THE MINSKY MOMENT redigeret 09092013 -...

25

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013 1 THE MINSKY MOMENT - Comparing Minsky to mainstream explanations of the financial crisis - Arvid Aagaard Jensen BSc Thesis Supervisor: Peter Erling Nielsen Institute of Economics University of Copenhagen Spring 2013

Transcript of THE MINSKY MOMENT redigeret 09092013 -...

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

1

THE MINSKY MOMENT - Comparing Minsky to mainstream explanations of the financial crisis -

Arvid Aagaard Jensen

BSc Thesis

Supervisor: Peter Erling Nielsen

Institute of Economics

University of Copenhagen

Spring 2013

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

2

RESUMÈ The purpose of the thesis is to investigate the prevalent mainstream explanations

for the financial crisis and how the work of the late Hyman Minsky(1919-1996) might

contribute with new angles from a contemporary point of view. In this regard, the report

contains an analysis of how the economists Paul Krugman and Gauti Eggertsson make use of

Minsky in the economic model they offer in their 2012 paper Debt, Deleveraging and the

Liquidity Trap and the policy recommendations their findings entail.

The basic question that the thesis poses is: how did the financial crisis of 2008

come to pass? With reference to a wide array of economists and institutional reports the

prevalent mainstream explanations are summarized in 10 points. 1. Credit boom due to low

interest rates. 2. Financial regulation had been too lax. 3. Housing policies had set wrong

incentives 4. Rating agencies had misled investors. 5. Banking sector had failed in its risk

setting. 6. Borrowers had taken on too much debt. 7. Widespread use of complex and obscure

financial instruments. 8. Increased interconnectedness among financial markets, nationally

and internationally. 9. High degree of leverage of financial institutions. 10. Central role of the

household sector. The key finding of the thesis in this regard, is that these explanations are

exogenous in nature and offer only diminutive systemic reasons for the crisis.

As a contrast to this, the Financial Instability Hypothesis of Hyman Minsky

offers an endogenous explanation rooted in the irrationality of financial players. He asserts

that the recurring phenomenon of financial breakdowns in the western economies arise from a

cyclical market failure propelled by incitements inherent in the very institutions of the

financial sector. Minsky emphasizes the role of debt creation in the financial sector, due to

financial innovation and its impact on aggregate demand.

In it its final part, the thesis analyses how Paul Krugman and Gauti Eggertsson

attempt to integrate Minsky’s more general findings concerning sudden deleveraging in the

financial sector in relation to the relevant problem of liquidity traps. This is done by altering

the well known New Keynesian model framework, focusing particularly on how debt

allocation in the financial sector influences aggregate demand and plays a key role in creating

financial crises. Their findings sheds light on the seemingly unorthodox macroeconomic

mechanisms, as well as the paradoxes of thrift, toil and flexibility, which follows after an

exogenously imposed sudden deleveraging. The policy recommendations that are offered

focuses on the need to revive debt financed government expenditure as a tool to alleviate a

depressed economy pressed up against the zero lower bound of a liquidity trap.

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

3

THE MINSKY MOMENT - Comparing Minsky to mainstream explanations of the financial crisis -

INTRODUCTION

How did the financial crisis of 2008 come to pass? The prevalent explanations assign the

causes of the crisis primarily to exogenous factors such bad monetary policy and deregulation

of the financial markets during the 90’s. However, the aftermath of the financial crisis has

brought to light an explanation that pin points the causes in the endogenous workings of the

financial institutions as such. In his work, the economist Hyman Minsky (1919 – 1996)1

outlined his Financial Instability Hypothesis, in which he asserted that the recurring

phenomenon of financial breakdowns in the western economies arise from a cyclical market

failure propelled by incitements inherent in the very institutions of the financial sector.

As most Post-Keynesian theory, Minsky’s work has to a large degree remained

marginalized and unknown to most economists. Recently this has changed however, as highly

profiled economists have sought to introduce Minsky’s ideas in a conventional framework.

This reformist approach we find in the recent work of Paul Krugman and Gauti Eggertsson

where they attempt to integrate Minsky’s key insights on debt deflation in a well known New

Keynesian model, focusing particularly on how debt allocation in the financial sector

influences aggregate demand and plays a key role in creating financial crises.

The main aim of this paper is to investigate the prevalent mainstream

explanations for the financial crisis and investigate why Minsky’s work might contribute with

new angles. Furthermore, the report will analyze how Krugman and Eggertsson make use of

him in their economic modeling and the policy recommendations this entails.

LITTERATURE

In portraying the mainstream explanations of the crisis I have examined various

works of esteemed mainstream economists such as Ben Bernanke, Kenneth Rogoff and Alan

Greenspan as well as official commission reports such as the Financial Inquiry Report headed

by Phil Angelides on behalf of president Obama and the report, Wall Street and The Financial

Collapse, worked out by Carl Levin on behalf of the Senate Committee on Homeland

Security and Governmental Affairs. I have also surveyed other important documents such as

the Basel Accords in my evaluation of the role of credit regulation in creating the crisis.

1 Minsky taught at Brown University from 1949 to 1958. From 1957 to 1965 he was Associate Professor of Economics at the University of California, Berkeley. In 1965 he became Professor of Economics, University of Washington in St Louis and retired from there in 1990. Until

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

4

Minsky was extremely productive as a scholar and authored hundreds of articles

and books throughout his career. In picking out my sources I have strived to use the works in

which he spells out his main theory, the Financial Instability Hypothesis and have narrowed it

in to three works. His first rigorous attempt was made in his book John Maynard Keynes,

from 1975, which despite the title is not a biography, but rather an outline of his

aforementioned hypothesis. His paper Can “It” Happen Again? A Reprise, from 1982, is also

of interest since he muses on the possibility of the Great Depression happening again, and is

by many considered as indicative to his correct anticipation of the crisis we’re in today. Lastly

I have chosen his paper Stabilizing an Unstable Economy from 1986, in which he delivers the

controversial theory that the stabilizing mechanisms used by monetarist policy actually paves

the way for more cataclysmic financial crises.

As a theorist Minsky was intellectually indebted to the works of John Maynard

Keynes, Joseph Schumpeter and Irving Fisher and I have chosen to include, their relevant

works here as well. A particularly vital contribution is Irving Fishers Paper The Debt-

Deflation Theory of Great Depressions, from 1933, which is of special importance with

regards to Krugman’s and Eggertsson’s model in their paper Debt, Deleveraging and the

Liquidity Trap published in the Oxford Journal The Quarterly Journal of Economics in 2012.

MAINSTREAM EXPLANATIONS FOR THE FINANCIAL CRISIS

Before probing into the key facets of Hyman Minsky’s Financial Instability Hypothesis, and

what it may contribute to macro economic modeling, it is prudent to first investigate what

prevalent explanations are given as to the cause of the 2008-9 financial crisis.

A suitable starting point for locating the mainstream view might be the

“authoritative study”2 This Time is Different, by Carmen Reinhart and Kenneth Rogoff, which

asserts that the trouble started with the deregulation of the financial sector.3 The period of

stagflation in the 70’s was the definitive end of Keynesianism, and through the influence of

Milton Friedman and others, the reliance on “big government” was replaced by renewed

belief in Adam Smiths harmony of interest reflected in free markets. In this regard, a note

worthy contribution was the Efficient Market Hypothesis by Eugene Fama, asserting that

financial markets are “informationally efficient”.4 On a political level, Ronald Reagan and

Margaret Thatcher supported the laissez faire ideas throughout the 80’s, evidenced by such

2 Claessens, Stijn and Kose, M. Ayhan. Financial Crises: Explanations, Types and Implications. IMF working paper 2013. P. 3 3 Reinhart, Carmen M. and Rogoff, Kenneth S. This Time is Different. Princeton Univeristy Press 2009. P. 199 4 Fama, Eugene F. Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, vol. 25, issue 2, 383-417, May 1970.

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

5

deregulation policies as Regan’s Garn-St. Germain Depository Institutions Act of 1982.5

The collapse of the Soviet Union in 1991 was successfully used by some as

definitive proof of the superiority of free market capitalism most amply stated by the

influential American political economist, Francis Fukuyama, when he declared “the end of

history”. 6 Liberalism was the name of the game, evidenced by the dramatic privatization

policies imposed on the former communist bloc. The advent of ‘western triumphalism’ in

economic matters, gave political momentum for continuing the trend of financial deregulation

from the 1980’s. Through the 1990’s many of the regulative structures put in place during the

1930’s, were rolled back under the auspice of Bill Clinton, and the incumbent Fed Chair Alan

Greenspan and the financial sector in the US, and in many parts of the world, consolidated in

a few giant, too-big-to-fail companies. However, events such as the crash of LTCM and the

collapse of the IT bubble eventually hampered the enthusiasm of the “new economy” and

hinted at the systemic risk associated with a fully globalized, intertwined and deregulated

financial system.7 It was in this globalized setting that the financial crisis of 2007/8, would

finally unfold.

