax: [email protected]

The Oregon Agent is the official magazine of the Independent Insurance Agents and Brokers of Oregon

and is published four times yearly. IIABO does not necessarily endorse any of the companies advertising in

this publication or the views of its writers.

WINTER 2013

INSIDE THIS ISSUE:

THANK YOU ADVERTISERS:

6 Letter from the President

8 IIABO 2012-2013 Leadership

10 Grow Your Agency & Improve Your Marketing by Tracking Key Metrics

16 “Take the Plunge” IIABO 2013 MidWinter Education Symposium

18 Four Ideas for Keeping Customers for Life

20 What Do Companies Want?

22 Five Tips for Staying Motivated Every Day

24 Ten Compelling Reasons to Deliver an Amazing

Customer Service Experience

25 Building Engagement and Reach on Facebook

AAA 29

Agency Software 13

Anderson and Murison 29

Burns & Wilcox 9

Capital Insurance Group 19

Charity First Insurance 31

Cooper Construction Co. 29

Grange Inc. 5

Griffin Underwriting 2

Hull & Company, Inc. 21

IES 7

Imperial PFS 23

J. R. Johnson 11

Liberty Northwest 32

Preferred Property Program 27

Ron Rothert Insurance Services 12

Superior Underwriters 27

TAPCO 24

Western National Ins Group 3

Winery Pak 11

4 The Oregon Agent • Winter 2013

5

6 The Oregon Agent • Winter 2013

The wheels are turning at the IIABO office and 2013 looks to be another exciting year. By the time this issue of the Oregon Agent is published, over 300 people will have attended

the January 10th Forecast Breakfast. This annual event has completely sold out in recent years.

Looking ahead at the balance of my term as president, the IIABO, the PIA Oregon/Idaho and NAIFA are engaged in planning a Legislative Day in Salem, February 27th . This event will be open to all agents and will include CE along with an opportunity to meet legislators at the Capital.

March 7th and 8th are the dates for the Annual MidWinter Education Symposium in Lincoln City. This year our instructor is Bill Wilson, CPCU, ARM, AIM, AAM. Bill is the Director of the IIABA Virtual University and is an incredible teacher. Besides being the “fastest” 12 hours of OR/WA CE, the MidWinter Education Symposium has become almost a mini convention. The event includes breakfast and lunch each day and a hosted reception on the 7th, all at the spectacular Inn at Spanish Head. Spouse activities this year will provide an opportunity to learn the art of glass

blowing and a chance to blow your own personalized float. Sixteen sponsors and exhibitors add company people to the mix.

In April, the IIABO leadership will join 49 other IIABA states for the Annual Legislative Conference in Washington DC. In a remarkable show of grassroots strength, over 1,500 agents meet to discuss issues on “the Hill” in face to face meetings with their representatives in congress and the senate.

Mark August 25-27, 2013 for the 85th Annual Convention, “Cheeseburgers in Paradise”. The title highlights the fun aspects of the convention, but at its core, the convention is about value and workshops that will help create better producers, owners and agency managers. The convention includes golf, an always sold out exhibit hall and lots of prizes.

To make sure you don’t miss anything, mark your calendars now.

I hope you have a prosperous 2013! Remember, the IIABO is there to serve members and please use both the board of directors and staff as “your” agency resource. Call me if you would like to get more involved.

Your association staff:

Executive VP Jim Perucca 503-274-0583 [email protected] & Communications Barb Demings 503-274-4000 ext. 26 [email protected] & Finance Tyra Dressel 503-274-4000 ext. 31 [email protected] & Services Abby Kahl 503-274-4000 ext. 23 [email protected]

Toll Free Numbers: 1-866-77-IIABO or 1-866-774-4226

FROM THE PRESIDENT

Gary GithensBeecher Carlson541-749-4954

Gary Githens

20Years

. . . . . . .

7

Ryan MillerFinance Chair

Miller InsuranceTualatin

Brian WilburNational Director

Pacific Insurance PartnersForest Grove

Steve WilsonVice President/Education Chair

Ashland Insurance, Inc.Ashland

Keith BlackerbyBoard Member

Bisnett Insurance, Inc.Lake Oswego

Steve FitzwalterBoard Member

Rogers, Fitzwalter & PowellPortland

2012 - 2013 IIABO LEADERSHIP

Bradd HillBoard Member

Chet Hill InsurancePortland

Trish FulwilerBoard Member

J.D. Fulwiler & Co.Portland

John TimmBoard Member

Timmco Insurance, Inc.Portland

Debbie KrambealBoard Member

CAL/OR Insurance Specialists, Inc.Harbor

Jim GingerBoard Member

KPD Insurance, Inc.Springfield

Gary GithensPresident

Beecher CarlsonBend

Adam HarrisBoard Member

LaPorte & Associates, Inc.Portland

Ed DavisBoard Member/Legislative ChairMaPS Insurance Services, LLC

Salem

Brett SlaterBoard Member

Slater & Assoc. Insurance, Inc.Tualatin

Matthew PidcockBoard Member

Valley InsuranceLaGrande

Greg HornerBoard MemberUSI Northwest

Portland

8 The Oregon Agent • Winter 2013

No one writes Excess/Umbrella with the capacity and speed of Burns & Wilcox.

Put the power and speed of the Burns & Wilcox pen to work

for you: Solidify your clients’ coverage with our breadth of

proprietary Excess/Umbrella solutions. Derived from our

exclusive binding contract authority, our assets allow us to

quote and bind policies at rocket speed. When it comes to

securing your clients’ financial interests, think fast. Think the

largest independent wholesale broker – Burns & Wilcox.

