the Nuclear Fuel Market- Post Fukushima - Nomura€¦ · The Nuclear Fuel Market-Post Fukushima ......

38

The Nuclear Fuel Market- Post Fukushima R. Gene Clark, Chief Executive Nomura Asia Equity Forum 2011 Singapore June 14, 2011

Transcript of the Nuclear Fuel Market- Post Fukushima - Nomura€¦ · The Nuclear Fuel Market-Post Fukushima ......

The Nuclear Fuel Market-Post Fukushima

R. Gene Clark, Chief Executive

Nomura Asia Equity Forum 2011

Singapore

June 14, 2011

2

Uranium Processing

“Enriched UF6”

“Natural” UF6 (uranium hexafluoride)

U3O8 or Yellow Cake

Uranium has to be further

processed to become

nuclear fuel.

The enrichment stage has

variable economic

efficiency, creating a

substitution factor of

electricity for uranium.

Nuclear Fuel Costs At Spot Prices

This fuel cost still represents only a small part of total electricity cost and are

rolled into the generating cost over the course of several years

2002 2004 2006 June 2007 2008 2010 YTD 2011

0

2

4

6

8

10

12

14

16

18US$/MWh

Other

Enrichm ent

UF6 Conversion

U3O8 ©2011-TradeTech

4

Topics

Uranium Market

Enrichment Market

Overall Market Conclusions

5

* TradeTech’s NUEXCO Exchange Value through 2009; TradeTech’s weekly Spot Price Indicator for 2010-2011YTD

** TradeTech’s Long-Term Price Indicator for U3O8

Jan 2

004

Jan 2

005

Jan 2

006

Jan 2

007

Jan 2

008

Jan 2

009

01/0

1/10

03/1

2/10

05/2

8/10

07/3

1/10

10/0

8/10

12/1

7/10

02/2

8/11

$0

$20

$40

$60

$80

$100

$120

$140US$/Pound U3O8

Spot Price*

Long-Term Price**

2004-2009 By Month 2010+ By Week

©2011-TradeTech

Uranium Prices in 2010+

Average Spot Price for

2010 is $46.71

Long-Term Price began to

climb after summer 2010, but in

light of Fukushima the price

has fallen slightly.

Spot Prices climbed significantly in the

second half of 2010, but began gradually

declining in January and dropped

significantly after the Fukushima

incident.

6

Uranium Market

Recent Developments Impacting Price

Uranium Demand Outlook

Uranium Supply Outlook

Price Outlook

Recent Developments…

2010 had the largest spot volume in history

of market; third year in a row of high volume

Uranium prices were low in 2009 and mid-

2010, but recovered later in 2010 through the

beginning of the year 2011

Excess US Government uranium stocks still

overhang the market, with announcements of

continued sales

7

…Recent Developments(post-Fukushima)

Incident at Fukushima Daiichi plant following earthquake/tsunami on March 11th

Germany announces immediate shut down of 7 older nuclear units and reevaluation of future plans to extend the lives of operating nuclear plants

China announces reassessment of safety standards for all future licensing of plants

8

9

How Does The Uranium Market Work?

Has been described as a very immature

“horse-trading” market, and is definitely a

boutique market

Market reporters like TradeTech publish

price indicators

No open exchange like LME

10

Primary and Secondary Supplie(r)s

Secondary supply is very large (40%)

A few producers control primary supply

0

10

20

30

40

50

Thousand tU

0

20

40

60

80

100

120

140

Million Pounds U3O8

Cameco

Kazatomprom

Rio TInto

AREVA

ARMZ

BHP BillitonNavoi

Other

Pu, U Recycling

Russian Stocks

Enrichment Tails StrippingU.S. DOE/USEC Stocks

US HEU

Russian Nuclear Weapons

Primary Supply Secondary Supply

Uranium One

Paladin

11

Current Uranium Supply Sources and Markets

Primary

Supply

= 69%

Secondary

Supply= 31%

Spot

Market= 13%

Longer-Term

Market

= 87%

6% 7%

63% 24%

Year

2010

Uranium Spot Volume By Buyer Type

12

2004 2005 2006 2007 2008 2009 2010 2011 YTD

0

10

20

30

40

50Million Pounds U3O8

Utility

Trader

Producer

Processor

Investor ©2011-TradeTech

Investors now have a major presence

and influence in the spot uranium market!