It is commonly agreed upon, that two specific exogenous shocks created the

circumstances for the crisis. The first was a substantial boom in the housing market, fueled

partly by low interest rates set unprecedentedly low by the Federal Reserve in the follow up

of the 2001 recession and was kept there, due to persistent low inflation, until 2004. The

second shock was the vast increase in securitization8 of sub prime borrowers on the US

housing market. Industry experts have estimated that a variant called the "option adjustable

rate mortgage" (option ARM), which offered a low "teaser" rate and later resets so that

minimum payments skyrocket, accounted for about 0.5% of all U.S. mortgages written in

2003, but close to thirteen percent (and up to fifty-one percent in some U.S. communities) in

2006.9 The securitizarion process created a market for mortgage-backed securities (MBS’s),

which was enhanced by major financial institutions such as Citigroup, Lehman Brothers and

Morgan Stanley, who apart from acquiring subprime lenders, provided lines of credit, and

purchase guarantees.

All in all, it is perceived that these events fueled an unsustainable demand in the

housing market, with a doubling of US housing prices in the period 1995-2006, resulting in a

burst ripe bubble. In the period 2006-2009 housing prices fell 30% which according to

5 Sherman, Matthew. A Short History of Financial Deregulation in the United States. Center for Economic and Policy Research 2009. P.1 6 This feeling of western superiority was most readily observed in the influential book from 1992, The End of History and the Last Man, by Francis Fukuyama. 7 Rogoff (2009) p. 279 8 Simply put, securitization is the bundling of loans of various qualities, such as student loans, car loan and not least mortgages with the aim of selling the bundle shares to investors. 9 Whalen: 2011. P. 157

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

6

standard economic theory shouldn’t have posed a problem as supply and demand should have

just settle in a appropriate equilibrium. The price deterioration had two effects that led to a

substantial fall in aggregate demand.

The first effect was that many homeowners were suddenly in a position where

they owed more to the bank than their homes were worth and thus unable to service their

loans. As banks tried to limit their losses this naturally led to a massive increase in mortgage

defaults and home foreclosures that flooded the housing market and exacerbated the decline

in prices. As might be predicted by appropriate use of the ‘q-theory of investment’ on the

housing market, the price decline of residential property relative to the construction of a new

home led to a decline in housing construction and related industries adding to the negative

shock to aggregate demand.10

The second effect was that many financial institutions, in expectation of a

continuously rising housing market, had invested heavily in high risk mortgage-backed

securities and thus suffered massive losses when the subprime bubble burst. Due to these

losses many institutions didn’t have funds to loan out, and the institutions that did were faced

with uncertainty as to the risk exposure of other agents in the market. Suddenly the financial

system was unable to allocate resources in a market efficient manner leaving even

creditworthy agents without finance for sound investments - the credit crunch was a reality.

The fear in the markets also led to the withdrawal of funds from the banks, which put a strain

on liquidity. One noteworthy example of this was the investment bank Lehman brothers who

after a massive exodus of clients, asset devaluation and plunging stocks filed for bankruptcy –

the largest in US history. The FED didn’t intervene as lender-of-last resort, which by some

critics has been raised as the primary reason for the ensuing volatility in the financial markets.

Market volatility was only eased when many governments around the world intervened with

bank-bailouts. This has led many economists to characterize the crisis as a widespread

liquidity run.11

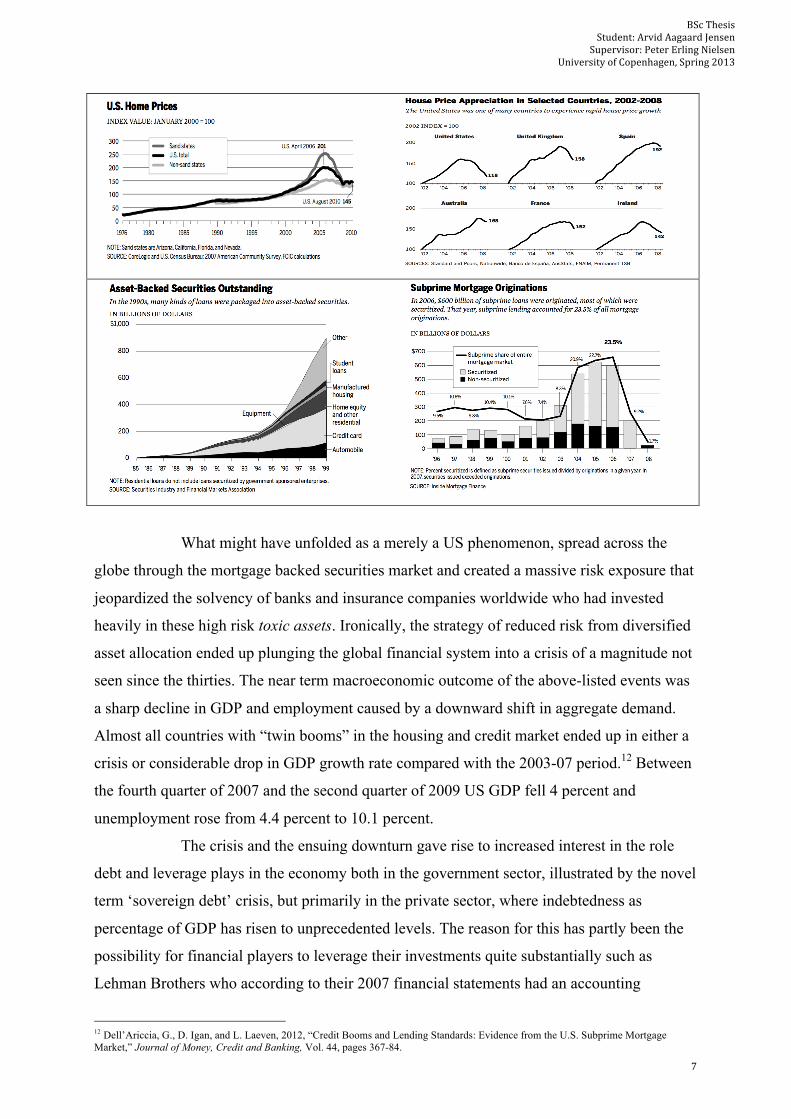

Figure 1. Overview of the Housing Crisis

10 Sørensen, Peter B. and Whitta-Jacobsen, Hans J. Introducing Advanced Macroeconomics: Growth and Business Cycles. McGraw-Hill 2010. P. 408 11 Gorton, G. Slapped in the Face by the Invisible Hand: Banking and the Panic of 2007. Paper prepared for the Federal Reserve Bank of Atlanta’s 2009 Financial Markets Conference: Financial Innovation and Crisis, May 11-13. 2009

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

7

What might have unfolded as a merely a US phenomenon, spread across the

globe through the mortgage backed securities market and created a massive risk exposure that

jeopardized the solvency of banks and insurance companies worldwide who had invested

heavily in these high risk toxic assets. Ironically, the strategy of reduced risk from diversified

asset allocation ended up plunging the global financial system into a crisis of a magnitude not

seen since the thirties. The near term macroeconomic outcome of the above-listed events was

a sharp decline in GDP and employment caused by a downward shift in aggregate demand.

Almost all countries with “twin booms” in the housing and credit market ended up in either a

crisis or considerable drop in GDP growth rate compared with the 2003-07 period.12 Between

the fourth quarter of 2007 and the second quarter of 2009 US GDP fell 4 percent and

unemployment rose from 4.4 percent to 10.1 percent.

The crisis and the ensuing downturn gave rise to increased interest in the role

debt and leverage plays in the economy both in the government sector, illustrated by the novel

term ‘sovereign debt’ crisis, but primarily in the private sector, where indebtedness as

percentage of GDP has risen to unprecedented levels. The reason for this has partly been the

possibility for financial players to leverage their investments quite substantially such as

Lehman Brothers who according to their 2007 financial statements had an accounting

12 Dell’Ariccia, G., D. Igan, and L. Laeven, 2012, “Credit Booms and Lending Standards: Evidence from the U.S. Subprime Mortgage Market,” Journal of Money, Credit and Banking, Vol. 44, pages 367-84.

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

8

leverage of 30.7 times. 13 The bankruptcy examiner of Lehman Brothers, Anton Valukas

determined that the accounting leverage was even higher.14 Although Basel I and II, had tried

to confront the issue, the industry was reluctant to implement the standards, which is not so

controversial considering the fact that it is difficult to institute a legal obligation to do so.