Commercial • Personal • Professional • Brokerage • Binding • Risk Management Services

San Fransico, California | 415.421.4244toll free 800.759.4855 | fax 415.421.0620sanfrancisco.burnsandwilcox.com

Reno, Nevada | 775.786.6061toll free 800.249.0119 | fax 775.786.6041reno.burnsandwilcox.com

Salt Lake City, Utah | 801.432.5422toll free 800.523.1409 | fax 801.944.4893saltlakecity.burnsandwilcox.com

31943_BURNS_RocketPen Resize_CA4_NV1_UT1.indd 1 12/3/12 3:09 PM

Independent agents should be winning in the personal lines marketplace, even dominating. Is there any other industry where companies selling just one option have a majority of the market share over other companies in

that industry selling multiple options of the same product? Think of cars, ice cream, or appliances. The company selling multiple brands consistently beats companies selling just one option. And yet, in the world of personal lines insurance where independent agencies have multiple insurance carriers to sell and choose from, independent agents have around 33% of the personal lines market share. (A.M. Best 2011 data) It’s been this way for five years, almost no movement. Many agencies claim they’re growing a little, but it takes 1.7% growth per year just to keep up with the population increase and stay flat with market share. (US Census Bureau, 2000 to 2010 population annual growth average)

High Growth Agencies Track MetricsWhile most agencies change little in size of their personal lines books, there are a select few high growth agencies consistently increasing their total personal lines books by 10 to 24%. (Safeco NW Region top 25 personal lines high growth agencies study in 2011) Comparing the commonalities of these agencies, it’s clear that they stand out in their sales methods, training, and support. One thing really was truly unique – these agencies tracked their marketing efforts and knew what was effective and what was not.

For the purposes of this article we’ll keep the discussion to personal lines, but many of the tracking metrics that follow will work for commercial as well.

Marketing an independent agency is different from

marketing an insurance company. Large insurance companies need to drive greater name recognition. But like all small businesses, insurance agencies need to be more efficient, more cost effective. Simply put, your marketing efforts should be the result of knowing where your new business comes from, and how much revenue you make from the new business, so you can focus on how to drive in more and keep more.

Key Metrics for GrowthTo gain back some of that market share, independent agents will need to get more effective with their marketing. Let’s take a look at what the high growth agencies specifically track to help achieve their high growth numbers. These tracking methods can help you grow too.

These 25 growth agencies tracked 12 common items. They fall into three categories: new business, average revenue per client, and retention. Here’s a look into each of the 12, along with a few key target examples so you can see how you compare. As you read through this, put a mental check mark by all that you’re currently tracking in your agency.

NEW BUSINESS

Item 1: Total new business items This is fairly easily tracked through agency management systems. Most can say how many new policies were written. But it gets tougher from here.

Item 2: Where each new policy comes fromHere’s the big one. The most important question each person must ask on every call is, “How did you hear about us?”

The author studied the differences between high growth agencies in his territory and those that were not growing or growing only marginally. He determined that a key differentiator for the high growth agencies is that they tracked and acted upon key metrics relating to the origins of their business, close ratios, revenue and policies per client, retention and average client tenure. Based upon his research, the author then outlines the twelve key metrics agencies should track to maximize their marketing efforts and grow their business. He also lays out how agencies can generate those metrics.

& Improve Your Marketing by

By Chuck Blondino, Safeco Insurance

Grow Your Agency

Tracking Key Metrics

10 The Oregon Agent • Winter 2013

Winter 2013 • The Oregon Agent 11

WITH JUST ONE CALL YOU CAN WRITE THEM ALL.

888-386-5701With customized programs from one market covering wineries, distilleries, breweries andwine and liquor stores, opportunities abound. Check out the one exceptional source for

all of your specialty program needs by visiting www.PakPrograms.com

UNDERWRITTEN BY MEMBER COMPANIES OF GREAT AMERICAN INSURANCE GROUP.

Your business. Our specialty.

Everyone knows it. Without this, everything else falls apart. You can tell where the business comes from, which advertising dollars are most effective, where to focus your efforts and more, just from this question. Once asked, then the tracking begins. The more detailed you get, the more you’ll learn. Here are 10 basic tracking categories:

Total new business items – 1. # from cross sell efforts2. # from client referrals3. # from mortgage referrals4. # from real estate referrals5. # from walk ins6. # from phone books7. # from print ads8. # from website9. # from Facebook10. # from otherYou can also track on a much deeper level. You can

break out referral leads by each producer’s clients. You can track referrals by individual mortgage companies, real estate agencies, title companies and credit unions. This helps you understand which centers of influence are high quantity referral sources and thus where to spend time enhancing relationships. Or you can view the low production sources,

so you can either change focus or drop the lead source completely.

Item 3: Close ratio by categoryLearning your close ratio by category can also be a big boost. It’s clear where you should spend your time if you know, for example, that your close ratios for mortgage companies and certain captive agent referrals are near 80% and other methods are at 25%,

Some of these agents who track close ratios know that their client referrals are closing around 70%, while other agencies know they close client referrals at 35%. Digging further, those with the higher close ratios are only considering true client referrals to be those where the person referred is calling for a quote. Agencies with the lower close ratio are accepting any name and phone number given by a client as a referral, but this means that the prospect may or may not be ready to look into insurance at the time you call, and the agency is spending resources to continue to call and follow up on each lead. Both methods can work, and several agents say that they want to encourage the behavior of giving any referral. But if you are tracking everything, at least you’ll know which ones are most effective.

12 The Oregon Agent • Winter 2013

Item 4: Monthly close ratio by producerThis is an excellent training tool. If you know your agency closes referrals at 55%, but that your three producers are closing referrals at close ratios of 70%, 50% and 35%, then you’ll know where you should focus your sales training internally. Sounds easy, but you can’t do this if you don’t track close ratios!

AVERAGE REVENUE PER CLIENT

Item 5: Total premium Another easy one to track. This needs to be done for all personal lines in the agency, not just by carrier, so compile the totals and read on.

Item 6: Total policies Also easy to track by totaling all of your policies by carrier into one agency number.

