The Matter is listed for hearing on 9 - derc.gov.in Order/MYT_TO... · The Matter is listed for...

164

BEFORE HON’BLE APPELLATE TRIBUNAL FOR ELECTRICITY NEW DELHI APPELLATE JURISDICTION APPEAL No. OF _36_ 2008 IN THE MATTER OF: BSES RAJDHANI POWER LIMITED …APPELLANT VERSUS DELHI ELECTRICITY REGULATORY COMMISSION & ORS …RESPONDENTS I N D E X VOLUME-I S. No. Particulars 1 Reply on behalf of Respondent No.1 along with supporting Affidavit 2 ANNEXURE 1 : Copy of incomplete supporting affidavits and verification as originally filed by the appellant along with the Appeal. 3 ANNEXURE-2 : Copy of the presentation on Sales Projection on January 16, 2008. 4 ANNEXURE 3 : Copy of letter dated 1.4.2008 from Appellant to Respondent No.1 evidencing the sales figures for Feb 07 to Jan 08. 5 ANNEXURE-4 : : Copy of the letter dated August 07, 2007 addressed to the Appellant 6 ANNEXURE-5 Copy of the judgment dated reported as 2007 APTEL 11 34 (ELR) dated 9.11.05 in Appeal No. 114 & 115 of 05. 7 ANNEXURE-6 : Copy of “Working Group of Power” of 11 th Plan constituted by the Government of India

Transcript of The Matter is listed for hearing on 9 - derc.gov.in Order/MYT_TO... · The Matter is listed for...

1

The Matter is listed for hearing on 9th July 2008

BEFORE HON’BLE APPELLATE TRIBUNAL FOR ELECTRICITY

NEW DELHI

APPELLATE JURISDICTION

APPEAL No. OF _36_ 2008

IN THE MATTER OF:

BSES RAJDHANI POWER LIMITED

…APPELLANT VERSUS

DELHI ELECTRICITY REGULATORY COMMISSION & ORS

…RESPONDENTS

I N D E X

VOLUME-I

S. No. Particulars 1 Reply on behalf of Respondent No.1 along with supporting

Affidavit

2 ANNEXURE 1: Copy of incomplete supporting affidavits and verification as originally filed by the appellant along with the Appeal.

3 ANNEXURE-2: Copy of the presentation on Sales Projection on January 16, 2008.

4 ANNEXURE 3: Copy of letter dated 1.4.2008 from Appellant to Respondent No.1 evidencing the sales figures for Feb 07 to Jan 08.

5 ANNEXURE-4: : Copy of the letter dated August 07, 2007 addressed to the Appellant

6 ANNEXURE-5 Copy of the judgment dated reported as 2007 APTEL 11 34 (ELR) dated 9.11.05 in Appeal No. 114 & 115 of 05.

7 ANNEXURE-6: Copy of “Working Group of Power” of 11th Plan constituted by the Government of India

2

8 ANNEXURE-7: : Copies of the Certificates issued by the Electrical Inspector

9 ANNEXURE-8: Copy of the Minutes of the Meeting dated on 02.04.2008.

10 ANNEXURE-9: Copies of the order passed by the Hon’ble High Court of Delhi in WP (C) 14232/05 and 10105/05.

11 ANNEXURE-10: Copy of the order dated 29th August 2006 of the Hon’ble Appellate Tribunal in Appeal No. 84 of 2006

12 ANNEXURE-11: Copy of the Order dated 4th December, 2007 of the Hon’ble Appellate Tribunal in Appeal No. 100 of 2007

13 ANNEXURE-12: Copy of the letter dated 23.01.06 from the Appellant to the Respondent No.1 along with the Note of Respondent No. 1

14 ANNEXURE-13(Colly): Copies of letters dated 30.6.2006 and 14.08.2006 from Respondent No.1 to Appellant along with evidence regarding excessive profit earned by the group company REL.

15 ANNEXURE-14: Copy of minutes of the meeting dated 10.3.2006

16 ANNEXURE-15: Copies of documents submitted by the Appellant for the Capital Expenditure Schemes in the year 2004-05.

17 ANNEXURE-16: Copy of the format of Quality Progress Report.

18 ANNEXURE-17: Copy of the disclosure made by the Appellant under the Companies Act.

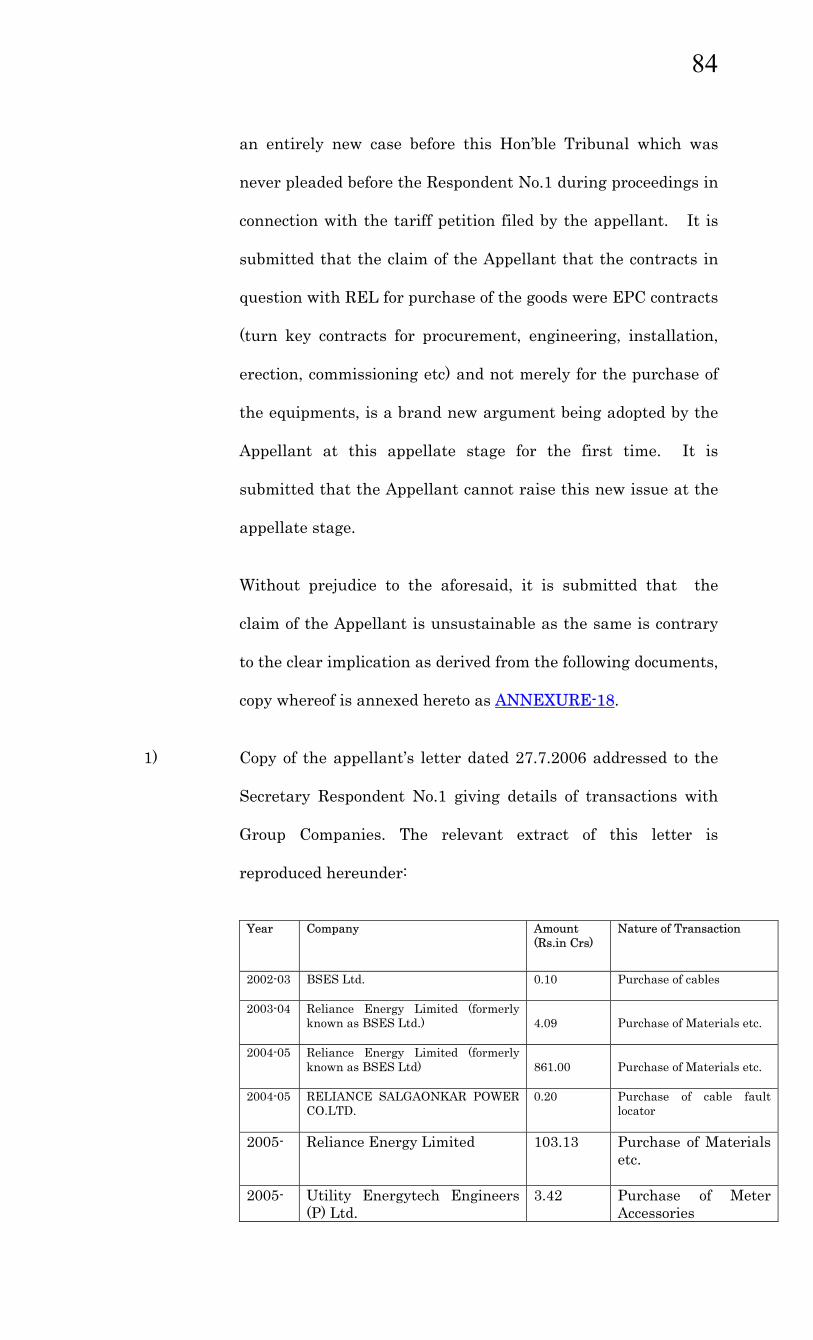

19 ANNEXURE-18: Copy of the appellant’s letter dated 27.7.2006 addressed to the Secretary Respondent No.1 giving details of transactions with Group Companies.

20 ANNEXURE-19: Copy of the notings on page 27 on the file of Respondent No.1’s office with reference to letter dated 4.10.04.

