The Offshore and Nearshore Outsourcing Outlook · PDF fileThe Offshore and Nearshore...

126

TECHNOLOGY The Offshore and Nearshore Outsourcing Outlook Key locations, outsourcing models and the leading players By Gary Eastwood

Transcript of The Offshore and Nearshore Outsourcing Outlook · PDF fileThe Offshore and Nearshore...

T E C H N O L O G Y

The Offshore and NearshoreOutsourcing OutlookKey locations, outsourcing models and the leadingplayers

By Gary Eastwood

ii

Gary Eastwood

Gary Eastwood is an experienced writer and editor on business and IT issues,

contributing too many of the leading IT publications and magazines that cover the

gamut of IT sectors. As well as holding senior positions on a number of IT trade

publications, he has worked with companies such as Microsoft, IBM, CSC, Oracle and

Intel on a variety of marketing communications projects.

Copyright © 2005 Business Insights Ltd This Management Report is published by Business Insights Ltd. All rights reserved.Reproduction or redistribution of this Management Report in any form for anypurpose is expressly prohibited without the prior consent of Business Insights Ltd. The views expressed in this Management Report are those of the publisher, not ofBusiness Insights. Business Insights Ltd accepts no liability for the accuracy orcompleteness of the information, advice or comment contained in this ManagementReport nor for any actions taken in reliance thereon. While information, advice or comment is believed to be correct at the time ofpublication, no responsibility can be accepted by Business Insights Ltd for itscompleteness or accuracy.

iii

Table of Contents

The Offshore and Nearshore Outsourcing Outlook

Executive summary 10

Offshore and nearshore outsourcing 10 Emerging models in offshore outsourcing 10 The 10 most influential offshore service providers 11 Overview of offshore locations 12 Nearshore locations (for Western Europe) 12 Nearshore locations (for North America) 13 Focus on call center offshore outsourcing 14

Chapter 1 Offshore and nearshore outsourcing 18

Summary 18 Introduction 18 Offshore outsourcing 20 Drivers and inhibitors 20

Key drivers for offshore outsourcing 20 Inhibitors of offshore outsourcing 21

Best practice 24 Offshore outsourcing models 25 Transactional partnering 25 Tactical partnering 26 Strategic partnering – a joint venture 26 Collaborative partnering – Build-Operate-Transfer (BOT) 27 Wholly-owned subsidiary 27 Build or Buy? 27 Buy models 28

Offshore staff augmentation 28 Project outsourcing 28 Offshore dedicated center (ODC) 28 Functional outsourcing 28

When to buy? 29

iv

Offshore resources 29 Value add 29 Performance 29 Cost 29

Build models 30 Do It Yourself (DIY) 30 Build Operate Transfer 30 M&A 30

When to Build? 31 Nearshore outsourcing 32 Drivers and inhibitors to nearshore outsourcing 34

Drivers 34 Risks 34

Chapter 2 Emerging models in offshore outsourcing 36

Summary 36 Introduction 36 Offshore outsourcing models 37 Buy models 37

Offshore staff augmentation 37 Project outsourcing 37 Offshore Dedicated Center (ODC) 37 Functional outsourcing 38 Tactical partnering 38 Strategic partnering – a joint venture 38

Build Models 39 Do It Yourself (DIY) 39 Captive center 39 Build Operate Transfer (BOT) 40 M&A 40 Wholly-owned subsidiary 40

Nearshore outsourcing models 41 Nearshore 41

Western Europe 41 North America 42

Homeshoring 42 Call centers 42 Software development 43

Insourcing 44

v

Chapter 3 The 10 most influential offshore service providers 46

Summary 46 Vendor selection 47

Pick the Country First 47 Recommendation 47 Domain & technical filtering 48

The 10 most influential offshore outsourcing firms 48 IBM Global Services 49 Infosys Technologies 50 Cognizant Technology Solutions 50 Convergys 51 Accenture 51 Tata Consultancy Services 52 Hong Kong and Shanghai Banking (HSBC) 52 Keane 52 General Electric 53 Epam 53

Chapter 4 Overview of offshore locations 56

Summary 56 Introduction 57 Relative levels of risk and cost 57 Locations 59 Argentina 59

Where is the market today? 59 Risks 59 Rewards 59 Conclusion 60

Brazil 60 Where is the market today? 60 Risks 60 Rewards 61 Conclusion 61

Canada 61 Where is the market today? 61 Risks 62 Rewards 62 Conclusions 62

Hungary 63 Where is the market today? 63 Risks 63

vi

Rewards 64 Conclusions 64

India 65 Where is the market today? 65 Risks 65 Rewards 65 Conclusions 66

Jamaica 66 Where is the market today? 66 Risks 66 Rewards 66 Conclusion 67

Mexico 67 What is the market today? 67 Risks 67 Rewards 67 Conclusion 68

Philippines 68 Where is the market today? 68 Risks 68 Rewards 69 Conclusion 69

Poland 69 Where is the market today? 69 Risks 69 Rewards 70 Conclusion 70

South Africa 70 Where is the market today? 70 Risks 71 Rewards 71 Conclusion 71

Chapter 5 Nearshore locations for Western Europe 74

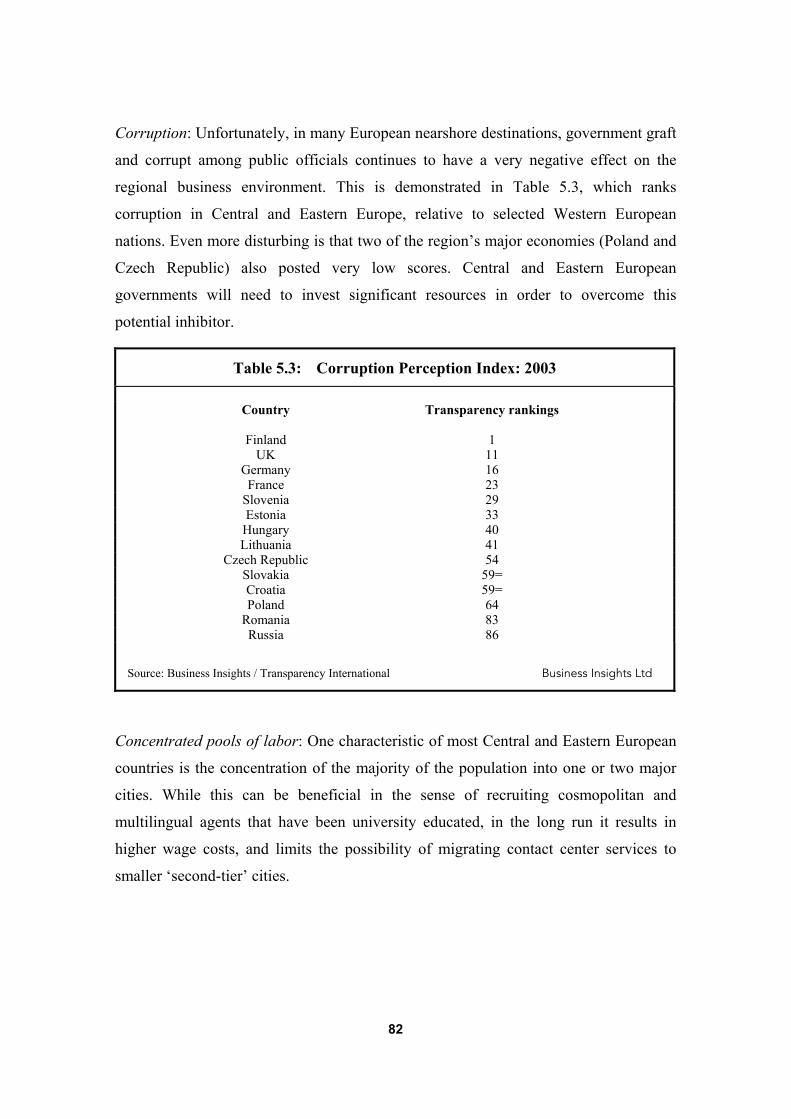

Summary 74 Introduction 75 Central and Eastern Europe 76 Strengths 76 Weaknesses 81 Opportunities 83 Threats 84 North Africa 85 Strengths 86 Weaknesses 87 Opportunities 88

vii

Threats 89

Chapter 6 Nearshore locations for North America 92

Introduction 92 Canada 93 Where is the market today? 93 Risks vs. rewards 93 Central America 95 Mexico 95

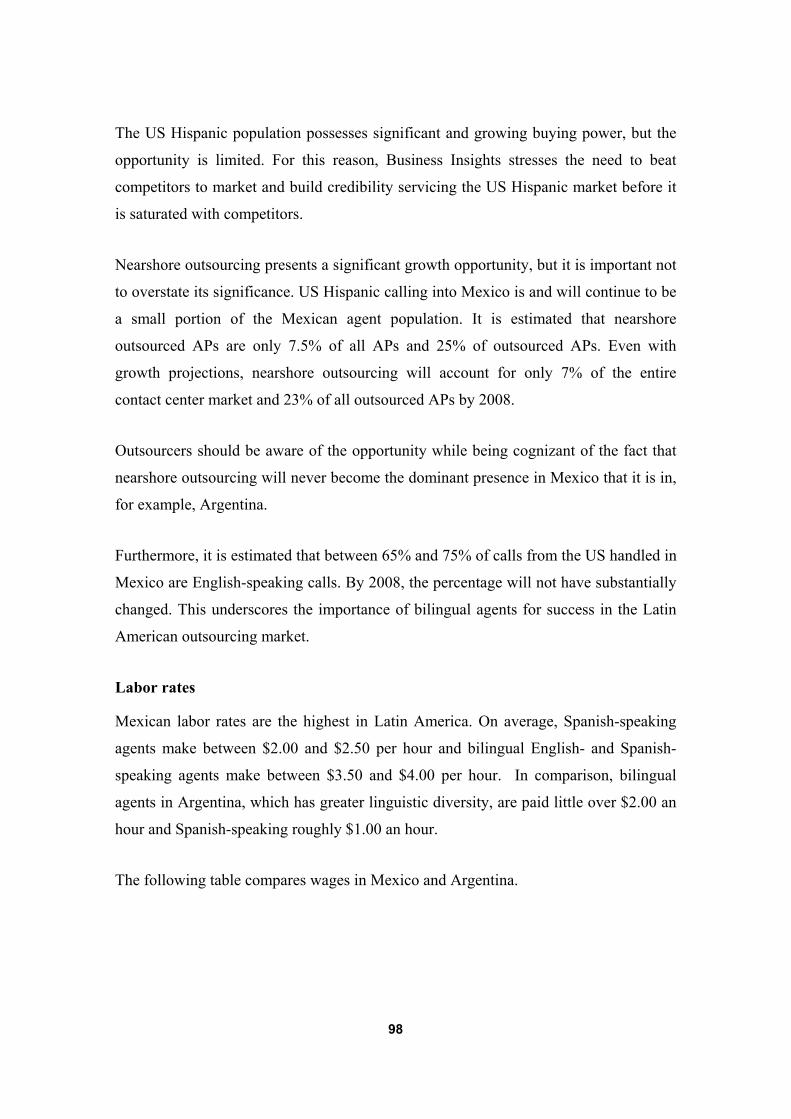

Where is the market? 95 Economic assessment 95 Nearshore outsourcing 96 Labor rates 98

Call center activity 99 Conclusions 99 The Caribbean 100 Jamaica 102

Government efforts to attract call center investment 102 Vertical market distribution 102 Labor market 103 Call center functions 104 Conclusions 104