Item 7: Total number of clients This equates to total households. Pull the total number of addresses from your agency management system to get this tally.

Item 8: Average number of policies per client Divide total policies into the total number of clients to get this number. This is one of the most helpful statistics you have to tell you how your team is cross selling your book. A rough average of number of policies per client to use is 1.6. If you’re averaging 1.4, you know that one of the first things you should do is a big cross sell effort throughout your book. Cross selling boosts both new business and retention, so if your average policies per client are 1.6 or less, you should focus your marketing efforts here first.

What is the high end ceiling for average policies per client? Very few agencies average 3 or more policies per personal lines client. It’s challenging to move your book one tenth of a point in this category. But if you track it monthly and can see growth over 3 months of 1.72, 1.73, 1.74, you know you’re making solid progress on cross selling. If not, you may want to do some cross selling mailings with phone call follow ups. Or it may show a need for you to do more internal sales training on cross selling to protect your clients properly.

Item 9: Average premium per policyTo find this amount, divide total premium by total number of policies.

Winter 2013 • The Oregon Agent 13

Your Local Insurance Software Solution since 1988

215 W Commerce Dr, Hayden, ID 83835

Come visit us at www.agencysoftware.com See if EasyApps, EZAgent, or AgencyPro are a right fit for your agency

800-342-7327

Agency Software Inc has software solutions designed to match virtually any sized agency and any budget

Scalable Insurance Software Solutions

Item 10: Average revenue per client This is more challenging, but it’s the jewel of tracking numbers for every agency. To determine the average revenue per client, multiply the average premium per policy by average policies per client. For example, if your average premium per policy is $1000, and your average policies per client is 1.6, then your average premium per client is $1600.

Now multiply your average premium per client by your average commission. For example, $1600 average premium per client times your average commission of 13% would equate to average revenue per client like this: $1600 x .13 = $208 average agency revenue per client.

What is a good target range for average revenue per client in personal lines? Heavy non-standard agencies selling mostly monoline auto will be in the $140 to $180 range. In low catastrophe areas, average preferred agencies will see $190 to $240. In more affluent areas or places with increased catastrophe exposure, the average revenue per client is higher, averaging $280 to $325 per client.

Once you know this number, and you know where your business comes from, you can easily track your return on your investment. Agents who know these numbers are shooting for a 1 to 1 first year return on all of their marketing. For example, if you’re spending $1000 per month on phone book ads, and your average revenue per client is $200, then you know you need to write 5 new clients each month to get a 1 to 1 return. If you’re not, then you may want to consider shrinking your marketing in that area. If your newsletters are driving a 1 to 1 first year return or better based on the increased referral traffic, then you know your marketing there is paying off.

RETENTION

Item 11: Retention for your entire book each month To determine your monthly average retention, you’ll need to know:

-- Total policies from 12 months ago -- Total policies as of the last month end -- New business total policies written over the past 12 months

For example, let’s say 12 months ago you had 1000 policies. At the end of the 12 months ending last month, you had 1150 policies. Subtract the 250 policies you wrote new over the 12 months from the ending total of 1150, and you kept 900 or 90% of the original 1000. (Be sure you’re not counting rewrites as new!)

Is focusing on retention worth it? Here’s how to find out. Multiply your current annual revenue by your current

retention rate. Do that over 10 years. Don’t add in new business; just see what happens to your current book over 10 years. Then multiply the same starting annual revenue by a retention number 3 points higher over 10 years, and calculate the difference. Here’s what it looks like for a $1 million revenue agency that moves it’s retention from 88% to 91%:

Item 12: Average length of time clients stay with youDetermine the number of years each client has been with you. Tracking in whole years as opposed to months is easier when you start. Add up all the years clients have been with you (this will be big). Then divide that total and divide by the number of clients you have. This will give you the average length of time clients stay with you. Excellent marketing tactics should deliver a $1.00 return for every $1.00 spent or better in the first year, but you get a much stronger picture for how profitable your marketing is when you know how long you retain your clients on average.

Keep tracking each of these metrics and you’ll enjoy seeing how your monthly report card can drive growth and stronger profitability.

Chuck Blondino is the Northwest Region Marketing Director for Safeco Insurance, Member of Liberty Mutual Group. Chuck wrote this article for ACT and he can be reached at [email protected]. This article reflects the views of the author and is not an official statement by Safeco Insurance or by ACT.

14 The Oregon Agent • Winter 2013

16 The Oregon Agent • Winter 2013

Winter 2013 • The Oregon Agent 17

18 The Oregon Agent • Winter 2013

These days I hear many excuses for agents losing

customers. The most prevalent by far is price. “The other company had

a better price. There was nothing I could do.” While price is always a factor, very rarely is it the main

consideration when considering a switch, the best estimates put the percentage at about 7%. The reality is, many agents simply aren’t building the strong relationships and they use price and other excuses when the customer naturally goes elsewhere. If you build a strong relationship and keep customers happy, they won’t jump ship the first chance they get. Also, if you thrill customers such that they are customers for life, they are much more likely to refer friends and family, thus increasing business and making your life a whole lot easier. In addition, if you’re working with happy, life-long customers all day, your work and life will be also be much more enjoyable. FIVE KEYS TO KEEPING CUSTOMERS FOR LIFE

1) Always make the customer your number one priority.You must bend over backwards for the customer and make sure that every experience with you and you company is an absolute pleasure. This begins with the number one rule of customer service: making sure the customer is always right. It also means doing what you say you’ll do when you say you’ll do it, and going above and beyond, doing more than you get paid for, to make sure the customer is always pleasantly surprised by the extra service they receive. In

Ideas forKeepingCustomersfor Life

By John Chapin

4U

UUU

addition, the customer comes before paperwork, phone calls, and other tasks you need to get done. When customers think of the best customer service they’ve ever received, you should be the one that comes to mind. They should always feel like a V.I.P.