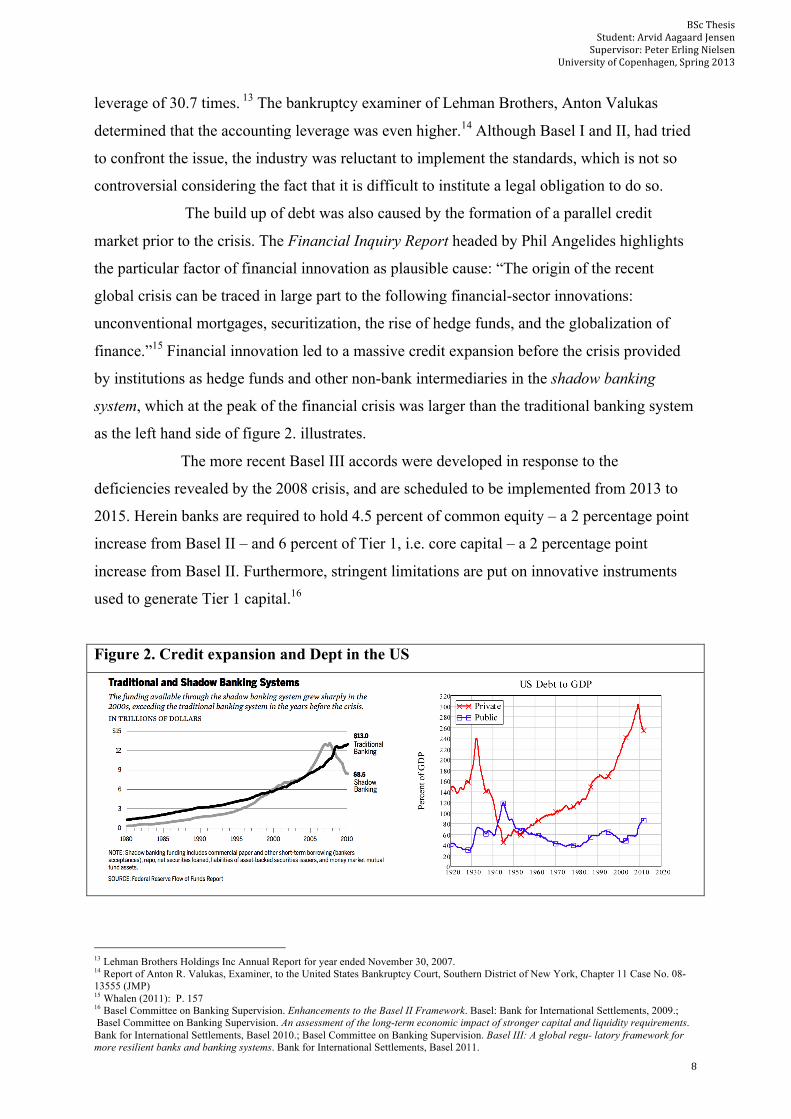

The build up of debt was also caused by the formation of a parallel credit

market prior to the crisis. The Financial Inquiry Report headed by Phil Angelides highlights

the particular factor of financial innovation as plausible cause: “The origin of the recent

global crisis can be traced in large part to the following financial-sector innovations:

unconventional mortgages, securitization, the rise of hedge funds, and the globalization of

finance.”15 Financial innovation led to a massive credit expansion before the crisis provided

by institutions as hedge funds and other non-bank intermediaries in the shadow banking

system, which at the peak of the financial crisis was larger than the traditional banking system

as the left hand side of figure 2. illustrates.

The more recent Basel III accords were developed in response to the

deficiencies revealed by the 2008 crisis, and are scheduled to be implemented from 2013 to

2015. Herein banks are required to hold 4.5 percent of common equity – a 2 percentage point

increase from Basel II – and 6 percent of Tier 1, i.e. core capital – a 2 percentage point

increase from Basel II. Furthermore, stringent limitations are put on innovative instruments

used to generate Tier 1 capital.16

Figure 2. Credit expansion and Dept in the US

13 Lehman Brothers Holdings Inc Annual Report for year ended November 30, 2007. 14 Report of Anton R. Valukas, Examiner, to the United States Bankruptcy Court, Southern District of New York, Chapter 11 Case No. 08-13555 (JMP) 15 Whalen (2011): P. 157 16 Basel Committee on Banking Supervision. Enhancements to the Basel II Framework. Basel: Bank for International Settlements, 2009.; Basel Committee on Banking Supervision. An assessment of the long-term economic impact of stronger capital and liquidity requirements. Bank for International Settlements, Basel 2010.; Basel Committee on Banking Supervision. Basel III: A global regu- latory framework for more resilient banks and banking systems. Bank for International Settlements, Basel 2011.

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

9

So, who should be blamed for this calamity? In 2005, a report issued by the

Basel Committee on Banking Supervisions Joint Forum posed the question whether financial

institutions fully appreciated the risks associated MBS’s and related securities, and concluded

that the credit risk was “Quite modest”.17 This has led the authors of the FDIC to conclude,

that “Regulators failed to rein in risky home mortgage lending. In particular, the Federal

Reserve failed to meet its statutory obligation to establish and maintain prudent mortgage

lending standards and to protect against predatory lending.”18 In regard to this, some have

accused economists and policy makers for uncritically accepting such theories as the Efficient

Market Hypothesis, since the crisis showed that “the credit rating agencies abysmally failed in

their central mission to provide quality ratings on securities for the benefit of investors.”19

In the aftermath of the crisis many economists have tried to give a satisfactory

explanation of its causes. An explanation common to most is the one given Harvard professor

and president of the National Bureau of Economic Research, Martin Feldstein, who lists 6

reasons for the meltdown: 1. Credit boom due to low interest rates. 2. financial regulation had

been too lax. 3. The housing policies had set wrong incentives 4. Rating agencies had misled

investors. 5. The banking sector had failed in its risk setting. 6. Borrowers had taken on too

much debt. In addition to this, Stijn Claessens, Chief of the Financial Studies Division in the

IMF Research Department, considers the following factors to be commonly accepted: 7. The

widespread use of complex and opaque financial instruments. 8. Increased interconnectedness

among financial markets, nationally and internationally, with the U.S. at the core. 9. High

degree of leverage of financial institutions. 10. Central role of the household sector.20

Although different weights are assigned to the impact of the factors most theories developed

over the years recognize the importance of booms in assets and credit markets, and credit

growth as “the most important, but still imperfect predictor.”21

As any prudent scientist should be, when confronted with the complexities of

economic systems, most distinguished economic researchers are reluctant to name a final

causal factor even with the benefit of hindsight. A great many even deem financial crises

unpredictable in nature. Most, however, are inclined to narrow it down to the 10 factors listed

by Feldstein and Stijn, although assigning different weights. This has implications for how the

crisis is categorized and consequently for which policy recommendations are given.

Nevertheless, all mainstream economists, by default, agree that the crisis might be explained

17 Basel Committee on Banking Supervision: Joint Forum. Credit Risk Transfer. Bank for International Settlements, March 2005, pp. 3–4, 6–7, 5–10; Angelides, Phil. The Financial Crisis Inquiry Report. Official government edition 2011. P. 206 18 Ibid. p. 101 19 Angelides, Phil. The Financial Crisis Inquiry Report. Official government edition 2011. P. 212 20 Stijn (2013) p. 22 21 Ibid. p. 33

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

10

by exogenous factors such as bad monetary policy and reprehensible risk management in the

financial sector.

Generally you find two types of explanations of the financial crisis:

1. Financial crises are caused by exogenous shocks. Followers of this interpretation

normally base their models on the hypothesis of rational expectations and

homogeneity of the economic actors.

2. Financial crises are caused by endogenous mechanisms. Followers of this type of

explanation often outline the institutionalized role of mass psychology and herd

behavior of economic actors.

It seems reasonable to conclude that the mainstream view that has just been accounted for is

firmly placed in the first category. Now let us turn to an explanation of the second type. Enter

Hyman Minsky.

MINSKY’S FINANCIAL INSTABILITY HYPOTHESIS

Despite the withstanding consensus, some economists put primary emphasis on endogenous

instead of exogenous factors when explaining not only the most recent financial calamity, but

also preceding ones. One proponent of this is the late Hyman Minsky, whose credit cycle

theory has attracted unprecedented attention after economists and news outlets called the

eruption of the crisis a ‘Minsky moment’.22 According to Minsky, “(i)nstability is an observed

characteristic of our economy. For a theory to be useful as a guide to policy for the control of

instability, the theory must show how instability is generated.”23 Explained through his

Financial Instability Hypothesis (FIH), laid out in his magnum opus John Maynard Keynes

from 197524, he claimed that financial crises are debt driven, cyclical phenomena,

promulgated by endogenous factors inherent in the institutions of the post-war, western-type

financial system.

To explain the Financial Instability Hypothesis (FIH), Minsky takes point of

departure in thriving economy without the intervention of a central bank or ‘big government’.