Chapter 7 Focus on call center offshore outsourcing 106

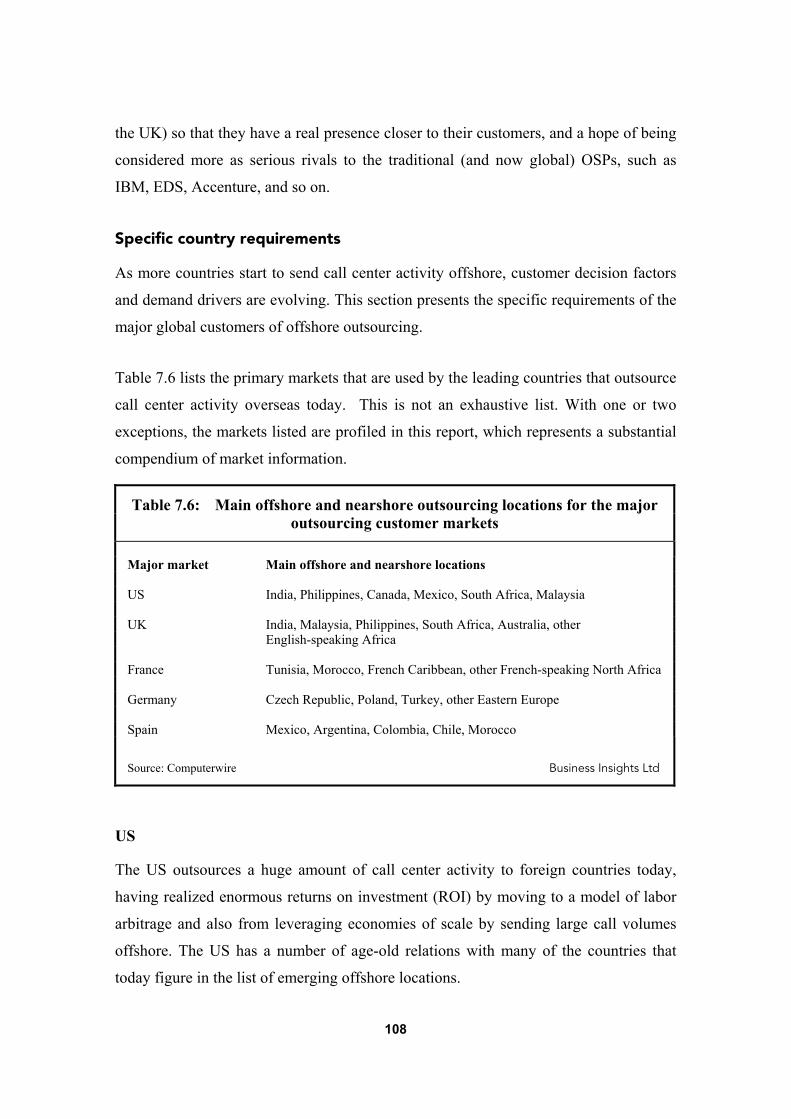

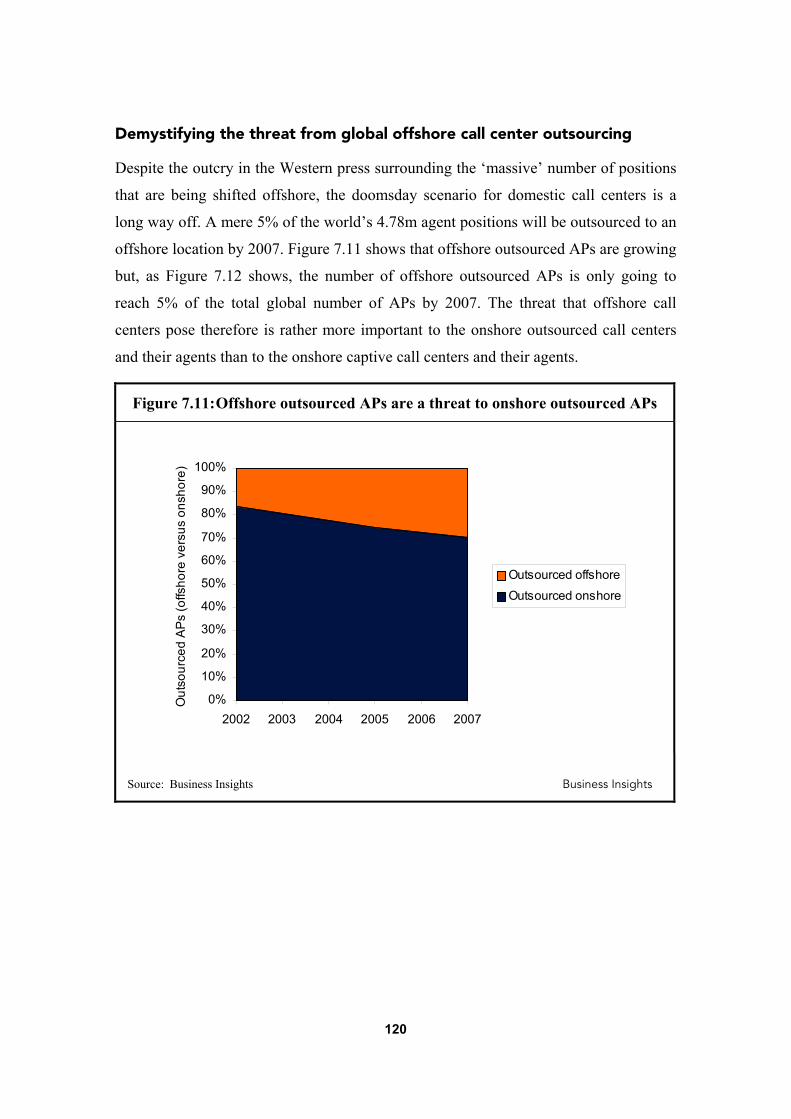

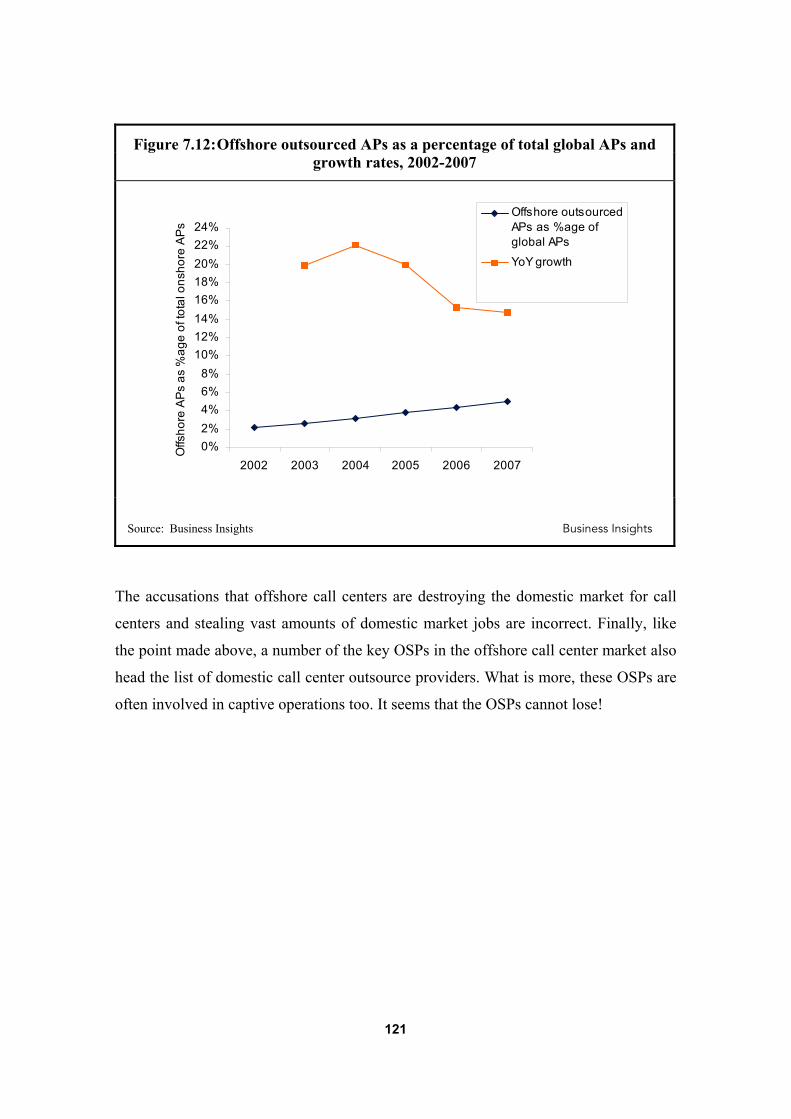

Summary 106 Demand for offshore call centers 107 Specific country requirements 108