2) Keep communicating.While some people require more communication than others, you want to reach out to people on a regular basis. This includes sending at least three cards to everyone you do business with: a Birthday Card, Holiday Card, and Anniversary Card on the date you started doing business with them. You also want to have your e-mail customers on an e-mail list that you send something of value to once a month. The title should make the content obvious to the recipient. In addition, you should talk to each client on the phone a minimum of once or twice a year, and meet with them in person at least once a year to review their coverage and find out if anything has changed that might affect their coverage.

A note on your cards: make sure they are personally signed by you in blue ink. Better yet, handwrite a personal note. If you don’t have good handwriting, you can have the note printed, but make sure you still sign it no matter what your signature looks like. Everyone from teenagers to centenarians appreciates a hand-written note. 3) Personalize the relationship and always seek to build and strengthen it. You want to take a personal interest in customers. Where are they from, where did they go to school, what

Winter 2013 • The Oregon Agent 19

interests do they have, do they have kids, grandkids, are they married? What activities are the people in their lives involved in? Once you have this information, show interest is what makes each customer unique. Ask about children, grand children, their personal interests, and the like.

Also, ask customers for their personal preferences and do business with them according to those preferences. For example, do people prefer e-mail or hardcopy? Are they okay receiving their renewal in the mail, or would they rather you deliver it personally? Yes, these are extra steps, but they are extra steps that your competition is more than likely not taking.

Ultimately you want to move customers from acquaintances, to friends, to good friends. The better relationship you have with a customer, the more likely they are to stay with you. If all your customers are good friends, and you take good care of them, they will stay with you. 4) Let them know you appreciate their business and that you don’t take them for granted. Thank customers for their business on a continual basis. You should be saying, “Thank you for your business, I really appreciate it” and/or “Thank you for being a customer” during phone calls and in-person meetings. You don’t have to mention this in the Birthday and Holiday Cards you send out, but you do want to mention it in the Anniversary Card as that is the main focus. The primary objective of the Holiday and Birthday cards is to add a personal touch. The bottom line: Treat customers right by making them a priority, taking a personal interest in them, and by letting them know that you appreciate and care about them. If you would like access to John’s free white paper on what it takes to be successful in sales along with a monthly newsletter, you can visit John›s website at http://www.completeselling.com John Chapin’s specialty is helping salespeople and sales teams double sales in 12 months. He is an award-winning sales speaker, trainer and coach, a number one sales rep in three industries, and the primary author of the gold-medal winning “Sales Encyclopedia”. In his 24 years of sales, customer service and management experience, he has sold in some of the toughest markets and economies.

??Many agents possess a significant fear that they are not big enough. To some degree, this feeling of inadequacy is nothing new. No matter if an agency has $500,000, $1 million, $5 million or $100 million, I’ve had agency executives tell me they do not have enough volume to please their carriers. The carriers simply have an insatiable appetite. With

such insatiable appetites, no one ever has enough and size in and of itself is the wrong goal.This is actually proven by most, though absolutely not all, carriers’ contingency contracts. Very

few contingency contracts actually pay materially more for pure size once the $1 million threshold is crossed. Instead, the majority pay materially more for higher growth rates without regard for

initial volume. The carriers are telling agencies that growth is more important than volume, but agency owners are not listening.

Growth is different than volume and maybe this is where the confusion originates. Growth is a percentage. Volume is a dollar based measure. Again, once the $1 million

threshold is crossed, the dollar basis is generally less important than the percentage of growth. Another reason agency owners may be confused is that company reps are

not always clear themselves so they send confusing messages. This is why agencies of all sizes feel inadequate. No matter how large

they are, the companies always want more. Many carriers are downright gluttonous. In years past, some companies have told their most profitable

agents they want more growth completely regardless of loss ratio. I saw some examples of companies completely unappreciative of quality loss ratios. They were basically telling their agents with 30% loss ratios, “If you can’t grow more quickly, you can take your loss ratios

elsewhere!”Times seem to be changing for some carriers though. I am

seeing some carriers express urgency now toward improved loss ratios. The market is now growing faster than any time in many years. This enables them to focus on loss ratios and simultaneously, the poor quality of business written the last few years is beginning to haunt and scare them. This would likely have occurred no matter what, but last year’s catastrophe claims and the severe under-reserving in workers’ compensation have accentuated the rush.

Yet, agents have been brainwashed that volume will always be king. Adjusting will be difficult. The result is that perfectly good agents are now making significant mistakes in an effort to finally achieve adequate volume once and for all (which will never actually occur). For example, some are beginning to make more acquisitions. All else being equal now is a good

By Chris Burand

What do Companies Want? ?

20 The Oregon Agent • Winter 2013

time to buy agencies because prices are lower. However, many of the sellers are under duress which is why prices are lower. Being under duress, some sellers’ prices are still too high because their retention will be less than expected and buyers who do not adequately consider this will be sorry. After all, what is the point of buying an agency to get volume if the business is not retained?

Clusters are probably the most common example. I am completely perplexed by most companies’ attitudes toward clusters. For example, why do some companies pay more in contingencies because these agencies use one code rather than five codes? The company is getting $0 additional volume, no improvement in loss ratios, and an even worse perpetuation problem. I am not writing about the firms that deliver a truly better set of results to the companies. Companies should pay more to these firms, but these firms are few and far between.

Another factor I do not believe company executives get is that most agencies of any size (I am excluding really small agencies) that join these organizations cannot sell insurance. They are not sales organizations. They have no true sales culture. They are account babysitters. This is not a bad characteristic. It just is not a characteristic that generates sales. So if a company wants growth, this is not where they will find it unless a consolidation strategy between the cluster and carriers are part of the deal. This of course, is not necessarily good ethics.