Physical traders have been

market players since the

mid-1980s.

Rising uranium prices

attracted a new class of spot

market participant: Financials

(physical investor/speculator).

1st Investor Activity

in 2004

Spot Volume By Buyer/Seller Type

13

Buyer Seller Buyer Seller Buyer Seller Buyer Seller0

10

20

30

40

50Million Pounds U3O8

Utility

Trader

Producer

Processor

Investor©2011-TradeTech

2008

2009

2010

2011 YTD

Investors still have a major presence, but the

financial crisis has lessened their buying interest/ability.

Investor/speculators

were net sellers in

2008, for the first

time.

14

Uranium Market

Developments in 2009 Impacting Price

Uranium Demand Outlook

Uranium Supply Outlook

Price Range Forecast

Nuclear Power Worldwide

Nuclear Power Units*

s

439 Operating

62 Under Construction

~150 Planned

~320 Proposed

Large existing base + growth from nuclear renaissance

Nuclear energy is a growth industry

15

*WNA April 2011 data

China MainlandIndia

KoreaJapan

RussiaUSA

FranceTaiwanCanada

IranUkraine

United Arab EmiratesSouth Africa

FinlandItaly

ArgentinaBrazil

Czech RepublicNetherlands

BelarusBulgaria

IndonesiaRomaniaSweden

PakistanSlovakia

LithuaniaMexico

BelgiumHungarySlovenia

SwitzerlandArmenia

SpainUK

Germany

0 10 20 30 40 50-10

*GW e To Be Added From 2008-2020

Nuclear Capacity GrowthWorld Nuclear Association Reference Case

Largest regional growth area: Asia

China’s growth

exceeds that of the

next highest 4

combined!

Following

Fukushima

accident Germany

likely to cancel

nuclear, UK?