21 ANNEXURE-20: Copy of sample of purchase order

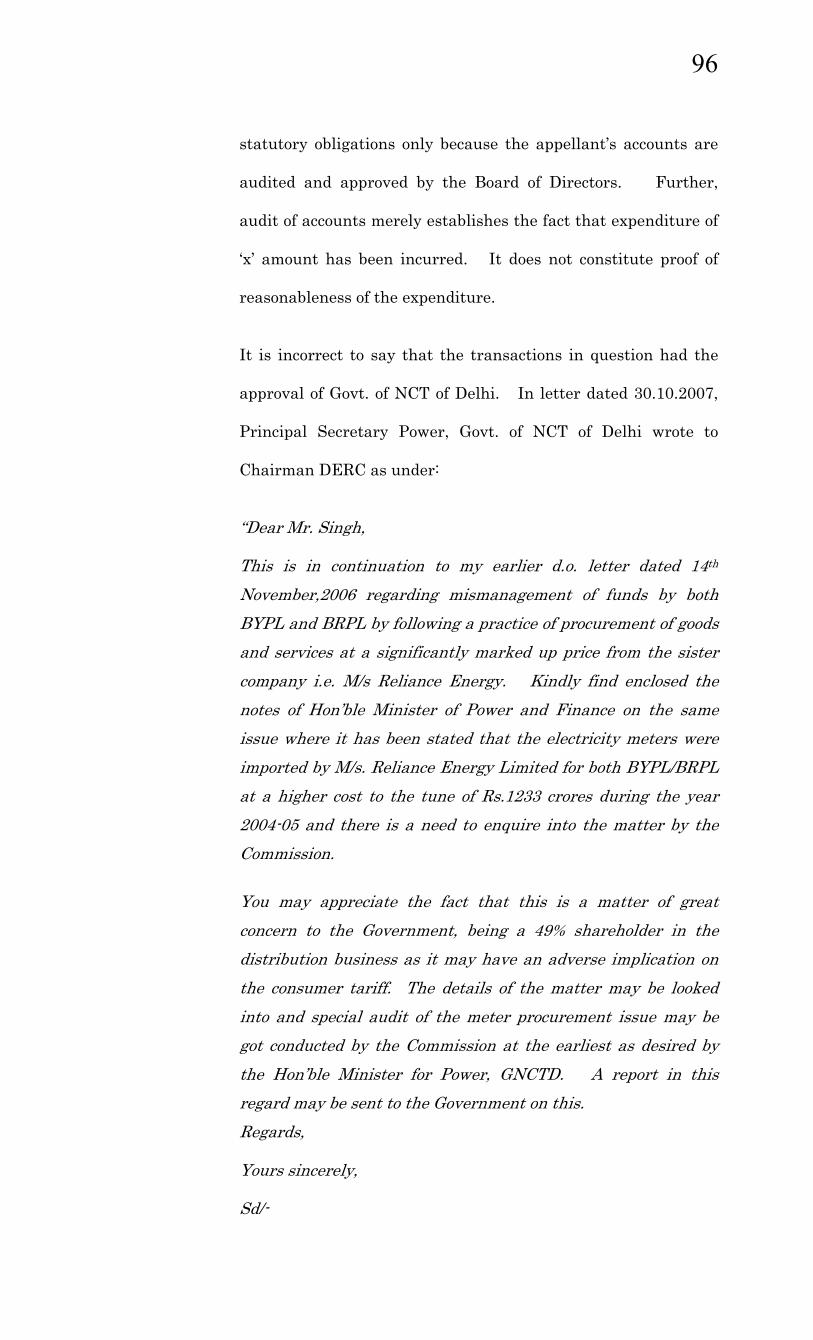

22 ANNEXURE-21: Photocopy of the letter dated 30.10.07 from Principal Secretary Power, Govt. of NCT of Delhi to Chairman, DERC.

23 ANNEXURE-22: Copy of the relevant extract of the MYT Petition

24 ANNEXURE-23: Copy of the letter dated 15th January, 2008

3

25 ANNEXURE-24: A copy of the relevant extract of the Tariff

Order of 2004-05.

26 ANNEXURE-25: Copy of the relevant extract of the Tariff Order 2006-07.

27 ANNEXURE-26: Copy of the relevant extract of the Tariff Order 2005-06

28 ANNEXURE-27: Copy of the relevant chart evidencing that the O & M expenses per unit, i.e. one of the highest.

29 ANNEXURE-28: Copy of the Writ Petition filed by Appellant

30 ANNEXURE-29: Copy of the letter letter dated 25th April 2006

31 ANNEXURE-30: Copy of the Tariff Order of 2005-06

32 ANNEXURE-31: Copy of the BRPL Tariff Order 2006-07.

33 ANNEXURE-32: Extract of the interest rate on the existing loans and the proposed loans which have been considered by the Respondent No.1 in determining the interest rate under the impugned order.

34 Reply to the Application for Interim Relief.

FILED THROUGH:

Luthra & Luthra Law Offices Counsel for Respondent No.1 103, Ashoka Estate, Barakhamba Road, New Delhi.-110 001 E-mail: [email protected] Tel: 41215100

New Delhi Dated:

1

BEFORE HON’BLE APPELLATE TRIBUNAL FOR ELECTRICITY

NEW DELHI

APPELLATE JURISDICTION

APPEAL No. __36__ OF 2008

IN THE MATTER OF:

BSES RAJDHANI POWER LIMITED

……APPELLANT

VERSUS

DELHI ELECTRICITY REGULATORY COMMISSION & ORS

…RESPONDENTS

REPLY ON BEHALF OF RESPONDENT No.1

MOST RESPECTFULLY SHOWETH;

At the outset, the Respondent No. 1 denies each and every averment and/or

submission made in the Appeal which is contrary to and inconsistent with

the averments made and facts stated in the present reply. It is submitted

that nothing stated in the Appeal may be deemed to have been admitted by

the Respondent No. 1 unless and until the same is expressly admitted in the

present reply. It is submitted that the Respondent No.1 (Delhi Electricity

Regulatory Commission/ DERC) is a State Regulatory Commission

constituted by the Government of NCT of Delhi on March 3, 1999 under the

provisions of the Electricity Regulatory Commissions Act, 1998 and Mr.

Amarendra.K. Tewary, Secretary is the duly authorized representative of

Respondent No.1 to, sign, verify, file and defend any case for and on behalf of

Respondent No.1 and as such competent to defend this appeal on behalf of

the Respondent No.1.

2

PRELIMINARY SUBMISSIONS

I. It is submitted at the very outset that the present appeal deserves

outright dismissal for the want of proper verification and supporting

affidavits as per the procedure of law. It is submitted that the

affidavits filed by the Appellant herein supporting the instant appeal

are contrary to the requirement of the rules as framed under the

Appellate Tribunal for Electricity (Procedure, Form, Fee and Record of

Proceedings) Rules, 2007. It is pertinent to mention here that the

answering Respondent had pointed out the apparent discrepancy and

brought the same to the notice of the Hon’ble Tribunal. It is submitted

that upon having noticed the same this Hon’ble Tribunal observed that

there has been a blatant and gross disregard of the requirements with

respect to mandatory need for verification of the instant appeal and

execution of the supporting affidavits, which were duly notarized

despite being incomplete in their content. A copy of such incomplete

supporting affidavits and verification as originally filed by the

appellant is annexed hereto as ANNEXURE-1. In view of such

incomplete affidavits having being filed this Hon’ble Tribunal directed

the Appellant to cure the defect appropriately. It is pertinent to

mention here that the appropriate manner to cure the technical defect,

as apparent in the Appeal of the Appellant, was to execute fresh

affidavits and verifications and to get the same duly notarized and file

afresh such affidavits. It is submitted that the appellant herein has, in

contradistinction to such appropriate way, made requisite changes in

the affidavits which had already been notarized and filed the same

after making necessary changes to the same. It is humbly submitted

that such act of the appellant amounts to gross professional

misconduct. The verifications of pleadings and filing of supporting

3

affidavits along with the same is not a mere formality. The importance

of the same has been brought to light by the Hon’ble Karnataka High

Court in T.L. Nagendra Babu Vs. Manohar Rao Pawar

ILR2005KAR884. Therefore it is submitted that the instant appeal is a

clear abuse of the process by the Appellant. In view of the act of breach

of professional ethics displayed by the Appellant, it is respectfully

submitted that the instant appeal is not maintainable and accordingly

deserves an outright dismissal.

II. The Appellant has played a fraud in the course of procurement of

capital goods from its related entity, namely, Reliance Energy Limited

(“REL”). This is evident from the documentary evidence on record

before this Hon’ble Tribunal. The Appeal merits dismissal on this

ground alone.

III. It is further submitted, without prejudice to the aforesaid, that a bare

perusal of the instant appeal makes it amply clear that the alleged

grievance of the Appellant is a result of the adherence by Respondent

No. 1 to the Delhi Electricity Regulation Commission (Terms and

Conditions for Determination of Wheeling Tariff and Retail Supply

Tariff) Regulations 2007 (the “MYT Regulations”). It is submitted that

in substance the alleged grievance is not so much towards the

Impugned Order as it is towards the MYT Regulations. These MYT

Regulations cannot be the subject matter of challenge in an appeal the

appropriate course of action for the appellant was to challenge the

MYT Regulations by way of filing writ petition under Article 226/227

of the Constitution.

IV. It is trite law that if there are to views possible, then merely because

an authority has taken one view, would not enable a Tribunal to

4

substitute its own view or the other view in the matter. There are no

malafides in passing the Impugned Order. For this reason alone the

Appeal must fail and be dismissed in liminne.

V. It is submitted that the issue of depreciation, being no longer res

integra, as held by this Hon’ble Tribunal cannot now be reopened by

virtue of the instant Appeal.

VI. The Appellant has not maintained accounts in compliance with various

regulations/ regulatory regime. Hence it is not entitled to any

allowances which cannot be verified by Respondent No.1 in absence of

such regulatory accounts.

The appeal is liable to be dismissed on the preliminary objections

mentioned hereinabove. Without prejudice to the foregoing preliminary

objections, parawise reply is as under:

REPLY ON MERITS:

1.1 It is submitted that the contents of para 1.1 are a matter of record and

merit no reply.

1.2 It is submitted that the contents of para 1.2 are a matter of record and

hence merit no reply. It is however, pertinent to mention here that the

Respondent No.1 is a State Regulatory Commission constituted by the

Government of NCT of Delhi on March 3, 1999 and it became of

operational from December 10, 1999. It is pertinent to mention that

the approach of Respondent No.1 towards regulation is driven by the

Electricity Act, 2003 (the Act), the National Electricity Plan, the

National Tariff Policy and the Delhi Electricity Reform Act, 2000 (the

DERA). It is submitted that the Act mandates Respondent No.1 to

take measures conducive to the development and management of the

5

electricity industry in an efficient, economic and competitive manner.

It is further submitted that the Respondent No.1 derives its powers

from DERA as well as the Act. The major function assigned to

Respondent No.1 under DERA are as follows:-

(a) to determine the tariff for ele tricity, wholesale, bulk, grid or retail and for the use of the transmission facilities.

c

r

(b) To regulate power purchase, transmission, distribution, sale and supply;

(c) To promote competition, efficiency and economy in the activities of the electricity industry in the National Capital Territory of Delhi;

(d) To aid and advise the Government on power policy;

(e) To collect and publish data and forecasts;

(f) To regulate the assets, prope ties and interest in properties concerned or related to the electricity industry in the NationalCapital Territory of Delhi including the conditions governing entry into, and exit from the electricity industry in such manner as to safeguard the public interest;

(g) To issue licenses for transmission, bulk supply, distribution or supply of electricity;

(h) To regulate the working of the licensees; and

(i) To adjudicate upon the disputes and differences between licensees.