Company executives advise they see many of their agencies happy to belong to such organizations and these agencies should be happier for the time being because: 1) their responsibility to grow has been diminished, at least for the short-term; 2) the company marketing rep is not focused on them, but on their cluster; 3) the members feel safer because the cluster has so much more volume than the agency could ever achieve on its own. This mindset obviously ignores the fact that growth is more important than volume, but nonetheless, they feel safer and feeling safer is worth a lot to most people.

We’re already seeing evidence that some companies are belatedly realizing or maybe just now feeling enough pain to act on the reality that not only are they getting $0 extra dollars and 0% extra growth, their loss ratios are also deteriorating because loss ratios tend to suffer when an agency’s contingency is no longer dependent on their personal loss ratio. The way most clusters are designed, contingencies are doled out based on volume. Rarely ever is loss ratio a component to the individual members. This is a great example of the economic lesson contained in what is commonly known as the “Death of the Commons.”

When individuals do not own the property, when it is held in common, little incentive exists to take care of the commonly owned property. In fact, it pays to exploit the property to its fullest extent. As a result, some carriers are already pulling

out of specific clusters leaving all those agencies that joined in a far worse situation than before they joined. They not only lost their contract, they have no way to get another one on their own.

My advice? Do not worry about figuring out what companies want. Agencies that have good organic growth rates and loss ratios will always find smart companies wanting to do business with them. Such companies may not be the hot company de jour. Such companies may be few and far between. But this industry is a slow growth industry in which steady, methodical, profitable growth ultimately will win. Focus on what you can control. Focus on the opportunity presented by others’ mistakes. Focus on one quality sale at a time and the agency will achieve enormous success.

Chris Burand is president of Burand & Associates, LLC, an insurance agency consulting firm. Readers may contact Chris at (719) 485-3868 or by e-mail at [email protected]

NOTE: None of the materials in this article should be construed as offering legal advice, and the specific advice of legal counsel is recommended before acting on any matter discussed in this article. Regulated individuals/entities should also ensure that they comply with all applicable laws, rules, and regulations.

Winter 2013 • The Oregon Agent 21

22 The Oregon Agent • Winter 2013

These days there are a lot of negatives flying around out there. Unemployment, the economy, and a plethora of other items are lurking around every corner in the form of newspapers, television, and

negative people, and they are waiting to pounce on you and sap your energy and your morale. In addition to that, there are the personal issues that occasionally arise in life from a simple flat tire to major issues such as those related to job, health, and relationships. You know the key to your sales success lies in your ability to show up every day, put your game face on, and get the job done, regardless of what’s going on in your life. With that in mind, how can you best ensure you stay on track and don’t let outside issues and problems hit you hard internally and derail your success?

5 STEPS TO STAY POSITIVE AT ALL TIMES Step 1: Insulate yourself from the negatives. The first way to insulate yourself from negatives is to limit the amount of them that go into your brain. Specifically, avoid as much negative news and as many negative people as you can. The second way to insulate yourself from negatives is to put lots of positives into your brain and to hang out with

positive people. Studies have shown that a positive thought and a negative thought can’t occupy your brain at the same time. We also develop habitual ways of thinking, either positive or negative. In this case you can’t get too much of a good thing. Read, watch, and listen to all the positive, up-beat information you can. Also remember, you are who you hang out with. Step 2: Accept that there will be problems.Yes, there will be days when life will try to run you over. Problems are a part of life, you will have problems, and some of them will be big. While you don’t want to dwell on what problems could arise, you do want to mentally prepare by accepting that you will run into them.

See your problems as a challenge. It’s simple, either your problems steam-roll you, or you steam-roll your problems. Your problems either stop you, or you stop them. In life, you’re either the windshield or the bug, and you decide which you will be. If you do get knocked down, get up as soon as possible. Studies have shown that the amount of time someone stays down after a personal crisis relates directly to how happy and financially successful someone is, the shorter the time, the more happy and successful the person is.

By John Chapin

5 TIPS forSTAYINGMOTIVATED

Every Day

Sales Success Ideas:

Winter 2013 • The Oregon Agent 23

Step 3: Have a support system in place.You have to have people that you can talk to both in good times and in bad. While you don’t want to “dump” negatives on people, it’s good to have a friend or two who are positive and up-beat and will first listen to you and then help you turn around a tough day.

Also, “people” are really what life and happiness are all about. You want to have some good, solid relationships and have a decent social life outside of work. We must have balance in life with work, play, health, etc., in order to feel good and be truly happy.

From a professional standpoint, it’s good to be a member of a mastermind group, have a mentor or two, and ultimately have someone who will hold accountable for your goals and dreams. Step 4: Have a powerful WHY.It’s simple, if you know where you are headed in life for yourself and for your friends and family, and you have powerful reasons WHY you must get there, you’ll get there, nothing will stop you. If you don’t know why you do what you do, you just roll out of bed in the morning and go through the motions all day, you won’t be motivated.

If you need a powerful WHY, decide what you really want out of life. What do you want your life to ultimately look like? What do you want for your family and your kids? What do you want to be able to do? Motivation is different for everyone, work hard at determining YOUR personal motivation, finding your highest levels of motivation will pay huge benefits. With a powerful enough WHY, you will endure through anything. Step 5: Take 100% responsibility for everything in your life. Take 100% responsibility for your health: what goes in your mouth, how much exercise you get, for relationships: 95% of the people you run into during the day will be a reflection of you, if you don’t like someone’s response or reaction to you, change your response or reaction to them, 95% will change. 100% responsibility for your business: how many calls you make, how many leads you get, how many sales you make. To be truly successful and to keep moving forward no matter what, you must take 100% responsibility for everything in your life because where you ultimately

end up with have nothing to do with the economy, the job market, who’s president, or anything else, it will come down to: Did you show up every day and do what needed to be done regardless of what was going on in your life? John Chapin’s specialty is helping salespeople and sales teams double sales in 12 months. He is an award-winning sales speaker, trainer and coach, a number one sales rep in three industries, and the primary author of the gold-medal winning “Sales Encyclopedia”. In his 24 years of sales, customer service and management experience, he has sold in some of the toughest markets and economies. If you would like access to John’s free white paper on what it takes to be successful in sales along with a monthly newsletter, you can visit John’s website at http://www.completeselling.com For permission to reprint, or to reach John, email him at [email protected].