16

17

Uranium Market

Developments in 2009 Impacting Price

Uranium Demand Outlook

Uranium Supply Outlook

Price Range Forecast

Current and Projected Uranium by Country

18

KazakhstanAustralia

CanadaRussia

NamibiaNigerUSA

South AfricaUzbekistan

ChinaMongolia

IndiaRomaniaUkraineMalawi

BrazilSpain

ArgentinaPakistan

Czech RepFrance

0 5 10 15 20 25 30 35

Thousand tU

0 10 20 30 40 50 60 70 80 90

Million Pounds U3O8

2010 Historical

2020 Potential

©2011-TradeTech

2010+ Uranium Supply Developments

Kazakhstan continues growth as new #1 producer

Paladin Energy initiates production in Malawi

BHP Billiton accident at Olympic Dam

ERA announces extension of shut-down at Ranger operations in northern Australia

McClean Lake Mill shut down in June 2010, due to lack of ore to process

Cameco continues remediation at Cigar Lake

Pace of exploration slows significantly

19

20

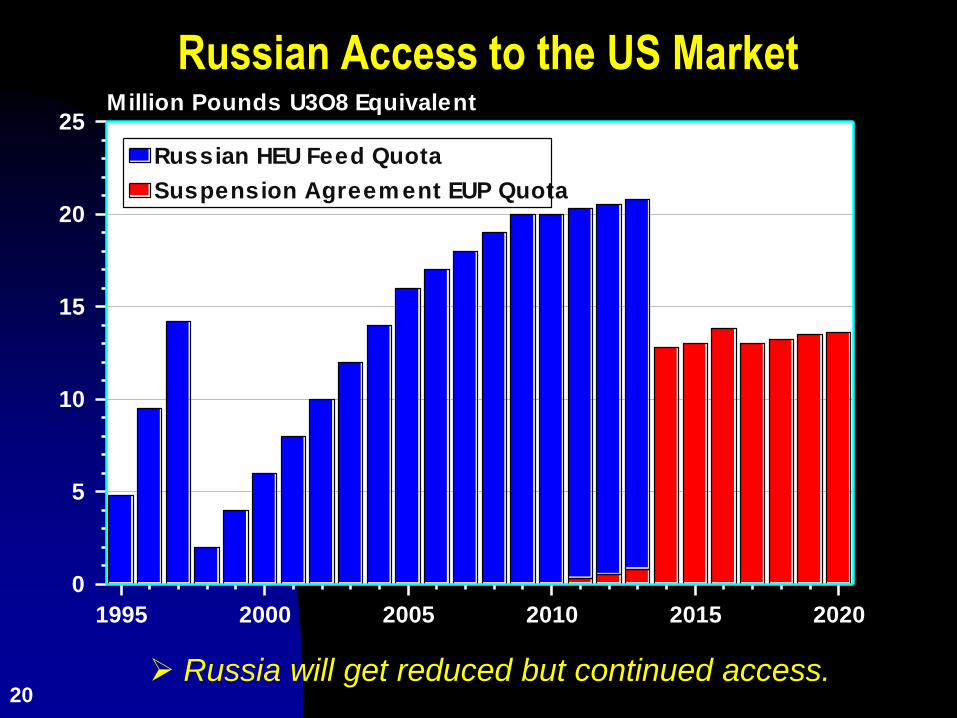

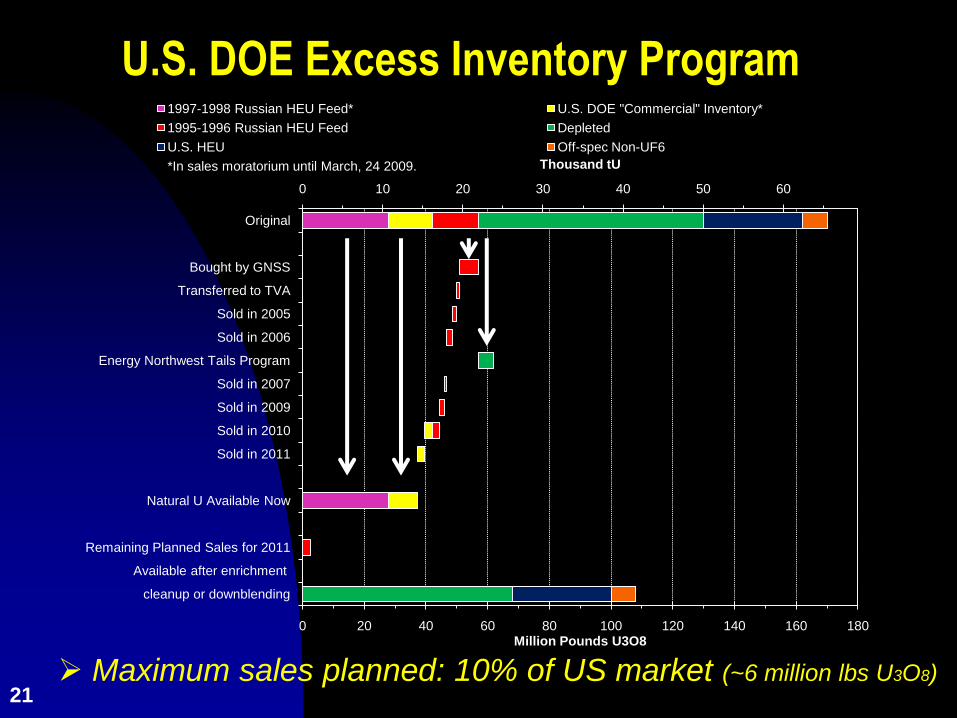

Russian Access to the US Market

Russia will get reduced but continued access.

1995 2000 2005 2010 2015 2020

0

5

10

15

20

25Million Pounds U3O8 Equivalent

Suspension Agreem ent EUP Quota

Russian HEU Feed Quota

0 10 20 30 40 50 60

0 20 40 60 80 100 120 140 160 180

cleanup or downblending

Available after enrichment

Remaining Planned Sales for 2011

Natural U Available Now

Sold in 2011

Sold in 2010

Sold in 2009

Sold in 2007

Energy Northwest Tails Program

Sold in 2006

Sold in 2005

Transferred to TVA

Bought by GNSS

Original

Thousand tU

Million Pounds U3O8

1997-1998 Russian HEU Feed* U.S. DOE "Commercial" Inventory*

1995-1996 Russian HEU Feed Depleted

U.S. HEU Off-spec Non-UF6

*In sales moratorium until March, 24 2009.