The functions assigned to Respondent No.1 under the Act are as follows:

“Section 86 (1) The State Commission shall discharge the

following functions, namely:-

(a) determine the tariff for generation, supply, transmission and wheeling of electricity, wholesale, bulk or retail, as the case may be, within the State: Provided that where open access has been permitted to a category of

6

consumers under Section 42, the State Commission shall determine only the wheeling charges and surcharge thereon, if any, for the said category of consumers;

(b) regulate electricity purchase and procurement process of distribution licensees including the price at which electricity shall be procured from the generating companies or licensees or from other sources through agreements for purchase of power for distribution and supply within the State;

(c) facilitate intra-state transmission and wheeling of electricity;

(d) issue licences to persons seeking to act as transmission licensees, distribution license and ele tricity traders with respe t to their operations within the State;

es cc

(e) promote cogeneration and generation of electricity from renewable sources of energy by providing suitable measures for connectivity with the grid and sale of electricity to any person, and also specify, for purchase of electricity from such sources, a percentage of the total consumption of electricity in the area of a distribution licensee;

(f) adjudicate upon the disputes between the licensees and generating companies and to refer any dispute for arbitration;

(g) levy fee for the purpose of this Act;

(h) specify State Grid Code consistent with the Grid Code specified under Clause (h) of sub-section (1) of Section 79;

(i) specify or enforce standards with respect to quality, continuity and reliability of service by licensees;

(j) fix the trading margin in the intra-state trading of electricity, if considered, necessary;

7

(k) discharge such other functions as may be assigned to it under this Act.

(2) The State Commission shall advise the State Government

on all or any of the following matters, namely:-

(i) promotion of competition, efficiency and economy in activities of the ele tricity industry; c

r

(ii) promotion of investment in electricity industry; (iii) reorganization and restructu ing of electricity

industry in the State; (iv) matters concerning generation, transmission,

distribution and trading of electricity or any other matter referred to the State Commission by that Government.”

It is submitted that the Respondent No.1 has to work within the frame

work of the above stated powers and in addition thereto be guided by

the National Electricity Policy, National Tariff Policy and the National

Electricity Plan.

1.3 The contents of para 1.3 in so far as they relate to matters of record are

not denied. However, it is pointed out that the contention of the

Appellant that while determining the Annual Revenue Requirement

(the “ARR”), the Respondent No.1 has made various disallowance,

which are unsustainable in law and facts is completely devoid of any

legal force and sanctity. It is submitted that the Impugned Order is a

reasoned one and the allegation that the reasons are not elaborate does

not make the Impugned Order erroneous or unsustainable in law. It is

submitted that the determination of Appellant’s ARR has been a result

of detailed analysis and due consideration of the submissions made by

the Appellant and in accordance with the law and the procedure

established by law. It is submitted that the impugned order is a

8

product of the following procedure followed by the Respondent No.1 in

consonance with the law and the principles of natural justice namely,

• The distribution part of the electricity sector was privatized w.e.f.

July 1, 2002 and the tariffs in Delhi were governed by the Policy

Directions issued by Government of NCT, Delhi vide its notification

dated November 22, 2001 as amended on May 31, 2002.

• The validity of the said notifications ended on March 31, 2007 (i.e

FY 2002 FY 07, the “Policy Period”) and therefore the Respondent

No.1 decided to adopt Multi Year Tariff (MYT) for determination of

tariff in consonance with Section 61 of the Act.

• The Respondent No.1 issued a Consultative paper and draft MYT

Regulation for generation transmission and distribution to all

concerned stakeholders including the Appellant herein. On October

11, 2006 a notice was published in leading Newspapers seeking

comments from public and stakeholders.

• After due deliberation of the comments received from the public and

stakeholders and public hearing with respect to the same, the

Respondent No.1 issued the Delhi Electricity Regulation

Commission (Terms and Conditions for Determination of Wheeling

Tariff and Retail Supply Tariff) Regulations 2007 (the “MYT

Regulations”) vide notification dated May 30, 2007 for the period

FY 08-FY 11 (the “Control Period”).

• In consonance with the provisions of the MYT Regulations, the

Appellant filed its Petition for approval of its ARR under the said

Regulation on October 1, 2007.

9

• Thereafter Respondent No.1 conducted preliminary analysis of the

Petition submitted and observed certain discrepancies which are

reproduced hereunder for the sake of ready reference:-

“(a) Calculations regarding AT&C losses, O&M Expenses, RoCE, etc., are not in accordance with the provisions made in the MYT Regulations, 2007.

(b) The accumulated depreciation and the Capital Work in

Progress (CWIP) have not been excluded while calculating Regulated Rate Base (RRB) as provided in the MYT Regulations, 2007.

(c) Allocation statement to apportion costs and revenues to

respective businesses of wheeling and retail supply has not been duly approved by the Board of Directors as required under Clause 4.4 of MYT Regulations, 2007.

(d) The allocation statement specifying the cost of power

purchase that is attributable to trading activity of the BRPL has not been made as per Clause 5.30 of the MYT Regulations, 2007.

(e) Power purchase cost has been fixed without taking into

considerati n the estimated revenues through bilateral exchanges and UI.

o

(f) The baselines and performance trajectory for all quality

parameters has not been proposed as specified in the Delhi Electricity Supply Code and Performance Standards Regulations, 2007 and as per sub-clause (d) and (h) of Clause 8.3 of the MYT Regulations, 2007.

(g) The tariff proposed for each consumer category, slab wise

and voltage wise is not duly supported by a cost of service model, allocating the cost of business to each category ofthe consumer based on voltage wise cost and losses.

10

(h) The business plan filing in general and the capital investment plan thereof in particular are not as per Clause 8.3 of the MYT Regulations, 2007.”

• Thereafter Respondent No.1 conducted a hearing on October 22,

2007 for admission of the Petition and discussing the discrepancies

observed. The Respondent No.1 after hearing the arguments

issued an order dated October 26, 2007 along with the directions

which are reproduced hereunder for the sake of easy reference :

“(a) All the calculations regarding AT & C loss level, O&M

expenses, RoCE, etc. shall be worked out in accordance with the provisions given in the MYT Regulations, 2007.

(b) The calculations for Regulated Rate Base (RRB) shall be

arrived at using provisions given in the MYT Regulations, 2007 after excluding accumulated depreciation and the CWIP.

s

c

(c) An allocation statement to apportion cost and revenue of

respective businesses shall be duly approved by the Board of Directors of the Licensee as per Clause 4.4 of the MYT Regulations, 2007.

(d) The power purchase cost shall take into account apart

from other parameters, the e timate of revenues received through bilateral exchanges and UI.

(e) To submit for each consumer category, slab wise and

voltage wise tariff in accordance with Clause 8.7 of the MYT Regulations, 2007, duly supported by cost of service model, allocating the cost of business to each category ofconsumer as well as subsidy, if any, being granted by GoNCTD.

(f) The Petitioner/Licensee shall propose the baseline

performan e trajectory for all quality parameters as specified by Delhi Electricity Supply Code Performance

11

Standard Regulations, 2007 and as per Clause 7.2 of MYT Regulations, 2007.

(g) The Petitioner/Licensee is directed to take up the issue of

past period true-up expenses with the GoNCTD. The Petitioner/Licensee is further directed to propose tariff structure for recovery of afo esaid expenses in case GoNCTD is not agreeable to provide these expenses in the form of government support and same needs to be recovered through tariff.

r

(h) The Commission has observed that prayer Clause of the

Petitioner/Licensee is vague. The Commission directed the Petitioner to have specific reference to the prayer and also the Orders of Appellate Tribunal, High Court and Supreme Court etc on which the Licensee intends to rely upon. The Licensee is further directed to file a copy of such Orders on which they have placed reliance.

(i) The Commission also directed that as the issue of

consumer security deposit is not related to the Multi Year Tariff Determination and has already been disposed off by the Commission by way of a speaking Order, this issue should not be made a part of this petition. The representative of the Petitioner present during the hearing, agreed to withdraw this issue and take it up separately before an appropriate forum.”

• In view of the above stated discrepancies, vide the said order, the

Respondent No.1 directed the Appellant herein to submit requisite

information with respect to the issues raised within seven days of

the said order.

• Though, on November 5, 2007, the Appellant herein made a

response to the said order dated October 26, 2007 by way of filing

re-submissions, however, Respondent No.1 observed that the

Appellant had not complied with any of the directions stated supra.

12

• The Respondent No.1 in order to determine the ARR of the

Appellant interacted regularly with the Appellant to seek

clarifications and justifications on various issues analysis of the

Petition.

• In addition thereto, the Appellant and the Respondent No.1,

respectively, published Public Notices highlighting the salient

features of the Petition inviting comments from the stakeholders on

the Petition filed by the Appellant. Vide the said public notices

stakeholders were asked to file their objections and suggestions on

the Petition by December 10, 2007 which date was later revised to

December 31, 2007.

• In response to the said public notices that Respondent

No.1/Appellant received objections from 276 respondents thereto.

The date of public hearing was informed to all the parties who had

submitted their objections/suggestions and the said public hearing

was held in eight sessions to discuss the issues related to the

Petition filed by the Appellant for determination of ARR.

• It is only after careful examination of the various concerns and

issues voiced by the stakeholders and the Appellant herein and in

accordance with the provisions of the MYT Regulations that the

Respondent No.1 finalized the impugned order.