John Chapin Complete Selling, Inc.

Helping you find and get all the business you want Cell: 508-243-7359

[email protected] www.completeselling.com

creativityinspired by

imperial pFs, the leader in premium financing, continues to focus on the success of our agency partners.

in today’s volatile credit environment, our experienced staff finds creative solutions to your most complex transactions. We focus on getting the deal done while providing you the highest standards in customer service.

CHALLENGING NEEDS, CREATIVE SOLUTIONS

ipfs.com [email protected] Bothell: 800-888-2750 Spokane: 800-234-7373

24 The Oregon Agent • Winter 2013

I love lists, especially when it comes to learning. The list

below was the result of a quick brainstorm-ing session about the advantages of delivering a great customer service experience. I came up with many more, but wanted to create the “Top Ten List” for you. 1. Amazing customer service builds credibility, trust and confi-

dence, which can lead to customer loyalty.2. It can help the marketing and sales budget. It costs less to keep

existing customers than it does to create new ones.3. Delivering amazing service creates a buzz, word-of-mouth

marketing and referrals, again helping the marketing budget.4. Delivering amazing customer service can lead to existing

customers buying more.5. Customer service saves money. When you do it right the first

time, you don’t have to fix it the next time.6. Customer service can give your company an advantage over

competitors.7. Amazing customer service can make price less relevant.8. Customer service focused companies are usually employee fo-

cused companies, thereby creating a better place to work. That means lower turnover, which could mean savings in hiring, training and more.

9. Customer service superstar companies are usually more profit-able than the ones that aren’t.

10. Customer service helps get and keep customers… because without customers, you don’t have a business.As you look at the list, what other ideas and strategies do you

think about? I would love for you to send me what you would add to the list. As an incentive, when you send me your submission you will receive a 20 page report – actually what I call a “manifesto” – about “The Cult of the Customer.” It contains a synopsis of the five phases/cults both employees and customers go through on their way to creating “Amazement.” It also contains excerpts from my new speech based on the book.

Shep Hyken, CSP, CPAE, Shepard Presentations, LLC711 Old Ballas Road, Suite 215, St. Louis, MO 63141, (314) [email protected] - www.hyken.com - www.TheCustomerFocus.comCopyright 2010 by Shep Hyken. Used with permission

By Shep Hyken

Ten Compelling Reasonsto Deliver anAMAZING CUSTOMER SERVICE Experience

I love lists, especially when it comes to learning. The list in this article was the result of a quick brainstorming session about the advantages of delivering a great customer service experience. I came up with many more, but wanted to create the “Top Ten List” for you.

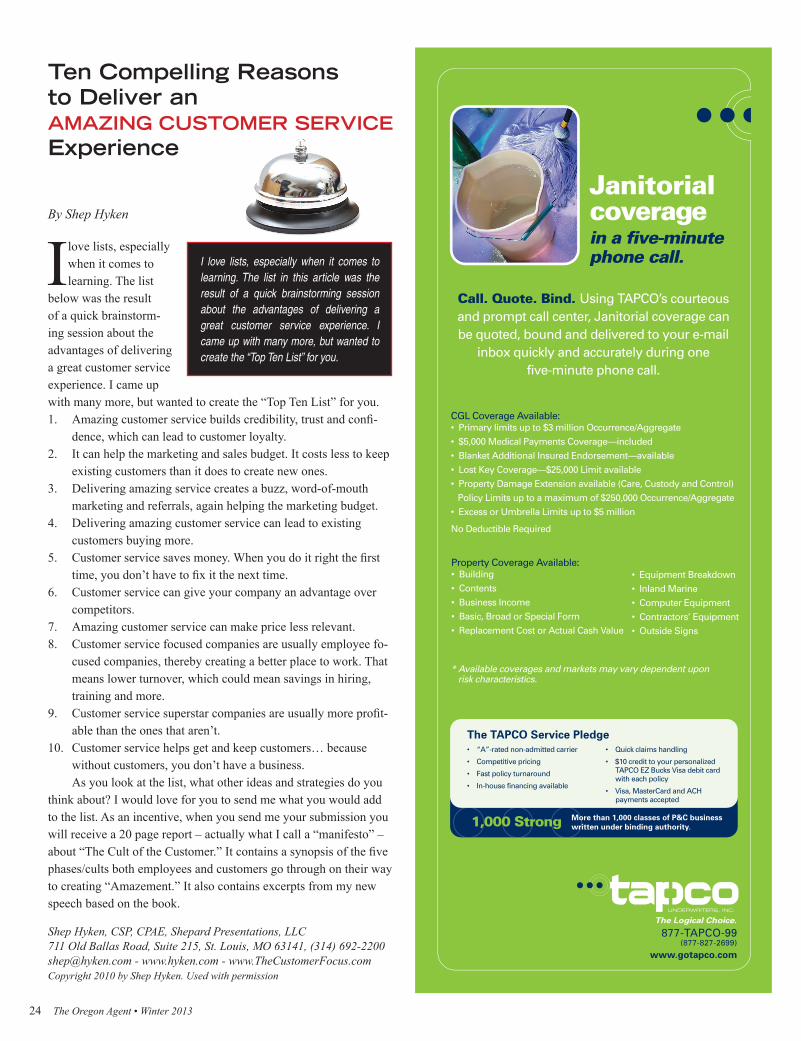

Janitorial coverage in a five-minute phone call.