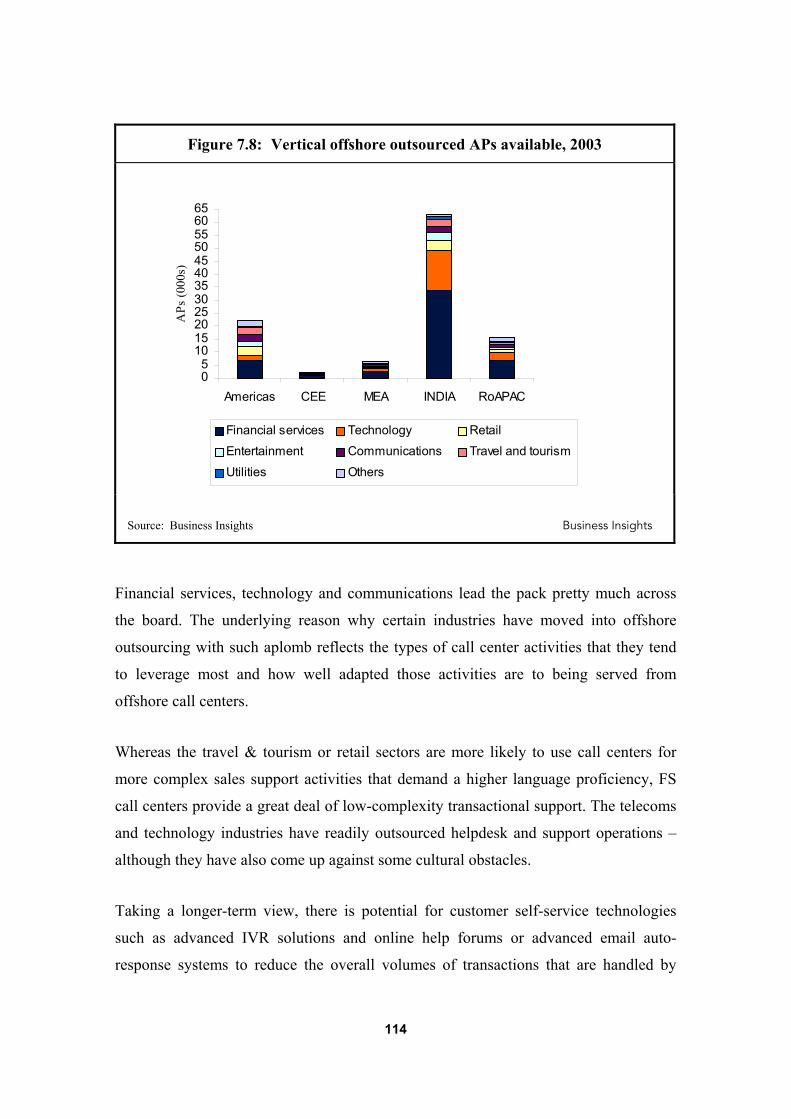

US 108 UK 109 France 110 Germany 110 Rest of Europe 112 Asia Pacific 113

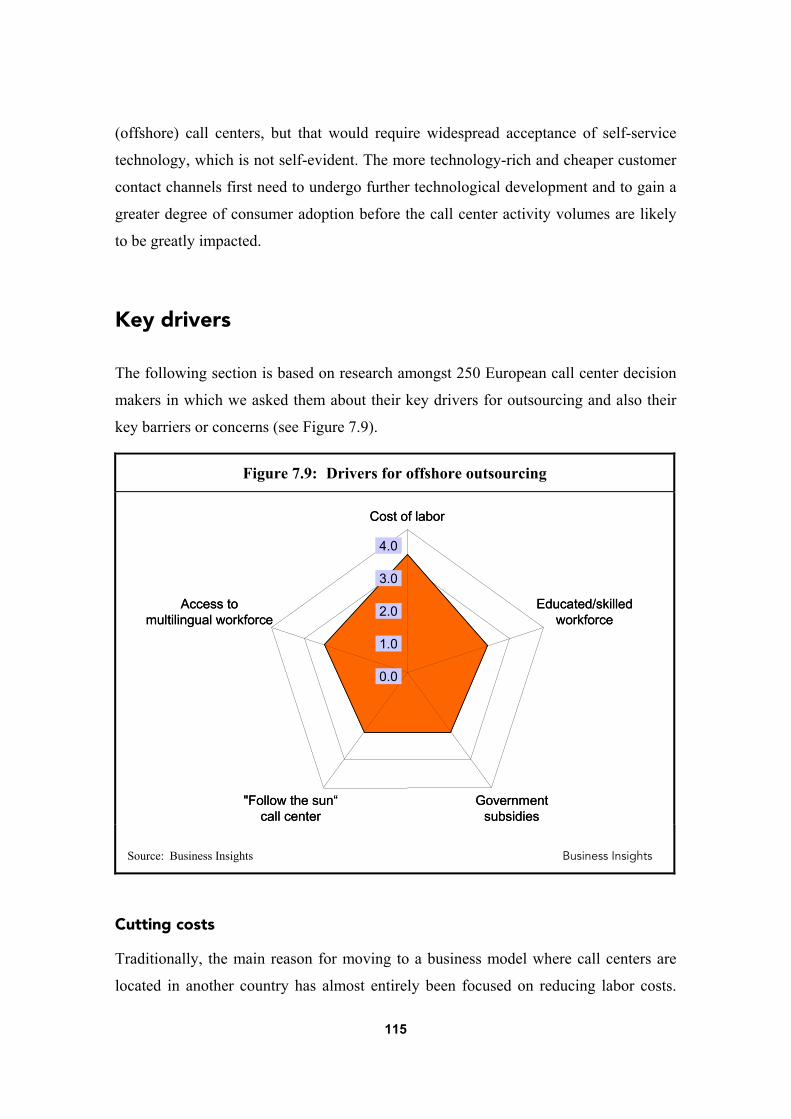

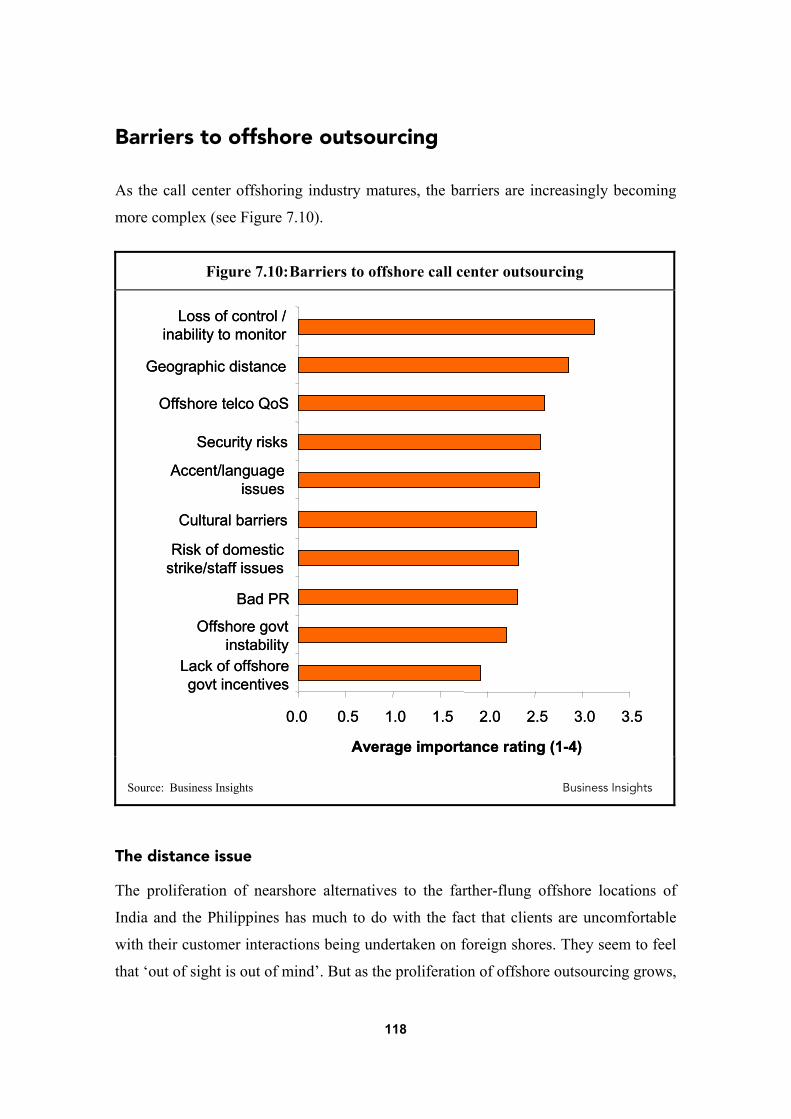

Demand for offshore call center outsourcing by vertical 113 Key drivers 115 Cutting costs 115 More demand for multilingual services 117 Barriers to offshore outsourcing 118 The distance issue 118

viii

Less concern for accents and more an issue of cultural affinity 119 Demystifying the threat from global offshore call center outsourcing 120 Action points 122 Refine sales approaches 122 Carve a niche and partner for success 122 Allay customers’ fears 123 Adopt appropriate pricing models 123 Exploit shared voice & data network new business opportunities 124 Index 125

List of Figures Figure 4.1: Relative risks and costs of nearshore and offshore outsourcing markets 57 Figure 5.2: Central and Eastern European nearshore outsourced agent positions, 2003 – 2008 76 Figure 5.3: Percentage of population between 20 – 24 years old in tertiary education, 2003 79 Figure 5.4: Commercial real estate rents – Selected urban centers, Q1 2004 80 Figure 5.5: Selected European unemployment rates: 2003 81 Figure 5.6: North African nearshore outsourced agent positions, 2003 – 2008 85 Figure 6.7: Mexican offshore and domestic outsourced APs, 2003 - 2008 97 Figure 7.8: Vertical offshore outsourced APs available, 2003 114 Figure 7.9: Drivers for offshore outsourcing 115 Figure 7.10: Barriers to offshore call center outsourcing 118 Figure 7.11: Offshore outsourced APs are a threat to onshore outsourced APs 120 Figure 7.12: Offshore outsourced APs as a percentage of total global APs and growth rates, 2002-

2007 121

List of Tables Table 3.1: The 10 most influential offshore outsourcing providers 48 Table 5.2: Selected travel times and prices for a single-day trip from London to selected

outsourcing destinations 77 Table 5.3: Corruption Perception Index: 2003 82 Table 6.4: Price per hour of Canadian outsourced agents, 2004 94 Table 6.5: Mexican call center wages and turnover, compared to Argentina 99 Table 7.6: Main offshore and nearshore outsourcing locations for the major outsourcing customer

markets 108

9

Executive summary

10

Executive summary

Offshore and nearshore outsourcing

The success of the offshore outsourcing model means that there are now over

10,000 vendors in more than 175 countries claiming to offer some form of offshore

outsourcing service.

In terms of IT, the key driver remains largely focused on cost savings.

As the offshore model matures, other considerations such as quality of service and

expertise, as well as knowledge of local markets knowledge, are further advantages

of offshoring.

Nearshoring has become a viable solution for many companies because nearshore

country locations offer the advantage of similar time zones, ease of travel and

potentially greater control due to familiarity or physical and cultural proximity to

the customer.

Emerging models in offshore outsourcing

Long term business strategy and commitment will determine an appropriate

business model for offshore outsourcing, of which there are a number to consider.

US companies are increasingly using locations such as The Philippines as a

nearshore location, in preference to India, for cultural and linguistic reasons.

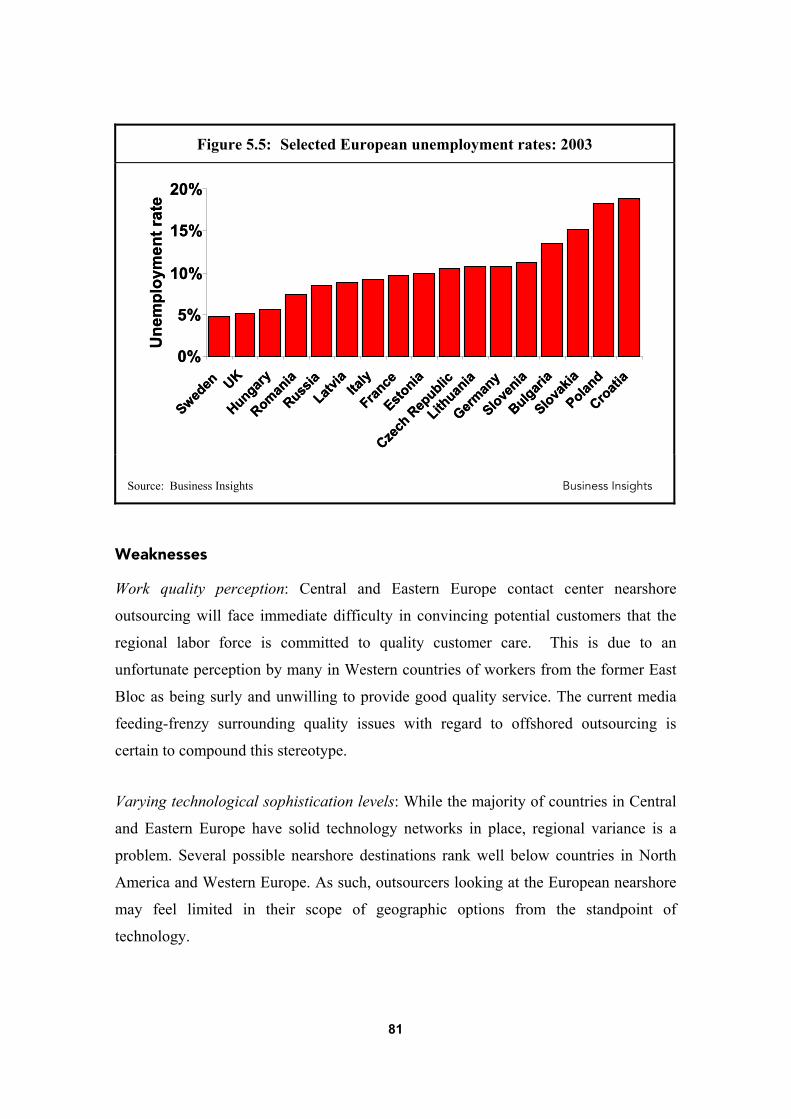

Central and Eastern Europe is emerging as a key region for nearshore outsourcing,

as West European companies are drawn to its low costs, ample labor pool, and pro-

commerce attitude.

The Build, Operate & Transfer (BOT) model is the lowest risk and can generate

some of the biggest cost savings and performance improvements.

11

Of all the potential options for building an offshore team, ‘Do-IT-Yourself’ is the

most expensive and least successful, with a success rate of less than 35% and

average cost exceeding $5 million.

The 10 most influential offshore service providers

The mantra “Pick the Country First” is perhaps the most widely known and

commonly used method for selecting an offshore vendor.

There is a growing trend in the market where buyers will use specific industry

domain and technical skills as the entry criteria for a tender process.

IBM Global Services has 6,000 people working in India, and has plans to expand

into China. The company only recently made its first acquisition in India in March

2004, paying $160m for India’s third largest BPO provider Daksh eServices, which

employs 6,000 people across five facilities in India and a new location in the

Philippines.

Infosys Technologies, the second largest Indian software services exporter, is

leading the expansion of Indian companies outside their homeland into China,

Eastern Europe, the Americas and Australia.

As one of the world’s largest suppliers of call center management services,

Convergys has pioneered the use of an offshore delivery model in contact center

management services, and is rapidly expanding its presence in India and the

Philippines.

12

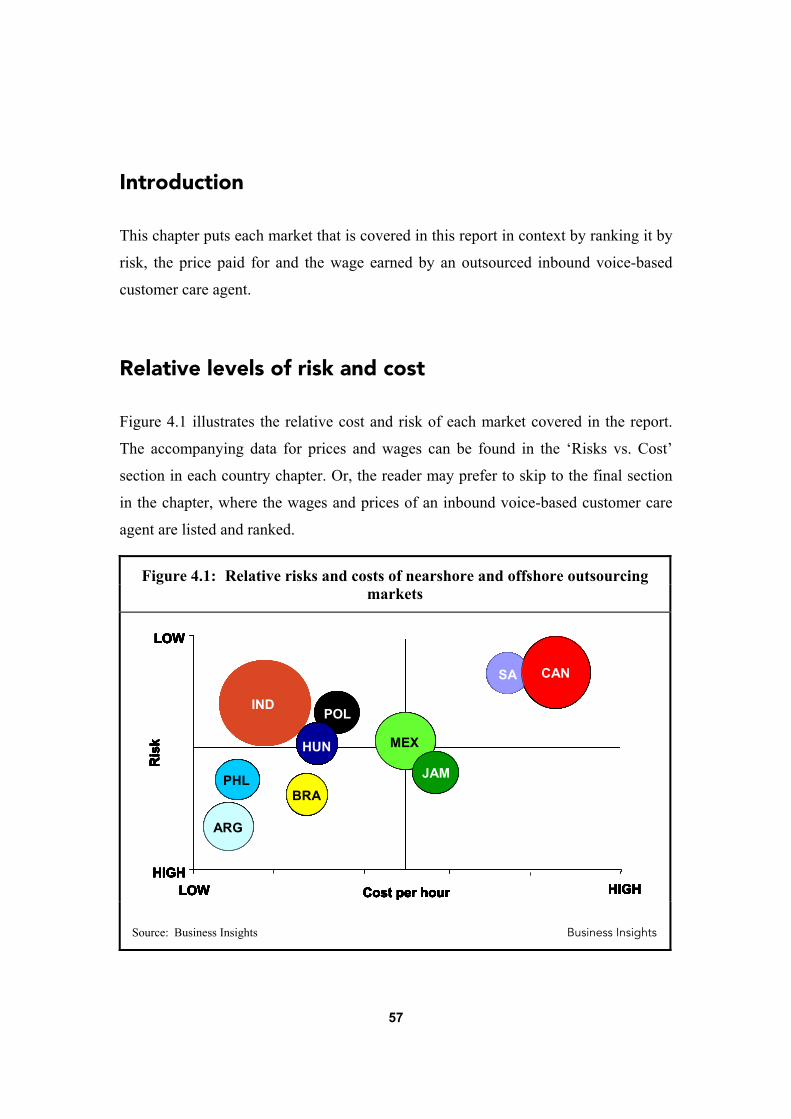

Overview of offshore locations

Enterprises from the US and UK will continue to locate centers in India despite

wage inflation, increasing turnover and negative press due to the level of service

from India and offshore outsourcing in general.

The Brazilian call center market offers the most balanced investment opportunity in

Latin America. It is the third largest call center market in the world behind the UK

and US and the most developed in Latin America.

Location is proving to be a determining factor for many US outsourcers as firms

become more cost and time conscious, and Canada is the classic example of the

benefits that nearshore outsourcing can provide.

Currently, Hungary is used primarily for mid-level calling but, as the market

matures, it will be used for increasingly complex services such as higher value

collections, technical support calling and cross- and up-selling.

The biggest attraction of the Philippines over India as an outsourcing location is its

cultural affinity with the US.

South Africa’s cultural affinity with Europe is making it an up and coming offshore

location, particularly in the call center and financial services sectors.

Nearshore locations (for Western Europe)

Western European companies will be prompted to action as more nearshore

alternatives to India, China and South Africa mature.

Eastern Europe call centers are far better placed to provide customer-facing

business process outsourcing (BPO) services – a rapidly growing sector for

outsourcing providers – to many European companies than are the traditional

offshore locations.