1.4 The contents of para 1.4 are wrong and hence denied. It is denied that

the impugned order has severely impacted the Appellant as a

consequence of the various disallowances. It is pointed out that there is

nothing in law or fact to support the correctness of the impact of

disallowances as suggested by the Appellant. In any event and as

13

would be evident from the succeeding paragraphs, the disallowances

by the Respondent No.1 are based on law and reason.

1.5 The contents of para 1.5 are misleading and hence denied. It is

submitted that the contention of the Appellant that the illegal

disallowances made by Respondent No.1 has gravely prejudiced the

operations of the Appellant is solely based on its own projections of the

figures vis-à-vis the Control Period which is nothing but a result of its

own whims and fancies. The contention raised by the Appellant is in

contradiction to the provisions of the MYT Regulations as explained

infra.

REPLY TO THE SUMMARY OF THE GROUNDS OF CHALLENGE

It is submitted that the contentions raised by the appellant as

“Summary of grounds of challenge” in the present appeal are dealt

with in detail in the reply of paragraph no. 8 and are not repeated

herein for the sake of brevity.

2-4. The contents of paras 2 to 4 are matters of record and hence, merit no

reply.

5. That the contents of paragraph No. 5 are denied for want of

knowledge.

6. REPLY TO THE FACTS OF THE CASE:

6.1 The contents of para 6.1 are matters of record and hence no reply.

6.2 The contents of para 6.2 are in so far as the same relate to matters of

record merit no reply.

14

6.3-6.5 The contents of para 6.3 to 6.5 are matters of record and hence

merit no reply.

6.6 The contents of para 6.6 are in so far as the same relate to matters of

record merit no reply. However, it is pertinent to mention that the

Hon’ble Supreme Court stated that the judgment is confined to the

facts of the case alone and the reasoning given therein is in the context

of the Policy Period, period of 5 years. The Respondent No.1 has duly

applied the judgment for the Policy Period. The judgment should not

be construed to apply for all times To come, especially when

subsequently the MYT Regulations have come into effect. The

Respondent No. 1 also craves leave to distinguish the judgment of the

Hon’ble Supreme Court from the facts and submissions in the instant

appeal.

6.7. The contents of para 6.7 are misleading and hence denied. It is

pertinent to mention herein that the Appellant is trying to portray that

the Respondent No. 1, pursuant to the passing of the order dated

15.02.07 by the Hon’ble Supreme Court in the matter of DERC Vs

BSES Yamuna Power Ltd & Ors. reported as (2007) 3 SCC 33, has not

followed the direction laid down by the Hon’ble Supreme Court while

passing order dated 22.09.06. It is respectfully submitted that

admittedly the Respondent No. 1 passed the order dated 22.09.06 prior

to the directions passed by the Hon’ble Supreme Court vide order

dated 15.02.07 with respect to depreciation.

6.8 The contents of para 6.8 are in so far as the same relate to the matter

of record merit no reply. However, it is pertinent to mention that the

Hon’ble Supreme Court stated that the judgment is confined to the

15

facts of the case alone and the reasoning given therein is in the context

of the Policy Period, period of 5 years. The judgment should not be

construed to apply for all times to come, especially since, subsequently

the MYT Regulations have been passed.

6.9. It is submitted that the contents of para 6.9 are a matter of record and

merit no reply.

6.10 It is submitted that the contents of para 6.10 are wrong and hence

denied.

6.11-6.12 It is submitted that the contents of paras 6.11 to 6.12 are a

matter of record and merit no reply.

6.13 It is submitted that the contents of para 6.13 are wrong and hence

denied. It is submitted that the minutes of the meeting on 27.7.2007

do not mention about any relaxation in the MYT Regulations 2007.

The detail comments with respect to the same have been offered in the

reply to para 8.4.1 infra, and the same are not being repeated here for

the sake of brevity.

6.14 The contents of para under reply in so far as the same relate to the

filing of ARR for wheeling business and ARR for retail supply business

for each year of the Control Period in accordance with MYT

Regulations 2007 on or around 1.10.2007 are a matter of record and

merit no reply. However, the contention of the Appellant that the

aforesaid filings were made by the Appellant on the understanding

that the Respondent No.1 would abide by its representation

considering the contentions and assumptions of the Appellant while it

would determine the tariff, including relaxation of the MYT

16

Regulations, where required is denied to the extent where the

Appellant is assuming that MYT Regulations would be relaxed as per

the Appellant’s requirement.

6.15 It is submitted that the contents of paras 6.15 absolutely wrong and

hence denied. It is submitted that the Respondent No.1 has acted in

strict adherence of the directions issued vide order of Hon’ble Supreme

Court dated 15.2.2007 and the order of the Hon’ble Tribunal dated

22.5.2007.

6.16-6.17 It is submitted that the contents of paras 6.16 to 6.17 are a

matter of record and merit no reply.

6.18 It is submitted that the contents of para 6.18 are denied. It is denied

that there are any reasonable grounds for relaxation of the provisions

of the MYT Regulations. Further it is denied that the Appellant by

filling the ARR Petition has not waived its right to challenge the MYT

Regulations.

6.19 It is submitted that the contents of para 6.19 in so far as the same

relate to the matter of record need no reply. However, it is submitted

that the contention of the Appellant that vide the impugned order, the

Respondent No.1 denied the Appellant its legal entitlement and/or

failed to provide the Appellant amount due and payable to it in law

and in facts is not correct and without any merit and hence denied.

7. The contents of para 7 are wrong and hence denied. It is denied that

there are any questions of law as raised by the Appellant which

deserve any adjudication by this Hon’ble Tribunal.

8. REPLY TO GROUNDS OF RELIEF WITH LEGAL PROVISIONS:

17

8.1 Sales Estimate 8.1.1 The contents of para 8.1.1 are false, misleading and hence denied. It is

submitted that the contention of the Appellant that the Respondent

No.1 has arbitrarily reduced sales estimates for the FY 2007-2008 and

FY 2008-2009 is contrary to abundantly clear facts and devoid of any

legal force.

8.1.2 The contents of para 8.1.2 are misleading and hence denied. It is

submitted that the contention of the Appellant that the sales

projections of Respondent No.1 deserves outright rejection as the

Respondent No.1 has without assigning any reasons reduced the year

on year growth to 7.3% for FY 2007-08 and 8.22% for FY 2008-09 is

contrary to the facts of the matter. A bare perusal of the order makes it

amply clear that the Respondent No.1 has considered the submissions

of the Appellant and came to its finding based on past trends and

projections made by the Appellant. It is submitted that not only has

the Respondent No.1 recorded the reasons of its coming to its finding

but also explained the methodology with respect to the same as

reproduced hereunder for the sake of ready reference:

“4.12 The Commission has analysed the sales projected by all the distribution licensees for the Control Period. The Commission has observed that the energy sale in the previous years of all the licensees does not show a uniform trend. Therefore, the Commission has considered the consolidated sales of a specific category (i.e. Domestic, Industrial, Commercial etc) of all the three DISCOMs namely, BRPL, BYPL and NDPL and has forecasted the same for the Control Period by considering an appropriate growth rate based on the past trends. The Commission has, thereby, calculated the weighted average share of sales of each distribution company in FY 06 and FY 07 in

18

a particular category and has allocated the consolidated sales forecasted for that category to the respe tive distribution company in the proportion of its weighted average share.”

c

“4.13. For deciding the appropriate growth rate for forecasting the energy sales for a particular category, the Commission has analysed the year-on-year variations in sales as well as the short term and long term trends in sales. The Commission has computed the CAGR for 2 years to 12 years duration. The Commission has, thereafter, considered the appropriate CAGR depending upon the consumer categories, consumption trend in recent period, excluding the abnormal variations.”

8.1.3 That the contents of para 8.1.3 are wrong and hence denied. It is

submitted that as per the Appellant’s own projections though the year

to year growth is 11.68% for the FY 2008 but the same is only 9.81%

for FY 2009. It is submitted that the Respondent No.1 had directed

the Appellant to make a presentation regarding the methodology

adopted by the Appellant for the sales forecast. It is submitted that

the Appellant made the said presentation on sales projection on

January 16, 2008. A copy of the said presentation is attached herewith

as ANNEXURE-2 It is submitted that on a perusal of the said

presentation, the Respondent No.1 observed certain discrepancies in

the sales figure submitted by the Appellant for the domestic sub-

categories and directed the Appellant to resubmit the correct estimates

and also to submit the assumption it has made with respect to increase

in energy consumption for various categories with respect to upcoming

commonwealth games. The Appellant admitted the inadvertent

mistake in its sales forecast and later submitted revised sales forecasts

vide letter no RCM-06-07/1030 dated 25 January 2008. However, it is

19

submitted that the Appellant failed to provide details of assumption

and reasoning which the Appellant has adopted for projection of sales

forecast with respect to upcoming commonwealth games for projecting

sales of various consumer categories. It is submitted that The

Respondent No.1 observed that the sales forecast of the Petitioner was

not appropriate. Some of the Respondent No.1’s observations were;

(a) Sudden increase in the specific consumption of the domestic

consumer, especially JJ Cluster and domestic consumer in 0 -

200 slab.

(b) The Appellant has projected increase in domestic sales @ 11%,

12%, 11% and 10% for FY08, FY09, FY10 and FY11, although

the year-wise increase in domestic sales in past three year were

13%,-8.23%, 6%.

(c) Sales projection for DMRC not in-line with the projection made by DMRC as given below:

Category FY08

FY09

FY 10 FY 11

Appella

nt

Commission/ DMRC

Appellant Commis

sion/ DMRC

Appellant Commis

sion/ DMRC

Appellant

Commission/

DMRC

DMRC 72 92 86 110

112

142

146 142

In fact, inspite of the lower projections by the Appellant for DMRC

sales, the Respondent No.1 has taken the sales projections for DMRC

based on DMRC’s estimates. Which shows that the Respondent No.1

has been transparent and fair in its projections for the sales. This also

shows that Appellant has not applied its mind while projecting sales

for various consumer categories.