U.S. DOE Excess Inventory Program

21 Maximum sales planned: 10% of US market (~6 million lbs U3O8)

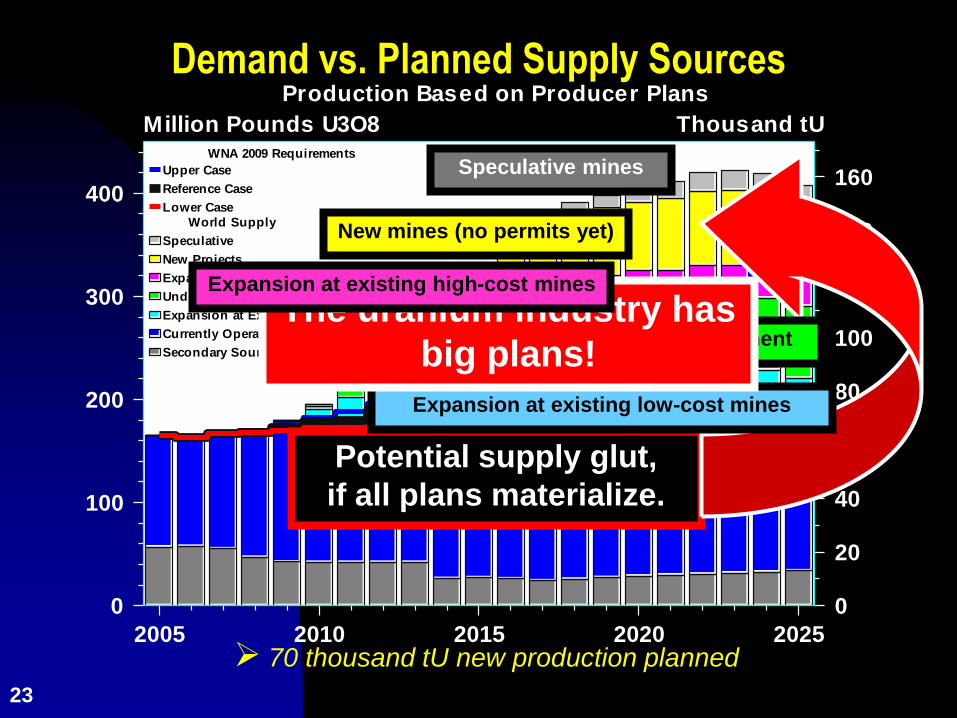

2005 2010 2015 2020 2025

0

100

200

300

400

Million Pounds U3O8

0

20

40

60

80

100

120

140

160

Thousand tU

WNA 2009 Requirem ents

Secondary Sources

Currently Operating

Low er Case World Supply

Reference Case

Upper Case

Demand vs. Existing Supply Sources

40-80 million pounds U3O8 new production needed

(Reference Demand Case)

Production from new sources

needed, especially starting in 2014

Supply from “secondary” sources.

Supply from currently producing

“primary” U3O8 mines.

The world needs new

uranium mines!

22

2005 2010 2015 2020 2025

0

100

200

300

400

Million Pounds U3O8

0

20

40

60

80

100

120

140

160

Thousand tUWNA 2009 Requirements

Secondary Sources

Currently Operating

Expansion at Existing Low-Cost Facilities

Under Active Development

Expansion at Existing High-Cost Facilities

New Projects

Speculative

Lower Case

World Supply

Reference Case

Upper Case

Production Based on Producer Plans

Demand vs. Planned Supply Sources

70 thousand tU new production planned

Potential supply glut,

if all plans materialize.

Expansion at existing low-cost mines

Under active developmentThe uranium industry has

big plans!