13

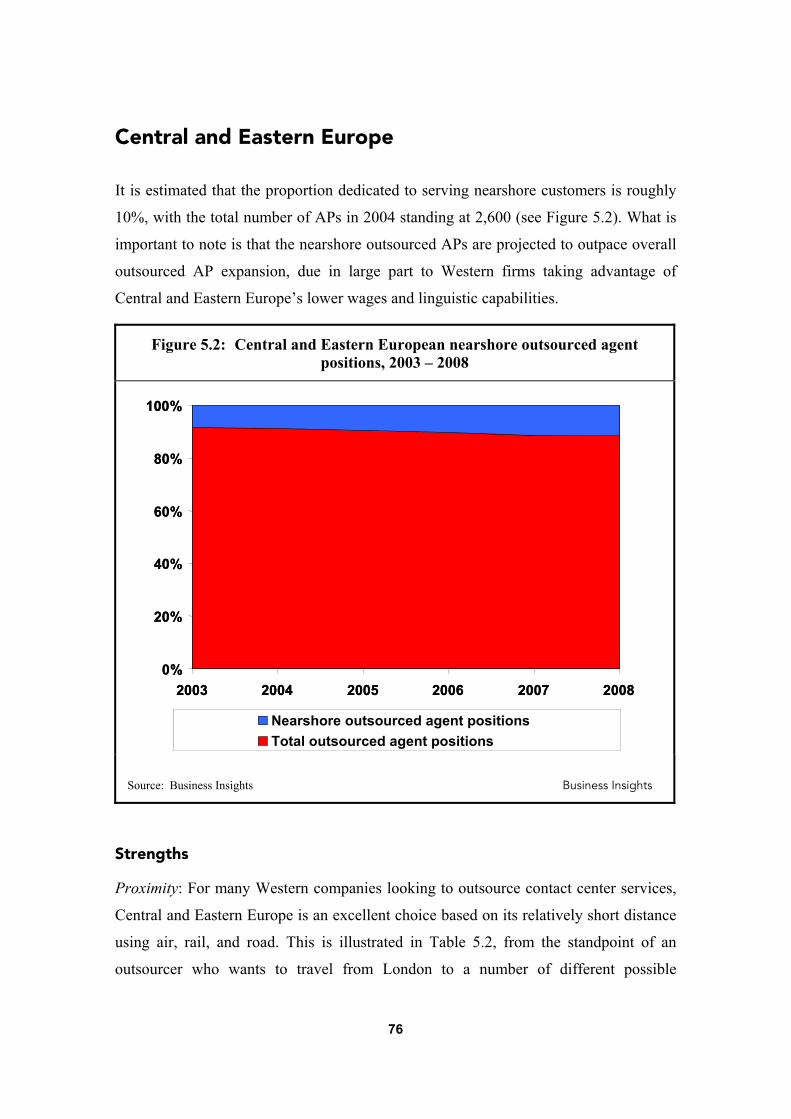

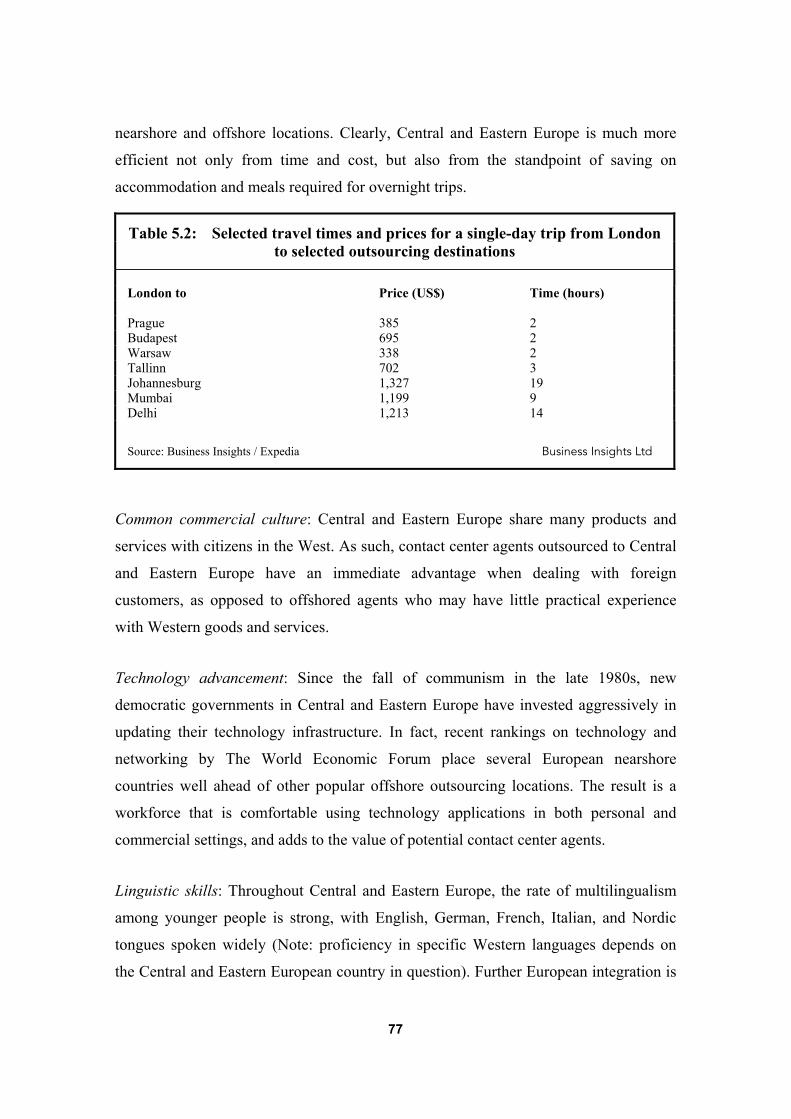

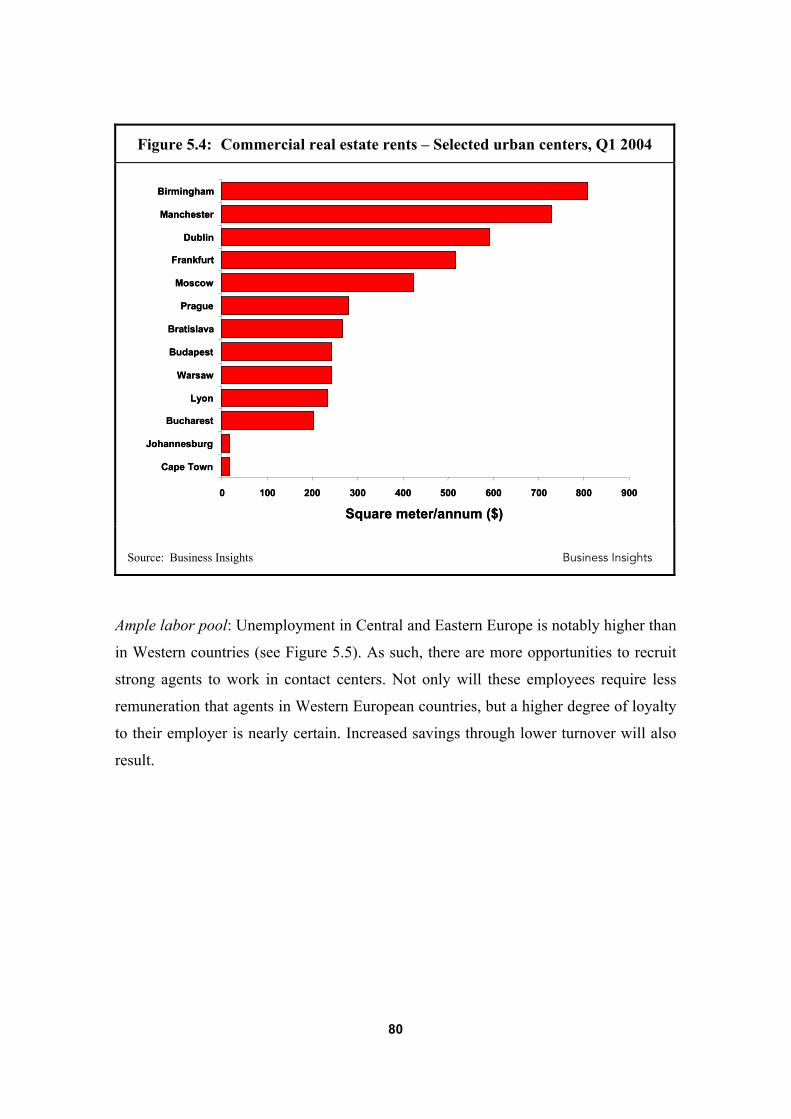

For many Western companies looking to outsource contact center services, Central

and Eastern Europe is an excellent choice based on its relatively short distance

using air, rail, and road.

In 2004, there were approximately 27,000 outsourced agent positions (APs) in

Central and Eastern Europe.

Throughout Central and Eastern Europe, the rate of multilingualism among younger

people is strong, with English, German, French, Italian, and Nordic tongues spoken

widely. Further European integration is certain to accelerate this trend.

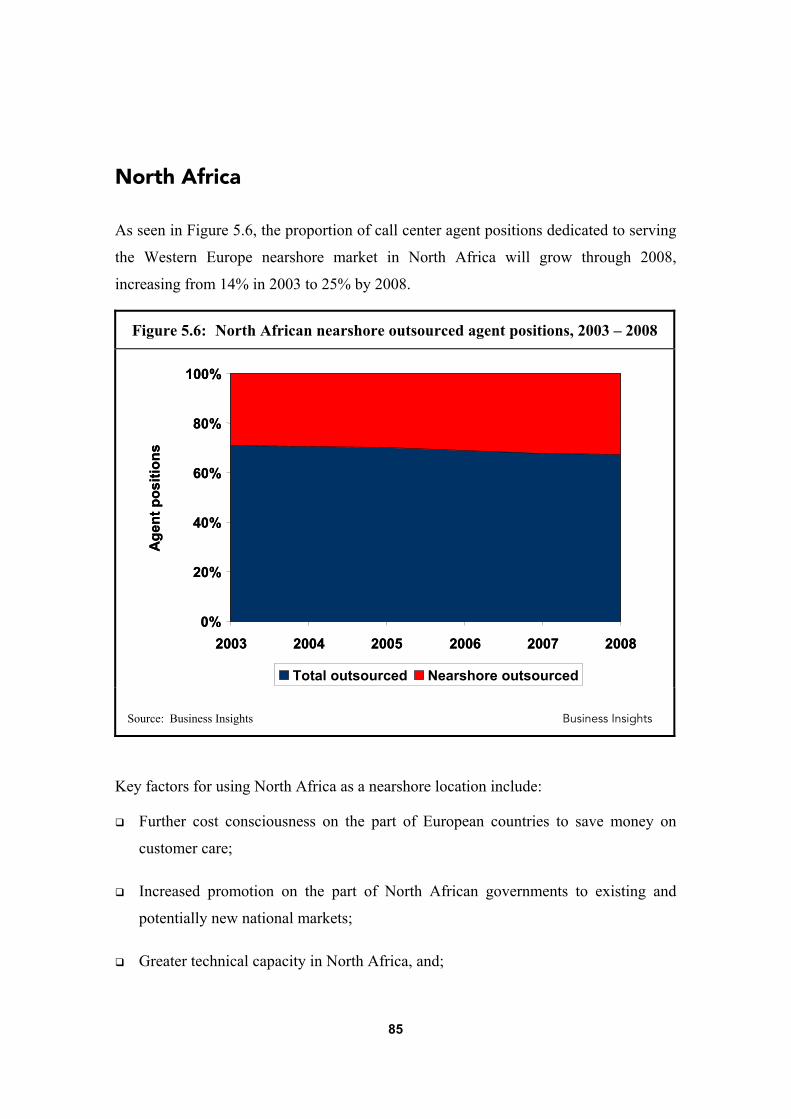

The proportion of call center agent positions dedicated to serving the Western

Europe nearshore market in North Africa will grow through 2008, increasing from

14% in 2003 to 25% by 2008.

Concerns abound within Central and Eastern Europe regarding the tightening

contact center agent market, which could result in higher wages, thus reducing the

advantageous margins that have been a key selling point for the region.

North Africa has effectively penetrated Europe’s French-speaking markets for

contact center outsourcing, and is its governments are now looking to other

countries to which it can offer customer care services. The main targets are the UK

and Spain.

Nearshore locations (for North America)

The main advantages of Canada as an outsourcing location are proximity to the US

and the quality of the Canadian agent.