(d) Increase in sales for Public Lighting lower than past years

20

The Appellant had no answer to the Respondent No.1’s queries and

was not able to explain the reasons. Therefore it is submitted that the

reduction in the sales estimates by Respondent No. 1 is not without

reason and on the contrary is in accordance with the justifications as

explained supra

Without prejudice to the aforesaid, it is submitted that the contention

of the Appellant is not only contrary to the abundantly clear facts but

also devoid of any legal sanctity. It is submitted that the Respondent

No.1 is a State Regulatory Commission performing quasi judicial

functions. It is a well established principle of law that a detailed order

is the requirement to be met by the decision of Court of law in order so

that the same is in consonance with the principles of natural justice.

However, as has been observed by the Hon’ble Supreme Court in the

matter titled S.N. Mukherjee vs. Union of India AIR 1990 SC 1984 the

same is not a requirement vis-à-vis the decision of a quasi judicial

authority. The Supreme Court while deliberating on the issue in the

matter stated supra observed as under:

“It may, however, be added that it is not required that the reasons should be as elaborate as in the decision of a Court of law. The extent and nature of the rea ons would depend on particular facts and circumstances. What is necessary is that the reasons are clear and explicit so a to indicate that the authority has given due consideration to the points in controversy.”

s

s

In light of the above, it is submitted that the Respondent No.1 being in

the nature of a quasi judicial authority is not required to deliver a

detailed order. It would meet the ends of justice if the same is

supported by reasons though not explained in a detailed manner.

21

8.1.4 &8.1.5 The contents of paras 8.1.4 & 8.1.5 are misleading and hence

denied. The contention of the Appellant that the rejection by

Respondent No.1 of the Appellant’s projections are unreasoned and

therefore in blatant disregard of this Hon’ble Tribunal directions in

Appeal No.266/2006 is devoid of factual accuracy. It is submitted that

as has been stated supra, the rejection of Appellant’s projections by the

Respondent No.1 are not without reason. On the contrary, it is

submitted that the Respondent No.1 has stated in the impugned order

the complete methodology adopted by it to derive the sales figures. It

is further submitted that a bare perusal of the impugned order makes

it amply clear that the Respondent No.1 has analyzed the sales

projected by all the distribution licensees for the Control Period. The

Respondent No.1 has observed that the energy sale in the previous

years of all the licensees does not show a uniform trend. The trend of

sales of Appellant as per their submission in MYT petition is given

below:

Year 2002-03 * 9 mts )

2003-04 * 2004-05 2005-06 2006-07 2007-08 projected by the petitioner

Sales in MUs 3328.41 4538.78 5364.52 5309.52 5872.14 6557.00

YOY growth ( % ) 18% -1% 11% 12%

It is submitted that a bare perusal of the above table makes it clear

that the increase in sales on year on year basis for FY 06-07 is 11%, for

FY 05-06 is -1% and FY 04-05 is 18%. Hence there is no definite

pattern of sales in the area of BRPL in the previous years.

Therefore, it is submitted that the Respondent No.1 has considered the

consolidated sales of a specific category (i.e. Domestic, Industrial,

Commercial etc) of all the three DISCOMs namely, BRPL, BYPL and

22

NDPL and has forecasted the same for the Control Period by

considering an appropriate growth rate based on the past trends. The

Respondent No.1 has, thereby, calculated the weighted average share

of sales of each distribution company in FY06 and FY07 in a particular

category and has allocated the consolidated sales forecasted for that

category to the respective distribution company in the proportion of its

weighted average share.

It is submitted that for deciding the appropriate growth rate for

forecasting the energy sales for a particular category, the Respondent

No.1 has analysed the year-on-year variations in sales as well as the

short term and long term trends in sales. The Respondent No.1 has

computed the CAGR for 2 years to 12 years duration. The Respondent

No.1 has, thereafter, considered the appropriate CAGR depending

upon the consumer categories, consumption trend in recent period,

excluding the abnormal variations.

It is submitted that the findings of the Respondent No.1 as reflected in

the impugned order is a result of a detailed reasoning. In order to

negate the contention of the appellant to the contrary it is submitted

that the Respondent No.1 believed that due to the commonwealth

games, the energy consumption would increase but this increase would

be mainly in Non-Domestic (Commercial) and Public lighting

categories. From a bare perusal of the impugned order it is amply clear

that that the answering Respondent has projected higher consumption

for these categories vis-à-vis projection of the Appellant. Accordingly

the answering Respondent has projected lower consumption vis-à-vis

Appellant’s projection for Domestic, Industrial and DMRC. Respondent

No.1 has factored in the Hon’ble Supreme Court’s order of relocation of

23

industries from the Appellant’s area to NDPL area for forecasting

industrial sales.

It is further submitted that for forecasting sales of bulk consumers like

DMRC and Railway, Respondent No.1 had relied on the interaction

with the consumer and projection made by them. Respondent No.1 has

used the same methodology as used by it in the previous tariff orders.

It is submitted that Respondent No.1 has calculated the weighted

averaged share of sales of Appellant in FY 2005-06 and FY 2006-07 in

a particular category and allocated the consolidated sales forecast for

that category in the proportion of its weighted average share. The

Respondent No.1 had considered the CAGR for domestic as 5.54%,for

non-domestic as 13.56%, for industrial as 1.03%,for public lighting as

12.19%, for agriculture & mushroom cultivation as (-)14.84% ,for

DMRC actual as submitted by DMRC and for others as 0.87%. The

CAGR for the last 7 years taken by the Respondent No.1 for

considering sales projection in MYT period has been tabulated below:

Year 7 yr 6 yr 5 yr 4 yr 3yr 2yr Approved

Domestic 5.54% 6.71% 4.21% 2.15% 0.86% 2.80% 5.54%

Non-Domestic 14.48% 15.55% 14.93% 13.56% 6.46% 7.92% 13.56%

Industrial 0.68% 0.84% 1.03% 10.00% 4.43% 1.64% 1.03%

Public Lighting

10.48% 12.19% 17.19% 18.11% 8.20% 7.59% 12.19%

Irrigation & Agriculture

-14.82% -16.64% -14.84% -19.75% -21.87% -13.91% -14.84%

Railway Traction -5.32% -11.16% 3.10% -2.06% -7.43% -11.54%

As projected by Railway

DMRC 90.73% 67.95% 31.80% as projected by DMRC

Others 0.87% 46.72% -4.39% 0.87%

TOTAL 6.70% 7.64% 6.83% 6.79% 3.85% 4.05%

It is submitted that in line with the above methodology, the

commission has approved energy billed in FY 2007-08 as 6305 MUs

24

against the actual of 5872 MUs for FY 2006-07, an increase of 433

MUs i.e. 7.37 % over the previous year.

It is further submitted that Respondent No.1 has also provided a

growth of 8.23% in sales for FY 2008-09 over FY 2007-08, 9% increase

for FY 2009-10 over FY 2008-09 and 8.29% for FY 2010-11 over FY

2009-10 which would take care of the growth of sales including that on

account of Commonwealth Game which are going to impact primarily

during FY 10-11.

It is submitted that the table below compares the sales forecast of the

Petitioner as per letter no RCM-06-07/1030 dated 25 January 2008 and

the Commission approved value.

S. No

Category FY08 FY08 FY09 FY09 FY10

FY 10 FY11 FY11

Appellant DERC Appellant DERC Appella

nt DERC Appellant DERC

1 Domestic 3190 3033.25 3553 3201.21 3935 3378.47 4325 3565.55

2 Non-domestic 2270 2239.48 2537 2543.13 2829 2887.96 3100 3279.54

3 Industrial 624 627.44 636 641.83 649 656.25 661 670.70

4 Public Lighting 148 152.8 160 171.42 173 192.31 187 215.75

5 Irrigation & Agriculture 32 24.8 32.03 21.12 32.03 17.98 3203 15.31

6 Railway 25 24.75 24 23.51 24 23.51 24 23.51

7 DMRC 72 92 86 110.00 112 142 146 142.0

8. Others 197 110.71 173 111.67 156 112.65 143 113.63

Total 6557 6305.22 7201 6823.89 7909 7411.14 8618 8025.99

It is clear from the above that the commission has considered increased

sales w.r.t. the projection of petitioner in case of Non domestic and

public lighting categories which will be the most impacted categories

on account of common wealth games.

At the cost of repetition it is submitted that as per the MYT

Regulations clause 4.10 to 4.12, Sales is an uncontrollable item and

would be trued up in subsequent years based on the actual sales.

25

8.2. Re: Distribution Loss Targets

8.2.1 The contents of para 8.2.1 are a matter of record and hence merit no

reply.