It is assumed that the economy has recently been through a systemic financial crisis with

many unsuccessful investments leaving many firms unable to finance borrowings and forcing

banks to discard bad debts. Thus, firms and banks are very risk aversive in their portfolio and

loan management respectively, favoring lower bound estimates of future cash flows and very

22 The phrase was coined by Paul Allen McCulley (1957-), an American economist and former managing director at the investment firm PIMCO, that manages assets worth of 2 trillion dollars. He is regularly used as a financial expert by CNBC and Bloomberg Television. He also introduced the term Shadow Banking System, used by among others the FCIC. On August 22nd, 2007, the Guardian leader had the headline: In praise of ... Hyman Minsky. 23 Minsky(1982): p.6 24 Minsky, H. P. John Maynard Keynes, Columbia University Press 1975.

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

11

high risk premiums. As time passes, the milieu of a growing economy and risk aversive

financing renders most investment projects successful and leaves firms and banks with the

view that increased financial leveraging pays off.

The expectation of future economic growth encourages firms and banks to

lessen their risk averseness using more optimistic estimates of future cash flows and lower

risk premium. The result is growing levels of investments and exponentially rising asset

prices. The economic boom raises also raises the demand for funds to finance speculation in

assets, and since investors and bankers alike share the optimism of the ‘new economy’, the

demand is met. The debt to equity ratio increases, liquidity decreases and credit provision

accelerates, demarcating a phase shift into what Minsky calls the ‘euphoric economy’25,

where creditors and debtors have steadfast expectations of continued upward appraisal of

asset prices and accept liabilities that in a more risk conscious environment would have been

rejected.26 Simultaneously, the increased debt to equity ratio makes firms more vulnerable to

increasing interest rates.

Even when ignoring the likely intervention from monetary authorities or an

active state to regulate the boom, the general decrease in liquidity and the rise in interest paid

on highly liquid induce a market driven increase in the interest rate. The economy experiences

a decline in the demand elasticity with respect to credit, since the projected pay offs from

speculative investments are prone to exceed interest rates by a large margin. Thus, the

increased credit costs has a negligent impact on mitigating the boom.

The ‘euphoric economy’ also sets the stage for an agent which plays a crucial

role in Minsky’s theory, namely the ‘Ponzi financier’. 27 This category of investors makes a

business of taking on massive debt, through leverage, to speculate in the rising market, and

although the servicing cost for Ponzi debtors surpass the cash flows from the firms they own,

the capital appreciation of their assets easily cover the costs of servicing their loans. The rise

of Ponzi scheme investors has two implications on the market. Firstly, they push up the

market interest rate and secondly, but not less significantly, their heavily leveraged positions

increase the fragility of the system should a reversal in asset growth occur. Viewing the 2008

financial crisis from this standpoint the monetary policy of low interest rates after 9/11,

actually increased instability further.

In due time the twin effects of rising interest rates and an increased debt to

equity ratio, has an impact on a wide range of business undertakings. The reduced interest rate

cover transforms conservatively funded business ventures into speculative ones and 25 Minsky 1982, pp. 120-124 26 Minsky 1982, p. 123 27 Minsky 1982, pp. 70, 115

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

12

speculative undertakings into ‘Ponzi’. Businesses in the latter category will at some point be

forced to sell assets to service their debt, which punctures the exponential growth in assets

prices, leading to dramatic consequences for the market.

The Ponzi agents suddenly find themselves in a situation with asset holdings

that may no longer be traded with a profit, and debt obligations that can’t be serviced by the

cash flow of their businesses, leaving them with no choice than to sell off and thus further

accelerate the price fall. Furthermore, the banks that financed the asset purchases, realize that

their customers can’t pay their debts, which leads them to hike up the interest rate. Amidst

doubt of ‘marked-to-market’ asset values liquidity becomes highly sought. In an attempt to

sell illiquid assets in return for liquidity the market is flooded with assets and the euphoria of

the boom gives way for the panic of the bust.

In the aftermath of the boom, the underlying problem facing the economy is the

disparity between debts incurred to finance investment, and the cash flows these investments

generate. The cash flows are highly dependent on the level of investment and on the inflation

rate. Since the investment level has plunged, asset price deflation or current price inflation

stand out as the only two forces that may restore the harmony between asset prices and cash

flows. The choice between the paths of ‘asset price deflation’ or ‘current price inflation’, were

important for Minsky’s controversial view of the role of inflation, which he outlined in his

analysis of the stagflation era of the 1970’s. In this regard he argues, that if the inflation rate

is high or the debt level is relatively low at the beginning of the crisis, then rising cash flows

may in short notice repay the loans taken on during the boom. The economy may then come

out of the crisis with hampered growth and high inflation, but also with minimal amount of

bankruptcies and a sustained fall in liquidity. So although this option invokes stagflation, it is

a self-correcting mechanism and a prolonged downturn is prevented.

However, even though a severe, depression-like, disaster has not unfolded due

to the above mentioned self-correcting mechanisms, the circumstance for the cycle to repeat

itself is soon established anew and, in due time one might expect a decrease in the liquidity

preference once again. As each new cycle begins before the accumulated debt in the previous

on has been repaid, there appears a trend towards increasingly higher debt to equity ratios in

each consecutive cycle, thus increases the instability of the financial system over time.

If alternatively, the rate of inflation are low and the debt levels are very high in

the beginning of the crisis, then cash flows will not be able to sustain the prevailing debt

structures. Affected firms, those with interest costs in excess of their cash flows, are left with

three options. They might sell of assets, cut their margins to increase their cash flows or file in

bankruptcy. Unlike the inflationary course, these actions are prone to further depress the

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

13

current price level and thus to some degree worsen the original disparities. So the path of

‘asset price deflation’ is self reinforcing, rather than self-correcting, and is how Minsky

explains a depression.

The above rendition of Minsky’s Financial Instability Hypothesis, excludes the

intervention of an active government. His view on government may be portrayed by the

following quote:

“An economy in which a government spends to assure capital formation rather

than support consumption is capable of achieving a closer approximation to

tranquil progress than is possible with our present policies. Thus while big

government virtually ensures that a great depression cannot happen again, the

resumption of tranquil progress depends on restructuring government so that it

enhances resource development. “28

Introducing an active state in the economic scenario might alter the story in

several ways, since it might intervene with expansionary fiscal policies and ameliorate the

collapse in cash flows through automatic stabilizers as well as Reserve Bank interventions. In

this regard he challenges the stabilizing effects of a policy of lender-of-last-resort, if not

followed up by structural changes. Policy must adapt as the economy is transformed and the

inherent behavior of financial players must be continuously regulated, matching the ceaseless

financial innovation. Thus “successful” efforts by governments and central banks on keeping

financial institutions afloat in the short run will actually deepen the inevitable future collapse.

In his from article from 1982, Can “it” happen again, Minsky sums up the thought-

provoking conclusion that “Stability…is destabilizing”29.

THE ISSUE OF DEBT REVISITED: MINSKY AND MAINSTREAM MODELING

In retrospect, Minsky’s FIH was meant to challenge the hailed Efficient Market

Hypothesis (EMH) of the 1970’s. As a consequence of the recent crisis EMH was left in such

shambles that even one of the most revered supporters of unregulated markets, Alan

Greenspan, testified to the US Senate that “(t)hose of us who have looked to the self-interest

of lending institutions to protect shareholders’ equity, myself included, are in a state of

shocked disbelief,”.30

Like Greenspan an overwhelming majority of economists were taken by surprise

and duly noted the dire analogies to the 1930’s raising the headline question posed by

28 Minsky(1982): p. 13 29 Minsky, Hyman P. Ph.D. Can "It" Happen Again? A Reprise. Hyman P. Minsky Archive, http://digitalcommons.bard.edu/hm_archive/155. Paper 155, 1982. 30 http://www.nytimes.com/2008/10/24/business/economy/24panel.html?_r=0

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

14

Minsky, can “it” happen again?31 In 2008, when asked a similar question, I.M.F. chief

economist, Olivier Blanchard32, wholly disregarded the idea claiming that economists had

learned their lesson, and wouldn’t repeat mistakes of the past. To which Gregory Mankiw

rhetorically countered “but have we learned enough?”33 Studies of the 1930’s have shown that

competing forecasting services at Harvard and Yale were caught completely by surprise as to

the gravity and longevity of the Great Depression.34 And similarly, contradicting Blanchard’s

claim, the progression in the tools and the data available to modern economists, still left most

oblivious of the impending crisis. In the aftermath Paul Krugman bluntly stated that the

economist profession had “failed” and called for a thorough reassessment of integral parts of

macroeconomics analysis.