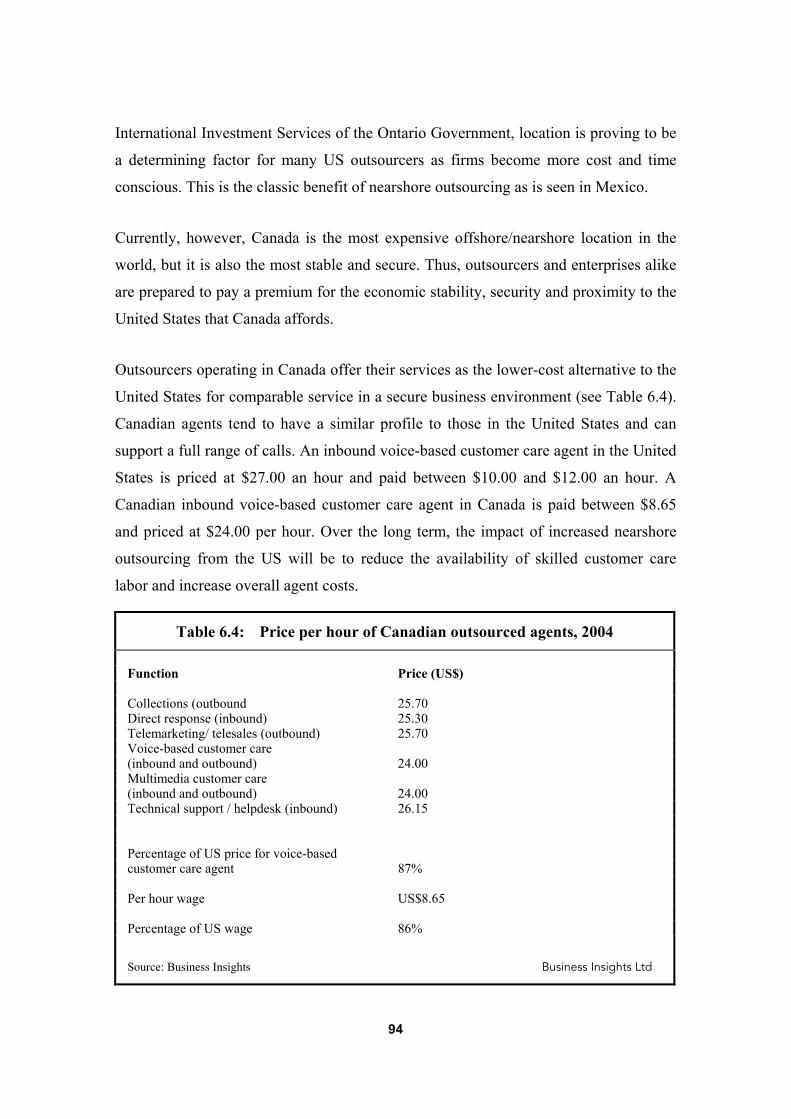

Outsourcers operating in Canada offer their services as the lower-cost alternative to

the United States for comparable service in a secure business environment.

While Canada is the most expensive offshore/nearshore location in the world, but it

is also the most stable and secure.

14

The Mexican call center market is the second largest in Latin America and is larger

than the Argentine, Chilean and Colombian combined.

Mexico offers substantial growth opportunities for equipment vendors, systems

integrators and domestic outsourcers alike.

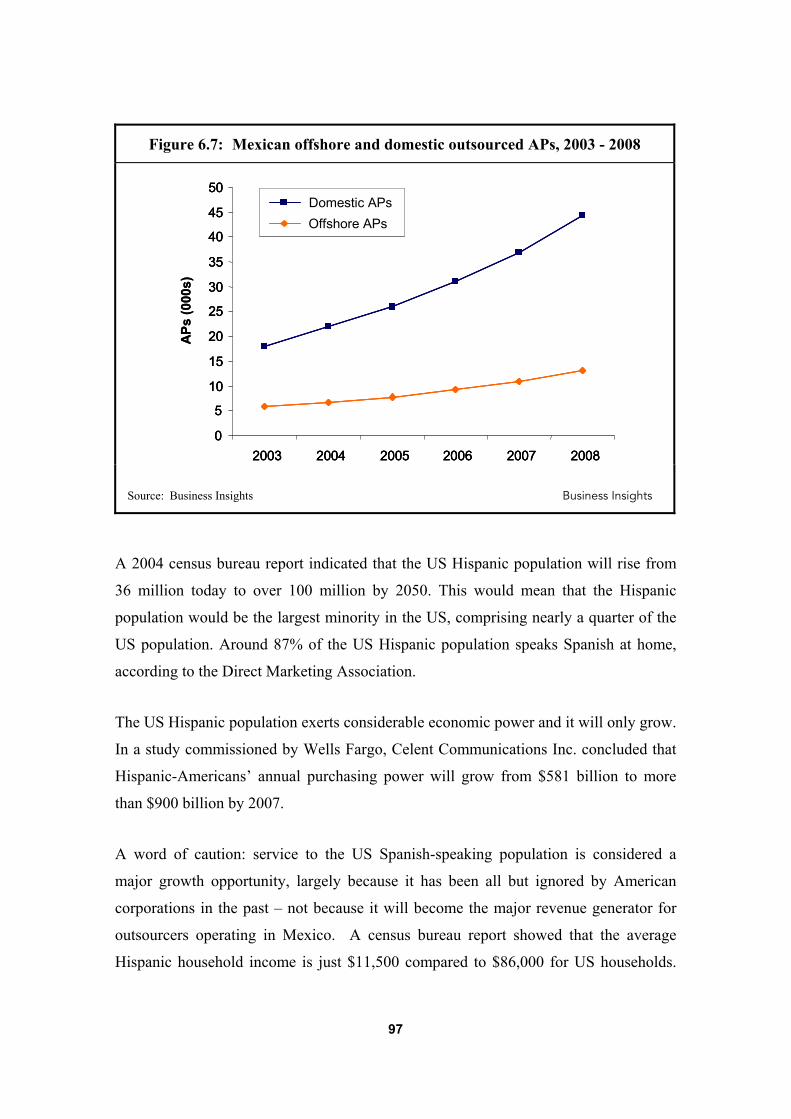

Mexican nearshore outsourcing will undergo substantial growth through 2008. By

2008, 23% or roughly 13,000 outsourced seats will be nearshore seats. This is

because Mexico has emerged as the most attractive location from which to serve

the US Hispanic population.

Jamaica’s call center market will continue to grow steadily, reaching 8,000 APs by

2008.

However, Jamaica’s small population places constraints on sustainable growth.

Focus on call center offshore outsourcing

India and the Philippines provided 70% of the world market offshore outsourced

APs in 2002; this will drop to 64% in a growing global offshore market by 2007.

South Africa is seen as a hidden gem of offshore call center outsourcing.

It can take up to 3 or 4 years before a new offshore market establishes a critical

mass of middle-management skill sets.

There is further growth in the offshore market for IP call center, shadow

infrastructure and remote-monitoring technology solutions.

Overall, demand is growing – strongly, but it is also starting to shift eastwards

away from the USA. With this shift come subtle differences in requirements.

Demand for offshore call center outsourcing is growing and shifting east to

countries across Europe and will also grow in the APAC region through 2007.

15

The financial services, technology and telecoms sectors are those most in demand

and best adapted to being outsourced offshore.

Cultural affinity of call center agents is more important than the accents they have.

Real-time monitoring and a supporting shadow infrastructure are needed to allay

clients’ fears about losing control of their customer interactions if they outsource

offshore.

Clients often do not fully understand their desired operating model, so SIs and

OSPs can assist them by undertaking business process reviews with them and

working out the blended solution of in-house and outsourced call centers.

16

17

CHAPTER 1

Offshore and nearshore outsourcing

18

Chapter 1 Offshore and nearshore outsourcing

Summary

The success of the offshore outsourcing model means that there are now over 10,000 vendors in more than 175 countries claiming to offer some form of offshore outsourcing service.

In terms of IT, the key driver remains largely focused on cost savings.

As the offshore model matures, other considerations such as quality of service and expertise, as well as knowledge of local markets knowledge, are further advantages of offshoring.

Nearshoring has become a viable solution for many companies because nearshore country locations offer the advantage of similar time zones, ease of travel and potentially greater control due to familiarity or physical and cultural proximity to the customer.

Introduction

The incredible success of the Indian offshore outsourcing market over the past five

years has proven that regardless of location, IT services providers can sell world-class

services to the biggest companies around the globe. As a result, there has been a boom

in offshore and nearshore outsourcing delivery models.

The offshore outsourcing market has experienced strong growth over recent years,

thanks to the cost advantages it offers. The market really took hold in the late 1990s

when global firms struggled to find enough engineers to staff Internet and Y2K projects

– the only requisite for an offshore vendor then was merely to have people!

19

When the technology market imploded in 2001, the offshore outsourcing market took

the opportunity to recreate itself as a genuine low-cost alternative to onshore resources.

Anticipating a change in the way outsourcing companies were used, offshore

outsourcing firms invested heavily in developing processes and gaining certifications,

so that when the market transitioned away from low resource cost models to a more

sophisticated project delivery model, they were positioned and ready.

As a result, offshore vendors have over recent years made significant progress in

delivering so-called global sourcing solutions using the optimal location for delivery of

each element of a contract. India, in particular, has come to define the term ‘offshore

outsourcing’ over the past decade. The aggressive leadership of several Indian

companies, such as Wipro, Infosys and Tata, has helped the global economy to adopt a

global fulfilment model for many IT functions and proved that the model can work.

As the solution offerings have been extended so too have the sizes of the addressable

market and the vendors in question. Today several of the Indian vendors have market

capitalization on par with most of their onshore competitors and are increasingly able

to benefit from the lessened perception of risk that they were in the past strongly

associated with.

20

Offshore outsourcing

Today, India is far from alone as an offshore outsourcing location. It is estimated that

there are more than 10,000 offshore outsourcing vendors offering some form of

outsourcing in over 175 countries as diverse as The Philippines, Eastern Europe, China,

South Africa, Latin America and The Caribbean.

Drivers and inhibitors

Key drivers for offshore outsourcing

Offshore outsourcing has been primarily driven by application management and, more

recently, contact center outsourcing, but is expanding to include business process

outsourcing (BPO) and customer relationship outsourcing. The market looks set to

continue its rapid growth as services mature and vendors explore opportunities in other

market segments and cost considerations remain key to IT strategy.

In terms of IT, the key driver, as previously mentioned, remains largely focused on cost

savings. During 2001 and 2002, IT budgets were slashed significantly, and the drivers

behind IT strategy made a clear shift away from effectiveness (e.g. revenue building,

IT and business strategy alignment) towards efficiency improvement (cost cutting and

improved cost efficiency of IT projects). This trend remained prevalent in 2003 as

organizations remained chiefly focused on maintaining efficiency, but some level of

balance has now returned as organizations are, once again, planning for the longer term

future.

The upturn in global markets, and improved company performance as a result, now

means that organizations are looking, once again, to offshore (and nearshore)

outsourcing to help drive renewed revenue building and IT / business alignment

strategies, in addition to cutting costs.

21

Another advantage of offshore outsourcing is the access it provides to industry

expertise, such as call center operations or application development, and local market

knowledge in a global economy, which would not otherwise be available to many

organizations – or at least at a reasonable cost. It is also a sign that offshore

outsourcing vendors are maturing, with providers from countries such as India and

Russia now able to compete on a par – and in some cases excel – against traditional

onshore business strategies.

Inhibitors of offshore outsourcing

Political backlash

There has been much political and media discussion in Western Europe and the US in

recent years, regarding the loss of ‘homeshore’ jobs to cheaper, offshore locations. One

notable example, being the apparent suicide of a programmer for Bank of America in

May 2003, who stepped out into the company’s car park, and shot himself having just

been made redundant, to be replaced by cheaper software programmers based offshore

in India.

Kevin Flanagan’s suicide triggered a torrent of bad press for the many US and UK-

based corporations that had been rushing to outsource their operations to countries

where labor and capital costs can be several magnitudes smaller than at home.

It also lit a spark under the anti-offshore movement, particularly in the US, where

Flanagan has become something of a martyr. This resulted in a growing number of

public protests, one of the first of which was held on 1 September 2003 at the BoA

Concord, California campus, where Flanagan died. In January 2004, 20 protestors

braved the New York winter to demonstrate outside an offshore business conference in

Manhattan. Despite the small number, the publicity created forced one speaker to bar

the press from his presentation entitled: “Is offshore outsourcing unpatriotic?”

Bad publicity, and public opinion, has already stopped a significant number of US

offshore deals in their tracks, particularly in the government sector. In November 2003,

public pressure forced Indiana's state government to cancel a $15m (£8m) IT contract

22

with Tata Consulting Services, after officials concluded it was inappropriate to use the

taxpayers’ money to pay foreign workers. This was followed by the New Jersey

department of human services, which for the same reasons relocated work sent to

Mumbai, India under a business process outsourcing contract with Arizona-based

company eFunds. The work is now being carried out from a call center in Camden,

New Jersey.

Indeed, public pressure has pushed the US Government into an increasingly anti-

offshore stance, culminating in George Bush signing a bill restricting, on 23 January

2004, which bans offshore outsourcing by certain Federal agencies.

In the UK the situation has so far been more subdued, but the anti-offshore movement

is gathering pace. Meanwhile, in France, the largest customer for North African

customer care outsourced services, political soundings about sending jobs offshore

have worried investors, who fear reprisals by the French government in retaliation for

sending jobs offshore. There is also concern that the French government may introduce

favourable tax incentives to keep these roles in France, which could affect North

African competitiveness.

The crux of the offshore outsourcing debate is the issue of job losses, and the related

effects on the home, or ‘onshore’, economy. Unfortunately, as with any complex

economic modelling, the truth of the matter is never clear. Indeed, in the US, where the

offshoring market is far more mature than in the UK, several government economic

research departments have admitted that they do not have the right data or resources to

measure and understand the true economic effects of offshoring.

There is a new, and perhaps more powerful reason to reconsider offshore strategies,

outside of the political and social issues, however. And it is to do with the quality of

service provided by offshore outsourcers; an issue that has come to increasing

prominence after a string of US and UK companies have started retracting their

offshore operations. And there is growing evidence that businesses are now beginning

23

to look not only at cost, but also at the broader holistic benefits and risks associated

with offshore outsourcing.