8.2.2 The contents of para 8.2.2 are misleading and hence denied. It is

submitted that the contention of the Appellant that determination of

Respondent No.1 seeking reduction of distribution losses without

specifying any reason to justify such a high reduction, is devoid of any

legal force and lacks factual accuracy. Contrary to the contention of the

Appellant that Respondent No.1’s reduction of the distribution losses is

in blatant disregard of the past trend, it is submitted that the

Respondent No.1 has followed the Aggregate Technical and

Commercial (AT&C) loss reduction trajectory as per regulations. For

the sake of clarification it is most respectfully submitted that

Respondent No.1 has assumed collection efficiency of 99.00%, 99.25%,

99.50% and 99.50% for FY08, FY09, FY10 and FY11 respectively as

followed by in its earlier Tariff Order. It is further submitted that

Respondent No.1 has derived Distribution losses for each year of the

Control Period for the Appellant from AT&C loss target after assuming

reasonable Collection Efficiency as explained hereunder:

Distribution Losses = 1 – (Energy Billed in MUs / Energy

Purchase in MUs)

Collection Efficiency = Revenue Collected (Rs Cr) / Revenue

Billed (Rs Cr)

= (Sales Realized in MUs * Average Billing Rate)/ (Energy Billed

in MUs * Average Billing Rate)

= (Sales Realized in MUs)/ (Energy Billed in MUs)

Distribution Losses = 1- ((1- AT&C Losses)/ Collection

Efficiency)

26

= 1 – (Sales Realized in MUs / Energy Purchase in MUs)/ (Sales

Realized in MUs)/ (Energy Billed in MUs)

= 1 – Energy Billed in MUs/ Energy Purchase in MUs

8.2.3 The contents of para 8.2.3 are misleading and hence denied. It is

further submitted that the contention of the Appellant with respect to

fixing higher target of distribution loss for the FY 07-08 is completely

misplaced and the argument that the loss reduction of 9.68%. in one

year is difficult to achieve more so when the Tariff Order itself has

been notified just one month before the end of FY2007-08 is not in

consonance with the sectoral practice. It is submitted that the

Appellant is well aware of the practice that distribution loss is

consequent of AT&C loss target. Despite the high distribution loss in

FY 2006-07, the Appellant was able to achieve AT&C targets because

of high collection efficiency of 108.8% thereby resulting in more

revenue. It is submitted that this incremental revenue and increased

collection efficiency offsets the incremental cost of power purchase on

account of higher distribution losses.

8.2.4 - 8.2.7 The contents of paras 8.2.4 to 8.2.7 are misleading hence denied.

It is submitted that Distribution targets are a consequent of AT&C

losses target arrived at after taking into account the collection

efficiency which has been considered as per the following table:

YEAR BRPL SUBMISSION COMM APPROVED

FY 08 104.66% 99.00% FY 09 100.28% 99.25% FY 10 99.62% 99.50% FY 11 99.63% 99.50%

27

Accordingly, the Respondent No.1 has set the following Distribution

loss targets trajectory for BRPL for the control period:

YEAR 2007-08 2008-09 2009-10 2010-11 Distribution Losses (%)

25.96 22.88 19.83 16.58

In light of the aforesaid, with respect to the contention of the Appellant

that the distribution loss targets as fixed by the appellant are

unachievable in view of the fact that the Impugned Order was notified

only one month prior to the closing of the financial year, it is submitted

that the Appellant knew the required achievement levels of AT&C

losses and thereby distribution losses well in advance as these were set

in accordance with the MYT Regulations which were issued in May

2007. Accordingly the contention of the appellant is completely

misplaced.

8.2.8 The contents of para 8.2.8 are misleading and hence denied. It is

submitted that the contention of the Appellant in the para under reply

is completely misplaced. The Respondent herein most respectfully

submits that the AT&C loss targets are binding on the Appellant while

distribution loss levels are not, though power purchase depends upon

distribution loss levels. It is submitted that in case the Appellant is

able to achieve higher collection efficiency than assumed by

Respondent No.1 for reaching the target AT&C loss level, it’s

distribution losses would be higher than the approved distribution

losses, which would result in higher power purchase quantum and cost.

At the same time, as the collection efficiency is higher, it would also

recover additional revenue than the answering Respondent’s projection

which would be balanced out with higher power purchase cost.

28

8.3 Re: Power Purchase

8.3.1 The contents of para 8.3.1 are wrong and hence denied. It is most

respectfully submitted by the Respondent No.1 that Power purchase

expense being the single largest component in the ARR of Distribution

Companies, has been analyzed with utmost care and diligence by the

Respondent No.1 with prudent checks. It is further submitted that the

contention of the Appellant that the Respondent No.1 has approved

power purchase of 8515 MUs in FY 2007-08 and 8849 MUs in FY 2008-

09 which is lower than 9122MU as approved by the Respondent No. 1

for FY 2006-07, is without any merit. It is submitted that the

Appellant is well versed with the fact that power purchase cannot be

analyzed in isolation and has to be considered along with the sales

approved, sales realized and AT&C losses.

8.3.2 The contents of para 8.3.2 are wrong and hence denied. It is submitted

that the Respondent No.1 has projected the Power Purchase

Requirement of the Appellant based on the sales approved and

distribution losses for each year of the Control Period i.e.

Power Purchase Requirement in MU = Sales Projection Approved by

the Respondent No.1/ (1- Distribution Loss Level Approved by the

Respondent No.1)

It is submitted that the Answering Respondent has explained the

methodology of sales forecast in paragraph 8.1.5 above, the contents

whereof are not repeated here for the sake of brevity. In addition, it is

submitted that the Respondent No.1 has arrived at the distribution

losses from AT&C losses and collection efficiency. It is submitted that

the Respondent No. 1 has approved 8515 MUs for FY 2007-08 by

taking into account the AT & C losses specified in the Regulations

29

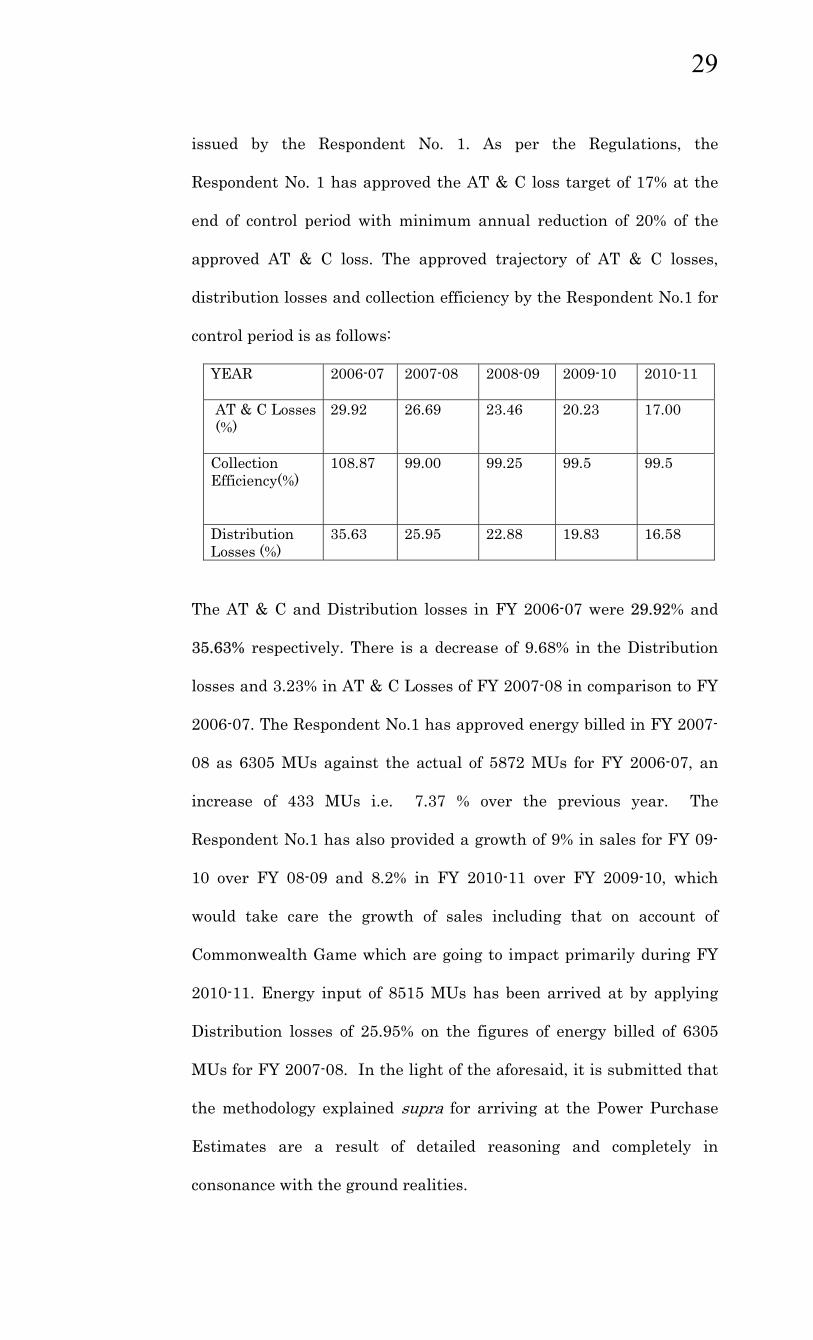

issued by the Respondent No. 1. As per the Regulations, the

Respondent No. 1 has approved the AT & C loss target of 17% at the

end of control period with minimum annual reduction of 20% of the

approved AT & C loss. The approved trajectory of AT & C losses,

distribution losses and collection efficiency by the Respondent No.1 for

control period is as follows:

YEAR 2006-07 2007-08 2008-09 2009-10 2010-11

AT & C Losses (%)

29.92 26.69 23.46 20.23 17.00

Collection Efficiency(%)

108.87 99.00 99.25 99.5 99.5

Distribution Losses (%)

35.63 25.95 22.88 19.83 16.58

The AT & C and Distribution losses in FY 2006-07 were 29.92% and

35.63% respectively. There is a decrease of 9.68% in the Distribution

losses and 3.23% in AT & C Losses of FY 2007-08 in comparison to FY

2006-07. The Respondent No.1 has approved energy billed in FY 2007-

08 as 6305 MUs against the actual of 5872 MUs for FY 2006-07, an

increase of 433 MUs i.e. 7.37 % over the previous year. The

Respondent No.1 has also provided a growth of 9% in sales for FY 09-

10 over FY 08-09 and 8.2% in FY 2010-11 over FY 2009-10, which

would take care the growth of sales including that on account of

Commonwealth Game which are going to impact primarily during FY

2010-11. Energy input of 8515 MUs has been arrived at by applying

Distribution losses of 25.95% on the figures of energy billed of 6305

MUs for FY 2007-08. In the light of the aforesaid, it is submitted that

the methodology explained sup a for arriving at the Power Purchase

Estimates are a result of detailed reasoning and completely in

consonance with the ground realities.

r

30

8.3.3-8.3.5 The contents of paras 8.3.3 to 8.3.5 are misleading and hence

denied. It is submitted that the contention of the Appellant that

Respondent No.1 has disregarded material facts while making its

determination with respect to the proposed power purchase is based on

misplaced and inaccurate facts. It is submitted that the reduction as

reflected by the Respondent No.1 in the impugned order is in

consonance with the reasoning as stated supra and the same may be

read with respect to the contents of the para under reply. For the sake

of clarification it is submitted that the Respondent No.1 has reduced

the power purchase for FY 2007-08 from 9122 MUs in (2006-07) to

8515MUs which is 607 MUs i.e. 6.65% less than the power purchased

in FY 2006-07. It is submitted that the higher quantum of the power

purchase in FY 2006-07 was required because of high Distribution

losses of 35.63% in comparison to 25.95% in FY 2007-08, a difference of

9.68%. It is further submitted that the Appellant has stated that the

actual power purchase of 7342MU upto December 2007 has been

submitted to the Respondent No.1 and the total power purchase

approved for FY 2007-08 is 8515MU i.e. only 1173MU is available for

three months which the Respondent No.1 is alleged to have arrived

that without taking into consideration the fact that the actual drawl

for the corresponding period of the previous year was 1920MU. As per

the Appellant if power purchase for January to March of FY 06-07 i.e.