Together with the Icelandic economist, Gauti Eggertsson, Krugman modeled

theories by Irving Fisher, Hyman Minsky and Richard Koo in their recently published Debt,

Deleveraging, and the Liquidity Trap. They claim that although the issue of debt is a key

factor in major economic downturns and although at the heart of the present “debt crisis” it is

commonly disregarded in mainstream economic modeling giving rise to severe blind angels

when analyzing monetary and fiscal policy35. In the paper they introduce a New Keynesian

model of aggregate demand is affected when various agents with an overhang of debt is

forced into deleveraging and argue that their findings may explain economic difficulties

historically as well as presently. Along with many others, KE argues that the rapid increase in

gross household debt in a number of countries, paved the way for the 2008 crisis and that it

furthermore hinders a recovery. In their view, critics use debt as an unjustified argument

against expansionary fiscal policy, asserting that you cannot cure a problem caused by debt,

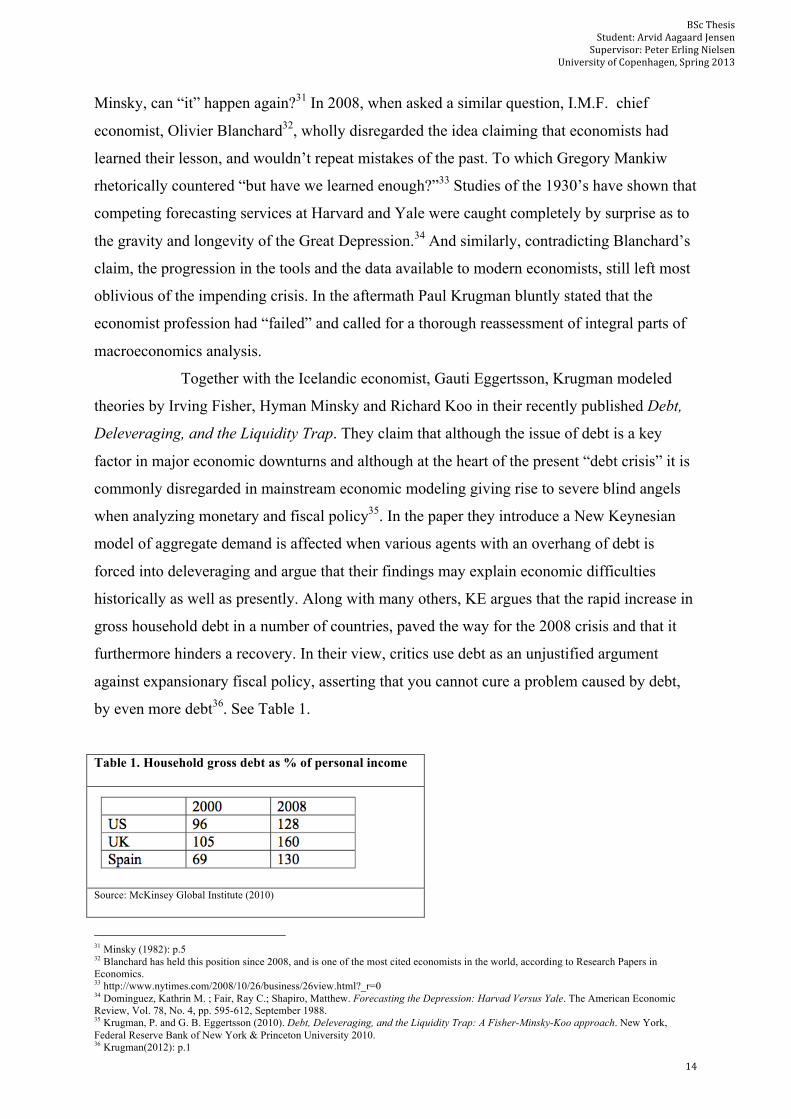

by even more debt36. See Table 1.

Table 1. Household gross debt as % of personal income

Source: McKinsey Global Institute (2010)

31 Minsky (1982): p.5 32 Blanchard has held this position since 2008, and is one of the most cited economists in the world, according to Research Papers in Economics. 33 http://www.nytimes.com/2008/10/26/business/26view.html?_r=0 34 Dominguez, Kathrin M. ; Fair, Ray C.; Shapiro, Matthew. Forecasting the Depression: Harvad Versus Yale. The American Economic Review, Vol. 78, No. 4, pp. 595-612, September 1988. 35 Krugman, P. and G. B. Eggertsson (2010). Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo approach. New York, Federal Reserve Bank of New York & Princeton University 2010. 36 Krugman(2012): p.1

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

15

A similar academic interest in the role of debt arose in the 1930’s, where the

notable economist Irving Fisher in his paper The Debt-Deflation Theory of Great

Depressions, from 1933, set forth the argument that the cause of the Great Depression was

rooted in the vicious circle of debt-deflation. Fisher describe this as a dynamic process in

which declining commodity and asset prices, puts pressure on nominal debt holders forcing

them to distress sales of assets leading to even more deflation and falling aggregate demand,

along with adverse effects on the financial markets. 37 It is worth of note, that what Fisher

here described was an endogenous explanation for the crisis, which was just as controversial

at the time as it is now.

In his treatment of the subject Ben Bernanke elaborates on how Fisher idea was

received by the economic profession:

"Fisher's Idea was less influential in academic circles though, because of the

counterargument that debt-deflation represented no more than a redistribution

from one group (debtors) to another (creditors). Absent implausibly large

differences in marginal spending propensities among the groups, it was

suggested, pure redistributions should have no signifiant macro-economic

effects"38

As Bernanke outlines the prime reason for dismissing the theory was that debt has no macro-

economic effects, and that debt merely involves a transfer of spending power from saver to

borrower. Thus, deflation simply increases the amount transferred in debt servicing and

repayment from the borrower to the saver and therefore has no impact on aggregate demand

unless savers and borrowers have very different spending propensities

Naturally, Eggertson and Krugman (KE) are well aquainted with the Bernanke’s

mainstream idea of seeing debt merely as a transfer of spending power. But argues that the

view is ill considered.

“It assumes, implicitly, that debt is debt -- that it doesn't matter who owes the

money. Yet that can't be right; if it were, debt wouldn't be a problem in the first

place… It follows that the level of debt matters only if the distribution of that

debt matters, if highly indebted players face different constraints from players

with low debt. And this means that all debt isn't created equal -- which is why

borrowing by some actors now can help cure problems created by excess

borrowing by other actors in the past.”39

37 Fisher, Irving. "The Debt-Deflation Theory of Great Depressions." (1933). Martino Publishing 2011. 38 Bernanke, B. S. Essays on the Great Depression. Princeton University Press 2000. P. 24 39 Krugman, P. and G. B. Eggertsson (2010). Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo approach. New York, Federal Reserve Bank of New York & Princeton University 2010. p. 3

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

16

How more debt may solve a problem arising from debt is the main issue when considering

KE’s mode.

THE MODEL

In the following exposition, I will focus on the main insights the model reveals

in relation to the current policy debate. A more elaborate walkthrough of the model may be

found in appendix A to which I will continuously refer.

It needs mentioning that one of the contentions among scholars with regard to

Minsky, is how to interpret him justly. Being a post-keynesian, Minsky himself stated that his

theories could not be modeled from a neoclassical perspective based on long run equilibrium

models and representative agents, which “abstract from time” and doesn’t “make great

depressions one of the possible states in which our type of capitalist economy can find

itself.”.40 However, Paul Krugman is quite clear on the matter when he writes: “my basic

reaction to discussions about What Minsky Really Meant — and, similarly, to discussions

about What Keynes Really Meant — is, I Don’t Care. I mean, intellectual history is a fine

endeavor. But for working economists the reason to read old books is for insight, not

authority”.41

Despite their reservations, KE follow Minsky’s lead and start of by explaining

that the “central idea of debt-centered accounts of economic instability…is that views about

safe levels of leverage are subject to change over time.”42 Furthermore they echo Minsky

when they explain how a stable period of growth and rising asset prices reassures banks and

firms that “(e)xisting debts are easily validated and units that were heavily in debt prospered:

it pays to lever”.43 However, “at some point this attitude is likely to change, perhaps abruptly

– an event known variously as the Wile E. Coyote moment or the Minksy moment.”44 In

relation to the 2008 crisis this was the point in time when it became clear that MBS’s were

overvalued and that the collateral in the financial sector was insufficient.

The model follows a basic textbook New Keynesian framework, with

monopolistic competition and infinite-lived optimizing consumers and is based on Michael

Woodfords ‘cashless economy’45, although goods prices are naturally given in money units.

There is time-dependent pricing, meaning that some fraction of firms can set prices at will and

40 Minsky (1982): p. 5 41 New York Times Blog, March 27, 2012. Minsky and Methodology (Wonkish). http://krugman.blogs.nytimes.com/2012/03/27/minksy-and-methodology-wonkish/ 42 Krugman (2012): p.7 43 Minsky 1982, p. 65 44 Krugman (2012): p.7 45 Woodford, Michael. Interest and Prices: Foundations of a Theory of Monetary Policy. Princeton University, 2003.