Engagement issues

Difficulty in communicating with the outsourcer is usually cited by organizations that

are considering offshore outsourcing as the most significant barrier or challenge.

Communication with for, example Indian vendors, is only in part a linguistic issue, and

in fact also a logistical and cultural hurdle. However, many offshore providers have

been aware of this challenge for some years, and have been taking steps to overcome it.

Many offshore providers will, depending on the project, now routinely have offices in

Western cities, in which their employees regularly spend months at a time, absorbing

the culture, and language, of Western organizations. Likewise, senior onshore

employees of the company that is outsourcing a project may spend time at the offshore

vendor building relationships, as well as bridges across the culture gap.

Lack of control is another commonly cited concern. Interestingly, this is a more

common issue amongst certain verticals than others, indicating a more conservative

attitude towards outsourcing and a greater historical focus on internal IT development

in some organizations or sectors, such as financial services, compared to others.

Organizations are also apprehensive about a possible lack of understanding of business

requirements on the part of the outsourcer, and that management personnel would need

to spend more time overseeing the vendor relationship. This is something that can be

linked to concerns over communication and the failure of vendors to establish business-

level credibility. Especially as offshore vendors aim to penetrate the business process

outsourcing (BPO) services market, it will become vital to demonstrate increased

business understanding and line of business focus.

The need for offshore outsourcing providers to have local operations within an

organization’s home market is seen as a minor concern amongst a minority of

organizations. But while this model of operation will continue to work in the

24

applications market, it is clear that for BPO services, for example, a closer and more

responsive relationship is required.

Other issues commonly cited include: security, quality of service, onshore employee

concerns, lack of customer support, lack of business driver and better onshore options.

In fact, it will be key for the outsourcing industry to tackle the issues and barriers to

offshore outsourcing over the next couple of years if long term demand is to be

sustained. As strategic IT drivers increasingly shift back towards growth enablement,

the outsourcing imperative will be driven increasingly by fulfilment excellence and

operational efficiency rather than straight cost considerations. Vendors must therefore

create a clear and robust communication structure with an element of onshore service

to match the nature of the services they are looking to provide.

Best practice

Client preparation and execution is one of the main causes of offshore outsourcing

failure. Both the outsourcing organization and the offshore provider need to perform

extensive preparation and planning, including setting high standards of benchmarks in

terms of performance and detail. Every detail should be recorded, reviewed and

planned. As a rule of thumb, the ‘outsourcee’ should be the one pushing this agenda,

rather than leaving it to the vendor.

Another leading cause of failure in offshore outsourcing engagements are problems

relating to the extent and quality of the client-vendor planning sessions prior to

commencing the engagement (21%). Often, offshore outsourcing vendors steamroll the

initial engagement process, trying to get signed contracts as fast as possible, and the

client does not demand clarity in roles, responsibilities, expectations, joint operations,

deliverables, short-term team plans, performance metrics, and so on. If these are not

clarified from the outset, it can lead to misperceptions and differences in expectations

between the two parties.

25

It may also be that the offshore outsourcing route is simply the “wrong answer” for a

specific business problem. This relates back to the commonly made mistake of viewing

outsourcing as a way to “wash your hands” of a particular IT problem or headache. It

may also be that there are better options, and that offshoring does not solve the root

problem.

There is also a significant issue with maintaining the support of the internal team

during an offshore outsourcing engagement. It is a fact offshore strategies are difficult

and will require employees to be active participants willing to help address issues as

the offshore strategy is implemented. Without in-house support successfully adopting

an offshore fulfilment model will be particularly challenging.

Competition between onshore and offshore teams is another problem, with onshore

teams keen to prove that they are still required by the organization. Organizations need

to take an active approach to mitigating this problem in order to avoid a dysfunctional

global team.

Finally, the reason for failure could fall squarely on the shoulders of the offshore

vendor, so choice of vendor and location should be one of the first considerations of

any organization tempted by the offshore outsourcing route.

Offshore outsourcing models

Long term business strategy and commitment will determine an appropriate business

model for offshore outsourcing, of which there are a number to consider:

Transactional partnering

This should be performed to “test the waters” or for isolated outsourcing. The work is

subcontracted on a project-only basis, and there should be low-level commitment to the

relationship from both parties. Essentially, this can be viewed as a “pilot”, but should

never be used as proof that the vendor can handle the work, as it may be that their best

26

people have been assigned to the project, or pilot, in order to secure a longer-term

working relationship and contract.

Tactical partnering

In essence, this reflects an offshore development center, and is major commitment from

both the organization and the offshore provider. The outsourcing enterprise “assures”

work for a dedicated number of resources for at least two to three years, including a

growth plan. The outsourcer would define the type of work it would outsource and the

skill levels that the provider should offer. Providers would supply dedicated facilities, a

dedicated communication link, and a dedicated offshore manager, responsible for

staffing and running the center, as well as training at its own cost and providing basic

infrastructure such as computers, telephone and fax. Both parties would work together

to build the “process manual” that would determine how the work would be done and

how the interfaces would work, and should establish service levels to be monitored

regularly.

Strategic partnering – a joint venture

A joint venture is more strategic in nature, with goals beyond opportunistic

outsourcing. The outsourcer establishes a presence in the geographic area where the

outsourcing work is to be performed. Goals may go beyond outsourcing to include

selling some of its own products or services in the geography. The service provider

may add value to further these interests of the outsourcer.

The outsourcer enterprise contributes to business knowledge whereas the provider

supplies local knowledge and local management skills. Both invest in the infrastructure

in the form of equity and establish common goals to be met. The biggest challenge to a

joint venture relates to the merging of two very different cultures.

27

Collaborative partnering – Build-Operate-Transfer (BOT)

Collaborative partnering takes the offshore development center a step further, whereby

the outsourcing company agrees to acquire the offshore center, its assets and its people

after a pre-determined period of time. The Build, Operate, Transfer (BOT) business

model allows a company to get comfortable with the location, with remote

development and also provides adequate time to structure an enterprise in the remote

location.

Wholly-owned subsidiary

Cadence, Microsoft, Intergraph, Motorola and Texas Instruments are all examples of

companies that have taken the wholly owned subsidiary route. The major challenge

here is knowing the local culture, laws and bureaucracy relating to business and

employment in the offshore location. Local managers should manage legal structuring,

human resources and government liaison; while expatriates or outsourcer managers

might be more suited to technical and operations management in the locale. A wholly

owned subsidiary will ramp up a lot slower and would also take a significant amount of

management time and attention. But once the creases have been ironed out, this has

potential to be the most rewarding structure.

Build or Buy?

Given some of the challenges of offshore outsourcing outlined above, many Western

organizations have preferred to build up their own offshore teams. However, this is a

decision that is frequently made as a knee-jerk, or ill thought out, reaction. This section

outlines some of the arguments “for” and “against” the Build versus Buy debate. First,

there are a number of different models that can be adopted within each camp.

28

Buy models

Offshore staff augmentation

The offshore staff augmentation model functions similar to onshore staff augmentation.

Here, onshore teams provide daily oversight of offshore resources. This model forces a

great deal of communication between onshore and offshore teams and requires a large

overhead in terms of resources and effort required.

Project outsourcing

In this model, the customer identifies a specific project needing completion and

prepares all necessary project-related materials. The customer then retains an offshore

vendor to deliver the project. At the completion of the project, the engagement ends. If

the project is likely to last more than three months, and there is no forecast beyond the

initial project, this is an appropriate model to choose.

Offshore dedicated center (ODC)

In the dedicated center, the vendor assigns a set number of resources to the client for an

ongoing series of projects. In this model, the client is responsible for a fully burdened

resource cost and will be responsible for downtime between projects. The upside to this

model is that for a series of related projects, it is possible to keep the same resources on

each project eliminating ramp-up time and costs. This is suited to projects with a long-

term forecast for a series of related projects.

Functional outsourcing

In this model, the vendor will outsource a complete function or application. While pay

models occasionally are structured on a time and materials basis, most functional

outsourcing engagements heavily leverage a risk-reward model. Also, these

engagements typically encourage the vendor to bring tools, methods, resources and

knowledge to the engagement in order to achieve a greater performing engagement.

With high-caliber offerings now being developed by outsourcing vendors around the

world, this model is now proving to generate the best possible value for customers.

29

When to buy?

Offshore resources

The best and brightest employees in the market want to work with the major local

vendors. Across India, Russia and other offshore hotspots, the top seasoned talent want

to work for the major local outsourcing providers – Wipro, Infosys and Tata in India

spring to mind – not Western multinationals. While it is possible to mitigate this, it is

an expensive, frustrating, and time-consuming process.

Value add

The best of the offshore outsourcing vendors invest millions of dollars every year in

order to develop new methodologies and intellectual property that help provide value

add for their customers. The alternative is to spend a large amount of money and

resources trying to catch up with this local and specialized expertise.

Performance

Offshore engagements that have used offshore vendors reach a positive ROI faster,

have a lower failure rate, generate a better ROI, and have the highest satisfaction rates.

Building an operation using in-house resources is likely to result in twice the cost than

working with a local vendor.

Cost

There is incredible overhead associated with managing remote teams. Offshore vendors

have two advantages: economy of scale – offshore vendors already have an

infrastructure built to facilitate management of various teams around the world and by

utilizing this built-in infrastructure, the cost is shared across all their accounts; catalysts

– offshore vendors have invested a large amount of time and money to solve the remote

team management issue. They are now leaders in this space and can manage remote

teams more cost-effectively than anyone else.

30

Build models

Do It Yourself (DIY)

Here the client develops everything from finding an offshore office, obtaining local

licenses and permits, hiring all employees and managing the daily activities of each

employee once the team is assembled. Of all the potential options, this can be the most

expensive and least successful with a success rate of less than 35% and average cost

exceeding $5 million.

Build Operate Transfer

In the Build-Operate-Transfer model organizations hire a local offshore outsourcing

vendor to completely build the offshore team. Once the offshore facility is up and

successfully running, the customer will then buy out the offshore facility under pre-

defined terms. This model is enjoying increasing success, due to the fact that it can

generate the best results of all the models outlined here. It is an incredibly low risk

model – if at the end of engagement, business needs change, organizations are not

stuck with a long-term offshore obligation. At the same time, depending on how the

contract is structured, organizations can simply hand the vendor the keys and walk

away without future liability. Statistically, this is also lower cost and higher performing

than DIY, as having a “local” firm that specializes in building outsourcing teams can

cut the cost and time required to generate a positive ROI by up to 30%.

M&A

As organizations emerge from the downturn and see a stability return to their financial

results, this is option is becoming more popular. This is a sound approach and buying

or merging with a mature offshore team can provide onshore companies with a fast

method for launching an offshore strategy. This option should be seriously considered

when an organization is in the offshore market to stay.

31

When to Build?

Building an “in-house” offshore strategy does have its advantages in specific situations.

Organizations should consider the following criteria when making the decision:

Do you have experience in both working in the selected country and in building

remote teams? If the answer is “yes”, consider the following criterion;

Honestly assess both the management team and the junior employees applying for

jobs. If it is not the “cream of the crop” for both groups, it may be wiser to follow

the “Buy” route.

Managing teams in multiple locations is a tough task. When building and running

an offshore team, organizations take on a sizable overhead simply trying to keep

multiple sites operational. If you do not have experience managing the activities of

two or more teams in multiple locations, do not attempt to build your offshore team

yourself.

Does building your own offshore team without the support from an offshore vendor

present a more cost compelling story when compared to using a vendor? It is rare

that an onshore firm can build an offshore team at a lower cost than a provider-

assisted option.

32

Nearshore outsourcing

As companies struggle to compete in today’s global economy, offshore outsourcing has

to other countries has emerged as a valid alternative in reducing the cost of business

operations. An increasing number of organizations – various surveys suggest around

one in four businesses – plan to use offshore outsourcing to perform vital business

functions, such as call centers, back-office operations, software development, business

process outsourcing and other strategic business operations, to stay competitive.

In recent years, offshoring has become the mantra for cost reduction. Despite all the

talk about security concerns including political instability, language and culture

barriers, legal difficulties and intellectual property rights protection among others,

companies continue to move large components of their business offshore. Although

offshoring received a lot of scrutiny and criticism in the early stages, it has proven to

be beneficial for companies that have embraced it. However, another cost-reducing

alternative – nearshoring – is also coming to the fore.

With nearshoring, organizations have the benefit of outsourcing operations offsite, but

in a way that is convenient — physically, culturally, managerially and financially — to

the overall business. A nearshore location is, essentially, one that is closer in terms of

geography, culture, time zone and language to an offshore location. So, for example,

US nearshore locations include Canada, Mexico and The Caribbean, while Western

European nearshore regions include Central and Eastern Europe and North Africa.

Other locations might include Cyprus for Israel, or China and India for Japanese

organizations.

Nearshoring has become a viable solution for many companies because nearshore

country locations offer the advantage of similar time zones, ease of travel and

potentially greater control due to familiarity or physical and cultural proximity to the

customer. While offshoring is still a very popular option with companies, organizations

33

that want to hedge their bets and curb the inherent risks of offshoring have an option

closer to home.