Expansion at existing high-cost mines

New mines (no permits yet)

Speculative mines

23

2005 2010 2015 2020 2025

0

100

200

300

400

Million Pounds U3O8

0

20

40

60

80

100

120

140

160

Thousand tUWNA 2009 Requirements

Secondary Sources

Currently Operating

Expansion at Existing Low-Cost Facilities

Under Active Development

Expansion at Existing High-Cost Facilities

New Projects

Speculative

Lower Case

World Supply

Reference Case

Upper Case

Demand vs. Deferred Supply Sources

Looming supply tightness,

especially in 2014-2017

Uranium supply will be

driven by price evolution

and financing availability!

Assuming several more

years of credit crunch and

depressed prices …

24

25

World Uranium Ore Quality

Source: CRU Strategies New uranium sources will be increasingly costly to produce.

26

The Major Current Suppliers

Kazatomprom: Kazakh government company

Cameco: Canadian company traded as CCO.TO

AREVA: French conglomerate 4% publicly traded

on NYSE Euronext

Rio Tinto (Energy Resources of Australian-ASX:

ERA)

ARMZ: Russian government company

Uranium One: Traded as UUU.TO on TSX

Navoi: Uzbek government company

BHP Billiton: Major mining company

Paladin: Traded as PDN on ASX

27

Uranium Market

Developments in 2010 Impacting Price

Uranium Demand Outlook

Uranium Supply Outlook

Price Range Forecast

Spot Price vs. Demand & Supply

28

Jan 04 Jan 05 Jan 06 Jan 07 Jan 08 Jan 09 Jan 10 Jan 11

0

5

10

15

0

50

100

150

Actual Spot Price*

Active Supply

Active Demand

Million Pounds U3 O8 U.S. Dollars per Pound U3O8

* TradeTech’s NUEXCO Exchange Value

©2011-TradeTech

Contrary to popular

belief, the uranium spot

market price DOES reflect

fundamental supply and

demand.

Jan 04Jan 05Jan 06Jan 07Jan 08Jan 09Jan 10Jan 11Jan 12Jan 13

0

5

10

Million Pounds U3O8

0

20

40

60

80

100

120

140U.S. Dollars per Pound U3O8

Actual Price

Actual Activ e Supply

Proj ected Activ e Supply

Activ e Demand

Proj ected Demand

©2011-TradeTech

Projected Spot Market

29

Recovery of spot price depends

on duration/extent of the credit

crunch and drawdown of utility

inventories

Assuming moderate supply and

demand for the next few years…

With continued moderate interest/ability

in the investor segment (low demand),

price could stay in the range of $40-60

for several years.

Uranium prices could recover faster,

with any combination of rekindled buyer

interest in the investor segment, utilities

buying for inventory, or producer

purchases due to production problems:

prices could then rebound to above $80

by early 2011

Conclusions

2009 -- the halt of the fall in spot prices, but downward pressure continued on the long-term price.

Uranium still not traded on an open exchange, in spite of efforts in the past few years

Next 2 years -- prices to stay in the $40-60 range (spot) and maybe $55-70 (long-term), unless a major supply event occurs

Growth in world nuclear power usage projected (especially Asia), with two major non-production supplies ending

Expansion of uranium enrichment capacity will tend to dampen demand growth for uranium, as enrichment substitutes for uranium on the margin.

30

31

Enrichment Market

32

Messages

The supply industry is in a technology transition

The USA is the enrichment battleground

Russia is the “500-pound gorilla”