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

17

others must set prices one period ahead. The nominal interest rate is determined using the

Taylor rule. It differs from conventional New Keynesian models in three ways. Firstly,

consumers have different time preferences and are divided into ‘patient’ and ‘impatient’.

‘Patient’ consumers are prone to lend, ‘impatient’ are prone to borrow, which in the

mathematical construction is done by giving the two types different discount factors.

Secondly, there is an exogenously given debt limit, set in real terms, for both consumer types

and it is assumed that utility maximized consumption of the impatient consumer is achieved

when he borrows to the limit. Thirdly, KE incorporates “Fisherian” debt deflation by

denominating debt in nominal terms.

First they model the ‘Minsky moment’ in a price flexible economy, by an the

exogenously imposed fall in the debt constraints of their two representative agents from Dhigh

to Dlow. This causes a deleveraging shock since the borrower has to reduce consumption. To

make up for the lower consumption, the real interest rate has to be lowered temporarily so the

saver will spend more, to uphold the consumption Euler condition.46 Furthermore, it is shown

that if the debt overhang is large enough the real interest rate must go negative causing a

liquidity trap, which is “an observation that goes to the heart of the economic problems we

currently face.”47 Under more realistic conditions a liquidity trap refers to a situation in which

central bank efforts to expand the money supply fails to lower the interest rate and kindle

economic growth. It is caused when people stockpile cash because they expect an unfavorable

economic event such as the fear of asset-price deflation in the advent of the 2008 crisis.

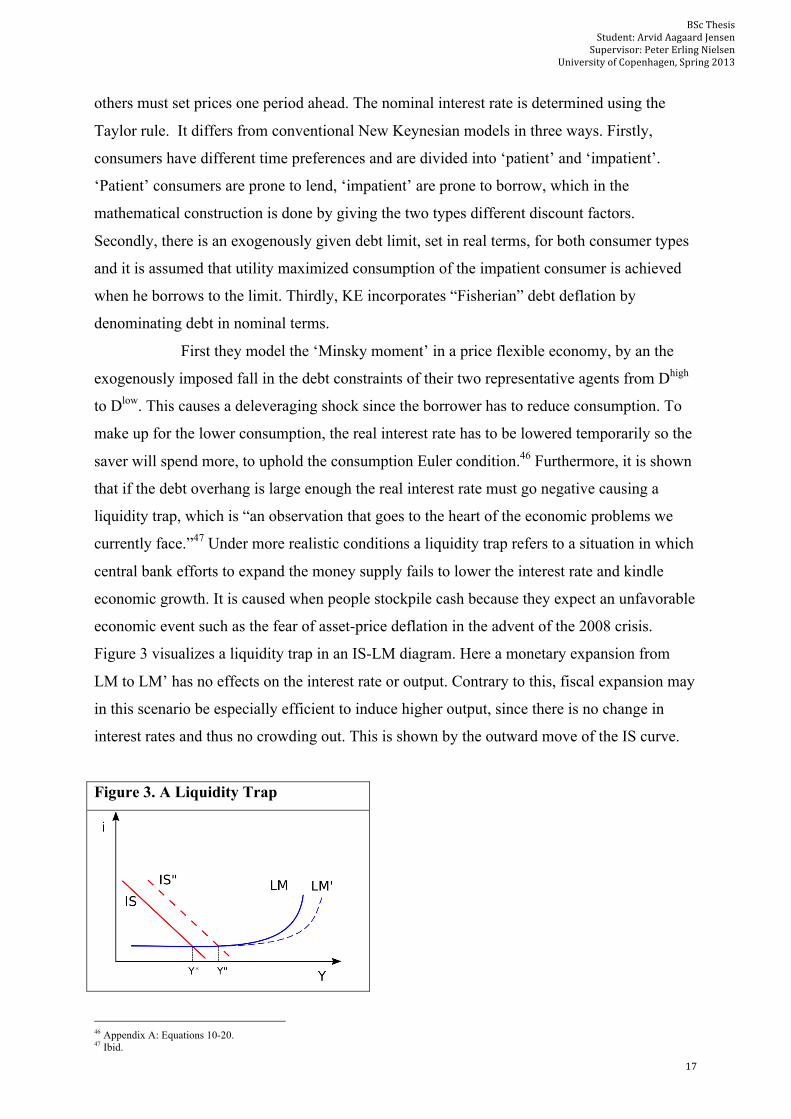

Figure 3 visualizes a liquidity trap in an IS-LM diagram. Here a monetary expansion from

LM to LM’ has no effects on the interest rate or output. Contrary to this, fiscal expansion may

in this scenario be especially efficient to induce higher output, since there is no change in

interest rates and thus no crowding out. This is shown by the outward move of the IS curve.

Figure 3. A Liquidity Trap

46 Appendix A: Equations 10-20. 47 Ibid.

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

18

When introducing debt in nominal terms, but keeping the debt limit given in real

terms, KE show that if the shock pushes the natural rate of interest below zero, it necessitates

a drop in the price level.48 As the price level falls, the natural rate of interest becomes even

more negative leading to a further price drop, repeating in a consecutive cycle. This is Irving

Fisher’s debt deflation, where the natural rate of interest is now endogenously given.

In the final part of the paper KE introduces production to their model. Ct now

refers to a continuum of goods giving producers of each good market power with elasticity of

demand given by 𝜃. Agents face the same budget constraints as before, but instead of an

endowment they receive income through wage Wt for each hour worked. Furthermore, there

is a continuum of monopolistically competitive firms of measure one; each producing one

type of the varieties the consumers like and with a production function linear in labor. 1− 𝜆

keep their prices fixed for a certain planning period and 𝜆 change their prices continuously.

Firms are committed to sell all that is demanded at the price they set and thus have to hire

labor to meet this demand. Since production is endogenous, agents must not only optimize

consumption but also how much they work. After deriving all the equilibrium conditions KE

make a linear approximation around the steady state.

Since production is endogenous and some prices are rigid a “New Classical

Phillips Curve” - or AS curve - is established49. They also develop an IS curve50 which they

combine with the assumed Taylor rule51 to obtain an AD curve. Assuming that the shock is

large enough for the zero bound to be binding, it is shown that the larger the shock the larger

is the fall in output and the price level.52 When graphing the model in a familiar supply and

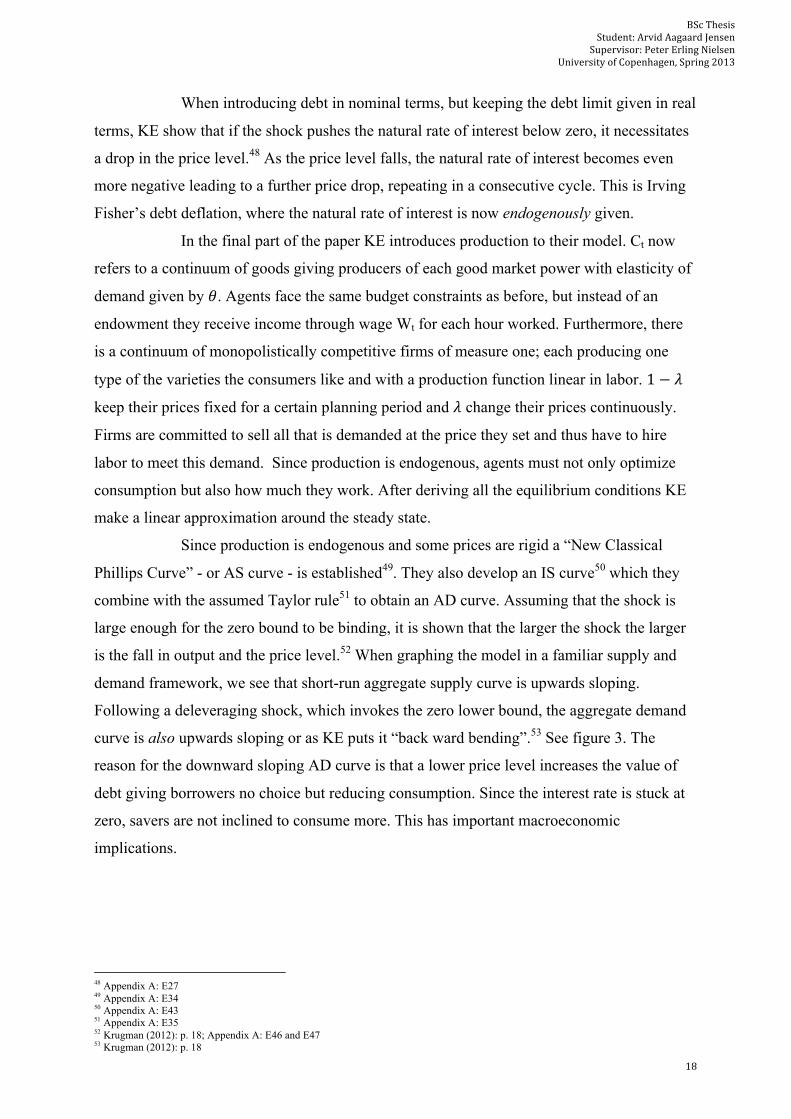

demand framework, we see that short-run aggregate supply curve is upwards sloping.