1920 MUs are considered for the corresponding period of FY 07-08, the

total power purchase for FY 07-08 comes to 9262 MUS i.e. 747 MU

more than approved by the Respondent No.1. Further, the Appellant

had submitted the AT&C losses till Nov-07 as 34.24% which was

higher than the year target of 26.69% resulting in higher power

31

purchase of about 554 MUs. It is however submitted that even

considering the total power purchase of 9262 MUs as indicated by

Appellant, it would result in sales realization of 6790 MUs by taking

into consideration 26.69 % AT&C losses for FY 2007-08 against the

6242 MUs as approved by the Commission. Hence BRPL will realise

548 MUs more than approved by the Respondent No.1. The average

billing rate approved for Appellant for FY 07-08 is 481.35 Ps/kWh and

it results in 264 crore rupees more revenue from increased realized

units as illustrated below:

S.No As per

Appellant As per MYT order

Actual Upto Jan

08 as submitted by BRPL

1 Units Input upto Dec 07 7342.00 2 From Jan-Mar08 1920.00 3 Total Input 9262.00 8515.00 8021.6 4 Extra input as per

Appellant (A3-B3) 747.00

5 Avg. power purchase cost (Ps/Kwh)

257.13

6 Extra cost in Crore(4*5/1000)

192.08

7 Approved AT & C losses 26.69 26.69 31.72 8 Units realised as per

above AT &C (MU) 6789.97 6242.35 5477.15*

9 Extra units realised(MU)(A12-B12)

547.63

10 Avg.billing rate (Ps/Kwh) 481.35 11 Extra revenue realised in

Crore(C9*C10/1000) 263.60

In addition to the aforesaid it is submitted that as January to March is

a comfortable period, the Appellant is likely to realise gross sales

around 6924 MUs for the year 2007-08, which should result in

increased revenue of Rs. 328 crores over the sale figure of the order.

This is evident from the rolling sales figure for Feb. 2007 to Jan. 2008

as submitted by the Appellant vide its letter dated 1.4.2008. A copy of

the said letter is annexed hereto as ANNEXURE-3.

32

8.3.6-8.3.9. The contents of paras 8.3.6 to 8.3.9 are misleading and hence

denied. It is submitted that the impact, as worked out by the

Appellant, of the power purchase quantum laid down by the

Respondent No.1 in the impugned order is based on inaccurate

calculations. It is submitted that while projecting power purchase

quantum and cost for FY 2007-08, the Respondent No.1 has included

actual power purchase from bilateral and short term arrangements

upto December, 2007. For January 2008 to March 2008 an additional

100 MUs from bilateral purchase through intra state sources has been

estimated by the Respondent No.1 while approving the power purchase

cost for FY 2007-08. The actual purchase through bilateral/intra state

& UI as per the SLDC for January-March, 2008 has been produced

below :

(in MUs)

Bilateral purchase 7.62

Intra state purchase 154.94

Net UI purchase 65.35

Total purchase including UI 227.91

Bilateral sale 253.41

Intra state sale 14.5

Total sale 267.91

Net sale 40.00

It is submitted that from the above table it is very much clear that

despite purchasing peak power as envisaged, the Appellant has a net

sale of 40 MUs which has resulted into a Net Revenue of Rs. 69 crores

for Appellant during the period January-March, 2008. The power

purchase cost for FY 2007-08 comes to Rs. 256.40 Ps./Kwh as per

SLDC submission in line with approved power purchase cost of Rs.

33

252.43. It is submitted that for the remaining control period, the

Respondent No.1 has assumed that 5% of net annual power

requirement shall be required to be sourced through bilateral

purchases and short term arrangements with trading companies for

meeting seasonal peak demands in summer and winter months.

Further, the Respondent No.1 has considered that 25% of such short

term peak power shall be available from intra state sources and 75%

through inter state sources. Further, the Respondent No.1 has

assumed that 20% of deficit power procured from inter-state sources

will be coming through banking arrangement and balance is bilateral

purchase through short term arrangements/trading companies. In

addition the Respondent No.1 has taken 100 MUs as additional power

purchase through intra state sources for meeting peak demand during

January, 2008 to March, 2008. It is also submitted that, as has been

explained supra, the Power purchase cost is an uncontrollable

parameter and would be trued up at the end of each financial year.

It is further submitted that the Appellant has submitted a gap of Rs

245 crore against power purchase without giving any calculation for

FY 2008-09, whereas Respondent No.1 has considered the above

methodology and regulated losses for deriving the figures for FY 2008-

09. The approved sales of Appellant for FY 2008-09 is 6824 MUs

against the fig. of 6305 MUs in FY 2007-08 ,an increase of 8.23%.

Further the power purchase cost will reduce in FY 2008-09 because

additional allocation of 80 MW by Delhi Government from unallocated

quota which was made effective after issue of impugned orders. This,

at PLF of 80% would result into an availability of 64 MW which, if

available round the clock, would result into an additional energy of 560

34

MUs which would be available at the regulated price. Thus, it would

further bring down the Appellant’s power purchase cost for FY 2009.

Re: Non inclusion of Reactive Energy Charges and Rebate arising out of

timely payments made by the Appellant to Delhi Transco Ltd

(DLT/Transmission Company) towards the power pur hase costs. c

8.3.10-8.3.18 The contents of paras 8.3.10-8.3.18 are wrong and hence denied.

It is submitted that the Respondent No.1 has allowed the reactive

energy charges of Rs.0.85 crores for the Appellant for FY 06 as directed

by the Hon’ble Tribunal vide its order dated May 23, 2007. It is

submitted that the reactive energy charges as approved by the

Respondent No.1 in the impugned order are strictly in consonance with

the directions of this Hon’ble Tribunal and as claimed by the Appellant

in the MYT Petition. It is submitted that since the Respondent No.1

did not allow the reactive energy charges under power purchase to the

Appellant in FY 06, the Hon’ble Tribunal had vide its order dated May

23, 2007 directed the Respondent No.1 to allow the same. Therefore, it

is submitted that in consonance with the direction of the Hon’ble

Tribunal the Respondent No.1 has allowed the reactive energy charges

in the impugned order to the extent of Rs.0.85 crores for the FY 06 as

claimed by the Appellant in the MYT Petition. It is submitted that the

Respondent No.1 has not followed any different methodology for the

FY 2007.

In the light of the aforestated facts, it is vehemently denied that the

Respondent had disallowed reactive energy charges as claimed by the

Appellant in the instant Appeal. It is submitted that the said issue of

35

disallowance of reactive energy charges to the extent of Rs.0.66 crores

has been raised for the first time. It is submitted that the discrepancy

was observed by the Respondent when it pointed out that in the MYT

Petition the Appellant had claimed power purchase expenses for FY 07

as Rs 2102.96 Crores. However, it was brought to the knowledge of the

Appellant that as per the Delhi Transco Limited’s (DTL) account, the

revenue on account of power purchase from Appellant was Rs 2095.91

Crores. The Appellant in reply to the aforesaid submitted that the

difference of 7.05 crores (between the power purchase cost submitted

by the Appellant and that submitted by the Delhi Transco Limited) is

on account of dispute on rebate calculation methodology adopted by

DTL with respect to which the Appellant had already filed a Petition

before the Hon’ble Respondent No.1. It is however pertinent to

mention here that the Respondent No.1 was never informed by the

Appellant that this difference is also due to reactive energy charges. It

is submitted that the whole issue of disallowance of reactive energy

charges to the extent of Rs.0.66 crores has been brought to the

knowledge of Respondent for the first time by way of the instant

Appeal. In support thereof it is pertinent to mention that neither Table

64 on Page 129 of the MYT Petition nor Form A1 as referred on page

211 in the MYT petition indicate the reactive energy charges. In view

of the aforesaid, it is submitted that the whole issue of alleged

disallowance of reactive energy charges to the extent of Rs.0.66 crores

is a mere afterthought and not supported by any facts.