CGL Coverage Available:• Primary limits up to $3 million Occurrence/Aggregate• $5,000 Medical Payments Coverage—included• Blanket Additional Insured Endorsement—available• Lost Key Coverage—$25,000 Limit available• Property Damage Extension available (Care, Custody and Control) Policy Limits up to a maximum of $250,000 Occurrence/Aggregate• Excess or Umbrella Limits up to $5 million

No Deductible Required

Property Coverage Available:• Building• Contents• Business Income• Basic, Broad or Special Form• Replacement Cost or Actual Cash Value

* Available coverages and markets may vary dependent upon risk characteristics.

1,000 Strong More than 1,000 classes of P&C businesswritten under binding authority.

• “A”-rated non-admitted carrier

• Competitive pricing

• Fast policy turnaround

• In-house financing available

• Quick claims handling

• $10 credit to your personalized TAPCO EZ Bucks Visa debit card with each policy

• Visa, MasterCard and ACH payments accepted

The TAPCO Service Pledge

877-TAPCO-99(877-827-2699)

www.gotapco.com

• Equipment Breakdown• Inland Marine• Computer Equipment• Contractors’ Equipment• Outside Signs

Call. Quote. Bind. Using TAPCO’s courteous and prompt call center, Janitorial coverage can be quoted, bound and delivered to your e-mail

inbox quickly and accurately during one five-minute phone call.

Winter 2013 • The Oregon Agent 25

At Facebook’s first-ever Marketing Conference in February 2012, the company released a startling number that quickly found its way into social media consultants’ Twitter streams and new

business pitch decks: 84 percent of business page fans do not see the page’s posts in their Facebook news feeds.

For agencies that are exploring social media’s potential (and asking tough questions about ROI), this number is alarming. Why should resource-strapped agents put energy into creating Facebook content when so few of their hard-earned fans are seeing the final product?

It’s a fair question, but before you shutter your Facebook page, you should understand what’s behind this number, and what you can do about it. With a few simple changes to your posts, you’ll be reaching more fans and building more engagement with minimal effort. WHY IT HAPPENS Just as Google uses an algorithm to pull the most relevant web content to the top of your search results list, Facebook uses an algorithm called EdgeRank to choose which status updates to display in your fans’ news feeds. The more friends they have and business pages they “like,” the more posts are competing for limited space. EdgeRank filters out all but the most relevant, and business page posts often don’t make the cut.

So which posts does EdgeRank usher through, and how do you get your posts on the shortlist?

HOW IT WORKS To outsmart the algorithm, it helps to understand it. That’s easier than it sounds. Vendors will often use the following formula to send you scrambling for your checkbook:

Don’t let the sigma scare you. Put simply, EdgeRank ranks your post based on three criteria: 1. The relationship between your page and the individual fan

(Affinity) 2. The value of the individual post (Weight), 3. The timeliness of the individual post (Decay). 1. Affinity The first criterion is an individual fan’s relationship with your page. Fans who regularly engage with your posts by clicking, liking, sharing, or commenting have a stronger “affinity” than fans who have stopped engaging (or who never engaged) with your posts. Unfortunately, this penalizes Facebook fans who

Facebook uses an algorithm called EdgeRank to choose which status updates to display in your fans’ news feeds. As a result, 84 percent of business page fans do not see the page’s posts in their Facebook news feeds! Kevin Ament provides the reader with three easy-to-implement tips that will increase the number of the agency’s fans that see its posts. These tips are essential for agencies to employ to build their reach and engagement on Facebook. The article also provides some great tools for agencies to use to monitor the reach of their posts and to keep up with changes in Facebook’s algorithm.

BuildingEngagementand Reach on Facebook

By Kevin Ament, Progressive Insurance

26 The Oregon Agent • Winter 2013

want to read your agency posts but don’t actively engage with them. I’ll share some tips for moving more of these passive readers into active fans later in this article. 2. Weight The second criterion, weight, creates a unique value for each post based on how much and what type of engagement your fans have with it. As more of your fans click, like, comment and share your post, its weight and reach increase. Higher-value engagement includes sharing and commenting, but even likes and clicks boost post weight.

The type of post can significantly influence fan engagement. Third party website EdgeRank Checker evaluates posts from more than 1,000 pages monthly and has found that photos drive more engagement than any other post type, followed by video, links and text-only status updates. 3. Decay The third factor, decay, is the most straightforward. Fans who are on Facebook during or shortly after you post are more likely to see your content. Fans who log in hours later have more (and more timely) content competing for their news feed, so there’s a lower chance your posts will break through.

Together, these three factors determine which posts show up in an individual fan’s news feed. So how can you use this information to create more impactful posts? WHAT YOU CAN DO ABOUT IT Here are three simple tactics to help you reach more fans with your Facebook posts. 1. Use more photos The most common problem I see on active agency Facebook pages is an over-reliance on text-only status updates. Posting more photos is an easy* way to

increase engagement and post weight. Photos grab audience attention and, given their size in the news feed, block out competing posts on the screen. Consider these two posts that use the same text. Which would you be more likely to read, “like” and share with your friends?

.

2. Ask for likes and shares A 2011 study from Momentus Media analyzing nearly 50,000 status updates found that directly asking fans for a “like” increased post engagement by 216 percent! Yet only 1.3 percent of posts include this specific call to action. We’ve seen this best practice dramatically increase engagement on our consumer Facebook pages.

One important caveat: pulling pictures from Google Images to use with your status updates is easy, but many of the images are copyrighted. To avoid potential legal exposure, consider creating an account with an inexpensive stock photography website like Shutterstock (you can purchase a quality pic for as little as 24 cents), or take your own pics and use a free app like Instagram to create a polished and consistent look for your pictures.