Following a deleveraging shock, which invokes the zero lower bound, the aggregate demand

curve is also upwards sloping or as KE puts it “back ward bending”.53 See figure 3. The

reason for the downward sloping AD curve is that a lower price level increases the value of

debt giving borrowers no choice but reducing consumption. Since the interest rate is stuck at

zero, savers are not inclined to consume more. This has important macroeconomic

implications.

48 Appendix A: E27 49 Appendix A: E34 50 Appendix A: E43 51 Appendix A: E35 52 Krugman (2012): p. 18; Appendix A: E46 and E47 53 Krugman (2012): p. 18

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

19

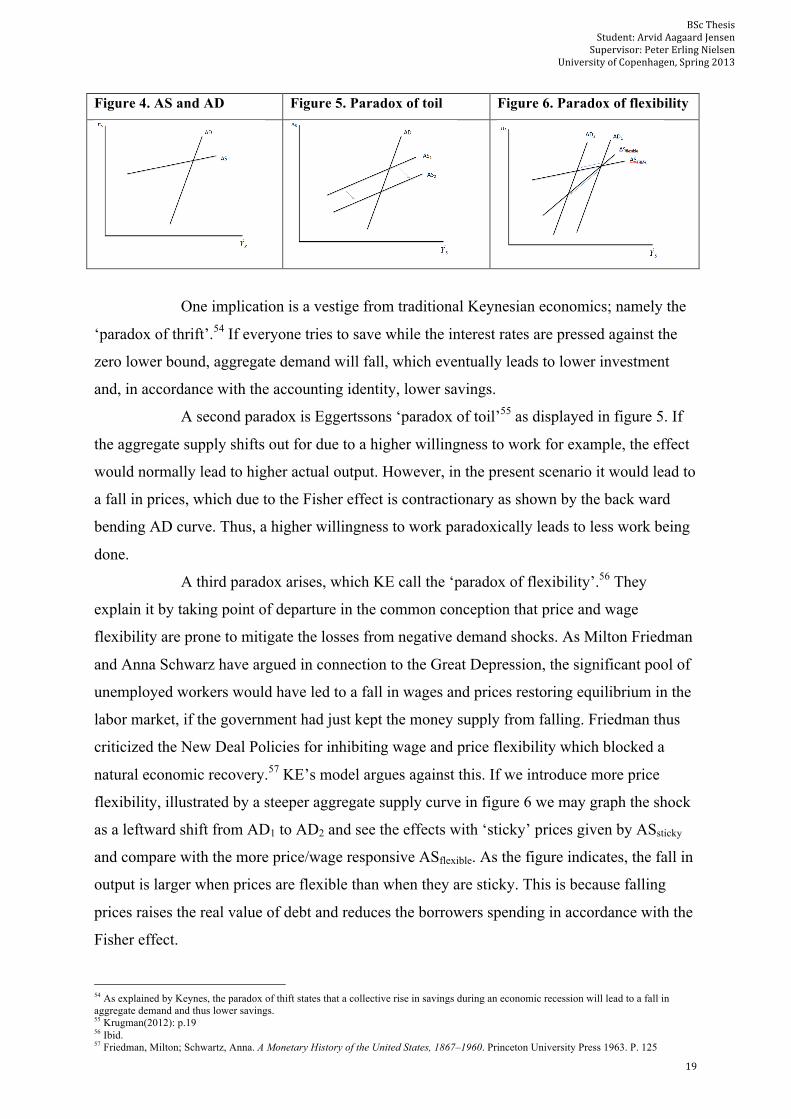

Figure 4. AS and AD Figure 5. Paradox of toil Figure 6. Paradox of flexibility

One implication is a vestige from traditional Keynesian economics; namely the

‘paradox of thrift’.54 If everyone tries to save while the interest rates are pressed against the

zero lower bound, aggregate demand will fall, which eventually leads to lower investment

and, in accordance with the accounting identity, lower savings.

A second paradox is Eggertssons ‘paradox of toil’55 as displayed in figure 5. If

the aggregate supply shifts out for due to a higher willingness to work for example, the effect

would normally lead to higher actual output. However, in the present scenario it would lead to

a fall in prices, which due to the Fisher effect is contractionary as shown by the back ward

bending AD curve. Thus, a higher willingness to work paradoxically leads to less work being

done.

A third paradox arises, which KE call the ‘paradox of flexibility’.56 They

explain it by taking point of departure in the common conception that price and wage

flexibility are prone to mitigate the losses from negative demand shocks. As Milton Friedman

and Anna Schwarz have argued in connection to the Great Depression, the significant pool of

unemployed workers would have led to a fall in wages and prices restoring equilibrium in the

labor market, if the government had just kept the money supply from falling. Friedman thus

criticized the New Deal Policies for inhibiting wage and price flexibility which blocked a

natural economic recovery.57 KE’s model argues against this. If we introduce more price

flexibility, illustrated by a steeper aggregate supply curve in figure 6 we may graph the shock

as a leftward shift from AD1 to AD2 and see the effects with ‘sticky’ prices given by ASsticky

and compare with the more price/wage responsive ASflexible. As the figure indicates, the fall in

output is larger when prices are flexible than when they are sticky. This is because falling

prices raises the real value of debt and reduces the borrowers spending in accordance with the

Fisher effect.

54 As explained by Keynes, the paradox of thift states that a collective rise in savings during an economic recession will lead to a fall in aggregate demand and thus lower savings. 55 Krugman(2012): p.19 56 Ibid. 57 Friedman, Milton; Schwartz, Anna. A Monetary History of the United States, 1867–1960. Princeton University Press 1963. P. 125

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

20

POLICY IMPLICATIONS

In terms of the monetary policy that should be put in place following a deleveraging shock,

KE suggest the solution of raising expected inflation since it may allow for a negative natural

interest rate even though nominal interest rates are bound at zero. In the context of KE’s

model, a rise in expected inflation might be achieved by changing the Taylor rule, such that

the central bank has a higher inflation target for a limited amount of time. This however,

would only work if the higher target is credible and many might be inclined to expect central

bankers to fall back into their normal habit of restricting inflation. The promise of future

inflation is therefore time-inconsistent, since the central bank may act in a discretionary

manner.58

In terms of fiscal policy KE argues, that their model gives reason to believe that

a liquidity trap caused by deleveraging is only temporary. In light of this, they argue that a

debt financed government fiscal expansion may indeed solve problems incurred by too much

private debt, since it sustains output and employment and allows the private sector to repair

its balance sheets. In contrast to this, some economists argue that fiscal expansion is futile due

to Ricardian equivalence, which simply mean that consumers will revise their intertemporal

budget plan and expect higher taxes in the future thus holding back spending in the present,

and fully offset government efforts. With reference to their model, KE argues that Ricardian

equivalence does not hold, because borrowers are liquidity constrained and forced to pay

down their debts just as Minsky anticipated in his theory. This means that their spending

depends on the margin of current income, not expected future income, which makes way for

an “old-fashioned Keynesian multiplier analysis”59 even when considering rational forward

looking consumers. KE also argue that tax cuts and transfer payments are effective, but only

to the extent that these fall on the debt-constrained agents.

Considering the difficulty in singling these agents out in a tax reform it is more

likely that government spending would be more effective after a large deleveraging shock and

the ensuing liquidity trap since “deficit-financed government spending can, at least in

principle, allow the economy to avoid unemployment and deflation while highly indebted

private-sector agents repair their balance sheets.”60 Expansionary fiscal policy not only limits

the output loss, but also works against the Fisherian debt deflation, due to rising prices, which

limits the shock itself.

58 Sørensen(2010): p. 662 59 Krugman(2012): p. 22 60 Krugman, P. and G. B. Eggertsson (2010). Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo approach. New York, Federal Reserve Bank of New York & Princeton University 2010. p. 3

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

21

CONCLUSION

It is a well-established consensus among scholars of history of economic thought, that

economic theory progresses neither in a linear nor cyclical manner, but rather as a spiral

where old ideas, in an evolved form, fit for a present context, regain preeminence.61 Thus

theoretical approaches once deemed obsolete might lay claim to new appraisal as

groundbreaking political, cultural or economics events unfold. The recent occurrence of

Minsky’s ideas in the avant-garde of mainstream economic theory, following the 2008 crisis,

is one such instance.