8.3.19-8.3.26 The contents of paras 8.3.19-3.8.26 are misleading and

hence denied. It is submitted that the Appellant has with respect to

the rebate payment to DTL observed in paragraph 3.145 of the

impugned order that “dispute on rebate calculation methodology

36

adopted by DTL against which the Petitioner has already submitted

petition to the Commission. As the adjudication on the matter is

awaited from the Commission, the Commission approves power

purchase cost for FY07 at Rs 2095.91 Cr, provisionally. The

Commission will allow additional power purchase cost to the Petitioner

depending upon the outcome of the case”. It is submitted that a bare

perusal of the aforesaid observation makes it clear that the

Respondent No.1 has not denied expenses on this account to the

Appellant. It has only been determined by the Respondent No.1 that

in the circumstance of the dispute relating to rebate calculation

pending adjudication before the Respondent No.1, it is prudent for the

Respondent No.1 to provisionally allow the power purchase cost as per

DTL submission subject to the condition that the Respondent No.1

would allow Additional Power Purchase cost to the Appellant

depending upon the outcome of the pending litigation. It is submitted

that the approach adopted by the Respondent No.1 to allow

provisionally the power purchase cost as per DLT submission is in no

manner arbitrary.

8.4 Re:Aggregate Technical & Commercial Losses (AT&C) Levels:

8.4.1 The contents of para 8.4.1 are wrong and hence denied. It is submitted

that the contention of the Appellant that the AT&C loss levels set up

in the MYT Regulations and the Respondent’s approach in fixing the

targets are contrary to the regulatory practice and the sectoral

realities in India is completely misplaced. It is submitted that the

AT&C loss reduction targets for the Appellant as specified in the MYT

Regulations 2007 have been fixed considering the past achievements

on loss reduction, capital expenditure programmes, consumer mix of

37

Delhi, metering status etc. It is further submitted that the meeting on

July 27, 2007 referred to by the Appellant did not imply any relaxation

in the regulation of the Respondent No.1 as is evident from the

minutes of the meeting and a copy of the letter dated August 07, 2007

addressed to the Appellant which is annexed herewith as

ANNEXURE-4.

8.4.2 The contents of para 8.4.2 are misleading and hence denied. It is

submitted that the contention of the Appellant that the Respondent

No.1 ought to relax the AT&C levels fixed under MYT Regulation is

without any legal force or sanctity. It is submitted that the

Respondent No.1 derives its powers from the provisions of DERA and

the Electricity Act. As per the provisions of the aforementioned

statutes the Respondent No.1 has to work within the framework of the

MYT Regulations and it cannot to go beyond the same.

8.4.2 & 8.4.3 The contents of paras 8.4.2 & 8.4.3 are misleading and hence

denied. It is submitted that the argument of the Appellant that the

refusal by the Respondent No.1 has gravely prejudiced the Appellant,

who now has a potential burden of Rs.57 crores (approx. in FY 08) and

Rs.111 crores (approx. in FY 09) is completely misplaced. The

Respondent No.1 most respectfully submits that in case, the Appellant

is able to achieve higher collection efficiency than assumed by the

Respondent No.1 for reaching the target AT&C loss level, it’s

distribution losses would be higher than the approved distribution

losses, which would result in higher power purchase quantum and cost.

At the same time, as the collection efficiency is higher, it would also

recover additional revenue than the Respondent No.1’s projection

which would be balanced out with higher power purchase cost.

38

Accordingly, the Respondent No.1 has set the following AT&C and

distribution targets trajectory for Appellant for the control period:

YEAR 2007-08 2008-09 2009-10 2010-11

AT & C Losses (%)

26.69 23.46 20.23 17.00

Distribution Losses (%)

25.96 22.88 19.83 16.58

8.4.4 & 8.4.5 The contents of paras 8.4.4 & 8.4.5 are wrong and hence

denied. It is submitted that the contention of the Appellant that the

Respondent had failed to exercise its discretionary powers to relax the

provisions of the MYT Regulation despite there being strong and

compelling grounds for the exercise of the said power is devoid of any

legal force. It is submitted that the powers to relax the MYT

Regulations on fixation of AT&C levels is discretionary power and the

discretion to use the same lies with the Respondent No.1. The

Respondent No.1 has not acted arbitrarily and has exercised

reasonable skill and care while passing the Impugned Order.It is

submitted that the Appellant cannot mandate the Respondent No.1 to

use its discretionary powers in a particular manner in the absence of

malafides.

It is further submitted that the contention of the Appellant that the

AT&C losses submitted by the Appellant were not accepted by the

Respondent No.1 despite good and cogent reasoning before the

Respondent No.1 is based on inaccurate facts and hence denied. In any

event, without prejudice to the other submissions of the Respondent

No. 1, it is submitted that the Appellant did not make any specific

prayer in their prayer clause of the MYT/ARR petition for considering

39

relaxation in the regulation in respect of loss target specified by the

Respondent No.1.

The Respondent No.1 had issued and notified MYT Regulations on

30th May, 2007 specifying the AT & C losses level to be achieved by

distribution companies at the end of control period. It had fixed AT &

C loss level of 17% for Appellant. These regulations were framed under

a valid process of law taking into consideration the views of various

stakeholders involved. While admitting the petition of Appellant, the

Respondent No.1 had issued an admission order no. 51/2007 dated

26.10.2007, wherein the Appellant submission of loss level targets was

not accepted by the Respondent No.1 and they were directed to follow

the targets given in the regulations. The relevant extracts of the said

Order is reproduced below :

a) “ All the calculations regarding AT&C loss level, O&M expenses, RoCE, etc. shall be worked out in accordance with the provisions given in the MYT Regulations, 2007.

It is further submitted that even as per the submission made by

Appellant vide their letter dated 1.04.2008, the rolling figures for loss

level from the period February 2007 to January 2008 stand at 25.04%

which are well within the target for 07-08.

Without prejudice to the aforesaid it is submitted that the issues

regarding the Hon’ble Tribunal’s jurisdiction to review the regulations

framed by the Respondent No.1 has been dealt at length in the matter

of Neyveli Lignite Corporation Ltd. Vs Tamil Nadu Electricity Board

and Others 2007 APTEL 1134(ELR), wherein the special bench

comprising of Hon’ble Justice Anil Dev Singh, Chairperson, Hon’ble

Justice E. Padmanabhan (Member Judicial) and Hon’ble Justice H. L.

40

Bajaj (Member Technical) held that the Hon’ble Tribunal has no

jurisdiction to examine the validity of the regulations in exercise of its

appellate jurisdiction under Section 111 of the Electricity Act, 2003. It

was further held that even, under Section 121 of the Electricity Act,

which confers on the Hon’ble Tribunal the supervisory jurisdiction on

the Respondent No.1, the Hon’ble Tribunal cannot examine the

validity of regulations framed by the Respondent No.1 as the Hon’ble

Tribunal can only issue orders, instructions or directions to the

Respondent No.1 for the performance of its statutory functions under

the Act. A copy of the said judgment is annexed hereto as

ANNEXURE-5.

8.4.7-8.4.9 The contents of paras 8.4.7-8.4.9 are misleading and hence

denied. It is submitted that the contention of the Appellant that the

Respondent No.1 failed to consider the observations of the Task Force

on Distribution Loss Reduction (Abraham Committee) is completely

devoid of any force. It is submitted that the recommendations of the

Abraham Committee Task Force on reduction of AT & C losses level as

indicated by Appellant, have neither been accepted by the Government

till date nor any policy on AT&C losses has been made by Government

of India as per Section 3 of Electricity Act. Hence, these

recommendations are not binding on the Regulatory Commissions and

therefore the contention of the Appellant is without any substance. It

is however pertinent to mention that the AT&C loss reduction targets

for the Appellant as specified in the MYT Regulation, 2007 have been

fixed considering the past achievements on loss reduction, capital

expenditure programs, consumer mix of Delhi, metering status, etc. It

is submitted that 212 towns in the country have brought down the

41

AT&C losses below 20 percent which also consist of 169 such towns

that have brought down the AT&C losses below 15 percent.

In addition to the aforesaid, the Respondent No.1 has also considered

the loss levels in similar private urban distribution licensees, such as

Ahmedabad Electricity Company, BEST and BSES, Mumbai, where

AT&C losses were in the range of 10 percent to 14 percent in FY05. It

is further submitted that referring to the recommendation of “Working

Group of Power” of 11th Plan constituted by the Government of India,

the relevant extracts of which are annexed hereto as ANNEXURE-6,

the urban areas of the country were expected to reduce their losses to

15% by the end of 11th Plan i.e. at the end of FY 2012. The Respondent

No.1 states that Delhi being an urban area with very small number of

agricultural consumers and almost 100 percent retail consumer

metering, loss reduction can be achieved at much faster rate.

8.4.10- 8.4.12 It is submitted that the contents of paras 8.4.10- 8.4.12 are

wrong and hence denied. It is submitted that the contention of the

Appellant that despite their being a difference in the base year AT&C

loss for NDPL and the Appellant, the two DISCOMS have been given

the same target of 17% at the end of the Control Period is

unsustainable in law and in fact. It is submitted that the said

contention of the Appellant instead of supporting the Appellant’s case

brings to the fore the Appellant’s own shortcoming. It is submitted

that Appellant’s claim of comparison of Appellant’s loss level targets

with that of NDPL does not sound reasonable as the opening level of

losses of both, NDPL and the Appellant were fixed at the same level of

48.1% at the beginning of the Policy Period and both were required to

reduce the losses by 17% at the end of the Policy Direction Period. It is

42

submitted that in the light of the aforesaid the claim of the Appellant

of discriminatory treatment is completely observed and deserves to be

outrightly rejected.

8.4.13-8.15 It is submitted that the contents of paras 8.4.13 to 8.4.15 are

misleading and hence denied. It is submitted that the contention of

the Appellant that the comparison of the Appellant with entities like

BEST, AEC, SEC and CESE is a comparison of unequals and therefore

unsustainable in fact is devoid of any force. It is submitted that all

these are distribution companies in urban areas with very small

number of agricultural consumers and almost 100 percent retail

consumer metering where loss reduction can be achieved at a much

faster rate. Also, substantial capital investments were made by the

Appellant in Delhi for improving the distribution network and

reducing technical and commercial losses. Government support in the