Winter 2013 • The Oregon Agent 27

JGSI N S U R A N C E

A subsidiary of

Umbrella Programs thatGive You More OptionsPreferred Property Program gives you broader,more flexible coverage with a range of limitsOur umbrella liability policies are written by XL Insurance with Chubb InsuranceGroup for the excess layer—two of the industry’s most highly rated carriers.We offer four umbrella limits, with coverage you can rely on.

• $5 to $25 Million in umbrella coverage with up to $50 Million in total limits.

• Hi-Rise apartments up to 35 stories eligible, with higher eligible by referral.

• Excess of D&O, General Liability, Auto, Employers Liability, EmployeeBenefits and more.

• Developer-sponsored boards eligible.

Contact us for a quote:

Service is our specialty; protecting you is our mission ®

960 Holmdel Road, Holmdel, NJ 07733

7.5 x 4.625jgs_umbrella_7.4x4.625v12012

XL Insurance is the global brand used by XL Group pic’s insurance companies.Our XL policies are underwritten by Greenwich Insurance Company.

®

28 The Oregon Agent • Winter 2013

3. Be provocative Posting on topics that people disagree on can drive up engagement, and every like, comment and share increases affinity and post weight. Religion and polarizing political topics remain danger areas, but asking for fan opinions on texting legislation, driving age minimums or limits, car seat age and weight guidelines, or product preferences (Harley or Honda: which has the superior engineering?) can generate strong opinions on either side. Even sillier questions that tap into strongly held opinions can have the desired effect. For example:

Use these three tips together to see the greatest gains in engagement and post reach, and be sure to track how fans are responding.

Your Facebook page administrators can see real-time reach data at the bottom of every post:

Winter 2013 • The Oregon Agent 29

Why AAA?Additional Revenue for Your Agency

Association with a High Quality Brand

Trusted, Long-Term Membership Organization − AAA Oregon/Idaho has been in business since 1905.

Largest Membership Organization in North America − More than 53 million members in North America.

Roadside Assistance Network − AAA has nearly 44,000 vehicles in our North America service network.

Most Widely Used Roadside Assistance − AAA membership continues to be the most widely used Roadside Assistance Program (RAP) among U.S. households.

Largest Leisure Travel Agency − AAA Travel is the largest Leisure Travel Agency in the U.S.

AAA Member Exclusive Savings − Members saved over $2 billion by taking advantage of AAA discounts including those available through the Show Your Card & Save® program.

To find out how to earn extra revenue selling AAA Membership, through your agency call us at 503-597-5824.

Learn more about AAA Oregon/Idaho and the benefits of AAA membership by visiting AAA.com.

*This program is only available to Independent Agents residing within the AAA Oregon/Idaho coverage area, which includes Oregon and the Southern 34 counties of Idaho.

ARE YOU LOOkINg fOR AN AddITIONAL REvENUE SOURCE?

AAA Oregon/Idaho Now Offers Select Independent Agents the Opportunity to Sell AAA Memberships.

We Say YES!

(800) 234-6977 x260www.andersonmurison.comA n d e r s o n a n d Mu r i s o n

One Submission – Multiple Markets.SM

On-Line Rate, Quote, Apply and Request Binding 24/7 or Call from 6am to 6pm PST.

Solutions For Over 40 years.

Personal UmbrellaSpecialists for

Oregon Producers

Endorsedby IIABA

C

M

Y

CM

MY

CY

CMY

K

AM Oregon Ad.pdf 1 9/18/12 4:24 PM

30 The Oregon Agent • Winter 2013

Kevin Ament is Agency Marketing Manager at Progressive Insurance. Kevin prepared this article for ACT and he can be reached at [email protected]. More Facebook and social networking tips from Progressive and others are available on the ACT website at the Websites & Social Media link.

Facebook Insights has helpful dashboards so you can track your progress and refine your strategy. If you’re not seeing traction (particularly if you’ve had an idle page for months, have a new strategy and want to give your page a jump start) you can

ensure all of your fans have an opportunity to see your post in their feed by using the “promote” tool. For a small fee, Facebook will add the post to a larger percentage of your fans’ news feeds, up to 100 percent.

KEEPING UP WITH EDGERANK Sites like EdgeRank Checker report regularly on any changes in the algorithm and provide additional tips on how and when to post for greatest engagement (Wednesday and weekends are the current leaders. You can even use the post scheduler feature on the bottom left of the status update window to schedule updates to post when you’re out of the office.)

With a little planning and a few best practices, you should see your Facebook engagement and reach rise over time. That’s the first step to achieving your goals, whether they’re acquisition, retention, public relations or a mix. Once you understand how to engage more of the fans you’ve already earned, take another step forward by learning to use the additional Facebook tools, like tagging and question, to extend your reach further, to the hundreds and thousands of prospects in your fans’ social networks.

CHARITY FIRST • 1 Market St., Spear Tower, Suite #200 • San Francisco, CA 94105 • Phone: 800-352-2761

At Charity First, we insure nonprofits. In fact, that’s all we do. And we have been doing it since our doors opened in 1985 in San Francisco. Today, our organization insures over 5,000 nonprofit organizations throughout the United States.

Combine this experience with our sole focus on the nonprofit community and it’s easy to see why we have become the nonprofit insurance experts.

Nonprofit Organizations

Social Service Agencies

Religious Organizations

With over 25 years focused on the nonprofit community, it’s easy to see why

we’re the nonprofit insurance experts.

Find out more at www.CharityFirst.com

Winter 2013 • The Oregon Agent 31

©2012 Liberty Mutual Insurance, 175 Berkeley Street, Boston, MA 02116

www.libertymutualgroup.com/business

Products, expertise, and services are one

thing. Delivering the solutions you need

is quite another. That combination is what

Liberty Mutual Insurance is all about.

We know how important it is for our agents

to have the right resources to support the

needs of their clients, which is why we pride

ourselves on strong agent relationships and

act with integrity and responsibility.

Your success is our success – we are proud

to support the Independent Insurance

Agents & Brokers of Oregon.