One of the main attractions of offshoring is the round-the-clock factor derived from

being in disparate time zones. The flip side of this is there is little to no opportunity for

businesses to work collaboratively with their offshore partner due to the time

difference. But the benefit of proximity, or nearshoring, is more than just working in

the same, or close, time zone. For small projects that require close interaction with the

company and its outsourcing partner, nearshoring more appropriate and less expensive

than the offshoring alternative. Furthermore, the complexity of managing security and

crisis issues is lessened with closer proximity. Another benefit of nearshoring

proximity is the ability to build trusted relationships with decreased risk of linguistic or

cultural misunderstandings. Predictability of service is another major factor in the

growing popularity of nearshoring.

At the same time, nearshore outsourcing can be seen as a complementary option for

offshore outsourcing, whereby organizations might outsource some aspects of business

operations to distant shores, outsourcing others nearer to home – i.e. nearshore –

dependent on the cultural, linguistic and physical requirements of a specific project.

The terms ‘best-shore’ or ‘right-shore’ have been coined to describe the use of a

combination of offshore and nearshore outsourcing in order for an organization to gain

the best possible combination of global sourcing requirements.

Nearshoring combines the best of both worlds offering cost-effective, off-site resource

deployment in relatively close geographical proximity to centers of business, thus

avoiding the logistical and empathic issues associated with, for example, the Indian and

Asian sub-continent.

Recently, there has been a trend to move non-critical back-off functions offshore, while

performing critical projects with nearshore resources due to the lower risks outlined

above. This model has proven to be successful for many companies because it allows

34

them to operate in a similar operating mode to which they have become accustomed to,

as the nearshore operation acts more like another office location than a separate entity.

Drivers and inhibitors to nearshore outsourcing

Drivers

While cost savings may not be as great as offshoring, having a nearshore partner run

essential business operations will nevertheless reduce costs. Of course, travel cost is

one way in which companies save, however, in most cases, the more significant area

for cost savings comes from infrastructure costs. At the same time, time zones are

likely to be much closer aligned than those of offshore locations, making collaboration

between tow locations easier. Of course, on the other hand, this offsets one of the

advantages of offshoring to a distant time zone, which can provide 24-hour business

cover.

Nearshore centers, like offshore facilities, upgrade their technologies in order to better

collaborate with their nearshore partner. There may be some nominal expense on the

part of the company to integrate with the nearshore facility, but the costs are generally

not as great. Furthermore, most nearshore partners tend to come with a more robust

technology offering than offshore partners, thus the need to purchase, enhance or build

is less than what may typically be true with an offshore partner.

Risks

There are far fewer risks of choosing nearshore versus offshore, but each model comes

with its own advantages and disadvantages. Of course, offshoring is cheaper than

onsite – but cost should not be the only criterion on which an outsourcing strategy is

built: Not only inexpensive labor, but also convenience; the ability to collaborate easily

and effectively; and manageable risk. Nearshoring allows businesses to manage

outsourced business operations with minimal risk. This does not mean, however, that

nearshoring is free of risks. Often the best solution is a combined model of onsite,

offshoring and nearshoring.

35

CHAPTER 2

Emerging models in offshore outsourcing

36

Chapter 2 Emerging models in offshore outsourcing

Summary

Long term business strategy and commitment will determine an appropriate business model for offshore outsourcing, of which there are a number to consider.

US companies are increasingly using locations such as The Philippines as a nearshore location, in preference to India, for cultural and linguistic reasons.

Central and Eastern Europe is emerging as a key region for nearshore outsourcing, as West European companies are drawn to its low costs, ample labor pool, and pro-commerce attitude.

The Build, Operate & Transfer (BOT) model is the lowest risk and can generate some of the biggest cost savings and performance improvements.

Of all the potential options for building an offshore team, ‘Do-IT-Yourself’ is the most expensive and least successful, with a success rate of less than 35% and average cost exceeding $5 million.

Introduction

As the offshore market matures, the range of business models increases accordingly.

While plotting out their crucial cost-cutting and value-enhancing measures, companies

often have to strike a balance between onshore and offshore labor – some core tasks

stay onshore, while other jobs, core or otherwise, go overseas. This section will explore

some of the emerging business models for both offshore and nearshore outsourcing.

37

Offshore outsourcing models

Long term business strategy and commitment will determine an appropriate business

model for offshore outsourcing, of which there are a number to consider.

Buy models

Offshore staff augmentation

The offshore staff augmentation model functions similar to onshore staff augmentation.

In this model, an onshore team will provide daily oversight of an offshore resource (or

team of resources). This model forces a great deal of communication between the

onshore and offshore teams and instances of positive ROI are difficult to come by when

factoring in the incredible overhead effort required.

Project outsourcing

In this model, the customer identifies a specific project needing completion and

prepares all necessary project-related materials. The customer then retains an offshore

vendor to deliver the project. At the completion of the project, the engagement ends.

For projects that are likely to last three months or more, or which do not have a

consistent forecast beyond the initial project, this is an appropriate model to choose.

Offshore Dedicated Center (ODC)

In the dedicated center, the vendor assigns a set number of resources to the client for an

ongoing series of projects. In this model, the client is responsible for a fully burdened

resource cost and will be responsible for downtime between projects. The upside to this

model is that if you have a series of related projects, you will keep the same resources

on each project eliminating the ramp time and will not end up paying for additional

team ramp costs. If you have a long-term forecasted need for a specific series of related

projects, it is strongly encouraged you explore an Offshore Dedicated Center model.

38

Functional outsourcing

In this model, the vendor will outsource a complete function or application. While pay

models occasionally are structured on a time and materials basis, most functional

outsourcing engagements heavily leverage a risk-reward model. Also, these

engagements typically encourage the vendor to bring tools, methods, resources and

knowledge to the engagement in order to achieve a greater performing engagement.

With the high-caliber offerings now being developed by outsourcing vendors around

the world, this model is now proving to generate the best possible value for customers.

Tactical partnering

In essence, this reflects an offshore development center, and is major commitment from

both the organization and the offshore provider. The outsourcing enterprise “assures”

work for a dedicated number of resources for at least two to three years, including a

growth plan. The outsourcer would define the type of work it would outsource and the

skill levels that the provider should offer. Providers would supply dedicated facilities, a

dedicated communication link, and a dedicated offshore manager, responsible for

staffing and running the center, as well as training at its own cost and providing basic

infrastructure such as computers, telephone and fax. Both parties would work together

to build the “process manual” that would determine how the work would be done and

how the interfaces would work, and should establish service levels to be monitored

regularly.

Strategic partnering – a joint venture

A joint venture is more strategic in nature, with goals beyond opportunistic

outsourcing. The outsourcer establishes a presence in the geographic area where the

outsourcing work is to be performed. Goals may go beyond outsourcing to include

selling some of its own products or services in the geography. The service provider

may add value to further these interests of the outsourcer.

The outsourcer enterprise contributes to business knowledge whereas the provider

supplies local knowledge and local management skills. Both invest in the infrastructure

39

in the form of equity and establish common goals to be met. The biggest challenge to a

joint venture relates to the merging of two very different cultures.

Build Models

Do It Yourself (DIY)

The Do It Yourself model is what it implies: You, the client, do everything from

finding an offshore office, obtaining all local licenses and permits, hiring all employees

and managing the daily activities of each employee once the team is assembled. Of all

the potential options for building an offshore team, this is proving to be the most

expensive and least successful with a success rate of less than 35% and average cost

exceeding $5 million.

Captive center

This is similar to the DIY model. Many large multinational organizations in the West,

especially those in the financial services industry for example, have been unwilling to

transfer the risk management aspects of offshoring to a local third-party provider, while

still wanting to take advantage of the labor arbitrage advantages of setting up in a

country such as India. If the offshored function is mission critical, either the risks are

considered too great or there is a lack of experience in the local providers for providing

such a service. As a result, many Western firms have set up ‘captive’ centers, whereby

control is maintained by that company, essentially as a subsidiary in a distant location.

While this model has clear advantages around risk management, it is one of the more

costly and time-consuming approaches and, as a result, is only within the grasp of the

largest organizations. There are also numerous examples of Western companies that

have tried this approach either withdrawing from the captive centers or selling them off

as businesses in their own right – for example General Electric’s Indian IT services arm

GECIS.

40

Build Operate Transfer (BOT)

In the Build-Operate-Transfer model the organization looking to offshore hires a local

outsourcing provider to completely build the offshore team. Once the offshore facility

is up and successfully running, the customer will then buy out the offshore facility

under pre-defined terms. Of all the build models, this generates some of the best

results. It is a low risk model. If, at the end of the ramp period of time, the offshoring

company needs change, it will not be stuck with a long-term offshore obligation, such

as a captive center, for example. Depending on how the contract is structured, the

offshoring organization can simply walk away without future liability. Statistically, this

model is also lower cost and higher performing than DIY. Having a firm that

specializes in building outsourcing teams to build an offshore team will cut the cost and

time required to generate a positive ROI by around 30%. This model is covered in

greater detail later in this chapter.

M&A

Becoming more fashionable, firms wanting to build an offshore team are turning to

Mergers and Acquisitions (M&A) strategies. This approach is sound and buying or

merging with a mature offshore team has given several onshore companies a

lightening-fast method for launching an offshore strategy. If organizations are going to

be in the offshore market to stay, the M&A approach is an extremely sound option and

should be seriously considered.

Wholly-owned subsidiary

Cadence, Microsoft, Intergraph, Motorola and Texas Instruments are all examples of

companies that have taken the wholly owned subsidiary route. The major challenge

here is knowing the local culture, laws and bureaucracy relating to business and

employment in the offshore location. Local managers should manage legal structuring,

human resources and government liaison; while expatriates or outsourcer managers

might be more suited to technical and operations management in the locale. A wholly

owned subsidiary will ramp up a lot slower and would also take a significant amount of

41

management time and attention. But once the creases have been ironed out, this has

potential to be the most rewarding structure.

Nearshore outsourcing models

Nearshore

Western Europe

The emergence of credible alternative sourcing locations to India will be key in

developing offshore outsourcing markets. As companies outsource increasingly core

applications and processes, being able to rely on a truly global sourcing framework will

act to hedge location- or event-specific risk.

Western European companies, in particular, will be prompted to action as more

nearshore alternatives to India, China and South Africa mature. For example, Eastern

Europe call centers are far better placed to provide customer-facing business process

outsourcing (BPO) services – a rapidly growing sector for outsourcing providers – to

many European companies than are the traditional offshore locations. Additionally,

such nearshore centers will to some extent be perceived to carry less operational risk

than, for example, centers in many parts of Asia.

In the near future, much of Europe will prefer to use nearshore resources to a far higher

degree than is currently the case, as cultural, language and regulatory barriers to

offshore will continue to prevent a full set of outsourcing services being provided from

any of the mature offshore locations.

Central and Eastern Europe is emerging as a key region for nearshore outsourcing, as

West European companies are drawn to its low costs, ample labor pool, and pro-

commerce attitude. However, drawbacks including varying levels of technology

infrastructure, a reputation for poor work standards and corruption are deterrents for

potential outsourcing investors. This section will outline the current state of nearshore

outsourcing in Central and Eastern Europe, and in North Africa – a key nearshore

42

location for France – and explore the key business issues surrounding the region from

the standpoint of contact center outsourcers.

North America

US companies, meanwhile, are increasingly using locations such as The Philippines as

a nearshore location, in preference to India, for cultural and linguistic reasons. The

Philippines school system is based on that of the US and its inhabitants are subject to

many of the same cultural influences, for example, TV shows. Combined with the

difficulty in understanding the India accent, American customers are more comfortable

with Filipino agents.

At the same time, the US has a burgeoning Hispanic population, so the use of Spanish-

speaking locations such as Mexico and to a lesser extent countries in Latin American

nearshore locations – ‘nearshore’ in relation to the US – is growing rapidly.

Canada offers lower cost, high-quality English-speaking agents to the US market.

Homeshoring

Call centers

While offshoring has recently proved popular with many major companies,

homeshoring provides a viable alternative by transferring jobs to cheaper locales while

simultaneously introducing efficient working practices. Therefore, reasonable salaries

can be paid while overheads are reduced.

Homeshoring, or homesourcing, in certain situations can boost productivity while

cutting costs. The practice also avoids the potential pitfall of sending such work

overseas, with the associated political issues, as well as the difficulties of matching

cultural and linguistic differences between locations, for example the US and India, and

managing risk.

43

For example, a company can transfer its operations out of a high-cost city locale to a

cheaper rural area or move jobs from conventional, physical facilities to lower-cost,

home-based operations.

It is estimated that there are already upwards of 100,000 home-based phone

representatives in the US. The benefit is that, compared to traditional outsourcing or

offshoring, companies utilizing home-based agents can access highly skilled

representatives that are closely attuned to the needs of the local market at a reasonable

cost.

At the same time, using home-based agents removes the need for paying more

expensive full-time agents to man call centers during times of limited call activity, or to

cover unsociable hours.

Challenges include data security risks, with home-based workers requiring the

appropriate levels of access to information, and alienation of home-based employees

from working practices and company culture.

However, homeshoring also gives employers access to home workers who might not

otherwise be available, such as disabled people and those with mobility problems. It

can reduce sickness time and costs, and avoid the impact of unforeseen circumstances

such as rail strikes and telephone outages.

Employers generally have two major concerns over homeshoring: how can they

guarantee cost efficiencies, and how can they ensure quality of work when managers

cannot stand over people to make sure they are being productive.

Software development

It is not just call center, or voice-centric, functions that can be performed from home.

Homeshoring software development, for example, provides access to quality

employees, while avoiding the risks of offshoring and the costs of onshoring.