Trade restrictions continue to distort the market

Centrifuge technology will dictate uranium

consumption

There may be “life after death” for old diffusion

33

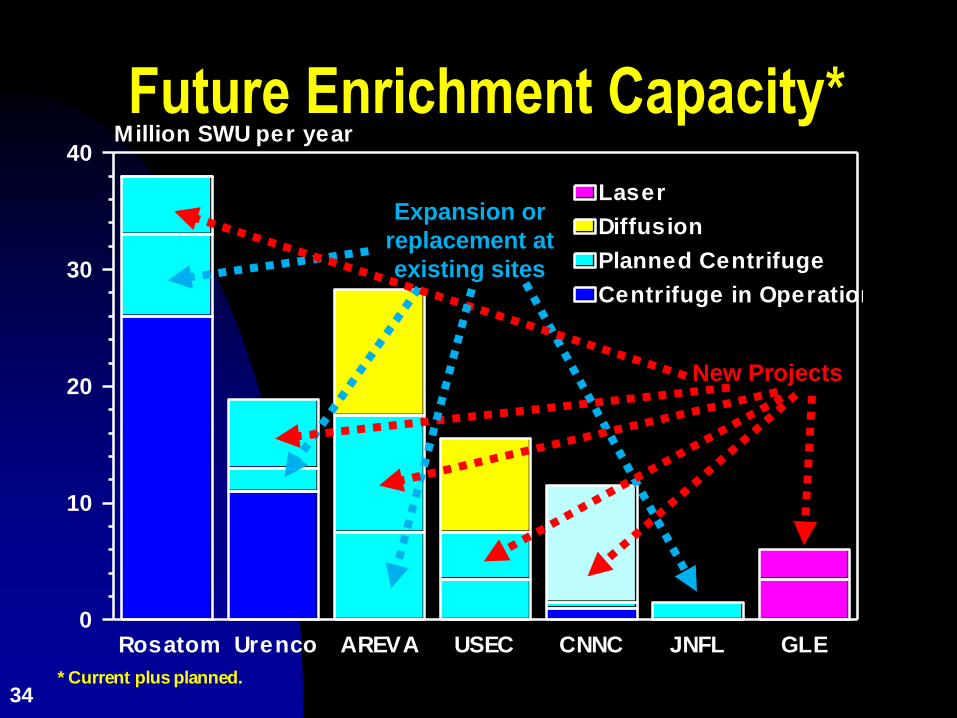

The Major Suppliers

Rosatom: The Russian nuclear conglomerate;

output marketed by Techsnabexport

AREVA: The French nuclear conglomerate; 4%

publicly traded on NYSE Euronext

Urenco: German/Netherlands/UK joint venture

USEC Inc: U.S. company publicly traded as

NYSE:USU

CNNC: Chinese nuclear company; some output

marketed by CNEIC

* Current plus planned.

Rosatom Urenco AREVA USEC CNNC JNFL GLE0

10

20

30

40Million SWU per year

Centrifuge in Operation

Planned Centrifuge

Diffusion

Laser

34

Future Enrichment Capacity*

Expansion or

replacement at

existing sites

New Projects

* Current plus planned.

Rosatom Urenco AREVA USEC CNNC JNFL GLE0

10

20

30

40Million SWU per year

Centrifuge in Operation

Planned Centrifuge

Diffusion

Laser

35

USA: The Battle Ground

Enrichment Import

Restrictions & The

Weakening Dollar

Foster Building

In The USA

36

Enrichment Implications All the major suppliers will be on the centrifuge technology by

the middle of the next decade, but the old gas diffusion plants might still have some useful life.

Once centrifuge manufacture becomes routine and the cost matures, there is “no stopping” the continual installation of centrifuge capacity; the installation rate is merely a function of the size of the centrifuge manufacturing capacity

Production costs (and thus possibly prices) could then stabilize or drop, given the centrifuge technology’s low operating costs.

But, maybe enrichment and uranium pricing will become locked in a competitive environment, if the relationship between the two becomes more transparent to the markets. Enrichment may serve as a long-term cap on uranium prices.

Trade restrictions against Russia will continue to result in a sub-optimal, economically-inefficient nuclear fuel market for the foreseeable future.

37

Overall Markets: Potential Surprises Cigar Lake uranium deposit may be delayed well into

the decade.

Olympic Dam expansion may not occur within a 10-year time.

GE’s SILEX enrichment system may rush to the forefront.

The USA may decide to process enrichment tails material, for sale into the market.

The USA may decide to release much more military stockpile into the market.

A lingering Fukushima crisis could slow the expansion of nuclear power in many regions

Russia could become integrated into the world fuel markets without restrictions.

38

R. Gene ClarkPresident

TradeTech Energy1289 North Fordham Blvd., Suite 202

Chapel Hill, North Carolina 27514 USA+1(919)933-7388 (office)

+1(919)933-6423 (fax)