One basic question that this thesis has posed is: how did the financial crisis of

2008 come to pass? With reference to a wide array of economists and institutional reports the

prevalent mainstream explanations a summarized in 10 points. 1. Credit boom due to low

interest rates. 2. Financial regulation had been too lax. 3. The housing policies had set wrong

incentives 4. Rating agencies had misled investors. 5. The banking sector had failed in its risk

setting. 6. Borrowers had taken on too much debt. 7. Widespread use of complex and opaque

financial instruments. 8. Increased interconnectedness among financial markets, nationally

and internationally. 9. High degree of leverage of financial institutions. 10. Central role of the

household sector. The key finding of the thesis in this regard, is that these explanations are

exogenous in nature and offer only diminutive systemic reasons for the crisis.

Minsky’s Financial Instability hypothesis offers a more systemic explanation of

the financial structure of the economy and may thus complement the more discrete

mainstream explanations. Krugman and Eggersson, who in their paper examine the effects of

a change in the debt limit, have certainly reviewed his emphasis on the importance of debt;

such as it happened during the crisis. They argue that such a ‘Minsky moment’ causes

deleveraging since borrowers are forced to reduce their debt by reducing their consumption

which in turn puts downward pressure on the real interest rate, due to the Taylor-rule policy,

pressing it up against the zero lower bound of the nominal interest rate, thus hampering

monetary policy. KE also show that Fisherian debt-deflation arise since the price level falls;

increasing the value of outstanding debt, which leads to further deleveraging and price falls.

KE’s findings are of special relevance to the present public debate concerning

the so called ‘sovereign debt crisis’. In the paper “Growth in Time of Debt” from 2010

Carmen and Rogoff propose a set of stylized facts with regards to the relationship between

61 Brue, Stanley and Grant, Randy. The History of Economic Thought. Thomson South Western, 2007. P 7

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

22

public debt and GDP growth based on they findings in table 2.62 Their findings have cause

many policy makers to heed the heed the view that “traditional debt management issues

should be at the forefront of public policy concerns”63, invoking ‘fiscal discipline’ manifested

in such measures as 2011 EU reform of the Stability and Growth Pact.

Table 2. Real GDP Growth as the Level of Public Debt Varies 20 advanced economies, 1946–2009

Sources: Reinhart, Carmen M. and Rogoff, Kenneth S. Growth in a Time of Debt Appendix Table 1, line 1.

Recently however, a study has brought to light the results in table 2 were incorrectly

calculated, and that the correct average annual real GDP growth rate for countries with a

public debt-to-GDP ratio over 90 percent is actually 2.2 percent and not -0.1.64 This might

renew support for government fiscal stimulus such as KE suggests.

62 Reinhart, Carmen M. and Rogoff, Kenneth S. Growth in a Time of Debt. American Economic Review: Papers & Proceedings 100 (May 2010): p. 573–578 63 Ibid. p. 578 64 Herndon, Thomas; Ash, Michael; Pollin, Robert. Does High Public Debt Consistently Stifle Economic Growth? A Critique of Reinhart and Rogoff. Political Economy Research Institute, 2013. P. 1

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

23

BIBLIOGRAPHY

Angelides, Phil. The Financial Crisis Inquiry Report. Official government edition 2011.

Barthalon, E. Crises financières - Un panorama des explications. Problèmes économiques, Nr. 2595 (16 décembre), p. 1-10, 1998.

Basel Committee on Banking Supervision: Joint Forum. Credit Risk Transfer. Bank for International Settlements, March 2005, pp. 3–4, 6–7, 5–10.

Basel Committee on Banking Supervision. Enhancements to the Basel II Framework. Basel: Bank for International Settlements, 2009.

Basel Committee on Banking Supervision. An assessment of the long-term economic impact of stronger capital and liquidity requirements. Bank for International Settlements, Basel 2010.

Basel Committee on Banking Supervision. Basel III: A global regu- latory framework for more resilient banks and banking systems. Bank for International Settlements, Basel 2011.

Bernanke, B. S. Essays on the Great Depression. Princeton University Press 2004.

Brue, Stanley and Grant, Randy. The History of Economic Thought. Thomson South Western, 2007.

Claessens, Stijn and Kose, M. Ayhan. Financial Crises: Explanations, Types and Implications. IMF working paper 2013.

Dell’Ariccia, G., D. Igan, and L. Laeven, 2012, “Credit Booms and Lending Standards: Evidence from the U.S. Subprime Mortgage Market,” Journal of Money, Credit and Banking, Vol. 44, pages 367-84.

Dominguez, Kathrin M. ; Fair, Ray C.; Shapiro, Matthew. Forecasting the Depression: Harvad Versus Yale. The American Economic Review, Vol. 78, No. 4, pp. 595-612, September 1988.

Eggertsson, Gauti. The Paradox of Toil. Staff report no. 433, Federal Reserve Bank of New York, March 2010.

Fama, Eugene F. Efficient Capital Markets: A Review of Theory and Empirical Work. Journal of Finance, vol. 25, issue 2, 383-417, May 1970.

Fama, E. F. and K. R. French. The Capital Asset Pricing Model: Theory and Evidence. The Journal of Economic Perspectives 18(3): 25-46, 2004.

Fisher, Irving. "The Debt-Deflation Theory of Great Depressions." (1933). Martino Publishing 2011.

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

24

Friedman, Milton; Schwartz, Anna. A Monetary History of the United States, 1867–1960. Princeton University Press 1963.

Gorton, G. Slapped in the Face by the Invisible Hand: Banking and the Panic of 2007. Paper prepared for the Federal Reserve Bank of Atlanta’s 2009 Financial Markets Conference: Financial Innovation and Crisis, May 11-13. 2009

Greenspan, A. Testimony of Chairman Alan Greenspan: The economic outlook. Washington, Joint Economic Committee, U.S. Congress, 2005.

Herndon, Thomas; Ash, Michael; Pollin, Robert. Does High Public Debt Consistently Stifle Economic Growth? A Critique of Reinhart and Rogoff. Political Economy Research Institute, 2013.

Krugman, P. and G. B. Eggertsson (2010). Debt, Deleveraging, and the Liquidity Trap: A Fisher-Minsky-Koo approach. New York, Federal Reserve Bank of New York & Princeton University 2010.

Lehman Brothers Holdings Inc Annual Report for year ended November 30, 2007.

Minsky, Hyman P. Ph.D. Can "It" Happen Again? A Reprise. Hyman P. Minsky Archive, http://digitalcommons.bard.edu/hm_archive/155. Paper 155, 1982.

Minsky, H. P. John Maynard Keynes, Columbia University Press 1975.

Minsky, Hyman P. The Financial Instability Hypothesis. Working Paper No. 74 May 1992.

Münchau, Wolfgang. The Meltdown Years. McGraw-Hill, 2010.

Reinhart, Carmen M. and Rogoff, Kenneth S. Growth in a Time of Debt. American Economic Review: Papers & Proceedings 100 (May 2010): 573–578

Reinhart, Carmen M. and Rogoff, Kenneth S. This Time is Different. Princeton Univeristy Press 2009.

Schumpeter, J. The Instability of Capitalism. The Economic Journal 38(151): 361-386, 1928.

Shiller, R. J. (2000). Irrational exuberance. Princeton, N.J., Princeton University Press.

Shiller, Robert J. and Akerlof, George A. Animal Spirits: How Human Psychology Drives the Economy, and Why It Matters for Global Capitalism. 1st Edition, Princeton University Press 2009.

Sherman, Matthew. A Short History of Financial Deregulation in the United States. Center for Economic and Policy Research 2009.

Sørensen, Peter B. and Whitta-Jacobsen, Hans J. Introducing Advanced Macroeconomics: Growth and Business Cycles. McGraw-Hill 2010.

Whalen, C.J. Economic Insecurity and the Institutional Prerequisites for Successful Capitalism. Journal of Post Keynesian Economics, Vol. 19, Nr. 2 (Winter), p. 155-169, 1998.

Woodford, Michael. Interest and Prices. Princeton University Press 2003.

Woodford, Michael. Monetary Policy in a World Without Money. International Finance 3:

BSc Thesis Student: Arvid Aagaard Jensen Supervisor: Peter Erling Nielsen University of Copenhagen, Spring 2013

25

229-260, 2000.

Websites:

Levi Institute: http://digitalcommons.bard.edu/hm_archive/index.4.html

New York Times:

- Alan Greenspan quote: http://www.nytimes.com/2008/10/24/business/economy/24panel.html?_r=0

- Krugman Blog: http://krugman.blogs.nytimes.com/2012/03/27/minksy-and-methodology-wonkish/