44

In the US, for example, homeshoring development centers can be located away from

the higher rent, higher labor areas, providing significant cost savings.

Homeshoring providers build and use high speed, high productivity-producing

development technologies that support using lower cost resources around the country.

Again, agents understand the business, culture, and work ethics in that locale. The

model also requires minimal travel, labor, training and project management costs that

are often required in offshoring models.

It is estimated that homeshoring development strategies can deliver savings of between

30% and 60% below onshore development costs, while being cost competitive with

offshore or blended offshore/onshore companies.

Insourcing

‘Insourcing’ can be defined as offshore outsourcing by a foreign organization. In which

case, workers in first-world nations benefit from consultation jobs from other first-

world nations.

Why insource? The need for workers who are intimately familiar with the cultural

nuances of a particular market may drive foreign companies to establish a stronger

handhold on a target country. This would require them to recruit domestic workers who

will be able to further the interests of their business in the local setting.

Another term for insourcing appears to be inshoring, though this term has also gained a

lot of mileage. Some have applied this term to the act of importing foreign workers.

45

CHAPTER 3

The 10 most influential offshore service providers

46

Chapter 3 The 10 most influential offshore service providers

Summary

The mantra “Pick the Country First” is perhaps the most widely known and commonly used method for selecting an offshore vendor.

There is a growing trend in the market where buyers will use specific industry domain and technical skills as the entry criteria for a tender process.

IBM Global Services has 6,000 people working in India, and has plans to expand into China. The company only recently made its first acquisition in India in March 2004, paying $160m for India’s third largest BPO provider Daksh eServices, which employs 6,000 people across five facilities in India and a new location in the Philippines.

Infosys Technologies, the second largest Indian software services exporter, is leading the expansion of Indian companies outside their homeland into China, Eastern Europe, the Americas and Australia.

As one of the world’s largest suppliers of call center management services, Convergys has pioneered the use of an offshore delivery model in contact center management services, and is rapidly expanding its presence in India and the Philippines.

47

Vendor selection

One of the most hotly debated issues with offshore outsourcing is how to find the best

– or most suitable – vendor. There are many conflicting opinions, as outlined below:

Pick the Country First

The mantra “Pick the Country First” is perhaps the most widely known and commonly

used method for selecting an offshore vendor. In this model, the buyer uses some form

of a “scorecard” approach to select the country most appropriate for their purposes.

After selecting the country, the buyer then selects the vendor(s) most likely to be able

to handle their needs out of the top vendors from the selected country. When going

down this route, there are a number of issues to consider:

Does the country’s legal framework adequately protect your IP?;

Some countries offer greater financial exposure;

Some countries are less ‘stable’ then others; and

Some countries have been involved with outsourcing longer than others and this

experience translates into a higher probability for success.

Generally, however, this method results in a less than 50% success rate – although

there are instances where selecting the country(ies) first was a sound option specifically

when there are significant cultural, language or legal issues relating to a project.

Recommendation

Either formally or informally, a relatively large percentage of customers buy on the

advice of their peers and contacts. In this model, a buyer will poll their counterpart in

other business groups (or other companies) and will use the information gathered to

select the vendor. If the buyer merely hires the vendor with the best recommendation,

success rates are low. However, if the buyer uses a strong recommendation from peers

48

as the entry criteria in a tender process and thoroughly investigates each recommended

vendor aggressively, the success rate jumps significantly.

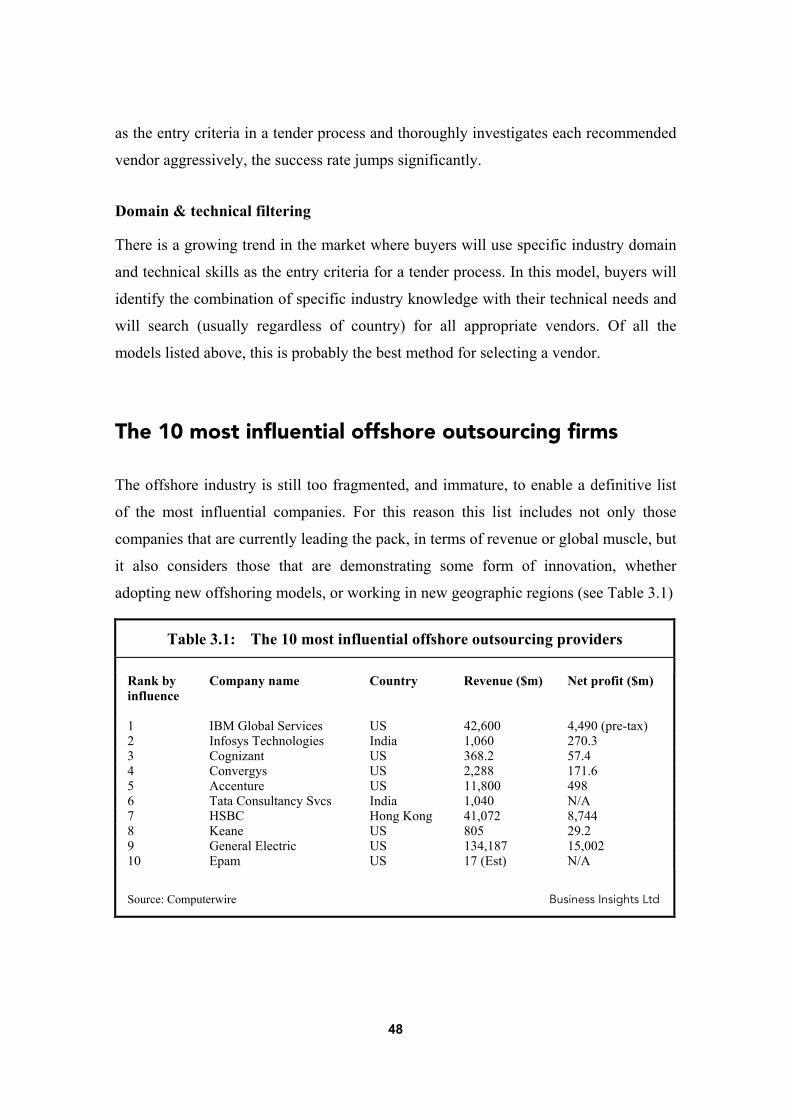

Domain & technical filtering

There is a growing trend in the market where buyers will use specific industry domain

and technical skills as the entry criteria for a tender process. In this model, buyers will

identify the combination of specific industry knowledge with their technical needs and

will search (usually regardless of country) for all appropriate vendors. Of all the

models listed above, this is probably the best method for selecting a vendor.

The 10 most influential offshore outsourcing firms

The offshore industry is still too fragmented, and immature, to enable a definitive list

of the most influential companies. For this reason this list includes not only those

companies that are currently leading the pack, in terms of revenue or global muscle, but

it also considers those that are demonstrating some form of innovation, whether

adopting new offshoring models, or working in new geographic regions (see Table 3.1)

Table 3.1: The 10 most influential offshore outsourcing providers Rank by Company name Country Revenue ($m) Net profit ($m) influence 1 IBM Global Services US 42,600 4,490 (pre-tax) 2 Infosys Technologies India 1,060 270.3 3 Cognizant US 368.2 57.4 4 Convergys US 2,288 171.6 5 Accenture US 11,800 498 6 Tata Consultancy Svcs India 1,040 N/A 7 HSBC Hong Kong 41,072 8,744 8 Keane US 805 29.2 9 General Electric US 134,187 15,002 10 Epam US 17 (Est) N/A

Source: Computerwire Business Insights Ltd

49

IBM Global Services

Despite IBM's mantra that it is a global company and does not do ‘offshore’, the

company’s increasing focus on low-cost locations such as India and China proves that

it is increasing its reliance on the offshore concept. IBM’s great strength is that its

distribution of global sales and development operations give it experience in a global

delivery model, and also enable it to rapidly adopt an offshore model.

IBM currently has 6,000 people working in India, but also has plans to expand into

China. The company made its first acquisition in India in March 2004, paying $160m

for India’s third largest BPO provider Daksh eServices, which employs 6,000 people

across five facilities in India and a new location in the Philippines.

The company provides call center outsourcing services around inbound and outbound

calls, email for customer service and fulfilment, chat services for customer care and

technical support, and back-office support services for transaction processing, which

covers research and analysis, claims processing, payroll, accounts and application

processing for 10 clients including Sprint, Citimortgage and Amazon.com.

Of course, many of IBM's rivals can claim similar abilities. Companies such as EDS,

CSC or Capgemini also have a global focus as well as owning facilities in low-cost

countries such as India and Latin America. But offshore outsourcing is not just about

being in the right location, it is about balancing services across different global regions

to enable quality and efficiency of delivery.

With the swift and overtly seamless integration of PricewaterhouseCoopers over the

past few years, IBM has proven itself capable of managing large cultural and

organizational shifts successfully. To bet against it doing the same with its offshore

strategy would be foolhardy. Combine this with the company's influence simply in IT,

let alone IT services or the offshore industry, and IBM earns a well-deserved first

place.

50

Infosys Technologies

Although the second largest Indian software services exporter, Infosys Technologies is

leading the expansion of Indian companies outside of their homeland into China,

Eastern Europe, the Americas and Australia.

Unlike many other Indian companies, Infosys is not only setting up glorified sales

offices but also making serious commitments to global development. In April 2004, the

company invested $20m to found a new US-based consulting unit called Infosys

Consulting, which will eventually employ 500 US-based workers and has been set up

with US-based employees from rivals including EDS Consulting, Capgemini and

Deloitte.

Its financial performance is nothing to sniff at either. The company grew revenue by

41% to $1.06bn in the year to March 2004, and expects sales to grow another 30%

over 2005.

Considering that the company's revenue was only $121m in 1999, and that its growth

has largely been organic, Infosys is a clear powerhouse in the industry.

Cognizant Technology Solutions

As a US-based company focused solely on delivering IT services from its Indian

operations, Cognizant is perhaps the most interesting offshore services company in the

industry at the moment. Its position as a Western company, with all decision-making

coming out of the US, gives it an edge over foreign firms when bidding for US

contracts. On the other hand its complete commitment to the offshore model gives it a

more competitive cost base than its local rivals.

Cognizant is in fact the industry’s fastest growing company, reporting net income up

66% at $57.4m on revenue that grew 60% to $368.2m for the full year ended December

31, 2003. The company has sustained revenue growth of between 20% and 50% since

1998, and the 2003 results prove that the company is now winning business

significantly faster than its rivals.

51

However, it is still far behind giants such as Wipro, Tata Consultancy Services, and

Infosys, all of which recorded revenues near $1bn. Nevertheless, with a market cap of

around $3bn, it clearly has investors' support.

Convergys

As one of the world's largest suppliers of call center management services, Convergys

has pioneered the use of an offshore delivery model in contact center management

services, and is rapidly expanding its presence in India and the Philippines.

Convergys opened the first US-owned contact center in India in December 2001, and

now plans to have seven centers in India by early 2004. It plans to employ 20,000 staff

in India by the end of 2005. It is also planning to increase its number of centers in the

Philippines from two to three next year.

Moreover, Convergys is an early mover in the human resources outsourcing space, for

which it recently acquired two companies in Singapore, which also give it offices in

Malaysia and Hong Kong.

Accenture

As one of the world’s most successful IT services and business process outsourcing

companies, Accenture has a similar edge as IBM in terms of its global scale and

experience in managing geographically distributed clients and projects.

Accenture’s significant services resources in every geographical area include 10,000

staff in Asia Pacific – a figure which will be doubled by the proposed addition of a

further 10,000 staff added to facilities in India. The size, scale and reach of Accenture,

combined with its increasing influence in the BPO sector means that it cannot be

discounted.

52

Tata Consultancy Services

India’s largest exporter of software and services is certainly a force to be reckoned

with. Employing over 25,000 staff, the Indian giant is planning to float on the Bombay

stock exchange soon, some say later this year. TCS has not yet decided on the issue

size, but it is expected to raise between INR 35bn and INR40bn ($800m-$913m)

through an IPO of about 10% of its equity, according to rumors.

The much-anticipated flotation would value TCS at as much as $9.1bn, making it

India's fourth-most-valuable company by market capitalization. Like its top-tier Indian

rivals, Wipro and Infosys, TCS is also spreading aggressively into other regions,

particularly China.

However, TCS' lead is that it has established itself as the largest, and most widely

known offshore service provider, and this position will only be reinforced by a

flotation.

Hong Kong and Shanghai Banking (HSBC)

The world's second largest bank, HSBC is one of the pioneers of the offshore software

development model among the banking industry, as a result of its historical presence in

the Far East and the Indian subcontinent.

By the end of 2003, HSBC was expecting to employ 8,000 people in India, China and

Malaysia in back-office processing and call center positions. Now the bank is actively

looking to sell services to other banking industry organizations within India and

globally. Given its large presence in Asia, and its experience and local knowledge,

HSBC could wield considerable influence in the offshore industry in the future.

Keane

The strategy of application outsourcing firm Keane reflects a new wave of North

American companies that are developing a mixture of 'nearshore' and offshore locations

to provide lower cost IT services and process outsourcing, with a similar risk profile to

53

those kept onshore. Keane has a nearshore location in Halifax, Canada, which it claims

is the first in the market to achieve SEI CMM Level 5 rating for the quality of its

software and services.

The company combines this with its 400-employee facility in India, which it gained